Embed Size (px)

Citation preview

C A S H E W Shigh l igh ts o f the cashew indus t r y

presented by Red River Foods, Inc.

JUNE 2011

Red River Foods, Inc. June 2011 1

Peru

Brazil

SenegalGuinea-BissauIvory CoastGhanaBeninNigeriaMaliTogoGuineaBurkina FasoGambia

ThailandMalaysiaCambodia

Indonesia

0° 0°EQUATOR

PhilippinesVietnamIndia

Sri LankaKenya

Tanzania

Mozambique

Madagascar

major cashew kernel trade

from India & Vietnam

To Europe

To Middle East

To Europe

from India

to India & Vietnam

major raw cashew trade

A WORLD VIEW The cashew is native to northeastern Brazil. In the mid-to-late 1500s, Portuguese traders and explorers introduced the cashew tree

to India and to the east coast of Africa in an area that is now Mozambique. In Africa, the tree was spread along the east coast (today,

Kenya and Tanzania) and was later introduced to the continent’s west coast, where it presently grows from Senegal to Nigeria. Portuguese

and Spanish traders also introduced the cashew tree to Southeast Asia. The cashew tree now grows in tropical climates of about thirty

countries across the globe within a band approximately 25-30 degrees north and south latitude of the equator. India is the largest

single producer of cashew nuts while West Africa--principally Ivory Coast, Benin, and Guinea-Bissau—is the largest regional producer.

Vietnam, Brazil, and East Africa are the other major sources of production. Indonesia has become a major producer and exporter in

Southeast Asia.

The world map below identifi es countries with estimated annual raw cashew production of one or more million kgs in 2011. Countries

which are identifi ed in bold are major producers and are the most important exporters of either raw cashews and/or processed cashew

kernels. The cashew kernel trade and the raw cashew trade are highlighted, showing the major kernel export destinations from India,

Vietnam, and Brazil and the sources of Indian and Vietnamese raw cashew imports.

The fi nal product: Roasted/Salted Cashew Nuts

2 Highlights of the cashew industry

INDUSTRY PERSPECTIVEThe international cashew market never suffers from a lack of uncertainty. The last eighteen months witnessed a “tightening” of the market

in all its many aspects, from supply to pricing, from collection to procurement to fi nancing to processing to shipping to inspection…

throughout the chain, from tree to table. Not to mention weather-related effects on crops worldwide. As we publish this brochure, the

industry is dealing with:

• Expanding quality and food safety requirements

• Tightening supplies as Indian domestic consumption rises and 2010-2011 crops from all major origins are below expectations

• Rising demand in China, adding further pressure on world supplies

• Halts and delays in major West African raw shipments to India and Vietnam because of civil war in the Ivory Coast

• The need for--but uncertainty about--the reliability of West African production and shipments because of sporadic

civil unrest

• Defaults and delays in shipments from India and Vietnam

• Record high prices

In 2010 Middle Eastern markets (including Turkey) remained strong with Indian exports to the region down only slightly to 24.9 million

kgs from 27.6 million kgs in 2009. In the meantime, Vietnamese exports to the region rose from 6.8 to 8.1 million kgs and Brazilian

shipments to the Middle East, though relatively minor, increased from 1.9 to 2.2 million kgs. The Vietnamese cross-border trade with

China grew by one-third between 2009 and 2010, from 32 to 42 million kgs. U.S. demand remained strong with imports increasing

from 117 to 119 million kgs. European Union imports from the three major origins were down less than one million kgs: 71.9 million

kgs in 2009 vs. 71.2 million kgs in 2010.

Thus, even without weather-related crop diffi culties, world demand remains strong and generally exceeds supply. Importantly, at any

given time demand is likely to exceed the availability of raw cashews and kernels, which could mean periodic defi cits and high prices

for particular grades.

Vacuum Sealed Bags

Red River Foods, Inc. June 2011 3

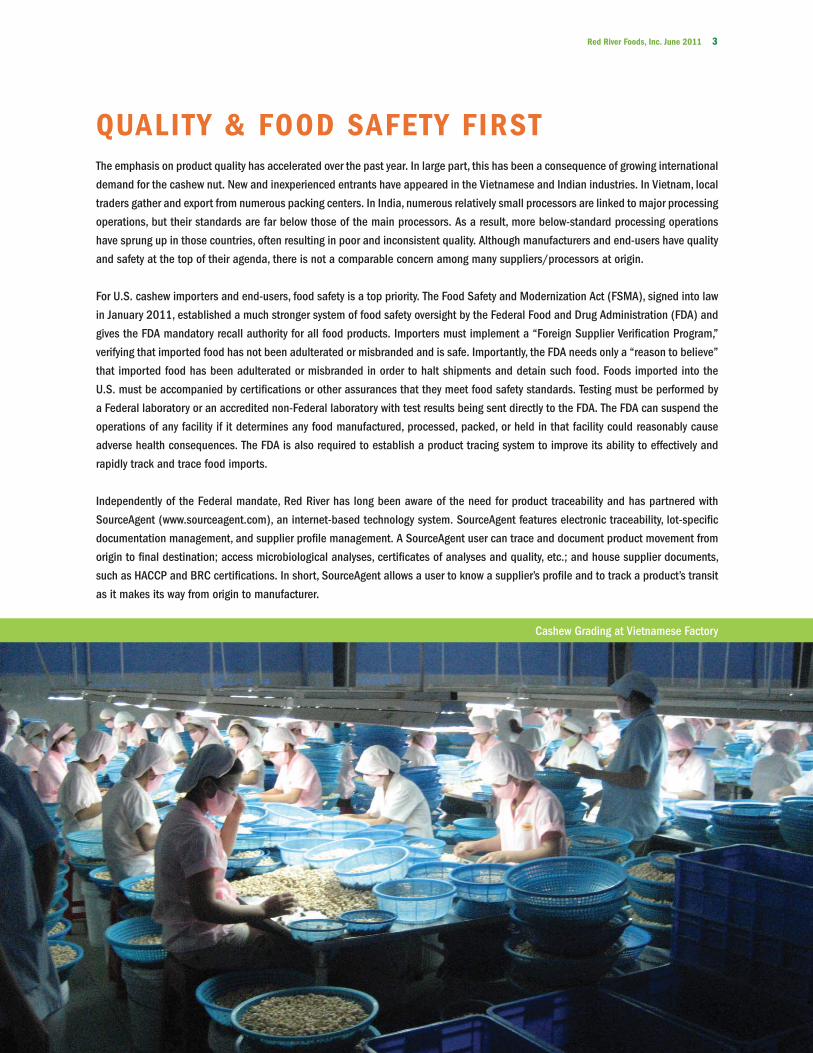

QUALITY & FOOD SAFETY FIRSTThe emphasis on product quality has accelerated over the past year. In large part, this has been a consequence of growing international

demand for the cashew nut. New and inexperienced entrants have appeared in the Vietnamese and Indian industries. In Vietnam, local

traders gather and export from numerous packing centers. In India, numerous relatively small processors are linked to major processing

operations, but their standards are far below those of the main processors. As a result, more below-standard processing operations

have sprung up in those countries, often resulting in poor and inconsistent quality. Although manufacturers and end-users have quality

and safety at the top of their agenda, there is not a comparable concern among many suppliers/processors at origin.

For U.S. cashew importers and end-users, food safety is a top priority. The Food Safety and Modernization Act (FSMA), signed into law

in January 2011, established a much stronger system of food safety oversight by the Federal Food and Drug Administration (FDA) and

gives the FDA mandatory recall authority for all food products. Importers must implement a “Foreign Supplier Verifi cation Program,”

verifying that imported food has not been adulterated or misbranded and is safe. Importantly, the FDA needs only a “reason to believe”

that imported food has been adulterated or misbranded in order to halt shipments and detain such food. Foods imported into the

U.S. must be accompanied by certifi cations or other assurances that they meet food safety standards. Testing must be performed by

a Federal laboratory or an accredited non-Federal laboratory with test results being sent directly to the FDA. The FDA can suspend the

operations of any facility if it determines any food manufactured, processed, packed, or held in that facility could reasonably cause

adverse health consequences. The FDA is also required to establish a product tracing system to improve its ability to effectively and

rapidly track and trace food imports.

Independently of the Federal mandate, Red River has long been aware of the need for product traceability and has partnered with

SourceAgent (www.sourceagent.com), an internet-based technology system. SourceAgent features electronic traceability, lot-specifi c

documentation management, and supplier profi le management. A SourceAgent user can trace and document product movement from

origin to fi nal destination; access microbiological analyses, certifi cates of analyses and quality, etc.; and house supplier documents,

such as HACCP and BRC certifi cations. In short, SourceAgent allows a user to know a supplier’s profi le and to track a product’s transit

as it makes its way from origin to manufacturer.

Cashew Grading at Vietnamese Factory

4 Highlights of the cashew industry

The world cashew trade is balanced on the annual cashew production cycle. Short or poor crops anywhere or abnormal weather conditions distort the trade pattern, consequently affecting prices. Vietnam produces the year’s fi rst crop, and shortly thereafter India’s crop comes in. At approximately the same time, West African crops are being harvested. Harvest of the Brazilian and East African crops begins in August/September, tying the trade over until the new crops of Vietnam, India, and West Africa are harvested early the following year.

Disruptions in the international market are not uncommon, but the 2010-2011 seasons put unusual pressures on the trade. The 2011 Brazilian crop of approximately 155 million kgs was only half the normal production of 300 million kgs, sharply reducing the amount available for orders from November through February. Wet weather in both India and Vietnam in early 2011 delayed early harvesting and interfered with drying of the raw seed.

Rising Indian domestic consumption has drawn down the amount of kernels available to the trade as Indian export tonnage declines, and Indian exports were down for the third consecutive year in 2010. With only limited processing capabilities, West Africa exports its raw seed to India and Vietnam. Civil disorder in the Ivory Coast early in 2011 introduced much uncertainty into availability of West African raw seed. Because of the resulting delay in shipments, the lack of storage space in the Ivory Coast raised questions about maintenance of seed quality. In turn, this contributed to Vietnamese and Indian suppliers holding out for higher prices. Thus, any one major disruption in the production cycle has multiple effects on the marketing of kernels.

Maturing Cashews

THE PRODUCTION CYCLE

JA

N FE

B

MAR

APR

MAY

JUN

JULA

UG

S E P

O C T

NO

V

DEC

Brazil

East Africa

India

Vietnam/W. Africa

FLOWERING

FLOWERING

FLOW

ERIN

GFL

OWER

ING

HARVESTING

HARV

ESTIN

G

HARV

ESTI

NG

HARVESTINGHARVESTING

HARVESTINGHARVESTING

Red River Foods, Inc. June 2011 5

HARVESTING SEASONSHarvesting seasons are generally similar in the producing countries, depending on their location relative to the equator. Countries

north of the equator, including India, Vietnam, and producers in West Africa, harvest from early in the calendar year to approximately

mid-year. Countries south of the equator, including Brazil and producers in East Africa, harvest from September or October to early in

the following calendar year.

Cashew Seed Drying in Vietnam

end of season

beginning of season Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

India

Vietnam

Benin

Guinea-Bissau

Ivory Coast

Nigeria

Togo

Brazil

Mozambique

Tanzania

Kenya

Mali

Ghana

Burkina Faso

Senegal

Gambia

Indonesia

Raw Seed Imports in Million Kgs

2006

572200

2007

599220

2008

649250

2009

728300

2010

644404

IndiaVietnam

THE PRODUCTION CYCLE CONTINUED

6 Highlights of the cashew industry

R A W P R O D U C T I O N T R E N D SThe edible cashew kernel is encased within a kidney-shaped seed or pod at the bottom of a cashew “apple” (The “apple” is actually a stem.) Cashews are not harvested in the conventional sense. Once the cashew apple falls to the ground, the cashew seed is removed from the apple. Cashew seeds are gathered and taken to various collection points. From there they are delivered to a processing facility. After drying, the cashew kernel is separated from the seed either mechanically or by hand. Where mechanical separation takes place, primarily in Brazil, there is a higher percentage of broken grades.

Cashew production is extremely diffi cult to estimate, and production estimates have to be offered with caveats. Crop size estimates for any one producing country can vary signifi cantly because of the inherent diffi culties in accounting for output. Crops are harvested from trees growing in their natural habitat, as there are few plantations in most countries. Cross-border activity, particularly in West Africa, inhibit accurate accounting. Further, there is little processing in West African countries, hence there are few sources from which reasonable estimates can be ventured. Cashew seeds are not weighed during any of the collecting, buying, or transfer stages. After being gathered and brought to a series of collection points, the cashews are delivered to processors. The crop size is frequently estimated after the raw cashews have been processed and some indication of average kernel weight has been ascertained. Thus, raw cashew estimates are extrapolations from processing outcomes and the “best guesses” of those active in the industry. Production estimates would be more accurately defi ned as collection estimates.

0

500

1,000

1,500

2,000

2,500

3,000

1990 1995 2000 2005 2010 2007 2008 2009 2010 2011P

Mil

lio

n K

gs

Year

Asia East Africa West Africa Cent/So Amer

source: Red River, Industry, FAO

Estimated World Raw Cashew Production by Major Region

Cashew Apples

Red River Foods, Inc. June 2011 7

Estimated World Raw Cashew Production by Major Origins and Regions

0

500

1,000

1,500

2,000

2,500

3,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011P

Millio

n K

gs

Calendar Year

source: Red River; Industry, FAOIndia Vietnam Brazil East Afr West Afr Other

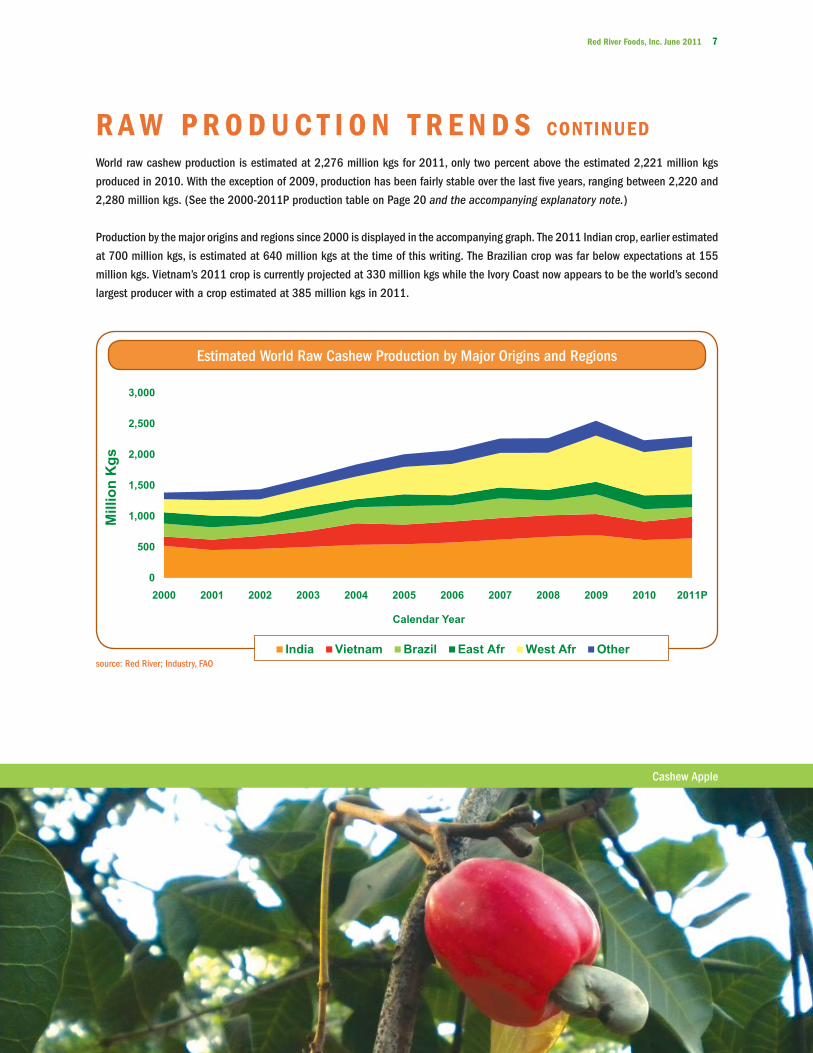

World raw cashew production is estimated at 2,276 million kgs for 2011, only two percent above the estimated 2,221 million kgs

produced in 2010. With the exception of 2009, production has been fairly stable over the last fi ve years, ranging between 2,220 and

2,280 million kgs. (See the 2000-2011P production table on Page 20 and the accompanying explanatory note.)

Production by the major origins and regions since 2000 is displayed in the accompanying graph. The 2011 Indian crop, earlier estimated

at 700 million kgs, is estimated at 640 million kgs at the time of this writing. The Brazilian crop was far below expectations at 155

million kgs. Vietnam’s 2011 crop is currently projected at 330 million kgs while the Ivory Coast now appears to be the world’s second

largest producer with a crop estimated at 385 million kgs in 2011.

R A W P R O D U C T I O N T R E N D S CONTINUED

Cashew Apple

8 Highlights of the cashew industry

Generally, cashew kernel yields range from about 20 to 24

percent. Thus, one metric ton of raw cashews can yield between

200 and 240 kgs of edible kernel wholes and pieces after

processing, depending on country of origin. A crop that yields 1

million kgs of cashew kernels, for example, might be estimated

to have been 4.2 to 5.0 million kgs of raw production.

The adjacent table displays the estimated average amounts (in

kgs) of exportable grade kernels produced per metric ton from

the three major exporting countries. These percentages may vary

from year to year and even during the same season because

of weather conditions, the quality of the seed, the time of the

season when the crop is being processed, and the capabilities

of the processor.

In India, for example, each metric ton of raw cashew seed

produced and processed in that country yields, on average, about

230 kgs (23 percent) of exportable grade kernels. Thus, if the

Indian 2011 crop was 640,000 metric tons of raw cashew nuts

and we applied the percentage yield for the country as a whole,

the approximate outturn would have been about 147 million kgs

of exportable grade wholes and pieces.

The accompanying graph displays the

estimated percentage of whole and broken

grades produced by the three major

producers/exporters. (These percentages

result after peeling losses and rejects are

discounted.) The high percentage of broken

grades in Brazil is the result of mechanical

processing. Most processing in India and

Vietnam is labor intensive, done by hand.

Estimated Percentage of Whole and Broken Gradesproduced by major processors/exporters

per metric ton of export kernels

80%

53%

75%

20%

47%

25%

Vietnam

Brazil

India

Whole Brokensource: Industry

EXPORTABLE GRADES

Senegal

Nigeria, Kenya

Mozambique

Guinea Bissau, Togo

Processing Country Country of Origin kgs

India (Kerala State) 250

India (Country) 230

India Indonesia 240

240

230

230

220

200

Brazil Brazil 210

Vietnam Vietnam 230

Ivory Coast, Benin

Estimated Amount of Export-Quality Kernelsproduced by major processors/exporters

per metric ton of raw cashew nuts

source: Industry

Red River Foods, Inc. June 2011 9

U.S. IMPORTS FOR CONSUMPTIONCashews constitute the single largest segment of the

U.S. shelled tree nut import market. Between 2006

and 2010, two thirds of all U.S. imports were cashews.

(The accompanying pie chart does not include tree nuts

imported in-shell, primarily pecans and brazil nuts).

Cashew imports increased in 2010 to 119 million kgs

from 117 in 2009. For the fi rst four months of 2011,

cashew imports were 34.6 million kgs vs. 32.2 million

kgs during the same period in 2010. If the pace of

imports during 2011 mirrors that of 2010, total imports

for the year could be about 128 million kgs. As of April

2011, imports from Vietnam were on a pace to exceed

70 million kgs, much higher than the 2010 high of 58

million kgs and would represent well over 50 percent of

all U.S. cashew imports.

The accompanying graph clearly displays the trend of U.S. imports since 1990. Imports from Brazil have remained relatively steady

compared to the shifts in import totals from India and Vietnam. Imports from Vietnam have been increasing annually since 2006, but

U.S. imports from India have fallen annually since a peak of 58 million kgs in 2004. In 2009 and 2010, U.S. imports of Indian cashews

were only 30.6 million kgs, a drop of over 27 million kgs over a fi ve year period.

U.S. Cashew Imports for Consumptionfrom India, Vietnam, and Brazil

0

20

40

60

80

100

120

140

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Millio

n K

gs

Calendar Year

India Vietnam Brazil Other

U.S. Tree Nut Imports 2010shelled weight in million kgs

Filberts3.3 Brazils

10.9

Macs 7.2

Chesnuts 4.9

Pine Nuts1.2

Pecans29.1

Other6.0

Cashews119.1

Filberts3.3 Brazils

10.9

Macs

Ch

Pi

Pecan29.1

Other6.0

Cashews119.1

source: U.S. Department of Agriculture181.7 Million Kgs

source: U.S. Department of Agriculture

10 Highlights of the cashew industry

The graph below depicts annual import volumes from each of the three major origins and the average annual CIF values of those

imports. Average CIF values from all three origins have been on an upward trend since 2003, with import values of Indian cashews

higher than those of both Brazil and Vietnam.

U.S. IMPORTS CONTINUED

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

$7.00

0

10

20

30

40

50

60

70

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Avg

CIF

Va

l P

er

Kg

Millio

n K

gs

Calendar Year

India Vietnam Brazil India Vietnam Brazil

U.S. Cashew Imports for Consumptionfrom India, Vietnam, and Brazil

Over the past year, the monthly average CIF values of total imports rose from $5.39 per kg in April 2010 to a record high in April 2011

of $8.03 per kg, an increase of $2.64 per kg. During this period, the monthly average CIF values of imports from Brazil and India

reached highs of $8.39 and $8.14, respectively, in March 2011. The monthly average CIF values of imports from Vietnam peaked at

$7.95 per kg in April 2011.

Source: U.S. Department of Agriculture

$5.39 $5.55 $5.69 $5.84 $6.02 $6.23 $6.06$6.67 $6.88

$7.39$7.76 $7.83 $8.03

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

$7.00

$8.00

$9.00

Apr 10 May 10 Jun 10 Jul 10 Aug 10 Sep 10 Oct 10 Nov 10 Dec 10 Jan 11 Feb 11 Mar 11 Apr 11

Do

lla

rs P

er

Kg

Month & Year

U.S. Cashew Imports Monthly Average CIF Import Values

Source: U.S. Department of Agriculture

Red River Foods, Inc. June 2011 11

U.S. IMPORTS CONTINUED

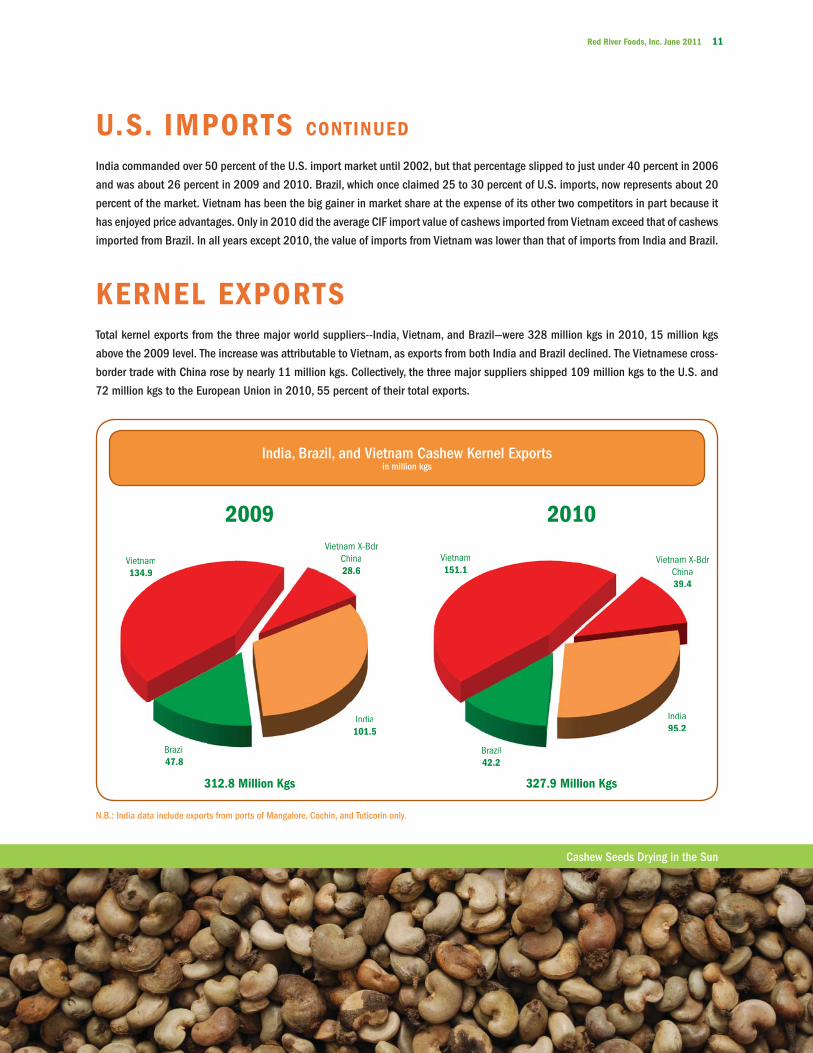

KERNEL EXPORTSTotal kernel exports from the three major world suppliers--India, Vietnam, and Brazil—were 328 million kgs in 2010, 15 million kgs

above the 2009 level. The increase was attributable to Vietnam, as exports from both India and Brazil declined. The Vietnamese cross-

border trade with China rose by nearly 11 million kgs. Collectively, the three major suppliers shipped 109 million kgs to the U.S. and

72 million kgs to the European Union in 2010, 55 percent of their total exports.

India commanded over 50 percent of the U.S. import market until 2002, but that percentage slipped to just under 40 percent in 2006

and was about 26 percent in 2009 and 2010. Brazil, which once claimed 25 to 30 percent of U.S. imports, now represents about 20

percent of the market. Vietnam has been the big gainer in market share at the expense of its other two competitors in part because it

has enjoyed price advantages. Only in 2010 did the average CIF import value of cashews imported from Vietnam exceed that of cashews

imported from Brazil. In all years except 2010, the value of imports from Vietnam was lower than that of imports from India and Brazil.

India, Brazil, and Vietnam Cashew Kernel Exports in million kgs

Vietnam134.9

Vietnam151.1

Vietnam X-BdrChina28.6

Vietnam X-BdrChina39.4

India101.5

India95.2

Brazil47.8

Brazil42.2

Vietnam134.9

China28.6

India101.5

Brazil

Vietnam151.1

Vietnam X-BdrChina39.4

India95.2

Brazil

N.B.: India data include exports from ports of Mangalore, Cochin, and Tuticorin only.

2009

312.8 Million Kgs

2010

327.9 Million Kgs

Cashew Seeds Drying in the Sun

12 Highlights of the cashew industry

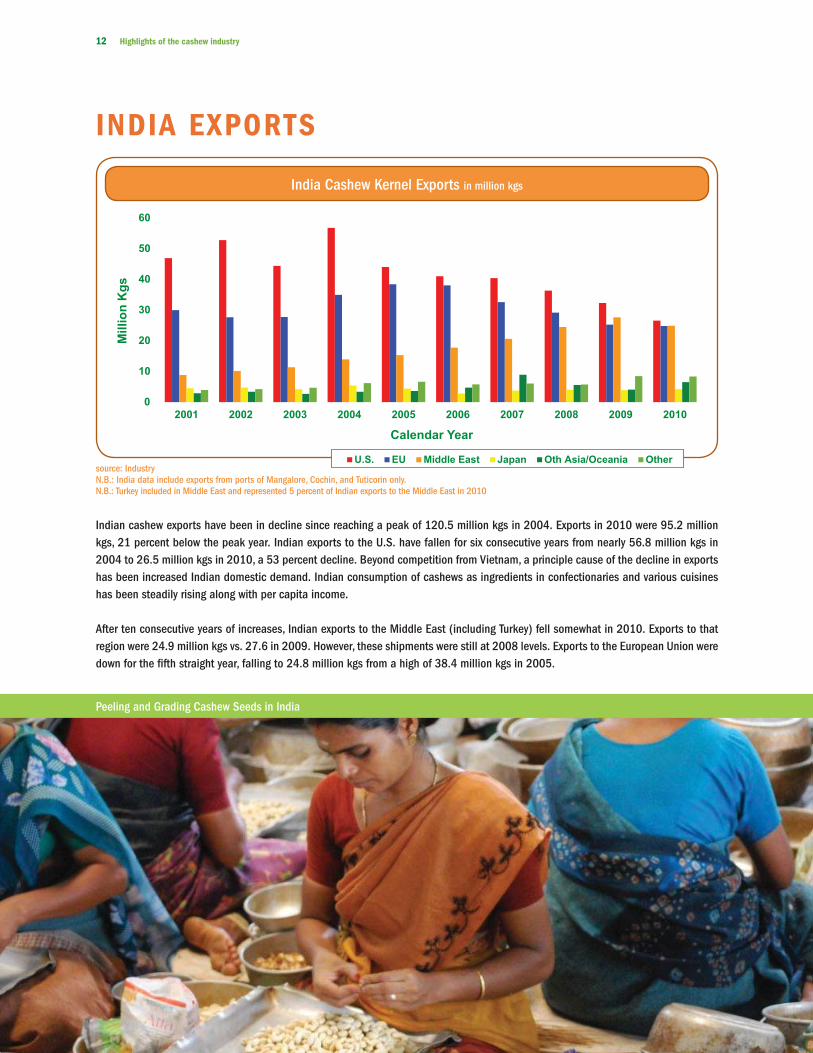

Indian cashew exports have been in decline since reaching a peak of 120.5 million kgs in 2004. Exports in 2010 were 95.2 million kgs, 21 percent below the peak year. Indian exports to the U.S. have fallen for six consecutive years from nearly 56.8 million kgs in 2004 to 26.5 million kgs in 2010, a 53 percent decline. Beyond competition from Vietnam, a principle cause of the decline in exports has been increased Indian domestic demand. Indian consumption of cashews as ingredients in confectionaries and various cuisines has been steadily rising along with per capita income.

After ten consecutive years of increases, Indian exports to the Middle East (including Turkey) fell somewhat in 2010. Exports to that region were 24.9 million kgs vs. 27.6 in 2009. However, these shipments were still at 2008 levels. Exports to the European Union were down for the fi fth straight year, falling to 24.8 million kgs from a high of 38.4 million kgs in 2005.

India Cashew Kernel Exports in million kgs

0

10

20

30

40

50

60

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Mil

lio

n K

gs

Calendar Year

U.S. EU Middle East Japan Oth Asia/Oceania Othersource: IndustryN.B.: India data include exports from ports of Mangalore, Cochin, and Tuticorin only.N.B.: Turkey included in Middle East and represented 5 percent of Indian exports to the Middle East in 2010

INDIA EXPORTS

Peeling and Grading Cashew Seeds in India

Red River Foods, Inc. June 2011 13

BRAZIL EXPORTS Brazilian exports fell to 42 million kgs in 2010 from nearly 48 million kgs in 2009. Sharply reduced exports to the U.S. accounted

for nearly all the decline. Exports to the U.S. fell over 20 percent from 30.5 to 24 million kgs. Since 2000 the U.S. share of Brazilian

exports has been falling: in 2000, 78 percent of Brazilian shipments were destined for the U.S.; in 2010 the U.S. accounted for 57

percent of Brazil’s cashew exports. The one other major destination for Brazilian cashews is the European Union; exports to the EU were

essentially stable in 2009-2010, 8.8 v. 8.5 million kgs. Over the same 2000-2010 period, exports to the EU have risen from about 10

percent of Brazil’s total shipments to about 20 percent. This increase is partially the result of the expansion of the European Union;

ten countries joined the EU in 2004 and two additional countries joined in 2007.

Brazil Cashew Kernel Exports in million kgs

0

5

10

15

20

25

30

35

40

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Millio

n K

gs

Calendar Year

USA Canada EU 15/25 Othersource: Industry

Cashew Seeds at Brazilian Factory

14 Highlights of the cashew industry

VIETNAM EXPORTSVietnam’s share of the international market continues to grow, particularly its share of U.S. imports. Total Vietnamese exports,

including the China cross-border trade, rose 27 million kgs between 2009 and 2010, from 163.5 to 190.5 million kgs. The China

cross-border trade jumped 38 percent from 28.6 to 39.4 million kgs. While exports to the European Union (EU) were the same at

37.9 million kgs in 2009 and 2010, exports to the U.S. rose from 50 to 58 million kgs. With the exception of the EU, Vietnamese

exports rose across the board, including shipments into the former USSR and the Middle East (including Turkey).

In 2010, wholes constituted 73 percent of cashew exports while pieces, butts, and splits accounted for 26 percent (excluding the China

cross-border trade.) At nearly 67 million kgs, exports of W320s represented 44 percent of total Vietnamese shipments while exports

of W240s totaled nearly 29 million kgs or 19 percent.

Vietnam’s Cashew Exports by region/country

source: Industry

USA50.3

USA58

Fmr USSR5.7

Fmr USSR6.9

EU37.9

EU37.9

Other6.7 Other

7.6

China31.7

China42

Oceania13.7

Oceania14.7

Other Asia10.7

Other Asia15.3

Mid East6.8

Mid East8.1

2009

163.5 Million Kgs

2010

190.5 Million Kgs

Harvested Cashew Apples Baskets of Raw Seed

Red River Foods, Inc. June 2011 15

The African cashew industr y

could represent the single biggest

opportunity for the international

cashew market over the next two

decades. With growing domestic

consumption in Asia (particularly in

India and China), the industry will

need increased supplies, and Africa

represents the greatest potential

for additional cashew product.

However, the African industry will

need long-term investment and

development: a complete value-

added infrastructure from growing

and harvesting to processing and

marketing.

The lack of processing capacity is the single biggest obstacle to industry growth in Africa. Of the approximately 700 million kgs produced

in West Africa annually, only about ten percent is processed in that region. For the approximately 200 million kgs produced in East Africa,

processing capacity is variously estimated at 35 to 50 million kgs. Nearly all African production is processed in India and Vietnam.

0

100

200

300

400

500

600

700

800

900

1,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010P

Estimated African Cashew Production in million kgs

West Africa East Africasource: Industry / African Cashew Alliance

AFRICA

Africa

16 Highlights of the cashew industry

AFRICA CONTINUED

AFRICAN CASHEW

PRODUCERSWestBenin

Burkina FasoGhanaGuinea

Guinea-BissauIvory Coast

MaliNigeriaSenegal

The GambiaTogo

EastKenya

MadagascarMozambique

Tanzania

Numerous parties are working to improve various segments of the African industry. The focal point for individual companies; non-profits; and various government agencies, including the U.S. Peace Corps, is often the African Cashew Alliance (ACA). The Alliance, headquartered in Accra, Ghana, was organized in 2005 and became operational one year later. The purpose of the Alliance is to invigorate and promote the African cashew industry, with a particular focus on expanding the processing sector and improving quality. In 2009 the Alliance helped steer a $25 million grant from the Gates Foundation to Benin, Burkina Faso, Ivory Coast, Ghana, and Mozambique for development of their respective industries. Later that year the ACA received a grant from USAID/West Africa to assist cashew entrepreneurs in the region obtain access to fi nancing. In December 2010, USAID West Africa, the ACA and the Economic Community of West African States (ECOWAS) Bank of Investment and Development signed a Memorandum of Understanding to open access to long-term fi nancing to processors.

Production in West Africa is diffi cult to estimate, but it is clear there has been a marked increase in that region’s output. Production there has grown by over 200 percent since 2001. The Ivory Coast is the leading producer by far, with estimated 2011 production at 385 million kgs. Guinea-Bissau is the next largest producer at about 130 million kgs. Production in East Africa is about 200 million kgs, principally in Mozambique and Tanzania.

Estimated African Cashew Production in million kgs

source: African Cashew Alliance, Industry

Ivory CoastGuinea-Bissau

MozambiqueTanzania

NigeriaBenin

SenegalGhanaKenyaOther

Total

290.0100.0

92.674.480.037.517.512.5

5.026.0

735.5

320.0100.0

99.164.281.045.020.012.5

5.027.5

774.3

350.0136.0

96.095.0

100.0100.0

20.012.5

8.533.5

951.5

335.0150.0112.0

97.070.070.035.012.011.033.5

925.0

385.0130.0100.0100.0

85.090.035.012.0

8.033.5

978.5

2007 2008 2009 2010 2011P

African Sunset

Red River Foods, Inc. June 2011 17

PRICES The vertical bar graph below clearly depicts the volatility of the cashew market over the last fi ve years. After shifting upward in 2004 and 2005, average FOB export prices fell back in 2006 as supplies increased. However, prices began to increase again in mid-2007 as Vietnamese and Indian shippers delayed and then defaulted on their contracts. By year’s end, the average FOB export price had risen to nearly $5.70 per kg. Prices continued to increase in 2008 and surged to $7.40 per kg at mid-year. The causes were numerous: a short crop in Brazil; new and inexperienced processors in Vietnam; and Vietnamese/Indian defaults, demands for renegotiated contracts, and shipping delays. However, monthly average prices did fall back to just under $5.00 per kg by the fi nal months of the year. Prices began another upward swing in mid-2009 and by December averaged $6.35 per kg. Prices continued their upward trend in 2010, reaching new levels. By December, the average monthly price was slightly above $8.00 per kg. Prices continued to accelerate during the fi rst quarter of 2011 and reached a record high in March, exceeding $8.50 per kg. An expected decline in prices in April failed to materialize as raw seed shipments were delayed from the Ivory Coast because of civil strife. Extended rainy weather caused uncertainties about the availability and quality of Indian and Vietnamese crops. Adding to the price pressure was the extremely short Brazilian crop.

$8.53$8.50

$8.02$8.07$8.00

$7.50$7.41

$7.00

$6.50

$6.35$6.11

$6.00

$5.62 $5.67$5.82$5.51

$5.50

$5.00

$4.78$4.63

$4.92$4.54$4.50

$4.32$4.67$4.25

$4.43$4.30

$4.19 $4.25$4.00

$3.86

$3.73$3.50 $3.66Janto Mar

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Estimated Avg Annual FOB Price Ranges—Cashews W320s in USD/kg

source: Industry

18 Highlights of the cashew industry

The accompanying graph depicts the average quarterly price movement of W320 cashews since 1998. The price spike in 1999 was caused

by crop shortfalls and processors contracting in advance for more product than they were able to deliver. Many processors defaulted on

their commitments, leaving importers with an eleventh hour need to fulfi ll their own obligations. The result was extremely strong demand

which led to intense upward pressure on prices. The price plunge in 2000 refl ected higher worldwide supplies. The estimated average

quarterly prices fell to about $4.40 per kg by 2001, and remained at historic lows, between $3.75 and $4.20 per kg, through 2003. Thus,

the market was relatively stable for these three years.

Cashew prices began increasing in early 2004 in part because of the collective efforts of Indian packers to seek higher prices. The Indian

example was followed by Vietnamese packers. The price increase was also a refl ection of the higher prices being paid for all nut products.

By the end of 2004 and early 2005 the estimated average quarterly price was $5.30 per kg. Prices began to decline in late 2005 and

from then until mid-2007 the estimated monthly price ranged from about $4.30 to $4.60 per kg. This relatively low price in the fi rst two

quarters of 2007 was attributed in part to the sale of large quantities of India’s 2006 crop to make way for the even bigger 2007 crop of

620 million kgs.

Prices rose sharply beginning in mid-2007, reached a quarterly high of more than $6.90 per kg in the second quarter of 2008, matching

the 1999 price peak, and then began to abate. The price surge originated with Vietnamese shippers. Faced with higher than expected raw

cashew prices, some delayed and then defaulted on shipments, forcing buyers to bid up prices. By the last quarter of 2008, the quarterly

average had declined to just above $5.00 per kg. Since then, quarterly average prices have been accelerating, exceeding $6.00 per kg in

the last quarter of 2009, and surging to $7.60 per kg during the last quarter of 2010 and $8.30 per kg in the fi rst quarter of 2011. The

causes of the unprecedented increases are many: shortfalls in both the Vietnamese and Brazilian crops, rising Indian domestic consumption,

higher African raw seed prices, and continued strong world demand. These pressures have been compounded by Vietnamese and Indian

suppliers holding out for higher prices.

PRICES CONTINUED

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

$7.00

$8.00

$9.00

1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1

98 99 00 01 02 03 04 05 06 07 08 09 10 11

Est A

vg F

OB E

xp P

rice

/ Kg

Year / Quarter

w320s—Quarterly Estimated Average Prices FOB Origin in USD/kg

source: Industry

Red River Foods, Inc. June 2011 19

CA

SH

EW I

ND

US

TRY

TIM

ELIN

E

Vie

tnam

ese, In

dia

n

prices b

egin

prices r

ise s

harp

ly;

Ivory

Coast

becom

es 2

nd

larg

est cashew

pro

ducer

only

by In

dia

Avg F

OB

export

prices d

eclin

e

dra

matic

ally

fro

m p

eak

1999 le

vels

Annual i

ncre

ases o

f cashew

import

s in

to the U

.S.

export

prices r

ecord

ed

2000

2002

cashew

pro

ducer

,

to in

cre

ase s

harp

ly

India

raw

cashew

Ivory

Coast

civ

il w

arf

are

India

export

s d

eclin

e

Manu, buyers

incre

ase e

mphasis

on q

ualit

y

Sharp

FO

B

FO

B e

xport

prices

reach

new

record

levels

pro

ble

ms e

merg

e

385 m

n k

gs

Incre

ases F

ed'l

overs

ight of

food im

port

s

2011

U.S

.

Food S

afe

ty

& M

od'z

'n A

ct

fm C

am

bodia

for

second la

rgest

cro

p r

educed

2010

rebound

FO

B p

rices

Bra

zil

by h

eat; e

st

low

ere

d to 3

00

auth

orizes

health

benefit

cla

ims f

or

2004

2003

cashew

pro

d

pro

cessin

g

est at 35 m

n k

gs

Vie

tnam

leases

6,0

00 h

ecta

res

to h

elp

develo

p

cro

p, export

s

countr

ies to in

cre

ase

pro

cessin

g, add p

roduct valu

edro

p s

harp

ly

Mozam

biq

ue

pro

cessin

g b

egin

s

fall

as m

kt

slo

w V

iet

$146 m

to A

frPeak

export

in 2

006 a

nd f

irst half 2

007

Cash A

lliance

gra

nts

$25 m

n

Vie

tnam

ese,

India

n d

efa

ults

and s

hip

pin

g

dela

ys

year

for

Bra

zil

Alliance

Vie

tnam

cro

pV

ietn

am

export

s a

t

record

levels

by y

ear

end

export

price

incre

ases; at

Majo

r qualit

y

2009; rise, fa

ll,

fluctu

ate

early

form

ed u

nder

Vie

tnam

ese r

aw

cashew

import

s in

cre

ase d

ram

atic

ally

;

dow

n 3

5%

;

2007

191 m

n k

gs

2005

US

AID

sponsors

hip

record

level:

labor

issues

2006

pro

ductio

n

record

level

Vie

tnam

ese

2009

fm 4

00 m

n k

gs

Afr

ican C

ashew

Alliance b

egin

s

industr

y

Bra

zil

Afr

ican

Cashew

belo

w s

tandard

import

s r

ise f

m 7

0 m

n k

gs in

2005 to 4

04 m

n k

gs in

2010

U.S

. FD

A

Vie

tnam

export

s a

t new

kern

el i

mport

s b

egin

Avg F

OB

export

export

Avg F

OB

incre

asin

g

Gate

s F

dn

peak

Jun 0

8

sto

cks

in In

dia

,

Avg F

OB

export

prices d

eclin

eV

ietn

am

U.S

. im

port

s:

mid

-2005; re

main

rela

tively

fla

t

Vie

tnam

becom

es

pro

cessin

g;

surp

assed o

nly

by

Peak

export

India

His

torically

low

avg F

OB

origin

price in

cre

ases

to r

ebound

Vie

tnam

becom

es

2nd la

rgest ke

rnel

export

er,

surp

assed

in V

ietn

am

Early 2

007

2008

export

s to U

.S.

org

aniz

ing c

ashew

inte

rests

in

2001

cert

ain

nuts

record

export

s

131 m

illio

n k

gs

year

for

India

:

122 m

n k

gs

export

prices

Avg F

OB

Vie

t re

covers

;

ship

pers

defa

ult,

dela

y; cause s

harp

Peak

year

for

155 m

n k

gs

Obje

ctiv

e is

to e

sta

blis

h c

ashew

ente

rprises s

o lo

cal p

opula

tions m

ay r

ealiz

e f

inancia

l benefits

fro

m a

ddin

g v

alu

e to the c

ashew

rath

er

than s

imply

export

ing the r

aw

mate

rial.

estim

ate

d a

t

Mozam

biq

ue

US

AID

gra

nts

to a

id in

d a

ccess

to f

inancin

g

Various e

ffort

s b

y in

tern

atio

nal g

overn

ment org

aniz

atio

ns a

nd N

GO

s to in

stit

ute

cashew

supply

chain

org

aniz

atio

n a

nd c

ashew

pro

cessin

g in

Afr

ican p

roducers

.

20-2

5 m

n k

gs

Afr

cashew

short

at

Rain

y w

eath

er

thre

ate

ns s

ize,

qualit

y o

f In

dia

n,

Vie

tnam

ese

U.S

. im

port

s f

luctu

ate

: declin

e 1

3%

in 2

005, flat in

2006 a

t 114 m

kgs, rise to 1

25

mn k

gs in

2007, fa

ll to

115 m

kgs in

2008, in

cre

ase to 1

17 in

2009 a

nd 1

19 in

2010; could

exceed 1

25 m

n k

gs in

2011

uncert

ain

ties

lead to s

urp

lus

pro

cessin

g c

ap

India

raw

import

s in

cre

ase f

m 3

94 m

n k

gs in

2002 to r

ecord

728 m

n k

gs in

2009; at 644 m

n k

gs in

2010

cro

ps

Bra

zilian

cro

p e

xtr

em

ely

thre

ate

ns, dela

ys

cro

p e

xport

s;

leads to h

igh

raw

seed p

rices

and le

vel

Mozam

biq

ue

20 Highlights of the cashew industry

PRODUCTION ESTIMATES in mill ion kgsR

eg

ion

/

Co

un

try

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011P

C

am

bo

dia

10

.02

0.0

25

.03

0.0

35

.04

0.0

45

.05

0.0

50

.05

0.0

60

.06

0.0

In

dia

52

0.0

45

0.0

47

0.0

50

0.0

53

5.0

54

4.0

57

3.0

62

0.0

66

5.0

69

5.0

61

3.0

64

0.0

In

do

ne

sia

69

.99

1.6

11

0.2

10

6.9

13

1.0

13

5.1

14

9.2

15

4.8

15

7.4

15

8.0

10

0.0

80

.0

P

hilip

pin

es

10

.11

0.0

10

.01

0.1

10

.01

0.0

10

.01

0.3

10

.31

0.3

10

.01

0.0

S

ri L

an

ka

4.7

6.2

6.4

6.5

6.5

6.2

6.0

6.0

6.0

6.0

6.0

6.0

T

ha

ila

nd

4.8

4.7

4.7

4.7

4.6

4.7

4.7

4.7

5.0

5.0

5.0

5.0

V

ietn

am

15

0.0

17

0.0

21

0.0

26

0.0

35

0.0

32

0.0

34

0.0

35

0.0

34

9.0

34

0.0

29

0.0

33

0.0

O

the

r1

.01

.01

.10

.91

.11

.01

.01

.01

.15

.05

.05

.0

Su

b-T

ota

l, A

sia

770.5

753.5

837.4

919.1

1,073.2

1,061.0

1,128.9

1,196.8

1,243.8

1,269.3

1,089.0

1,136.0

Afr

ica

We

st

As

ia

B

en

in3

0.0

35

.04

3.1

40

.04

3.0

43

.03

7.5

37

.64

5.0

10

0.0

70

.09

0.0

G

ha

na

5.5

5.0

5.2

5.2

10

.01

0.0

10

.01

2.5

12

.51

2.5

12

.01

2.0

G

uin

ea

-Bis

sa

u7

2.7

70

.07

0.0

75

.09

2.0

10

0.8

10

0.0

10

0.0

10

0.0

13

6.0

15

0.0

13

0.0

Ivo

ry C

oa

st

60

.01

00

.01

04

.81

20

.01

50

.02

00

.02

50

.02

90

.03

20

.03

50

.03

35

.03

85

.0

N

ige

ria

30

.03

0.0

40

.05

0.0

50

.06

0.0

75

.08

0.0

81

.01

00

.07

0.0

85

.0

S

en

eg

al

6.8

3.2

4.0

6.0

8.5

12

.01

5.0

17

.52

0.0

20

.03

5.0

35

.0

O

the

r8

.18

.79

.21

1.5

14

.01

9.5

21

.82

1.9

23

.52

9.5

28

.02

9.5

Su

b-T

ota

l, A

fr W

213.1

251.9

276.3

307.7

367.5

445.3

509.3

559.5

602.0

748.0

700.0

766.5

Afr

ica

Ea

st

K

en

ya

5.1

10

.14

.15

.25

.25

.21

.05

.05

.08

.51

1.0

8.0

M

ad

ag

as

ca

r4

.04

.04

.04

.04

.04

.04

.04

.04

.04

.04

.04

.0

M

oza

mb

iqu

e5

2.6

52

.15

0.2

63

.84

2.3

10

4.4

62

.87

4.4

64

.29

5.0

112

.01

00

.0

T

an

za

nia

12

1.2

12

2.3

67

.49

2.2

78

.67

7.4

92

.69

2.6

99

.19

6.0

98

.01

00

.0

Su

b-T

ota

l, A

fr E

182.9

188.5

125.7

165.2

130.1

191.0

160.4

176.0

172.3

203.5

225.0

212.0

La

tin

Am

eri

ca

B

razil

21

0.0

20

0.0

19

0.0

23

0.0

26

0.0

30

0.0

26

5.0

32

0.0

24

0.0

32

0.0

20

0.0

15

5.0

P

eru

2.7

2.5

2.1

2.2

2.4

2.2

2.2

2.3

2.3

2.3

2.3

2.3

O

the

r4

.24

.24

.64

.54

.34

.24

.34

.44

.54

.64

.64

.6

Su

b-T

ota

l, L

at

Am

216.9

206.7

196.7

236.7

266.7

306.4

271.5

326.7

246.8

326.9

206.9

161.9

Wo

rld

To

tal

1,383.4

1,400.6

1,436.1

1,628.7

1,837.5

2,003.7

2,070.1

2,259.0

2,264.9

2,547.7

2,220.9

2,276.4

N.B.

: Pr

oduc

tion

estim

ates

for a

ny o

ne c

ount

ry c

an a

nd o

ften

do v

ary

grea

tly.

Thus

, man

y es

timat

es h

ere

are

deriv

ed b

y ex

trapo

latio

n, in

terp

olat

ion,

and

“be

st g

uess

es,”

while

oth

er e

stim

ates

der

ived

from

kno

wn a

nd

relia

ble

sour

ces

are

reas

onab

ly a

ccur

ate.

Unt

il th

ere

is a

will

ingn

ess

on th

e pa

rt o

f res

pons

ible

indu

stry

and

gov

ernm

ent p

artie

s at

orig

in to

ven

ture

thei

r bes

t est

imat

es, t

he in

dust

ry w

ill b

e ha

mpe

red

in a

sses

sing

av

aila

ble

supp

lies.

Red River Foods is pleased to provide information about the world cashew trade. Preparing this brief report has been a challenging, but

we think important, step in trying to develop a more complete picture of the cashew industry. The information and data herein represent

estimates from a variety of sources as well as our own estimates. We wish to extend our grateful appreciation to the many individuals who

helped make this brochure possible by contributing to our research. The company makes no warranty about the accuracy of these data and

assumes no duty to update any materials contained in this report. Within the industry it is generally accepted that production, export, and

other data can be understated, overestimated, or even unreported.

Red River wishes to emphasize that unforeseen events caused by political, legal, economic, or other circumstances, as well as weather

conditions, could affect current expectations for any one market or for the world situation generally. Readers should not unduly rely on any

estimates, forward-looking statements, or data cited herein to reach conclusions or make decisions about the various markets or market prices.

Red R ive r Foods , Inc .9020 Stony Po int Parkway

Sui te 380Richmond, V i rg in ia 23235

USA

te l— 804.320.1800 fax—804.320.1896 phipps j@redr i ve r foods .com

Red River Foods , Inc .9020 Stony Po int Parkway

Sui te 380Richmond, V i rg in ia 23235

USA

te l— 804.320.1800 fax—804.320.1896 email—[email protected]

![Chapter - I Introduction - Shodhgangashodhganga.inflibnet.ac.in/bitstream/10603/24891/6/06...1998 [38]. The cashew nut tree consists of the cashew nut fruit, the apple, leaf and bark](https://img.pdfslide.us/doc/110x75/5e83338a059b5b3a95726ed1/chapter-i-introduction-1998-38-the-cashew-nut-tree-consists-of-the-cashew.jpg)