Embed Size (px)

Citation preview

YFS Case Study No. #15: Youth-Inclusive Financial Services: Scaling Up

and Mobile Banking

Page | 0

Youth-Inclusive Financial Services Case Study Series 2010

Youth-Inclusive Financial

Services Linkage Program

(YFS-Link)

Case Study No. 15:

Youth-Inclusive Financial Services:

Scaling Up and Mobile Banking

Updated: September 2012

Author: Making Cents International

YFS Case Study No. #15: Youth-Inclusive Financial Services: Scaling Up

and Mobile Banking

Page | 1

Copyright © 2012 Making Cents International

Sections of this publication may be copied or adapted without permission from Making Cents

International provided that the parts copied are distributed for free or at cost - not for profit.

Please credit Making Cents International and Equity Bank Ltd., Youth-Inclusive Financial

Services Linkage Program Case Study #15, for those sections excerpted.

For any commercial reproduction, please obtain permission from Making Cents International.

For additional information, contact:

Making Cents International

Youth-Inclusive Financial Services Linkage Program (YFS-Link)

1155 30th

St. NW, Suite 300

Washington, DC 20007

Tel.: 202-783-4090 Fax: 202-783-4091

Skype: makingcentsinfo

Email: [email protected]

Web: www.makingcents.com

YFS Case Study No. #15: Youth-Inclusive Financial Services: Scaling Up

and Mobile Banking

Page | 2

ABSTRACT

Equity Bank is a commercial bank based in Nairobi, Kenya and is the largest African majority

owned company in East and Central Africa with a base of over 7.15 million customers. In Kenya

job creation and the development of small and medium enterprises are key to the well-being of

the youth population. Currently, about 70% of Kenyans are below 29 years old and by 2017 more

than 24 million Kenyans will be between 18 and 35 years. Young people account for 61% of the

unemployed population. In Equity Bank’s experience the business and social case are strong for

youth-inclusive financial services as its youth product grew by 216% from December 2008

through December 2011 and the portfolio quality, in terms of portfolio at risk greater than 90

days, at the end of September 2011 was 0.32% for loans to youth. Considering the extent of

Kenya’s growing youth population, Equity has had to learn to quickly scale-up its financial and

non-financial services through a variety of innovative and youth oriented strategies, including

increase of and training for staff and mobile banking service delivery channels.

YFS Case Study No. #15: Youth-Inclusive Financial Services: Scaling Up

and Mobile Banking

Page | 3

Background

Equity Bank is a commercial bank based in Nairobi, Kenya and is the largest African majority

owned company in East and Central Africa with a base of 7.15 million customers. Equity Bank

comprises of over 57% of all bank accounts in Kenya and has 834,000 borrowers, 186 branches,

700 ATMs 6,000 point of sale machines and over 3,200 agents. The Bank’s mission is to offer

inclusive customer focused financial services that socially and economically empower their

clients and other stakeholders.

Currently, 70% of Kenyans are below 29 and by 2017 more than 24 million Kenyans will be

between 18 and 35 years. Young people account for 61% of the unemployed and 92% of these

youth have no technical training other than formal schooling. In addition to lack of expertise,

Kenyan youth face additional challenges to starting a business. Currently, Kenya ranks 125 out of

183 economies in terms of ease of starting a business (World Bank Doing Business 2011 Report).

Additionally, 8 out of 10 businesses collapse after 2 years in operation.

The Government of Kenya believes that job creation and the development of small and medium

enterprises are key to the well-being and advancement of the youth population. In 2006 it created

the Youth Enterprise Development Fund. The Fund, backed by approximately US$27 million,

provides financial institutions and NGO’s with subsidized loan capital designated for young

entrepreneurs between the ages of 18 to 35. Equity Bank received an initial US$1.2 million from

the fund in 2007. The bank was to supplement this disbursement with its own funds at the rate of

Kes 1 to 9 (i.e. 9 shillings for every shilling given by government) in order to reach out to as

many youth entrepreneurs as possible. The lending to youth stood at US$ 68M at the end of 2011,

meaning the bank had managed to lend 56 fold.

I. Making the Business Case for YFS

Equity’s experience lending to young entrepreneurs demonstrates a strong business case for

youth-inclusive financial services. Not only do young people make up the majority of the Kenyan

market for financial services, young people also offer the institution the ability to grow a strong

and long-lasting client base. Young people are also attractive clients in that they bring fresh ideas

and new energy that pressure the Bank to be innovative and look toward the future. Anecdotal

evidence also shows that youth learn faster and are able to benefit from trainings more than

adults, and they are able to quickly transform training to real business solutions and growth.

Since its launch Equity Bank’s youth product has grown faster than the rest of its products. From

December of 2010 through December of 2011, the youth product grew by 52% while the rest of

the bank’s portfolio grew by 45%. The youth product also performed better than the banks other

loan products in terms of portfolio quality where portfolio at risk greater than 90 days, at the end

of September 2011 was 0.32% for loans to young people and 2.84% for the rest of the Bank.

YFS Case Study No. #15: Youth-Inclusive Financial Services: Scaling Up

and Mobile Banking

Page | 4

Historical analysis of the youth portfolio also revealed some promising trends. Of those youth

who began borrowing in 2007, 83% have remained with the bank after five years. Twenty-seven

per cent of these youth borrowers have also borrowed additional products, indicating a strong case

for profitability over time. Average loan size also tells a promising story where initial loan sizes

of between US$200-250 have nearly quadrupled in five years to an average loan size of $860 for

those youth who began borrowing in 2007. On average, these youth have taken out 6 loans in five

years, indicating a consistent revenue stream for the bank. Equity also noted a strong increase in

savings of these initial borrowers. Over 90% of the youth entrepreneurs came to Equity without a

savings account. In five years, these young borrowers have opened between 2-3 savings accounts

within the bank.

II. Youth Products and Services

Equity Bank began providing youth specific financial and non-financial services in Kenya in

2007. Market research found that most Kenyan youth are associated with some form of a group or

club including church, community or student groups. Equity Bank leverages this structure as a

platform for delivering group lending as well as accompanying non-financial services including

financial and entrepreneurship education. The youth groups comprise of 15 to 30 young people

between the ages of 18 to 35 years. Equity Bank currently serves 140,000 young people.

Equity’s requires young entrepreneurs to save 10% of their loan amount. On a weekly basis the

average young person saves KES 100 (approximately US$1). Currently youth savings at Equity

totals 7.1 million USD (KES 568 million) and loans outstanding total 18.6 million USD (KES

1,487 million). This suggests that young people are savings well above the 10% minimum and the

high value they place on savings (the ratio currently stands at 38% of savings to the outstanding

book).

Complementary to the youth loan product, the Equity Group Foundation, in partnership with the

MasterCard Foundation, launched a three-year training program in 2010 aimed at providing

financial literacy training to 619,500 women and youth across Kenya. This program has now been

reviewed and it was found that demand was extremely high. The bank had to adjust the program

to accommodate more women and youth and now targets 1 million trainees. The six education

modules focus on savings, budgets, debt management, financial negotiation, banking services,

and micro-insurance. In 2012, an agricultural business curriculum was also developed to

accommodate demand from the additional trainees. The modules will help to cultivate

responsible management of income, loans and savings that enables youth to improve their overall

livelihoods and ability to participate in the labor force and business development.

In addition to financial education, Equity Bank provides follow up business advisory services to

ensure that youth businesses are not at risk of collapsing. Equity Bank also links young

entrepreneurs with successful local and international entrepreneurs to form mentoring

relationships. These mentors provide young people with guidance and advice on managing and

YFS Case Study No. #15: Youth-Inclusive Financial Services: Scaling Up

and Mobile Banking

Page | 5

growing their businesses. The mentoring process is anchored with the group lending structure

where a section of the members are above a specific age with business experience and acumen.

The clubs/groups are designed to create an environment where the youth entrepreneurial ideas are

incubated to maturity. The bank in conjunction with Google has recently launched a channel on

you tube called the “African Success Story: Generation X,” where successful youth can exhibit

their businesses & enterprises1. The bank has also been partnering with the Government’s

Ministry of Youth in facilitating the National Youth Trade Fair, where the youth can show case

their products and enterprises

Equity Bank also offers scholarship programs for secondary school and university students. The

bank has provided over 10,000 students with scholarships. Students also intern at the bank during

their school holidays and gain valuable employment experience that helps them in their job search

after graduation. These young scholars have become a type of ambassador for Equity Bank and

for the banking sector in general.

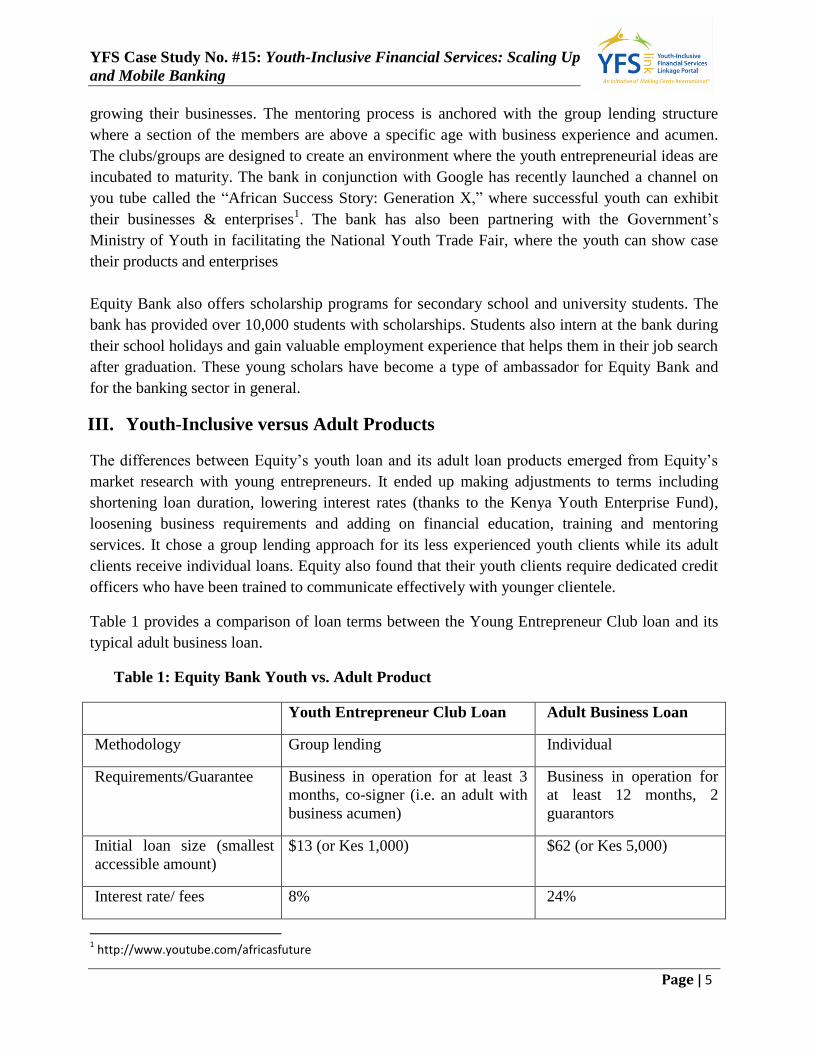

III. Youth-Inclusive versus Adult Products

The differences between Equity’s youth loan and its adult loan products emerged from Equity’s

market research with young entrepreneurs. It ended up making adjustments to terms including

shortening loan duration, lowering interest rates (thanks to the Kenya Youth Enterprise Fund),

loosening business requirements and adding on financial education, training and mentoring

services. It chose a group lending approach for its less experienced youth clients while its adult

clients receive individual loans. Equity also found that their youth clients require dedicated credit

officers who have been trained to communicate effectively with younger clientele.

Table 1 provides a comparison of loan terms between the Young Entrepreneur Club loan and its

typical adult business loan.

Table 1: Equity Bank Youth vs. Adult Product

Youth Entrepreneur Club Loan Adult Business Loan

Methodology Group lending Individual

Requirements/Guarantee Business in operation for at least 3

months, co-signer (i.e. an adult with

business acumen)

Business in operation for

at least 12 months, 2

guarantors

Initial loan size (smallest

accessible amount)

$13 (or Kes 1,000) $62 (or Kes 5,000)

Interest rate/ fees 8% 24%

1 http://www.youtube.com/africasfuture

YFS Case Study No. #15: Youth-Inclusive Financial Services: Scaling Up

and Mobile Banking

Page | 6

Add-on advantages Financial literacy training,

mentorship, business advice

Financial literacy training

Incentives 100% repayment provides access to

larger loan sizes in next cycle.

Maximum amount is $1,250, access

to trainings & trade fairs/workshops

Larger amounts for repeat

borrowing, interest rebates

for good repayers.

Maximum amount $6,250

Frequency of payment weekly monthly

Length of Loan cycle 6 months 6 months

Delivery Mechanism colleges and clubs Bank branches, mobile

banks, ATMs

Marketing and Promotion Advertisements at schools/radio/TV

Free budgeting workshop

Media (television,

testimonials, quarterly

newsletters)

Currently, Equity Bank is in the process of developing a second level, “bridging product” that will

be based on age and business experience to transfer young people from youth products to adult

products. This product reduces the group size to two individuals who co-sign each other’s loan.

IV. Marketing and Delivery Channels: Mobile Banking

Equity has three types of branches: “regular” for its core individual and small business clients;

“mobile” for rural customers living in areas for which a permanent location is not yet

economically viable; and “prestige” for Equity’s emerging affluent segment who has grown with

the bank over time. Other delivery channels include automated teller machines and partnerships

with shopkeepers in rural areas to provide banking services. By Dec 2011, ATMs accounted for

46 percent of all Equity Bank. Throughout Kenya, Equity Bank has 165 branches, 700 ATMs, and

6,000 Point of Sale Machines. For youth, there are some specific capabilities in the mobile

application that target youth.

In addition to these standard delivery channels, Equity Bank is increasingly looking to

technology-based solutions for increasing scale and reducing transaction costs. Youth clients can

now use their cell phones to apply for loans, make payments, and deposit or withdraw money

without having to spend time and money traveling to and waiting in line at the bank. The mobile

channel (called Eazzy 247) provides services like money transfers, utility/bill payments, loan

application, balance enquiry, air time top-ups, cheque book related services and mini statements.

In the year 2011, this service gained momentum and became very popular (annexure 1) going

from 417, 914 to 1,362,917 users between January of 2011 to January of 2012.

YFS Case Study No. #15: Youth-Inclusive Financial Services: Scaling Up

and Mobile Banking

Page | 7

V. Overcoming Challenges

The key challenges of scaling youth-inclusive financial services include:

1) Staff prejudice against young people. Equity found that it needed to hire and train staff to

be sensitive to young people’s needs and knowledgeable about the financial and non-

financial challenges facing youth, which was assessed through focus group discussions,

customer interviews, and general field research

2) Decreased youth mobility. Because young people are not as readily able to travel to a bank

branch, Equity youth loan staff had to adapt their schedules to travel and market the

product in places that youth frequent including colleges, social clubs, etc.

3) Rapid Growth. The rapid growth in demand of the Youth Entrepreneur Clubs forced

Equity to nearly double its initial staff of 120 loan officers to 300 in the first year.

Management learned to quickly mobilize specialized youth staff to respond to the rapidly

increasing demand.

4) Institutional capacity to utilize technology (i.e. the video channel on YouTube) to engage

young people and showcase success cases of young entrepreneurs;

5) Financial resources to support institutional capacity to scale up staff, services and delivery

channels. In order to increase resources dedicated to this effort, Equity Bank engaged

several partners both external and internal government ministries (i.e. Ministry of Finance,

Ministry of Youth, Ministry of Agriculture, etc.)

VI. Lessons Learned

1) Conduct market research to ensure that the financial product or service is appropriately

targeted to youth. Additionally young people should review products and be encouraged

to provide feedback.

2) Provide young clients with financial education in order to cultivate clients who can

successfully use the Bank’s products and services and to encourage them to stay with the

Bank and to access multiple financial products and services over time.

3) Technology can increase awareness of financial services and deliver services to youth

who are adaptable to new innovations.

4) With the appropriate financial services and education, young people promise

profitability over time

VII. Next Steps at Equity Bank

Based on the positive experiences with the Youth Entrepreneur Clubs, Equity is now in the

process of developing a youth strategy that will brand itself as Kenya’s bank for young people,

providing them with a range of tailored, life-cycle appropriate financial services and supporting

them to achieve their life and career goals.

YFS Case Study No. #15: Youth-Inclusive Financial Services: Scaling Up

and Mobile Banking

Page | 8

Specifically, Equity plans to diversify its reach of young people to include those working in

sectors including: commercial agriculture, tourism, infrastructure development, services,

ICT/Business Process Outsourcing, manufacturing, retail/wholesale trade, and the entertainment

industry. In particular, Equity Bank estimates that about 75% of Kenyan youth are farmers. In

order to reach deeper into rural areas and engage young people working in the agriculture sector,

Equity Bank will need to adapt to their needs. The major challenge for these young people living

in remote areas is physical access to financial services so delivery channels must adapt to the

available means. Additionally, agro-based youth will require different types of financial products

that respond to the planting and harvesting seasons; technology; access to market information;

and expertise in agricultural businesses to create more jobs and make it profitable and attractive to

youth.

YFS Case Study No. #15: Youth-Inclusive Financial Services: Scaling Up

and Mobile Banking

Page | i

ANNEX 1: Mobile Phone Service Uptake

YFS Case Study No. #15: Youth-Inclusive Financial Services: Scaling Up

and Mobile Banking

Page | ii

ANNEX 2: BIBLIOGRAPHY OF YFS CASE STUDY SERIES

1. Abeywickrema, C. (2009, September). The role of the Hatton National Bank in creating access to financial services for youth in

Sri Lanka. Hatton National Bank. Accessible at: http://www.makingcents.com/products_services/resources.php

Hatton National Bank (HNB), a prominent commercial bank in Sri Lanka, has been committed to providing financial services in rural

areas and to more vulnerable populations for years. More recently, HNB has begun to focus on serving youth in two key ways: 1)

establishing Student Banking Centers in schools 2) targeting youth in rural areas in their village microfinance programs to receive both

financial and non-financial services. This case study examines key methodologies to effectively serving youth with financial services

through a commercial lending model.

2. Ahammed, I. (2009, September). A case study on financial services for street children. Padakhep. Accessible at:

http://www.makingcents.com/products_services/resources.php

Padakhep is a non-government organization (NGO) in Bangladesh that strives to reach street children through an integrated approach.

This case study details the innovative “Introduction of Financial Services” program which provides both credit and savings services to

Dhaka street kids to encourage them to initiate income generating activities of their own. A key lesson that emerged was that flexible

terms and conditions of financial products are essential for working with an extremely vulnerable target population like urban street

children.

3. Austrian, K. & Ngurukie, C. (2009, September). Safe and smart savings products for vulnerable adolescent girls in Kenya &

Uganda. Population Council & MicroSave Consulting Ltd.

Accessible at: http://www.makingcents.com/products_services/resources.php

This case study details the unique partnership between Population Council, a research-focused NGO, and MicroSave, a consulting firm, to

develop and deliver critical financial services to adolescent girls by partnering with four financial institutions in Kenya. This case study

shows that by offering girls secure savings products they can mitigate some of the hardships they endure as well as encourage positive

savings habits, thereby increasing their economic stability as they transition to adulthood.

4. Chandani, T. & Twamuhabwa, W. (2009, September). A partnership to offer educational loans to nursing students in Uganda.

Banyan Global & Equity Bank. Accessible at: http://www.makingcents.com/products_services/resources.php

Equity Bank-Uganda and Banyan Global have successfully partnered in Uganda to develop an innovative loan product that links

workforce development in the health sector with microfinance. This case study describes the key elements of success of their pilot to bring

education loans to aspiring nurses between the ages of 17 and 24. Equity Bank proves that by approaching youth who are formally

affiliated with a training institution can be critical to alleviating risk, gaining trust and achieving market share.

5. Kashfi, F. (2009, September). Youth financial services: The case of BRAC and the adolescent girls of Bangladesh. BRAC.

Accessible at: http://www.cyesnetwork.org/sites/default/files/Case%20Study%20on%20BRAC%20and%20Youth.pdf

Ten years after beginning adolescent-focused initiatives in Bangladesh, BRAC realized that financial independence can play a key role in

empowering adolescent girls further. This case study focuses on the Employment and Livelihood for Adolescents (ELA), which offers both

credit and savings services to adolescent girls. Findings indicate that using a holistic approach to financial service delivery customized to the

needs of adolescents will equip the girls to invest better and take higher loans on average.

6. Gepaya, L.Y. (2009, September). Youth inclusive financial services: Marketing and delivery is what matters. Panabo Multi-

Purpose Cooperative. Accessible at: http://www.makingcents.com/products_services/resources.php

The Panabo Multi-Purpose Cooperative (PMPC) is a cooperative based in the Philippines and a part of the global World Council of Credit

Unions (WOCCU) network. This case study describes how PMPC discovered that partnerships with schools can be an effective form of

growing membership, promoting a culture of savings at a young age, and delivering much-needed financial services to underserved youth

populations.

7. Harnest, J. & Neilson, E. (2009, September). Microfinance and “the next generation” The FINCA Aflatoun curriculum

implemented in an MFI setting. Finca Peru & Aflatoun. Accessible at:

http://www.makingcents.com/products_services/resources.php

Aflatoun, an organization committed to social development and financial literacy for children between the ages of 6-14, has begun

partnering with select microfinance institutions (MFIs) to offer its curricula to clients’ children. This case study discusses Aflatoun’s work

with FINCA Peru detailing the strengths, weaknesses, opportunities and challenges associated with implementing Aflatoun curricula in a

non-formal school setting with children of microfinance beneficiaries. Findings from this project indicate that children who consistently

attend classes have demonstrated a strong willingness to save.

YFS Case Study No. #15: Youth-Inclusive Financial Services: Scaling Up

and Mobile Banking

Page | iii

8. Denomy, J. (2009, September). MEDA works with youth: YouthInvest. Mennonite Economic Development Associates.

Accessible at: http://www.makingcents.com/products_services/resources.php

This case study provides an overview of MEDA’s work on increasing youth access to financial services, particularly through YouthInvest

in Egypt and Morocco. Detailed in this case study, YouthInvest was designed with a strong market research component, the results of

which are crucial to designing successful financial and non-financial services for youth.

9. Massie, J.(2009, September). Using innovative partnerships and market research to link financial education and savings

products for girls. MicroFinance Opportunities. Accessible at: http://www.makingcents.com/products_services/resources.php

Microfinance Opportunities working with Savings and Economic Empowerment grantees to develop financial literacy modules that will

be closely linked to their savings products. For the first time, market research is informing both the design of financial education and

financial products for young women. This effort is carried out through innovative partnerships between MFO, youth service organizations,

and financial institutions. This case study provides an overview of these partnerships and how they conduct market research, the integral

role of these results in designing of appropriate savings products for youth.

10. Nazneen, S. (2009, September). Save the Children’s youth financial services: Adolescent girls project. Save the Children.

Accessible at: http://www.makingcents.com/products_services/resources.php

This case study describes the Kishoree Kontha (Adolescent Girls’ Voices) Project implemented by Save the Children in 5 sub-districts of

southern Bangladesh. The goal of this intervention is to link savings schemes with other non-financial services, such as health and

education, to allow rural adolescent girls to build their human, social and economic assets. Additionally, this case study details how Save

the Children dealt with traditional gender roles, as adolescent girls are not decision-makers, through intense community outreach and

sensitization.

11. Cilimkovic, S. & Jahic, S. (2009, September). Youth inclusive financial services: A case study from Bosnia. Partner

Microcredit Foundation. Accessible at: http://www.makingcents.com/products_services/resources.php

Partner Microcredit Foundation is a non-profit microfinance institution in Bosnia Herzogovina that recently piloted a youth loan product.

The goal of this youth program was to increase self-employment opportunities for young people in Bosnia and Herzegovina by providing

access to loan capital in addition to market-oriented business training and mentorship services for youth clients. This case study describes

in extensive detail the experience of Partner MK in conducting market, research, designing a specialized youth loan product, and the

preliminary outcomes and lessons learned of this program.

12. Schiller, J. (2009, September). Making financial services and business skills development available to African children and

youth: Accomplishments and limitations of research and monitoring. Plan International. Accessible at: http://www.makingcents.com/products_services/resources.php

This case study examines Plan International’s situation analysis research carried out in Senegal, Niger and Sierra Leone. This project

identifies active youth groups and presents a profile of youth and their activities and their general socio-economic conditions in each

locality. This project focuses on the Village Savings and Loan (VSL) program in the three countries. The associations formed are

sustainable and replicable, and the local implementing partner institutions have been effective and successful in all three program

countries Overall, youth’s response has encouraged the project to believe that dramatic upscale is possible.

13. Storm-Swire, L. (2009, September). Exploring youth financial services: The case of ProMujer in Bolivia. ProMujer. Accessible

at: http://www.makingcents.com/products_services/resources.php

Pro Mujer is an international women’s development and microfinance organization that alleviates poverty in Latin America by providing

financial services, healthcare and training to poor women entrepreneurs. This case study details the process of developing a group-based

loan product targeted at youth, with results indicating that significant investment in proper market research, product development, staff

and infrastructure is required to determine the differing needs of this heterogeneous market.

14. Shell, B. (2009, September). Product development for girls: Girls’ savings and financial education. Women’s World Banking.

Accessible at: http://www.makingcents.com/products_services/resources.php

This case study examines how Women’s World Banking has helped two of its network members, XacBank of Mongolia and Banco

ADOPEM in the Dominican Republic, design and roll out savings products and financial education programs for girls and young woman

ages 7-24. WWB found that reaching girls cost-effectively required developing strategic partnerships – with experienced youth education

professionals, since the bank did not have that expertise in-house, and with institutions already interacting with girls, since convenience is

an important issue for both the products and the financial education program.

YFS Case Study No. #15: Youth-Inclusive Financial Services: Scaling Up

and Mobile Banking

Page | iv

15. Making Cents International and Equity Bank LTD. (2010, February, updated 2012, September). Youth-Inclusive Financial

Services: Scaling Up and Mobile Banking. Equity Bank. Accessible at:

http://www.makingcents.com/products_services/resources.php

This case study explores the experience of Equity Bank, a commercial bank based in Nairobi, Kenya and the largest African majority

owned company in East and Central Africa with a base of over 7.15 million customers. In Equity Bank’s experience the business and

social case are strong for youth-inclusive financial services as its youth product grew by 216% from December 2008 through December

2011. Considering the extent of Kenya’s growing youth population, Equity has had to learn to quickly scale-up its financial and non-

financial services through a variety of innovative and youth oriented strategies, including increase of and training for staff and mobile

banking service delivery channels.

16. Al-Waell, A. and Storm, L. (2011, March). First Middle Eastern Microfinance Bank Puts Youth First. Al-Amal Microfinance

Bank. Accessible at: http://www.makingcents.com/products_services/resources.php

A pioneer in Islamic microfinance, Al-Amal Microfinance Bank (Al-Amal) was established in October 2008 as the first microfinance

bank in Yemen. Dedicated to providing poor micro-entrepreneurs with access to financial services, Al-Amal targets youth and women

with microcredit, savings, and insurance, among other services. Through slight adaptations to its product offerings, including collateral

requirements and minimum balances, Al-Amal has quickly grown its reach to thousands of Yemeni youth. In this case study, Al-Amal

discusses techniques for providing young people with appropriate financial services, including staff training and youth-friendly marketing

and delivery channels.