Embed Size (px)

Citation preview

CARIM

IN PETRO

LEUM

BERHA

D(Com

pany No.: 908388-k)

Corporate Presentationin conjunction w

ith

Initial Public Offering on the

Main M

arket of Bursa Malaysia Securities Berhad

24 October 2014

IR Adviser

Se

t to S

ail…

Se

t to S

ail…

TABLE O

F CON

TENTS

�Corporate Profile

�Industry H

ighlights�

Grow

th Strategies�

Financial Highlights

�IPO

Statistics�

Investment M

erits�

Appendix

�Corporate Profile

�Industry H

ighlights�

Grow

th Strategies�

Financial Highlights

�IPO

Statistics�

Investment M

erits�

Appendix

CORPO

RATE PROFILE

CORPO

RATE PROFILE

Pro

fileF

inan

cia

lsIn

du

stry

Gro

wth

IPO

Sta

tsIn

vM

erits

Ap

pen

dix

Se

t to S

ail…

Se

t to S

ail…

An

inte

gra

ted

serv

icep

rov

ide

rsu

pp

ortin

gth

eo

ffsho

reo

ila

nd

ga

sin

du

stryin

Ma

lay

siasin

ce1

98

9…

de

live

red

mo

reth

an

RM

1b

illion

wo

rtho

fp

roje

ctsa

nd

serv

ices

4BA

CKGRO

UN

D

�Incorporated in 1989, Carim

in is principally involved in providing technical support services in the offshore oil and gas (O

&G

) industry in Malaysia

�Predom

inantly involved in the provision of: �

hook up and comm

issioning (HU

C)�

production platform system

maintenance and upgrading services (PM

US)

�inspection and m

anpower supply services

�Supporting activities include equipm

ent rental and minor fabrication services

�Carim

in supports O&

G PSC operators and contractors, engineering and fabrication com

panies, and supporting service providers. N

otable clients include Petronas Carigali, Shell, Murphy O

il, Talisman, ExxonM

obil, New

field, and Petrofac etc.

�To date, Carim

in has delivered more than RM

1 billion worth of projects and services

Telok Kalong Yard in Kemam

an, Terengganu

Corporate head office in Kuala Lum

pur

1 fabrication yard in Kem

aman, Terengganu

Pro

fileF

inan

cia

lsIn

du

stry

Gro

wth

IPO

Sta

tsIn

vM

erits

Ap

pen

dix

Se

t to S

ail…

Se

t to S

ail…

Offsh

ore

HU

C&

PM

US

an

dm

an

po

we

rsu

pp

lyse

rvice

sco

ntrib

ute

the

bu

lko

f

the

Gro

up

’sre

ve

nu

e…

5REV

ENU

E STREAM

S & PRIN

CIPAL A

CTIVITIES

Offshore H

UC &

PMU

S①

64.72%

FY14 Revenue

RM158.9 m

il

�Started production platform

system m

aintenance services in 2004 �

Received ISO 9001:2008 quality m

anagement system

certification in 2011

Manpow

er supply services②

35.08% RM86.2 m

il

�Supplying project developm

ent personnel, exploration & engineering personnel, and

production/operations including inspection services personnel to clients�

Involves identifying, screening, interviewing

and shortlisting personnel and expertise�

Obtained ISO

9001:2008 quality managem

ent system certification in 2011

Hook up process m

ainly involves inter-connecting and interfacing the various structures, process and control system

s that, together, form an offshore platform

, including steel structures, piping and equipm

ent.

Comm

issioningw

orks include all testing, pre-comm

issioning and/or preservation, and final com

missioning of all installed

facilities to ensure the platform is ready for production.

← P

rovisio

n fo

r HU

C o

f Pe

tron

as C

arig

ali fa

cilities in

Sa

ba

h

Pro

fileF

inan

cia

lsIn

du

stry

Gro

wth

IPO

Sta

tsIn

vM

erits

Ap

pen

dix

Se

t to S

ail…

Se

t to S

ail…

Su

pp

ortin

gse

rvice

sin

clud

ee

qu

ipm

en

tre

nta

l,m

ino

rfa

brica

tion

an

dm

arin

e

serv

ices…

for

exte

rna

lcu

stom

ers

an

dto

sup

po

rtin

tern

al

offsh

ore

HU

C&

PM

US

pro

jects

6REV

ENU

E STREAM

S & PRIN

CIPAL A

CTIVITIES (cont)

FY14 Revenue

Minor fabrication services

③0.05%

RM0.1 m

il

�Supports internal H

UC &

PMU

S projects by fabricating structures and equipment

�Third-party w

orks include piping systems, skids and other m

inor steel structures �

Operates from

its Telok Kalong yard, Terengganu (land area: 7,288 sqm

; built-up area: 1,499 sqm

)

Marine services

⑤0.00%

Negligible

�Acquired Carim

in Airis, an Anchor Handling Tug Supply (AH

TS) vessel, in 2013 �

Has 14%

stake in SK Offshore, w

hich owns an accom

modation w

orkboat (AWB), nam

ely SK Deep Sea

�Carim

in Airis and SK Deep Sea are currently used to support internal offshore H

UC &

PMU

S projects

← C

arim

in A

iris, an

AH

TS v

esse

l with

larg

er o

pe

n d

eck

spa

ce to

tran

spo

rt sup

plie

s

Equipment rental services

④0.15%

RM0.4 m

il

�Started equipm

ent rental services by renting out welding equipm

ent in 2011�

Supports in-house offshore HU

C & PM

US projects

Pro

fileF

inan

cia

lsIn

du

stry

Gro

wth

IPO

Sta

tsIn

vM

erits

Ap

pen

dix

Se

t to S

ail…

Se

t to S

ail… 7

OU

TSTAN

DIN

G W

ORK VA

LUE

RM

90

0m

illion

wo

rtho

fw

ork

va

lue

tok

ee

pG

rou

pb

usy

un

til2

01

8…

#Project D

escriptionClient

Contract D

urationA

pproximate

Contract Value

1Peninsular M

alaysia HU

C contractPetronas Carigali

2013-2018RM

800.0 mil^

RM

80

0.0

mil

2D

rilling programN

ewfield

2013-2015* RM

38.0 mil

3U

mbrella contract

Carigali Hess

2013-2017RM

7.5 mil

4M

anpower suppply contract

Hess (M

alaysia SB302)2011-2014

RM6.4 m

il

5D

rilling manpow

er supply (expatriates)N

ewfield

2014-2015RM

6.0 mil

6O

ther manpow

er supply contractsV

arious PSCV

ariedRM

42.9 mil

RM

10

0.8

mil

RM

90

0.8

mil

HU

C, and production platform system

maintenance and upgrading services

Manpow

er supply services

^ as at LPD, total contract value am

ounting to RM899.0 m

il, of which RM

92.4 mil of w

ork orders have been rolled out* w

ith 6-month extension option

Ou

tstan

din

g w

ork

va

lue

am

ou

nt fo

r HU

C &

PM

US

Ou

tstan

din

g w

ork

va

lue

am

ou

nt fo

r Ma

np

ow

er

To

tal o

utsta

nd

ing

wo

rk v

alu

e a

mo

un

t

Pro

fileF

inan

cia

lsIn

du

stry

Gro

wth

IPO

Sta

tsIn

vM

erits

Ap

pen

dix

Se

t to S

ail…

Se

t to S

ail…

Clie

nte

lein

clud

es

the

O&

Gb

ign

am

es…

8M

AJO

R CUSTO

MERS

On-going contracts

Percentage of FY11-FY14 revenue

Percentage of FY14 revenue

Length of relationship

Customers

Types of servicesrendered

PetronasCarigali

PetrofacExxonM

obilN

ewfield

�H

UC &

PMU

S�

Manpow

er supply�

Minor fabrication

services

�M

anpower supply

�H

UC &

PMU

SM

anpower supply

Manpow

er supply

17 years8

years22 years

6years

59.7%

RM146.7 m

il

10.6% RM25.9 m

il

0.0% Negligible

12.4% RM30.4 m

il

58.8%

RM645.6 m

il

6.4% RM70.0 m

il

9.8% RM107.6 m

il

3.2% RM34.8 m

il

�H

UC Contract w

orth RM

899.0 mil that lasts

until 2018�

Manpow

er supply contracts w

orth RM3.3

mil that last until 2016

�M

anpower supply

contract worth RM

2.0m

il that lasts until 2015

�N

il�

Manpow

er supply contracts w

orth RM44.0

mil that last until 2015

Pro

fileF

inan

cia

lsIn

du

stry

Gro

wth

IPO

Sta

tsIn

vM

erits

Ap

pen

dix

Se

t to S

ail…

Se

t to S

ail… 9

COM

PETITIVE A

DVA

NTA

GES &

KEY STRENG

THS

Inb

ette

rp

ositio

nto

bid

for

offsh

ore

HU

C&

PM

US

pro

jects

with

ow

no

ffsho

re

sup

po

rtv

esse

ls(O

SV)

an

dth

esu

pp

ort

of

am

ino

rfa

brica

tion

ya

rd…

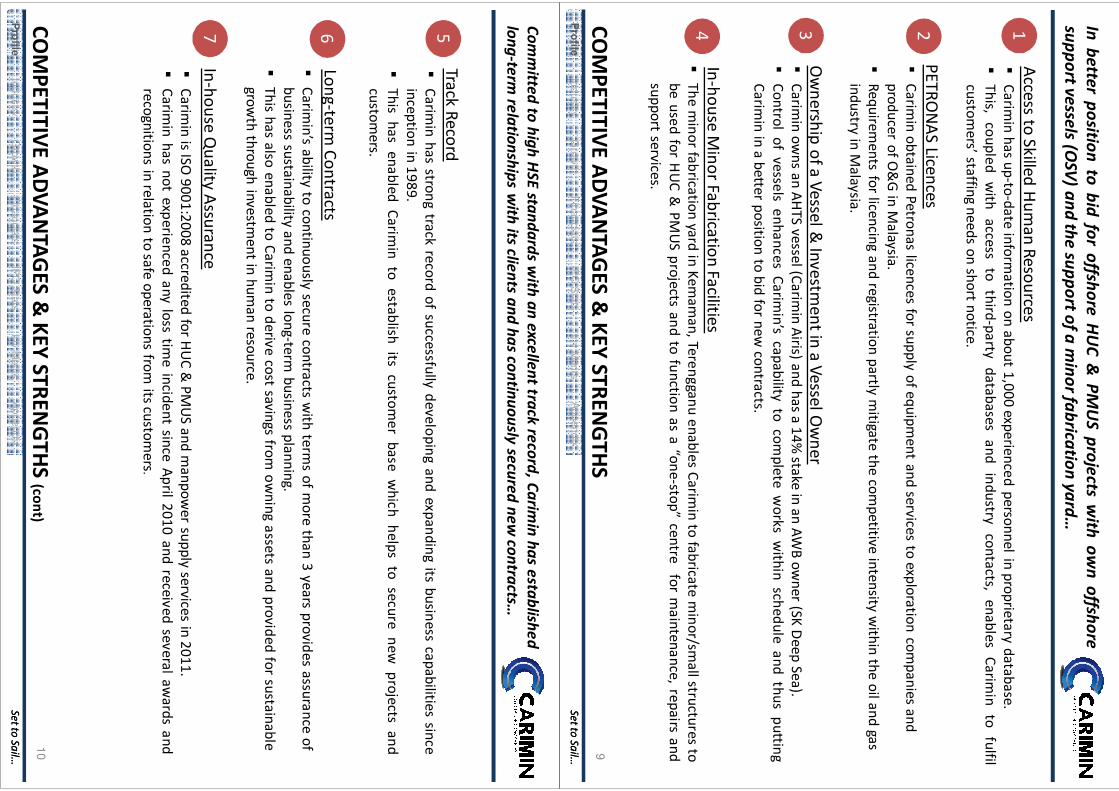

Access to Skilled H

uman Resources

1�

Carimin

hasup-to-date

information

onabout

1,000experienced

personnelin

proprietarydatabase.

�This,

coupledw

ithaccess

tothird-party

databasesand

industrycontacts,

enablesCarim

into

fulfilcustom

ers’staffingneeds

onshort

notice.

PETRON

AS Licences

2�

Carimin obtained Petronas licences for supply of equipm

ent and services to exploration companies and

producer of O&

G in M

alaysia. �

Requirements for licencing and registration partly m

itigate the competitive intensity w

ithin the oil and gas industry in M

alaysia.

Ow

nership of a Vessel & Investm

ent in a Vessel Ow

ner3

�Carim

inow

nsan

AHTS

vessel(Carimin

Airis)andhas

a14%

stakein

anAW

Bow

ner(SK

Deep

Sea).�

Controlof

vesselsenhances

Carimin’s

capabilityto

complete

works

within

scheduleand

thusputting

Carimin

ina

betterposition

tobid

fornew

contracts.

In-house Minor Fabrication Facilities

4�

Them

inorfabrication

yardin

Kemam

an,Terengganuenables

Carimin

tofabricate

minor/sm

allstructuresto

beused

forH

UC

&PM

US

projectsand

tofunction

asa

“one-stop”centre

form

aintenance,repairs

andsupport

services.

Pro

fileF

inan

cia

lsIn

du

stry

Gro

wth

IPO

Sta

tsIn

vM

erits

Ap

pen

dix

Se

t to S

ail…

Se

t to S

ail…

10

COM

PETITIVE A

DVA

NTA

GES &

KEY STRENG

THS (cont)

Co

mm

itted

toh

igh

HS

Esta

nd

ard

sw

itha

ne

xcelle

nt

track

reco

rd,

Ca

rimin

ha

se

stab

lishe

d

lon

g-te

rmre

latio

nsh

ips

with

itsclie

nts

an

dh

as

con

tinu

ou

slyse

cure

dn

ew

con

tracts…

Track Record5

�Carim

inhas

strongtrack

recordof

successfullydeveloping

andexpanding

itsbusiness

capabilitiessince

inceptionin

1989.�

Thishas

enabledCarim

into

establishits

customer

basew

hichhelps

tosecure

newprojects

andcustom

ers.

Long-term Contracts

6�

Carimin’s

abilityto

continuouslysecure

contractsw

ithterm

sof

more

than3

yearsprovides

assuranceof

businesssustainability

andenables

long-termbusiness

planning.�

Thishas

alsoenabled

toCarim

into

derivecost

savingsfrom

owning

assetsand

providedfor

sustainablegrow

ththrough

investment

inhum

anresource.

In-house Quality A

ssurance7

�Carim

inis

ISO9001:2008

accreditedfor

HU

C&

PMU

Sand

manpow

ersupply

servicesin

2011.�

Carimin

hasnot

experiencedany

losstim

eincident

sinceApril

2010and

receivedseveral

awards

andrecognitions

inrelation

tosafe

operationsfrom

itscustom

ers.

Pro

fileF

inan

cia

lsIn

du

stry

Gro

wth

IPO

Sta

tsIn

vM

erits

Ap

pen

dix

Se

t to S

ail…

Se

t to S

ail…

He

lme

db

yin

du

stryv

ete

ran

s…

11

KEY MA

NA

GEM

ENT

Mokhtar

Bin Hashim

Managing D

irector�

Involved in overall managem

ent and review for subm

ission of tender documents

�Engineer by training, he holds a Bachelor of Science in Civil Engineering from

the University of Salford, U

K �

25 years of hands-on operational experience, especially in hook-up, comm

issioning and onshore fabrication, ex Esso Production M

alaysia employee

ShatarBin A

bdul Ham

idExecutive D

irector�

In charge of project managem

ent�

Dip. in A

PI 653 Tank Managem

ent from Singapore W

elding Institute �

23 years of hands-on work experience in various roles e.g. Project

Director, Senior Construction Engineer/Project M

anager, Client Construction Site Representative (CSR)

Muham

mad H

attaBin

Noah

Supply Chain M

anagement M

anager

�Bsc. Petroleum

Engineering from

Texas Tech U

niversity, US

�23 years of w

ork experience in offshore oil &

gas industry

Mazhar

Bin PalilH

uman Resources

and Adm

inistration M

anager

�Bsc. Petroleum

Engineering from

Texas Tech U

niversity, US

�11 years of relevant experience in oil &

gas industry

Abd H

amid Bin H

usinD

eputy General

Manager of

Project Managem

ent

�Bsc. Civil Engineering from

University College

London, UK

�26 years of w

ork experience in offshore oil &

gas industry

Mad D

audBin

Sukarmin

Maintenance M

anager

�D

ip. in Mechanical

Engineering from

Akashi N

ational College of Technology, Japan

�24 years of relevant w

ork experience

Lee Heng A

unChief Financial

Officer

�FCCA

; MBA

from

Multim

edia University

�24 years of accounting and finance experience

RoslanBin M

oktiQ

uality Control M

anager

�D

ip. in Mechanical

Engineering from U

iTM�

32 years of work

experience in QA

/QC

IND

USTRY H

IGH

LIGH

TS

Se

t to S

ail…

Se

t to S

ail…

Pro

fileF

inan

cia

lsIn

du

stry

Gro

wth

IPO

Sta

tsIn

vM

erits

Ap

pen

dix

13

IND

USTRY STRU

CTURE

Ca

rimin

sup

po

rtsth

eo

ila

nd

ga

su

pstre

am

secto

r…

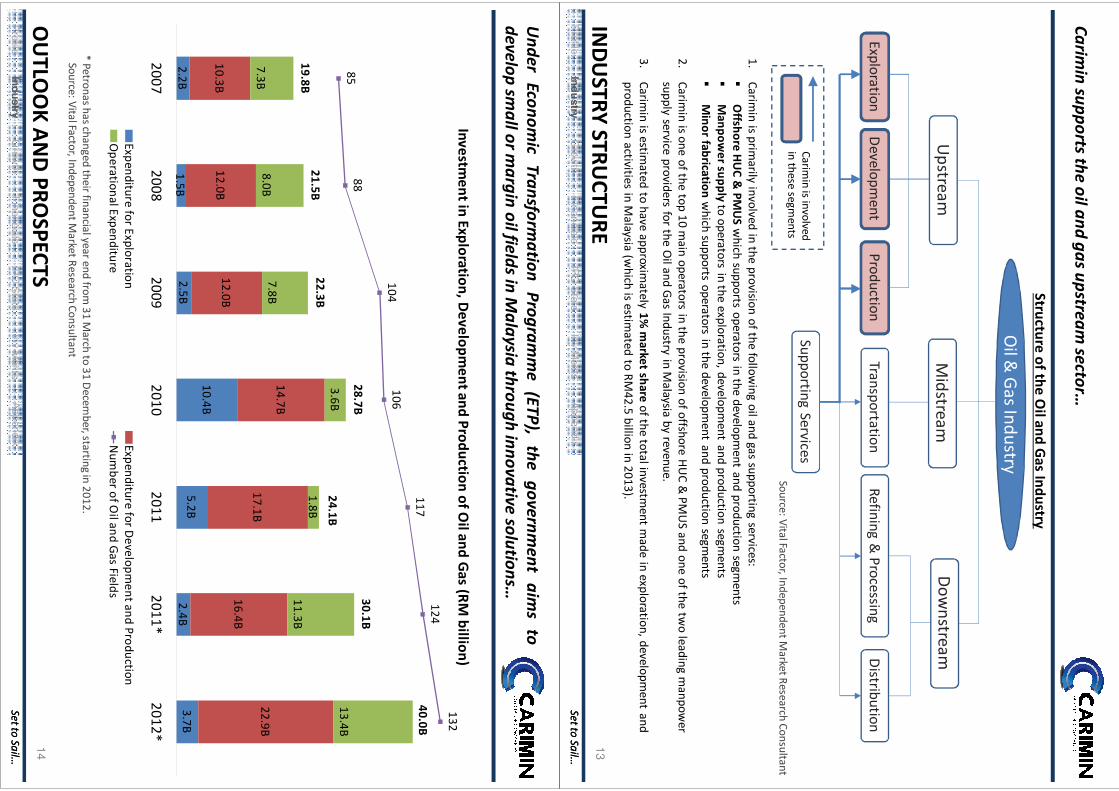

Structure of the Oil and G

as Industry

Oil &

Gas Industry

Upstream

Midstream

Dow

nstream

TransportationRefining &

ProcessingD

istributionExploration

Developm

entProduction

Supporting ServicesCarim

in is involved in these segm

ents

1.Carim

in is primarily involved in the provision of the follow

ing oil and gas supporting services:�

Offshore

HU

C & PM

US w

hich supports operators in the development and production segm

ents�

Manpow

er supply to operators in the exploration, development and production segm

ents�

Minor fabrication w

hich supports operators in the development and production segm

ents

2.Carim

in is one of the top 10 main operators in the provision of offshore H

UC &

PMU

S and one of the two leading m

anpower

supply service providers for the Oil and G

as Industry in Malaysia by revenue.

3.Carim

in is estimated to have approxim

ately 1% m

arket share of the total investment m

ade in exploration, development and

production activities in Malaysia (w

hich is estimated to RM

42.5 billion in 2013).

Source: Vital Factor, Independent Market Research Consultant

Se

t to S

ail…

Se

t to S

ail…

Pro

fileF

inan

cia

lsIn

du

stry

Gro

wth

IPO

Sta

tsIn

vM

erits

Ap

pen

dix

14

OU

TLOO

K AN

D PRO

SPECTS

Un

de

rE

con

om

icT

ran

sform

atio

nP

rog

ram

me

(ET

P),

the

go

ve

rnm

en

ta

ims

to

de

ve

lop

sma

llo

rm

arg

ino

ilfie

lds

inM

ala

ysia

thro

ug

hin

no

va

tive

solu

tion

s…

2.2B1.5B

2.5B

10.4B5.2B

2.4B3.7B

10.3B12.0B

12.0B

14.7B

17.1B

16.4B

22.9B7.3B

8.0B7.8B

3.6B

1.8B11.3B

13.4B

19.8B21.5B

22.3B

28.7B

24.1B

30.1B

40.0B

8588

104106

117124

132

20072008

20092010

20112011*

2012*

Investment in Exploration, D

evelopment and Production of O

il and Gas (RM

billion)

Expenditure for ExplorationExpenditure for D

evelopment and Production

Operational Expenditure

Num

ber of Oil and G

as Fields

* Petronas has changed their financial year end from 31 M

arch to 31 Decem

ber, starting in 2012.Source: Vital Factor, Independent M

arket Research Consultant

GRO

WTH

STRATEGIES

IND

USTRY H

IGH

LIGH

TSG

ROW

TH STRATEG

IES

Se

t to S

ail…

Se

t to S

ail…

Pro

fileF

inan

cia

lsIn

du

stry

Gro

wth

IPO

Sta

tsIn

vM

erits

Ap

pen

dix

16

GRO

WTH

STRATEGIES

Toa

cqu

iren

ew

ve

ssel,

de

ve

lop

min

or

fab

ricatio

ny

ard

an

dp

urch

ase

ne

w

eq

uip

me

nt

tosu

pp

ort

HU

C&

PM

US

op

era

tion

so

ffsho

rep

en

insu

lar

Ma

lay

sia…

Grow

th Strategies

Delivering O

utstanding Work Value Efficiently

�Secured a H

UC &

PMU

S contract with total value of

RM899 m

il from Petronas Carigali in N

ovember

2013

�W

ork orders amounting RM

92.4 mil has been

rolled out; remaining RM

800 mil to last until 2018

Investing in New

VesselD

eveloping New

Revenue Stream

�To develop its m

inor fabrication yard in Kemam

an, Terengganu by constructing new

facilities to support in-house operations

�To also purchase new

equipment to equip the yard

and to expand equipment rental services

Enhancing Capability and Equipment

�Purchase an AW

B (Ca

rimin

Aca

cia) w

hich is scheduled for delivery in June 2015 to support in-house H

UC &

PMU

S operations and to provide m

arine services to external customers

oRM

2.48 mil deposit has been paid; balance to be

funded via IPO proceeds (RM

35.32 mil) and bank

financing (RM57.20 m

il)

�Carim

in owns an A

HTS vessel (C

arim

in A

iris) and has a joint venture com

pany that is owner of an

AWB (S

K D

ee

p S

ea

) to support HU

C & PM

US

�Together w

ith Ca

rimin

Aca

cia, Carimin intends to

provide marine services to external custom

ers by 2015 to diversify custom

er and revenue base

FINA

NCIA

L HIG

HLIG

HTS

FINA

NCIA

L HIG

HLIG

HTS

Se

t to S

ail…

Se

t to S

ail…

Pro

fileF

inan

cia

lsIn

du

stry

Gro

wth

IPO

Sta

tsIn

vM

erits

Ap

pen

dix

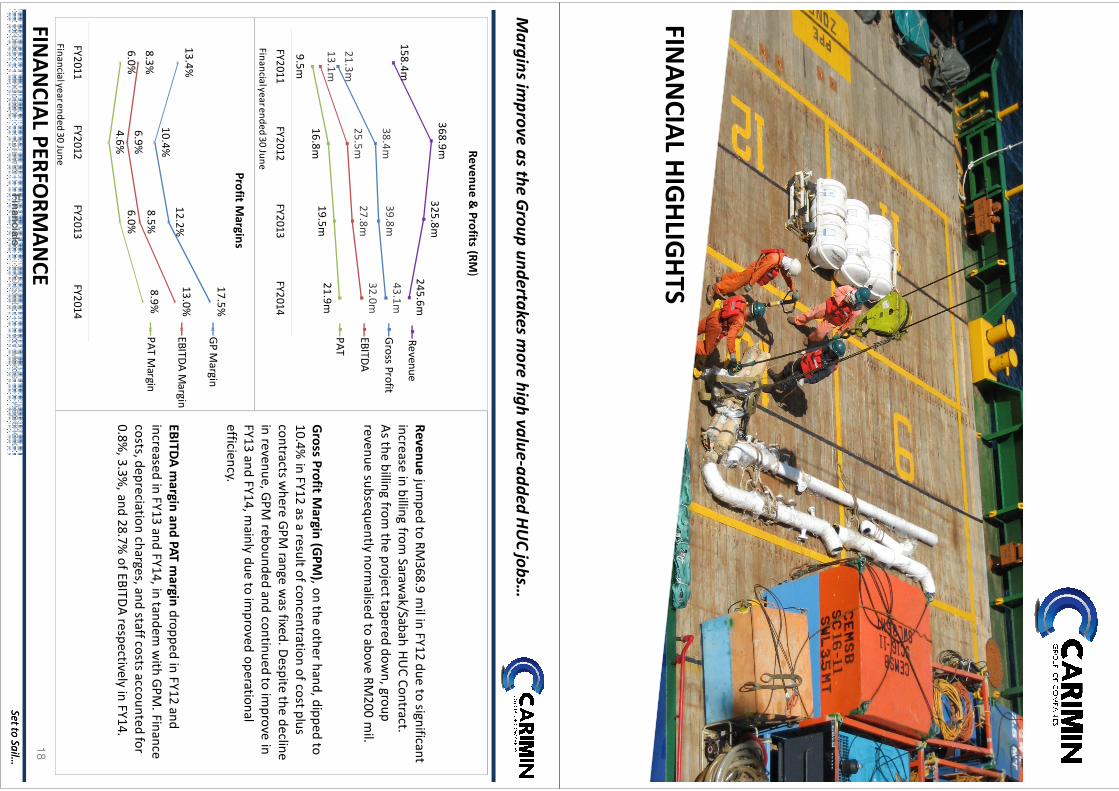

21.3m

38.4m39.8m

43.1m

13.1m

25.5m27.8m

32.0m

9.5m16.8m

19.5m21.9m

FY2011FY2012

FY2013FY2014

Revenue & Profits (RM

)

Gross Profit

EBITDA

PAT

158.4m

368.9m325.8m

245.6mRevenue

13.4%

10.4%12.2%

17.5%

8.3%6.9%

8.5%

13.0%

6.0%4.6%

6.0%

8.9%

FY2011FY2012

FY2013FY2014

Profit Margins

GP M

argin

EBITDA

Margin

PAT Margin

18

FINA

NCIA

L PERFORM

AN

CE

Ma

rgin

s imp

rov

e a

s the

Gro

up

un

de

rtak

es m

ore

hig

h v

alu

e-a

dd

ed

HU

C jo

bs…

Revenuejum

ped to RM368.9 m

il in FY12 due to significant increase in billing from

Sarawak/Sabah H

UC Contract.

As the billing from

the project tapered down, group

revenue subsequently normalised to above RM

200 mil.

Gross Profit M

argin (GPM

), on the other hand, dipped to 10.4%

in FY12 as a result of concentration of cost plus contracts w

here GPM

range was fixed. D

espite the decline in revenue, G

PM rebounded and continued to im

prove in FY13 and FY14, m

ainly due to improved operational

efficiency.

EBITDA

margin and PAT m

argin dropped in FY12 and increased in FY13 and FY14, in tandem

with G

PM. Finance

costs, depreciation charges, and staff costs accounted for 0.8%

, 3.3%, and 28.7%

of EBITDA

respectively in FY14.

Revenue & Profits (RM

)

Financialyear ended 30 June

Financial year ended 30 June

Revenue & Profits (RM

)

Se

t to S

ail…

Se

t to S

ail…

Pro

fileF

inan

cia

lsIn

du

stry

Gro

wth

IPO

Sta

tsIn

vM

erits

Ap

pen

dix

19

SEGM

ENTA

L REVEN

UE

Ma

np

ow

er su

pp

ly se

rvice

s ge

ne

ratin

g ste

ad

y re

ve

nu

e stre

am

wh

ile H

UC

& P

MU

S

seg

me

nt h

ad

be

com

e a

ma

jor re

ve

nu

e co

ntrib

uto

r…

Revenue by Market

(RM‘m

il)FY11

FY12FY13

FY14

Malaysia

158.4367.2

321.8237.3

Overseas

-1.7

3.98.2

Total Revenue158.4

368.9325.8

24

5.6

158.4

-

367.2

1.7

321.8

3.9

237.3

8.2

Malaysia

Overseas

Revenue by Market (RM

mil)

FY11FY12

FY13FY14

Revenue by Activities

(RM‘m

il)FY11

FY12FY13

FY14

Offshore H

UC &

PMU

S43.9

237.2206.0

158.9

Manpow

er

-Engineering &

exploration 16.0

18.622.7

31.4

-Project development

56.566.0

81.754.7

-Production/operations 18.4

24.213.2

0.0

90.9108.8

116.686.2

Minor fabrication

23.622.9

3.20.1

Equipment

rental*

-*

0.4

Total Revenue158.4

368.9325.8

24

5.6

27.7%

64.3%63.2%

64.7%

57.4%

29.5%35.8%

35.1%14.9%

6.2%1.0%

0%

20%

40%

60%

80%

100%

FY11FY12

FY13FY14

Revenue by Activities (%

)

HU

C & PM

US

Manpow

er

Minor Fabrication

Equipment Rental

*Negligible

Financial year ended 30 June

Financial year ended 30 June

Se

t to S

ail…

Se

t to S

ail…

Pro

fileF

inan

cia

lsIn

du

stry

Gro

wth

IPO

Sta

tsIn

vM

erits

Ap

pen

dix

13.4%

10.4%12.2%

17.5%

FY11FY12

FY13FY14

Group G

PM

20

Gro

up

GP

M w

as la

rge

ly d

rive

n b

y G

PM

for H

UC

& P

MU

S se

gm

en

t…w

hile

GP

M fo

r

ma

np

ow

er su

pp

ly se

rvice

s rem

ain

ed

rela

tive

ly sta

ble

SEGM

ENT M

ARG

IN

35.8%

7.3%12.0%

19.5%

FY11FY12

FY13FY14

GPM

(HU

C & PM

US Segm

ent)

HU

C & PM

US

�The high G

PM 35.8%

in FY11 was m

ainly due to extension of Talisman’s H

UC contract

where associated costs w

ere already incurred in FY10. �

GPM

dipped in FY12 mostly due to m

anpower and m

aterial costs that had lower

gross margin.

�G

PM then im

proved in FY13 and FY14 largely due to lump sum

method of w

ork orders and the com

pletion of Sarawak/Sabah H

UC Contracts.

Manpow

er Supply Services�

GPM

for manpow

er supply business, ranging from 10.5%

to 13.2% from

FY11 to FY14, are relatively stable com

pared to HU

C & PM

US segm

ent. Segment G

PM w

as largely driven by scale of w

ork orders from project developm

ent segment.

SegmentG

P & G

PMFY11

FY12FY13

FY14RM

‘m

il%

RM

‘mil

%RM

‘m

il%

RM

‘mil

%

Manpow

er

-Engineering & exploration

0.85

.11.5

7.9

2.19

.63.2

10

.2

-Project development

6.51

1.5

9.11

3.8

11.31

3.8

7.91

4.5

-Production/operations 2.4

12

.83.3

13

.62.1

15

.90.0

16

.7

9.71

0.5

13.81

2.7

15.41

3.2

11.11

3.9

Offshore H

UC &

PMU

S15.7

35

.817.2

7.3

24.71

2.0

31.01

9.5

Minor fabrication

(4.1)(1

7.5

)7.7

33

.71.4

44

.81.2

98

1.7

Equipmentrental

0.00

.0(0.4)

*(1.7)

*(0.3)

(69

.0)

Total GP/G

roup GPM

21.31

3.4

38.41

0.4

39.81

2.2

43.11

7.5

* Not applicable as revenue is generated internally.

10.5%12.7%

13.2%12.9%

FY11FY12

FY13FY14

GPM

(Manpow

er Segment)

0

Se

t to S

ail…

Se

t to S

ail…

Pro

fileF

inan

cia

lsIn

du

stry

Gro

wth

IPO

Sta

tsIn

vM

erits

Ap

pen

dix

21

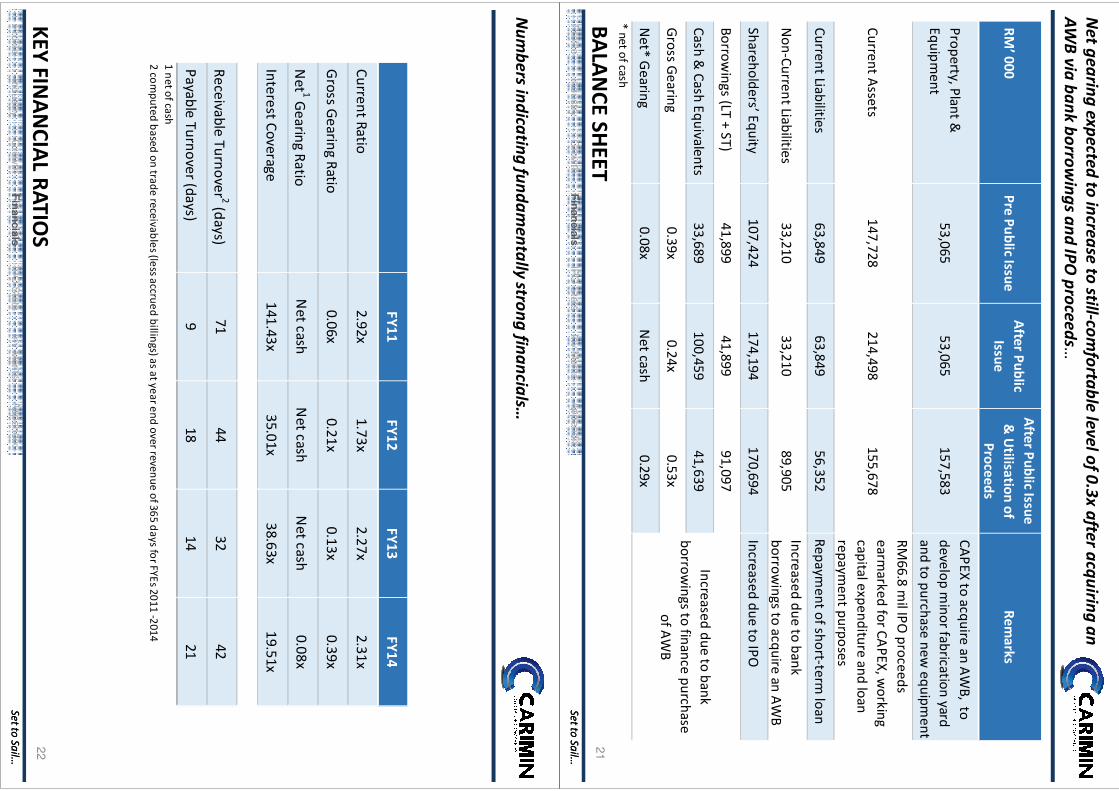

BALA

NCE SH

EET

Ne

t ge

arin

g e

xp

ecte

d to

incre

ase

to still-co

mfo

rtab

le le

ve

l of 0

.3x

afte

r acq

uirin

g a

n

AW

B v

ia b

an

k b

orro

win

gs a

nd

IPO

pro

cee

ds…

RM’ 000

Pre Public IssueA

fter Public Issue

After Public Issue &

Utilisation of

ProceedsRem

arks

Property, Plant &

Equipment

53,06553,065

157,583CA

PEX to acquire an AW

B, to develop m

inor fabrication yard and to purchase new

equipment

Current Assets

147,728214,498

155,678

RM66.8 m

il IPO proceeds

earmarked for CA

PEX, working

capital expenditure and loan repaym

ent purposes

Current Liabilities63,849

63,84956,352

Repayment of short-term

loan

Non-Current Liabilities

33,21033,210

89,905Increased due to bank borrow

ings to acquire an AW

B

Shareholders’ Equity107,424

174,194170,694

Increased due to IPO

Borrowings (LT + ST)

41,89941,899

91,097

Cash & Cash Equivalents

33,689100,459

41,639

Gross G

earing0.39x

0.24x0.53x

Net* G

earing0.08x

Net cash

0.29x* net of cash

Increased due to bank borrow

ings to finance purchase of A

WB

Se

t to S

ail…

Se

t to S

ail…

Pro

fileF

inan

cia

lsIn

du

stry

Gro

wth

IPO

Sta

tsIn

vM

erits

Ap

pen

dix

22

KEY FINA

NCIA

L RATIOS

Nu

mb

ers in

dica

ting

fun

da

me

nta

lly stro

ng

fina

ncia

ls…

FY11FY12

FY13FY14

Current Ratio2.92x

1.73x2.27x

2.31x

Gross G

earing Ratio0.06x

0.21x0.13x

0.39x

Net 1 G

earing RatioN

et cashN

et cashN

et cash0.08x

Interest Coverage141.43x

35.01x38.63x

19.51x

Receivable Turnover 2 (days)71

4432

42

Payable Turnover (days)9

1814

211 net of cash2 com

puted based on trade receivables (less accrued billings) as at year end over revenue of 365 days for FYEs 2011 -2014

IPO STATISTICS

IPO STATISTICS

Se

t to S

ail…

Se

t to S

ail…

Pro

fileF

inan

cia

lsIn

du

stry

Gro

wth

IPO

Sta

tsIn

vM

erits

Ap

pen

dix

24

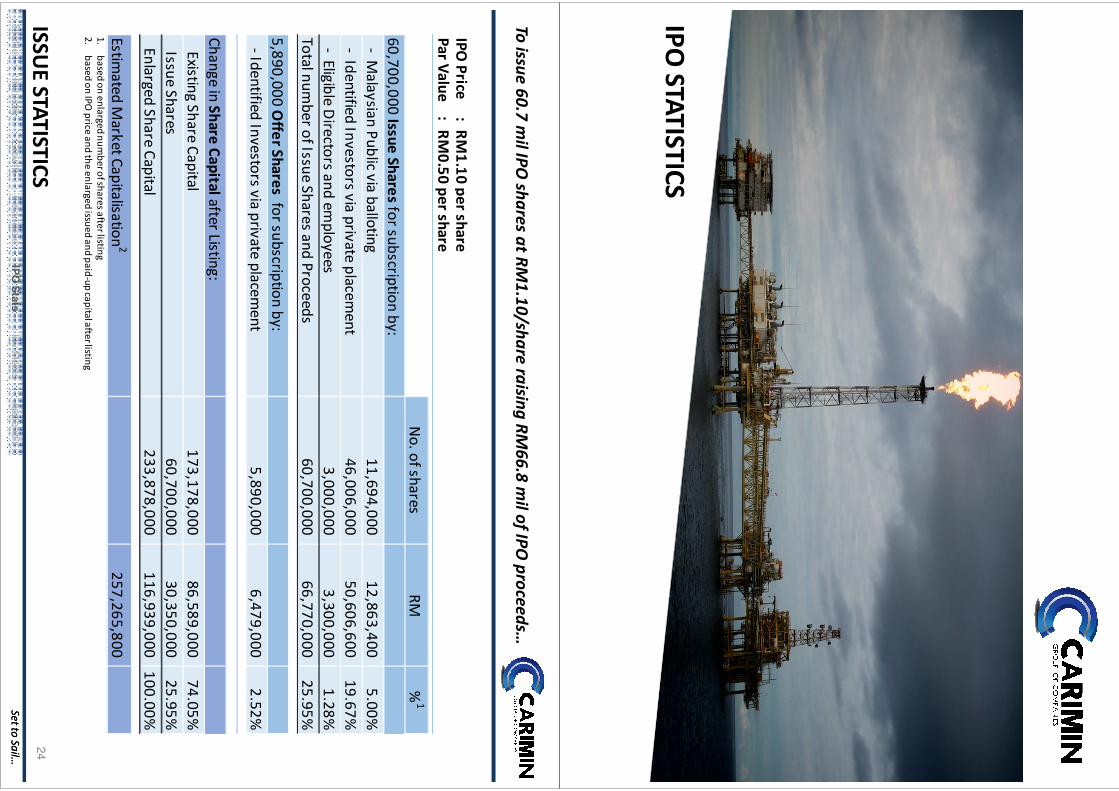

ISSUE STATISTICS

Toissu

e6

0.7

mil

IPO

sha

res

at

RM

1.1

0/sh

are

raisin

gR

M6

6.8

mil

of

IPO

pro

cee

ds…

IPO Price :

RM

1.10 per sharePar Value : R

M0.50 per share

No. of shares

RM%

1

60,700,000 Issue Shares for subscription by: 11,694,000

12,863,400

5.00%

46,006,000

50,606,600

19.67%3,000,000

3,300,000

1.28%

60,700,000

66,770,000

25.95%

5,890,000 Offer Shares for subscription by:

- Identified Investors via private placement

5,890,000

6,479,000

2.52%

Existing Share Capital 173,178,000

86,589,000

74.05%

60,700,000

30,350,000

25.95% Enlarged Share Capital

233,878,000

116,939,000

100.00%

257,265,800

Estimated M

arket Capitalisation2

Issue Shares

Change in Share Capital after Listing:

- Malaysian Public via balloting

- Identified Investors via private placement

- Eligible Directors and em

ployees Total num

ber of Issue Shares and Proceeds

1.based on enlarged num

ber of shares after listing2.

based on IPO price and the enlarged issued and paid-up capital after listing

Se

t to S

ail…

Se

t to S

ail…

Pro

fileF

inan

cia

lsIn

du

stry

Gro

wth

IPO

Sta

tsIn

vM

erits

Ap

pen

dix

25

ISSUE STRU

CTURE &

POST IPO

SHA

REHO

LDIN

GS

Ab

ou

t2

8%

free

floa

t…

Private Placement to

Identified Investors

①46.0 m

il new shares, 19.7%

*②

5.9 mil vendor shares^, 2.5%

*

RM 57.1m

Eligible Directors

and Employees

(Pink form)

3.0 mil new

shares, 1.3%*

RM 3.3m

Balloting(w

hite form)

11.7 mil new

shares, 5.0%*

RM 12.9m

Public Shareholders

66.6 mil shares, 27.9%

*

Promoters &

Substantial Shareholders

167.3 mil shares, 72.1%

*RM

6.5m

RM 66.7m

CARIM

IN PETRO

LEUM

BERHA

DIssue Price

: RM 1.10 per share

Par Value: RM

0.50 per shareEnlarged Share Capital

: RM 116.9 m

il Enlarged N

umber of Shares

: 233.9 mil

Post IPO Shareholdings

1. Mokhtar

Bin Hashim

: 31.8%2. Cipta

Pantas: 17.4%

3. Platinum Castle Sdn Bhd : 12.8%

4. ShatarBin A

bdul Ham

id : 6.9%5. Tan Sri D

ato’ Kam

aruzzaman

Bin Shariff: 3.0%

6. Others

: 0.1%

* Percentage of enlarged number of shares after IPO

^ Offerors

of the vendor shares are MokhtarBin H

ashim(offering 3.39 m

il shares) and Platinum Castle Sdn Bhd (offering 2.5 m

il shares)# M

okhtarBin Hashim

, ShatarBin Abdul H

amid and Tan Sri D

ato’ Kamaruzzam

anBin Shariffare eligible to subscribe 1.05 m

il shares, ie. 0.45% of enlarged num

ber of share after IPO

1.05 mil shares, 0.45%

#

Se

t to S

ail…

Se

t to S

ail…

Pro

fileF

inan

cia

lsIn

du

stry

Gro

wth

IPO

Sta

tsIn

vM

erits

Ap

pen

dix

26

UTILISATIO

N O

F IPO PRO

CEEDS

70

.8%

of

pro

cee

ds

or

RM

47

.3m

ilu

sed

for

the

pu

rcha

seo

fv

esse

la

nd

de

ve

lop

me

nt

of

min

or

fab

ricatio

ny

ard

toe

nh

an

cem

arin

ese

rvice

sa

nd

min

or

fab

ricatio

nca

pa

bilitie

s…

Utilisation of Proceeds

35.32m

12.00m

8.00m

7.95m

3.50m

Total: RM66.77m

%RM

Time fram

e

Purchase of offshore support vessel52.9%

12 months

Developm

ent of minor fabrication yard

18.0%18 m

onths

Repayment of bank borrow

ings12.0%

6m

onths

General w

orking capital11.9%

12 months

Estimated listing expenses

5.2%3 m

onths

100.0%

Se

t to S

ail…

Se

t to S

ail…

Pro

fileF

inan

cia

lsIn

du

stry

Gro

wth

IPO

Sta

tsIn

vM

erits

Ap

pen

dix

27

VALU

ATION

Ma

rke

tca

pita

lisatio

ne

stima

ted

tob

eR

M2

57

.3m

ilw

ithP

Ea

t1

1.8

x…

Market Capitalisation

1RM

257.3 mil

PE Multiple (FY14) 2

11.8x

P/NTA

31.5x

1 Based on IPO price of RM

1.10 per share and enlarged number of shares of 233.9 m

il2 Based on pro form

a FY14 EPS of 9.36 sen and enlarged number of shares of 233.9 m

il 3 Based on pro form

a post-IPO N

TA of 74 sen per share and enlarged num

ber of shares of 233.9 mil

Se

t to S

ail…

Se

t to S

ail…

Pro

fileF

inan

cia

lsIn

du

stry

Gro

wth

IPO

Sta

tsIn

vM

erits

Ap

pen

dix

28

TENTATIV

E IPO TIM

ELINE

Targ

et

tolist

by

ea

rlyN

ov

em

be

r2

01

4…

23 Oct 2014 (Thu)

Launch of Prospectus&

Application O

pen

29 Oct 2014 (W

ed)A

pplication Close

31 Oct 2014 (Fri)

Announcem

ent ofSubscription Results6

Nov 2014 (Thu)

Notice of A

llotment

To Shareholders

10 Nov 2014 (M

on)Listing on the M

ain Market

of Bursa Malaysia

INV

ESTMEN

T MERITS

INV

ESTMEN

T MERITS

Se

t to S

ail…

Se

t to S

ail…

Pro

fileF

inan

cia

lsIn

du

stry

Gro

wth

IPO

Sta

tsIn

v M

erits

Ap

pen

dix

30

INV

ESTMEN

T MERITS

Po

sitive

po

licies

pro

mo

ting

gro

wth

ino

ila

nd

ga

sin

du

stry…

un

de

ma

nd

ing

va

lua

tion

with

po

ten

tial

cap

italg

ain

Industry Outlook

1

Track Record2

Work Value

3

Grow

th4

Valuation5

PETRON

AS’ policy of promoting and encouraging the participation of local

operators in the oil and gas industry would facilitate grow

th in the industry, especially in exploration and production segm

ents.

Carimin has established long-term

relationships with m

any oil majors, providing

earnings and deal flows sustainability.

Carimin’s outstanding w

ork value amounted to approxim

ately RM900 m

il lasting 5 years up to 2018.

Moving forw

ard, Carimin w

ill acquire an AWB and upgrade its fabrication yard,

enhancing operational efficiencies and putting Carimin in better position in bidding

for projects.

Undem

anding valuation at historical PE of 11.8x compared to other oil and gas

peers in Malaysia.

Dividend Policy

6Carim

in intends to pay dividends to shareholders in the future, subject to financial perform

ance, capital expenditure and cash flows.

31

IR Contacts:M

r. Terence LooT: 03-2711 1391 / 012-629 5618

.my

THA

NK YO

U

APPEN

DIX

APPEN

DIX

Se

t to S

ail…

Se

t to S

ail…

Pro

fileF

inan

cia

lsIn

du

stry

Gro

wth

IPO

Sta

tsIn

vM

erits

Ap

pen

dix

33

GRO

UP STRU

CTURE

Carimin Petroleum

Berhad

Investment holding

Carimin

Engineering Sdn Bhd

HU

C & PM

US,

engineering and m

inor fabrication services

Carimin

Sdn Bhd(CSB)

Inspection, project m

anagement

support servicesOil &

Gas support

services

Dorm

ant

Investment holding

100%100%

Carimin

Corporate Services Sdn

Bhd

Corporate, m

anagement and

support services

Carimin

Airis

Offshore

Sdn Bhd

Marine related

support services

100%

Carimin

Marine

Services Sdn Bhd

Marine related

support services

Carimin

Equipment

Managem

entSdn Bhd

Provision of equipm

ent and tools

100%100%

Carimin

Resources Services Sdn

Bhd

Dorm

ant

100%100%

Se

t to S

ail…

Se

t to S

ail…

Pro

fileF

inan

cia

lsIn

du

stry

Gro

wth

IPO

Sta

tsIn

vM

erits

Ap

pen

dix

34

KEY MILESTO

NES

PeriodM

ilestones

1989CSB w

as incorporated

1990CSB began business operations w

ith theprovision of m

anpower supply services

1992Secured

a 2-year contract from Esso M

alaysia to provide general inspection services

1997Secured a contract from

Petronas Carigali to supplytechnical professionals over 4-year period

2000Secured a m

anpower supply services contract to supply drilling professionals from

Murphy O

il

2003D

iversified itsbusiness to provide m

inor fabrication services for the offshore oil and gas industry

2004Started

to provide production platform system

maintenance services for Petronas Carigali

2005M

inor fabrication yard located at Kemam

an,Terengganu began operations

2006Carim

in Engineering began business operations

2007Secured first offshore H

UC contract from

Murphy O

il and another offshore HU

C contract from Talism

an

2010Secured the Saraw

ak/Sabah HU

C Contract from Petronas Carigali

2011

Began provision of equipment rental services

CSB received ISO 9001:2008 quality m

anagement system

certificationfor the scope of “provision of m

anpower supply for oil and

gas industry” while Carim

inEngineering

received ISO 9001:2008 quality m

anagement system

certificationfor the scope of

“provision of engineering, procurement, construction, hook up and com

missioning for oil and gas industry”

2012A

cquired Carimin M

arine, which has

a 14% investm

ent in SK Offshore, w

ho owns SK D

eep Sea, an AWB, to pave w

ay for the provision of offshore m

arine support vessel services

2013A

cquired Carimin A

iris Vessel, an AH

TS vessel

Secured the Peninsular Malaysia H

UC Contract from

Petronas Carigali

2014Com

missioned to build Carim

in Acacia, an AW

B

Se

t to S

ail…

Se

t to S

ail…

Pro

fileF

inan

cia

lsIn

du

stry

Gro

wth

IPO

Sta

tsIn

vM

erits

Ap

pen

dix

35

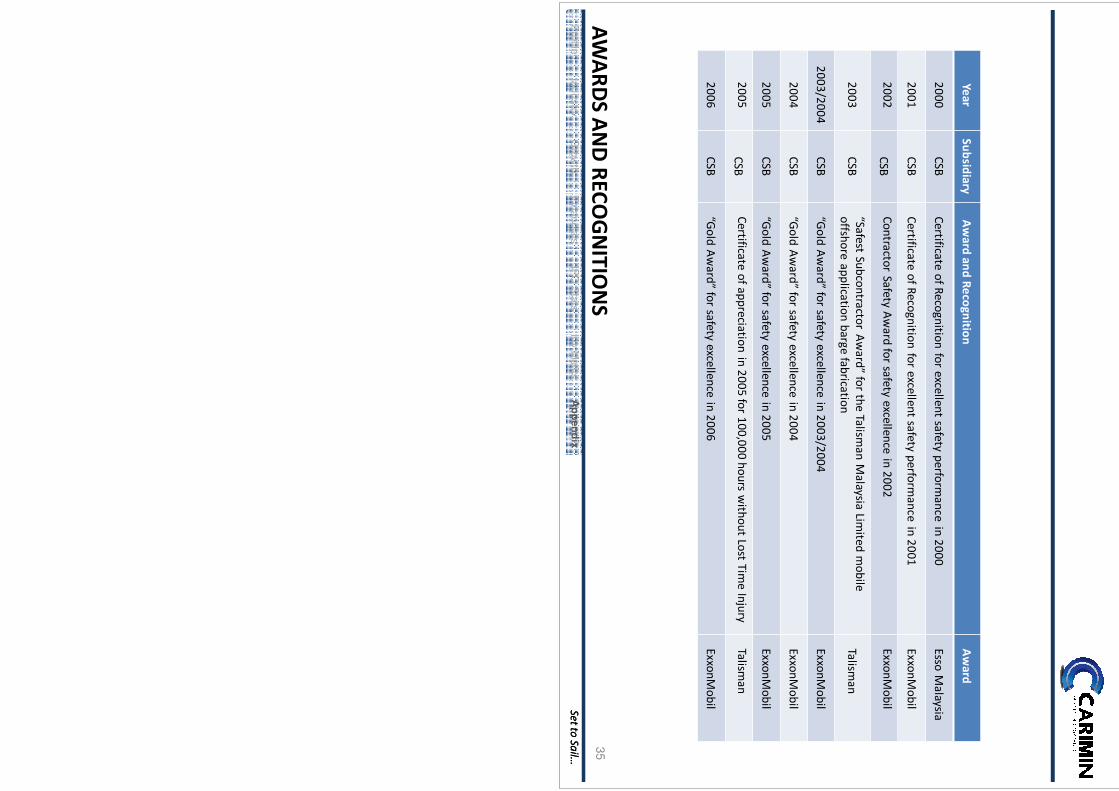

AWA

RDS A

ND

RECOG

NITIO

NS

YearSubsidiary

Aw

ard and RecognitionA

ward

2000CSB

Certificate of Recognitionfor excellent safety perform

ance in 2000Esso M

alaysia

2001CSB

Certificate of Recognition for excellent safetyperform

ance in 2001ExxonM

obil

2002CSB

Contractor SafetyA

ward for safety excellence in 2002

ExxonMobil

2003CSB

“Safest Subcontractor Aw

ard” for the Talisman

Malaysia Lim

ited mobile

offshore application barge fabricationTalism

an

2003/2004CSB

“Gold A

ward” for safety excellence in 2003/2004

ExxonMobil

2004CSB

“Gold A

ward” for safety excellence in 2004

ExxonMobil

2005CSB

“Gold A

ward” for safety excellence in 2005

ExxonMobil

2005CSB

Certificate ofappreciation in 2005 for 100,000 hours without Lost Tim

e InjuryTalism

an

2006CSB

“Gold A

ward” for safety excellence in 2006

ExxonMobil