Embed Size (px)

Citation preview

1 © InfoTrends www.infotrends.com © InfoTrends

Capturing the Revenue Opportunity

Tim Greene Director – Wide Format, InfoTrends Kate Dunn Director – Business Development Group, InfoTrends January 2014

2 © InfoTrends www.infotrends.com

Agenda

• Current State of Print for Pay Market

• Capturing the Large Format Revenue Opportunity

• Next Steps

3 © InfoTrends www.infotrends.com

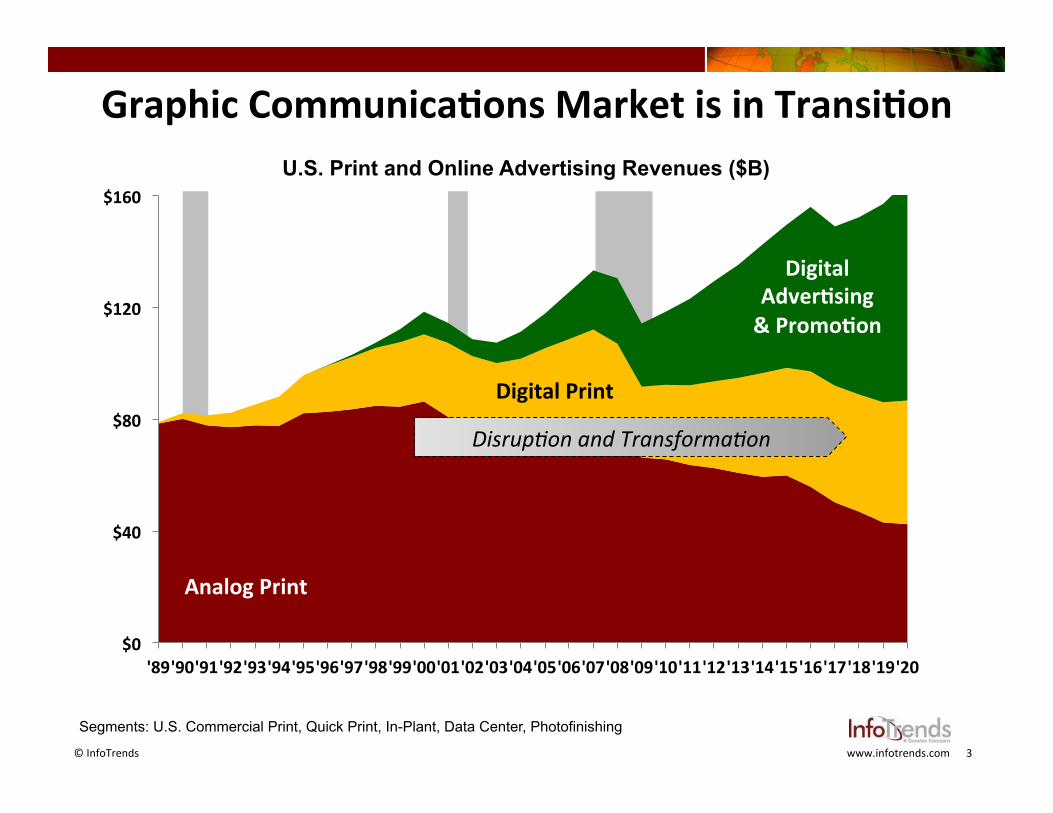

$0

$40

$80

$120

$160

'89 '90 '91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20

Graphic CommunicaPons Market is in TransiPon

Analog Print

Digital AdverPsing & PromoPon

Digital Print

U.S. Print and Online Advertising Revenues ($B)

Segments: U.S. Commercial Print, Quick Print, In-Plant, Data Center, Photofinishing

Disrup'on and Transforma'on

4 © InfoTrends www.infotrends.com

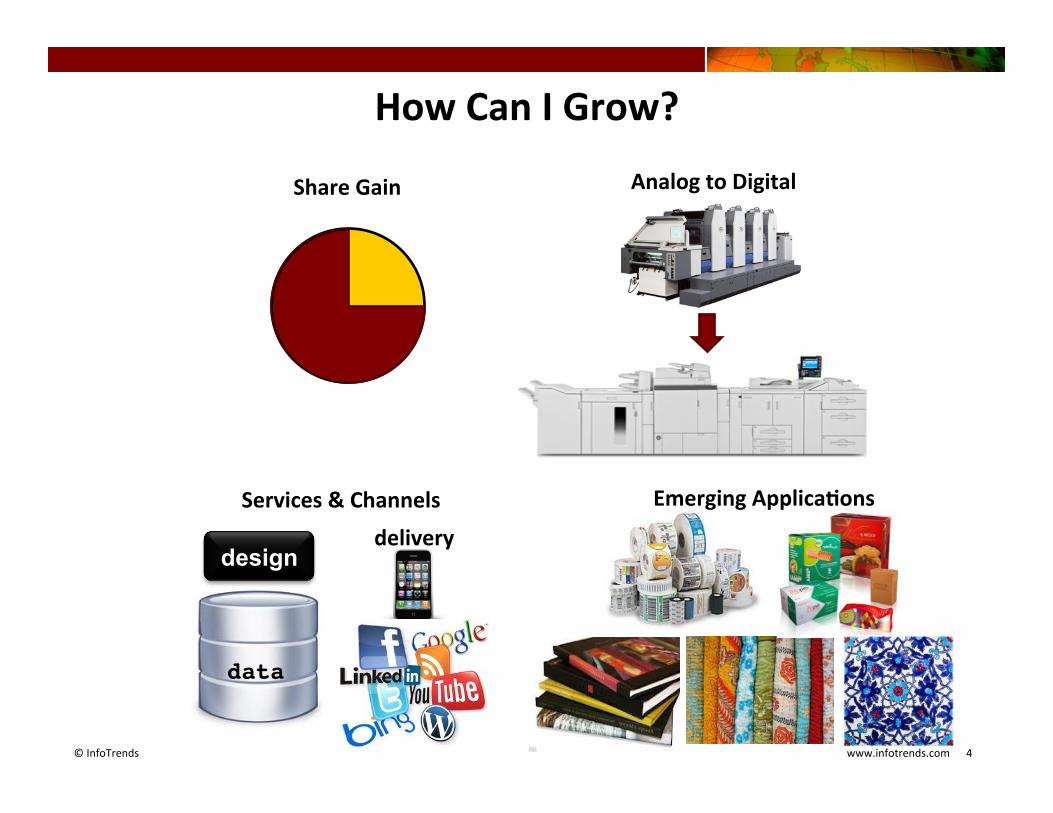

How Can I Grow?

Share Gain

Emerging ApplicaPons

delivery design

data!

Services & Channels

Analog to Digital

5 © InfoTrends www.infotrends.com

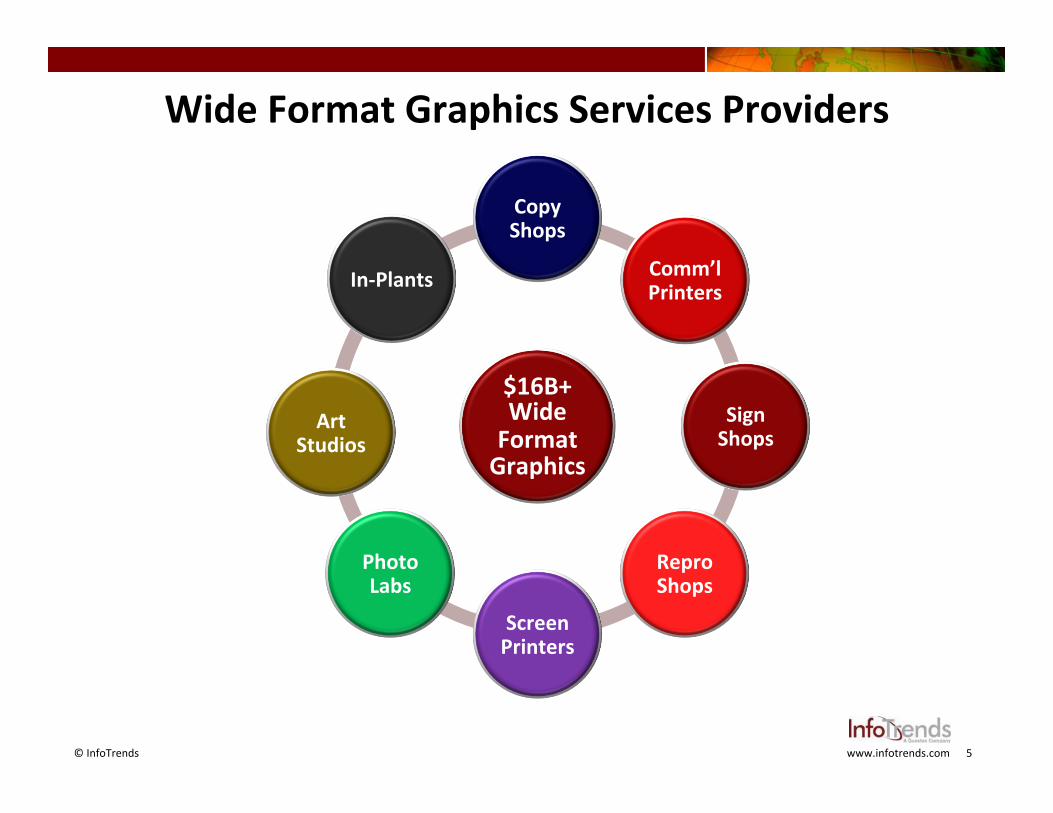

Wide Format Graphics Services Providers

$16B+ Wide Format Graphics

Copy Shops

Comm’l Printers

Sign Shops

Repro Shops

Screen Printers

Photo Labs

Art Studios

In-‐Plants

6 © InfoTrends www.infotrends.com

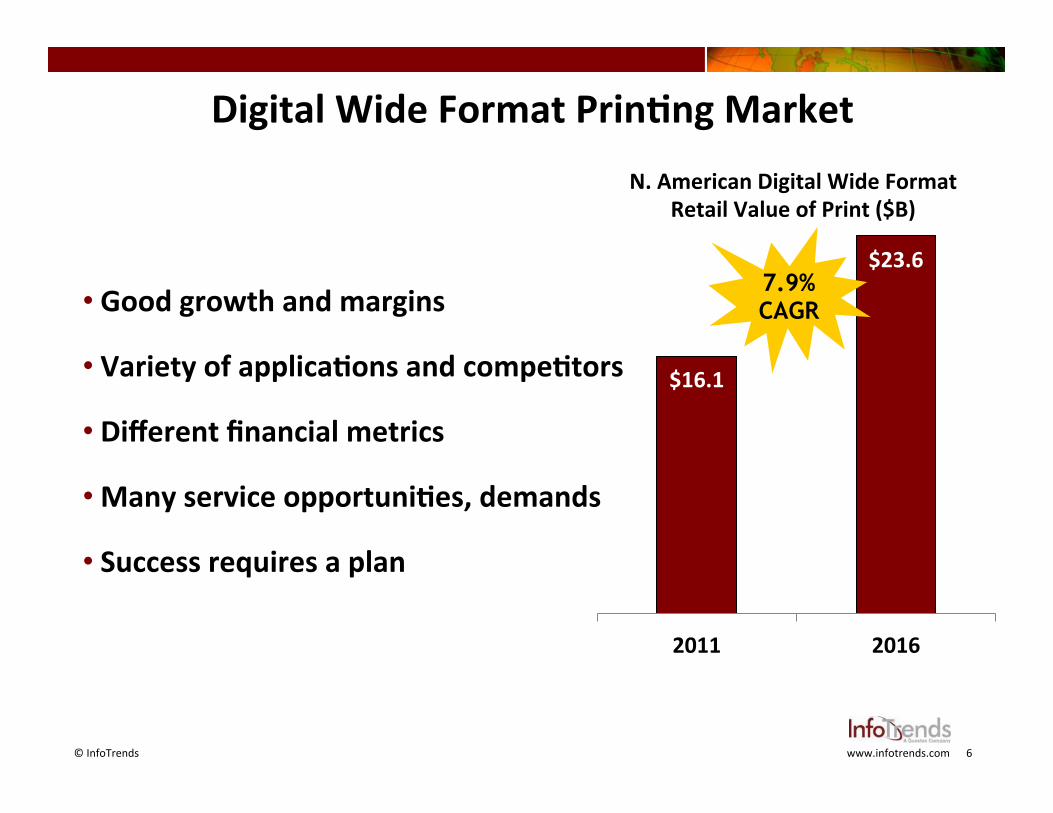

• Good growth and margins

• Variety of applicaPons and compePtors

• Different financial metrics

• Many service opportuniPes, demands

• Success requires a plan

Digital Wide Format PrinPng Market

$16.1

$23.6

2011 2016

N. American Digital Wide Format Retail Value of Print ($B)

7.9% CAGR

7 © InfoTrends www.infotrends.com

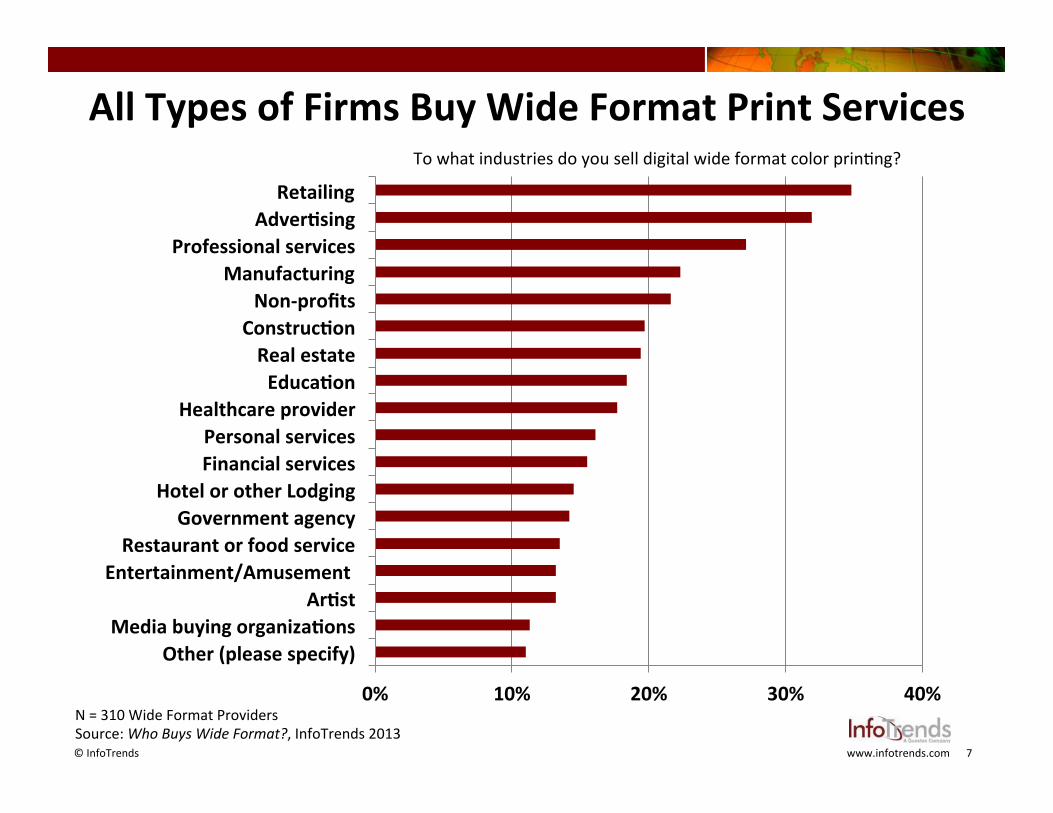

All Types of Firms Buy Wide Format Print Services

0% 10% 20% 30% 40%

Other (please specify) Media buying organizaPons

ArPst Entertainment/Amusement Restaurant or food service

Government agency Hotel or other Lodging

Financial services Personal services

Healthcare provider EducaPon Real estate

ConstrucPon Non-‐profits

Manufacturing Professional services

AdverPsing Retailing

N = 310 Wide Format Providers Source: Who Buys Wide Format?, InfoTrends 2013

To what industries do you sell digital wide format color prinOng?

8 © InfoTrends www.infotrends.com

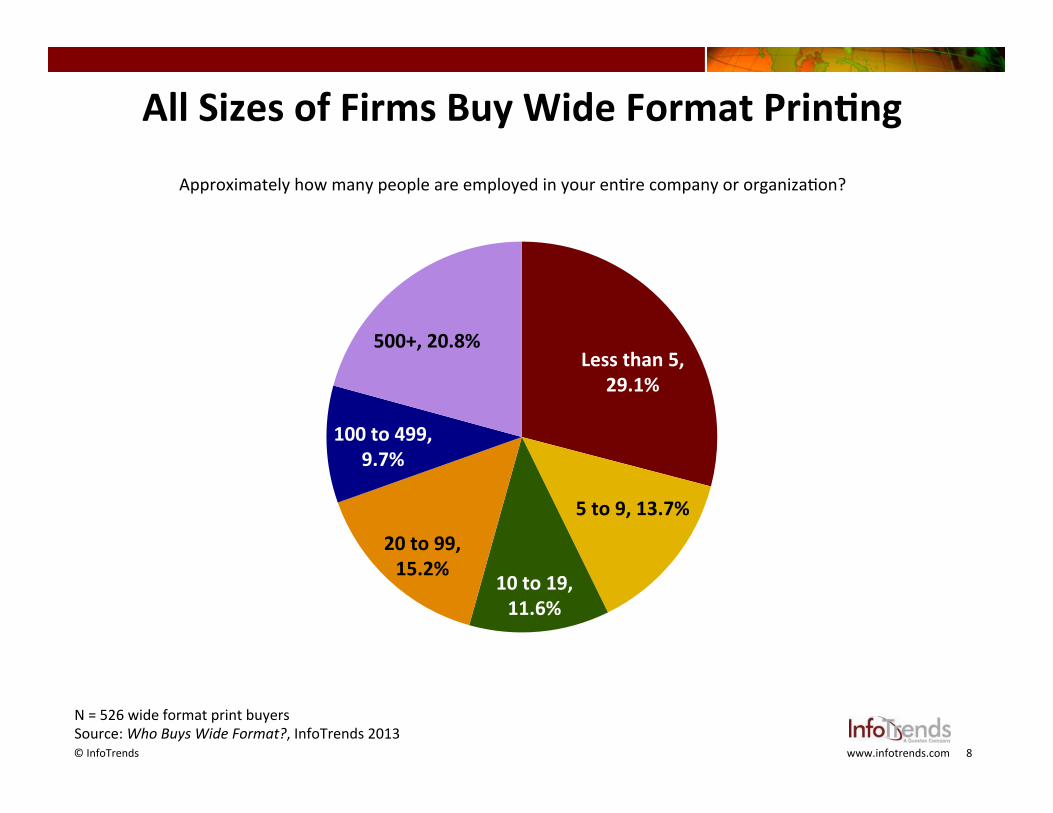

N = 526 wide format print buyers Source: Who Buys Wide Format?, InfoTrends 2013

Approximately how many people are employed in your enOre company or organizaOon?

All Sizes of Firms Buy Wide Format PrinPng

Less than 5, 29.1%

5 to 9, 13.7%

10 to 19, 11.6%

20 to 99, 15.2%

100 to 499, 9.7%

500+, 20.8%

9 © InfoTrends www.infotrends.com

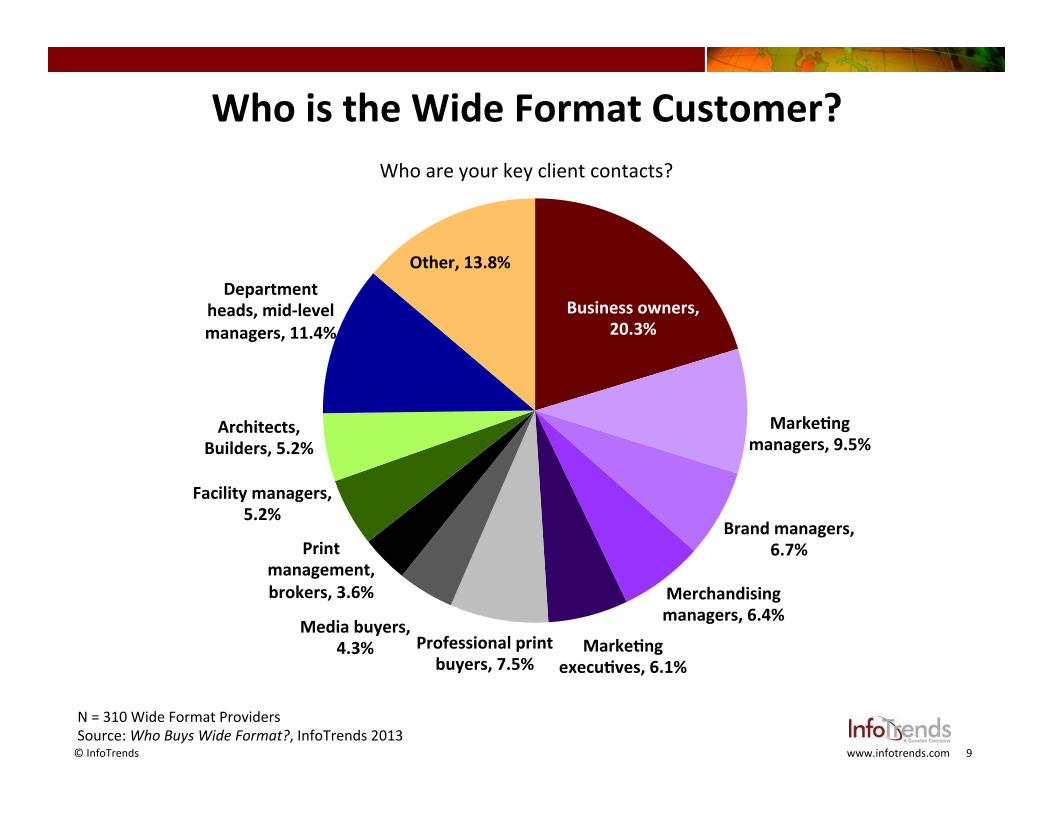

Who are your key client contacts?

N = 310 Wide Format Providers Source: Who Buys Wide Format?, InfoTrends 2013

Who is the Wide Format Customer?

Business owners, 20.3%

MarkePng managers, 9.5%

Brand managers, 6.7%

Merchandising managers, 6.4%

MarkePng execuPves, 6.1%

Professional print buyers, 7.5%

Media buyers, 4.3%

Print management, brokers, 3.6%

Facility managers, 5.2%

Architects, Builders, 5.2%

Department heads, mid-‐level managers, 11.4%

Other, 13.8%

10 © InfoTrends www.infotrends.com

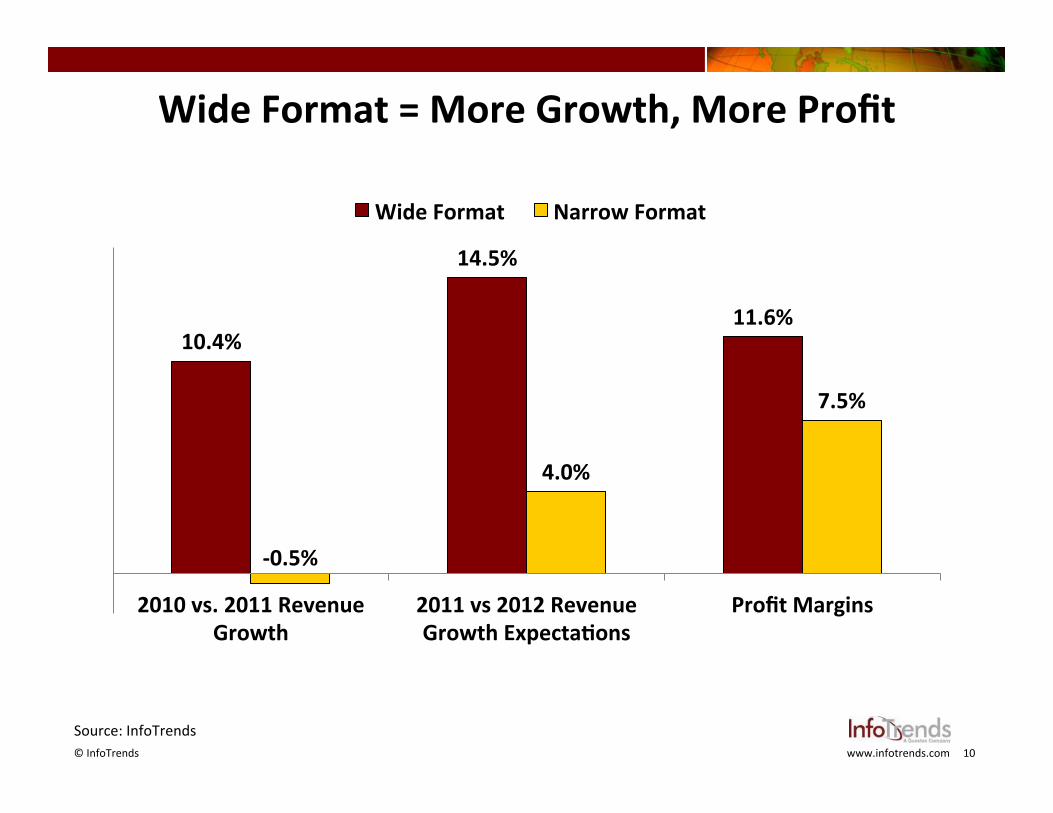

Wide Format = More Growth, More Profit

10.4%

14.5%

11.6%

-‐0.5%

4.0%

7.5%

2010 vs. 2011 Revenue Growth

2011 vs 2012 Revenue Growth ExpectaPons

Profit Margins

Wide Format Narrow Format

Source: InfoTrends

11 © InfoTrends www.infotrends.com

• Interior décor

• Rigid applicaPons

• Short-‐run packaging

New Wide Format ApplicaPons

12 © InfoTrends www.infotrends.com

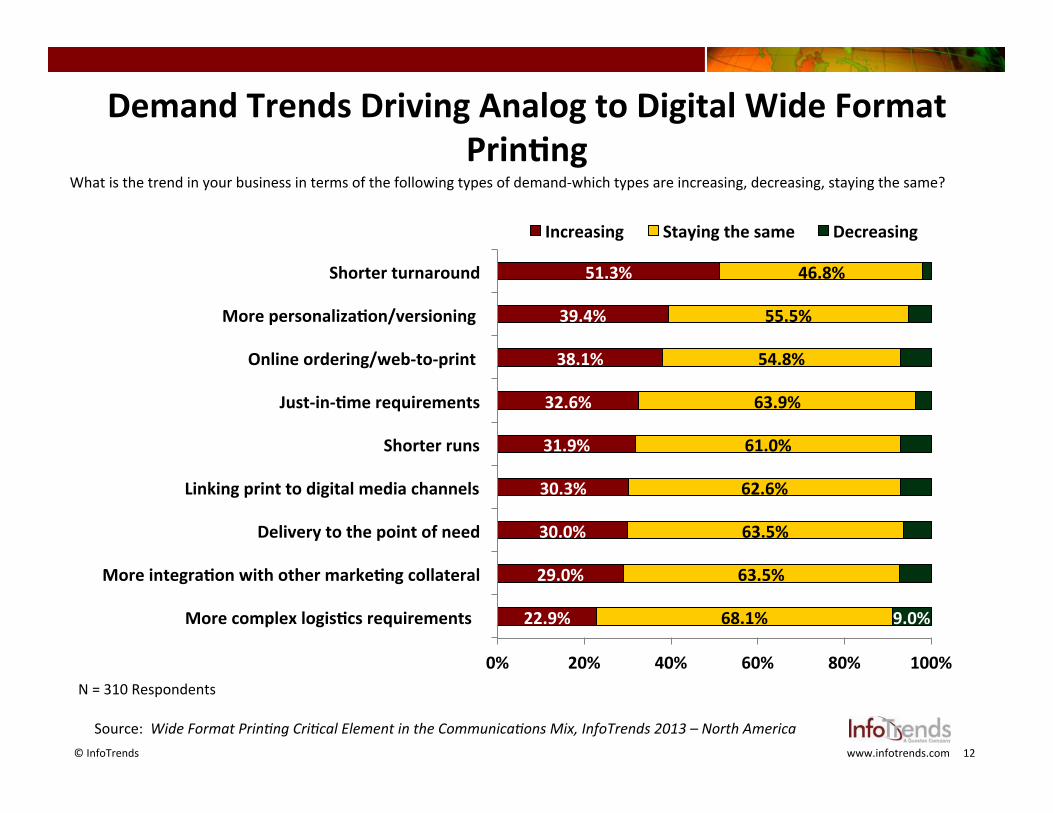

22.9%

29.0%

30.0%

30.3%

31.9%

32.6%

38.1%

39.4%

51.3%

68.1%

63.5%

63.5%

62.6%

61.0%

63.9%

54.8%

55.5%

46.8%

9.0%

0% 20% 40% 60% 80% 100%

More complex logisPcs requirements

More integraPon with other markePng collateral

Delivery to the point of need

Linking print to digital media channels

Shorter runs

Just-‐in-‐Pme requirements

Online ordering/web-‐to-‐print

More personalizaPon/versioning

Shorter turnaround

Increasing Staying the same Decreasing

Demand Trends Driving Analog to Digital Wide Format PrinPng

What is the trend in your business in terms of the following types of demand-‐which types are increasing, decreasing, staying the same?

N = 310 Respondents

Source: Wide Format Prin'ng Cri'cal Element in the Communica'ons Mix, InfoTrends 2013 – North America

13 © InfoTrends www.infotrends.com

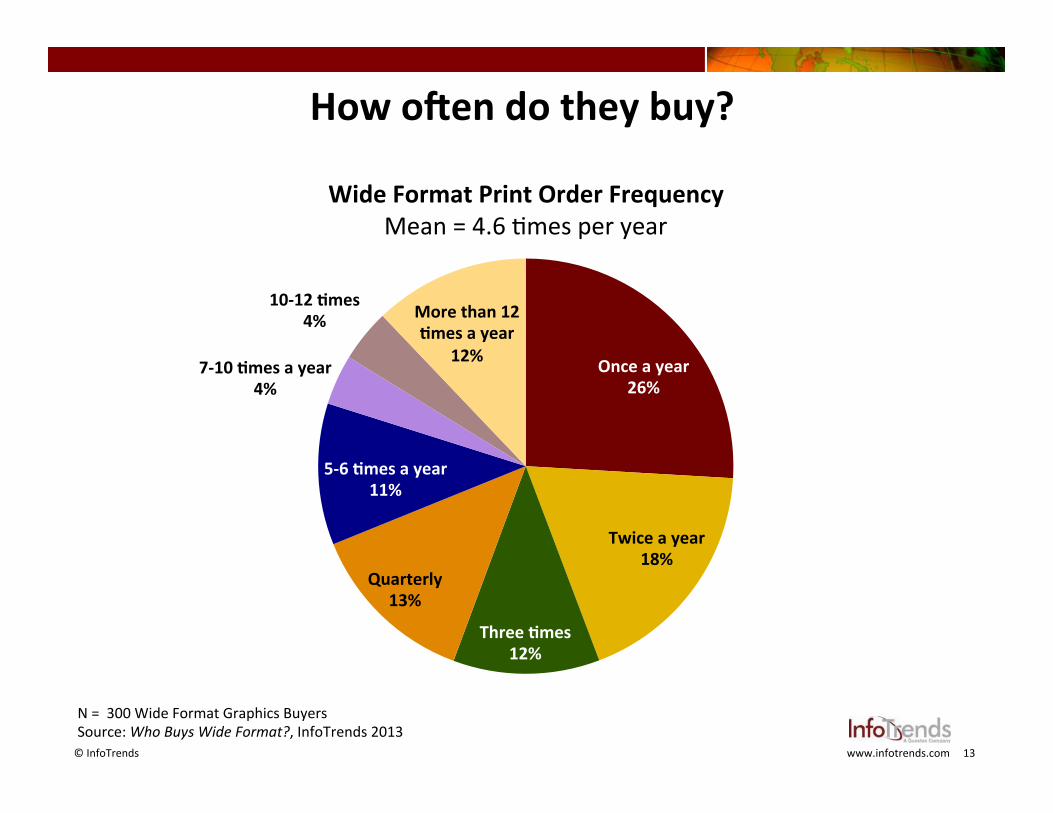

N = 300 Wide Format Graphics Buyers Source: Who Buys Wide Format?, InfoTrends 2013

How olen do they buy?

Once a year 26%

Twice a year 18%

Three Pmes 12%

Quarterly 13%

5-‐6 Pmes a year 11%

7-‐10 Pmes a year 4%

10-‐12 Pmes 4% More than 12

Pmes a year 12%

Wide Format Print Order Frequency Mean = 4.6 Omes per year

14 © InfoTrends www.infotrends.com

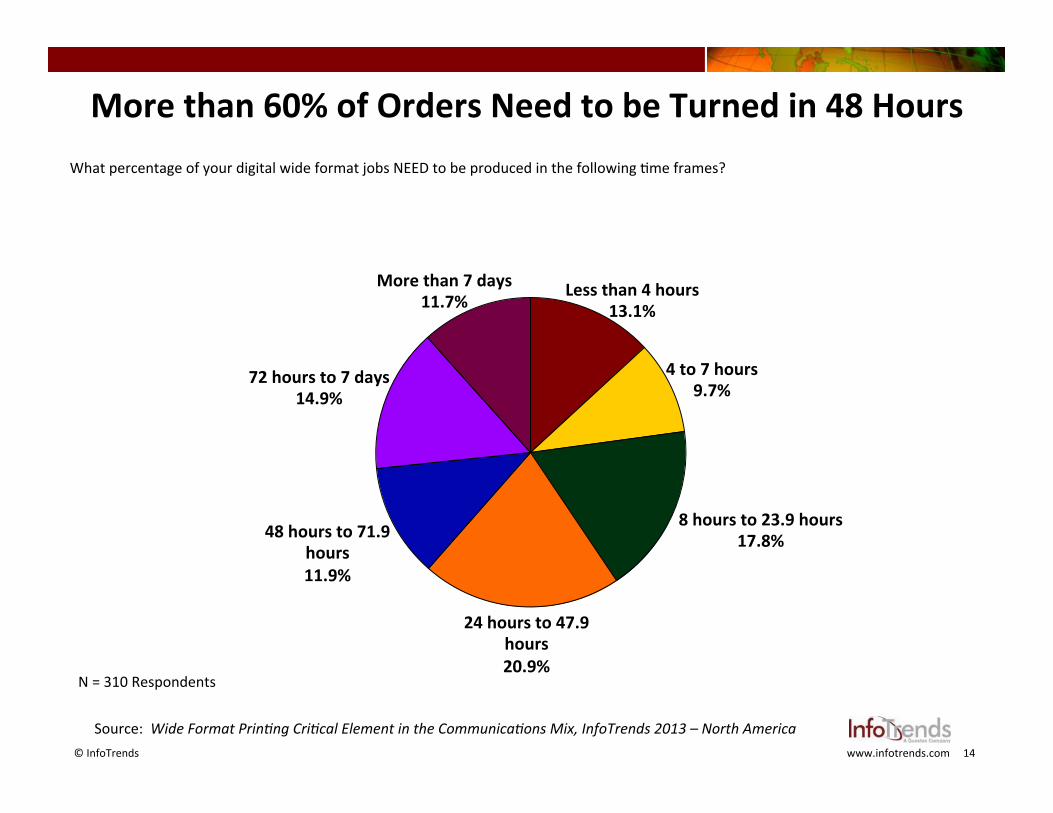

More than 60% of Orders Need to be Turned in 48 Hours

Less than 4 hours 13.1%

4 to 7 hours 9.7%

8 hours to 23.9 hours 17.8%

24 hours to 47.9 hours 20.9%

48 hours to 71.9 hours 11.9%

72 hours to 7 days 14.9%

More than 7 days 11.7%

What percentage of your digital wide format jobs NEED to be produced in the following Ome frames?

N = 310 Respondents

Source: Wide Format Prin'ng Cri'cal Element in the Communica'ons Mix, InfoTrends 2013 – North America

15 © InfoTrends www.infotrends.com

www.858graphics.com

Service Providers Step Up to the Challenge

16 © InfoTrends www.infotrends.com

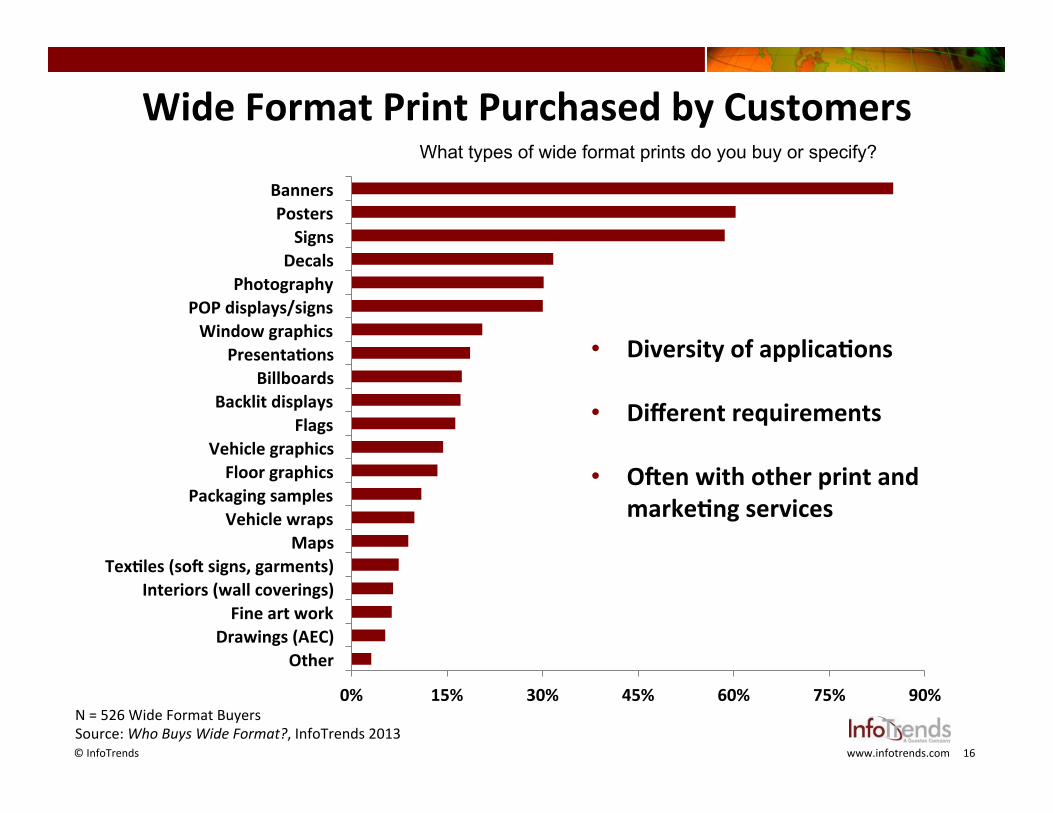

Wide Format Print Purchased by Customers

0% 15% 30% 45% 60% 75% 90%

Other Drawings (AEC) Fine art work

Interiors (wall coverings) TexPles (sol signs, garments)

Maps Vehicle wraps

Packaging samples Floor graphics

Vehicle graphics Flags

Backlit displays Billboards

PresentaPons Window graphics

POP displays/signs Photography

Decals Signs

Posters Banners

N = 526 Wide Format Buyers Source: Who Buys Wide Format?, InfoTrends 2013

What types of wide format prints do you buy or specify?

• Diversity of applicaPons

• Different requirements

• Olen with other print and markePng services

17 © InfoTrends www.infotrends.com

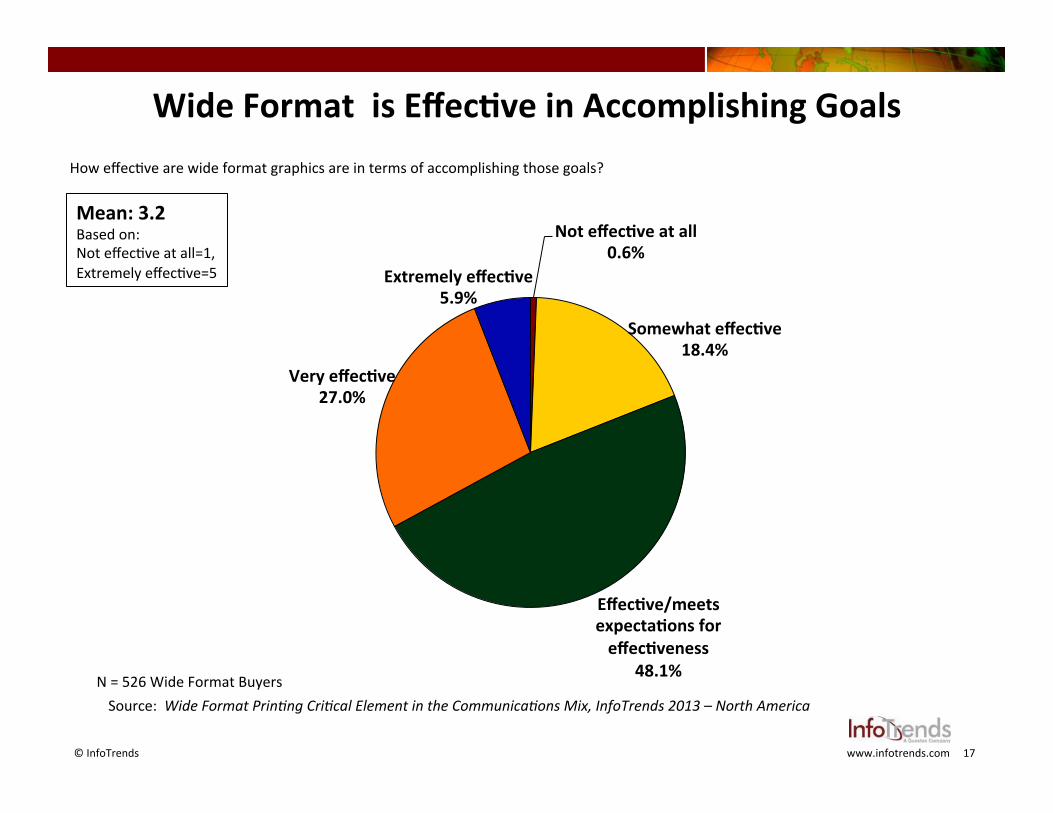

Wide Format is EffecPve in Accomplishing Goals

Not effecPve at all 0.6%

Somewhat effecPve 18.4%

EffecPve/meets expectaPons for effecPveness

48.1%

Very effecPve 27.0%

Extremely effecPve 5.9%

How effecOve are wide format graphics are in terms of accomplishing those goals?

N = 526 Wide Format Buyers

Mean: 3.2 Based on: Not effecOve at all=1, Extremely effecOve=5

Source: Wide Format Prin'ng Cri'cal Element in the Communica'ons Mix, InfoTrends 2013 – North America

18 © InfoTrends www.infotrends.com

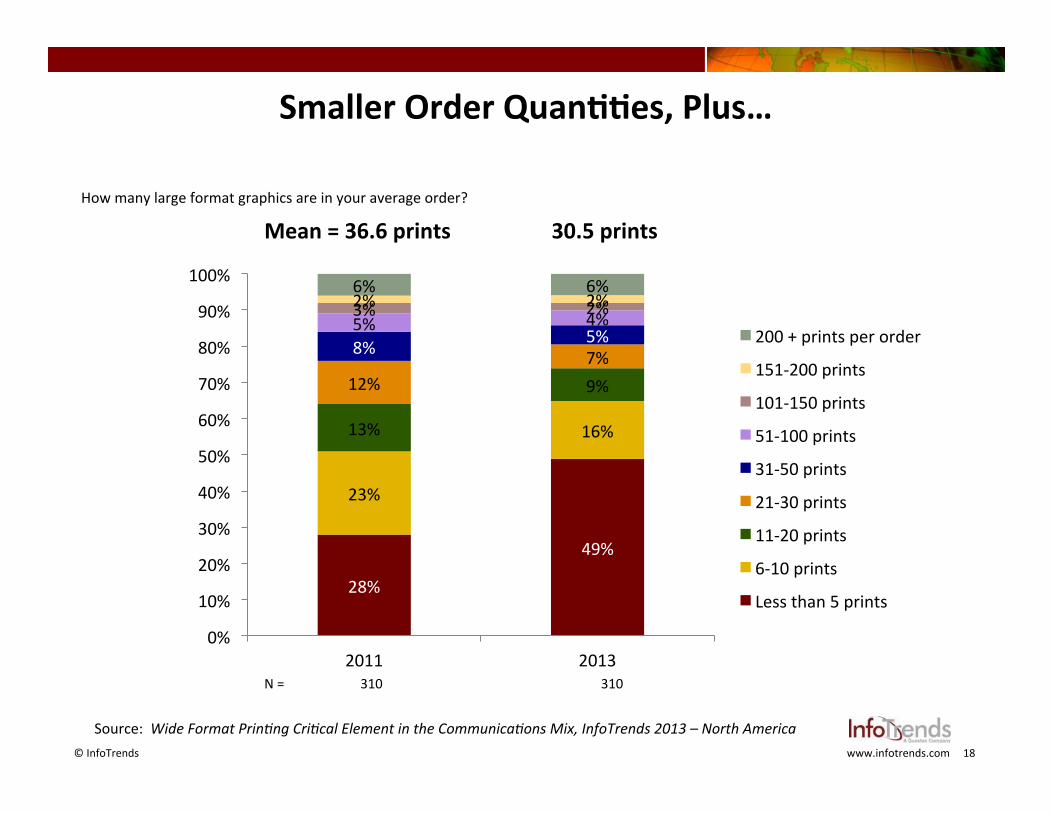

How many large format graphics are in your average order?

N = 310 310

Smaller Order QuanPPes, Plus…

28%

49%

23%

16% 13%

9% 12% 7% 8% 5%

5% 4% 3% 2% 2% 2% 6% 6%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2011 2013

200 + prints per order

151-‐200 prints

101-‐150 prints

51-‐100 prints

31-‐50 prints

21-‐30 prints

11-‐20 prints

6-‐10 prints

Less than 5 prints

Mean = 36.6 prints 30.5 prints

Source: Wide Format Prin'ng Cri'cal Element in the Communica'ons Mix, InfoTrends 2013 – North America

19 © InfoTrends www.infotrends.com

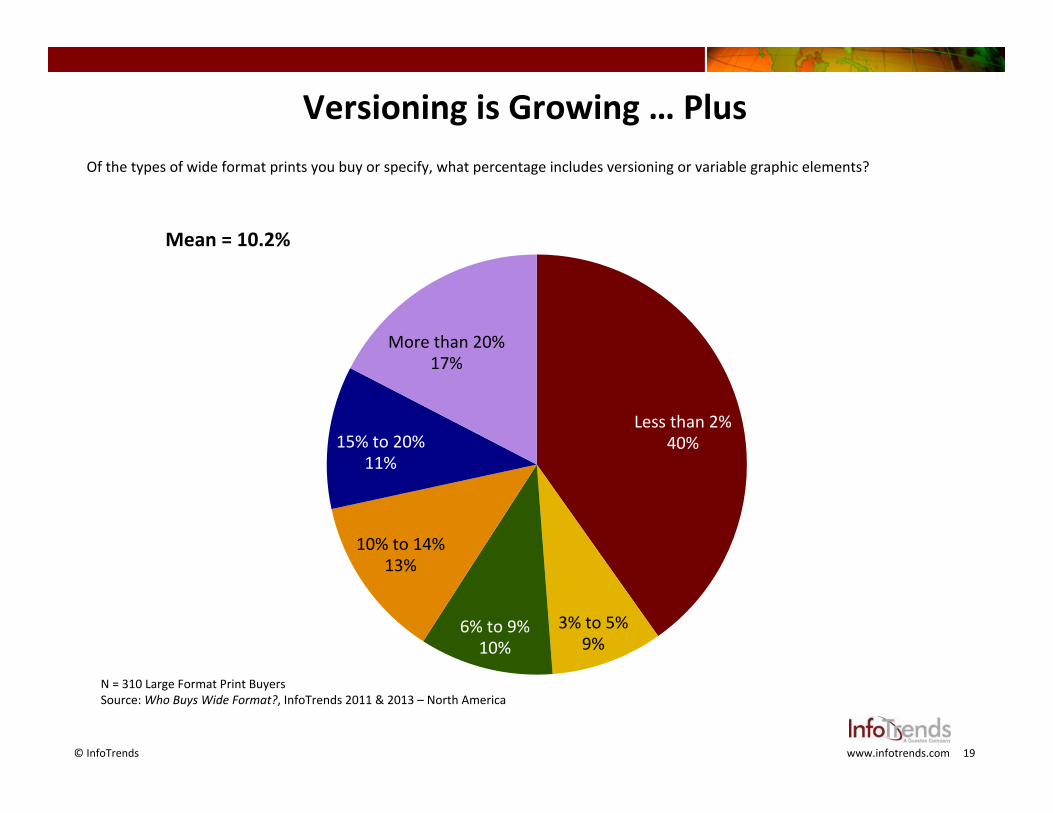

Versioning is Growing … Plus

N = 310 Large Format Print Buyers Source: Who Buys Wide Format?, InfoTrends 2011 & 2013 – North America

Of the types of wide format prints you buy or specify, what percentage includes versioning or variable graphic elements?

Less than 2% 40%

3% to 5% 9%

6% to 9% 10%

10% to 14% 13%

15% to 20% 11%

More than 20% 17%

Mean = 10.2%

20 © InfoTrends www.infotrends.com

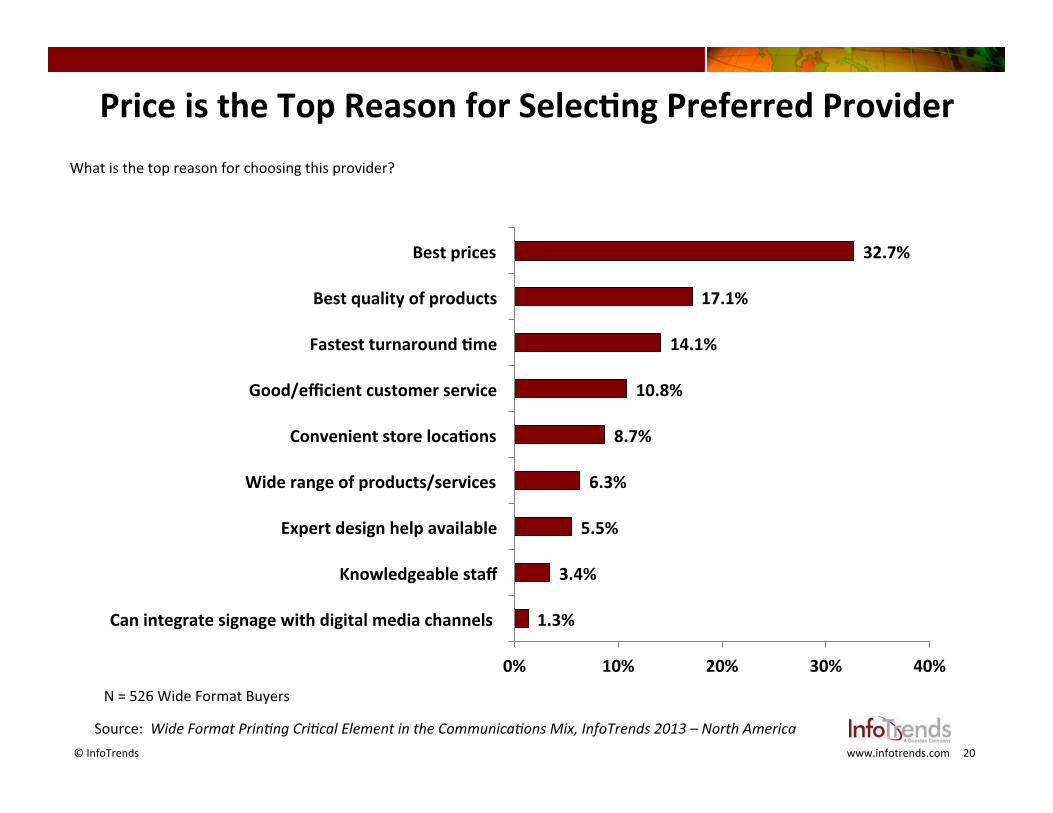

1.3%

3.4%

5.5%

6.3%

8.7%

10.8%

14.1%

17.1%

32.7%

0% 10% 20% 30% 40%

Can integrate signage with digital media channels

Knowledgeable staff

Expert design help available

Wide range of products/services

Convenient store locaPons

Good/efficient customer service

Fastest turnaround Pme

Best quality of products

Best prices

Price is the Top Reason for SelecPng Preferred Provider What is the top reason for choosing this provider?

N = 526 Wide Format Buyers

Source: Wide Format Prin'ng Cri'cal Element in the Communica'ons Mix, InfoTrends 2013 – North America

21 © InfoTrends www.infotrends.com

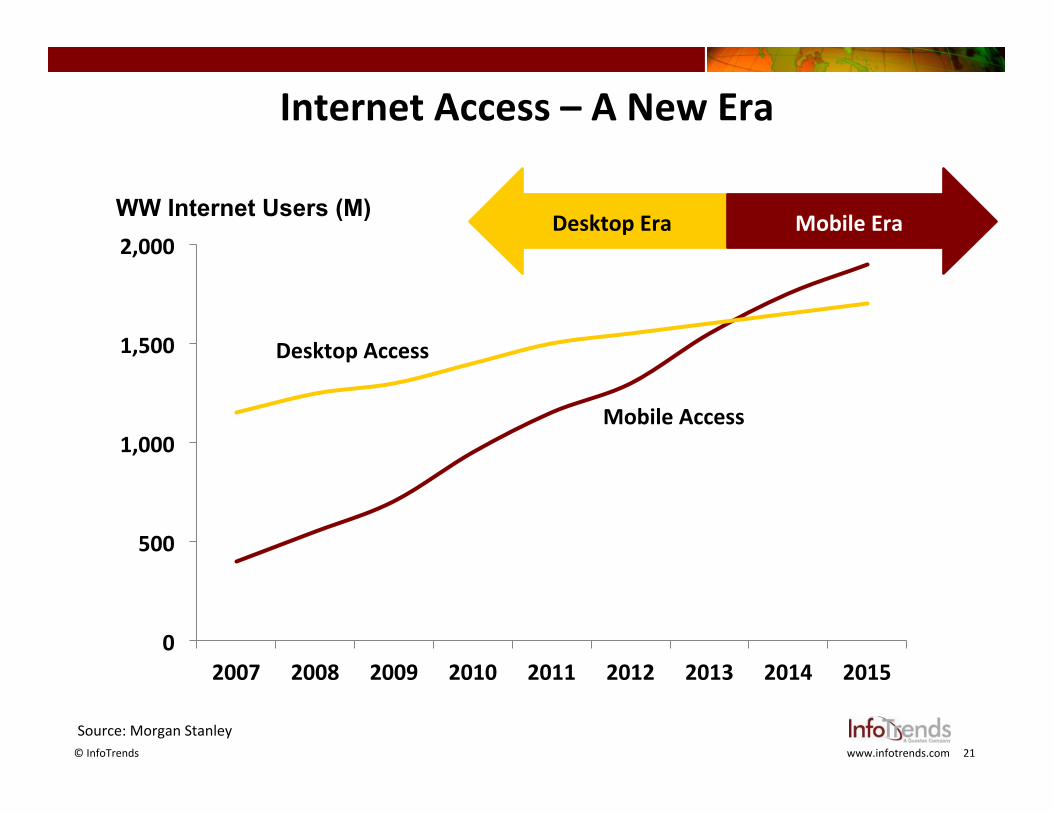

Internet Access – A New Era

0

500

1,000

1,500

2,000

2007 2008 2009 2010 2011 2012 2013 2014 2015

Desktop Access

Mobile Access

Source: Morgan Stanley

WW Internet Users (M) Desktop Era Mobile Era

22 © InfoTrends www.infotrends.com

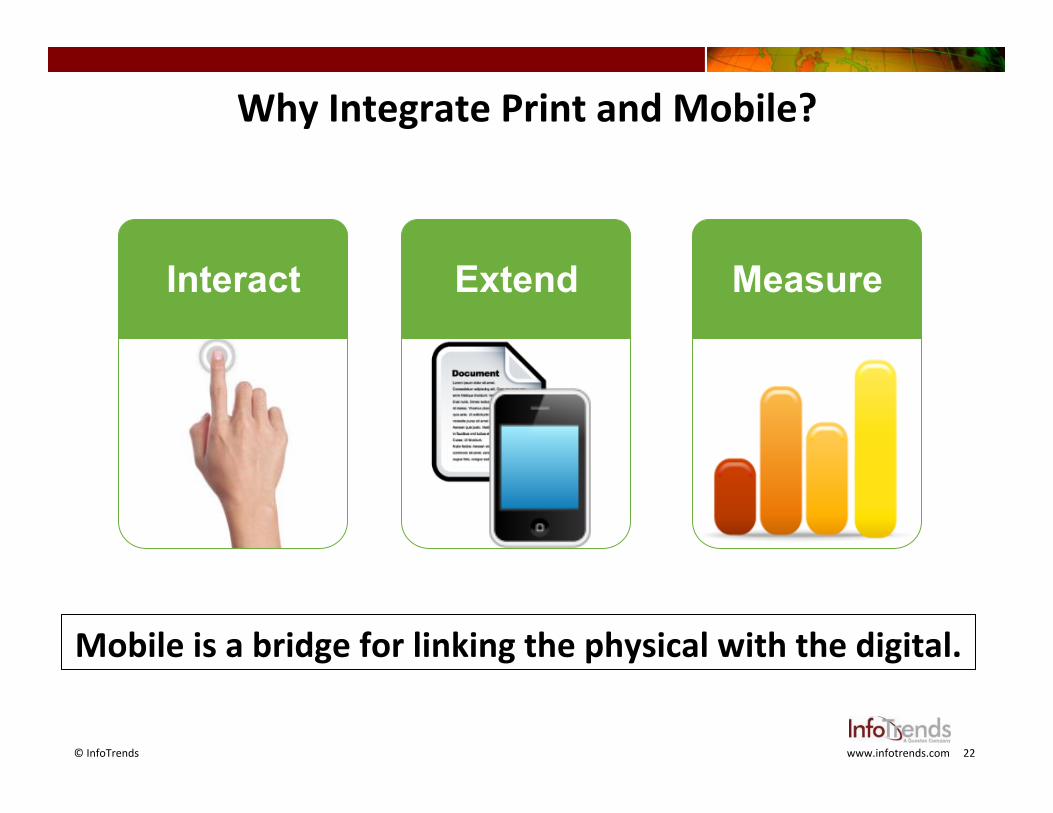

Why Integrate Print and Mobile?

Interact Extend Measure

Mobile is a bridge for linking the physical with the digital.

23 © InfoTrends www.infotrends.com

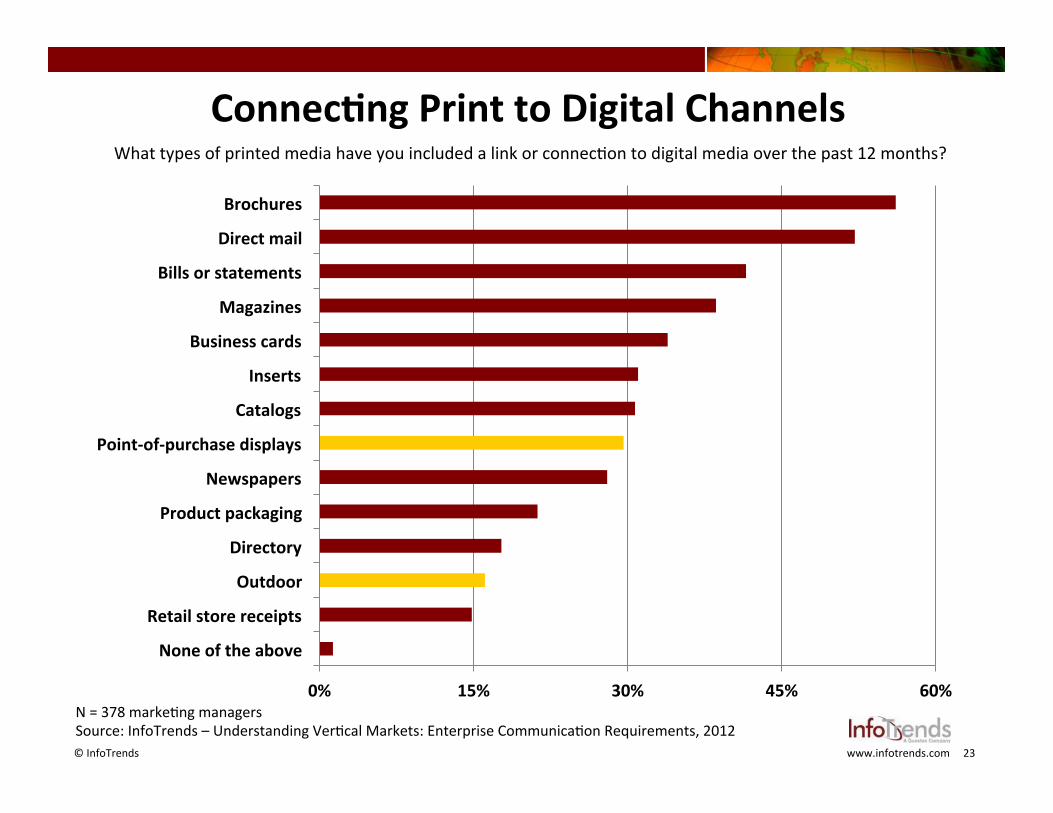

ConnecPng Print to Digital Channels

0% 15% 30% 45% 60%

None of the above

Retail store receipts

Outdoor

Directory

Product packaging

Newspapers

Point-‐of-‐purchase displays

Catalogs

Inserts

Business cards

Magazines

Bills or statements

Direct mail

Brochures

What types of printed media have you included a link or connecOon to digital media over the past 12 months?

N = 378 markeOng managers Source: InfoTrends – Understanding VerOcal Markets: Enterprise CommunicaOon Requirements, 2012

24 © InfoTrends www.infotrends.com

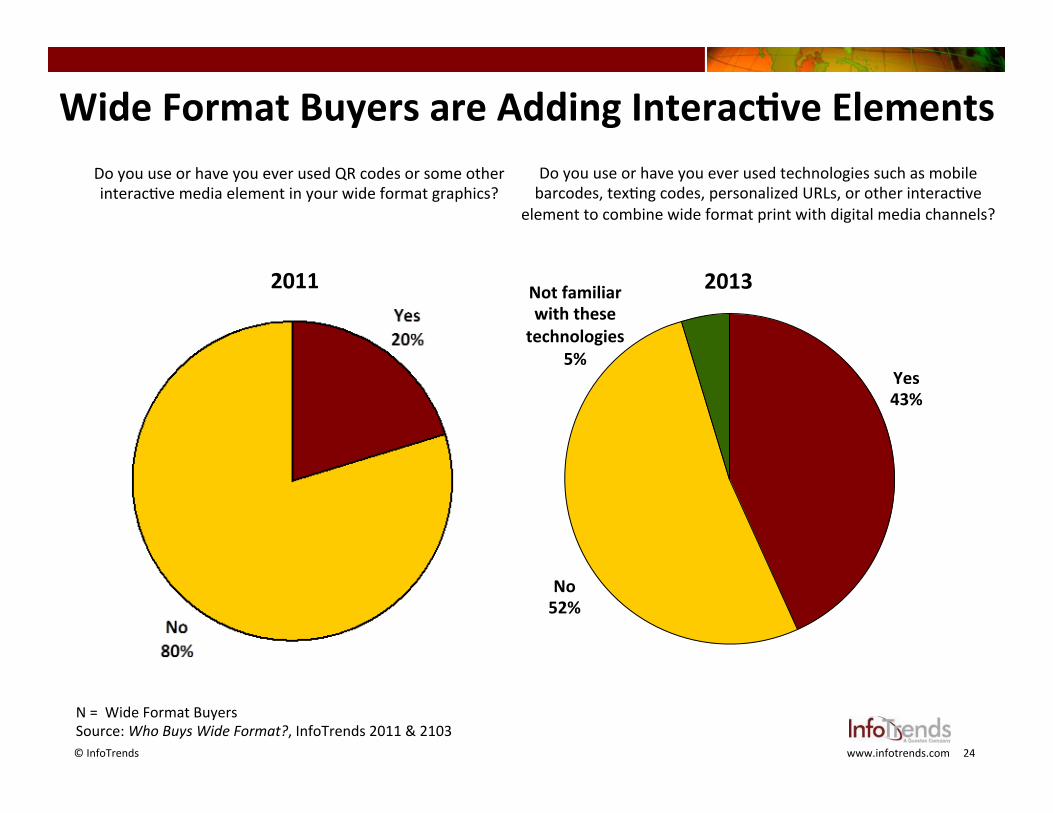

N = Wide Format Buyers Source: Who Buys Wide Format?, InfoTrends 2011 & 2103

Do you use or have you ever used QR codes or some other interacOve media element in your wide format graphics?

Wide Format Buyers are Adding InteracPve Elements

Yes 43%

No 52%

Not familiar with these technologies

5%

Do you use or have you ever used technologies such as mobile barcodes, texOng codes, personalized URLs, or other interacOve

element to combine wide format print with digital media channels?

2011 2013

25 © InfoTrends www.infotrends.com

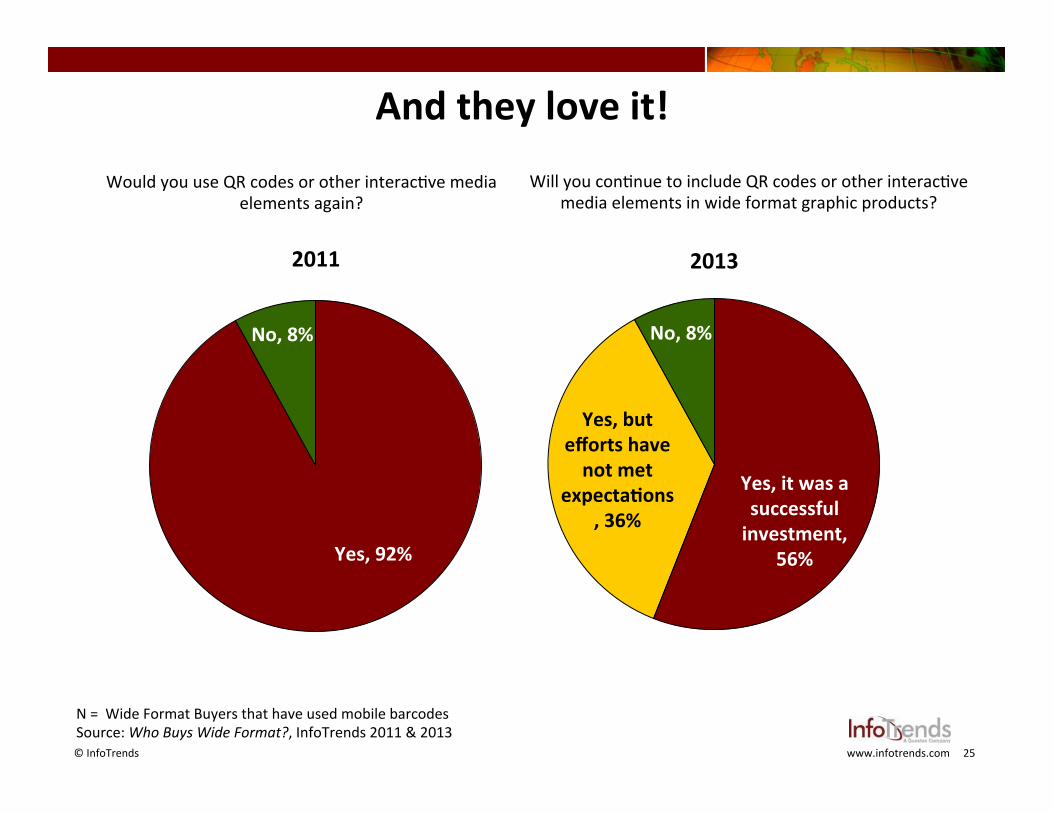

Yes, 92%

No, 8%

N = Wide Format Buyers that have used mobile barcodes Source: Who Buys Wide Format?, InfoTrends 2011 & 2013

Would you use QR codes or other interacOve media elements again?

And they love it!

Will you conOnue to include QR codes or other interacOve media elements in wide format graphic products?

2011 2013

Yes, it was a successful investment,

56%

Yes, but efforts have not met

expectaPons, 36%

No, 8%

26 © InfoTrends www.infotrends.com

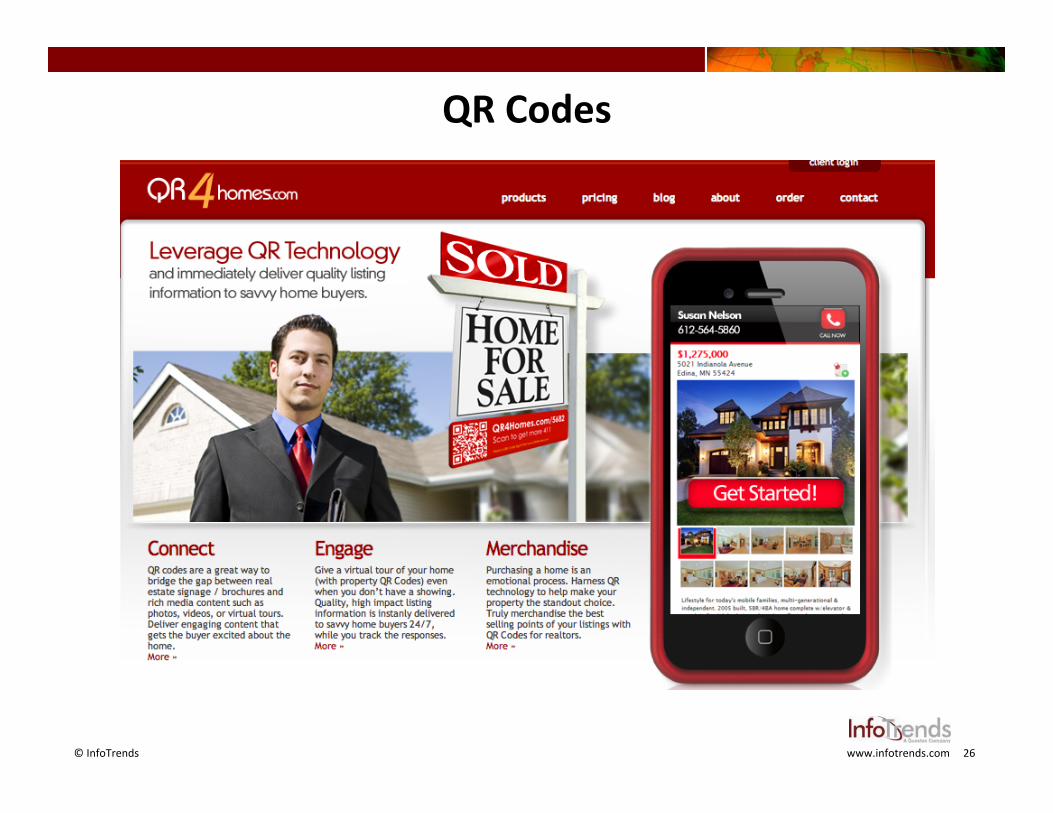

QR Codes

27 © InfoTrends www.infotrends.com

Calvin Klein: Signage Meets QR Codes

28 © InfoTrends www.infotrends.com

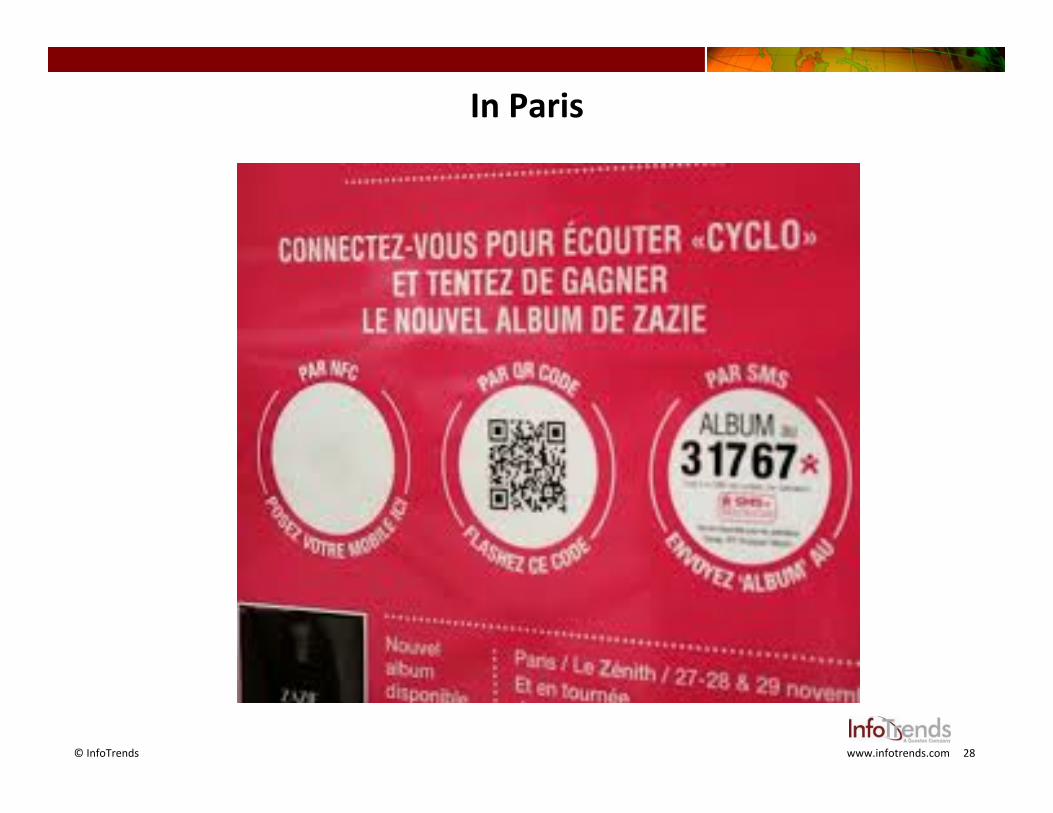

In Paris

29 © InfoTrends www.infotrends.com

ScoPabank Campaign in Canada

30 © InfoTrends www.infotrends.com

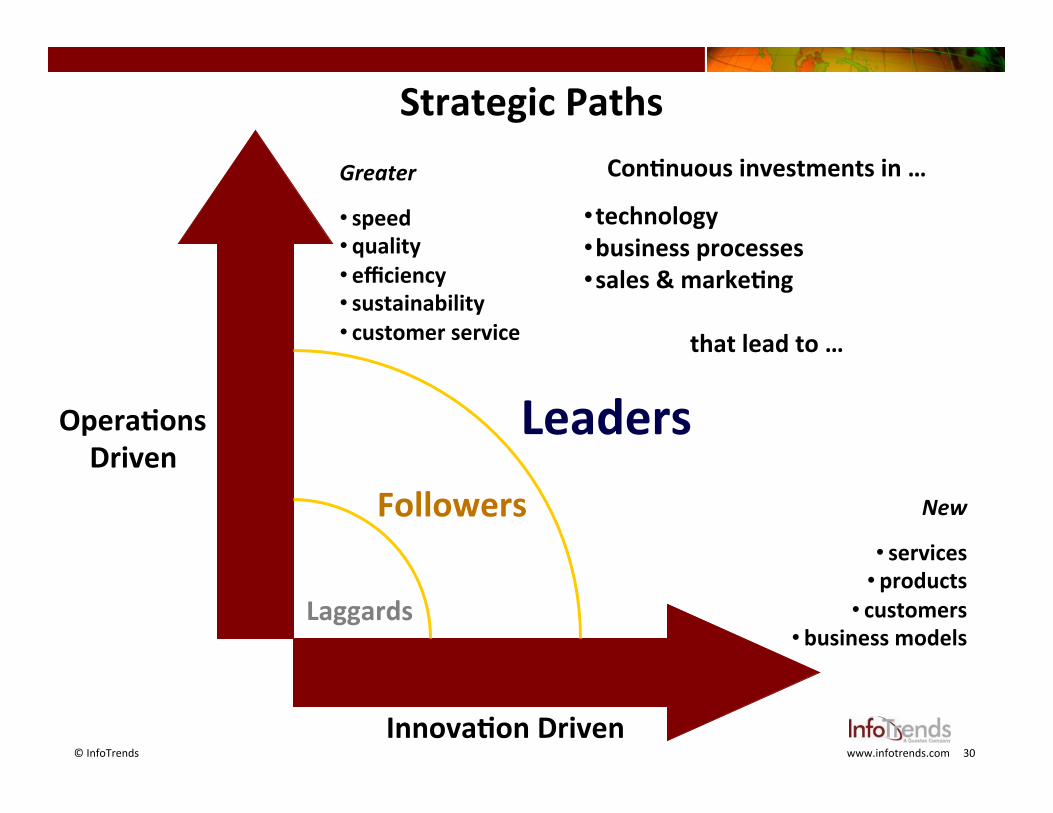

Strategic Paths

InnovaPon Driven

OperaPons Driven

Greater

• speed • quality • efficiency • sustainability • customer service

New

• services • products

• customers • business models

ConPnuous investments in …

• technology • business processes • sales & markePng

that lead to …

Laggards

Followers

Leaders

31 © InfoTrends www.infotrends.com

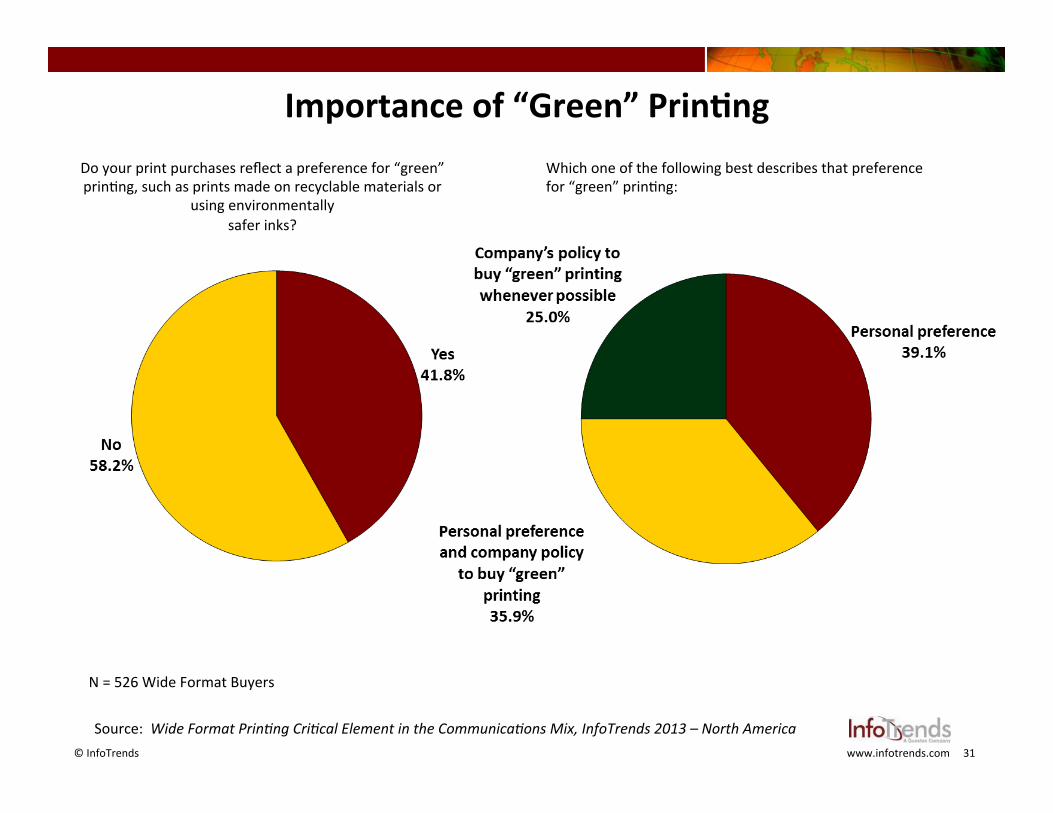

Importance of “Green” PrinPng Do your print purchases reflect a preference for “green” prinOng, such as prints made on recyclable materials or

using environmentally safer inks?

N = 526 Wide Format Buyers

Which one of the following best describes that preference for “green” prinOng:

Source: Wide Format Prin'ng Cri'cal Element in the Communica'ons Mix, InfoTrends 2013 – North America

32 © InfoTrends www.infotrends.com

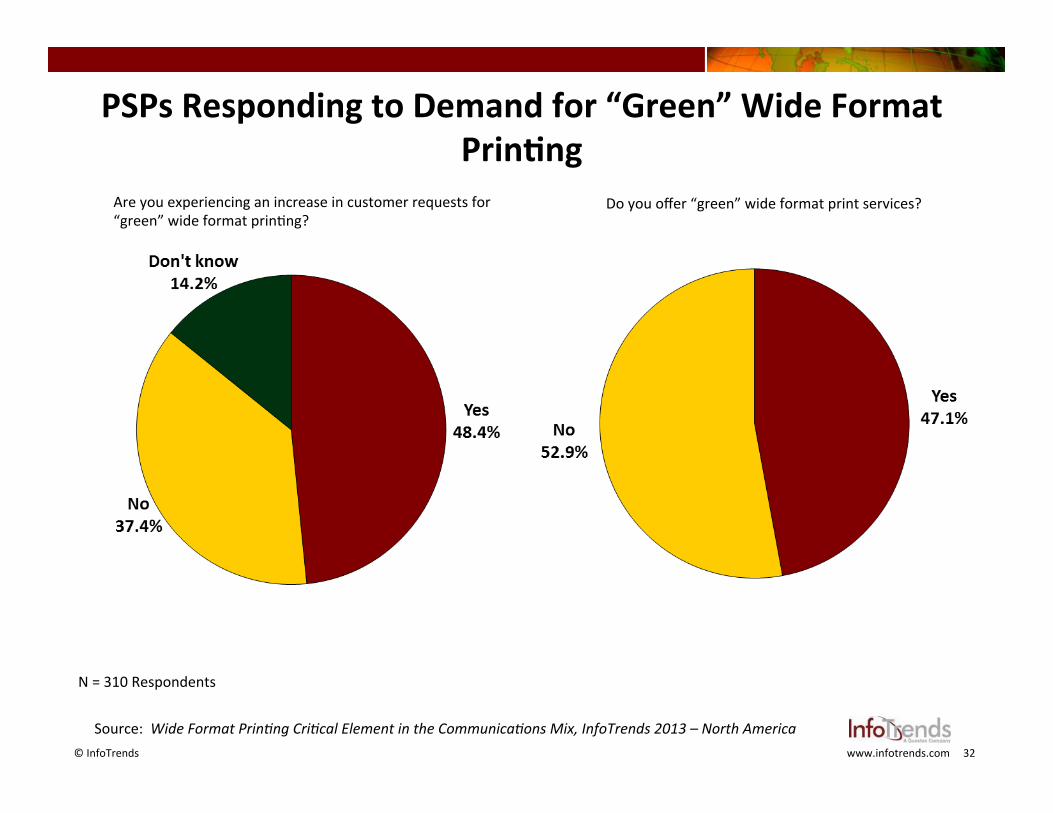

PSPs Responding to Demand for “Green” Wide Format PrinPng

Are you experiencing an increase in customer requests for “green” wide format prinOng?

N = 310 Respondents

Do you offer “green” wide format print services?

Source: Wide Format Prin'ng Cri'cal Element in the Communica'ons Mix, InfoTrends 2013 – North America

33 © InfoTrends www.infotrends.com

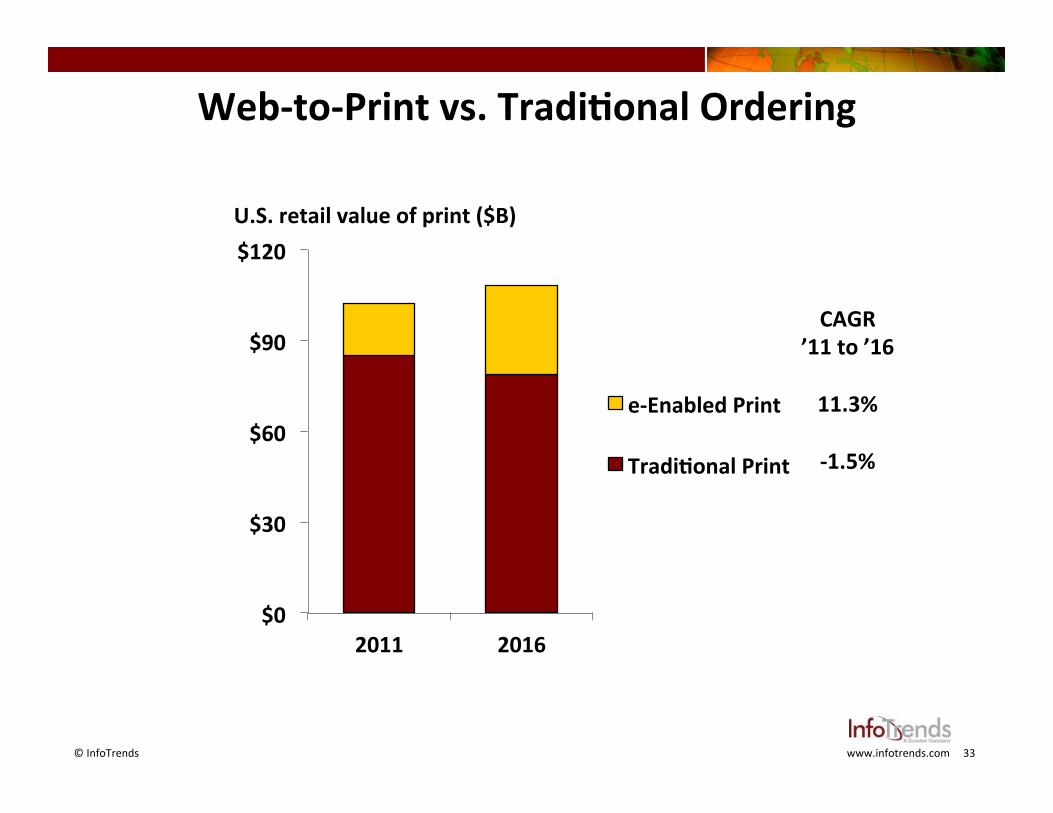

Web-‐to-‐Print vs. TradiPonal Ordering

$0

$30

$60

$90

$120

2011 2016

e-‐Enabled Print

TradiPonal Print

CAGR ’11 to ’16

11.3%

-‐1.5%

U.S. retail value of print ($B)

34 © InfoTrends www.infotrends.com

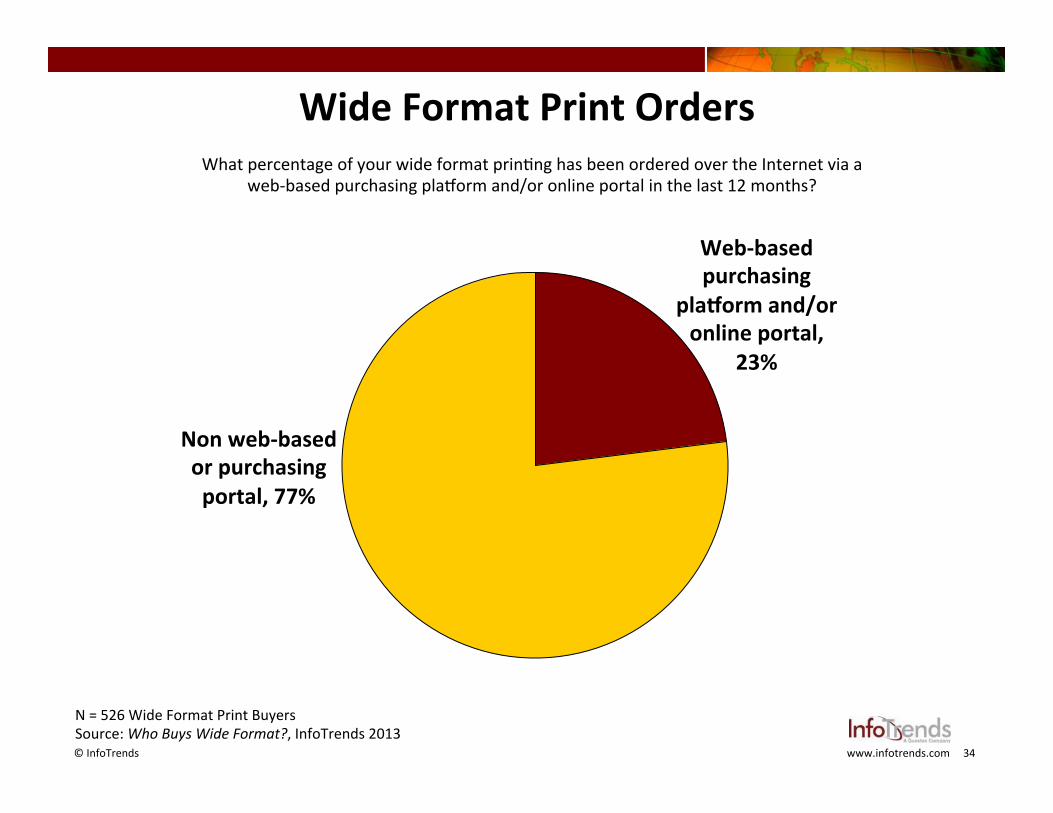

Wide Format Print Orders

Web-‐based purchasing

plaworm and/or online portal,

23%

Non web-‐based or purchasing portal, 77%

N = 526 Wide Format Print Buyers Source: Who Buys Wide Format?, InfoTrends 2013

What percentage of your wide format prinOng has been ordered over the Internet via a web-‐based purchasing plalorm and/or online portal in the last 12 months?

35 © InfoTrends www.infotrends.com

www.858graphics.com

Providers Move to Online Ordering

36 © InfoTrends www.infotrends.com

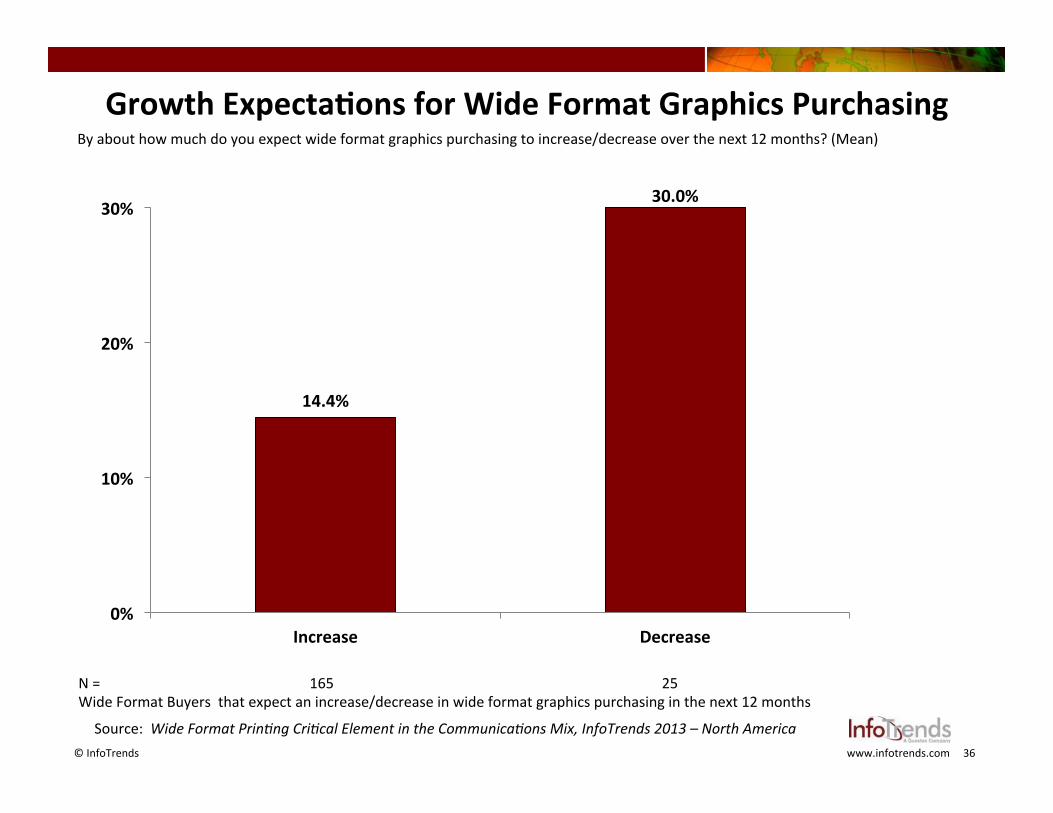

14.4%

30.0%

0%

10%

20%

30%

Increase Decrease

Growth ExpectaPons for Wide Format Graphics Purchasing By about how much do you expect wide format graphics purchasing to increase/decrease over the next 12 months? (Mean)

N = 165 25 Wide Format Buyers that expect an increase/decrease in wide format graphics purchasing in the next 12 months

Source: Wide Format Prin'ng Cri'cal Element in the Communica'ons Mix, InfoTrends 2013 – North America

37 © InfoTrends www.infotrends.com

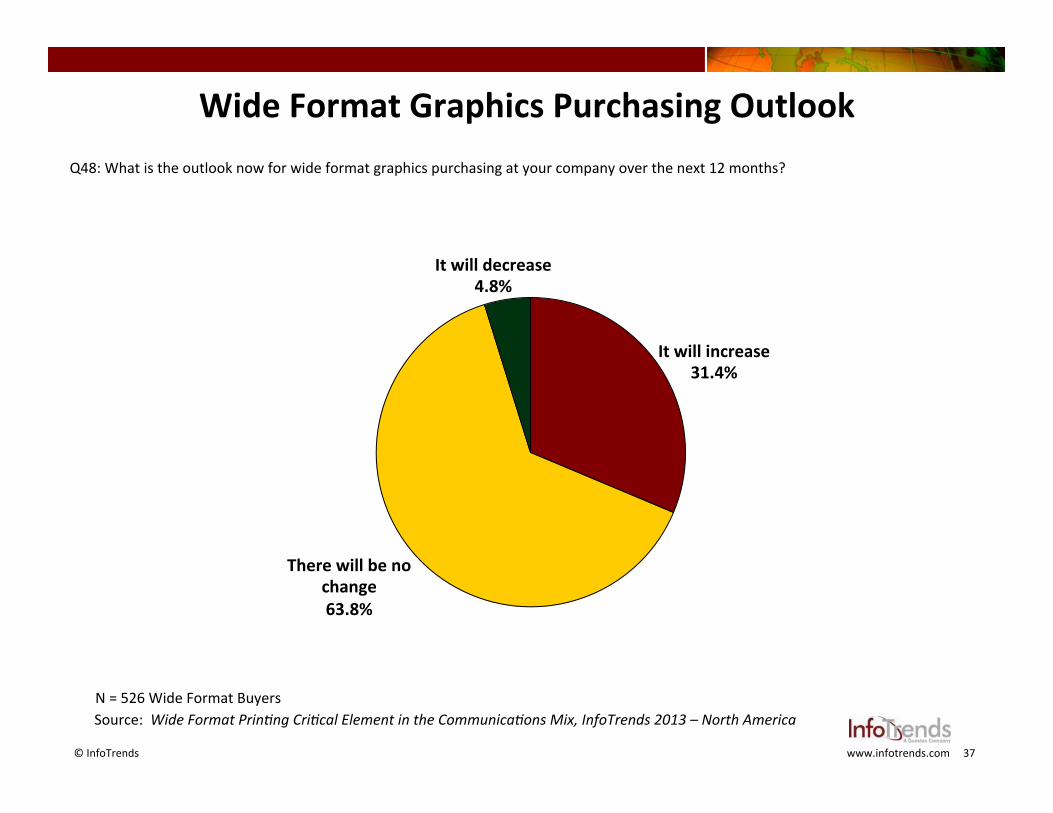

Wide Format Graphics Purchasing Outlook

It will increase 31.4%

There will be no change 63.8%

It will decrease 4.8%

Q48: What is the outlook now for wide format graphics purchasing at your company over the next 12 months?

N = 526 Wide Format Buyers Source: Wide Format Prin'ng Cri'cal Element in the Communica'ons Mix, InfoTrends 2013 – North America

38 © InfoTrends www.infotrends.com

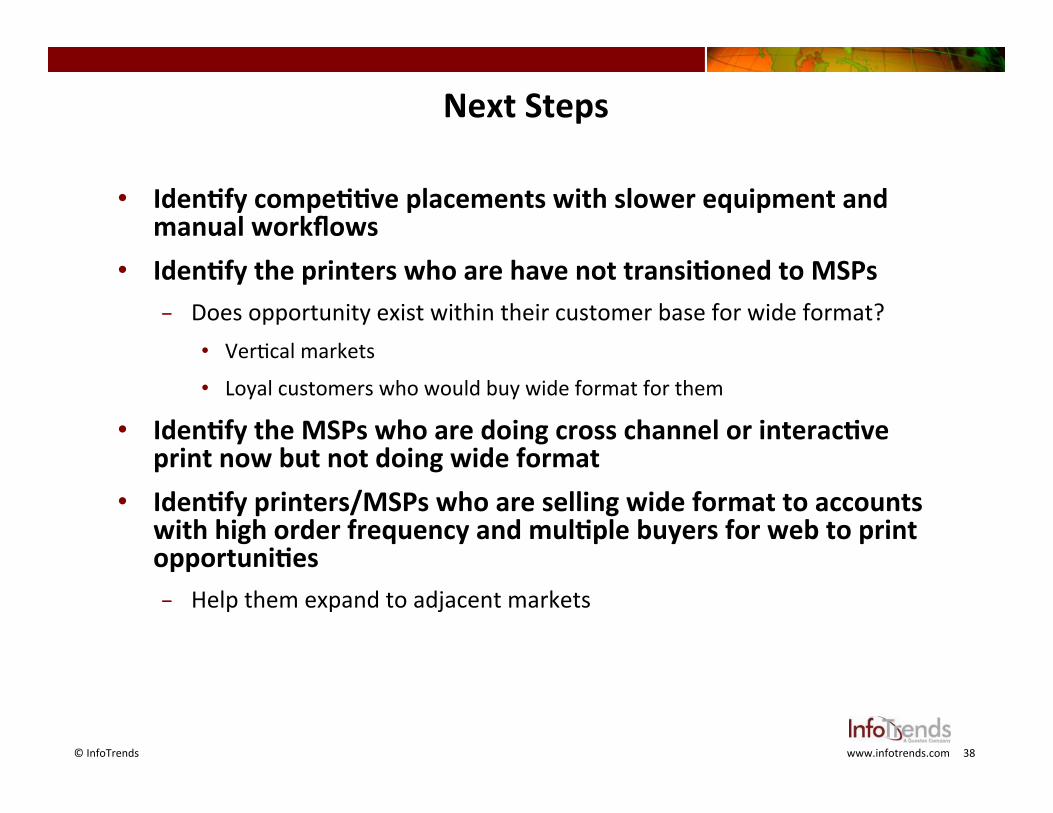

Next Steps

• IdenPfy compePPve placements with slower equipment and manual workflows

• IdenPfy the printers who are have not transiPoned to MSPs − Does opportunity exist within their customer base for wide format?

• VerOcal markets

• Loyal customers who would buy wide format for them

• IdenPfy the MSPs who are doing cross channel or interacPve print now but not doing wide format

• IdenPfy printers/MSPs who are selling wide format to accounts with high order frequency and mulPple buyers for web to print opportuniPes − Help them expand to adjacent markets

39 © InfoTrends www.infotrends.com

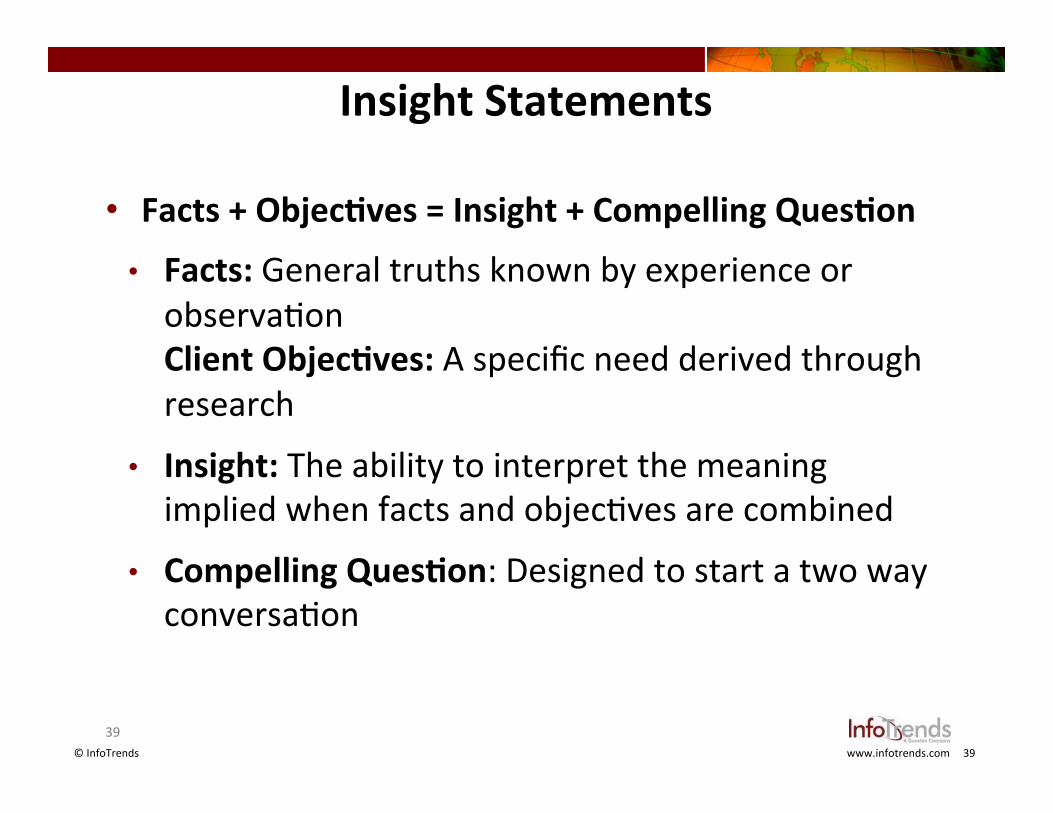

Insight Statements

• Facts + ObjecPves = Insight + Compelling QuesPon

• Facts: General truths known by experience or observaOon Client ObjecPves: A specific need derived through research

• Insight: The ability to interpret the meaning implied when facts and objecOves are combined

• Compelling QuesPon: Designed to start a two way conversaOon

39

40 © InfoTrends www.infotrends.com

Lead to, Not With

Pitch

41 © InfoTrends www.infotrends.com

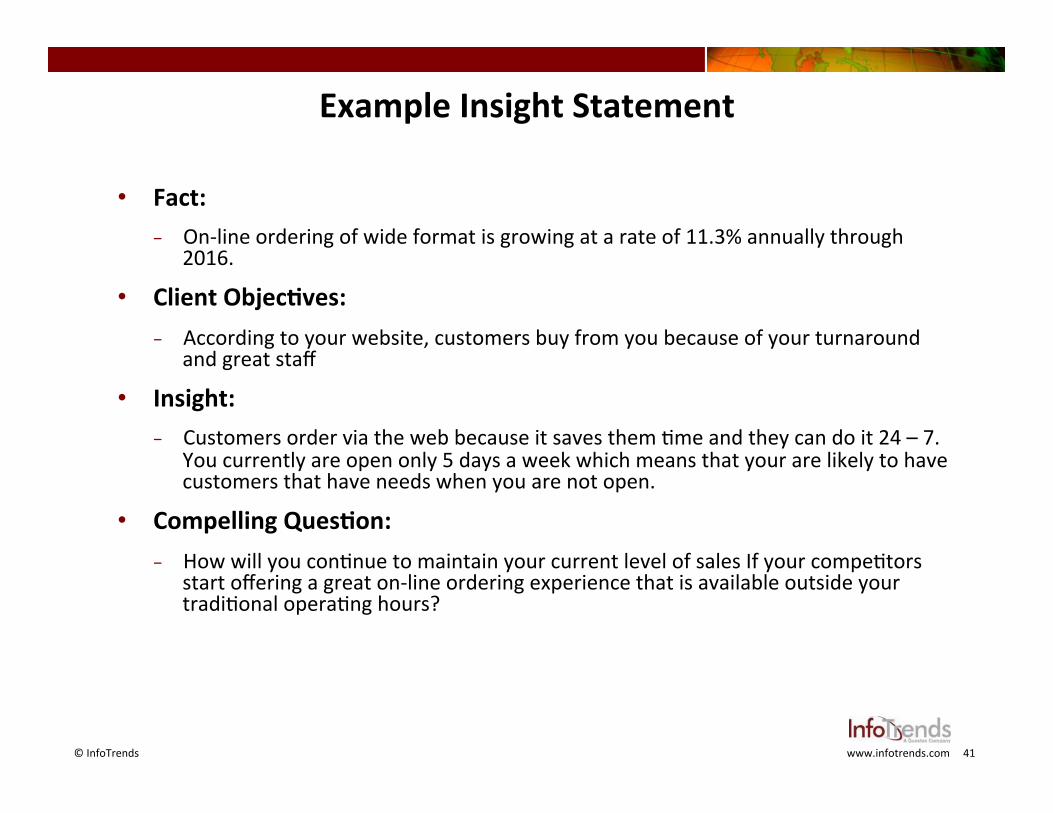

Example Insight Statement

• Fact: − On-‐line ordering of wide format is growing at a rate of 11.3% annually through

2016.

• Client ObjecPves: − According to your website, customers buy from you because of your turnaround

and great staff

• Insight: − Customers order via the web because it saves them Ome and they can do it 24 – 7.

You currently are open only 5 days a week which means that your are likely to have customers that have needs when you are not open.

• Compelling QuesPon: − How will you conOnue to maintain your current level of sales If your compeOtors

start offering a great on-‐line ordering experience that is available outside your tradiOonal operaOng hours?

42 © InfoTrends www.infotrends.com

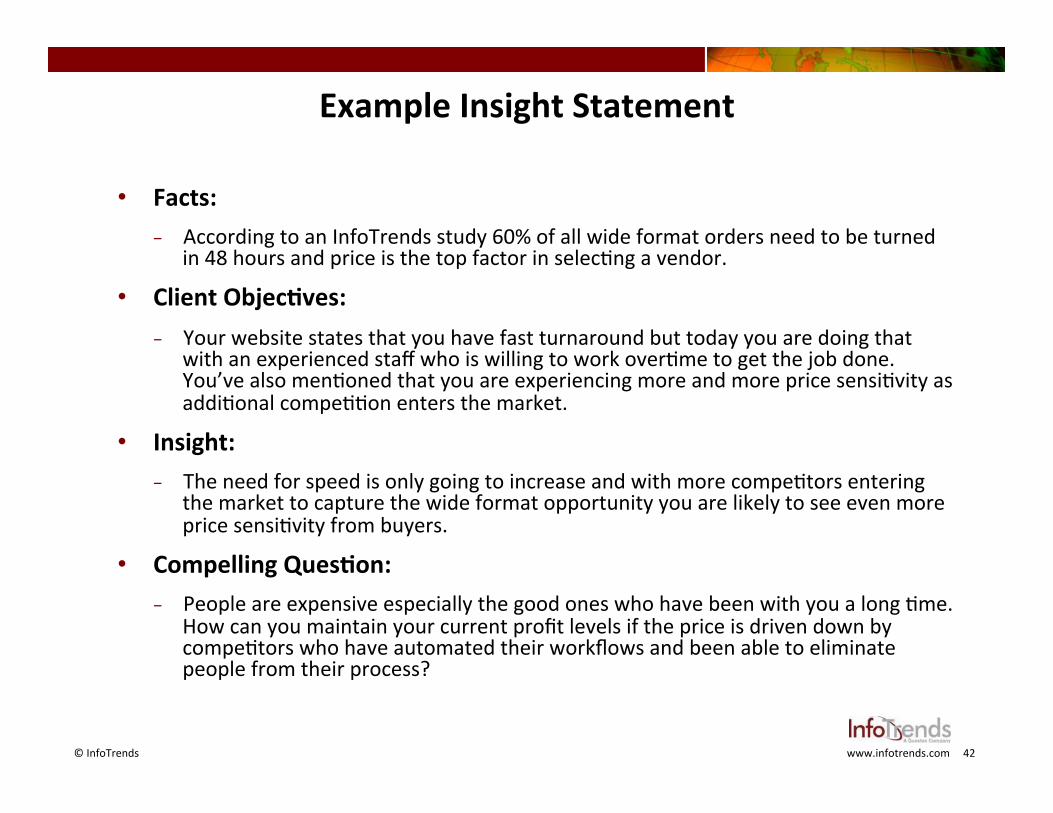

Example Insight Statement

• Facts: − According to an InfoTrends study 60% of all wide format orders need to be turned

in 48 hours and price is the top factor in selecOng a vendor.

• Client ObjecPves: − Your website states that you have fast turnaround but today you are doing that

with an experienced staff who is willing to work overOme to get the job done. You’ve also menOoned that you are experiencing more and more price sensiOvity as addiOonal compeOOon enters the market.

• Insight: − The need for speed is only going to increase and with more compeOtors entering

the market to capture the wide format opportunity you are likely to see even more price sensiOvity from buyers.

• Compelling QuesPon: − People are expensive especially the good ones who have been with you a long Ome.

How can you maintain your current profit levels if the price is driven down by compeOtors who have automated their workflows and been able to eliminate people from their process?

43 © InfoTrends www.infotrends.com

Example Insight Statement

• Facts: In 2011 only 20% of buyers were incorporaPng interacPve elements into their wide format prinPng. Today that number has grown to 43%.

• Client ObjecPves: Your customers are non profits and you are adding a lot of value in helping them increase response rates with personalized urls and landing pages.

• Insight: The reason your have loyal non profit customers is because you are helping them grow revenue and retain donors. These same non profits are also hosPng events and they use signage to promote the events and during the events. I think that by adding your cross channel experPse to wide format you could help increase the success of your customer’s events and also collect vital data through interacPve signage that could enhance their fundraising in the other channels like Direct mail

• Compelling QuesPons: Would you like to explore the financial opportunity that might exist if you added wide format to your service offering?

44 © InfoTrends www.infotrends.com

Go Forth and Sell!