Embed Size (px)

Citation preview

Casualty Exposure Rating

Chris Svendsgaard, Swiss ReCasualty Exposure RatingCARe Boot Camp 7-28-05

Page 2

Outline

Basics of Exposure-Rating

Practical Issues

Chris Svendsgaard, Swiss ReCasualty Exposure RatingCARe Boot Camp 7-28-05

Page 3

Basics of Exposure-Rating

What is exposure-rating?

Why do it?

How

Chris Svendsgaard, Swiss ReCasualty Exposure RatingCARe Boot Camp 7-28-05

Page 4

What is Exposure Rating?

An estimate of the covered Loss + ALAE in an excess layer

Based on reinsured information

– Policy Limits

– Insured characteristics (hazard)

But not

– Reinsured loss experience

Chris Svendsgaard, Swiss ReCasualty Exposure RatingCARe Boot Camp 7-28-05

Page 5

Typical Submission Data

Chris Svendsgaard, Swiss ReCasualty Exposure RatingCARe Boot Camp 7-28-05

Policy Limit Range

Bottomto Top

Policy Count

Premium ($000)

1 0 250,000 7 20

2 250,001 500,000 100 250

3 500,001 1,000,000 200 700

4 1,000,001 2,000,000 700 3,500

5 2,000,001 5,000,000 30 500

Page 6

Typical output of exposure rating

Chris Svendsgaard, Swiss ReCasualty Exposure RatingCARe Boot Camp 7-28-05

Policy Limit RangeLayer = 500x500

Bottom to Top

Loss To Layer ($000)

1 0 250,000 0

2 250,001 500,000 0

3 500,001 1,000,000 200

4 1,000,001 2,000,000 700

5 2,000,001 5,000,000 100

Page 7

Why Exposure-Rate

Provide complement of credibility for experience rate

Relate higher layer to lower (credible) layer

Price “Free Cover”

– Layer higher than largest trended claim in the experience

Adjust experience rate for shift in limits/deductibles

“Use eclectic methods”

– Armstrong, Long-Range Forecasting

Chris Svendsgaard, Swiss ReCasualty Exposure RatingCARe Boot Camp 7-28-05

Page 8

Why Exposure-Rate

Why experience rate not 100% credible/relevant

– Volume

– Shift in business

– Difficulties in estimating

- Trend, Development, On-leveling, Data problems

Pricing “Free Cover” is a case where experience rate given 0% credibility

Chris Svendsgaard, Swiss ReCasualty Exposure RatingCARe Boot Camp 7-28-05

Page 9

How to exposure-rate

How

– Estimate fgu loss

– Use severity distribution to allocate to layers

Chris Svendsgaard, Swiss ReCasualty Exposure RatingCARe Boot Camp 7-28-05

Page 10

Estimate fgu loss

Fac: Extend exposures

– (Projected Exposures) x (Manual Rate)

Treaty: Loss ratio approach

– (Projected Subject Premium) x (Estimated Loss Ratio)

Chris Svendsgaard, Swiss ReCasualty Exposure RatingCARe Boot Camp 7-28-05

Page 11

Estimate fgu loss

Fac: Extend exposures

Manual Rate contains provisons for

– ALAE

– ULAE

– Profit

– Internal and external expense

which must be stripped out.

Should you INCLUDE (primary) experience mod?

Some LOB’s and some classes of business must be judgementally estimated

– E.g., “a-rated” Products

Chris Svendsgaard, Swiss ReCasualty Exposure RatingCARe Boot Camp 7-28-05

Page 12

Estimate fgu loss

Treaty: Projected subject premium x loss ratio

Loss ratio sources

– Client internal data

– Client Annual Statement data

– Peer group AS data

– Industry AS data

– Rate filings?

– Underwriting audit

Chris Svendsgaard, Swiss ReCasualty Exposure RatingCARe Boot Camp 7-28-05

Page 13

Estimating Loss Ratios-Issues

Problems with Annual Statement data

– AS LOB, not program

– Net (mostly)

Reliability of data

– Relevance

– Predicted vs achieved rate-level changes

– As-if data

Is the loss ratio the same for all policy limits?

(ditto) tables

Chris Svendsgaard, Swiss ReCasualty Exposure RatingCARe Boot Camp 7-28-05

Page 14

Use severity distribution to allocate fgu expected loss to layers

What exposes the layer?

Using the “LEV” function

Why not use ILFs?

Chris Svendsgaard, Swiss ReCasualty Exposure RatingCARe Boot Camp 7-28-05

Page 15

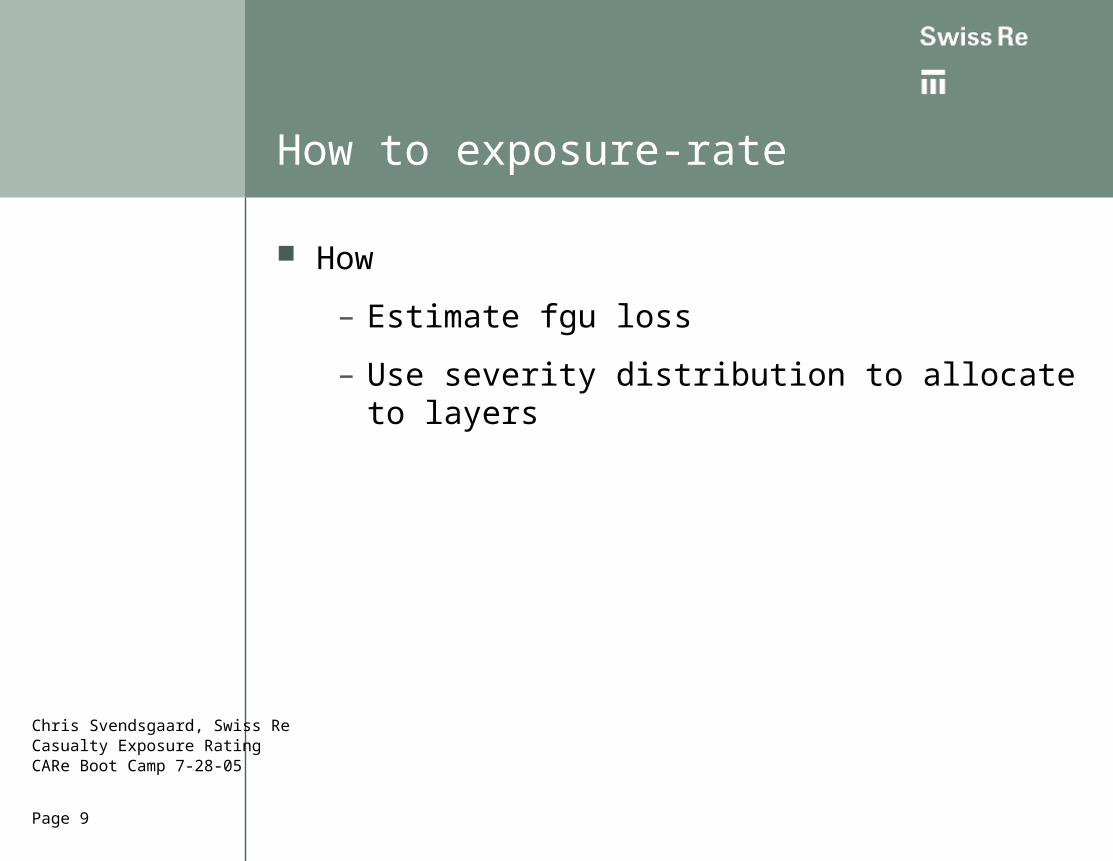

What exposes the layer?

Chris Svendsgaard, Swiss ReCasualty Exposure RatingCARe Boot Camp 7-28-05

A B C

Policy Limit A

Policy Limit B

Policy Limit C

Page 16

What exposes the layer?

Chris Svendsgaard, Swiss ReCasualty Exposure RatingCARe Boot Camp 7-28-05

A B C

Top of Layer

Bottom of Layer

Policy Limit A

Policy Limit B

Policy Limit C

Page 17

What exposes the layer?

Chris Svendsgaard, Swiss ReCasualty Exposure RatingCARe Boot Camp 7-28-05

A B C

Top of Layer

Bottom of Layer

Policy Limit A

Policy Limit B

Policy Limit C

Page 18

What exposes the layer?

Chris Svendsgaard, Swiss ReCasualty Exposure RatingCARe Boot Camp 7-28-05

A B C

Top of Layer

Bottom of Layer

Policy Limit A

Policy Limit B

Policy Limit C

“Top”

Page 19

What exposes the layer?

Chris Svendsgaard, Swiss ReCasualty Exposure RatingCARe Boot Camp 7-28-05

A B C

Top of Layer

Bottom of Layer

Policy Limit A

Policy Limit B

Policy Limit C

“Bottom”

Page 20

Contribution to expected losses

Contribution to expected layer losses from policy =

FGU losses up to “Top” – FGU losses up to “Bottom”

Contribution to all expected losses from policy =

FGU losses up to policy limit*

______________________________________________

*assuming no deductible, SIRChris Svendsgaard, Swiss ReCasualty Exposure RatingCARe Boot Camp 7-28-05

Page 21

Contribution to expected losses

Contribution to expected layer losses from policy =

{LEV(“Top”) – LEV(“Bottom”)} x frequency

Contribution to all expected losses from policy =

{LEV(Policy Limit) – LEV(0*)} x frequency

______________________________________________

*assuming no deductible, SIR

Chris Svendsgaard, Swiss ReCasualty Exposure RatingCARe Boot Camp 7-28-05

Page 22

What is a LEV?

Limited Expected Value function

– LEV(k)

- = “Losses up to k”

- Expected loss fgu, up to the value k, per ground-up claim

- Also written E(X; k)

- Also written LAS(k)

- (Limited Avg Sev)

Chris Svendsgaard, Swiss ReCasualty Exposure RatingCARe Boot Camp 7-28-05

Page 23

Contribution to expected losses

Contribution to expected layer losses from policy =

{LEV(“Top”) – LEV(“Bottom”)} x frequency

Contribution to all expected losses from policy =

{LEV(Policy Limit) – LEV(0*)} x frequency

______________________________________________

The FRACTION of fgu losses that gets into the layer does not depend on the frequency. When you divide, it drops out. Only need the LEV.

Note that aggregate limits could make this statement false.

Chris Svendsgaard, Swiss ReCasualty Exposure RatingCARe Boot Camp 7-28-05

Page 24

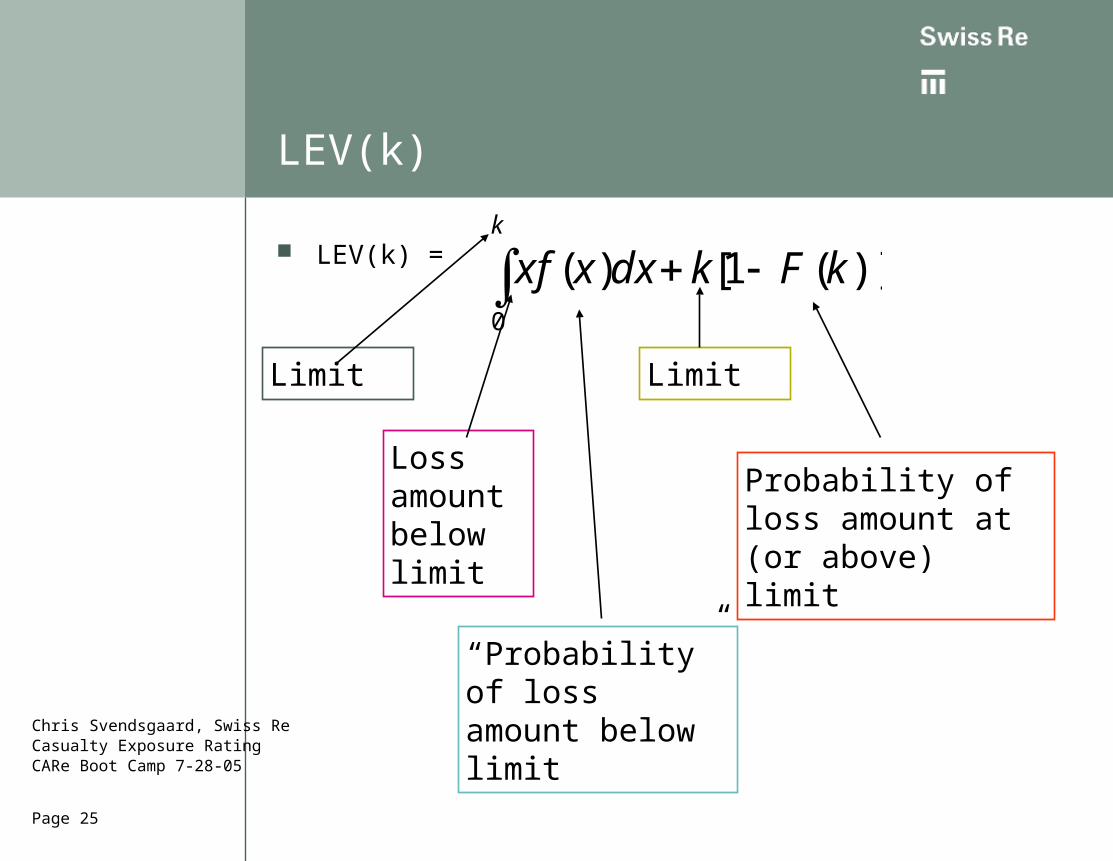

LEV(k)

LEV(k) =

X = random severity amount

x = realization of X

F(x) = cdf of x = Prob (X <=x)

f(x) = pdf of x

k = “limit”

Chris Svendsgaard, Swiss ReCasualty Exposure RatingCARe Boot Camp 7-28-05

k

kFkdxxxf0

)](1[)(

Page 25

LEV(k)

LEV(k) =

Chris Svendsgaard, Swiss ReCasualty Exposure RatingCARe Boot Camp 7-28-05

k

kFkdxxxf0

)](1[)(

Limit

Loss amount below limit

“Probability” of loss amount below limit

Limit

Probability of loss amount at (or above) limit

Page 26

Why use LEV function

Difference LEVs to get losses in layer

If expect λ losses from ground-up (fgu) then loss to layer A xs B is

Chris Svendsgaard, Swiss ReCasualty Exposure RatingCARe Boot Camp 7-28-05

))](1[)()(

BA

B

BAFAdxxfBx

Page 27

Why use LEV function (cont)

Chris Svendsgaard, Swiss ReCasualty Exposure RatingCARe Boot Camp 7-28-05

))](1[)()(

BA

B

BAFAdxxfBx

)](1[)](1[)()( BFBBAFAdxxfxBA

B

)]()([ BLEVBALEV

Page 28

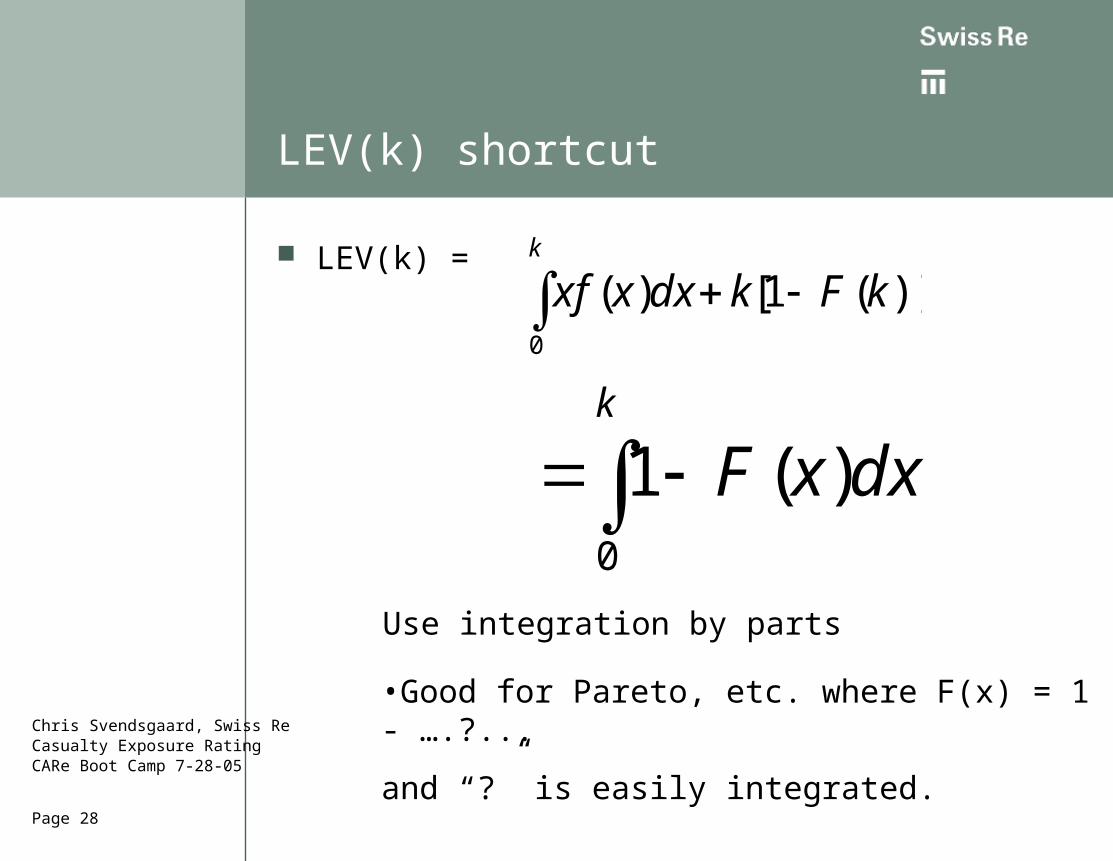

LEV(k) shortcut

LEV(k) =

k

kFkdxxxf0

)](1[)(

Chris Svendsgaard, Swiss ReCasualty Exposure RatingCARe Boot Camp 7-28-05

k

dxxF0

)(1

Use integration by parts

•Good for Pareto, etc. where F(x) = 1 - ….?...

and “?” is easily integrated.

Page 29

Why not use ILFs?

ILFs are meant for all costs, not just losses + ALAE

– ISO ILF = Ratio (all costs at Policy Limit) to (all costs at Basic Limit)

Using ISO ILFs:

– ISO Risk Load gets in

– ULAE creeps in

– Aggregate limits distort values (depending on which ILFs you use)

– ALAE drops out (because is loaded 100% in basic limit)

– Reinsurance treatment of ALAE not reflected

Page 30

Practical Issues

Submission data issues

Trend in limits

Treatment of ALAE

Gaps in exposure-rating

How good is the severity distribution?

Chris Svendsgaard, Swiss ReCasualty Exposure RatingCARe Boot Camp 7-28-05

Page 31

Submission Data

Typical Submission Data

Chris Svendsgaard, Swiss ReCasualty Exposure RatingCARe Boot Camp 7-28-05

Policy Limit Range

Bottomto Top

Policy Count Prem %

1 0 250,000 7 0.1%

2 250,001 500,000 100 2%

3 500,001 1,000,000 200 10%

4 1,000,001 2,000,000 700 80%

5 2,000,001 5,000,000 30 2%

Page 32

Submission Data

Things to look out for

Policy Limit Ranges

– But limits are round #’s

Numbers do not add up

– Written premium vs. Earned

– Historical vs. projected

Missing data

– Post-merger

Chris Svendsgaard, Swiss ReCasualty Exposure RatingCARe Boot Camp 7-28-05

Page 33

Submission Data

More things to look out for

Policy Limit Warrant

No information about ILF table breakdown

– Or, worse, underwriter’s vague feeling

Chris Svendsgaard, Swiss ReCasualty Exposure RatingCARe Boot Camp 7-28-05

Page 34

ISO Increase Limits Factors

By Table

– Prem/Ops

- 1, 2, 3 x State Group

– Products

- A, B, C

– C. Auto

- Wt Class x State Group

Chris Svendsgaard, Swiss ReCasualty Exposure RatingCARe Boot Camp 7-28-05

Page 35

Policy Limit Trend

“Policy limits trend with inflation”

How trend round numbers?

Chris Svendsgaard, Swiss ReCasualty Exposure RatingCARe Boot Camp 7-28-05

Question

You are covering the 1 x 1 layer: By how much will your exposure change if policy limits are trending at 5% per annum?

Page 37

Avg Policy Limit over time (fake ISO data)

0

100

200

300

400

500

600

700

1980

1982

1984

1986

1988

1990

1992

1994

1996

AvgLimit

Page 38

Simple Example

Limit 1,000,000 2,000,000 Average Limit

2001 Weight

95% 5% 1,050,000

2002 Weight

90% 10% 1,100,000

Page 39

Treatment of ALAE

Ways reinsurance can cover ALAE

– Pro-rata

– “Added To”

– other

How to handle

Page 40

Joint model

Chris Svendsgaard, Swiss ReCasualty Exposure RatingCARe Boot Camp 7-28-05

0

0 0

),(),(

),(),(

PL

tPolicyLimi

dIdAAIfAPLg

dIdAAIfAIg

g(I,A) = reinsurance payment given indemnity I and ALAE A.

Expected reinsurance payment per fgu claim is

Good Luck.

Page 41

Simpler (but less accurate) ways to handle ALAE

Pro-rata: Apply appropriate ALAE/Indmenity ratio

Added to:

– Twiddle the severity distribution, and (possibly) limits, retentions, etc.

– DOES NOT pick up all exposure to highest layers

Chris Svendsgaard, Swiss ReCasualty Exposure RatingCARe Boot Camp 7-28-05

Page 42

Gaps in traditional Exposure-Rating

Does not estimate

– Clash

– Extra-Contractual Obligations (ECO)

– Declatory Judgement (DJ) expense

- Is not ALAE?

– “Cat” potential?

- Asbestos, DES, . . .

Chris Svendsgaard, Swiss ReCasualty Exposure RatingCARe Boot Camp 7-28-05

Page 43

How good is the severity distribution?

ISO data is sparse above (say) $5,000,000

– Umbrella/XS data is often not reported to ISO

Mixed exponential maxes out at $10,000,000

Big swings in exposure rate for many tables 20042005

Non-bureau:

– No distribution

– ILF’s from client: do they care? Are they ept?

- Is “ept” a word?Chris Svendsgaard, Swiss ReCasualty Exposure RatingCARe Boot Camp 7-28-05

Page 44

How good is the severity distribution?

How reflect parameter risk?

How reflect possible “anti-selection” effects?

– They buy big limits because they need to . . .?

Chris Svendsgaard, Swiss ReCasualty Exposure RatingCARe Boot Camp 7-28-05