Embed Size (px)

Citation preview

2 0 1 4 I N V E S T O R D A Y

INVESTOR DAY 2014

Today’s Participants

2

Dave Clary Chief Technology Officer & Vice President Performance Chemicals Research & Technology

Vice President, Catalysts Research & TechnologyEdwin Berends

President & Chief Executive OfficerLuke Kissam

Michael Wilson Senior Vice President & President, Catalyst Solutions

Matthew Juneau Senior Vice President & President, Performance Chemicals

Scott Tozier Senior Vice President & Chief Financial Officer

DisclaimersForward Looking Statements

Some of the information presented in this document and discussions that follow, including, without limitation, statements with respect to product development,

changes in productivity, market trends, price, volume and mix changes, expected growth and earnings, input costs, surcharges, tax rates, stock repurchases,

dividends, economic trends, outlook and all other information relating to matters that are not historical facts may constitute forward-looking statements within

the meaning of the Private Securities Litigation Reform Act of 1995. There can be no assurance that actual results will not differ materially. Factors that could

cause actual results to differ materially include, without limitation: changes in economic and business conditions; changes in financial and operating

performance of our major customers and industries and markets served by us; the timing of orders received from customers; the gain or loss of significant

customers; competition from other manufacturers; changes in the demand for our products; limitations or prohibitions on the manufacture and sale of our

products; availability of raw materials; changes in the cost of raw materials and energy and in our ability to pass through such increases; acquisitions and

divestitures, and changes in performance of acquired companies; changes in our markets in general; fluctuations in foreign currencies; changes in laws and

government regulation impacting our operations or our products; the occurrence of claims or litigation; the occurrence of natural disasters; the inability to

maintain current levels of product or premises liability insurance or the denial of such coverage; political unrest affecting the global economy, including adverse

effects from terrorism or hostilities; political instability affecting our manufacturing operations or joint ventures; changes in accounting standards; the inability to

achieve results from our global manufacturing cost reduction initiatives as well as our ongoing continuous improvement and rationalization programs; changes

in the jurisdictional mix of our earnings and changes in tax laws and rates; changes in monetary policies, inflation or interest rates that may impact our ability to

raise capital or increase our cost of funds, impact the performance of our pension fund investments and increase our pension expense and funding obligations;

volatility and substantial uncertainties in the debt and equity markets; technology or intellectual property infringement, including cyber security breaches, and

other innovation risks; decisions we may make in the future; and the other factors detailed from time to time in the reports we file with the SEC, including those

described under "Risk Factors" in our Annual Report on Form 10-K and our Quarterly Reports on Form 10-Q.

It should be noted that this presentation contains certain financial measures, including Net Sales, Segment Income, Capital Expenditures and Free Cash Flow,

that are not required by, or presented in accordance with, accounting principles generally accepted in the United States, or GAAP. These measures are

presented here to provide additional useful measurements to review our operations, provide transparency to investors and enable period-to-period

comparability of financial performance. A description of non-GAAP financial measures that we use to evaluate our operations and financial performance, and

reconciliation of these non-GAAP financial measures to the most directly comparable financial measures calculated and reported in accordance with GAAP,

can be found in the Investors section of our website at www.albemarle.com, under “Non-GAAP Reconciliations” under “Financials.”

3

2 0 1 4 I N V E S T O R D A Y

OVERVIEWLuke KissamPresident & Chief Executive Officer

Albemarle: Compelling Investment Opportunity

• History of industry-leading returns to shareholders

• Global leader in attractive markets: catalysts and bromine

• Differentiated, performance-based core technologies driving innovative solutions

• Capacity in place to serve future growth to drive improved profitability and ROCE

• Outstanding cash generation capacity

• Disciplined capital allocation

• Valuation not reflective of current or future earnings power

• Management incentives aligned with growth and total shareholder return

5

Well-positioned to improve returns, drive increased free cash flow and deliver value to shareholders

A History of Value Creation

-50%

0%

50%

100%

150%

200%

250%

300%

350%

400%

450%

Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14

ALBDow Jones US Chemicals IndexS&P 500

Ten-Year Total Shareholder Return

Source: BloombergAs of 4/23/2014 6

416%

109%

207%

6

Outstanding Cash Generation Capacity

7

FCF defined as cash flow from operations + pension contributions – CAPEXFinancial data for 2010‐2013 adjusted for impact of rare earth and recent divestures.

$100‐$125

$141

$110

$283

$158

$268$297

$317

$282

$203

$275

$340 - $390

$58$70

$100 $99 $100$101

$71

$186

$274

$152

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014E

Historical Free Cash Flow and CAPEX*

Free Cash Flow CAPEX

Strong history of cash flow generation Poised to rise as CAPEX declines and utilization rates increase

*FCF defined as cash flow from operations + pension contributions – CAPEX*Financial data for 2010-2013 excludes the impact of rare earth and the recently announced proposed divestiture of Albemarle’s antioxidant, ibuprofen and propofol businesses and assets

($ in millions)

A Focused Strategy and Clear Deliverables

8

Strategy

• Strengthen and grow catalyst franchise

• Maximize profitability of existing bromine products

• Identify, develop and accelerate commercialization of new applications for bromine

• Drive operational excellence

Deliverables

• Best-in-class Health, Safety & Environmental performance

• Mid to high 20% segment income margins

• Drive higher free cash flow

• $100M in working capital savings by 2015

• Continued dividend increases

• Disciplined M&A

• Improve or exit underperforming businesses

• Return to consistent growth

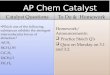

Organizational Structure Supports Strategy Execution

• Simpler organization drives faster decision making and time to market

• Enhanced market and customer focus

• Improved transparency and accountability

• Redeploying approximately $25M into R&D, sales and business development to accelerate growth

Performance Chemicals

Catalyst Solutions

Fire Safety Solutions

Specialty Chemicals

Fine Chemistry Services

Refinery Catalyst

Solutions

9

Non-Flame Retardant Bromine Derivatives, Specialty Materials, and Curatives

Custom Manufacturing

Bromine and Mineral Flame Retardants

Performance Catalyst

Solutions

Catalyst Solutions Performance ChemicalsPerformance Catalyst

Solutions Refinery Catalyst

SolutionsFire Safety Solutions

Specialty Chemicals

Fine Chemistry Services

Common Customers: Deeper wallet penetration & strategic relevance

Shared R&D: Proprietary expertise (organic / inorganic), processes, cross fertilization of ideas

Core Capabilities Overlap: Materials handling expertise, technology, manufacturing & operations, chemicals analysis

Supply Chain Efficiencies: Common raw materials, joint worksites

Shared Processes: One Albemarle strategy

10

Faster speed to marketGreater share of customer wallet and solutions breadth

Raw materials savings and optionality Stronger R&D innovation platform

Integrated Platform Increases Speed to Market, Customer Influence, Supplier Leverage & Innovation

Divestitures & Exits

A History of Actions to Drive Value

Thann

Growth & Innovation

2006 201020082005 2007 201120092004 2012 2013

Nanjing Avonmouth

Acquired refinery catalysts platform

AFX - Maximum propylene platform

Biocides for food safety

STAXTM (Advanced Performance

Modeling)

Activcat Single Site Catalyst

platform

PureGrowthTM High Purity Metal Organics

platform Products to address tight oil

New polymer catalysts plants in Korea & Saudi Arabia

Expanded bromine capacity in Jordan

Proprietary phosphorous

FR platform

Polymeric FR platform for

construction

2014

Port de BoucTeesport

Antioxidants, Ibuprofen & Propofol

Announced exit of high cost toll production

Established UOP hydroprocessing alliance

Sorbent Technologies

11

2004 2009 2013

Revenue $1,514 $2,005 $2,372

Seg. Income $101 $257 $533

Financial data for 2010 - 2013 excludes the impact of rare earth and the recently announced proposed divesture of Albemarle’s antioxidant, ibuprofen and propofol businesses and assets

HTE – Amsterdam

HTE – Bayport & Baton Rouge

Added HPC capacity w/ state-of-the-art technology

Polymeric FR platform for enclosures

Expanded FCC capacity

GBU realignment

($ in millions)

12

Managing Portfolio to Focus on Our Core and Maximize Growth and Profitability

Invest & Grow Maximize Profitability Improve or Exit

• Refinery catalysts

• Organometallics

• Single site catalysts

• Brominated derivatives into faster growing apps(1)

• Fine Chemistry Services

• Curatives

• Mineral flame retardants

• Brominated derivatives into slower growing apps(2)

• Antioxidants

• Ibuprofen

• Phosphorus

• Catilin

(1) Digital technology, mobile computing, mercury control, completion fluids, bromobutyl rubber, pharma and ag intermediates, new apps driven by Bromine Task Force(2) PCs, notebooks and TVs

• Well-positioned to capitalize on catalysts and bromine market trends with major investments already in place

• Productivity enhancements to drive improved profitability and ROCE

» At target bromine and PCS catalyst utilization rates, ALB has the potential to drive segment margin improvement to 26% - 29%

» Both catalysts and bromine enjoy incremental margins in the range of 50%

• Portfolio management» Recent exits expected to deliver 100 to 150 bps

segment margin increase

Substantial Earnings Potential with Minimal Incremental Capital Spend

13

24%

26%26%

22%

26% - 29%

2010 2011 2012 2013 Target

Total Segment Margins*

Meaningful operating leverage per incremental MT of catalysts and bromine sold

*Financial data for 2010 - 2013 excludes the impact of rare earth and the recently announced proposed divesture of Albemarle’s antioxidant, ibuprofen and propofol businesses and assets*Segment margins do not include corporate expenses

14

Valuation Not Reflective of Structurally Improved Margins

10-Year Average Relative P/E: 95% Current Relative P/E: 85%

10-Year Average Relative P/E

Source: FactSet as of 4/24/2014 - Jefferies U.S. Chemicals Universe

Invested for future growth, well positioned to take advantage of market trends and poised to improve margins

Today’s Agenda

1:50 – 2:25 pm Catalyst Solutions Michael Wilson, Senior Vice President & President, Catalyst Solutions

2:25 - 2:45 pmCatalyst Solutions R&D Edwin Berends, Vice President, Catalysts Research and Technology

2:45 - 3:00 pm Q&A

3:00 - 3:10 pm Break

3:10 - 3:45 pmPerformance Chemicals Matt Juneau, Senior Vice President & President, Performance Chemicals

3:45 - 4:05 pmPerformance Chemicals R&D Dave Clary, CTO & Vice President Performance Chemicals Research & Technology

4:05 - 4:20 pm Q&A

4:20 - 4:30 pm Break

4:30 - 4:50 pm Financial Performance & Outlook Scott Tozier, Senior Vice President & Chief Financial Officer

4:50 - 5:25 pm Q&A

5:25 - 5:30 pm Closing Remarks Luke Kissam, President & Chief Executive Officer

5:30 - 7:00 pm Reception / Exhibit Hall Open

15

2 0 1 4 I N V E S T O R D A Y

CATALYST SOLUTIONS

Michael WilsonSenior Vice President & President, Catalyst Solutions

Edwin BerendsVice President, Catalyst Solutions Research & Technology

What is a Catalyst?

catalyst [kat-l-ist] – nounChemistry. A substance that initiates, accelerates or selectively directs a chemical reaction, without being consumed

• Used at some stage in the manufacture of 90% of all commercially produced chemicals

• Vast number of forms and types; shapes, colors and sizes

• Geometry often as important as chemical composition

17

SolidCatalysts

Liquid Catalysts

Typically low in cost, but essential to the end product

18

70 µm

x10

x1,000Clay

Zeolite

FunctionalSilica/Alumina

Binder

Pores

Catalyst development involves tailoring:• Components to impact chemistry• Architecture to determine reactivity

200 nm

Catalysts are a solutions business requiring constant innovation

Complex, Highly Engineered Materials Designed at the Atomic and Molecular Level

Transmission Electron Microscopy

FCC‐ Resid

FCC‐ VGO

AlkyClean

Reforming

Hydrocracking(including mild hydrocracking)

Hydrotreating

Isomerization

FCC‐max C3=

SSC PE

Chromium

Peroxides

Power

Aromatics Oxidation

Hydrogenation

Dehydrogenation

Deg

ree

of C

ompe

titiv

e A

dvan

tage

Market Attractiveness

Resid Hydrotreating

Ziegler Natta PP

Ziegler Natta PE

Syngas

Automotive (light/med)

Automotive (other)

Automotive (med/hv)Other Stationary

Organic Synthesis

Albemarle Segment (RCS)

Albemarle Segment (PCS)

Non‐Albemarle Segment

Total

$5.6B

$0.7B

$17.5B

$23.8B

Global Catalyst Market – Our View

19

We provide refinery and polymer catalyst solutions where we are competitively advantaged based on our technology or cost position

SSC PP

Catalyst Solutions OverviewRefinery Catalyst Solutions (RCS)• Heavy Oil Upgrading (HOU)

» FCC catalysts for resid» FCC catalysts for max propylene» FCC catalysts for vacuum gas oil

• Clean Fuels Technologies (CFT)» Hydroprocessing catalysts » Isomerization» Technology licensing

Performance Catalyst Solutions (PCS)• Polyolefin catalysts and components• Organometallics and co-catalysts• Electronic materials – high purity metal organics

20

Net Sales*

$-

$200

$400

$600

$800

$1,000

$1,200

2010 2011 2012 2013

Net Sales Distribution*

2013 Net Sales: $1B

($ in millions)

($ in millions)

24%

76%

By Business

PCS

RCS 44%

35%

21%

By Region

Americas

EUMEI

Asia Pacific

0%

5%

10%

15%

20%

25%

30%

35%

$-

$50

$100

$150

$200

$250

$300

2010 2011 2012 2013

Segment Income*Segment Income

Segment Margin

*Financial data for 2010 ‐ 2013 excludes the impact of rare earth and the recently announced proposed divesture of Albemarle’s antioxidant, ibuprofen and propofol businesses and assets

Segment Market Position

FCC Catalysts 2

Max Propylene 1

Resid 2

Distillates 1

Vacuum Gas Oil 2

Reactivation Technology 1

Organometallics 1

MAO 1

Custom Single Site Catalysts/Metallocenes 1

Market Position

21

Clean Fuels Technologies

Heavy Oil Upgrading

Performance Catalyst Solutions

Core Strengths

• Deep customer understanding

• Heavy investment in R&D

• Global footprint

• Unparalleled network of partnerships and alliances

• Breadth and depth of talent

We are leaders in our core segments

Our Goal

To be the leading catalyst company in the world

Refinery Catalyst SolutionsHeavy Oil Upgrading• Capitalize on FCC units shifting to maximize propylene• Extend leadership position in tight oil FCC applications• Develop next generation FCC catalysts for resid processing• Capture increasing share of new FCC units

Clean Fuels Technologies• Provide customized STAX® solutions for challenged feedstocks• Expand position in Vacuum Gas Oil (VGO)• Increase win rate for new units in distillates, VGO and resid via

UOP alliance • Provide REACTTM reactivation solutions to our STARSTM

customers globally

Performance Catalyst Solutions• Leverage strength in core organometallics business,

while moving downstream to finished catalysts • Capture growth in high purity electronics market via

PureGrowthTM technology• Drive higher asset utilization at SOCC, Pasadena

and Yeosu; rationalize excess capacity

Catalyst Solutions Goal and Strategy

22

Deliverables

• Double-digit earnings growth• Mid-20% segment income margins

• Maintain >50% of annual sales from new products• World class Health, Safety & Environmental performance

Safi, Jordan

St. Jakob/Breitenau, Austria

Regional/Sales Office

Manufacturing

R&D

Global Headquarters

Joint Venture

Shared Services Center

Saudi Arabia• SOCC - aluminum

alkyls JV with SABIC

Korea• Catalyst R&D and

manufacturing facility for PureGrowthTM, MAO, SSC & ActivCat®

Amsterdam• Refinery catalyst manufacturing• HTE & pilot plant capabilities• HTT capabilities

Japan• Nippon Ketjen JV

with Sumitomo• Nippon Aluminum

Alkyls JV with Mitsui

Brazil• FCCSA JV with

Petrobras (FCC)

Integrated Global Network

23

U.S. – Pasadena, TX• World class aluminum

alkyls facilityU.S. – Bayport, TX• World-class facility for

refinery catalysts• EureCat JV with IFP for

REACTTM technology• FCC capacity expansion • High throughput testing

(HTT)U.S. – Baton Rouge, LA• High throughput

experimentation (HTE) facility & polymer lab

• Manufacturing facility for Ziegler Natta, MAO, SSC & ActivCat®

U.S. – Mobile, AL• Stannica JV with PMC

Strategically positioned to deliver value to customers globally

Structure and Focus Strategic Value

• 50/50 JV with Petrobras• Leading provider of FCC catalysts and additives in

South America• Extensive R&D collaboration

• Supplies majority of Petrobras’ requirements (65% of South American FCC demand)

• Provides strategic access to South American markets

• Alliance with UOP• One of the most successful licensors of hydrotreating

units in the world• Comprehensive portfolio of technologies (licenses),

processes, catalyst equipment and services

• Uniquely combines Albemarle’s extensive portfolio of hydrotreating catalysts with UOP’s hydrocrackingknow-how

• 50/50 JV with IFP • Certified provider of REACTTM reactivation

technology

• Global leader in regeneration and reactivation of hydroprocessing catalysts enabling multi-cycle use

• Operating assets in France, U.S., Italy, Germany,India and Saudi Arabia

• 50/50 JV with Sumitomo Mining• HPC production assets and R&D facilities in Japan

• Developed STARS™ technology; Ketjenfine™ and Ketjenfine Residue™

• Strong market position in Asia Pacific• Integrated R&D and common IP between Albemarle

and Nippon Ketjen

Refinery Catalyst Solutions - Joint Ventures and Partnerships

24

Structure and Focus Strategic Value

• 50/50 JV with SABIC• World-class 6,000MT aluminium alkyls production

facility in Saudi Arabia• First producer of TEA in the Middle East

• Solidifies long-term presence in Middle East• Serves largest global growth area with regionally

produced aluminium alkyls • Provides security of supply for key customers in

GCC region such as SABIC and Chevron Phillips

• 50/50 JV with Mitsui Chemicals• 3,200MT aluminium and zinc alkyls production

facility in Japan• Resale of various Albemarle organometallics• Sales channels reaching into rest of Asia

• Access to high-value Japanese polyolefin polymersmarket for both NAA-produced alkyls and Albemarle products

• Alternative sourcing point for reliability of supply• Leverage organometallics R&D and handling

practices

• 50/50 JV with PMC• Produces organic and inorganic tin intermediates

which are key materials for the production of tin-based PVC heat stabilizers

• Uses tin alkyl as raw material• Serves an adjacent market outside of

Albemarle’s focus• Facilitates leveraging of fixed cost base by running

higher production volumes for alkyls

Nippon Aluminum Alkyls

Performance Catalyst Solutions - Joint Ventures

25

Saudi Organometallic Chemicals Company (SOCC)

Our partnerships and alliances broaden our reach, extend our technology platform and significantly enhance the value of our catalyst franchise

Refinery Catalyst Solutions (RCS)

26

Heavy Oil Upgrading Clean Fuels Technologies

• FCC for Resid

• FCC for Max Propylene

• FCC for Vacuum Gas Oil (VGO)

• Hydroprocessing

• Isomerization

• Alkylation

• Solid Phosphoric Acid (SPA) Catalysts

• Technology Licensing

38%

27%6%

10%

2%

17%

Refinery Catalysts – A Large Market with Attractive Growth

27

Projected Growth (2013 – 2019E)($ in millions)

$0.00

$0.25

$0.50

$0.75

$1.00

$1.25

CAGR = 2.3%

CAGR = 7.0%

Source: The Catalyst Group Resources

Global Revenues (2013) ($6.9B)

CAGR = 0.8%

CAGR = 3.3%

CAGR = 2.8%CAGR = 1.0%

$5.6B$1.3B

FCC

Hydrotreating

Hydrocracking

Other

Alkylation

Reforming

Addressable market growth >$1.0B

Albemarle maintains leadership positions in the most attractive refinery catalyst segments

Catalyst Solutions Throughout the Refinery

28

Heavy Oil Upgrading (FCC)

Clean Fuels Technologies (HPC)

Albemarle provides the global refining industry with a wide range of catalyst solutions to convert crude oil into high value finished products

Global FCC Catalyst Demand Driven by:• Continuous investment in refining capacity for

transportation fuels with demand shifting to developing regions

» Large scale and efficient refinery additions and revamps in AP, China and ME to meet increased regional demand

» FCC flexibility required to maximize profitability from different unit designs, varying feed qualities and desired product slate across the globe

» FCC innovation driven by atypical feeds such as tight oil and increased resid feed processing

• Pursuit of integrated refinery-petrochemical facilities

» Ongoing shale boom favors ethane-based steam cracking and less light olefin co-products

» Maximize production of light olefins such as propylene in the FCC unit to fill the supply

» New FCC units built to maximize propylene output

29

Gasoline Consumption by Region, bcm

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

2010 2015 2020 2025

Sources: HIS CERA, LUKOIL estimates

0

10

20

30

40

50

60

70

80

90

Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14

Tota

l Cat

alys

t Con

sum

ptio

n (k

tpy)

FCC Max Propylene Market Evolution

ChinaOther non-OECDOther OECDNorth America

HOU: FCC Catalyst Demand Driven by Propylene Growth and Increased Transportation Fuels Demand

CFT: Catalyst Growth Will Be Accelerated by Clean Air Mandates

Global HPC Demand Growing:• Substantial global capacity additions in

refineries for hydroprocessing & hydrocracking

Driven by Combination of: • Steady increase of demand for transportation

fuels, driven by rising global passenger car ownership and expansion of commercial vehicles fleet

• Increasingly stringent fuel standards across the globe

» ULSD implementation in China, Latin America, CIS and other regions

» Tier 3 gasoline in NA» Tighter emission standards for marine

fleet

• Changing crude slates and increasing conversion of bottom-of-the-barrel

30

Desulfurization Capacity Requirements (2012 – 2035)

Sulfur Standards per Region

Mb/

d

10-15 ppm

16-50 ppm

51-350 ppm

351-500 ppm

501-2000 ppm

>2000 ppm

Source: Hart Energy Research & Consulting, September 2013

Source: Hart Energy Research & Consulting, September 2013

0

1

2

3

4

5

6

7

US &Canada

LatinAmerica

Africa Europe Russia &Casplan

Middle East China Other Asia-Pacific

Vacuum Gas Oil/Residual Fuel

Middle Distillates

Gasoline

0%

20%

40%

60%

80%

100%

ConventionalCrude Oil

Tight Oil

LPG

Naphtha

Distillate

Gas oil

Resid

Source: Management estimates

Implications of Tight Oil

31

0

1

2

3

4

5

2010 2015 2020 2025

Forecast for Shale Oil Production in the U.S., mb/d

What is Tight Oil?• Liquid hydrocarbons obtained by hydraulically fracturing shale

formations; today a NA phenomenon

• Typically a light, sweet, paraffinic feed

• Generally easy to crack, but often contains uncommon FCC contaminant metals - primarily iron, calcium, sodium and lead

CFT• Although lower in sulfur, tight oil requires additional guard bed

catalysts to protect the main bed catalysts from iron poisoning

• Albemarle’s robust portfolio of guard bed catalysts is well-suited to handle these conditions

HOU• The paraffinic and contaminant metals nature of tight oils creates

new FCC unit constraints that can result in subpar profitability

• Albemarle’s AMBERTM T and UPGRADERTM T are specially formulated to optimize FCC units processing tight oil

Implications and Opportunities

Source: EIA, LUKOIL estimates

Our robust portfolio of catalyst solutions handles a broad array of feed characteristics

Market Driver Innovation Value to Customer

Global Fuel Consumption ACTION™ FCC catalysts • Enhances transportation fuels and alky feedstock

• Raises octane value of gasoline

Heavier Crudes UPGRADER™ FCC catalysts • Upgrades resids and heavy, contaminated feedstocks

Maximum Propylene AFX™ FCC catalysts • Maximizes propylene (chemical feedstock) and bottoms conversion

Tight Oil AMBER T™ and UPGRADER T™ FCC catalysts

• Tuned to optimize tight oil processing

Global Fuel Consumption REACT™ catalyst rejuvenation technology

STAX® advanced performance modeling

• Enhances fresh catalyst value offering

• Maximizes value from the use of catalyst

Clean Air Mandates Nebula™ platform • Avoids capex

Tight Oil Ketjenguard® guard-bed catalyst platform

• High capacity contaminant trapping for main-bed catalyst protection

Capitalizing on RCS Market Trends

32

Heavy Oil Upgrading

Clean Fuels Technologies

Polymer Catalysts Electronic Materials

• Organometallics

• Single Site Catalysts

• Ziegler Natta Catalysts

• High Purity Metal Organics used in LED, semiconductors and photovoltaic solar panels

33

Performance Catalyst Solutions (PCS)

16%5%

19%

3%57%

Polymer Catalyst Market

34

$0.0

$0.2

$0.4

$0.6

$0.8

$1.0

$1B~

CAGR = 5.0%

CAGR = 5.8%

Source: The Catalyst Group ResourcesOther category includes PET, PVC , PS & ABS

Global Revenues (2013)($3.4B)

CAGR = 4.6%

Projected Growth (2013 – 2019E)($ in millions)

CAGR = 3.5%

$0.7B

$2.7B

Addressable market growth ~ $246M

Zeigler Natta - PE

Single Site

Chromium

Other

Zeigler Natta – PP CAGR = 5.0%

Leading co-catalyst position in the largest polyolefin catalyst market (ZN) as well as a custom catalyst & catalyst components producer in the fastest growing segment (SSC)

0

50

100

150

200

250

300

350

400

450

2005 2006 2007 2008 2009 2010 2011 2012 2013E 2014E 2015E 2016E 2017E 2018E

PCS: Developing Economies Drive Growing Polyolefin Demand

35

Global Ethylene CapacityConsumer trends and feedstock advantages will drive regional polyolefin demand and supply• Growing middle-class in rapidly developing economies

• Downstream effect of new ethane cracking capacity in U.S.

• Differential between ethane-based and naphtha-based economics

Capacity is well positioned to capture market growth • Investments in Saudi Arabia, North America and South Korea

• New catalyst capacity (South Korea + USA) enables 300% expansion of profitable and defensible SSC business

• Rationalizing capacity where regional feedstock/polyolefin economics are mismatched

Proprietary activation technology enables favorable economics in specialty polymers • ActivCat® in commercial scale adoption in 2014

• 2nd-generation technology in pilot phase and 3rd-generation in lab

• 20 active finished catalyst projects, of which 9 are in Asia

Cap

acity

, mn

lbs

Source: HIS Chemical, BofA Merrill Lynch Global Research

South America

Middle East

Europe

Asia

North America

0

50

100

150

200

250

300

1998 2003 2008 2013 2018

Rest of World

Middle East

Rest of Asia

China

North America

Europe

Global Polymer Demand

+3.1% CAGR +3.9% CAGR +3.9% CAGR

Dem

and,

Mt/y

Albemarle is well positioned, geographically and technically, to capture supplySource: The Catalyst Group Resources

PCS: Poised to Capitalize on LED Opportunity

36

Demand for LED lighting is increasing• Government mandates being advanced

• Asia lighting market growth of 10-14% per year*

• Capacity expansion has pushed down prices in the supply chain

Albemarle has built world-class capacity• New TMG unit and clean-room lab & packaging in

South Korea

• Acquired proprietary purification technology to enable transition to high-purity materials

Market entry progressing, though slower than anticipated• Advancing up steep learning curve on high-purity production

• Increasing qualifications (33 TMG & TEG qualifications to date, representing 30% of the market for these products)

• Evaluating commercial channels in targeted markets to accelerate repeat sales

Catalyst Grade TMA & TEA

High Purity Metal Organics

LEDs

Back Integration

* Source: Strategies Unlimited

Yeosu, Korea

• Single-site catalyst production • State-of-the-art research &

operations center• Metal organics expansion to

support electronic materials growth platform

SOCC, Saudi Arabia

• JV with SABIC• First TEA facility in the region• Meeting security of supply and

demand needs for polyolefin producers in Middle East

HTE & Polymer Lab, Global

• HTE capabilities in Amsterdam, Baton Rouge and Bayport

• Parallel Polymerization Reactor system facilitates up to 48 experiments per run

Catalyst Innovation Center, U.S.

• 5,400 square foot state-of-the-art laboratory complex

• Supports R&D efforts for Albemarle’s rapidly growing polyolefin catalyst portfolio

• Hosts eight new chemical synthesis stations

PCS: Investments in Future Growth

37

Performance Catalyst Solutions Technology Portfolio

38

Market Driver Innovation Value to Customer

Customers Demanding Innovative Polymers

Activcat™ Single Site Catalyst (SSC) platform

Methylaluminoxane (MAO)Aluminoxane activator

• Enabler of favorable polymer economics by lowering the overall cost-in-use of the catalyst system

• Dependable metalloceneactivator supply to meet growing specialty polymer demand

NA Shale Gas Driven Expansions / Growing Consumerism

Triethylaluminum (TEA) Aluminum alkyls organometallic

Advantage® Ziegler Natta catalyst platform

• Dependable co-catalyst and catalyst supply to meet growing polymer demand

• High-performance catalysts for polyethylene production

LED Emergence / Growing Consumerism

PureGrowth™ High Purity Metal Organics platform for electronics

• Alternative source of high quality key ingredient for electronics / LED industry

Performance Catalyst Solutions

Catalyst Solutions: Innovation Is Essential to Our Success

39

37% 39%

50% 49%

56%59% 58%

0%

10%

20%

30%

40%

50%

60%

2007 2008 2009 2010 2011 2012 2013

(% of total sales from products introduced in past five years)

Catalyst Solutions New Product Velocity

Strategic Pillars“Grow the Core”

Breakthrough technology development

• Longer-term product development anticipating future market needs

• Business input/market intimacy critical for success

• Develops fertile ground for future efforts

• Technology push

Manufacturing technology development

Technology and product extensions

• High capacity

• Low cost

• Low working capital

• Safe processes

• Continually raising the performance bar to meet current market needs

• Market/customer-driven pull

• Competitive leap-frogs

VISION: Advance our recognized leadership position in catalyst technologies

40

Actively managing resources to best serve customer and market needs

Safi, Jordan

St. Jakob/Breitenau, Austria

Albemarle Research & Technology facility

JV Research & Technology facility

Catalyst Resources Aligned to Support Growth

41

U.S. - Bayport, TXU.S. - Baton Rouge, LA

Amsterdam, The NetherlandsLouvain-la-Neuve, Belgium

Nippon KetjenTokyo, Japan

Petrobras/FCCSARio de Janeiro, Brazil

Yeosu, South Korea

Global reach extended by network of external experts & institutions

The Catalyst Innovation Chain

42

Pilot Scale Commercial Scale

Understanding Customer

Challenges

• High Throughput Experimentation

• Conducts up to 48 experiments per run

• Efficiently optimizes catalyst formulations

• Evaluates technology scalability

• Supported by specialized/proprietary modeling

grams kilograms metric tons

• Full-service technical support team assists with start-up through optimization and beyond

• Work collaboratively with customers to understand operating constraints and feedstock conditions

Small Scale

Proof of Concept Research Development CommercializationIdeation

Providing customized solutions for specific customer needs

Decreasing Time-to-Market for New Technologies

43

HIGH THROUGHPUT EXPERIMENTATION (HTE)• High throughput system accelerates development and decreases time-to-market

• Reactor models and bench scale units are utilized for product testing

• Samples are tested using innovative analytical techniques for key components

• Test results are used for product optimization and new product development

1 experiment per run

48 experiments per run

past

presen

t ‐HTE

Catalyst Technology Requires a Robust and Highly-Specialized Skill Set

44

HOU CFT PCS

Gel Chemistry

Specialty Zeolites

Washing/Separation

Ion Exchange

Drying/Calcination

Particle Sizing

Metals Impregnation

Powder Handling

Process Optimization

HTE Testing

Pelletizing

Extruding

Spray Drying

Quality Control

Packaging

45

70 µm

x10

x1,000Clay

Zeolite

FunctionalSilica/Alumina

Binder

Pores

Catalyst development involves tailoring:• Components to impact chemistry• Architecture to determine reactivity

200 nm

Catalysts are a solutions business, requiring constant innovation

Complex, Highly Engineered Materials Designed at the Atomic and Molecular Level

Transmission Electron Microscopy

CFT: Catalyst Optimization for Specific Customer Needs

46

• Mastering surface area and properties

• Active species well dispersed

• Balance of active functions

• Extensive experience in long-term testing of catalyst properties

THE RIGHT CATALYST FOR THE RIGHT APPLICATION

Log S, N

SN

S < 10 ppm

Zone 1

Zone 2

Zone 3

UNDERSTANDING THE REACTOR

• STAX® Technology: Applies an understanding of reactor zone behaviors to optimize catalyst selection and packing

Time-on-stream 100 hrs

Parameter A

Par

amet

er B

2

High

Low Activity

Time-on-stream 1000 hrs

2

01234

Reference 1st Gen 2nd Gen

PCS: Beyond Organometallics

47

Advantage®

• Ziegler Natta catalyst platform• High performance catalysts for PE production

PureGrowthTM

• High Purity Metal Organics platform• Used to manufacture components used in LED

lights and solar panels

Relativ

e Ac

tivity

ActivCat®

• High performance SSC for PE and PP production• More efficient "activation,” significant performance

enhancement and increased catalyst life• Lower cost in use for customer

• Developing performance-based finished catalysts and components

• Engineering “step-out” activators and supported catalysts

• Implementing high-purity production, packaging and analysis for electronics applications

2011 2012 2013 Price ManufacturingExcellence

PortfolioManagement

CapacityUtilization

AdditionalCosts

Target

20%

24% - 27%

22%20%

Segment Income Margins*

Catalyst Solutions: Delivering Sustained Results

48

*Financial data for 2011 - 2013 excludes the impact of rare earth

• Hold leading positions in strong markets

• Deep customer relationships

• Global footprint

• Strong partnerships/alliances

• Broad technology platform to capitalize on market trends

• Improving efficiency through better asset utilization, de-bottlenecking and rationalization of capacity

• Leveraging core strengths to expand positions in attractive new markets and deliver greater-than-GDP growth

49

8% to 10% Catalysts profit growth outlook over next 3 to 5 years

Catalyst Solutions: Positioned to Deliver Profitable Growth and Margin Enhancement

2 0 1 4 I N V E S T O R D A Y

PERFORMANCE CHEMICALS

Matt Juneau Senior Vice President & President, Performance Chemicals

Dave Clary CTO & Vice President, Performance Chemicals Research & Technology

45%

38%

17%

By Business

FSS

SPC

FCS48%

29%

23%

By Region

AM

EUMEI

AP

Performance Chemicals Overview

51

Fire Safety Solutions• Brominated Flame Retardants• Mineral Flame RetardantsSpecialty Chemicals• Non-Flame Retardant Bromine Derivatives• Curatives• Specialty MaterialsFine Chemistry Services• Custom Services for Pharmaceuticals, Agricultural & Electronics• Generic & Pharmaceutical Actives• Specialty Ag Intermediates

Net Sales*

Segment Income*Net Sales Distribution *

2013 Net Sales: $1.4 B

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

2010 2011 2012 2013

($ in millions)

0%

5%

10%

15%

20%

25%

30%

35%

$0$50

$100$150$200$250$300$350$400$450

2010 2011 2012 2013

Segment Margin

*Financial data for 2010 - 2013 excludes the recently announced proposed divesture of Albemarle’s ibuprofen and propofol businesses and assets

($ in millions)

Our Goal

Maintain and strengthen our position as the leadingbromine company in the world

Fire Safety Solutions• Maintain and strengthen industry-leading FR portfolio

• Drive FR growth via strong focus on customer partnerships and applications expertise

• Continue to bring new innovations in FR to the market

• Promote the safety and efficacy of BFRs to OEMs, regulators and NGOs

• Grow the FR market through a focus on key developing economies and high growth applications for fire safety

Specialty Chemicals• Maintain and strengthen industry-leading position in

bromine reserves, recovery and production

• Take advantage of integrated production assets to drive operational efficiency and cost reduction

• Use strong global position to drive above-trend growth in core applications (oilfield, automotive, mercury control, and pharma and ag chemicals)

• Develop new, large-volume uses for bromine

Performance Chemicals Goal and Strategy

52

Deliverables• Industry-leading profitability and return on capital

and a return to strong earnings growth

• High-20% segment income margins

• 80% utilization of bromine assets

• 4-6% annual revenue growth

• World-class Health, Safety & Environmental performance

Bromine is Essential to Performance Chemicals

53

Water Treatment

Oil Drilling

Food Safety

Consumer Electronics

Mercury Abatement

Transportation

Pharma/ Ag

Albemarle delivers value from bromine uses across multiple end markets

• Recovery is both capital & energy intensive

• Difficult & expensive to transport• Additional technology & capital

needed to derivatize• Product stewardship and Health,

Safety & Environmental expertise crucial

Strong Barriers to Entry for Bromine

Mobile Computing &

Data Processing

Strong Core of Bromine & Derivatives with High Value

54

2004 2007 2010 2013

Fire Safety Solutions Specialty Chemicals

Gross Profit from Bromine-based Products Relative Contribution/Kg Bromine Utilized(2013)

Diverse Bromine and Bromine Derivatives Offering

Delivering Attractive High-Value Margins

0 2000 4000 6000 8000 10000 12000

Seawater

China

India Concentrate

Michigan

Arkansas

Dead Sea

Dead Sea Concentrate

Competitive

Noncompetitive

80%

20%

Competitive Noncompetitive

2014 Global CapacityALB & ICL

ALB & CHMT

Closed in 2006

UK plant in 2003. France plant in 2005.

Leading Bromine Sourcing Position

55

Only producer with access to the two best sources of bromine

(ppm)

• Albemarle has capacity to efficiently meet demand growth• China production capacity continues structural decline• Remaining producers (except ICL) operating at/near capacity

56

Bromine: Snapshot of Global Capacity, 2009 to 2014

0

50

100

150

200

250

300

ICL ALB CHMT China Tosoh India

2009

2014

Source: Management estimates; market research; Arkansas Oil and Gas Commission

Capacity available for future growth

ICL52%ALB

47%

Other1%

Albemarle is positioned to capture significant growth

(thousands of MTs)

Oilfield

Rubber/ PTA

Pharma / Ag

Mercury

Water Treatment

Other

57

Strong Core and Solid Growth Prospects

• Flame retardants for auto, data processing, communications and industrial electronics

• Completion fluids for oil drilling

• Mercury abatement

• Water treatment and biocides for food safety

• Bromobutyl rubber for tires

Projected 4-6% Growth over Next 5 Years

• Flame retardants for construction

• Ag / Pharma intermediates

Significant Opportunity to Capitalize on Value of Bromine MoleculeSignificant Opportunity to Capitalize on Value of Bromine Molecule

Trend Growth Markets Above-Trend Growth Markets

$2.75B Global Market (2013E)

Albemarle is well positioned to capitalize based on:Diverse End Markets

Product Portfolio BreadthFavorable Globalization Trends

Unique Global Footprint & Cost Position

FlameRetardants

Market Trends: Performance Chemicals

58

OilfieldData Processing and Communications

Mercury AbatementTransportation Pharmaceutical and Agricultural

Automotive

FR: High Growth in Data Processing and Communications

59

$0

$50

$100

$150

$200

$250

$300

$350

$400

2012 2017

Current and Future Drivers Core Applications (PCs, etc.)

~ 9% CAGR

(1) Includes: Smartphones, TVs, Servers, Tablets, Industrial Electronics, Automotive Electronics(2) Includes: Consumer Electronics, Communications Electronics, Peripherals & Other Data Processing Electronics, Traditional Mobile Phones, Appliances, Military and Civil Aerospace Electronics

Source: Gartner 2013

(1) (2)

Semiconductor Consumption by Application ($ in millions)

Compelling growth opportunities in:• Communication & Mobile Devices:

Smartphones, Tablets• Computing, Data Processing:

Servers• Automotive/Transportation• Industrial & Medical• Home/Office Electronics &

Appliances

Stable core product set

0

100

200

300

400

500

600

700

800

900

1000

2012 2013 2014 2015 2016Desktop Portable Tablet Smartphone

Source: IHS; Gartner; IDC; IC Insights; DisplaySearch; Albemarle management

Devices Sold(MM)

FR: Communication & Mobile Devices Key to Growth

60

0

2

4

6

8

10

12

2012 2013 2014 2015 2016

Data Processing,

Communication &

Mobile Devices Markets Driving Server Growth

Servers

Estimated Circuit Board FR Consumption per Device(weighted by device unit sales)

Source: Management estimates

Server

Desktop

Laptop

Tablet +Mobile Phone

FR: Changing Consumption Pattern in Circuit Board Applications

61

Servers have overtaken PCs as key to BFR consumption in Printed Circuit Boards

Source: Infineon; BofA Merrill Lynch Global Research estimates; World Bank; IHS; KPMG; Management estimates*Western Europe includes: EU-15 plus Norway and Switzerland

Semiconductor Opportunity by Category(Sales)

Infotainment

Body

Safety

Powertrain

2010 2015

$4.4B$7.8B

$5.1B

$5.2B

$3.5B

$8.9B

$8.2B

$5.2B

62

FR: Automotive Electronics Becoming Growth Driver

Key Drivers• Stricter fuel economy and emissions mandates• Requirements for advanced safety systems• Consumer demand for greater infotainment capabilities• Consumer demand for luxury vehicles and convenience features• Growth of hybrid and electric vehicles

» Hybrid vehicle worldwide market projected to grow 200% from 2014 to 2017

Vehicle Penetration by Country (2013)(Car ownership per 1,000 people)

0

10

20

30

40

50

60

India China Brazil WesternEurope*

US

Increasing use of electronics and increasing car market in developing world will fuel growth

Well-positioned to Capitalize on New Demand for FRs

63

Best product portfolio for widest range of electrical and electronic applications across all markets

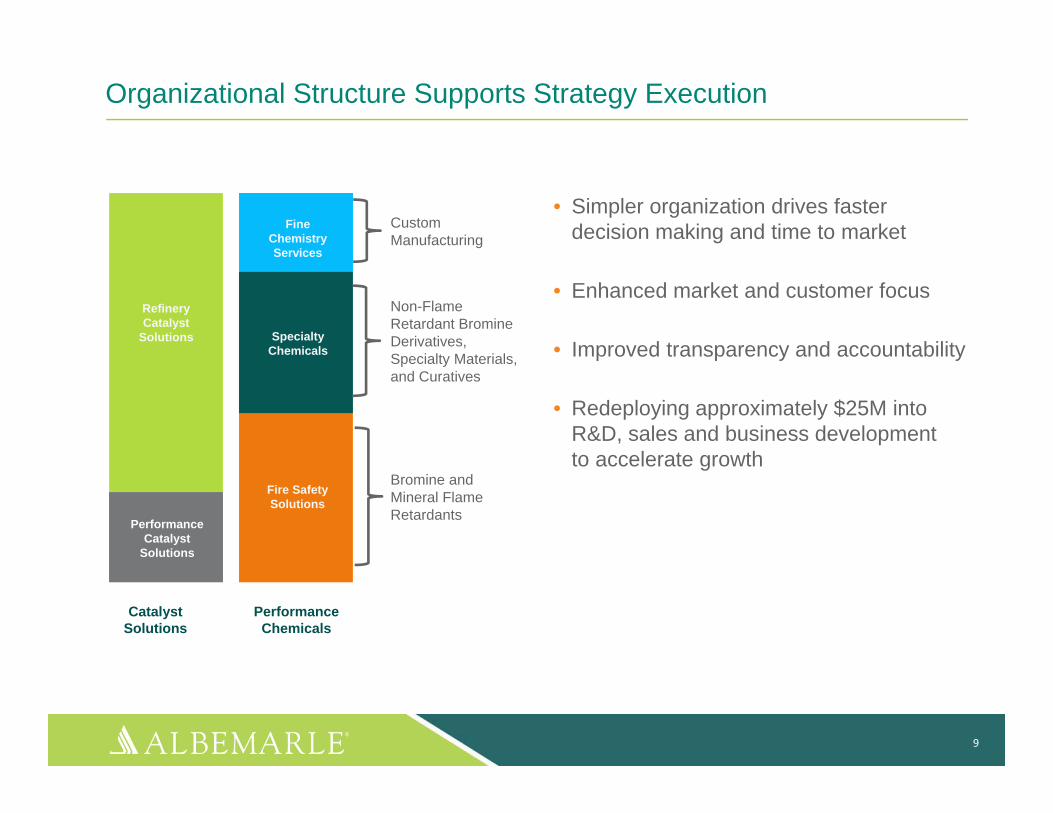

Global Completion & Production Services

0

20

40

60

80

100

120

140

160

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

North America South and Central AmericaEurope Middle East and AfricaAsia Pacific

Rev

enue

in b

illion

s

7% CAGR (2011-2016)

Source: GBI Research; JP Morgan* Reflects 2014 forecasted CAPEX growth vs. 2013

64

Oilfield Chemicals: Surging Global Exploration & Completions

Key Drivers• Offshore Gulf of Mexico rig count forecasted to rise from 43 to near 50 by end of 2014, and 60 by end of 2015• International CAPEX growth driven by Middle East (14%), Latin America (13%) and Russia/FSU (11%)*

608

621 623

659669

570

580

590

600

610

620

630

640

650

660

670

680

4Q12 1Q13 2Q13 3Q13 4Q13

Middle East Rig Count

Global use of completion fluids increasing rapidly

Source: Primary Research and Industry Sources; Ken Research; Morgan Stanley Research

Total (Mtpa)

Lanxess 70,000

Reliance/ Sibur 100,000

SABIC/ ExxonMobil 110,000

ExxonMobil 140,000

Panjin Heyn 150,000

Other 75,000

Bromobutyl Rubber Key ProjectExpansion Announcements (2013-2018)

65

Bromobutyl Rubber: Mobility & Modernization Driving Growth

China Tire Market Segmentation on the Basis of Radial and Non-Radial Tire Production (2012)

71.4%

28.6%Radial

Non‐Radial

India Tire Market Segmentation on the Basis of Level of Radialisation (2012)

0%20%40%60%80%

100%

Passenger Cars CommercialVehicles

Key Drivers• Recovery in car markets in developed world• Higher rates of car ownership in developing world (India, China, etc.)• Additional “radialisation” of the tire market in developing world, especially in commercial vehicles

Global consumerism driving 6-7% CAGR

Ag & Pharmaceuticals: Steady Growth with Upside Potential

66

16.5

10.8

4.5

3

3

0.6

0 5 10 15 20

Korea

Japan

United States

Global Average

Europe

India

Average Global Pesticide Use(2012)

Kg/Hectare

Source: Ken Research*Other includes Argentina, Egypt, Indonesia, Mexico, Pakistan, Poland, Romania, South Africa, Thailand, Turkey, Ukraine, Venezuela and Vietnam

66.9

25.6 20.7 15.6

76.6

175.8

57.345.1 48.8

172.2

0

20

40

60

80

100

120

140

160

180

200

China Brazil Russia India Other*

Sales in 2011 Projected Sales in 2020

Demand for Medicine is Rising Rapidly in Growth Markets

US

$ bi

llion

s

Key Drivers• Aging population continues to drive pharmaceuticals demand in U.S., Europe, Japan, etc.• Increasing standards of living in developing world impacting both medicine and food demand

Albemarle’s Offerings in Pharma and Ag Products: Bromine, HBr and organic bromides used as synthesis intermediates

Well positioned to take advantage of globalization trends

Mercury Control: Strength in Major Market Channels

67

- 5,000

10,000 15,000 20,000 25,000 30,000 35,000 40,000

2012 2013 2014 2015 2016 2017

Key Drivers• EPA MATS standard (2Q 2015) will drive NA growth• China is a major long-term opportunity• Europe, industrial boilers, cement kilns are add-on opportunities

Albemarle’s Offerings in Mercury Control: • Section 45 – Calcium Bromide• Pre-combustion – Calcium Bromide• Brominated PAC – Bromine

NA Bromine Demand in Mercury Control

Source: Albemarle estimates; US Energy Information Administration.

Capital Plans

Unknown

Plan to Retire

Capital Spent/ Being spent to

comply with MATS

NA Coal Power Plant – MATS Compliance Strategy

76%

16%

8%mT

Leveraging strength in bromine derivatives to address more stringent industry standards

• High-growth, attractive markets» Etching for semiconductors» Water Treatment» Food Safety» Precision cleaning solvents for electronics & automotive

• Leverages every bromine molecule» Reduces recycle» Optimizes production

68

Specialty Applications: Optimize Bromine Assets & Create Added Value

Bromine SpecialtyProduct A

SpecialtyProduct B

SpecialtyProduct C

SpecialtyProduct D

Source: Management estimates

Relative Contribution/Kg Bromine Utilized

Demonstrates versatility and value of bromine technology

42%

23%

11%

3%

3%19%16%

48%3%

1%

8%

24%

Flame Retardants Gas Additives Clear Brine Fluids Water Treatment PTA Methyl Bromide Other

36%

26%

9%3%

26%

1970s-1980s 2013 Future

Source: Management estimatesOther includes: photographic chemicals, halons, non-water treating biocides, pharma intermediates, ag intermediates, high purity HBr for electronics and mercury control

Historical Evolution of US Bromine Consumption

69

A proven history of successfully managing changing market demands

Bromine: The Wonder Element

70

Unique and versatile combination of properties provides value across a wide range of applications

Dense Oxidizes Metal

BulkyForms Stable

Radicals

Liquid & High Redox

Potential

Affects Light

Absorption

Creates Polar

Molecules

Oxidizes Organic

Compounds

A Strong and Growing Pipeline of Projects

Addressing Substantial Market Opportunities

• Delivering value by leveraging bromine properties

• Executable and realistic

Uniquely Positioned to Succeed

• Bromine strength, focus and reputation

• Catalyst expertise and process development

• Custom Services provides speed-to-market and low-cost sample production

• Stand-alone technical and business development team able to leverage the larger organization as needed

71

Creating New Bromine Demand Drivers

Growing new high-revenue, high-value businesses

The Right Skill Set & Capabilities to Develop New Bromine Businesses

72

Bromine Custom Services Catalysts Outside

Collaboration

Process Optimization

Corrosive/Hazardous Material Handling

High Throughput Experimentation

Bromination Chemistry

Process Scale-up

Quality Control

Metal Impregnation

Electrochemistry

Catalyst Screening

Broad Chemistry Expertise

Process Evaluation

Polymer Science

Application Testing

Activated Carbon

Market Research

Low-cost Sample Production

Speed to Market

Idea Generation

020406080100120140160180200

$-

$20

$40

$60

$80

$100

$120

$140

2012 2013 2014 2015 2016 2017Billion USD GWh

Lux Research $113B by 2017BCG $345B by 2030Piper Jaffray $100B by 2017

$600B by 2022

$B GWh

Global Market for Grid-Scale Energy Storage

Key Drivers• Increased reliance on distributed solar and wind power generation • Micro-grids for commercial and defense applications • Backup power for developing nations with rising diesel fuel costs and growing pollution concerns (India, Africa)

Source: BP Statistical Review of World Energy 2012; BP Energy Outlook 2030; Lux Research

0

50000

100000

150000

200000

250000

300000

350000

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Wind Solar Geothermal TOTAL

Global Cumulative Installed Energy Capacity From Renewable Sources

Megaw

atts

Growth Opportunity: Energy Storage Market

73

Advantages• Decoupling of power and storage (allowing long-duration discharge)

• Less expensive materials: $300/kW vs. $1000/kW for Li-ion

• Can fully charge/discharge with little electrode damage

• Scalable

Energy Storage: The Flow Battery Solution

74

Source: Management estimates

Enabling the electrical grid of the future

Albemarle is moving quickly• Developing high-performance electrolytes• Providing qualification samples to customers• Building customer relationships and positioning for sales

Bromine is well positioned• Advantages versus other flow-battery chemistries:

» Bromine is liquid at standard conditions» High-energy density » Lower electrolyte costs

• Zinc Bromide and Hydrogen Bromide are most commercially-advanced

• Other bromine-based systems under development

Source: Management estimates

Flow Batteries: Bromine’s Potential

75

• Security of supply will be very important – large volumes, logistics, global market• Customers need suppliers with strong base in bromine technology• Ongoing customer support will be critical – Health, Safety & Environmental, technical

service, materials of construction, transportation and handling expertise

Why Will Albemarle Win?

Total market opportunity 25K-50K MT/yr of bromine

Albemarle’s Program• Lab-scale and pilot-scale testing• Albemarle developing a bromine-based process in cooperation

with a leading industry laboratory

Increased Regulatory Pressure on the Use of Cyanide in Heap Leaching• Caused by environmental damage from past spills (especially in

Colorado and Romania)• Montana, Wisconsin, Czech Republic, Hungary, Turkey, parts

of Argentina, Costa Rica and Germany have banned this use of cyanide

• Increased regulatory and stakeholder scrutiny in other areas

Source: Management estimates

Key Drivers• Environmental pressure on existing cyanide technology• Better performance for some types of gold ore

Bromine offers a sustainable, effective alternative to cyanide in gold recovery

Growth Opportunity: Gold Recovery

76

Total market opportunity > 20K MT/yr of bromine

Performance Chemicals: Delivering Sustained Results

77

26% 26%21%

2011 2012 2013 Mineral FRImprovement

PortfolioManagement

Price Bromine @80% Utilization

AdditionalCosts

Target

27% - 30%

Segment Income Margins

78

Performance Chemicals: Leading the Way in Bromine

The right people, resources, assets and technology to win

Committed to delivering:• Industry-leading segment margins and profitability

• 20+% ROCE

• Revenue growth of 4-6%

• World-class Health, Safety & Environmental performance

Through intense focus on:• Our bromine and bromine chemicals assets

• The “right” markets and customers across our businesses

• Value-based differentiation

• Leveraging the global reach of our business

• Driving new businesses based on bromine chemistry

2 0 1 4 I N V E S T O R D A Y

FINANCIAL PERFORMANCE & OUTLOOKScott TozierSenior Vice President & Chief Financial Officer

Financial Performance Summary

80

$2,155 $2,516 $2,443 $2,372

$2.5 -$2.6B

2010 2011 2012 2013 2014F

Net Sales*

Total Net Sales Catalyst Solutions Performance Chemicals

$521

$651 $646

$533 $540 - $570

2010 2011 2012 2013 2014F

Segment Income*

Total Segment Income Catalyst Solutions Performance Chemicals

$317 $282

$203

$275

$340 - $390

6.2% 6.2%

3.7%

5.4%

6-7%

2010 2011 2012 2013 2014F

Free Cash Flow*

Free Cash Flow FCF Yield

$305 $271 $205

$588 $590 - $615

0.5x0.4x

0.3x

1.0x1.0x

2010 2011 2012 2013 2014F

Net-Debt-to-EBITDA

Net Debt Net-Debt-to-EBITDA

*Financial data for 2010 - 2013 excludes the impact of rare earth and the recently announced proposed divesture of Albemarle’s antioxidant, ibuprofen and propofol businesses and assets

($ in millions)

Cap

ital R

etur

nsInvest in core to drive innovation and organic growth

Focus on return on capital employed

Sustainable working capital reductions

Disciplined merger and acquisition strategy

Consistent dividend growth and total shareholder return

Maintain investment grade status and strong balance sheet

Our Financial Priorities

81

10%13%

12%

15% 16%

12%14%

16%15% 16%

5%

9%

14%

14%14%

11%

23%

26%25%

19%20%

0%

5%

10%

15%

20%

25%

30%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014F

Dow Jones U.S. Chemicals Index ALB

Return on Capital Employed

Margins Capital Efficiency Portfolio Management

ROCE = Adjusted EBIT / Total Assets - Current Liabilities (ex short term debt) – Cash

82

Recent Trend Reflects Major InvestmentsPortfolio Actions & Improved Asset Utilization to Drive Improvement

5yr Average 10yr Average

ALB 21% 16%

Dow Jones U.S. Chemicals Index 15% 14%

• Cost management• Asset utilization• Operating leverage

• Working capital reductions • Product innovation• Disciplined M&A• Divest underperformners

Financial data for 2010 - 2013 excludes the impact of rare earth and the recently announced proposed divesture of Albemarle’s antioxidant, ibuprofen and propofol businesses and assets

3746

65

AlbemarleCorporation

Median Upper Quartile

~$88M potential impact

5957

53

AlbemarleCorporation

Median Upper Quartile

Working Capital: Substantial Cash Flow Opportunity

Days Payable OutstandingDays Inventory Outstanding

94

6257

AlbemarleCorporation

Median Upper Quartile

Source: Hackett Group Peer Study – 2013. Peers: PolyOne, Celanese, Ashland, Grace, Sherwin-Williams, Akzo Nobel, BASF, Huntsman, RPM, Clariant, Chemtura

Days Sales Outstanding

83

~$165M potential impact

~$27M potential impact

Committed to delivering $100M in permanent working capital savings by 2015 with upside opportunity

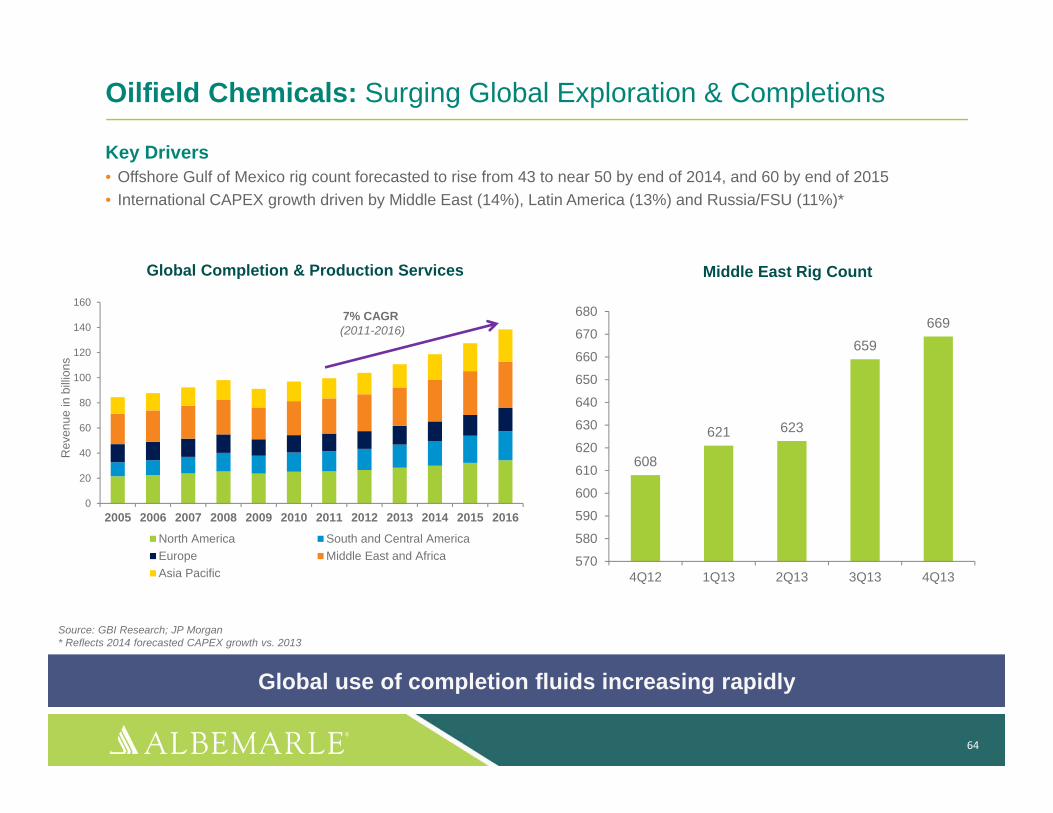

Improve Working Capital: Transforming the Supply Chain

• Assessing every part of supply chain to identify overlaps and opportunities

• Significant opportunity to deliver working capital improvement

• Reworking structural elements to create more effective and efficient processes

» Better align supply chain assets and capacity with demand

» More responsive to customer needs

• Redefining approach to inventory management

» Focus on standardization and simplification

• Dedicated cross-functional team focused on delivering results

Supply Chain

Operating Model

Delivery Excellence

Network Strategy

Inventory Strategy

Customer & Vendor Contracts

Leverage Technology

Operations Planning

84

Comprehensive approach drives operational excellence across the full supply chain

Disciplined Mergers and Acquisitions

• Consistent with our strategy» Strengthen and grow catalysts

» Expand uses for bromine

• Technological synergies

• Market leaders

• Attractive industry structure

• Creates stronger free cash flow

• Accretive and value enhancing

85

Financial strength allows for M&A opportunities

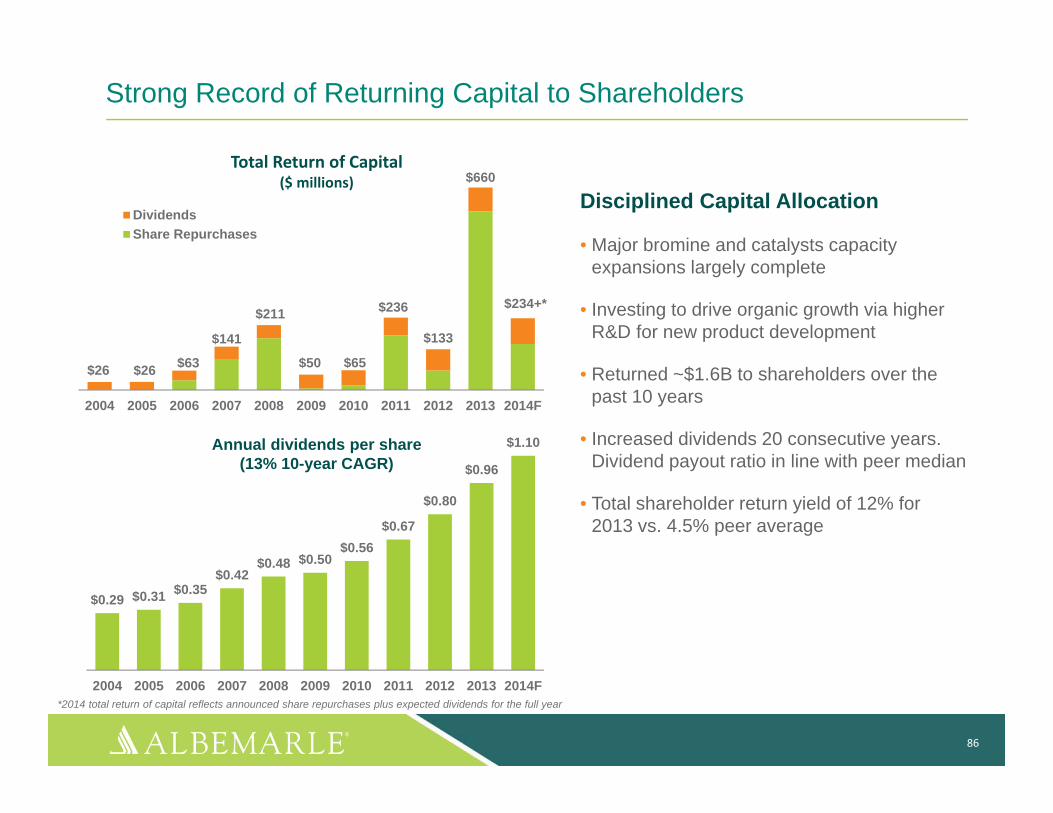

Total Return of Capital ($ millions)

$0.29 $0.31 $0.35$0.42

$0.48 $0.50$0.56

$0.67

$0.80

$0.96

$1.10

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014F

Annual dividends per share(13% 10-year CAGR)

$26 $26 $63

$141

$211

$50 $65

$236

$133

$660

$234+*

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014F

DividendsShare Repurchases

Strong Record of Returning Capital to Shareholders

Disciplined Capital Allocation

• Major bromine and catalysts capacity expansions largely complete

• Investing to drive organic growth via higher R&D for new product development

• Returned ~$1.6B to shareholders over the past 10 years

• Increased dividends 20 consecutive years. Dividend payout ratio in line with peer median

• Total shareholder return yield of 12% for 2013 vs. 4.5% peer average

86

*2014 total return of capital reflects announced share repurchases plus expected dividends for the full year

$1.2B

$0.3B

$0.9B

$1.6B

Continued Disciplined Approach to Capital Allocation

Outlook

• Committed to continued dividend growth

• CAPEX in the range of 4% of sales

• Working capital reduction of $100M by 2015

• Disciplined M&A

• No voluntary pension contributions in 2014

• Maintain investment grade credit rating

• Continued use of excess cash flow to fund share buybacks

2004-2013($ in millions)

87

Total Return of Capital (repurchases & dividends)

CAPEX

Pension Contributions & Other

Acquisitions

1x Net-Debt-to-EBITDA guideline = flexibility and consistent return of cash

Operating Segment

Revenue Growth Targets

2013 SegmentMargin*

Segment Margin Target Growth and Profitability Drivers

1.0x - 2.0x GDP 22% 24% - 27%

• Improved asset utilization• High incremental margins• Market trends• New products

1.0x – 1.5x GDP 23% 27% - 30%

• Improved asset utilization• High incremental margins• Improvement in electronics

and mix shift• New uses of bromine• Market trends

1.0x – 2.0x GDP 22% 26% - 29% • Committed to higher return on capital• Continued focus on cost efficiency

Financial Outlook

88

Total Company

Market trends, asset utilization & portfolio actions drive growth & profitability

*Financial data for 2010 - 2013 excludes the impact of rare earth and the recently announced proposed divesture of Albemarle’s antioxidant, ibuprofen and propofol businesses and assets*Segment margins do not include corporate expenses

Catalyst Solutions

Performance Chemicals

Albemarle: Compelling Investment Opportunity

• History of industry-leading returns to shareholders

• Global leader in attractive markets: catalysts and bromine

• Differentiated, performance-based core technologies driving innovative solutions

• Capacity in place to serve future growth to drive improved profitability and ROCE

• Outstanding cash generation capacity

• Disciplined capital allocation

• Valuation not reflective of current or future earnings power

• Management incentives aligned with growth and total shareholder return

89

Well-positioned to improve returns, drive increased free cash flow and deliver value to shareholders

Albemarle is Positioned to Succeed

90

Products• Constantly

innovating• Performance-based

value propositions • Highly-customized• Aligned with

market trends

R&D• Investing in the

future• 2,400 patents

awarded over 10 years

• Well over 100 PhDs

Financials• Outstanding profit

margins • Strong cash flow • Balance sheet

flexibility • Excellent banking

relationships • Investment grade

rating

People• Experienced

leadership with incentives aligned with shareholder returns

• World-class, talented, creative employee base

• Strong Board of Directors

Tomorrow’s Agenda

• Depart for Plant

• Welcome/Safety Review

• Plant Tour

• Texas BBQ

• Closing Remarks

91