Embed Size (px)

Citation preview

capitalideasonline.com

CREATING SHAREHOLDER VALUE DURING ECONOMY DOWNTURN

WITH VBM TOOLS AND STRATEGIES

Chetan J Parikh

capitalideasonline.com

• Owners of invested capital

• Stewards of invested capital

• Adapting to economic paradigms of the 21st Century

• The role of finance in determining shareholder value

• Cost leadership strategy and supporting tactics

Creating Shareholder Value

~Introduction

Themes

capitalideasonline.com

Owners of Invested Capital- The Shareholders

capitalideasonline.com

Shrinking competitive advantage periods (CAPs) means that an investor has to understand

– The dynamics of organizational change – The mental models that owners need to have to keep up with change

Creating Shareholder Value

~Owners of Invested Capital

What does ownership mean?

capitalideasonline.com

• Owners must demonstrate – Rational allocation of capital– Reduction of fundamental business risks

• Develop systems thinking based on feedback loops

Creating Shareholder Value

~Owners of Invested Capital

Competences that owners need

capitalideasonline.com

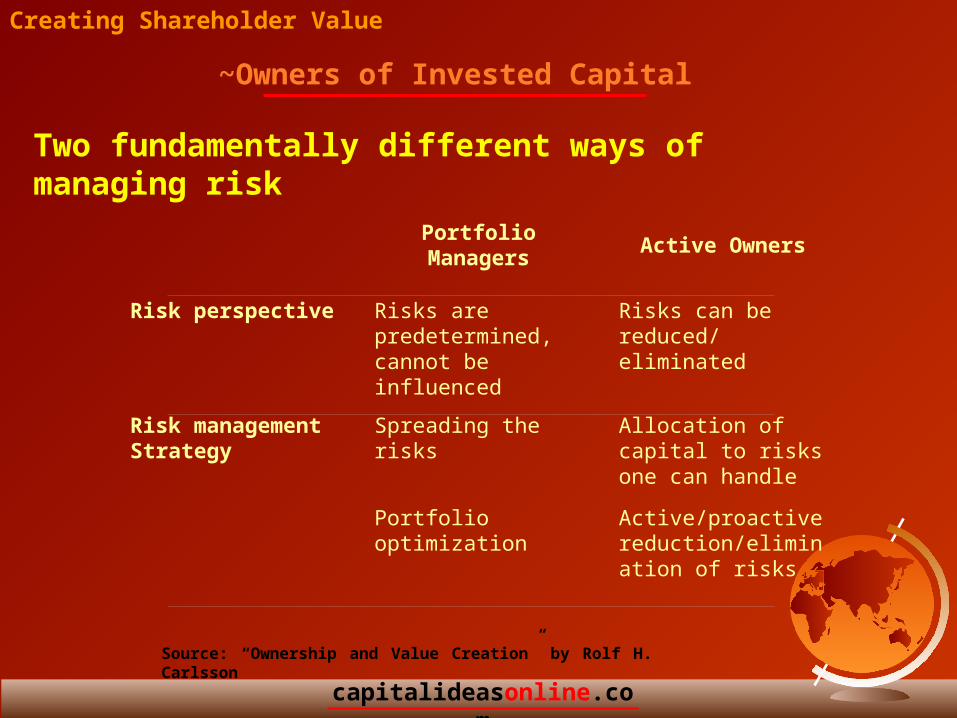

Portfolio Managers

Active Owners

Risk perspective Risks are predetermined, cannot be influenced

Risks can be reduced/ eliminated

Risk management Strategy

Spreading the risks Allocation of capital to risks one can handle

Portfolio optimization

Active/proactive reduction/elimination of risks

Source: “Ownership and Value Creation” by Rolf H. Carlsson

Creating Shareholder Value

~Owners of Invested Capital

Two fundamentally different ways of managing risk

capitalideasonline.com

Source: ‘Ownership and Value Creation’ by Rolf H. Carlsson

Creating Shareholder Value

Through: Affecting market developments Superior competitive capability

Dominance Market leadership

Organizational Learning When the competitive situation changesstructurallyDeveloping a whole new business

Planning ForecastingContingency planning

‘Protection’ for Mobilizing power – political, military,example mafia through Forming cartels

~Owners of Invested Capital

Different ways of reducing / eliminating business-related risk

capitalideasonline.com

Stewards of Invested Capital- The Corporate Managers

capitalideasonline.com

Two major differences between CEOs and other employees

– Standards for measuring CEO’s performance are easy to manipulate, makes a CEOs performance harder to measure

– Relations between CEOs and board of directors are very congenial

Creating Shareholder Value

~Stewards of Invested Capital

Why is CEO performance difficult to measure?

capitalideasonline.com

• Short term imperatives have forced CEOs to

– Meet the quarterly numbers– Have a wrong implicit valuation model– Disjointed the interests of shareholders from those of

other stakeholders

Creating Shareholder Value

~Stewards of Invested Capital

Long term must be balanced with the short term

capitalideasonline.com

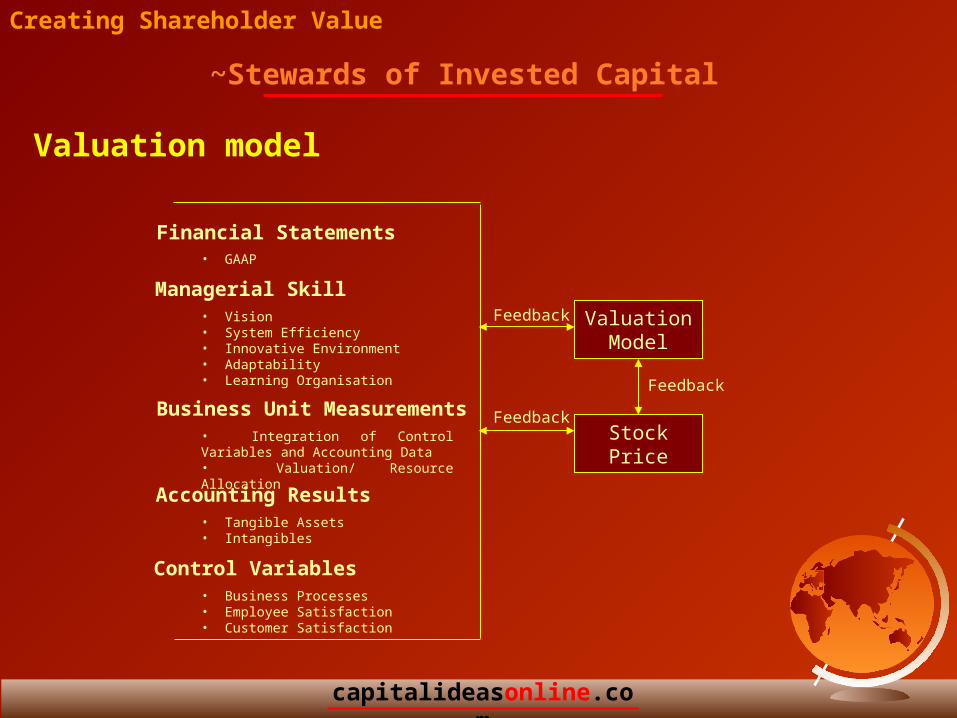

Valuation Model

Stock Price

Financial Statements

Managerial Skill

Business Unit Measurements

Accounting Results

Control Variables• Business Processes• Employee Satisfaction • Customer Satisfaction

• Tangible Assets• Intangibles

• Integration of Control Variables and Accounting Data• Valuation/ Resource Allocation

• Vision• System Efficiency• Innovative Environment• Adaptability• Learning Organisation

• GAAP

Feedback

Feedback

Feedback

Creating Shareholder Value

~Stewards of Invested Capital

Valuation model

capitalideasonline.com

Adapting to economic paradigms of the 21st century

capitalideasonline.com

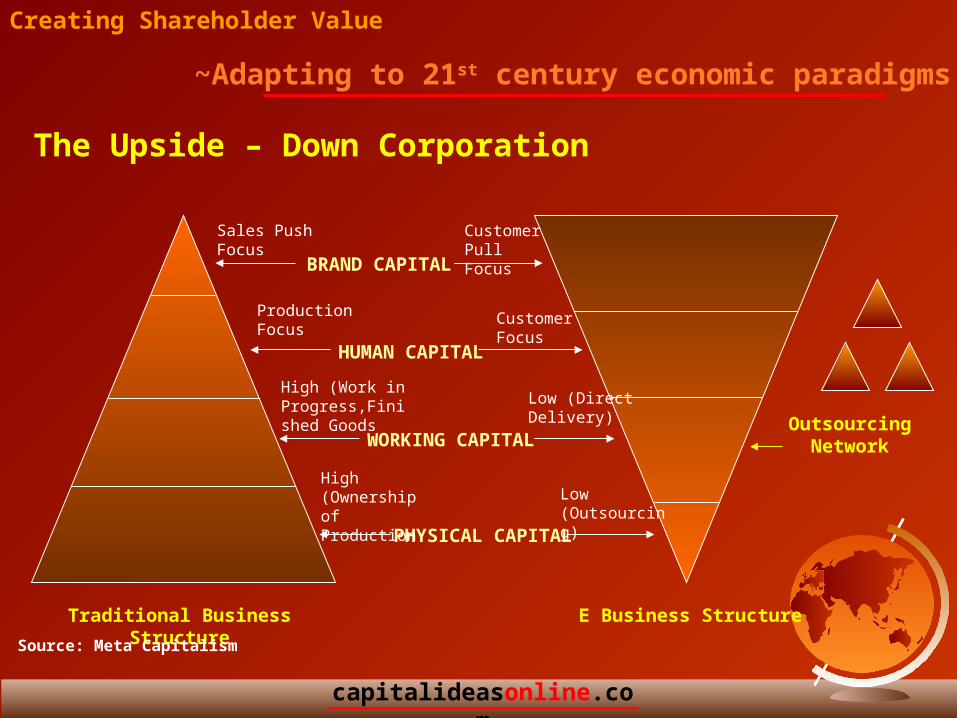

Traditional Business Structure E Business Structure

Creating Shareholder Value

BRAND CAPITAL

HUMAN CAPITAL

WORKING CAPITAL

PHYSICAL CAPITAL

Outsourcing Network

Sales Push Focus

Production Focus

High (Work in Progress,Finished Goods

High (Ownership of Production

Customer Pull Focus

Customer Focus

Low (Direct Delivery)

Low (Outsourcing)

~Adapting to 21st century economic paradigms

The Upside – Down Corporation

Source: Meta Capitalism

capitalideasonline.com

Creating Shareholder Value

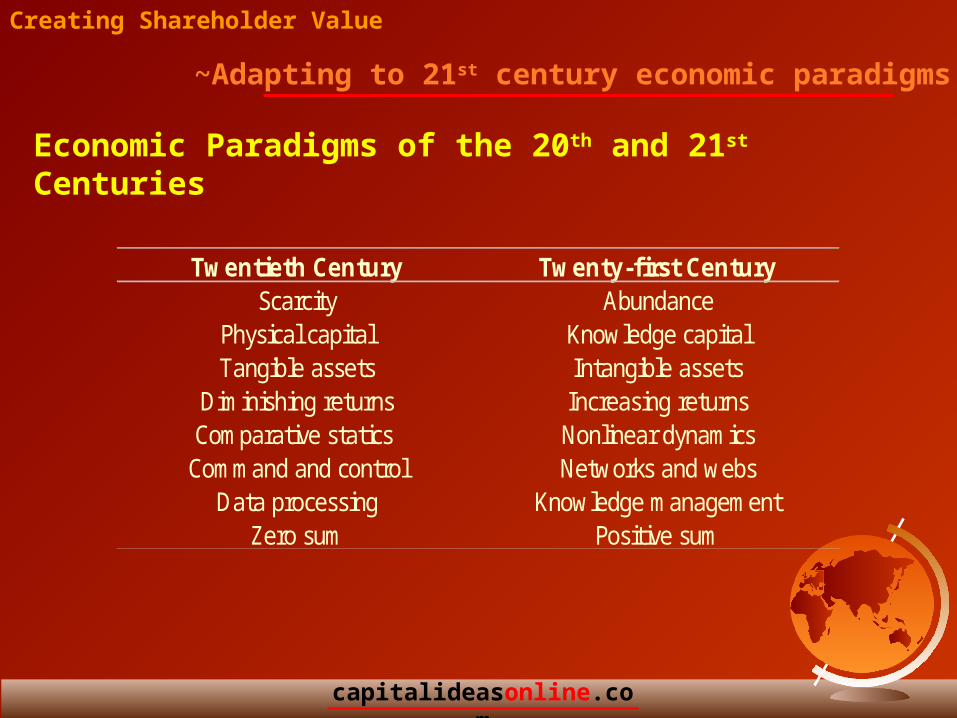

Twentieth Century Twenty-first CenturyScarcity Abundance

Physical capital Knowledge capitalTangible assets Intangible assets

Diminishing returns Increasing returnsComparative statics Nonlinear dynamicsCommand and control Networks and webs

Data processing Knowledge managementZero sum Positive sum

~Adapting to 21st century economic paradigms

Economic Paradigms of the 20th and 21st Centuries

capitalideasonline.com

Creating Shareholder Value

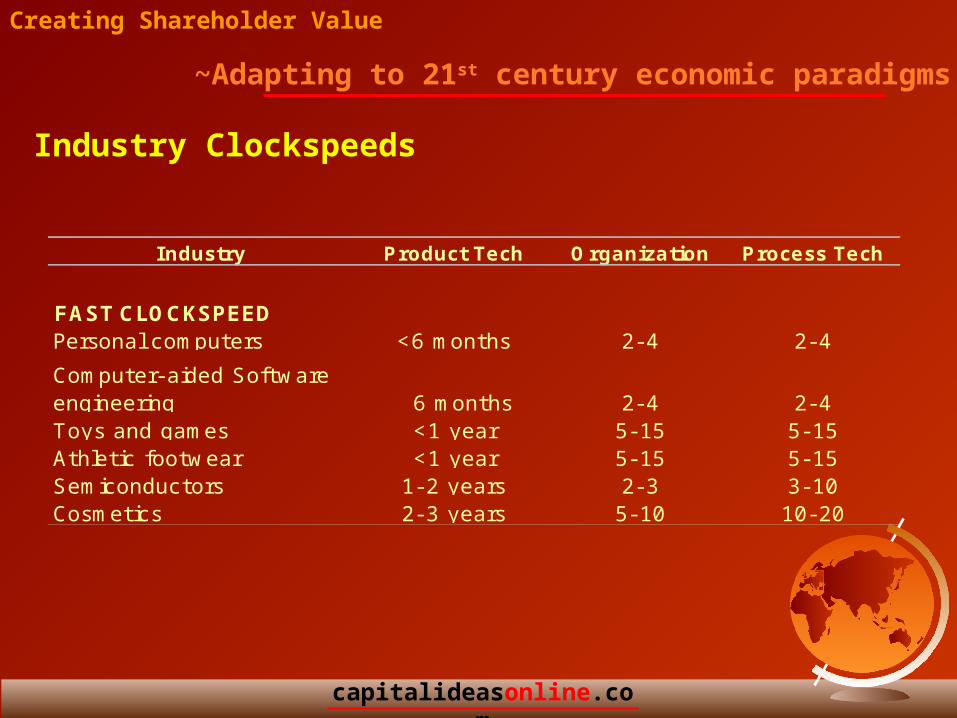

Industry Product Tech Organization Process Tech

FAST CLOCKSPEEDPersonal computers <6 months 2- 4 2- 4

Computer- aided Software engineering 6 months 2- 4 2- 4Toys and games <1 year 5- 15 5- 15Athletic footwear <1 year 5- 15 5- 15Semiconductors 1- 2 years 2- 3 3- 10Cosmetics 2- 3 years 5- 10 10- 20

~Adapting to 21st century economic paradigms

Industry Clockspeeds

capitalideasonline.com

Creating Shareholder Value

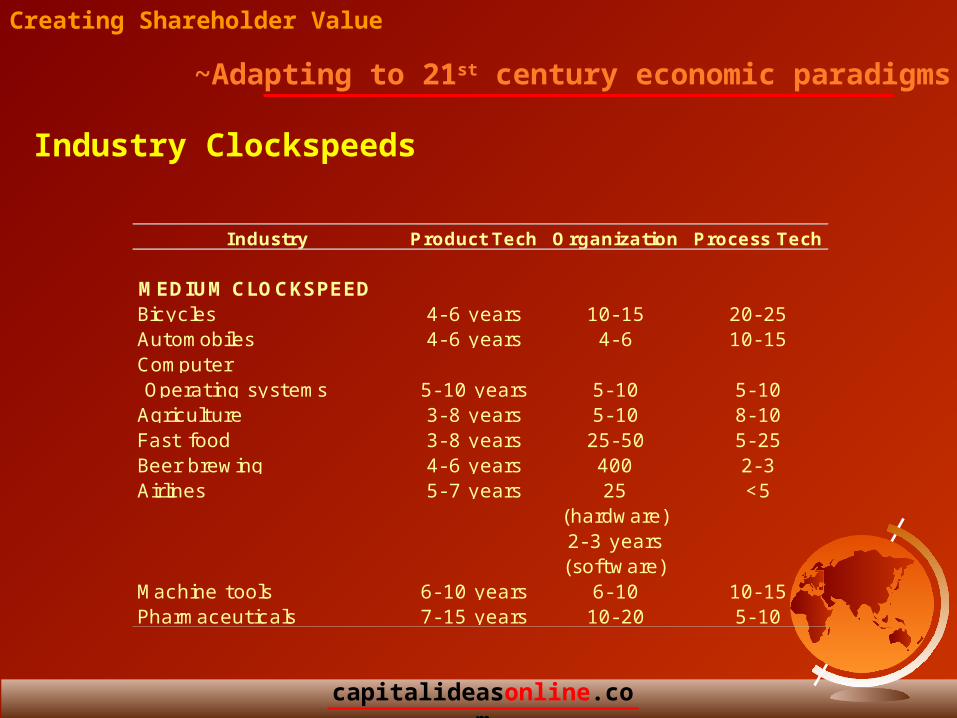

Industry Product Tech Organization Process Tech

MEDIUM CLOCKSPEEDBicycles 4- 6 years 10- 15 20- 25Automobiles 4- 6 years 4- 6 10- 15Computer Operating systems 5- 10 years 5- 10 5- 10Agriculture 3- 8 years 5- 10 8- 10Fast food 3- 8 years 25- 50 5- 25Beer brewing 4- 6 years 400 2- 3Airlines 5- 7 years 25 <5

(hardware)2- 3 years(software)

Machine tools 6- 10 years 6- 10 10- 15Pharmaceuticals 7- 15 years 10- 20 5- 10

~Adapting to 21st century economic paradigms

Industry Clockspeeds

capitalideasonline.com

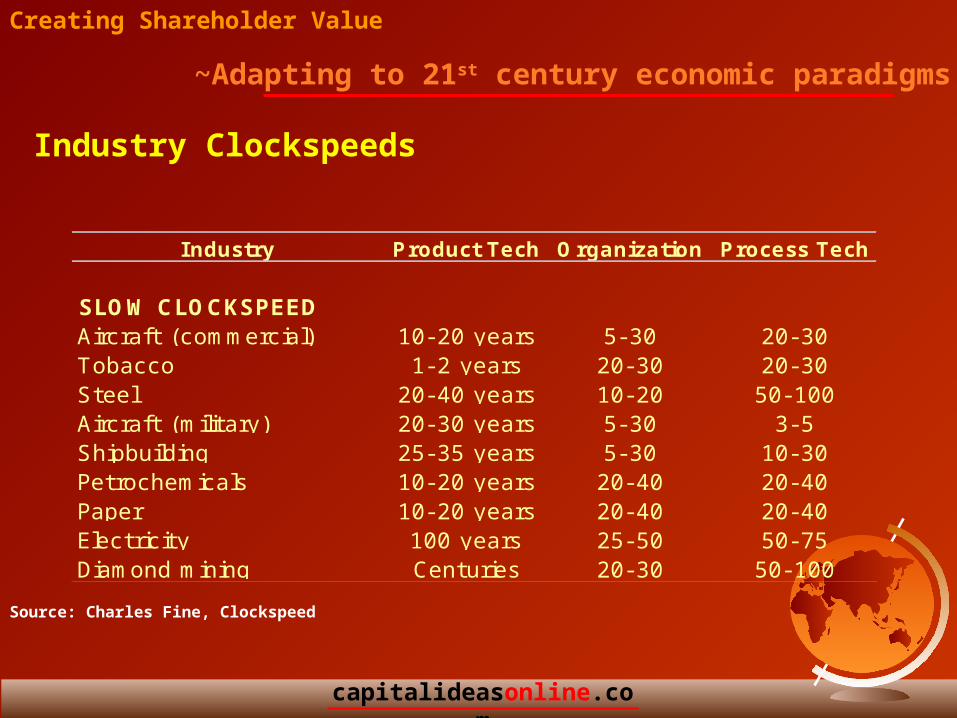

Source: Charles Fine, Clockspeed

Creating Shareholder Value

Industry Product Tech Organization Process Tech

SLOW CLOCKSPEEDAircraft (commercial) 10- 20 years 5- 30 20- 30Tobacco 1- 2 years 20- 30 20- 30Steel 20- 40 years 10- 20 50- 100Aircraft (military) 20- 30 years 5- 30 3- 5Shipbuilding 25- 35 years 5- 30 10- 30Petrochemicals 10- 20 years 20- 40 20- 40Paper 10- 20 years 20- 40 20- 40Electricity 100 years 25- 50 50- 75Diamond mining Centuries 20- 30 50- 100

~Adapting to 21st century economic paradigms

Industry Clockspeeds

capitalideasonline.com

The role of Finance in Determining Shareholder Value

capitalideasonline.com

Creating Shareholder Value

~Using Finance to Determine Shareholder Value

“What remains of his profits after deducting interest on his capital at the current rate may be called his earnings at undertaking or management”.

- Alfred Marshall

A

capitalideasonline.com

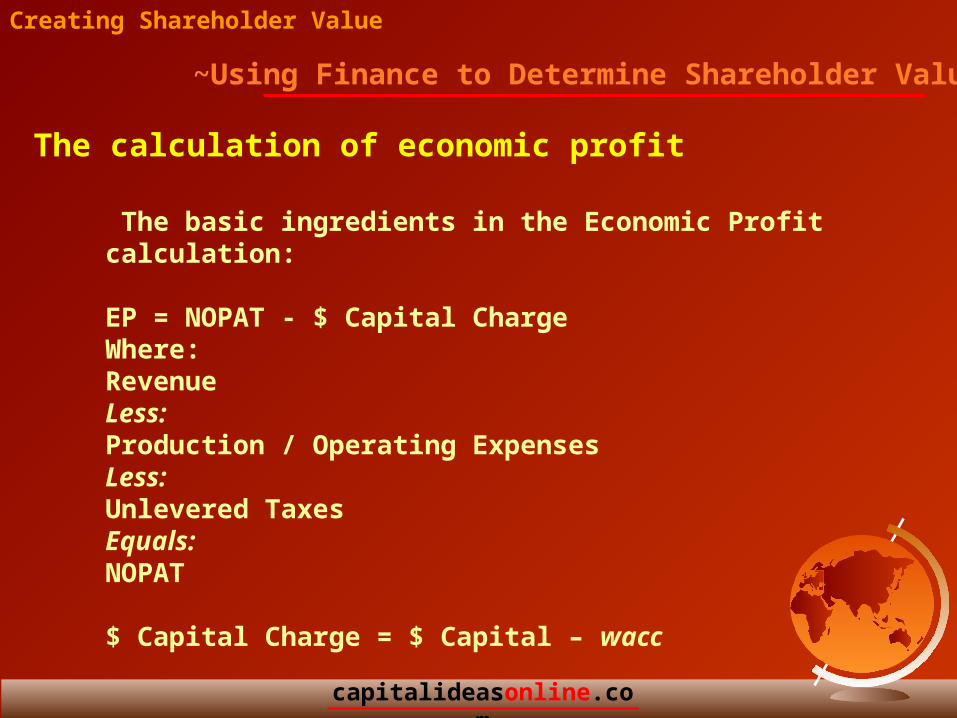

The basic ingredients in the Economic Profit calculation:

EP = NOPAT - $ Capital ChargeWhere:RevenueLess:Production / Operating ExpensesLess:Unlevered Taxes Equals:NOPAT $ Capital Charge = $ Capital – wacc

~Using Finance to Determine Shareholder Value

Creating Shareholder Value

The calculation of economic profit

capitalideasonline.com

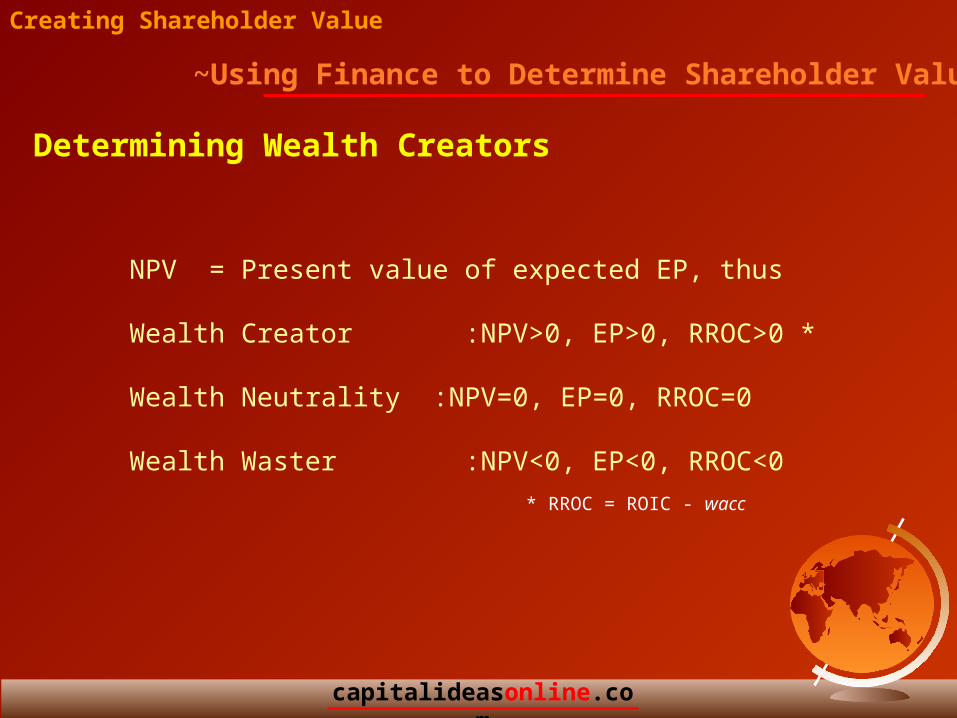

NPV = Present value of expected EP, thus

Wealth Creator :NPV>0, EP>0, RROC>0 * Wealth Neutrality :NPV=0, EP=0, RROC=0 Wealth Waster :NPV<0, EP<0, RROC<0

* RROC = ROIC - wacc

~Using Finance to Determine Shareholder Value

Creating Shareholder Value

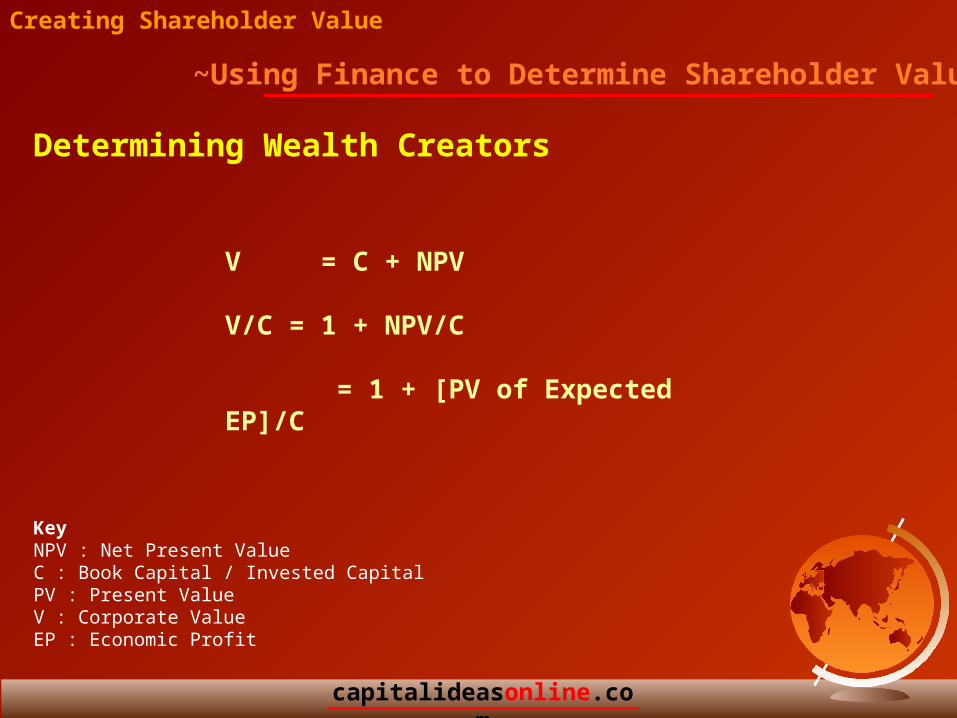

Determining Wealth Creators

capitalideasonline.com

~Using Finance to Determine Shareholder Value

Creating Shareholder Value

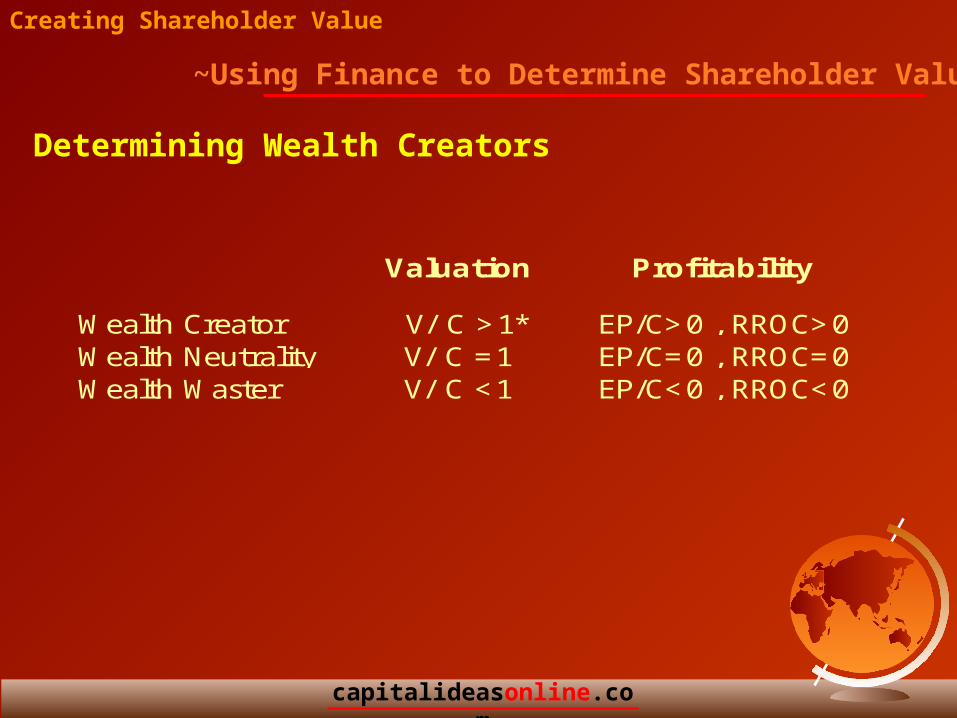

Determining Wealth Creators

V = C + NPV

V/C = 1 + NPV/C

= 1 + [PV of Expected EP]/C

KeyNPV : Net Present ValueC : Book Capital / Invested CapitalPV : Present ValueV : Corporate ValueEP : Economic Profit

capitalideasonline.com

~Using Finance to Determine Shareholder Value

Creating Shareholder Value

Determining Wealth Creators

Valuation Profitability

Wealth Creator V/ C >1* EP/C>0 , RROC>0Wealth Neutrality V/ C =1 EP/C=0 , RROC=0Wealth Waster V/ C <1 EP/C<0 , RROC<0

capitalideasonline.com

~Using Finance to Determine Shareholder Value

Creating Shareholder Value

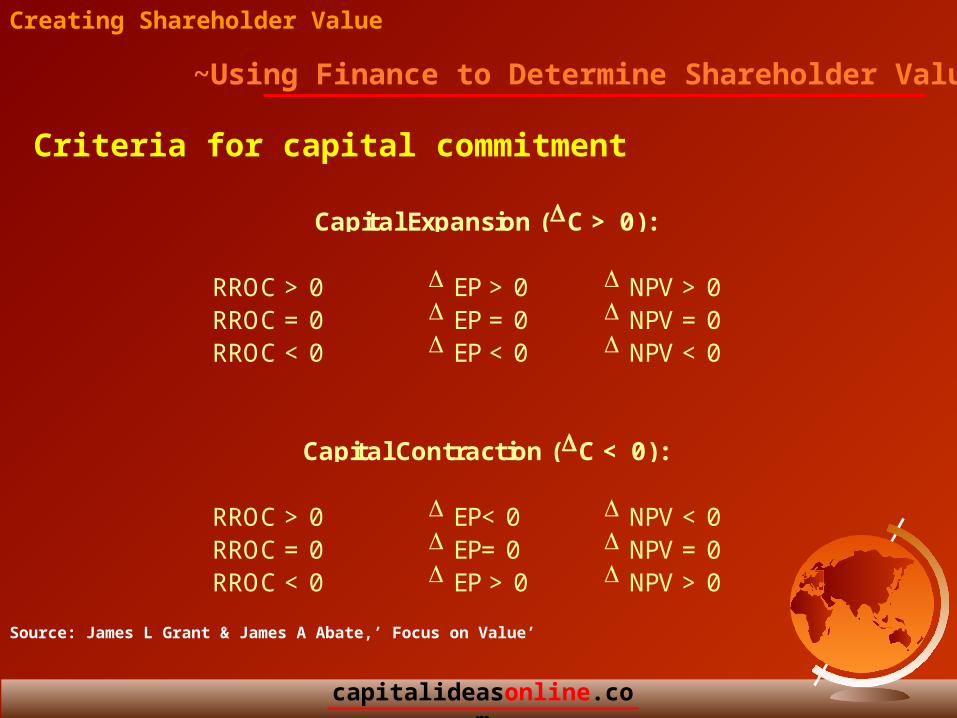

Criteria for capital commitment

RROC > 0 EP > 0 NPV > 0RROC = 0 EP = 0 NPV = 0RROC < 0 EP < 0 NPV < 0

RROC > 0 EP< 0 NPV < 0RROC = 0 EP= 0 NPV = 0RROC < 0 EP > 0 NPV > 0

Capital Expansion (C > 0):

Capital Contraction (C < 0):

Source: James L Grant & James A Abate,’ Focus on Value’

capitalideasonline.com

Source :James L Grant &James A Abate,’Focus on Value’

Creating Shareholder Value

~Using Finance to Determine Shareholder Value

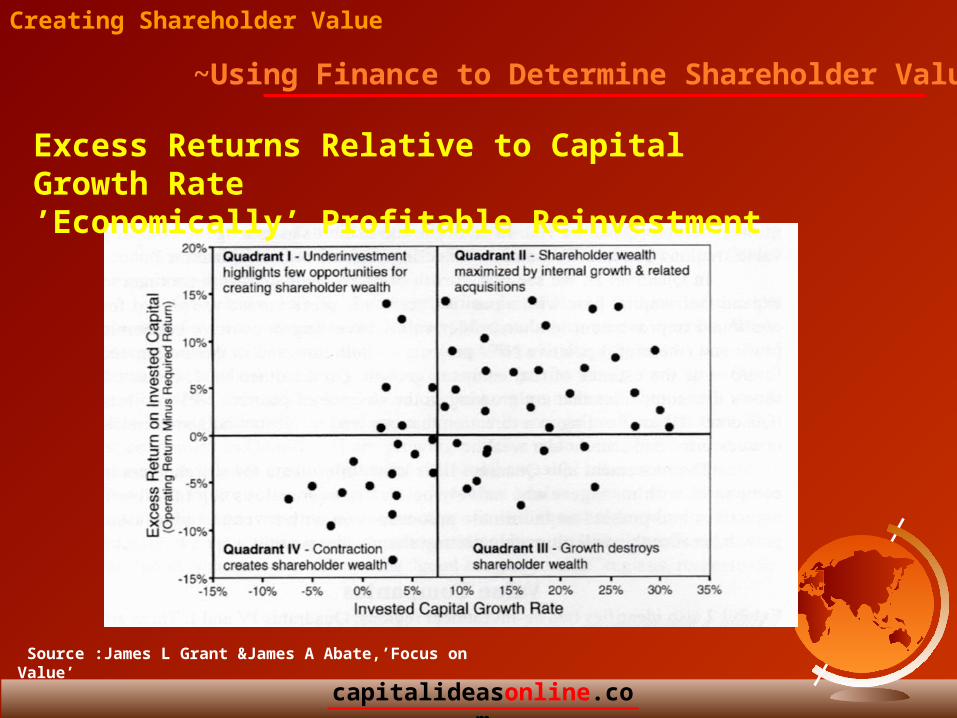

Excess Returns Relative to Capital Growth Rate’Economically’ Profitable Reinvestment

capitalideasonline.com

• Is the company a major force in a growing market?

• Is the company holding or increasing its shares on those segments?

• Is it resulting in increasing cash flows?

• Is the cash flow being used in a wise manner?

• Does the management walk the talk?

Creating Shareholder ValueCreating Shareholder Value

~Using Finance to Determine Shareholder Value

Questions Shareholders Ask..

capitalideasonline.com

Cost Leadership and Supporting Tactics

capitalideasonline.com

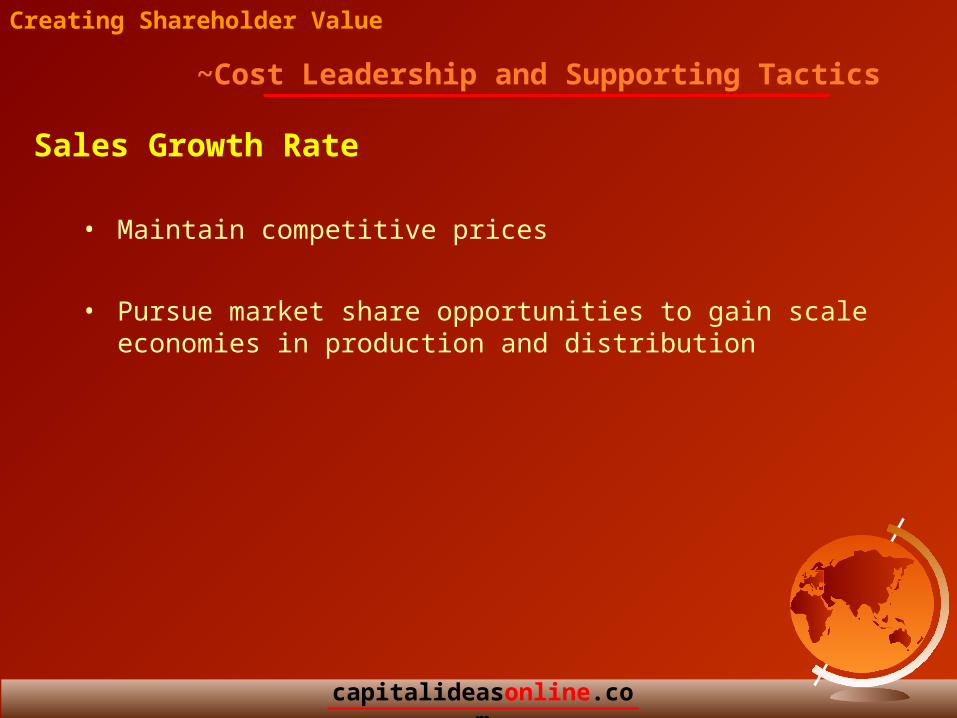

• Maintain competitive prices

• Pursue market share opportunities to gain scale economies in production and distribution

Creating Shareholder Value

~Cost Leadership and Supporting Tactics

Sales Growth Rate

capitalideasonline.com

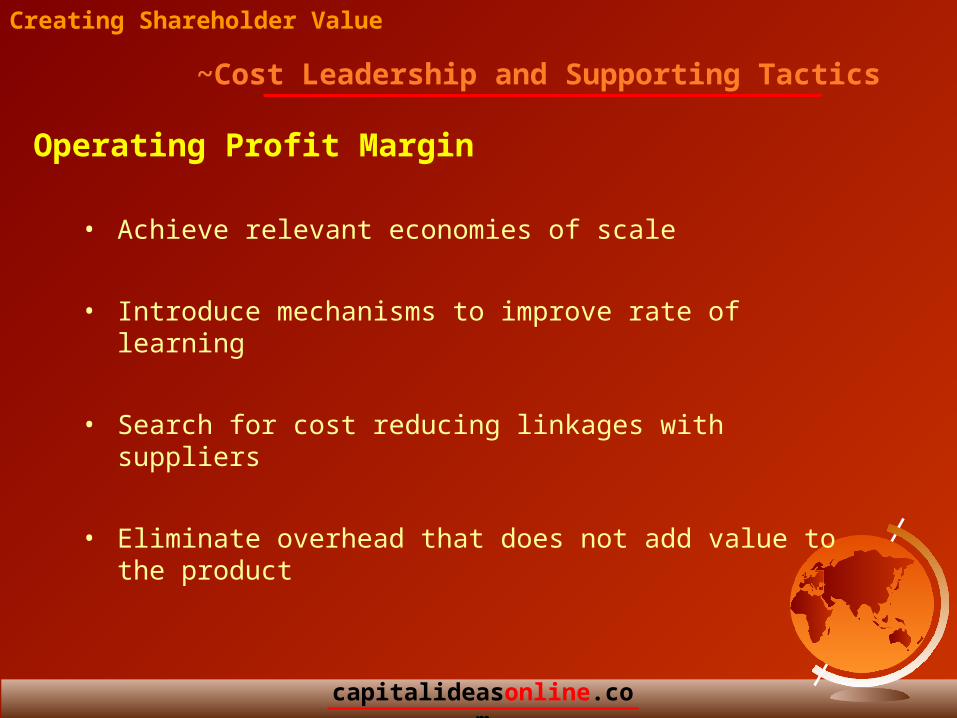

• Achieve relevant economies of scale

• Introduce mechanisms to improve rate of learning

• Search for cost reducing linkages with suppliers

• Eliminate overhead that does not add value to the product

Creating Shareholder Value

~Cost Leadership and Supporting Tactics

Operating Profit Margin

capitalideasonline.com

• Minimise cash balance

• Reduce accounts receivables

• Minimise inventory without impairing customer service

Creating Shareholder Value

~Cost Leadership and Supporting Tactics

Working Capital Investment

capitalideasonline.com

• Promote policies to increase utilization of fixed assets

• Obtain productivity-increasing assets

• Sell unused fixed assets

• Obtain assets at least cost, e.g. lease versus purchase

Creating Shareholder Value

~Cost Leadership and Supporting Tactics

Fixed Capital Investment

capitalideasonline.com

• Target an optimal capital structure

• Select least-cost debt and equity instruments

• Reduce business risk factors in manner consistent with strategy

Creating Shareholder Value

~Cost Leadership and Supporting Tactics

Cost of Capital

Source: Alfred Rappaport, ‘Creating Shareholder Value’

capitalideasonline.com

Thank You