Embed Size (px)

Citation preview

CASE STUDY

LightSquared: A Bitter Bankruptcy

Alan Carr, Drivetrain Advisors, Ltd. (Moderator)

Hon. Shelley C. Chapman, U.S. Bankruptcy Court, Southern District of New York

Mark Hootnick, Millstein & Co.

Thomas Lauria, White & Case

Jack Neumark, Fortress Investment Group, Credit Funds Business

LightSquared Background

• LightSquared’s principal line of business was developing a nationwide,

terrestrial 4G network for wholesale deployment from owned/leased

satellite-only spectrum

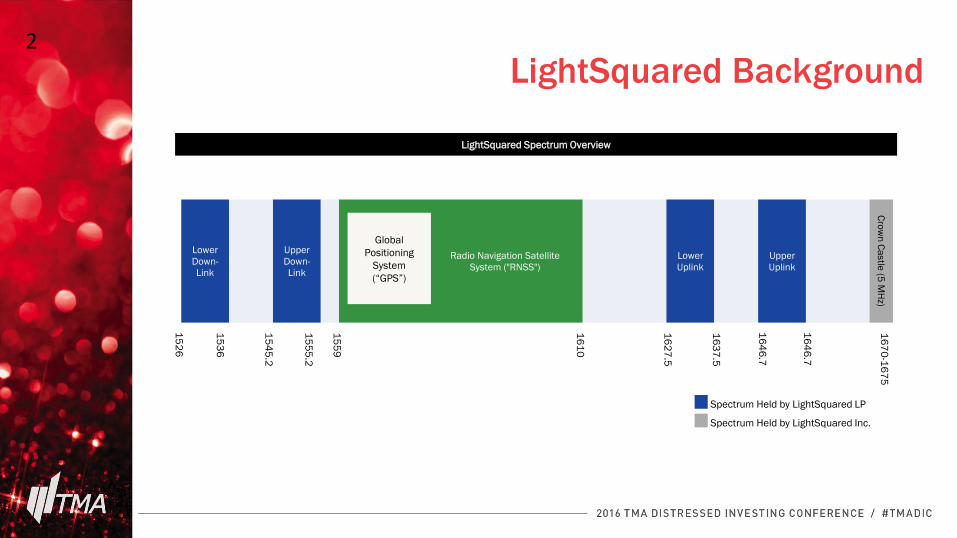

• LightSquared controlled the following spectrum assets:

– 40 MHz + 6MHz of owned/leased L-Band Mobile Satellite Service

spectrum (“L-Band)

– 5 MHz of 1.6 GHz leased terrestrial spectrum of One Dot Six Corp. (“One

Dot Six” or “Crown Castle”)

– LightSquared owned two next-generation satellites

• In February 2012, the Federal Communications Commission proposed to

modify LightSquared's satellite license to indefinitely suspend its underlying

terrestrial component

• On May 14, 2012, LightSquared filed for Chapter 11

1

Lower

Down-

Link

Upper

Down-

Link

Radio Navigation Satellite

System ("RNSS")

Lower

Uplink

Upper

Uplink

Cro

wn

Ca

stle

(5 M

Hz)

LightSquared Background

Spectrum Held by LightSquared LP

Spectrum Held by LightSquared Inc.

Global

Positioning

System

(“GPS”)

15

26

15

36

15

45

.2

15

55

.2

15

59

16

10

16

27

.5

16

37

.5

16

46

.7

16

46

.7

16

70

-16

75

LightSquared Spectrum Overview

2

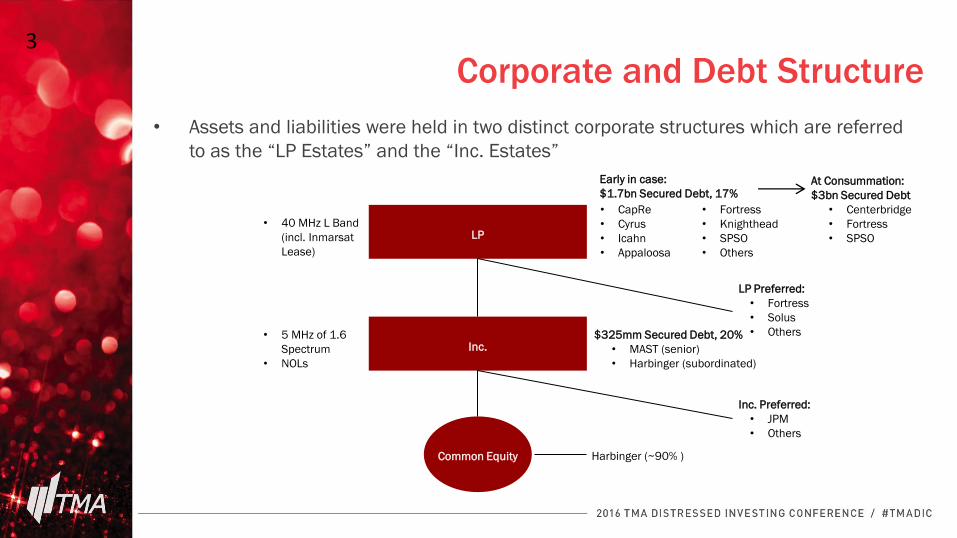

• Assets and liabilities were held in two distinct corporate structures which are referred

to as the “LP Estates” and the “Inc. Estates”

Corporate and Debt Structure

• 40 MHz L Band

(incl. Inmarsat

Lease)

LP

Common Equity

LP Preferred:

• Fortress

• Solus

• Others • 5 MHz of 1.6

Spectrum

• NOLs

$325mm Secured Debt, 20%

• MAST (senior)

• Harbinger (subordinated)

Inc. Preferred:

• JPM

• Others

Harbinger (~90% )

Inc.

3

At Consummation:

$3bn Secured Debt

• Centerbridge

• Fortress

• SPSO

• CapRe

• Cyrus

• Icahn

• Appaloosa

• Fortress

• Knighthead

• SPSO

• Others

Early in case:

$1.7bn Secured Debt, 17%

Lower

Down-

Link

Upper

Down-

Link

Radio Navigation Satellite

System ("RNSS")

Lower

Uplink

Upper

Uplink

Cro

wn

Ca

stle

(5 M

Hz)

NO

AA

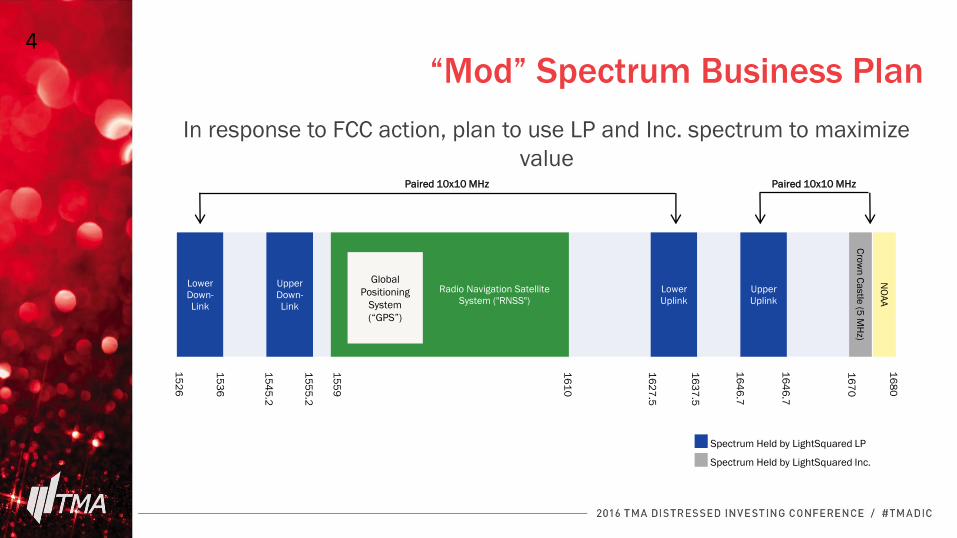

“Mod” Spectrum Business Plan

In response to FCC action, plan to use LP and Inc. spectrum to maximize

value

Spectrum Held by LightSquared LP

Spectrum Held by LightSquared Inc.

Global

Positioning

System

(“GPS”)

15

26

15

36

15

45

.2

15

55

.2

15

59

16

10

16

27

.5

16

37

.5

16

46

.7

16

46

.7

16

70

16

80

Paired 10x10 MHz Paired 10x10 MHz

4

Governance and Competitor Involvement

• Board controlled by Harbinger Group

– Majority Shareholder

– Held subordinated secured claim at Inc.

• Charles Ergen

– Controlled DISH – alleged competitor to LightSquared

– Controlled SPSO – purchased over $1 billion of LP senior

secured debt

• Blocking position

• Discount to par

• Suspected of delaying closing trades to hide identity

5

Governance

• LBAC (DISH subsidiary) bid $2.2 billion for LP’s wireless spectrum licenses

• Harbinger / Falcone opposed bid

– Low-ball bid

– Value of bid comparable to face value of LP’s outstanding secured debt obligations

– Alleged that SPSO’s debt purchases were impermissible because SPSO was controlled by a competitor and did not meet the definition of “eligible assignee” under LP’s credit agreement

• Group of LP Secured Lenders (including SPSO) entered into an RSA with LBAC

6

Governance

• Mid-2013, as a condition to extension of exclusivity,

Special Committee of 3 Independent Directors

appointed to oversee restructuring and auction of all

of LightSquared’s assets

– Premise that the combined value of LightSquared’s

assets was greater than LP and Inc.’s assets valued

separately

7

Auction

• Break-up Fees

– LBAC entitled to breakup fee of 2 1/3% (and potentially 3%) of the

final transaction price, or at least $51.8 million

– Inc. Lenders not granted break up fee

• Special Committee vigorously marketed LightSquared

• Unsuccessful in creating robust auction process

– Impact of existing LBAC bid / RSA with Group of LP Secured Lenders

• No other qualified bids from third parties outside of LightSquared’s

capital structure

• LBAC requirement of claims releases

• Special Committee cancelled the auction

9

Auction

• Subsequently, LBAC terminated its bid and PSA with

the Ad Hoc Group of LP Lenders

– LBAC’s right to terminate the LBAC bid and PSA was

challenged by the Ad Hoc Group of LP Lenders but

upheld by the bankruptcy court

10

First Confirmation Hearing: Overview of Plan

• May 2014

• Proposed Plan Key Terms

– Backed by Harbinger, Fortress, JPMorgan & Melody Capital Partners

– Would have restructured $4 Billion

• Harbinger would have retained minimum 30% equity stake, potentially up to 36%

– Would have repaid Ergen / SPSO through seven-year 3rd Lien note

• Required Equitable Disallowance

11

First Confirmation Hearing: Valuation

• Judge Chapman denied confirmation

• Valuation

– Uncertainty regarding FCC approvals regarding

LightSquared’s ability to use certain wireless spectrum

made it impossible to value the company

– Made claim that Ergen would eventually be repaid in full

unreliable

• Plan was not fair and equitable to SPSO

12

First Confirmation Hearing: Equitable Disallowance

• Debtors sought equitable disallowance of SPSO’s

claim, arguing SPSO was a competitor

– SPSO / Ergen would have received no distribution on

account of claim

• Judge Chapman found inequitable conduct, but

denied disallowance remedy

– in order for claim to be disallowable, agreement must

provide that breach renders assignment void

13

First Confirmation Hearing: Equitable Subordination

• Debtors sought equitable subordination of SPSO’s claim

• Judge Chapman determined some of SPSO’s claim should be subordinated, with the amount to be determined at a later date

• Found SPSO / Ergen was buying debt for the benefit of DISH and purposely “hung trades” in an attempt to control the bankruptcy proceedings

• Rejected the notion that equitable subordination should be linked to the purchase price of a claimant’s debt

14

First Confirmation Hearing: Confirmation Denied

• Judge Chapman gave the parties 2 weeks to resolve

their differences consensually.

• If the parties failed to reach agreement, Judge

Chapman said that she would appoint Judge Drain as

mediator

15

Mediation & Development of Restructuring

Alternatives

• Judge Drain was appointed as mediator at the end of May 2014. Mediation stretched from June to December 2014

• Several alternative restructuring plans were proposed, with the balance of power shifting several times

• Paradigm shift occurred when FCC Auction 97 dramatically changed value dynamic (November 2014)

• In light of spectrum value, stakeholders reconsidered approach to restructuring

16

Second Confirmation Hearing

• New Plan

– Kept all of Debtors’ estates together to maximize value of

collective assets

– Controlled by Centerbridge Partners, Fortress Investment

Group and JPMorgan (Harbinger retained 44% of equity, but

ceded voting control)

– Provided senior stakeholders with same or better treatment

• Ergen paid in full in cash

– Junior stakeholders received sizeable recovery

19

Second Confirmation Hearing

• Valuation

– LightSquared presented two valuations of its assets

– The second approach considered the implications of the

FCC’s recent auction of AWS-3 wireless spectrum on the

value of LightSquared’s spectrum, while the first

approach did not

17

Second Confirmation Hearing

• Competing Plans & Objections

– Solus proposed a competing plan, which it withdrew when

Fortress, Centerbridge and Chase purchased its claims

– Ergen had objected, but withdrew objection when plan was

changed to pay his claims in full in cash (as opposed to with a

note)

• Consensually resolved

18

Second Confirmation Hearing

• FCC conditionality

– Conditioned on FCC approval of transfer of licenses from

Debtors to New LightSquared

• Company locked in financing during a robust financing

market; proved to be good decision given market

volatility in 4Q2015

• December 7, 2015 – Plan went effective when FCC

approved Debtors’ change of control application

20

Tweet @TMAGlobal

What was your biggest takeaway from the

LightSquared bankruptcy?

Tweet your answer now to @TMAGlobal

![Chapter 3 Wireless LANs Reading materials: [1]Part 4 in textbbok [2]M. Ergen (UC Berkeley), 802.11 tutorial](https://img.pdfslide.us/doc/110x75/56649dbc5503460f94aadcf1/chapter-3-wireless-lans-reading-materials-1part-4-in-textbbok-2m-ergen.jpg)