Embed Size (px)

DESCRIPTION

Microeconomic Theory

Citation preview

EC901 MICROECONOMIC THEORY

(For teaching only - Do not cite)

Andres Carvajal 1

Fall term, 2008 - 09

1E-mail address: [email protected].

1 CONSUMER THEORY

Human beings are complicated objects, and human behavior is difficult to model.

Here we consider the problem of a decision-maker who has to choose a bundle of

commodities, subject to a budgetary constraint. The decision-maker could be a per-

son, or a group of people (for instance a family); for simplicity we will treat the

decision-maker as a person. In order to make this problem tractable, we will ab-

stract from the problems of what commodities are available (we take them as given),

and will model the person through two elements: what she wants, and what she can

do.

1.1 CONSUMPTION SPACE AND PREFERENCES

We consider a situation in which a person is to choose a bundle of L commodities.

These commodities are perfectly divisible and can be consumed in any nonnegative

amount: the consumption set is the nonnegative orthant RL+, so a bundle of commodi-

ties is x = (x1, . . . , xL), where each xl represents the number of units of commodity

l that make part of the bundle. We take the facts that these commodities exist as

exogenous.

The first element in our model of the person is what she wants. For us, the indi-

vidual’s preferences are subjective judgments about the relative desirability of bun-

dles: given two bundles, preferences are defined by her answer to the question ‘is the

first bundle at least as good as the second one? Formally, then, the decision-maker’s

preferences are a binary relation % defined on the consumption set: given a pair of

commodity bundles x and x′, we write x % x′ if, according to the person’s tastes,

x is at least as good as x′.1 We also take the person’s preferences as exogenous, in

the sense that we do not explain where they come from. Instead, we concentrate on

the problem of studying the individual’s behavior given her preferences, under the

assumption that these preferences will not be affected by the person’s choices.

We start by studying properties that the individual’s preferences may (but need

not) satisfy. We first study properties of a binary relation under which it makes sense

to identify this relation with someone’s preferences.

DEFINITION. We say that a binary relation % is

1. complete if for any x and any x′, either x % x′ or x′ % x;

1 Formally, % can be seen as a subset of RL+ × RL

+.

1

2. reflexive if for any x, x % x;

3. transitive if x % x′ and x′ % x′′ imply x % x′′; and

4. rational if it is complete, reflexive and transitive.

Consumers with incomplete preferences may find instances in which they are un-

able to choose: they are simply unable to make a value judgments about the relative

(subjective) quality of two bundle. Reflexivity is consistent with our interpretation

of ‘weak’ preference. Consumers with nontransitive preferences are open to full rent

extraction, as a person could find a cycle of bundles for which the person is willing

to pay a positive premium at each step. In economics, one usually assumes that the

decision-maker under consideration has rational preferences, although in some cases

(e.g. very complicated problems) it may be reasonable to consider that in individual’s

preferences are incomplete; also, some cases of nontransitive preferences are some-

times observed in real life. In any case, from now on, we fix a rational binary relation

%, and define the following (induced) binary relations on the consumption set: (i)

the strict preference relation �, by saying x � x′ if it is not true that x′ % x; and the

indifference relation ∼, by saying x ∼ x′ if it is true that x % x′ and that x′ % x.

EXERCISE 1.1. Argue that � is transitive, but not reflexive, and that ∼ is reflexive and

transitive. Could these relations be complete? Could they be rational?

A second set of properties studies whether our consumer “likes” the commodities

available, in the sense that the more she consumes them the happier she is.

DEFINITION. We say that a binary relation % is

1. strictly monotone if x > x′ implies x � x′;

2. monotone if x� x′ implies x � x′;

3. locally nonsatiated if for every x and every ε > 0, one can find x′ with ||x − x′|| < ε

and x′ � x.

The first property captures the case when all goods, one by one, are good for the

individual: with strictly monotone preferences, getting more of any one commodity

improves the bundle. With monotone preferences, getting more of all commodities

improves the bundle. Local nonsatiation does not capture that the commodities are

2

good,2 but it implies that the individual will not have bliss points, in the sense that

any bundle can be improved, even with a small perturbation. In particular, the as-

sumption of locally nonsatiated preferences rules out thick indifference curves.

EXERCISE 1.2. Argue that strict monotonicity implies monotonicity and that monotonicity

implies local nonsatiation. Does monotonicity imply strict monotonicity? Does local non-

satiation imply monotonicity or strict monotonicity? Does strict monotonicity imply local

nonsatiation?

A third group of properties studies whether our consumer likes to ‘combine’ com-

modities in bundles.

DEFINITION. We say that a binary relation % is

1. convex if for any bundle x, any bundle x′ such that x % x′, and any scalar 0 ≤ α ≤ 1,

it is true that αx+ (1− α)x′ % x′;

2. strongly convex if for any bundle x, any bundle x′ 6= x such that x % x′, and any

scalar 0 < α < 1, it is true that αx+ (1− α)x′ � x′.

Convex preferences favor “balanced” bundles, in the sense that if the individual

has two bundles that have different composition but make her equally happy, then

she would not be worse off with a third bundle that just combined (took an average)

of them . Strongly convex preferences do too, in a strong sense: if the two original

bundles were different, then the combination is considered to be strictly better by

the consumer. The indifference map of a convex binary relation has the usual shape,

whereas if the relation is strongly convex, then its indifference curves cannot have

straight portions.

EXERCISE 1.3. Argue that strong convexity implies convexity. Does convexity imply strong

convexity?

It is most usual in economics to represent a decision-maker’s preferences by a

function that gives a higher value the more the person likes a bundle.

DEFINITION. We say that a binary relation % is

1. represented by function u : RL+ → R if u(x) ≥ u(x′) occurs if, and only if, x % x′;

2 Except in the very weak sense that it cannot be that not getting anything of any commodity is the

best that can happen to the consumer

3

2. representable if there is some u : RL+ → R that represents it.

The function u that represents% is called “utility function.” Notice that if a prefer-

ence relation is representable, then there are infinitely many different utility functions

that represent it. All these representations will have the same contour sets (i.e. the

same ordinal information), but may give nontrivially different utility levels (i.e. dif-

ferent cardinal information). It is for this reason that interpersonal comparisons of

utility are problematic.

EXERCISE 1.4. Argue that representability implies rationality. Does rationality imply repre-

sentability? What property must u satisfy if it represents a convex %? What property must u

satisfy if it represents a monotone %?

1.2 PREFERENCE MAXIMIZATION: MARSHALLIAN DEMAND

We now study the consumer’s behavior when deciding a consumption bundle. The

second element in the formalization of this behavior is the definition of what bun-

dles are available for the person to choose. Here, we adopt the competitive setting:

a price is given for each commodity, and the consumer has a nominal wealth that

she can spend in her bundle. Both of these variables are here considered to be ex-

ogenous; later, when studying general equilibrium, we will endogenize them. For-

mally, let us fix some rational preferences %, a vector of prices for all commodities

p = (p1, . . . , pL) � 0 and nominal income m ≥ 0. The preference maximization prob-

lem is to find x that (i) is affordable: p · x ≤ m; and (ii) cannot be improved upon:

for every other x′ that is affordable (i.e. such that p · x′ ≤ m), it is true that x % x′.

In consumer theory, we will assume that a (competitive) consumer behaves as if she

solved the problem above.

The most immediate questions are whether this problem has solutions and, if so,

how many. The problem of existence of solution is somewhat technical, so we’ll skew

it: suffice it to say that when preferences are such that they don’t change abruptly

as one changes consumption (e.g. if they can be represented by a continuous utility

function), the problem has a solution. From now on, let us assume that a solution

exists. Notice that if preferences are strongly convex, the solution is unique. From

now on, let us assume that % is strongly convex and denote by x(p,m) the unique

solution to this problem. As we vary prices and income, the preference maximization

problem defines an “optimal demand” function x : RL++×R+ → RL

+, which is known

as the Marshallian demand function.

4

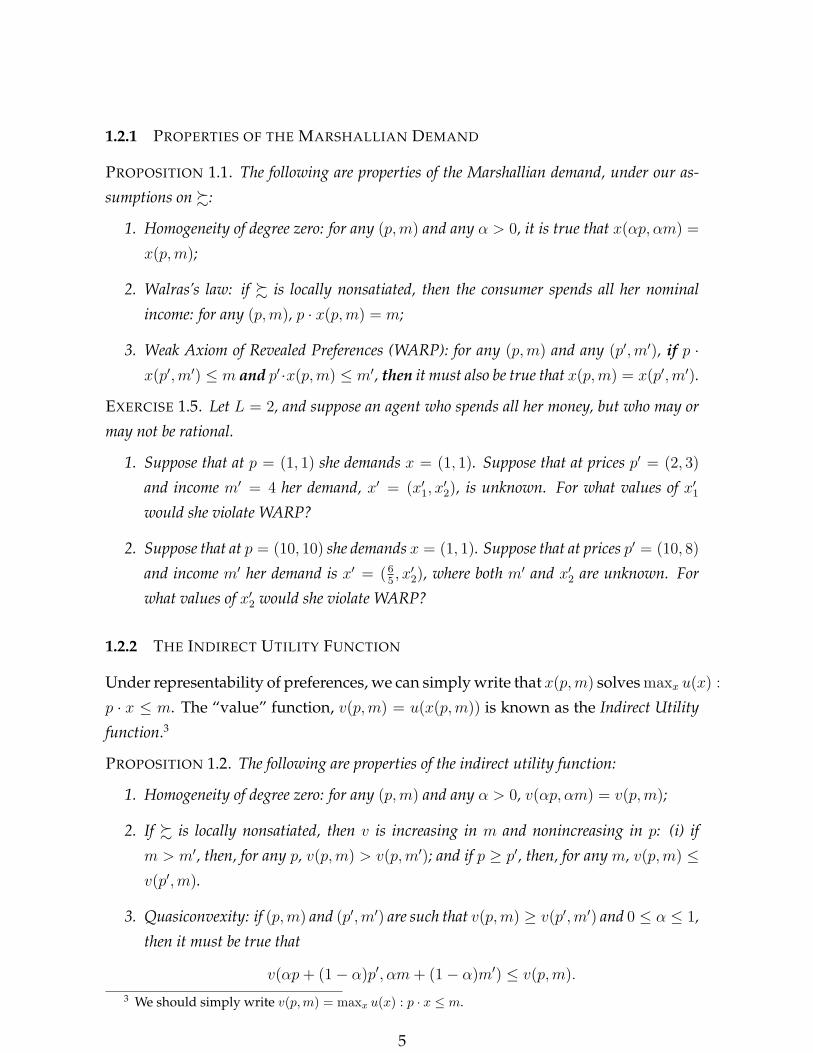

1.2.1 PROPERTIES OF THE MARSHALLIAN DEMAND

PROPOSITION 1.1. The following are properties of the Marshallian demand, under our as-

sumptions on %:

1. Homogeneity of degree zero: for any (p,m) and any α > 0, it is true that x(αp, αm) =

x(p,m);

2. Walras’s law: if % is locally nonsatiated, then the consumer spends all her nominal

income: for any (p,m), p · x(p,m) = m;

3. Weak Axiom of Revealed Preferences (WARP): for any (p,m) and any (p′,m′), if p ·x(p′,m′) ≤ m and p′ ·x(p,m) ≤ m′, then it must also be true that x(p,m) = x(p′,m′).

EXERCISE 1.5. Let L = 2, and suppose an agent who spends all her money, but who may or

may not be rational.

1. Suppose that at p = (1, 1) she demands x = (1, 1). Suppose that at prices p′ = (2, 3)

and income m′ = 4 her demand, x′ = (x′1, x′2), is unknown. For what values of x′1

would she violate WARP?

2. Suppose that at p = (10, 10) she demands x = (1, 1). Suppose that at prices p′ = (10, 8)

and income m′ her demand is x′ = (65, x′2), where both m′ and x′2 are unknown. For

what values of x′2 would she violate WARP?

1.2.2 THE INDIRECT UTILITY FUNCTION

Under representability of preferences, we can simply write that x(p,m) solves maxx u(x) :

p · x ≤ m. The “value” function, v(p,m) = u(x(p,m)) is known as the Indirect Utility

function.3

PROPOSITION 1.2. The following are properties of the indirect utility function:

1. Homogeneity of degree zero: for any (p,m) and any α > 0, v(αp, αm) = v(p,m);

2. If % is locally nonsatiated, then v is increasing in m and nonincreasing in p: (i) if

m > m′, then, for any p, v(p,m) > v(p,m′); and if p ≥ p′, then, for any m, v(p,m) ≤v(p′,m).

3. Quasiconvexity: if (p,m) and (p′,m′) are such that v(p,m) ≥ v(p′,m′) and 0 ≤ α ≤ 1,

then it must be true that

v(αp+ (1− α)p′, αm+ (1− α)m′) ≤ v(p,m).

3 We should simply write v(p,m) = maxx u(x) : p · x ≤ m.

5

1.2.3 DIFFERENTIABLE CONSUMER

Suppose furthermore that u is twice continuously differentiable4 and has interior con-

tours.5 Suppose that u is strictly monotone and strongly quasiconcave,6 and consider

only m > 0.

PROPOSITION 1.3. Under the assumptions stated above,

1. Marshallian demand is interior: for any (p,m), x(p,m)� 0;

2. For given (p,m), bundle x(p,m) is the only x for which there exists λ > 0 such that

Du(x) = λp and p · x = m;

3. The Marshallian demand function x is differentiable;

4. The indirect utility function, v, is differentiable, and the marginal utility is given by

∂mv(p,m) = λ(p,m) = 1p1∂x1u(x(p,m)).

Moreover, the following properties are important restrictions in applied work:

PROPOSITION 1.4. Under the assumptions stated above, the following are properties of the

Marshallian demands, at all (p,m):

1. Cournot aggregation: for any commodity l′,

xl′(p,m) +∑l

pl∂pl′xl(p,m) = 0;

2. Engle aggregation:∑

l pl∂mxl(p,m) = 1;

3. Euler aggregation: for any l′,∑

l pl∂plxl′(p,m) +m∂mxl′(p,m) = 0.

And the following property of the indirect utility function is very useful in theo-

retical work:

PROPOSITION 1.5 (Roy’s identity). Under the assumptions stated above, for any commod-

ity l′ we have that

−∂pl′v(p,m)

∂mv(p,m)= xl′(p,m).

4 The following notation will be used: for any function f(x, y), the partial derivative with respect

to x will be denoted by ∂xf(x, y); the gradient of any function f(x) will be denoted by Df(x) and its

Hessian will be D2f(x).5 That is, that for every x ∈ RL

++, it is true that {x′|u(x′) ≥ u(x)} ⊆ RL++.

6 In this setting, we are assuming that, whenever x � 0, it is true that Du(x) � 0 and that

δTD2u(x)δ < 0 for any δ 6= 0 such that δ ·Du(x) = 0.

6

Proof: A direct proof can be given by the Envelope theorem. Alternatively, recall that

v(p,m) = u(x(p,m)). Then, differentiating with respect to pl′ , by the chain rule,

∂pl′v(p,m) =∑l

∂xlu(x(p,m))∂pl′xl(p,m).

By the first order conditions (Proposition 1.3), we can substitute ∂xlu(x(p,m)) = λ(p,m)pl,

to get

∂pl′v(p,m) = λ(p,m)∑l

pl∂pl′xl(p,m) = −λ(p,m)xl′(p,m),

where the second equality comes from Cournot aggregation (Proposition 1.4). Simi-

larly, but using Engle aggregation,7

∂mv(p,m) =∑l

∂xlu(x(p,m))∂mxl(p,m)

= λ(p,m)∑l

pl∂mxl(p,m)

= λ(p,m).

Q.E.D.

EXERCISE 1.6. Suppose that L = 2, and consider a consumer whose preferences are repre-

sented by

u(x) = α ln(x1) + (1− α) ln(x2),

for 0 < α < 1. Are the preferences of this consumer rational? Are they locally nonsatiated?

Are they convex? Find the Marshallian demand and the indirect utility functions? Verify

homogeneity of degree zero of both functions. Verify Walras’s law. Verify that the indirect

utility is increasing in income and nonincreasing in prices. Verify differentiability. Verify the

conditions of aggregation of Cournot, Engel and Euler. Verify Roy’s identity.

1.3 EXPENDITURE MINIMIZATION: HICKSIAN DEMAND

Fix rational, strongly convex preferences %. Suppose that a continuous utility func-

tion u represents %.

For prices p� 0 and a feasible utility level υ, the expenditure minimization prob-

lem is to find x such that: (i) it gives utility at least equal to υ: u(x) ≥ υ; and (ii) for

every other x′ such that u(x′) ≥ υ, it is true that p · x′ ≥ p · x. That is, to find x that

solves minx p · x : u(x) ≥ υ.7 The equations that follow prove the last statement in Proposition 1.3.

7

Under our assumptions, the problem is guaranteed to have a unique solution,

which we denote by h(p, υ). Function h : RL++ × u[RL

+]→ RL+ is known as the Hicksian

demand function.8

1.3.1 PROPERTIES OF THE HICKSIAN DEMAND

PROPOSITION 1.6. The following are properties of the Hicksian demand, under our assump-

tions on %:

1. Homogeneity of degree zero in p: for any (p, υ) and any α > 0, it is true that h(αp, υ) =

h(p, υ).

2. No excess utility: for any (p, υ), it is true that u(h(p, υ)) = υ.

3. The compensated law of demand: for any p and p′, and any υ, it is true that

(p− p′) · (h(p, υ)− h(p′, υ)) ≤ 0.

Proof: We only proof the compesated law of demand. Notice that, by definition,

p · h(p, υ) ≤ p · h(p′, υ) and p′ · h(p′, υ) ≤ p′ · h(p, υ). Immediately,

p · h(p, υ) + p′ · h(p′, υ) ≤ p · h(p′, υ) + p′ · h(p, υ).

Q.E.D.

Notice that there is no analogous of the last property that holds true for the Mar-

shallian demand!

EXERCISE 1.7. For the consumer considered in Exercise 1.6, find the Hicksian demand func-

tion. Verify homogeneity of degree zero in p, no excess utility and the compensated law of

demand.

1.3.2 THE EXPENDITURE FUNCTION

The value function of the expenditure minimization problem is the Expenditure Func-

tion: e : RL++ × u[RL

+]→ R+, defined by e(p, υ) = p · h(p, υ).9

PROPOSITION 1.7. The following are properties of the expenditure function:

8 Here, u[RL+] denotes the set of feasible utility levels: u[RL

+] = {υ ∈ R|∃x ∈ RL+ : u(x) = υ}.

9 Or, e(p, υ) = minx p · x : u(x) ≥ υ.

8

1. Homogeneity of degree one in p: for any (p, υ) and any α > 0, e(αp, υ) = αe(p, υ).

2. If preferences are monotonic, then e is increasing in υ and nondecreasing in p: if υ > υ′,

then, for any p, it is true that e(p, υ) > e(p, υ′); and if p ≥ p′, then, for any υ, it is true

that e(p, υ) ≥ e(p′, υ).

3. Concavity in p: for any p, p′ and υ and any 0 ≤ α ≤ 1, it is true that

e(αp+ (1− α)p′, υ) ≥ αe(p, υ) + (1− α)e(p′, υ).

Proof: We prove only concavity in p. Notice that, by definition, e(p, υ) ≤ p · h(αp +

(1− α)p′, υ) and e(p′, υ) ≤ p′ · h(αp+ (1− α)p′, υ). Then, taking the average,

αe(p, υ) + (1− α)e(p′, υ) ≤ (αp+ (1− α)p′) · h(αp+ (1− α)p′, υ).

Q.E.D.

Notice that the last property is cardinal, while the analogous result for in the indi-

rect utility function is only ordinal!

1.3.3 DIFFERENTIABLE CONSUMER

Suppose again that the utility function u representing the consumer’s preferences is

(twice continuously) differentiable and has interior indifference curves. Suppose also

that u is strictly monotone and strongly quasiconcave.

PROPOSITION 1.8. Under the assumptions stated above, and considering only interior utility

levels υ > u(0), the following is true:

1. Hicksian demand is interior: for any (p, υ), h(p, υ)� 0.

2. For given (p, υ), bundle h(p, υ) is the only x for which there exists γ > 0 such that

p = γDu(x) and u(x) = υ.

3. The Hicksian demand function, h, is differentiable;

4. The expenditure function, e, is differentiable, and the marginal expenditure is given by

∂υe(p, υ) = γ(p, υ) = (∂x1u(x(p, υ)))−1p1.

Furthermore, the following restrictions are important in applied and theoretical

work:

9

PROPOSITION 1.9. Under the assumptions stated above, and considering only interior utility

levels υ > u(0),the following is true:

1. Negative semidefiniteness: for any p and υ, matrix D2p,pe(p, υ) is negative semidefinite;

2. Shephard’s lemma: for any commodity l′, ∂pl′e(p, υ) = hl′(p, υ);

3. Symmetry and negative-semidefiniteness of substitution effects: matrix Dph(p, υ) is

symmetric and negative semidefinite.

Proof: Negative semidefiniteness of D2p,pe(p, υ) is immediate from the fact that e is

concave (Proposition 1.8).

For Shephard’s lemma, notice first that, by no excess utility (Proposition 1.6),

u(h(p, υ)) = υ. Then, taking derivatives,∑l

∂xlu(h(p, υ))∂pl′hl(p, υ) = 0.

By first-order conditions (Proposition 1.8), we can substitute ∂xlu(h(p, υ) = 1γ(p,υ)

pl, to

get that∑

l pl∂pl′hl(p, υ) = 0. Now, recall that e(p, υ) = p · h(p, υ), so, differentiating,

∂pl′e(p, υ) = hl′(p, υ) +∑l

pl∂pl′hl(p, υ) = hl′(p, υ).

Shephard’s lemma immediately implies that Dph(p, υ) = D2p,pe(p, υ), so negative

semidefiniteness follows from part 1, while symmetry follows from a well-known re-

sult in mathematics, Young’s Theorem. Q.E.D.

Symmetry of Dph(p, υ) is an example of a result that was discovered after the

application of mathematics, but was not anticipated by intuitive arguments.

EXERCISE 1.8. For the same consumer as in Exercise 1.6, verify that e is increasing in p and

in υ. Verify that e is homogeneous of degree one and concave in p. Verify Shephard’s lemma.

1.4 DUALITY

For the purposes of this section, fix rational, strongly convex, locally nonsatiated pref-

erences %, and let the utility function u represent %.

PROPOSITION 1.10 (Duality Theorem). Fix prices p� 0, nominal incomem and a feasible

utility level υ. Under the assumptions above, the following is true:

10

1. Marsallian demand at income equal to minimized expenditure is the same as Hicksian

demand: x(p, e(p, υ)) = h(p, υ);

2. Hicksian demand at utility level equal to maximized utility is the same as Marshallian

demand: h(p, v(p,m)) = x(p,m);

3. Maximized utility at income equal to minimized expenditure is the same as required

utility: v(p, e(p, υ)) = υ;

4. Minimized expenditure at utility level equal to maximized utility is the same as nominal

income: e(p, v(p,m)) = m.

Proof: For part 1, suppose that the equality does not hold. Since p ·h(p, υ) = e(p, υ), it

must be that u(x(p, e(p, υ))) > u(h(p, υ)) = υ. But then, since p · x(p, e(p, υ)) ≤ e(p, υ),

we have that x(p, e(p, υ)) solves the expenditure minimization problem too, which

would violate “no excess utility” (Proposition 1.6).

For part 2, again suppose otherwise. Since u(x(p,m)) = v(p,m), it must be that

p · h(p, v(p,m)) < p · x(p,m) = m. But then, since u(h(p, v(p,m)) ≥ v(p,m), we have

that h(p, v(p,m)) solves the utility maximization problem too, which would violate

Walras’s law (Proposition 1.1).

Part 3 is immediate from part 1, given no excess utility, and part 4 follows from

part 2, given Walras’s law. Q.E.D.

The Duality Theorem allows us to go from one problem to the other without need-

ing to solve them both. Notice that the assumption that p� 0 is crucial. For instance,

if p = 0, then any bundle with u(x) ≥ υ solves the expenditure minimization problem

(and at least one such bundle exists), whereas the utility maximization problem has

no solution, given that preferences are locally nonsatiated.

EXERCISE 1.9. For the same consumer as in Exercise 1.6, verify the duality equalities.

When the utility function u is twice continuously differentiable and has interior

indifference curves, one has the following crucial result.

PROPOSITION 1.11 (Slutsky’s Identity). Suppose that u is strictly monotone and strongly

quasiconcave. Fix a feasible utility level υ and define a nominal income m = e(p, υ). Then,

for each pair of commodities l and l′, the following is true:

∂pl′xl(p,m) = ∂pl′hl(p, υ)− xl′(p,m)∂mxl(p,m).

11

Proof: From the Duality Theorem (Proposition 1.10), we know that xl(p, e(p, υ)) =

hl(p, υ). Then, differentiating,

∂pl′xl(p, e(p, υ)) + ∂mxl(p, e(p, υ))∂pl′e(p, υ) = ∂pl′hl(p, υ).

By Shephard’s Lemma (Proposition 1.9) and duality, we can substitute ∂pl′e(p, υ) =

hl′(p, υ) = xl′(p, e(p, υ)). The result follows since m = e(p, υ). Q.E.D.

EXERCISE 1.10. For the same consumer as in exercise 1.6, verify the duality equalities and

Slutsky’s identity.

Letting the substitution matrix be S(p,m) = Dph(p, v(p,m)), Slutsky’s Identity

writes in matrix terms as Dpx(p,m) = S(p,m) −Dmx(p,m)x(p,m)T. That the substi-

tution matrix is symmetric and negative semidefinite is a necessary condition implied

by rationality of the consumer. Another necessary condition is that the matrix should

have (exactly)L−1 of its columns linearly independent. Remarkably, these conditions

are also sufficient for rationality!

1.5 ADDITIONAL EXERCISES

EXERCISE 1.11. Consider a standard consumer with preferences %, over nonnegative con-

sumption of two commodities, represented by u(x) = x1 + ln(x2). Answer and solve:

1. Are these preferences rational? Are they convex? Are they strongly convex? Are they

monotone? Are they strictly monotone?

2. Find Marshallian demands and the indirect utility function. Verify Roy’s identity.

(Warning: be careful about the nonnegativity constraint!)

3. Find the expenditure function and the Hicksian demands.

EXERCISE 1.12. For a consumer in a two-commodity world, solve:

1. Suppose that the following information is known: when her income is m = 5 and prices

are p = (1, 1), her demand of commodity 1 is x1 = 3; when her income is m′ = 5α

and prices are p′ = (α, α), all that is known is that her consumption of commodity 2 is

x′2 ≥ 3. For what values of x2, α and x′ does this consumer satisfy WARP? When are

these observations consistent with maximization of strongly convex, locally nonsatiated

preferences?

12

2. Suppose that the following information is known: when her income is m = 5 and prices

are p = (1, 1), her demand of commodity 1 is x1 = 3; when her income is m′ = 5α

and the price of commodity 1 is p′1 = α, all that is known is that her consumption of

commodity 2 is x′2 ≥ 3. For what values of x2, α, p′2 and x′ does this consumer satisfy

WARP?

EXERCISE 1.13. Consider a standard consumer with preferences %, over nonnegative con-

sumption of two commodities, represented by

u(x) =1

2(x1)

12 +

1

2(x2)

12 .

Answer and solve:

1. Are these preferences rational? Are they convex? Are they strongly convex? Are they

monotone? Are they strictly monotone?

2. Find Marshallian demands and the indirect utility function. Verify Roy’s identity.

(Warning: be careful about the nonnegativity constraint!)

3. Find the expenditure function and the Hicksian demands.

EXERCISE 1.14. Suppose that L = 3, and consider a consumer whose preferences are repre-

sented by

u(x) = min{x1, x2 + x3}.

Let prices be p� 0.

1. Are the preferences of this consumer rational? Are they locally nonsatiated? Are they

convex?

2. Find the Marshallian demand and the indirect utility function. Verify also that the

indirect utility is homogeneous of degree zero, increasing in income and nonincreasing

in prices.

3. Considering only p such that p2 < p3, verify that the Marshallian demand and the

indirect utility are differentiable functions, verify the condition of aggregation of Engel,

and verify Roy’s identity for commodity 1.

4. Find the Hicksian demand and the expenditure function. Verify that the expenditure

function is homogeneous of degree 1 in prices, and verify Shephard’s lemma for com-

modity 1.

13

APPENDIX: WHY?

Here, I briefly sketch the arguments why the various propositions stated above are true. Somebits here are technical, and this appendix is to be seen as optional.

• Marshallian demand is guaranteed to exist when preferences can be represented by acontinuous utility function and prices are strictly positive, thanks to Weierstrass’s Theo-rem, since set {x ∈ RL

+|p · x ≤ m} is, then, closed and bounded.

• Marshallian demand is guaranteed to be unique when preferences are strongly convex,since if there were more than one solution, an average of two of these solutions wouldbe strictly better and still affordable.

• In Proposition 1.1:

1. Homogeneity of degree-zero holds because the budget set does not change whenone multiplies all prices and nominal income by the same positive constant.

2. Walras’s law follows since otherwise the consumer would be able to find ε > 0such that all x′ with ||x′ − x(p,m)|| < ε is affordable; by local nonsatiation, at leastone of these x′ would also be strictly superior to x(p,m).

3. For WARP, suppose otherwise; then, x(p,m) % x(p′,m′) and x(p′,m′) % x(p,m)while, by strong convexity, 1

2x(p′,m′) + 12x(p,m) � x(p,m); but this is impossible,

since p · (12x(p′,m′) + 1

2x(p,m)) ≤ m.

• In Proposition 1.2:

1. Homogeneity of degree zero is immediate from the same property of Marshalliandemand.

2. That v is increasing in m follows from Walras’s law: otherwise, x(p,m′) would beoptimal at (p,m) and p · x(p,m) < m′; that v is nonincreasing in p is immediate asp ≥ p′ implies that p′ · x ≤ m is true whenever p · x ≤ m.

3. For quasiconvexity, notice that

(αp+ (1− α)p′) · x ≤ αm+ (1− α)m′

implies that either p · x ≤ m or p′ · x ≤ m′, and hence that

v(αp+ (1− α)p′, αm+ (1− α)m′) ≤ max{v(p,m), v(p′,m′)}.

• In Proposition 1.3:

1. Interiority of demand follows from interiority of the contour sets, given m > 0.

2. The characterization of demand via first-order conditions follows from Kuhn-Tucker’stheorem, given that strong quasiconcavity guarantees the second-order conditions.

3. Differentiability follows from the Implicit Function Theorem: differentiate the sys-tem of first-order conditions, and notice that the Jacobian with respect to (x, λ) isnonsingular when u is strongly quasiconcave.

14

4. That v is differentiable is immediate from the previous result; the derivative canbe taken by the Envelope theorem, or it can be obtained as in the proof of Roy’sidentity.

• In Proposition 1.4:

1. Cournot aggregation follows from Walras’s law: differentiate with respect to prices.

2. And so does Engle aggregation: differentiate with respect to income.

3. Euler aggregation follows from homogeneity of degree zero of demand, via Euler’stheorem.

• That the expenditure minimization problem has a solution again follows from Weier-strass’s theorem: since υ is feasible, one can bound the feasible set of the problem to costless than some feasible bundle x′; the set {x ∈ RL

+|u(x) ≥ υ and p · x ≤ p · x′} is closedand boundsd, given that u is continuous.

• That the solution to the expenditure minimization problem is unique follows fromstrong quasiconcavity: if there are multiple solutions, an average of any two of thenwill give strictly more utility than υ; this average bundle x must satisfy p · x > 0 andthen, multiplying x by a number ε < 1, close enough to 1, one gets a feasible andcheaper bundle.

• In Proposition 1.6:

1. Homogeneity of degree zero follows from the fact that multiplying all prices by apositive constant only re-scales the objective function.

2. No excess utility follows by continuity: if u(h(p, υ)) > υ, then p · h(p, υ) > 0 andthen, multiplying h(p, υ) by a number ε < 1, close enough to 1, one gets a feasibleand cheaper bundle.

15

2 PRODUCER THEORY

Firms are complicated. Unlike with consumers, we have to wonder why and how

they are created; what a firm can do is the result of decisions made within and without

the firm; many different people may work for a firm, and it isn’t always the case

that they all agree when they make a decision; moreover, they may all have different

objectives and interests leading their decisions. While all these issues are interesting,

we will assume them away. We take take a given capacity to produce and study the

implications of the assumption that (everyone involved agrees that) the firm wants

to make as much money as possible.

2.1 TECHNOLOGY

As before, let us assume that there exist L commodities. A firm is a set F ⊆ RL. This

set says what is technologically feasible for the firm to produce: a production plan is

a bundle y = (y1, . . . , yL); in this plan, commodity l is used as an input if yl < 0 and

is produced as an output if yl > 0; a production plan y is feasible for the firm if and

only if y ∈ F .

Obviously, we want to consider a firm that is able to do something, so we as-

sume that F 6= ∅. For technical reasons, we also want to assume that the technology

does not change abruptly from feasible to unfeasible: we assume that F contains its

boundary (i.e., is closed).10

2.1.1 PROPERTIES OF A TECHNOLOGY:

The following are properties that may be satisfied by a firm:

DEFINITION. Firm F is said to satisfy

1. no-free-lunch if y > 0 implies y /∈ F ;

2. possibility of inaction if 0 ∈ F ;

3. free disposal if y ∈ F and y′ ≤ y imply that y′ ∈ F ;

4. non-increasing returns to scale if y ∈ F and 0 ≤ α ≤ 1 imply that αy ∈ F ;

5. non-decreasing returns to scale if y ∈ F and α ≥ 1 imply that αy ∈ F ;10 That is, we assume that if we take a sequence (yn)∞n=1 of feasible production plans (i.e. yn ∈ F for

every n) that converges to some production plan y, then that limit plan is feasible too (i.e., y ∈ F).

16

6. constant returns to scale if if y ∈ F and α ≥ 0 imply that αy ∈ F ;

7. free entry if y, y′ ∈ F implies that y + y′ ∈ F .

No-free-lunch says that the firm cannot get output without using inputs. Possibil-

ity of inaction means that one can just shut the firm down (there are no sunk costs).

Free disposal says that wasting (either inputs or outputs) is possible. Non-increasing

returns to scale says that one can shrink the firm, whereas non-decreasing returns

imply that any expansion is possible; with constant returns, both contractions and

expansions are possible. Free entry says that feasible production plans don’t interfere

with one another.

EXERCISE 2.1. Argue that nonincreasing returns to scale implies possibility of inaction. Ar-

gue that if F satisfies nonincreasing returns to scale and free entry, then it is a convex set.

Argue that if if F satisfies free entry, then the following “integer-constant returns to scale”

holds: y ∈ F and α ∈ N imply αy ∈ F .11 Are the opposite assertions true?

2.2 PROFIT MAXIMIZATION

Let us fix a firm F and prices p� 0.

The profit maximization problem is to find y that (i) is feasible: y ∈ F ; and (ii) and

cannot be improved upon, in the sense of profits at the given prices: every y′ ∈ Fyields p · y ≤ p · y. Put another way, we want to find a solution to the problem

maxy p · y : y ∈ F .

Let Y (p) be the set of all values of y that satisfy the two conditions (which may

be none, so Y (p) = ∅ is possible). As we vary prices, this set of optimal production

plans may change, so we are defining an optimal supply correspondence Y : RL++ ⇒ F .

EXERCISE 2.2. Argue that ifF satisfies nondecreasing returns to scale and there exists y ∈ Fsuch that p · y > 0, then Y (p) = ∅.

2.2.1 PROPERTIES OF THE SUPPLY CORRESPONDENCE

We only want to consider prices at which the firm is able to find a profit-maximizing

production plan, so let us define that set of prices D = {p� 0|Y (p) 6= ∅}.

PROPOSITION 2.1. The following are properties of the supply correspondence:

11 Here, N denotes the set of Natural numbers.

17

1. Homogeneity of degree zero: for any p ∈ D and any α > 0, it is true that αp ∈ D and

Y (αp) = Y (p);12

2. Convexity: IfF is convex, then y, y′ ∈ Y (p) and 0 ≤ α ≤ 1 imply that αy+(1−α)y′ ∈Y (p);

3. Single-valuedness: suppose that F further satisfies the following property: whenever

y, y′ ∈ F , y 6= y′ and 0 < α < 1, one can find y′′ ∈ F such that

y′′ > αy + (1− α)y;

then, Y (p) is singleton for any p ∈ D;

4. The law of supply: for any p and p′, for any y ∈ Y (p) and any y′ ∈ Y (p′), it is true that

(p− p′) · (y − y′) ≥ 0.

Proof: We prove the law of supply only: by definition, p · y′ ≤ p · y and p′ · y ≤ p′ · y′.Immediately, p · y + p′ · y′ ≥ p · y′ + p′ · y. Q.E.D.

2.3 PROFIT FUNCTION

For prices for which the profit maximization problem does have a solution, we define

the value function π : D → R by π(p) = p ·y, for any y ∈ Y (p). This function is known

as the profit function.13

PROPOSITION 2.2. The following are properties of the profit function:

1. Homogeneity of degree 1: for any p ∈ D and any α > 0, it is true that π(αp) = απ(p);

2. Convexity: for any p, p′ ∈ D and any 0 ≤ α ≤ 1 such that αp + (1 − α)p′ ∈ D, it is

true that

π(αp+ (1− α)p′) ≤ απ(p) + (1− α)π(p′).

Proof: We prove convexity only: by definition, for any y ∈ Y (αp+ (1−α)p′), we have

that π(p) ≥ p · y and π(p′) ≥ p′ · y. Immediately,

αp · y + (1− α)p′ · y ≤ απ(p) + (1− α)π(p′).

Q.E.D.12 Implicitly, we are saying also that D is a “positive cone.”13 Formally, π(p) = maxy∈F p · y.

18

2.4 DIFFERENTIABLE FIRM

As with consumers, we would like to have a setting in which we can use calculus to

deal with the optimization problem. So again, as there, we need to represent the firm

with a function.

Firm F is said to be represented by a function F : RL → R, if y ∈ F occurs if, and

only if, F (y) ≤ 0. Function F is the transformation function.

So, for the remainder of this section, let us fix a representable firm, and let F be

the transformation function. Furthermore, let us suppose that

1. functionF is twice continuously differentiable, nondecreasing and strongly con-

vex;

2. the transformation frontier, which is the boundary of the technology, is the set of

production plans y for which F (y) = 0.14

Under the assumptions above, we can define, for any production plan y in the

transformation frontier, and for any pair of commodities, l, l′, the Marginal Rate of

Transformation

MRTl,l′(y) =∂ylF (y)

∂yl′F (y).

whenever the denominator is not zero. The meaning of the marginal rate of transfor-

mation depends on whether l and l′ are inputs or outputs:

1. If both commodities are outputs, it is the usual definition: the slope of the “pro-

duction possibilities frontier.”

2. If l is an output and l′ is an input, it is the (negative) of the marginal product of

l′ (in the production of l).

3. If both commodities are inputs, it is the marginal rate of technical substitution.

Now, let us assume that for every p, Y (p) is singleton set.15 Then, we can further14 Formally, the transformation frontier is ∂F , the set of all production plans y with the property

that for any ε > 0, one can find production plans y′ and y′′ such that (i) ||y − y′|| < ε; (ii) ||y − y′′|| < ε;

(iii) y′ ∈ F ; and (iv) y′′ /∈ F . That is, a boundary point is arbitrarily close to points within and without

the set. Since we are assuming that F is closed, we have that the transformation frontier is part of the

feasible set, ∂F ⊆ F . The assumption we are imposing is that ∂F = F−1(0).15 It suffices, for instance, that F be increasing and that F−1(0) be bounded. In this case, the problem

is guaranteed to have a solution, as the set F−1(0) is closed (because F is continuous) and bounded,

and the function p · y is continuous. To see that the solution has to be unique, notice that since F is

strongly convex and continuous, the result follows from single-valuedness in proposition 2.1.

19

take the only solution to the profit maximization problem, y(p), to define the supply

function, and we have the following property:

PROPOSITION 2.3. Under the assumptions above,

1. for any p, y(p) is the only production plan y for which there exists µ > 0 such that

p = µDF (y) and F (y) = 0;

2. function y is differentiable;

3. Hotelling’s lemma: function π is differentiable, and for any commodity l, we have that

∂plπ(p) = yl(p);

4. matrix D2π(p) is positive semi-definite;

5. matrix Dy(p) is symmetric and positive semi-definite.16

Remarkably, we obtain symmetry of Dy(p) (notice that this is not naturally true

in consumer theory), thanks to the fact that “income effects” have no analogous in a

firm.

EXERCISE 2.3. Suppose that L = 3. Suppose that if a firm uses y2 units of commodity 2 and

y3 units of commodity 3, then it obtains yα2 yβ3 units of commodity 1. Assume that α, β > 0 and

α + β < 1. Describe F . What properties does F satisfy? Derive the supply function, verify

the law of supply, derive the profit function, verify that π is convex and verify Hotelling’s

lemma.

An associated problem, for the case when there is only one commodity which is

output and the remaining ones can be used only as inputs, fixes the level of produc-

tion of the output and only finds the cheapest combination of inputs that delivers

at least that level of output. This problem is known as the cost minimization problem

and the resulting bundles are known as conditional demands for inputs. Formally, this

problem is equivalent to the expenditure minimization problem, and we can translate

most of the results we know from Hicksian demands and the expenditure function

to this setting. The exception to the latter is the fact that “duality” theory is less

16 This matrix is

Dy(p) =

∂p1y1(p) . . . ∂pL

y1(p)...

. . ....

∂p1yL(p) . . . ∂pLyL(p)

.

20

rich in this setting, for an obvious reason: in consumer’s duality, both problems de-

termine an optimal bundle of commodities; here, the profit maximization problem

determines a full production plan (of L commodities), whereas the cost minimization

problem fixes the level of one of those variables and only determines the remaining

(L− 1) of them optimally. Thus, while profit maximization implies cost minimization

(at the optimally chosen level of output), the fact that a combination of inputs is opti-

mal at some production level does not imply that the production plan with that level

of output and the chosen combination of inputs will maximize profits.17

2.5 ADDITIONAL EXERCISES

EXERCISE 2.4. 1. Consider a firm

F = {x ∈ R2| − 1 ≤ x1 ≤ 0 and x2 ≤ −x1}.

Does this firm satisfy possibility of inaction? Free disposal? No-free-lunch? Free entry?

Nondecreasing returns to scale? Nonincreasing returns to scale? Constant returns to

scale? Convexity? Find the supply correspondence and the profit function, considering

prices p� 0.

2. Consider now a different firm:

F = {x ∈ R3| − 1 ≤ x1 ≤ 0, x2 ≤ −x1 and x3 = −1}.

Does this firm satisfy possibility of inaction? Suppose that p2 = 3 and p1 = 1, and find

the supply and expenditure functions of this firm, for any value of p3 > 0.

3. Consider now a different firm:

F = {x ∈ R3|x2 ≤ 0, x3 ≤ 0 and x1 = max{−x2,−x3}}.

Does this firm satisfy possibility of inaction? Free disposal? No-free-lunch? Free entry?

Nondecreasing returns to scale? Nonincreasing returns to scale? Constant returns to

scale? Convexity? Find the supply correspondence and the profit function, considering

prices p� 0.

17 Unless, of course, the pre-fixed production level is optimal, but then we are very close to a tautol-

ogy!

21

EXERCISE 2.5. Answer and solve:

1. Given a production function X = f(K,L), define the firm F = {y ∈ R3 : y2 ≤ 0, y3 ≤0, y1 ≤ f(−y2,−y3)}. Argue that if f is homogeneous of degree 1, the firm satisfies

constant returns to scale. Argue that if f is homogeneous of degree d ≤ 1, the firm

satisfies nonincreasing returns to scale.

2. Consider the following firm:

F = {y ∈ R2 : y2 ≤ min{αy1, βy1}},

where α < β < 0 are technological parameters. What properties does this firm satisfy?

Find the optimal supply correspondence, and the profit function.

EXERCISE 2.6. Consider a Leontieff production function: X = min{αK, βL}, where X

represents output of one commodity,K andL represent input of capital and labor, respectively,

and α > 0 and β > 0 are technological coefficients. Answer and solve:

1. Write the technology set, F , representing the firm.

2. Does this firm satisfy nondecreasing returns to scale? nonincreasing returns to scale?

No free lunch? Possibility of inaction? Free entry?

3. Is optimal supply defined, for this firm, for all positive prices? For those prices for which

optimal supply is defined, determine the optimal supply and the profit function.

Suppose now that the production function is X = ln(1 + min{αK, βL}). Answer the same

questions as before and, also, for those prices for which optimal supply is defined, verify

Hotelling’s lemma.

EXERCISE 2.7. Consider the following firm:

F = {y ∈ R2 : (1 + y1)2 + (y2)2 ≤ 1}.

Answer and solve:

1. Does this firm satisfy possibility of inaction? Nondecreasing returns to scale? Nonin-

creasing returns to scale? Constant returns to scale? No free lunch? Free entry? Free

disposal?

2. Find the optimal supply function (for strictly positive prices) and the profit function.

3. Verify Hotelling’s lemma.

22

APPENDIX: WHY?

Again, the more formal arguments for statements made in this section are given here.

• Homogeneity of degree 1 in Proposition 2.2 follows directly from homogeneity of de-gree zero in the supply correspondence.

• For Proposition 2.3:

1. That optimal supply is characterized by the first-order conditions is immediatefrom Kuhn-Tucker’s Theorem.

2. Differentiability follows from the Inverse Function Theorem, by differentiation of thesystem of first-order conditions, given that F is twice continuously differentiableand strongly convex.

3. For Hotelling’s lemma,18 notice that ∂plπ(p) =∑

l′ pl′∂plyl′(p) + yl(p). By the firstorder conditions, this implies

∂plπ(p) = µ∑l′

∂yl′F (y(p))∂plyl′(p) + yl(p) = µ∂plF (y(p)) + yl(p) = yl(p),

where the last equality follows from the fact that F (y(p)) = 0 for all p. Alterna-tively, a simpler proof can be obtained using the Envelope theorem.

4. Positive semidefiniteness of D2π(p) follows from convexity of π in proposition2.2.19

5. Symmetry and positive semidefiniteness ofDy(p) follows from Hotelling’s lemma:Dy(p) = D2π(p).

18 That π is differentiable is immediate, since so is y.19 Strictly speaking, we now require π to be differentiable twice, for which we would need to assume

that F is differentiable three times.

23

3 GENERAL EQUILIBRIUM

3.1 DEFINITIONS

Suppose that there is a finite number, L, of commodities that can be consumed in

nonnegative amounts.

3.1.1 THE ECONOMY

We assume a society populated by a finite number of individuals, which we denote

by i = 1, . . . , I . In this society, we will consider the case in which only exchange of

commodities takes place, and also the case when production is undertaken.

Consumer i is modeled by what she likes and what she has. For simplicity of

expression, we will assume here that our consumers have preferences that are repre-

sentable by utility functions ui : RL+ → R.20 In general equilibrium, we want to en-

dogenize the individuals’ nominal income, so we will assume that they are endowed

with a bundle, wi ∈ RL+, of commodities. Notice that, by the latter assumption, we

are introducing one institution in our society: private property.

When the economy has production, we will assume that it has an industry con-

sisting of a finite number of firms, which we will denote by j = 1, . . . , J . Firm j is

a nonempty set F j ⊆ RL, which represents its technology.21 In this case, we will

maintain the assumption of private property and will also assume that the economy

is closed: we will assume that each individual i owns a proportion si,j ≥ 0 of the

stock of firm j, and will impose the condition that∑I

i=1 si,j = 1 for every firm j.

An exchange economy is defined by a society, and by the full description of its mem-

bers,

{{1, . . . , I}, (ui, wi)Ii=1}.

Later, for simplicity, we will simply write {(ui, wi)Ii=1}, leaving the society implicit,

unless we need to be explicit about it.

A production economy consists of a society and an industry, and by the full descrip-

tion of the members of both sets,

{{1, . . . , I}, {1, . . . , J}, (ui, wi, (si,j)Jj=1)Ii=1, (F j)Jj=1}.20 The standard properties of preferences may be invoked. Here, we will interchangeably say that

the individual has convex preferences or that her utility function is quasiconcave.21 The standard properties of preferences may be invoked.

24

Later, for simplicity, we will simply write {(ui, wi, (si,j)Jj=1)Ii=1, (F j)Jj=1}, leaving both

the society and the industry implicit.

3.1.2 COMPETITIVE EQUILIBRIUM

We want to study situations where agents trade voluntarily and where they think

that their actions do not impact the aggregate conditions at which trade takes place.

We, then, add a second institution, competitive markets, which are exchange facilities

where an anonymous price is announced for each commodity, denoted pl, and where

all traders can trade at that given price.

Let p = (p1, . . . , pL) ∈ RL denote commodity prices, and use xi and yj to denote,

respectively, individual i’s consumption plan and firm j’s production plan.

In an exchange economy with competitive markets, consumers take all prices as

independent of their demands, and the only constraint that individual i recognizes

is that she cannot spend more than her nominal wealth, which is the nominal value

of her endowment. If it is a production economy, individual i’s nominal wealth is

given by the nominal value of her endowments and the dividends she receives from

the firms. In the latter case, firms too take all prices as fixed, and only recognize their

own technology as a constraint.

DEFINITION. In an exchange economy {(ui, wi)Ii=1}, a competitive equilibrium is a pair

consisting of a vector of prices and a profile of consumption plans, (p, (xi)Ii=1), such that

1. for each consumer i, bundle xi solves the problem maxx ui(x) : p · x ≤ p · wi;

2. all markets clear:∑I

i=1 xi =

∑Ii=1w

i.

(Later on, for simplicity of notation, we will write as x the allocation (xi)Ii=1.)

The definition of equilibrium takes preferences and endowments as given funda-

mentals, and determines values for all endogenous variables of the problem; in the

case of an exchange economy, the endogenous variables are all the prices and the

consumption decisions of all individuals. Equilibrium is then the requirement that

all these variables be feasible and that no agent regret the decision she is making at

the time she is making it. Importantly, notice that in the interpretation of the defini-

tion of competitive equilibrium, there are endogenous variables that are not decided

by any one particular agent: while prices are endogenous to the whole economy, each

decision-maker thinks that she cannot affect them. Notice also that the definition of

equilibrium does not say what occurs in the economy when it is not in equilibrium.

25

Finally, notice the assumptions implicit in the definition: (i) it is assumed, as an in-

stitution, the existence of complete competitive markets; (ii) it is assumed, as a rule

of behavior, that all agents are price takers; (iii) each individual’s behavior affects her

well-being only; and (iv) no unit of a commodity can be consumed by more than one

consumer. Many results crucially depend on these assumptions.22

The following property is well known, and simplifies the treatment of competitive

equilibrium.

PROPOSITION (Walras’s law). Fix an exchange economy {(ui, wi)Ii=1} in which all con-

sumers have locally nonsatiated preferences, and at least one of them has strongly monotone

preferences. Suppose that (p, (xi)Ii=1) satisfies that:

1. for each individual i, xi solves maxx ui(x) : p · x ≤ p · wi;

2. for all commodities but one, say for all l ∈ {1, ..., L − 1}, it is true that∑I

i=1 xil =∑I

i=1wil .

Then, all prices are positive, p� 0, and it is true that (p, (xi)Ii=1), ( 1p1p, (xi)Ii=1), ( 1

||p||p, (xi)Ii=1)

and ( 1Pl plp, (xi)Ii=1) are all competitive equilibria.

Proof: Since one individual’s preferences are strictly monotone, it follows from con-

dition 1 that all prices must be strictly positive. Since all consumers are locally non-

satiated, condition 1 also implies, by the version of Walras’s covered in Consumer’s

theory, that∑I

i=1 p · (xi − wi) = 0. But then, by condition 2, pL∑I

i=1(xiL − wiL) = 0,

which implies that∑I

i=1(xiL − wiL) = 0, since pL > 0. This means that (p, (xi)Ii=1) is

a competitive equilibrium for the economy. That the other pairs are equilibria too

follows from homogeneity of degree zero of Marshallian demand. Q.E.D.

The result says that when looking for general equilibria of an economy with strongly

monotone consumers, it suffices to guarantee that all of the markets but one clear.

This says that the L× L system of market-clearing equations is underdetermined (as

a function of prices), and is in fact an L×(L−1) system. So, one can drop one variable

by letting, for instance, p1 = 1 and solving a (L− 1)× (L− 1) system.

EXERCISE 3.1. Consider an exchange economy with two consumers and two commodities:

u1(x1, x2) = x1 + x2 , w1 = (1, 1),

u2(x1, x2) = x1 + x2 , w2 = (1, 1).

22 When there are two consumers and two commodities, a graphical representation of the economy,

its equilibria and other concepts is obtained via Edgeworth boxes.

26

Find all competitive equilibria.

DEFINITION. In a production economy {(ui, wi, (si,j)Jj=1)Ii=1, (F j)Jj=1}, a competitive equi-

librium is a triple consisting of a vector of prices, a profile of consumption plans and a profile

of production plans, (p, (xi)Ii=1, (yj)Jj=1), such that

1. for each consumer i, bundle xi solves the problem

maxx

ui(x) : p · x ≤ p · wi +J∑j=1

si,jp · yj;

2. for each firm j, bundle yj solves the problem maxy p · y : y ∈ F j ;

3. all markets clear:∑I

i=1 xi =

∑Ii=1w

i +∑J

j=1 yj .

Later on, again for simplicity of notation, we will write as y the profile (yj)Jj=1 of

production plans. For production economies, a version of Walras’s law also holds.

3.1.3 PARETO EFFICIENCY

Competitive equilibrium is the canonical noncooperative (some people say ‘individ-

ualistic’) solution. The simplest form of cooperative solution is the concept of Pareto

efficiency.

In an exchange economy, an allocation is a profile of consumption plans, x =

(xi)Ii=1, such that∑I

i=1 xi =

∑Ii=1w

i.23 In a production economy, an allocation is a pair

consisting of a profile of consumption plans and a profile of production plans, (x, y) =

((xi)Ii=1, (yj)Jj=1) such that yj ∈ F j , for each firm j, and

∑Ii=1 x

i =∑I

i=1wi +∑J

j=1 yj .

DEFINITION. In an exchange economy {(ui, wi)Ii=1}, an allocation x is Pareto efficient if

there does not exist an alternative allocation x that

1. no consumer finds worse: for every i, ui(xi) ≥ ui(xi); and

2. at least one consumer prefers: for some i, ui(xi) > ui(xi).

EXERCISE 3.2. For the same economy as in Exercise 3.1, find all Pareto efficient allocations.

What can you say about the competitive equilibrium allocations?

DEFINITION. In a production economy {(ui, wi, (si,j)Jj=1)Ii=1, (F j)Jj=1}, an allocation (x, y)

is Pareto efficient if there does not exist an alternative allocation (x, y) that23 Sometimes, when the latter condition is imposed people say that x is a “feasible allocation,” while

the term “allocation” is used for any profile of consumption plans.

27

1. no consumer finds worse: for every i, ui(xi) ≥ ui(xi); and

2. at least one consumer prefers: for some i, ui(xi) > ui(xi).

It is important to notice that: (i) Pareto efficiency does away with the institutions

of competitive markets (and hence prices) and private property; (ii) it does not replace

the latter institutions by alternative mechanisms; and (iii) in production economies,

only the welfare of consumers, and not the profits of the firms, matters.

EXERCISE 3.3. Argue the following: given a production economy, an allocation (x, y) is

Pareto efficient if, and only if, for each individual i′ the allocation solves the following problem:

max(x,y)

ui′(xi′) :

ui(xi) ≥ ui(xi), for all individual i 6= i′;

yj ∈ F j, for all firm j;∑Ii=1 x

i =∑I

i=1wi +∑J

j=1 yj.

3.1.4 THE CORE

If one maintains the institution of private property and the self-interest of individuals,

one can refine the definition of Pareto efficiency to a coalitional solution for exchange

economies:

DEFINITION. An allocation x is in the core of exchange economy {(ui, wi)Ii=1}, if there do

not exist a (nonempty) group of individuals, H ⊆ {1, . . . , I}, and a sub-profile of consump-

tion plans x = (xi)i∈H such that

1. groupH can implement the sub-profile x:∑

i∈H xi =

∑i∈Hw

i;

2. no individual in group H finds herself worse off: for all i ∈ H, it is true that ui(xi) ≥ui(xi); and

3. at least one individual in group H finds herself better off: for some i ∈ H, ui(xi) >

ui(xi).

EXERCISE 3.4. For the same economy as in Exercise 3.1, find all core allocations. What can

you say about the competitive equilibrium and the Pareto efficient allocations?

EXERCISE 3.5. Argue that any allocation in the core of an exchange economy is Pareto effi-

cient. Is the opposite true?

The relation between the core and efficiency is studied in the previous exercise.

The relation between efficiency (and hence the core) and competitive equilibrium is

studied in subsection 3.3.

28

3.2 POSITIVE ANALYSIS

Properties are said to be positive when they are necessary conditions that do not

involve any value judgement. Some of these properties are very important, but their

exposition is somewhat technical. For instance, one can use fixed point theorems to

show that any well behaved economy24 has a competitive equilibrium. Moreover, if

one assumes that preferences and technologies are sufficiently differentiable, one can

use calculus, transversality theory in particular, to show that, for “almost all” values of

the profile of endowments, there are only finitely many competitive equilibria and,

at least in a local sense, competitive equilibrium changes smoothly in response to

small perturbations in endowments.25 Here, we will skip these interesting, but more

technical, issues. For the sake of completeness, and appendix includes a proof of

existence of competitive equilibrium for exchange economies.

3.3 NORMATIVE ANALYSIS

We now study whether, ethically, competitive equilibria are acceptable: we study

the relationship between the competitive equilibrium allocations, the set of Pareto

efficient allocations and the core of the economy.

3.3.1 THE FIRST FUNDAMENTAL THEOREM OF WELFARE ECONOMICS

Pareto efficiency is a minimal criterion for social optimality.26 The first key result in

normative general equilibrium theory is that, under mild assumptions, equilibrium

allocations display this minimal property.

PROPOSITION (The FFTWE for production economies). Given a production economy,

{(ui, wi, (si,j)Jj=1)Ii=1, (F j)Jj=1},

let (p, x, y) be a competitive equilibrium. If all consumers have locally nonsatiated preferences,

then the equilibrium allocation (x, y) is Pareto efficient.

24 The key properties are that the economy be bounded, in the sense that arbitrarily large production

is unfeasible, convex, in the sense that its demand and supply correspondences are convex-valued, and

continuous, in the sense that these latter correspondences are also continuous.25 Importantly, one must notice that the last result holds for “almost all” values of endowments,

but not for all of them: a result known as the Sonnenschein-Mantel-Debreu Theorem shows that there are

economies where the predictive power of competitive equilibrium is very low.26 This is a personal value judgement: just my opinion.

29

Proof: Suppose that the statement is not true: suppose that there exists an alternative

allocation (x, y) such that

1. for all i, ui(xi) ≥ ui(xi); and

2. for some i′, ui′(xi′) > ui′(xi′).

By feasibility, we must also have that

3. for all j, yj ∈ F j ;

4.∑I

i=1 xi =

∑Ii=1 w

i +∑J

j=1 yj ;

By 3, it must be that for all j, p · yj ≥ p · yj , since yj maximizes profits for firm j at

prices p. By 2, p · xi′ > p ·wi′ +∑J

j=1 si′,jp · yj , since xi′ maximizes utility for individual

i′, given prices p. Suppose now that for some i, p · xi < p · wi +∑J

j=1 si,jp · yj ; then,

by local nonsatiation and 1, there exists an alternative bundle x such that p · x ≤p · wi +

∑Jj=1 s

i,jp · yj and ui(x) > ui(xi), which is impossible since xi maximizes

utility for individual i, given prices p. Since∑I

i=1 si,j = 1 for all j, all this implies that∑I

i=1 p · xi > p · (∑J

j=1 yj +∑I

i=1wi), which contradicts condition 4.

It must be, then, that such alternative allocation does not exist. Q.E.D.

For exchange economies, we can, in fact, say more.

PROPOSITION (The FFTWE for exchange economies). Let (p, (xi)Ii=1) be a competitive

equilibrium of exchange economy {(ui, wi)Ii=1}. If all consumers have locally nonsatiated

preferences, then the equilibrium allocation (xi)Ii=1 is Pareto efficient and is a core allocation.

EXERCISE 3.6. Notice that the previous theorem makes two statements: that, under the given

hypotheses, the equilibrium allocation is Pareto efficient, and that it lies in the core of the

economy. Which of the two statements is stronger? Argue the stronger statement, and obtain

the weaker one by immediate implication.

Notice that these two theorems: (i) do require local nonsatiation; (ii) do not use

continuity or convexity, and take as given a competitive equilibrium (so they do not

imply its existence); and (iii) crucially require the implicit assumptions of compet-

itive equilibrium (as we have so far defined it): markets are complete, all agents,

firms and producers, are price takers, and there are no external effects. On the other

hand, it is necessary to understand the implication of the theorem. If one accepts its

assumptions, the theorem implies that competitive markets deliver allocations with

30

the minimal property of social desirability, as Smith had suggested. But it does not

say more than that! It is clear that Pareto efficiency does not take into account any

distributional considerations, and hence many efficient allocations may be socially

objectionable. In that sense, the theorem should not be understood to imply that eco-

nomic policy is unnecessary if competitive markets operate. What the theorem does

say is that any economic policy beyond the equilibrium outcome will make at least

one individual worse off; although this result may be socially desirable, what cannot

be expected is “victimless” policies.

EXERCISE 3.7. Suppose that there are two societies, I1 = {1, . . . , I1} and I2 = {I1 +

1, . . . , I1 + I2}, where all individuals are locally nonsatiated. Let the global society be de-

noted by I = I1 ∪ I2. Argue that there can be no unanimous opposition to globalization in

any of the two societies: suppose that (p, x) is a competitive equilibrium of the global economy,

{I, (ui, wi)i∈I} and (xi)i∈Ik is an allocation of the autarkic economy {Ik, (ui, wi)i∈Ik}, for

k = 1, 2; if there is an individual i ∈ Ik that would prefer autarky, ui(xi) > ui(xi), then there

is also an individual i′ ∈ Ik who prefers globalization: ui′(xi′) < ui′(xi′).

EXERCISE 3.8. Consider an exchange economy with two consumers and two commodities:

u1(x1, x2) = min{x1, 2x2} , w1 = (3, 1),

u2(x1, x2) = min{2x1, x2} , w2 = (1, 3).

Find all competitive equilibria, all Pareto efficient allocations and the core of this economy.

Verify the relations that exist between these solutions.

3.4 THE SECOND FUNDAMENTAL THEOREM OF WELFARE ECONOMICS

We now study the opposite problem: given an efficient allocation, can we say that,

for sure, it is an equilibrium allocation? Stated like this, the answer to the question is

obviously negative: there are efficient allocations that cannot be sustained as equilib-

rium. However, we now show that if redistribution policies are allowed, all efficient

allocations can be sustained by competitive trading.

PROPOSITION (The SFTWE for exchange economies). Given an exchange economy {(ui, wi)Ii=1},let x be a Pareto efficient allocation. If all consumers have continuous, convex, locally non-

satiated preferences and∑I

i=1wi � 0, then there exist prices p and a distribution of wealth

(wi)Ii=1 such that

31

1. distribution (wi)Ii=1 is a reallocation of the existing aggregate endowment:∑I

i=1 wi =∑I

i=1wi;

2. (p, x) is competitive equilibrium for the economy after redistribution, {(ui, wi)Ii=1}.

The simplest argument to see that the theorem is true is as follows. Redistribute

wealth so that each individual receives the allocation that would correspond her in

the efficient allocation: let wi = xi for each i. The first condition in the theorem is

immediate, since x is an allocation for the economy. The economy after redistribution,

{(ui, wi)Ii=1}, must have a competitive equilibrium (p, x).27 By individual rationality,

ui(xi) ≥ ui(wi) for all i, and, since (xi)Ii=1 is efficient, it must be that a fortiori ui(xi) =

ui(wi), so (p, (xi)Ii=1) is a competitive equilibrium for {(ui, wi)Ii=1}. This proves the

second claim and completes the argument.

In the case of production economies, the argument is more complicated and re-

quires the use of a result known as the Separating Hyperplane Theorem. We won’t cover

that argument here, but if you really feel like studying it you can find it in the ap-

pendix of this note. The theorem itself is a bit more complicated.

PROPOSITION (The SFTWE for production economies). Given a production economy,

{(ui, wi, (si,j)Jj=1)Ii=1, (F j)Jj=1},

let (x, y) be a Pareto efficient allocation such that xi � 0 for all i. If all preferences are

continuous, convex and locally nonsatiated and all technologies are convex and closed and

satisfy free disposal, then there exist prices p and a distribution of nominal wealth in the

economy (mi)Ii=1 that satisfy the following conditions:

1. the nominal wealth being distributed is indeed the nominal value of the aggregate wealth

of the economy at the Pareto efficient allocation:∑I

i=1mi = p · (

∑Ii=1w

i +∑J

j=1 yj);

2. given their nominal wealth, each consumer is individually rational at prices p: for all i,

xi solves the problem maxx ui(x) : p · x ≤ mi; and

3. each firm maximizes profits at prices p: for all j, yj solves the problem maxy p · y : y ∈F j .

27 This is the step where the argument is less formal: we have not studied existence results in detail,

yet we are arguing that an equilibrium must exist given the assumptions that we have made. While

the latter is true (see the appendix: an equilibrium is guaranteed to exist under these assumptions),

here we will have to take it for granted.

32

Notice that, unlike the first theorem, the second fundamental does imply exis-

tence of equilibrium, so the convexity assumption is crucial. The policy implication

is that policy-makers do not need to close competitive markets to attain social ob-

jectives (which, one assumes, are Pareto efficient). Quite the opposite: well chosen

redistribution policies and competitive markets, under the assumptions of the theo-

rem, deliver the desired objectives! Of course, the problem of how much information

a policy-maker needs in order to figure out the correct redistribution is not addressed

by the theorem.

EXERCISE 3.9. Fix an exchange economy {(ui, wi)Ii=1}. An allocation x is said to be envy-

free if no agent would (strictly) prefer someone else’s consumption: for every pair of individ-

uals i and i′, it is true that ui(xi) ≥ ui(xi′). Argue that income reallocation can ensure that

every competitive allocation is envy-free: there exists a distribution of endowments (wi)Ii=1

such that:

1. distribution (wi)Ii=1 is a reallocation of the existing aggregate endowment:∑I

i=1 wi =∑I

i=1wi;

2. after redistribution, competitive allocations are envy free: if (p, x) is a competitive equi-

librium of {(ui, wi)Ii=1}, then x is envy-free.

EXERCISE 3.10. Suppose that there are two societies, I1 = {1, . . . , I1} and I2 = {I1 +

1, . . . , I1 +I2}. Let the global society be denoted by I = I1∪I2. For each society, k = 1, 2, let

(pk, (xi)i∈Ik) be a competitive equilibrium of the autarkic exchange economy {Ik, (ui, wi)i∈Ik}.Argue that there exists an global income reallocation (wi)I1+I2

i=1 such that:

1. income reallocation is balanced in each society: for each k = 1, 2,∑

i∈Ik wi =

∑i∈Ik w

i;

2. every competitive equilibrium of the global economy gives an allocation that everybody

prefers to the given autarkic allocation: for any equilibrium (p, (xi)i∈I) of the global

economy after redistribution, {I, (ui, wi)i∈I}, it is true that ui(xi) ≥ ui(xi) for every

individual i.

3.5 ADDITIONAL EXERCISES

EXERCISE 3.11. Consider an exchange economy. An allocation x is said to be Weakly Pareto

efficient if there does not exist an allocation x such that ui(xi) > ui(xi) for all i. Argue that:

1. any Pareto efficient allocation is also weakly Pareto efficient;

33

2. if all preferences are continuous and strongly monotone, any weakly Pareto efficient

allocation is also Pareto efficient.

EXERCISE 3.12. In a production economy, a profile of production plans y = (yj)Jj=1 is said

to be (i) feasible if it is true that yj ∈ F j for each firm j; and (ii) technically efficient if it

is feasible and there does not exist an alternative, feasible production plan y = (yj)Jj=1 such

that∑

j yj >

∑j y

j . Argue the following: if at least one individual has strictly mono-

tone preferences and allocation (x, y) is Pareto efficient, then the profile of production

plans y must be technically efficient.

EXERCISE 3.13. Consider an exchange economy with two consumers and two commodities:

u1(x1, x2) = x1 , w1 = (1, 1),

u2(x1, x2) = x2 , w2 = (1, 1).

Find all competitive equilibria, all Pareto efficient allocations and the core of this economy.

Verify the relations that exist between these solutions.

EXERCISE 3.14. Consider an exchange economy with two commodities and two consumers.

Preferences are u1(x) = min{x1, x2} and u2(x) = x1x2. Endowments for individual 2 are

w2 = (0, 20).

1. Compute all competitive equilibria if w1 = (30, 0).

2. Compute all competitive equilibria if w1 = (5, 0).

Aren’t these results funny?

EXERCISE 3.15. Given an exchange economy ({1, ..., I}, (ui, wi)Ii=1), argue:

1. That if the endowment (wi)Ii=1 is itself an efficient allocation, then it lies in the core of

the economy.

2. That if all individuals have strongly convex preferences and the endowment (wi)Ii=1 is

an efficient allocation, then it is the only allocation in the core of the economy.

3. That if all individuals have locally nonsatiated and strongly convex preferences and the

endowment (wi)Ii=1 is an efficient allocation, all competitive equilibria of the economy

involve no (nontrivial) trade between agents.

34

EXERCISE 3.16. Let C and P be, respectively, the core and the set of efficient allocations of a

given exchange economy with two consumers. Argue that

C = {(xi)Ii=1 ∈ P|ui(xi) ≥ ui(wi) for both i}.

Argue that if there are three or more individuals, then the claim is not true.

EXERCISE 3.17. Consider an economy with one consumer, one firm and two commodities; the

individual has preferences over both commodities represented by u and has an endowment w

of commodity 1 only; the firm transforms commodity 1 into commodity 2, under a production

function f ; the individual owns the stock of the firm. Define competitive equilibrium for this

economy; define Pareto efficiency for this economy; state and prove the First Fundamental

Theorem of Welfare Economics for this economy.

EXERCISE 3.18. Consider an exchange economy in which each ui represents locally nonsa-

tiated, strongly convex preferences. For each i, denote by hi the Hicksian demand function.

Define, (p, (xi)Ii=1) to be a pseudoequilibrium if:

1. For all i, xi = hi(p, ui(xi)) and p · xi = p · wi;

2.∑I

i=1 xi =

∑Ii=1 w

i.

Considering only strictly positive prices, argue that (p, (xi)Ii=1) is a pseudoequilibrium if, and

only if, it is a competitive equilibrium.

35

APPENDIX: EXISTENCE OF COMPETITIVE EQUILIBRIUM

The key mathematical result that we will be invoking in this appendix is the following:

THEOREM (Kakutani’s fixed-point theorem). Let ∆ ⊆ RL and let Γ : ∆ ⇒ ∆ be a non-empty-valued correspondence. If ∆ is compact and convex, and Γ is convex-valued and upper hemicontinu-ous, then there exists δ ∈ ∆ such that δ ∈ Γ(δ).

When Γ is single-valued (i.e. a function), the result is referred to as Brower’s fixed-pointtheorem and is easy enough to visualize in the case L = 1.

PROPOSITION. Suppose that∑I

i=1wi � 0 and that each ui is strongly quasiconcave and strictly

monotone. Then, there exists a competitive equilibrium.

Proof: Denote by ∆o and ∆∂ the relative interior and the boundary of the (L−1)-dimensionalunit simplex, ∆, respectively. The aggregate excess demand function over strictly positiveprices, Z : ∆o → RL, is continuous and bounded below and satisfies that for all p ∈ ∆o,p · Z(p) = 0.

Let a sequence (pn)∞n=1 in ∆o be such that pn → p ∈ ∆∂ . Suppose it is not true thatmaxl=1,...,L{Zl(pn)} → ∞. Then, for some x ∈ R it is true that for all n∗, there exists n ≥ n∗

such that maxl=1,...,L{Zl(pn)} ≤ x. Since Z is bounded below, there exists (pn(m))∞m=1 suchthat (Z(pn(m)))∞m=1 is bounded. Since

∑Ii=1w

i � 0, then for some i ∈ {1, . . . , I} we musthave p · wi > 0. Fix one such i. Since (Z(pn(m)))∞m=1 is bounded, then (xi(pn(m)))∞m=1 isbounded and, hence, has a convergent subsequence. For notational simplicity, assume that(xi(pn(m)))∞m=1 itself converges to x ∈ RL

+. Let l ∈ {1, . . . , L} be such that pl = 0. Let x ∈ RL+

be defined as follows:

xl =

{xl, if l 6= l;xl + 1 if l = l.

Since x > x, ui(x) > ui(x). By continuity, ∃ε > 0 such that for all x′ ∈ Bε(x) ∩ RL+ and all

x′′ ∈ Bε(x), ui(x′) > ui(x′′). Since xi(pn(m)) → x, there exists some m1 ∈ N such that for allm ≥ m1, xi(pn(m)) ∈ Bε(x). Fix l′ ∈ {1, . . . , L} such that pl′ > 0. Define (xn(m))∞m=1 as follows:

xl,n(m) =

xil(pn(m)) + 1, if l = l;

xil′(pn(m))− ε2 , if l = l′;

xil(pn(m)), otherwise.

Since pl′,n(m) → pl′ > 0 and pl,n(m) → pl > 0, there exists m2 ∈ N such that for all m ≥ m2,pl′,k(m)(− ε

2) + pl,n(m) < 0. Now, let m ≥ max{m1,m2}. Then,

pn(m) · xn(m) = pn(m) · xi(pn(m)) + pl′,n(m) − pl′,n(m)(ε

2)

< pn(m) · xi(pn(m))

≤ pn(m) · wi,

and, nonetheless, xi(pn(m)) ∈ Bε(x) and xn(m) ∈ Bε(x), so ui(xn(m)) > ui(xi(pn(m))), which isa contradiction. It follows that maxl∈{1,...,L}{Zl(pn)} → ∞.

36

Now, define correspondence Γ : ∆⇒ ∆ as follows:

Γ(p) =

{argmaxγ∈∆Z(p) · γ, if p ∈ ∆o;{γ ∈ ∆|p · γ = 0}, if p ∈ ∆∂ .

Notice that: (i) Γ is nonempty- and convex-valued; (ii) if p ∈ ∆o and Z(p) 6= (0, . . . , 0) thenΓ(p) ⊆ ∆∂ ; (iii) if p ∈ ∆∂ , then p /∈ Γ(p). That Γ is upper hemicontinuous at p ∈ ∆o followsfrom the Theorem of the Maximum, given that Z is continuous. Now, let p ∈ ∆∂ , (pn)∞n=1 in ∆such that pn → p, and (γn)∞n=1 in ∆ such that γn ∈ Γ(pn) for each n. Since ∆ is compact, thereexist a subsequence (γn(m))∞m=1 and a γ ∈ ∆ such that γn(m) → γ. Consider two cases: (1)(pn(m))∞n(m)=1 has no subsequences in ∆o; and (2) (pn(m))∞m=1 has a subsequence in ∆o. In (1),since pn(m) → p, for some m∗ ∈ N we have that for all m ≥ m∗, pn(m) ∈ ∆∂ and pn(m) · γn(m) =0, so p · γ = 0. In (2), take the subsequence (pn(m(k)))∞k=1 in ∆o. Since pn(m(k)) → p ∈ ∆∂ , bythe property above, there exists k∗ ∈ N such that, for all k ≥ k∗ and all l ∈ {1, . . . , L} suchthat pl > 0, Zl(pn(m(k))) < maxl′∈{1,...,L}{Zl′(pn(m(k)))}. It follows that for all k ≥ k∗ and alll ∈ {1, . . . , L} such that pl > 0, one has that γl,n(m(k)) = 0 and, hence, pn(m(k)) · γn(m(k)) = 0.Again, this implies that p · γ = 0, and hence that Γ is upper hemicontinuous at p ∈ ∆∂ .

Since Γ is upper hemicontinuous, by property (i) and Kakutani’s theorem there existssome p ∈ ∆ such that p ∈ Γ(p). By (iii), p ∈ ∆o and hence, by (ii), Z(p) = 0. Q.E.D.

Existence results under milder conditions can be given. For example, for productioneconomies:

THEOREM. Given a standard production economy where each wi > 0, if each Y j satisfies free disposaland possibility of inaction, and

{(x, y) ∈ (RL+)I ×

J∏j=1

Y j |I∑i=1

xi ≤I∑i=1

wi +∑j∈J

yj}

is compact, then there is a competitive equilibrium.

APPENDIX: PROOF OF THE SFTWE FOR PRODUCTION ECONOMIES

The key mathematical result needed for this proof is the following.