Embed Size (px)

Citation preview

Capturing the Valueof Your Business

Selling a Company is an Important Decision

“Now, if you’ll just sign right here, Mr. Hark,you’ll make the biggest mistake of your life!”

PAT is the Key to Value Enhancement

Presentation

Audience

Timing

Value Enhancement Through

Presentation

Clearly describe the opportunity

Concisely deliver the message

Focus on the most effective topics

Enhance the value of your company

Appeal to quality acquirers Motivate the acquirer to buy

written material

telephone interaction

face-to-face meetings

coordination of all participants

highly skilled, professional advisors well trained in the process

The presentation of your company must:

Superior presentation of your company requires outstanding:

Value Enhancement ThroughEstablishing the Right

Audience

A competitor A customer A vendor A company in your town A company in your industry A company you know very well

Markets Distribution Customers Products Technology

We have found that the best acquirer for your company is seldom any of these:

The best acquirer usually provides a synergistic fit in one or more of these areas:

Operations Strategic direction Management style Financial

resources

The best acquirers for your company can be found through investigative research conducted by experienced professional advisors who are well informed about your company’s operations and who are constantly interacting with large numbers of acquirers.

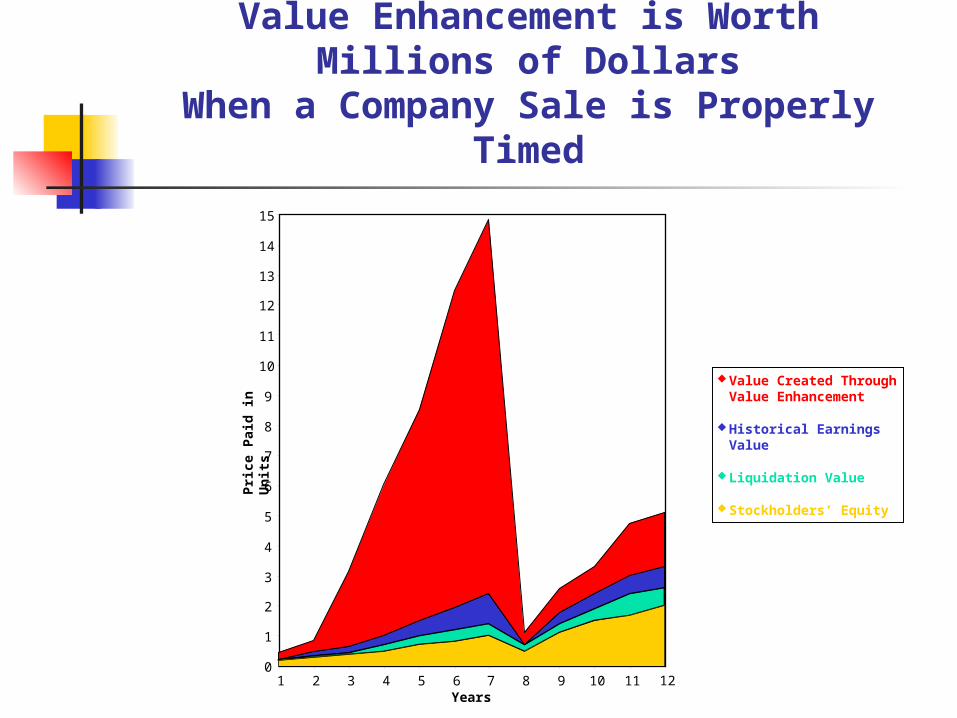

Value Enhancement is WorthMillions of Dollars

When a Company Sale is Properly Timed

0

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

1 2 3 4 5 6 7 8 9 10 11 12

Pri

ce P

aid

in U

nit

s

Years

Value Created ThroughValue Enhancement

Historical Earnings Value

Liquidation Value

Stockholders’ Equity

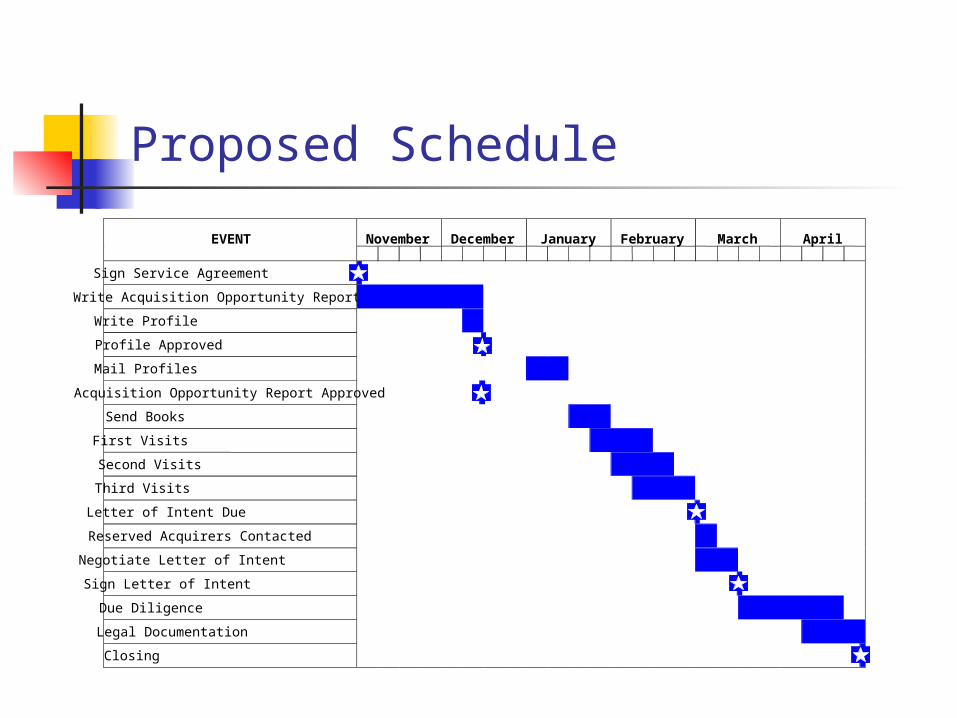

Proposed Schedule

EVENT

November

December

January

February

March

April

Sign Service Agreement

Write Acquisition Opportunity Report

Write Profile

Profile Approved

Mail Profiles

Acquisition Opportunity Report Approved

Send Books

First Visits

Second Visits

Third Visits

Letter of Intent Due

Reserved Acquirers Contacted

Negotiate Letter of Intent

Sign Letter of Intent

Due Diligence

Legal Documentation

Closing

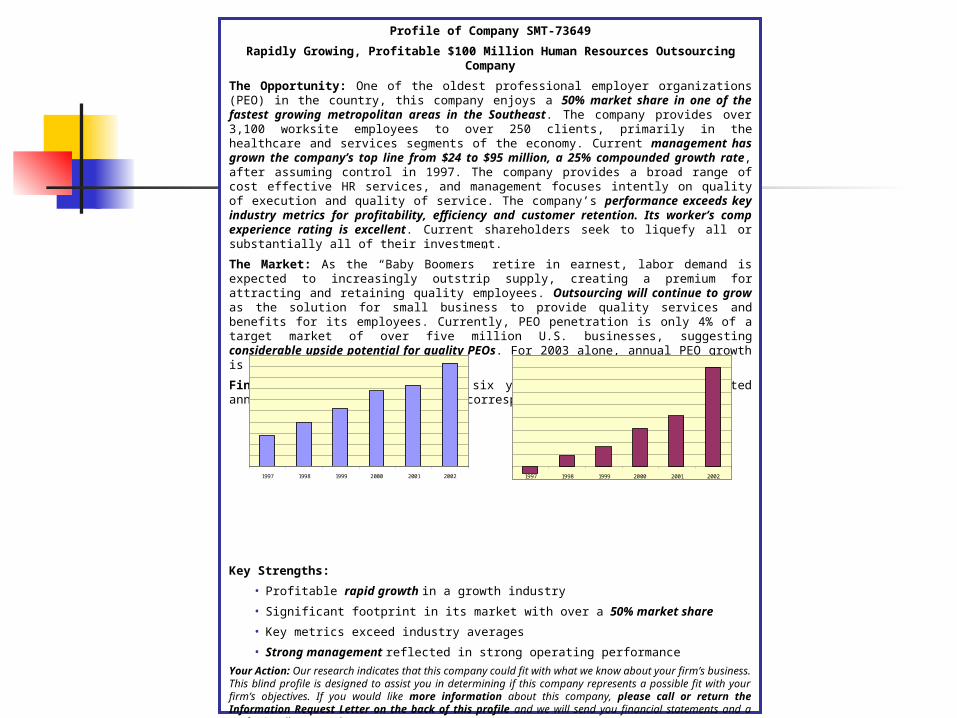

Profile of Company SMT-73649

Rapidly Growing, Profitable $100 Million Human Resources Outsourcing Company

The Opportunity: One of the oldest professional employer organizations (PEO) in the country, this company enjoys a 50% market share in one of the fastest growing metropolitan areas in the Southeast. The company provides over 3,100 worksite employees to over 250 clients, primarily in the healthcare and services segments of the economy. Current management has grown the company’s top line from $24 to $95 million, a 25% compounded growth rate, after assuming control in 1997. The company provides a broad range of cost effective HR services, and management focuses intently on quality of execution and quality of service. The company’s performance exceeds key industry metrics for profitability, efficiency and customer retention. Its worker’s comp experience rating is excellent. Current shareholders seek to liquefy all or substantially all of their investment.

The Market: As the “Baby Boomers” retire in earnest, labor demand is expected to increasingly outstrip supply, creating a premium for attracting and retaining quality employees. Outsourcing will continue to grow as the solution for small business to provide quality services and benefits for its employees. Currently, PEO penetration is only 4% of a target market of over five million U.S. businesses, suggesting considerable upside potential for quality PEOs. For 2003 alone, annual PEO growth is projected to be 25%.

Financial Summary: In the past six years, the company has generated annual revenue growth of 25% and corresponding EBITDA growth of 75%.

Gross Billings EBITDA

Key Strengths:

• Profitable rapid growth in a growth industry

• Significant footprint in its market with over a 50% market share

• Key metrics exceed industry averages

• Strong management reflected in strong operating performance

Your Action: Our research indicates that this company could fit with what we know about your firm’s business. This blind profile is designed to assist you in determining if this company represents a possible fit with your firm’s objectives. If you would like more information about this company, please call or return the Information Request Letter on the back of this profile and we will send you financial statements and a professionally prepared summary.

Note: We are solely compensated by the seller. We are a performance organization with over 25 years of experience closing transactions in a wide variety of industries.

Contact: Tim McMillin or Brad Buttermore 214-638-8280 Profile No. SMT-73649

1997 1998 1999 2000 2001 2002 1997 1998 1999 2000 2001 2002

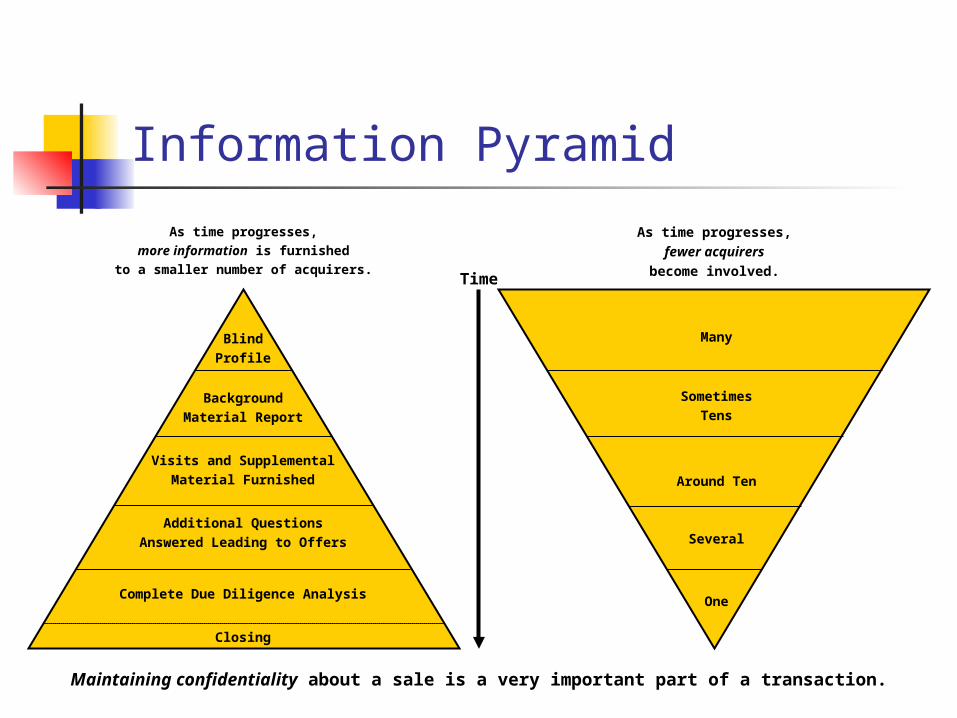

Information Pyramid

As time progresses,

more information is furnished

to a smaller number of acquirers.

As time progresses,

fewer acquirers

become involved.Time

Blind

Profile

Background

Material Report

Visits and Supplemental

Material Furnished

Additional Questions

Answered Leading to Offers

Complete Due Diligence Analysis

Closing

Many

Sometimes

Tens

Around Ten

Several

One

Maintaining confidentiality about a sale is a very important part of a transaction.

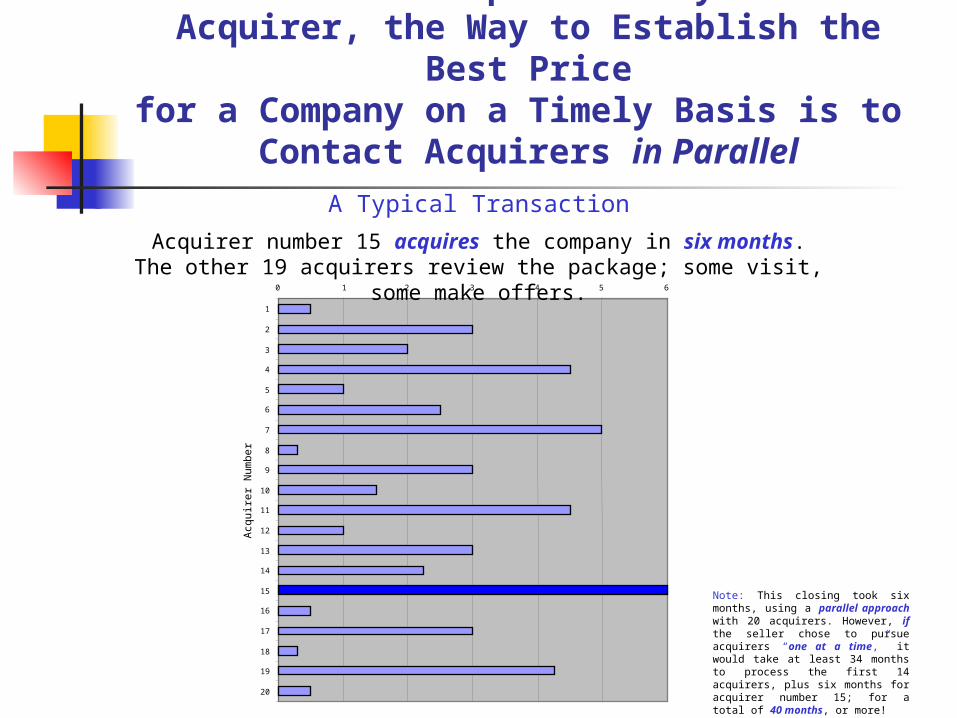

Since Price Perceptions Vary With Each Acquirer, the Way to Establish the Best Price

for a Company on a Timely Basis is to Contact Acquirers in Parallel

0 1 2 3 4 5 6

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

A Typical Transaction

Acquirer number 15 acquires the company in six months.The other 19 acquirers review the package; some visit, some make offers.

Note: This closing took six months, using a parallel approach with 20 acquirers. However, if the seller chose to pursue acquirers “one at a time,” it would take at least 34 months to process the first 14 acquirers, plus six months for acquirer number 15; for a total of 40 months, or more!

Acq

uire

r N

umbe

r

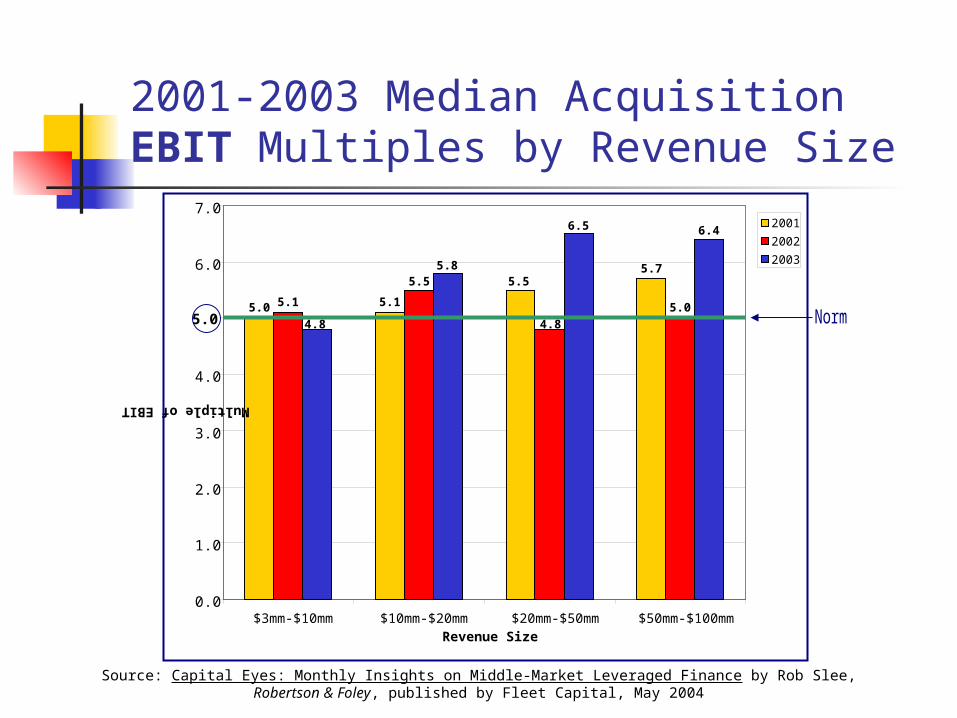

2001-2003 Median Acquisition EBIT Multiples by Revenue Size

5.1

5.7

5.1 5.05.0

5.55.5

4.8

6.5 6.4

5.8

4.8

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

$3mm-$10mm $10mm-$20mm $20mm-$50mm $50mm-$100mmRevenue Size

Multiple of EBIT

2001

2002

2003

Source: Capital Eyes: Monthly Insights on Middle-Market Leveraged Finance by Rob Slee,Robertson & Foley, published by Fleet Capital, May 2004

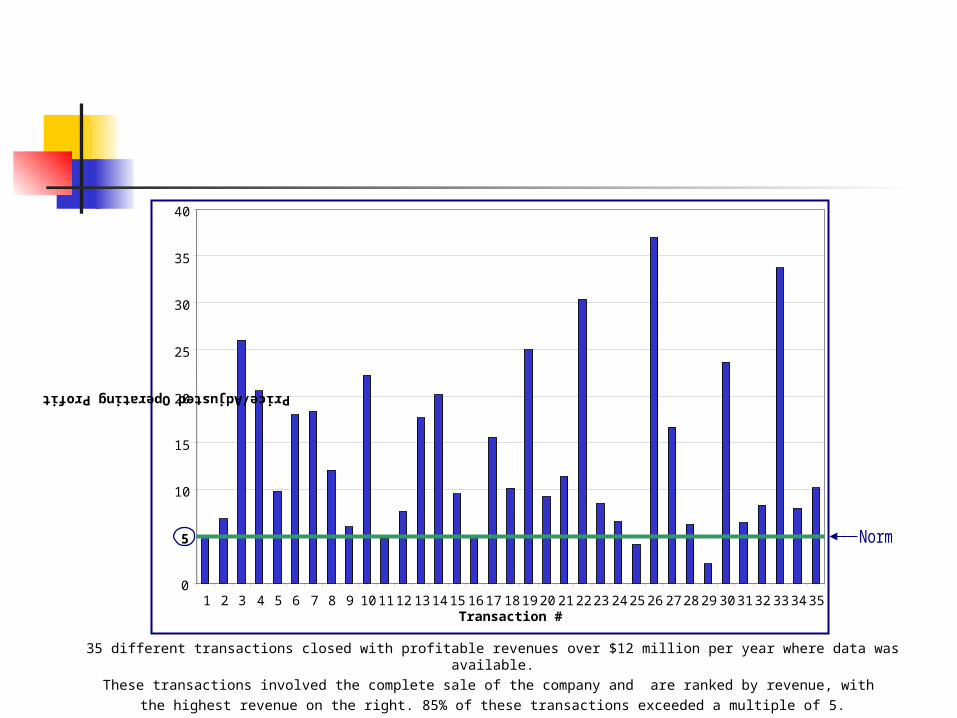

35 different transactions closed with profitable revenues over $12 million per year where data was available.

These transactions involved the complete sale of the company and are ranked by revenue, with

the highest revenue on the right. 85% of these transactions exceeded a multiple of 5.

0

5

10

15

20

25

30

35

40

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35

Price/Adjusted Operating Profit

Transaction #

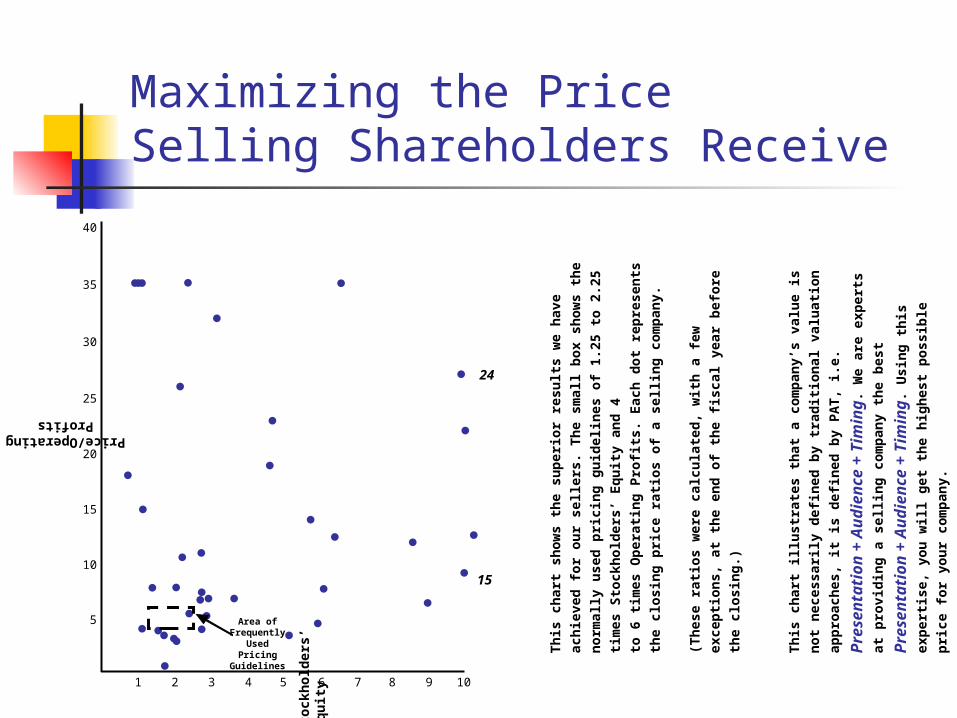

Maximizing the Price Selling Shareholders Receive

Area of Frequently

Used Pricing Guidelines

40

30

35

25

20

15

10

5

1 2 3 4 5 6 7 8 9 10

24

15

Price/Operating Profits

Th

is c

har

t sh

ow

s th

e su

per

ior

resu

lts

we

hav

e ac

hie

ved

fo

r

ou

r se

llers

. Th

e sm

all b

ox

sho

ws

the

no

rmal

ly u

sed

pri

cin

g

gu

idel

ines

of

1.25

to

2.2

5 ti

mes

Sto

ckh

old

ers’

Eq

uit

y an

d 4

to 6

tim

es O

per

atin

g P

rofi

ts. E

ach

do

t re

pre

sen

ts t

he

clo

sin

g

pri

ce r

atio

s o

f a

selli

ng

co

mp

any.

(Th

ese

rati

os

wer

e ca

lcu

late

d, w

ith

a f

ew e

xcep

tio

ns,

at

the

end

of

the

fisc

al y

ear

bef

ore

th

e cl

osi

ng

.)

Th

is c

har

t ill

ust

rate

s th

at a

co

mp

any’

s va

lue

is n

ot

nec

essa

rily

def

ined

by

trad

itio

nal

val

uat

ion

ap

pro

ach

es, i

t is

def

ined

by

PA

T, i

.e. P

res

en

tati

on

+ A

ud

ien

ce

+ T

imin

g. W

e ar

e

exp

erts

at

pro

vid

ing

a s

ellin

g c

om

pan

y th

e b

est

Pre

se

nta

tio

n +

Au

die

nc

e +

Tim

ing

. Usi

ng

th

is e

xper

tise

,

you

will

get

th

e h

igh

est

po

ssib

le p

rice

fo

r yo

ur

com

pan

y.

Pri

ce/S

tock

ho

lder

s’ E

qu

ity

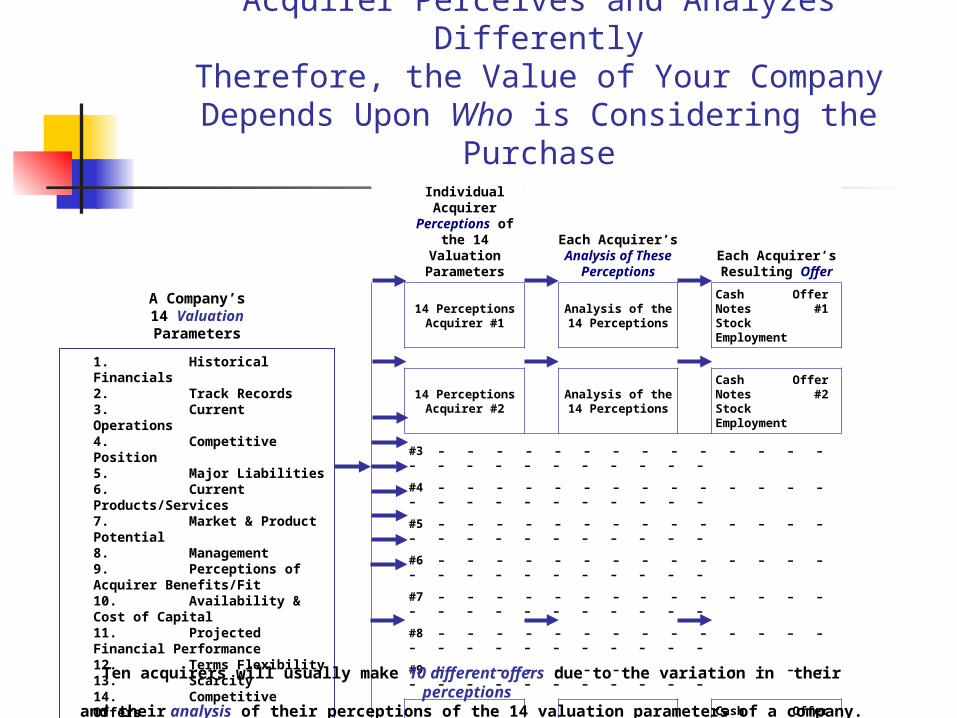

Offers Vary Because EachAcquirer Perceives and Analyzes Differently

Therefore, the Value of Your CompanyDepends Upon Who is Considering the Purchase

Individual Acquirer

Perceptions of the 14

Valuation Parameters

Each Acquirer’s Analysis of

These Perceptions

Each Acquirer’sResulting Offer

14 PerceptionsAcquirer #1

Analysis of the14 Perceptions

Cash OfferNotes #1StockEmployment

14 PerceptionsAcquirer #2

Analysis of the14 Perceptions

Cash OfferNotes #2StockEmployment

#3 – – – – – – – – – – – – – – – – – – – – – – – – –

#4 – – – – – – – – – – – – – – – – – – – – – – – – –

#5 – – – – – – – – – – – – – – – – – – – – – – – – –

#6 – – – – – – – – – – – – – – – – – – – – – – – – –

#7 – – – – – – – – – – – – – – – – – – – – – – – – –

#8 – – – – – – – – – – – – – – – – – – – – – – – – –

#9 – – – – – – – – – – – – – – – – – – – – – – – – –

14 PerceptionsAcquirer #10

Analysis of the14 Perceptions

Cash OfferNotes #10StockEmployment

1.Historical Financials2.Track Records3.Current Operations4.Competitive Position5.Major Liabilities6.Current Products/Services7.Market & Product Potential8.Management9.Perceptions of Acquirer Benefits/Fit10. Availability & Cost of Capital11. Projected Financial Performance12. Terms Flexibility13. Scarcity14. Competitive Offers

A Company’s14 ValuationParameters

Ten acquirers will usually make 10 different offers due to the variation in their perceptions and their analysis of their perceptions of the 14 valuation parameters of a company.

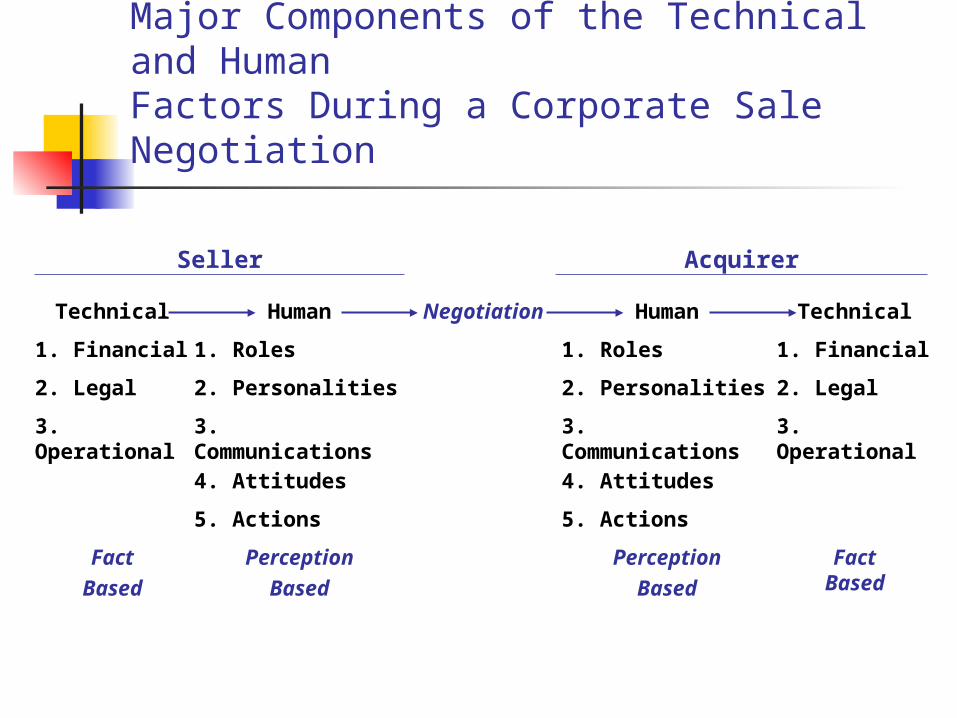

Major Components of the Technical and HumanFactors During a Corporate Sale Negotiation

Technical Human Negotiation Human Technical

1. Financial 1. Roles 1. Roles 1. Financial

2. Legal 2. Personalities 2. Personalities 2. Legal

3. Operational 3. Communications 3. Communications 3. Operational

4. Attitudes 4. Attitudes

5. Actions 5. Actions

Fact

Based

Perception

Based

Perception

Based

FactBased

Seller Acquirer

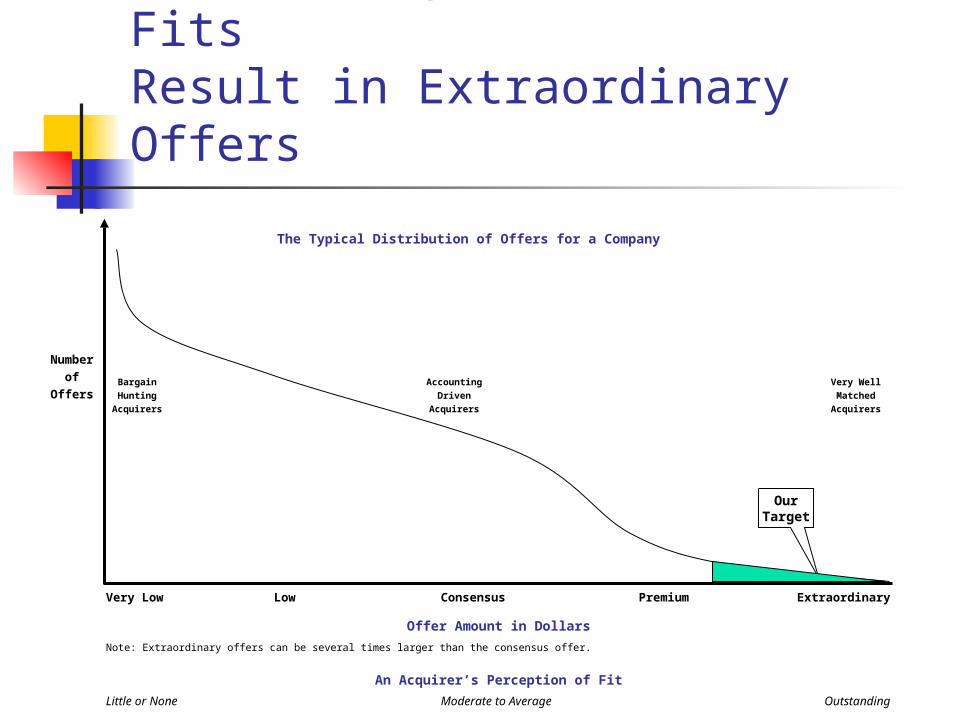

Outstanding Operational FitsResult in Extraordinary Offers

OurTarget

The Typical Distribution of Offers for a Company

Very Low Low Consensus Premium Extraordinary

Number

of

Offers

Note: Extraordinary offers can be several times larger than the consensus offer.

Offer Amount in Dollars

An Acquirer’s Perception of Fit

Little or None Moderate to Average Outstanding

Bargain Accounting Very Well

Hunting Driven Matched

Acquirers Acquirers Acquirers

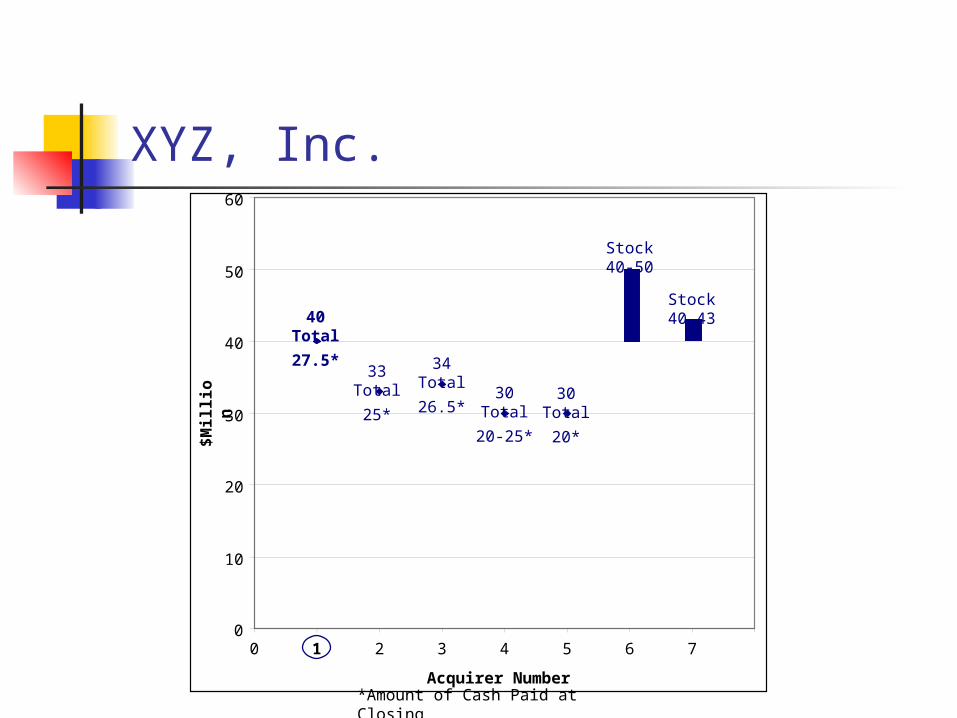

XYZ, Inc.

Acquirer Number

0

10

20

30

40

50

60

0 1 2 3 4 5 6 7

40Total

27.5*33

Total

25*

34Total

26.5*30

Total

20-25*

30Total

20*

Stock40-50

Stock40-43

$M

illi

on

*Amount of Cash Paid at Closing

Negotiations Will Have Many Ups and Downs

“And, while there’s no reason yet to panic,I think it only prudent that we make preparations to panic.”

Manage Transaction Resources

“Would everyone check to see if they have an attorney?I seem to have ended up with two.”

Deal Breakers/Deal Makers

Deal Breakers One-man show syndrome Abandon ship after closing “Commodity” product lines Dilapidated or under-maintained

equipment Insincere Seller Last minute surprises

undisclosed lawsuits recent loss of major customer(s) recent loss of financial

personnel/advisors inaccurate balance sheet financial underperformance

Deal Makers Retention and depth of the

management team Not a one-man company Good systems and records Differentiated or proprietary

products Strong relative market share Commitment to the buyer for

a smooth transition

![thesongoftherighteous.files.wordpress.com · Hark the Herald Angels Sing Score (Come Thou Fount of Every Blessing) Voice Piano [Composer] Michael D. Young Hark the her ald an gels](https://img.pdfslide.us/doc/110x75/5ae90def7f8b9ab24d8b8b5f/t-the-herald-angels-sing-score-come-thou-fount-of-every-blessing-voice-piano-composer.jpg)

![Hark Hark [E,134 bpm,6/8] - Brentwood Benson...Hark [G, 134 bpm, 6/8] [Hillsong Worship] Intro |G.\.|.Csus2.Cmaj9.|.Dsus.\.|.Em7..\.| Verse.1 Csus2.Cmaj9 Hark.the.herald.angels.sing](https://img.pdfslide.us/doc/110x75/60d22042ffbbf117fb1a77a3/hark-hark-e134-bpm68-brentwood-benson-hark-g-134-bpm-68-hillsong.jpg)