Embed Size (px)

Citation preview

1

CARICOM Foreign Direct Investment Flows

Preeya Shalini Mohan ([email protected])

&

Patrick Kent Watson1 ([email protected])

Sir Arthur Lewis Institute of Social and Economic Studies

University of the West Indies St. Augustine

Trinidad & Tobago

Tel: (868) 662-6965 Fax: (868) 645-6329

Abstract

Foreign direct investment (FDI) flows to the Caribbean play a critical role in relation to growth

and development. This paper provides evidence about the nature and pattern of CARICOM FDI

flows. A Gravity model, estimated using the Hausman-Taylor procedure for panel data, is used

to explain such flows between a selection of CARICOM and OECD countries. Income in both

the host and destination countries play a significant role in FDI flows, as do the level of financial

development and tax regime in the host country, and the existence of trading and service

agreements between host and destination countries. Policy recommendations are made to improve

the flows to and within CARICOM markets.

JEL Classification: F21; F36; G11; G34

Keywords: Foreign direct investment flows; CARICOM, Gravity Model

January 2012

1Corresponding author.

1

Introduction

The extent of globalization and financial integration has caused cross-border

Foreign Direct Investment (FDI) flows to increase exponentially since the 1980’s,

outpacing growth in world trade and GDP (UNCTAD 2008). In the existing

literature, primary focus is on FDI flows arising out of industrialized countries

and the larger developing countries of Latin America, Asia and Africa while the

study of FDI flows among small countries, such as those in the CARICOM2

region, is relatively limited. Where they do exist, studies of CARICOM FDI to

date focus mainly on its theoretical aspects (Craigwell 2006).

This paper is an attempt to fill that knowledge gap. It offers both a theoretical

explanation and empirical evidence about the nature and pattern of CARICOM

FDI flows and a Gravity model is used to explain such flows between OECD and

CARICOM countries. The OECD countries are chosen because they are the

largest source of such flows into the CARICOM region.

It is a matter of debate whether these flows are useful for a country’s development

or whether they do more harm than good. There is some evidence that FDI flows

may be associated with increasing economic growth and development: the World

Bank (2010), for instance, suggests that increases in these flows are associated

with higher growth in GDP per capita and vice versa. Furthermore, although

inflows to low income economies have historically been lower than inflows into

high income economies, since 2005, inflows into low income economies have

2 CARICOM (the Caribbean Community and Common Market) is a grouping of 14 Caribbean

countries: Antigua & Barbuda, Belize, Grenada, Montserrat, St. Vincent & the Grenadines, The Bahamas, British Virgin Islands, Guyana, St. Kitts & Nevis, Suriname, Barbados, Dominica, Jamaica, Saint Lucia and Trinidad & Tobago.

2

been higher and the growth in GDP per capita of these countries correspondingly

higher. As a consequence, low income countries, and even not-so-low income

countries like those of the CARICOM region, continue to adopt loose capital

control policies and pursue an agenda of open capital markets to encourage such

flows. On the other hand, arguments have been put forward about the volatility

and possible dangers associated with these flows, but Grabel (1999) makes the

important point that, despite such arguments, it is unrealistic for countries to cut

them off. Instead, appropriate policies and institutions should be put in place to

maximize the benefits from these flows and minimize their costs.

A major problem faced in attempting a study like this one is the lack of data on

FDI inflows and outflows by geographic source and destination for Caribbean

countries (Harrison 2005). All Central Banks of the CARICOM region, except

that of Trinidad & Tobago, do not have data on FDI inflows and outflows by

source and destination. The United Nations Conference on Trade and

Development (UNCTAD) also has data on FDI inflows and outflows for Trinidad

& Tobago only and cover the period 1990 to 2002.

The rest of this paper is structured as follows: in the following section, stylized

facts about CARICOM cross-border equity flows are presented. This is followed

by some theoretical considerations about the principal determinants of such flows,

which is then used in the construction of the gravity model employed to

investigate the FDI outflows of a selection of CARICOM and OECD countries.

The results obtained from the estimation of this model by the Hausman-Taylor

estimator are then discussed, then followed by policy recommendations, which

3

are based both on the stylized facts and the results of the estimation of the gravity

model. The paper then concludes.

CARICOM FDI flows: some stylized facts

CARICOM FDI is primarily Greenfield3 investments, which is not unusual for

developing countries as foreign investors find that there are not many suitable

firms to merge with or acquire. Among CARICOM countries, Trinidad & Tobago

is both the main recipient and investor of FDI. Compared to its regional

counterparts, Trinidad and Tobago is a relatively high-income country, with stable

inflation and exchange rates and relatively more developed financial markets.

Trinidad & Tobago is also the only country in that grouping that has

disaggregated FDI data, which makes measuring CARICOM cross-county FDI

difficult.

Table 1 shows that world FDI inflows have increased four-fold from 1995 to

2010. CARICOM inflows have also increased by a similar margin: from US$827

million in 1995 to US$ 3000 million in 2010 (UNCTAD 2009). The region’s

share of world FDI inflows is minuscule, averaging approximately 0.3% of world

FDI inflows (see table 1). Compared to the larger developing economies, the

group appears to be quite insignificant, but the picture changes somewhat when it

is compared with other emerging countries: for example, the region attracted

greater FDI inflows than developing Oceana, a region of comparable level of

development.

3 FDI takes two forms: Greenfield investments and mergers and acquisitions. The acquisition of new plant

and equipment in an overseas country is a Greenfield investment. A merger or acquisition takes place when a foreign firm acquires an existing firm in the target country. Greenfield investments are less popular and the data show that mergers and acquisitions have been the primary form of world FDI flows since the 1980’s (UNCTAD 2002).

4

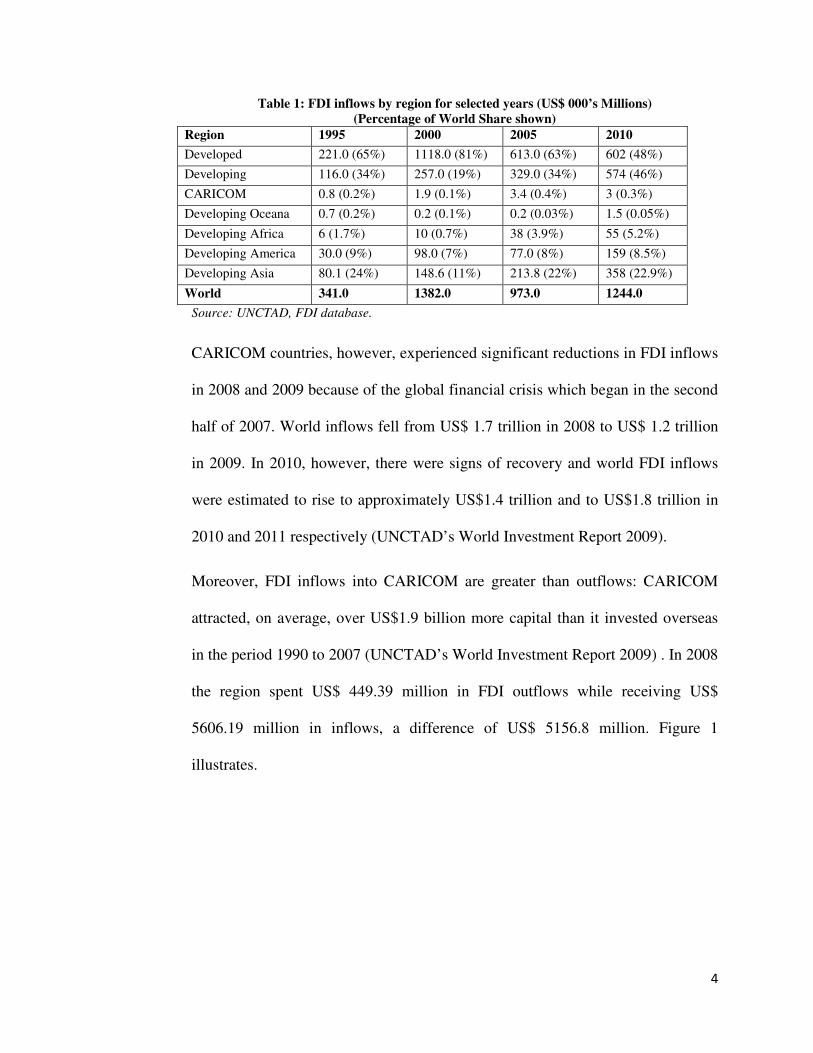

Table 1: FDI inflows by region for selected years (US$ 000’s Millions) (Percentage of World Share shown)

Region 1995 2000 2005 2010

Developed 221.0 (65%) 1118.0 (81%) 613.0 (63%) 602 (48%)

Developing 116.0 (34%) 257.0 (19%) 329.0 (34%) 574 (46%)

CARICOM 0.8 (0.2%) 1.9 (0.1%) 3.4 (0.4%) 3 (0.3%)

Developing Oceana 0.7 (0.2%) 0.2 (0.1%) 0.2 (0.03%) 1.5 (0.05%)

Developing Africa 6 (1.7%) 10 (0.7%) 38 (3.9%) 55 (5.2%)

Developing America 30.0 (9%) 98.0 (7%) 77.0 (8%) 159 (8.5%)

Developing Asia 80.1 (24%) 148.6 (11%) 213.8 (22%) 358 (22.9%)

World 341.0 1382.0 973.0 1244.0

Source: UNCTAD, FDI database.

CARICOM countries, however, experienced significant reductions in FDI inflows

in 2008 and 2009 because of the global financial crisis which began in the second

half of 2007. World inflows fell from US$ 1.7 trillion in 2008 to US$ 1.2 trillion

in 2009. In 2010, however, there were signs of recovery and world FDI inflows

were estimated to rise to approximately US$1.4 trillion and to US$1.8 trillion in

2010 and 2011 respectively (UNCTAD’s World Investment Report 2009).

Moreover, FDI inflows into CARICOM are greater than outflows: CARICOM

attracted, on average, over US$1.9 billion more capital than it invested overseas

in the period 1990 to 2007 (UNCTAD’s World Investment Report 2009) . In 2008

the region spent US$ 449.39 million in FDI outflows while receiving US$

5606.19 million in inflows, a difference of US$ 5156.8 million. Figure 1

illustrates.

Figure 1: CARICOM FDI inflows and o

Source: UNCTAD, FDI Statistics database

All CARICOM countries

from increases in

significant year to ye

region are becoming progressively concentrated

Tobago followed by the Bahamas and then Jamaica (see figure 2)

Trade and Investment Report (2005) found tha

Bahamas, Jamaica, Saint Lucia, Suriname and Trinidad

investment recipients

& Tobago, the Bahamas and Jamaica

1: CARICOM FDI inflows and outflows, 1990-2008 (

FDI Statistics database.

CARICOM countries, except Saint Kitts & Nevis and Suriname

in FDI inflows over the period 2000 to 2008 but

significant year to year fluctuations. In recent times, inflows to the CARICOM

region are becoming progressively concentrated going mainly to Trinidad &

Tobago followed by the Bahamas and then Jamaica (see figure 2)

Trade and Investment Report (2005) found that, in 2005, Antigua & Barbuda, t

ahamas, Jamaica, Saint Lucia, Suriname and Trinidad & Tobago were the main

investment recipients, attracting 85% of FDI inflows but, in 2008, only Trinidad

the Bahamas and Jamaica accounted for this same percentage.

5

2008 (US$ Million)

Nevis and Suriname, benefitted

over the period 2000 to 2008 but there were

inflows to the CARICOM

going mainly to Trinidad &

Tobago followed by the Bahamas and then Jamaica (see figure 2). The Caribbean

t, in 2005, Antigua & Barbuda, the

Tobago were the main

but, in 2008, only Trinidad

his same percentage.

Figure 2: CARICOM FDI

Source: UNCTAD, FDI database.

The UNCTAD’s

Trinidad & Tobago as having high FDI

Guyana were classified as having

Haiti and Suriname were

ranked the Bahamas

countries in terms of

Guyana 11th in 2007,

ranked 40th in 2004

CARICOM FDI inflows, 2000-2008(US$ Million)

Source: UNCTAD, FDI database.

World Investment Report (2008) classified the Bahamas and

Tobago as having high FDI performance and potential,

classified as having high FDI performance but low potential while

Haiti and Suriname were considered to be underperformers. T

ranked the Bahamas 5th, Jamaica 26th and Trinidad & Tobago 54

countries in terms of FDI inflows for 2007. Additionally, the report ranke

in 2007, which is a significant improvement given that Guyana

in 2004. Although Trinidad & Tobago fell from 15th in 2004 to 54

6

World Investment Report (2008) classified the Bahamas and

performance and potential, Jamaica and

formance but low potential while

underperformers. The report also

and Trinidad & Tobago 54th out of 141

Additionally, the report ranked

ignificant improvement given that Guyana was

in 2004 to 54th in

7

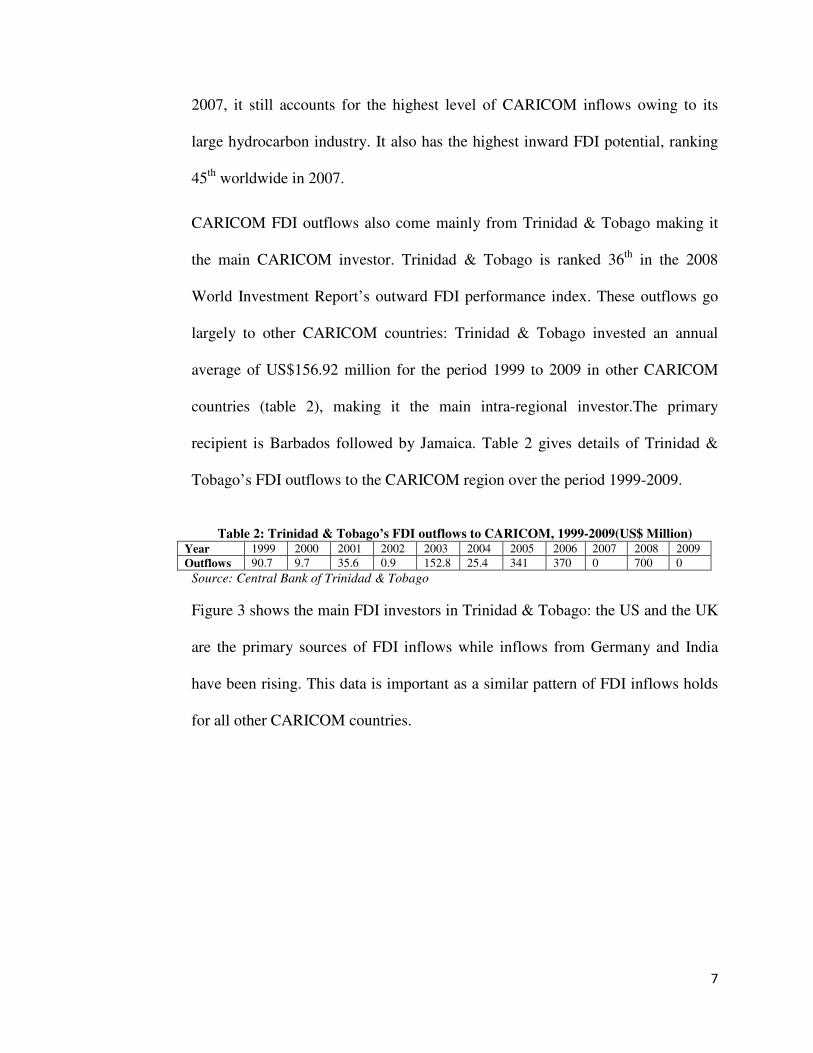

2007, it still accounts for the highest level of CARICOM inflows owing to its

large hydrocarbon industry. It also has the highest inward FDI potential, ranking

45th worldwide in 2007.

CARICOM FDI outflows also come mainly from Trinidad & Tobago making it

the main CARICOM investor. Trinidad & Tobago is ranked 36th in the 2008

World Investment Report’s outward FDI performance index. These outflows go

largely to other CARICOM countries: Trinidad & Tobago invested an annual

average of US$156.92 million for the period 1999 to 2009 in other CARICOM

countries (table 2), making it the main intra-regional investor.The primary

recipient is Barbados followed by Jamaica. Table 2 gives details of Trinidad &

Tobago’s FDI outflows to the CARICOM region over the period 1999-2009.

Table 2: Trinidad & Tobago’s FDI outflows to CARICOM, 1999-2009(US$ Million)

Year 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Outflows 90.7 9.7 35.6 0.9 152.8 25.4 341 370 0 700 0

Source: Central Bank of Trinidad & Tobago

Figure 3 shows the main FDI investors in Trinidad & Tobago: the US and the UK

are the primary sources of FDI inflows while inflows from Germany and India

have been rising. This data is important as a similar pattern of FDI inflows holds

for all other CARICOM countries.

Figure 3: Trinidad & Tobago

Source: Central Bank of

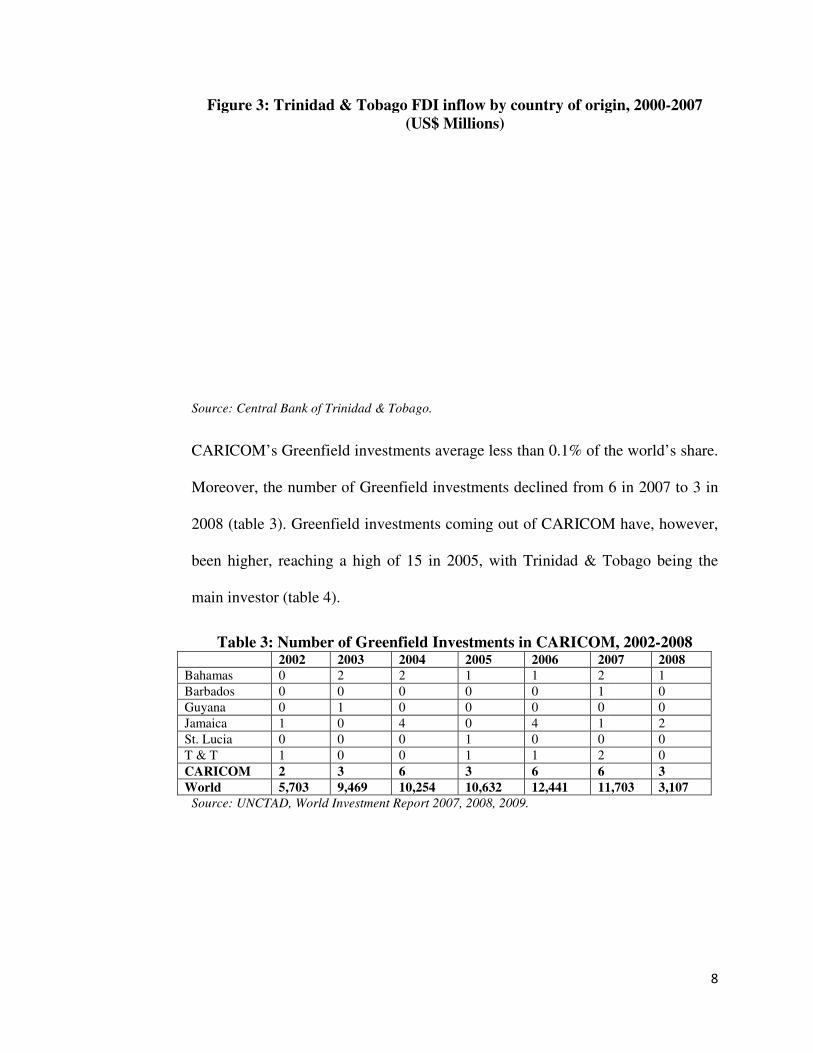

CARICOM’s Greenfield investments average less than 0.1% of the world’s share

Moreover, the number of Greenfield investments declined from

2008 (table 3). Greenfield investments coming out of CARICOM have

been higher, reaching a high of

main investor (table 4

Table 3: Number of 2002Bahamas 0

Barbados 0

Guyana 0

Jamaica 1

St. Lucia 0

T & T 1

CARICOM 2

World 5,703Source: UNCTAD, World Investment Report 2007, 2008, 2009.

Figure 3: Trinidad & Tobago FDI inflow by country of origin, 2000(US$ Millions)

Source: Central Bank of Trinidad & Tobago.

CARICOM’s Greenfield investments average less than 0.1% of the world’s share

Moreover, the number of Greenfield investments declined from

). Greenfield investments coming out of CARICOM have

been higher, reaching a high of 15 in 2005, with Trinidad & Tobago

or (table 4).

Number of Greenfield Investments in CARICOM, 2002 2003 2004 2005 2006 2007

2 2 1 1 2

0 0 0 0 1

1 0 0 0 0

0 4 0 4 1

0 0 1 0 0

0 0 1 1 2

3 6 3 6 6

5,703 9,469 10,254 10,632 12,441 11,703UNCTAD, World Investment Report 2007, 2008, 2009.

8

inflow by country of origin, 2000-2007

CARICOM’s Greenfield investments average less than 0.1% of the world’s share.

6 in 2007 to 3 in

). Greenfield investments coming out of CARICOM have, however,

Trinidad & Tobago being the

in CARICOM, 2002-2008 2007 2008

1

0

0

2

0

0

3

11,703 3,107

9

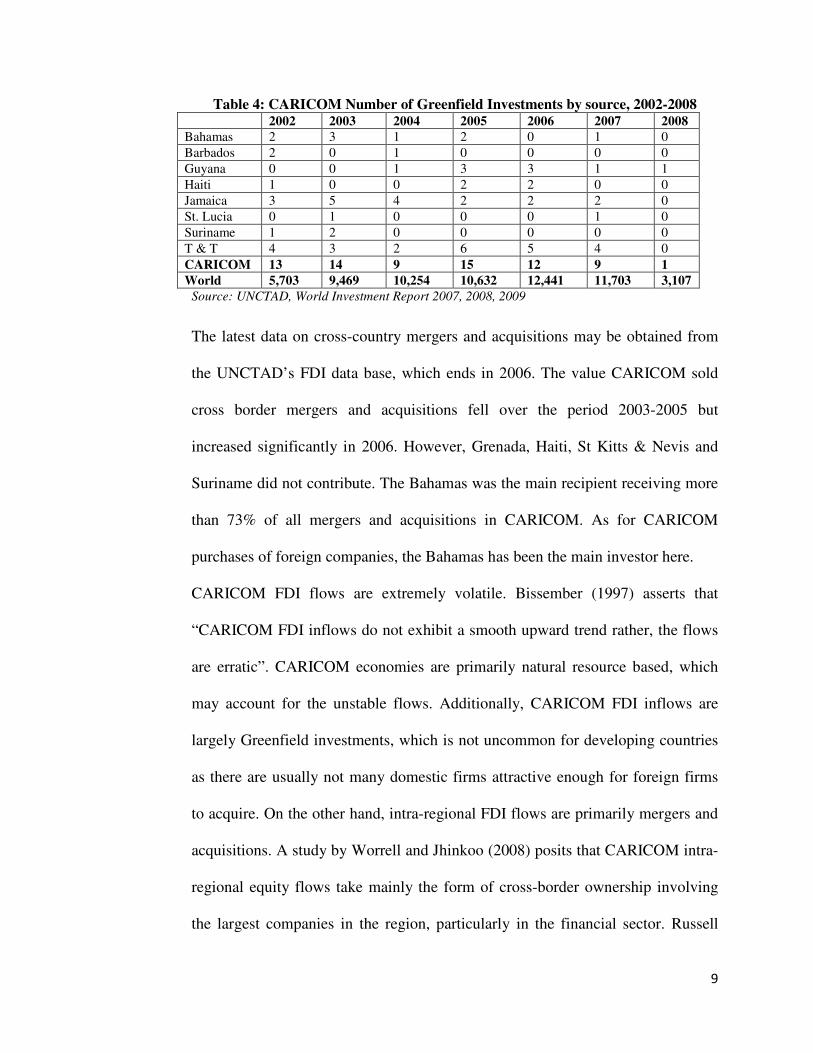

Table 4: CARICOM Number of Greenfield Investments by source, 2002-2008 2002 2003 2004 2005 2006 2007 2008 Bahamas 2 3 1 2 0 1 0

Barbados 2 0 1 0 0 0 0

Guyana 0 0 1 3 3 1 1

Haiti 1 0 0 2 2 0 0

Jamaica 3 5 4 2 2 2 0

St. Lucia 0 1 0 0 0 1 0

Suriname 1 2 0 0 0 0 0

T & T 4 3 2 6 5 4 0

CARICOM 13 14 9 15 12 9 1 World 5,703 9,469 10,254 10,632 12,441 11,703 3,107

Source: UNCTAD, World Investment Report 2007, 2008, 2009

The latest data on cross-country mergers and acquisitions may be obtained from

the UNCTAD’s FDI data base, which ends in 2006. The value CARICOM sold

cross border mergers and acquisitions fell over the period 2003-2005 but

increased significantly in 2006. However, Grenada, Haiti, St Kitts & Nevis and

Suriname did not contribute. The Bahamas was the main recipient receiving more

than 73% of all mergers and acquisitions in CARICOM. As for CARICOM

purchases of foreign companies, the Bahamas has been the main investor here.

CARICOM FDI flows are extremely volatile. Bissember (1997) asserts that

“CARICOM FDI inflows do not exhibit a smooth upward trend rather, the flows

are erratic”. CARICOM economies are primarily natural resource based, which

may account for the unstable flows. Additionally, CARICOM FDI inflows are

largely Greenfield investments, which is not uncommon for developing countries

as there are usually not many domestic firms attractive enough for foreign firms

to acquire. On the other hand, intra-regional FDI flows are primarily mergers and

acquisitions. A study by Worrell and Jhinkoo (2008) posits that CARICOM intra-

regional equity flows take mainly the form of cross-border ownership involving

the largest companies in the region, particularly in the financial sector. Russell

10

and Khan (1996) and Rambarran and Elbourne (2006) have suggested several

reasons for this: it is cheap for CARICOM firms to expand this way, government

divesture mainly among commercial banks and some activity among insurance

companies and directives from multilateral lending agencies. Moreover,

CARICOM mergers and acquisitions come from the commercial banking sector.

This is not uncommon and, internationally, the same trend is observed as

companies in the financial sector frequently expand through mergers and

acquisitions.

However, merger and acquisition activity in the region is still quite limited. This

may be due to “the thinness of CARICOM stock exchanges, the low level of

development in the financial sector and a predominance of family owned and

controlled businesses” (Russell and Khan 1996).

In summary there have been few empirical studies on CARICOM FDI flows.

Furthermore, data limitations in the region do not permit a comprehensive

measure of the amount of cross-country flows that do take place. Although the

CARICOM region has been subject to a fair amount of FDI activity, there are

wide disparities across member states. Intra-regional investments come largely

from Trinidad & Tobago with the major recipient being Barbados, followed by

Jamaica. The smaller CARICOM economies must avoid marginalization and seek

to attract external capital as the region seeks to become a single integrated

regional space.

11

Theoretical Considerations

Possible determinants of FDI flows have been identified in the literature as

economic size, macroeconomic stability, level of financial sophistication, trade,

transactions cost, geography, common culture, information asymmetries, the level

of financial liberalization, institutional, political and legal factors. See for

example Portes and Rey (2005), Di Giovanni (2005), Portes et al (2001) and

Tesar, and Werner (1994). These factors are divided into external “push’ factors

and domestic “pull” factors. Push factors are forces which act to drive investors

away from an investment and pull factors are what draws investors to a new

location.

The literature identifies the size of the economy of both the investor and target

countries as primary determinants of FDI flows (Di Giovanni 2005): the larger the

size of a country’s GDP, the more it becomes attractive to foreign investors, who

see greater profit opportunities there, but also the more that country itself has the

wherewithal to invest elsewhere. Foreign investors also tend to consider the

inflation and exchange rates of the host country: high inflation and unstable

exchange rates tend to discourage FDI (Froot and Stein 1991 and Grosse and

Trevino 1996).

Investment also seems to flow from, and flow to countries with relatively

developed financial markets (Hijzen et al 2007). Financial markets provide the

necessary capital to undertake costly foreign investment. .

Trade flows and FDI flows are also related. See for example Brainard (1997),

Markusen (2002), Carr et al (2001) and Blonigen et al (2003). According to the

12

“tariff-jumping” hypothesis foreign firms enter domestic markets through exports

or by setting up a local subsidiary: as export costs increase, mainly through the

implementation of higher tariffs, foreign firms are more likely to set up a local

branch creating a negative relationship between FDI and trade. However,

empirical models also provide evidence that FDI and trade are directly related.

The breakup of the production process, the large distribution of global networks

and improvements in communication and production technology have been

identified as reasons for this finding. Moreover, Regional Trade and Service

Agreements (RTSAs) may also affect FDI since they normally include clauses

favouring investment and rules which regulate such cross-border investment (Di

Giovanni 2005).

The greater the distance between the investor and the host country, the higher the

‘transactions costs’ are likely to be, and this is likely to reduce FDI. However,

empirical evidence shows that FDI and distance are positively related (Portes and

Rey 2005, Di Giovanni 2005 and Tesar and Werner 1994). On the other hand, a

common culture and legal system would logically tend to encourage FDI (Buch,

Gayle and De Long 2004). The tax regime in the host country can also act to

attract or discourage FDI: the more oppressive it is, the less the likely FDI flows

(Di Giovanni 2005).

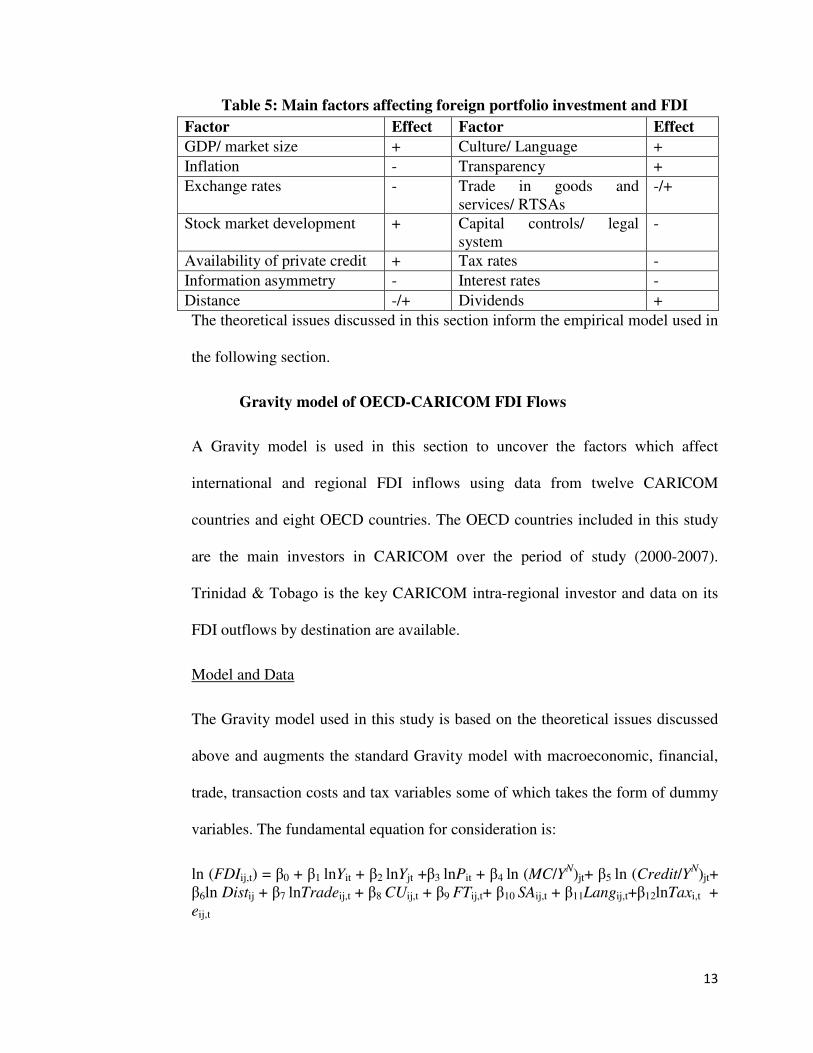

Table 5 summarizes the main factor affecting FDI.

13

Table 5: Main factors affecting foreign portfolio investment and FDI

Factor Effect Factor Effect

GDP/ market size + Culture/ Language +

Inflation - Transparency +

Exchange rates - Trade in goods and services/ RTSAs

-/+

Stock market development + Capital controls/ legal system

-

Availability of private credit + Tax rates -

Information asymmetry - Interest rates -

Distance -/+ Dividends +

The theoretical issues discussed in this section inform the empirical model used in

the following section.

Gravity model of OECD-CARICOM FDI Flows

A Gravity model is used in this section to uncover the factors which affect

international and regional FDI inflows using data from twelve CARICOM

countries and eight OECD countries. The OECD countries included in this study

are the main investors in CARICOM over the period of study (2000-2007).

Trinidad & Tobago is the key CARICOM intra-regional investor and data on its

FDI outflows by destination are available.

Model and Data

The Gravity model used in this study is based on the theoretical issues discussed

above and augments the standard Gravity model with macroeconomic, financial,

trade, transaction costs and tax variables some of which takes the form of dummy

variables. The fundamental equation for consideration is:

ln (FDIij,t) = β0 + β1 lnYit + β2 lnYjt +β3 lnPit + β4 ln (MC/YN)jt+ β5 ln (Credit/YN)jt+ β6ln Distij + β7 lnTradeij,t + β8 CUij,t + β9 FTij,t+ β10 SAij,t + β11Langij,t+β12lnTaxi,t + eij,t

14

where “i” is the target country, “j” the investor country, t represents time, FDIij,t

measures gross FDI outflows from country i to country j in year t, Y real GDP, P

the price level, MC stock market capitalization, Credit is credit provided by the

private sector (bank and other non bank financial institutions), YN nominal GDP,

Distij the distance between the capital cities of countries i and j, Tradeij is real

goods trade flow from country i to j, CUij is a dummy variable equal to1 if

countries i and j belong to a common Customs Union, FTij is a dummy variable

equal to 1 if countries i and j belong to a common Free Trade Agreement, SAij is a

dummy variable equal to 1 if i and j belong to a common Service Agreement,

Langi,j is a dummy variable equal to 1 if countries i and j share a common

language, Tax is the average corporate tax rate and eij,t is the error term assumed

to be normally distributed with zero mean and variance equal to 1. Based on what

appears in table 9 above, a priori, the coefficients of Y, Trade, MC, Credit and

Lang should be positively signed while P and Tax are expected to be negatively

signed. Dist, FT, CU and SA may be either positively or negatively signed.

A panel of annual data, covering the period 2000-2007 for twelve CARCOM and

eight OECD countries, is used. FDI data were taken from two sources: the

OECD’s data base, which gives FDI inflows and outflows of all OECD countries

to the rest of the world in millions of US dollars for the period 2000-2007 and

Trinidad & Tobago’s Balance of Payments Annual Report (2008). The OECD

countries represented are France, Germany, Hungary, Luxembourg, Mexico,

Netherlands, the UK and the US while the CARICOM countries are Antigua &

Barbuda, Bahamas, Barbados, Belize, Dominica, Grenada, Haiti, Jamaica, St.

15

Kitts & Nevis, St. Lucia, St. Vincent & the Grenadines and Trinidad & Tobago. A

limitation of the study is that the dataset is incomplete in that FDI inflows and

outflows were only given for the OECD countries and Trinidad & Tobago. The

data for all other CARICOM countries represent FDI outflows from OECD

countries to CARICOM countries only. Notwithstanding this limitation, the

majority of the FDI flows are being captured as the OECD countries used in the

study and Trinidad & Tobago are the main CARICOM investors. Furthermore,

CARICOM equity flows are mainly FDI flows coming largely from the US and

UK (both OECD countries).

Real GDP data are obtained from the World Bank’s World Development

Indicators (WDI) where they are recorded in billions of US dollars (base year

1995). The price level is measured by the consumer price index in each country

and the data obtained from the International Financial Statistics (IFS) database

with 2005 as the base year. Market capitalization data in millions of US dollars

are from Standards and Poor’s Emerging Stock Markets Factbook (2008) and they

cover most of the countries in the study for all the years considered. Private credit

data are from the IFS database and comprise credit provided by banks and non-

bank financial institutions. Data denominated in each country’s national currency

are converted to US dollars using the end of period national currency to US

dollars exchange rate for each year considered. Exchange rate data are also taken

from the IFS database. Nominal GDP data are from the WDI and are denominated

in millions of US dollars. The market capitalization to GDP ratio and the private

credit to GDP ratio for each year of the study are constructed from the data.

16

Data on the gross bilateral trade flows among countries are compiled from two

sources: the Caribbean trade (Carib trade) database and the United Nations

Commodity Trade Statistics (UN Comtrade) database. The Carib trade database

records bilateral trade of Caribbean countries only. The UN Comtrade database is

thus used as a supplement. Information on whether both countries belong to a

common Customs Union, Free Trade Agreement and Service Agreement is

obtained from the World Trade Organization Regional Trade Agreements

database. The database covers all trade agreements up to December 2008 and

covers agreements which are in force but have not been notified, those signed but

not yet in force, those currently being negotiated, and those in the proposal stage.

It also covers all the countries in the study.

Distance is taken to mean the physical distance between the capital cities and data

on this are provided by the Central Intelligence Agency World Fact Book.

Information on whether two countries share a common language was also

obtained from this source. Tax data are obtained from the World Tax Database,

created by the Office of Tax Policy Research at the University of Michigan

Business. The database offers a wide range of tax rates for one hundred and fifty

(150) countries. It however does not cover all the years of the study. The average

corporate tax rate of the target country is used in the model.

Since the bilateral outflows from each of the 20 countries is being modeled, this

model effectively comprises 380 (20x19) panels, which, for a total of 8 years,

involves the use of 3040 observations (380x8).

17

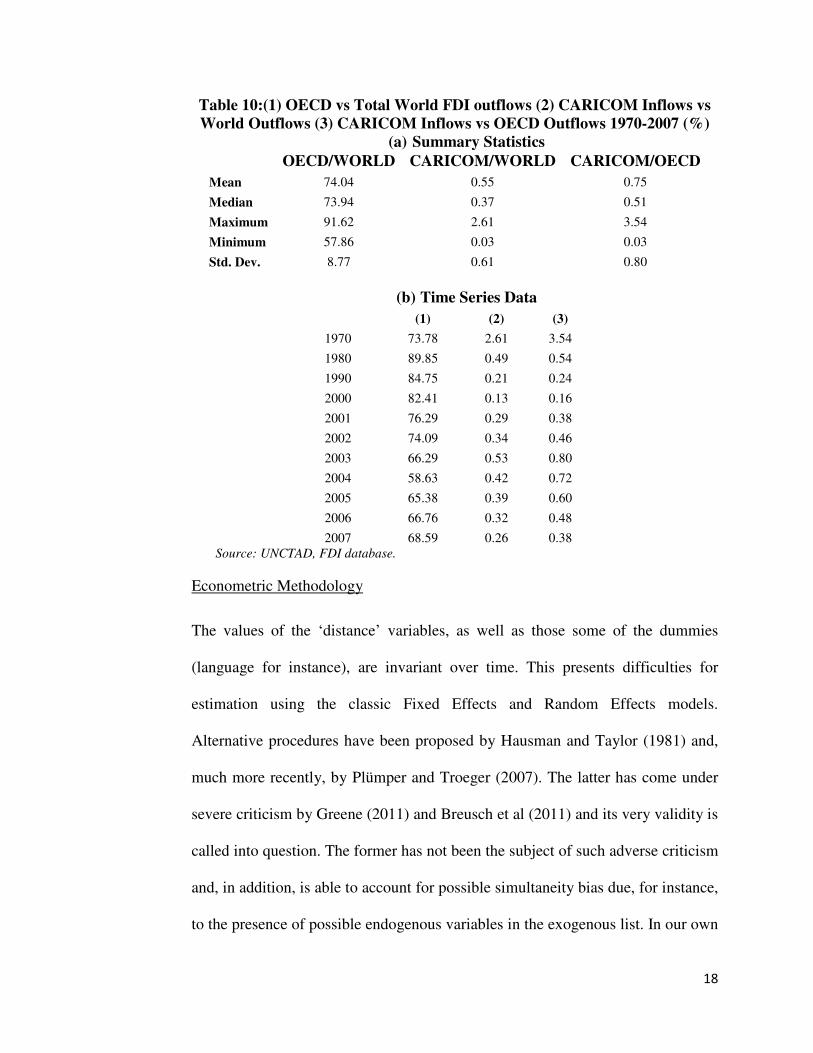

Table 10 (a)-(b) below shows some basic statistical information about the ratio of

OECD to world FDI outflows, of CARICOM FDI inflows to world FDI outflows

and of CARICOM FDI inflows to OECD FDI outflows. FDI outflows from

OECD countries account for a consistently large share of world flows over the

period 1970-2007: on average, they account for 74% of the total over the period,

with a maximum of 92% and a minimum of 58%. CARICOM inflows, on the

other hand, are a miniscule proportion of world outflows with an average of

0.55% over the period 1970-2007, a maximum of 2.61% and a minimum of

0.03%.

18

Table 10:(1) OECD vs Total World FDI outflows (2) CARICOM Inflows vs World Outflows (3) CARICOM Inflows vs OECD Outflows 1970-2007 (%)

(a) Summary Statistics OECD/WORLD CARICOM/WORLD CARICOM/OECD

Mean 74.04 0.55 0.75

Median 73.94 0.37 0.51

Maximum 91.62 2.61 3.54

Minimum 57.86 0.03 0.03

Std. Dev. 8.77 0.61 0.80

(b) Time Series Data

(1) (2) (3)

1970 73.78 2.61 3.54

1980 89.85 0.49 0.54

1990 84.75 0.21 0.24

2000 82.41 0.13 0.16

2001 76.29 0.29 0.38

2002 74.09 0.34 0.46

2003 66.29 0.53 0.80

2004 58.63 0.42 0.72

2005 65.38 0.39 0.60

2006 66.76 0.32 0.48

2007 68.59 0.26 0.38 Source: UNCTAD, FDI database.

Econometric Methodology

The values of the ‘distance’ variables, as well as those some of the dummies

(language for instance), are invariant over time. This presents difficulties for

estimation using the classic Fixed Effects and Random Effects models.

Alternative procedures have been proposed by Hausman and Taylor (1981) and,

much more recently, by Plümper and Troeger (2007). The latter has come under

severe criticism by Greene (2011) and Breusch et al (2011) and its very validity is

called into question. The former has not been the subject of such adverse criticism

and, in addition, is able to account for possible simultaneity bias due, for instance,

to the presence of possible endogenous variables in the exogenous list. In our own

19

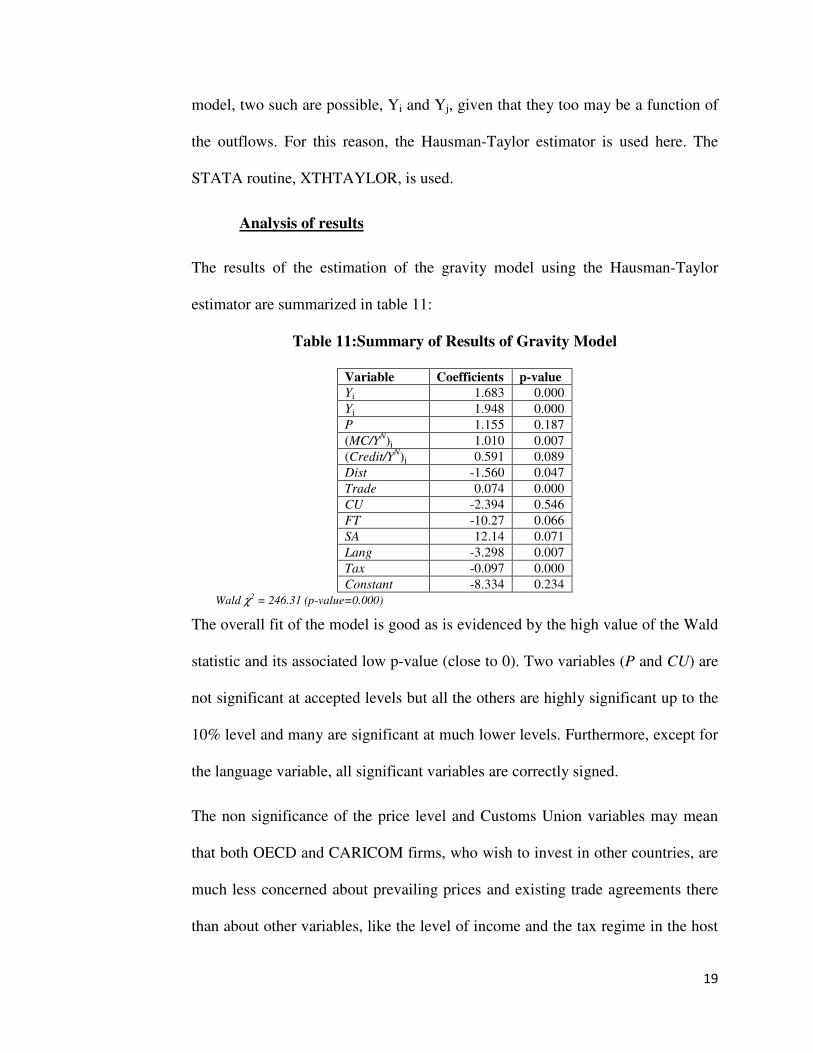

model, two such are possible, Yi and Yj, given that they too may be a function of

the outflows. For this reason, the Hausman-Taylor estimator is used here. The

STATA routine, XTHTAYLOR, is used.

Analysis of results

The results of the estimation of the gravity model using the Hausman-Taylor

estimator are summarized in table 11:

Table 11:Summary of Results of Gravity Model

Variable Coefficients p-value Yi 1.683 0.000

Yj 1.948 0.000

P 1.155 0.187

(MC/YN)j 1.010 0.007

(Credit/YN)j 0.591 0.089

Dist -1.560 0.047

Trade 0.074 0.000

CU -2.394 0.546

FT -10.27 0.066

SA 12.14 0.071

Lang -3.298 0.007

Tax -0.097 0.000

Constant -8.334 0.234 Wald χ2 = 246.31 (p-value=0.000)

The overall fit of the model is good as is evidenced by the high value of the Wald

statistic and its associated low p-value (close to 0). Two variables (P and CU) are

not significant at accepted levels but all the others are highly significant up to the

10% level and many are significant at much lower levels. Furthermore, except for

the language variable, all significant variables are correctly signed.

The non significance of the price level and Customs Union variables may mean

that both OECD and CARICOM firms, who wish to invest in other countries, are

much less concerned about prevailing prices and existing trade agreements there

than about other variables, like the level of income and the tax regime in the host

20

country. Di Giovanni (2005) also found trade agreements were not significant

(and negatively signed).

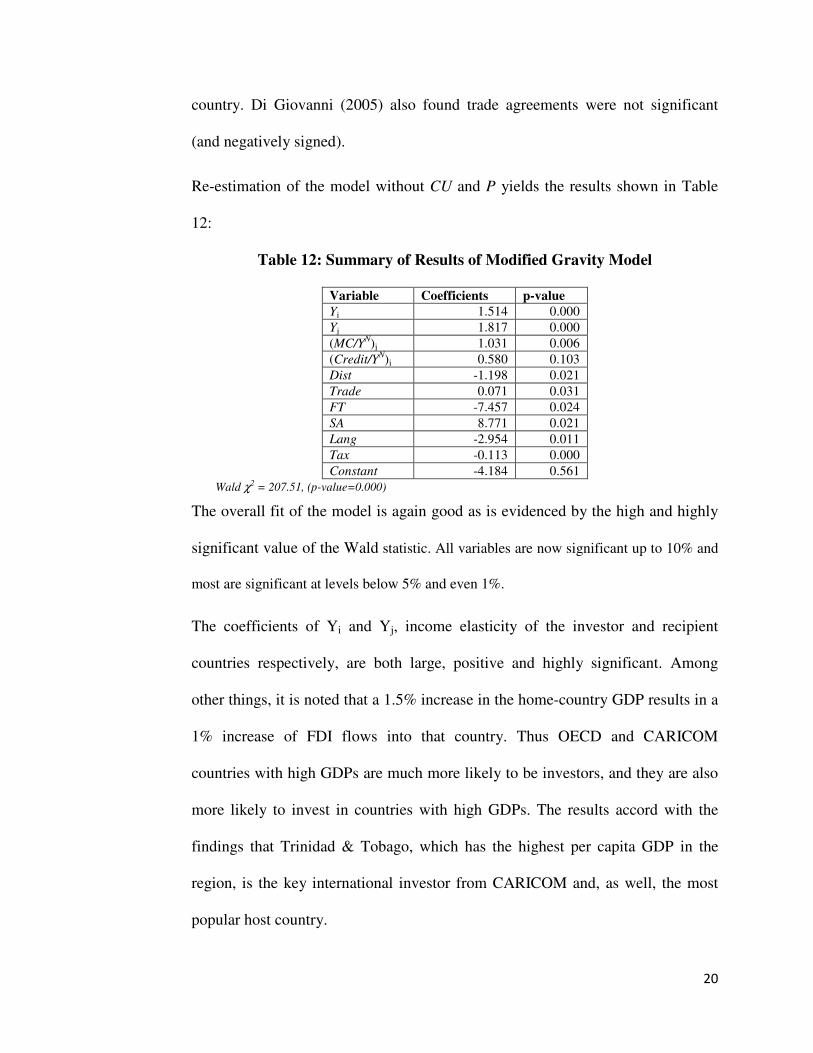

Re-estimation of the model without CU and P yields the results shown in Table

12:

Table 12: Summary of Results of Modified Gravity Model

Variable Coefficients p-value Yi 1.514 0.000

Yj 1.817 0.000

(MC/YN)j 1.031 0.006

(Credit/YN)j 0.580 0.103

Dist -1.198 0.021

Trade 0.071 0.031

FT -7.457 0.024

SA 8.771 0.021

Lang -2.954 0.011

Tax -0.113 0.000

Constant -4.184 0.561 Wald χ2 = 207.51, (p-value=0.000)

The overall fit of the model is again good as is evidenced by the high and highly

significant value of the Wald statistic. All variables are now significant up to 10% and

most are significant at levels below 5% and even 1%.

The coefficients of Yi and Yj, income elasticity of the investor and recipient

countries respectively, are both large, positive and highly significant. Among

other things, it is noted that a 1.5% increase in the home-country GDP results in a

1% increase of FDI flows into that country. Thus OECD and CARICOM

countries with high GDPs are much more likely to be investors, and they are also

more likely to invest in countries with high GDPs. The results accord with the

findings that Trinidad & Tobago, which has the highest per capita GDP in the

region, is the key international investor from CARICOM and, as well, the most

popular host country.

21

Financial variables appear to play an important role in the attraction of FDI flows.

A 1% increase in the market capitalization ratio results in an increase in FDI

inflows by just over 1%. Private credit plays a smaller role: a 1% increase in this

ratio leads to 0.58% increase in FDI inflows. Similar results were obtained by Di

Giovanni (2005) who found that both the market capitalization and private credit

to GDP ratios were highly significant but that the stock market played a greater

role than private credit.

The trade coefficient is positive indicating that foreign firms are willing to invest

in domestic markets not because of increasing tariff costs but because of the ease

in investing in countries with which they are active trading partners. The

existence of Free Trade Agreements appears to have a negative impact on FDI

flows, which may simply be reflecting the fact that there are relatively low flows

between the CARICOM countries (where there is a free trade agreement over the

entire period of the study) and relatively high flows from the OECD to

CARICOM countries (between whom there was no free trade agreement over the

period of the study). On the other hand, a common service agreement positively

impacts FDI flows among the countries in this study, which seems to reflect the

trade between the OECD countries of Europe in particular, where there is a

services agreement. Di Giovanni (2005), who found that trade agreements were

not significant, established that service agreements were significant and positively

signed.

The distance coefficient is negative and highly significant, which is a similar

result obtained by Portes and Rey (2005) and Di Giovanni (2005), where

22

information asymmetries across countries deter FDI flows and the larger apart

two countries are the higher the information cost. The language dummy has a

highly significant negative value, which is contrary to expectations. This may be

reflecting certain peculiarities of the countries that make up the study: whereas

English is not the first language of most of the OECD countries, they are not

deterred by the use of the English language and in fact use in widely in

communication with each other. English is also the official language of all

CARICOM countries in the study, except Haiti. The negative sign may be

reflecting the large movements from countries whose official language is not

English (but for whom that is not a deterrent) to countries where English is widely

practised or to countries whose official language is English.

The tax coefficient is negative and significant but quite low implying that, though

lower taxes attract greater FDI, they are not a major consideration. A 1% increase

in taxes results in a mere 0.113% fall in FDI. This is in line with previous studies,

such as Di Giovanni (2005), where taxes were found not to affect FDI flows

significantly.

Policy and other recommendations

The following appear to be the most obvious policy measures that follow from the

study, on the assumption that the intention is to encourage greater FDI flows into

and within the CARICOM region.

Development of the financial system is to be encouraged as both the extant

literature and the empirical study in this paper verify that this encourages FDI

flows. It is important, in particular, to develop all stock markets in the CARICOM

23

region through the listing of more local companies. Both the literature studied and

the empirical study show that FDI flows increase with increasing market

capitalization. This may require interventions to lower listing fees which would

have the effect of encouraging more listings (and even cross-listings) and,

consequently, more FDI activity in the form of mergers and acquisitions. It may

also require interventions at the level of families who own most of the businesses

that may be listed.

The fact that each domestic stock exchange is at a different level of development

may also pose another hindrance to FDI flows, particularly within the CARICOM

region. It is therefore necessary that all exchanges be brought to the same level of

sophistication. Special efforts must be made to develop the less active exchanges

(Suriname, Haiti, Guyana and Belize), including the introduction of electronic

trading platforms, since it has been shown that FDI activity in the region is

favoured when the exchanges are at a similar level of sophistication. All

exchanges must then work closely together to attract more firms to list and by

extension cross-list.

Listing and cross-listing of stocks may not be the only way to encourage

CARICOM FDI flows. Cross-listing, for instance, takes various forms and

CARICOM firms have to date engaged mainly in ordinary listing whereby a firm

lists its shares for trading on at least two exchanges (its domestic exchange and a

foreign exchange). To increase intra-regional flows, CARICOM countries have to

implement modern trading systems.

24

Governments of the region should aim at a friendlier tax regime since both the

study of the literature and this study show that FDI flows increase in the presence

of lower taxes.

Finally, the Central Banks of the region must take steps to develop procedures for

recording the inflows, by country of origin, and outflows, by country of

destination, of both portfolio and foreign direct investment. This would ensure

empirical testing in the future to better understand these flows.

Conclusion

This study provides evidence about the nature and pattern of CARICOM FDI

flows and provides an explanation for FDI flows between OECD and CARICOM

countries. FDI inflows come mainly from the US and the UK and intra-regional

FDI outflows originate mainly from Trinidad & Tobago followed by the Bahamas

and Jamaica. Trinidad & Tobago is also the key recipient of FDI inflows followed

by the Bahamas and Jamaica.

Growth in GDP will go a long way to improving the levels of cross-border flows.

The financial systems and private credit facilities must be expanded and

oppressive tax regimes avoided. International trade must also be encouraged and

further enhanced though not necessarily through trade agreements.

References

Bissember, E.1997. A Regional Capital Market.Paper presented at the Annual

Monetary Studies Conference, Caribbean Centre for Monetary Studies, October

1997

25

Blonigen, B.A., R.B. Davies. and K. Head. 2003. Estimating the Knowledge-

Capital Model of the Multinational Enterprise. American Economic Review. 93:

980-94.

Brainard, S.L. 1997. An Empirical Assessment of the Proximity-Concentration

Trade-Off Between Multinational Sales and Trade. American Economic Review.

87(4): 520-44.

Breusch, T., M.B.Ward, M. H. Nguyen and T.Kompas.2011. On the Fixed Effects

Vector decomposition. Political Analysis. 19(2): 123-134.

Buch, C. and G. DeLong.2004. Cross-border Bank Mergers: What lures the rare

animal? Journal of Banking & Finance. 28(9): 2077-2102.

Caribbean Trade and Investment Report 2005: Corporate Integration and Cross-

border Development. Caribbean Community (CARICOM) Secretariat. Available

online:

http://www.caricom.org/jsp/community/regional_issues/ctir2005_index.jsp.

Carr, D.L., J.R. Markusen and K.E. Maskus. 2001. Estimating the Knowledge-

Capital model of the Multinational Enterprise. American Economic Review. 91(3):

693-708.

Craigwell, R. 2006. Foreign Direct Investment and Employment in the English

and Dutch-Speaking Caribbean. Project prepared for ILO, Trinidad and Tobago.

Di Giovanni, J. 2005. What Drives Capital Flows? The case of cross-border

merger and acquisition activity and financial deepening.Journal of International

Economics.65: 127-149.

Froot, K.A. and J.C. Stein. 1991 Exchange Rates and Foreign Direct Investment:

An Imperfect Capital Markets Approach, Quarterly Journal of Economics.106:

1191-1217.

26

Grabel,I. 1999. Emerging Stock Markets and Third World development: The

Post-Keynesian Case of Pessimism. Foundations of International Economics.

Greene, W. H. 2011. Fixed Effects Vector Decomposition: A Magical Solution to

the Problem of Time Invariant Variables in Fixed Effects Models?Political

Analysis. 19(2): 135-146.

Grosse, R. and L.J. Trevino.1996. Foreign Direct Investment in the United States:

an Analysis by Country of Origin. Journal of World Business. 39(3): 233-243.

Harrison, P. 2005. Expert Meeting on Capacity Building in the Area of FDI: Data

Compilation and Policy Formulation in Developing Countries. Caribbean

Community, Guyana. http://www.unctad.org/en/docs//c2em18d3_en.pdf

Hausman.J. and W.Taylor. 1981. Panel Data and Unobservable Individual

Effects. Econometrica. 49(6): 1377-1398.

Hijzen, A., H. Gorg and M. Manchin. 2007. Cross-border Mergers and

Acquisitions and the Role of Trade Costs. European Economic Review. 52(5):

849–866.

Markusen, J.R. 2002. Multinational Firms and the Theory of International Trade.

The MIT Press, Cambridge.

Portes, R., R. Rey and Y. Oh. 2001. Information and Capital flows: The

determinants of transactions in financial assets. European Economic Review. 45:

783-796.

Portes, R. and R. Rey. 2005. The Determinants of Cross border Equity Flows.

Journal of International Economics.65: 269- 296.

27

Plümper, T. and V. Troeger. 2007. Efficient Estimation of Time-Invariant and

Rarely Changing Variables in Panel Data Analysis with UnitFixed

Effects.Political Analysis. 15(2): 124-139.

Rambarran, J. and C. Elbourne. 2006. Caribbean Mergers and Acquisitions

Recent Experiences and Lessons. Paper Presented at the Annual Monetary

Studies Conference, Caribbean Centre for Monetary Studies, October 2006.

Russell, P. and G.Khan. 1996 .Mergers and Acquisitions in the Financial Sector:

some issues and lessons for the Caribbean. Paper Presented at the Annual

Monetary Studies Conference, Caribbean Centre for Monetary Studies, October

1996.

Tesar, L.L. and I.M. Werner.1994. International Equity Transactions and U.S.

Portfolio Choice. Working paper 4611.National Bureau of Economic Research.

UNCTAD. 2009. World Investment Report, 2002-2009.

http://www.unctad.org/Templates/Page.asp?intItemID=1465

World Bank. 2010. World Development Indicators. The World Bank

Worrell, D. and J. Jhinkoo. 2008.The Extent of Financial Integration within

CARICOM. Paper Presented at the Annual Monetary Studies Conference,

Caribbean Centre for Money and Finance, November 2008.