Embed Size (px)

Citation preview

© Oliver Wyman | LON-FSP03201-076FINANCIAL SERVICES

CASE STUDYDEPOSIT GUARANTEE FRAMEWORKS

19 NOVEMBER 2014

Introduction to Oliver WymanSection 1

22© Oliver Wyman | LON-FSP03201-076

Oliver Wyman serves a wide range of industries, but focus in the Nordics is Financial Services

Industries Financial Services Practice

Corporate Strategy

Finance & Risk

Corporate & Institutional Banking

Insurance

Public Policy

Strategic IT & Operations

Retail & Business Banking

Wealth & Asset Management

Corporate Finance and Advisory

Industry groups

Key capabilities

3© Oliver Wyman | LON-FSP03201-076 3

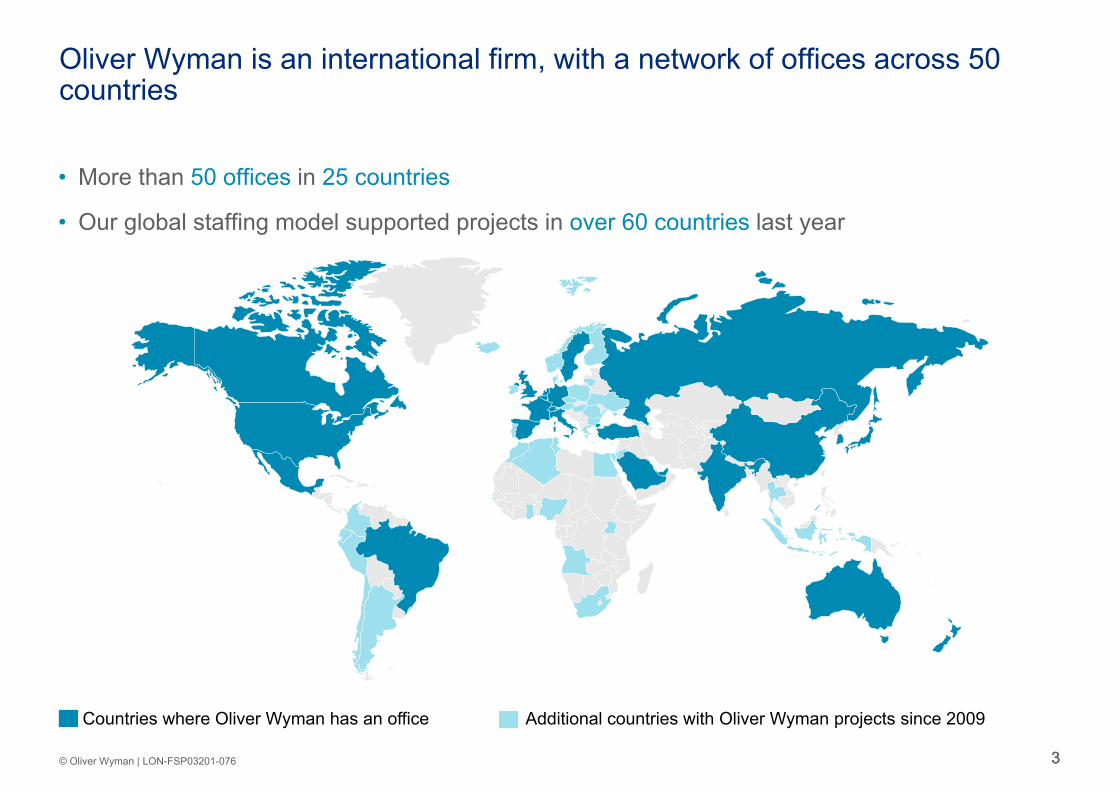

• More than 50 offices in 25 countries

• Our global staffing model supported projects in over 60 countries last year

Oliver Wyman is an international firm, with a network of offices across 50 countries

Countries where Oliver Wyman has an office Additional countries with Oliver Wyman projects since 2009

44© Oliver Wyman | LON-FSP03201-076

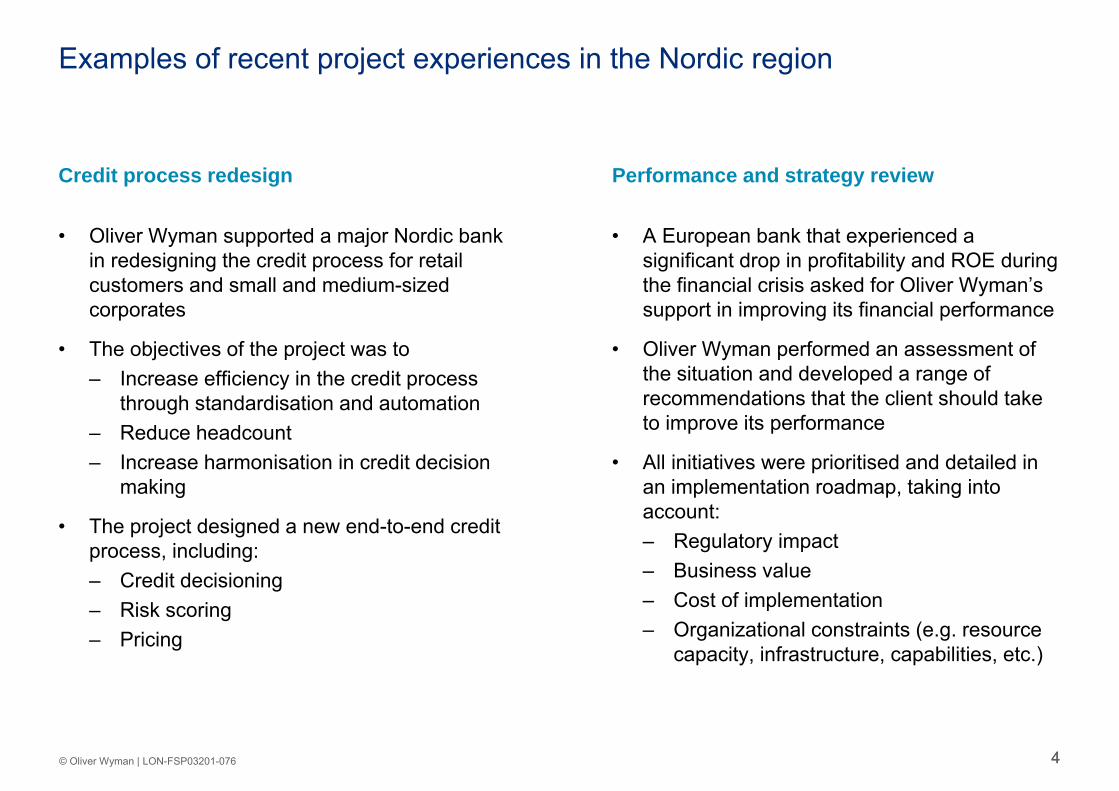

Examples of recent project experiences in the Nordic region

Credit process redesign Performance and strategy review

• Oliver Wyman supported a major Nordic bank in redesigning the credit process for retail customers and small and medium-sized corporates

• The objectives of the project was to – Increase efficiency in the credit process

through standardisation and automation– Reduce headcount– Increase harmonisation in credit decision

making

• The project designed a new end-to-end credit process, including:– Credit decisioning– Risk scoring– Pricing

• A European bank that experienced a significant drop in profitability and ROE during the financial crisis asked for Oliver Wyman’s support in improving its financial performance

• Oliver Wyman performed an assessment of the situation and developed a range of recommendations that the client should take to improve its performance

• All initiatives were prioritised and detailed in an implementation roadmap, taking into account:– Regulatory impact– Business value– Cost of implementation– Organizational constraints (e.g. resource

capacity, infrastructure, capabilities, etc.)

55© Oliver Wyman | LON-FSP03201-076

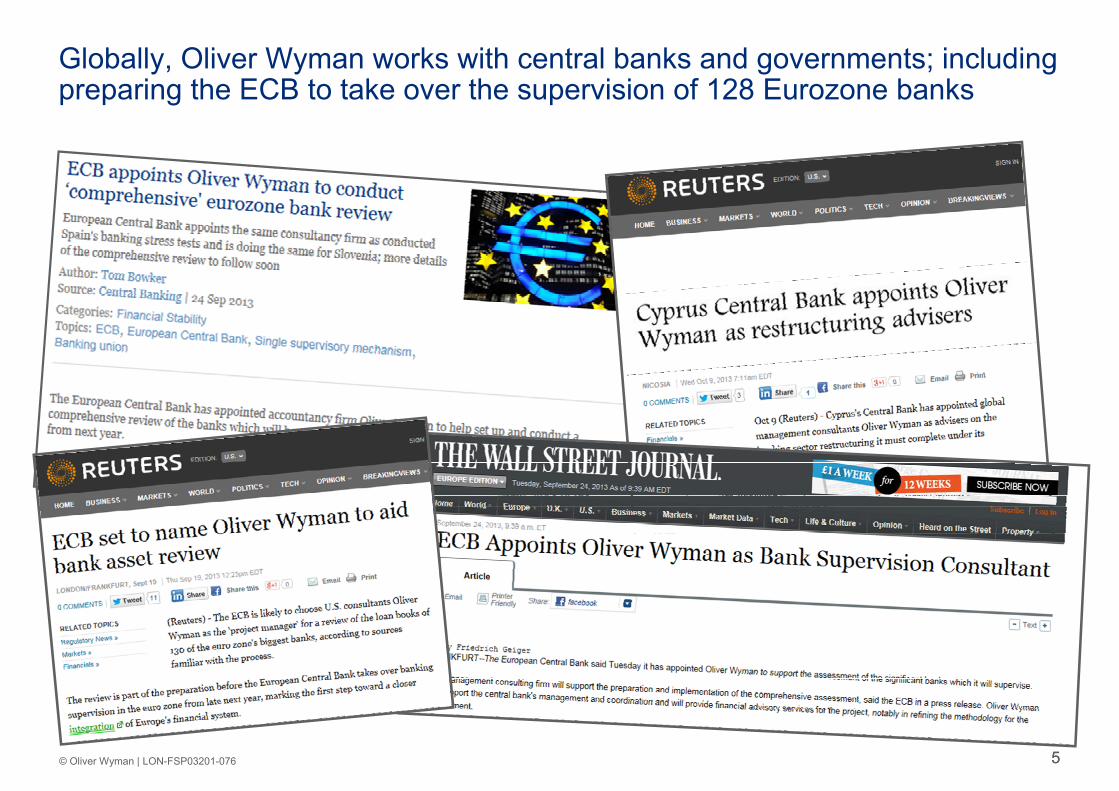

Globally, Oliver Wyman works with central banks and governments; including preparing the ECB to take over the supervision of 128 Eurozone banks

Case study – Deposit guarantee framework

Section 2

77© Oliver Wyman | LON-FSP03201-076

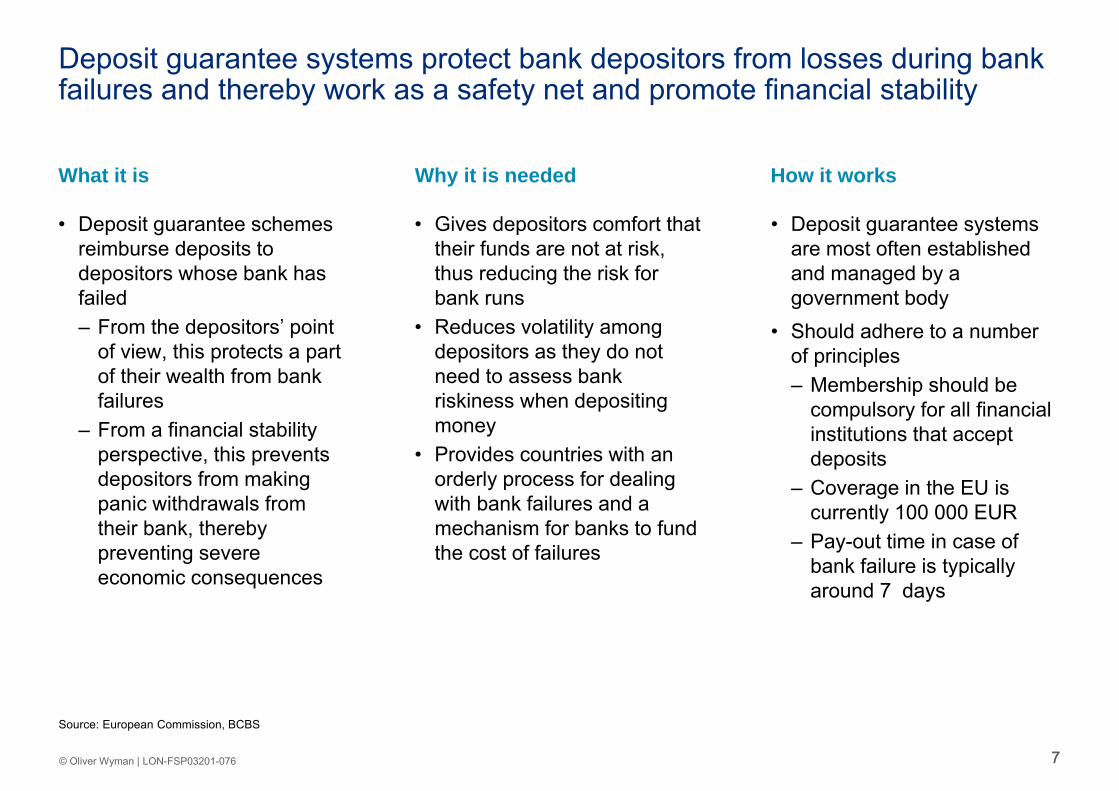

Deposit guarantee systems protect bank depositors from losses during bank failures and thereby work as a safety net and promote financial stability

• Deposit guarantee schemes reimburse deposits to depositors whose bank has failed– From the depositors’ point

of view, this protects a part of their wealth from bank failures

– From a financial stability perspective, this prevents depositors from making panic withdrawals from their bank, thereby preventing severe economic consequences

• Gives depositors comfort that their funds are not at risk, thus reducing the risk for bank runs

• Reduces volatility among depositors as they do not need to assess bank riskiness when depositing money

• Provides countries with an orderly process for dealing with bank failures and a mechanism for banks to fund the cost of failures

• Deposit guarantee systems are most often established and managed by a government body

• Should adhere to a number of principles– Membership should be

compulsory for all financial institutions that accept deposits

– Coverage in the EU is currently 100 000 EUR

– Pay-out time in case of bank failure is typically around 7 days

What it is How it worksWhy it is needed

Source: European Commission, BCBS

88© Oliver Wyman | LON-FSP03201-076

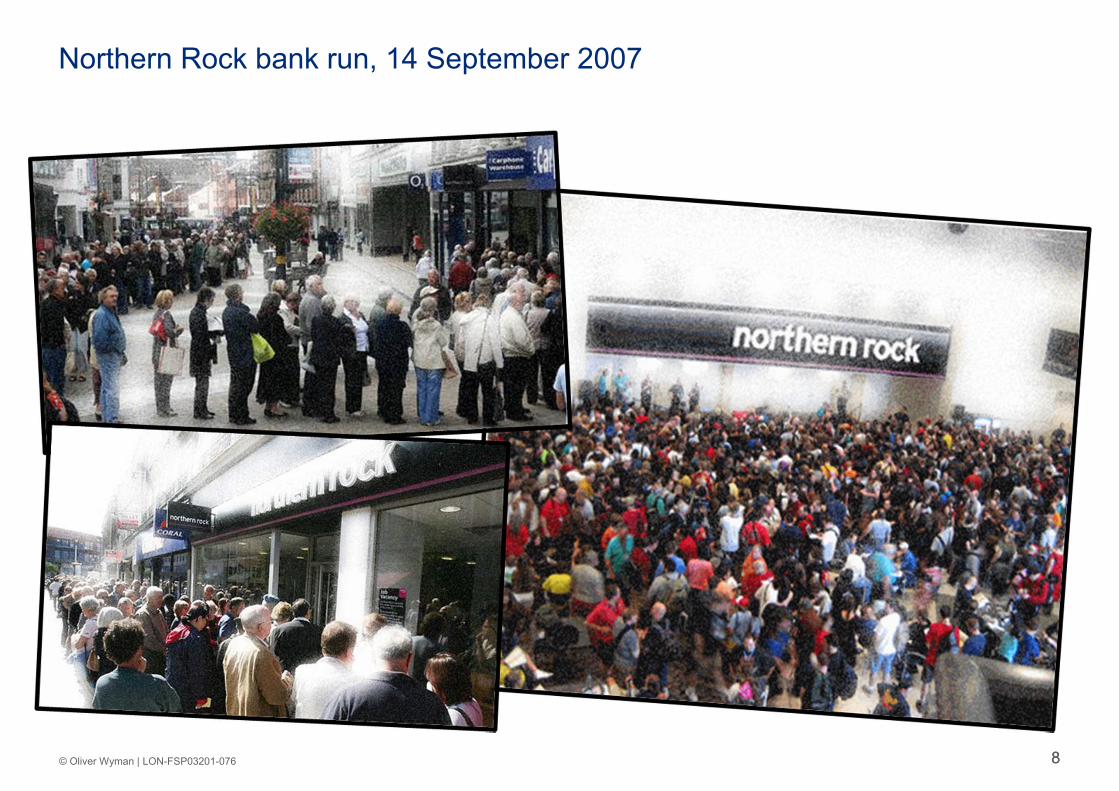

Northern Rock bank run, 14 September 2007

99© Oliver Wyman | LON-FSP03201-076

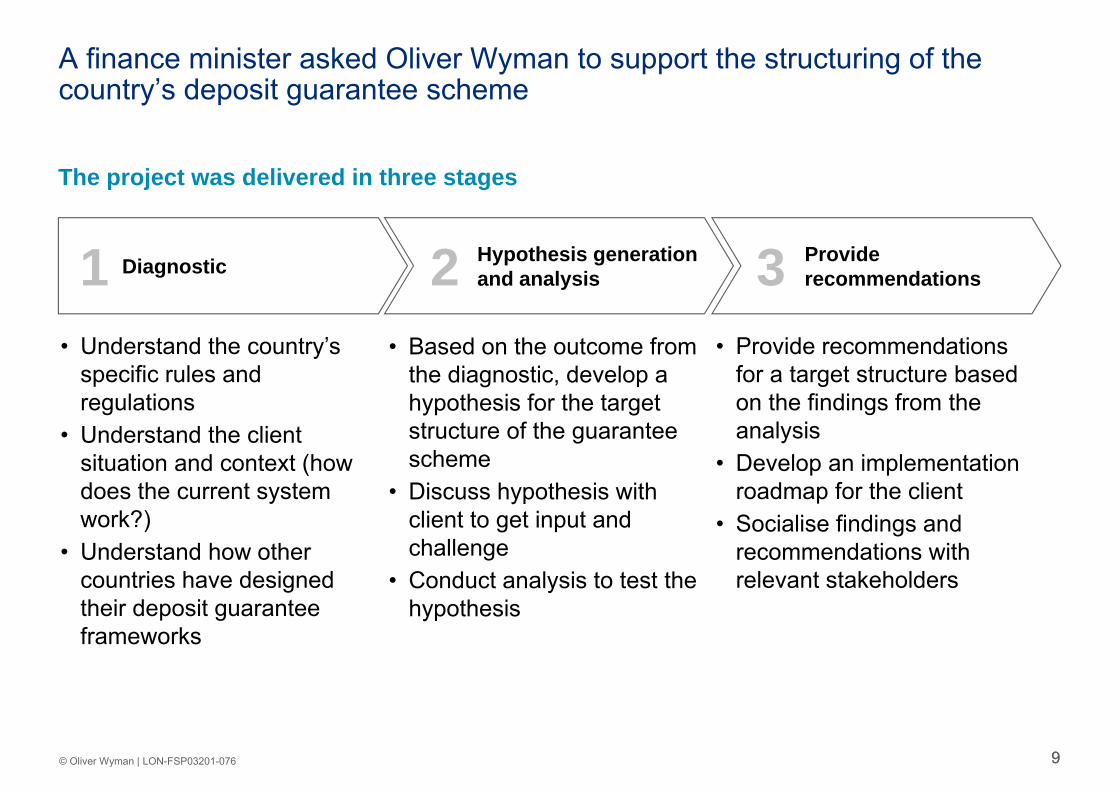

A finance minister asked Oliver Wyman to support the structuring of the country’s deposit guarantee scheme

• Understand the country’s specific rules and regulations

• Understand the client situation and context (how does the current system work?)

• Understand how other countries have designed their deposit guarantee frameworks

• Based on the outcome from the diagnostic, develop a hypothesis for the target structure of the guarantee scheme

• Discuss hypothesis with client to get input and challenge

• Conduct analysis to test the hypothesis

Provide recommendations

Hypothesis generation and analysisDiagnostic1 2 3

• Provide recommendations for a target structure based on the findings from the analysis

• Develop an implementation roadmap for the client

• Socialise findings and recommendations with relevant stakeholders

The project was delivered in three stages

10© Oliver Wyman | LON-FSP03201-076 10

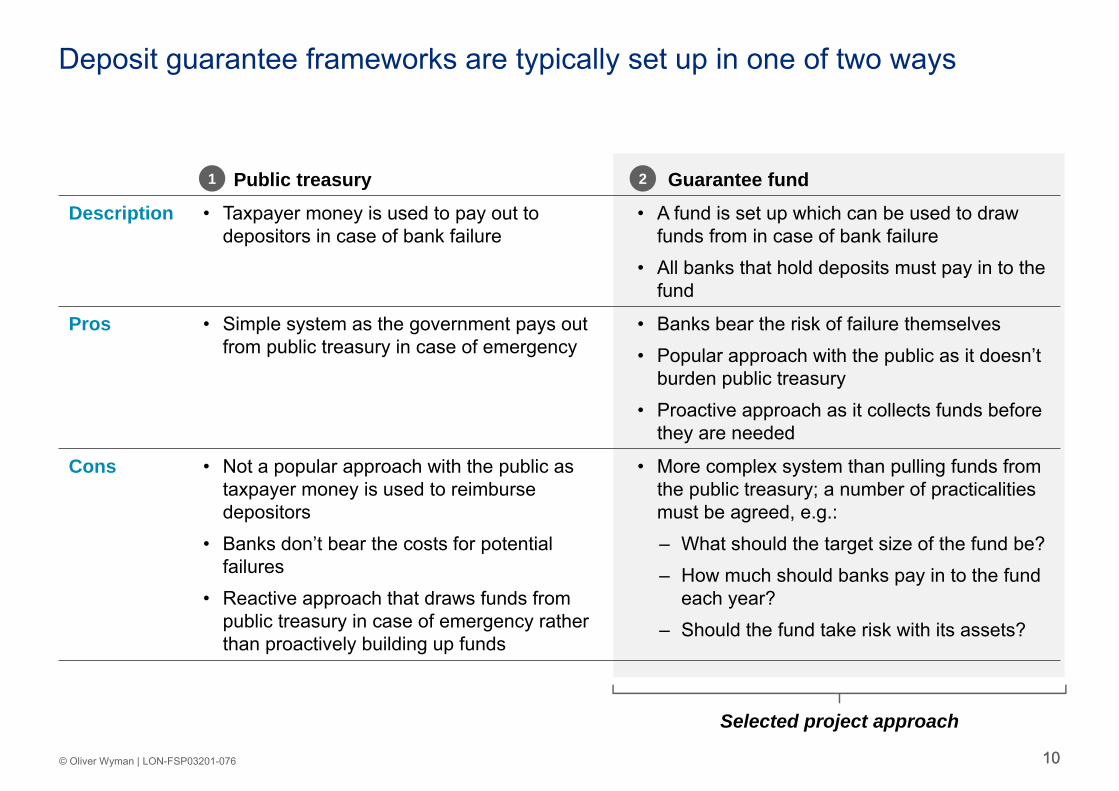

Deposit guarantee frameworks are typically set up in one of two ways

Public treasury Guarantee fund

Description • Taxpayer money is used to pay out to depositors in case of bank failure

• A fund is set up which can be used to draw funds from in case of bank failure

• All banks that hold deposits must pay in to the fund

Pros • Simple system as the government pays out from public treasury in case of emergency

• Banks bear the risk of failure themselves• Popular approach with the public as it doesn’t

burden public treasury• Proactive approach as it collects funds before

they are needed

Cons • Not a popular approach with the public as taxpayer money is used to reimburse depositors

• Banks don’t bear the costs for potential failures

• Reactive approach that draws funds from public treasury in case of emergency rather than proactively building up funds

• More complex system than pulling funds from the public treasury; a number of practicalitiesmust be agreed, e.g.:– What should the target size of the fund be?– How much should banks pay in to the fund

each year?– Should the fund take risk with its assets?

1 2

Selected project approach

11© Oliver Wyman | LON-FSP03201-076 11

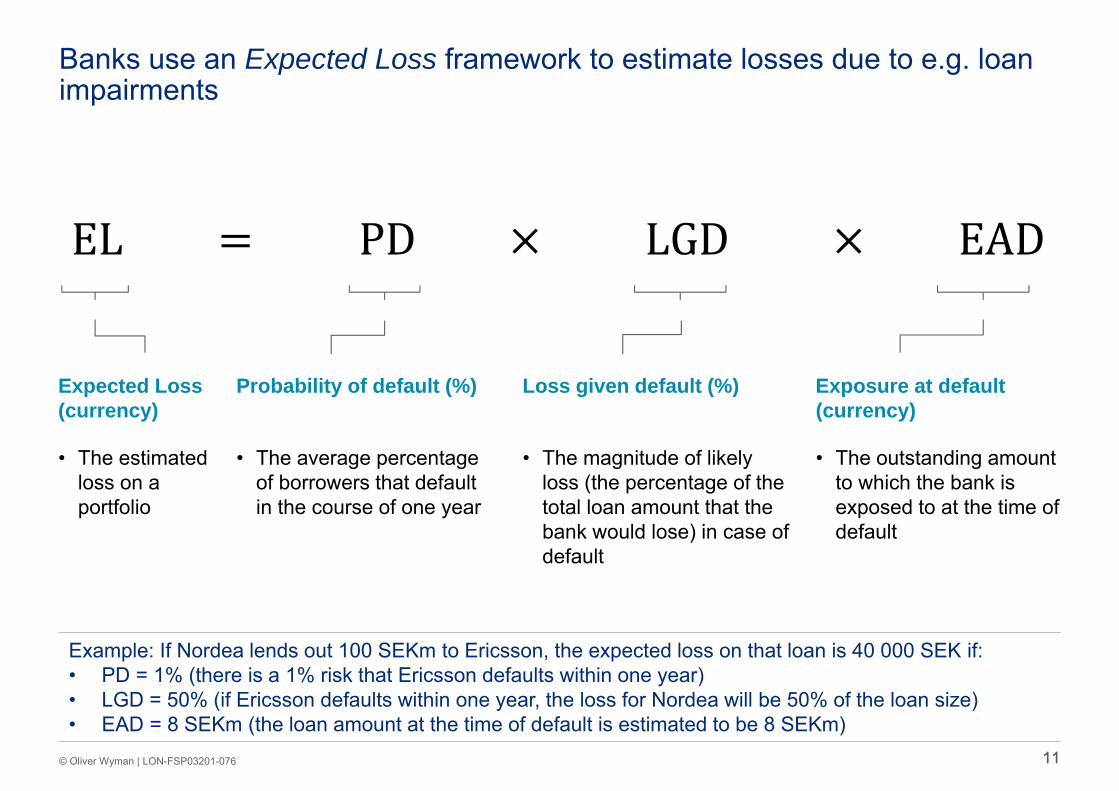

Banks use an Expected Loss framework to estimate losses due to e.g. loan impairments

• The estimated loss on a portfolio

• The average percentage of borrowers that default in the course of one year

• The magnitude of likely loss (the percentage of the total loan amount that the bank would lose) in case of default

• The outstanding amount to which the bank is exposed to at the time of default

Expected Loss (currency)

Probability of default (%) Loss given default (%) Exposure at default (currency)

Example: If Nordea lends out 100 SEKm to Ericsson, the expected loss on that loan is 40 000 SEK if:• PD = 1% (there is a 1% risk that Ericsson defaults within one year)• LGD = 50% (if Ericsson defaults within one year, the loss for Nordea will be 50% of the loan size)• EAD = 8 SEKm (the loan amount at the time of default is estimated to be 8 SEKm)

12© Oliver Wyman | LON-FSP03201-076 12

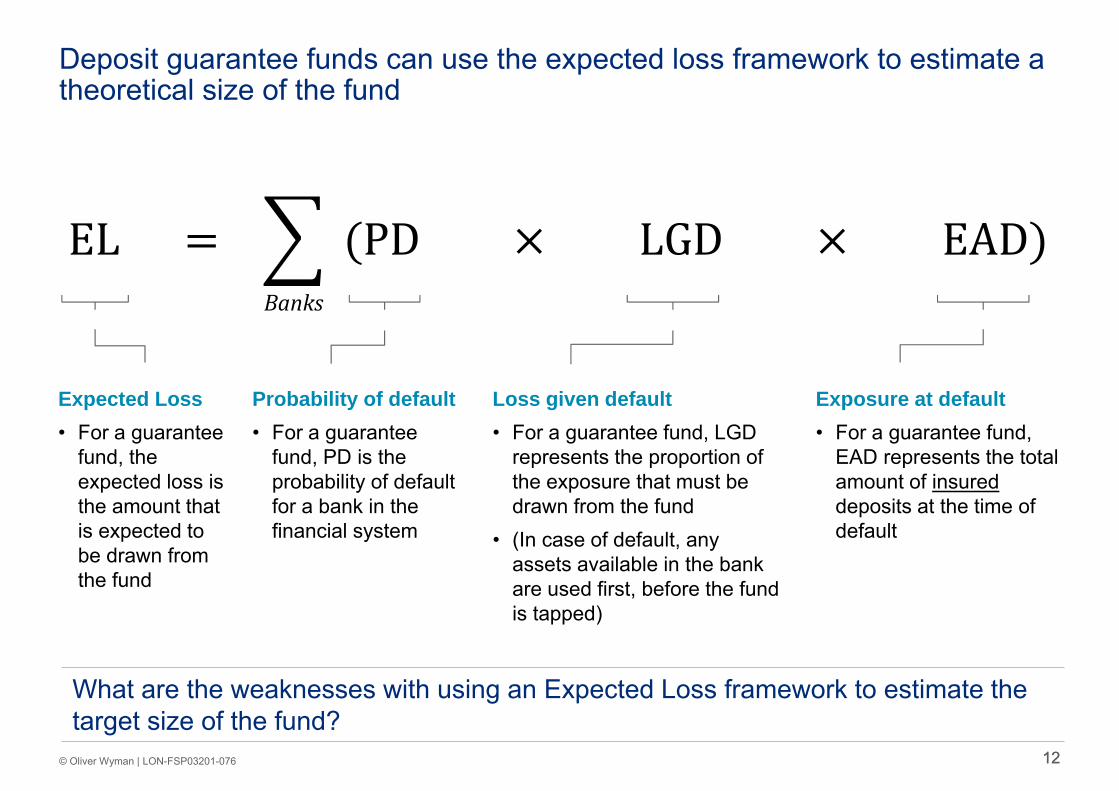

Deposit guarantee funds can use the expected loss framework to estimate a theoretical size of the fund

Expected Loss• For a guarantee

fund, the expected loss is the amount that is expected to be drawn from the fund

Probability of default• For a guarantee

fund, PD is the probability of default for a bank in the financial system

Loss given default• For a guarantee fund, LGD

represents the proportion of the exposure that must be drawn from the fund

• (In case of default, any assets available in the bank are used first, before the fund is tapped)

Exposure at default• For a guarantee fund,

EAD represents the total amount of insureddeposits at the time of default

Banks

What are the weaknesses with using an Expected Loss framework to estimate the target size of the fund?

1313© Oliver Wyman | LON-FSP03201-076

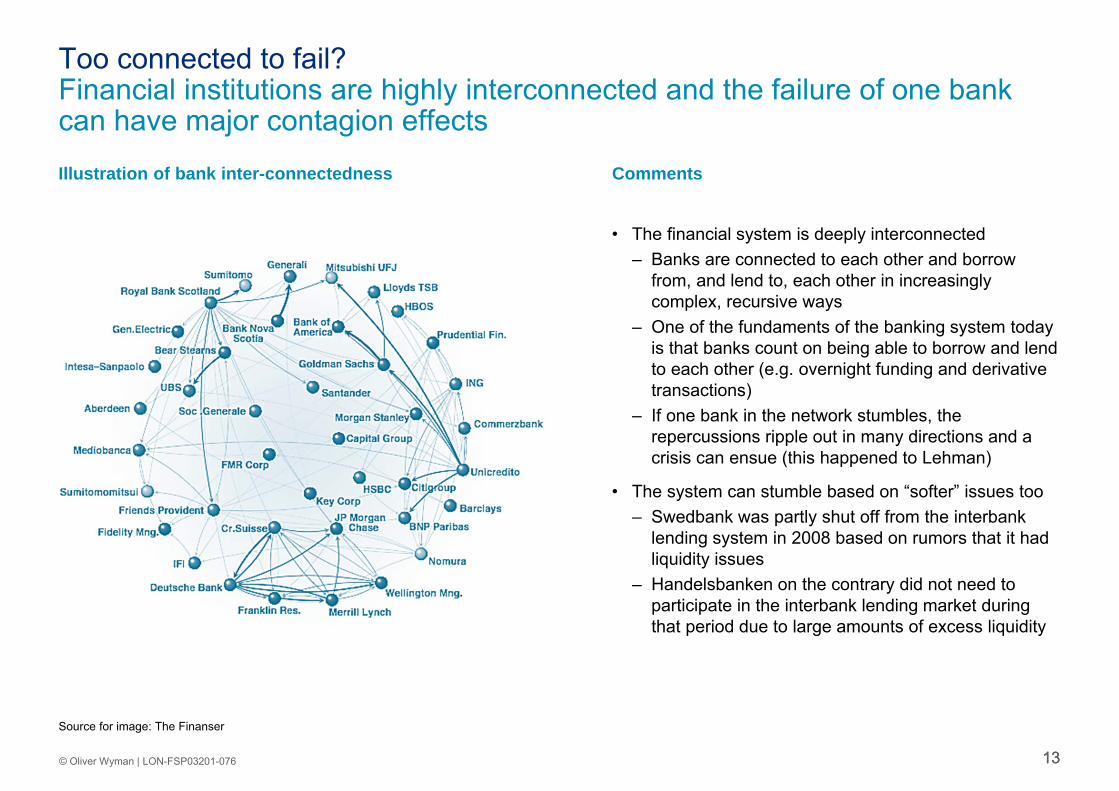

Too connected to fail?Financial institutions are highly interconnected and the failure of one bank can have major contagion effects

Illustration of bank inter-connectedness Comments

• The financial system is deeply interconnected– Banks are connected to each other and borrow

from, and lend to, each other in increasingly complex, recursive ways

– One of the fundaments of the banking system today is that banks count on being able to borrow and lend to each other (e.g. overnight funding and derivative transactions)

– If one bank in the network stumbles, the repercussions ripple out in many directions and a crisis can ensue (this happened to Lehman)

• The system can stumble based on “softer” issues too– Swedbank was partly shut off from the interbank

lending system in 2008 based on rumors that it had liquidity issues

– Handelsbanken on the contrary did not need to participate in the interbank lending market during that period due to large amounts of excess liquidity

Source for image: The Finanser

1414© Oliver Wyman | LON-FSP03201-076

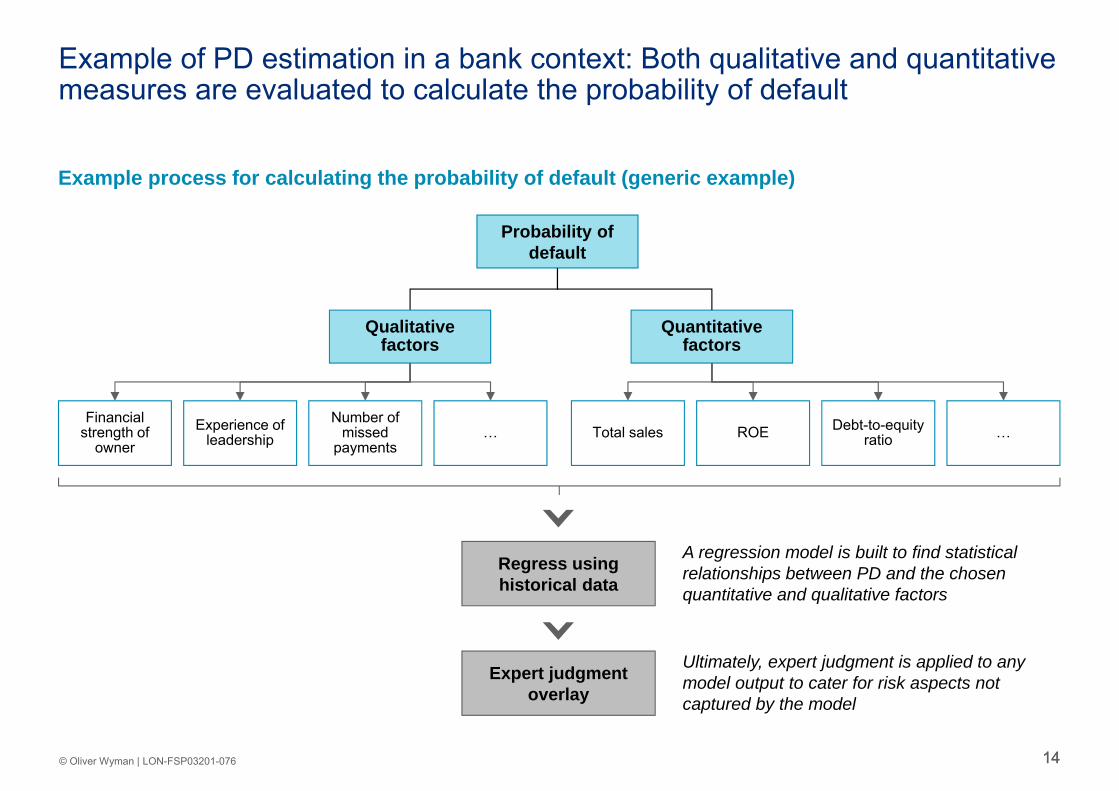

Example of PD estimation in a bank context: Both qualitative and quantitative measures are evaluated to calculate the probability of default

Example process for calculating the probability of default (generic example)

Probability of default

Qualitative factors

ROE

Quantitative factors

…Total salesNumber of

missed payments

Experience of leadership

Financial strength of

owner

Regress using historical data

Expert judgment overlay

A regression model is built to find statistical relationships between PD and the chosen quantitative and qualitative factors

Ultimately, expert judgment is applied to any model output to cater for risk aspects not captured by the model

… Debt-to-equity ratio

15© Oliver Wyman | LON-FSP03201-076 15

Probability of default is inherently difficult to estimate in practice as it is a measure of a potential future event

• Some of the problems with estimating PD are:– Most estimates are based on historical experiences, which may or may not be representative

of the future– There are correlation effects that are difficult to assess– Models may be overly simplistic and make crude assumptions of reality– Available information regarding the borrower or institution is not always available, correct or

sufficiently detailed– Etc.

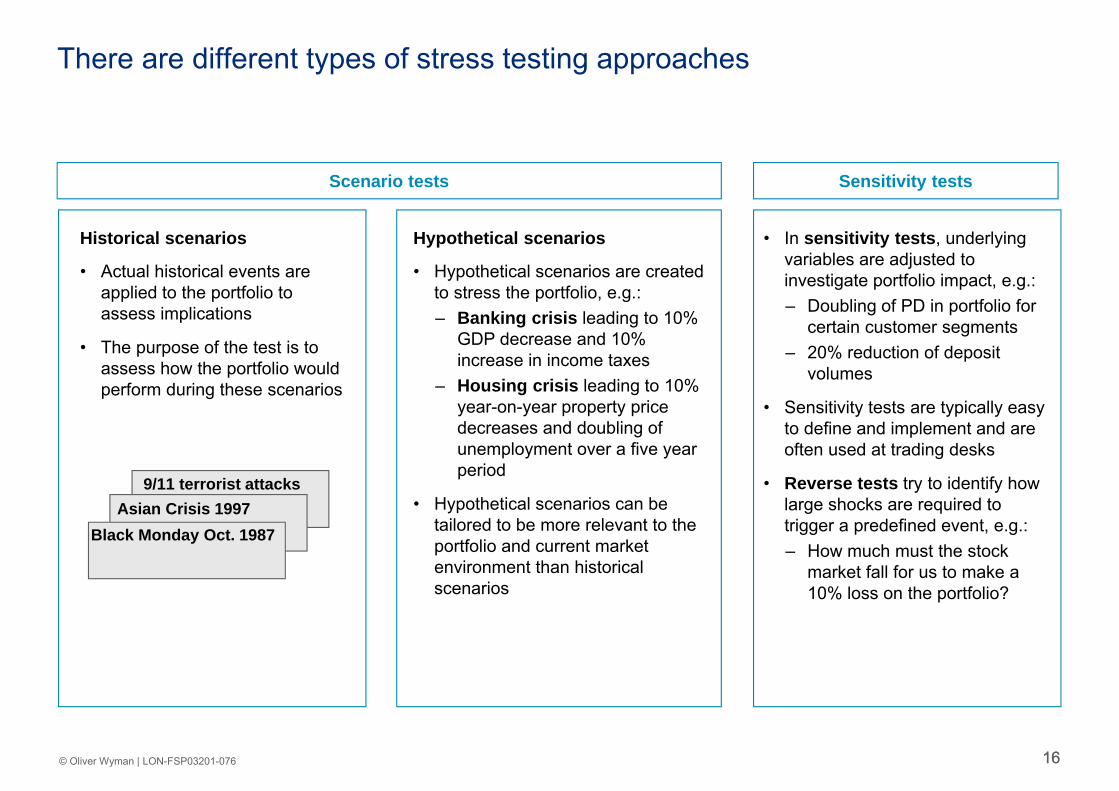

Due to these reasons, many institutions complement their PD models with stress testing, e.g.:• Scenario analysis• Sensitivity test of input parameters

1616© Oliver Wyman | LON-FSP03201-076

Hypothetical scenarios

• Hypothetical scenarios are created to stress the portfolio, e.g.:– Banking crisis leading to 10%

GDP decrease and 10% increase in income taxes

– Housing crisis leading to 10% year-on-year property price decreases and doubling of unemployment over a five year period

• Hypothetical scenarios can be tailored to be more relevant to the portfolio and current market environment than historical scenarios

• In sensitivity tests, underlying variables are adjusted to investigate portfolio impact, e.g.:– Doubling of PD in portfolio for

certain customer segments– 20% reduction of deposit

volumes

• Sensitivity tests are typically easy to define and implement and are often used at trading desks

• Reverse tests try to identify how large shocks are required to trigger a predefined event, e.g.:– How much must the stock

market fall for us to make a 10% loss on the portfolio?

Historical scenarios

• Actual historical events are applied to the portfolio to assess implications

• The purpose of the test is to assess how the portfolio would perform during these scenarios

Scenario tests

Black Monday Oct. 1987Asian Crisis 1997

9/11 terrorist attacks

There are different types of stress testing approaches

Sensitivity tests

1717© Oliver Wyman | LON-FSP03201-076

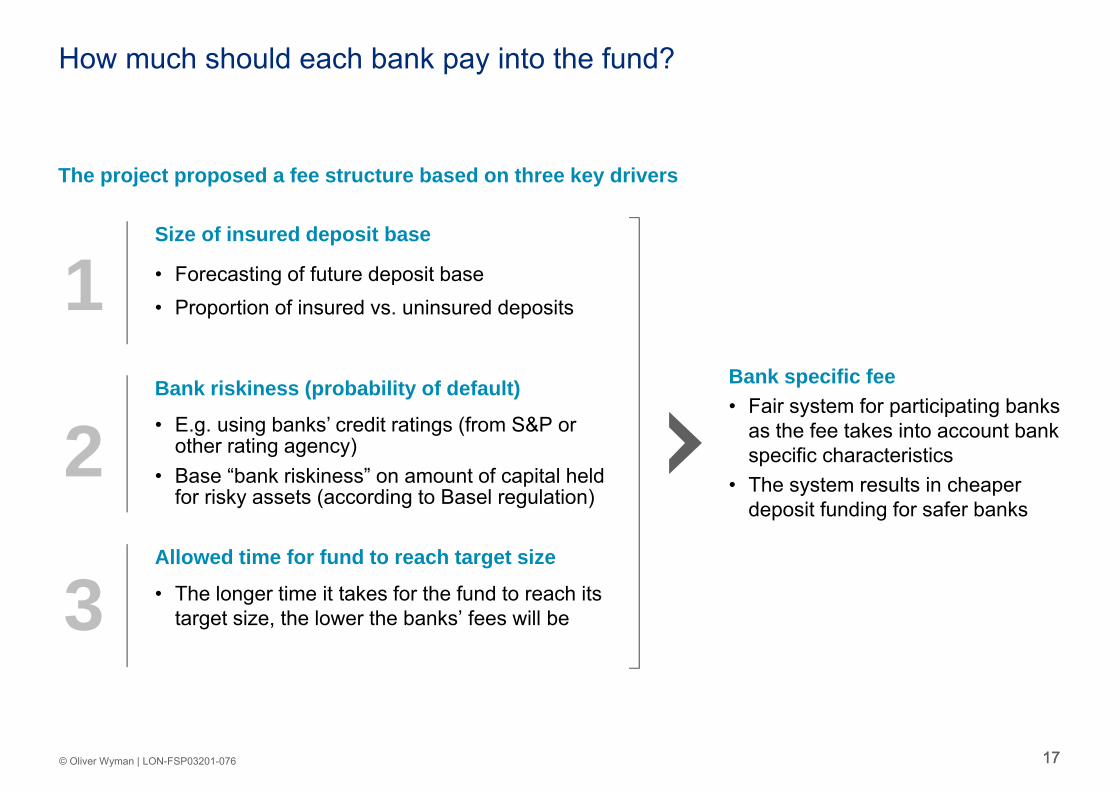

How much should each bank pay into the fund?

Bank specific fee• Fair system for participating banks

as the fee takes into account bank specific characteristics

• The system results in cheaper deposit funding for safer banks

Size of insured deposit base

• Forecasting of future deposit base• Proportion of insured vs. uninsured deposits1

The project proposed a fee structure based on three key drivers

Allowed time for fund to reach target size

• The longer time it takes for the fund to reach its target size, the lower the banks’ fees will be3

Bank riskiness (probability of default)

• E.g. using banks’ credit ratings (from S&P or other rating agency)

• Base “bank riskiness” on amount of capital held for risky assets (according to Basel regulation)

2

1818© Oliver Wyman | LON-FSP03201-076

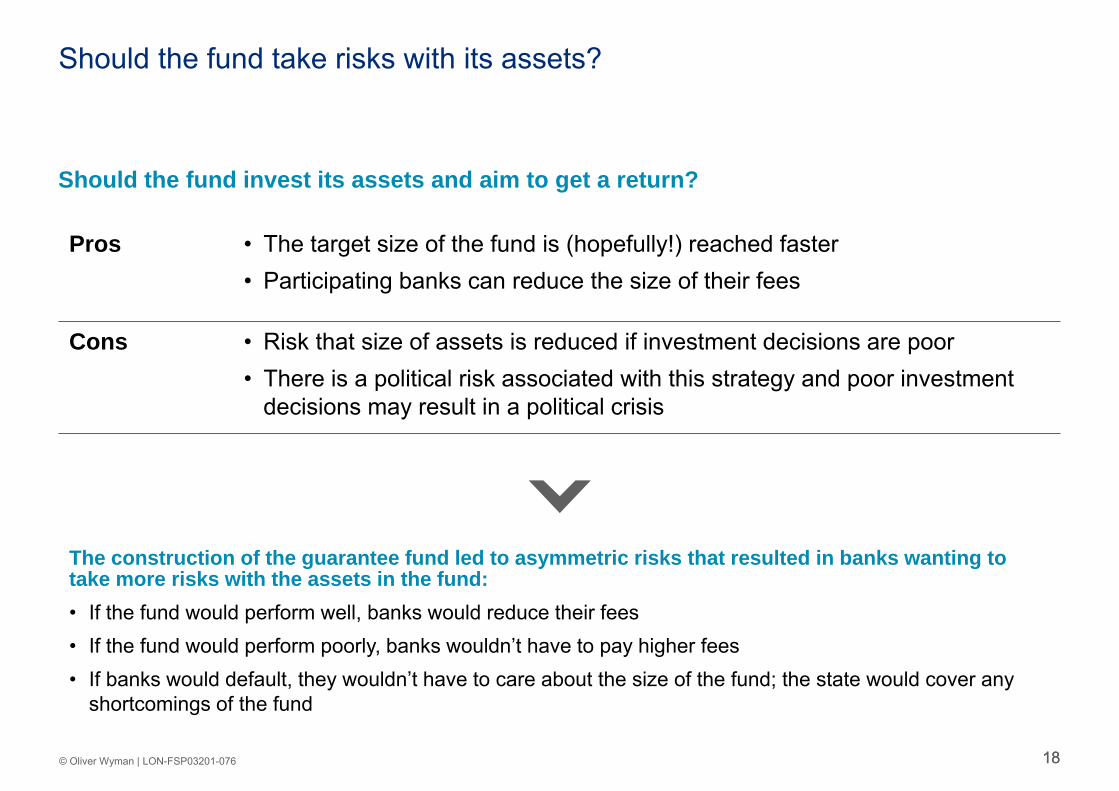

Should the fund take risks with its assets?

Pros • The target size of the fund is (hopefully!) reached faster• Participating banks can reduce the size of their fees

Cons • Risk that size of assets is reduced if investment decisions are poor• There is a political risk associated with this strategy and poor investment

decisions may result in a political crisis

The construction of the guarantee fund led to asymmetric risks that resulted in banks wanting to take more risks with the assets in the fund:• If the fund would perform well, banks would reduce their fees• If the fund would perform poorly, banks wouldn’t have to pay higher fees• If banks would default, they wouldn’t have to care about the size of the fund; the state would cover any

shortcomings of the fund

Should the fund invest its assets and aim to get a return?

1919© Oliver Wyman | LON-FSP03201-076

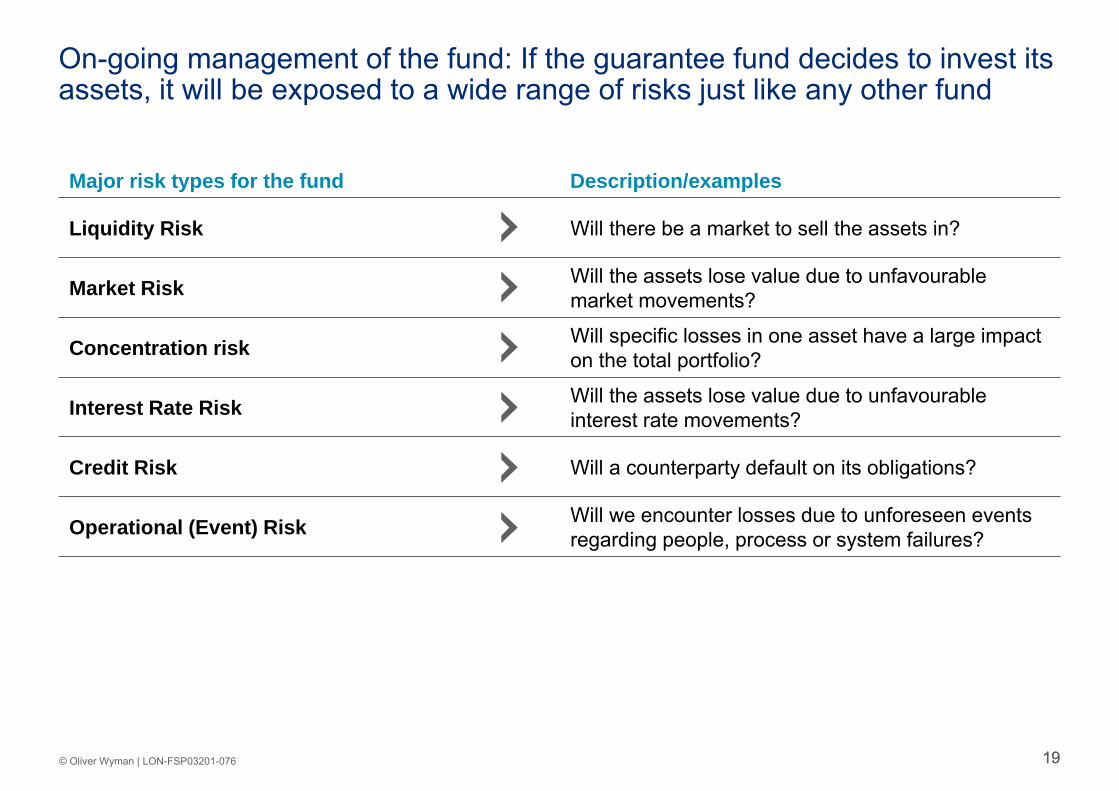

On-going management of the fund: If the guarantee fund decides to invest its assets, it will be exposed to a wide range of risks just like any other fund

Major risk types for the fund Description/examples

Liquidity Risk Will there be a market to sell the assets in?

Market Risk Will the assets lose value due to unfavourable market movements?

Concentration risk Will specific losses in one asset have a large impact on the total portfolio?

Interest Rate Risk Will the assets lose value due to unfavourable interest rate movements?

Credit Risk Will a counterparty default on its obligations?

Operational (Event) Risk Will we encounter losses due to unforeseen events regarding people, process or system failures?

20© Oliver Wyman | LON-FSP03201-076 20

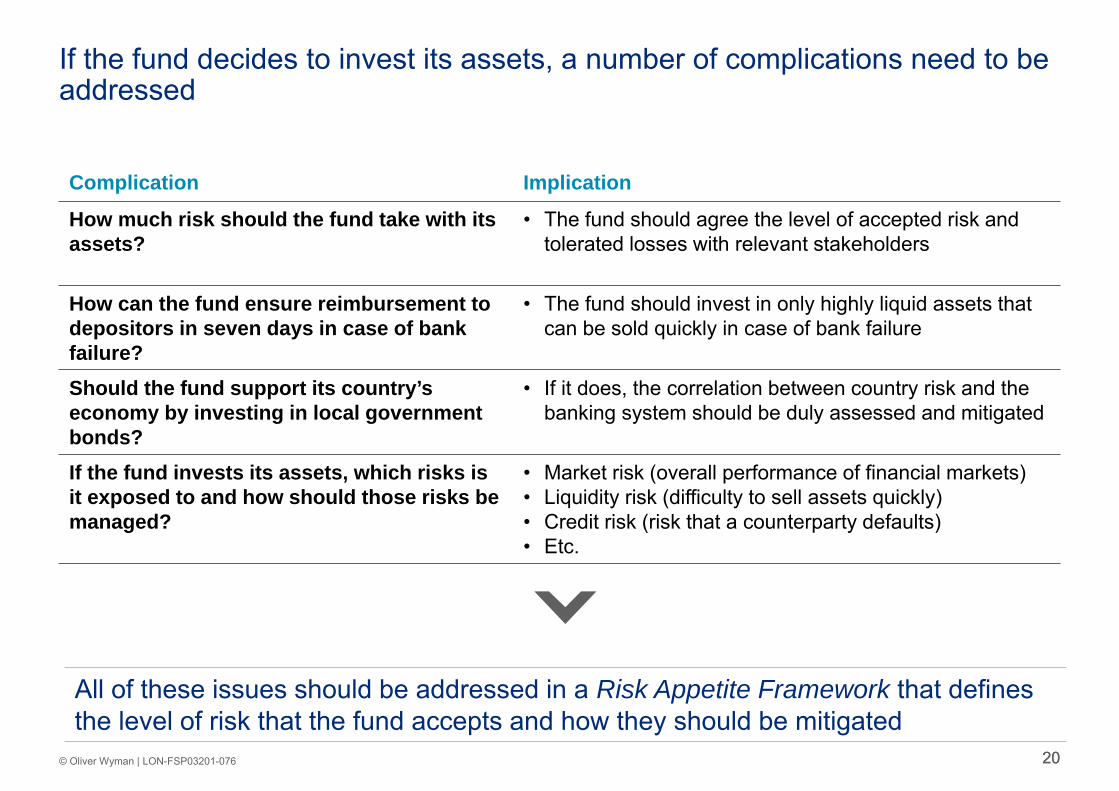

If the fund decides to invest its assets, a number of complications need to be addressed

Complication Implication

How much risk should the fund take with its assets?

• The fund should agree the level of accepted risk and tolerated losses with relevant stakeholders

How can the fund ensure reimbursement to depositors in seven days in case of bank failure?

• The fund should invest in only highly liquid assets that can be sold quickly in case of bank failure

Should the fund support its country’s economy by investing in local government bonds?

• If it does, the correlation between country risk and the banking system should be duly assessed and mitigated

If the fund invests its assets, which risks is it exposed to and how should those risks be managed?

• Market risk (overall performance of financial markets)• Liquidity risk (difficulty to sell assets quickly)• Credit risk (risk that a counterparty defaults)• Etc.

All of these issues should be addressed in a Risk Appetite Framework that defines the level of risk that the fund accepts and how they should be mitigated

21© Oliver Wyman | LON-FSP03201-076 21

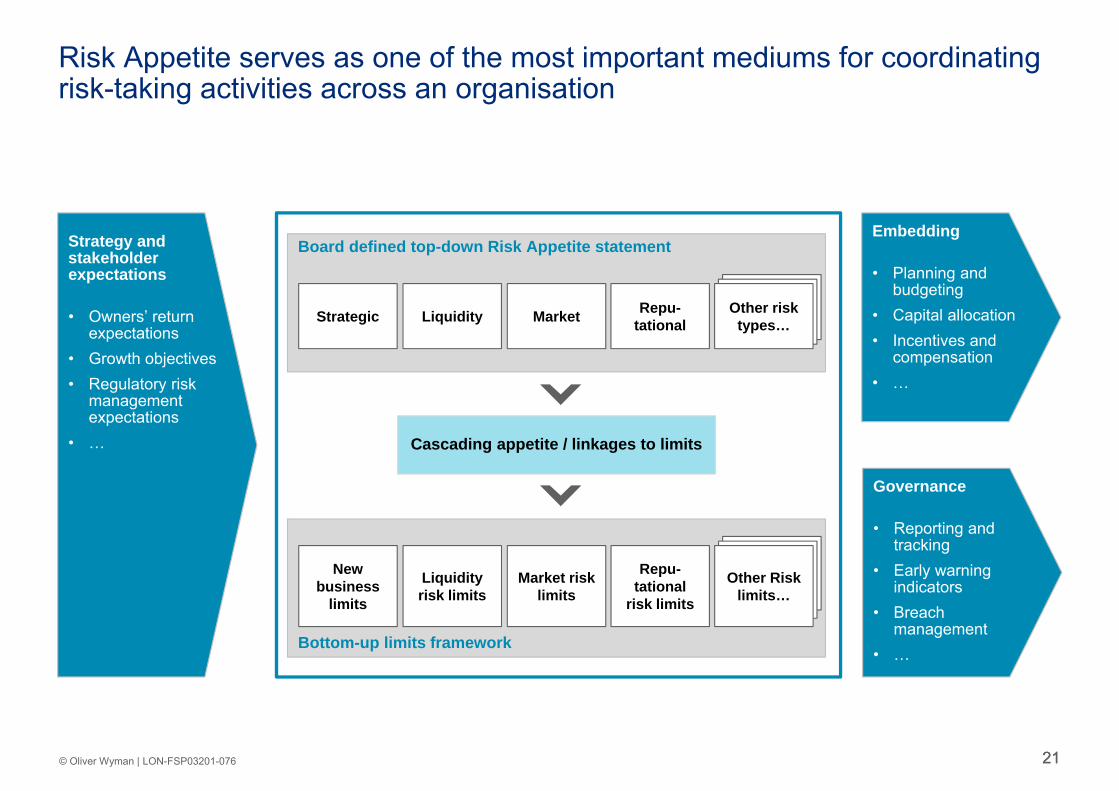

Board defined top-down Risk Appetite statement

CreditCredit

Risk Appetite serves as one of the most important mediums for coordinating risk-taking activities across an organisation

Cascading appetite / linkages to limits

Strategy and stakeholder expectations

• Owners’ return expectations

• Growth objectives• Regulatory risk

management expectations

• …

Strategic Liquidity Market Other risk types…

Repu-tational

Bottom-up limits framework

CreditCreditNew

business limits

Liquidity risk limits

Market risk limits

Other Risk limits…

Repu-tational

risk limits

Embedding

• Planning and budgeting

• Capital allocation• Incentives and

compensation• …

Governance

• Reporting and tracking

• Early warning indicators

• Breach management

• …

2222© Oliver Wyman | LON-FSP03201-076

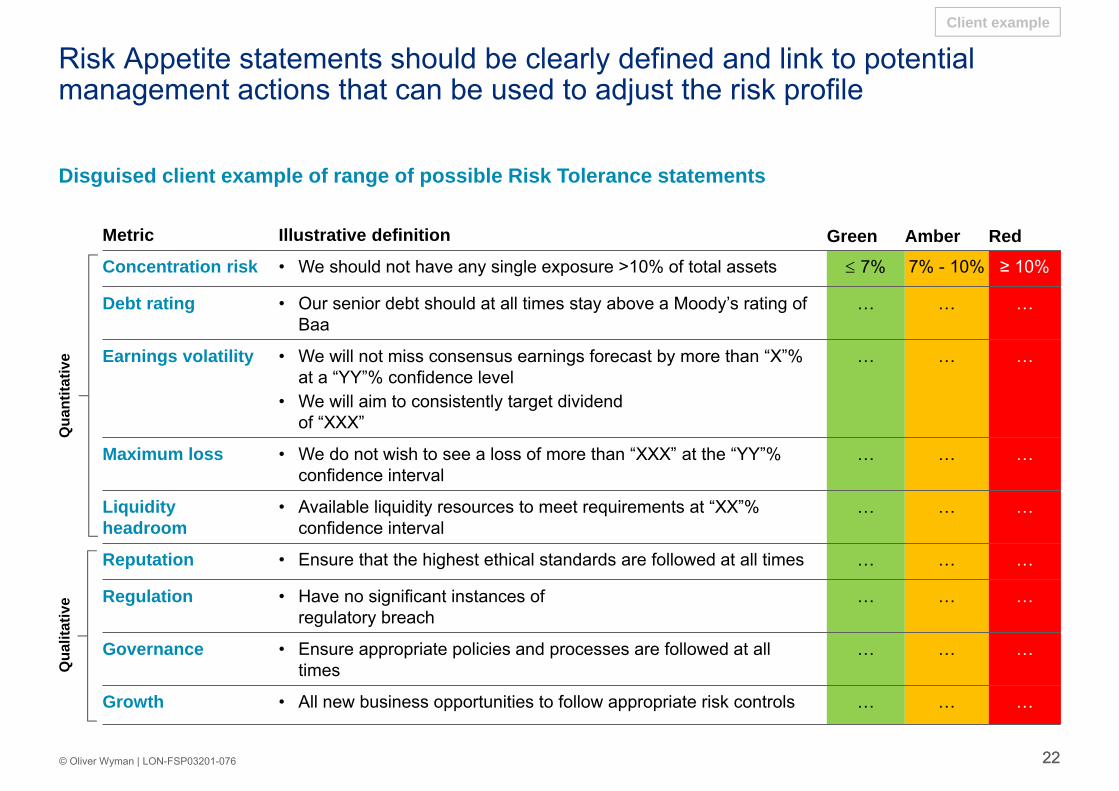

Risk Appetite statements should be clearly defined and link to potential management actions that can be used to adjust the risk profile

Metric Illustrative definition Green Amber RedConcentration risk • We should not have any single exposure >10% of total assets 7% 7% - 10% ≥ 10%

Debt rating • Our senior debt should at all times stay above a Moody’s rating of Baa

… … …

Earnings volatility • We will not miss consensus earnings forecast by more than “X”% at a “YY”% confidence level

• We will aim to consistently target dividend of “XXX”

… … …

Maximum loss • We do not wish to see a loss of more than “XXX” at the “YY”% confidence interval

… … …

Liquidity headroom

• Available liquidity resources to meet requirements at “XX”% confidence interval

… … …

Reputation • Ensure that the highest ethical standards are followed at all times … … …

Regulation • Have no significant instances of regulatory breach

… … …

Governance • Ensure appropriate policies and processes are followed at all times

… … …

Growth • All new business opportunities to follow appropriate risk controls … … …

Qua

ntita

tive

Qua

litat

ive

Client example

Disguised client example of range of possible Risk Tolerance statements

2323© Oliver Wyman | LON-FSP03201-076

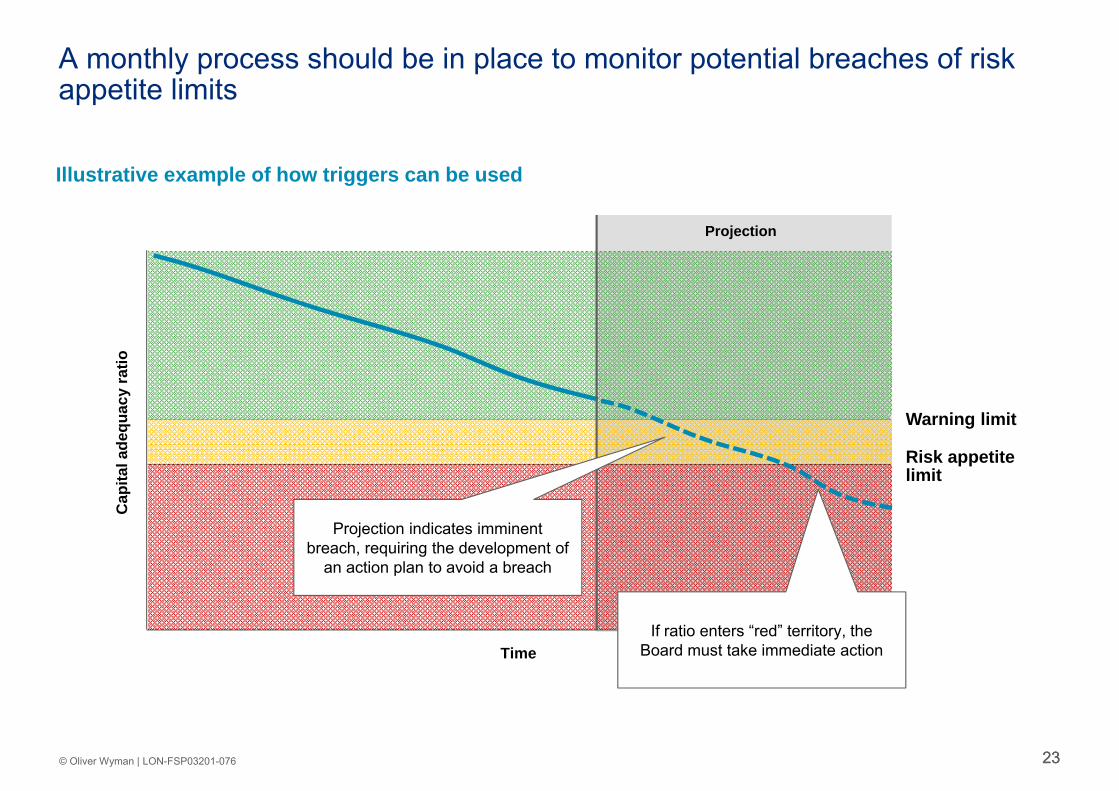

A monthly process should be in place to monitor potential breaches of risk appetite limits

Illustrative example of how triggers can be used

Warning limit

Risk appetite limit

Cap

ital a

dequ

acy

ratio

Time

Projection

Projection indicates imminent breach, requiring the development of

an action plan to avoid a breach

If ratio enters “red” territory, the Board must take immediate action

Black swan eventsAppendix

2525© Oliver Wyman | LON-FSP03201-076

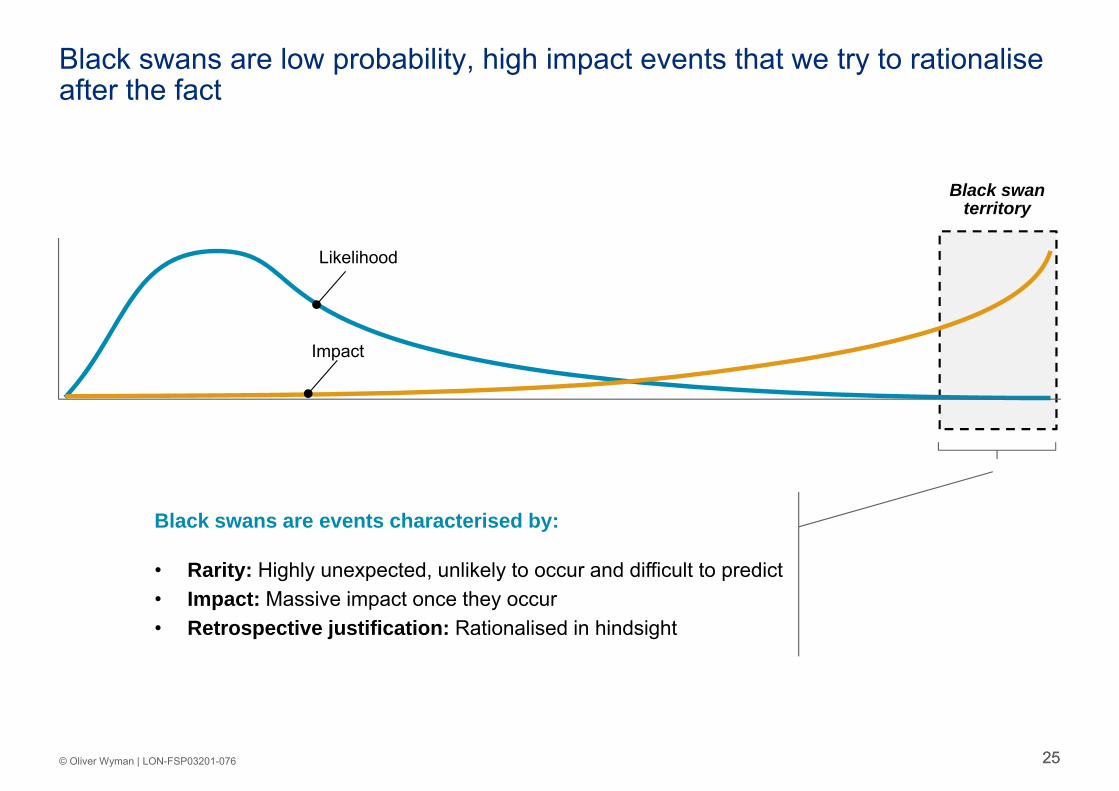

Black swan territory

Black swans are low probability, high impact events that we try to rationalise after the fact

Black swans are events characterised by:

• Rarity: Highly unexpected, unlikely to occur and difficult to predict• Impact: Massive impact once they occur• Retrospective justification: Rationalised in hindsight

Likelihood

Impact

26© Oliver Wyman | LON-FSP03201-076 26

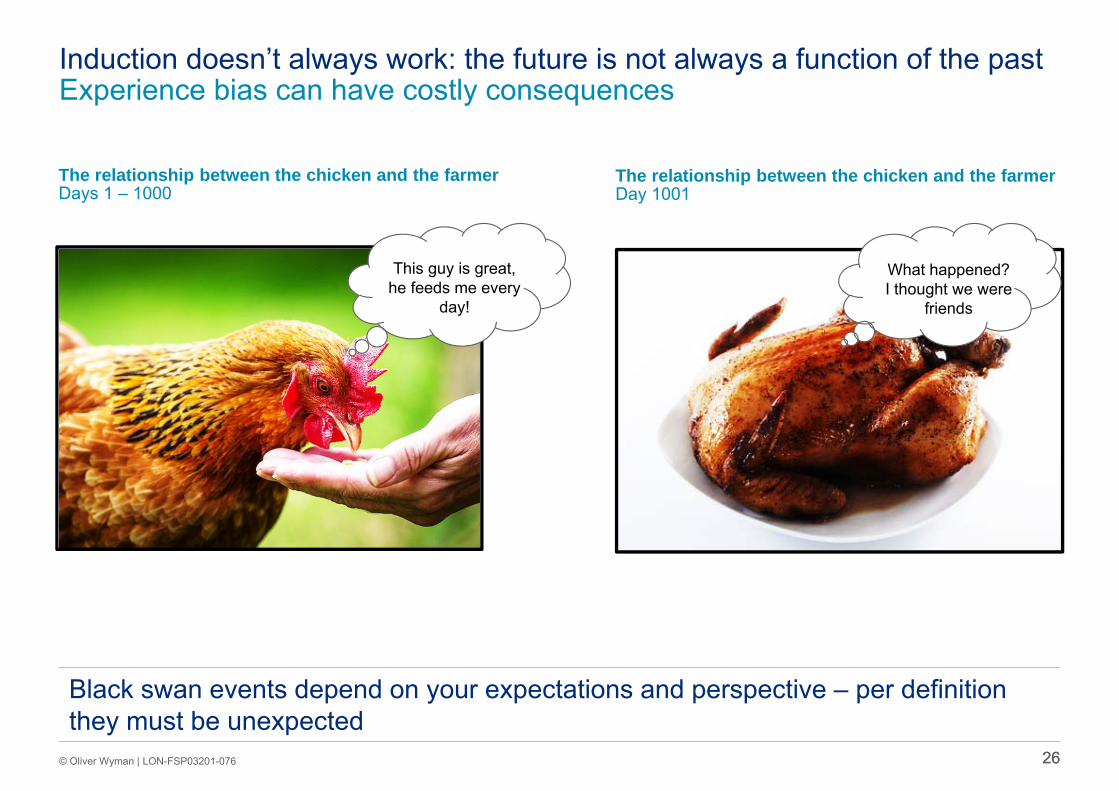

Induction doesn’t always work: the future is not always a function of the pastExperience bias can have costly consequences

The relationship between the chicken and the farmerDays 1 – 1000

This guy is great, he feeds me every

day!

What happened?I thought we were

friends

Black swan events depend on your expectations and perspective – per definition they must be unexpected

The relationship between the chicken and the farmerDay 1001

27© Oliver Wyman | LON-FSP03201-076 27

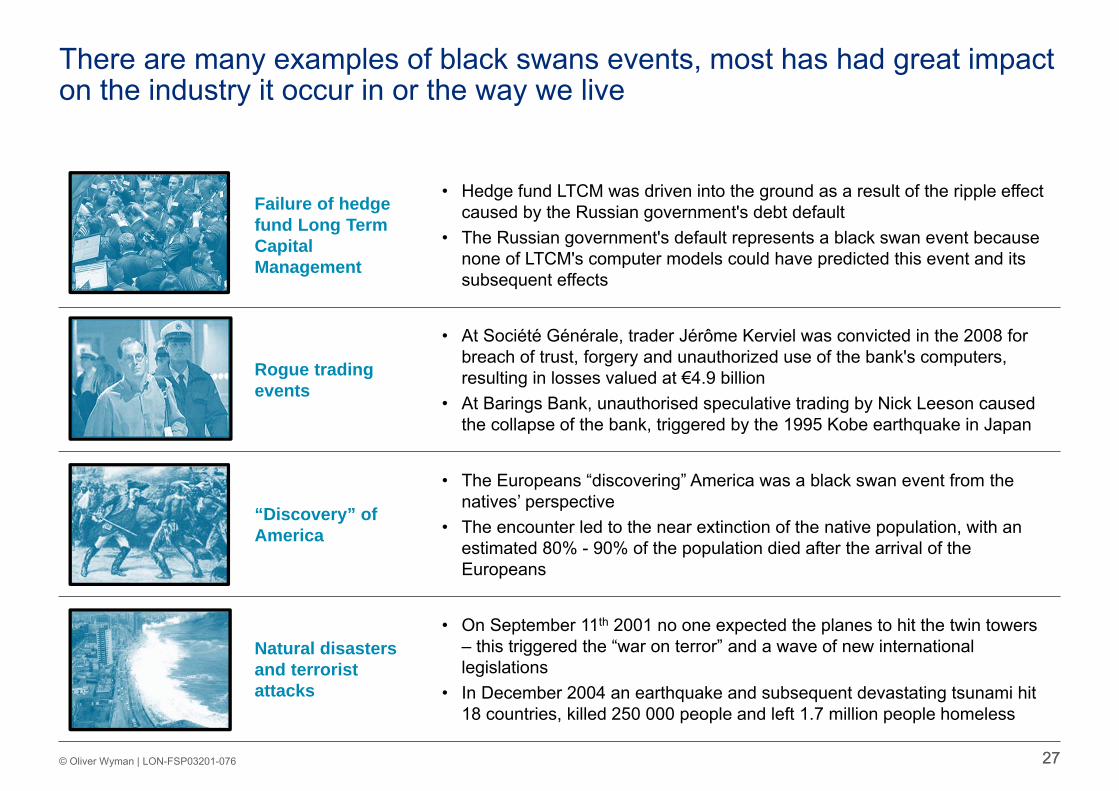

There are many examples of black swans events, most has had great impact on the industry it occur in or the way we live

Failure of hedge fund Long Term Capital Management

• Hedge fund LTCM was driven into the ground as a result of the ripple effect caused by the Russian government's debt default

• The Russian government's default represents a black swan event because none of LTCM's computer models could have predicted this event and its subsequent effects

Rogue tradingevents

• At Société Générale, trader Jérôme Kerviel was convicted in the 2008 for breach of trust, forgery and unauthorized use of the bank's computers, resulting in losses valued at €4.9 billion

• At Barings Bank, unauthorised speculative trading by Nick Leeson caused the collapse of the bank, triggered by the 1995 Kobe earthquake in Japan

“Discovery” of America

• The Europeans “discovering” America was a black swan event from the natives’ perspective

• The encounter led to the near extinction of the native population, with an estimated 80% - 90% of the population died after the arrival of the Europeans

Natural disastersand terrorist attacks

• On September 11th 2001 no one expected the planes to hit the twin towers – this triggered the “war on terror” and a wave of new international legislations

• In December 2004 an earthquake and subsequent devastating tsunami hit 18 countries, killed 250 000 people and left 1.7 million people homeless

2828© Oliver Wyman | LON-FSP03201-076

Setting up identification and control processes for black swan events is difficult, but an institution’s general preparedness can often be improved

• If black swan events are so difficult to identify, should we even try to set up controls in order to mitigate them?– Even if it was possible to

identify all possible black swan events, the cost of mitigating all would be momentous, making it implausible in reality

– E.g. Sweden could improve border control in the Baltic sea to mitigate intrusion from Eastern neighbours, but the cost of 100% control of the border can likely not be motivated – a balance must be found against a pre-defined risk appetite

– Equally, the size of a deposit guarantee fund can be equal to the size of all deposits in the country

• In the financial world, it is the role of the CRO to identify and mitigate risks– Most CROs are experienced

and realistic; they know that black swan events could happen – but they equally know it is impossible to build a defence against all potential risks

– However, they also know that they will likely get fired if a black swan event indeed does happen

• It is impossible to calibrate models to predict all possible black swan events (e.g. terrorist attacks, IT failures, political decisions and epidemics)

• But the general crisis preparation can be improved, e.g.:– A recovery and resolution plan

can be defined (if an external event happens that effects our business significantly, the board and senior management will be gathered within 12 hours; systems will auto close all trades; etc.)

– Events can be bundled into major categories with action plans assigned against each

– Etc.

The cost of mitigating all potential events is too high

So what should institutions do?The CRO is responsible for predicting and mitigating risks