Embed Size (px)

Citation preview

Capital Markets Infrastructure:

What Is the New Normal After COVID-19?

Consider Everything

BNY Mellon

Perspectives

Capital Markets Infrastructure:

What Is the New Normal After COVID-19?The world’s capital markets infrastructure (CMI) has demonstrated impressive resilience during the period of COVID-19 —induced volatility. While CMI service providers can be proud of the industry response during a time of great pressure, the lessons of the COVID-19 crisis can help to prepare for further shocks, which (based on previous crises) could still occur. This paper, written by BNY Mellon with contributions and data from SWIFT, assesses the key themes that should drive CMI development in the coming years, so that it can further embed resiliency and strengthen the overall capital markets community.

Through times of calm and crisis, BNY Mellon’s perspective has made us the trusted steward of the financial system. To help our clients make stronger decisions, our experts explore the many angles of our industry in our Perspectives Content Series.

Capital Markets Infrastructure: What is the New Normal After COVID-19? 3

How CMI withstood the COVID-19 crisisThe COVID-19 pandemic, and the government-imposed lockdowns introduced to stem its spread, created unprecedented disruption to people’s lives and jobs, and to global economic activity. Capital markets responded in an agile manner, even as market participants moved to remote working. The pandemic ended the 11-year U.S. stock market bull run and prompted the quickest drawdown on record. As volatility increased in financial markets, there was a brief spike in redemptions while investors sold stocks and piled into cash or fixed income markets.

Overall, the period was the most extreme stress event since the 2007–09 global financial crisis. SWIFT data shows that message volumes in March 2020 were four times normal levels (Fig. 1) while transaction sizes slumped by 46% during the first half of 2020, as the industry came under pressure.

WHAT IS CAPITAL MARKETS INFRASTRUCTURE?

If we imagine the global financial markets as a vast network, with money in various forms in constant motion, then capital markets infrastructure (CMI) consists of all of the components that make this flow possible. CMI providers offer participants in capital markets critical elements, including global trading access and connectivity, data and analytics, process efficiency, and regulatory, risk and compliance management.

Historically, these providers were mainly traditional exchange complexes, clearinghouses, and depositaries, but the landscape of participants has broadened over time to include alternative exchange venues, inter-broker dealers/banks, and information providers.

Fig. 1

4

CMI providers remained resoluteDespite sharply increased trading volumes, the industry—including exchanges, clearinghouses, central depositories, alternative exchange venues, inter-broker dealers/banks, custodians, collateral management and information providers—all functioned well. While large margin calls impacted clearing member banks’ liquidity, default rates at clearinghouses were low compared with the 2007–09 global financial crisis.

The resilience of capital markets infrastructure indicates that the post-crisis reforms of the financial markets worked as intended. Being the focus of efforts to manage volatility and defaults (both from an infrastructure and regulatory perspective), capital markets infrastructure served as a breakwater, helping to absorb the massive shocks to capital markets.

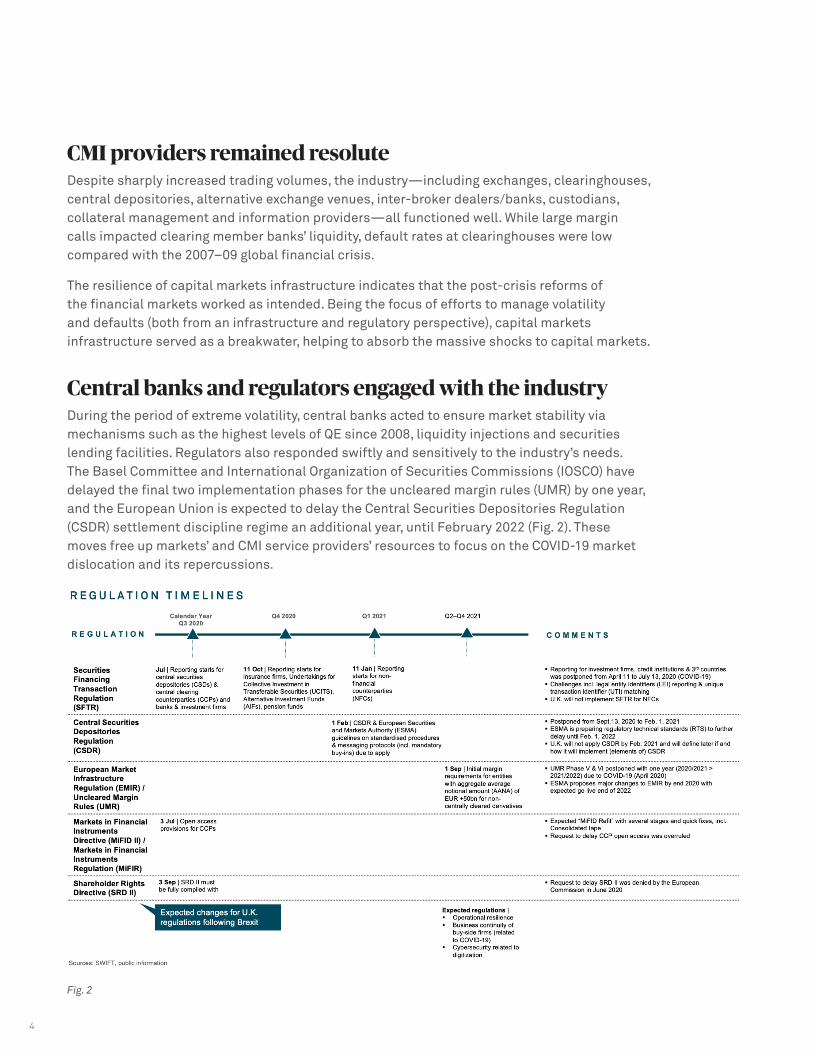

Central banks and regulators engaged with the industryDuring the period of extreme volatility, central banks acted to ensure market stability via mechanisms such as the highest levels of QE since 2008, liquidity injections and securities lending facilities. Regulators also responded swiftly and sensitively to the industry’s needs. The Basel Committee and International Organization of Securities Commissions (IOSCO) have delayed the final two implementation phases for the uncleared margin rules (UMR) by one year, and the European Union is expected to delay the Central Securities Depositories Regulation (CSDR) settlement discipline regime an additional year, until February 2022 (Fig. 2). These moves free up markets’ and CMI service providers’ resources to focus on the COVID-19 market dislocation and its repercussions.

Fig. 2

Capital Markets Infrastructure: What is the New Normal After COVID-19? 5

Notably, during the crisis, central banks—a crucial component of the CMI fabric—engaged deeply and intensively with CMI service providers. For example, the Federal Reserve and BNY Mellon interacted systematically on the clearance of U.S. government securities, while SWIFT regularly connected with market infrastructures, including regulators, both directly and via monthly COVID-19 traffic tracker reports.

How behavior evolved during the crisisThe COVID-19 crisis and resultant heightened volatility increased the exposure of clearinghouses, resulting in regular calls to market participants for collateral to cover heightened margin variation—at times intraday. Many market participants sought to enhance their liquidity in order to manage further potential volatility. Because variation margins are usually met with cash, the demand for cash, as well as highly liquid assets such as U.S. Treasuries, bunds or gilts—which can be easily converted to cash—rose sharply. There was also an increased focus on balance sheet management and greater use of funding programs by market participants to further bolster liquidity. CMI providers played a critical role during this time by providing insights about liquid positions and efficient movement and allocation of collateral.

More generally, there have been fundamental changes to how capital market participants and CMI providers interact as a result of the COVID-19 crisis. Most obviously, with remote working predominant, physical client and industry engagements have been redirected to digital channels. For example, like many other flagship industry events, SWIFT’s annual Sibos event, where the community engages with CMI service providers, will this year be digital. In an effort to keep the community connected, Sibos 2020, scheduled for October 5–8, is being offered free to SWIFT community members.

In the medium term, banks and other financial institutions are shoring up their balance sheets and preparing for potential M&A activity. Some fintechs’ economics have been impacted by adverse market conditions and the challenges of client interaction; they may become acquisition targets. Similarly, financial institutions struggling with their cost/income ratio might consider selling or exiting some business lines or reducing their geographic footprint, prompting possible further industry consolidation.

6

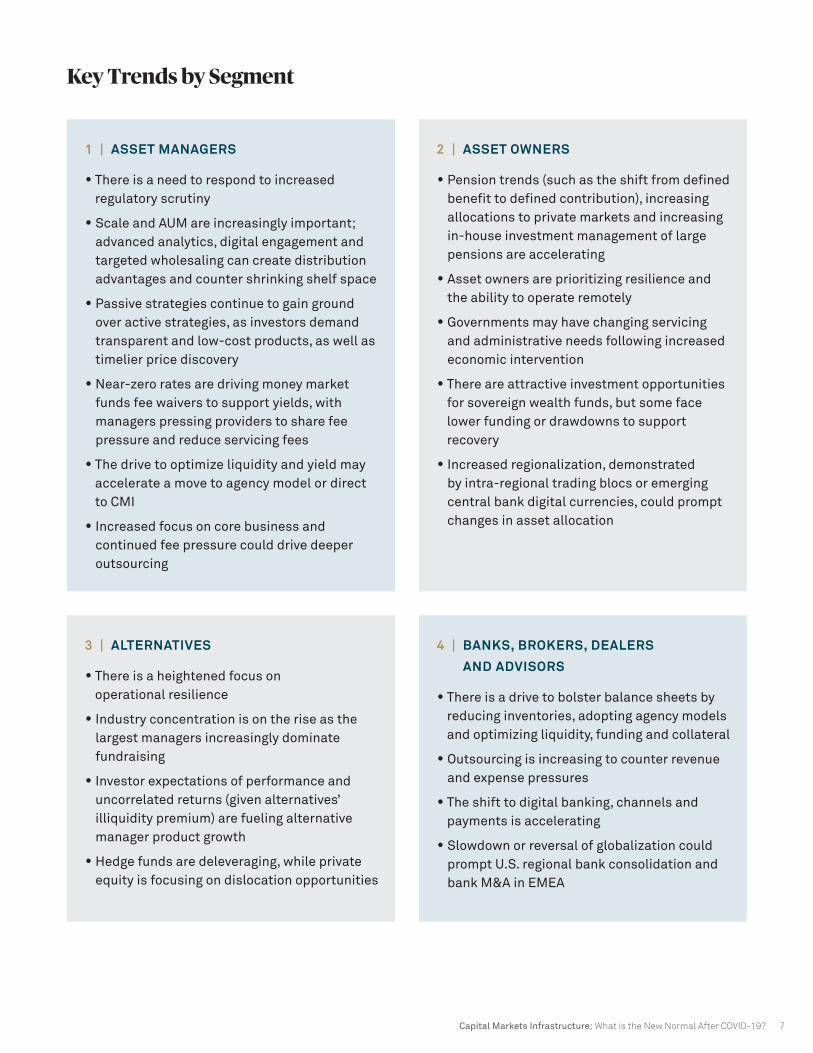

What’s driving market behavior?The COVID-19 crisis and consequent market volatility has played out against a backdrop of a fast-changing financial services environment. The surge of digitalization, combined with regulations, competitive dynamics and evolving investor behavior, are driving a transformation of various financial services segments. Some of the key drivers and trends in each segment, which may be further accelerated by the COVID-19 dislocation, are summarized here.

Capital Markets Infrastructure: What is the New Normal After COVID-19? 7

1 | ASSET MANAGERS

• There is a need to respond to increased regulatory scrutiny

• Scale and AUM are increasingly important; advanced analytics, digital engagement and targeted wholesaling can create distribution advantages and counter shrinking shelf space

• Passive strategies continue to gain ground over active strategies, as investors demand transparent and low-cost products, as well as timelier price discovery

• Near-zero rates are driving money market funds fee waivers to support yields, with managers pressing providers to share fee pressure and reduce servicing fees

• The drive to optimize liquidity and yield may accelerate a move to agency model or direct to CMI

• Increased focus on core business and continued fee pressure could drive deeper outsourcing

3 | ALTERNATIVES

• There is a heightened focus on operational resilience

• Industry concentration is on the rise as the largest managers increasingly dominate fundraising

• Investor expectations of performance and uncorrelated returns (given alternatives’ illiquidity premium) are fueling alternative manager product growth

• Hedge funds are deleveraging, while private equity is focusing on dislocation opportunities

4 | BANKS, BROKERS, DEALERS

AND ADVISORS

• There is a drive to bolster balance sheets by reducing inventories, adopting agency models and optimizing liquidity, funding and collateral

• Outsourcing is increasing to counter revenue and expense pressures

• The shift to digital banking, channels and payments is accelerating

• Slowdown or reversal of globalization could prompt U.S. regional bank consolidation and bank M&A in EMEA

2 | ASSET OWNERS

• Pension trends (such as the shift from defined benefit to defined contribution), increasing allocations to private markets and increasing in-house investment management of large pensions are accelerating

• Asset owners are prioritizing resilience and the ability to operate remotely

• Governments may have changing servicing and administrative needs following increased economic intervention

• There are attractive investment opportunities for sovereign wealth funds, but some face lower funding or drawdowns to support recovery

• Increased regionalization, demonstrated by intra-regional trading blocs or emerging central bank digital currencies, could prompt changes in asset allocation

Key Trends by Segment

8

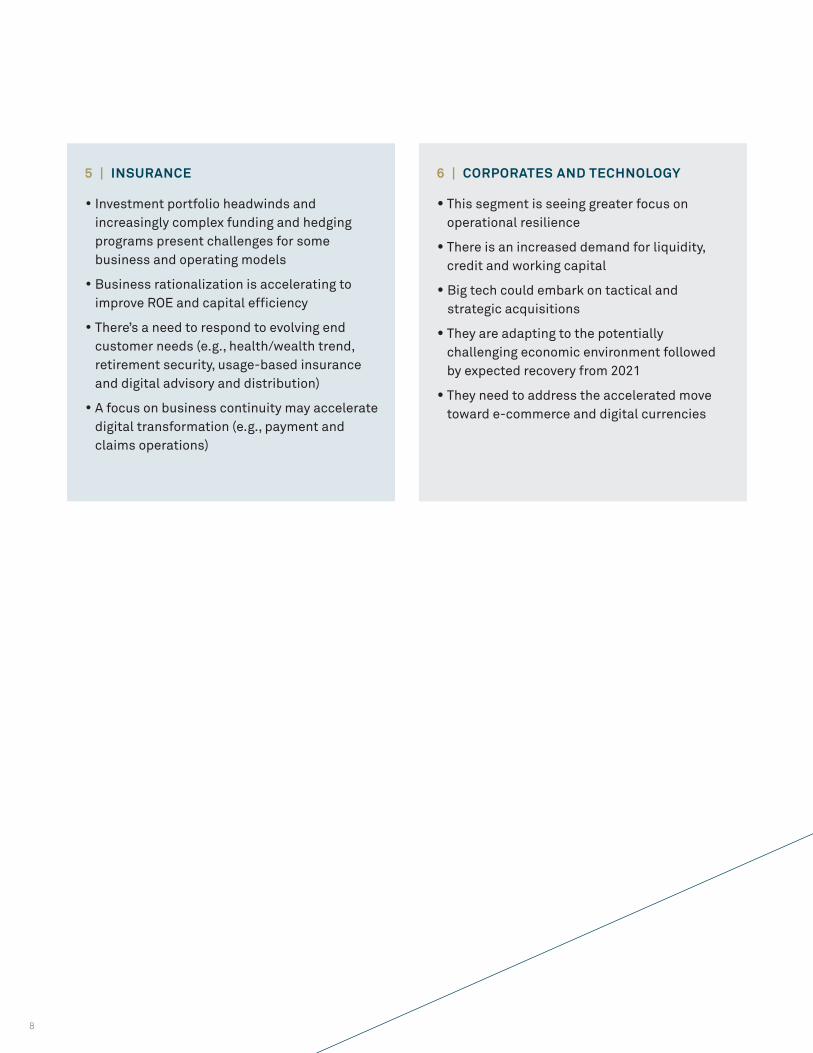

5 | INSURANCE

• Investment portfolio headwinds and increasingly complex funding and hedging programs present challenges for some business and operating models

• Business rationalization is accelerating to improve ROE and capital efficiency

• There’s a need to respond to evolving end customer needs (e.g., health/wealth trend, retirement security, usage-based insurance and digital advisory and distribution)

• A focus on business continuity may accelerate digital transformation (e.g., payment and claims operations)

6 | CORPORATES AND TECHNOLOGY

• This segment is seeing greater focus on operational resilience

• There is an increased demand for liquidity, credit and working capital

• Big tech could embark on tactical and strategic acquisitions

• They are adapting to the potentially challenging economic environment followed by expected recovery from 2021

• They need to address the accelerated move toward e-commerce and digital currencies

Capital Markets Infrastructure: What is the New Normal After COVID-19? 9

How can CMI providers respond to a changing industry?Changes in various financial services segments and developments in the CMI world, including more effective use of data and deeper outsourcing, were well under way as 2020 began. The COVID-19 crisis will further reinforce and accelerate many of these. While it is important that industry and regulators assess the resilience of the financial markets, CMI’s performance during the COVID-19 crisis was robust, as a result of the reforms that followed the 2007–09 global financial crisis.

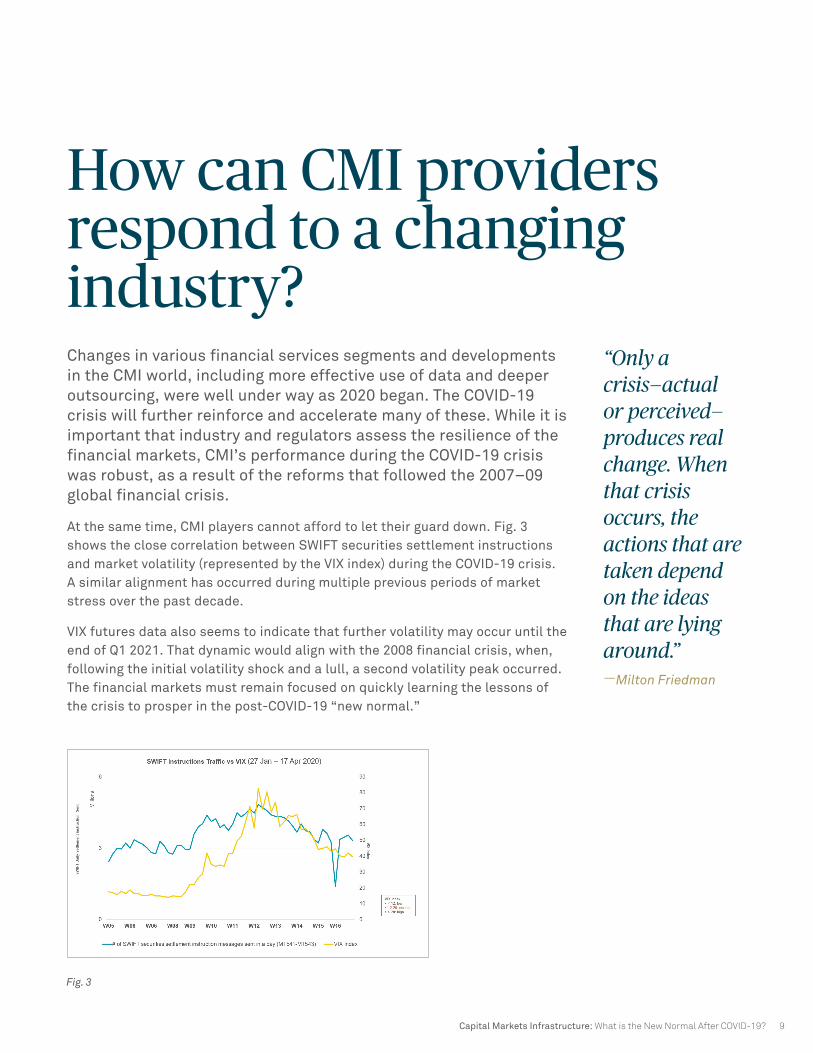

At the same time, CMI players cannot afford to let their guard down. Fig. 3shows the close correlation between SWIFT securities settlement instructionsand market volatility (represented by the VIX index) during the COVID-19 crisis.A similar alignment has occurred during multiple previous periods of marketstress over the past decade.

VIX futures data also seems to indicate that further volatility may occur until the end of Q1 2021. That dynamic would align with the 2008 financial crisis, when, following the initial volatility shock and a lull, a second volatility peak occurred. The financial markets must remain focused on quickly learning the lessons of the crisis to prosper in the post-COVID-19 “new normal.”

“Only a crisis—actual or perceived—produces real change. When that crisis occurs, the actions that are taken depend on the ideas that are lying around.”— Milton Friedman

Fig. 3

10

Compared with the 2007–09 global financial crisis, the COVID-19 market dislocation demonstrated to an even greater extent the criticality of rapid action and response for markets, players and CMI providers. The following aspects of the financial markets and CMI interaction are of particular importance.

Streamlined communicationThe COVID-19 crisis has shown the value of speed when it comes to communications. Transparent, frequent and flexible client and regulatory communications, outside of traditional reporting cycles, are likely to become a prerequisite for market participants to a greater extent. At the same time, many asset managers, custodians and vendors will focus on front-to-back offerings, using post-trade information in new ways, including improving reporting and generating insights.

Further harmonization and standardization of data and messaging are critical to enhance markets’ responsiveness in times of heightened volatility. There are no magic bullets. But recent advancements in community APIs to enable better and timelier communication, in areas such as the net asset value of a fund and status reports, are advancing the industry toward streamlined and faster communications.

Increasing digitization of markets—for example, corporate bonds and repo—also helps to streamline the interaction among market players. Although significant volumes in such markets remain OTC because of limited liquidity, new technology deployed by CMI players has the potential to overcome these challenges by lowering cost and enhancing communication flows, ultimately benefiting the entire market.

Enhanced collaborationVolatility shocks during the COVID-19 crisis brought credit, collateral and liquidity management to the fore for asset managers, banks, brokers, dealers, advisors and insurance firms, as demonstrated by the criticality of meeting margin calls, at times on tight deadlines.

Collateral and liquidity management efficiency are offered in the market by specialized CMI players such as BNY Mellon, providing access to a wide and global ecosystem of collateral takers and givers and vast pools of collateral. Further broadening the reach and depth of these ecosystems, as well as offering institutions an aggregated view of their exposures, positions and allocation optimization, enhances collateral and liquidity at market level and hence resilience in times of heightened volatility.

Capital Markets Infrastructure: What is the New Normal After COVID-19? 11

Corresponding operating models are evolving, seeking to enhance connectivity between ecosystems and collateral pools, further strengthening the overall collateral and liquidity environment to withstand times of volatility. There should be an increased focus on building partnerships, broadening collaboration, introducing micro-service technology (single-function modules with well-defined interfaces and operations) and open business architecture. By combining forces, CMI providers can give clients additional flexibility and improve overall market efficiency.

Standardized dataData is at the core of the pre- to post-trade chain, and has proved critical to managing the COVID-19 crisis and instrumental to regulatory reporting and compliance. The likelihood of trade fails and subsequent fines under the upcoming European Central Securities Depositories Regulation (CSDR) settlement discipline regime increases with incomplete or outdated data. Continued efforts to standardize data would help avoid such outcomes. SWIFT, collaborating with the Securities Market Practice Group, has updated its messages and continues to support the evolution of market practices to reflect new CSDR requirements.

High-quality standardized data has a key role in driving efficiency in CMI flows as digitization progresses, while timely and granular multi-asset data is essential to optimally defining investment strategies, e.g., incorporating environmental, social and governance (ESG) criteria. Standardized qualitative data also powers deployment of newer technologies such as artificial intelligence and machine learning, facilitating predictive and prescriptive analytics. Such data also fuels the various platforms that aggregate information and optimally direct flows, while providing additional value-added services such as collateral management, billing reconciliation and analytical insights gleaned from those flows, so that market participants can make faster and better-informed decisions.

Emerging innovations such as distributed ledger technology (DLT) and tokenization, underpinned by qualitative data, will allow multiple parties to see the same record on a real-time basis, eliminating the need for labor-intensive data reconciliation. Current core systems and new technology ecosystems such as DLT will require agreed-upon data definitions to be interoperable. Such common data dictionaries endorsed by the industry can help foster technological innovation.

12

Business and market resiliencyThe pandemic has vividly highlighted opportunities for improving resiliency. Both the COVID-19 crisis and the various trends taking place across financial services segments are likely to encourage many firms to reassess their existing operational setups and processes, with the objective of further enhancing their resiliency. Firms may seek to stress test their operating models beyond current stretched scenarios, in areas such as remote working capabilities, digitalization and cloud-enabled infrastructure, and asset diversification toward alternatives. Risk management models will need to incorporate new and emerging investment factors, such as the rate of COVID-19 infections.

Systems access rights and remote working made it difficult for the financial industry to manage nonautomated processes in particular. Where regulation permits, adoption of cloud and hosted solutions, including SWIFT’s Alliance Cloud, seems certain to increase. Going forward, collaboration between CMI providers and the asset management industry will help enhance business continuity by advancing cloud and hosted solutions and appropriate backups. In addition, CMI providers can help market players to apply best practices in cyber and fraud prevention, which has become increasingly important given remote working.

Similarly, the COVID-19 crisis may accelerate the outsourcing of post-trade activities, which may not be seen as core to asset managers and asset owners, as part of their efforts to improve business resiliency. Asset managers and asset owners increasingly see the benefit of outsourcing middle- and back-office operations, which do not create value and can be done more efficiently by dedicated players. Outsourcing continues to free up the buy side for its core activity. As such, it provides enhanced efficiency for asset managers and asset owners, and the ability to better manage potential future shocks.

Advisory services are a potential next step in this continuum, one can envisage increasingly by CMI service providers. Once market participants recognize the value of outsourcing non-core functions to dedicated service providers, it is easier for CMI players to develop and provide market services such as balance sheet optimization, risk and performance analytics, and strategic advice regarding “new normal” investment strategies to asset owners, and advisory for holistic end-client service models to insurance firms, for example. Ultimately, there is growing acceptance that in an ever more competitive environment, where efficiency is paramount, asset managers and owners must focus on core activities to generate real value.

Capital Markets Infrastructure: What is the New Normal After COVID-19? 13

Safe haven status remains CMI providers’ greatest strengthCapital markets infrastructures have the characteristics of a public good that go beyond being just a business: They safeguard the broader financial system. During the COVID-19 market dislocation, the CMI community demonstrated robustness and resilience. They were a safe haven on which market participants relied to withstand the shocks of heightened volatility.

To a large extent, this safe haven status derives from robust and resilient operating models at scale, as well as depth and breadth. For instance, BNY Mellon’s status as a global systemically important bank (G-SIFI) and global collateral management platform, and SWIFT’s role as a global provider of secure financial messaging services, are valued by the markets because they provide solidity and the ability to maintain infrastructure during challenging times.

As financial markets further evolve, considerations of safety and resiliency of market participants and the broader financial system will continue to determine the actions of the CMI community. Safeguarding clients, continued awareness of their challenges, and standing by them during tough times are the hallmarks of successful CMI businesses.

The COVID-19 crisis has highlighted how CMI can rise to the challenge. CMI players take their responsibilities seriously, and their resilience and maturity bode well for the ongoing evolution of the CMI community as we move toward a post-COVID-19 “new normal.”

For more on capital markets infrastructure's resilience through volatility, see "The Pandemic Stress Test: U.S. Government Securities Clearance & Repo.”

bnymellon.com

BNY Mellon is the corporate brand of The Bank of New York Mellon Corporation and may be used as a generic term to reference the corporation as a whole and/or its various group entities. This material and any products and services may be issued or provided under various brand names of BNY Mellon in various countries by duly authorized and regulated subsidiaries, affiliates, and joint ventures of BNY Mellon, which may include any of those listed below:

The Bank of New York Mellon, a banking corporation organized pursuant to the laws of the State of New York, whose registered office is at 240 Greenwich St, NY, NY 10286, USA. The Bank of New York Mellon is supervised and regulated by the New York State Department of Financial Services and the US Federal Reserve and is authorized by the Prudential Regulation Authority (“PRA”) (Firm Reference Number: 122467).

The Bank of New York Mellon operates in the UK through its London branch (UK companies house numbers FC005522 and BR000818) at One Canada Square, London E14 5AL and is subject to regulation by the Financial Conduct Authority (“FCA”) at 12 Endeavour Square, London, E20 1JN, UK and limited regulation by the PRA at Bank of England, Threadneedle St, London, EC2R 8AH, UK. Details about the extent of our regulation by the PRA are available from us on request.

The Bank of New York Mellon SA/NV, a Belgian limited liability company, registered in the RPM Brussels with company number 0806.743.159, whose registered office is at 46 Rue Montoyerstraat, B-1000 Brussels, Belgium, authorized and regulated as a significant credit institution by the European Central Bank (“ECB”) at Sonnemannstrasse 20, 60314 Frankfurt am Main, Germany, and the National Bank of Belgium (“NBB”) at Boulevard de Berlaimont/de Berlaimontlaan 14, 1000 Brussels, Belgium, under the Single Supervisory Mechanism and by the Belgian Financial Services and Markets Authority (FSMA) at Rue du Congrès/Congresstraat 12-14, 1000 Brussels, Belgium for conduct of business rules, and is a subsidiary of The Bank of New York Mellon.

The Bank of New York Mellon SA/NV operates in Ireland through its Dublin branch at Riverside II, Sir John Rogerson’s Quay Grand Canal Dock, Dublin 2, D02KV60, Ireland and is registered with the Companies Registration Office in Ireland No. 907126 & with VAT No. IE 9578054E. The Bank of New York Mellon SA/NV, Dublin Branch is subject to limited additional regulation by the Central Bank of Ireland at New Wapping Street, North Wall Quay, Dublin 1, D01 F7X3, Ireland for conduct of business rules and registered with the Companies Registration Office in Ireland No. 907126 & with VAT No. IE 9578054E.

The Bank of New York Mellon SA/NV is trading in Germany as The Bank of New York Mellon SA/NV, Asset Servicing, Niederlassung Frankfurt am Main, and has its registered office at MesseTurm, Friedrich-Ebert-Anlage 49, 60327 Frankfurt am Main, Germany. It is subject to limited additional regulation by the Federal Financial Supervisory Authority (Bundesanstalt für Finanzdienstleistungsaufsicht, Marie-Curie-Str. 24-28, 60439 Frankfurt, Germany) under registration number 122721.

The Bank of New York Mellon SA/NV operates in the Netherlands through its Amsterdam branch at Strawinskylaan 337, WTC Building, Amsterdam, 1077 XX, the Netherlands. The Bank of New York Mellon SA/NV, Amsterdam Branch is subject to limited additional supervision by the Dutch Central Bank (“De Nederlandsche Bank” or “DNB”) on integrity issues only (registration number 34363596). DNB holds office at Westeinde 1, 1017 ZN Amsterdam, the Netherlands.

The Bank of New York Mellon SA/NV operates in Luxembourg through its Luxembourg branch at 2-4 rue Eugene Ruppert, Vertigo Building – Polaris, L- 2453, Luxembourg. The Bank of New York Mellon SA/NV, Luxembourg Branch is subject to limited additional regulation by the Commission de Surveillance du Secteur Financier at 283, route d’Arlon, L-1150 Luxembourg for conduct of business rules, and in its role as UCITS/AIF depositary and central administration agent.

The Bank of New York Mellon SA/NV operates in France through its Paris branch at 7 Rue Scribe, Paris, Paris 75009, France. The Bank of New York Mellon SA/NV, Paris Branch is subject to limitted additional regulation by Secrétariat Général de l’Autorité de Contrôle Prudentiel at Première Direction du Contrôle de Banques (DCB 1), Service 2, 61, Rue Taitbout, 75436 Paris Cedex 09, France (registration number (SIREN) Nr. 538 228 420 RCS Paris - CIB 13733).

The Bank of New York Mellon SA/NV operates in Italy through its Milan branch at Via Mike Bongiorno no. 13, Diamantino building, 5th floor, Milan, 20124, Italy. The Bank of New York Mellon SA/NV, Milan Branch is subject to limiteed additional regulation by Banca d’Italia - Sede di Milano at Divisione Supervisione Banche, Via Cordusio no. 5, 20123 Milano, Italy (registration number 03351).

The Bank of New York Mellon SA/NV operates in England through its London branch at 160 Queen Victoria Street, London EC4V 4LA, UK, registered in England and Wales with numbers FC029379 and BR014361. The Bank of New York Mellon SA/NV, London branch is authorized by the ECB (address above) and subject to limited regulation by the FCA (address above) and the PRA (address above).

Regulatory information in relation to the above BNY Mellon entities operating out of Europe can be accessed at the following website: https://www.bnymellon.com/RID.

The Bank of New York Mellon, Singapore Branch, is subject to regulation by the Monetary Authority of Singapore. For recipients of this information located in Singapore: This material has not been reviewed by the Monetary Authority of Singapore. The Bank of New York Mellon, Hong Kong Branch (a branch of a banking corporation organized and existing under the laws of the State of New York with limited liability), is subject to regulation by the Hong Kong Monetary Authority and the Securities & Futures Commission of Hong Kong.

The Bank of New York Mellon is exempt from the requirement to hold, and does not hold, an Australian financial services license as issued by the Australian Securities and Investments Commission under the Corporations Act 2001 (Cth) in respect of the financial services provided by it to persons in Australia. The Bank of New York Mellon is regulated by the New York State Department of Financial Services and the US Federal Reserve under Chapter 2 of the Consolidated Laws, The Banking Law enacted April 16, 1914 in the State of New York, which differs from Australian laws.

The Bank of New York Mellon has various other branches in the Asia-Pacific Region which are subject to regulation by the relevant local regulator in that jurisdiction.

The Bank of New York Mellon Securities Company Japan Ltd, as intermediary for The Bank of New York Mellon.

The Bank of New York Mellon, DIFC Branch, regulated by the Dubai Financial Services Authority (“DFSA”) and located at DIFC, The Exchange Building 5 North, Level 6, Room 601, P.O. Box 506723, Dubai, UAE, on behalf of The Bank of New York Mellon, which is a wholly-owned subsidiary of The Bank of New York Mellon Corporation.

Pershing is the umbrella name for Pershing LLC (member FINRA, SIPC and NYSE), Pershing Advisor Solutions (member FINRA and SIPC), Pershing Prime Services (a service of Pershing LLC), Pershing Limited (UK), Pershing Securities Limited, Pershing Securities International Limited (Ireland), Pershing (Channel Islands) Limited, Pershing Securities Canada Limited, Pershing Securities Singapore Private Limited and Pershing Securities Australia Pty. Ltd. SIPC protects securities in customer accounts of its members up to $500,000 in securities (including $250,000 for claims for cash). Explanatory brochure available upon request or at www.sipc.org. SIPC does not protect against loss due to market fluctuation. SIPC protection is not the same as, and should not be confused with, FDIC insurance.

Past performance is not a guide to future performance of any instrument, transaction or financial structure and a loss of original capital may occur. Calls and communications with BNY Mellon may be recorded, for regulatory and other reasons.

Disclosures in relation to certain other BNY Mellon group entities can be accessed at the following website: http://disclaimer.bnymellon.com/eu.htm.

This material is intended for wholesale/professional clients (or the equivalent only), is not intended for use by retail clients and no other person should act upon it. Persons who do not have professional experience in matters relating to investments should not rely on this material. BNY Mellon will only provide the relevant investment services to investment professionals.

Not all products and services are offered in all countries.

If distributed in the UK, this material is a financial promotion. If distributed in the EU, this material is a marketing communication.

This material, which may be considered advertising, is for general information purposes only and is not intended to provide legal, tax, accounting, investment, financial or other professional advice on any matter. This material does not constitute a recommendation or advice by BNY Mellon of any kind. Use of our products and services is subject to various regulations and regulatory oversight. You should discuss this material with appropriate advisors in the context of your circumstances before acting in any manner on this material or agreeing to use any of the referenced products or services and make your own independent assessment (based on such advice) as to whether the referenced products or services are appropriate or suitable for you. This material may not be comprehensive or up to date and there is no undertaking as to the accuracy, timeliness, completeness or fitness for a particular purpose of information given. BNY Mellon will not be responsible for updating any information contained within this material and opinions and information contained herein are subject to change without notice. BNY Mellon assumes no direct or consequential liability for any errors in or reliance upon this material.

This material may not be distributed or used for the purpose of providing any referenced products or services or making any offers or solicitations in any jurisdiction or in any circumstances in which such products, services, offers or solicitations are unlawful or not authorized, or where there would be, by virtue of such distribution, new or additional registration requirements.

Any references to dollars are to US dollars unless specified otherwise.

This material may not be reproduced or disseminated in any form without the prior written permission of BNY Mellon. Trademarks, logos and other intellectual property marks belong to their respective owners.

The Bank of New York Mellon, member of the Federal Deposit Insurance Corporation (“FDIC”).

© 2020 The Bank of New York Mellon Corporation. All rights reserved.