Embed Size (px)

Citation preview

Capital Punishment?The Challenge of Profitability and

Growth in an Industry and World Awash in Capital

Geneva Association10th Annual Insurance and Finance Seminar

London, UK4 November 2014

Download at: www.iii.org/presentationsRobert P. Hartwig, Ph.D., CPCU, President & Economist

Insurance Information Institute 110 William Street New York, NY 10038Tel: 212.346.5520 Cell: 917.453.1885 [email protected] www.iii.org

2

A World Awash in Capital

2

Too Much of a Good Thing?The Global Glut of Capital is Not

Unique to (Re)Insurance

S&P 500 (Excl. Financials):Cash & Short-Term Investments

3Source: Fact Set Fundamentals.

Holdings of Cash and Liquid Asset Holdings Have Soared Across Virtually All Industries Since the Financial Crisis

Cash and ST investments holdings have nearly doubled since 2007

Hedge Fund Industry: Assets Under Management: 1997–2014:Q21

$118

.2

$143

.1

$188

.9

$236

.6

$1,2

29.0

$1,3

60.7

$1,7

13.1 $2

,136

.8

$1,4

57.9

$1,5

54.1

$1,6

93.9

$1,7

10.0

$1,7

98.7

$2,1

56.7

$2,3

52.6

$321

.9

$505

.5 $825

.6

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14:Q2

Yield Hungry Pension Funds Have Grown Rapidly Since the Financial Crisis, Deploying Oceans of Capital in Industries Across the Globe—

Including the Global Reinsurance Industry

1 Figures for 2011-2013 are as of Q4 for each year.Sources: BarclayHedge: http://www.barclayhedge.com/research/indices/ghs/mum/Hedge_Fund.html; Insurance Information Institute.

($ Billions)

Assets managed by hedge funds are up 63% or $894.7 billion since 2008 to $2.35 trillion

5

8.6% 8.4% 8.0%6.4%

5.5%4.4%

2.3%

9.9%10.1%10.6%11.4%13.3%

14.9%

0%2%4%6%8%

10%12%14%16%

Compound Annual Growth Rate (%)

5

Global Pension Assets Growth,2008 – 2013*

Global pension assets for the top 13 pension

markets reached $31.98 trillion in 2013 (+9.5% from 2012), an

amount equal to 83.4% of these economies

CAGR of pension fund assets in most major pension markets has

been quite strong since the financial crisis

*As of year-end. Source: Towers Watson Global Pensions Asset Study 2014 at: http://www.towerswatson.com/en-US/Insights/IC-Types/Survey-Research-Results/2014/02/Global-Pensions-Asset-Study-2014

Pension Asset Allocation(World’s 7 Largest Pension Markets)

6

Holdings of Cash and Liquid Asset Holdings Have Soared Across Virtually All Industries Since the Financial Crisis

Alternative investment’s

share of assets is up +15 points since 2001 from 5% to

18%

*Australia, Canada, Japan, Netherlands, Switzerland, UK, US. Source: Towers Watson Global Pensions Asset Study 2014 at: http://www.towerswatson.com/en-US/Insights/IC-Types/Survey-Research-Results/2014/02/Global-Pensions-Asset-Study-2014

$0$50

$100$150$200$250$300$350$400$450$500$550$600$650$700$750

75 77 79 81 83 85 87 89 91 93 95 97 99 01 03 05 07 09 11 13

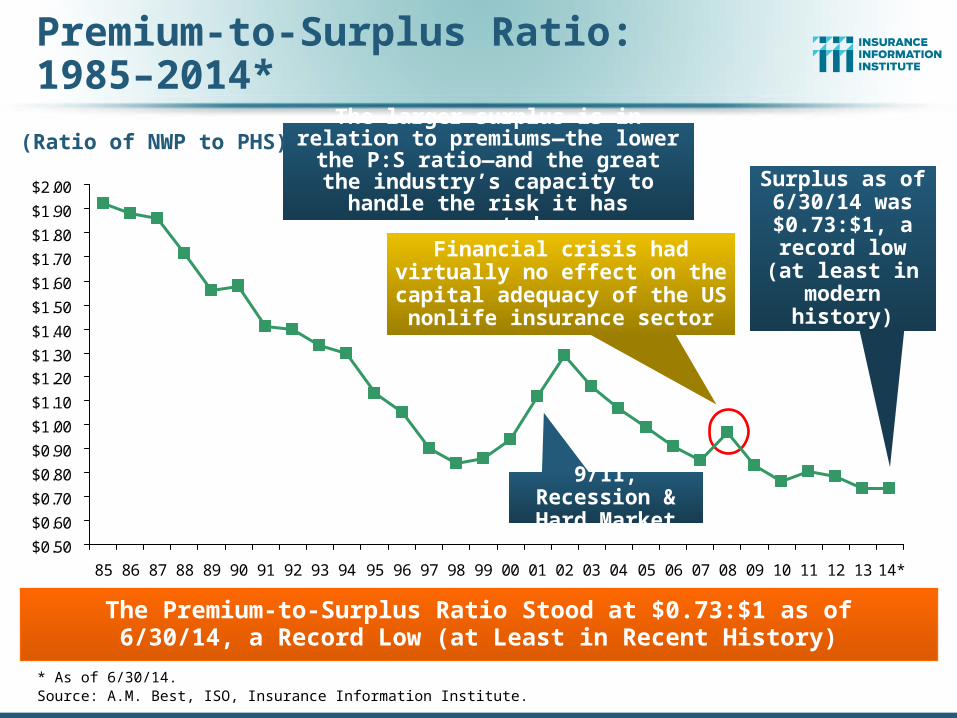

U.S. Policyholder Surplus:1975–2014*

* As of 6/30/14.Source: A.M. Best, ISO, Insurance Information Institute.

“Surplus” is a measure of underwriting capacity. It is analogous to “Owners

Equity” or “Net Worth” in non-insurance organizations

($ Billions)

The Premium-to-Surplus Ratio Stood at $0.73:$1 as of6/30/14, a Near Record Low (at Least in Recent History)

Surplus as of 6/30/14 was a record $671.6, up 2.8% from $653.3 of 12/31/13, and up 53.6% ($234.5B)

from the crisis trough of $437.1B at 3/31/09

$0.50

$0.60

$0.70

$0.80

$0.90

$1.00

$1.10

$1.20

$1.30

$1.40

$1.50

$1.60

$1.70

$1.80

$1.90

$2.00

85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14*

Premium-to-Surplus Ratio:1985–2014*

* As of 6/30/14.Source: A.M. Best, ISO, Insurance Information Institute.

The larger surplus is in relation to premiums—the lower the P:S ratio—

and the great the industry’s capacity to handle the risk it has accepted

(Ratio of NWP to PHS)

The Premium-to-Surplus Ratio Stood at $0.73:$1 as of6/30/14, a Record Low (at Least in Recent History)

Surplus as of 6/30/14 was $0.73:$1, a

record low (at least in modern

history)

9/11, Recession & Hard Market

Financial crisis had virtually no effect on the capital adequacy of the US nonlife insurance sector

10

A World of Low Yields

10

Capital Will Seek Its Highest (Risk-Adjusted) Return

11

U.S. Treasury Security Yields:A Long Downward Trend, 1990–2014*

*Monthly, constant maturity, nominal rates, through September 2014.Sources: Federal Reserve Bank at http://www.federalreserve.gov/releases/h15/data.htm. National Bureau of Economic Research (recession dates); Insurance Information Institute.

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

'90 '91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14

Recession2-Yr Yield10-Yr Yield

Yields on 10-Year U.S. Treasury Notes have been essentially below 5% for a full decade.

Since roughly 80% of P/C bond/cash investments are in 10-year or shorter durations, most P/C insurer portfolios will have low-yielding bonds for years to come.

U.S. Treasury yields plunged to historic lows in 2013. Longer-

term yields have rebounded a bit.

11

Key European Central Bank Interest Rates, 2000 - 2014

12Source: European Central Bank from www.cbrates.com; Insurance Information Institute.

Interest Rates Have Been Slashed by Most Major Central Banks, Igniting a Global Quest for Yield. Reinsurance Is Just One of

Many New Areas “Discovered” by Large Institutional Investors

ECB’s cut its key rate to 0.05% on 4 Sept. 2014

13

Alternative Capital in Global Reinsurance Markets

13

The Global Hunt for Yield Pushed Institutional Investors Into

Countless New Areas—(Re)Insurance Being One of Them

14

Mentions of the Term “Alternative Capital” with “Insurance” or “Reinsurance”

* Estimate is annualized figure based on actual data through September 30, 2014.Source: Insurance Information Institute search of Factiva database.

11 9 20 21 35 52 29 4379 83

55 59116

409

712

0

100

200

300

400

500

600

700

800

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14*

Should the Increased Use of Terms Such as “Alternative Capital,” “Hedge Fund” and “Pension Fund” in Conjunction with a (Re)Insurance Be a Concern

Global Reinsurance Capital (Traditional and Alternative), 2006 - 2014

2014 data is as of June 30, 2014.Source: Aon Benfield Analytics; Insurance Information Institute.

Total reinsurance capital reached a record $570B in 2013, up 68% from

2008.

2006 2007 2008 2009 2010 2011 2012 2013 2014$0

$100

$200

$300

$400

$500

$600

17 22 19 22 24 28 39 50 59

368 388321

378447 428

466 490 511

385410

340400

470 455505

540570

Alternative Capital Traditional Capital Total

(Billions of USD)

But alternative capacity has grown 210% since 2008, to $50B. It has more than doubled in the past three years.

Global Reinsurance Capital Share (Traditional and Alternative), 2006 - 2014

2014 data is as of June 30, 2014.Source: Aon Benfield Analytics; Insurance Information Institute.

2006 2007 2008 2009 2010 2011 2012 2013 2014

-2%

0%

2%

4%

6%

8%

10%

12%

4.6%5.7% 5.9% 5.8% 5.4%

6.5%

8.4%

10.2%

11.5%

Alternative Capital’s Share of Global Reinsurance Capital Has More Than Doubled Since 2010.

Growth in Traditional and Alternative Capital, 2007-2014

2014 reflects growth through June 30 from prior year end.Source: Aon Benfield Analytics; Insurance Information Institute.

Post 2011, alternative capital is

growing four and five times

faster than traditional capital.

2007 2008 2009 2010 2011 2012 2013 2014-20%

-10%

0%

10%

20%

30%

40%

29%

-14%

16%

9%

17%

39%

28%

18%

5%

-17%

18% 18%

-4%

9%5% 4%

Alternative Capital Traditional Capital

(Change from Previous Year)

Japan, NZ quakes, US tornadoes drove

traditional capital slightly lower.

Economic meltdown depleted all forms of capital.

2009-10: Low cat losses, recovering markets fueled tra-

ditional capital growth.

Alternative capital has grown 247% since 2006, vs. 39% growth in traditional capital.

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014$0

$5

$10

$15

$20

$25

$30

Cat Bonds Sidecars ILWs Collateralized Re

(Billions of USD)

Growth of Alternative Capital Structures, 2002 - 2014

2014 data is as of June 30, 2014.Source: Aon Benfield Analytics; Insurance Information Institute.

Collateralize Re’s Growth Has Accelerated in the Past Three Years.

Collateralized Reinsurance and Catastrophe Bonds Currently Dominate the Alternative Capital Market.

ILS: Issuance and Outstanding, 1997- 2014:Q2Risk Capital Amount ($ Millions)

Sources: Artemis.bm, Insurance Information Institute.

71

4.0

74

2.2

82

4.8

1,1

25

.0

96

6.9 2,9

79

.9

3,4

79

.8

5,0

24

.8

4,5

80

.3

6,2

79

.2

7,6

41

.7

6,6

32

.7

2,500.0

1,142.82,388.2

8,2

41

.6

5,6

95

.7

989.5

4,5

94

.5

4,6

44

.5

6,4

41

.5 10

,11

4.5

17

,04

2.9

15

,67

6.8

14

,86

5.5

14

,04

3.6

13

,69

1.1

2,3

78

.9

1,8

84

.1

1,0

04

.8

89

5.6

22

,92

0.6

16

,47

9.2

20

,53

2.4

2,8

01

.4

$0

$4,000

$8,000

$12,000

$16,000

$20,000

$24,000

97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14:Q2Risk Capital IssuedRisk Capital Outstandng at Year End

2014 Has Seen the Largest Cat Bond Ever - $1.5 Billion (Florida Citizens). Bond Issuance Will Set a Record.

Model Uncertainty, Concerns on Economy Pushed Issuance Lower.

Risk Capital Outstanding Is at

a Record

Financial Crisis Depressed Issuance

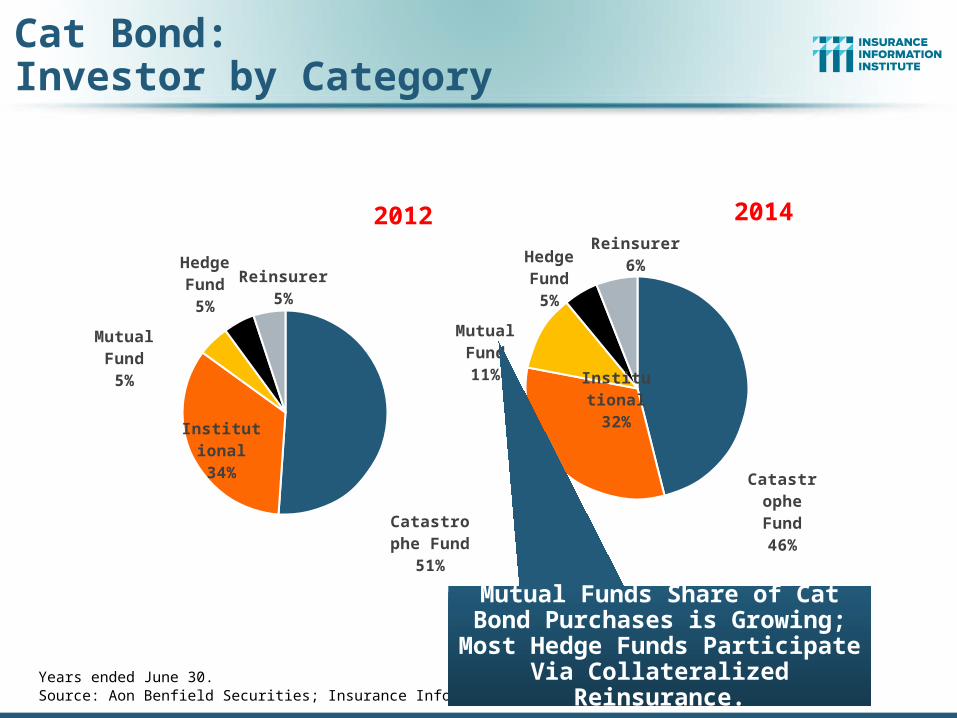

Cat Bond:Investor by Category

Years ended June 30.Source: Aon Benfield Securities; Insurance Information Institute.

Catas-trophe Fund46%

Insti-tu-

tional32%

Mutual Fund11%

Hedge Fund5%

Reinsurer6%

2014

Mutual Funds Share of Cat Bond Purchases is Growing; Most Hedge

Funds Participate Via Collateralized Reinsurance.

Catas-trophe Fund51%

Insti-tu-

tional34%

Mutual Fund5%

Hedge Fund5%

Reinsurer5%

2012

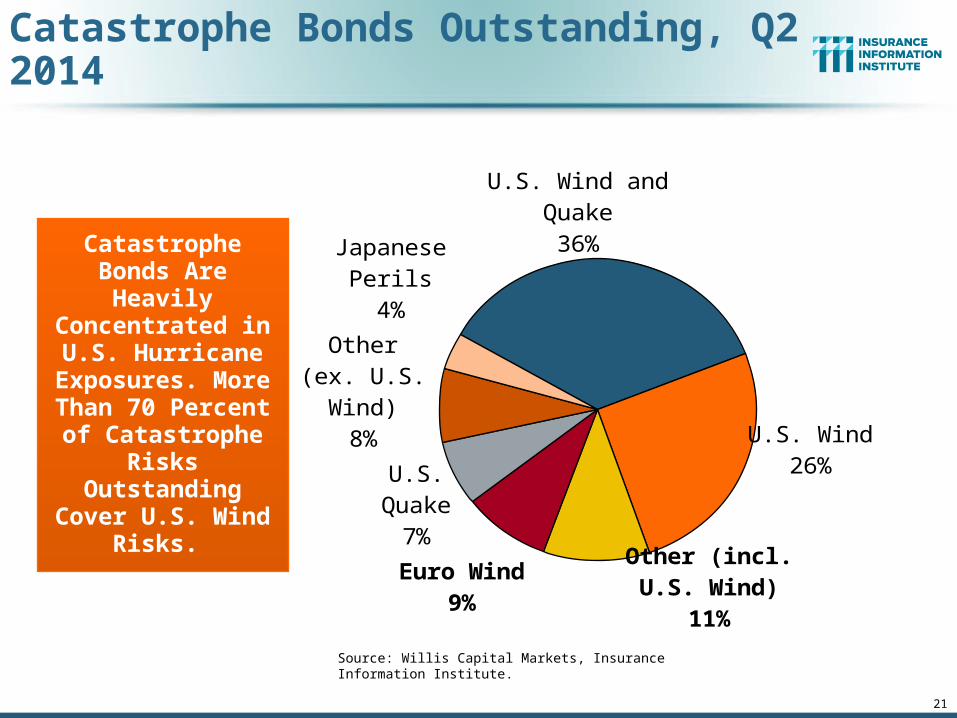

U.S. Wind and Quake36%

U.S. Wind26%

Other (incl. U.S. Wind)11%

Euro Wind9%

U.S. Quake7%

Other (ex. U.S. Wind)

8%

Japanese Perils4%

21

Catastrophe Bonds Outstanding, Q2 2014

Source: Willis Capital Markets, Insurance Information Institute.

Catastrophe Bonds Are Heavily

Concentrated in U.S. Hurricane

Exposures. More Than 70 Percent of Catastrophe Risks Outstanding Cover U.S. Wind Risks.

22

Alternative Capital Is Impacting the Reinsurance

Pricing Environment

22

Traditional and Alternative Returns Are Under Pressure

U.S. Wind-Exposed Risk Premium* 2010:Q1 to 2014: Q1

Q1-10

Q2-10

Q3-10

Q4-10

Q1-11

Q2-11

Q3-11

Q4-11

Q1-12

Q2-12

Q3-12

Q4-12

Q1-13

Q2-13

Q3-13

Q4-13

Q1-14

Q2-14

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

11.0%

12.0%

13.0%

10.9%

8.2% 8.0%

8.0%

7.9%8.2%

8.2%

10.1%

10.9%

12.0%

12.0%

11.6%

11.0%

7.6%

7.4% 7.2%

6.4%6.2%

Ris

k S

pre

ad

(c

ou

po

n –

ris

k-f

ree

ra

te)

23

* Trailing 12-month averageSOURCE: Willis Capital Markets, Insurance Information Institute.

Risk spreads dropped –

equivalent to lower rates –

low cat losses, capital entering

market.

Risk spreads rose in 2011-2012 from cat activity and changes to catastrophe

models.

Non-U.S. Wind-Exposed Risk Premium* 2010:Q1-2014: Q1

Q1-10

Q2-10

Q3-10

Q4-10

Q1-11

Q2-11

Q3-11

Q4-11

Q1-12

Q2-12

Q3-12

Q4-12

Q1-13

Q2-13

Q3-13

Q4-13

Q1-14

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

8.5%

7.2%

6.9%

4.2%

4.2%4.5%

5.7% 5.7%5.7%

5.6%

4.9%

5.4%

4.8%

4.2%

3.6%

2.7%2.6%

Wtd. Avg. Risk Spread

Ris

k S

pre

ad

(c

ou

po

n –

ris

k-f

ree

ra

te)

24

* Trailing 12-month average.SOURCE: Willis Capital Markets, Insurance Information Institute.

Spreads are also falling in non-U.S. wind exposures, but

less sharply and in line with

expected losses

Reinsurance Pricing: Change in Rate on Line for U.S. CAT Business

2014 reflects growth through June 30 from prior year end.Source: Guy Carpenter; Insurance Information Institute.

Alternative Capital, Low

Levels of Catastrophe Drive Rates

Down.

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014-20%

-10%

0%

10%

20%

30%

40%

14% 14%

-11%

-6%

76%

-9%

-16%

10%

-12%

-3%

7%

-7%

-17%

(Change from Previous Year)

Japan, NZ Quakes, US Tornadoes.

2001-02: WTC Losses, Falling

Stock, Bond Prices Dry Up Capital.

2006: Higher Rates After Record Hurri-

canes.

Some Observers Predict Catastrophe Prices Will Fall Another 10 Percent in 2015, Driven by Emergence of New Capital.

76%

What Is Happening to Insurer Profitability?

27

Has Capital Accumulation Impacted Profitability?

Déjà Vu: Does History Suggest Cycles or Super-Cycles in Insurance?

27

-5%

0%

5%

10%

15%

20%

25%

75

76

77

78

79

80

81

82

83

84

85

86

87

88

89

90

91

92

93

94

95

96

97

98

99

00

01

02

03

04

05

06

07

08

09

10

11

12

13

14

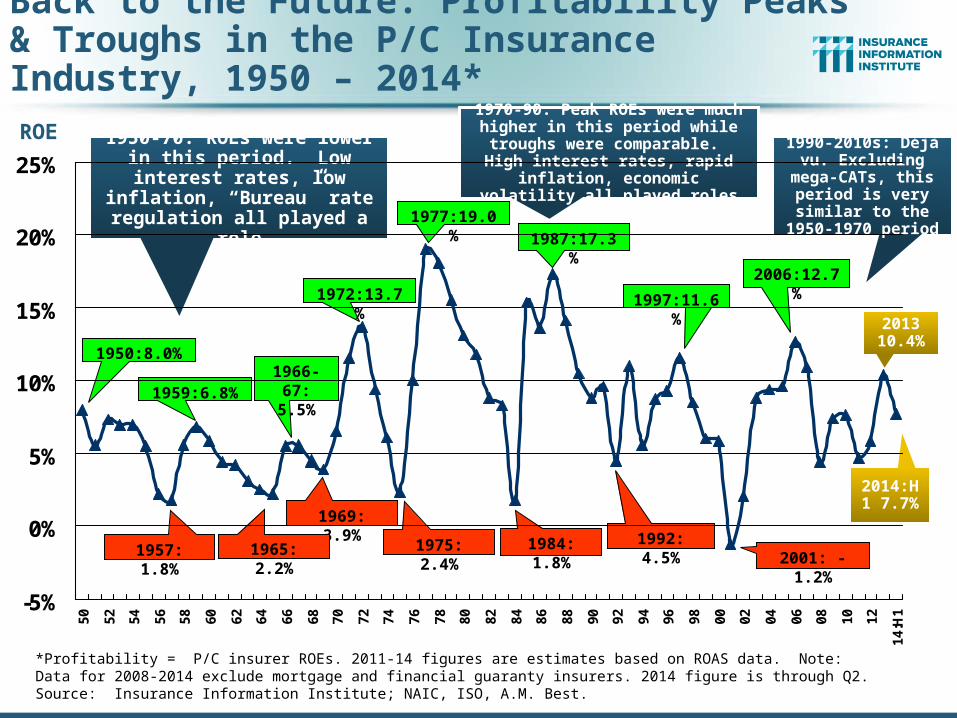

Profitability Peaks & Troughs in the P/C Insurance Industry, 1975 – 2014:H1*

*Profitability = P/C insurer ROEs. 2011-14 figures are estimates based on ROAS data. Note: Data for 2008-2014 exclude mortgage and financial guaranty insurers.Source: Insurance Information Institute; NAIC, ISO, A.M. Best.

1977:19.0%1987:17.3%

1997:11.6% 2006:12.7%

1984: 1.8% 1992: 4.5% 2001: -1.2%

10 Years

10 Years9 Years

History suggests next ROE peak will be in 2015-2016

ROE

1975: 2.4%

2013 10.4%

2014:H1 7.7%

30

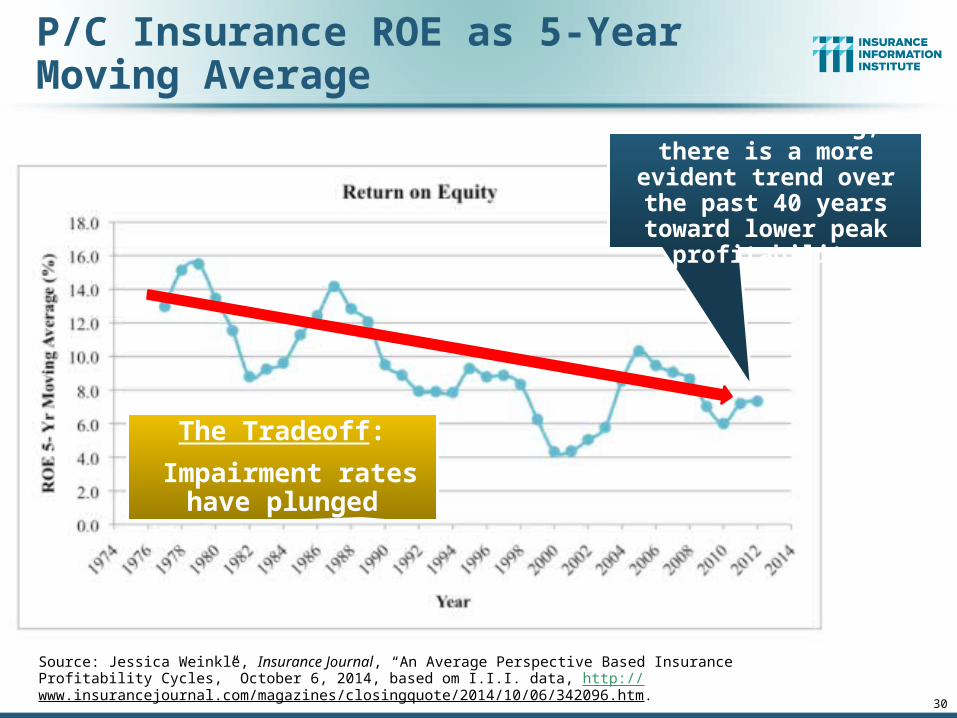

P/C Insurance ROE as 5-Year Moving Average

Source: Jessica Weinkle, Insurance Journal, “An Average Perspective Based Insurance Profitability Cycles,” October 6, 2014, based om I.I.I. data, http://www.insurancejournal.com/magazines/closingquote/2014/10/06/342096.htm.

After smoothing, there is a more evident trend over the past 40 years toward lower peak profitability

The Tradeoff:

Impairment rates have plunged

31

P/C Insurance ROE Index(1974-2014:Q1 = 100)

Source: Jessica Weinkle, Insurance Journal, “An Average Perspective Based Insurance Profitability Cycles,” October 6, 2014, based om I.I.I. data, http://www.insurancejournal.com/magazines/closingquote/2014/10/06/342096.htm.

Lower peak profitability seems to be the norm after

1994. Is RBC a cause? Greater use of modeling?

Lower interest rates?

The Tradeoff:

Industry impairment rates have plunged

-5%

0%

5%

10%

15%

20%

25%

50 52 54 56 58 60 62 64 66 68 70 72 74 76 78 80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10 12

14:H

1

*Profitability = P/C insurer ROEs. 2011-14 figures are estimates based on ROAS data. Note: Data for 2008-2014 exclude mortgage and financial guaranty insurers. 2014 figure is through Q2.Source: Insurance Information Institute; NAIC, ISO, A.M. Best.

1977:19.0%

1987:17.3%

1997:11.6%

2006:12.7%

1984: 1.8%

1992: 4.5%2001: -1.2%

ROE

1975: 2.4%

2013 10.4%

2014:H1 7.7%

Back to the Future: Profitability Peaks & Troughs in the P/C Insurance Industry, 1950 – 2014*

1969: 3.9%

1965: 2.2%1957: 1.8%

1972:13.7%

1966-67: 5.5%1959:6.8%

1950:8.0%

1950-70: ROEs were lower in this period. Low interest rates,

low inflation, “Bureau” rate regulation all played a role

1970-90: Peak ROEs were much higher in this period while troughs

were comparable. High interest rates, rapid inflation, economic

volatility all played roles

1990-2010s: Déjà vu. Excluding mega-

CATs, this period is very similar to the 1950-1970 period

33

7.3%7.0%8.4%

11.5%11.2%

4.2%5.7%

0%

2%

4%

6%

8%

10%

12%

14%

1950-59 1960-69 1970-79 1980-89 1990-99 2000-09 2010-14*

Average Annual Percent Change (%)

Profitability in the current low yield, low Inflation environment has declined since the highs of the 1970s and

1980s, but is above that of the 1950s and 1960s and the industry’s impairment rates have dropped since the 1980s

33Sources: Insurance Information Institute research.

Average ROE for the P/C Insurance Industry by Decade, 1950s – 2010s

Profitability peaked in the 1970s and 1980s but has tapered off

since thenP/C profitability was much lower in the 1960s and

1970s

35

BANK LESSON: Profitability, Capital and Systemically Important Banks

Source: The Economist, “No Respite,” September 27, 2014.

Global Systemically Important bank Tier-1

capital ratios are up since the global financial crisis,

but ROEs are lower

The Message from Bank Regulators:

Get used to it!

P/C Insurer Impairments, 1969–20137

07

17

27

37

47

57

67

77

87

98

08

18

28

38

48

58

68

78

88

99

09

19

29

39

49

59

69

79

89

90

00

10

20

30

40

50

60

70

80

91

01

11

21

3

0

10

20

30

40

50

60

70

15

12

71

19

34

91

31

21

99

16

14

13

36

49

31 3

45

04

85

56

05

84

12

91

61

23

11

8 19

49 50

47

35

18

14 15

51

6 19 2

13

42

51

4

Source: A.M. Best Special Report “U.S. P/C Impairments Down Sharply in 2013; Alternative Risk Players Faltered,” June 23, 2014; Insurance Information Institute.

The Number of Impairments Varies Significantly Over the P/C Insurance Cycle, With Peaks Occurring Well into Hard Markets

36

Impairments among P/C insurers remain infrequent

37

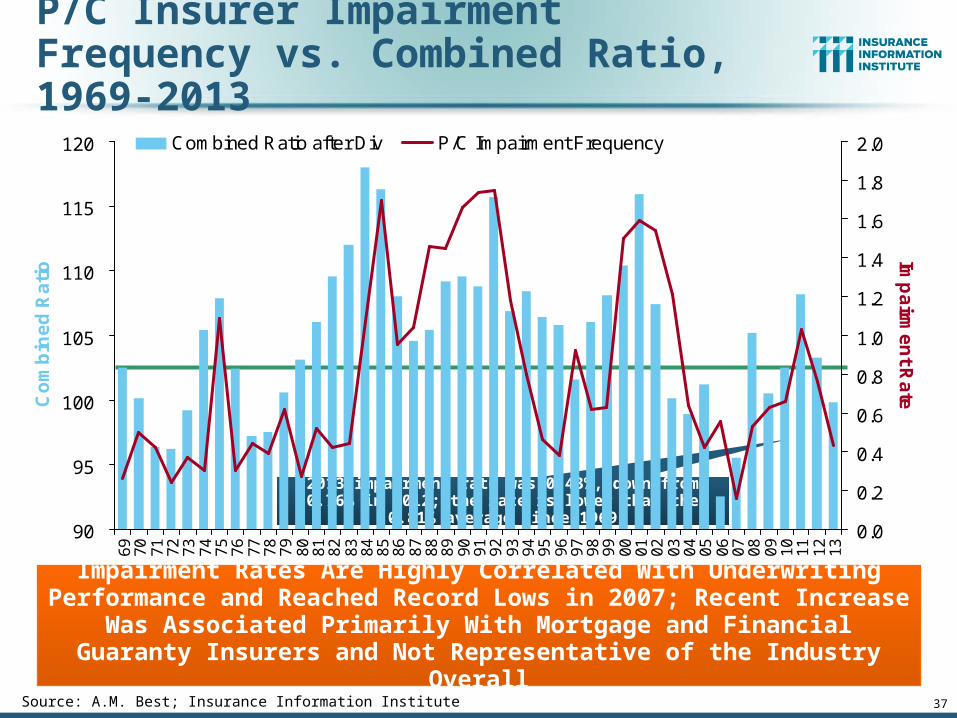

P/C Insurer Impairment Frequency vs. Combined Ratio, 1969-2013

90

95

100

105

110

115

1206

97

07

17

27

37

47

57

67

77

87

98

08

18

28

38

48

58

68

78

88

99

09

19

29

39

49

59

69

79

89

90

00

10

20

30

40

50

60

70

80

91

01

11

21

3

Co

mb

ine

d R

ati

o

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

Imp

airm

en

t Ra

te

Combined Ratio after Div P/C Impairment Frequency

Source: A.M. Best; Insurance Information Institute

2013 impairment rate was 0.43%, down from 0.76% in 2012; the rate is lower than the 0.81% average since 1969

Impairment Rates Are Highly Correlated With Underwriting Performance and Reached Record Lows in 2007; Recent Increase Was Associated

Primarily With Mortgage and Financial Guaranty Insurers and Not Representative of the Industry Overall

39

Summary

Capital Accumulation is Not Unique to (Re)InsuranceLarge corporations, institutional investors (e.g.,

pension funds), hedge funds, sovereign wealth funds have experienced rapid cash (or equivalent) accumulation

All Are Chasing Yield—Globally

Capital Has Generally Been Accumulating on the Balance Sheets of Nonlife (Re)Insurers for YearsEra of rapid accumulation pre-dates financial crisisPace has accelerated post-financial crisisProfits, capital gains and “alternative capital” all

contribute

40

Summary (Continued) Nonlife ROEs Have Trended Downward

Downward trend pre-dates financial crisis Capital accumulation, RBC requirements are factors; Low yields Tradeoff: Impairment rates have trended downward

Quantum Shift or Evidence of a Super-Cycle? Profitability patterns today are more reminiscent of the pre-1970

era (and in the US back to WW II and even pre-war)

Capital Allocation Challenges: Excess capital seemingly “stuck” in the industry Sluggish economy diminishes rate of exposure growth Insurance penetration lags economic growth in emerging markets Changes in the nature of insurable exposures (e.g., cyber, IP, etc.) Share repurchases preferred over long-term investments or

acquisitions (situation is not unique to insurance) Tax and regulatory obstacles

www.iii.org

Thank you for your timeand your attention!

Twitter: twitter.com/bob_hartwigDownload at www.iii.org/presentations

Insurance Information Institute Online:

41