Embed Size (px)

Citation preview

Capital Markets: Observations and Insights Earnings Resurgence Spring 2017

Key Observations

Page 2

Table of Contents

Performance

Fundamentals

Valuation

Pages 3-11

Pages 12-20

Pages 21-28

• After diverging in 2016, fundamentals once again drove performance in 1Q17

• There is a resurgence in earnings growth after a couple of years of weakness

• Leading indicators suggest that economic and corporate profits will continue

to expand

• Some areas of the equity market are attractively valued, particularly relative to fixed

income and real estate

This presentation is directed only at professional investors as defined by the MIFID. It should not be read by retail investors.

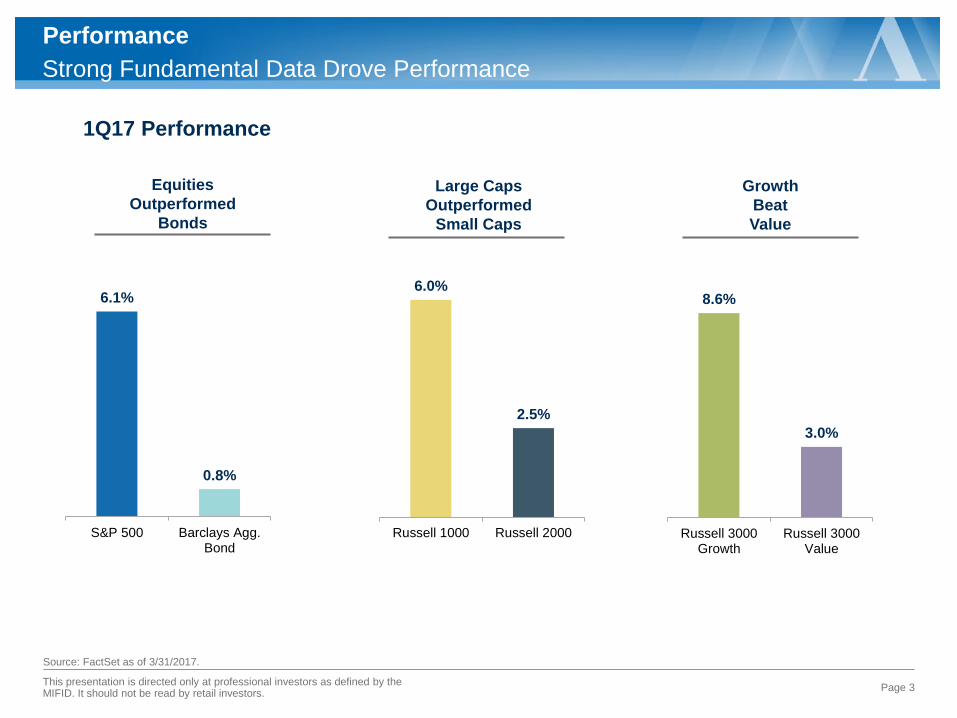

Strong Fundamental Data Drove Performance

Performance

Page 3

Source: FactSet as of 3/31/2017.

6.1%

0.8%

S&P 500 Barclays Agg.Bond

Equities

Outperformed

Bonds

Large Caps

Outperformed

Small Caps

Growth

Beat

Value

6.0%

2.5%

Russell 1000 Russell 2000

8.6%

3.0%

Russell 3000Growth

Russell 3000Value

1Q17 Performance

This presentation is directed only at professional investors as defined by the MIFID. It should not be read by retail investors.

-10

-5

0

5

10

15

20

25

30

Energ

y

Tele

com

Fin

ancia

ls

Industr

ials

Ma

teri

als

Utilit

ies

Techn

olo

gy

Co

nsum

er

Dis

cre

tio

nary

Co

nsum

er

Sta

ple

s

He

alth C

are

U.S. World

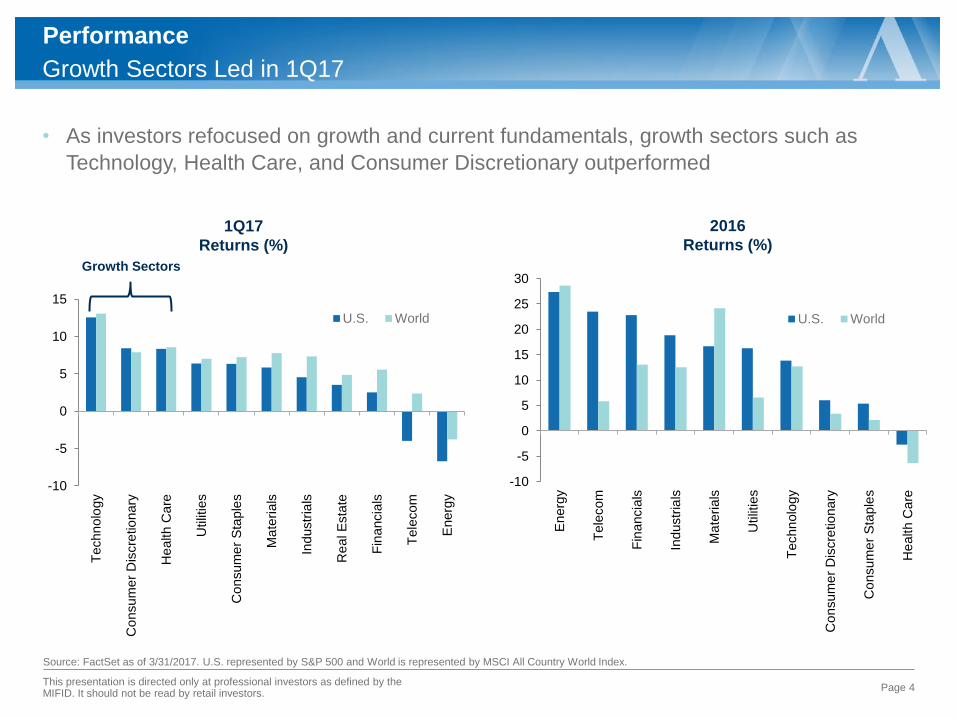

Growth Sectors Led in 1Q17

Performance

Page 4

Source: FactSet as of 3/31/2017. U.S. represented by S&P 500 and World is represented by MSCI All Country World Index.

-10

-5

0

5

10

15

Techn

olo

gy

Co

nsum

er

Dis

cre

tio

nary

He

alth C

are

Utilit

ies

Co

nsum

er

Sta

ple

s

Ma

teri

als

Industr

ials

Re

al E

sta

te

Fin

ancia

ls

Tele

com

Energ

y

U.S. World

• As investors refocused on growth and current fundamentals, growth sectors such as

Technology, Health Care, and Consumer Discretionary outperformed

1Q17

Returns (%)

2016

Returns (%)

Growth Sectors

This presentation is directed only at professional investors as defined by the MIFID. It should not be read by retail investors.

0

20

40

60

80

100

-10

-5

0

5

10

15

Techn

olo

gy

Co

nsum

er

Dis

c

He

alth C

are

Utilit

ies

Co

nsum

er

Sta

ple

s

S&

P 5

00

Ma

teri

als

Industr

ials

Re

al E

sta

te

Fin

ancia

ls

Tele

com

Energ

y

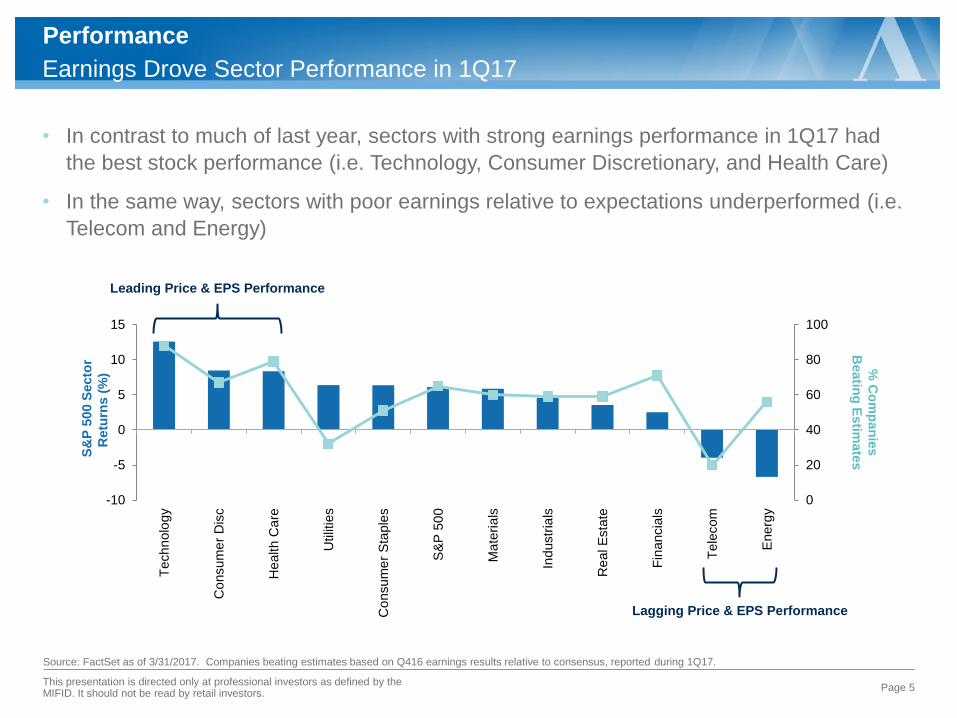

Earnings Drove Sector Performance in 1Q17

Performance

Page 5

Source: FactSet as of 3/31/2017. Companies beating estimates based on Q416 earnings results relative to consensus, reported during 1Q17.

S&

P 5

00 S

ecto

r

Retu

rns (

%)

% C

om

pan

ies

Beatin

g E

stim

ate

s

• In contrast to much of last year, sectors with strong earnings performance in 1Q17 had

the best stock performance (i.e. Technology, Consumer Discretionary, and Health Care)

• In the same way, sectors with poor earnings relative to expectations underperformed (i.e.

Telecom and Energy)

Lagging Price & EPS Performance

Leading Price & EPS Performance

This presentation is directed only at professional investors as defined by the MIFID. It should not be read by retail investors.

Page 6

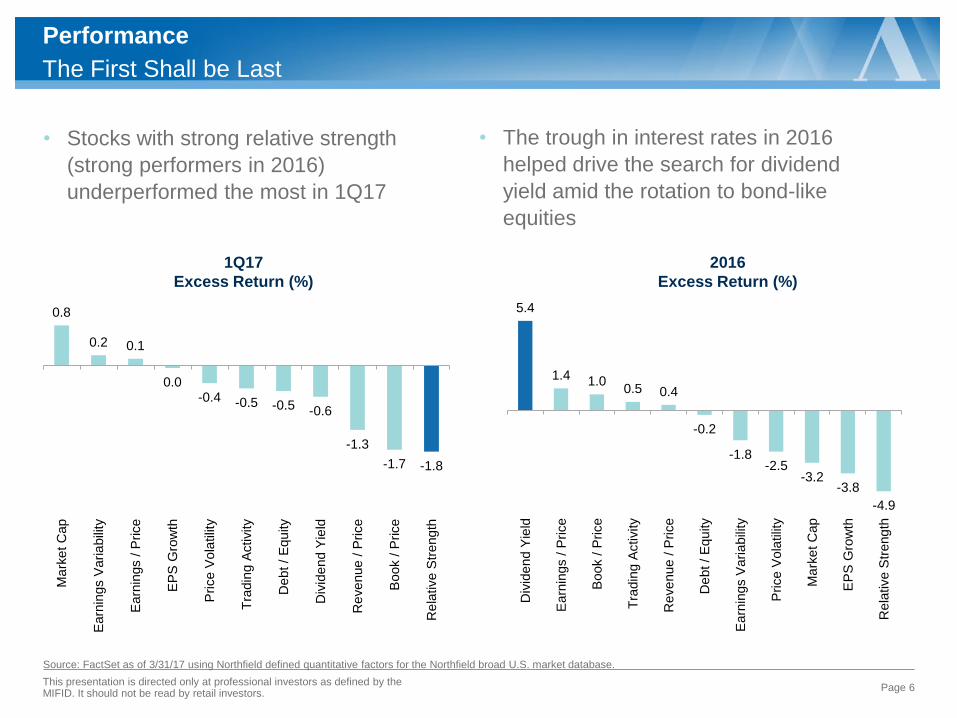

• Stocks with strong relative strength

(strong performers in 2016)

underperformed the most in 1Q17

The First Shall be Last

Performance

0.8

0.2 0.1

0.0 -0.4 -0.5 -0.5 -0.6

-1.3

-1.7 -1.8

Ma

rke

t C

ap

Earn

ings V

aria

bili

ty

Earn

ings / P

rice

EP

S G

row

th

Price V

ola

tilit

y

Tra

din

g A

ctivity

De

bt /

Equ

ity

Div

ide

nd Y

ield

Re

ve

nue

/ P

rice

Book / P

rice

Re

lative S

treng

th

1Q17

Excess Return (%)

5.4

1.4 1.0 0.5 0.4

-0.2

-1.8 -2.5

-3.2 -3.8

-4.9

Div

ide

nd Y

ield

Earn

ings / P

rice

Book / P

rice

Tra

din

g A

ctivity

Re

ve

nue

/ P

rice

De

bt /

Equ

ity

Earn

ings V

aria

bili

ty

Price V

ola

tilit

y

Ma

rke

t C

ap

EP

S G

row

th

Re

lative S

tre

ng

th

2016

Excess Return (%)

• The trough in interest rates in 2016

helped drive the search for dividend

yield amid the rotation to bond-like

equities

This presentation is directed only at professional investors as defined by the MIFID. It should not be read by retail investors.

Source: FactSet as of 3/31/17 using Northfield defined quantitative factors for the Northfield broad U.S. market database.

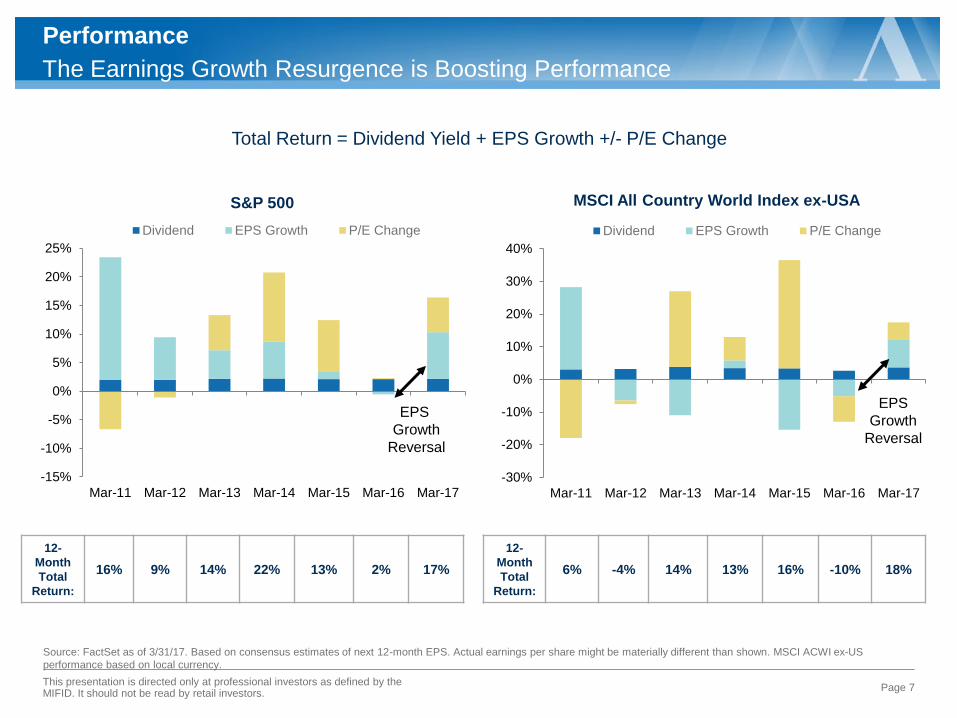

The Earnings Growth Resurgence is Boosting Performance

Performance

Page 7

Source: FactSet as of 3/31/17. Based on consensus estimates of next 12-month EPS. Actual earnings per share might be materially different than shown. MSCI ACWI ex-US

performance based on local currency.

Total Return = Dividend Yield + EPS Growth +/- P/E Change

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

Mar-11 Mar-12 Mar-13 Mar-14 Mar-15 Mar-16 Mar-17

Dividend EPS Growth P/E Change

12-

Month

Total

Return:

16% 9% 14% 22% 13% 2% 17%

12-

Month

Total

Return:

6% -4% 14% 13% 16% -10% 18%

S&P 500 MSCI All Country World Index ex-USA

-30%

-20%

-10%

0%

10%

20%

30%

40%

Mar-11 Mar-12 Mar-13 Mar-14 Mar-15 Mar-16 Mar-17

Dividend EPS Growth P/E Change

EPS

Growth

Reversal

This presentation is directed only at professional investors as defined by the MIFID. It should not be read by retail investors.

EPS

Growth

Reversal

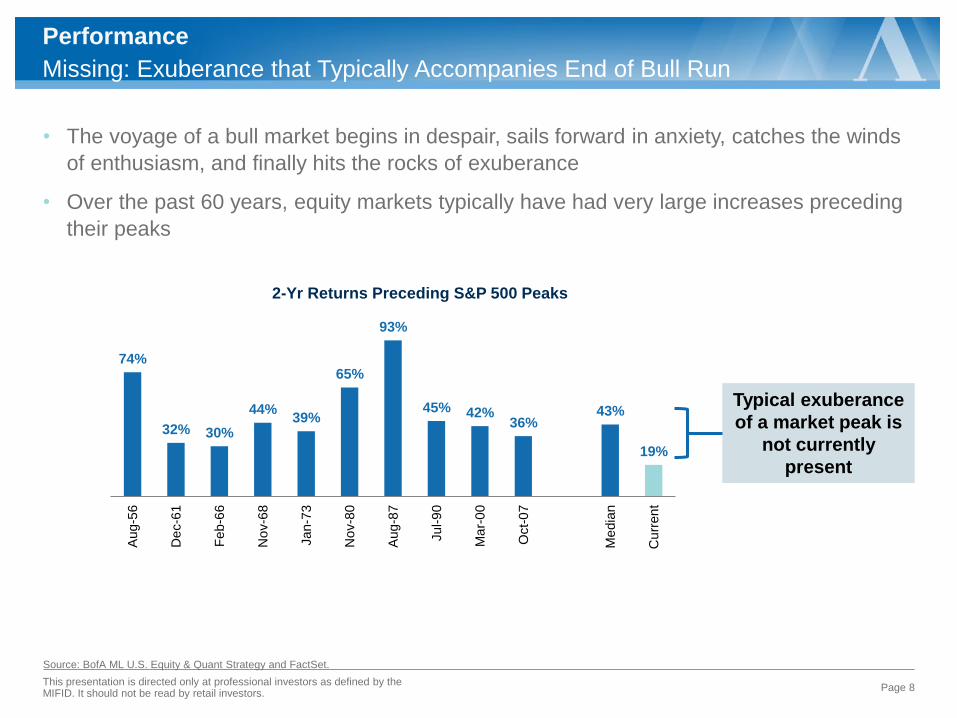

74%

32% 30%

44% 39%

65%

93%

45% 42% 36%

43%

19%

Aug-5

6

De

c-6

1

Feb

-66

No

v-6

8

Jan-7

3

No

v-8

0

Aug-8

7

Jul-9

0

Ma

r-0

0

Oct-

07

Me

dia

n

Cu

rren

t

This presentation is directed only at professional investors as defined by the MIFID. It should not be read by retail investors.

Missing: Exuberance that Typically Accompanies End of Bull Run

Source: BofA ML U.S. Equity & Quant Strategy and FactSet.

• The voyage of a bull market begins in despair, sails forward in anxiety, catches the winds

of enthusiasm, and finally hits the rocks of exuberance

• Over the past 60 years, equity markets typically have had very large increases preceding

their peaks

Page 8

Performance

Typical exuberance

of a market peak is

not currently

present

2-Yr Returns Preceding S&P 500 Peaks

0

2

4

6

8

10

12

14

1920 1934 1947 1961 1975 1988 2002 2016 2030

Dura

tion o

f B

ull

Mark

et (Y

ears

)

Year that Bull Market Ended

1990s Bull

Market

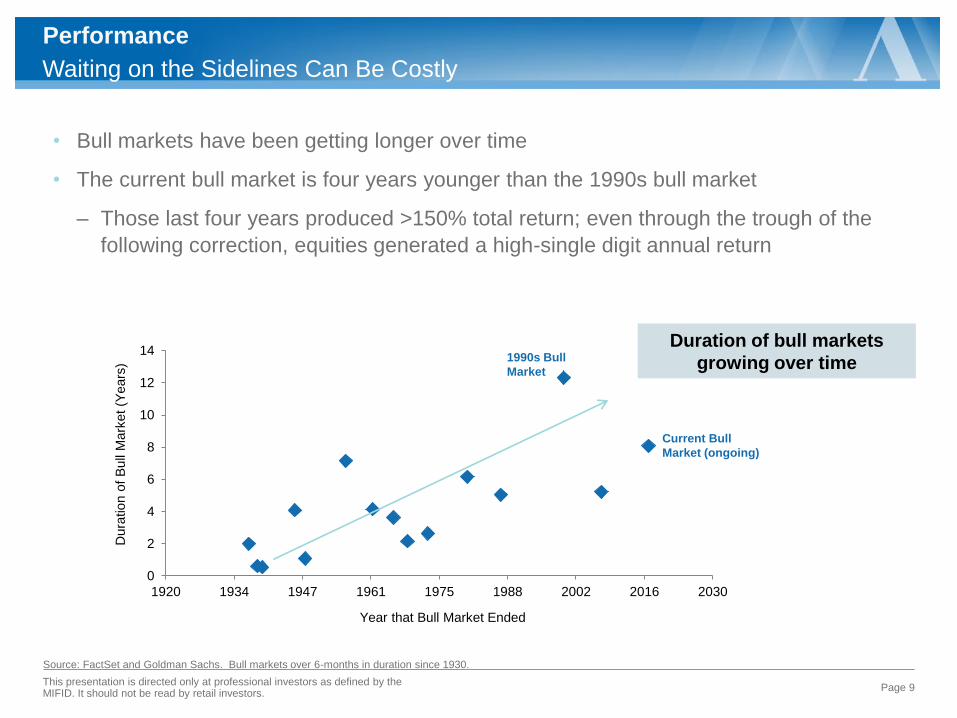

Waiting on the Sidelines Can Be Costly

Source: FactSet and Goldman Sachs. Bull markets over 6-months in duration since 1930.

• Bull markets have been getting longer over time

• The current bull market is four years younger than the 1990s bull market

‒ Those last four years produced >150% total return; even through the trough of the

following correction, equities generated a high-single digit annual return

Page 9

Performance

Duration of bull markets

growing over time

Current Bull

Market (ongoing)

This presentation is directed only at professional investors as defined by the MIFID. It should not be read by retail investors.

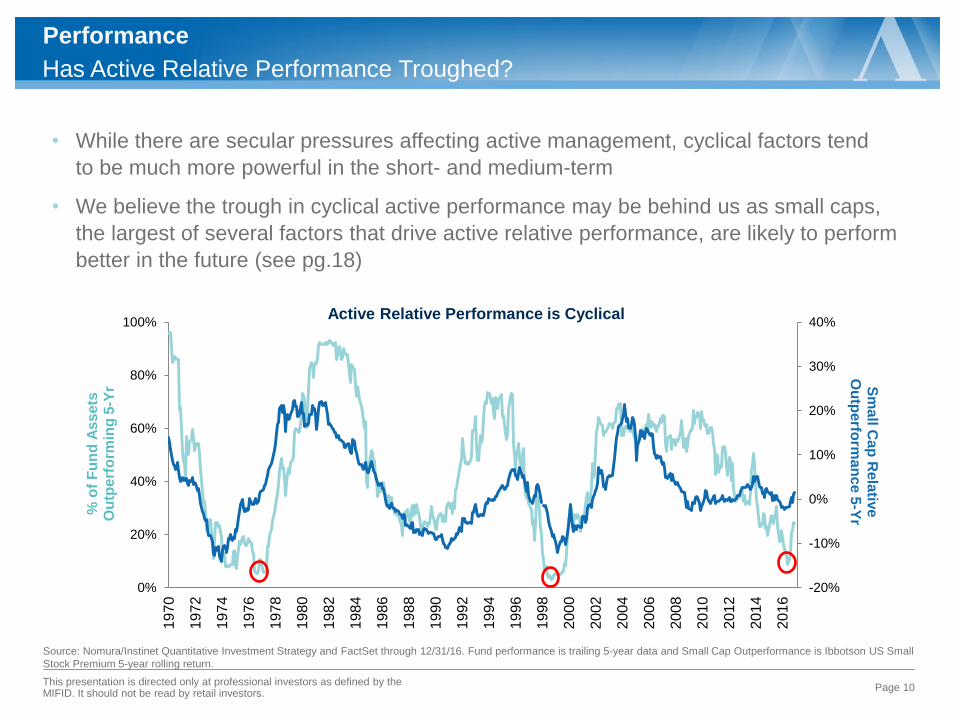

Has Active Relative Performance Troughed?

Source: Nomura/Instinet Quantitative Investment Strategy and FactSet through 12/31/16. Fund performance is trailing 5-year data and Small Cap Outperformance is Ibbotson US Small

Stock Premium 5-year rolling return.

Page 10

• While there are secular pressures affecting active management, cyclical factors tend

to be much more powerful in the short- and medium-term

• We believe the trough in cyclical active performance may be behind us as small caps,

the largest of several factors that drive active relative performance, are likely to perform

better in the future (see pg.18)

Performance

Active Relative Performance is Cyclical

-20%

-10%

0%

10%

20%

30%

40%

0%

20%

40%

60%

80%

100%

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

Sm

all C

ap

Re

lativ

e

Ou

tpe

rform

an

ce

5-Y

r %

of

Fu

nd

As

se

ts

Ou

tpe

rfo

rmin

g 5

-Yr

This presentation is directed only at professional investors as defined by the MIFID. It should not be read by retail investors.

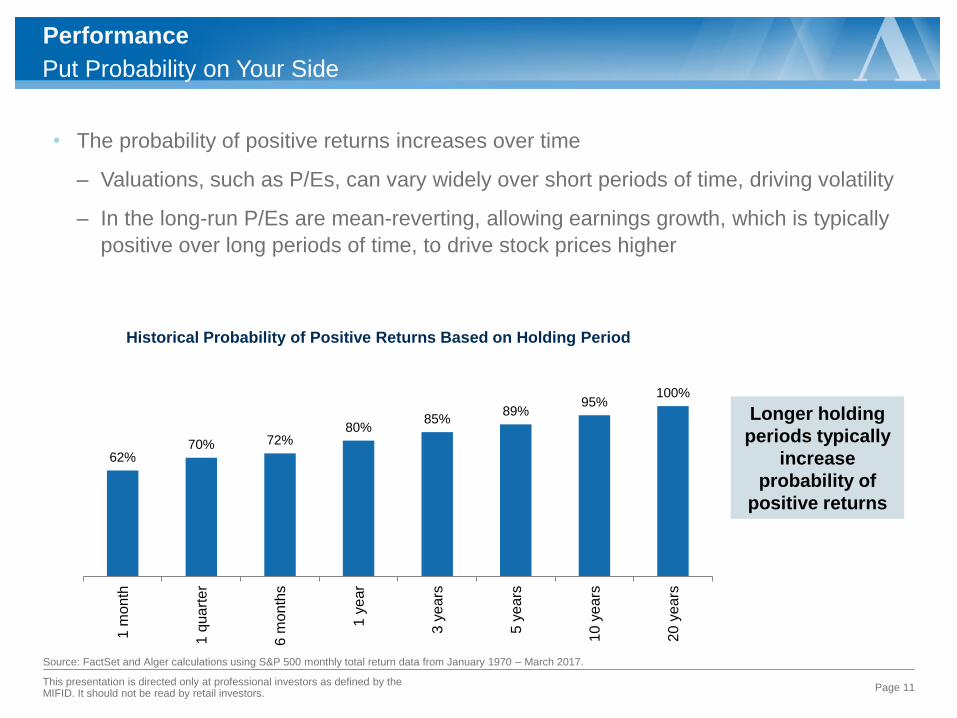

Put Probability on Your Side

Source: FactSet and Alger calculations using S&P 500 monthly total return data from January 1970 – March 2017.

• The probability of positive returns increases over time

‒ Valuations, such as P/Es, can vary widely over short periods of time, driving volatility

‒ In the long-run P/Es are mean-reverting, allowing earnings growth, which is typically

positive over long periods of time, to drive stock prices higher

Page 11

Performance

Historical Probability of Positive Returns Based on Holding Period

62% 70% 72%

80% 85%

89% 95%

100%

1 m

onth

1 q

ua

rte

r

6 m

onth

s

1 y

ear

3 y

ears

5 y

ears

10 y

ears

20 y

ears

Longer holding

periods typically

increase

probability of

positive returns

This presentation is directed only at professional investors as defined by the MIFID. It should not be read by retail investors.

$0

$1

$10

$100

$1,000

1

10

100

1,000

10,000

1900 1925 1950 1975 2000

S&

P 5

00 P

rice (

Lo

g S

cale

)

Source: FactSet, S&P, Robert Shiller. Data through March 31, 2017.

The Stock Market Engine Runs on Earnings Growth

This presentation is directed only at professional investors as defined by the MIFID. It should not be read by retail investors.

• “In the short run, the market is a voting machine, but in the long run, it is a weighing

machine.” –Ben Graham

• EPS growth has averaged approximately 6% annually over the past 50 years

Page 12

Fundamentals

In the short term,

sentiment/valuation drives

returns; in the long term,

stock prices grow

exponentially with earnings

2017

S&

P 5

00 E

PS

(Lo

g S

cale

)

$50

$75

$100

$125

$150

90

100

110

120

130

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

S&

P 5

00 E

PS

Lead

ing

Eco

no

mic

In

dex

17

Month

Lead

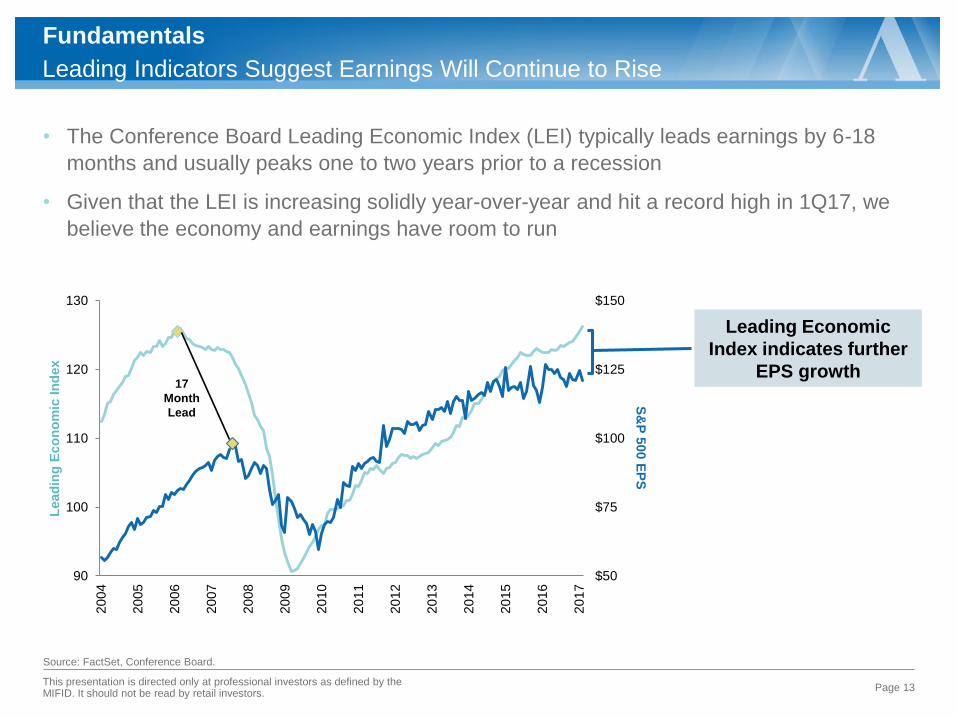

Source: FactSet, Conference Board.

Leading Indicators Suggest Earnings Will Continue to Rise

This presentation is directed only at professional investors as defined by the MIFID. It should not be read by retail investors.

• The Conference Board Leading Economic Index (LEI) typically leads earnings by 6-18

months and usually peaks one to two years prior to a recession

• Given that the LEI is increasing solidly year-over-year and hit a record high in 1Q17, we

believe the economy and earnings have room to run

Page 13

Fundamentals

Leading Economic

Index indicates further

EPS growth

Page 14

Source: FactSet as of 3/31/17. Inflation represented by PCE Price Index ex-food and energy (year over year).

-2

0

2

4

6

8

10

12

14

16

18

20

19

66

19

69

19

72

19

75

19

78

19

81

19

84

19

87

19

90

19

93

19

96

19

99

20

02

20

05

20

08

20

11

20

14

20

17

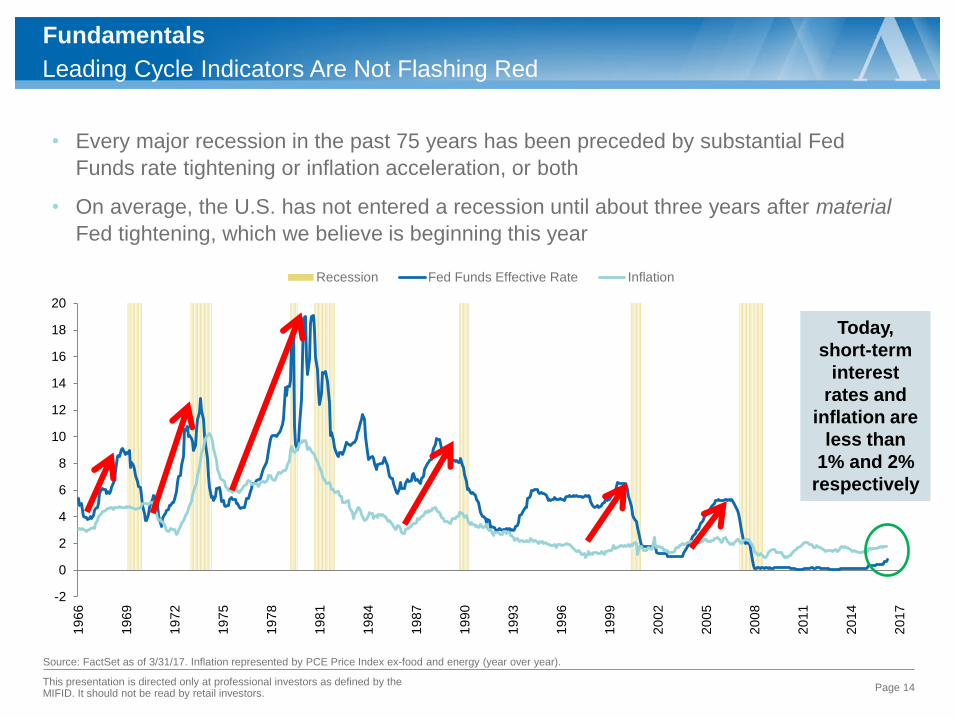

Recession Fed Funds Effective Rate Inflation

• Every major recession in the past 75 years has been preceded by substantial Fed

Funds rate tightening or inflation acceleration, or both

• On average, the U.S. has not entered a recession until about three years after material

Fed tightening, which we believe is beginning this year

Today,

short-term

interest

rates and

inflation are

less than

1% and 2%

respectively

Leading Cycle Indicators Are Not Flashing Red

Fundamentals

This presentation is directed only at professional investors as defined by the MIFID. It should not be read by retail investors.

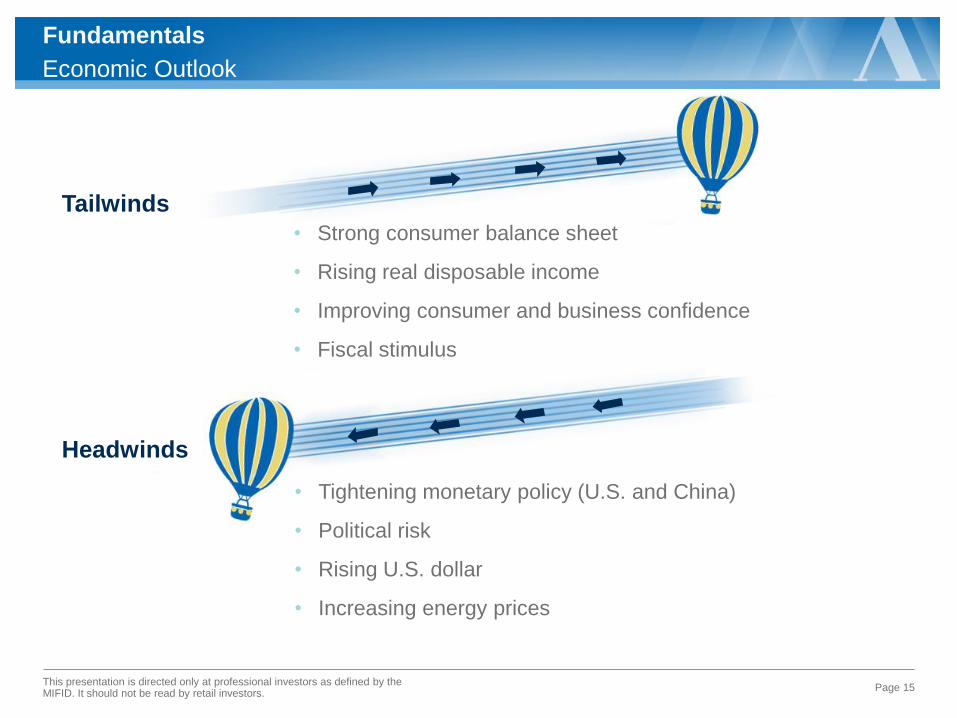

Economic Outlook

• Strong consumer balance sheet

• Rising real disposable income

• Improving consumer and business confidence

• Fiscal stimulus

• Tightening monetary policy (U.S. and China)

• Political risk

• Rising U.S. dollar

• Increasing energy prices

Tailwinds

Headwinds

Page 15

Fundamentals

This presentation is directed only at professional investors as defined by the MIFID. It should not be read by retail investors.

Fiscal Policy Could Boost Earnings Materially

Source: Tax Foundation and Cornerstone Macro. “Consumer” is higher wages and “Business” is capital stock.

• A 10 percentage point decline in the corporate tax rate would likely boost S&P 500 EPS

by about 8%

• Business spending would likely benefit more than consumer spending given lower

corporate tax rates increase in enterprise cash flow higher business spending

‒ The Tax Foundation’s analysis of the Trump plan suggests that wages should increase

5% but capital stock (i.e. business spending) would be 20% higher!

Page 16

Fundamentals

5%

20%

Consumer Business

Impact of Trump Plan Relative to Baseline (Over a Decade)

Business spending to

outpace consumer spending

This presentation is directed only at professional investors as defined by the MIFID. It should not be read by retail investors.

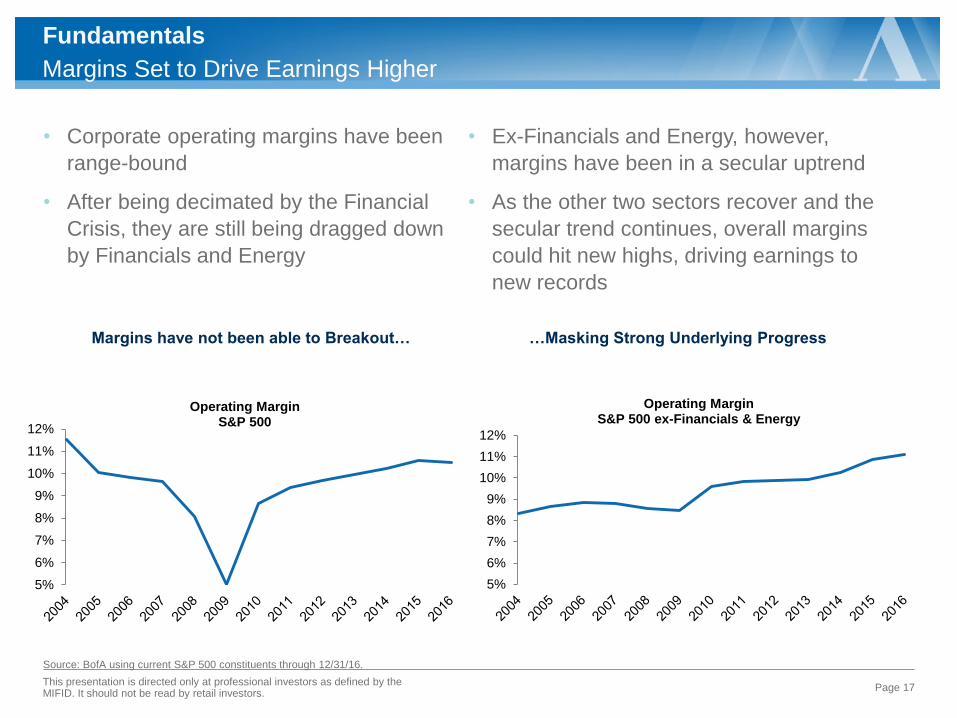

Margins Set to Drive Earnings Higher

Fundamentals

Page 17

Source: BofA using current S&P 500 constituents through 12/31/16.

• Corporate operating margins have been

range-bound

• After being decimated by the Financial

Crisis, they are still being dragged down

by Financials and Energy

• Ex-Financials and Energy, however,

margins have been in a secular uptrend

• As the other two sectors recover and the

secular trend continues, overall margins

could hit new highs, driving earnings to

new records

Margins have not been able to Breakout…

5%

6%

7%

8%

9%

10%

11%

12%

Operating Margin S&P 500

5%

6%

7%

8%

9%

10%

11%

12%

Operating Margin S&P 500 ex-Financials & Energy

…Masking Strong Underlying Progress

This presentation is directed only at professional investors as defined by the MIFID. It should not be read by retail investors.

80

100

120

140

160

180

200

20

13

20

14

20

15

20

16

20

17

20

18

Earnings Per Share

Russell 2000 Russell 1000

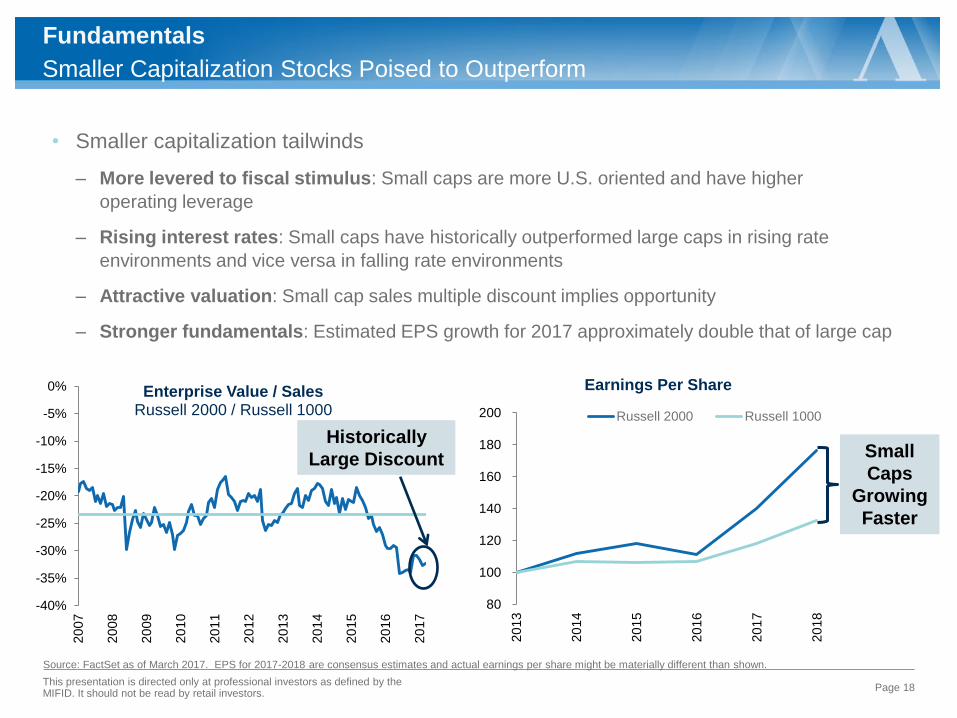

Smaller Capitalization Stocks Poised to Outperform

Fundamentals

Page 18

Source: FactSet as of March 2017. EPS for 2017-2018 are consensus estimates and actual earnings per share might be materially different than shown.

• Smaller capitalization tailwinds

‒ More levered to fiscal stimulus: Small caps are more U.S. oriented and have higher

operating leverage

‒ Rising interest rates: Small caps have historically outperformed large caps in rising rate

environments and vice versa in falling rate environments

‒ Attractive valuation: Small cap sales multiple discount implies opportunity

‒ Stronger fundamentals: Estimated EPS growth for 2017 approximately double that of large cap

-40%

-35%

-30%

-25%

-20%

-15%

-10%

-5%

0%

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

Enterprise Value / Sales Russell 2000 / Russell 1000

Historically

Large Discount Small

Caps

Growing

Faster

This presentation is directed only at professional investors as defined by the MIFID. It should not be read by retail investors.

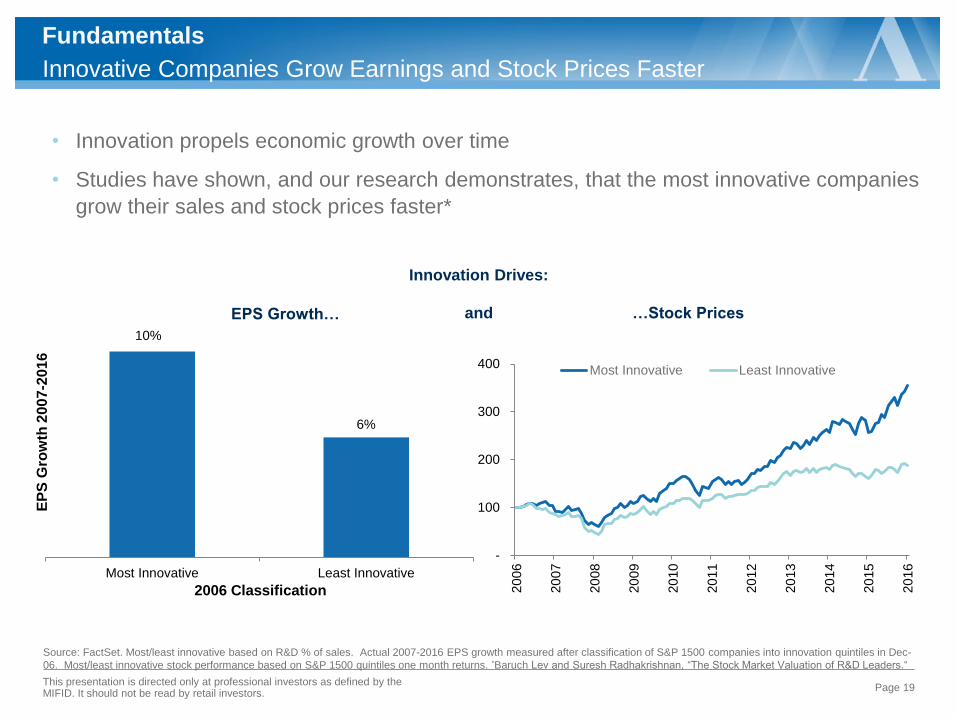

Innovative Companies Grow Earnings and Stock Prices Faster

Source: FactSet. Most/least innovative based on R&D % of sales. Actual 2007-2016 EPS growth measured after classification of S&P 1500 companies into innovation quintiles in Dec-

06. Most/least innovative stock performance based on S&P 1500 quintiles one month returns. *Baruch Lev and Suresh Radhakrishnan, “The Stock Market Valuation of R&D Leaders.“

• Innovation propels economic growth over time

• Studies have shown, and our research demonstrates, that the most innovative companies

grow their sales and stock prices faster*

Page 19

Fundamentals

10%

6%

Most Innovative Least Innovative

EP

S G

row

th 2

00

7-2

016

2006 Classification

EPS Growth…

-

100

200

300

400

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

Most Innovative Least Innovative

…Stock Prices

Innovation Drives:

and

This presentation is directed only at professional investors as defined by the MIFID. It should not be read by retail investors.

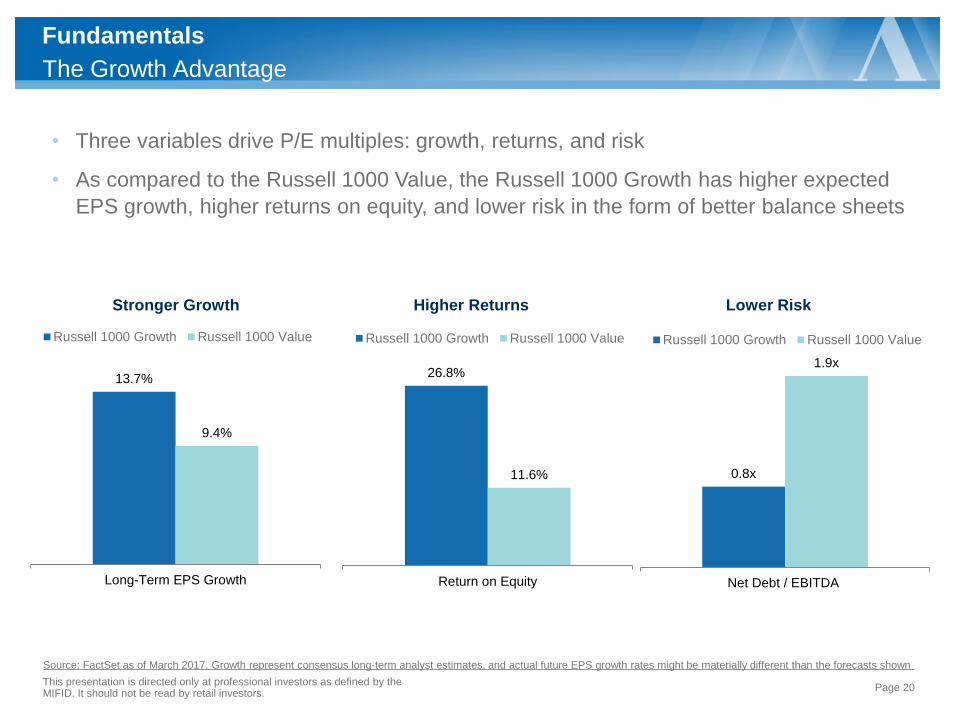

The Growth Advantage

Source: FactSet as of March 2017. Growth represent consensus long-term analyst estimates, and actual future EPS growth rates might be materially different than the forecasts shown

• Three variables drive P/E multiples: growth, returns, and risk

• As compared to the Russell 1000 Value, the Russell 1000 Growth has higher expected

EPS growth, higher returns on equity, and lower risk in the form of better balance sheets

Page 20

Fundamentals

This presentation is directed only at professional investors as defined by the MIFID. It should not be read by retail investors.

Stronger Growth

13.7%

9.4%

Long-Term EPS Growth

Russell 1000 Growth Russell 1000 Value

Higher Returns

26.8%

11.6%

Return on Equity

Russell 1000 Growth Russell 1000 Value

Lower Risk

0.8x

1.9x

Net Debt / EBITDA

Russell 1000 Growth Russell 1000 Value

-5%

0%

5%

10%

15%

20%

25%

5 10 15 20 25 30

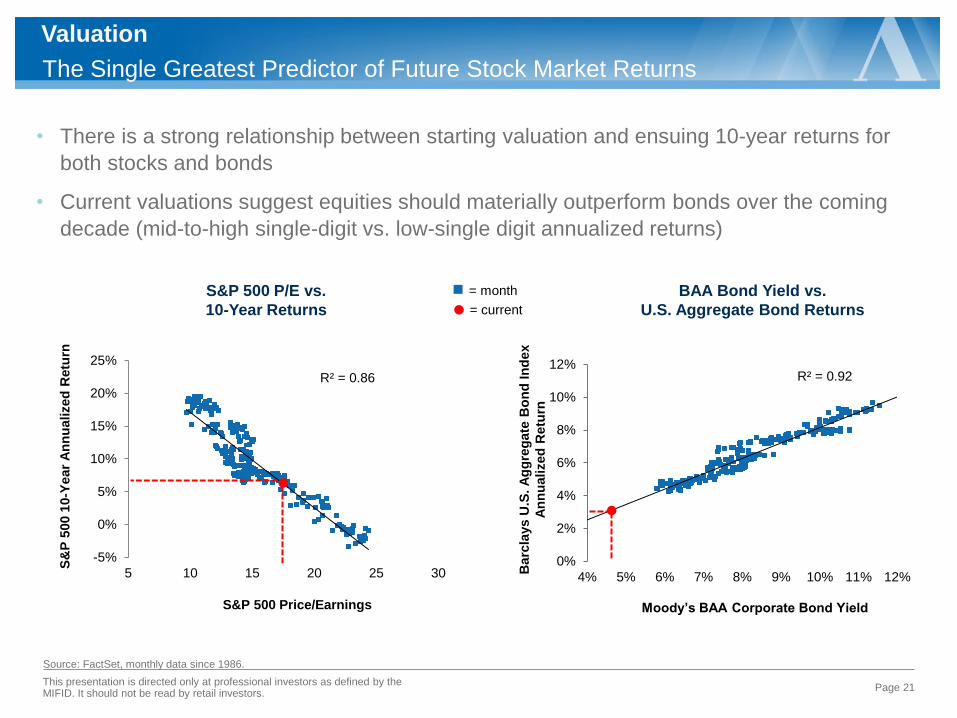

Source: FactSet, monthly data since 1986.

• There is a strong relationship between starting valuation and ensuing 10-year returns for

both stocks and bonds

• Current valuations suggest equities should materially outperform bonds over the coming

decade (mid-to-high single-digit vs. low-single digit annualized returns)

Page 21

S&P 500 P/E vs.

10-Year Returns

S&P 500 Price/Earnings

S&

P 5

00 1

0-Y

ear

An

nu

alized

Retu

rn

R² = 0.86

= month

0%

2%

4%

6%

8%

10%

12%

4% 5% 6% 7% 8% 9% 10% 11% 12%

BAA Bond Yield vs.

U.S. Aggregate Bond Returns

R² = 0.92

Barc

lays U

.S. A

gg

reg

ate

Bo

nd

In

dex

An

nu

alized

Retu

rn

Moody’s BAA Corporate Bond Yield

Valuation

The Single Greatest Predictor of Future Stock Market Returns

= current

This presentation is directed only at professional investors as defined by the MIFID. It should not be read by retail investors.

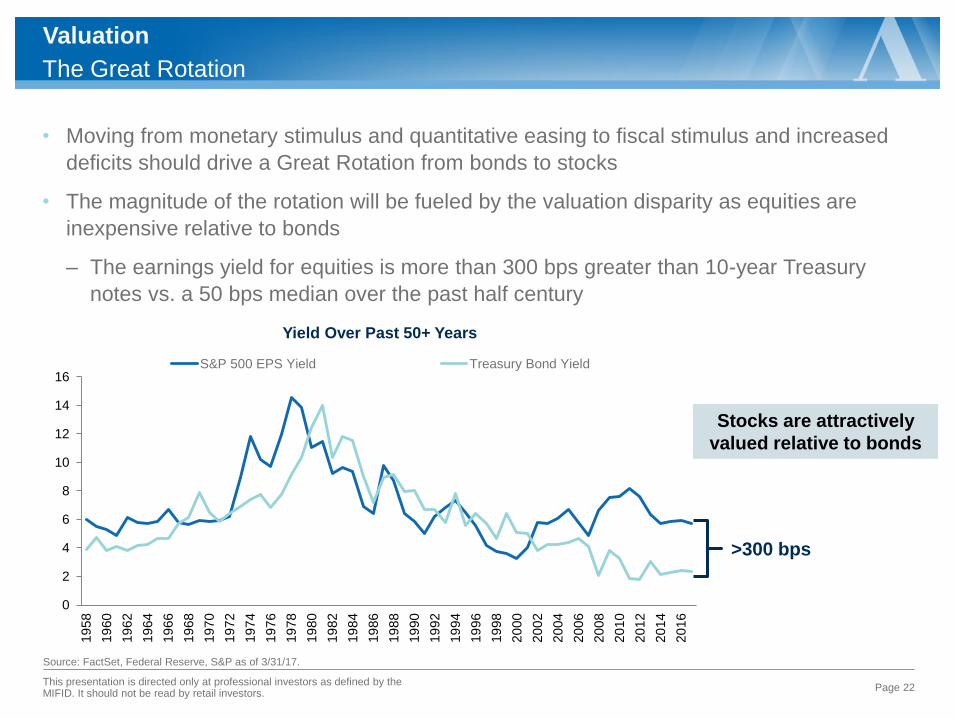

The Great Rotation

Valuation

Page 22

Source: FactSet, Federal Reserve, S&P as of 3/31/17.

• Moving from monetary stimulus and quantitative easing to fiscal stimulus and increased

deficits should drive a Great Rotation from bonds to stocks

• The magnitude of the rotation will be fueled by the valuation disparity as equities are

inexpensive relative to bonds

‒ The earnings yield for equities is more than 300 bps greater than 10-year Treasury

notes vs. a 50 bps median over the past half century

0

2

4

6

8

10

12

14

16

19

58

19

60

19

62

19

64

19

66

19

68

19

70

19

72

19

74

19

76

19

78

19

80

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

20

12

20

14

20

16

S&P 500 EPS Yield Treasury Bond Yield

>300 bps

Yield Over Past 50+ Years

Stocks are attractively

valued relative to bonds

This presentation is directed only at professional investors as defined by the MIFID. It should not be read by retail investors.

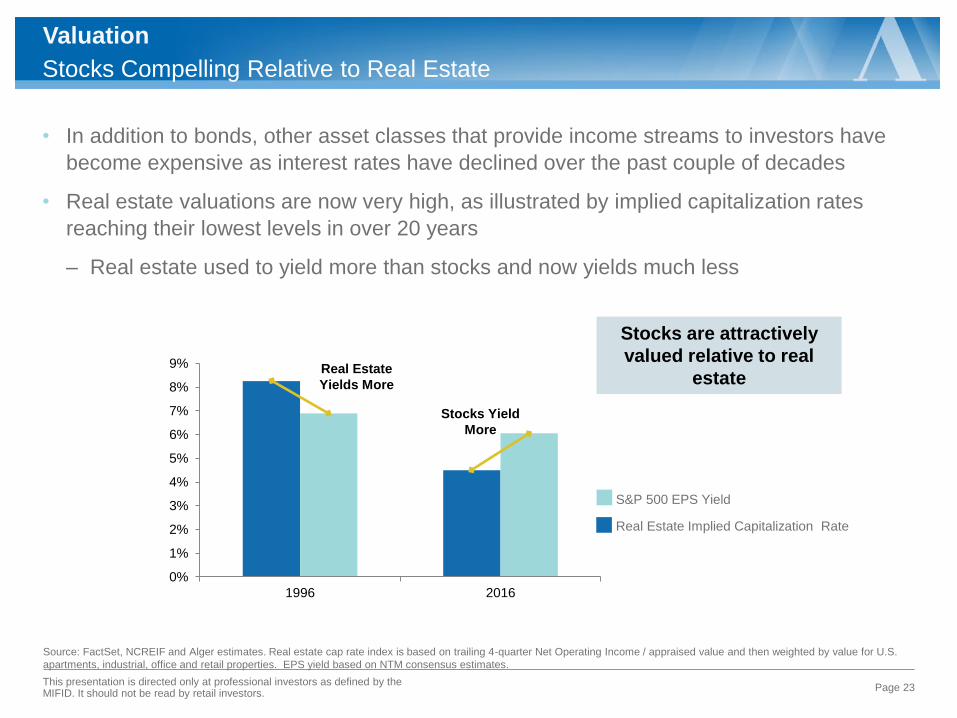

Stocks Compelling Relative to Real Estate

Valuation

Page 23 This presentation is directed only at professional investors as defined by the MIFID. It should not be read by retail investors.

Source: FactSet, NCREIF and Alger estimates. Real estate cap rate index is based on trailing 4-quarter Net Operating Income / appraised value and then weighted by value for U.S.

apartments, industrial, office and retail properties. EPS yield based on NTM consensus estimates.

• In addition to bonds, other asset classes that provide income streams to investors have

become expensive as interest rates have declined over the past couple of decades

• Real estate valuations are now very high, as illustrated by implied capitalization rates

reaching their lowest levels in over 20 years

‒ Real estate used to yield more than stocks and now yields much less

Stocks are attractively

valued relative to real

estate

S&P 500 EPS Yield

Real Estate Implied Capitalization Rate

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

1996 2016

Real Estate

Yields More

Stocks Yield

More

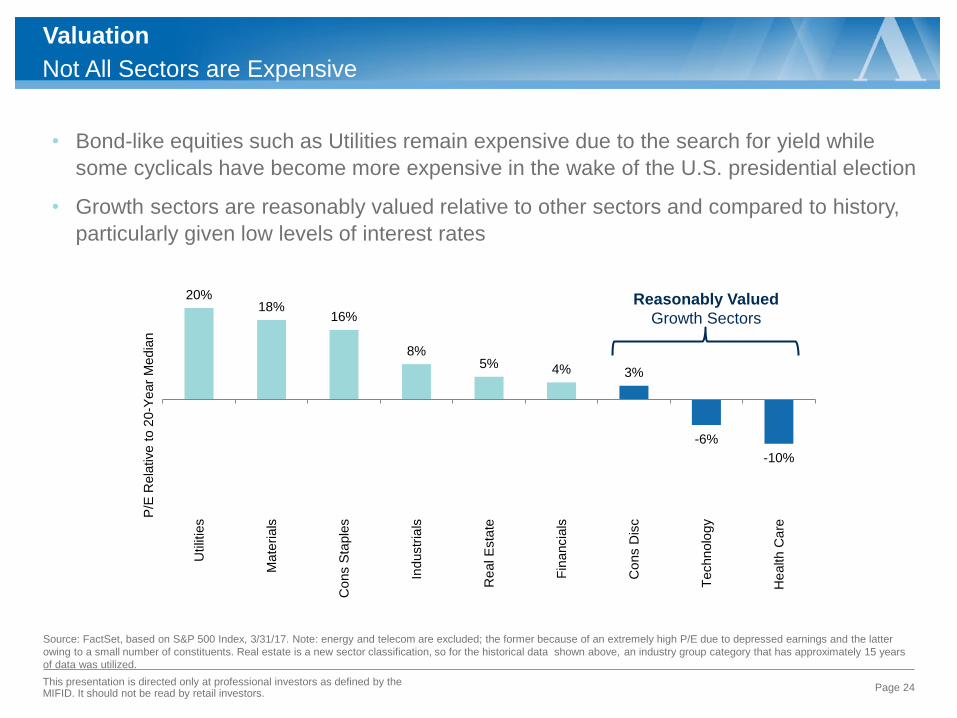

Not All Sectors are Expensive

Valuation

Page 24

Source: FactSet, based on S&P 500 Index, 3/31/17. Note: energy and telecom are excluded; the former because of an extremely high P/E due to depressed earnings and the latter

owing to a small number of constituents. Real estate is a new sector classification, so for the historical data shown above, an industry group category that has approximately 15 years

of data was utilized.

• Bond-like equities such as Utilities remain expensive due to the search for yield while

some cyclicals have become more expensive in the wake of the U.S. presidential election

• Growth sectors are reasonably valued relative to other sectors and compared to history,

particularly given low levels of interest rates

20%

18% 16%

8% 5% 4% 3%

-6%

-10%

Utilit

ies

Ma

teri

als

Co

ns S

taple

s

Industr

ials

Re

al E

sta

te

Fin

ancia

ls

Co

ns D

isc

Techn

olo

gy

He

alth C

are

Reasonably Valued

Growth Sectors

P/E

Rela

tive t

o 2

0-Y

ear

Media

n

This presentation is directed only at professional investors as defined by the MIFID. It should not be read by retail investors.

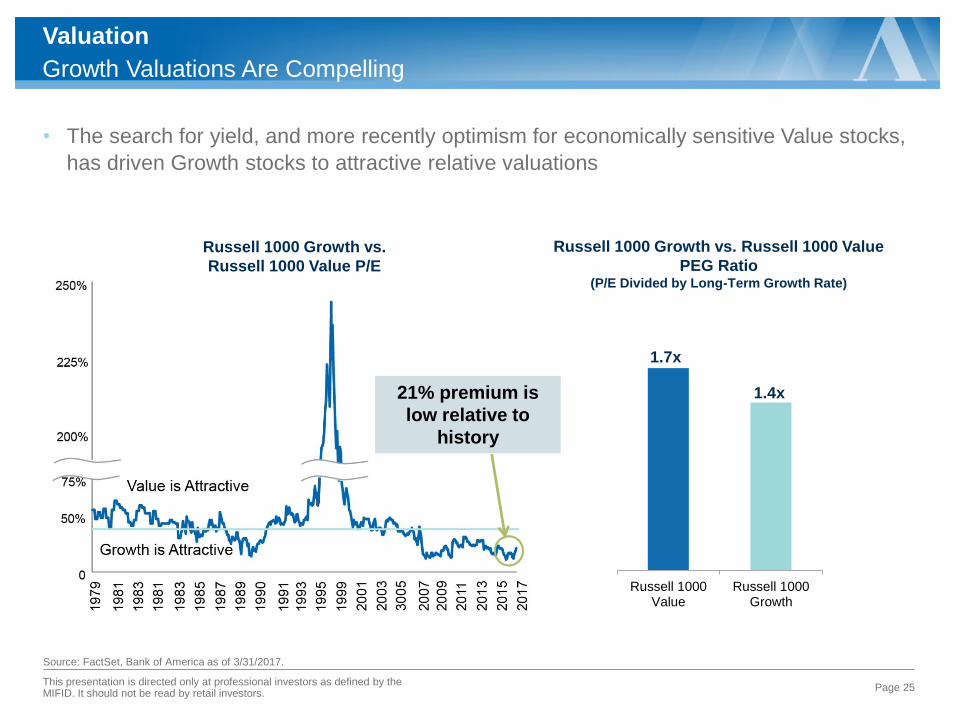

Growth Valuations Are Compelling

Valuation

Page 25

Source: FactSet, Bank of America as of 3/31/2017.

• The search for yield, and more recently optimism for economically sensitive Value stocks,

has driven Growth stocks to attractive relative valuations

This presentation is directed only at professional investors as defined by the MIFID. It should not be read by retail investors.

Russell 1000 Growth vs. Russell 1000 Value

PEG Ratio (P/E Divided by Long-Term Growth Rate)

Russell 1000Value

Russell 1000Growth

1.7x

1.4x

Russell 1000 Growth vs.

Russell 1000 Value P/E

21% premium is

low relative to

history

0

5

10

15

20

25

30

0 5 10 15

P/E

10-Year Yield

S&P 500 NTM P/E vs. 10-Yr Treasury Note Yield 1950-2016

= Year

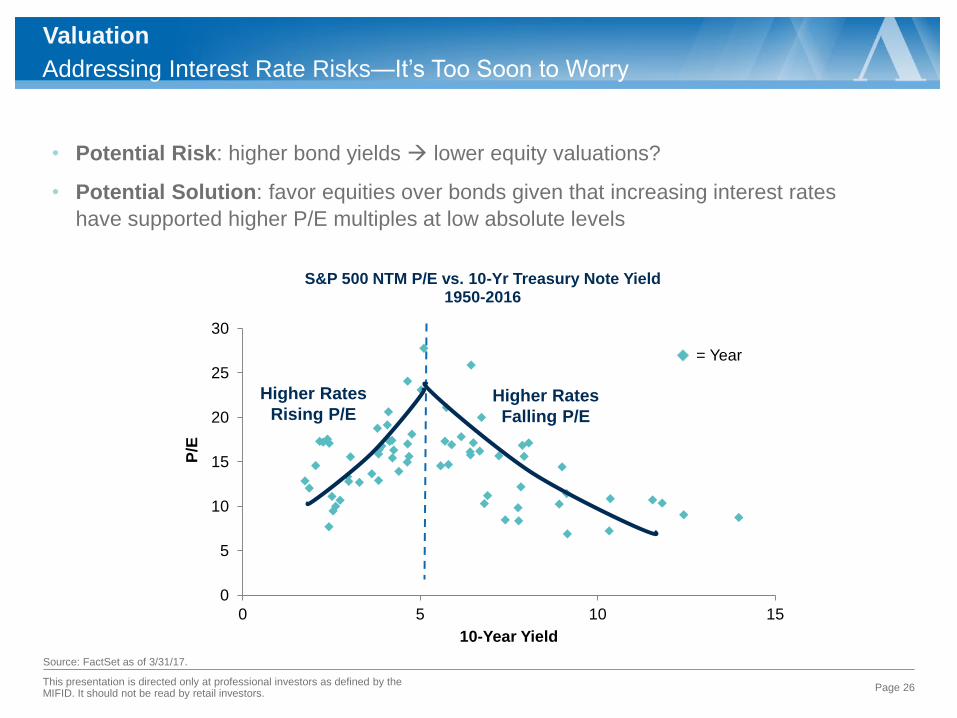

Addressing Interest Rate Risks—It’s Too Soon to Worry

Valuation

Page 26

Source: FactSet as of 3/31/17.

Higher Rates

Rising P/E Higher Rates

Falling P/E

• Potential Risk: higher bond yields lower equity valuations?

• Potential Solution: favor equities over bonds given that increasing interest rates

have supported higher P/E multiples at low absolute levels

This presentation is directed only at professional investors as defined by the MIFID. It should not be read by retail investors.

-7%

-6%

-5%

-4%

-3%

-2%

-1%

0%

1%

2%

19

96

19

97

19

98

19

99

20

00

20

01

20

03

20

04

20

05

20

06

20

07

20

08

20

10

20

11

20

12

20

13

20

14

20

15

20

17

Average

0%

1%

2%

3%

4%

5%

6%

7%

8%

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

S&P 500 Dividend Yield S&P 500 Buyback Yield

Total Yield

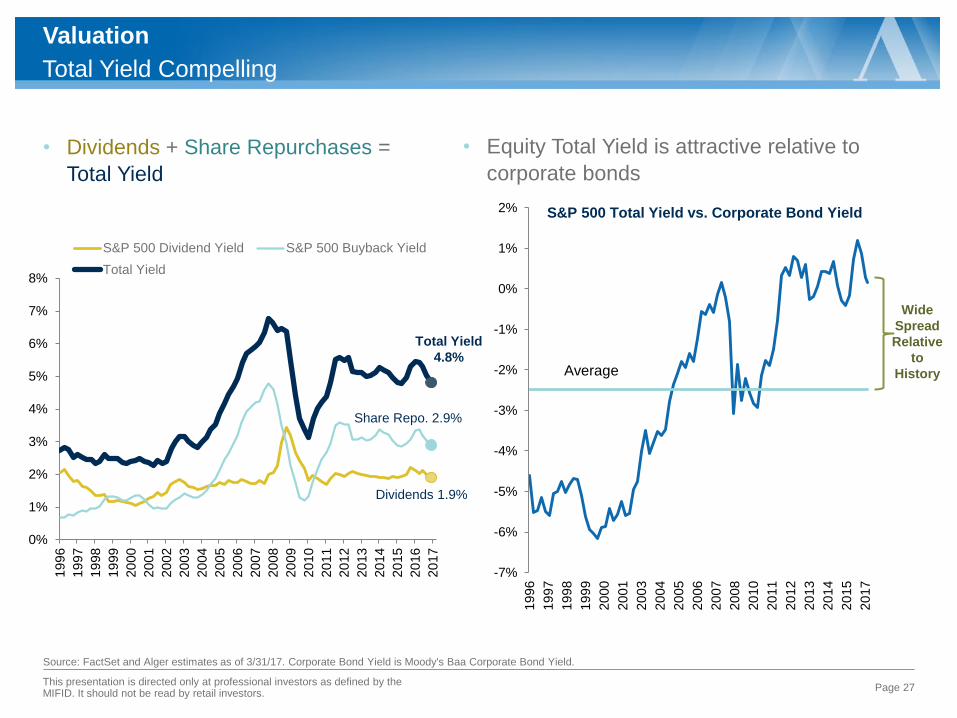

Total Yield Compelling

Valuation

Page 27

Source: FactSet and Alger estimates as of 3/31/17. Corporate Bond Yield is Moody's Baa Corporate Bond Yield.

• Dividends + Share Repurchases =

Total Yield

• Equity Total Yield is attractive relative to

corporate bonds

Share Repo. 2.9%

Total Yield

4.8%

Dividends 1.9%

Wide

Spread

Relative

to

History

S&P 500 Total Yield vs. Corporate Bond Yield

This presentation is directed only at professional investors as defined by the MIFID. It should not be read by retail investors.

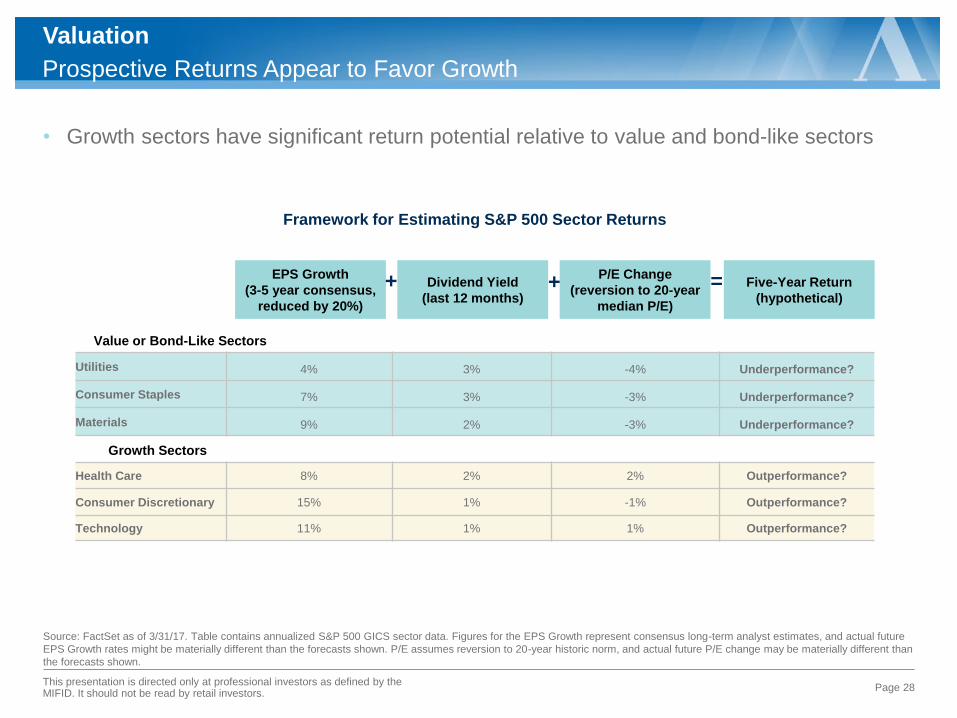

Prospective Returns Appear to Favor Growth

Valuation

Page 28

Source: FactSet as of 3/31/17. Table contains annualized S&P 500 GICS sector data. Figures for the EPS Growth represent consensus long-term analyst estimates, and actual future

EPS Growth rates might be materially different than the forecasts shown. P/E assumes reversion to 20-year historic norm, and actual future P/E change may be materially different than

the forecasts shown.

• Growth sectors have significant return potential relative to value and bond-like sectors

EPS Growth

(3-5 year consensus,

reduced by 20%)

Dividend Yield

(last 12 months)

P/E Change

(reversion to 20-year

median P/E)

Five-Year Return

(hypothetical) + + =

Framework for Estimating S&P 500 Sector Returns

Value or Bond-Like Sectors

Utilities 4% 3% -4% Underperformance?

Consumer Staples 7% 3% -3% Underperformance?

Materials 9% 2% -3% Underperformance?

Growth Sectors

Health Care 8% 2% 2% Outperformance?

Consumer Discretionary 15% 1% -1% Outperformance?

Technology 11% 1% 1% Outperformance?

This presentation is directed only at professional investors as defined by the MIFID. It should not be read by retail investors.

Disclosure

The views expressed are the views of Alger Management, Ltd. as of March 2017. Alger has used sources of information which it believes to be

reliable; however, this publication is not intended to be and does not constitute investment advice. These views are subject to change at any time and

they do not guarantee the future performance of the markets, any security, or any funds managed by Fred Alger Management, Inc. These views

should not be considered a recommendation to purchase or sell securities. Individual securities or industries/sectors mentioned, if any, should be

considered in the context of an overall portfolio and therefore reference to them should not be construed as a recommendation or offer to purchase or

sell securities. References to or implications regarding the performance of an individual security or group of securities are not intended as an

indication of the characteristics or performance of any specific sector, industry, security, group of securities, or a portfolio and are for illustrative

purposes only.

Risk Disclosures: Investing in the stock market involves gains and losses and may not be suitable for all investors. Growth stocks tend to be more

volatile than other stocks as the prices of growth stocks tend to be higher in relation to their companies’ earnings and may be more sensitive to

market, political and economic developments.

The S&P 500 Index is an unmanaged index generally representative of the U.S. stock market without regard to company size. The Russell 1000®

Growth Index is an unmanaged index designed to measure the performance of the largest 1000 companies in the Russell 3000 Index with higher

price-to-book ratios and higher forecasted growth values. The Russell 1000 Value Index measures the performance of those Russell 1000

companies with lower price-to-book ratios and lower forecasted growth values. The Russell 2000 Growth Index is an unmanaged index generally

representative of common stocks designed to track performance of small-capitalization companies with greater than average growth orientation. The

Russell 2000 Value Index is an unmanaged index generally representative of the small-cap value segment of the U.S. equity universe and measures

the performance of Russell 2000 companies with lower price-to-book ratios and lower forecasted growth values. The Russell 3000® Growth Index is

an unmanaged index designed to measure the performance of those Russell 3000® Index companies with higher price-to-book ratios and higher

forecasted growth values. The Russell 3000 Value Index is an unmanaged index generally representative of stocks from the Russell 3000 Index with

lower price-to-book ratios and lower expected growth rates. The indices presented are provided for illustrative purposes, reflect the reinvestment of

dividends and do not assess fees and expenses that would have the effect of reducing returns. Investors cannot invest directly in any index. The

index performance does not represent the returns of any portfolio advised by Fred Alger Management, Inc. and actual client results might differ

materially than the indices shown. Note that past performance is no guarantee of future results. Comparison to a different index might have

materially different results than those shown.

Alger Management, Ltd. (company house number 8634056, domiciled at 78 Brook Street, London W1K 5EF, UK) is authorised and regulated by the

Financial Conduct Authority, for the distribution of regulated financial products and services. La Française AM International has a signed agreement

with Alger Management Ltd, whereby La Française AM International is authorized to distribute Fred Alger Management Inc. products in Europe.

ALCAPPRESWIN-0417

Alger Management, Ltd. • 78 Brook Street, London, W1K 5EF • www.alger.com

Page 29 This presentation is directed only at professional investors as defined by the MIFID. It should not be read by retail investors.