Embed Size (px)

Citation preview

Cash vs. Electronic Payments in Small RetailingEstimating the Global Size

© 2016 International Bank for Reconstruction and Development / The World Bank

1818 H Street NW, Washington DC 20433

Telephone: 202-473-1000; Internet: www.worldbank.org

This work is a product of the staff of The World Bank with external contributions. The findings, interpretations, and conclusions expressed in this work do not necessarily reflect the views of The World Bank, its Board of Executive Directors, or the governments they represent. The World Bank does not guarantee the accuracy of the data included in this work. The boundaries, colors, denominations, and other information shown on any map in this work do not imply any judgment on the part of The World Bank concerning the legal status of any territory or the endorsement or acceptance of such boundaries.

Rights and Permissions

The material in this work is subject to copyright. Because the World Bank encourages dissemination of its knowledge, this work may be reproduced, in whole or in part, for noncommercial purposes as long as full attribution to this work is given.

All queries on rights and licenses should be addressed to the Office of the Publisher, The World Bank, 1818 H Street NW, Washington, DC 20433, USA; fax: 202-522-2625; e-mail: [email protected].

Photo Credit: Shutterstock

1.

Acknowledgements

i

Acknowledgements III

Acronyms And Abbreviations V

Executive Summary VII

1. Introduction 1

2. Methodology 5

2.1. Scope 5

2.2. Estimation 8

3. Country Research 9

4. Global Size Of Digital Vs. Cash Transactions By MSMRs 15

4.1. Person-To-Business Payments For MSMRs 15

4.2. Business-To-Business Payments From MSMRs To Suppliers 17

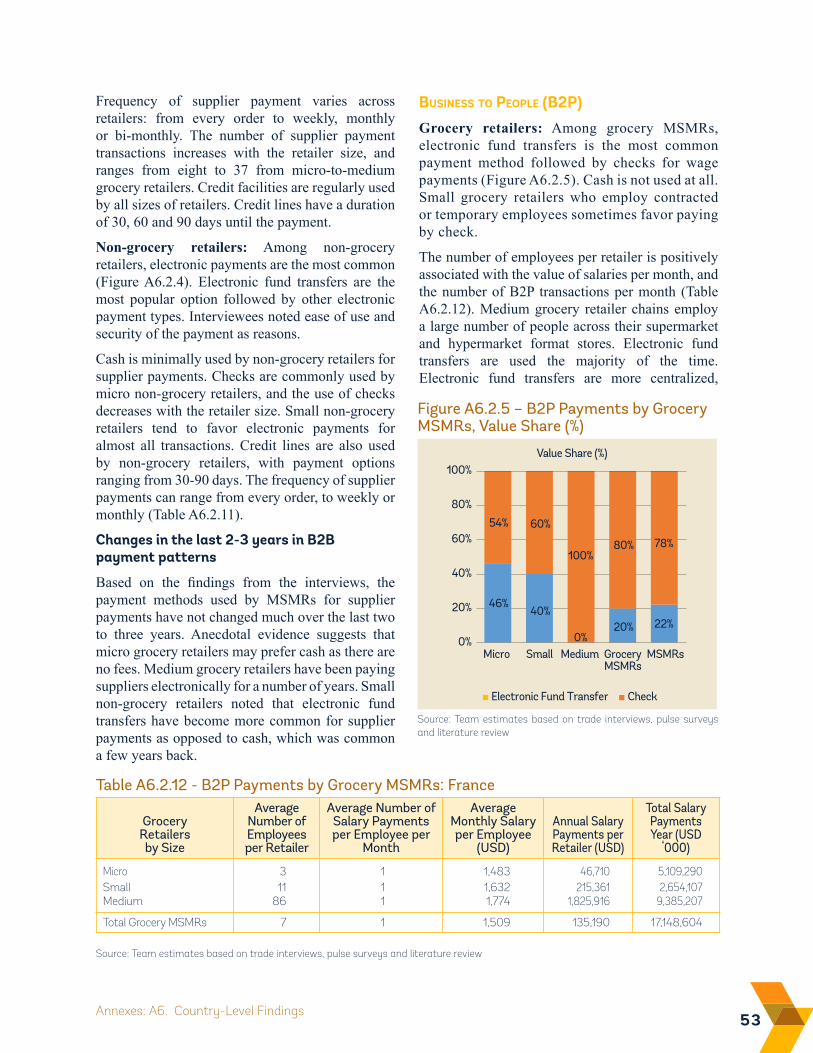

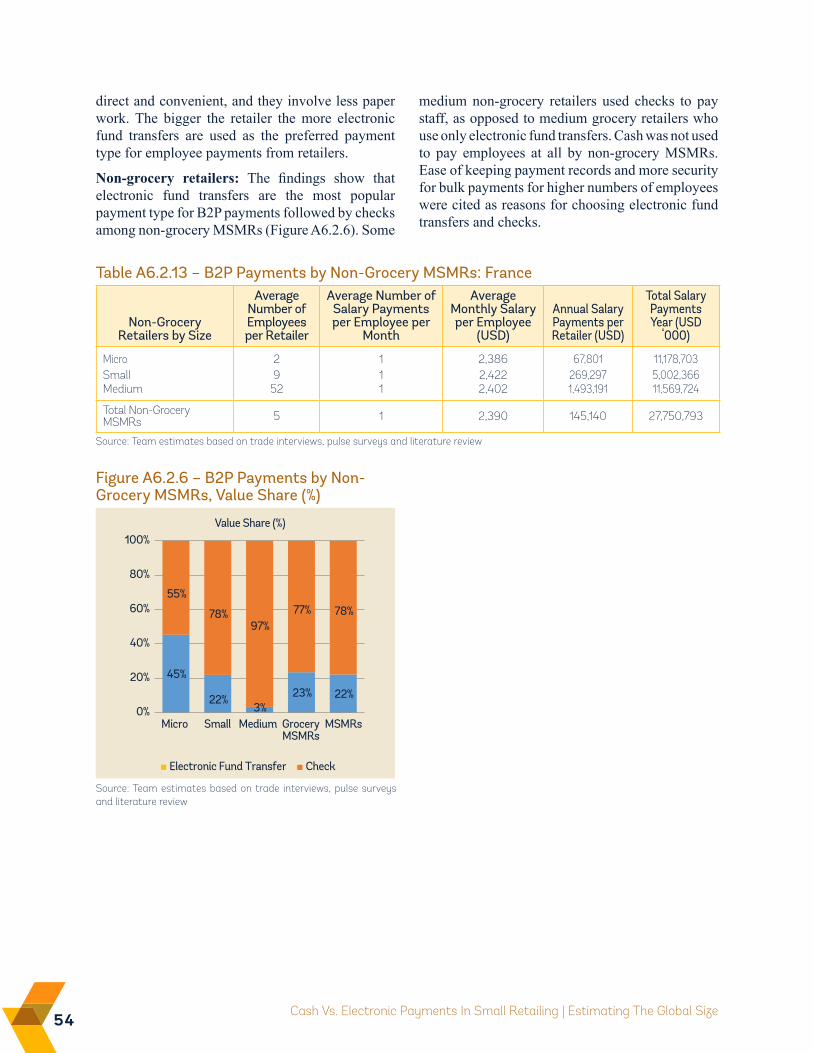

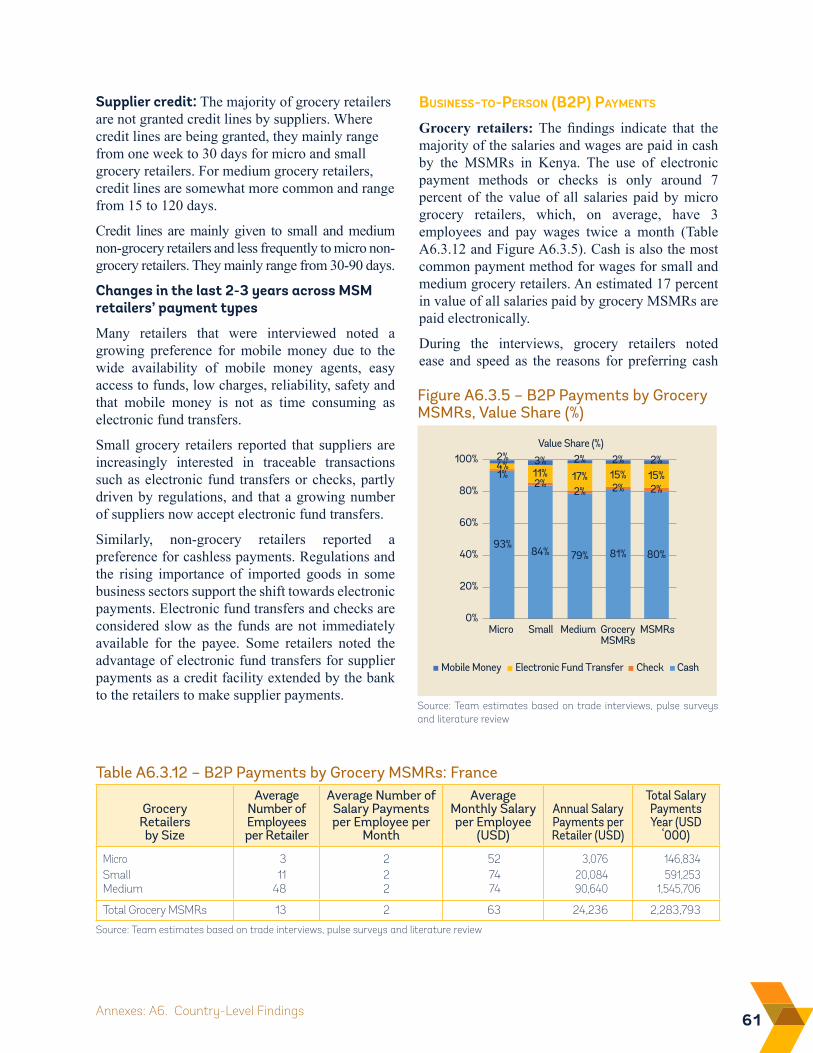

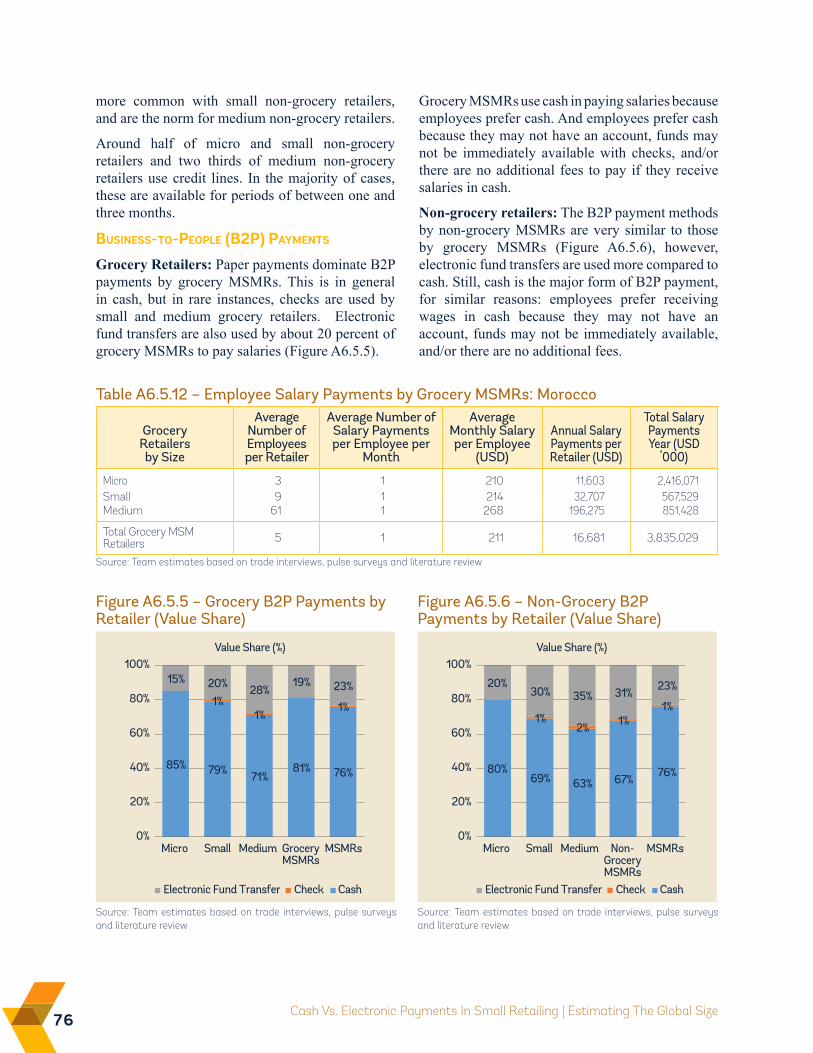

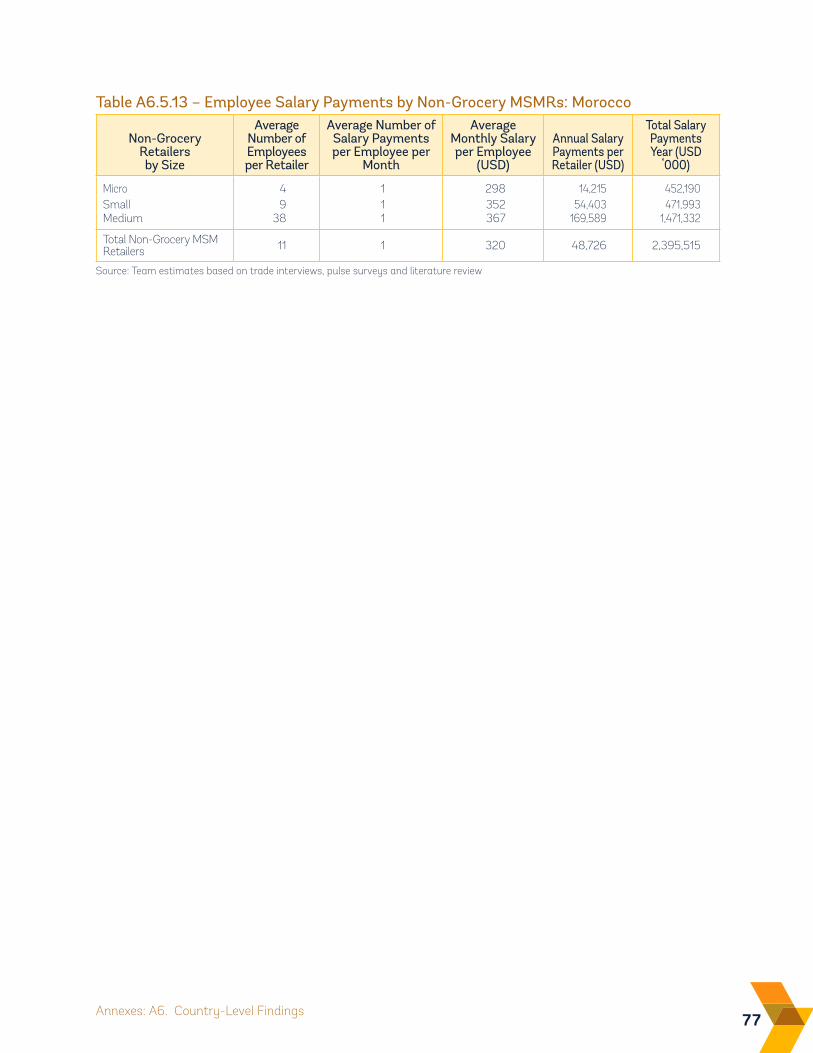

4.3. Business-To-Person Payments by MSMRs: Payments Of Salaries 18

Annexes 21

A1. Glossary 22

A2. Euromonitor Passport Databases 24

A3. List Of Economies 25

A4. Methodology – Detailed Descriptions 26

A5. Discussion Guides And Questionnaires 34

A6. Country-Level Findings 39

References 93

Endnotes 95

1.

Acknowledgements

iiiAcknowledgements

This report is a product of a collaborative effort across the World Bank Group’s Finance & Markets Global Practice (WBG) and the World Economic Forum (Forum) Financial Services Industry Team, specifically with the Promoting Global Financial Inclusion Initiative.

The collaboration was led by Ghada Teima (Program Manager and Lead Financial Sector Specialist, WBG) working with a core team – Nina Bilandzic (Financial Sector Specialist, WBG), Oya Pinar Ardic Alper (Financial Sector Specialist, WBG), Nicole Meyers (Project Manager, Forum, and Financial Inclusion Fellow, McKinsey & Company). Tony Lythgoe (Practice Manager, WBG), Douglas Pearce (Practice Manager, WBG), Massimo Cirasino (Adviser, WBG), Matthew Gamser (CEO, SME Finance Forum, IFC), and Peer Stein (Adviser, IFC) provided overall guidance to the team. Ivan Mortimer-Schutts (Senior Operations Officer, WBG), Harish Natarajan (Lead Financial Sector Specialist, WBG), Thomas Lammer (Senior Financial Sector Specialist, WBG) and Lois Quinn (Senior Payment Systems Specialist, WBG) provided technical guidance. The team is

thankful for the multi-phase collaboration with the World Economic Forum on this topic and for the contribution from Michael Koenitzer (formerly Forum), Annelyse Freyman (formerly Forum) and Lisa Donegan (formerly Forum) at the project design stages. Euromonitor International provided analytical support for the study. Aichin Jones (Graphic Designer, WBG) designed the report.

The team is grateful to the peer reviewers of this report for their valuable input and guidance chaired by Samuel Maimbo (Practice Manager, WBG), including – Matthew Gamser (CEO, SME Finance Forum, IFC), Harish Natarajan (Lead Financial Sector Specialist, WBG), Ivan Mortimer-Schutts (Senior Operations Officer, WBG), Thomas Lammer (Senior Financial Sector Specialist, WBG), and Chris Dooley (Project Lead, Promoting Financial Inclusion Initiative, Forum).

This report would not be possible without the generous support of the Netherlands’ Ministry of Foreign Affairs and the Bill and Melinda Gates Foundation provided through WBG’s Financial Inclusion Support Framework (FISF) program as well as the support of the SME Finance Forum.

1.

Acknowledgements

vAcronyms and Abbreviations

ACH Automated Clearing House

ATM Automatic teller machine

B2B Business-to-business

B2P Business-to-person

B2C Business-to-consumer

C2B Consumer-to-business

IFC International Financial Corporation

MSME Micro, small and medium enterprises

MSMR Micro, small and medium retailers

SME Small and medium enterprises

P2B Person-to-business

POS Point of sale

USD United States Dollars

WB World Bank

WBG World Bank Group

Forum World Economic Forum

1.

Acknowledgements

viiExecutive Summary

In 2014, the World Bank Group (WBG) and the World Economic Forum (Forum) agreed to promote a shared vision of financial inclusion. This study is a part of that collaborative effort to foster knowledge to grow responsible financial inclusion through usage by merchants of electronic payments (often nowadays referred to as digital payments), in particular by small retailers, with a specific focus of the retailers’ role in person-to-business (P2B), business-to-business (B2B) and business-to-person (B2P) payments: payments for retail sales, supplier payments, and wage payments.

For this purpose, concurrent with the underlying study, the WBG and the Forum conducted a stocktaking analysis of innovative cases of electronic payment adoption and usage by small merchants (World Bank Group and World Economic Forum, 2016). This study is a companion piece to that, and aims to identify the value of the digital gap—the value of cash transactions that could be migrated to electronic payments—in retail payments globally with a focus on formal micro, small and medium retailers (MSMRs), and in doing so, inform the analysis and recommendations of the stocktaking study.

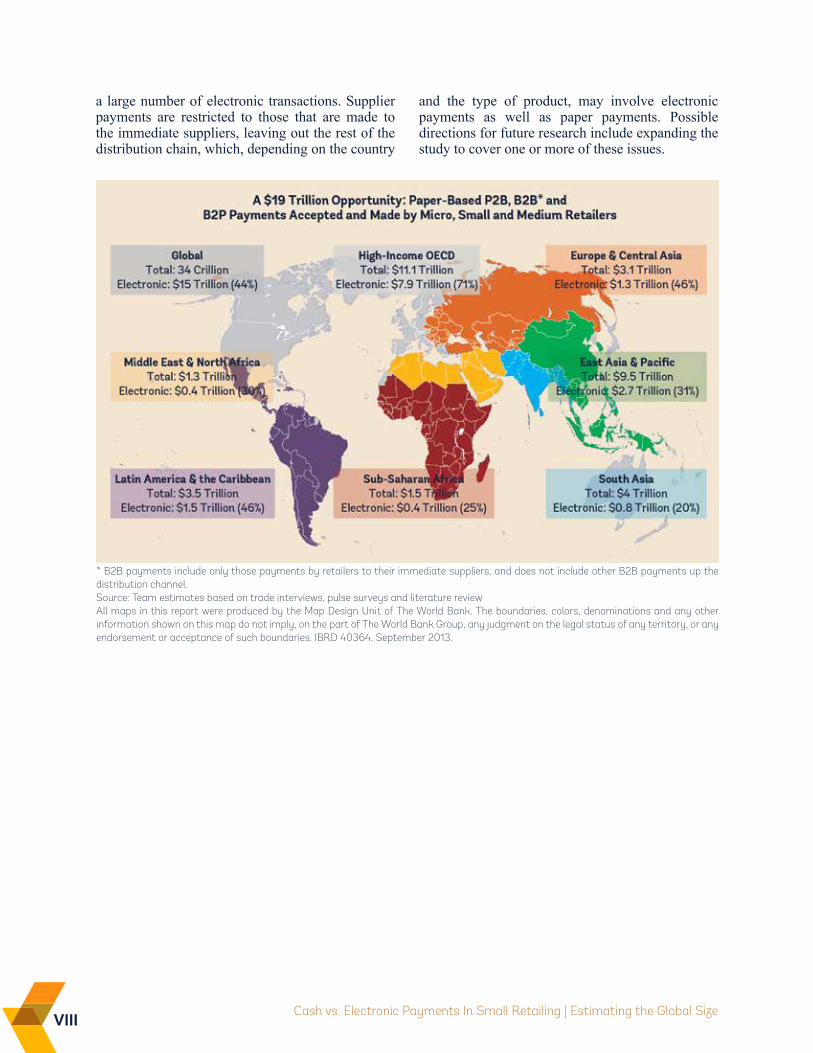

The findings of this study indicate that MSMRs make and accept payments estimated at USD 34 trillion in an annual basis in the form of supplier payments, wages and salaries, and receipts from consumers, USD 15 trillion of which are estimated to be done electronically and the rest, USD 19 trillion, is in paper form (cash and checks). Electronic payments,

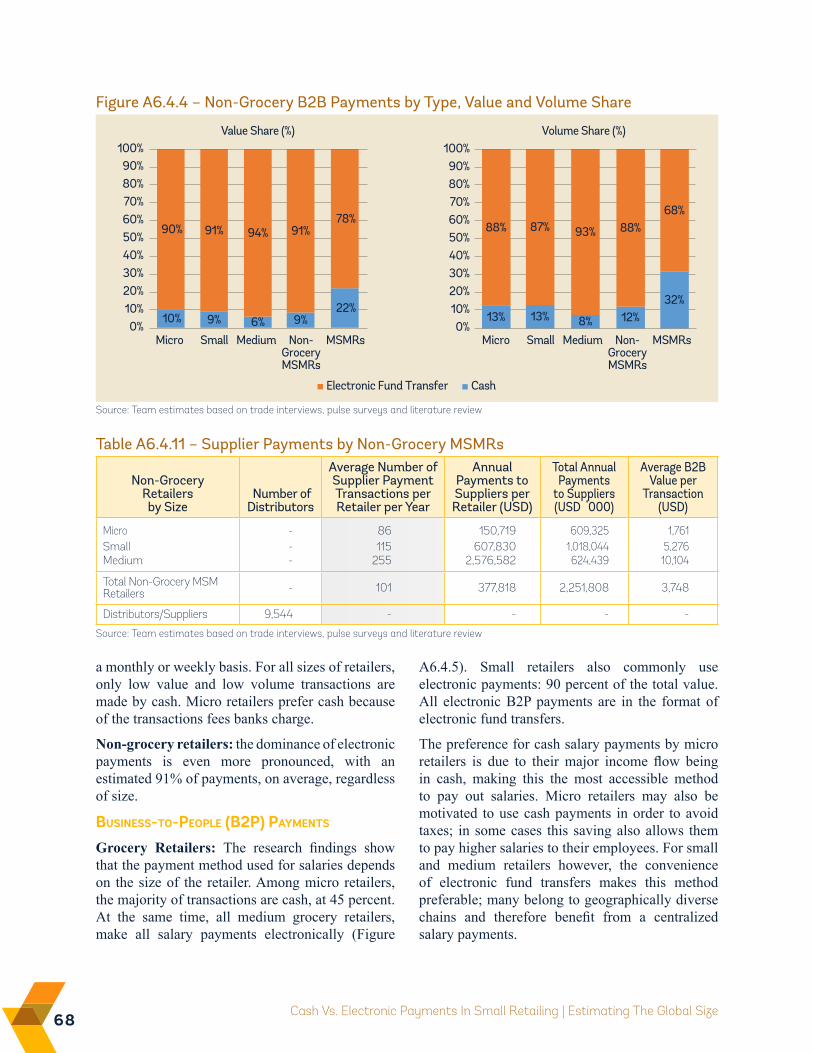

as opposed to cash, are more commonly accepted and used by non-grocery retailers, and by retailers larger in size.

At the same time, there is a large variance across countries in terms of the use and acceptance of electronic payments by MSMRs. In developed and upper-middle income countries, almost all the salaries are paid electronically by medium retailers, and the majority are paid electronically by small and medium retailers. However, MSMRs in lower-middle income and low income countries use mainly cash for the same purpose. The majority of the P2B and B2B payments, both in terms of value and volume, are electronic in the more developed economies.

Data availability has been a big challenge in identifying the global size of cash and electronic payments in retail. To fill the gap, this study undertook primary research in seven economies, and simulations were run to estimate the global size. This paper is a reference paper that discusses the scope and the methodology of this exercise, and presents the findings. As data availability has been a challenge, the scope of this research was defined to ensure reliability of the estimates at the global level. For example, informal sector was left out as it is a vast exercise by itself to estimate the payment flows in the informal retail sector, with the acknowledgement that a large number of cash transactions are done in the informal sector. Also, the scope is restricted to micro, small, and medium retailers, leaving out large retailers. This excludes

viii Cash vs. Electronic Payments In Small Retailing | Estimating the Global Size

a large number of electronic transactions. Supplier payments are restricted to those that are made to the immediate suppliers, leaving out the rest of the distribution chain, which, depending on the country

and the type of product, may involve electronic payments as well as paper payments. Possible directions for future research include expanding the study to cover one or more of these issues.

* B2B payments include only those payments by retailers to their immediate suppliers, and does not include other B2B payments up the distribution channel. Source: Team estimates based on trade interviews, pulse surveys and literature reviewAll maps in this report were produced by the Map Design Unit of The World Bank. The boundaries, colors, denominations and any other information shown on this map do not imply, on the part of The World Bank Group, any judgment on the legal status of any territory, or any endorsement or acceptance of such boundaries. IBRD 40364, September 2013.

1.

Acknowledgements

1

The importance of financial inclusion for development has been recognized in the international development community and by most policy makers in developing economies. According to the Global Findex database, an estimated 2 billion adults globally do not have access to a transaction account with an authorized and/or regulated service provider and that can be used to send and receive payments or to store some value. Yet, research shows that poor people have active financial lives and need a range of financial services to take advantage of economic opportunities and manage and mitigate risks. Similarly, while small and medium enterprises (SMEs) generate the most new jobs, employ the largest number of people in aggregate, and hence are important for job creation and economic growth, 200 million enterprises in developing economies are constrained in terms of financing.

Recognizing the transformational potential of universal financial inclusion for economic development, the World Bank Group (WBG) President put forward an ambitious goal of universal financial access. Universal Financial Access by 2020 vision is to ensure that everyone has access to a transaction or deposit account -- whether accessed through a bank account, payment card, mobile wallet, or other financial instrument. This will provide a strong foundation to achieve the broader future goal of universal financial inclusion, in addition to being instrumental in achieving the WBG’s twin goals of

eradicating extreme poverty by 2030, and increasing the share of income held by the bottom 40%.

While there are many ingredients to achieving universal financial access, the potential impact of extending digital financial services through a more widespread acceptance at small retailers is substantial. Traditional retailers in developing economies, the majority of which are micro, small, and medium enterprises (MSMEs), most often do not use electronic payments and are excluded from the formal financial sector. They can help expand the use of electronic payments by consumers. It is through the regularity and the frequency of purchases from everyday retailers that retail payment solutions become valuable to consumers and generate an anchor for them within the formal financial sector.

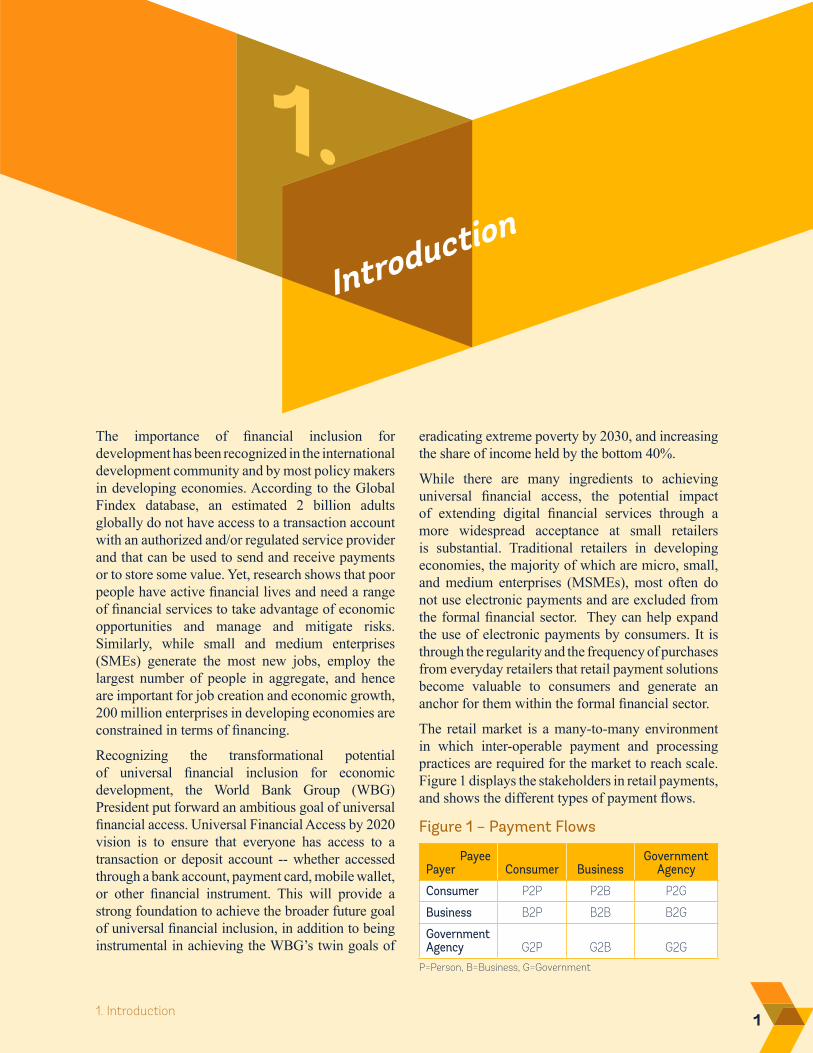

The retail market is a many-to-many environment in which inter-operable payment and processing practices are required for the market to reach scale. Figure 1 displays the stakeholders in retail payments, and shows the different types of payment flows.

1. Introduction

Figure 1 – Payment Flows

P=Person, B=Business, G=Government

PayeePayer Consumer Business

Government Agency

Consumer P2P P2B P2G

Business B2P B2B B2G

Government Agency G2P G2B G2G

2 Cash vs. Electronic Payments In Small Retailing | Estimating the Global Size

Small retailers have a potentially key role in adoption and eventual widespread use of digital payment instruments. The benefits of transforming small retailers into non-cash transaction partners include:

• Boosting the value of non-cash payments to a broader consumer market (P2B payments).

• Using the information on timely supplier payments in credit decisioning (B2B payments).

• Expansion of transaction account ownership (B2P payments).

Expanding access to a basic transaction account that allows for payments and store of value is considered a first step to broader financial inclusion. The use of basic payment or savings accounts can gradually lead to access to and usage of other financial services, such as credit, insurance, or pensions. Figure 2 summarizes the foundations and catalytic pillars for universal access to and frequent usage of transaction accounts (CPMI and World Bank Group, 2016).

The aim of this study is to understand the digital payments gap globally, with a focus on B2B, P2B, and B2P transactions of micro, small and medium retailers. In doing so, this study will form the basis of, and motivate, an analysis of the foundations for accelerating the integration of small retailers into the financial sector by providing estimates for the size of the electronic vs. paper-based transactions in the B2B, P2B and B2P small retail segments globally. Concurrent with the underlying study, the WBG and the Forum also conducted a stocktaking analysis of innovative cases of electronic payment adoption and

usage by small merchants (WBG and WEF, 2016). This study is a companion piece to that joint report.

Unfortunately, reliable data comparable across countries do not exist to gauge the size of these payment flows either in terms of value or in terms of volume. The focus of this current study, therefore, is to generate and map reliable estimates of the global size of the digital vs. cash transactions for B2B, P2B and B2P transactions in the small retailer context. These estimates would correspond to only parts of the dark shaded rectangles in Figure 1 as large retailers are left out. Measuring the size of these payment flows is in fact fundamental for informed policy making as well as raising the appetite of the private sector to implement innovative approaches to retail payments for micro, small, and medium retailers (MSMRs).

An analytical approach is developed to estimate the global value and volume of P2B, B2B and B2P payments by MSMRs. The analysis therefore generates a more detailed understanding of the role small merchants play in accelerating financial inclusion through their adoption of digital payments mechanisms by providing the relative size of cash vs. digital payment flows for the MSMR segment. In doing so, this study aims to fill the gap in understanding the barriers and incentives for the use of digital payments use from the perspective of small retailers.

The main findings of the analysis are as follows:

• Total value of B2B retail payments worldwide by MSMRs to immediate suppliers are estimated to

Figure 2 – Foundations And Catalytic Pillars For Effective Usage To Reach Universal Financial Access

Public and Private Sector CommitmentLegal and Regulatory FrameworkFinancial and ICT Infrastructures

Universal AccessTo and Frequent Usage of Transaction Accounts

TransactionAccount and

PaymentProduct Design

Awarenessand Financial

Literacy

Leveraginglarge-Volume

RecurrentPayment Streams

ReadilyAvailable

Access Points

Critical EnablersFoundations

Drivers of Accessand Usage

Catalytic Pillars

31. Introduction

be $13.3 trillion, 53% of which (approximately $7 trillion) are made electronically, and the remaining $6.3 trillion is in cash and checks.

• Total value of B2P retail payments worldwide by MSMRs are estimated to be $2 trillion, 50% of which are made electronically.

• These imply a market size of $34 trillion globally for payments by small retailers, $15 trillion of which are made electronically, and $19 trillion made in cash and checks.

• Electronic payments are more widely used by non-grocery retailers compared to grocery retailers, regardless of whether it is B2B, P2B or B2P transactions.

Developing and accelerating acceptance of electronic payments by small merchants is essential to expand financial access. A basic transaction account that enables payments and store of value is considered an entry point to the formal financial system and can act as a gateway for individuals to adopt other

relevant financial services they need to smooth their consumption and manage income shocks. However, it is not sufficient to just equip individuals with basic transaction accounts. The use case becomes more and more effective as individuals gradually move to a cashless economy where electronic payments are widely accepted for regular and frequent purchases.

The rest of this report is organized as follows. Section 2 provides an overview of the methodology. Findings of the analysis are presented in sections 3 and 4, on country research and global research, respectively. The report also has six annexes: a glossary of terms is provided in Annex 1. Annex 2 includes information on the proprietary databases by Euromonitor International used in this study. The list of economies used in estimating the global size is in Annex 3. Annex 4 provides technical details on the methodology. Discussion guides and questionnaires on which the primary research is based are provided in Annex 5. Annex 6 includes detailed country-level results.

52. Methodology

2.1 SCOPE

FORMAL MiCRO, SMALL, AND MEDiUM RETAiLERS

The scope of this research is restricted to B2B, P2B and B2P transactions of formal (i.e. officially registered as a business) micro, small and medium retailers (MSMRs), which are defined as those up to 100 employees. Both grocery (modern and traditional) and non-grocery retailers are included. Modern grocery retailing includes hypermarkets, supermarkets, discounters, forecourt retailers, and convenience stores. Traditional grocery retailing includes independent small grocers, food/drink/tobacco specialists and other grocery retailers. Annex 1 has the Glossary with definitions of different types of retailers.

While very relevant for including individuals who are outside the regulated financial system, the informal retail sector is excluded because it is challenging to come up with a measure of the informal retail sector within a country as well as a measure that is comparable across countries. At the same time, it is difficult to define the extent of the informal sector even within a country.

P2B PAYMENTS, B2P PAYMENTS, AND B2B PAYMENTS TO iMMEDiATE SUPPLiERS

P2B payments in this study include all payment transactions made by consumers/persons to MSMRs in return for products or services. B2P payment flows, on the other hand, are payments by MSMRs to persons, which are wages and additional benefits.

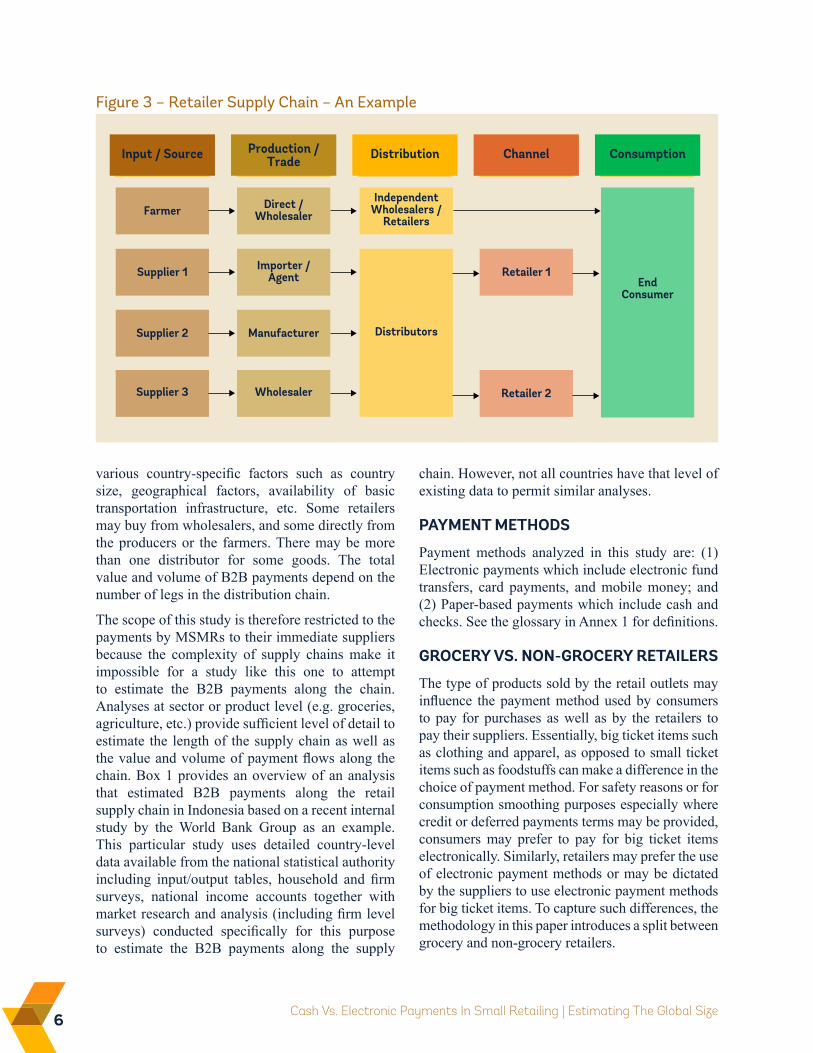

The study measures B2B payments as those by MSMRs to immediate suppliers, i.e. the first leg in the supply chain. The full extent of B2B payments, however, is much larger and depends on the length of the supply/distribution chain, including all payment flows through the chain in either direction. Figure 3 plots an example of a supply chain where the product is distributed along the various layers of the chain by various agents, e.g. distributors, wholesalers, etc. from the actual producer to the retailer. However, not all retailer supply chains are the same.

The complexity and differences in measuring supply chain length depend on the type of the product, the degree of integration of the supply chain itself and the degree of concentration and fragmentation of the retailer markets/suppliers, in addition to

6 Cash Vs. Electronic Payments In Small Retailing | Estimating The Global Size

various country-specific factors such as country size, geographical factors, availability of basic transportation infrastructure, etc. Some retailers may buy from wholesalers, and some directly from the producers or the farmers. There may be more than one distributor for some goods. The total value and volume of B2B payments depend on the number of legs in the distribution chain.

The scope of this study is therefore restricted to the payments by MSMRs to their immediate suppliers because the complexity of supply chains make it impossible for a study like this one to attempt to estimate the B2B payments along the chain. Analyses at sector or product level (e.g. groceries, agriculture, etc.) provide sufficient level of detail to estimate the length of the supply chain as well as the value and volume of payment flows along the chain. Box 1 provides an overview of an analysis that estimated B2B payments along the retail supply chain in Indonesia based on a recent internal study by the World Bank Group as an example. This particular study uses detailed country-level data available from the national statistical authority including input/output tables, household and firm surveys, national income accounts together with market research and analysis (including firm level surveys) conducted specifically for this purpose to estimate the B2B payments along the supply

chain. However, not all countries have that level of existing data to permit similar analyses.

PAYMENT METHODS

Payment methods analyzed in this study are: (1) Electronic payments which include electronic fund transfers, card payments, and mobile money; and (2) Paper-based payments which include cash and checks. See the glossary in Annex 1 for definitions.

GROCERY vS. NON-GROCERY RETAiLERS

The type of products sold by the retail outlets may influence the payment method used by consumers to pay for purchases as well as by the retailers to pay their suppliers. Essentially, big ticket items such as clothing and apparel, as opposed to small ticket items such as foodstuffs can make a difference in the choice of payment method. For safety reasons or for consumption smoothing purposes especially where credit or deferred payments terms may be provided, consumers may prefer to pay for big ticket items electronically. Similarly, retailers may prefer the use of electronic payment methods or may be dictated by the suppliers to use electronic payment methods for big ticket items. To capture such differences, the methodology in this paper introduces a split between grocery and non-grocery retailers.

Figure 3 – Retailer Supply Chain – An Example

Input / Source

Farmer

Supplier 1

Supplier 2

Supplier 3

Production /Trade

Direct /Wholesaler

Importer /Agent

Manufacturer

Wholesaler

Distribution

IndependentWholesalers /

Retailers

Distributors

Channel

Retailer 1

Retailer 2

Consumption

EndConsumer

72. Methodology

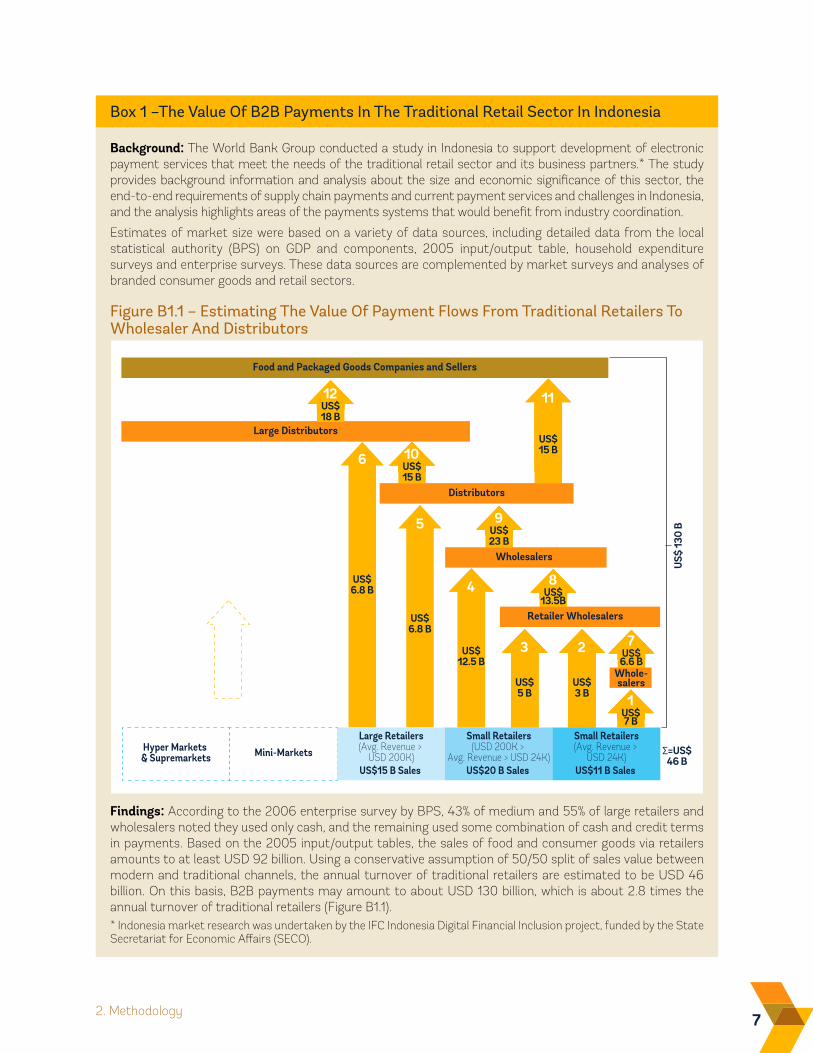

Background: The World Bank Group conducted a study in Indonesia to support development of electronic payment services that meet the needs of the traditional retail sector and its business partners.* The study provides background information and analysis about the size and economic significance of this sector, the end-to-end requirements of supply chain payments and current payment services and challenges in Indonesia, and the analysis highlights areas of the payments systems that would benefit from industry coordination.

Estimates of market size were based on a variety of data sources, including detailed data from the local statistical authority (BPS) on GDP and components, 2005 input/output table, household expenditure surveys and enterprise surveys. These data sources are complemented by market surveys and analyses of branded consumer goods and retail sectors.

Figure B1.1 – Estimating The Value Of Payment Flows From Traditional Retailers To Wholesaler And Distributors

Findings: According to the 2006 enterprise survey by BPS, 43% of medium and 55% of large retailers and wholesalers noted they used only cash, and the remaining used some combination of cash and credit terms in payments. Based on the 2005 input/output tables, the sales of food and consumer goods via retailers amounts to at least USD 92 billion. Using a conservative assumption of 50/50 split of sales value between modern and traditional channels, the annual turnover of traditional retailers are estimated to be USD 46 billion. On this basis, B2B payments may amount to about USD 130 billion, which is about 2.8 times the annual turnover of traditional retailers (Figure B1.1).* Indonesia market research was undertaken by the IFC Indonesia Digital Financial Inclusion project, funded by the State Secretariat for Economic Affairs (SECO).

Box 1 –The Value Of B2B Payments In The Traditional Retail Sector In Indonesia

6

US$6.8 B

Food and Packaged Goods Companies and Sellers

Large Distributors

US$6.8 B

US$6.8 B

US$12.5 B

5

4

US$6.8 BUS$6.8 BUS$6.8 BUS$

7 B

1

US$6.8 BUS$6.8 BUS$6.8 BUS$6.6 B

7US$6.8 BUS$6.8 BUS$6.8 B

US$3 B

2US$6.8 BUS$6.8 BUS$6.8 B

US$5 B

3

Mini-MarketsLarge Retailers(Avg. Revenue >

USD 200K)US$15 B Sales

Small Retailers(USD 200K >

Avg. Revenue > USD 24K)US$20 B Sales

Small Retailers(Avg. Revenue >

USD 24K)US$11 B Sales

Hyper Markets & Supremarkets

US$6.8 BUS$6.8 BUS$6.8 BUS$23 B

9

Wholesalers

US$6.8 BUS$6.8 BUS$6.8 BUS$15 B

10

US$6.8 BUS$6.8 BUS$6.8 B

US$15 B

11US$6.8 BUS$6.8 BUS$6.8 BUS$18 B

12

Whole-salers

US$6.8 BUS$6.8 BUS$6.8 BUS$13.5B

8

Retailer Wholesalers

Distributors

US$

130

B

Σ=US$46 B

8 Cash vs. Electronic Payments In Small Retailing | Estimating the Global Size

2.2 ESTiMATiONThe aim of this study is to estimate the value and volume of cash vs. electronic P2B, B2B and B2P payments by formal MSMRs globally. While there exists some data regarding the size of electronic payments in a number of countries, data on paper-based payment transactions are limited. This type of data is not available for a sufficient number of countries to facilitate a global estimation either. Additionally, data on electronic transactions are not necessarily granular enough to provide information on different types of payment flows (e.g. B2B or P2B) or on MSMRs.

To overcome these challenges, this study is based on the following three-step methodology:

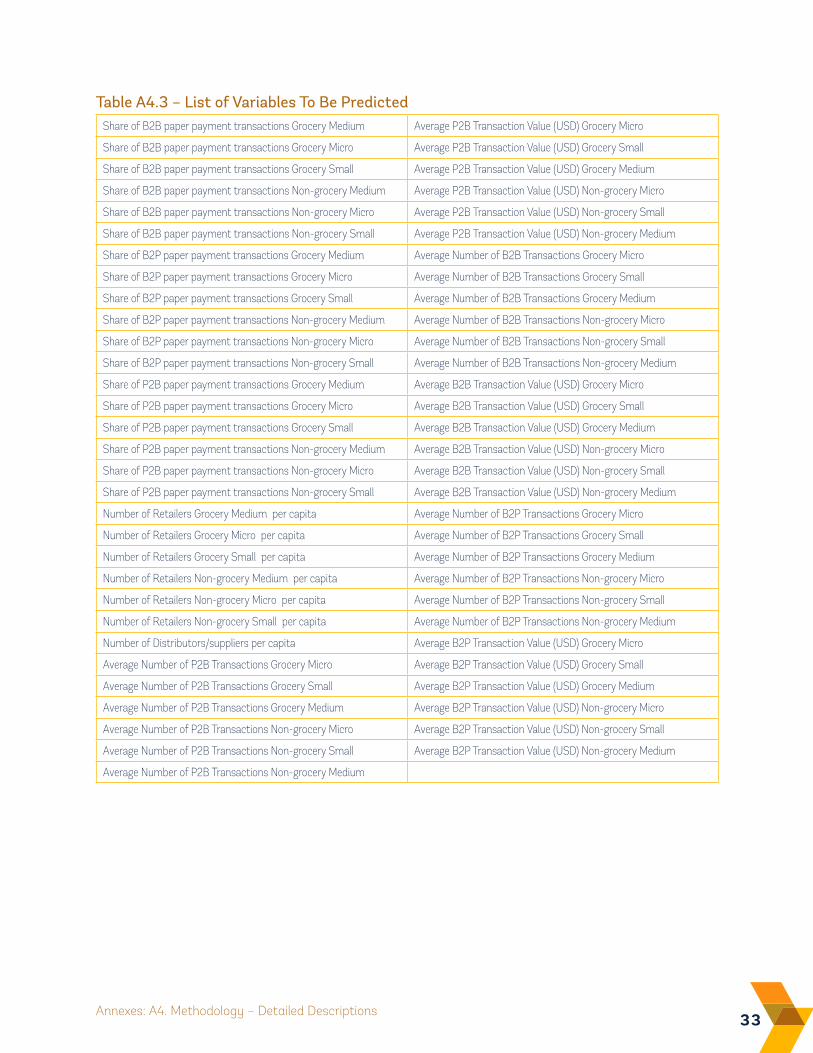

1. Preliminary analysis: Statistical cluster analysis to group 168 countries into six clusters (Annex 5 provides a list of all countries included in the analysis). The underlying idea is to create typologies and therefore focus on a smaller number of countries in the second stage rather than having a global scope.

2. Primary research: Primary research in one representative country per cluster (two from cluster six as cluster six is large compared to the other five clusters) to enhance existing data. Trade interviews and pulse surveys were conducted with retailers, distributors, wholesalers, trade associations, financial institutions, and/or government agencies.

3. Simulations: Simulations based on primary research countries to forecast market size (value and volume) in each of the 150+ countries included in the analysis. Each cluster is modeled based on the additional data collected through primary research in the country that is chosen from that cluster. Country-level estimates for all other countries are based on the primary research countries within respective clusters. Global and regional estimates are simply aggregations of relevant country-level estimates.

The rest of this section provides an overview of the methodology. Further technical details and model specifications for each step are provided in Annex 4.

The cluster analysis in step one was conducted based on indicators on the retail sector and financial

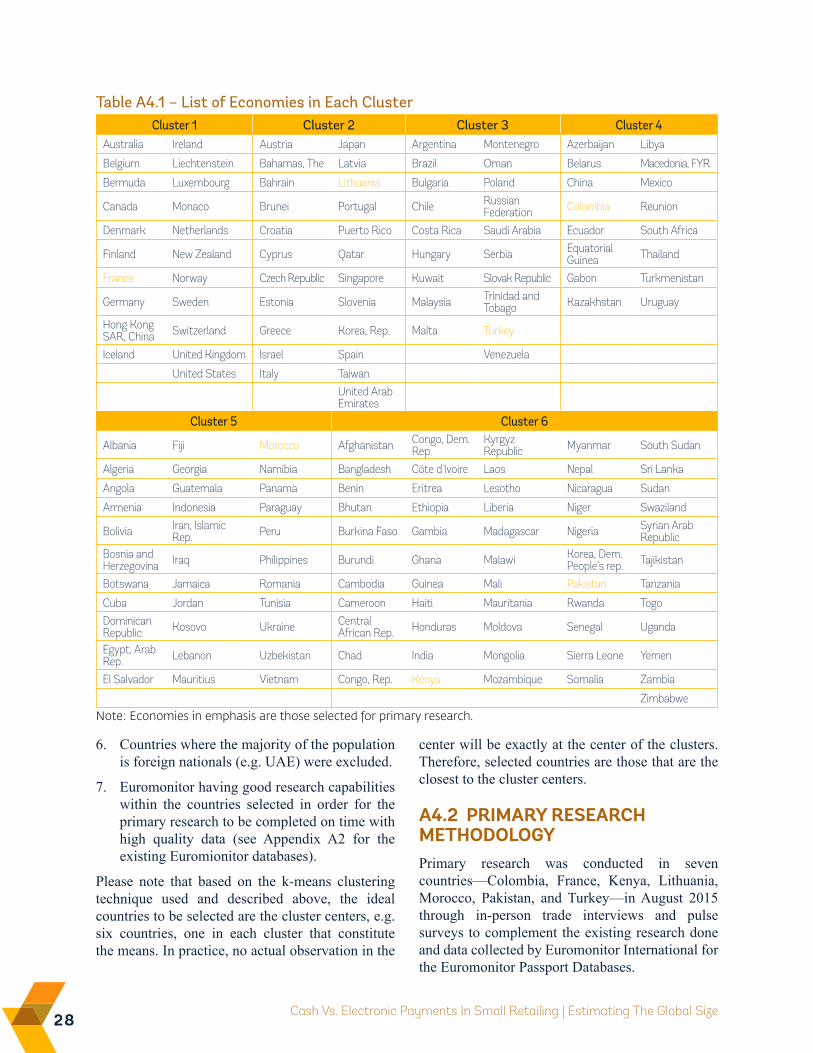

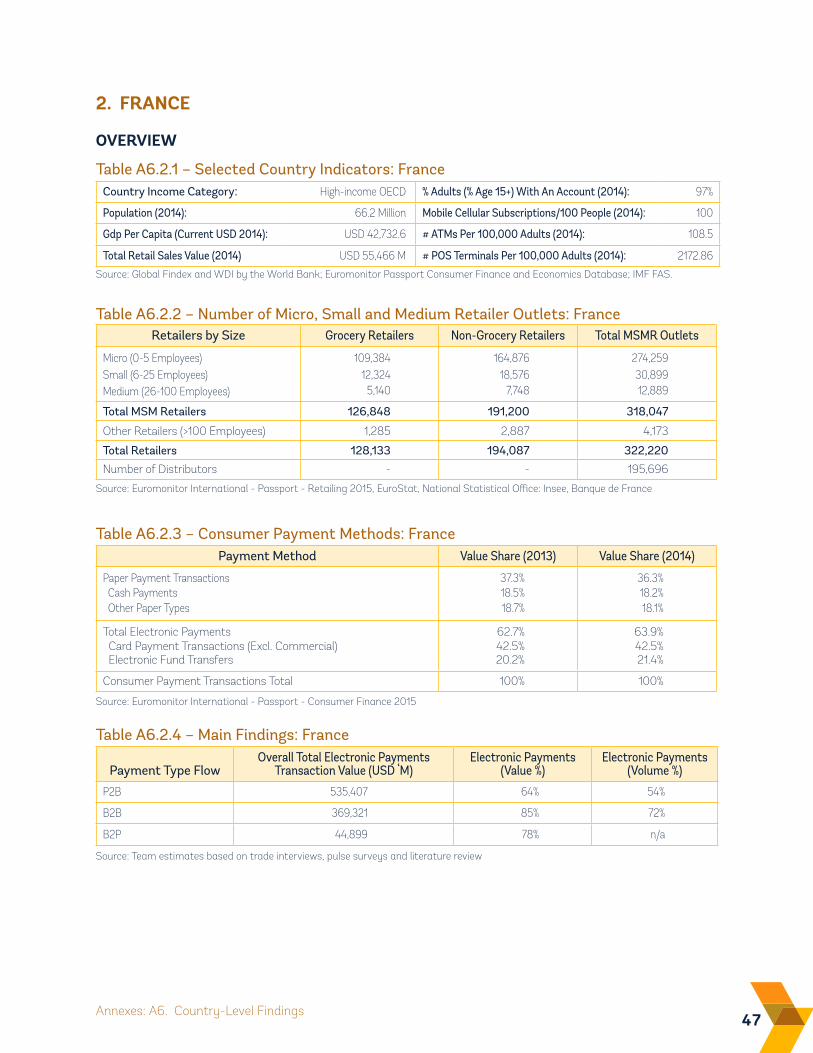

access as well as economic and demographic country-specific factors such as population and real per capita GDP. As a result, 168 countries in the sample was categorized into six groups of varying sizes, with group one including more developed countries to group six including less developed countries. Seven countries were selected as a result of step one: one country from each group, except for group six—the largest group—from which two countries were selected: France, Lithuania, Turkey, Colombia, Morocco, Kenya and Pakistan. Annex 4 provides a list of economies in each group.

In step two, primary research was conducted in these seven countries in the form of face-to-face pulse interviews with MSMRs, trade interviews with wholesalers, industry associations, financial institutions, telecoms, and/or government agencies. The interviews are not based on representative samples, but were conducted to complement the existing research of Euromonitor International in these seven countries which form the basis of the Euromonitor Passport databases on the retail sector. The discussion guides with questions asked during these interviews are enclosed in Annex 5. Using the findings of primary research together with the data from Euromonitor Passport databases, estimates of the value and volume of P2B, B2B and B2P payments by MSMRs were constructed for the seven countries in addition to estimates of other variables of interest such as the frequency of supplier payments, the method of payments, etc. Furthermore, these interviews were also instrumental in collecting anecdotal evidence on preferred payment methods, reasons for cash use, etc.

Finally, in step three, simulations were used to extrapolate the data on seven countries to 168. This step is different from a standard regression and prediction analysis where estimation sample size is large and forecast sample is small: estimation sample is seven countries and forecast sample is 161. The details of the simulation methodology are provided in Annex 4.3. Once the 168 country-level estimates were formed on the basis of these simulations, regional and global estimates of the value and volume of P2B, B2B and B2P payments by MSMRs were constructed by aggregating these country-level estimates.

93. Country Research

Figure 4 – Summary Information On Primary Data Collections

Country-Specific Research

Pulse SurveysA Short, 10-20 Minute Conversation Conducted

During A Store Visit585 Interviews

Global Stakeholder Engagement

Trade InterviewsA Detailed, 30-60 Minute Conversation

With Trade Source182 Interviews

Bottom-UpTop-Down

Global Stakeholder Engagement

ConsensusTriangulation

Validation

Number of MSMRs and distributors/wholesalersNumber and value of digital versus cash B2B transactionsNumber and value of digital versus cash C2B transactionsNumber and value of digital versus cash B2P transactions (wages, tips and others)

�

�

�

Output:

MSMR retailersSuppliers�

�

Sources:

Dynamics of the retail sector in the country (formal versus informal, domestic versus international, independent versus chained)Policy, financial, regulatory and cultural factors impacting integration of MSMR into the formal financial systemQualitative insights on barriers to financial inclusion and/or any successful cases

�

�

�

Output:

Government organisationsRetail associationsLocal banks and financial institutionsNon-bank financial service providers

�

�

�

�

Sources:

In combination with Euromonitor Passport Databases

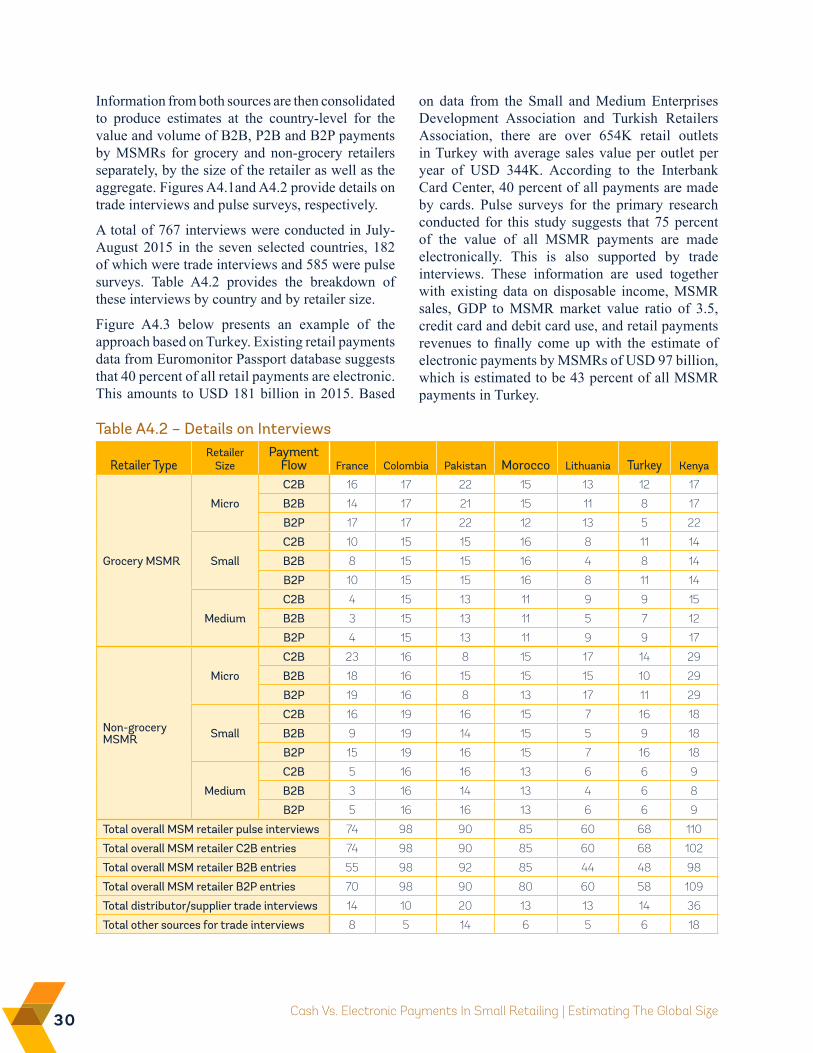

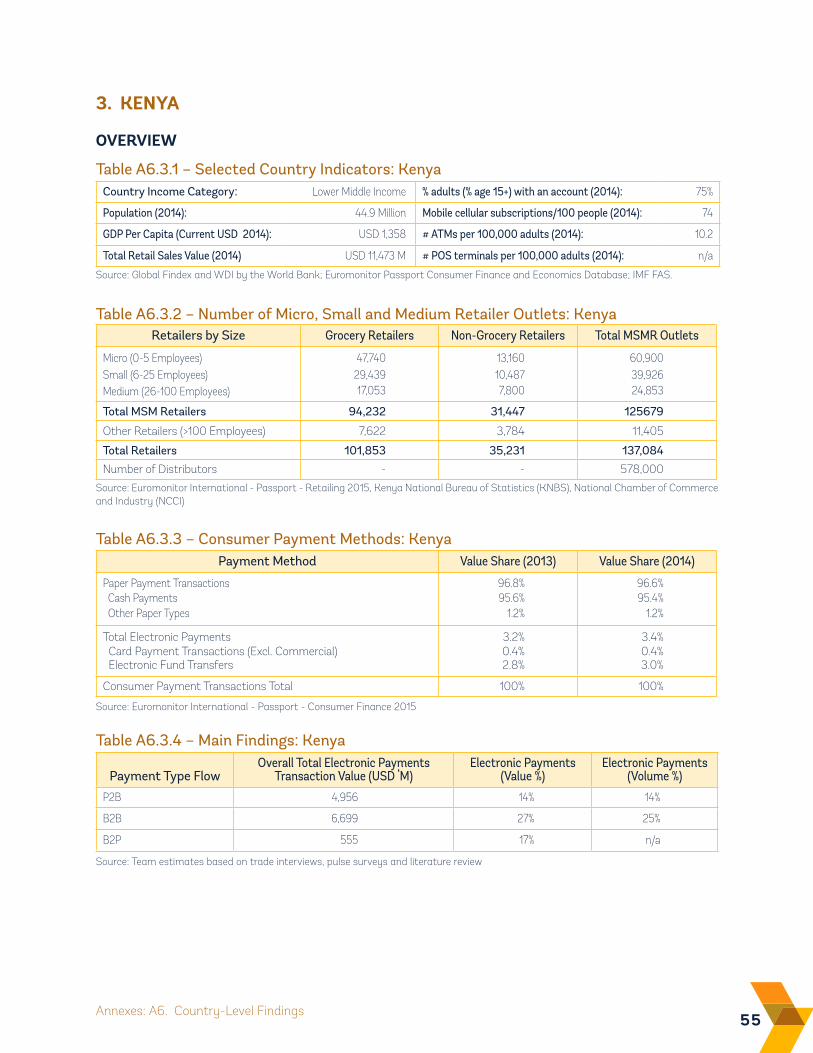

Step one of the methodology is to fill the data gaps in the retail payment landscape to facilitate the estimation of global figures. For this purpose, primary research has been conducted in seven selected countries: Colombia, France, Kenya, Lithuania, Morocco, Pakistan and Turkey. In addition to enabling the estimation of global size of cash vs. electronic B2B, B2P, and P2B payments for MSMRs, the data collected through this primary research exercise provides interesting and deeper insights for these seven countries.

A total of 767 trade interviews and pulse surveys were done in these seven countries to collect data on retail payments. These surveys are done with MSMRs, suppliers, trade associations, financial institutions, etc. Figure 4 provides a visual summary of these surveys. The data collected through these surveys provide estimates on the value and volume of P2B, B2B and B2P payments by MSMRs in each of these seven countries, along with the payment method.

10 Cash Vs. Electronic Payments In Small Retailing | Estimating The Global Size

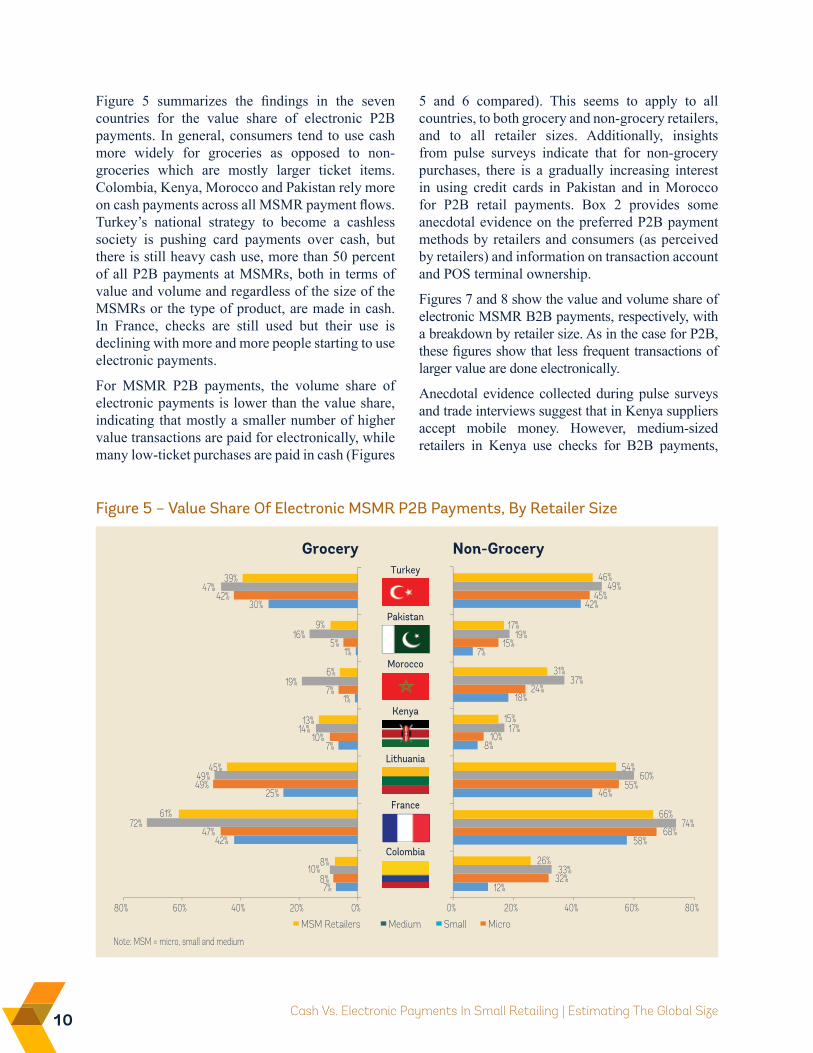

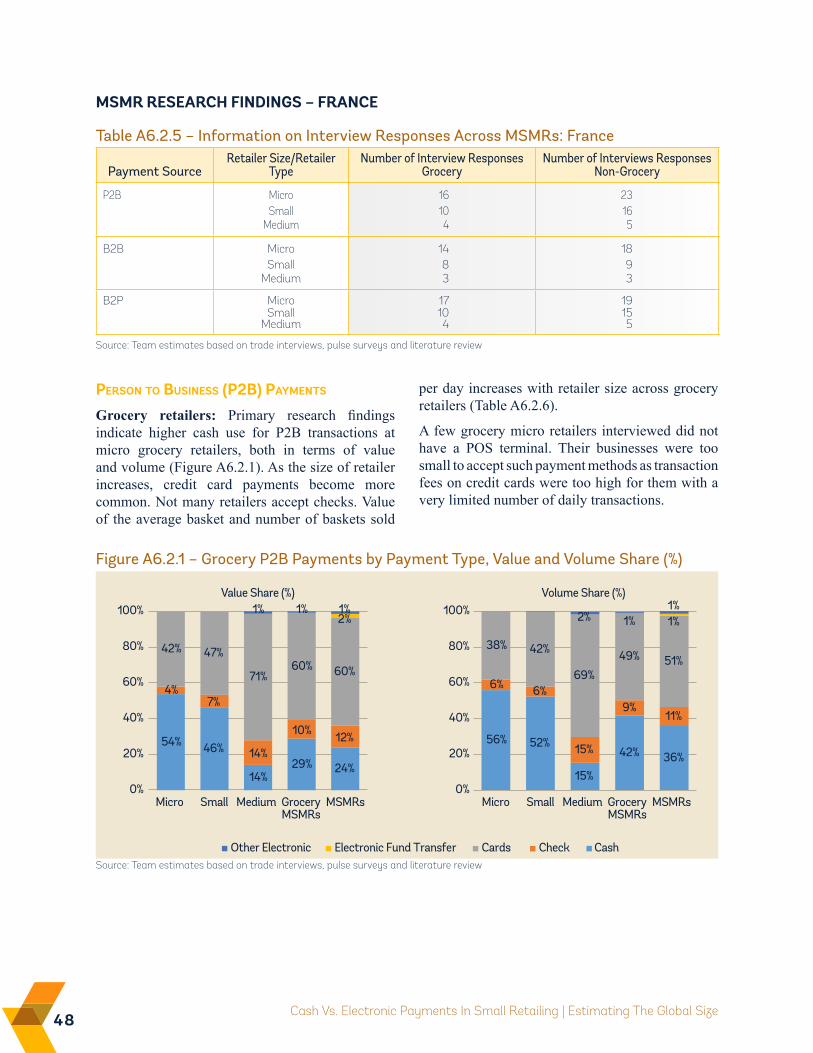

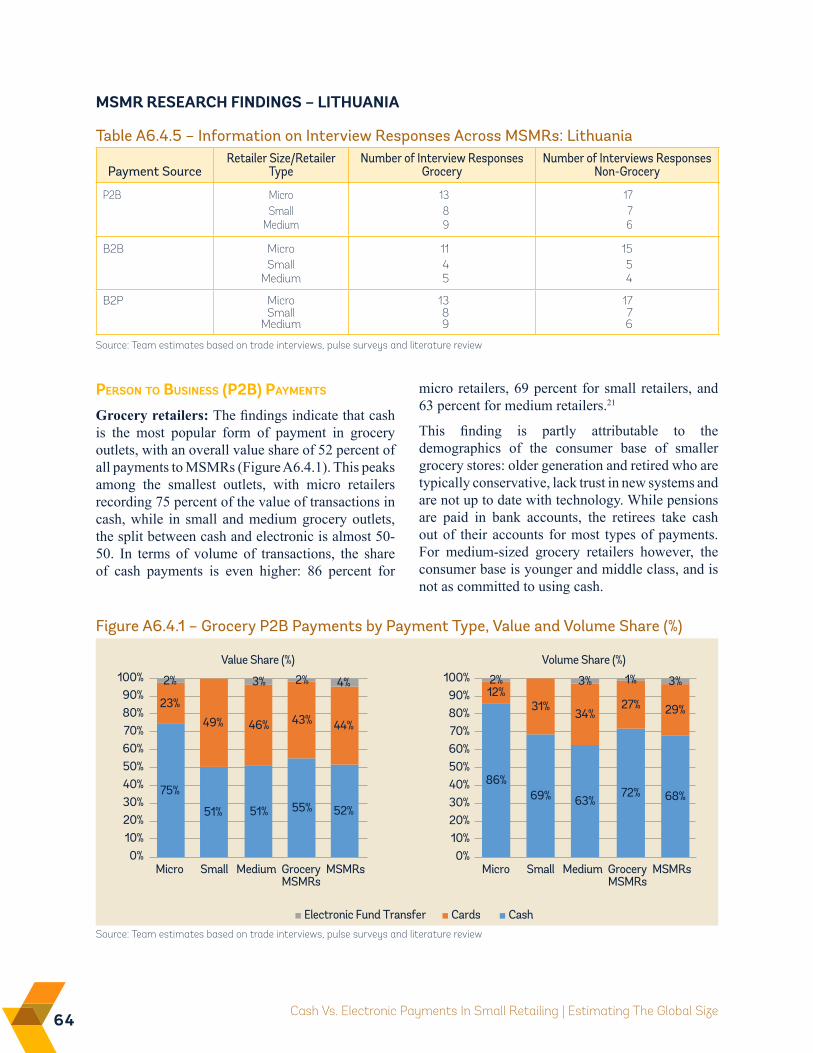

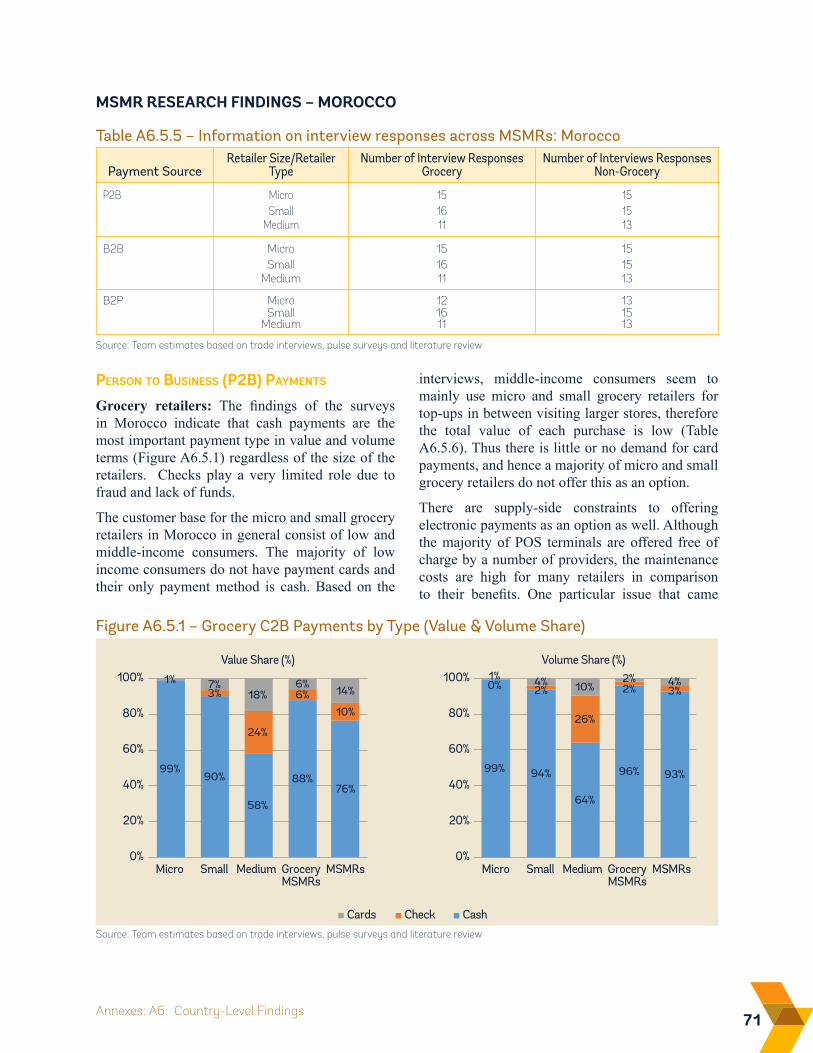

Figure 5 summarizes the findings in the seven countries for the value share of electronic P2B payments. In general, consumers tend to use cash more widely for groceries as opposed to non-groceries which are mostly larger ticket items. Colombia, Kenya, Morocco and Pakistan rely more on cash payments across all MSMR payment flows. Turkey’s national strategy to become a cashless society is pushing card payments over cash, but there is still heavy cash use, more than 50 percent of all P2B payments at MSMRs, both in terms of value and volume and regardless of the size of the MSMRs or the type of product, are made in cash. In France, checks are still used but their use is declining with more and more people starting to use electronic payments.

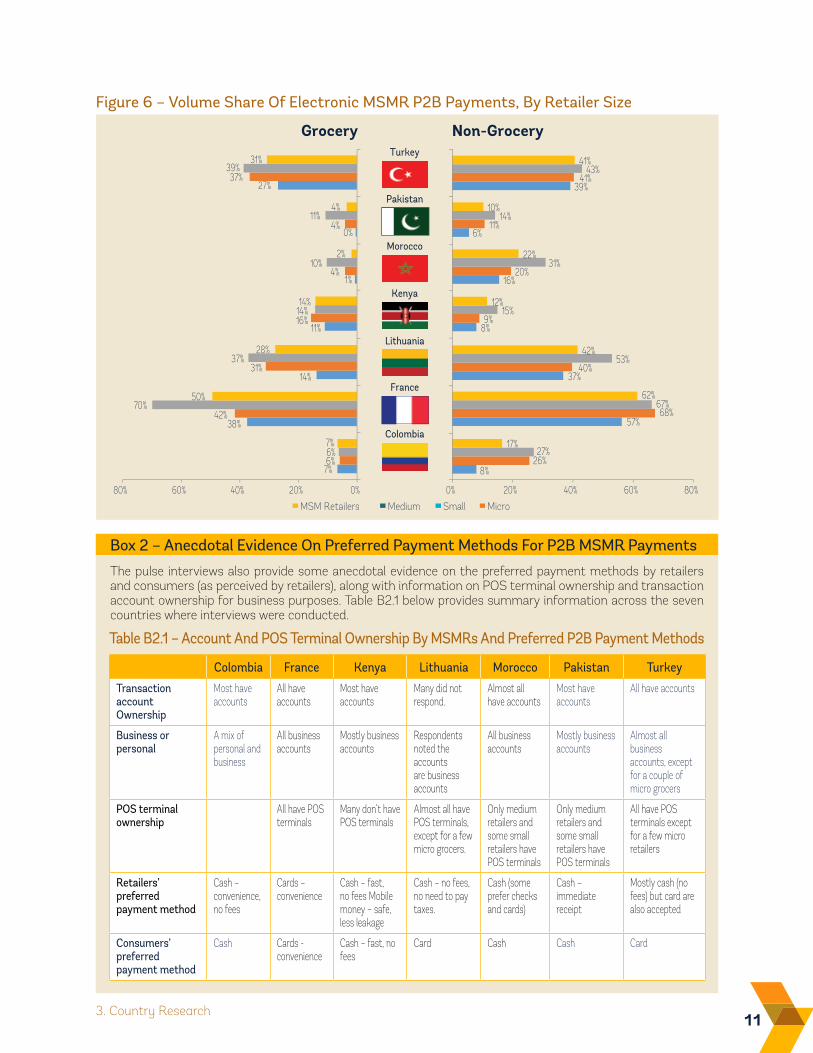

For MSMR P2B payments, the volume share of electronic payments is lower than the value share, indicating that mostly a smaller number of higher value transactions are paid for electronically, while many low-ticket purchases are paid in cash (Figures

Figure 5 – Value Share Of Electronic MSMR P2B Payments, By Retailer Size

7%

42%

25%

7%

1%

1%

30%

8%

47%

49%

10%

7%

5%

42%

10%

72%

49%

14%

19%

16%

47%

8%

61%

45%

13%

6%

9%

39%

0%20%40%60%80%

12%

58%

46%

8%

18%

7%

42%

32%

68%

55%

10%

24%

15%

45%

33%

74%

60%

17%

37%

19%

49%

26%

66%

54%

15%

31%

17%

46%

0% 20% 40% 60% 80%

Grocery Non-Grocery

MSM Retailers Medium Small Micro

Turkey

Pakistan

Morocco

Lithuania

Kenya

Colombia

France

Note: MSM = micro, small and medium

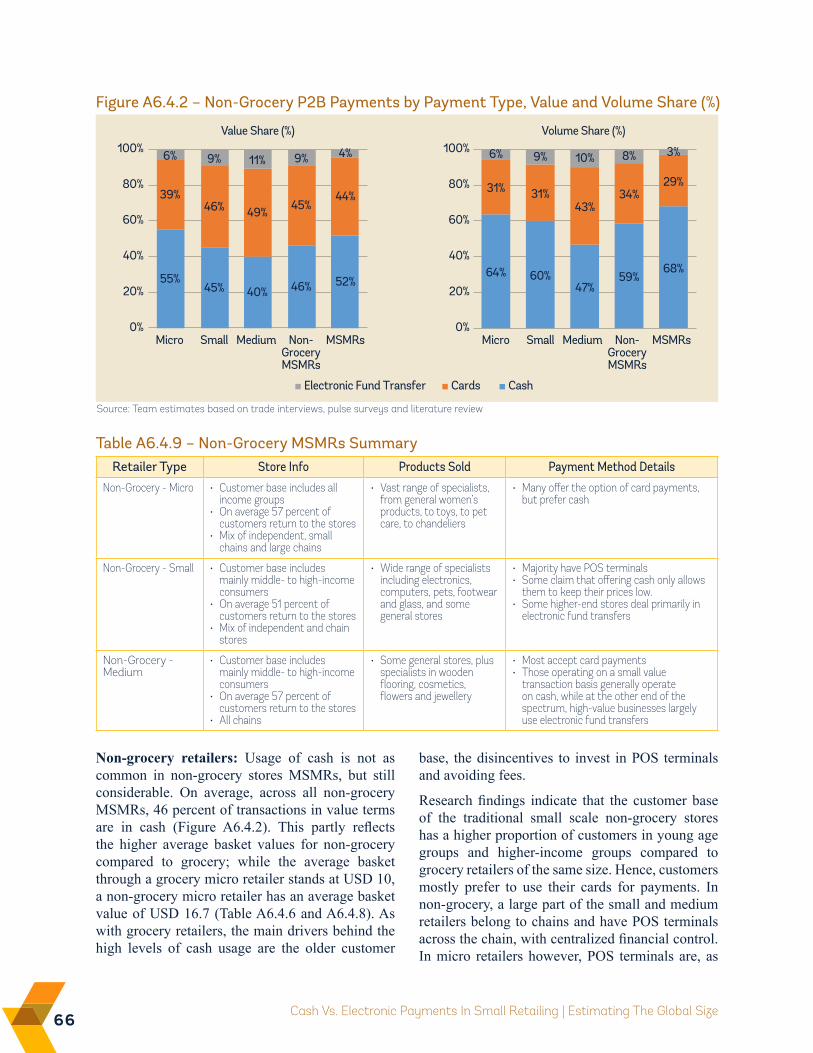

5 and 6 compared). This seems to apply to all countries, to both grocery and non-grocery retailers, and to all retailer sizes. Additionally, insights from pulse surveys indicate that for non-grocery purchases, there is a gradually increasing interest in using credit cards in Pakistan and in Morocco for P2B retail payments. Box 2 provides some anecdotal evidence on the preferred P2B payment methods by retailers and consumers (as perceived by retailers) and information on transaction account and POS terminal ownership.

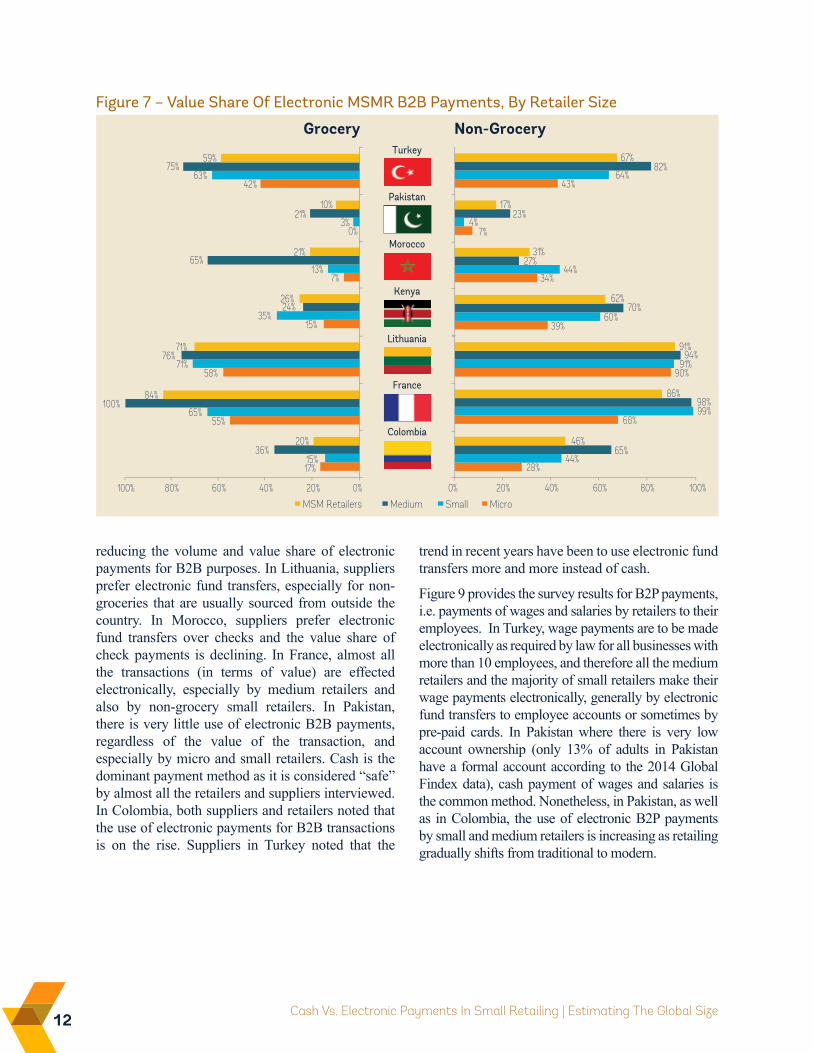

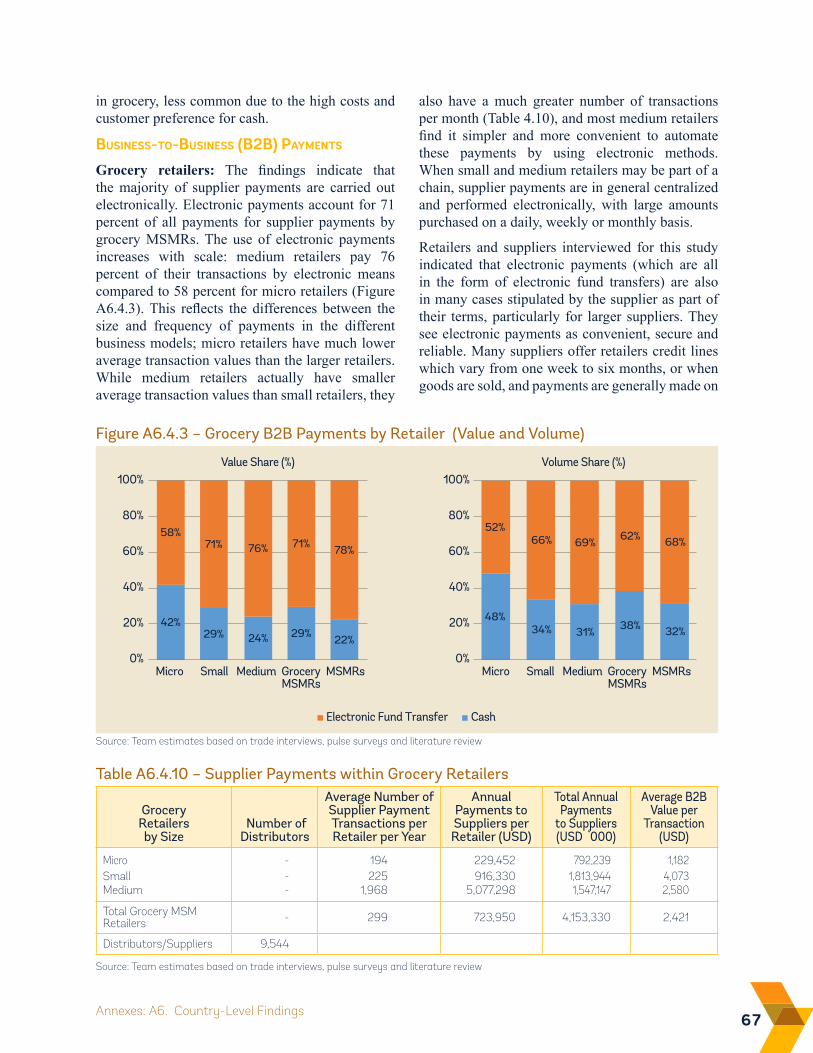

Figures 7 and 8 show the value and volume share of electronic MSMR B2B payments, respectively, with a breakdown by retailer size. As in the case for P2B, these figures show that less frequent transactions of larger value are done electronically.

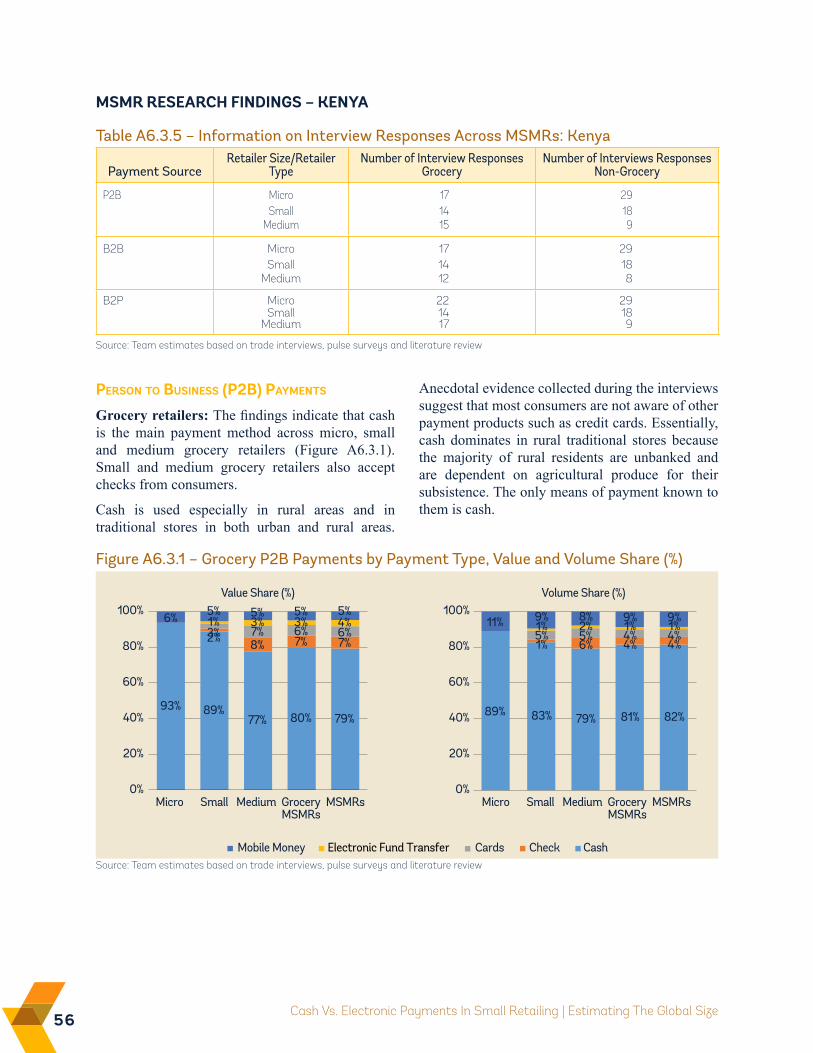

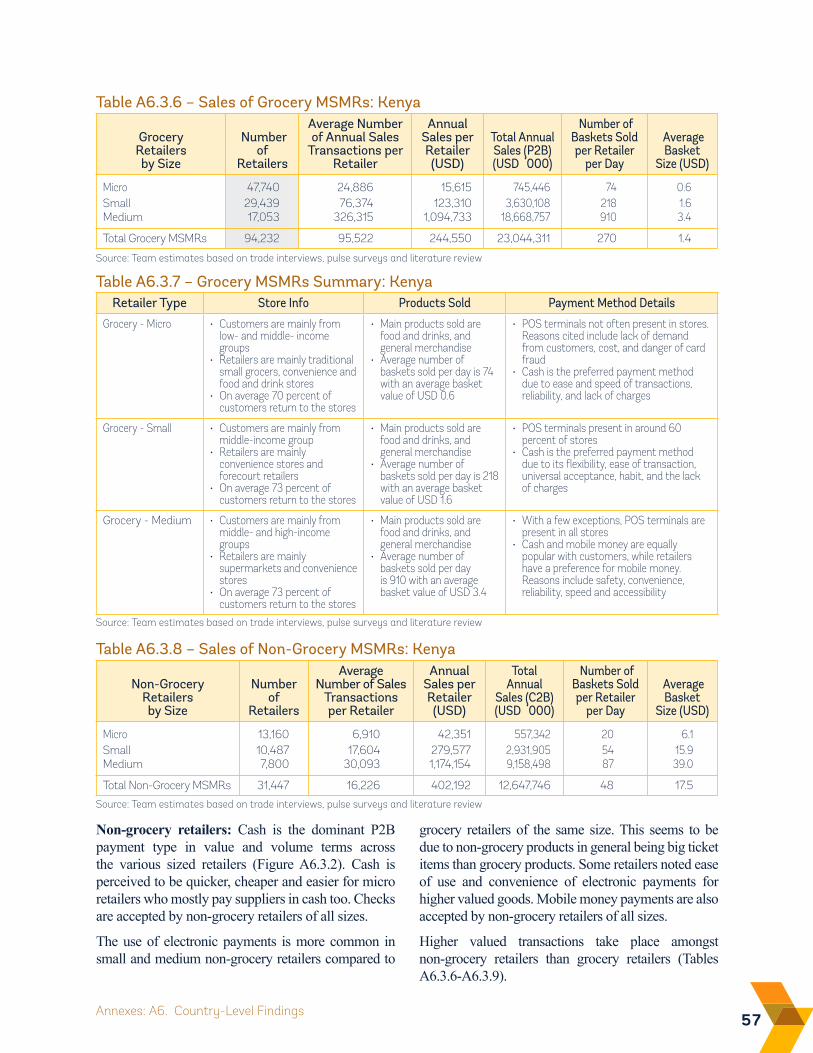

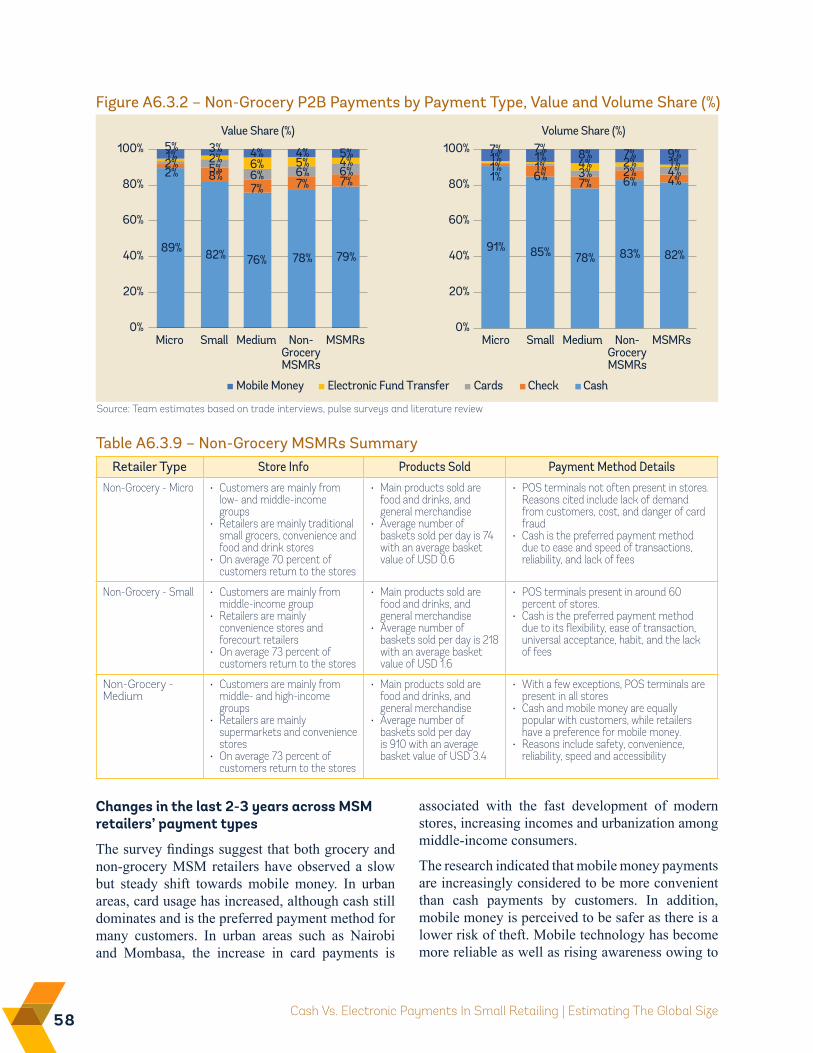

Anecdotal evidence collected during pulse surveys and trade interviews suggest that in Kenya suppliers accept mobile money. However, medium-sized retailers in Kenya use checks for B2B payments,

113. Country Research

Figure 6 – Volume Share Of Electronic MSMR P2B Payments, By Retailer Size

7%

38%

14%

11%

1%

0%

27%

6%

42%

31%

16%

4%

4%

37%

6%

70%

37%

14%

10%

11%

39%

7%

50%

28%

14%

2%

4%

31%

68%

8%

57%

37%

8%

16%

6%

39%

26%

40%

9%

20%

11%

41%

27%

67%

53%

15%

31%

14%

43%

17%

62%

42%

12%

22%

10%

41%

0%20%40%60%80% 0% 20% 40% 60% 80%

Grocery Non-Grocery

MSM Retailers Medium Small Micro

Turkey

Pakistan

Morocco

Lithuania

Kenya

Colombia

France

The pulse interviews also provide some anecdotal evidence on the preferred payment methods by retailers and consumers (as perceived by retailers), along with information on POS terminal ownership and transaction account ownership for business purposes. Table B2.1 below provides summary information across the seven countries where interviews were conducted.

Box 2 – Anecdotal Evidence On Preferred Payment Methods For P2B MSMR Payments

Table B2.1 – Account And POS Terminal Ownership By MSMRs And Preferred P2B Payment Methods

Colombia France Kenya Lithuania Morocco Pakistan Turkey

Transaction account Ownership

Most have accounts

All have accounts

Most have accounts

Many did not respond.

Almost all have accounts

Most have accounts

All have accounts

Business or personal

A mix of personal and business

All business accounts

Mostly business accounts

Respondents noted the accounts are business accounts

All business accounts

Mostly business accounts

Almost all business accounts, except for a couple of micro grocers

POS terminal ownership

All have POS terminals

Many don’t have POS terminals

Almost all have POS terminals, except for a few micro grocers.

Only medium retailers and some small retailers have POS terminals

Only medium retailers and some small retailers have POS terminals

All have POS terminals except for a few micro retailers

Retailers’ preferred payment method

Cash – convenience, no fees

Cards – convenience

Cash – fast, no fees Mobile money – safe, less leakage

Cash – no fees, no need to pay taxes.

Cash (some prefer checks and cards)

Cash – immediate receipt

Mostly cash (no fees) but card are also accepted

Consumers’ preferred payment method

Cash Cards - convenience

Cash – fast, no fees

Card Cash Cash Card

12 Cash Vs. Electronic Payments In Small Retailing | Estimating The Global Size

Figure 7 – Value Share Of Electronic MSMR B2B Payments, By Retailer Size

0%20%40%60%80%100% 0% 20% 40% 60% 100%80%

Grocery Non-Grocery

MSM Retailers Medium Small Micro

Turkey

Pakistan

Morocco

Lithuania

Kenya

Colombia

France

17%

55%

58%

15%

7%

0%

42%

15%

65%

71%

35%

13%

3%

63%

36%

100%

76%

24%

65%

21%

75%

20%

84%

71%

26%

21%

10%

59%

28%

68%

90%

39%

34%

7%

43%

44%

99%

91%

60%

44%

4%

64%

65%

98%

94%

70%

27%

23%

82%

46%

86%

91%

62%

31%

17%

67%

reducing the volume and value share of electronic payments for B2B purposes. In Lithuania, suppliers prefer electronic fund transfers, especially for non-groceries that are usually sourced from outside the country. In Morocco, suppliers prefer electronic fund transfers over checks and the value share of check payments is declining. In France, almost all the transactions (in terms of value) are effected electronically, especially by medium retailers and also by non-grocery small retailers. In Pakistan, there is very little use of electronic B2B payments, regardless of the value of the transaction, and especially by micro and small retailers. Cash is the dominant payment method as it is considered “safe” by almost all the retailers and suppliers interviewed. In Colombia, both suppliers and retailers noted that the use of electronic payments for B2B transactions is on the rise. Suppliers in Turkey noted that the

trend in recent years have been to use electronic fund transfers more and more instead of cash.

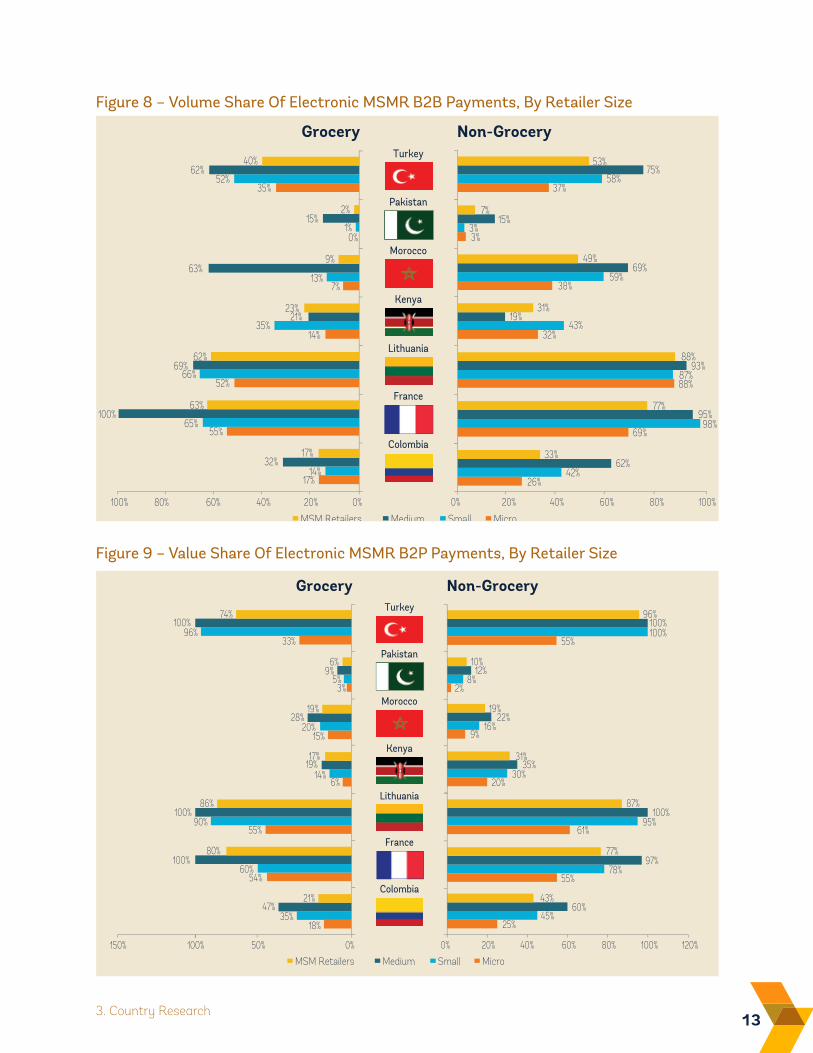

Figure 9 provides the survey results for B2P payments, i.e. payments of wages and salaries by retailers to their employees. In Turkey, wage payments are to be made electronically as required by law for all businesses with more than 10 employees, and therefore all the medium retailers and the majority of small retailers make their wage payments electronically, generally by electronic fund transfers to employee accounts or sometimes by pre-paid cards. In Pakistan where there is very low account ownership (only 13% of adults in Pakistan have a formal account according to the 2014 Global Findex data), cash payment of wages and salaries is the common method. Nonetheless, in Pakistan, as well as in Colombia, the use of electronic B2P payments by small and medium retailers is increasing as retailing gradually shifts from traditional to modern.

133. Country Research

Figure 9 – Value Share Of Electronic MSMR B2P Payments, By Retailer Size

Figure 8 – Volume Share Of Electronic MSMR B2B Payments, By Retailer Size

0%20%40%60%100% 0% 20% 40% 60% 100%80%

Grocery Non-Grocery

MSM Retailers Medium Small Micro

Turkey

Pakistan

Morocco

Lithuania

Kenya

Colombia

France

17%

55%

52%

14%

7%

0%

35%

14%

65%

66%

35%

13%

1%

52%

32%

100%

69%

21%

63%

15%

62%

17%

63%

62%

23%

9%

2%

40%

80%

26%

69%

88%

32%

38%

3%

37%

42%

98%

87%

43%

59%

3%

58%

62%

95%

93%

19%

69%

15%

75%

33%

77%

88%

31%

49%

7%

53%

0%50%100%150% 0% 20% 40% 80%60% 120%100%

Grocery Non-Grocery

MSM Retailers Medium Small Micro

Turkey

Pakistan

Morocco

Lithuania

Kenya

Colombia

France

25%

55%

61%

20%

9%

2%

55%

45%

78%

95%

30%

16%

8%

100%

60%

97%

100%

35%

22%

12%

100%

43%

77%

87%

31%

19%

10%

96%

18%

54%

55%

6%

15%

3%

33%

35%

60%

90%

14%

20%

5%

96%

47%

100%

100%

19%

28%

9%

100%

21%

80%

86%

17%

19%

6%

74%

14 Cash vs. Electronic Payments In Small Retailing | Estimating the Global Size

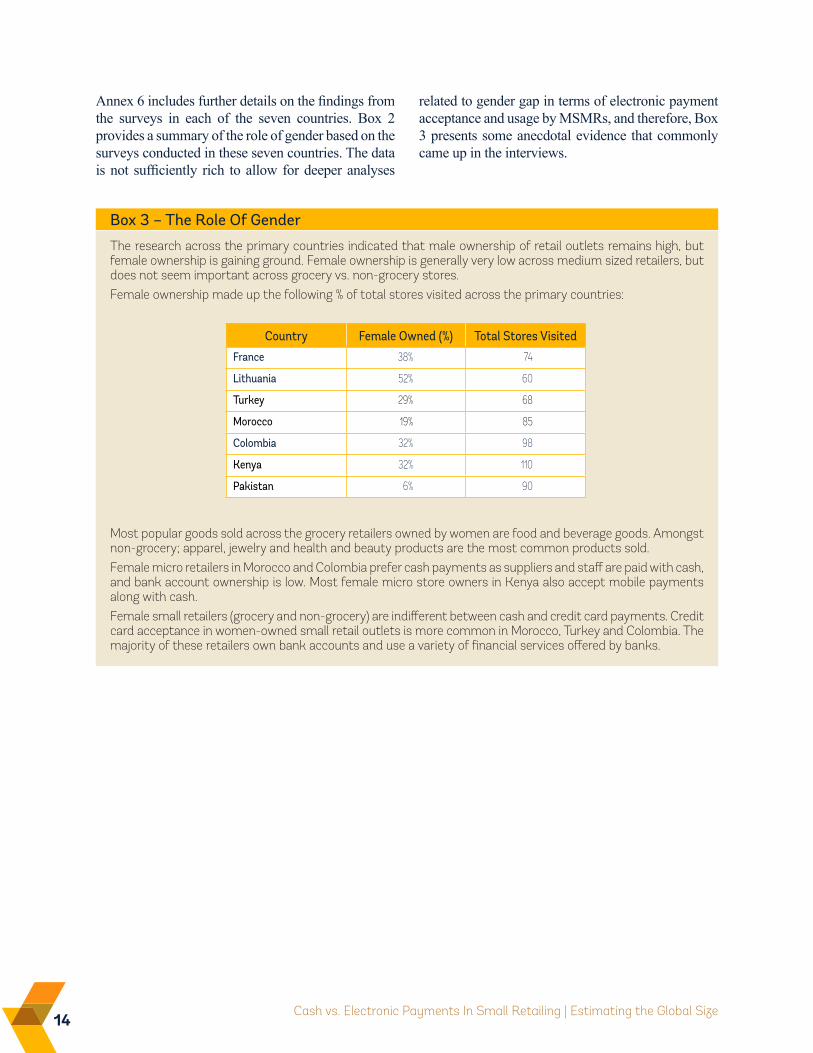

Annex 6 includes further details on the findings from the surveys in each of the seven countries. Box 2 provides a summary of the role of gender based on the surveys conducted in these seven countries. The data is not sufficiently rich to allow for deeper analyses

The research across the primary countries indicated that male ownership of retail outlets remains high, but female ownership is gaining ground. Female ownership is generally very low across medium sized retailers, but does not seem important across grocery vs. non-grocery stores. Female ownership made up the following % of total stores visited across the primary countries:

Most popular goods sold across the grocery retailers owned by women are food and beverage goods. Amongst non-grocery; apparel, jewelry and health and beauty products are the most common products sold. Female micro retailers in Morocco and Colombia prefer cash payments as suppliers and staff are paid with cash, and bank account ownership is low. Most female micro store owners in Kenya also accept mobile payments along with cash.Female small retailers (grocery and non-grocery) are indifferent between cash and credit card payments. Credit card acceptance in women-owned small retail outlets is more common in Morocco, Turkey and Colombia. The majority of these retailers own bank accounts and use a variety of financial services offered by banks.

Box 3 – The Role Of Gender

Country Female Owned (%) Total Stores Visited

France 38% 74

Lithuania 52% 60

Turkey 29% 68

Morocco 19% 85

Colombia 32% 98

Kenya 32% 110

Pakistan 6% 90

related to gender gap in terms of electronic payment acceptance and usage by MSMRs, and therefore, Box 3 presents some anecdotal evidence that commonly came up in the interviews.

154. Global Size of Digital vs Cash Transactions by MSMRs

This section provides an overview of the estimated share of electronic payments across different payment flow types for MSMRs. Global results are based on aggregations of country-level estimates, which are based on simulations using data from seven primary research countries: Colombia, France, Kenya, Lithuania, Morocco, Pakistan and Turkey.

4.1 PERSON-TO-BUSiNESS PAYMENTS FOR MSMRsAccording to the estimation results, developing regions exhibit a higher percentage of paper-based payment transactions (cash and checks) compared to developed markets. The trend is also more prominent with micro retailers where many self-employed firms or mom-and-pop stores tend to shy away from electronic transactions such as debit or credit cards due to extra costs including fees and service charges, lack of awareness, difficulty in accessing financial services and other challenges.

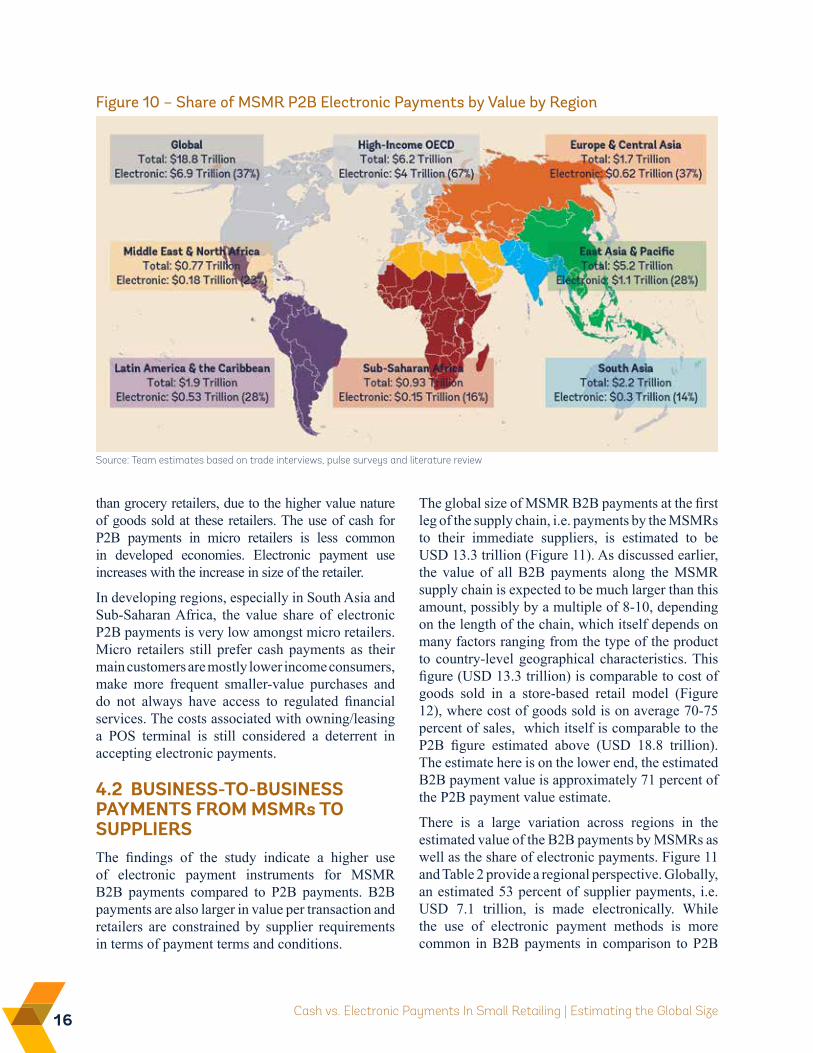

Figure 10 provides consolidated results globally and per region. The global value of MSMR P2B payments is estimated at USD 18.8 trillion. This figure is consistent with other similar studies. For example, the Economist Intelligence Unit (EIU) estimates the 2014 value of total retail sales at USD 17.5 trillion for 58 countries. A new report by Visa (2016) estimates that 43 percent of consumer payments globally are made in cash, which amount

to USD 21 trillion. According to eMarketer, global retail sales was an estimated USD 24 trillion in 2015. A recent report by Citigroup (2016) estimates the global consumer retail payments as USD 23 trillion as of 2014, and forecasts it to reach USD 32 trillion by 2020. And Deloitte (2015) estimates the retail sales of the largest 250 retailers in globally at USD 4.5 trillion.

The share of electronic payments in total MSMR P2B payment value varies largely across countries. While electronic payments are estimated to constitute 37 percent of MSMR P2B payments value globally, this share is as high as 64 percent in high-income OECD economies. Sub-Saharan African economies and South Asian economies have the lowest share by 16 percent and 14 percent, respectively.

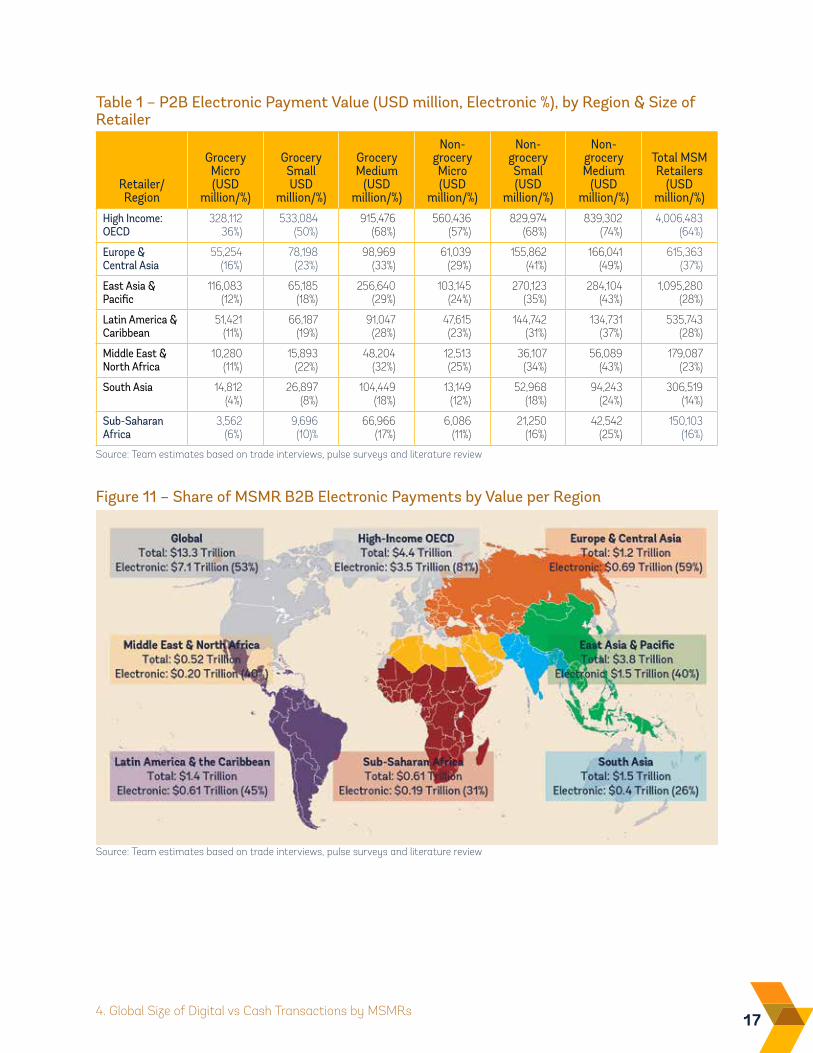

Table 1 shows the estimated electronic payment value and percentage of overall MSM retail value across the regions and retailer type for P2B payments.

The findings show, perhaps not surprisingly, that within each region it is more common to use electronic payments amongst small and medium retailers compared to micro retailers. Electronic payment use increases with the increase in size of the retailer. During the interviews, small and medium retailers cited convenience and safety as reasons for accepting electronic payments. There is a higher use of electronic payments amongst non-grocery retailers

16 Cash vs. Electronic Payments In Small Retailing | Estimating the Global Size

than grocery retailers, due to the higher value nature of goods sold at these retailers. The use of cash for P2B payments in micro retailers is less common in developed economies. Electronic payment use increases with the increase in size of the retailer.

In developing regions, especially in South Asia and Sub-Saharan Africa, the value share of electronic P2B payments is very low amongst micro retailers. Micro retailers still prefer cash payments as their main customers are mostly lower income consumers, make more frequent smaller-value purchases and do not always have access to regulated financial services. The costs associated with owning/leasing a POS terminal is still considered a deterrent in accepting electronic payments.

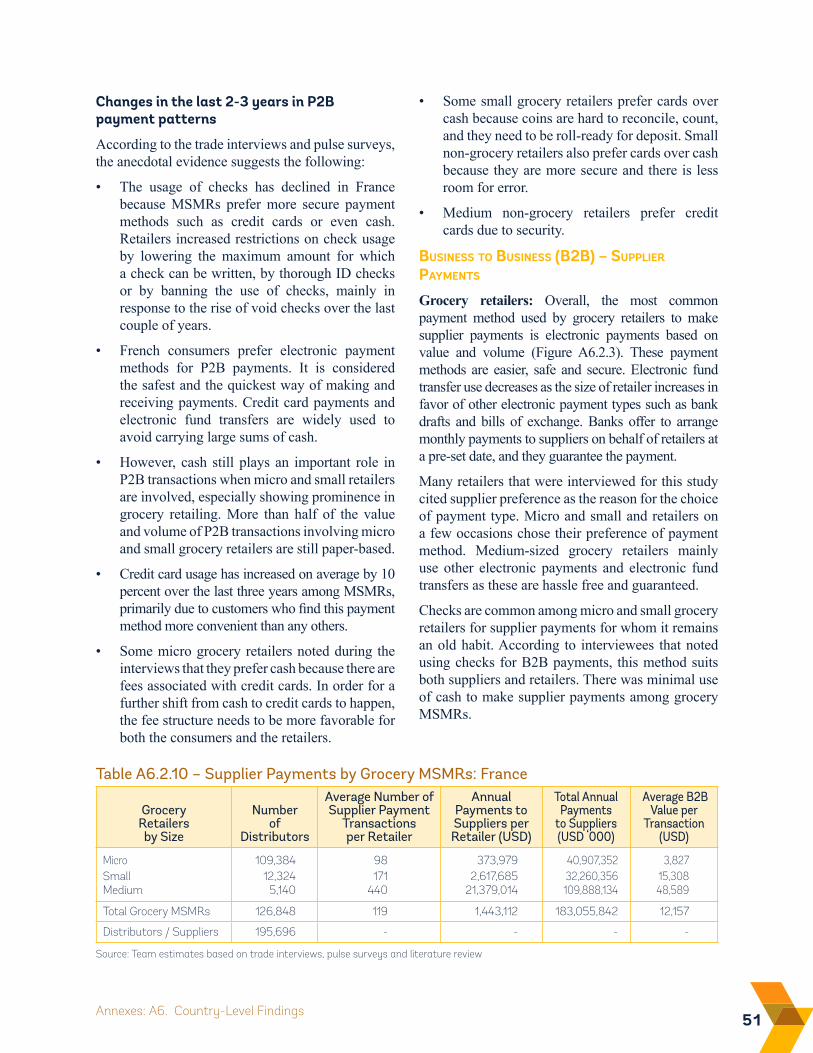

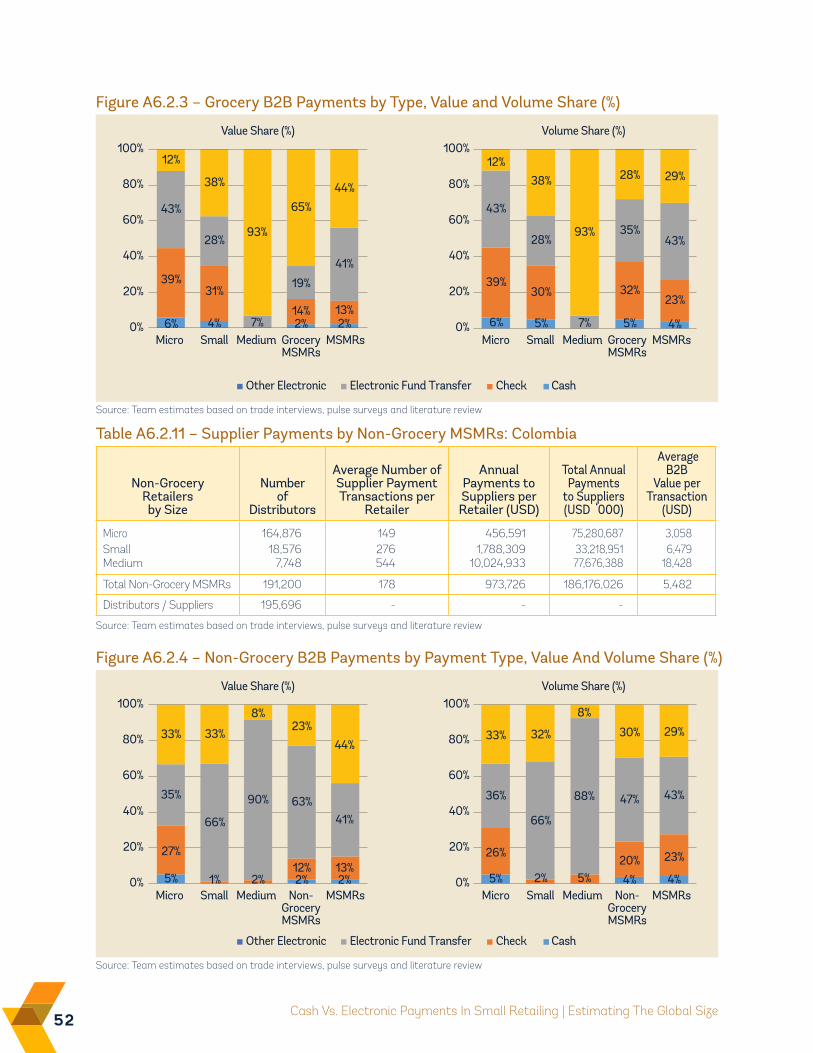

4.2 BUSiNESS-TO-BUSiNESS PAYMENTS FROM MSMRs TO SUPPLiERSThe findings of the study indicate a higher use of electronic payment instruments for MSMR B2B payments compared to P2B payments. B2B payments are also larger in value per transaction and retailers are constrained by supplier requirements in terms of payment terms and conditions.

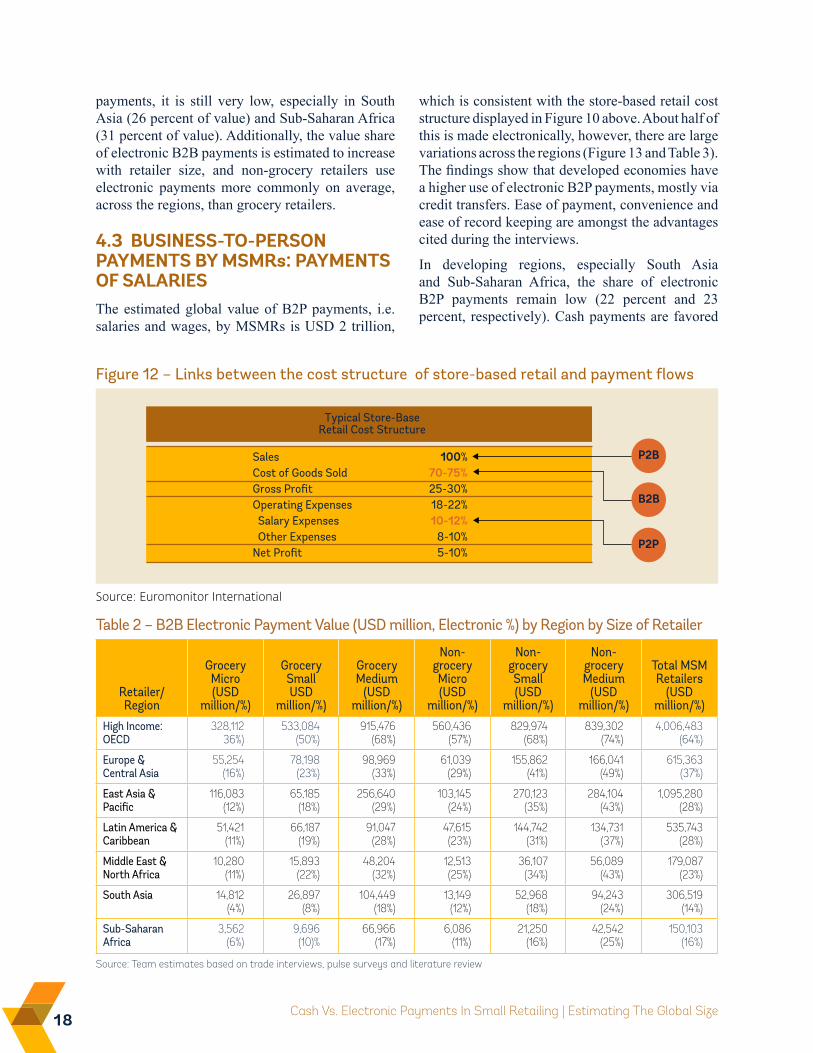

The global size of MSMR B2B payments at the first leg of the supply chain, i.e. payments by the MSMRs to their immediate suppliers, is estimated to be USD 13.3 trillion (Figure 11). As discussed earlier, the value of all B2B payments along the MSMR supply chain is expected to be much larger than this amount, possibly by a multiple of 8-10, depending on the length of the chain, which itself depends on many factors ranging from the type of the product to country-level geographical characteristics. This figure (USD 13.3 trillion) is comparable to cost of goods sold in a store-based retail model (Figure 12), where cost of goods sold is on average 70-75 percent of sales, which itself is comparable to the P2B figure estimated above (USD 18.8 trillion). The estimate here is on the lower end, the estimated B2B payment value is approximately 71 percent of the P2B payment value estimate.

There is a large variation across regions in the estimated value of the B2B payments by MSMRs as well as the share of electronic payments. Figure 11 and Table 2 provide a regional perspective. Globally, an estimated 53 percent of supplier payments, i.e. USD 7.1 trillion, is made electronically. While the use of electronic payment methods is more common in B2B payments in comparison to P2B

Figure 10 – Share of MSMR P2B Electronic Payments by Value by Region

Source: Team estimates based on trade interviews, pulse surveys and literature review

174. Global Size of Digital vs Cash Transactions by MSMRs

Table 1 – P2B Electronic Payment Value (USD million, Electronic %), by Region & Size of Retailer

P=Person, B=Business, G=Government

Retailer/Region

Grocery Micro (USD

million/%)

Grocery Small USD

million/%)

Grocery Medium

(USD million/%)

Non-grocery Micro (USD

million/%)

Non-grocery Small (USD

million/%)

Non-grocery Medium

(USD million/%)

Total MSM Retailers

(USD million/%)

High Income: OECD

328,112 36%)

533,084 (50%)

915,476 (68%)

560,436 (57%)

829,974 (68%)

839,302 (74%)

4,006,483 (64%)

Europe & Central Asia

55,254 (16%)

78,198 (23%)

98,969 (33%)

61,039 (29%)

155,862 (41%)

166,041 (49%)

615,363 (37%)

East Asia & Pacific

116,083 (12%)

65,185 (18%)

256,640 (29%)

103,145 (24%)

270,123 (35%)

284,104 (43%)

1,095,280 (28%)

Latin America & Caribbean

51,421 (11%)

66,187 (19%)

91,047 (28%)

47,615 (23%)

144,742 (31%)

134,731 (37%)

535,743 (28%)

Middle East & North Africa

10,280 (11%)

15,893 (22%)

48,204 (32%)

12,513 (25%)

36,107 (34%)

56,089 (43%)

179,087 (23%)

South Asia 14,812 (4%)

26,897 (8%)

104,449 (18%)

13,149 (12%)

52,968 (18%)

94,243 (24%)

306,519 (14%)

Sub-Saharan Africa

3,562 (6%)

9,696 (10)%

66,966 (17%)

6,086 (11%)

21,250 (16%)

42,542 (25%)

150,103 (16%)

Source: Team estimates based on trade interviews, pulse surveys and literature review

Figure 11 – Share of MSMR B2B Electronic Payments by Value per Region

Source: Team estimates based on trade interviews, pulse surveys and literature review

18 Cash Vs. Electronic Payments In Small Retailing | Estimating The Global Size

payments, it is still very low, especially in South Asia (26 percent of value) and Sub-Saharan Africa (31 percent of value). Additionally, the value share of electronic B2B payments is estimated to increase with retailer size, and non-grocery retailers use electronic payments more commonly on average, across the regions, than grocery retailers.

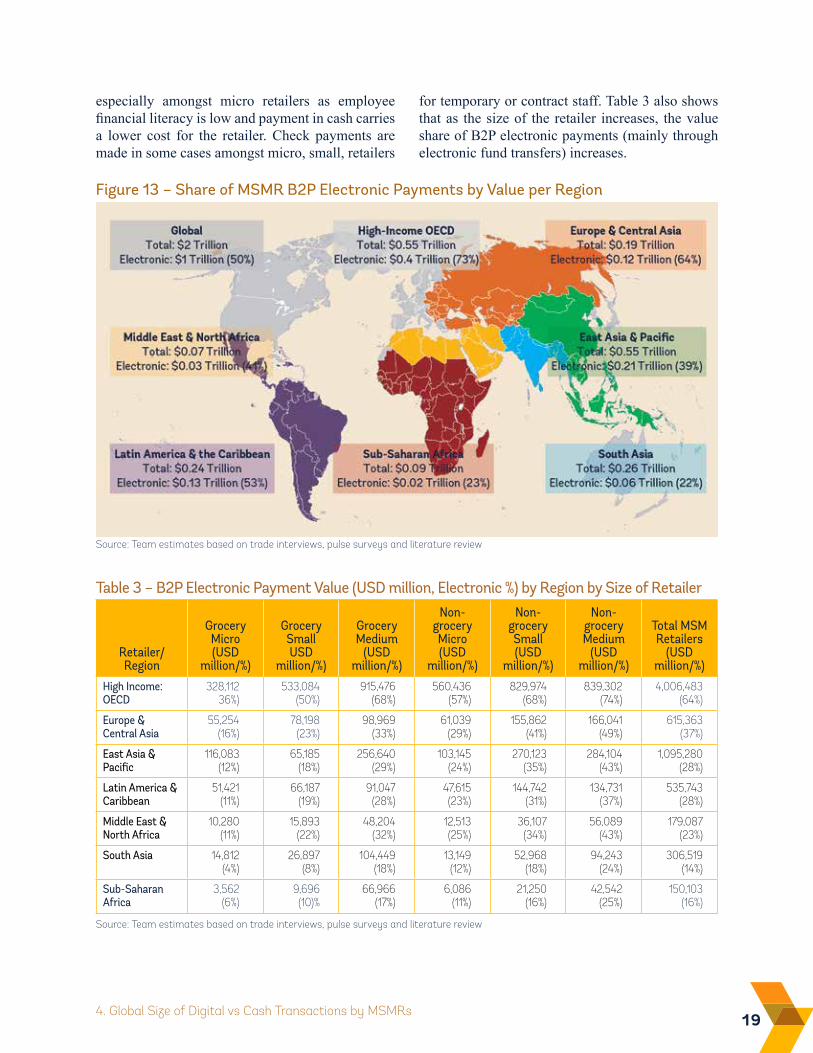

4.3 BUSiNESS-TO-PERSON PAYMENTS BY MSMRs: PAYMENTS OF SALARiESThe estimated global value of B2P payments, i.e. salaries and wages, by MSMRs is USD 2 trillion,

which is consistent with the store-based retail cost structure displayed in Figure 10 above. About half of this is made electronically, however, there are large variations across the regions (Figure 13 and Table 3). The findings show that developed economies have a higher use of electronic B2P payments, mostly via credit transfers. Ease of payment, convenience and ease of record keeping are amongst the advantages cited during the interviews.

In developing regions, especially South Asia and Sub-Saharan Africa, the share of electronic B2P payments remain low (22 percent and 23 percent, respectively). Cash payments are favored

Table 2 – B2B Electronic Payment Value (USD million, Electronic %) by Region by Size of Retailer

P=Person, B=Business, G=Government

Retailer/Region

Grocery Micro (USD

million/%)

Grocery Small USD

million/%)

Grocery Medium

(USD million/%)

Non-grocery Micro (USD

million/%)

Non-grocery Small (USD

million/%)

Non-grocery Medium

(USD million/%)

Total MSM Retailers

(USD million/%)

High Income: OECD

328,112 36%)

533,084 (50%)

915,476 (68%)

560,436 (57%)

829,974 (68%)

839,302 (74%)

4,006,483 (64%)

Europe & Central Asia

55,254 (16%)

78,198 (23%)

98,969 (33%)

61,039 (29%)

155,862 (41%)

166,041 (49%)

615,363 (37%)

East Asia & Pacific

116,083 (12%)

65,185 (18%)

256,640 (29%)

103,145 (24%)

270,123 (35%)

284,104 (43%)

1,095,280 (28%)

Latin America & Caribbean

51,421 (11%)

66,187 (19%)

91,047 (28%)

47,615 (23%)

144,742 (31%)

134,731 (37%)

535,743 (28%)

Middle East & North Africa

10,280 (11%)

15,893 (22%)

48,204 (32%)

12,513 (25%)

36,107 (34%)

56,089 (43%)

179,087 (23%)

South Asia 14,812 (4%)

26,897 (8%)

104,449 (18%)

13,149 (12%)

52,968 (18%)

94,243 (24%)

306,519 (14%)

Sub-Saharan Africa

3,562 (6%)

9,696 (10)%

66,966 (17%)

6,086 (11%)

21,250 (16%)

42,542 (25%)

150,103 (16%)

Source: Team estimates based on trade interviews, pulse surveys and literature review

Figure 12 – Links between the cost structure of store-based retail and payment flows

Source: Euromonitor International

SalesCost of Goods SoldGross ProfitOperating Expenses Salary Expenses Other ExpensesNet Profit

100%70-75%25-30%18-22%10-12%

8-10%5-10%

Typical Store-BaseRetail Cost Structure

B2B

P2P

P2B

194. Global Size of Digital vs Cash Transactions by MSMRs

especially amongst micro retailers as employee financial literacy is low and payment in cash carries a lower cost for the retailer. Check payments are made in some cases amongst micro, small, retailers

Table 3 – B2P Electronic Payment Value (USD million, Electronic %) by Region by Size of Retailer

Retailer/Region

Grocery Micro (USD

million/%)

Grocery Small USD

million/%)

Grocery Medium

(USD million/%)

Non-grocery Micro (USD

million/%)

Non-grocery Small (USD

million/%)

Non-grocery Medium

(USD million/%)

Total MSM Retailers

(USD million/%)

High Income: OECD

328,112 36%)

533,084 (50%)

915,476 (68%)

560,436 (57%)

829,974 (68%)

839,302 (74%)

4,006,483 (64%)

Europe & Central Asia

55,254 (16%)

78,198 (23%)

98,969 (33%)

61,039 (29%)

155,862 (41%)

166,041 (49%)

615,363 (37%)

East Asia & Pacific

116,083 (12%)

65,185 (18%)

256,640 (29%)

103,145 (24%)

270,123 (35%)

284,104 (43%)

1,095,280 (28%)

Latin America & Caribbean

51,421 (11%)

66,187 (19%)

91,047 (28%)

47,615 (23%)

144,742 (31%)

134,731 (37%)

535,743 (28%)

Middle East & North Africa

10,280 (11%)

15,893 (22%)

48,204 (32%)

12,513 (25%)

36,107 (34%)

56,089 (43%)

179,087 (23%)

South Asia 14,812 (4%)

26,897 (8%)

104,449 (18%)

13,149 (12%)

52,968 (18%)

94,243 (24%)

306,519 (14%)

Sub-Saharan Africa

3,562 (6%)

9,696 (10)%

66,966 (17%)

6,086 (11%)

21,250 (16%)

42,542 (25%)

150,103 (16%)

Source: Team estimates based on trade interviews, pulse surveys and literature review

Figure 13 – Share of MSMR B2P Electronic Payments by Value per Region

Source: Team estimates based on trade interviews, pulse surveys and literature review

for temporary or contract staff. Table 3 also shows that as the size of the retailer increases, the value share of B2P electronic payments (mainly through electronic fund transfers) increases.

21Annexes

Annexes

AnnexesA1. Glossary 22

A2. Euromonitor Passport Databases 24

A3. List of Economies Used in the Analyses 25

A4. Methodology – Detailed Descriptions 26

A4.1. Cluster Analysis: Details on Methodology 26

A4.2. Primary Research: Details on Methodology 28

A4.3. Modeling and Simulations: Details on Methodology 31

A5. Discussion Guides and Questionnaires 34

A5.1. Trade Interviews 34

A5.2. Pulse Interviews 35

A6. Country Research Findings 39

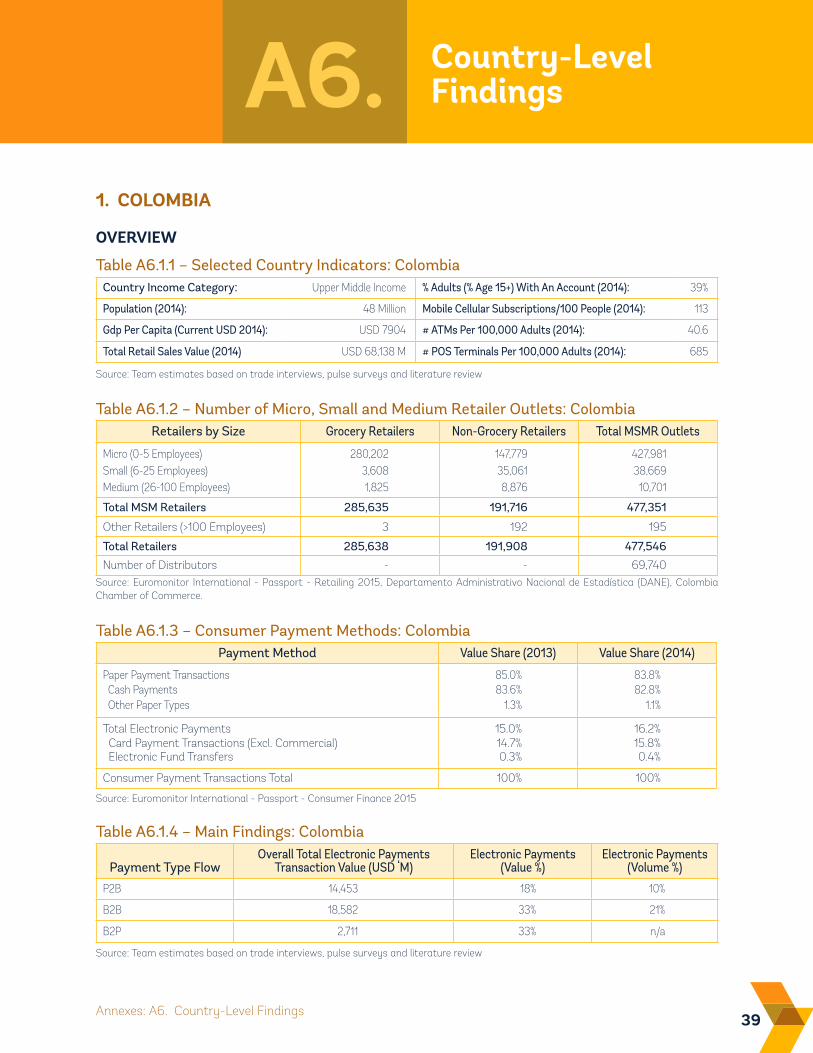

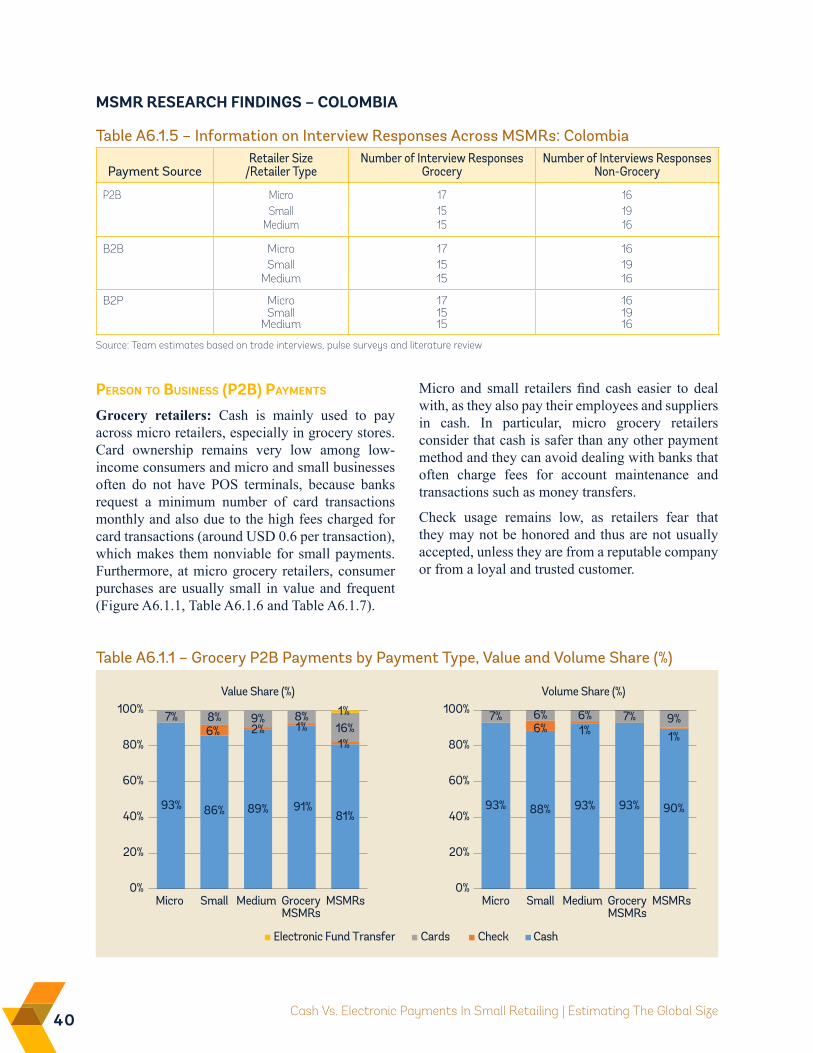

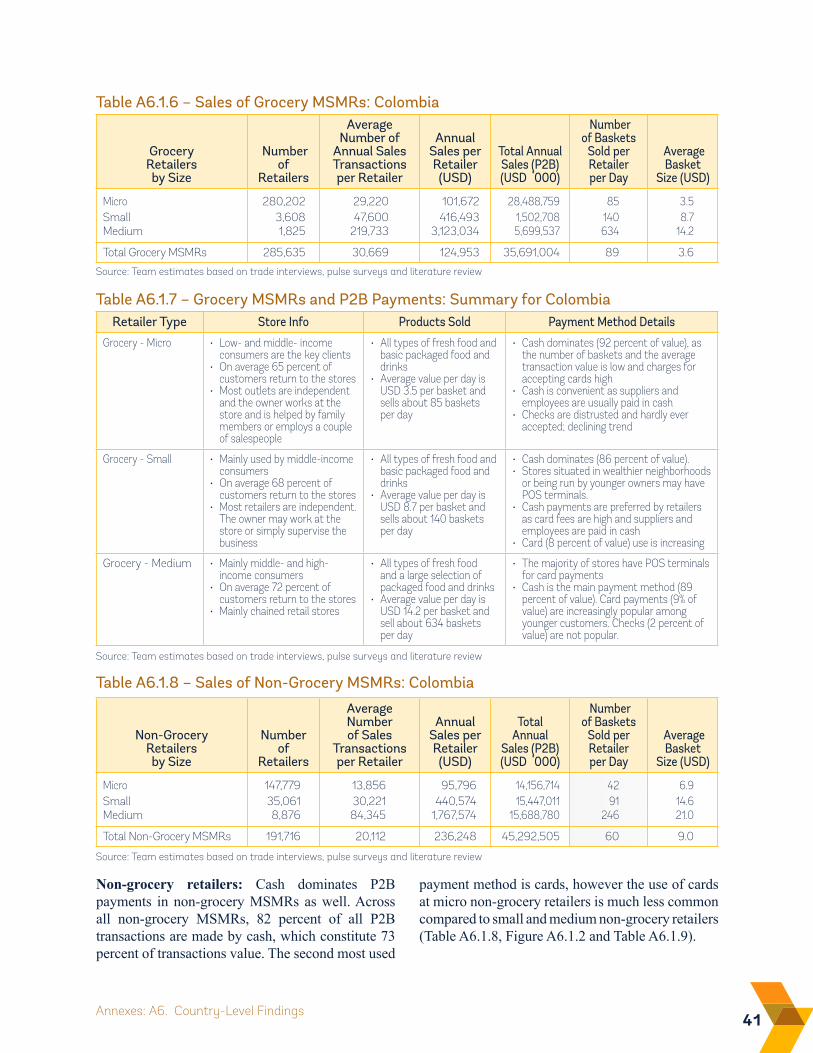

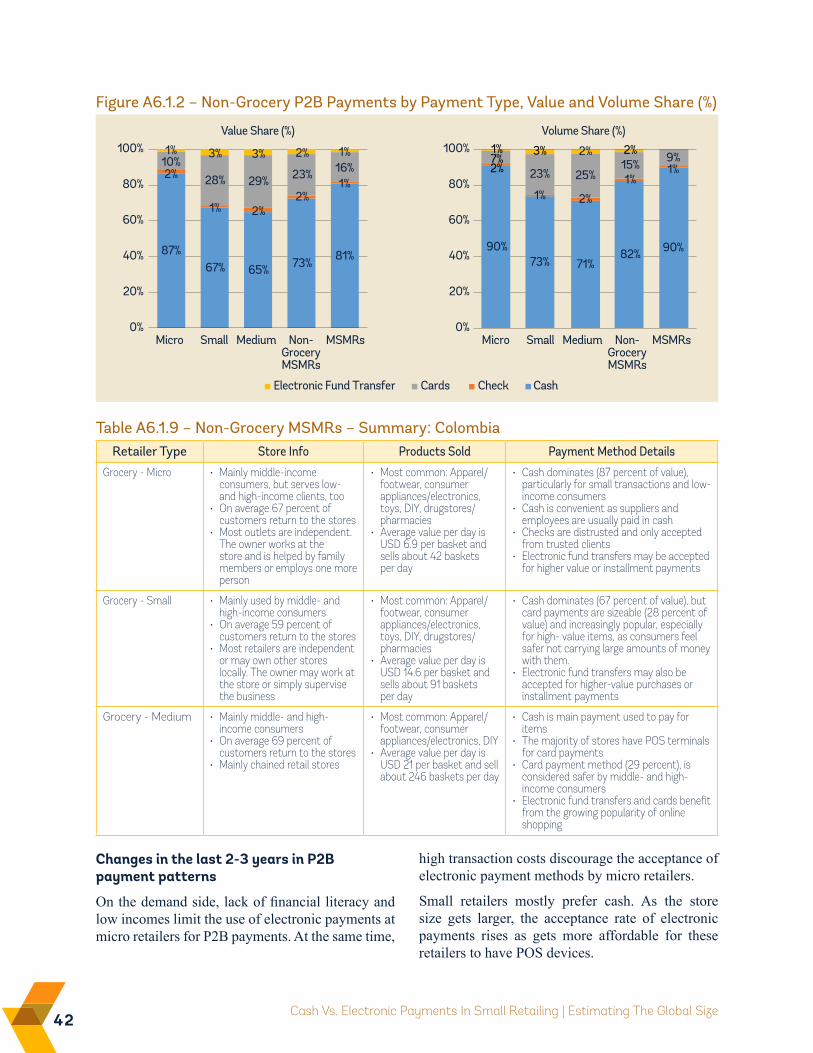

1. Colombia 39

2. France 47

3. Kenya 55

4. Lithuania 63

5. Morocco 70

6. Pakistan 78

7. Turkey 86

22 Cash vs. Electronic Payments In Small Retailing | Estimating the Global Size

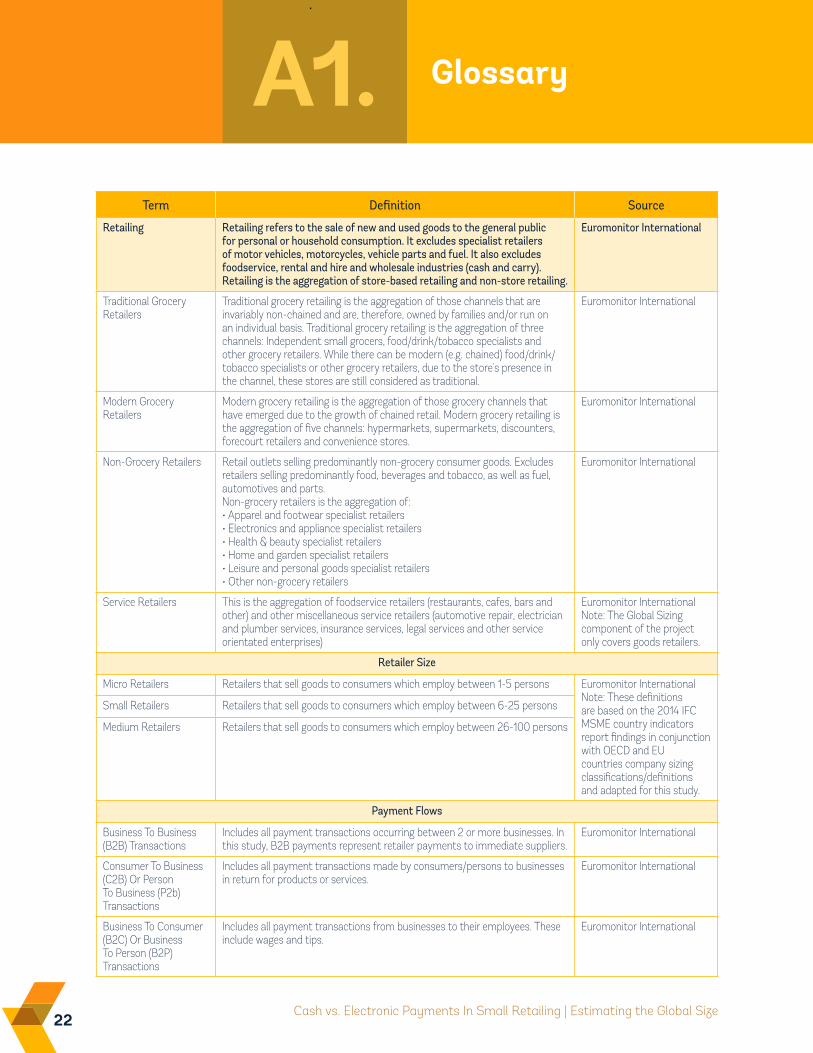

GlossaryA1.Term Definition Source

Retailing Retailing refers to the sale of new and used goods to the general public for personal or household consumption. It excludes specialist retailers of motor vehicles, motorcycles, vehicle parts and fuel. It also excludes foodservice, rental and hire and wholesale industries (cash and carry). Retailing is the aggregation of store-based retailing and non-store retailing.

Euromonitor International

Traditional Grocery Retailers

Traditional grocery retailing is the aggregation of those channels that are invariably non-chained and are, therefore, owned by families and/or run on an individual basis. Traditional grocery retailing is the aggregation of three channels: Independent small grocers, food/drink/tobacco specialists and other grocery retailers. While there can be modern (e.g. chained) food/drink/tobacco specialists or other grocery retailers, due to the store's presence in the channel, these stores are still considered as traditional.

Euromonitor International

Modern Grocery Retailers

Modern grocery retailing is the aggregation of those grocery channels that have emerged due to the growth of chained retail. Modern grocery retailing is the aggregation of five channels: hypermarkets, supermarkets, discounters, forecourt retailers and convenience stores.

Euromonitor International

Non-Grocery Retailers Retail outlets selling predominantly non-grocery consumer goods. Excludes retailers selling predominantly food, beverages and tobacco, as well as fuel, automotives and parts. Non-grocery retailers is the aggregation of: • Apparel and footwear specialist retailers• Electronics and appliance specialist retailers• Health & beauty specialist retailers• Home and garden specialist retailers• Leisure and personal goods specialist retailers• Other non-grocery retailers

Euromonitor International

Service Retailers This is the aggregation of foodservice retailers (restaurants, cafes, bars and other) and other miscellaneous service retailers (automotive repair, electrician and plumber services, insurance services, legal services and other service orientated enterprises)

Euromonitor InternationalNote: The Global Sizing component of the project only covers goods retailers.

Retailer Size

Micro Retailers Retailers that sell goods to consumers which employ between 1-5 persons Euromonitor InternationalNote: These definitions are based on the 2014 IFC MSME country indicators report findings in conjunction with OECD and EU countries company sizing classifications/definitions and adapted for this study.

Small Retailers Retailers that sell goods to consumers which employ between 6-25 persons

Medium Retailers Retailers that sell goods to consumers which employ between 26-100 persons

Payment Flows

Business To Business (B2B) Transactions

Includes all payment transactions occurring between 2 or more businesses. In this study, B2B payments represent retailer payments to immediate suppliers.

Euromonitor International

Consumer To Business (C2B) Or Person To Business (P2b) Transactions

Includes all payment transactions made by consumers/persons to businesses in return for products or services.

Euromonitor International

Business To Consumer (B2C) Or Business To Person (B2P) Transactions

Includes all payment transactions from businesses to their employees. These include wages and tips.

Euromonitor International

23Annexes: A1. Glossary 23

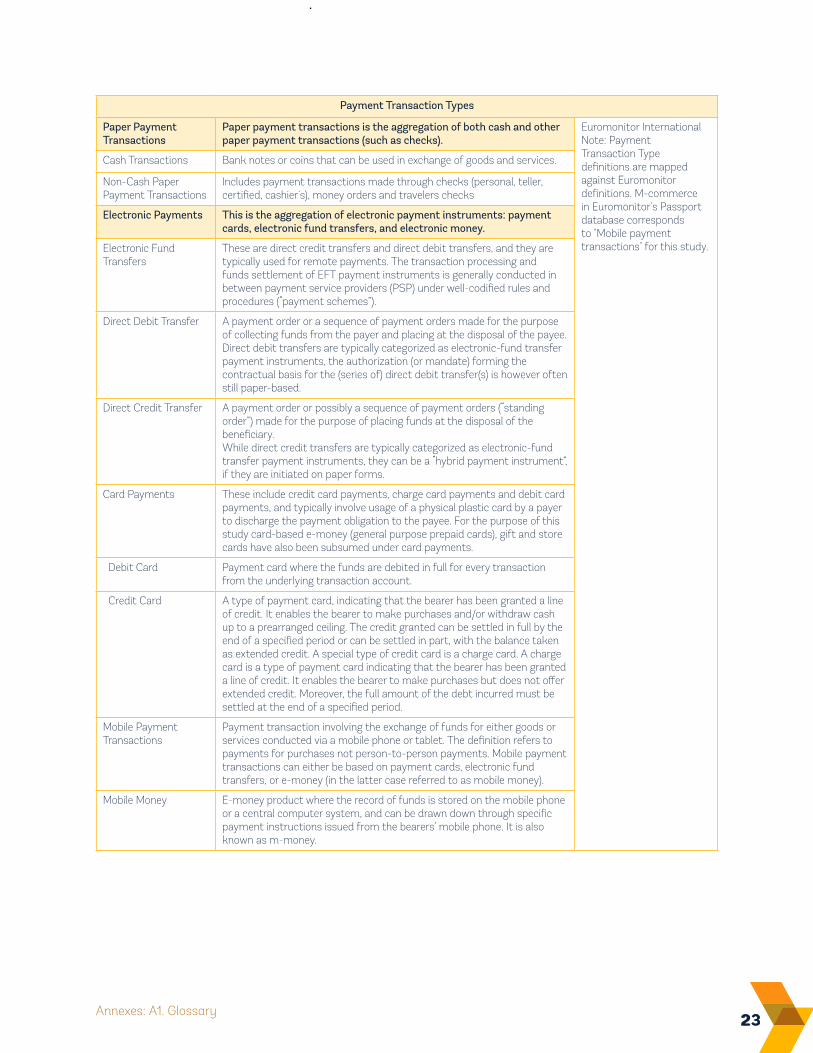

Payment Transaction Types

Paper Payment Transactions

Paper payment transactions is the aggregation of both cash and other paper payment transactions (such as checks).

Euromonitor InternationalNote: Payment Transaction Type definitions are mapped against Euromonitor definitions. M-commerce in Euromonitor's Passport database corresponds to "Mobile payment transactions" for this study.

Cash Transactions Bank notes or coins that can be used in exchange of goods and services.

Non-Cash Paper Payment Transactions

Includes payment transactions made through checks (personal, teller, certified, cashier's), money orders and travelers checks

Electronic Payments This is the aggregation of electronic payment instruments: payment cards, electronic fund transfers, and electronic money.

Electronic Fund Transfers

These are direct credit transfers and direct debit transfers, and they are typically used for remote payments. The transaction processing and funds settlement of EFT payment instruments is generally conducted in between payment service providers (PSP) under well-codified rules and procedures (“payment schemes”).

Direct Debit Transfer A payment order or a sequence of payment orders made for the purpose of collecting funds from the payer and placing at the disposal of the payee. Direct debit transfers are typically categorized as electronic-fund transfer payment instruments, the authorization (or mandate) forming the contractual basis for the (series of) direct debit transfer(s) is however often still paper-based.

Direct Credit Transfer A payment order or possibly a sequence of payment orders (“standing order”) made for the purpose of placing funds at the disposal of the beneficiary. While direct credit transfers are typically categorized as electronic-fund transfer payment instruments, they can be a “hybrid payment instrument”, if they are initiated on paper forms.

Card Payments These include credit card payments, charge card payments and debit card payments, and typically involve usage of a physical plastic card by a payer to discharge the payment obligation to the payee. For the purpose of this study card-based e-money (general purpose prepaid cards), gift and store cards have also been subsumed under card payments.

Debit Card Payment card where the funds are debited in full for every transaction from the underlying transaction account.

Credit Card A type of payment card, indicating that the bearer has been granted a line of credit. It enables the bearer to make purchases and/or withdraw cash up to a prearranged ceiling. The credit granted can be settled in full by the end of a specified period or can be settled in part, with the balance taken as extended credit. A special type of credit card is a charge card. A charge card is a type of payment card indicating that the bearer has been granted a line of credit. It enables the bearer to make purchases but does not offer extended credit. Moreover, the full amount of the debt incurred must be settled at the end of a specified period.

Mobile Payment Transactions

Payment transaction involving the exchange of funds for either goods or services conducted via a mobile phone or tablet. The definition refers to payments for purchases not person-to-person payments. Mobile payment transactions can either be based on payment cards, electronic fund transfers, or e-money (in the latter case referred to as mobile money).

Mobile Money E-money product where the record of funds is stored on the mobile phone or a central computer system, and can be drawn down through specific payment instructions issued from the bearers’ mobile phone. It is also known as m-money.

24 Cash vs. Electronic Payments In Small Retailing | Estimating the Global Size

Euromonitor Passport DatabasesA2.

The Passport database data on consumer finance, retail, industrials, and numerous other categories of packaged consumer goods is used in this research. Key Euromonitor databases used in this project include:

• Passport: Consumer Finance: Euromonitor’s Passport consumer finance database originates from annual on-the-ground research in 46 core markets. Indicators in this database include estimates of P2B retail transactions value made electronically and by paper.

• Passport: Retail: Euromonitor’s Passport retail database has data on 80 countries. Estimates for each country are updated annually, ensuring comparability across countries. Indicators in this database include total retail market size, total number of outlets, and market shares of the main players. Data are broken down into

grocery, non-grocery and over 18 subcategories of specialist retailers. This is further segmented into traditional and modern retailers for all 80 markets.

• Passport: Industrial: Euromonitor’s This database is built up using input/output tables for 18 core and secondary markets. Included in this database for each industry is a breakdown by number of firms in each employment category. The database also includes analysis of the buyers and suppliers for up to 177 industries including retail and wholesale providing a picture of the industry’s supply chain.

• Passport: Countries and Consumers: Euromonitor’s Countries and Consumer database includes secondary data taken from hundreds of sources globally. This data is standardized to allow comparisons to be made.

25Annexes: A3. List Of Economies Used In The Analyses

List Of Economies Used in The AnalysesA3.

Afghanistan Ecuador Lesotho RomaniaAlbania Egypt, arab Rep. Liberia Russian FederationAlgeria El Salvador Libya RwandaAngola Equatorial Guinea Liechtenstein Saudi ArabiaArgentina Eritrea Lithuania SenegalArmenia Estonia Luxembourg SerbiaAustralia Ethiopia Macedonia, FYR Sierra LeoneAustria Fiji Madagascar SingaporeAzerbaijan Finland Malawi Slovak RepublicBahamas, The France Malaysia SloveniaBahrain Gabon Mali SomaliaBangladesh Gambia, The Malta South AfricaBelarus Georgia Mauritania South KoreaBelgium Germany Mauritius South SudanBenin Ghana Mexico SpainBermuda Greece Moldova Sri LankaBhutan Guatemala Monaco SudanBolivia Guinea Mongolia SwazilandBosnia and Herzegovina Haiti Montenegro SwedenBotswana Honduras Morocco SwitzerlandBrazil Hong Kong SAR, China Mozambique Syrian Arab RepublicBrunei Hungary Myanmar Taiwan, ChinaBulgaria Iceland Namibia TajikistanBurkina Faso India Nepal TanzaniaBurundi Indonesia Netherlands ThailandCambodia Iran, Islamic Rep. New Zealand TogoCameroon Iraq Nicaragua Trinidad and TobagoCanada Ireland Niger TunisiaCentral African Republic Israel Nigeria TurkeyChad Italy North Korea TurkmenistanChile Jamaica Norway UgandaChina Japan Oman UkraineColombia Jordan Pakistan United Arab EmiratesCongo, Dem. Rep. Kazakhstan Panama United KingdomCongo, Rep. Kenya Paraguay United StatesCosta Rica Korea, Dem. People’s Rep. Peru UruguayCöte d'Ivoire Korea, Rep. Philippines UzbekistanCroatia Kosovo Poland Venezuela, RBCuba Kuwait Portugal VietnamCyprus Kyrgyzstan Puerto Rico Yemen, Rep.Czech Republic Lao, PDR Qatar ZambiaDenmark Latvia Reunion ZimbabweDominican Republic Lebanon

26 Cash vs. Electronic Payments In Small Retailing | Estimating the Global Size

Methodology – Detailed DescriptionsA4.

A4.1 CLUSTER ANALYSiS: DETAiLS ON METHODOLOGYThis annex summarizes how the cluster analysis was performed. The variables and the rationale for using them are described, as well as the clustering methodology and output is presented.

vARiABLES iNCLUDED iN THE CLUSTER ANALYSiS

Five variables are included in the analysis. The variables are selected to account for variation across countries in terms of the retail sector and financial inclusion. The definitions of these variables along with the sources are listed below.15

1. Retail sales per capita: (USD , nominal, converted using 2014 exchange rates, source: Euromonitor)

• Sales per capita of new and used goods to the general public for personal or household consumption.

• Excludes specialist retailers of motor vehicles, motorcycles, vehicle parts, fuel; and foodservice, rental and hire and wholesale industries (Cash and Carry). Sales value excluding or including VAT/Sales Tax.

• Retailing is the aggregation of store-based and non-store retailing. Retailing excludes the informal retail sector. Informal retailing is retail trade which is not declared to the tax authorities, and encompasses (a) sales generated by unregistered and unlicensed retailers, i.e. retailers operating illegally, and (b) any proportion of sales generated by a registered and licensed retailer which is not declared to the tax authorities. Unregistered and unlicensed retailers operate predominantly (although not exclusively) as street hawkers or operate open market stalls, as these channels are harder for the authorities to monitor than

permanent outlets. Activities in the “black market”, i.e. those refer to trade in illegal, counterfeit or stolen merchandise, are included within our definition of informal retailing. Activities in the “grey market”, i.e. those refer to trade in legal merchandise that is sold through unauthorized channels–for example cigarettes bought legally in another country, legally imported, but sold at lower prices than in authorized channels–will be included as informal retailing if no tax is paid on sale by the retailer. However if the retailer pays tax–for example on cigarettes bought legally in another country but sold at a lower price than standard–the sale is included within formal retailing.

• In relation to click and collect purchases (i.e. where purchases are made over the internet but picked up at store) where the sales data is attributed depends on where the payment is made: If payment is made in store, then the sale is included in store-based sales. If payment is made over the internet, then the sale is included in internet retailing.

• Retail sales per capita provides an indication of the income that the population spends on retail purchases.

2. Share of modern grocery retailers in grocery retailing: (%, based on local currency prices at current prices, source: Euromonitor)

• Modern grocery retailing is the aggregation of those grocery channels that have emerged alongside the growth of chained retail: Hypermarkets, Supermarkets, Discounters, Forecourt Retailers and Convenience Stores. While there can be traditional (i.e. non-chained) supermarkets or forecourt retailers, e.g., due to the store's presence in the channel, these stores are still considered as modern in Euromonitor Passport Databases.

27Annexes: A4. Methodology – Detailed Descriptions

• This variable provides an indication of the retail sector development of a country.

3. Urban population: (% of total population, source: UN)

• Urban population is defined as population of areas defined as urban in each country and reported to the UN. The infrastructure, types of houses and dwellings in agglomerations, density, landscapes, etc., are very different between the countries, and thus it is impossible to have a uniform definition. Urban population by city refers to population of “city proper”, or a "locality with legally fixed boundaries and an administratively recognized urban status that is usually characterized by some form of local government”.

• Higher urbanization, particularly in developing countries, is expected to facilitate ownership of a bank account and use of non-paper payments.

4. Share of paper payments in consumer payment transactions: (%, source: Euromonitor)

• Consumer payment transactions is the sum of card payment transactions, cash transactions, other paper payment transactions and electronic transactions (excluding commercial). Paper payment transactions contains both cash and other paper payment transactions such as checks (personal, teller, certified, cashier's), money orders and travelers’ checks. Electronic transactions include electronic fund transfers, and examples of electronic fund transfers include direct debit and direct credit transfers.

• Measures financial system development and consumer cultural preferences over paper vs. electronic payments

5. Adults with a formal account at a financial institution, poorest 40%: (%, source: World Bank Global Findex)

• Denotes the percentage of respondents in the bottom 40 percent of income earners, aged 15+, with an account (self or together

with someone else) at a bank, credit union, another financial institution (e.g., cooperative, microfinance institution), or the post office (if applicable) including respondents who reported having a debit card.

CLUSTER METHODOLOGY

K-Means Clustering:The objective of this method is to seek items in the same cluster that would be as similar as possible and different clusters would be as dissimilar as possible. This method aims to partition the countries into k clusters in which each observation belongs to the cluster with the nearest mean (i.e. cluster center or mean), serving as a prototype of the cluster. The methodology used employs an iterative algorithm to classify an observation into a cluster by minimizing the squared distance of each observation from the cluster centers.

Using the variables above for 168 developed and developing economies, the countries are grouped into six clusters. Small island countries were not included in the analysis due to low spend and low population. Table A4.1 lists the countries in each cluster.

Country Selection:

The next step is to choose one country per cluster to conduct the primary research in. The selection criteria used for this purpose are:

1. Whether the country is researched across Euromonitor’s Retail and Consumer Finance Passport databases as opposed to modeled, i.e. forecasted. This ensures a solid starting point in terms of data availability.

2. Geographical location in order to have a representative selection across cluster groupings

3. Whether the country had good data availability across the variables to be used for the purposes of cluster analysis and also for the modeling stage to follow.

4. Potential for success in collecting data during primary research to be used during the modeling phase.

5. Countries too big in geographic size and overall population to complete the research in a timely manner within the project timeline are excluded (e.g. Brazil, China, India, Nigeria).

28 Cash Vs. Electronic Payments In Small Retailing | Estimating The Global Size

6. Countries where the majority of the population is foreign nationals (e.g. UAE) were excluded.

7. Euromonitor having good research capabilities within the countries selected in order for the primary research to be completed on time with high quality data (see Appendix A2 for the existing Euromionitor databases).

Please note that based on the k-means clustering technique used and described above, the ideal countries to be selected are the cluster centers, e.g. six countries, one in each cluster that constitute the means. In practice, no actual observation in the

center will be exactly at the center of the clusters. Therefore, selected countries are those that are the closest to the cluster centers.

A4.2 PRiMARY RESEARCH METHODOLOGYPrimary research was conducted in seven countries—Colombia, France, Kenya, Lithuania, Morocco, Pakistan, and Turkey—in August 2015 through in-person trade interviews and pulse surveys to complement the existing research done and data collected by Euromonitor International for the Euromonitor Passport Databases.

Cluster 1 Cluster 2 Cluster 3 Cluster 4Australia Ireland Austria Japan Argentina Montenegro Azerbaijan Libya

Belgium Liechtenstein Bahamas, The Latvia Brazil Oman Belarus Macedonia, FYR

Bermuda Luxembourg Bahrain Lithuania Bulgaria Poland China Mexico

Canada Monaco Brunei Portugal Chile Russian Federation Colombia Reunion

Denmark Netherlands Croatia Puerto Rico Costa Rica Saudi Arabia Ecuador South Africa

Finland New Zealand Cyprus Qatar Hungary Serbia Equatorial Guinea Thailand

France Norway Czech Republic Singapore Kuwait Slovak Republic Gabon Turkmenistan

Germany Sweden Estonia Slovenia Malaysia Trinidad and Tobago Kazakhstan Uruguay

Hong Kong SAR, China Switzerland Greece Korea, Rep. Malta Turkey

Iceland United Kingdom Israel Spain Venezuela

United States Italy Taiwan

United Arab Emirates

Cluster 5 Cluster 6

Albania Fiji Morocco Afghanistan Congo, Dem. Rep.

Kyrgyz Republic Myanmar South Sudan

Algeria Georgia Namibia Bangladesh Cöte d'Ivoire Laos Nepal Sri Lanka

Angola Guatemala Panama Benin Eritrea Lesotho Nicaragua Sudan

Armenia Indonesia Paraguay Bhutan Ethiopia Liberia Niger Swaziland

Bolivia Iran, Islamic Rep. Peru Burkina Faso Gambia Madagascar Nigeria Syrian Arab

RepublicBosnia and Herzegovina Iraq Philippines Burundi Ghana Malawi Korea, Dem.

People’s rep. Tajikistan

Botswana Jamaica Romania Cambodia Guinea Mali Pakistan Tanzania