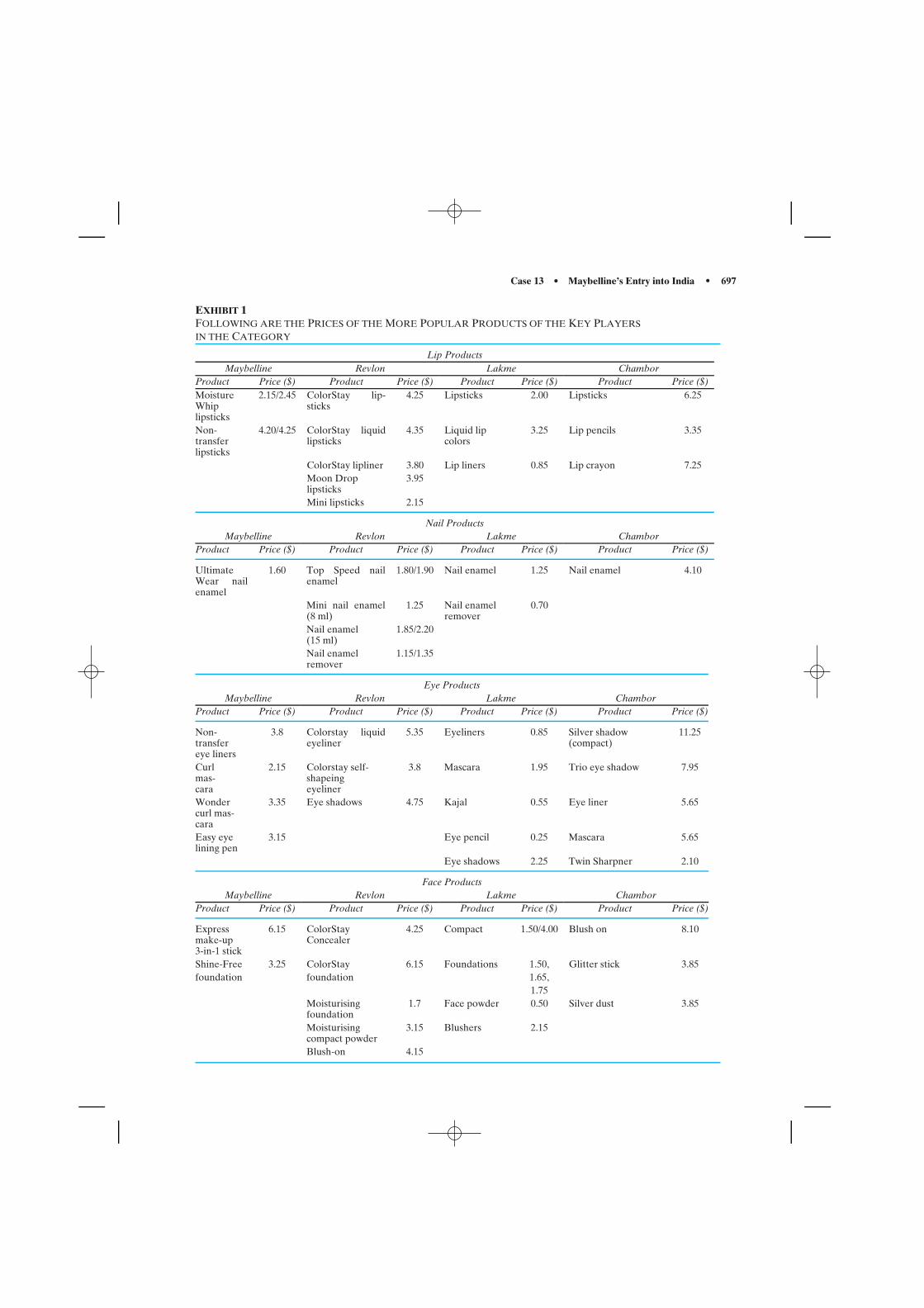

Embed Size (px)

Citation preview

Case 7 • Starbucks Coffee: Expansion in Asia • 655

� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

CASE 7

STARBUCKS COFFEE: EXPANSION IN ASIA

HISTORY

Starbucks Coffee Company was founded in 1971 by threecoffee aficionados. Starbucks, named after the coffee-lovingfirst mate in Moby Dick, opened its first store in Seattle’s PikePlace Public Market. During this time, most coffee was pur-chased in a can directly from supermarket shelves. Starbucks’concept of selling fresh-roasted whole beans in a specialtystore was a revolutionary idea.

In 1987, Howard Schultz, a former Starbucks employee,acquired the company. When Schultz first joined Starbucks inthe early 1980s as director of retail operations, Starbucks wasa local, highly respected roaster and retailer of whole beanand ground coffees. A business trip to Milan’s famous coffeeshops in 1983 opened Schultz’s eyes to the rich tradition ofthe espresso beverage. Schultz recalls, ‘‘What I saw was theunique relationship that the Italian people had with the ubiq-uitous coffee bars around Italy. People used the local coffeebar as the third place from home and work. What I wantedto try and do was re-create that in North America.’’ Inspiredby the Italian espresso bars, Schultz convinced executives tohave Starbucks’ stores serve coffee by the cup. And the rest ishistory! The company has seen phenomenal growth from 17coffee outlets in Seattle almost 35 years back to 9000 shops inaround 28 countries worldwide.

Starbucks went public in 1993 and has done extremely wellin turning an everyday beverage into a premium product. Thegreen and white mermaid logo is widely recognized; the brandis defined not only by its products, but also by attitude. Busi-ness Week’s most recent survey (2004) of the top global brandsreported Starbucks as one of the fastest growing brands witha cult following. It is all about the Starbucks experience, theatmosphere, and the place that is a refuge for most people toget away from everyday stresses. The average customer visitsa Starbucks 18 times in a month, and about 10 percent of allcustomers visit twice a day. Starbucks has created an affinitywith customers that is almost cult-like. Today, Starbucks isthe leading roaster and retailer of specialty coffee in NorthAmerica, with more than 1000 retail stores in 35 markets.

MISSION STATEMENT

Starbucks’ corporate mission statement is as follows: ‘‘Estab-lish Starbucks as the premier purveyor of the finest coffeein the world, while maintaining our uncompromising princi-ples as we grow. The following guiding principles will help usmeasure the appropriateness of our decisions:

1. Provide a great work environment and treat each otherwith respect and dignity.

This case was prepared by Valerie Darguste, Ana Su, Ai-Lin Tu, andPeggy Wei of Stern School of Business at New York University andupdated by Sonia Ketkar of the Fox School of Business and Managementat Temple University under the supervision of Professor Masaaki Kotabefor class discussion rather than to illustrate either effective or ineffectivemanagement of a situation described (2006).

2. Apply the highest standards of excellence to the purchasing,roasting, and fresh delivery of our coffee.

3. Develop enthusiastically satisfied customers all of the time.

4. Contribute positively to our communities and our environ-ment.

5. Recognize that profitability is essential to our future suc-cess.

6. Embrace diversity as an essential component in the way wedo business.

Starbucks’ corporate objective to is become the most rec-ognized and respected brand of coffee in the world. To achievethis goal, Starbucks plans to continue to expand its retail oper-ations rapidly in two ways: first, to increase its market share inexisting markets, and second, to open stores in new markets.In 2004 alone, Starbucks opened 4 stores a day on average.Starbucks’ retail objective is to become a leading retailer andcoffee brand in each of its target markets by selling first-qualitycoffees and related products. In addition, Starbucks providesa superior level of customer service, thereby building a highdegree of customer loyalty.

SALES AND PROFITS

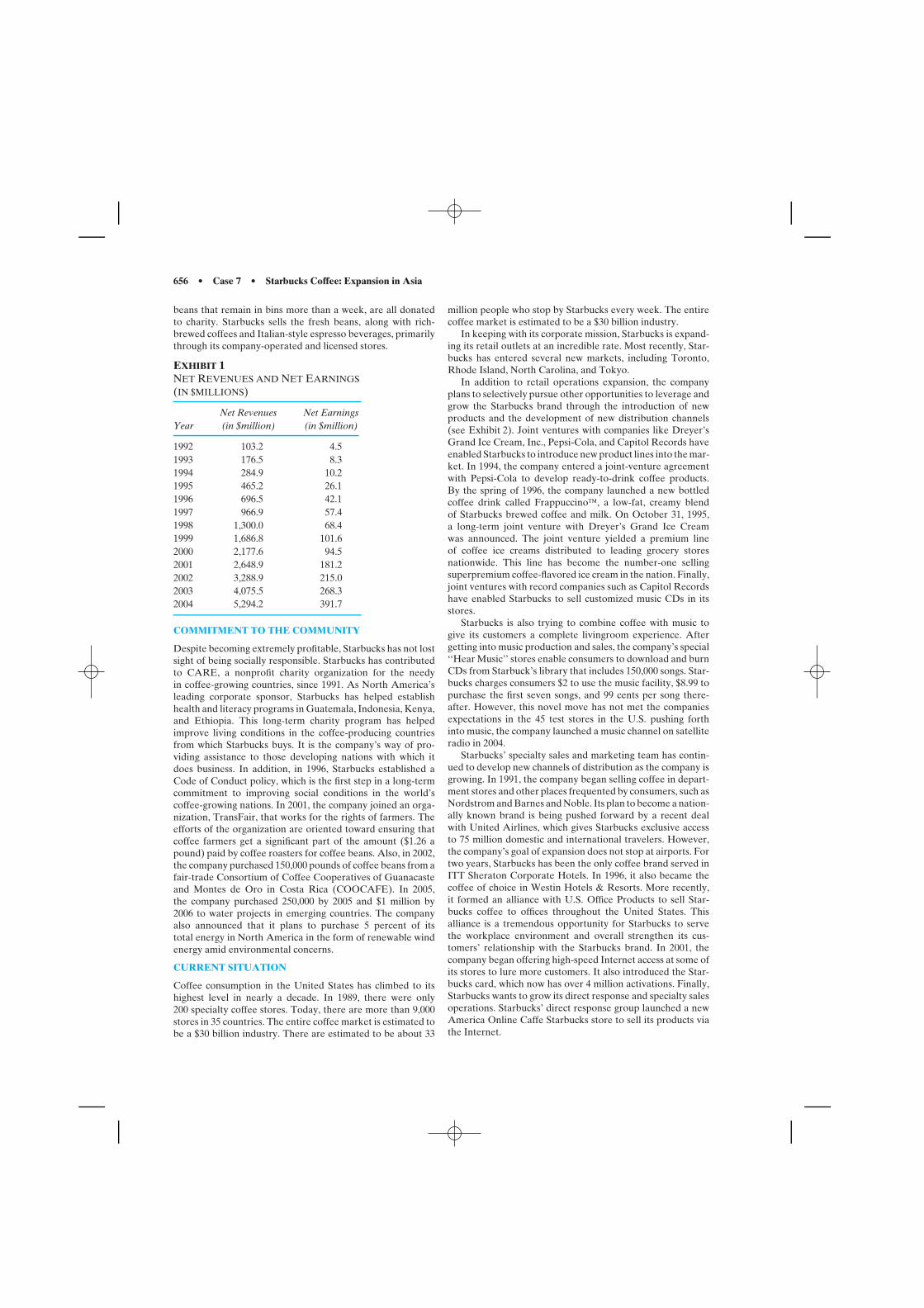

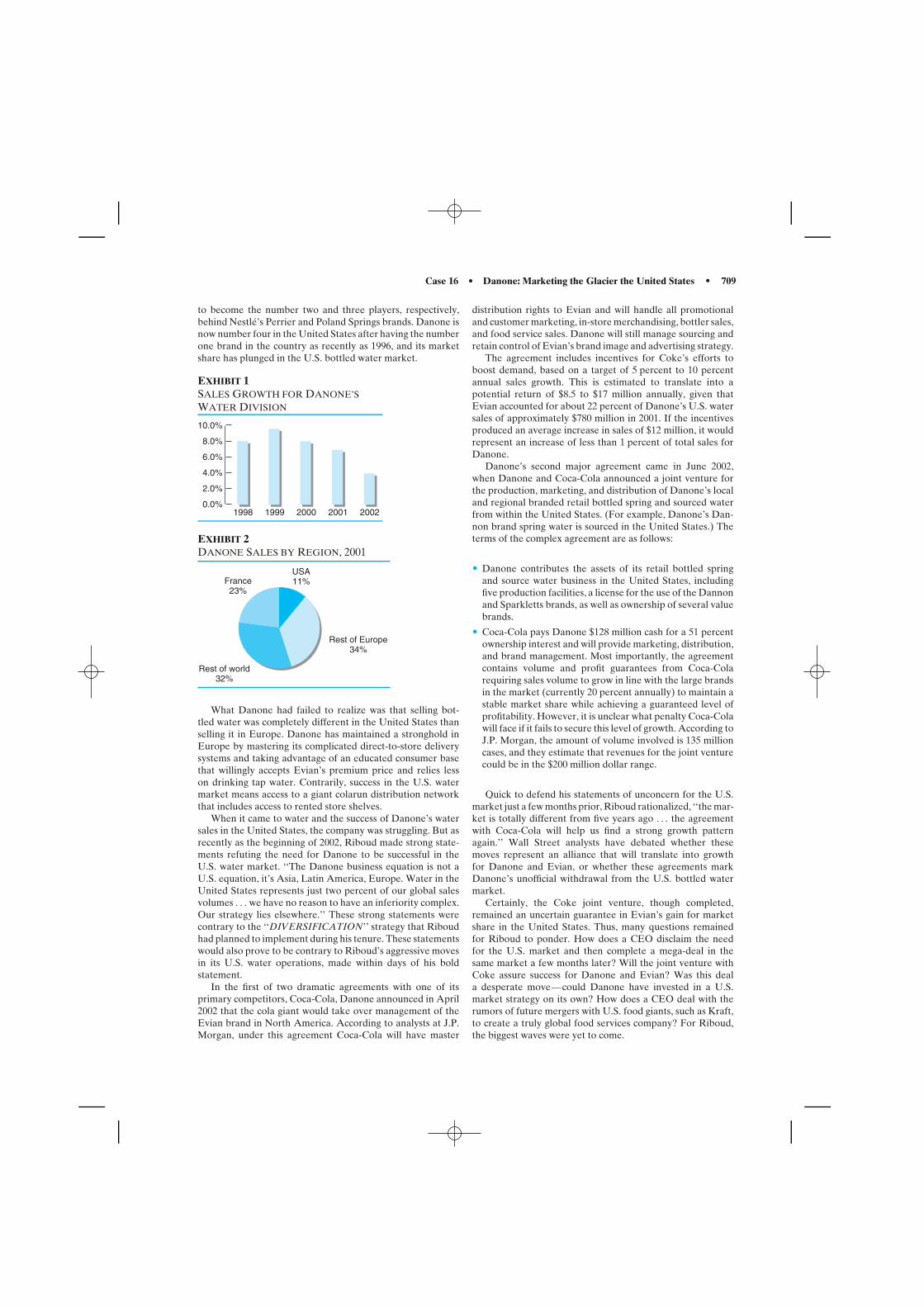

Starbucks’ net earnings in 2004 were $391.7 million, which isa significant increase from the $181.2 million earnings threeyears earlier. Furthermore, its revenues grew more than 12times from $103.2 million in 1992 to $1.3 billion in 1998.The increase in revenues and sales was a direct result of thenumerous new stores that were opened. During this period,Starbucks stores grew 508 percent from 165 stores to over 1400.By the third quarter of the year 2004, sales had increased 30percent over those of the previous year to $5.34 billion. Thecompany’s stock saw a rise of over 2200 percent in the lastdecade (see Exhibit 1).

COMMITMENT TO COFFEE

Starbucks is committed to selling only the finest whole-beancoffees and coffee beverages. Currently the fifth largest pur-chaser of coffee, Starbucks roasts more than 30 varieties ofthe world’s finest Arabica coffee beans; therefore, the com-pany goes to extreme lengths to buy the very finest Arabicacoffee beans available on the world market, regardless ofprice. Arabica beans have a very refined flavor and containabout 1 percent caffeine by weight. These beans account for75 percent of the world production and are sought by specialtyroasters.

To ensure compliance with its rigorous standards, Star-bucks is vertically integrated, controlling its coffee sourcing,roasting, and distribution through its company-operated retailstores. It purchases green coffee beans for its many blends andvarieties from coffee-producing regions throughout the worldand custom roasts them to its exacting standards. Currently,there are three roasting plants in the United States. Roaststhat do not meet the company’s rigorous specifications, or

656 • Case 7 • Starbucks Coffee: Expansion in Asia

beans that remain in bins more than a week, are all donatedto charity. Starbucks sells the fresh beans, along with rich-brewed coffees and Italian-style espresso beverages, primarilythrough its company-operated and licensed stores.

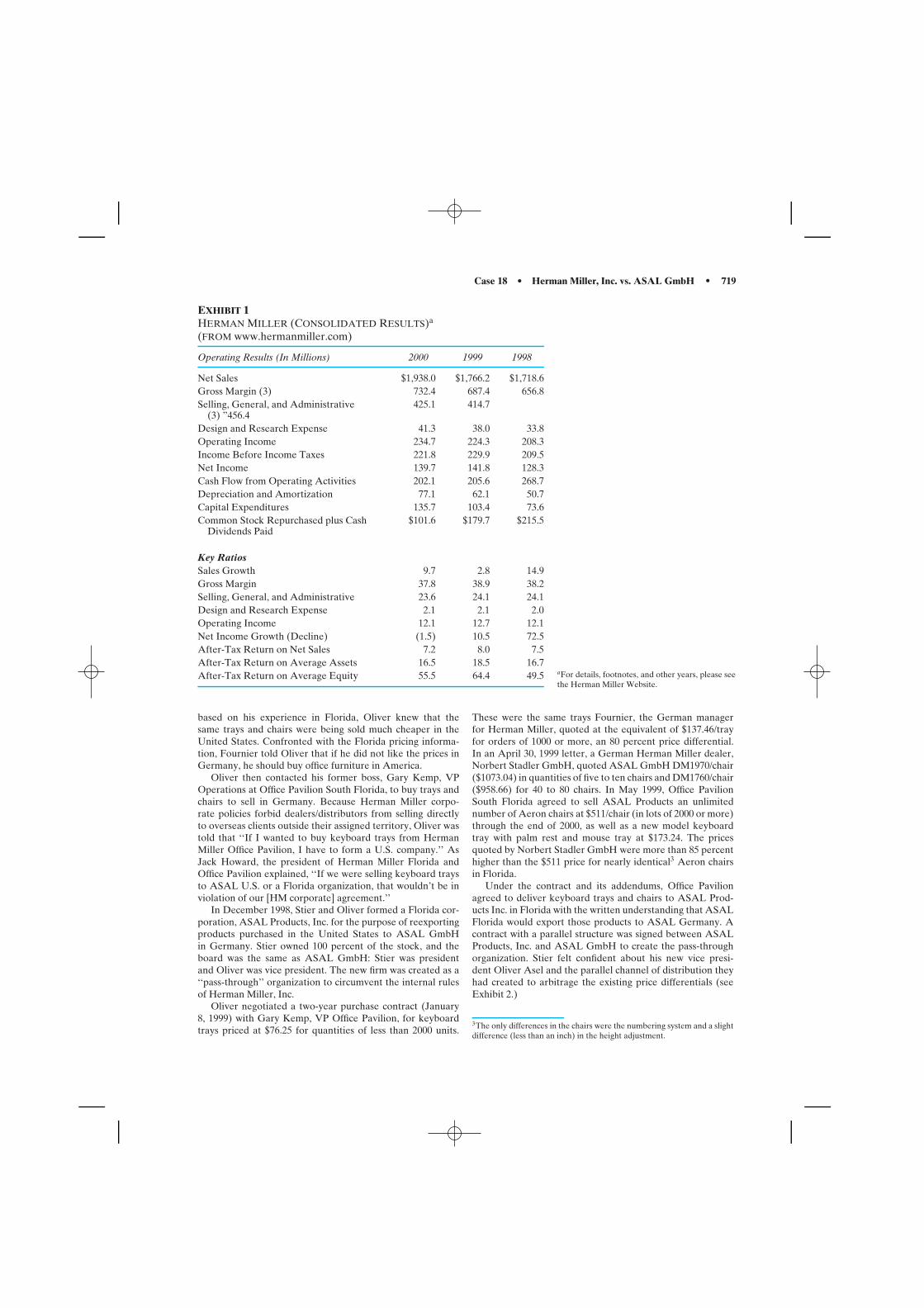

EXHIBIT 1NET REVENUES AND NET EARNINGS(IN $MILLIONS)

Net Revenues Net EarningsYear (in $million) (in $million)

1992 103.2 4.51993 176.5 8.31994 284.9 10.21995 465.2 26.11996 696.5 42.11997 966.9 57.41998 1,300.0 68.41999 1,686.8 101.62000 2,177.6 94.52001 2,648.9 181.22002 3,288.9 215.02003 4,075.5 268.32004 5,294.2 391.7

COMMITMENT TO THE COMMUNITY

Despite becoming extremely profitable, Starbucks has not lostsight of being socially responsible. Starbucks has contributedto CARE, a nonprofit charity organization for the needyin coffee-growing countries, since 1991. As North America’sleading corporate sponsor, Starbucks has helped establishhealth and literacy programs in Guatemala, Indonesia, Kenya,and Ethiopia. This long-term charity program has helpedimprove living conditions in the coffee-producing countriesfrom which Starbucks buys. It is the company’s way of pro-viding assistance to those developing nations with which itdoes business. In addition, in 1996, Starbucks established aCode of Conduct policy, which is the first step in a long-termcommitment to improving social conditions in the world’scoffee-growing nations. In 2001, the company joined an orga-nization, TransFair, that works for the rights of farmers. Theefforts of the organization are oriented toward ensuring thatcoffee farmers get a significant part of the amount ($1.26 apound) paid by coffee roasters for coffee beans. Also, in 2002,the company purchased 150,000 pounds of coffee beans from afair-trade Consortium of Coffee Cooperatives of Guanacasteand Montes de Oro in Costa Rica (COOCAFE). In 2005,the company purchased 250,000 by 2005 and $1 million by2006 to water projects in emerging countries. The companyalso announced that it plans to purchase 5 percent of itstotal energy in North America in the form of renewable windenergy amid environmental concerns.

CURRENT SITUATION

Coffee consumption in the United States has climbed to itshighest level in nearly a decade. In 1989, there were only200 specialty coffee stores. Today, there are more than 9,000stores in 35 countries. The entire coffee market is estimated tobe a $30 billion industry. There are estimated to be about 33

million people who stop by Starbucks every week. The entirecoffee market is estimated to be a $30 billion industry.

In keeping with its corporate mission, Starbucks is expand-ing its retail outlets at an incredible rate. Most recently, Star-bucks has entered several new markets, including Toronto,Rhode Island, North Carolina, and Tokyo.

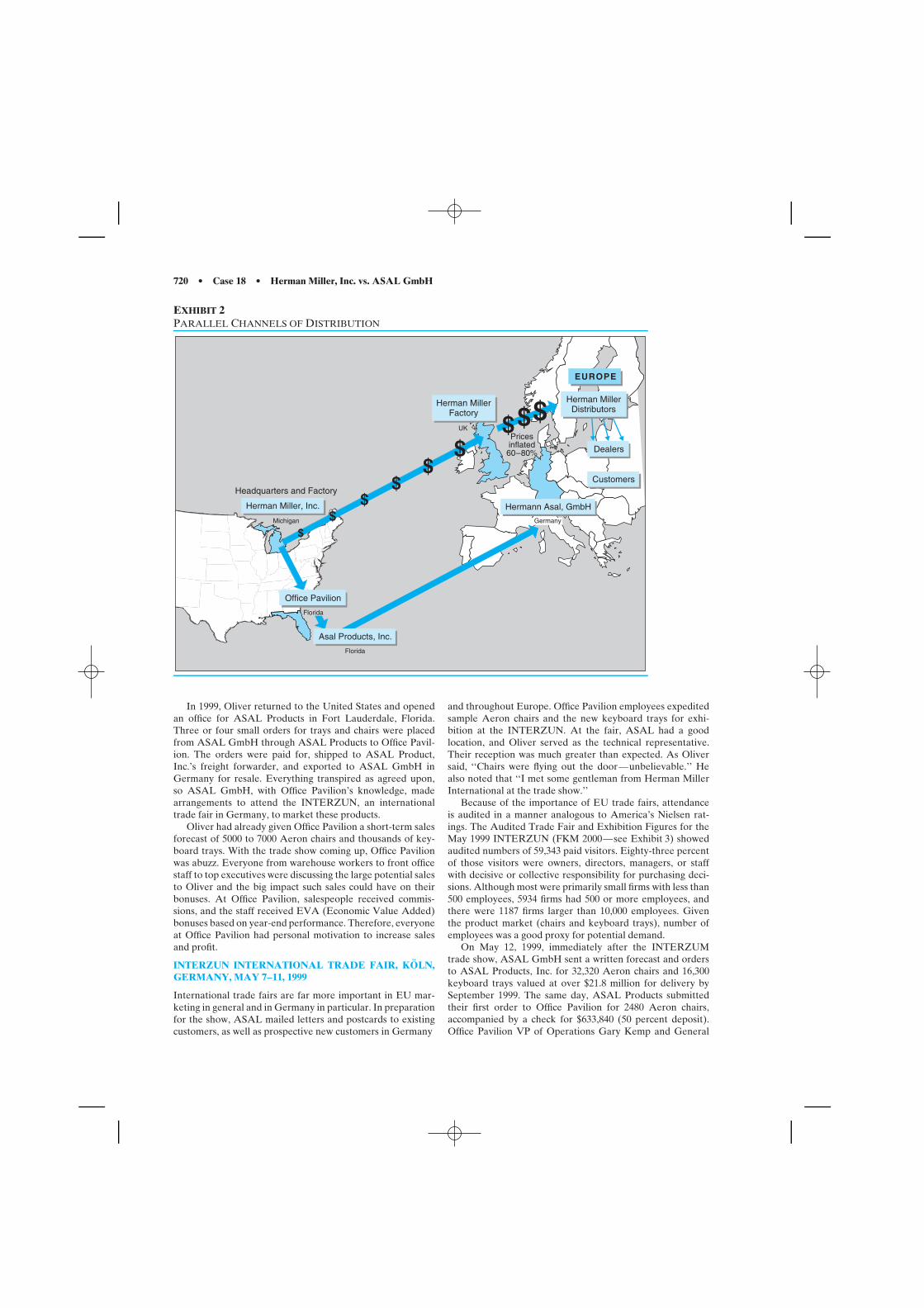

In addition to retail operations expansion, the companyplans to selectively pursue other opportunities to leverage andgrow the Starbucks brand through the introduction of newproducts and the development of new distribution channels(see Exhibit 2). Joint ventures with companies like Dreyer’sGrand Ice Cream, Inc., Pepsi-Cola, and Capitol Records haveenabled Starbucks to introduce new product lines into the mar-ket. In 1994, the company entered a joint-venture agreementwith Pepsi-Cola to develop ready-to-drink coffee products.By the spring of 1996, the company launched a new bottledcoffee drink called Frappuccino, a low-fat, creamy blendof Starbucks brewed coffee and milk. On October 31, 1995,a long-term joint venture with Dreyer’s Grand Ice Creamwas announced. The joint venture yielded a premium lineof coffee ice creams distributed to leading grocery storesnationwide. This line has become the number-one sellingsuperpremium coffee-flavored ice cream in the nation. Finally,joint ventures with record companies such as Capitol Recordshave enabled Starbucks to sell customized music CDs in itsstores.

Starbucks is also trying to combine coffee with music togive its customers a complete livingroom experience. Aftergetting into music production and sales, the company’s special‘‘Hear Music’’ stores enable consumers to download and burnCDs from Starbuck’s library that includes 150,000 songs. Star-bucks charges consumers $2 to use the music facility, $8.99 topurchase the first seven songs, and 99 cents per song there-after. However, this novel move has not met the companiesexpectations in the 45 test stores in the U.S. pushing forthinto music, the company launched a music channel on satelliteradio in 2004.

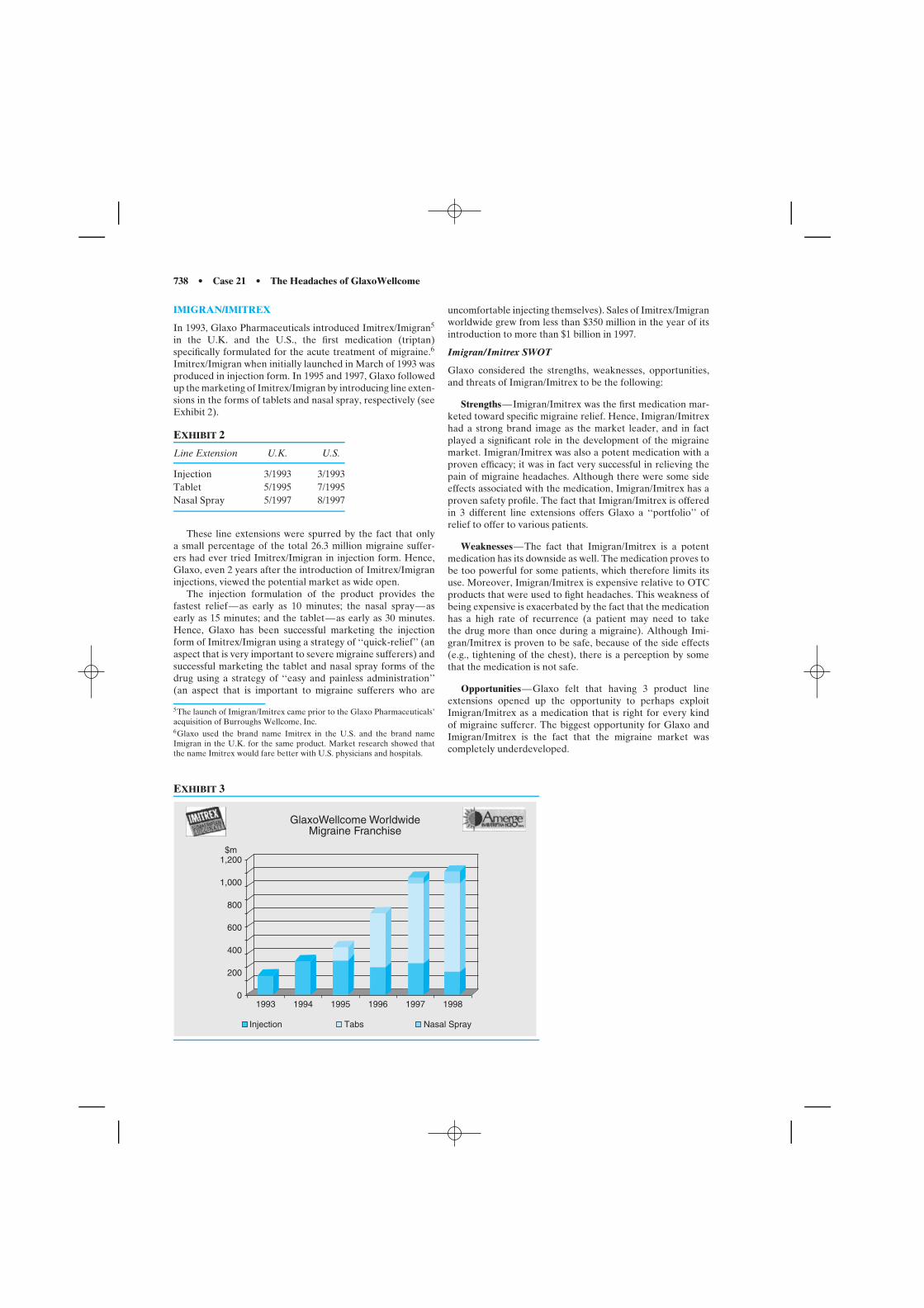

Starbucks’ specialty sales and marketing team has contin-ued to develop new channels of distribution as the company isgrowing. In 1991, the company began selling coffee in depart-ment stores and other places frequented by consumers, such asNordstrom and Barnes and Noble. Its plan to become a nation-ally known brand is being pushed forward by a recent dealwith United Airlines, which gives Starbucks exclusive accessto 75 million domestic and international travelers. However,the company’s goal of expansion does not stop at airports. Fortwo years, Starbucks has been the only coffee brand served inITT Sheraton Corporate Hotels. In 1996, it also became thecoffee of choice in Westin Hotels & Resorts. More recently,it formed an alliance with U.S. Office Products to sell Star-bucks coffee to offices throughout the United States. Thisalliance is a tremendous opportunity for Starbucks to servethe workplace environment and overall strengthen its cus-tomers’ relationship with the Starbucks brand. In 2001, thecompany began offering high-speed Internet access at some ofits stores to lure more customers. It also introduced the Star-bucks card, which now has over 4 million activations. Finally,Starbucks wants to grow its direct response and specialty salesoperations. Starbucks’ direct response group launched a newAmerica Online Caffe Starbucks store to sell its products viathe Internet.

Case 7 • Starbucks Coffee: Expansion in Asia • 657

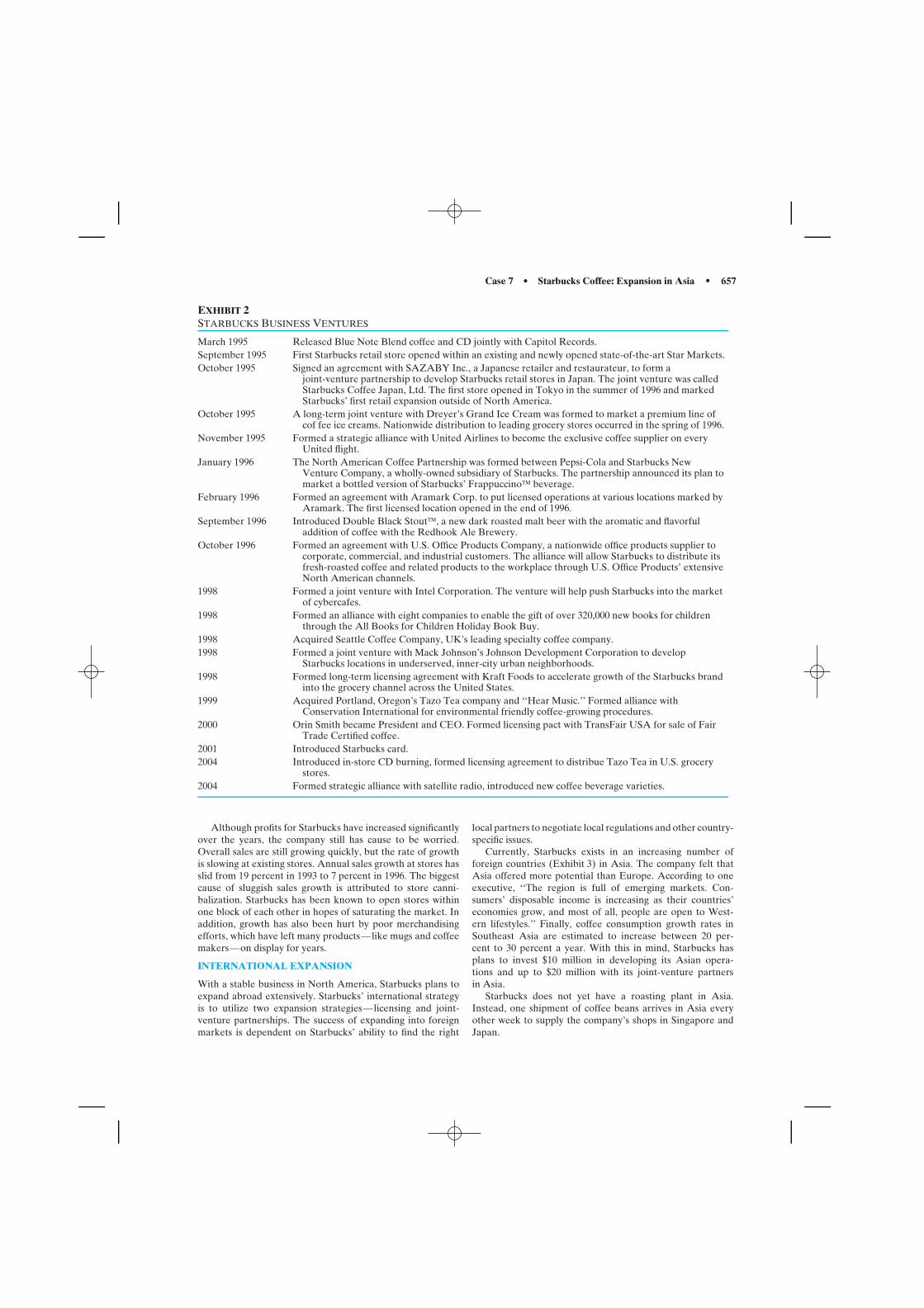

EXHIBIT 2STARBUCKS BUSINESS VENTURES

March 1995 Released Blue Note Blend coffee and CD jointly with Capitol Records.September 1995 First Starbucks retail store opened within an existing and newly opened state-of-the-art Star Markets.October 1995 Signed an agreement with SAZABY Inc., a Japanese retailer and restaurateur, to form a

joint-venture partnership to develop Starbucks retail stores in Japan. The joint venture was calledStarbucks Coffee Japan, Ltd. The first store opened in Tokyo in the summer of 1996 and markedStarbucks’ first retail expansion outside of North America.

October 1995 A long-term joint venture with Dreyer’s Grand Ice Cream was formed to market a premium line ofcof fee ice creams. Nationwide distribution to leading grocery stores occurred in the spring of 1996.

November 1995 Formed a strategic alliance with United Airlines to become the exclusive coffee supplier on everyUnited flight.

January 1996 The North American Coffee Partnership was formed between Pepsi-Cola and Starbucks NewVenture Company, a wholly-owned subsidiary of Starbucks. The partnership announced its plan tomarket a bottled version of Starbucks’ Frappuccino beverage.

February 1996 Formed an agreement with Aramark Corp. to put licensed operations at various locations marked byAramark. The first licensed location opened in the end of 1996.

September 1996 Introduced Double Black Stout, a new dark roasted malt beer with the aromatic and flavorfuladdition of coffee with the Redhook Ale Brewery.

October 1996 Formed an agreement with U.S. Office Products Company, a nationwide office products supplier tocorporate, commercial, and industrial customers. The alliance will allow Starbucks to distribute itsfresh-roasted coffee and related products to the workplace through U.S. Office Products’ extensiveNorth American channels.

1998 Formed a joint venture with Intel Corporation. The venture will help push Starbucks into the marketof cybercafes.

1998 Formed an alliance with eight companies to enable the gift of over 320,000 new books for childrenthrough the All Books for Children Holiday Book Buy.

1998 Acquired Seattle Coffee Company, UK’s leading specialty coffee company.1998 Formed a joint venture with Mack Johnson’s Johnson Development Corporation to develop

Starbucks locations in underserved, inner-city urban neighborhoods.1998 Formed long-term licensing agreement with Kraft Foods to accelerate growth of the Starbucks brand

into the grocery channel across the United States.1999 Acquired Portland, Oregon’s Tazo Tea company and ‘‘Hear Music.’’ Formed alliance with

Conservation International for environmental friendly coffee-growing procedures.2000 Orin Smith became President and CEO. Formed licensing pact with TransFair USA for sale of Fair

Trade Certified coffee.2001 Introduced Starbucks card.2004 Introduced in-store CD burning, formed licensing agreement to distribue Tazo Tea in U.S. grocery

stores.2004 Formed strategic alliance with satellite radio, introduced new coffee beverage varieties.

Although profits for Starbucks have increased significantlyover the years, the company still has cause to be worried.Overall sales are still growing quickly, but the rate of growthis slowing at existing stores. Annual sales growth at stores hasslid from 19 percent in 1993 to 7 percent in 1996. The biggestcause of sluggish sales growth is attributed to store canni-balization. Starbucks has been known to open stores withinone block of each other in hopes of saturating the market. Inaddition, growth has also been hurt by poor merchandisingefforts, which have left many products—like mugs and coffeemakers—on display for years.

INTERNATIONAL EXPANSION

With a stable business in North America, Starbucks plans toexpand abroad extensively. Starbucks’ international strategyis to utilize two expansion strategies—licensing and joint-venture partnerships. The success of expanding into foreignmarkets is dependent on Starbucks’ ability to find the right

local partners to negotiate local regulations and other country-specific issues.

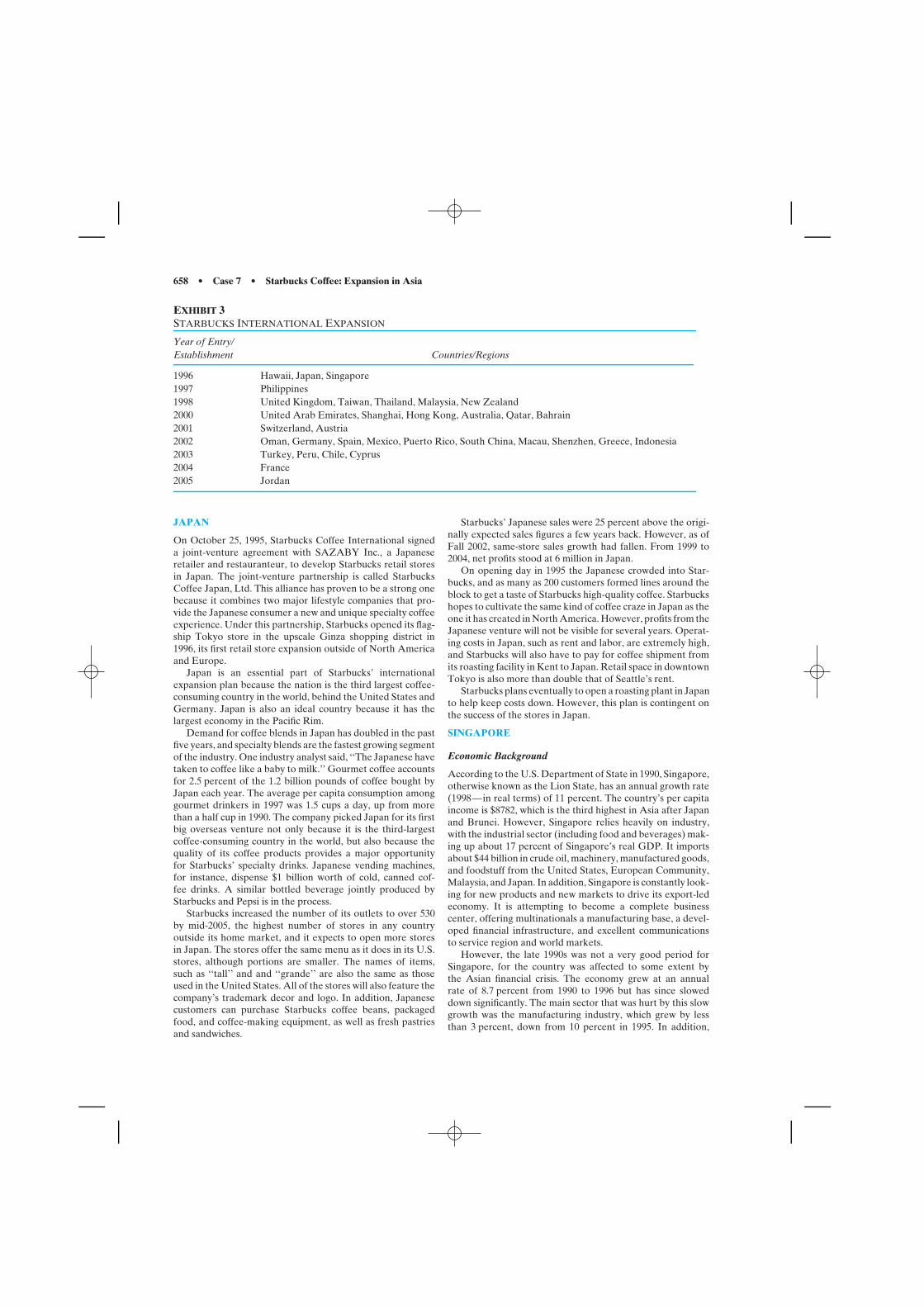

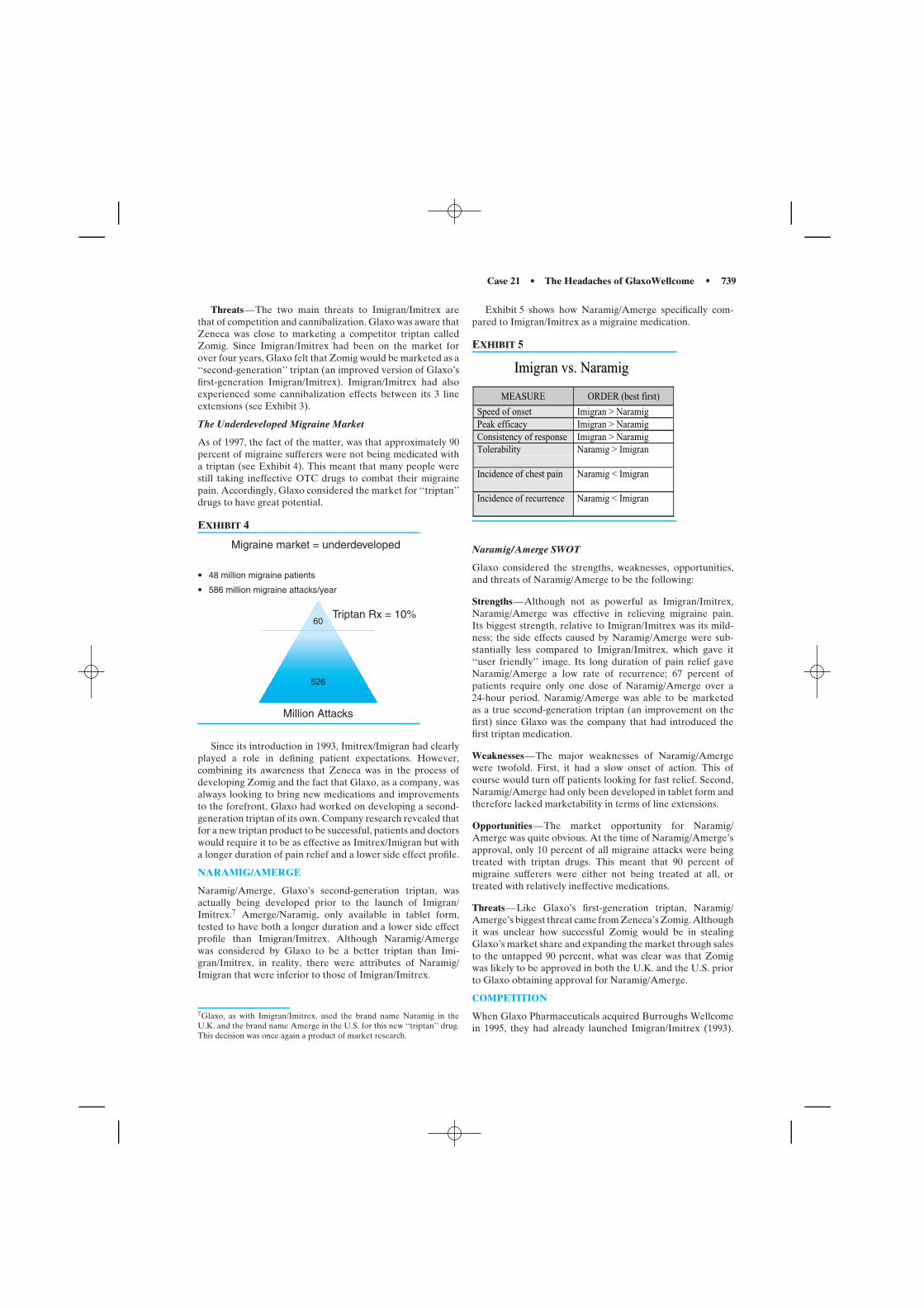

Currently, Starbucks exists in an increasing number offoreign countries (Exhibit 3) in Asia. The company felt thatAsia offered more potential than Europe. According to oneexecutive, ‘‘The region is full of emerging markets. Con-sumers’ disposable income is increasing as their countries’economies grow, and most of all, people are open to West-ern lifestyles.’’ Finally, coffee consumption growth rates inSoutheast Asia are estimated to increase between 20 per-cent to 30 percent a year. With this in mind, Starbucks hasplans to invest $10 million in developing its Asian opera-tions and up to $20 million with its joint-venture partnersin Asia.

Starbucks does not yet have a roasting plant in Asia.Instead, one shipment of coffee beans arrives in Asia everyother week to supply the company’s shops in Singapore andJapan.

658 • Case 7 • Starbucks Coffee: Expansion in Asia

EXHIBIT 3STARBUCKS INTERNATIONAL EXPANSION

Year of Entry/Establishment Countries/Regions

1996 Hawaii, Japan, Singapore1997 Philippines1998 United Kingdom, Taiwan, Thailand, Malaysia, New Zealand2000 United Arab Emirates, Shanghai, Hong Kong, Australia, Qatar, Bahrain2001 Switzerland, Austria2002 Oman, Germany, Spain, Mexico, Puerto Rico, South China, Macau, Shenzhen, Greece, Indonesia2003 Turkey, Peru, Chile, Cyprus2004 France2005 Jordan

JAPAN

On October 25, 1995, Starbucks Coffee International signeda joint-venture agreement with SAZABY Inc., a Japaneseretailer and restauranteur, to develop Starbucks retail storesin Japan. The joint-venture partnership is called StarbucksCoffee Japan, Ltd. This alliance has proven to be a strong onebecause it combines two major lifestyle companies that pro-vide the Japanese consumer a new and unique specialty coffeeexperience. Under this partnership, Starbucks opened its flag-ship Tokyo store in the upscale Ginza shopping district in1996, its first retail store expansion outside of North Americaand Europe.

Japan is an essential part of Starbucks’ internationalexpansion plan because the nation is the third largest coffee-consuming country in the world, behind the United States andGermany. Japan is also an ideal country because it has thelargest economy in the Pacific Rim.

Demand for coffee blends in Japan has doubled in the pastfive years, and specialty blends are the fastest growing segmentof the industry. One industry analyst said, ‘‘The Japanese havetaken to coffee like a baby to milk.’’ Gourmet coffee accountsfor 2.5 percent of the 1.2 billion pounds of coffee bought byJapan each year. The average per capita consumption amonggourmet drinkers in 1997 was 1.5 cups a day, up from morethan a half cup in 1990. The company picked Japan for its firstbig overseas venture not only because it is the third-largestcoffee-consuming country in the world, but also because thequality of its coffee products provides a major opportunityfor Starbucks’ specialty drinks. Japanese vending machines,for instance, dispense $1 billion worth of cold, canned cof-fee drinks. A similar bottled beverage jointly produced byStarbucks and Pepsi is in the process.

Starbucks increased the number of its outlets to over 530by mid-2005, the highest number of stores in any countryoutside its home market, and it expects to open more storesin Japan. The stores offer the same menu as it does in its U.S.stores, although portions are smaller. The names of items,such as ‘‘tall’’ and and ‘‘grande’’ are also the same as thoseused in the United States. All of the stores will also feature thecompany’s trademark decor and logo. In addition, Japanesecustomers can purchase Starbucks coffee beans, packagedfood, and coffee-making equipment, as well as fresh pastriesand sandwiches.

Starbucks’ Japanese sales were 25 percent above the origi-nally expected sales figures a few years back. However, as ofFall 2002, same-store sales growth had fallen. From 1999 to2004, net profits stood at 6 million in Japan.

On opening day in 1995 the Japanese crowded into Star-bucks, and as many as 200 customers formed lines around theblock to get a taste of Starbucks high-quality coffee. Starbuckshopes to cultivate the same kind of coffee craze in Japan as theone it has created in North America. However, profits from theJapanese venture will not be visible for several years. Operat-ing costs in Japan, such as rent and labor, are extremely high,and Starbucks will also have to pay for coffee shipment fromits roasting facility in Kent to Japan. Retail space in downtownTokyo is also more than double that of Seattle’s rent.

Starbucks plans eventually to open a roasting plant in Japanto help keep costs down. However, this plan is contingent onthe success of the stores in Japan.

SINGAPORE

Economic Background

According to the U.S. Department of State in 1990, Singapore,otherwise known as the Lion State, has an annual growth rate(1998—in real terms) of 11 percent. The country’s per capitaincome is $8782, which is the third highest in Asia after Japanand Brunei. However, Singapore relies heavily on industry,with the industrial sector (including food and beverages) mak-ing up about 17 percent of Singapore’s real GDP. It importsabout $44 billion in crude oil, machinery, manufactured goods,and foodstuff from the United States, European Community,Malaysia, and Japan. In addition, Singapore is constantly look-ing for new products and new markets to drive its export-ledeconomy. It is attempting to become a complete businesscenter, offering multinationals a manufacturing base, a devel-oped financial infrastructure, and excellent communicationsto service region and world markets.

However, the late 1990s was not a very good period forSingapore, for the country was affected to some extent bythe Asian financial crisis. The economy grew at an annualrate of 8.7 percent from 1990 to 1996 but has since sloweddown significantly. The main sector that was hurt by this slowgrowth was the manufacturing industry, which grew by lessthan 3 percent, down from 10 percent in 1995. In addition,

Case 7 • Starbucks Coffee: Expansion in Asia • 659

the commerce sector grew by less than 4 percent, down from9 percent in 1995. Analysts claim that weak economic growth,global competition, and a very slow tourist season made Singa-pore’s retail industry very sluggish. The restaurants and hotelsalso recorded weak growth.

LIVING IN SINGAPORE

Singapore has one of the best living conditions in Asia. In 1999,its per capita GNP was US$27,480. Furthermore, Singaporeis known for its diversity. There are 3.4 million Singapore-ans: ethnic Chinese, Malays, and Indians make 77 percent,14 percent, and 7 percent of the population, respectively. Themost practiced religions are Buddhism/Taoism (53.9 percent),Islam (14.9 percent), Christianity (12.9 percent) and Hin-duism (3.3 percent). The main languages are Malay, Chinese(Mandarin), Tamil, and English. English is the language ofadministration, whereas Malay is the national language.

With a moderately high cost of living, Singaporeans areable to indulge in luxury goods. Much of Singapore’s enter-tainment is influenced by Western culture. For instance, manytheaters show Broadway musicals such as Les Miserablesand feature pop concert artists like Michael Jackson. Televi-sion programs are in English, Chinese, Malay, and Tamil. In1992, pay TV channels such as CNN, Movievision, HBO, andChinese Variety were introduced.

Singaporeans are known to indulge themselves with food.‘‘So discriminating have the Singaporeans become on the sub-ject of quality and price that eating has become a nationalobsession.’’ Singapore has an array of restaurants, coffee-houses, fast-food outlets, and food centers that are easilyaccessible and offer a variety of foods at affordable prices.Most of these food places are not air-conditioned exceptfor those located in shopping complexes. However, eating inan air-conditioned restaurant, regardless of income level, isan affordable luxury. ‘‘The average lunch or high tea buffetspread offering a wide variety of dishes is available at manyhotel coffee houses and restaurants, and it costs about $15(Singaporean currency) or more per person. Most restaurantsand coffeehouses impose a 10 percent service charge, buttipping is not encouraged.’’

SINGAPORE’S LOVE AFFAIR WITH COFFEE

According to Singaporean social commentator Francis Yim,‘‘Coffeehouses are a sign that Singaporeans have achieved thestatus of a developed nation and we are breaking new groundin the area of becoming a cultured society.’’ In the past duringthe construction of Singapore, Singaporeans did not have thetime to enjoy their cup of java. Regardless of their religionand beliefs, Singaporeans went to coffeehouses in the eveningsfor their meals and drank coffee in order to keep themselvesawake. Now coffee is viewed as a beverage instead of a drink.People want to take the time to savor their coffee. It is not justa drink but a personality altogether. The various flavors thatcoffeehouses offer reflect the different moods as well as taste.

The first Starbucks coffee outlet in Singapore opened onDecember 14, 1996, in Liat Towers, with the help of BonStarPte. Ltd., a subsidiary of Bonvests Holding Ltd., a Singaporeancompany with food services and real estate interests. The storein Liat Towers is located in Singapore’s main shopping districton Orchard Road, which is a very trendy shopping centerincluding the French department store, Gallery Lafayette,

and Planet Hollywood. There are plans to open 10 to 12 moreStarbucks in Singapore within the next year. Currently, thelicensing agreement with Starbucks only covers Singapore,but Bonvests hopes to expand the franchises into other Asianmarkets. Starbucks’ venture into Singapore is its first expan-sion into Southeast Asia. Bonvests Holdings anticipates thatthe Starbucks retail stores will generate at least $40 million insales over the next five to six years.

Bonvests is an ideal partner for several reasons. Bonvestshas acquired expertise in running food businesses, such as thelocal Burger King chain. They also know and understand thelocal consumer market, government regulations, and the localreal estate market.

Starbucks chose Singapore for its entry in the SoutheastAsian market because of the highly ‘‘Westernized’’ ideas andlifestyles it had adopted. Some have described Starbucks asanother American icon, like McDonald’s. Some even say thatStarbucks has created an American coffee cult. Slowly, butsurely, gourmet coffee bars have been penetrating into thefood scene in Singapore. It is estimated that Singaporeansdrink more than 10,000 gourmet cups a day. In addition,the market in Singapore has tremendous growth potential.According to Bruce Rolph, head of research at SalomanBrothers Singapore Pte. Ltd., ‘‘People should increasinglyfocus on Singapore not as a mature market with low earningsand growth potential, but as a uniquely positioned beachheadto get leverage over what’s happening in Asia.’’ Finally, theSingaporean market still has no clear leader in the specialtycoffee industry. This means that Starbucks still has a goodchance to become one of the top contenders in this market.

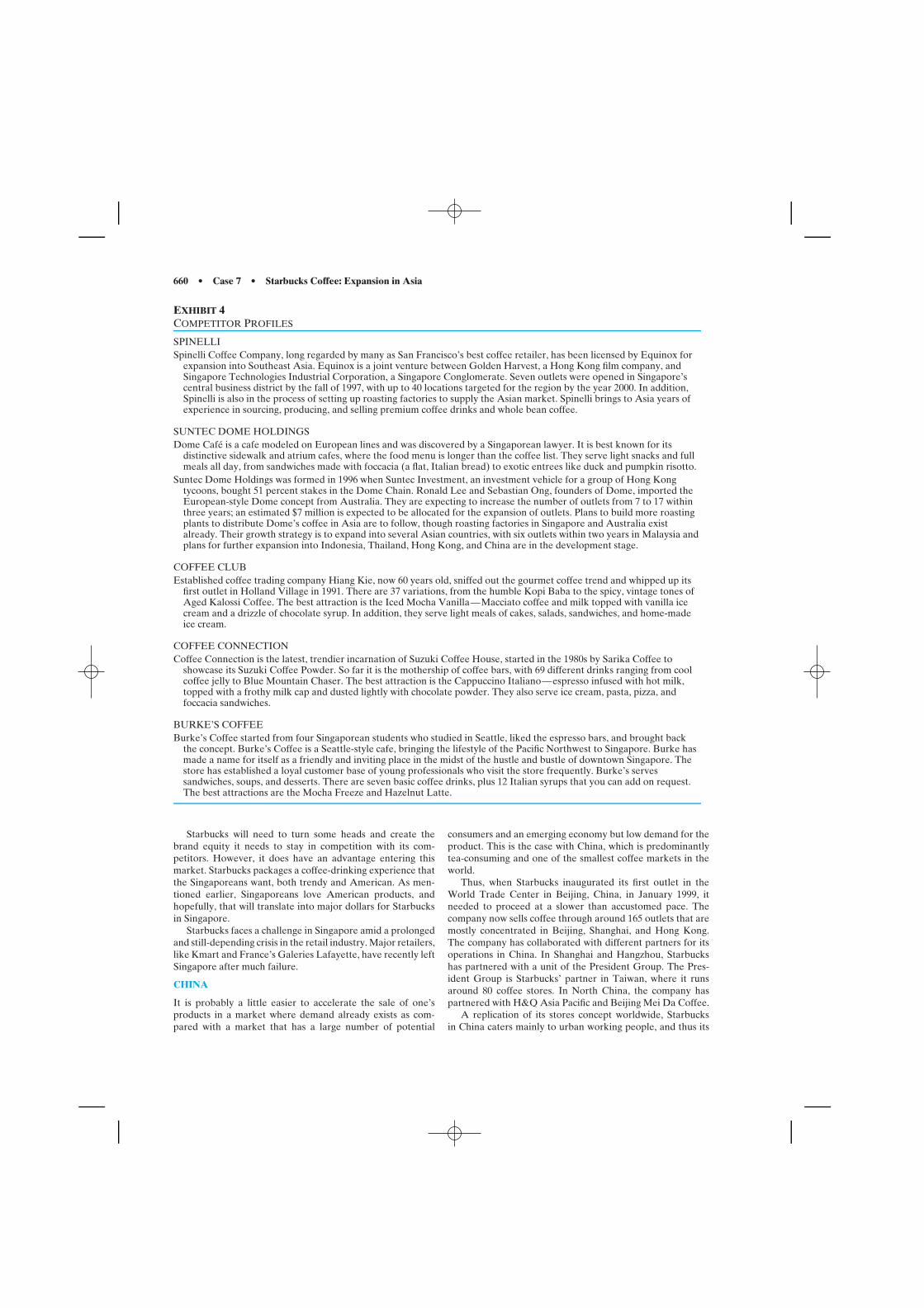

Despite the opportunities that exist for Starbucks in Sin-gapore, Starbucks still must overcome certain obstacles tobe successful. Competition is fierce, with 14 players and 38stores between them (see Exhibit 4). With Starbucks entryinto the Asian market, bigger retail stores, like Suntec DomeHoldings, are already gearing up for a coffee battle. However,smaller companies like Burke’s Cafe and Spinelli are welcom-ing Starbucks’ entry. Their strategy is to open an outlet rightnext to Starbucks to attract the customers that overflow fromStarbucks.

One of Starbucks’ biggest competitors, Suntec Dome Hold-ings, has already established itself in Singapore. It already hasgood name recognition with Suntec Walk, Suntec City, DomeCafe, and so on. Suntec is distinctive from the other retailcoffee stores in that it is seen more as a restaurant than as acoffee chain. It targets a broader market segment with a lowerbudget range. They are also backed by major supporters withthe capital to counter Starbucks’ expansion strategy. In addi-tion to Singapore, Suntec Dome Holdings has plans to expandto other markets such as Malaysia, Indonesia, Thailand, HongKong, and China. Spinelli, a smaller competitor, also plansto expand into the region. With these expansion plans havingbeen completed by the year 2000, Spinelli is potentially amajor threat to Starbucks.

More well-known coffee spots to Singaporeans are CoffeeConnection and Coffee Club, which are also direct competitorsof Starbucks. The customers that go to Coffee Connection andCoffee Club like the atmosphere and the service they receivethere. As reflected here, Singapore has seen a proliferationof gourmet coffee outlets in the past few years; therefore, themarket is slowly becoming overcrowded.

660 • Case 7 • Starbucks Coffee: Expansion in Asia

EXHIBIT 4COMPETITOR PROFILES

SPINELLISpinelli Coffee Company, long regarded by many as San Francisco’s best coffee retailer, has been licensed by Equinox for

expansion into Southeast Asia. Equinox is a joint venture between Golden Harvest, a Hong Kong film company, andSingapore Technologies Industrial Corporation, a Singapore Conglomerate. Seven outlets were opened in Singapore’scentral business district by the fall of 1997, with up to 40 locations targeted for the region by the year 2000. In addition,Spinelli is also in the process of setting up roasting factories to supply the Asian market. Spinelli brings to Asia years ofexperience in sourcing, producing, and selling premium coffee drinks and whole bean coffee.

SUNTEC DOME HOLDINGSDome Cafe is a cafe modeled on European lines and was discovered by a Singaporean lawyer. It is best known for its

distinctive sidewalk and atrium cafes, where the food menu is longer than the coffee list. They serve light snacks and fullmeals all day, from sandwiches made with foccacia (a flat, Italian bread) to exotic entrees like duck and pumpkin risotto.

Suntec Dome Holdings was formed in 1996 when Suntec Investment, an investment vehicle for a group of Hong Kongtycoons, bought 51 percent stakes in the Dome Chain. Ronald Lee and Sebastian Ong, founders of Dome, imported theEuropean-style Dome concept from Australia. They are expecting to increase the number of outlets from 7 to 17 withinthree years; an estimated $7 million is expected to be allocated for the expansion of outlets. Plans to build more roastingplants to distribute Dome’s coffee in Asia are to follow, though roasting factories in Singapore and Australia existalready. Their growth strategy is to expand into several Asian countries, with six outlets within two years in Malaysia andplans for further expansion into Indonesia, Thailand, Hong Kong, and China are in the development stage.

COFFEE CLUBEstablished coffee trading company Hiang Kie, now 60 years old, sniffed out the gourmet coffee trend and whipped up its

first outlet in Holland Village in 1991. There are 37 variations, from the humble Kopi Baba to the spicy, vintage tones ofAged Kalossi Coffee. The best attraction is the Iced Mocha Vanilla—Macciato coffee and milk topped with vanilla icecream and a drizzle of chocolate syrup. In addition, they serve light meals of cakes, salads, sandwiches, and home-madeice cream.

COFFEE CONNECTIONCoffee Connection is the latest, trendier incarnation of Suzuki Coffee House, started in the 1980s by Sarika Coffee to

showcase its Suzuki Coffee Powder. So far it is the mothership of coffee bars, with 69 different drinks ranging from coolcoffee jelly to Blue Mountain Chaser. The best attraction is the Cappuccino Italiano—espresso infused with hot milk,topped with a frothy milk cap and dusted lightly with chocolate powder. They also serve ice cream, pasta, pizza, andfoccacia sandwiches.

BURKE’S COFFEEBurke’s Coffee started from four Singaporean students who studied in Seattle, liked the espresso bars, and brought back

the concept. Burke’s Coffee is a Seattle-style cafe, bringing the lifestyle of the Pacific Northwest to Singapore. Burke hasmade a name for itself as a friendly and inviting place in the midst of the hustle and bustle of downtown Singapore. Thestore has established a loyal customer base of young professionals who visit the store frequently. Burke’s servessandwiches, soups, and desserts. There are seven basic coffee drinks, plus 12 Italian syrups that you can add on request.The best attractions are the Mocha Freeze and Hazelnut Latte.

Starbucks will need to turn some heads and create thebrand equity it needs to stay in competition with its com-petitors. However, it does have an advantage entering thismarket. Starbucks packages a coffee-drinking experience thatthe Singaporeans want, both trendy and American. As men-tioned earlier, Singaporeans love American products, andhopefully, that will translate into major dollars for Starbucksin Singapore.

Starbucks faces a challenge in Singapore amid a prolongedand still-depending crisis in the retail industry. Major retailers,like Kmart and France’s Galeries Lafayette, have recently leftSingapore after much failure.

CHINA

It is probably a little easier to accelerate the sale of one’sproducts in a market where demand already exists as com-pared with a market that has a large number of potential

consumers and an emerging economy but low demand for theproduct. This is the case with China, which is predominantlytea-consuming and one of the smallest coffee markets in theworld.

Thus, when Starbucks inaugurated its first outlet in theWorld Trade Center in Beijing, China, in January 1999, itneeded to proceed at a slower than accustomed pace. Thecompany now sells coffee through around 165 outlets that aremostly concentrated in Beijing, Shanghai, and Hong Kong.The company has collaborated with different partners for itsoperations in China. In Shanghai and Hangzhou, Starbuckshas partnered with a unit of the President Group. The Pres-ident Group is Starbucks’ partner in Taiwan, where it runsaround 80 coffee stores. In North China, the company haspartnered with H&Q Asia Pacific and Beijing Mei Da Coffee.

A replication of its stores concept worldwide, Starbucksin China caters mainly to urban working people, and thus its

Case 8 • Gap Inc. • 661

outlets are located in commercial areas. As for advertisingfor the Chinese market, Starbucks depends less on domesticadvertising and more on promotion through coupons and vis-its, which draw first-time consumers. Hence, although it facesa challenging task, the company is determined to carve a nichefor itself in China’s beverage market. In 2005, the companyannounced that in the long term, it expects the Chinese marketto be its second largest in the U.S.

INDONESIA

In 2002, Starbucks launched its first coffee store in Jakarta,Indonesia, after signing a licensing agreement with PT SariCoffee Indonesia. It is housed on the ground floor of the PlazaIndonesia, an upscale fashion shopping center, and boasts ofthe familiar Starbucks atmosphere of coffee, conversation,and more. The company plans to expand its operations inIndonesia based on the response it gets to its first store.

� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

CASE 8

GAP INC.

Since it started in 1969, Gap Inc. has been consistently grow-ing and expanding. With more than 3000 stores in the UnitedStates, Canada, the United Kingdom, France, and Japan, GapInc. is currently the second largest-selling brand in the worldand is ranked second among all U.S. retailers in sales.

A HISTORY OF GAP INC.

Gap Inc. was established in August 1969 by Donald G. Fisher,a real estate developer educated at the University of Califor-nia–Berkeley. Fisher conceived the idea when he went to adepartment store to exchange a pair of Levi’s and was unableto because the jeans department was so disorganized. Backedby a $63,000 family investment and a $112,000 bank loanguaranteed by his father-in-law, Donald Fisher introduced thefirst Gap store in San Francisco. His original idea was to focuson the mid-teen market with three types of goods: records,cassette tapes, and Levi’s jeans. Unlike the local departmentstores, which stocked only a limited number of styles and sizesof Levi’s jeans, the Gap store carried every size and styleavailable. Furthermore, they were neatly arranged and easyto find. Donald Fisher and his wife had a discussion about the‘‘generation gap’’ in 1969, and from that discussion came thename Gap Inc., under which the company was incorporated inCalifornia in July 1969. Gap Inc. was reincorporated in 1988under the laws of Delaware.

GROWTH AND EXPANSION

Although the original targeted customers were primarilyyoung people, the convenience of a neatly organized jeansstore with Levi’s products attracted customers of all ages. Inless than one year, Gap’s business took off, and a second Gapwas opened in San Jose. In less than two years, there were sixGap stores in California. By 1972, Gap Inc. had 25 stores in sixstates. In 1973, Gap Inc. ventured into the East Coast market,opening 12 stores in New York, New Jersey, and Pennsylvania.In 1974, Gap expanded into Washington, Minnesota, Missouri,Oklahoma, Maryland, Virginia, Georgia, Arizona, Texas, andIllinois, with a total of 90 stores. In 1976, Gap Inc. wentpublic with its stocks, offering 1.2 million shares on the NewYork and Pacific stock exchanges, selling at 75 cents a share.

This case was prepared by Masaaki Kotabe and updated by Sonia Ketkarfor class discussion rather than to illustrate either effective or ineffectivemanagement of a situation described (2006).

In 1979, Gap Inc. opened a modern distribution facility inDenver, Colorado. By 1981, Gap Inc. had opened 500 storesnationwide. In 1983, Gap Inc. purchased Banana Republic, atravel clothing company that sold mainly through catalogs. By1985, there were 613 Gap stores and 35 Banana Republics.The first GapKids store was introduced in 1987; then in 1988,the Old Navy Clothing Company was first introduced. In thesame year, Gap opened two factory outlets selling merchan-dise at discount prices. In 1990, GapKids formed a separatedepartment for baby clothing called BabyGap. In 1992, Gapstores also formed a separate department called Gap Shoes.The year 1993 was marked by the opening of Gap warehouseor outlet stores as well as an entry into the French market. OldNavy was started in 1994, and the following years witnessedthe introduction of online Gap Maternity and the launch ofthe e-businesses of Gap, Banana Republic, and Old Navy.

As of 2005, the company operated:

• 3,010 stores in the United States, Canada, United Kingdom,and Japan.

• 462 Banana Republic stores, including 18 in Canada.

• 907 Old Navy stores.

• the total number of stores in:

United Kingdom 134Canada 173France 33Japan 84

SELLING PRIVATE STORE BRAND PRODUCT

Within three months of opening the Gap, Fisher realized thatthe real business was in selling Levi’s jeans, so he dropped therecords and cassette tapes from his inventory. Until the end of1973, Gap advertised and carried only Levi’s brand products.In 1974, Gap introduced its first private-label clothing intothe merchandising mix. When price maintenance crumbledbecause of a Federal Trade Commission directive in 1976,Levi’s products began to sell at discount, and Fisher was con-vinced that Gap’s competitive advantage could not rely solelyon the low prices of Levi’s products. Since then, he has focusedon reducing Gap’s reliance on sales of Levi’s products. As aresult, Levi’s products began to decrease as a percentage ofGap’s total sales. By 1987, Levi’s made up less than 50 per-cent of Gap’s total sales. By 1985, Levi’s sales dropped to 21

662 • Case 8 • Gap Inc.

percent of Gap’s total sales, then 14 percent in 1987. Finally, in1990, Gap dropped Levi’s altogether and started selling onlyprivate-labeled products.

GAP INC. OPERATING COMPONENTS

Gap Inc. is a specialty retailer that operates stores sellingcasual apparel, shoes, and other accessories for men, women,and children. It includes the following registered trade names:Gap, GapKids, BabyGap, Gap Shoes, Gap Maternity, BananaRepublic, and Old Navy Clothing Company. In April 2005,Gap Inc. announced the launch of its newest brand, Forth& Towne apparel and accessories for women over 35. Thecompany planned to open four test stores in Chicago and NewYork in Fall 2005. The baby boomer age and the spreadingability of this age group has created an opportunity for thecompany.

The company has continued to focus on developing andgrowing its brands, and it believes that its brands are amongits most important assets. The company is taking action tomaintain and strengthen brand loyalty, including significantlyincreasing its investment in advertising and marketing.

Besides expanding the number of print ads placed in majormetropolitan newspapers and their Sunday magazines, majornews weeklies and lifestyle and fashion magazines, the com-pany’s ads appear in various outdoor venues, such as masstransit posters, exterior bus panels, bus shelters, and giganticbillboards spanning entire buildings. The company continuesto run TV ads for all of its brands and radio ads for OldNavy.

The company continues to add flagship stores and increasetelevision advertising to complement its in-store customerservice focus. The company also continues to invest in storeexpansion as well as development of new distribution channelsto address changing market requirements. Its new channelsof distribution include Gap Online, Old Navy Online, GapMaternity Online, and a catalog for Banana Republic. Thecompany has a limited operating history in these new channelsof distribution and is faced with competition from establishedretailers in these new lines.

The retail apparel business fluctuates according to changesin customer preferences dictated in part by fashion and season.These fluctuations especially affect the inventory owned byapparel retailers, since merchandise usually must be orderedwell in advance of the season and sometimes before fashiontrends are evidenced by customer purchases. Gap is also vul-nerable to changing fashion trends. In addition, the cyclicalnature of the retail business requires the company to carry asignificant amount of inventory, especially prior to peak sell-ing seasons when the company and other retailers generallybuild up their inventory levels. Gap must enter into contractsfor the purchase and manufacture of apparel well in advanceof the applicable selling season. As a result, the company isvulnerable to demand and pricing shifts and to suboptimalselection and timing of merchandise purchases.

RETAIL DIVISIONS

Gap operates under different divisions: Gap, Banana Repub-lic, GapKids, BabyGap, Old Navy, and International Division,among others. The first seven operate domestically, and thelast one operates all of the stores from the first seven divi-sions that open overseas. The company continues to expand

internationally each year. It is faced with competition inEuropean and Japanese markets from established regionaland national chains. If international expansion is not success-ful, the company’s results of operations could be adverselyaffected. The company’s ability to grow successfully in thecontinental European markets will depend in part on deter-mining a sustainable profit formula to build brand loyaltyand gain market share in the especially challenging retailenvironments of France.

Gap Division. This division has by far the most stores—morethan all of the other divisions combined—with 1,291 storesoperating in the United States in 2005. The Gap Shoes sub-division also operates under this division. All stores underthe Gap division are called The Gap. The Gap stores areclassified as clothing retail stores for men and women, withStandard Industrial Code 5651. In the United States, thereare 145 domestic competitors for The Gap; and in 1998 TheGap ranked third in sales. In the beginning, products underthis division consisted of an assortment of unisex basics; butrecently they have evolved to become more gender specific. In2004–2005, the company engaged well-know celebrities likeSarah Jessica Parker and musician Joss Stone to promote theGap brand.

Banana Republic Division. When purchased in February1983, Banana Republic was already famous for its travel andsafari wear, but only two Banana Republic stores existed.After the purchase was completed, the parent company cre-ated a new division to operate all Banana Republic stores. GapInc. also invested capital to create a product development andproduction team for Banana Republic, allowing it to introduceits own new private-label fashions. In addition, there was rapidexpansion into other parts of the country. Products under theBanana Republic division are more upscale, more tailored, andcome in more refined fabrics than those in The Gap stores.Leather goods and jewelry goods have been introduced intothe merchandise mix. Internationally, Banana Republic storesare run only in Canada but in 2005, the company announcedthat it would open two stores in Japan in the shopping districtsof Ginza and Roppongi. The company also offers these prod-ucts online on www.bananarepublic.com. Banana Republichas sales of over $2 billion in the North America. Presently,the company is trying to move toward being a fashion houseby showcasing its designs in fashion shows.

GapKids Division. After this division was formed in 1986,it became the fastest growing division of Gap Inc. All storesunder this division are called GapKids stores. Products in thisdivision are essentially miniature versions of The Gap prod-ucts, but with more focus on color variations. These productshave also switched from unisex to more gender specific. Theformation of the BabyGap subdivision under GapKids isanother reason for the rapid growth of this division.

Old Navy Clothing Company Division. This division oper-ates all Old Navy Stores and Gap Warehouses. There arenow 907 Old Navy stores operating under this division sincethe first introduction in 1994. There is also a Gap Warehouseoperating under this division. The formation of the Old Navydivision came at a time when sales were down, and Gap Inc.

Case 8 • Gap Inc. • 663

needed new ways to attract customers. The strategy was tosell merchandise similar to Gap stores but at lower costs.This division is expected to surpass the GapKids division andbecome the fastest growing division of Gap Inc. Internation-ally, Old Navy stores, too, exist only in Canada. The companyalso offers these products online on www.oldnavy.com. Thecompany plans to open 200 new stores by 2007 and add newlines such as plus sizes, maternity, and personal care.

International Division. All stores located in foreign coun-tries are under the control of the International Division. Thisdivision includes Gap, GapKids, Banana Republic, and OldNavy stores. The first overseas store was established in 1987in London, thus gaining entry into the British apparel market.In 1988 the first store in Canada was established, and in 1993the first store in France was opened. As of 1994, the Inter-national Division operated 40 Gap and GapKids in England,59 in Canada, and 3 in France. International Division alsooperates Banana Republic in Canada and Australia. Interna-tional Division shows strong growth potential and continuesto expand existing markets in Europe and to gain major entryinto new market including Japan.

PRODUCTS AND CUSTOMER BASE

The Gap division sells mainly men’s and women’s casualand active wear. Clothing items, including jeans, sweat suits,sweatshirts, denim wear, and polo-style pocket T-shirts aremarketed. The Gap division has also expanded its market toinclude handbags, shoes, and a higher fashion line of eveningwear. In addition, during the 1990s, the Gap division enteredthe bodycare products and cosmetics market, introducingsoaps, body lotions, shower gels, shampoos, conditioners, aro-matic candles, and other related items. In addition to sellingtravel and safari wear, the Banana Republic division sellsmen’s and women’s casual wear, made of finer fabrics andpriced higher than can be found in Gap stores. Together, theGap stores and the Banana Republic divisions target mainlycustomers 20 years or older. GapKids, which sells miniaturizedversions of Gap store products, originally aimed at childrenaged 2 to 12, but with the introduction of BabyGap, it hasbeen able to add even younger customers to its customer base.The most recently introduced Gap Maternity sells maternitywear only through its Web site. The Old Navy Division, sell-ing cheaper products, targets lower-income shoppers. TheInternational Division targets foreign customers in similar agegroups mentioned earlier.

SOURCING

Gap purchases merchandise from some 700 sources locatedboth in the United States and in around 50 countries overseas.This procurement strategy is designed to reduce each sup-plier’s importance, so that no single supplier can affect Gap’soverall operations significantly. All suppliers account for nomore than 5 percent of the purchase. The suppliers manu-facture the Gap’s private-label merchandise according to thecompany’s specifications. Gap purchases are comprised of 40percent domestic-made merchandise and 60 percent foreign-made merchandise. Of the foreign sources, approximately 23percent are from Hong Kong, and the remaining purchasesare spread across 42 other countries. Hong Kong, Taiwan,South Korea, Singapore, and China constitute over 50 percent

of Gap’s foreign merchandise sources. Sudden political insta-bility in any of these countries could quickly have an adverseeffect on Gap’s sourcing operations, as would any impositionof import restrictions such as tariffs and quotas by the U.S.government on products made in these countries.

Hong Kong is by far the most important foreign sourceof Gap’s merchandise. Hong Kong has a total population of6.019 million, of which 17.8 percent are engaged in manufac-turing and 33.6 percent are in either retail trade or wholesale.Until recently, Hong Kong had an unemployment rate ofonly 2.2 percent, and the Hong Kong government had toimport labor from abroad to counter a shortage in laborsupply. Despite this labor shortage, the well-educated laborforce in Hong Kong is relatively cheap to employ, and withthe increased pressure of manufacturing companies movingacross the border into China, even cheaper labor may result.U.S. retailers, including Gap Inc., have long been the targetof criticism for selling goods imported from Hong Kong andother low-wage countries such as Taiwan and South Korea. Inaddition to its low-wage rate, Hong Kong is a favored apparelsource for many retailers because of the flexible manufac-turing and quick response strategies introduced by the HongKong Productivity Council and adapted by many of HongKong’s apparel producers. Both of these strategies reduceinventory costs for the retailers. Furthermore, the apparelindustry in Hong Kong is now adapting to many new tech-nologies and production methodologies, all aimed at reducingapparel production costs.

Like other Western firms that employ labor at sweat shopsin emerging countries, Gap has often been accused of profitingfrom such practices. Therefore, Gap now has over 85 sup-plier compliance officers who screen prospective and presentsuppliers for acceptable labor practices.

ADVERTISING

Gap Inc. advertises mainly through major newspaper publi-cations, but it also advertises in fashion magazines and onmass transit posters, billboards, and exterior bus panels. Alladvertisements stress the central theme of American design,quality, and moderate pricing, although they are producedseparately in each country to suit local tastes.

DISTRIBUTION

All merchandise is shipped to distribution centers for dis-tribution. These centers are located in California, Kentucky,Maryland, Canada, and the United Kingdom.

MARKETING

The company has a separate marketing team for each brand.The teams are headquartered in San Francisco’s Bay areain California. These headquarters are also responsible foradvertising.

PERFORMANCE

Although Gap Inc. saw increasing earnings until 1999, the nextfew years witnessed a fall in earnings (see Exhibit 1). Indus-try experts cited a variety of reasons for dipping revenues,such as launching too many stores to having no differentiationbetween its brands. Although the company presently has ade-quate cash flow to settle its debts in the immediate future, itwill have to find a way to get back on track to profitability to

664 • Case 8 • Gap Inc.

sustain itself in an economy characterized by fierce competi-tion. In 2002, Gap’s debt was downgraded by analysts to junkbond status. The company fared better in the next couple ofyears. However, profits fell again in the first quarter of 2005,so the company is now looking into bringing about more stylesand designs in women’s clothing to bring it back on track toprofitability.

EXHIBIT 1NET SALES AND EARNINGS COMPARISON

Net Sales Net EarningsYear (in US$ Billion) (in US$ Million)

1993 3.2 258.41994 3.7 320.21995 4.4 354.01996 5.2 452.91997 6.5 533.91998 9.1 824.51999 11.6 1127.12000 13.6 877.52001 13.8 −7.82002 14.4 477.42003 15.8 1030.02004 16.3 1150.0

GAP’S FOREIGN MARKETS

Gap’s foreign markets include Canada, Britain, and France.Following is a detailed analysis of these markets.

CANADIAN MARKET

As store openings increased across the United States dur-ing the 1980s, Gap Inc. began to realize the potential forexpanding into the Canadian market.

General Economy. During the mid-1980s, prior to Gap Inc.’sCanadian involvement, Canada enjoyed a stable and slowlygrowing economy. This brief boom was followed by a recessionin the late 1980s. While other Canadian companies suffered,Gap Inc. sought to gain first-mover advantages by riding a pos-sible rebound in the economy and tried to become a dominantplayer in the Canadian apparel industry. The Canadian gov-ernment imposes few restrictions on foreign direct investment.This was a major decision factor in Gap Inc.’s move to set upstores in Canada with the opening of eight stores in Vancouverin March 1989. The first of these was in Vancouver’s PacificCenter.

Government Regulations. Since it is a good environment forapparel market penetration, Canada subscribes to the Gen-eral Agreement on Tariffs and Trade. This greatly influencedGap’s later decisions to expand into other countries as well.Even though Gap Inc. conducts its sourcing mostly outsideof the United States, it ships those goods back through theUnited States, so that they have to be imported into countrieslike Canada. In addition, Canada’s goal of totally eliminatingtariffs on goods of U.S. origin by 2000 provided Gap Inc. withan advantage on entering the Canadian apparel market. Thistrend has enabled American companies like Gap Inc. to lower

their cost of doing business in Canada by making it cheaperto import their products from the United States. Canada evenassists U.S. companies planning to enter the Canadian marketthrough the United States and FCS Export Assistance Ser-vice. Along with fewer government restrictions, Gap Inc. didnot encounter the traditional barriers of entry such as localcontent requirements, political turmoil, and import quotas.

Market Expansion. In 1992, Gap Inc. made a big expansionmove further into the Canadian apparel market. In a jointventure with John Forsyth Company Inc., Gap Inc. began tocompete on the same level as native Canadian apparel compa-nies such as Hudson Bay Company. With the impending NorthAmerican Free Trade Agreement, Canada’s borders were nowcompletely open to outside competition. This developmentpaved the way for even more store openings for Gap Inc.

Now, Gap Inc. not only has to compete with Canadianapparel companies like Hudson Bay Company for marketshare, but also with new U.S. companies in Canada such asThe Limited. This increased competition has made Gap Inc.look at further Canadian expansion from a different perspec-tive. According to Gap Inc.’s Ken Rapp, ‘‘The holdup is nolonger a free trade issue, but a dearth of good retail space inCanada where there are fewer shopping malls per capita andlower vacancy rates.’’

With ever-increasing success, Gap Inc.’s Canadian storesbegan to branch out with Canadian versions of the U.S. Gap-Kids and BabyGap in the early 1990s. This expansion wasmade possible in part by Canada’s recovering economy andnotable growth in the apparel industry. Turtleneck jerseys, aGap staple, rose in sales 122 percent. Men’s outerwear rose 17percent after a three-year decline.

Growth Projections. Riding on the success of Gap and Gap-Kids stores, Gap Inc. believed its Banana Republic divisionwould not have a difficult time establishing stores in Canada.Thus, Banana Republic, a more upscale, higher-priced ver-sion of The Gap, opened stores in Eaton Center in Torontoand West Edmonton Mall in Alberta. Gap Inc. seeks to stealsome market share from existing Canadian chain stores suchas Roots, River Road, and Eddie Bauer by installing BananaRepublic stores.

Market Characteristics. According to the InternationalTrade Administration’s Canadian Market Overview, the newtrend in the Canadian apparel market is to economize by sav-ing money on clothing. This is because of increases in housingcosts and taxes. Female consumers are becoming more time-pressured, and as a result, they are spending half as muchtime per month shopping as they did 10 years ago. In general,adult consumers are becoming more knowledgeable aboutthe clothing they buy and are more careful in evaluating theirpurchases in terms of value.

UNITED KINGDOM MARKET

According to UK trade journals, American apparel is makinga strong showing in the British market and will continue todo so in the near future. Approximately 60 percent of men’sapparel and 35 percent of women’s apparel are sold throughretail stores. However, Gap stores in the U.K. have not beenable to satisfy the market, and in mid-2003, the company

Case 8 • Gap Inc. • 665

decided to close 13 of its stores in the region. In 2004, lossesat UK stores were at all time high.

Market Size. According to the 2001 International MarketReport, the British market for men’s apparel was about $3.34billion, and the women’s apparel market about $4.59 billion.Both are in decline because of recession.

Market Health. The UK market for apparels is currently in arecession. British retailers are hoping for ‘‘business as usual’’once again in the not too distant future, but according tomarket analysts, recovery is still a long way off. There areoccasional mini-surges in consumer spending, and retailershave devised some strategies to capitalize on these surges.One strategy is to lower price while stressing quality. Anotheris to adopt the ‘‘one-stop-shopping’’ concept, that is, pairingmen’s and women’s merchandise together in one store so bothcan be bought simultaneously. This strategy was in response toan observation that consumers now have a tendency to comein couples. Some retailers even place children’s apparel itemsalong with men’s and women’s apparel items, thus creating atrue ‘‘one-stop-shop.’’

Market Trends. British consumers are highly receptive toU.S.-designed and -manufactured apparel items. Studies showthat the average British consumer thinks of American design-ers as firm believers in making practical clothes for real people,as compared to European designers who make fashion show-style clothing that is unwearable. Outerwear sold by suchretailers as Gap Inc. and Timberland is very popular. Men’sand women’s apparel trends differ in that menswear tends tobe more basic; the changes are usually in color and fabric,not style. Men are moving toward plainer pieces and awayfrom heavily logoed styles. Women’s purchases focus more onfashion designer labels.

Customer Base. The 15- to 25-year-old age group tends tomake purchases in boutiques. Older consumers shop in storesthat are well known for quality, durability, and good value.Most retailers now are focusing on customers who are over25 years old. This is because of increasing youth unemploy-ment and an aging population of baby boomers. A significantpercentage of the customer base is made up of large-sizedcustomers, particularly women.

Competition. American-made apparel faces competitionfrom European designers, Asian-made apparel, and fromeach other. European designers from the European Unioncan ship their goods to the United Kingdom duty-free, andAsian-made items are usually produced by cheap labor.

Government Regulations and Market Access. There are fewtrade barriers for apparel. No special forms of documentationare required for apparel items going to the United Kingdom.No special standards are set. No import licenses are necessary.Textile raw materials enter the United Kingdom with up to15 percent duty, while finished apparel items are charged withup to 14 percent duty and value-added tax of 17.5 percent.No duties have to be paid for goods imported temporarily tothe United Kingdom or located in free ports (UK free-tradezones).

FRENCH MARKET

France is Gap’s new foreign market, and 33 Gap stores operatein France. The following analysis of the French apparel marketincludes size of market, characteristics of growth, growth pro-jection, industry structure, competitors and substitutes, andgovernment regulations.

Market Size. According to the U.S. Department of Com-merce World Apparel Market Research Report publishedrecently, France was the sixth largest market for apparel, withdemand of over $12 billion. It was also the sixth largest marketfor apparel imports from the United States, with total demandof $200 million.

Market Characteristics and Current Growth. The Frenchapparel market can be characterized as a mature, sophisti-cated, slow-growth market rather than an emerging market. Itis experiencing 4 percent average annual growth and 2 percentannual growth in its market for U.S. imports. The UnitedStates does not have a large share of the French market at themoment. However, the French are becoming more receptiveto U.S. fashion, especially U.S. sportswear. French womenare just beginning to buy American-made apparel, and thenatural ‘‘American look,’’ especially Western-wear clothing,is becoming popular in France. The 15- to 25-year-old agegroup is very fashion conscious and strongly influenced byAmerican styles, especially jeans and college or football teamlogo apparel.

Growth Projections. The industry has suffered from theworldwide economic slowdown since 1991, but some salesimprovements have occurred since 1994. Apparel sales areexpected to grow at a rate of 2 percent. In spite of the lowmarket share of U.S. firms, France is very promising forGap Inc. The French have a high level of receptiveness toU.S. goods, and the market for U.S. imports is expected tocontinue to grow at 2 to 3 percent annually. Unfortunately,local and third-party competition is high, but market barri-ers in this area are negligible and do not pose a problem.According to the U.S. Department of Commerce, Interna-tional Trade Administration, currently the two most promisingsubsectors in apparel for U.S. companies are sportswear andjeans.

Business Environment. The French commercial environ-ment is very dynamic and sophisticated, and quickly reflectsconsumer trends. There is a strong market for high-qualityconsumer goods. Independent specialty stores are the mainmeans of distribution in affluent cities.

Business Attitude Toward the United States and Exit/EntryBarriers. In general, the attitude toward American compa-nies is favorable, and the French are quite receptive to U.S.goods and services. However, strong interest groups are pow-erful influences on business judgment and government actionor inaction. These interest groups have been known to stagenoisy demonstrations, but they usually are a problem only forcompanies that pose a major threat to French suppliers.

There are no major entry or exit barriers to doing businessin France for most companies. Tariffs and duties on Americanproducts are discussed later.

666 • Case 8 • Gap Inc.

Competitors and Substitutes. Local and third-party competi-tion is rampant in the French market. It is particularly heavyin the consumer area where buyers are just beginning to lookfor ‘‘value’’ in their product choices, and most product linesthat are available are mature. In this mature and sophisticatedmarket, consumers are well served by suppliers around theworld. Therefore, major business breakthroughs are unlikely,but opportunities can be created in niche markets.

There is a natural tendency now for the French to buyapparel from within the European Union because of theincreasingly free flow of goods since the integration of Europe.Italy is and always has been a significant high-quality clothingcompetitor in France. However, Gap’s main competitors areNorth African and Southeast Asian companies, which havea strong presence in France because of their low productioncosts. At the moment, Asian countries have 31.7 percent ofthe French market for women’s clothing, and this number isexpected to remain constant.

There has also been an increase in imports from Morocco,Tunisia, Portugal, and, recently, Eastern Europe. Again, com-panies from these countries enjoy low production costs andclose proximity to the French market. Morocco and Tunisiaare actually the main suppliers of menswear imports to France,but the U.S. share of the menswear market has been increasingrapidly.

As far as substitutes, there has been a massive growth ofsupermarkets and hypermarkets (huge shopping stores with awide variety of products) in France, not just in food but alsoin apparel. These stores could pose a threat to specialty storessuch as The Gap if people begin doing all of their shopping athypermarkets and stop going to the specialty stores.

Government Regulations and Controls. France has had atradition of highly centralized administrative and governmen-tal control of its essentially market economy. However, theapparel industry has little restrictions other than tariffs andduties on imported products.

As part of the European Union, the TARIC system appliesduties to all imports from non-EU countries. This gives Euro-pean companies a slight cost advantage over U.S. companies.However, this advantage can be negated if production costsfor U.S. companies can be lowered. Duties on manufacturedgoods from the United States are moderate, ranging from5 to 17 percent; they are calculated as a percentage of thevalue of the imported goods. Under the Lome Convention,varying preferential tariff treatment is given to imports fromdeveloping countries in Africa, the Caribbean, and the Pacific,which gives companies an incentive to manufacture in thesecountries.

AUSTRALIAN MARKET

Following the lead of successful U.S. retailer Toys ‘‘ R’’ Us,Gap Inc. has been negotiating possible sites for anotherinternational outlet. Store location, product positioning, andmarketing and advertising decisions depend heavily on howGap executives assess the following conditions.

Economic Health. Consumption expenditures continue toincrease in the face of high unemployment, which rose by2 percent in 1992 and by 7 percent in 1993. A reverse in thistrend in 1994 and 1995 has since been the key to a robust

recovery. The average annual growth rate for the apparelmarket during this period is expected to be between 3 and5 percent.

The downward push against inflation was one of the fewpositive effects of the recent recession. Lower inflation num-bers are a positive sign to potential investors, many of whomhave been discouraged by the sliding Australian dollar. Astrong local currency is helpful for specialty retailers like theGap on two levels. First, its products will become relativelymore price competitive. Second, Gap would benefit from astrong Australian dollar through translation gains, as profitsare repatriated.

Others are wary that the removal of quotas and tariffs willfoster a fiscally unhealthy demand for imports. If past per-formance is any indication, economic expansion would mostlikely lead to a rise in the current account deficit. Officials citethat if the Australian president’s goal of 4 to 5 percent GDPgrowth is realized, the current account deficit will increasefrom 3.75 to 4.25 percent of GDP during the same period.

Market Barriers and Government Regulations. In the recentpast, currency exchange rate levels and hefty import dutiesmade it difficult to sell U.S. apparel products in Australia.Thankfully, import duties are on the decline, and the Aus-tralian government promised that this figure would continueto fall, via the TCF tariff reduction program, by 3 percentannually until the year 2000. The tariff on textiles and apparelwas then expected to level off at 25 percent. Add to thisthe abolition of import quotas in February 1993, and for-eign apparel retailers and their products become increasinglyattractive in the face of domestic competition. This despite therecent ‘‘Buy Australian’’ campaign, which Australian officialsinsist has successfully increased consumers’ preferences forlocally made products.

Gap Inc. executives must also consider the additional costsassociated with the newest clothing standards to be adoptedby Standards Australia, a national regulatory committee. Thenew standard rates clothing according to the protection itoffers from the sun. If adopted, Gap must carefully considerwhich products should be introduced in Australia and possiblyreconsider its own internal manufacturing standards.

Competition. Competitors vying for the US$1.5 billion inapparel revenues include traditional department stores, dis-count retailers, mail-order companies, home shopping clubs,and a growing contingent of specialty shops, including Gap.Industry sources estimate that 15 percent of the market iscaptured by traditional retailers and 85 percent of the marketis sold through other means. Experts also say that, of theexpected 4 percent growth in the apparel market, an increas-ing proportion is expected to be captured by competitivelypriced imports. Competitors in Australia’s apparel marketbreak down as follows:

Department Stores. Department store leaders like ColesMyer, David Jones, and Georges sell to the middle of the mar-ket. These stores tend to sell higher-quality apparel goods,with various departments devoted to discount and specialtyapparel. Coles Myer, for example, has a Myer’s Bargain Base-ment department, and its rival Georges offers a floor devotedexclusively to international apparel. Gap will take businessmainly from David Jones and Coles Myer.

Case 8 • Gap Inc. • 667

Chain Stores and Boutiques. These stores generally sellaccording to the selective tastes of their target markets. Gapstores are somewhat different from these retailers in that theywould sell Gap brand items exclusively. Sportsgirl, catering tofemale teenagers, and Portmans are the largest in this segmentand would compete directly with Gap.

Mail-Order Companies/Home Shopping Clubs. Throughits subsidiary Myer’s Direct, Coles Myer has broadened itsattack on consumers on two fronts: mail-order catalogues anda new home shopping program. The initial response to thehome shopping program was not very enthusiastic; however,its mail-order business, the largest in the country, has beenmore successful, averaging 50 to 60 percent growth since itsinception in 1989.

Positioning. Gap Inc. should continue to take advantage ofits niche appeal as a U.S./California-based apparel company.Although U.S. companies, in general, face heavy competitionin Australia, single-brand stand-alone stores like the Gap willalways find opportunities in niche markets. Gap should avoidcompeting on the basis of price with imports from China andHong Kong. Gap’s greatest initial success will come fromproviding one of Australia’s populous cities, such as Sydneyor Melbourne, fashionable, high-quality ‘‘American’’ apparelproducts.

GERMAN MARKET

Gap operated 20 stores in Germany until the beginning of 2004when it sold all of its unprofitable German stores to Swedishapparel retailer H&M. Gap executives faced the followingchallenges and opportunities that are unique to the Germanapparel market.

Market and Economic Health. In 1998, Germany was rankedat the top of the list of apparel importers at over $30 billion.A closer look shows that the most promising subsectors weresports, leisure and casual wear (US$7 billion), and jeans wear(US$4 billion). Average annual growth for Germany’s apparelindustry through 2000 is estimated to be around 3 percent.

The German clothing industry fared well under the prevail-ing conditions of the late 1980s and early 1990s, which werea result of the ongoing reunification process. The opening ofEast Germany, with a population of 16 million, offers poten-tially large profits and a number of challenges for apparelmanagers seeking new markets. For the most part, apparelretailers are choosing to enter this market through joint ven-tures and partnerships, but others, like Levi Strauss, havechosen to establish their own branches. Still, progress in thisregion is painfully slow as the transition from a commandeconomy to a market economy progresses.

Consumer Attitudes. Consumer spending is an integral partof economic growth in Germany and for Europe as a whole.Lately, however, German consumers have been unwilling toparticipate, and recovery in the region has stalled. Severalfactors have contributed to this cautious consumer attitude:rising unemployment, which was already 10 percent, higherrents, which have increased by 6 percent in the West and by asmuch as 58 percent in the East, and high tax rates—currently34.4 percent for the average worker. Even Germans from theEast, who were hungry for consumer goods from the West,

are becoming finicky shoppers. The bargain shopping attitudethat is prevalent in the United States has found its way to EastGermany. ‘‘They don’t buy so many trendy articles— it’s backto basics like T-shirts, jeans, blazers, and sweaters.’’

Competition. Because of these recent changes in consumerattitudes, low-cost apparel imports now dominate the Germanmarket. Basic items from Eastern Europe, Turkey, and Asiacan be found for one-tenth of the price of comparable U.S.offerings. This is not to say that consumers in Germany arenot willing to pay higher prices for U.S. goods. Items mustnot only be of good quality, but must also carry a well-knownAmerican trademark.

Leading competitors include Hugo Boss, a men’s-wearmanufacturer and retailer that is currently the most profitablein Germany. Boss’s success is mostly a result of repositioningits product lines. It has recently included a lower-end productline under a different label, in addition to its traditional mid-priced and premium-priced offerings. Gap will be in directcompetition with Hugo Boss for casual wear revenues. Adler,a discount fashion chain, has 60 stores in Germany, 10 ofwhich were recently opened in East Germany. Gap shouldavoid competing head to head with Adler on a price per unitbasis.

Positioning. Germans have shown a willingness to pay a pre-mium for highly recognizable American goods and have doneso, paying between $80 and $100 for a pair of Levi’s jeans.Strong, pervasive television and print advertising is the key tocreating this image awareness.

JAPANESE MARKET

Gap currently operates 84 stores in Japan. With a total popu-lation of 125 million people, Japan is an excellent market forGap’s products. The following is an overview of this market.

Market Size. The U.S. Department of Commerce WorldApparel Market Research Report shows Japan as being thelargest total market for apparel with total demand of $70 bil-lion. It is the second largest market for apparel imports fromthe United States with a demand of over $600 million, but thisstatistic is slightly misleading. This is because the DominicanRepublic, which tops Japan in this category, is merely a majorassembly point for U.S. apparel and not a major market. Thegoods are assembled there in a low-cost environment but aretransported abroad and sold in other countries. Thus, Japan isin reality the largest market for U.S.-made apparel products.

Market Characteristics and Current Growth. As a result ofthe economic recession in Japan over the last several years,the average annual growth rate for apparel in Japan has onlybeen a meager 2 to 3 percent, but imports from the UnitedStates have been increasing at an annual rate of 11 percent.This large growth is due to the boom of ‘‘American casualfashion’’ in Japan.

In the past, Japan closely followed European fashions,especially Italian fashions. However, today many Japaneseprefer American fashions, in particular, casual apparel. Sports-related products such as T-shirts, sweat suits, and clothing withprofessional sports team logos are particularly popular, and soare jeans, outdoor wear, and any items with a casual, uniquely

668 • Case 8 • Gap Inc.

American look. Individuals in the 15- to 25-year-old age groupfollow U.S. fashion trends closely. However, women’s wearand children’s clothing wear in the United States are notgaining popularity quickly and are facing difficulties in theJapanese market.

Another trend in the Japanese market, and indeed in allsectors of business, is the growing tendency of consumersto demand ‘‘value.’’ Consumers are noticing that Japaneseprices are much higher than those of comparable industrial-ized countries. (Japanese consumer prices average 40 percenthigher than those in the United States.) Consumers still wanthigh quality but are also demanding lower prices.

Growth Projections. According to the U.S. Department ofCommerce International Trade Administration, apparel wasthe thirteenth best prospect industry sector in Japan for U.S.exporters in 2000. Analysts predict that the overall Japaneseeconomy, which has been in recession until recently, willimprove, but consumers are likely to be more cautious aboutspending money. This is in line with the growing trend toward‘‘value.’’ The apparel market is expected to continue growingat 3 percent, but import growth is expected to increase. Japanhas a very high level of receptivity to U.S. goods, not muchlocal and third-country competition, and almost no marketbarriers to entry. For Gap Inc., this indicates a favorable envi-ronment. However, the distribution system in Japan is themain obstacle to market entry and may pose major problems.