Embed Size (px)

Citation preview

Junior Tukkies 2017 ACCOUNTING - COMPANIES

Page 1 of 25

CASH FLOW STATEMENT

ANALYSIS AND

INTERPRETATION

QUESTION PAPER

ANSWER BOOK

Junior Tukkies 2017 ACCOUNTING - COMPANIES

Page 2 of 25

Junior Tukkies 2017 ACCOUNTING - COMPANIES

Page 3 of 25

Junior Tukkies 2017 ACCOUNTING - COMPANIES

Page 4 of 25

Junior Tukkies 2017 ACCOUNTING - COMPANIES

Page 5 of 25

Junior Tukkies 2017 ACCOUNTING - COMPANIES

Page 6 of 25

Junior Tukkies 2017 ACCOUNTING - COMPANIES

Page 7 of 25

Junior Tukkies 2017 ACCOUNTING - COMPANIES

Page 8 of 25

Junior Tukkies 2017 ACCOUNTING - COMPANIES

Page 9 of 25

Junior Tukkies 2017 ACCOUNTING - COMPANIES

Page 10 of 25

Junior Tukkies 2017 ACCOUNTING - COMPANIES

Page 11 of 25

Junior Tukkies 2017 ACCOUNTING - COMPANIES

Page 12 of 25

Junior Tukkies 2017 ACCOUNTING - COMPANIES

Page 13 of 25

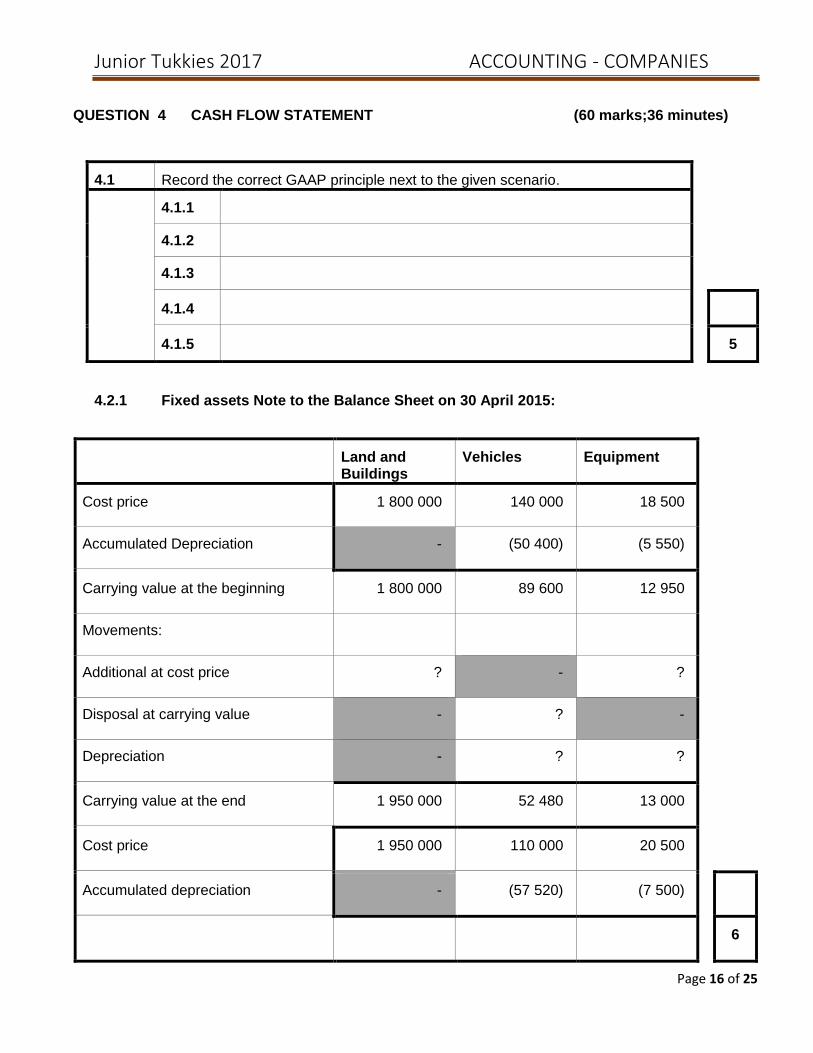

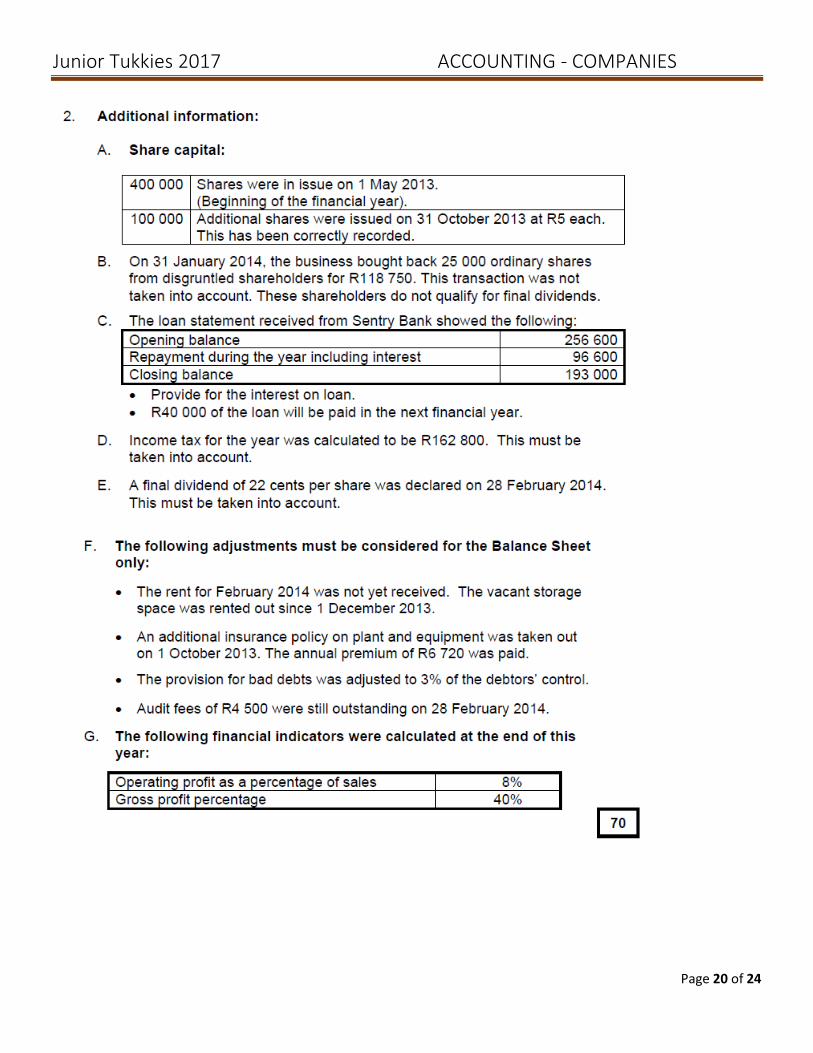

QUESTION 4 CASH FLOW STATEMENT (60 marks;36 minutes)

Ema Traders Limited trades with stationery. Their mark-up is 75% on cost price. Ema Traders Limited year-end is on 30 APRIL 2015. The company is authorised to issue an unlimited number ordinary shares.

REQUIRED :

4.1 Record the correct GAAP principle next to the given scenario (5)

4.1.1 Financial statements are prepared as if the business will be trading in the foreseeable future.

(1)

4.1.2 Consumable stores, stationery and postage can be posted to the Sundry expenses account.

(1)

4.1.3 If a business purchased Land and Buildings 5 years ago at R1 950 000 and it was currently re-valued at R2 380 000, the Land and Buildings will still be recorded as R1 950 000 in the books of the business.

(1)

4.1.4 The owner inherited R50 000 from his grandfather and he did not record the inheritance in the books of the business.

(1)

4.1.5 At the end of the financial year the telephone account was still outstanding. This transaction will be recorded in the telephone account in the General Ledger before the account is closed off to the Profit and Loss account.

(1)

4.2 Use the given information to complete the following:

4.2.1 Record the missing figures/ amounts in NOTE TO THE FIXED ASSETS. (6)

4.2.2 Cash flow statement for the year ended 30 April 2015 (18)

4.2.3 Cash generated from operations (18)

4.2.4 Cash and cash equivalents (4)

4.2.5 Dividends paid (5)

4.2.6 Taxation paid (4)

Junior Tukkies 2017 ACCOUNTING - COMPANIES

Page 14 of 25

INFORMATION

1. Extracts from the Income Statement for the year ended 30 April 2015

30 April 2015

Depreciation: Vehicles 15 520

Depreciation: Equipment ?

Interest expense (13% p.a.) 58 500

Net profit before taxation 410 000

Income tax (30%) ?

Net Profit after tax 287 000

2. Extracts from the Balance Sheet and notes to the Financial Statements.

30 April 2015 30 April 2014

Ordinary share Capital (see note ) 1 825 000 1 500 000

Retained income 19 500 126 500

Land and Buildings 1 950 000 1 800 000

Vehicles at cost price 110 000 140 000

Equipment at cost price 20 500 18 500

Accumulated depreciation on vehicles 57 520 50 400

Accumulated depreciation on equipment 7 500 5 550

Trading stock 146 200 129 280

Debtors Control 65 500 56 800

Deposit: Water and electricity 1 550 1 750

Fixed deposit LKL Bank 200 000 60 000

SARS (Income tax) 69 500(Dr) 31 480(Dr)

Bank 4 510(Dr) 17 100(Cr)

Petty cash 600 600

Cash float 1 000 800

Shareholders for dividends 212 500 150 000

Loan: PASS Bank (9% p.a.) 425 000 350 000

Creditors control 34 840 39 660

Junior Tukkies 2017 ACCOUNTING - COMPANIES

Page 15 of 25

Note 7: Ordinary Share Capital l (30 April 2015) R

750 000 Issued at issue price of R2 per share 1 500 000

150 000 Issued during the year at an issue price of R3 per share 450 000

50 000 Repurchased at an average price of R2,50 per share. (125 000)

850 000 In issue at the end of the year 30 April 2015 1 825 000

ADDITIONAL INFORMATION:

1. No(zero) equipment was sold during the year.

2. Vehicles was sold at carrying value, R21 600 cash.

3. Authorised share capital is 1 200 000 ordinary shares

4. 750 000 ordinary shares were issued by 30 April 2014 at R2 per share.

5. Issued an additional 150 000 ordinary shares during the year at R3 per share.

6. 50 000 ordinary shares were repurchased at market value of R3,50. The average price

of shares was R2,50 per share at the time of the buy back.

7. On 28 February 2015 an interim dividend of R144 000 was declared and paid.

8. A final dividend of 25 cents per share was declared on 30 April 2015.

60

Junior Tukkies 2017 ACCOUNTING - COMPANIES

Page 16 of 25

QUESTION 4 CASH FLOW STATEMENT (60 marks;36 minutes)

4.1 Record the correct GAAP principle next to the given scenario.

4.1.1

4.1.2

4.1.3

4.1.4

4.1.5 5

4.2.1 Fixed assets Note to the Balance Sheet on 30 April 2015:

Land and Buildings

Vehicles Equipment

Cost price 1 800 000 140 000 18 500

Accumulated Depreciation - (50 400) (5 550)

Carrying value at the beginning 1 800 000 89 600 12 950

Movements:

Additional at cost price ? - ?

Disposal at carrying value - ? -

Depreciation - ? ?

Carrying value at the end 1 950 000 52 480 13 000

Cost price 1 950 000 110 000 20 500

Accumulated depreciation - (57 520) (7 500)

6

Junior Tukkies 2017 ACCOUNTING - COMPANIES

Page 17 of 25

4.2.2 CASH FLOW STATEMENT FOR THE YEAR ENDED 30 APRIL 2015

Note R

CASH FLOW FROM OPERATING ACTIVITIES

Cash generated from operations 1

Interest paid (58 500)

Dividends paid 3

Taxation paid 4

CASH FROM INVESTING ACTIVITIES

Purchases of fixed assets

Proceeds from sale of fixed assets

Investments Increase

CASH FROME FINANCING ACTIVITIES

Proceeds from shares issued

Repurchases of shares

Increase of loan

Net change in cash and cash equivalents 2

Cash and cash equivalents Cash at the beginning of

year 2

Cash and cash equivalents at end of year 2

18

Junior Tukkies 2017 ACCOUNTING - COMPANIES

Page 18 of 25

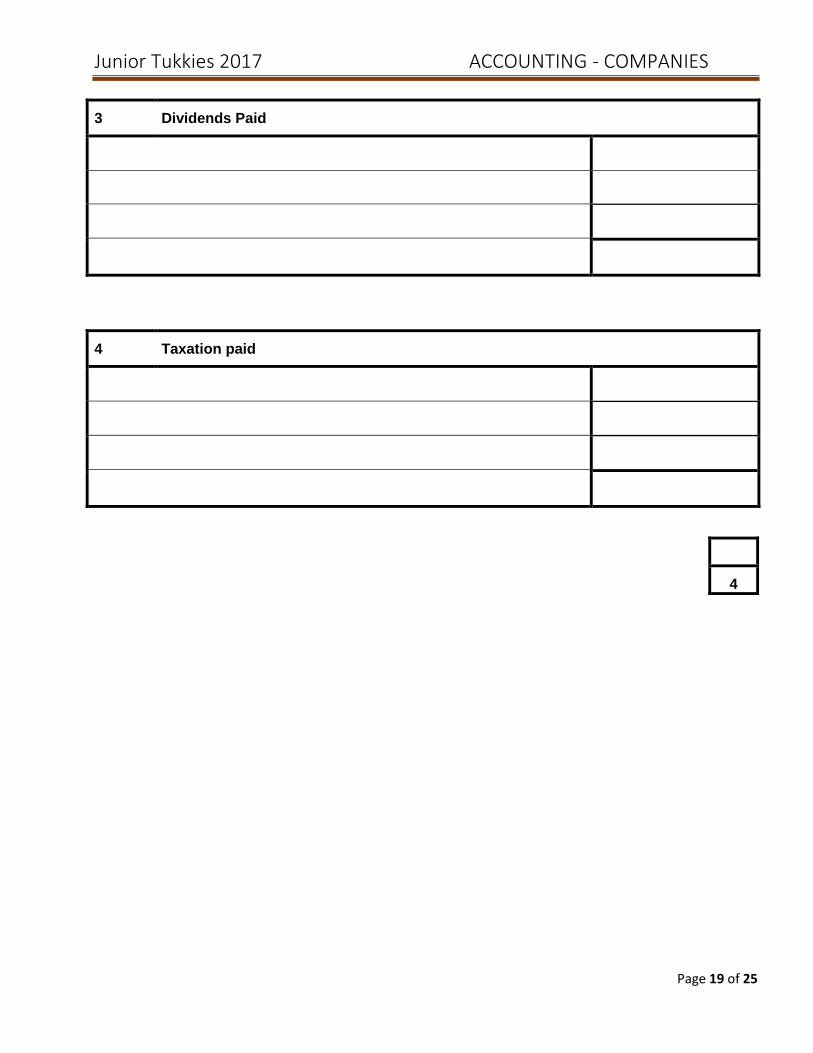

Notes to the Cash flow Statement

1 Cash generated from operations

Net profit before tax

Depreciation

Interest expense

Cash generated from operations before changes in net working capital

Changes in net working capital

18

2 Cash and cash equivalents

Net change 2014 2015

4

Junior Tukkies 2017 ACCOUNTING - COMPANIES

Page 19 of 25

3 Dividends Paid

4 Taxation paid

4

Junior Tukkies 2017 ACCOUNTING - COMPANIES

Page 20 of 25

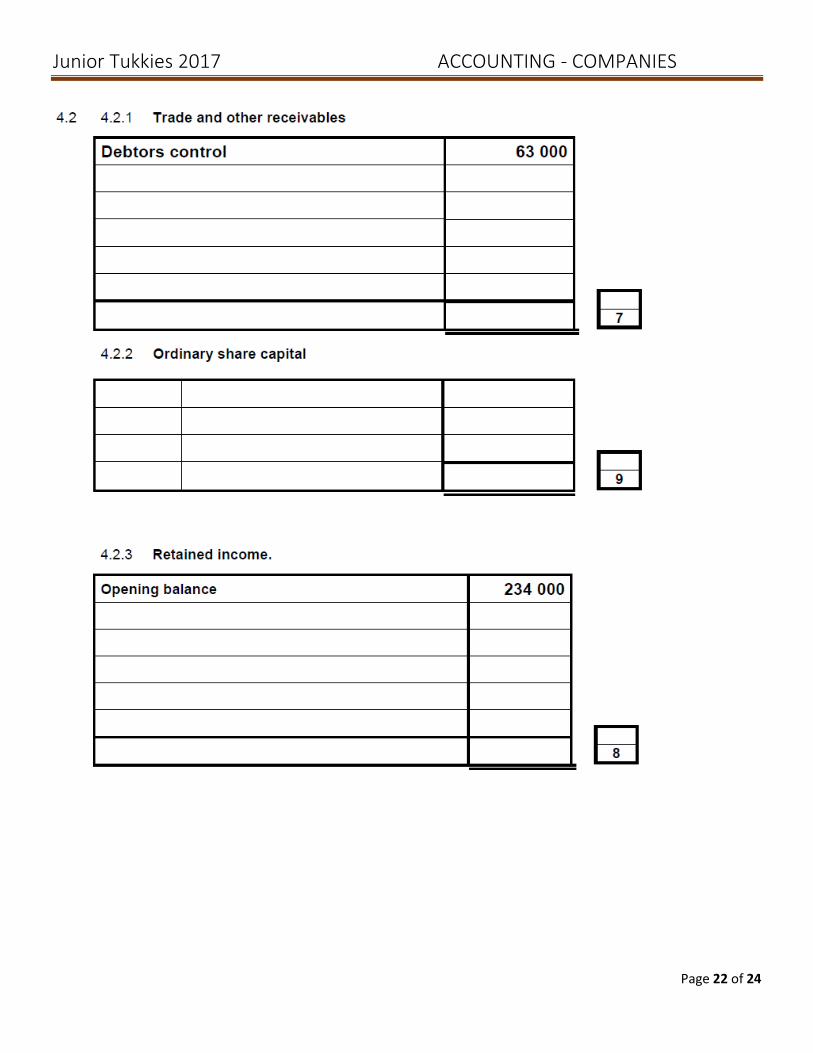

QUESTION 2 ANALYSIS AND INTERPRETATION (45 marks; 27 minutes)

The following information appeared in the books of Nature Limited. They buy and sell chocolate bars at a mark–up of 50% at cost price. The company was registered with an authorised share capital of 500 000 ordinary shares. During the financial year additional 25 000 ordinary shares were issued at a constant issue price of R2 per share. INFORMATION

1 An extract from the Balance Sheets

31 MAY 2015 31 MAY 2014

Land and Buildings 1 600 000 1 550 000

Equipment at cost price 165 000 145 000

Accumulated depreciation on equipment 89 000 58 000

Trading stock 102 500 92 000

Trade and other receivables ( Debtors) 19 500 17 550

Fixed Deposit: JJ Bank (12%p.a.) 100 000 150 000

Bank 1 650(cr) 450 (cr)

Cash float 1 000 1 000

Ordinary Share Capital 800 000 750 000

Retained Income 16 500 23 450

Current Liabilities 25 000 16 800

Loan: KL Bank (7%p.a) 230 000 125 000

2. An extract from the Income Statement for the year ended 31 May 2015

Sales (15% op credit) 668 000

Cost of Sales 460 000

Operating expenses 200 400

Net profit before taxation 265 400

Income tax 79 620

Net profit for the year/ Net profit after taxation 185 780

Junior Tukkies 2017 ACCOUNTING - COMPANIES

Page 21 of 25

3 An extract of Financial indicators

31 MAY 2015 31 MAY 2014

Percentage on operating expenses on sales ? 21%

Mark-up achieved ? 49%

Acid test ratio 0,82:1 1,12:1

Stock turnover rate 5 times 7 times

Debtors average collection period ? 54 days

Creditors average payment period 33 days 65 days

31 MAY 2015 31 MAY 2014

Debt equity ratio 0,28:1 0,16:1

Percentage return on shareholders’ equity ? 20%

Net Asset Value per share ? R4

Percentage return on capital employed 46% 24%

Earnings per share 46 cents 35 cents

Dividends per share 26 cents 12 cents

REQUIRED:

2.1 Calculate the following indicators for 2015.

2.1.1 Percentage operating expenses on sales. (4)

2.1.2 Debtors average collection period. (5)

2.1.3 Percentage return on average shareholders’ equity. (7)

Junior Tukkies 2017 ACCOUNTING - COMPANIES

Page 22 of 25

2.2 Use the above information to comment and to answer the questions.

2.2.1 Comment on the liquidity of the business by indicating THREE indicators. Quote the names of the THREE financial indicators, discuss the trends and the implications thereof.

(9)

2.2.2 The business is considering to negotiate an additional loan of

R300 000. Do you think it is a good idea? Give TWO reasons for your answer by quoting TWO relevant indicators and their trends.

(7)

2.2.3 The business tries to maintain a mark-up of 50% on cost price.

Calculate the relevant indicator.

Did the business achieve the mark –up of 50% on cost price?

Give TWO possible reasons if the mark–up was not achieved

(6)

2.2.4 If you were a shareholder of the company, would you be satisfied with the return on shareholders’ equity, earnings per share and dividends per share over the past two years? Discuss the trend and the implications thereof.

(7)

QUESTION 2 ANALYSIS AND INTERPRETATION (45 marks; 27 minutes)

2.1 Calculate the following indicators for 2015

2.1.1 Percentage operating expenses on sales

4

Junior Tukkies 2017 ACCOUNTING - COMPANIES

Page 23 of 25

2.1.2 Debtors average collection period

5

2.1.3 Percentage return on shareholders’ equity

7

2.2 Use the above information to comment and to answer the questions.

2.2.1 Comment on the liquidity of the business by indicating THREE indicators. Quote the names of the THREE financial indicators, discuss the trends and the implications thereof. .

1 .

2.

Junior Tukkies 2017 ACCOUNTING - COMPANIES

Page 24 of 25

3.

9

2.2.2 The business is considering to negotiate an additional loan of R300 000. Do you think it is a good idea? Give TWO reasons for your answer by quoting TWO relevant indicators and their trends..

7

Junior Tukkies 2017 ACCOUNTING - COMPANIES

Page 25 of 25

2.2.3 The business tries to maintain a mark-up of 50% on cost price.

Calculate the relevant indicator.

Did the business achieve the mark –up of 50% on cost price?

Give TWO possible reasons if the mark–up was not achieved

Calculation:

Yes / No

Reasons:

6

2.2.4 If you were a shareholder of the company, would you be satisfied with the return shareholders equity, earnings per share and dividends per share over the past two years? Discuss the trend and the implications thereof.

7

Junior Tukkies 2017 ACCOUNTING - COMPANIES

Page 1

BUYING BACK OF SHARES

QUESTION PAPER

ANSWER BOOK

Junior Tukkies 2017 ACCOUNTING - COMPANIES

Page 2

QUESTION 1: BUY BACK OF SHARES (60 marks; 36 minutes)

1.2. COMPANY ACCOUNTS AND BUY BACK OF SHARES (55)

. Kalel Company Limited has been authorised to issue an unlimited number of ordinary

shares to prospective shareholders. On 1 March 2013 the company issued 2 000 000

ordinary shares at an issue price of 300 cents per share (R3). During the same financial

year March 2013 to February 2014, another 2 000 000 ordinary shares were issued at an

issue price of 600 cents per share.

REQUIRED

1.2.1 Complete Note 7 of the Financial Statements: Ordinary Share Capital. (11)

1.2.2 Complete Note 8 of the Financial Statements: Retained Income (14)

1.2.3 Complete SARS (INCOME TAX) LEDGER ACCOUNT and balance the account at the

end of the financial year.

(10)

1.2.4 Complete DIVIDENDS ON ORDINARY SHARES LEDGER ACCOUNT and close off

the account at the end of the financial year.

(6)

1.2.5 Show the calculation of the average price of the total issued shares on 1 October 2014. (3)

1.2.6 What was the total amount paid to the estate of the deceased shareholder? Show

calculations.

(5)

1.2.7 Show the calculation of the final dividend per share on 28 February 2015. (4)

1.2.8 Give TWO possible reasons for the company’s decision to buy back the shares from

the deceased estate on 1 October 2014.

(2)

Junior Tukkies 2017 ACCOUNTING - COMPANIES

Page 3

INFORMATION

At the beginning of the new financial year, 1 March 2014, the following balances appeared in

the General Ledger of Kalel Company Limited:

Ordinary share Capital R18 000 000

Retained Income R1 800 000

SARS(income tax) (credit) R 500 000

Shareholders for dividends R640 000

EXTRACTS OF TRANSACTIONS DURING THE FINANCIAL YEAR:

1 March 2014 Kalel Company Limited offered more shares to prospective shareholders

at an issue price of 700 cents per share. All the shares were sold and

R7 000 000 were recorded in the Cash Receipts Journal.

31 March 2014 The amount owing on 1 March 2014 to SARS and to the Shareholders

were settled and recorded.

31 August 2014 The directors paid provisional tax of R420 000 and interim dividends of

8 cents per share. This was NOT APPLICABLE to the shares issued

on 1 March 2014 to shareholders.

1 October 2014 The directors decided to buy back 200 000 ordinary shares from an estate

of a deceased shareholder at a price of R2 more than the average price

and an internet payment was made to the estate of the deceased.

25 February 2015 Close to the end of the financial year the company paid the second

provisional tax payment of R460 000.

28 February 2015 After the completion of the audit, the following was determined:

1. The net profit for the year was R 2 800 000

2. Income tax was calculated at 30 % of net profit

3. A final dividend was declared at 22 cents per share. This is

applicable to all existing shareholders.

60

Junior Tukkies 2017 ACCOUNTING - COMPANIES

Page 4

1.2 COMPANY ACCOUNTS AND BUY BACK OF SHARES (55)

1.2.1 NOTES TO THE BALANCE SHEET

Note 7: Ordinary Share Capital

Issued:

11

1.2.2 NOTES TO THE BALANCE SHEET

Note 8: Retained income

14

Junior Tukkies 2017 ACCOUNTING - COMPANIES

Page 5

1.2.3 GENERAL LEDGER OF KALEL COMPANY LIMITED

Dr. SARS(INCOME TAX) Cr.

10

1.2.4 GENERAL LEDGER OF KALEL COMPANY LIMITED

Dr. DIVIDENDS ON ORDINARY SHARES Cr.

6

Junior Tukkies 2017 ACCOUNTING - COMPANIES

Page 6

ANSWER ALL THE FOLLOWING QUESTIONS

1.2.5 Show the calculation of the average price of the total issued shares on 1

October 2014

3

1.2.6 What was the total amount paid to the estate of the deceased shareholder?

Show calculations

5

1.2.7 Show the calculation of the final dividend per share on 28 February 2015.

4

1.2.8 Give TWO possible reasons for the company’s decision to buy back the shares

from the deceased estate on 1 October 2014.

2

60

Junior Tukkies 2017 ACCOUNTING - COMPANIES

Page 1 of 24

INCOME STATEMENT AND

BALANCE SHEET

QUESTION PAPER

ANSWER BOOK

Junior Tukkies 2017 ACCOUNTING - COMPANIES

Page 2 of 24

ADJUSTMENTS

1. Prepaid expense

Balance sheet – Note 5

Always subtracted from the expense account.

Income statement

2. Accrued expense

Balance sheet – Note 9

Always added to expense account

Income statement

3. Income received in advance/deferred income

Balance sheet – Note 9

Always subtracted from the income account.

Income statement

4. Accrued income

Balance sheet – Note 5

Always added to the income account.

Income statement

5. Received bank statement:

Bank charges (Service fee, cash deposit fee, credit card levy fee etc.)

Always added to bank charges

Income Statement

Interest on credit balance Interest on a favourable bank balance

Note 1 – Balance sheet

Income statement – Interest income

Interest on debit balance Interest on bank overdraft

Note 2

Income statement – Interest expense

R/D cheque from a debtor Note 6 – Bank decrease (Assets decrease)/

Bank overdraft – Added to bank (Liabilities will increase)

Note 5 – Debtors increase with the amount paid by debtor. If discount was allowed, discount will need to be cancelled.

Income statement – Discount allowed cancelled – will need to decrease discount allowed.

R/D cheques to a creditor Nota 6 – Bank will increase (assets increase)

Bank overdraft – Bank will decrease (liabilities decrease)

Note 9 – Creditors increase

If discount was received, will need to cancel. Subtract discount received in Income statement.

Junior Tukkies 2017 ACCOUNTING - COMPANIES

Page 3 of 24

6. Interest capitalised Income

Added to Fixed deposit – Balance sheet

Add to interest income – Note 1 and Income statement.

Expenses

Added to the loan account – Noncurrent liabilities

Add to interest expense – Note 2 and Income statement.

7. Interest not capitalised Income

Add to interest income – Note 1 and Income statement.

Add to Accrued income if still outstanding.

Expenses

Add to interest expense – Note 2 and Income statement.

Add to Accrued expense of still outstanding.

8. Depreciation It does not show at all on the pre-adjustment trial balance – need to calculate.

Depreciation could have been done, but could be a correction.

9 Bad debts Income statement

10 Provision for bad debts Balance sheet

Increase: Provision for bad debts adjustment - Expense

Decrease: Provision for bad debts adjustment - Income

11 Insurance claim Calculate the loss. The cost of the good damaged/stolen must be shown in the cost account.

12. Physical stock take Calculate trading stock deficit – Expense

Calculate trading stock surplus – Income

Consumable store on hand – What is left over is always subtracted from the expense account.

13. Salaries and wages omitted or included.

If omitted – always add.

If added incorrectly – always subtract.

14. Post-dated cheque issued Bank will be debited – add to bank if bank has a favourable balance and subtract from liabilities if bank has an unfavourable balance.

Creditors control will be credited.

Junior Tukkies 2017 ACCOUNTING - COMPANIES

Page 4 of 24

15. Post-dated cheque received Do nothing.

If incorrectly recorded, will need to do a reversal entry.

16. Debtor’s ledger account with a credit balance.

Need to transfer the balance to creditor’s control.

Debit – Debtors control

Credit – Creditors control

17. Creditor’s ledger account with a debit balance.

Need to transfer to the balance to the debtor’s control account.

Debit – Debtors control

Credit – Creditors control

18. Share issued during the year.

19. Shares repurchased during the year.

20. Income tax – calculate the income tax for the year.

Calculate if we owe SARS or does SARS owe us.

We owe SARS – Note 9, Current liability.

SARS owes us – Note 6. Current asset.

21. Dividends declared and paid.

NOTA:

THE TRANSACTIONS REMAIN THE SAME; IT IS THE LEVEL OF DIFFICULTY THAT CHANGES!!!

ADJUSTMENTS: CALCULATIONS

RENT INCOME

INCOME RECEIVED IN ADVANCE / DEFFERED INCOME

1. The total rent received is R26 000. One month was received in advance.

2. The tenant paid his rent in in advance. The rent increased with R2 000 per month from 1 October 2015.

The total rent received was R27 200.

3. The total rent per month is R2 000. The rent increased with 10% on 30 September 2016. The rent was

received in February for March and April.

4. The total rent received was R27 400. The rent increased with 10% from 1 September 2016. The tenant

paid the rent in February for March.

Junior Tukkies 2017 ACCOUNTING - COMPANIES

Page 5 of 24

ACCRUED INCOME

5. The rent for February is still outstanding. The total rent received was R23 000. The rent increased with

10% on 30 August 2016.

6. The rent for February was still outstanding. The total rent received was R52 000. Take note, the rent

decreased with 20% on 30 October 2016.

SALARIES AND WAGES

1. Gross Salaries Posted to the salaries and wages account – an expense to the

business.

minus Deductions Indicated in the fund account – liability to the business.

Examples: SARS (PAYE), Medical Aid, Pension fund, UIF etc.

= Nett salary Indicated in creditors for salaries and wages – Liability to the

business.

plus Contributions Dit Always added to the fund account – any contributions is an

expense to the business. The business can contribute to all

except for SARS(PAYE).

2. Types of adjustments:

The employee’s salary is omitted.

The employee’s salary is omitted. The salary increased with a %.

The employee received an increase – The salary was recorded without the increase.

An employee retired – the bookkeeper added the salary.

Junior Tukkies 2017 ACCOUNTING - COMPANIES

Page 6 of 24

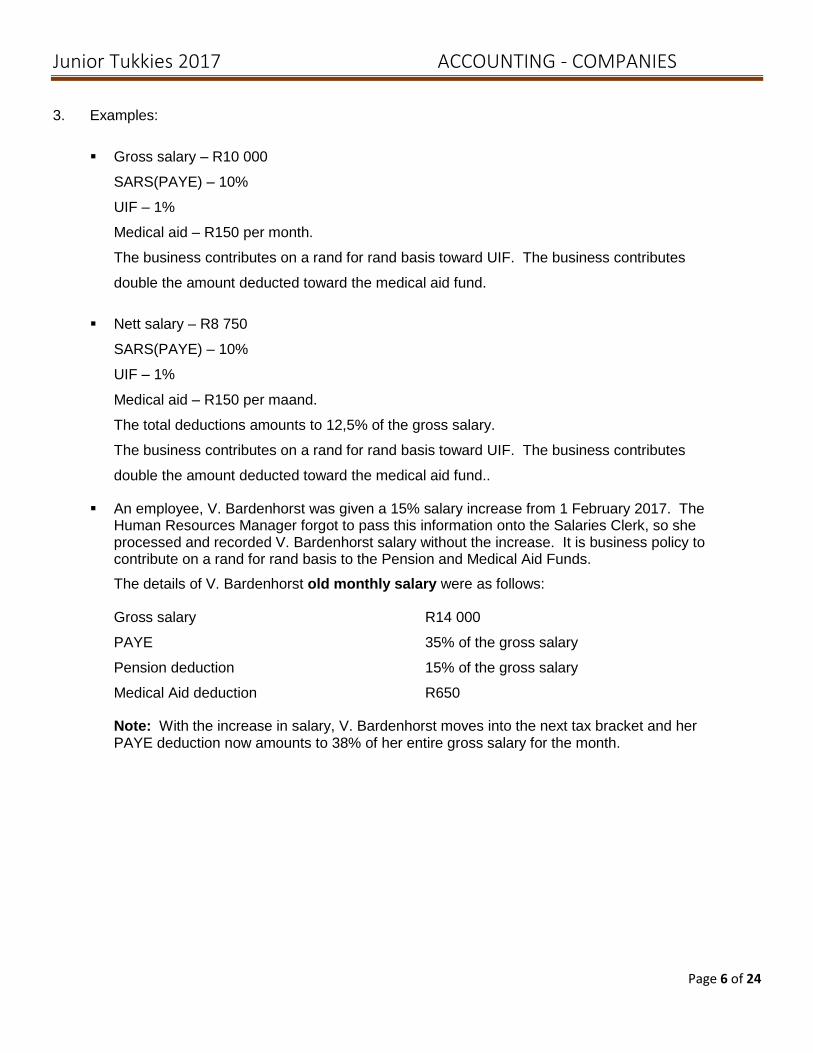

3. Examples:

Gross salary – R10 000

SARS(PAYE) – 10%

UIF – 1%

Medical aid – R150 per month.

The business contributes on a rand for rand basis toward UIF. The business contributes

double the amount deducted toward the medical aid fund.

Nett salary – R8 750

SARS(PAYE) – 10%

UIF – 1%

Medical aid – R150 per maand.

The total deductions amounts to 12,5% of the gross salary.

The business contributes on a rand for rand basis toward UIF. The business contributes

double the amount deducted toward the medical aid fund..

An employee, V. Bardenhorst was given a 15% salary increase from 1 February 2017. The

Human Resources Manager forgot to pass this information onto the Salaries Clerk, so she processed and recorded V. Bardenhorst salary without the increase. It is business policy to contribute on a rand for rand basis to the Pension and Medical Aid Funds.

The details of V. Bardenhorst old monthly salary were as follows:

Gross salary R14 000

PAYE 35% of the gross salary

Pension deduction 15% of the gross salary

Medical Aid deduction R650

Note: With the increase in salary, V. Bardenhorst moves into the next tax bracket and her PAYE deduction now amounts to 38% of her entire gross salary for the month.

Junior Tukkies 2017 ACCOUNTING - COMPANIES

Page 7 of 24

Junior Tukkies 2017 ACCOUNTING - COMPANIES

Page 8 of 24

Junior Tukkies 2017 ACCOUNTING - COMPANIES

Page 9 of 24

Junior Tukkies 2017 ACCOUNTING - COMPANIES

Page 10 of 24

Junior Tukkies 2017 ACCOUNTING - COMPANIES

Page 11 of 24

Junior Tukkies 2017 ACCOUNTING - COMPANIES

Page 12 of 24

Junior Tukkies 2017 ACCOUNTING - COMPANIES

Page 13 of 24

Junior Tukkies 2017 ACCOUNTING - COMPANIES

Page 14 of 24

Junior Tukkies 2017 ACCOUNTING - COMPANIES

Page 15 of 24

Junior Tukkies 2017 ACCOUNTING - COMPANIES

Page 16 of 24

Junior Tukkies 2017 ACCOUNTING - COMPANIES

Page 17 of 24

Junior Tukkies 2017 ACCOUNTING - COMPANIES

Page 18 of 24

Junior Tukkies 2017 ACCOUNTING - COMPANIES

Page 19 of 24

Junior Tukkies 2017 ACCOUNTING - COMPANIES

Page 20 of 24

Junior Tukkies 2017 ACCOUNTING - COMPANIES

Page 21 of 24

Junior Tukkies 2017 ACCOUNTING - COMPANIES

Page 22 of 24

Junior Tukkies 2017 ACCOUNTING - COMPANIES

Page 23 of 24

Junior Tukkies 2017 ACCOUNTING - COMPANIES

Page 24 of 24

Junior Tukkies 2017 ACCOUNTING - INVENTORIES

Page 1 of 15

INVENTORY

QUESTION PAPER

ANSWER BOOK

Junior Tukkies 2017 ACCOUNTING - INVENTORIES

Page 2 of 15

Junior Tukkies 2017 ACCOUNTING - INVENTORIES

Page 3 of 15

Junior Tukkies 2017 ACCOUNTING - INVENTORIES

Page 4 of 15

JUNE EXAM 2016 – EASTERN CAPE

Junior Tukkies 2017 ACCOUNTING - INVENTORIES

Page 5 of 15

Junior Tukkies 2017 ACCOUNTING - INVENTORIES

Page 6 of 15

Junior Tukkies 2017 ACCOUNTING - INVENTORIES

Page 7 of 15

JUNE 2015 – GAUTENG

QUESTION 5: STOCK VALIDATION ( 50 marks; 30 minutes)

5.1 STOCK VALIDATION METHODS (5)

REQUIRED

5.1 Complete the following statements by writing down the correct answer on the

answer book provided.

5.1.1 When stock is valued at the end of year, all the stock on hand has been

recorded at the original cost price to determine the value of the closing

stock. This stock validation method is called ….

(1)

5.1.2 First in First out means that …………………. (2)

5.1.3 When calculating the weighted average method you need to calculate the

average price per …….. to determine the value of the closing stock.

(1)

5.1.4 Which of the following costs DO NOT form part of the calculation of stock

validation? Carriage on purchases; carriage on sales; import duties;

custom duties; freight cost.

(1)

Junior Tukkies 2017 ACCOUNTING - INVENTORIES

Page 8 of 15

5.2 FIFO AND WEIGHTED AVERAGE METHODS (45)

You are provided with information from CAELI AND MPHO Wholesalers who sells

gym weights and gym equipment to all sport clubs in Gauteng. They make use of

the periodic stock system and value their stock as follows:

Gym weights at weighted average method.

Gym Equipment at FIFO.

REQUIRED:

GYM WEIGHTS AT WEIGHTED AVERAGE METHOD

5.2.1 Calculate the weighted average per unit. (5)

5.2.2 Calculate the value of the closing stock of the gym weights according to

the weighted average method on 28 February 2015.

(3)

5.2.3 Caeli and Mpho suspect that gym weights stock disappeared from their

storeroom during the last two months. Calculate the number of weights

missing.

(6)

5.2.4 Calculate the Cost of sales at year end 28 February 2015. (6)

5.2.5 What internal control measures can Caeli and Mpho put in place to avoid

the disappearance of stock in future? Name TWO.

(2)

5.2.6 The business considers changing their stock validation method. They

want to do it legally and follow the correct method of changing from

weighted average to FIFO.

.

5.2.6.1 Why do you think do they want to change from Weighted to

FIFO? Give ONE explanation.

(2)

5.2.6.2 Give ONE advice how to go about doing the changeover legally. (2)

GYM EQUIPMENT AT FIFO

5.2.7 Calculate the value of the closing stock of gym equipment on 28 February

2015.

(7)

5.2.8 Complete the Trading Account using the periodic system. (7)

5.2.9 Use the figures calculated in 5.2.8 to calculate the COST OF SALES of

the Gym equipment.

(5)

Junior Tukkies 2017 ACCOUNTING - INVENTORIES

Page 9 of 15

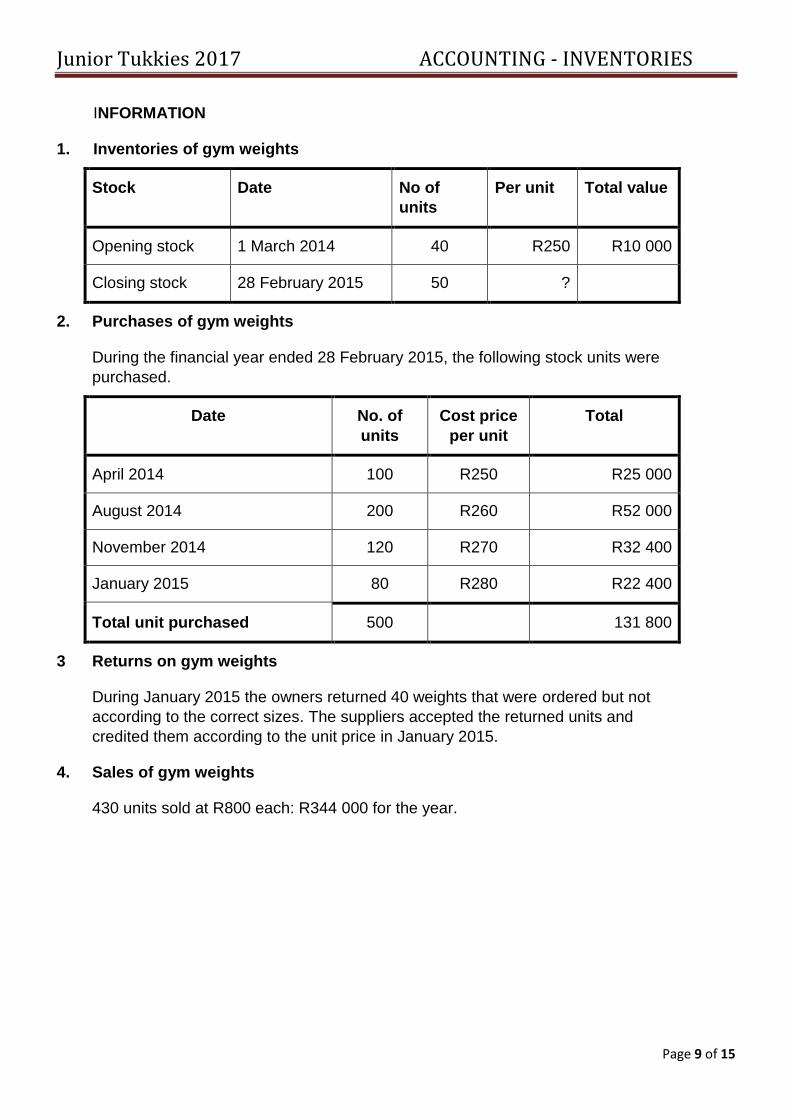

INFORMATION

1. Inventories of gym weights

Stock Date No of

units

Per unit Total value

Opening stock 1 March 2014 40 R250 R10 000

Closing stock 28 February 2015 50 ?

2. Purchases of gym weights

During the financial year ended 28 February 2015, the following stock units were

purchased.

Date No. of

units

Cost price

per unit

Total

April 2014 100 R250 R25 000

August 2014 200 R260 R52 000

November 2014 120 R270 R32 400

January 2015 80 R280 R22 400

Total unit purchased 500 131 800

3 Returns on gym weights

During January 2015 the owners returned 40 weights that were ordered but not

according to the correct sizes. The suppliers accepted the returned units and

credited them according to the unit price in January 2015.

4. Sales of gym weights

430 units sold at R800 each: R344 000 for the year.

Junior Tukkies 2017 ACCOUNTING - INVENTORIES

Page 10 of 15

5 STOCK, PURCHASES AND SALES OF GYM EQUIPMENT

Details Date No.

of

units

Cost

price per

unit

Total

Opening stock 1 March 2014 20 R15 000 R300 000

Total purchases 140 R2 230 000

Purchases during

the year

April 2014 10 R16 000 R160 000

August 2014 30 R17 000 R510 000

November 2014 40 R18 000 R720 000

January 2015 60 R14 000 R840 000

Carriage on

purchases

April 2014 to Jan 2015 R 2 000 R 280 000

Closing stock 28 February 2015 65 ? ?

Sales for the

financial year

1 Mar 2014–28 Feb

2015

95 R40 000 R3 800 000

QUESTION5: STOCK VALIDATIONS / INTERNAL CONTROL (50 marks; 30 minutes)

5.1 CONCEPTS (5)

Match the correct description in the first column with the concept in the second column

5.1.1 1

5.1.2 2

5.1.3 1

5.1.4 1 5

Junior Tukkies 2017 ACCOUNTING - INVENTORIES

Page 11 of 15

5.2 FIFO AND WEIGHTED AVERAGE METHODS (55)

GYM WEIGHTS AT WEIGHTED AVERAGE METHOD GIMNASIUM

5.2.1 Calculate the weighted average per unit.

5

5.2.2 . Calculate the value of the closing stock of the gym weights according to the

weighted average method on 28 February 2015.

3

Junior Tukkies 2017 ACCOUNTING - INVENTORIES

Page 12 of 15

5.2.3 Caeli and Mpho suspect that gym weights disappeared from their

storeroom during the last two months. Show the calculation of the number

of weights missing.

6

5.2.4 Calculate the Cost of sales at year end 28 February 2015

6

Junior Tukkies 2017 ACCOUNTING - INVENTORIES

Page 13 of 15

5.2.5 What internal control measures can Caeli and Mpho put in place to avoid

the disappearance of stock in future? Name TWO.

2

5.2.6 The business considers changing their stock validation method. They

want to do it legally and follow the correct root of changing from weighted

average to FIFO.

5.2.6.1

Why do you think do they want to change from Weighted to

FIFO? Give ONE explanation

2

5.2.6.2 Give ONE advice how to go about doing the changeover legally

2

Junior Tukkies 2017 ACCOUNTING - INVENTORIES

Page 14 of 15

GYM EQUIPMENT AT FIFO

5.2.7 Calculate the value of the closing stock of gym equipment on 28 February

2015.

7

5.2.8 GENERAL LEDGER OF CAELI AND MPHO

Dr TRADING ACCOUNT: GYM EQUIPMWENT (F1) Cr

2014

Mar

1

Opening stock GJ 2015

Feb

28 Closing stock GJ

2015

Feb

28 Purchases(net) GJ Sales(net) GJ

...........................

GJ

Profit and

loss(gross profit)

GJ

7

Junior Tukkies 2017 ACCOUNTING - INVENTORIES

Page 15 of 15

5.2.9 Use the figures calculated in 5.2.8 to calculate the COST OF SALES of the

Gym equipment.

5

Junior Tukkies 2017 ACCOUNTING - RECONCILIATION

Page 1 of 16

RECONCILIATION

QUESTION PAPER

ANSWER BOOK

Junior Tukkies 2017 ACCOUNTING - RECONCILIATION

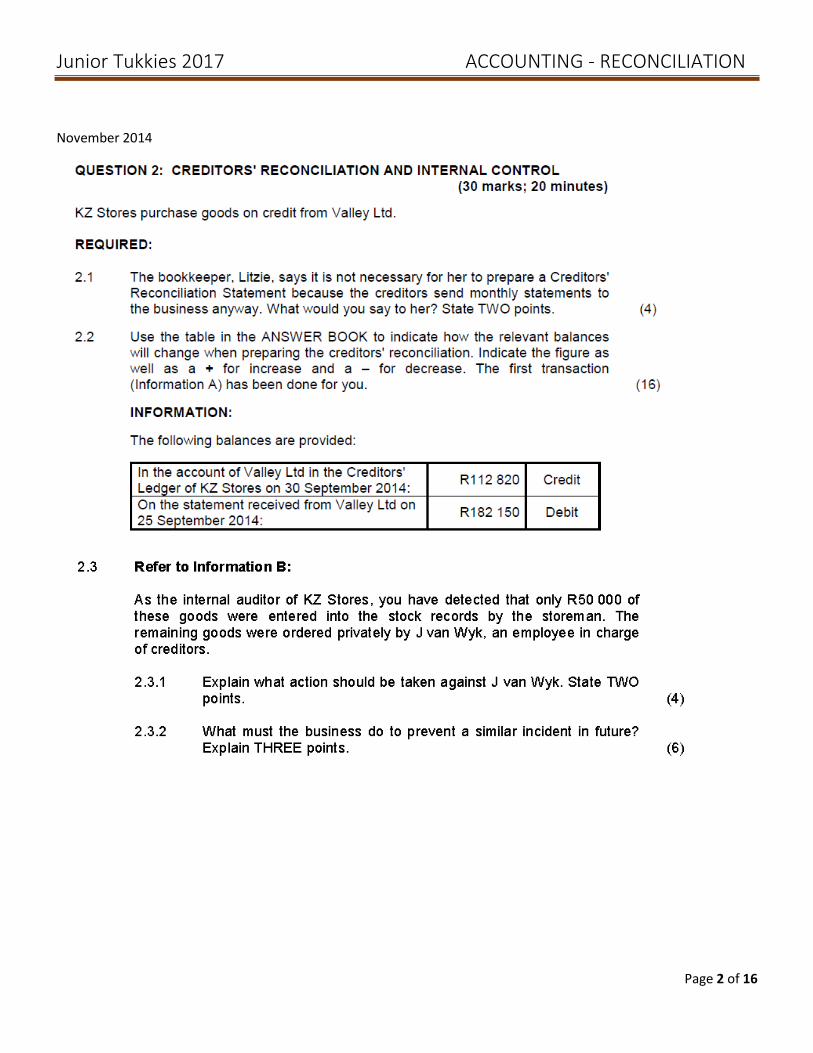

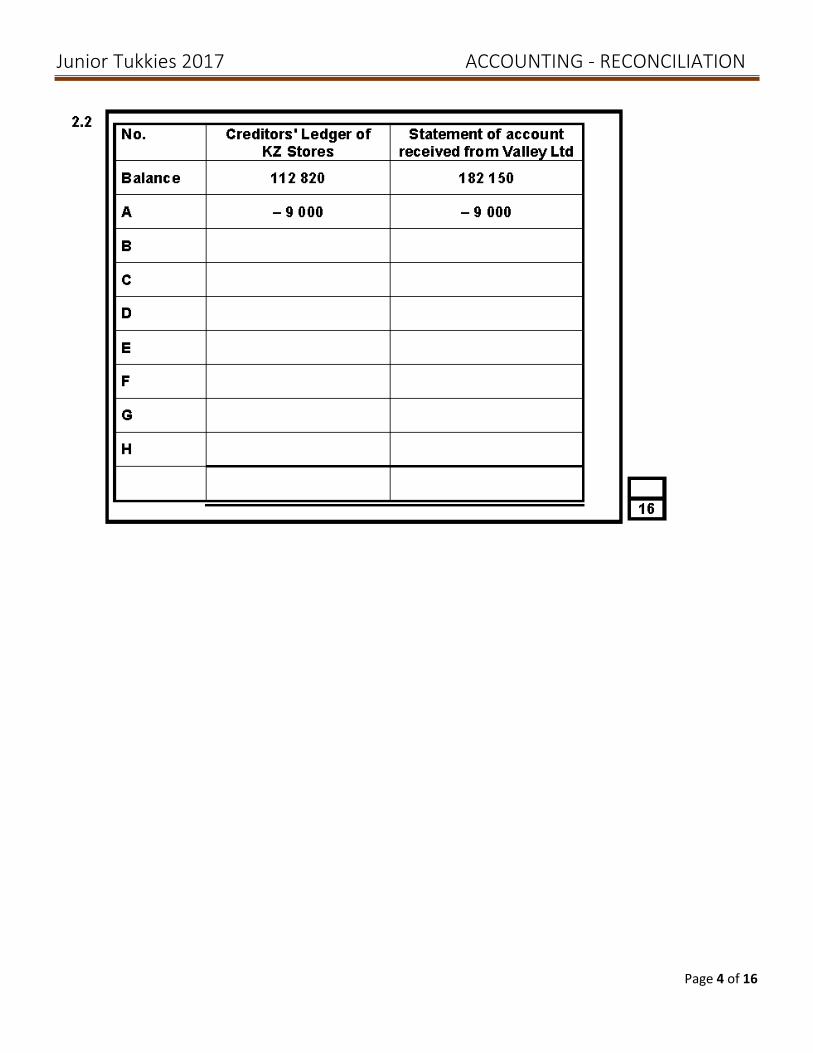

Page 2 of 16

November 2014

Junior Tukkies 2017 ACCOUNTING - RECONCILIATION

Page 3 of 16

Junior Tukkies 2017 ACCOUNTING - RECONCILIATION

Page 4 of 16

Junior Tukkies 2017 ACCOUNTING - RECONCILIATION

Page 5 of 16

February/March 2016

Junior Tukkies 2017 ACCOUNTING - RECONCILIATION

Page 6 of 16

Junior Tukkies 2017 ACCOUNTING - RECONCILIATION

Page 7 of 16

Junior Tukkies 2017 ACCOUNTING - RECONCILIATION

Page 8 of 16

Junior Tukkies 2017 ACCOUNTING - RECONCILIATION

Page 9 of 16

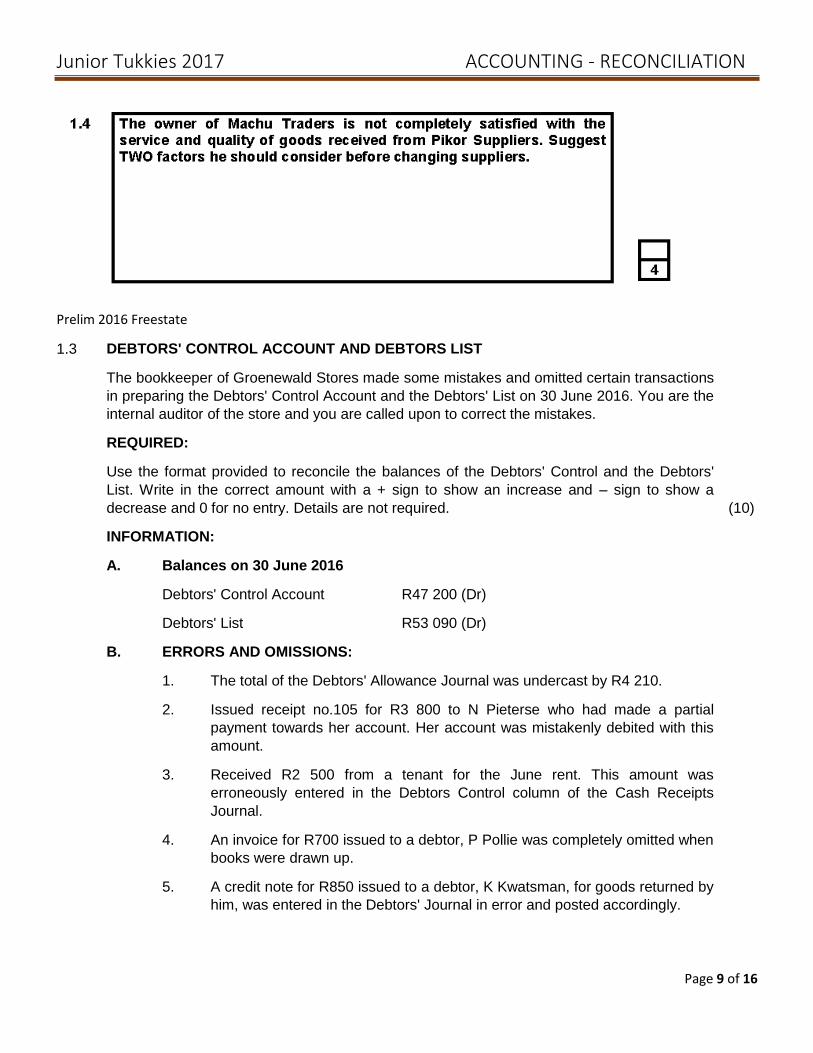

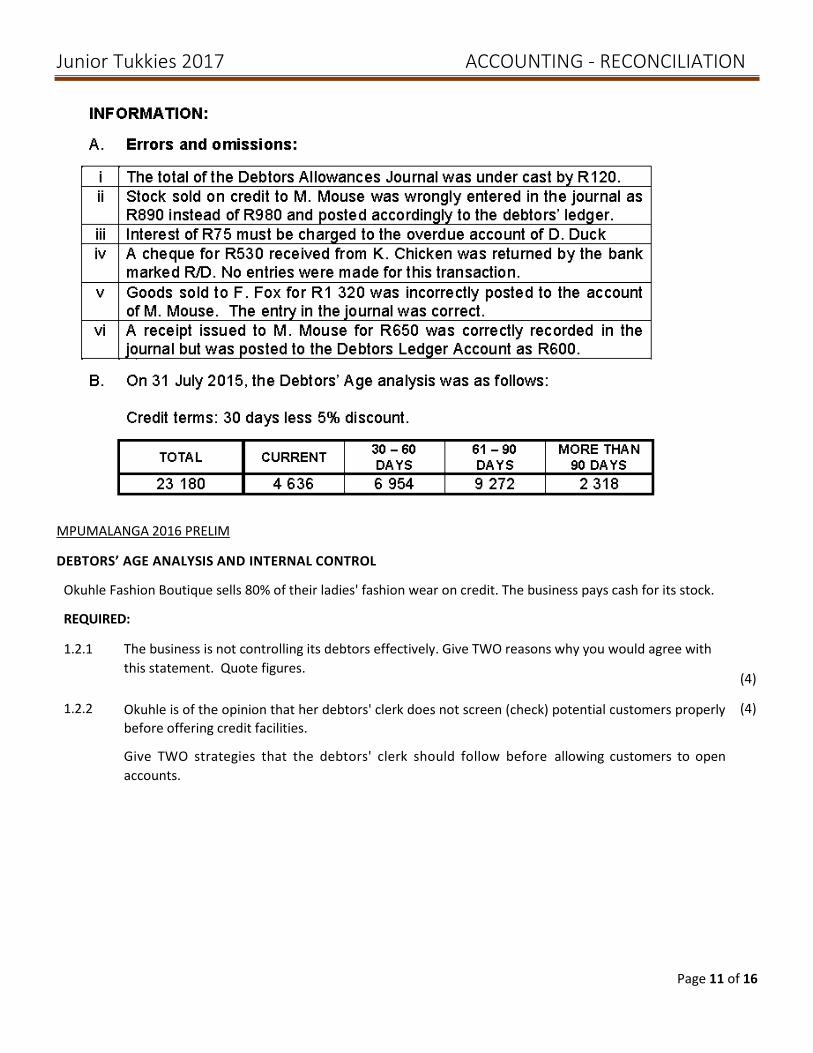

Prelim 2016 Freestate

1.3 DEBTORS' CONTROL ACCOUNT AND DEBTORS LIST

The bookkeeper of Groenewald Stores made some mistakes and omitted certain transactions

in preparing the Debtors' Control Account and the Debtors' List on 30 June 2016. You are the

internal auditor of the store and you are called upon to correct the mistakes.

REQUIRED:

Use the format provided to reconcile the balances of the Debtors' Control and the Debtors'

List. Write in the correct amount with a + sign to show an increase and – sign to show a

decrease and 0 for no entry. Details are not required. (10)

INFORMATION:

A. Balances on 30 June 2016

Debtors' Control Account R47 200 (Dr)

Debtors' List R53 090 (Dr)

B. ERRORS AND OMISSIONS:

1. The total of the Debtors' Allowance Journal was undercast by R4 210.

2. Issued receipt no.105 for R3 800 to N Pieterse who had made a partial

payment towards her account. Her account was mistakenly debited with this

amount.

3. Received R2 500 from a tenant for the June rent. This amount was

erroneously entered in the Debtors Control column of the Cash Receipts

Journal.

4. An invoice for R700 issued to a debtor, P Pollie was completely omitted when

books were drawn up.

5. A credit note for R850 issued to a debtor, K Kwatsman, for goods returned by

him, was entered in the Debtors' Journal in error and posted accordingly.

Junior Tukkies 2017 ACCOUNTING - RECONCILIATION

Page 10 of 16

Debtors Reconciliation

No Details Debtors' Control Debtors' List

A

Pre-adjustment balances/total

47 200

53 090

1

2

3

4

5

Balances

Eastern Cape 2015 Prelim

10

Junior Tukkies 2017 ACCOUNTING - RECONCILIATION

Page 11 of 16

MPUMALANGA 2016 PRELIM

DEBTORS’ AGE ANALYSIS AND INTERNAL CONTROL

Okuhle Fashion Boutique sells 80% of their ladies' fashion wear on credit. The business pays cash for its stock.

REQUIRED:

1.2.1 The business is not controlling its debtors effectively. Give TWO reasons why you would agree with

this statement. Quote figures.

(4)

1.2.2 Okuhle is of the opinion that her debtors' clerk does not screen (check) potential customers properly

before offering credit facilities.

Give TWO strategies that the debtors' clerk should follow before allowing customers to open

accounts.

(4)

Junior Tukkies 2017 ACCOUNTING - RECONCILIATION

Page 12 of 16

INFORMATION

The age analysis of debtors extracted at the end of August 2016 showed the following:

Credit Policy: Debtors are allowed 30 days to settle their accounts.

NAME OF DEBTOR

CREDIT LIMIT

TOTAL OWING

CURRENT MONTH

30 DAYS 60 DAYS 60 DAYS+

L.Ndlovu 8 000 7 700 2 800 3 100 1 800

N.Nel 5 000 6 120 3 820 2 300

S.Shy 4 000 1 380 1 380

B.Ben 10 000 10 600 3 420 4 280 2 900

25 800 8 620 9 380 6 000 1 800

33% 36% 24% 7%

DEBTOR’S AGE ANALYSIS AND INTERNAL CONTROL

1.2.1 The business is not controlling its debtors effectively. Give TWO reasons why you would agree with this statement. Quote figures in your answer.

4

1.2.2 Okuhle is of the opinion that her debtors' clerk does not screen (check) potential customers properly before offering credit facilities. Give TWO strategies that the debtors' clerk should follow before allowing customers to open accounts.

4

Junior Tukkies 2017 ACCOUNTING - RECONCILIATION

Page 13 of 16

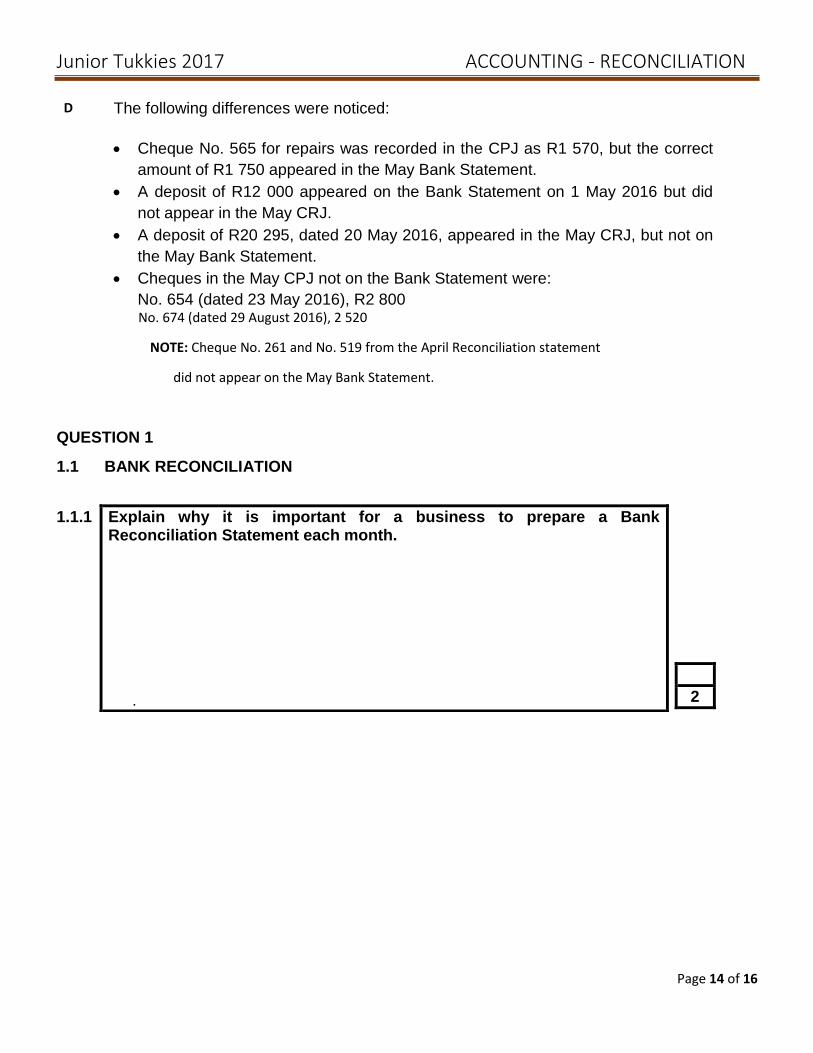

QUESTION 1: RECONCILIATION, AGE ANALYSIS AND INTERNAL CONTROL (40 marks; 20 minutes)

1.1 BANK RECONCILIATION

You are provided with information relating to Golden Jewellers. The financial year ended on 31 May 2016. REQUIRED:

1.1.1 Explain why it is important for a business to prepare a Bank Reconciliation Statement each month.

(2)

1.1.2 Calculate the correct totals for the Cash Receipts Journal and the Cash Payments Journal for May 2016.

(12)

1.1.3 Calculate the Bank balance on 31 May 2016. State whether this is a favourable or unfavourable balance.

(6)

1.1.4 Prepare the Bank Reconciliation Statement on 31 May 2016. (8)

1.1.5 The fixed deposit of R84 000 matures next month. Suggest TWO ways in which the business should use this money. Quote figures to support your answer.

(4)

INFORMATION:

A The following items appeared on the Bank Reconciliation Statement on 30 April 2016:

Favourable bank balance in the ledger of Golden Jewellers R 6 325

Favourable balance on the Bank Statement 12 545

Outstanding deposit (dated 30 April 2016) 12 000

Outstanding cheques:

No. 261 (dated 3 November 2015) 5 000

No. 519 (dated 14 April 2016) 8 920

No. 543 (dated 12 May 2016) 4 300

B On 31 May 2016, the provisional totals in the Cash Journals were as follows:

Cash Receipts Journal : R70 600 Cash Payments Journal : R105 320

C The following items appeared on the Bank Statement but not in the Cash Journals for May 2016:

Direct deposit by debtor Kwela, R2 400

Bank charges, R520

Interest on fixed deposit for May, R700

Interest on overdraft for May, R810

Stop-order in favour of Rama Insurance Co, R660

Dishonoured cheque originally received from a debtor, M Maduna, R6 200.

Junior Tukkies 2017 ACCOUNTING - RECONCILIATION

Page 14 of 16

D The following differences were noticed:

Cheque No. 565 for repairs was recorded in the CPJ as R1 570, but the correct

amount of R1 750 appeared in the May Bank Statement.

A deposit of R12 000 appeared on the Bank Statement on 1 May 2016 but did

not appear in the May CRJ.

A deposit of R20 295, dated 20 May 2016, appeared in the May CRJ, but not on

the May Bank Statement.

Cheques in the May CPJ not on the Bank Statement were:

No. 654 (dated 23 May 2016), R2 800 No. 674 (dated 29 August 2016), 2 520

NOTE: Cheque No. 261 and No. 519 from the April Reconciliation statement

did not appear on the May Bank Statement.

QUESTION 1

1.1 BANK RECONCILIATION

1.1.1 Explain why it is important for a business to prepare a Bank Reconciliation Statement each month.

.

2

Junior Tukkies 2017 ACCOUNTING - RECONCILIATION

Page 15 of 16

1.1.2 Calculate the correct totals for the Cash Receipts Journal and the Cash Payments Journal for May 2016. (Details are not required)

CRJ Bank CPJ Bank

12

Provisional total 70 600 Provisional total 105 320

1.1.3 Calculate the Bank Balance on 31 May 2016.

State whether this is a favourable or unfavourable balance.

6

Junior Tukkies 2017 ACCOUNTING - RECONCILIATION

Page 16 of 16

1.1.4 BANK RECONCILIATION STATEMENT ON 31 MAY 2016

8

Debit Credit

1.1.5 The fixed deposit of R84 000 matures next month. Suggest TWO ways in which the business can use this money. Quote figures to support your answer.

4

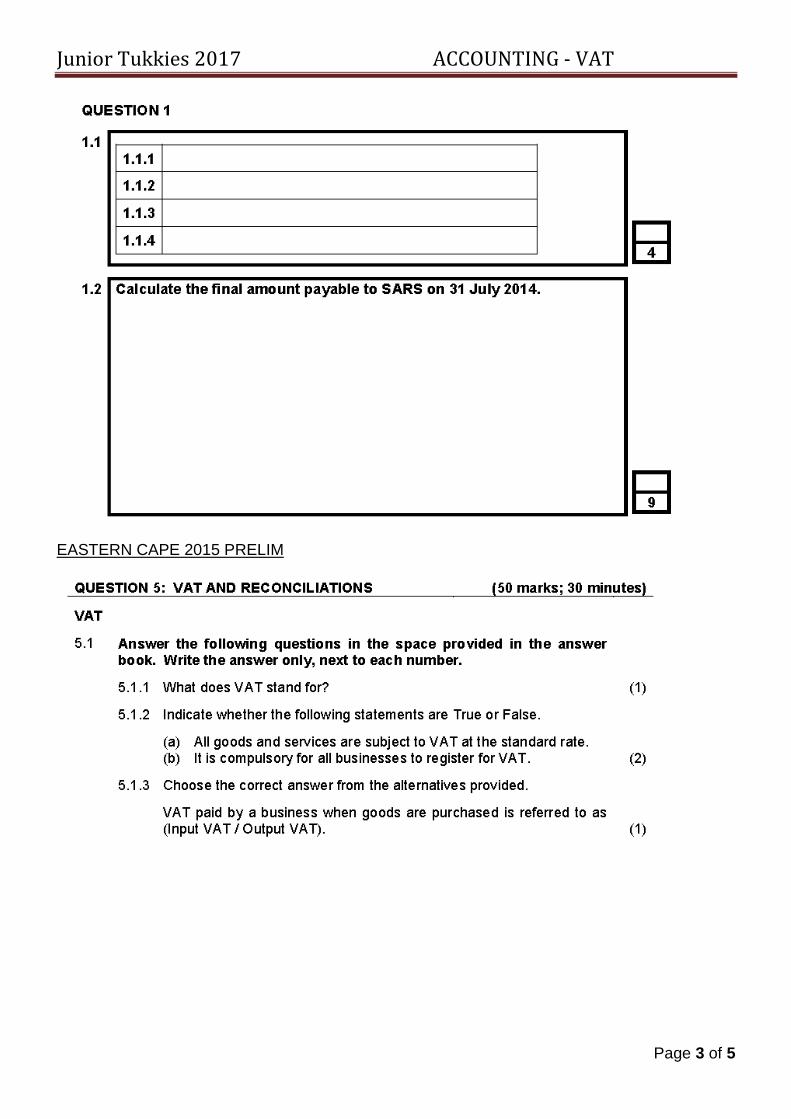

Junior Tukkies 2017 ACCOUNTING - VAT

Page 1 of 5

VAT

QUESTION PAPER

ANSWER BOOK

Junior Tukkies 2017 ACCOUNTING - VAT

Page 2 of 5

NOVEMBER 2014

Junior Tukkies 2017 ACCOUNTING - VAT

Page 3 of 5

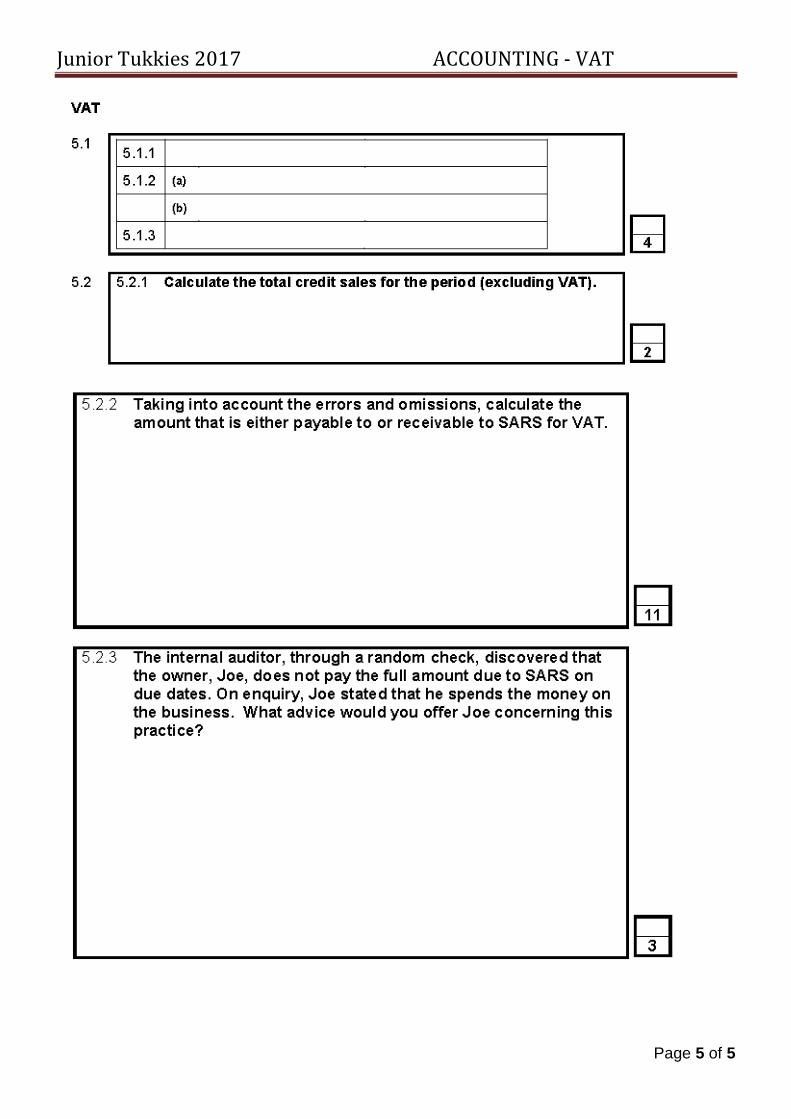

EASTERN CAPE 2015 PRELIM

Junior Tukkies 2017 ACCOUNTING - VAT

Page 4 of 5

Junior Tukkies 2017 ACCOUNTING - VAT

Page 5 of 5

![Cash Flow Statement[1]](https://img.pdfslide.us/doc/110x75/5467c3c1b4af9f42298b48d9/cash-flow-statement1.jpg)