Embed Size (px)

Citation preview

Case Study (BERST region): Biobase Westland

8/15/2015

Project acronym: BERST Project full title: "BioEconomy Regional Strategy Toolkit "

Grant agreement no: 613671

Case Study (BERST region): Biobase Westland

2

Contents

1. Introduction ............................................................................................................... 2

1.1 Bioeconomy clusters ............................................................................................. 3

1.2 Key assets and development paths of bioeconomy clusters ................................ 3

1.3 Bioeconomy clusters in BERST project .................................................................. 5

2. BioBase Westland (the Netherlands) ......................................................................... 6

2.1 Executive summary ............................................................................................... 6

2.2 Introduction .......................................................................................................... 7

2.3 Environmental and socio-economic indicators of the region and clusters .......... 9

2.4 Analysis of the development path of the biocluster ........................................... 12

2.5 Concluding remarks and lessons for other regions ............................................ 22

2.6 References/ Links ................................................................................................ 26

1. Introduction

The BERST project explains the bioeconomy development path of a) BERST regions

and b) selected Good Practices. Aim is to provide a practical guide and source of

inspiration for other regions that wish to develop their bioeconomy potential. Under

this analysis:

- BERST regions are structured narratives for development pathways of

clusters in different bioeconomy sectors in the regions of partners in the

BERST project;

- Good Practices are examples of regions that contain one or more successful

bioeconomy clusters at the mature production stage.

Especially, Good Practices have been analysed in order to:

- understand how the various key assets interacted and performed during the

development stages;

- draw a number of lessons for the development of bioeconomy clusters within

their respective regions; and

- provide recommendations to other regions and clusters for each key asset

and each bioeconomy sector on which issues they have to take into account

in order to establish, develop and successfully operate similar clusters.

Case Study (BERST region): Biobase Westland

3

1.1 Bioeconomy clusters

The bioeconomy can be described in terms of an economy that ‘encompasses the

production of renewable biological resources and their conversion into food, feed,

bio-based products and bioenergy. In BERST, a bioeconomy cluster is perceived as a

geographical concentration of actors in vertical and horizontal relationships aiming

to develop the bioeconomy. Bioeconomy clusters have been categorised to allow

comparison and better understand synergies and interactions of the various

elements involved in the formation of bioregions. BERST recognises eight

bioeconomy sectors, namely:

- primary biomass;

- food and feed;

- construction;

- chemicals and polymers;

- pulp and paper;

- textile and clothing;

- energy;

- R&D biotechnology.

Given the broad coverage of sectors within the bioeconomy, bioeconomy clusters

might be rather heterogeneous in their specific focus. The development and

marketing of bioeconomy products does not differ from other products: the

challenge is to introduce competitive bioeconomy products that can be sold in

profitable quantities on the basis of its price, quality, and service combination

preferred by buyers over that offered by competing products. This implies that in the

analysis of the development of the bioeconomy clusters the same three factors play

a role as in the case of clusters aiming at the introduction and marketing of

televisions or cars: input-output linkages among firms, social capital and institutional

thickness.

1.2 Key assets and development paths of bioeconomy clusters

The input-output linkages among firms, social capital and institutional thickness in

the cluster are all embodied by actors with varying properties. In the analysis of the

development path of a bioeconomy cluster, we assume that the actors of the region,

in which the cluster is located, apply a strategy to develop the bioeconomy by

transforming biomass into competitive bioeconomy products. Such a transformation

process takes time. Hence, our analysis is guided by two starting points:

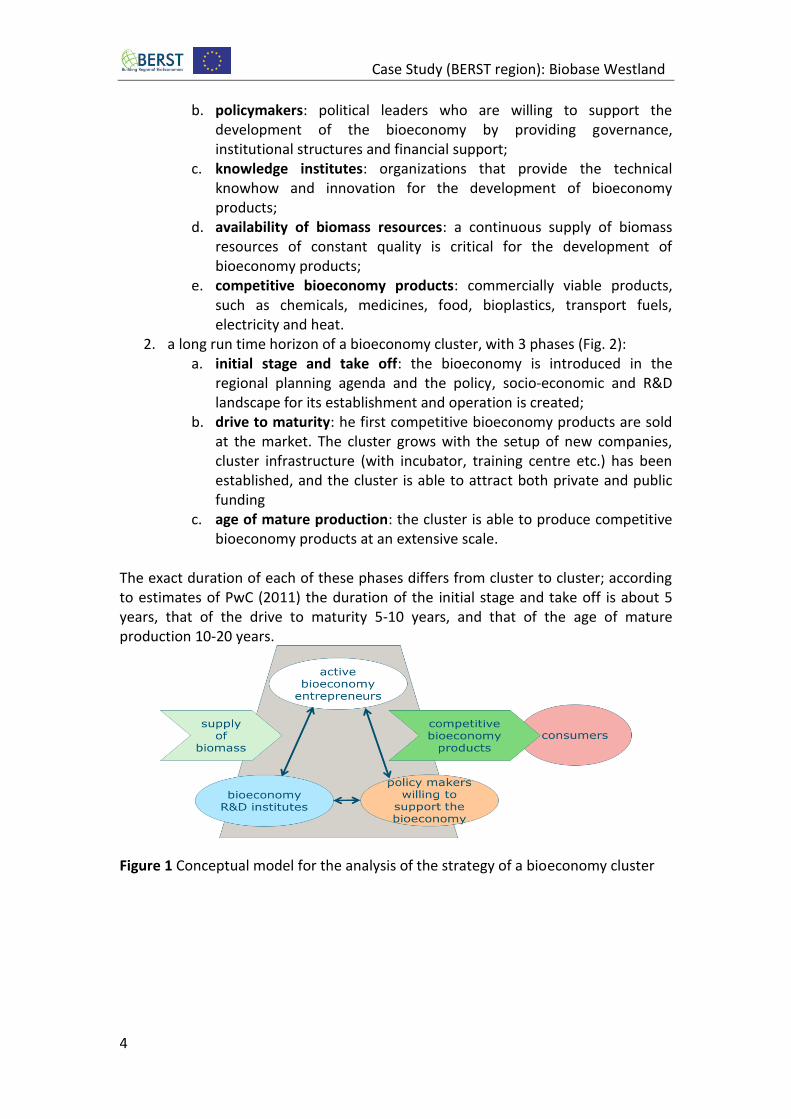

1. a focus on five key assets of a bioeconomy cluster, as outlined in our conceptual model for the analysis of the strategy of a bioeconomy cluster (Fig. 1). These are:

a. entrepreneurs: the presence of an entrepreneurial culture with active, innovative, flexible and risk taking entrepreneurs plays a pivotal role in driving clusters towards successful development;

Case Study (BERST region): Biobase Westland

4

b. policymakers: political leaders who are willing to support the development of the bioeconomy by providing governance, institutional structures and financial support;

c. knowledge institutes: organizations that provide the technical knowhow and innovation for the development of bioeconomy products;

d. availability of biomass resources: a continuous supply of biomass resources of constant quality is critical for the development of bioeconomy products;

e. competitive bioeconomy products: commercially viable products, such as chemicals, medicines, food, bioplastics, transport fuels, electricity and heat.

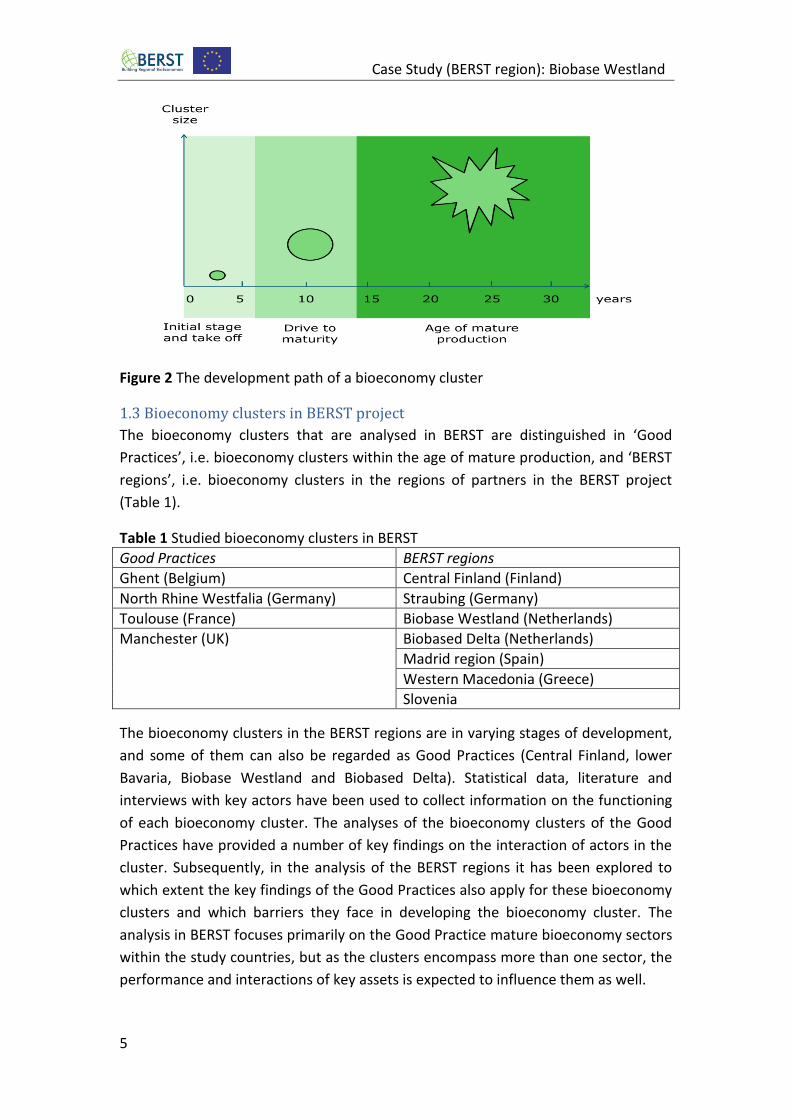

2. a long run time horizon of a bioeconomy cluster, with 3 phases (Fig. 2): a. initial stage and take off: the bioeconomy is introduced in the

regional planning agenda and the policy, socio-economic and R&D landscape for its establishment and operation is created;

b. drive to maturity: he first competitive bioeconomy products are sold at the market. The cluster grows with the setup of new companies, cluster infrastructure (with incubator, training centre etc.) has been established, and the cluster is able to attract both private and public funding

c. age of mature production: the cluster is able to produce competitive bioeconomy products at an extensive scale.

The exact duration of each of these phases differs from cluster to cluster; according to estimates of PwC (2011) the duration of the initial stage and take off is about 5 years, that of the drive to maturity 5-10 years, and that of the age of mature production 10-20 years.

Figure 1 Conceptual model for the analysis of the strategy of a bioeconomy cluster

Case Study (BERST region): Biobase Westland

5

Figure 2 The development path of a bioeconomy cluster

1.3 Bioeconomy clusters in BERST project

The bioeconomy clusters that are analysed in BERST are distinguished in ‘Good

Practices’, i.e. bioeconomy clusters within the age of mature production, and ‘BERST

regions’, i.e. bioeconomy clusters in the regions of partners in the BERST project

(Table 1).

Table 1 Studied bioeconomy clusters in BERST

Good Practices BERST regions

Ghent (Belgium) Central Finland (Finland)

North Rhine Westfalia (Germany) Straubing (Germany)

Toulouse (France) Biobase Westland (Netherlands)

Manchester (UK) Biobased Delta (Netherlands)

Madrid region (Spain)

Western Macedonia (Greece)

Slovenia

The bioeconomy clusters in the BERST regions are in varying stages of development,

and some of them can also be regarded as Good Practices (Central Finland, lower

Bavaria, Biobase Westland and Biobased Delta). Statistical data, literature and

interviews with key actors have been used to collect information on the functioning

of each bioeconomy cluster. The analyses of the bioeconomy clusters of the Good

Practices have provided a number of key findings on the interaction of actors in the

cluster. Subsequently, in the analysis of the BERST regions it has been explored to

which extent the key findings of the Good Practices also apply for these bioeconomy

clusters and which barriers they face in developing the bioeconomy cluster. The

analysis in BERST focuses primarily on the Good Practice mature bioeconomy sectors

within the study countries, but as the clusters encompass more than one sector, the

performance and interactions of key assets is expected to influence them as well.

Case Study (BERST region): Biobase Westland

6

2. BioBase Westland (the Netherlands) Authors: Arie van der Bent (Wageningen UR), Judith Zuiderwijk-Groenewegen and

Jan Smits (Gemeente Westland) and Calliope Panoutsou (Imperial)

Place and date: Wageningen,‘s-Gravenzande and London, June 2015

2.1 Executive summary

The Westland area in South Holland is the location of an internationally recognised

horticulture industry. Its location on the coast provides favourable climate conditions

year-round, including relatively high light intensity. In addition, the region lies

between several Dutch cities and towns and has good transport connections,

including road and air. Westland is a prosperous and innovative area, in part due to

fast-growing agribusiness. In the greenhouse cluster, there is extensive cooperation

through the value chain, including suppliers, producers, traders and knowledge

institutes. Total annual turnover in the region is approximately two billion euros.

The Municipality of Westland had the initiative to start a biobased cluster in 2013.

The main driver was the presence of a large area of greenhouses (approximately

3.000 ha) with vegetables, flowers and plants and the concept was to use residue

materials such as stems, leaves and class 3 products. Key recommendations were

drawn from the interviews and categorised as follows.

Organisation:

Do not make it complex but start partnerships with strong innovative companies

or parties and focus on smart portfolio of projects.

Actors:

Mid- and long-term commitment and a shared vision is essential, as well as good

communication.

Biomass supply:

Concentrate supplies on a biobase valorisation facility where in cascade useful

components are extracted. Start with an almost economic feasible business case

and develop additional value by extracting more components.

Competitive biobased products:

Focus on market demand for functionality and strong preference for natural

products.

Funding:

Case Study (BERST region): Biobase Westland

7

Involve industrial or private partners and support them with governmental

subsidies.

Policy and measures:

Arrange a portfolio of policy measures including knowledge, finances,

communication, matchmaking events, licences and an entrepreneurs’ platform.

2.2 Introduction

The work presented here provides a structured narrative for the development of the

biocluster in Westland, which may serve as a practical guidance and source of

inspiration for other regions that are willing to develop their bioeconomy potential.

It is based on analysis of statistical data, literature and interviews with key actors

involved in the development of bioeconomy and the biocluster in the region.

The report is structured in three main chapters. Chapter 2 provides an overview of

the socio-economic and environmental situation in the region. Chapter 3 translates

the findings from literature review, stakeholder interviews and consultations with

regional partners in a narrative that follows the two main dimensions of the analysis

conducted in BERST; i.e key assets and long time horizon. Finally, chapter 4 provides

concluding remarks, lessons learnt, opportunities, barriers and recommendations.

The Westland Cluster has been categorised into sectors in order to allow comparison

and better understand synergies and interactions of the various elements involved in

the formation of bioregions. The BERST project recognises eight bioeconomy sectors,

agreed with regional partners and interviewees, namely: primary biomass; food;

construction; chemicals and polymers; pulp and paper; textile and clothing; energy;

R&D services.

Two research dimensions have been used to analyse the development of the

bioeconomy sectors within the bioclusters in the study regions, as follows:

1. Clusters’ key assets and their interaction

2. Time horizon and stages of development

Clusters’ key assets and their interaction

Clusters can be considered forms of network structures. A cluster is characterised by

multiple, networked groups or teams who seek to accomplish organizational

objectives. Team-based organizations offer much by way of flexibility while projects

can be approached on a planned or ad hoc basis.

The actors in a cluster are thus a key asset. Several groups play a key role, as follows:

Case Study (BERST region): Biobase Westland

8

• Entrepreneurs. The presence of entrepreneurial culture plays a pivotal role in

driving clusters towards successful development. Clusters usually leverage on the

presence and active participation of various individuals with an entrepreneurial

spirit who are flexible, risk-takers and willing to try new ideas. The level of

entrepreneurial culture can therefore be seen as a critical success factor whereas

low levels of entrepreneurship would be a cause for concern (PWC, 2011).

• Policymakers. Political leaders who are willing to support the development of the

bioeconomy, providing governance, institutional structures and financial support.

• Knowledge institutes. Organisations that provide technical know-how and

innovation for the development of bio-products.

Other assets involved in clusters are:

Biomass supply: Consistent provision of biomass resources is critical. The analysis

of case studies and best practices in BERST project includes both indigenous raw

material streams and imports (if applicable) and elaborates on the advantages

and disadvantages of each option to the cluster development pathway.

Competitive bioeconomy products: commercially viable products such as fine

chemicals, medicines, food, chemicals, bioplastics, transport fuels, electricity and

heat.

Funding: consistent funding both from public and private sources, new funding

resources and attractive funding mechanisms for the entrepreneurs and

investors.

Policies and measures: legislative and policy framework conditions affecting the

introduction of products made from biomass including measures relating to

legislation, policies, standards, labels, certification and public procurement.

Time horizon and stages of development

Biocluster development passes through three main stages, typically taking 10- 15

years to reach maturity. The challenges at the initiation of the biocluster differ from

that during a mature stage. Hence it makes sense to distinguish the phases in the

development path of the biocluster. This dimension forms the basis for the second

starting point in the analysis within BERST.

Case Study (BERST region): Biobase Westland

9

It takes considerable time from the launch of a bioeconomy cluster to the time by

which a mature cluster is in place. In the analysis of the development path in BESRT

project, we distinguish three phases1:

• Initial stage and take off (IS): Introducing the bioeconomy in the regional

planning agenda and creating the policy, socio-economic and R&D landscape for

its establishment and operation.

• Drive to maturity (DMS): The first competitive bioeconomy products are sold at

the market. The cluster grows with the setup of new companies, cluster

infrastructure (incubator, training centre etc.) has been established, and the

cluster is able to attract both private and public funding.

• Age of mature production (MS): The cluster is able to produce competitive

bioeconomy products at an extensive scale.

The duration of each of these stages differs from region to region; according to

estimates of PwC (2011)2 the duration of the initial stage and take off is about 5

years, that of the drive to maturity 5-10 years and that of the age of mature

production 10-20 years. Within each stage, we analyse the interaction of the key

assets, as given in our conceptual model. It is notable that clusters studies were

considered to be either in initial stage or in the drive to maturity stage. No clusters

were considered to be fully mature although, in some regions, elements of clusters

had reached mature state of development (link to chapter from the main report).

2.3 Environmental and socio-economic indicators of the region and clusters

The region

1 Inspired by Rostow’s stages of growth.

2PriceWaterhouseCoopers (2011), Regional Biotechnology: Establishing a methodology and

performance indicators for assessing bioclusters and bioregions relevant to the KBBE area; Brussels;

via website: http://ec.europa.eu/research/bioeconomy/pdf/regional-biotech-report.pdf

Case Study (BERST region): Biobase Westland

10

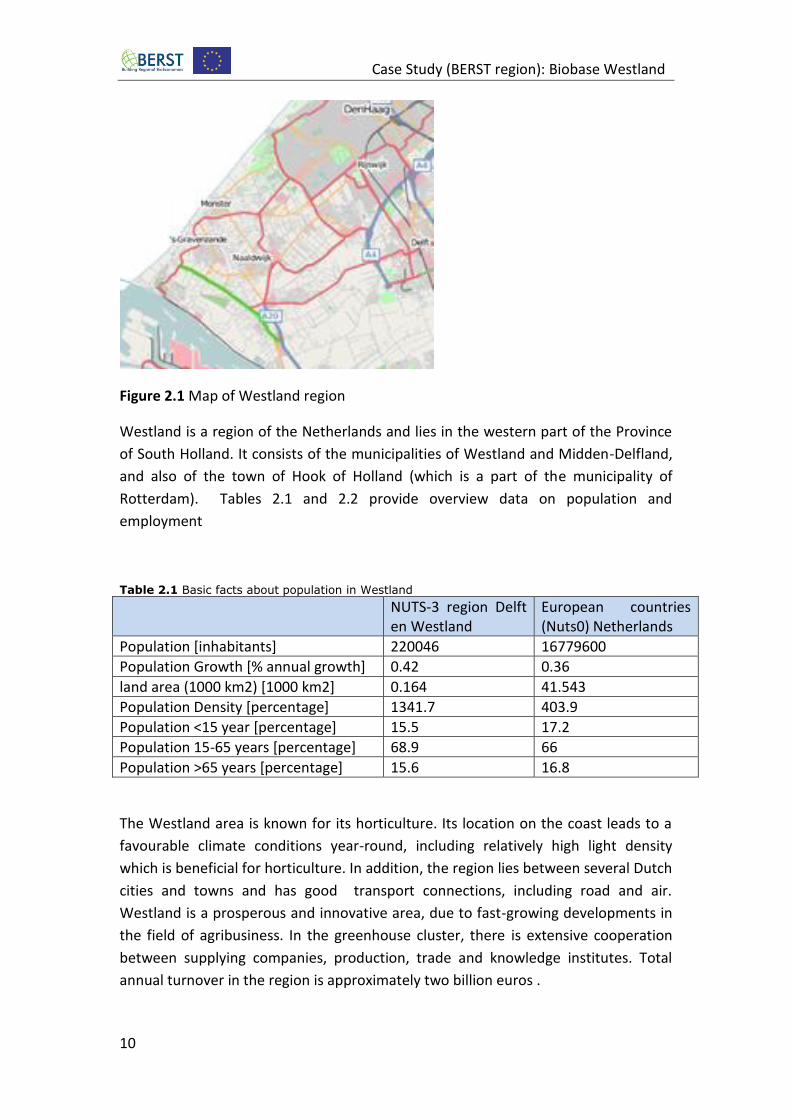

Figure 2.1 Map of Westland region

Westland is a region of the Netherlands and lies in the western part of the Province

of South Holland. It consists of the municipalities of Westland and Midden-Delfland,

and also of the town of Hook of Holland (which is a part of the municipality of

Rotterdam). Tables 2.1 and 2.2 provide overview data on population and

employment

Table 2.1 Basic facts about population in Westland

NUTS-3 region Delft en Westland

European countries (Nuts0) Netherlands

Population [inhabitants] 220046 16779600

Population Growth [% annual growth] 0.42 0.36

land area (1000 km2) [1000 km2] 0.164 41.543

Population Density [percentage] 1341.7 403.9

Population <15 year [percentage] 15.5 17.2

Population 15-65 years [percentage] 68.9 66

Population >65 years [percentage] 15.6 16.8

The Westland area is known for its horticulture. Its location on the coast leads to a

favourable climate conditions year-round, including relatively high light density

which is beneficial for horticulture. In addition, the region lies between several Dutch

cities and towns and has good transport connections, including road and air.

Westland is a prosperous and innovative area, due to fast-growing developments in

the field of agribusiness. In the greenhouse cluster, there is extensive cooperation

between supplying companies, production, trade and knowledge institutes. Total

annual turnover in the region is approximately two billion euros .

Case Study (BERST region): Biobase Westland

11

The region has identified five focus economic activities around which the capabilities,

target markets and strategic development priorities are shaped, bioeconomy, digital

economy and knowledge based economy.

Table 2.2 Environmental and socio-economic indicators of Westland

NUTS-3 region Delft en Westland

European countries (Nuts0) Netherlands

Total employment [employees] 113908 8017144

Agricultural employment as % in total employment [percentage]

9.4 2.3

Industrial employment as % in total employment [percentage]

7.2 10

Service employment as % in total employment [percentage] 83.4 87.7

GDP [mio_euro] 8212 599047

GDP (PPP; EU=100) [index (EU=100)] 128 129

GDP in chemical sector as % of regional GDP (est) [% in GVA] 0.3 1.2

GDP in energy sector as % of regional GDP (est) [% in GVA] 1.5 0.5

R&D expenditure [index (EU=1)] 0.476 0.675

% primary education [percentage] 24.6 24.2

% Secundary & Tertiary education [percentage] 75.4 75.8

Table 2.3 Focus economic activities for South Netherlands (source: S3Platform)3

Description Capabilities Target Markets EU Priorities

Organic aromatics 1. Manufacturing & industry 2. Chemicals & chemical products

1. Energy production & distribution 2. Power generation/renewable sources

1. Sustainable innovation 2. Sustainable energy & renewables

Promoting linkages between research and development centres and diverse sectoral clusters, promoting implementation of newly developed innovations

1. Services 2. Scientific research & development

1. Manufacturing & industry

1. Specific local policy priority

Research centre for food and health

1. Services 2. Scientific research & development

1. Human health & social work activities

1. Public health & security 2. Food security & safety

3 http://s3platform.jrc.ec.europa.eu/regions/nl4

Case Study (BERST region): Biobase Westland

12

Supply chain innovation 1. Transporting & storage 2. Warehousing & support activities for transportation (logistics storage)

1. Manufacturing & industry

1. Service innovation 2. New or improved organisational models

Cluster development, linkages between private sector and educational research facilities

1. Services 2. Education

1. Manufacturing & industry

1. Service innovation 2. New or improved organisational models

The cluster of Westland

The initiative to start a biobased cluster was undertaken by the Municipality of

Westland in 2013. The main driver was the presence of a large area (approximately

3.000 ha) of greenhouses with vegetables, flowers and plants and the concept was to

use residue materials such as stems,leaves and class 3 products.

Table 2.4 Employment and firms dynamics in bioeconomy sectors in Westland, 2004-2013

Employment Firms Micro- firms

2004 2013 2004 2013 2004 2013

Agriculture regional 12,097 10,698 2,080 1,310 0 1194

Agriculture national 215,015 186,186 71,199 64,235 0 62374

% of national 6 6 3 2 2

Energy regional 1895 1678 8 8 0 6

Energy national 33929 37491 586 744 0 947

% of national 6 4 1 1 1

Pulp & paper regional

653 557 68 59 0 49

Pulp & paper national

76628 61090 7291 6882 0 5778

% of national 1 1 1 1 1

Construction regional

7,482 6,627 2,040 1,993 0 1,881

Construction national

465,242 397,251 116,739 121,003 0 115,452

% of national 2 2 2 2 2

Chemicals regional 366 393 14 16 0 13

Chemicals national 100905 94287 2397 2319 0 1947

% of national 0 0 1 1 1

Total regional 120527 113908 15744 15219 0 16,240

Total national 8163638 8017144 1147170 1286261 0 1,150,510

2.4 Analysis of the development path of the biocluster

This chapter translates the findings from literature review, stakeholder interviews

and consultations with regional partners in a narrative that follows the two main

Case Study (BERST region): Biobase Westland

13

dimensions of the analysis conducted in BERST i.e. key assets and long time horizon.

The work presented here provides comparative analysis of the key assets, their

performance and rationale as well as their evolution and interactions across the

development stages of the cluster. The outputs from this analysis facilitate the

development of recommendations i) for the cluster’s successful transition to the

next stage and ii) for other clusters with similar characteristics in terms of sectors

and assets.

Lines of demarcation

Before the key assets for Bio Base Westland are discussed, it is important to exactly

specify which (sub) sectors are covered and why.

Bio Base Westland builds upon the strength of mature regional sectors, to develop

new, explicitly biobased, economic activities that are therefore generally still in the

initial stage. The biobased economy is a subset of the total bioeconomy and does not

include the food sector.

(I) This case study exclusively covers biobased economy sectors.

One opportunity for the region is that a high volume of biomass is already produced

locally, mostly from agricultural activity. There is also the opportunity to import

biomass from nearby sea ports. Sectors downstream in the value chain are selected

on the basis of the anticipated economic activity boost from the processing of this

biomass. In many cases, this involves a gradual shift from the currently used fossil

feedstock to biomass in sectors that are already important in the region. Another

opportunity is the production of special plants dedicated to produce plant extracts

and plant compounds for high end markets such as pharmaceuticals.

(II) The seven specific sectors that are included are:

- the primary biomass sector - paper and cardboard - building materials - biofuels & bioenergy - pharmaceutical purposes - cosmetics - green pesticides

- food additives such as aroma compounds, vegetal E-numbers, colourants

The last four of them are grouped in the chemicals & polymers bioeconomy sector

for the BERST analysis.

Replacement of fossil feedstock by biomass is a transition that is generally accepted

to take decades to reach significant scale. This introduces a potential definition

problem when describing assets and rating the degree of maturity of the sectors

downstream in the value chain. The sectors are mature already, but their transition

to biobased sectors is in its initial stage.

Case Study (BERST region): Biobase Westland

14

We distinguish two biobased subsectors that differ strongly in their maturity:

A. The mature primary biomass subsector. This ‘traditional’ sector mainly

concentrates on producing food and flowers, but also produces large waste

streams that can be valorised in the biobased economy.

B. The initial stage primary biomass subsector. This consists of three areas:

Specific crops for natural fibres

Specific crops for high value ingredients

Summarizing:

(IV) Combining I and II, only the part of the primary biomass sector that provides

biomass for the biobased economy is covered. This part is split in two subsectors

A mature subsector* (P1), of which only the waste stream output is relevant

and covered in this study;

An initial stage subsector (P2), which specifically produces biomass for the

biobased economy.

A final issue that needs to be addressed is the assignment of biorefinery activities to

one or more of the above subsectors. As a process, biorefinery is the splitting of

(generally complex) biomass in fractions that can be individually used in any of the

subsectors downstream from primary production (food, feed, chemicals, energy,

etc). It generally consists of multiple individual steps, that could in principle take

place in each of the mentioned subsectors. Biorefinery activities may dramatically

increase the value of the processed biomass stream, depending on the isolated

compounds and their purity. It is therefore a great opportunity for new economic

activity as well. Without major innovations in biorefinery, the biobased economy

(‘new bioeconomy’) on which Bio Base Westland concentrates cannot be realized in

full. As it takes place at the interface between sectors, it is a matter of definition to

which subsector biorefinery is assigned.

(V) In this case study, biorefinery is considered to be (an implicit) part of the

individual downstream subsectors that use the separated fractions as input.

NB: There are exceptions, but these are made explicit where appropriate.

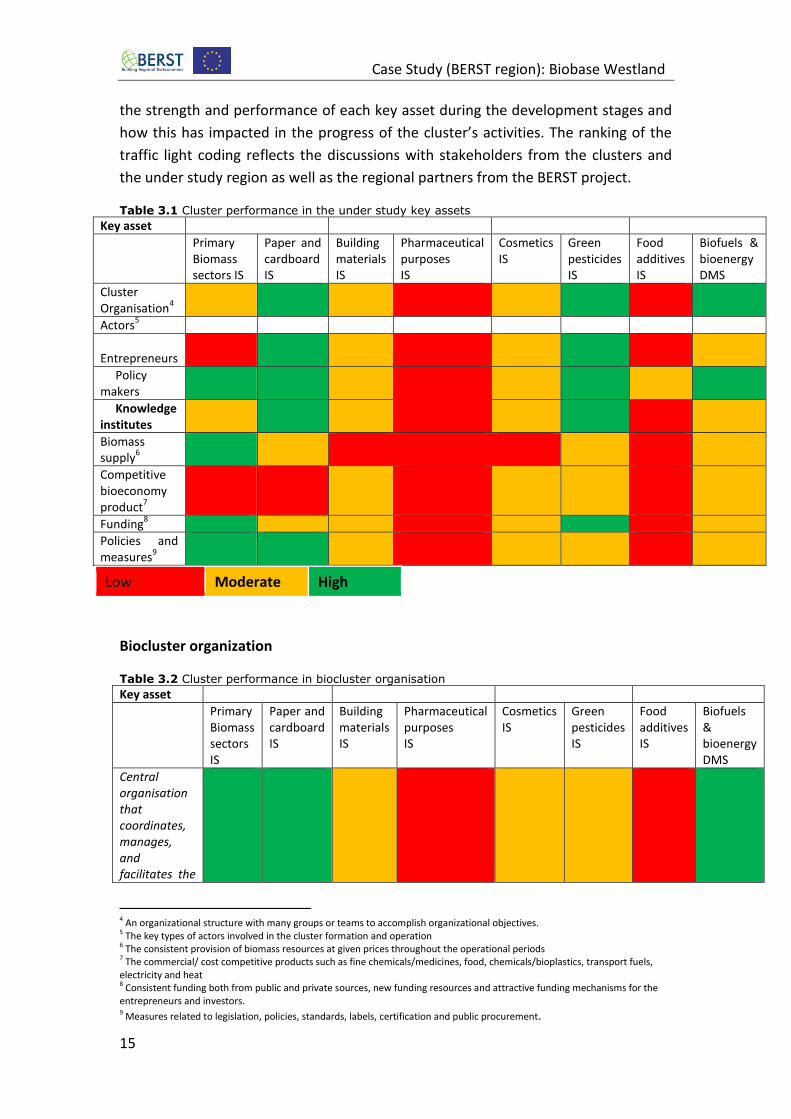

Table 3.1 presents the performance of the various bioeconomy sectors which are

present in the cluster across the key assets, during the initial (IS) and the drive to

maturity stage (DMS), based on the results from the questionnaire survey. Details on

how the individual key assets performed across the two development stages are

provided in the following sections alongside with barriers and enabling factors which

have framed their progress. Traffic light colour coding has been introduced to reflect

Case Study (BERST region): Biobase Westland

15

the strength and performance of each key asset during the development stages and

how this has impacted in the progress of the cluster’s activities. The ranking of the

traffic light coding reflects the discussions with stakeholders from the clusters and

the under study region as well as the regional partners from the BERST project.

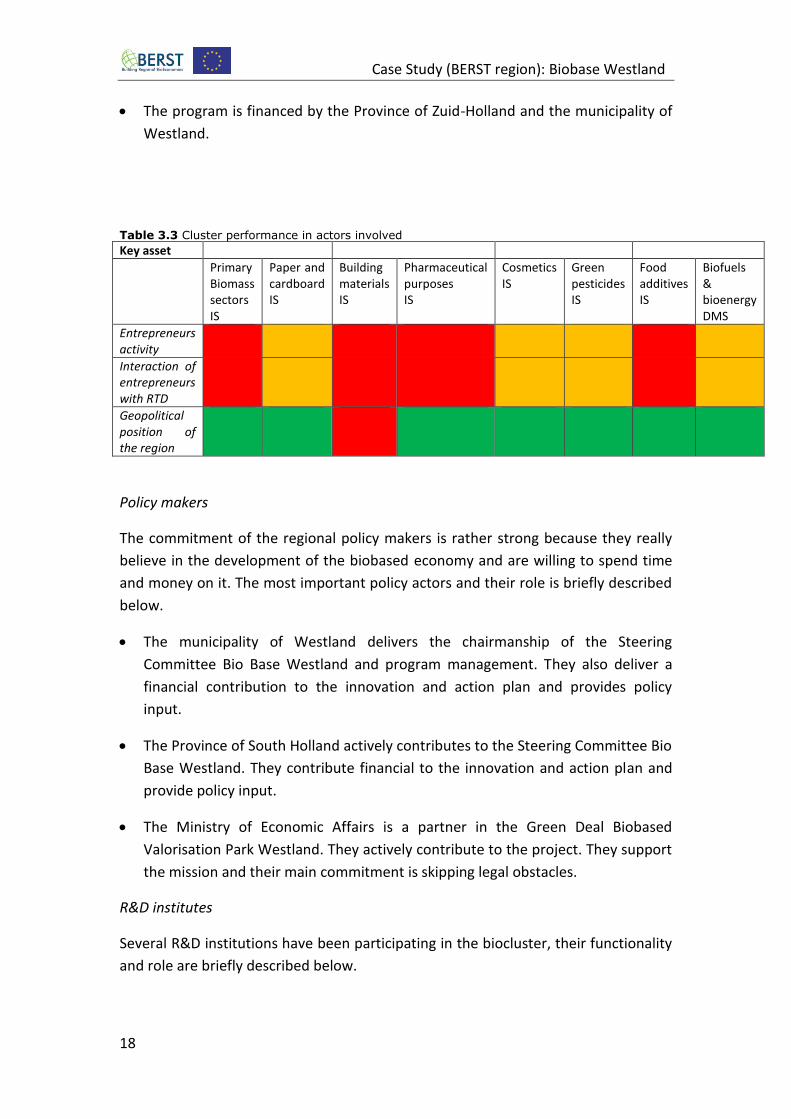

Table 3.1 Cluster performance in the under study key assets

Key asset

Primary Biomass sectors IS

Paper and cardboard IS

Building materials IS

Pharmaceutical purposes IS

Cosmetics IS

Green pesticides IS

Food additives IS

Biofuels & bioenergy DMS

Cluster Organisation

4

Actors5

Entrepreneurs

Policy makers

Knowledge institutes

Biomass supply

6

Competitive bioeconomy product

7

Funding8

Policies and measures

9

Low Moderate High

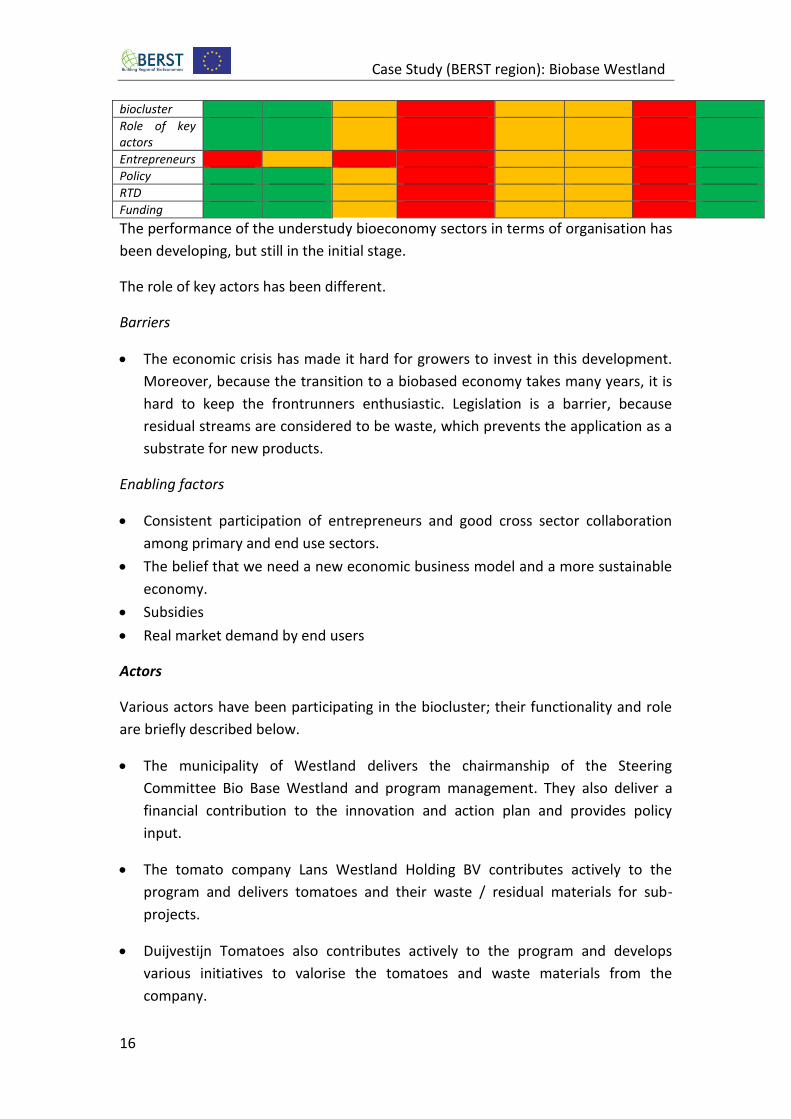

Biocluster organization

Table 3.2 Cluster performance in biocluster organisation

Key asset

Primary Biomass sectors IS

Paper and cardboard IS

Building materials IS

Pharmaceutical purposes IS

Cosmetics IS

Green pesticides IS

Food additives IS

Biofuels & bioenergy DMS

Central organisation that coordinates, manages, and facilitates the

4 An organizational structure with many groups or teams to accomplish organizational objectives. 5 The key types of actors involved in the cluster formation and operation 6 The consistent provision of biomass resources at given prices throughout the operational periods 7 The commercial/ cost competitive products such as fine chemicals/medicines, food, chemicals/bioplastics, transport fuels, electricity and heat 8 Consistent funding both from public and private sources, new funding resources and attractive funding mechanisms for the entrepreneurs and investors. 9 Measures related to legislation, policies, standards, labels, certification and public procurement.

Case Study (BERST region): Biobase Westland

16

biocluster

Role of key actors

Entrepreneurs

Policy

RTD

Funding

The performance of the understudy bioeconomy sectors in terms of organisation has

been developing, but still in the initial stage.

The role of key actors has been different.

Barriers

The economic crisis has made it hard for growers to invest in this development.

Moreover, because the transition to a biobased economy takes many years, it is

hard to keep the frontrunners enthusiastic. Legislation is a barrier, because

residual streams are considered to be waste, which prevents the application as a

substrate for new products.

Enabling factors

Consistent participation of entrepreneurs and good cross sector collaboration

among primary and end use sectors.

The belief that we need a new economic business model and a more sustainable

economy.

Subsidies

Real market demand by end users

Actors

Various actors have been participating in the biocluster; their functionality and role

are briefly described below.

The municipality of Westland delivers the chairmanship of the Steering

Committee Bio Base Westland and program management. They also deliver a

financial contribution to the innovation and action plan and provides policy

input.

The tomato company Lans Westland Holding BV contributes actively to the

program and delivers tomatoes and their waste / residual materials for sub-

projects.

Duijvestijn Tomatoes also contributes actively to the program and develops

various initiatives to valorise the tomatoes and waste materials from the

company.

Case Study (BERST region): Biobase Westland

17

Van Vliet Contrans also contributes actively and is leader of the project in which

the fibres of tomatostems are refined and used for making paper and cardboard

for tomato boxes.

LTO Glaskracht Westland actively contributes to the Steering Committee Bio Base

Westland.

FloraHolland actively contributes to the Steering Committee Bio Base Westland

and participates in various projects.

Rabobank Westland actively contributes to the Steering Committee.

Van der Windt develops and spreads biobased packaging materials.

The Chamber of Commerce actively contributes to the organization of meetings

and clustering. They connect chain parties and connects knowledge institutes

with SMEs.

The Expert Center for Plant Compounds provides knowledge and information

about promising product-market combinations and plant compounds. They

contribute actively to the Steering Committee Bio Base Westland.

The Province of South Holland actively contributes to the Steering Committee Bio

Base Westland. They contribute financial to the innovation and action plan and

provide policy input.

The Ministry of Economic Affairs is a partner in the Green Deal Biobased

Valorisation Park Westland. They actively contribute to the project.

Inholland takes care of the organization and supervision of a knowledgegroup

with (horticulture) entrepreneurs and plays an active role in translating issues for

entrepreneurs in knowledge projects. They do research on "Successful business

and network models for the valorization of biomass in horticulture'' and

opportunities for "Creating Additional Market Value out of Fruit & Vegetables".

Frans Zwinkels Project and Technology is leader of the project biobased tomato

boxes 2015

Wageningen UR Greenhouse Horticulture researches (improved) production of

components in existing glasshouse crops and cultivation methods for developing

new crops.

Perfect Plants Holding is engaged in the cultivation of crops for winning plant

compounds and extracts for use in the pharmaceutical industry.

Case Study (BERST region): Biobase Westland

18

The program is financed by the Province of Zuid-Holland and the municipality of

Westland.

Table 3.3 Cluster performance in actors involved

Key asset

Primary Biomass sectors IS

Paper and cardboard IS

Building materials IS

Pharmaceutical purposes IS

Cosmetics IS

Green pesticides IS

Food additives IS

Biofuels & bioenergy DMS

Entrepreneurs activity

Interaction of entrepreneurs with RTD

Geopolitical position of the region

Policy makers

The commitment of the regional policy makers is rather strong because they really

believe in the development of the biobased economy and are willing to spend time

and money on it. The most important policy actors and their role is briefly described

below.

The municipality of Westland delivers the chairmanship of the Steering

Committee Bio Base Westland and program management. They also deliver a

financial contribution to the innovation and action plan and provides policy

input.

The Province of South Holland actively contributes to the Steering Committee Bio

Base Westland. They contribute financial to the innovation and action plan and

provide policy input.

The Ministry of Economic Affairs is a partner in the Green Deal Biobased

Valorisation Park Westland. They actively contribute to the project. They support

the mission and their main commitment is skipping legal obstacles.

R&D institutes

Several R&D institutions have been participating in the biocluster, their functionality

and role are briefly described below.

Case Study (BERST region): Biobase Westland

19

The Expert Center for Plant Compounds provides knowledge and information

about promising product-market combinations and plant compounds. They

contribute actively to the Steering Committee Bio Base Westland.

Inholland takes care of the organization and supervision of a knowledgegroup

with (horticulture) entrepreneurs and plays an active role in translating issues for

entrepreneurs in knowledge projects. They do research on "Successful business

and network models for the valorization of biomass in horticulture'' and

opportunities for "Creating Additional Market Value out of Fruit & Vegetables".

Wageningen UR Greenhouse Horticulture researches (improved) production of

components in existing glasshouse crops and cultivation methods for developing

new crops.

Leiden University is partner in an project which aims to produce plant

compounds against obesitas. They are testing the functionality of plant

compounds on health and wellbeing aspects.

Barriers

It is a difficult task to find market partners willing to use the plant compounds in

their products.

Enabling factors

Strong commitment from policy makers because they really believe in the

development of the biobased economy and are willing to spend time and money

on it.

Strong collaboration with R&D, regional partners and entrepreneurs in several

EU and nationally funded projects.

Secure start-up funding from regional government.

Biomass supply

Biomass supply is primarily based on the residuals from flowers-, vegetables- and

plants production; and specifically grown plants in greenhouses under optimal and

controlled growing conditions.

Barriers

It is hard to have long-term contracts for obtaining biomass with the many

different entrepreneurs in the region.

Enabling factors

High biomass availability from the well-developed agricultural sector

Case Study (BERST region): Biobase Westland

20

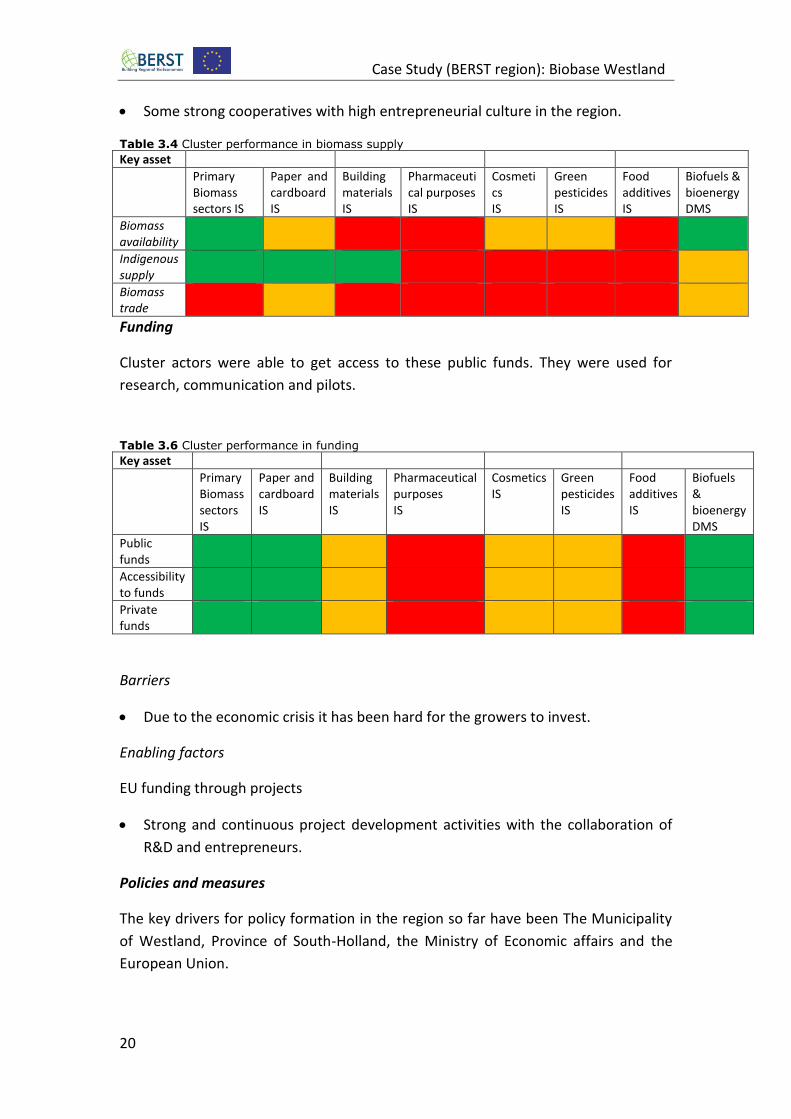

Some strong cooperatives with high entrepreneurial culture in the region.

Table 3.4 Cluster performance in biomass supply

Key asset

Primary Biomass sectors IS

Paper and cardboard IS

Building materials IS

Pharmaceutical purposes IS

Cosmetics IS

Green pesticides IS

Food additives IS

Biofuels & bioenergy DMS

Biomass availability

Indigenous supply

Biomass trade

Funding

Cluster actors were able to get access to these public funds. They were used for

research, communication and pilots.

Table 3.6 Cluster performance in funding

Key asset

Primary Biomass sectors IS

Paper and cardboard IS

Building materials IS

Pharmaceutical purposes IS

Cosmetics IS

Green pesticides IS

Food additives IS

Biofuels & bioenergy DMS

Public funds

Accessibility to funds

Private funds

Barriers

Due to the economic crisis it has been hard for the growers to invest.

Enabling factors

EU funding through projects

Strong and continuous project development activities with the collaboration of

R&D and entrepreneurs.

Policies and measures

The key drivers for policy formation in the region so far have been The Municipality

of Westland, Province of South-Holland, the Ministry of Economic affairs and the

European Union.

Case Study (BERST region): Biobase Westland

21

The Bio Base Westland agenda is embedded in the national policy ‘topsectoren

beleid’ (i.e.: topsector policy) and in provincial economic policies. In this framework

Bio Base Westland is partner in the national innovation and research agenda ‘New

business with high quality and green plant compounds from horticulture’.

Table 3.7 Cluster performance in policies and measures

Key asset

Primary Biomass sectors MS

Paper and cardboard IS

Building materials IS

Pharmaceutical purposes IS

Cosmetics IS

Green pesticides IS

Food additives IS

Biofuels & bioenergy DMS

Presence of policy instruments

Effectiveness of policy instruments

Consistency of policy

Monitoring procedures

An important policy driver so far has been the so-called Green Deals (in which the

national government commits to take away legislation difficulties that hamper new

sustainable activities/processes/products), agreements of intention, subsidy

programs of the province (clusterregeling) and Topsectorprogram.

Barriers

Legislation in national and EU laws discourages the application of rest streams.

Rest streams are considered as waste with all kinds of limiting factors.

The fragmented nature of the various bio-based economy sectors prohibits the

fast design and uptake of cross sector targets and the subsequent sectorial policy

alignment.

The environmental impact of fossil substrates is not part of the price. Because of

that fossil fuels have an advantage.

Enabling factors

Consistency and stability of policy aims and targets.

Case Study (BERST region): Biobase Westland

22

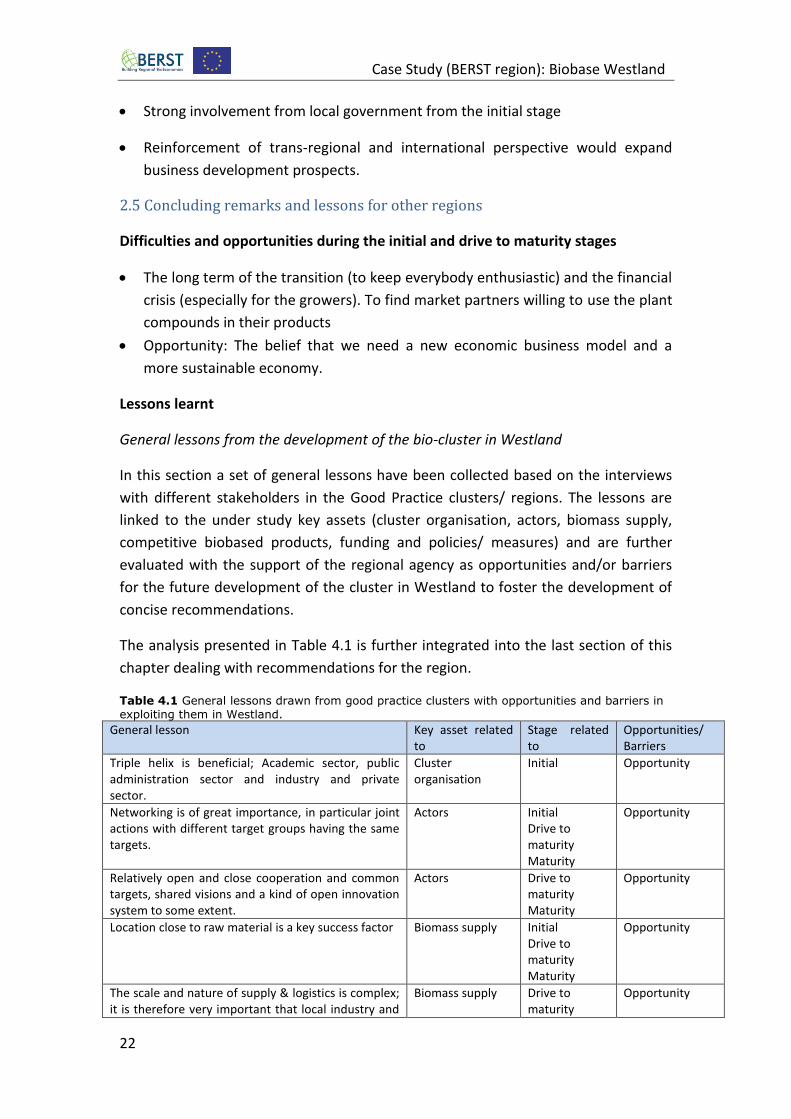

Strong involvement from local government from the initial stage

Reinforcement of trans-regional and international perspective would expand

business development prospects.

2.5 Concluding remarks and lessons for other regions

Difficulties and opportunities during the initial and drive to maturity stages

The long term of the transition (to keep everybody enthusiastic) and the financial

crisis (especially for the growers). To find market partners willing to use the plant

compounds in their products

Opportunity: The belief that we need a new economic business model and a

more sustainable economy.

Lessons learnt

General lessons from the development of the bio-cluster in Westland

In this section a set of general lessons have been collected based on the interviews

with different stakeholders in the Good Practice clusters/ regions. The lessons are

linked to the under study key assets (cluster organisation, actors, biomass supply,

competitive biobased products, funding and policies/ measures) and are further

evaluated with the support of the regional agency as opportunities and/or barriers

for the future development of the cluster in Westland to foster the development of

concise recommendations.

The analysis presented in Table 4.1 is further integrated into the last section of this

chapter dealing with recommendations for the region.

Table 4.1 General lessons drawn from good practice clusters with opportunities and barriers in exploiting them in Westland.

General lesson Key asset related to

Stage related to

Opportunities/ Barriers

Triple helix is beneficial; Academic sector, public administration sector and industry and private sector.

Cluster organisation

Initial Opportunity

Networking is of great importance, in particular joint actions with different target groups having the same targets.

Actors Initial Drive to maturity Maturity

Opportunity

Relatively open and close cooperation and common targets, shared visions and a kind of open innovation system to some extent.

Actors Drive to maturity Maturity

Opportunity

Location close to raw material is a key success factor Biomass supply Initial Drive to maturity Maturity

Opportunity

The scale and nature of supply & logistics is complex; it is therefore very important that local industry and

Biomass supply Drive to maturity

Opportunity

Case Study (BERST region): Biobase Westland

23

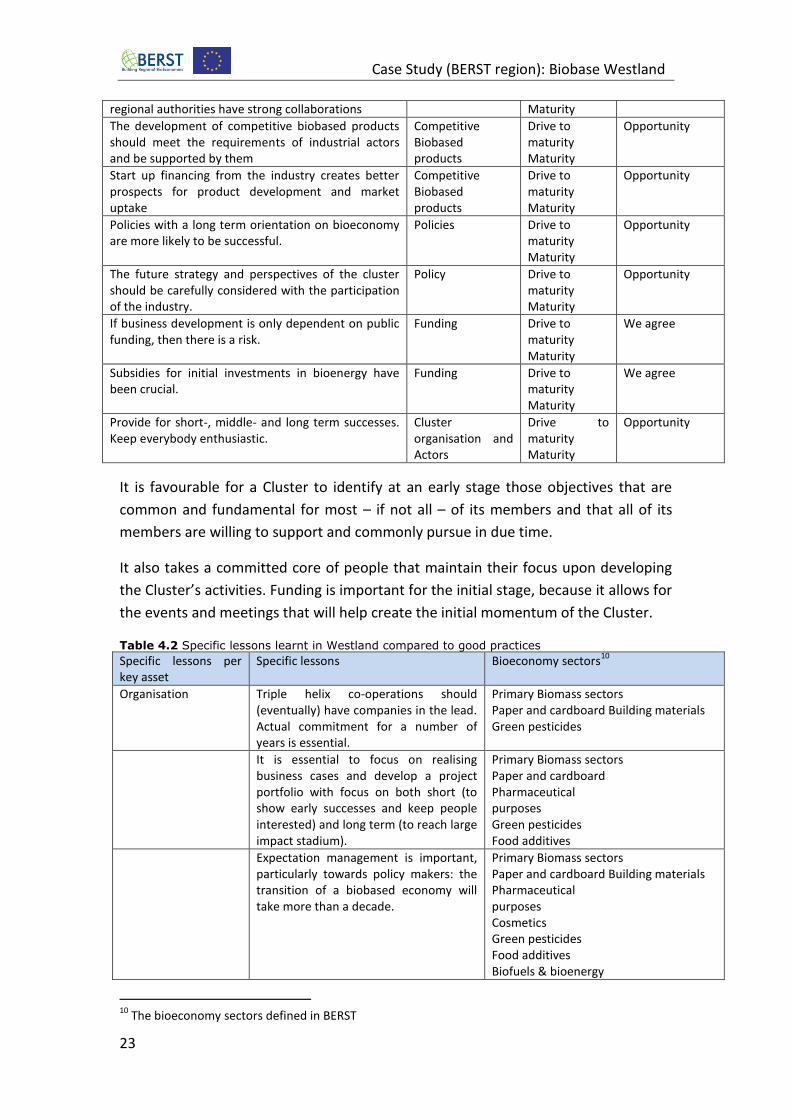

regional authorities have strong collaborations Maturity

The development of competitive biobased products should meet the requirements of industrial actors and be supported by them

Competitive Biobased products

Drive to maturity Maturity

Opportunity

Start up financing from the industry creates better prospects for product development and market uptake

Competitive Biobased products

Drive to maturity Maturity

Opportunity

Policies with a long term orientation on bioeconomy are more likely to be successful.

Policies Drive to maturity Maturity

Opportunity

The future strategy and perspectives of the cluster should be carefully considered with the participation of the industry.

Policy Drive to maturity Maturity

Opportunity

If business development is only dependent on public funding, then there is a risk.

Funding Drive to maturity Maturity

We agree

Subsidies for initial investments in bioenergy have been crucial.

Funding Drive to maturity Maturity

We agree

Provide for short-, middle- and long term successes. Keep everybody enthusiastic.

Cluster organisation and Actors

Drive to maturity Maturity

Opportunity

It is favourable for a Cluster to identify at an early stage those objectives that are

common and fundamental for most – if not all – of its members and that all of its

members are willing to support and commonly pursue in due time.

It also takes a committed core of people that maintain their focus upon developing

the Cluster’s activities. Funding is important for the initial stage, because it allows for

the events and meetings that will help create the initial momentum of the Cluster.

Table 4.2 Specific lessons learnt in Westland compared to good practices

Specific lessons per key asset

Specific lessons Bioeconomy sectors10

Organisation Triple helix co-operations should (eventually) have companies in the lead. Actual commitment for a number of years is essential.

Primary Biomass sectors Paper and cardboard Building materials Green pesticides

It is essential to focus on realising business cases and develop a project portfolio with focus on both short (to show early successes and keep people interested) and long term (to reach large impact stadium).

Primary Biomass sectors Paper and cardboard Pharmaceutical purposes Green pesticides Food additives

Expectation management is important, particularly towards policy makers: the transition of a biobased economy will take more than a decade.

Primary Biomass sectors Paper and cardboard Building materials Pharmaceutical purposes Cosmetics Green pesticides Food additives Biofuels & bioenergy

10

The bioeconomy sectors defined in BERST

Case Study (BERST region): Biobase Westland

24

Actors Effective cooperation between agro and chemistry requires parties to overcome large differences in cultures and interests. This is a time consuming process.

Primary Biomass sectors Paper and cardboard Building materials Pharmaceutical purposes Cosmetics Green pesticides Food additives Biofuels & bioenergy

Research organisations have strong expertise and international leadership

Primary Biomass sectors Paper and cardboard Building materials Pharmaceutical purposes Cosmetics Green pesticides Food additives Biofuels & bioenergy

Strong cooperatives with high entrepreneurial culture in the region.

Primary Biomass sectors Paper and cardboard Building materials Pharmaceutical purposes Cosmetics Green pesticides Food additives Biofuels & bioenergy

Products Variability of bio-based market sectors increases the complexity for cross over technological transfers, scaling up of new pathways and commercialisation of new bio-base products.

Primary Biomass sectors Paper and cardboard Building materials Pharmaceutical purposes Cosmetics Green pesticides Food additives Biofuels & bioenergy

Efficient transfer of knowledge and high rates of adoption of innovation

Primary Biomass sectors Paper and cardboard Building materials Pharmaceutical purposes Cosmetics Green pesticides Food additives Biofuels & bioenergy

Funding Financial instruments of governments really help business development for new, high risk activities.

Primary Biomass sectors Paper and cardboard Building materials Pharmaceutical purposes Cosmetics Green pesticides Food additives Biofuels & bioenergy

Policies Strategic/plan should be based on the strengths of local bioeconomy (availability of biomass, knowledge institutions, logistics, availability of crossover industries (energy, process industry, food, feed, pharma, technology providers).

Primary Biomass sectors Paper and cardboard Building materials Pharmaceutical purposes Cosmetics Green pesticides Food additives Biofuels & bioenergy Reinforcement of trans- regional and

Case Study (BERST region): Biobase Westland

25

international perspective would expand business development prospects.

It is essential to focus on realising business cases. Do not develop many formal

organisations and relationships; this takes up a lot of time that should be spent on

concrete projects.

For the large transition agenda, international cooperation in Europe (and abroad) is

necessary. European funding of flagships and demo’s is important.

Try to connect the whole value chain, try not to work with (too many) competing

companies.

Organise sufficient development power: companies often need intermediates that

connecting value chains.

Recommendations

Based on the conclusions and the general and specific lessons presented in the

tables above, recommendations are provided for the transition to the next

development stage (maturity) for each of the key assets examined in the previous

sections..

The key recommendations for organisation include the following:

Don’t make it complex but start partnerships with strong innovative companies

or parties and focus on smart portfolio of projects.

The key recommendations for actors include the following:

Mid- and long-term commitment and a shared vision is essential, as well as good

communication.

The key recommendations for biomass supply include the following:

Concentrate supplies on a biobase valorisation facility where in cascade useful

components are extracted. Start with an almost economic feasible business case

and develop additional value by extracting more components.

The key recommendations for competitive biobased products include the following:

Focus on market demand for functionality and strong preference for natural

products.

The key recommendations for funding include the following:

Case Study (BERST region): Biobase Westland

26

Involve industrial or private partners and support them with governmental

subsidies.

The key recommendations for policy and measures include the following:

Arrange a portfolio of policy measures including knowledge, finances,

communication, matchmaking events, licences and an entrepreneurs’ platform.

2.6 References/ Links www.gemeentewestland.nl

www.biobasewestland.nl