Embed Size (px)

Citation preview

CARD FRAUD MANAGEMENT SYSTEMS

Technology Analysis Abstract*

November 2012

CEB TOWERGROUP

RETAIL BANKING & CARDS PRACTICE

Vendor Assessment & Quantitative Teams

* For full copies please contact Peter Johnson at CEB TowerGroup

Brian Riley Senior Research Director, Retail Banking & Cards Practice

1

2 © 2012 The Corporate Executive Board Company. All Rights Reserved.

Retail Banking and Cards Practice

Executive Director

Aaron Kissel

Managing Director

Joanne Pollitt

Senior Research Director

Brian Riley

Quantitative Insight Team

Project Manager

Carolina Valencia

Research Analyst

Ben Fieselmann

Vendor Assessment Team

Project Manager

Magda Rolfes

Research Analyst

Helen McCann

COPIES AND COPYRIGHT

As always, members are welcome to an unlimited number of

copies of the materials contained within this handout.

Furthermore, members may copy any graphic herein for their own

internal purpose. The Corporate Executive Board Company

requests only that members retain the copyright mark on all pages

produced. Please contact your Member Support Center at

+1-866-913-6450 for any help we may provide.

The pages herein are the property of The Corporate Executive

Board Company. Beyond the membership, no copyrighted

materials of The Corporate Executive Board may be reproduced

without prior approval.

LEGAL CAVEAT

CEB TowerGroup has worked to ensure the accuracy of the

information it provides to its members. This report relies upon data

obtained from many sources, however, and CEB TowerGroup cannot

guarantee the accuracy of the information or its analysis in all cases.

Furthermore, CEB TowerGroup is not engaged in rendering legal,

accounting, or other professional services. Its reports should not be

construed as professional advice on any particular set of facts or

circumstances. Members requiring such services are advised to

consult an appropriate professional. Neither The Corporate Executive

Board Company nor its programs are responsible for any claims or

losses that may arise from a) any errors or omissions in their reports,

whether caused by CEB TowerGroup or its sources, or b) reliance

upon any recommendation made by CEB TowerGroup.

3 © 2012 The Corporate Executive Board Company. All Rights Reserved.

ANALYSIS SCOPE & METHODOLOGY

In response to feedback from our membership, CEB TowerGroup and Corporate Executive Board developed this technology analysis product

to identify key components of a technology investment decision and effectively compare vendor technology products. Our methodology comes

from the knowledge that investment decisions center around the benefit to the individual and enterprise of a technology rather than the

feature set alone.

This analysis is tailored to reflect the needs of the end user, in this case the card fraud management system user, to diagnose the technology

attributes particular to a firm, and to effectively identify vendor products that align with the firm’s needs. To that end, CEB TowerGroup

conducted a series of interviews and surveys with financial services executives, industry experts, and vendors regarding card fraud

management technology. The results of this research formed the basis of our anatomy and informed the proprietary five point rating system

on which we scored individual products.

CURRENT MARKET & FUTURE INVESTMENT

Rising consumer confidence swells payments volumes and increases demand on fraud management systems. US Consumer Sentiment

rose to 68.7 in 2012, the highest it’s been since 2008. As customers’ confidence in economic spending conditions has increased, payment

volumes in the top four credit and charge card companies have also increased by up to 16% from 2009 to 2011. This growth is putting new

strains on card fraud management systems, forcing executives to reconsider their fraud management strategies.

New innovations in card usage are accompanied by new risks. The number of card not present transactions, stimulated by the increase in

mobile and internet banking transactions, will have increased tenfold between 2009 and 2013. Thirty-four percent of fraud-related losses are

already attributed to card not present, making this the leading type of global fraud loss. As this type of fraud increases, issuers will continue

to invest in fraud mitigation tools to shield against new risks.

Investment in fraud management expected to increase most in developing markets. IT Spend for card products in established markets will

remain relatively flat through 2016, but spending is expected to increase by a CAGR of more than 7% in Asia and Latin America. Meanwhile,

emerging technologies in the realms of product improvement, performance optimization and operational enhancement are expected to effect

a major shift in the industry’s methods of fraud management.

EXECUTIVE SUMMARY

4 © 2012 The Corporate Executive Board Company. All Rights Reserved.

VENDOR LANDSCAPE & PRODUCT RANKINGS

CEB TowerGroup identified vendors for this analysis based on expert opinion, product maturity, size of installations and technological innovation.

This technology analysis includes ACI Worldwide, Alaric, BPC Technologies, FICO, NICE Actimize, Retail Decisions, SAS, and Tieto Corporation.

Please note that this analysis compares software platforms only. CEB TowerGroup included profiles of selected Service Models to illustrate how

operational enhancements can add depth to platform offerings and recognize that not all FSIs are inclined to manage their software requirements.

By combining our qualitative and quantitative data from interviews and surveys of industry experts, financial institutions, and vendors, CEB

TowerGroup identified 22 attributes that define a “best-in-class” card fraud management technology. These attributes are grouped into four

categories that highlight a firm’s user, customer, and enterprise needs. Product rankings are based on our proprietary five point rating scale for

each of the 22 “best-in-class” attributes. The top vendors were designated as best-in-class performers based on their composite scores in each of

the technology categories below.

BEST-IN-CLASS TECHNOLOGY CATEGORIES

Financial services executives investing in Card Fraud Management technology should use the Card Fraud Management Systems Diagnostic Anatomy on

page 21 to select the vendor that best aligns with their firm’s needs and business objectives.

• FRAUD ANALYTIC TOOLS includes those attributes that provide metrics to card issuers that enable fraud detection, offer insight into risk, and help

shield against loss to the FSI.

Leaders are ACI Worldwide, FICO, and SAS (in alphabetical order)

• ENTERPRISE OPERATIONS includes those attributes that affect the comprehensive handling of an account and overall customer exposure across

other retail banking products.

Leaders are ACI Worldwide, FICO, and NICE Actimize (in alphabetical order)

• WORKFLOW MANAGEMENT includes those attributes that help card issuers effectively process work by streamlining account and transaction

flows, deploying operational strategies, and bringing accounts to a final disposition.

Leaders are ACI Worldwide, FICO, and NICE Actimize (in alphabetical order)

• ENTERPRISE SUPPORT includes those attributes that influence the enterprise’s tactical fit and strategic alignment with the vendor.

Leaders are ACI Worldwide, FICO, and SAS (in alphabetical order)

EXECUTIVE SUMMARY

Source: CEB TowerGroup Research

Mission Statement: CEB

TowerGroup technology

analysis process provides a

customer-driven,

transparent, and unbiased

review designed to drive

informed business decisions.

Current Market: Provides a view

of industry and customer changes,

and best practices for technology

investment and implementation.

Future Investment: Forecasts IT

spending and identifies emerging

technologies and innovations.

Vendor Landscape: Provides an

overview of key vendors, product

features, and market position.

Product Rankings: Highlights

best-in-class attributes and shows

a comparative perspective of

leading products.

Technology Analysis Presentation Roadmap

Current Market

Future Investment

Vendor Landscape

Product Ranking

Market Drivers:

Assess changes in the

industry and customer

behavior

Spending Forecasts:

Benchmark global Card

Fraud Management IT

spending in key

technology areas

List of Players: Identify

key technology firms

and their products

“Best-in-Class” Products:

See the top products

based on our anatomy

categories

Case Study:

Learn how a leading

bank implemented a

new Card Fraud

Management system to

transfer to a single

platform

Emerging Technology

Landscape:

Pinpoint emerging

technologies and

innovations

Diagnostic Anatomy:

Choose your investment

priorities with our

proprietary framework

Ranking Methodology:

Review the key

components of an

investment decision

Feature Audit:

Compare the relative

feature offerings by

vendors

Vendor Profiles:

Understand the key

differentiators between

products

TECHNOLOGY ANALYSIS OVERVIEW

5 © 2012 The Corporate Executive Board Company. All Rights Reserved.

6 © 2012 The Corporate Executive Board Company. All Rights Reserved.

Current Market Future

Investment

Vendor

Landscape Product Rankings

EVEN IN A RECESSION, THE CARD BUSINESS STILL GROWS

Although consumer

confidence hit a low point in

2011, customers are growing

more confident, so US

payment volumes are

increasing.

Customer sentiment was at its

all-time low at the end of 2011

with 40.9 US Customer

Sentiment, but customers

bounced back in 2012 raising

the US Consumer Sentiment to

68.7, the highest it’s been since

2008.

As customers’ confidence in

economic spending conditions

has increased, payment volumes

in the top four credit and

charge card companies also

increased by up to 16% (Visa)

from 2009 to 2011.

7 © 2012 The Corporate Executive Board Company. All Rights Reserved.

Source: US Consumer Sentiment Index Conference

Board, Payments Source

US Consumer Sentiment Index

Indexed at Year 1985=100, 2000 – 2012

95.2

40.9

68.7

20

40

60

80

100

120

140

Q1 2

000

Q1 2

001

Q1 2

002

Q1 2

003

Q1 2

004

Q1 2

005

Q1 2

006

Q1 2

007

Q1 2

008

Q1 2

009

Q1 2

010

Q1 2

011

Q1 2

012

$1,934 $1,752 $1,860

$2,039

2008 2009 2010 2011

Discover* American Express

MasterCard Visa

US Annual Credit and Charge Card Payment Volumes

In US$ Billions, 2008-2011

1.2

3

5.6

9.4

14

2009 2010 2011 2012P 2013P

8 © 2012 The Corporate Executive Board Company. All Rights Reserved.

NEW ENTRY POINTS BRING ADDITIONAL RISKS

As issuers empower users

with innovative ways to use

their cards, new risks emerge

in the card fraud industry.

In 2011, fraud rates hit .87%

when a card was not present,

and were only .05% when the

card was present. As card not

present fraud increases, issuers

will continue to invest in fraud

mitigation tools to shield against

new risks.

As more people use the internet

for online banking, online

transactions are expected to

increase by a multiple of 1.5 by

2013.

Similarly, the number of mobile

banking transactions in 2013

will skyrocket to over 10 times

the number of mobile

transactions in 2009.

23.3

26.8 30

33.3 35

2009 2010 2011 2012P 2013P

US Online Banking Channel Growth

Billions of Transactions, 2009-2013P

US Mobile Banking Channel Growth

Billions of Transactions, 2009-2013P

1.5X 10.7X

Source: CEB TowerGroup

Card Present vs. Card Not Present Fraud Rates

Percentage of Transactions, 2006-2011

1.10%

1.30%

1.10%

0.90% 0.88% 0.87%

0.09% 0.08% 0.08% 0.06% 0.05% 0.05%

2006 2007 2008 2009 2010 2011

Card Not Present Card Present

=0.82%

22%

Lost &

Stolen

9 © 2012 The Corporate Executive Board Company. All Rights Reserved.

CARD FRAUD EVOLVES THROUGH MULTIPLE CHANNELS

Financial institutions

experienced multiple types

of fraud within the past year,

and card not present causes

fraud rates to skyrocket.

Thirty-four percent of losses are

now attributed to card not

present due to the increase in

mobile and internet banking

transactions. This has made card

not present the leading type of

global fraud loss.

As mobile payments continue to

develop, almost 92% of

financial institutions anticipate a

change in their fraud strategies.

Q: As mobile payments start to develop, do you

anticipate a change in your fraud strategies?

Percentage of Respondents, 2012

Source: CEB TowerGroup, CEB TowerGroup

Fraud User Survey 2012

31%

Counterfeit

Global Fraud Losses by Type

Percentage of Respondents, 2011

13%

Other

34%

Card Not

Present

91.7%

Yes

8.3%

No

10 © 2012 The Corporate Executive Board Company. All Rights Reserved.

INVESTMENT IN FRAUD SYSTEMS DECREASES LOSSES

As the majority of firms only

have somewhat effective

fraud controls, firms are

looking to enhance their

fraud systems.

Sixty-six percent of firms say

that their anti- fraud security

controls are somewhat effective,

only 10% say they are

effective, and 18% think they

have ineffective fraud controls.

When asked to define the

changes made at their firm that

contributed to a decrease in

losses, 82% of executives said

they enhanced their fraud

monitoring system.

Source: 2012 Faces of Fraud Survey (ISMG), 2012 Payments Fraud Survey Bank of Dallas

82%

73%

64%

46%

46%

Enhanced FraudMonitoring System

Staff Training& Education

Enhanced InternalProcedures

Adopted or IncreasedUse of a Financial

Service

EnhancedAuthentication

Methods

Changes Made Contributing to Decrease in Losses

Percentage of Respondents, 2012

66%

Somewhat

Effective

12%

Not Effective

10%

Very Effective/

Effective

6%

Unsure

Current Effectiveness of Card Fraud

Percentage of Respondents, 2012

Challenges Technology Enhancement Operational Impact

• Disjointed homegrown debit

card fraud management

technology inhibits full view of

customer transactions across the

enterprise.

• New debit card fraud

management technology easily

integrates with other platforms,

allowing fraud managers to

view all customer transactions

across the enterprise.

Greater customer visibility equips

fraud managers with the necessary

perspective to better anticipate and

identify fraud.

• Three discrete fraud

management systems exist for

credit card, debit card, and

nonmonetary transactions,

preventing cross-system

improvement

• Consolidated fraud management

systems enable systems to learn

from each other, facilitating

mutual cross-system

improvement.

Integrated fraud management

capabilities eliminate redundancies

and increase sophistication of fraud

identification processes.

• IT intervention is required for all

rule additions and modifications,

slowing bank’s response to the

ever-changing landscape of

fraud.

• New fraud management system

pushes operational controls to

fraud managers, eliminating

delays and permitting real-time

new rule implementation.

Improved agility enables fraud

management system to adapt to

changing trends and quickly stifle new

methods of fraud.

11 © 2012 The Corporate Executive Board Company. All Rights Reserved.

Source: CEB TowerGroup, Standard Bank, FICO.

CASE STUDY: TECHNOLOGY EMPOWERS THE FRAUD MANAGER

Standard Bank uses

improved technology and

enhanced training to

transform the role of the

fraud manager.

Standard Bank invests in a new

card fraud management

technology solution to increase

fraud managers’ visibility,

decrease the required degree

of low-skill manual intervention,

and improve the fraud

manager’s ability to react and

adapt to changing patterns in

fraud.

Standard bank is a publicly traded company headquartered in Johannesburg, South Africa. It operates in 18

countries on the African continent and is the largest African bank by assets and earnings. Its three main

pillars of business are Personal & Business Banking, Corporate & Investment Banking, and Wealth & Liberty.

2011 Earnings: $1.9 billion 2011Assets: $185 billion Employees: 52,000

12 © 2012 The Corporate Executive Board Company. All Rights Reserved.

A comprehensive and

standardized training

curriculum equips the fraud

manager to fully optimize

the new technology,

generating quantifiable

operational results.

Improved Fraud

Detection

Source: CEB TowerGroup, Standard Bank, FICO.

Effective implementation

that supports best practice

techniques coupled with

continuous knowledge

transfer from world class

fraud experts enables

Standard Bank to achieve

impressive results.

DEMONSTRATED RESULTS

CASE STUDY: TRAINING ENRICHES OPERATIONAL SKILLS

10%

65%

Old System

New System

Key Results

48% Reduction of Net Fraud

Losses by start of Phase 2

67% reduction in Net Fraud

over 18 months

Reduced fraud transactions per

case by 68%

86% increase in operational

productivity

Training Curriculum

• Core banking system functionality

• Volume sensitivity

• Customer engagement techniques

• Effective Metrics

• Targets and expectations

• Key deliverables of the

environment

Standard Bank collaborates

with a technology vendor to

produce a comprehensive

training curriculum.

Standard Bank and

vendor implemented

a one year skills

transfer session

Rise of highly skilled fraud

managers leads to operational

results.

Current Market Future

Investment

Vendor

Landscape Product Rankings

13

REGIONAL FORECAST OF CARD FRAUD MANAGEMENT SPENDING

IT Spend for card products in

established markets will

remain relatively flat

through 2016.

Regional Spend

(In millions of USD) 2011 E 2012 P 2013 P 2014 P 2015 P 2016 P CAGR

North America $794 $794 $799 $800 $806 $816 0.5%

Europe $444 $453 $460 $463 $465 $466 1.0%

Asia Pacific $379 $416 $455 $491 $528 $564 8.3%

Latin America and the

Caribbean $98 $106 $114 $122 $130 $137 7.0%

Middle East and Africa $31 $33 $34 $35 $36 $36 3.2%

Source: CEB TowerGroup research. Note: E indicates estimated values; P indicates predicted values; CAGR: compound annual growth rate.

Region Definitions

North America USA and Canada

Europe Includes Western,

Central and

Eastern Europe

Asia Pacific Includes Australia

and New Zealand

Latin America

and

Caribbean

Includes Mexico

Middle East

and Africa

Includes Turkey

and all African

and Middle Eastern

countries

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

2011 E 2012 P 2013 P 2014 P 2015 P 2016 P

North America EuropeAsia Pacific

$0

$20

$40

$60

$80

$100

$120

$140

$160

2011 E 2012 P 2013 P 2014 P 2015 P 2016 P

Latin America and the Caribbean Middle East and Africa

Developing regions are

expected to require larger

investments in Card Fraud Risk

Management IT spend,

particularly in Latin America

and the Asia Pacific, as those

markets grow.

14 © 2012 The Corporate Executive Board Company. All Rights Reserved.

Regional Forecast of Card Fraud Management Technology Spending

In Millions USD, 2011(E) – 2015(P)

15 © 2012 The Corporate Executive Board Company. All Rights Reserved.

EMERGING TECHNOLOGY LANDSCAPE IN CARD FRAUD

CEB TowerGroup expects

new capabilities and

functionalities to reflect a

major shift in the industry’s

fraud management.

Technology

State

ROI

Potential

Market-Ready In Pilot

Low

High

Product Improvement

technologies include:

• Customer Alerts

• Real Time Transaction

Control

Performance Optimization

technologies include:

• Channel Specific Coverage

• Integration of External Data

• Biometrics

• Voice Printing

• Device Tracking

Operational Enhancement

technologies include:

• Enterprise Fraud

Management

• Mobile Payment Controls

Enterprise Fraud

Management

Customer Alerts

Real Time Transaction

Control

Integration of

External Data

Channel Specific

Coverage Biometrics

Voice Printing

Device

Tracking

Mobile

Payment

Controls

Definitions

• ROI Potential: Measures the

relative returns an institution can

expect to receive from an

investment in the technology

• Technology State: Measures

the technology’s level of

development

• User Impact: Measures the

level of benefit the technology

will have on the portfolio

management user

Minimal

Moderate

Medium

High

User Impact

16 © 2012 The Corporate Executive Board Company. All Rights Reserved.

LEVERAGING PRODUCT IMPROVEMENT

CEB TowerGroup suggests

that card issuers reconsider

their channel strategies in

order to address the

challenges of authorization,

transaction fraud and

merchant malfeasance. ROI

Potential

Market-Ready In Development

Low

High

Minimal

Moderate

Medium

High

User Impact Product Improvement Matrix

Technology

State

Customer Alerts

Real Time Transaction Control

Key Takeaways from Product Improvement

Definitions

• ROI Potential: Measures the

relative returns an institution can

expect to receive from an

investment in the technology

• Technology State: Measures

the technology’s level of

development

• User Impact: Measures the

level of benefit the technology

will have on the portfolio

management user

• Improvements outside of the US, such as EMV smart chip cards, will have little-to-no impact to the United

States, which has operated with 100% transaction authorizations for the last 30 years.

• Customer alerts, such as real time or near real time SMS messaging and emailing to confirm transactions

provides a low cost risk enhancement.

• Real time transaction controls provide issuers with the ability to react quickly to fraud challenges in

both the physical and virtual world.

17 © 2012 The Corporate Executive Board Company. All Rights Reserved.

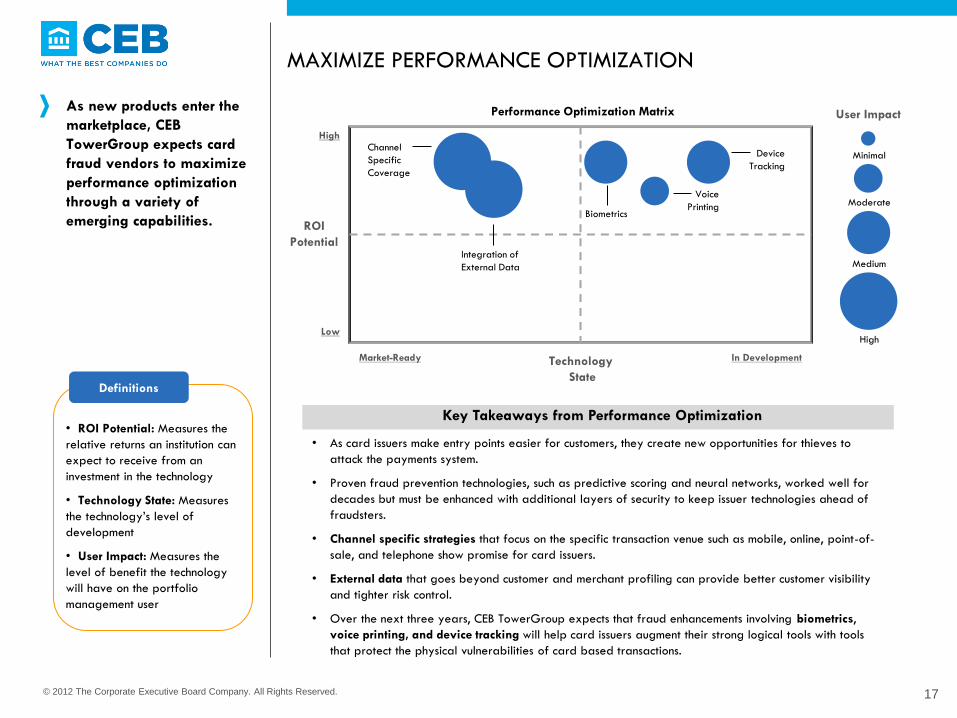

MAXIMIZE PERFORMANCE OPTIMIZATION

As new products enter the

marketplace, CEB

TowerGroup expects card

fraud vendors to maximize

performance optimization

through a variety of

emerging capabilities. ROI

Potential

Market-Ready In Development

Low

High

Minimal

Moderate

Medium

High

User Impact Performance Optimization Matrix

Technology

State

Channel

Specific

Coverage

Integration of

External Data

Key Takeaways from Performance Optimization

Biometrics

Device

Tracking

Voice

Printing

Definitions

• ROI Potential: Measures the

relative returns an institution can

expect to receive from an

investment in the technology

• Technology State: Measures

the technology’s level of

development

• User Impact: Measures the

level of benefit the technology

will have on the portfolio

management user

• As card issuers make entry points easier for customers, they create new opportunities for thieves to

attack the payments system.

• Proven fraud prevention technologies, such as predictive scoring and neural networks, worked well for

decades but must be enhanced with additional layers of security to keep issuer technologies ahead of

fraudsters.

• Channel specific strategies that focus on the specific transaction venue such as mobile, online, point-of-

sale, and telephone show promise for card issuers.

• External data that goes beyond customer and merchant profiling can provide better customer visibility

and tighter risk control.

• Over the next three years, CEB TowerGroup expects that fraud enhancements involving biometrics,

voice printing, and device tracking will help card issuers augment their strong logical tools with tools

that protect the physical vulnerabilities of card based transactions.

18 © 2012 The Corporate Executive Board Company. All Rights Reserved.

FOCUSING ON OPERATIONAL ENHANCEMENT

Card issuers should

anticipate no improvement

from newly mandated EMV

smart cards. Logical controls

remain the strongest

protection layer but they

must be augmented with

stronger physical controls. ROI

Potential

Market-Ready In Development

Low

High

Minimal

Moderate

Medium

High

User Impact Operational Enhancement Matrix

Technology

State

Enterprise Fraud

Management

Key Takeaways from Operational Enhancement

Mobile Payment

Controls

Definitions

• ROI Potential: Measures the

relative returns an institution can

expect to receive from an

investment in the technology

• Technology State: Measures

the technology’s level of

development

• User Impact: Measures the

level of benefit the technology

will have on the portfolio

management user

• Card issuers must continually develop their fraud staff to ensure that high powered software solutions

can address the full features of their capabilities.

• As the card industry deals with saturated markets in high volume countries, cross-selling other financial

service products becomes an essential strategy to protect revenue.

• Cross-selling provides opportunity to maximize customer revenue but brings a higher level of exposure

to issuers, particularly for first party fraud.

• Mobile payments will be adopted slowly in the US, but issuers must prepare for high volume/low value

transactions once they begin to gain traction.

• Card issuers need to consider how the world of payments is evolving, particularly as it affects non-

regulated companies who facilitate transactions and do not typically operate with business disciplines

such as audits, balancing, and financial reserves.

Current

Market

Future

Investment

Vendor

Landscape

Product

Rankings

19

20 © 2012 The Corporate Executive Board Company. All Rights Reserved.

MAPPING THE VENDOR LANDSCAPE

CEB TowerGroup identified vendors for this analysis based on expert opinion, product maturity, size of installations, and vendor stability.

We included 8 large platform

vendors and profiled 3 large

service models. The service

models are not ranked in this

technology analysis because

they enhance platform software

with additional capabilities such

as analytics. Platform Software

ACI Worldwide Proactive Risk

Manager

Alaric Fractals

BPC Technologies

SmartGuard

FICO Falcon Fraud Manager 6

NICE Actimize Actimize Card

Fraud

Retail Decisions ReD PRISM

SAS SAS Fraud

Management

Tieto Corporation

Card Suite Fraud

Management

Service Model

First Data First Data

Fraud Management

FIS FIS Card Fraud Management

TSYS TSYS Fraud

Management

Vendor: Product:

Vendor: Product:

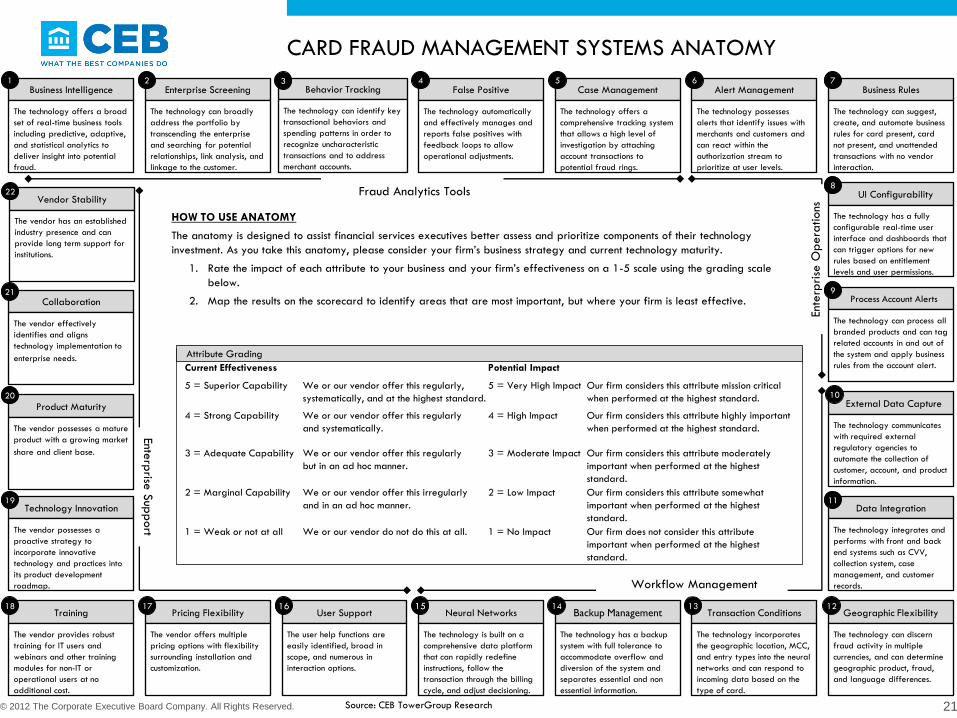

CARD FRAUD MANAGEMENT SYSTEMS ANATOMY

21 © 2012 The Corporate Executive Board Company. All Rights Reserved.

Business Intelligence

The technology offers a broad

set of real-time business tools

including predictive, adaptive,

and statistical analytics to

deliver insight into potential

fraud.

Enterprise Screening

The technology can broadly

address the portfolio by

transcending the enterprise

and searching for potential

relationships, link analysis, and

linkage to the customer.

Behavior Tracking

The technology can identify key

transactional behaviors and

spending patterns in order to

recognize uncharacteristic

transactions and to address

merchant accounts.

False Positive

The technology automatically

and effectively manages and

reports false positives with

feedback loops to allow

operational adjustments.

Case Management

The technology offers a

comprehensive tracking system

that allows a high level of

investigation by attaching

account transactions to

potential fraud rings.

Alert Management

The technology possesses

alerts that identify issues with

merchants and customers and

can react within the

authorization stream to

prioritize at user levels.

Business Rules

The technology can suggest,

create, and automate business

rules for card present, card

not present, and unattended

transactions with no vendor

interaction.

6 5 4 3 2 1

UI Configurability

The technology has a fully

configurable real-time user

interface and dashboards that

can trigger options for new

rules based on entitlement

levels and user permissions.

Process Account Alerts

The technology can process all

branded products and can tag

related accounts in and out of

the system and apply business

rules from the account alert.

External Data Capture

The technology communicates

with required external

regulatory agencies to

automate the collection of

customer, account, and product

information.

Geographic Flexibility

The technology can discern

fraud activity in multiple

currencies, and can determine

geographic product, fraud,

and language differences.

9

10

7

8

Transaction Conditions

The technology incorporates

the geographic location, MCC,

and entry types into the neural

networks and can respond to

incoming data based on the

type of card.

Neural Networks

The technology is built on a

comprehensive data platform

that can rapidly redefine

instructions, follow the

transaction through the billing

cycle, and adjust decisioning.

User Support

The user help functions are

easily identified, broad in

scope, and numerous in

interaction options.

Pricing Flexibility

The vendor offers multiple

pricing options with flexibility

surrounding installation and

customization.

Training

The vendor provides robust

training for IT users and

webinars and other training

modules for non-IT or

operational users at no

additional cost.

13 15 16 17 18 12

Technology Innovation

The vendor possesses a

proactive strategy to

incorporate innovative

technology and practices into

its product development

roadmap.

Product Maturity

The vendor possesses a mature

product with a growing market

share and client base.

Collaboration

The vendor effectively

identifies and aligns

technology implementation to

enterprise needs.

20

19

21

Fraud Analytics Tools

Enterp

rise S

upp

ort

Source: CEB TowerGroup Research

Workflow Management

Ente

rpri

se O

pera

tions

Current Effectiveness Potential Impact

5 = Superior Capability We or our vendor offer this regularly,

systematically, and at the highest standard.

5 = Very High Impact Our firm considers this attribute mission critical

when performed at the highest standard.

4 = Strong Capability We or our vendor offer this regularly

and systematically.

4 = High Impact Our firm considers this attribute highly important

when performed at the highest standard.

3 = Adequate Capability We or our vendor offer this regularly

but in an ad hoc manner.

3 = Moderate Impact Our firm considers this attribute moderately

important when performed at the highest

standard.

2 = Marginal Capability We or our vendor offer this irregularly

and in an ad hoc manner.

2 = Low Impact Our firm considers this attribute somewhat

important when performed at the highest

standard.

1 = Weak or not at all We or our vendor do not do this at all. 1 = No Impact Our firm does not consider this attribute

important when performed at the highest

standard.

Attribute Grading

HOW TO USE ANATOMY

The anatomy is designed to assist financial services executives better assess and prioritize components of their technology

investment. As you take this anatomy, please consider your firm’s business strategy and current technology maturity.

1. Rate the impact of each attribute to your business and your firm’s effectiveness on a 1-5 scale using the grading scale

below.

2. Map the results on the scorecard to identify areas that are most important, but where your firm is least effective.

Data Integration

The technology integrates and

performs with front and back

end systems such as CVV,

collection system, case

management, and customer

records.

11

Vendor Stability

The vendor has an established

industry presence and can

provide long term support for

institutions.

22

Backup Management

The technology has a backup

system with full tolerance to

accommodate overflow and

diversion of the system and

separates essential and non

essential information.

14

DIAGNOSTIC ANATOMY SCORECARD

Score Your Technology

Needs With the Anatomy

Scorecard.

Financial services executives

should complete the scorecard

using the card fraud

management anatomy

diagnostic tool.

Attribute Categories Alignment Attributes Potential Impact Importance of Improvement

1. Business Intelligence

2. Enterprise Screening

Fraud Analytics 3. Behavior Tracking

Tools 4. False Positive

5. Case Management

6. Alert Management

Enterprise 7. Business Rules

Operations 8. UI Configurability

9. Process Account Alerts

10. External Data Capture

11. Data Integration

Workflow 12. Geographic Flexibility

Management 13. Transaction Conditions

14. Backup Management

15. Neural Networks

16. User Support

17. Pricing Flexibility

Enterprise 18. Training

Support 19. Technology Innovation

20. Product Maturity

21. Collaboration

22. Vendor Stability

22 © 2012 The Corporate Executive Board Company. All Rights Reserved.

Source: CEB TowerGroup Research

DIAGNOSTIC ANATOMY SCORECARD

Map Your Technology

Needs:

Financial services executives

should map their attribute scores

from rating their impact and

effectiveness on the Anatomy

Scorecard.

Po

ten

tial Im

pact

5 =Very High

4 =High

3 = Moderate

2 =Low

1 =No Impact

1 =

Weak

2 =

Margin

al

3 =

Adequate

4 =

Strong

5 =

Superio

r

Current Effectiveness

23 © 2012 The Corporate Executive Board Company. All Rights Reserved.

Source: CEB TowerGroup Research

Feature Definition

Account Verification Value The system can integrate Account Verifications Value (AVV) into the authorization process.

Batch Review Capability The system operates in real time but can provide batch functions for offline processing.

Fraud Early Warning The system has a proactive process to mitigate fraud and to reach out to customers.

Input Channels The system can accept input from POS, ATM, branch systems phone, and online channels.

Internal Fraud Control The system has controls in place to mitigate internal fraud.

MasterCard SecureCode Integration The system can integrate with MasterCard SecureCode cards.

Multichannel Protection The system can add layers of protection based on a transaction source.

PCI Compliant The system conforms to all functions in the Payment Card Industry Data Security Standards and is capable of identifying data breeches.

Track I Name Matching The system can match “name on card” for Card Not Present (CNP) transactions.

Transaction Blocking The system can block potential high risk fraud categories.

Transaction Clearing File The system has day-end review of transaction file to ferret fraud trends.

Traveling Customer Accommodation The system can discern traveling customers for out of region activity.

Verified by Visa Integration The system can integrate with Verified by Visa cards.

Visualization Tools The system can create a summary of key business metrics customized to an organization.

Feature Type Definition

Standard Native Feature The feature is standard to the system and is offered as an out-of-box functionality of the base product.

Premium Native Feature The feature is part of an optional module to the solution developed by the vendor, and is offered for an additional fee on top of the base price.

Emerging Feature The feature is emerging and will be offered in the next 12 months.

Developing Feature The feature is in the development stage and will be offered in the next 12-24 months.

FEATURE AUDIT DEFINITIONS

Source: CEB TowerGroup Research

© 2012 The Corporate Executive Board Company. All Rights Reserved.

Platform Software Only

Feature Definition

Coding The system has a proprietary code that only licensees can customize.

m

m

24

FEATURE AUDIT

Features FICO FALCON

FRAUD MANAGER 6

% of Vendors Offering as

Standard Feature

Inte

gra

tion

– P

latf

orm

Soft

ware

Account Verification

Value l 100%

MasterCard SecureCode

Integration l 100%

Input Channels l 100%

Verified by Visa

Integration l 100%

Fra

ud P

rote

ctio

n– P

latf

orm

Soft

ware

Internal Fraud Control l 100%

Multichannel

Protection l 100%

PCI Compliant l 100%

Transaction Blocking l 100%

Fraud Early Warning l 100%

Anci

llary

Capabilitie

s– P

latf

orm

Soft

ware

Batch Review

Capability l 100%

Track I Name

Matching l 100%

Transaction Clearing

File l 88%

Traveling Customer

Accommodation l 88%

Visualization Tools l 75%

Coding l 100%

Feature Type Definition

Standard Native

Feature

The feature is standard to the system and is

offered as an out-of-box functionality of

the base product.

Premium Native

Feature

The feature is part of an optional module

to the solution developed by the vendor,

and is offered for an additional fee on top

of the base price.

Emerging Feature The feature is emerging and will be

offered in the next 12 months.

Developing Feature The feature is in the development stage

and will be offered in the next 12-24

months.

m

m

25

FALCON FRAUD MANAGER 6 FICO

© 2012 The Corporate Executive Board Company.

All Rights Reserved.

Source: CEB TowerGroup Research, FICO

26

Company Overview:

Founded in 1956, the Fair Isaac Corporation (FICO) is a pioneer in the development and application of decision

management solutions, most notably the FICO Score. FICO’s businesses are organized into 4 primary segments: ubiquitous

scoring services, applications for decision management, tools for decision management, and professional services. Seeking

to expand its service offerings, in 2012 FICO launched the FICO Merchant Monitor Solution, which limits merchant-related

risk to banks and acquirers. It also acquired Entiera, a provider of SaaS-based marketing platforms, and Adeptra, a firm

specializing in mobile customer engagement and risk intervention.

Product Overview:

A pioneer among modern fraud solutions, Falcon Fraud Manager was launched in 1992 with proprietary neural network

models for card payments. Today, Falcon Fraud Manager is an end-to-end enterprise fraud detection and case

management solution capable of supporting any electronic payment or account access channel. The current release, Falcon

6, introduced significant analytic innovations that automate the refinement of detection models through machine learning

and feedback mechanisms.

Product Demonstration Highlights:

• Data Consortium: FICO manages a data consortium of 2.5 billion active payment card accounts. The data consortium

enables customers both small and large to benefit from the experiences of their peers and enables FICO to build

effective detection models with a highly controlled false positive rate. The predictive analytic models based on the

consortium data offer the industry’s largest test bed of card production data.

• Implementation Options: Falcon Fraud Manager operates in more than 20 countries for more than 9,000 clients. FICO

offers its platform directly to medium and large card issuers and supports a wide range of service models through

leading card management programs offered by companies such as First Data, FIS, Fiserv, SINSYS and TSYS. When

implementing Falcon Fraud Manager, a company may access FICO’s broad training and consulting resources.

• Data Integration: CEB TowerGroup estimates that FICO platform and service model versions of FICO Falcon help

protect more than 2.5 billion cards around the world, representing 66% of outstanding cards. Integration is standard

with most card systems.

CEB TowerGroup View:

FICO’s long standing and pervasive exposure to card analytic functions makes Falcon well worthy of consideration, though

CEB TowerGroup suggests that both platform and service models benchmark results for champion and challenger

transaction files. As the market leading solution in fraud, FICO constantly enhances its Falcon system through upgrades, like

its innovative adaptive analytics and global profiling techniques. Specifically, Version 6 enhancements include Falcon’s

profiling techniques that utilize global profiles targeting high-risk ATMs, merchants, risky geographic regions, and other

criteria. FICO’s consulting services, coupled with its extensive training options and user support, ensure a smooth transition

to Falcon.

Key Statistics

Company Type: Public

HQ: Minneapolis, MN

Founded: 1956

Employees: 2,079

Revenue: $619.6 million

Client Base: not disclosed

Global

Ov

er

$1

5 B

illio

n

96%

Betw

een

$5

-15

Billio

n

2%

Un

der

$5

Billio

n

2%

Client Siz

e (

by A

ssets

)

Target

Target Market

Platform

Current Market Future

Investment

Vendor

Landscape Product Rankings

27

CREATING OUR “BEST-IN-CLASS” PRODUCT RANKINGS

28 © 2012 The Corporate Executive Board Company. All Rights Reserved.

Categories:

Fraud Analytic Tools

Those attributes that

provide metrics to card

issuers that enable fraud

detection, offer insight

into risk, and help shield

against loss to the FSI.

Enterprise Operations

Those attributes that

affect the comprehensive

handling of an account

and overall customer

exposure across other

retail banking products.

Workflow Management

Those attributes that help

card issuers effectively

process work by

streamlining account and

transaction flows,

deploying operational

strategies, and bringing

accounts to a final

disposition.

Enterprise Support

Those attributes that

influence the enterprise’s

tactical fit and strategic

alignment with the

vendor.

Phase 2

Recognizing that all

attributes are not

equally important, CEB

TowerGroup divides

them into tiers to reflect

their level of

importance as mission

critical, strong priority

or differentiators.

Phase 1

Utilizing qualitative and

quantitative data, CEB

TowerGroup identified

22 attributes that define

a “Best-in-Class” Card

Fraud Management

System, which are

grouped into four

categories.

Phase 3

Certain products are

recognized as “Best-in-

Class” after scoring

each product based on

its performance at an

attribute level.

“Best-in-Class”

Fraud Analytic

Tools

“Best-in-Class”

Enterprise Support

“Best-in-Class”

Workflow

Management

“Best-in-Class”

Enterprise

Operations

Mission

Critical

Enterprise Screening

Behavior Tracking

Business Rules

Process Account Alerts

External Data

Capture

Data Integration

Neural Networks

User Support

Training Requirements

Technology Innovation

Vendor Stability

Strong

Priority

Business Intelligence

False Positive Alert Management

Geographic

Flexibility

Transaction Conditions

Product Maturity

Vendor Collaboration

Product

Differentiator Case Management

User Interface

Configurability Backup Management Pricing Flexibility

Attributes

29 © 2012 The Corporate Executive Board Company. All Rights Reserved.

PRODUCT RANKING MATRIX

Overall, high performing vendors exhibited excellence in multiple categories. Product Leaders are the top scoring products in a given category and are chosen based on the differentiation in scoring a particular category.

Fraud Analytic Tools includes

those attributes that provide

metrics to card issuers that

enable fraud detection, offer

insight into risk and help shield

against loss to the FSI.

Enterprise Operations includes

those attributes that affect the

comprehensive handling of an

account and overall customer

exposure across other retail

banking products.

Workflow Management

includes those attributes that

help card issuers effectively

process work by streamlining

account and transaction flows,

deploying operational

strategies, and bringing

accounts to a final disposition.

Enterprise Support includes

those attributes that influence

the enterprise’s tactical fit and

strategic alignment with the

vendor.

Fraud

Analytic

Tools

Enterprise

Operations

Workflow

Management

Enterprise

Support

Vendor A Product A 4.81 4.82 4.81 4.84

Vendor B Product B 4.24 4.29 4.46 3.84

Vendor C Product C 4.43 4.35 4.42 4.26

FICO

Falcon

Fraud

Manager

4.86 5 4.85 4.84

Vendor D Product D 4.67 4.76 4.81 4.39

Vendor E Product E 4.38 4.29 4.27 4.10

Vendor F Product F 4.86 4.41 4.65 4.68

Vendor G Product G 4.10 3.76 4.08 4.13

Ranking Methodology

Vendor rankings are

based on our

proprietary 5-point

rating system for each

of the 22 attributes in

our card fraud

management systems

anatomy (see page 21).

= Best-in-Class in

Anatomy

Category

30

Vendor B

Vendor A

Vendor A Vendor A

Vendor F

Vendor D

Vendor D

Vendor D

Vendor E Vendor D

FICO FICO FICO FICO

Vendor C

Vendor B

Vendor B

Vendor C

Vendor E

Vendor E

Vendor F

Vendor A

Vendor C Vendor C

Vendor B

Vendor E

0.25

0.50

0.75

1.00

FRAUD

ANALYTIC

TOOLS

ENTERPRISE

OPERATIONS

© 2012 The Corporate Executive Board Company. All Rights Reserved.

Source: CEB TowerGroup Research

WORKFLOW

MANAGEMENT

ENTERPRISE

SUPPORT

“Best-in-

Class”

Products

MAPPING THE VENDOR LANDSCAPE

“Best-in-Class” Product Rankings

Normalized Scores, 0.0-1.0 Scale

CATEGORY SCORING ANALYSIS

Fraud Analytic Tools

Business Intelligence: Runs on flexible rules engine with 3+ consortium data and a fraud

predictor that provides merchant profiling and adaptive analytics with 56 fraud patents.

Behavior Tracking: Includes multiple levels of user-defined profiles which enable clients to

build their own profiles to track behavior at the customer, account, or service level.

False Positive: Integral rules engine can override false positives and learn retrospectively

using tools that analyze false positives and return to refine algorithms.

Enterprise Operations

Alert Management: Automatically sends SMSs and sets up rules so fraud manager can

focus on high risk accounts and can categorize rules into different modes such as manual,

priority, and round robin.

Business Rules: Flexible rules engine holds unlimited data and provides a set of

performance statistics to enable users to develop business strategies.

User Interface Configurability: Customizable user interface provides extensive options for

queues, user and group options, page options, filters, and a variety of others.

Workflow Management

External Data Capture: Automatically communicates with external reporting and regulatory

agencies; includes the ability to call client systems for a customer and to produce account

updates.

Data Integration: Integrates seamlessly with front and back-end systems including over 100

CVV systems, 20 collection systems and over 100 customer records.

Neural Networks: Provides accessibility to FICO fraud consortium data with over 2.4 billion

payment card accounts and the ability to adjust decisioning based on previous outcomes.

Enterprise Support

Training: Includes multiple training options at FICO university including case management

training, expert business rules training, consulting for operational and system integration

training.

Product Maturity: Industry-leading product initiated scoring in the card sector and owns

roughly 60% of the marketplace.

Vendor Collaboration: Offers several customer collaboration outlets to enhance FICO’s

product including customer forums, FICO world, fraud alert networks, business reviews, and

surveys.

31 © 2012 The Corporate Executive Board Company. All Rights Reserved.

“BEST-IN-CLASS” ACHIEVEMENTS FOR FICO

FICO Falcon Fraud Manager 6 received “Best-in-Class” in Fraud Analytic Tools, Enterprise Operations, Workflow Management, and Enterprise Support.

Fraud Analytic Tools include

those attributes that provide

metrics to card issuers that

enable fraud detection, offer

insight into risk, and help shield

against loss to the FSI.

Enterprise Operations include

those attributes that affect the

comprehensive handling of an

account and overall customer

exposure across other retail

banking products.

Workflow Management includes

those attributes that help card

issuers effectively process work

by streamlining account and

transaction flows, deploying

operational strategies, and

bringing accounts to a final

disposition.

Enterprise Support includes

those attributes that influence

the enterprise’s tactical fit and

strategic alignment with the

vendor.

32

Business Intelligence

The technology offers a broad

set of real-time business tools

including predictive, adaptive,

and statistical analytics to

deliver insight into potential

fraud.

© 2012 The Corporate Executive Board Company. All Rights Reserved.

Enterprise Screening

The technology can broadly

address the portfolio by

transcending the enterprise

and searching for potential

relationships, link analysis, and

linkage to the customer.

Behavior Tracking

The technology can identify key

transactional behaviors and

spending patterns in order to

recognize uncharacteristic

transactions and to address

merchant accounts.

False Positive

The technology automatically

and effectively manages and

reports false positives with

feedback loops to allow

operational adjustments.

Case Management

The technology offers a

comprehensive tracking system

that allows a high level of

investigation by attaching

account transactions to

potential fraud rings.

Alert Management

The technology possesses

alerts that identify issues with

merchants and customers and

can react within the

authorization stream to

prioritize at user levels.

Business Rules

The technology can suggest,

create, and automate business

rules for card present, card

not present, and unattended

transactions with no vendor

interaction.

6 5 4 3 2 1

UI Configurability

The technology has a fully

configurable real-time user

interface and dashboards that

can trigger options for new

rules based on entitlement

levels and user permissions.

Process Account Alerts

The technology can process all

branded products and can tag

related accounts in and out of

the system and apply business

rules from the account alert.

External Data Capture

The technology communicates

with required external

regulatory agencies to

automate the collection of

customer, account, and product

information.

The technology can discern

fraud activity in multiple

currencies, and can determine

geographic product, fraud,

and language differences.

Geographic Flexibility

9

10

7

8

Transaction Conditions

The technology incorporates

the geographic location, MCC,

and entry types into the neural

networks and can respond to

incoming data based on the

type of card.

Neural Networks

The technology is built on a

comprehensive data platform

that can rapidly redefine

instructions, follow the

transaction through the billing

cycle, and adjust decisioning.

User Support

The user help functions are

easily identified, broad in

scope, and numerous in

interaction options.

Pricing Flexibility

The vendor offers multiple

pricing options with flexibility

surrounding installation and

customization.

Training

The vendor provides robust

training for IT users and

webinars and other training

modules for non-IT or

operational users at no

additional cost.

13 15 16 17 18 12

Technology Innovation

The vendor possesses a

proactive strategy to

incorporate innovative

technology and practices into

its product development

roadmap.

Product Maturity

The vendor possesses a mature

product with a growing market

share and client base.

Collaboration

The vendor effectively

identifies and aligns

technology implementation to

enterprise needs.

20

19

21

Fraud Analytics Tools

Enterp

rise S

upp

ort

Source: CEB TowerGroup Research

Workflow Management

Ente

rpri

se O

pera

tions

Data Integration

The technology integrates and

performs with front and back

end systems such as CVV,

collection system, case

management, and customer

records.

11

Vendor Stability

The vendor has an established

industry presence and can

provide long term support for

institutions.

22

Backup Management

The technology has a backup

system with full tolerance to

accommodate overflow and

diversion of the system and

separates essential and non

essential information.

14

CARD FRAUD MANAGEMENT SYSTEMS SCORING METHODOLOGY

Scoring Methodology

To arrive at a vendor ranking, CEB TowerGroup developed a proprietary scoring metric outlined by the

attributes within this anatomy that highlights the major elements of an enterprise investment decision. This

metric assumes that every element is not equally important, and therefore assigns a higher level of

importance to those attributes critical to a card fraud management system. The remaining attributes are

then divided further into two tiers to reflect their level of importance, highlighted below.

Tier 1 Attributes – “Mission

Critical” Tier 2 Attributes – “Strong

Priority” Tier 3 Attributes – “Product

Differentiators”

Enterprise Screening

Behavior Tracking

Business Rules

Process Account Alerts

External Data Capture

Data Integration

Neural Networks

User Support

Training

Technology Innovation

Vendor Stability

Business Intelligence

False Positive

Alert Management

Geographic Flexibility

Transaction Conditions

Product Maturity

Collaboration

Case Management

User Interface Configurability

Backup Management

Pricing Flexibility

UNDERSTANDING OUR SCORING METHODOLOGY

CEB TowerGroup developed

a unique and proprietary

scoring methodology that

highlights the key priorities

for an executive’s

investment decision.

Every vendor product featured

in this report is scored against

each of the 22 attributes

outlined in the Card Fraud

Management System Diagnostic

Anatomy on a standardized 1-5

scale.

We calculate the weighted

average of a product’s attribute

scores in each of the four

categories of the anatomy to

arrive at an overall category

score.

Anato

my

Category Fraud Analytic Tools Workflow Management

Attribute Title Enterprise Screening Neural Networks

Attribute

Definition

The technology can broadly address the

portfolio by transcending the enterprise and

searching for potential relationships, link

analysis, and linkage to the customer.

The technology is built on a comprehensive

data platform that can rapidly redefine

instructions, follow the transaction through the

billing cycle, and adjust decisioning.

Sco

ring M

etr

ic

5

The technology can broadly address the portfolio by

transcending the enterprise and searching for potential

relationships, link analysis, and linkage to the customer.

The technology is built on a comprehensive data

platform and can rapidly redefine instructions, follow

the transaction through the billing cycle, and adjust

easily decisioning based on previous outcomes.

4

The technology can transcend the enterprise and can

search for potential relationships but has limited ability

to link to the customer and perform link analysis.

The technology can refine the instructions, follow the

transaction through the billing cycle, but has limited

capabilities in adjusting decisioning based on previous

outcomes.

3 The technology can transcend the enterprise but has

limited searching ability for potential relationships and

cannot link to the customer.

The technology can refine the instructions, follow the

transaction through the billing cycle, but cannot adjust

decisioning based on previous outcomes.

2 The technology can transcend the enterprise but cannot

search for potential relationships.

The technology can refine the instructions, but cannot

follow the transaction through the billing cycle.

1 The technology cannot transcend the enterprise and

cannot link potential relationships to the customer.

The technology does not support a neural network.

Attribute Score: 5.0 3.0

SCORE

Sample Technology Analysis Internal Anatomy Scoring Guide

Illustrative

33 © 2012 The Corporate Executive Board Company. All Rights Reserved.

Source: CEB TowerGroup Research

34