Embed Size (px)

Citation preview

Capital Markets Day Hydro AgriCapital Markets Day Capital Markets Day Hydro Hydro AgriAgri

Executive Vice PresidentThorleif Enger

Oslo, December 9, 2002

Executive Vice PresidentExecutive Vice PresidentThorleifThorleif EngerEnger

Oslo, Oslo, December December 9, 20029, 2002

36207_5H - 12.2002 - * 2 - Hydro Media

2

Hydro Hydro Agri perspectivesAgri perspectives

● From Turnaround to industry leadership■ Debunking myths■ Our ability to deliver

● Hydro Agri’s unique business model and areas of global strength

● Opportunities ahead

36207_5H - 12.2002 - * 3 - Hydro Media

3

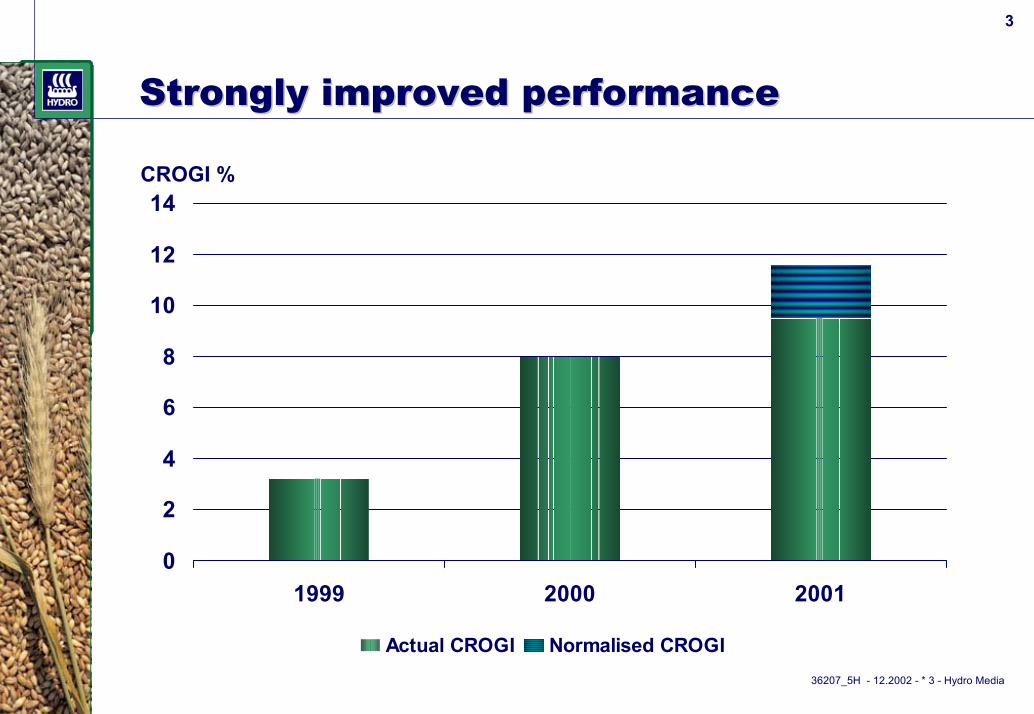

Strongly improved performanceStrongly improved performance

0

2

4

6

8

10

12

14

1999 2000 2001

Actual CROGI Normalised CROGI

CROGI %

36207_5H - 12.2002 - * 4 - Hydro Media

4

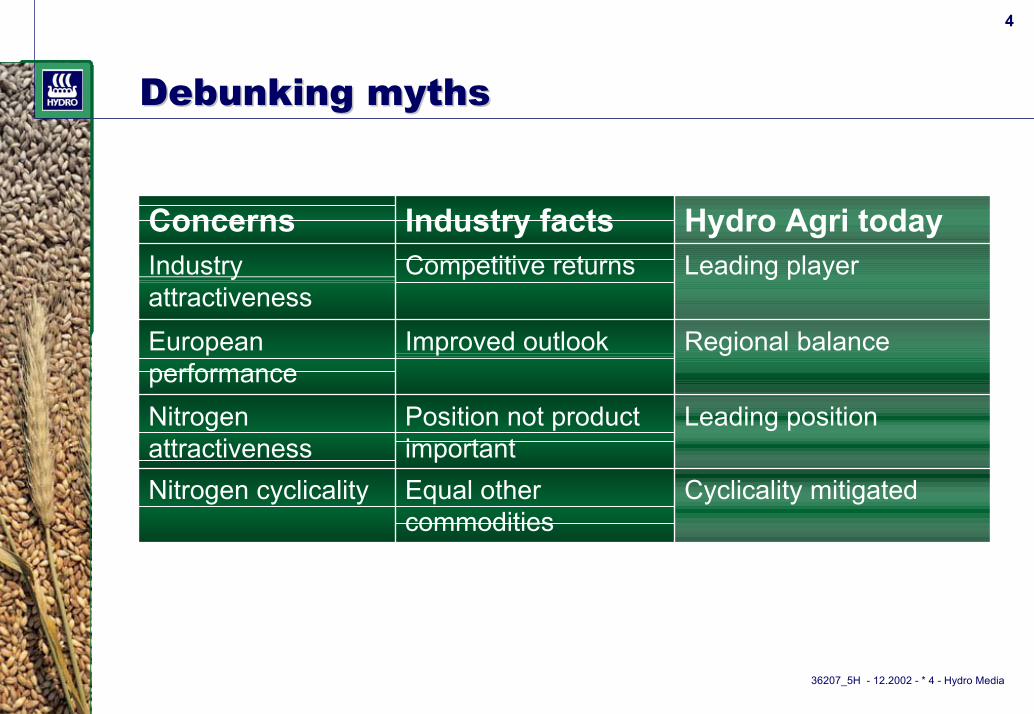

Debunking mythsDebunking myths

Cyclicality mitigatedEqual other commodities

Nitrogen cyclicality

Leading positionPosition not product important

Nitrogen attractiveness

Regional balanceImproved outlookEuropean performance

Leading playerCompetitive returnsIndustry attractiveness

Hydro Agri todayIndustry factsConcerns

36207_5H - 12.2002 - * 5 - Hydro Media

5

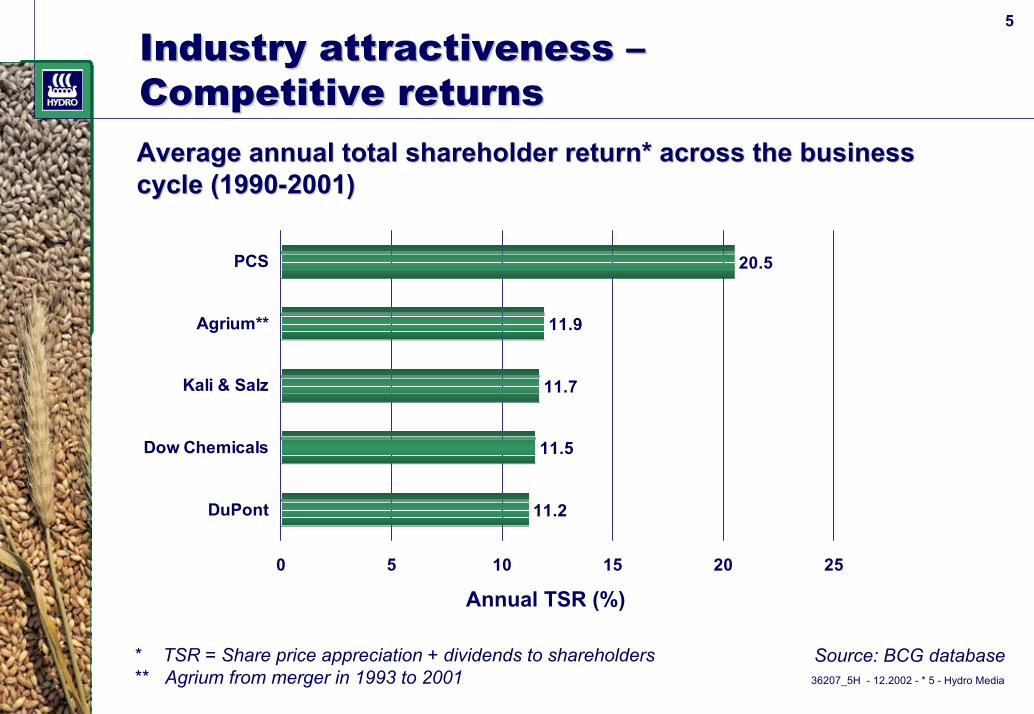

Industry attractiveness Industry attractiveness ––Competitive returnsCompetitive returnsAverage annual total shareholder return* across the businessAverage annual total shareholder return* across the businesscycle (1990cycle (1990--2001)2001)

11.2

11.5

11.7

11.9

20.5

0 5 10 15 20 25

DuPont

Dow Chemicals

Kali & Salz

Agrium**

PCS

Annual TSR (%)

* TSR = Share price appreciation + dividends to shareholders** Agrium from merger in 1993 to 2001

Source: BCG database

36207_5H - 12.2002 - * 6 - Hydro Media

6

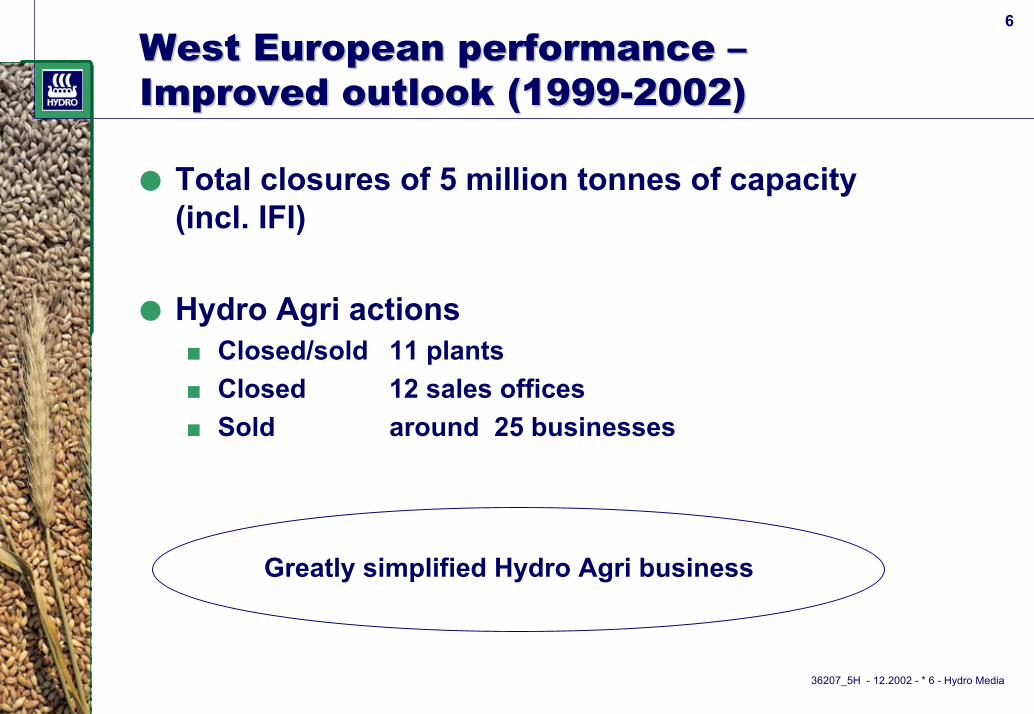

West European performanceWest European performance ––Improved outlook Improved outlook (1999(1999--2002)2002)

● Total closures of 5 million tonnes of capacity (incl. IFI)

● Hydro Agri actions■ Closed/sold 11 plants■ Closed 12 sales offices■ Sold around 25 businesses

Greatly simplified Hydro Agri business

36207_5H - 12.2002 - * 7 - Hydro Media

7

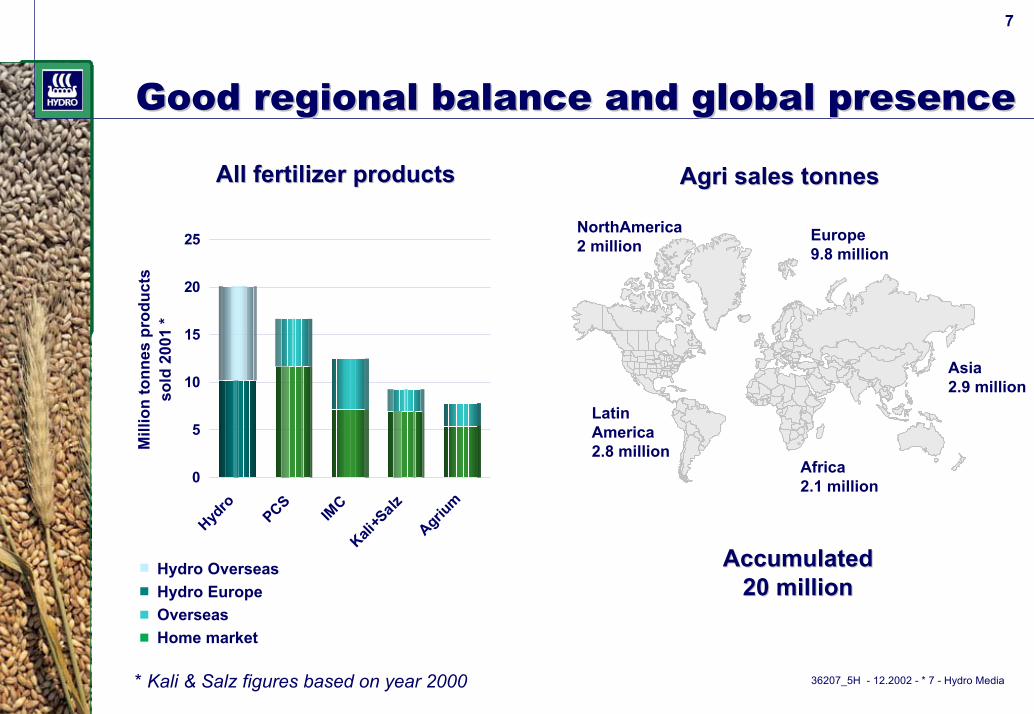

GoodGood regional regional balancebalance and global and global presencepresence

0

5

10

15

20

25

Hydro

PCS

IMC

Kali+S

alz

Agrium

All fertilizer productsAll fertilizer products M

illio

n to

nnes

pro

duct

s s

old

2001

*

Hydro Overseas Hydro Europe Overseas Home market

AccumulatedAccumulated20 million20 million

Latin America2.8 million

NorthAmerica2 million

Africa2.1 million

Asia2.9 million

Europe9.8 million

AgriAgri sales sales tonnestonnes

* Kali & Salz figures based on year 2000

36207_5H - 12.2002 - * 8 - Hydro Media

8

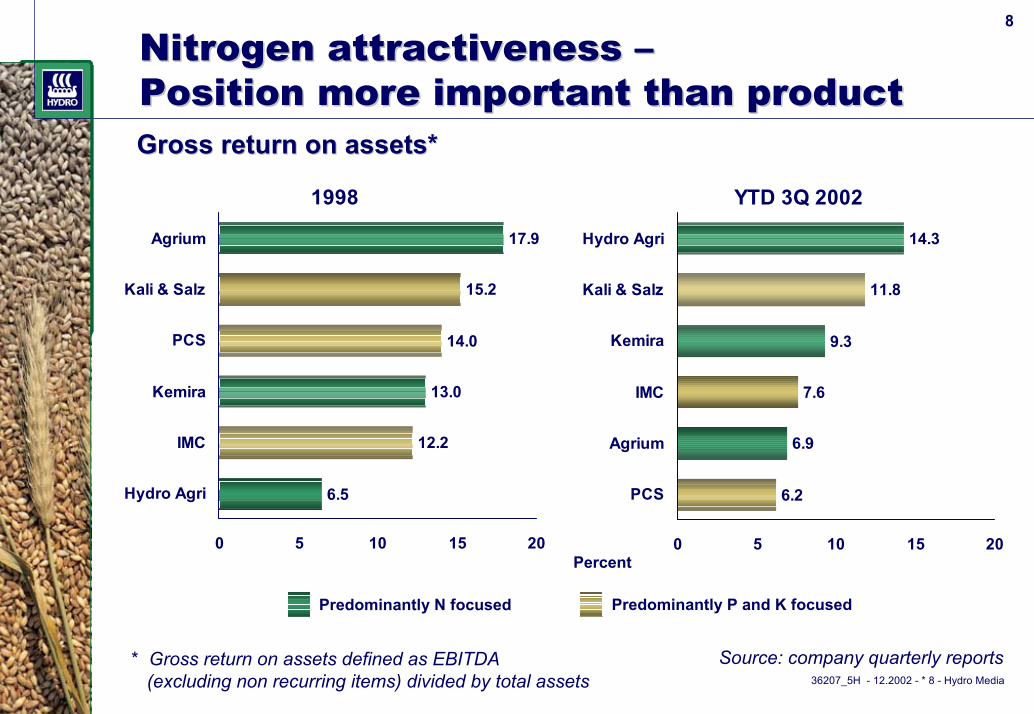

Gross return on assets*Gross return on assets*

Percent

1998

12.2

13.0

14.0

15.2

6.5

17.9

0 5 10 15 20

Hydro Agri

IMC

Kemira

PCS

Kali & Salz

Agrium

YTD 3Q 2002

6.2

6.9

7.6

9.3

11.8

14.3

0 5 10 15 20

PCS

Agrium

IMC

Kemira

Kali & Salz

Hydro Agri

Nitrogen Nitrogen attractivenessattractiveness ––PositionPosition more more important than productimportant than product

Predominantly P and K focused Predominantly N focused

Source: company quarterly reports* Gross return on assets defined as EBITDA (excluding non recurring items) divided by total assets

36207_5H - 12.2002 - * 9 - Hydro Media

9

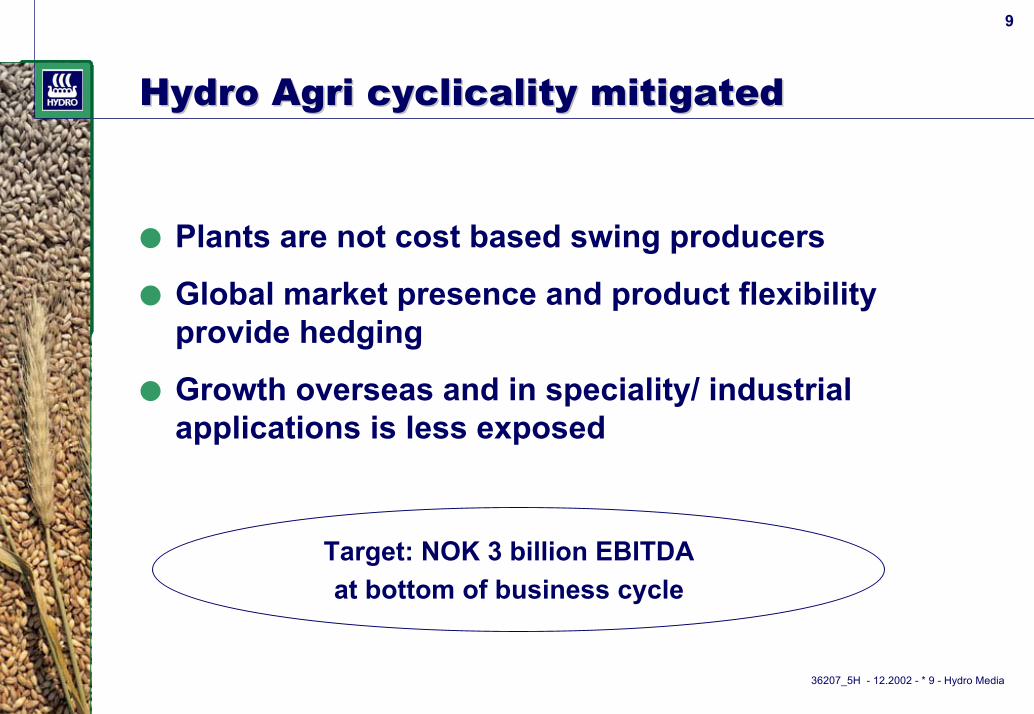

Hydro Hydro Agri cyclicality mitigatedAgri cyclicality mitigated

● Plants are not cost based swing producers

● Global market presence and product flexibility provide hedging

● Growth overseas and in speciality/ industrial applications is less exposed

Target: NOK 3 billion EBITDA at bottom of business cycle

36207_5H - 12.2002 - * 10 - Hydro Media

10

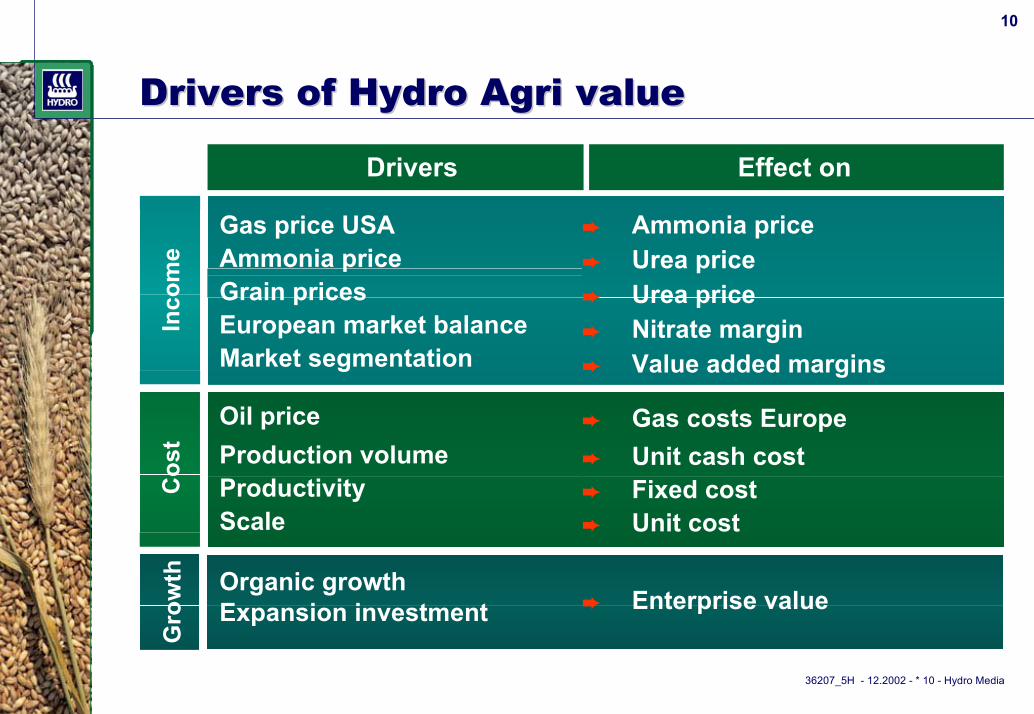

Drivers Drivers ofof Hydro Hydro Agri valueAgri value

Drivers Effect onIn

com

eC

ost

Gro

wth

Gas price USAAmmonia priceGrain pricesEuropean market balanceMarket segmentation

Oil priceProduction volumeProductivity Scale

Organic growthExpansion investment

➨ Ammonia price➨ Urea price➨ Urea price➨ Nitrate margin➨ Value added margins

➨ Gas costs Europe➨ Unit cash cost➨ Fixed cost➨ Unit cost

➨ Enterprise value

36207_5H - 12.2002 - * 11 - Hydro Media

11

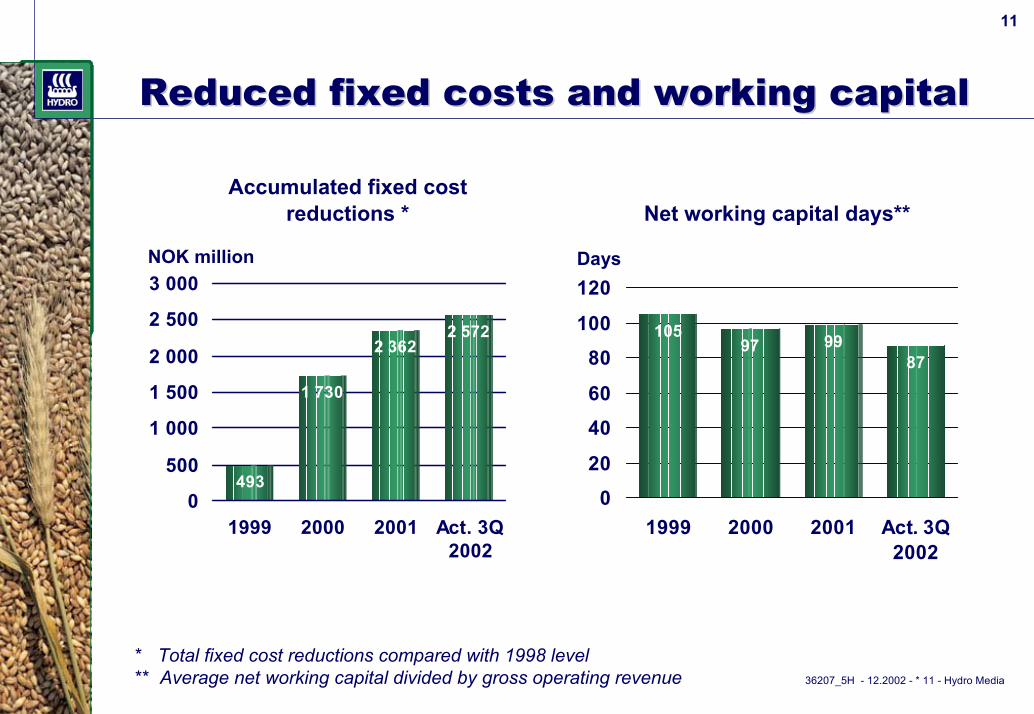

Reduced fixed costs and working capitalReduced fixed costs and working capital

Days

493

1 730

2 3622 572

0

500

1 000

1 500

2 000

2 500

3 000

1999 2000 2001 Act. 3Q2002

NOK million

Accumulated fixed cost reductions * Net working capital days**

10597 99

87

020

4060

80100

120

1999 2000 2001 Act. 3Q2002

* Total fixed cost reductions compared with 1998 level** Average net working capital divided by gross operating revenue

36207_5H - 12.2002 - * 12 - Hydro Media

12

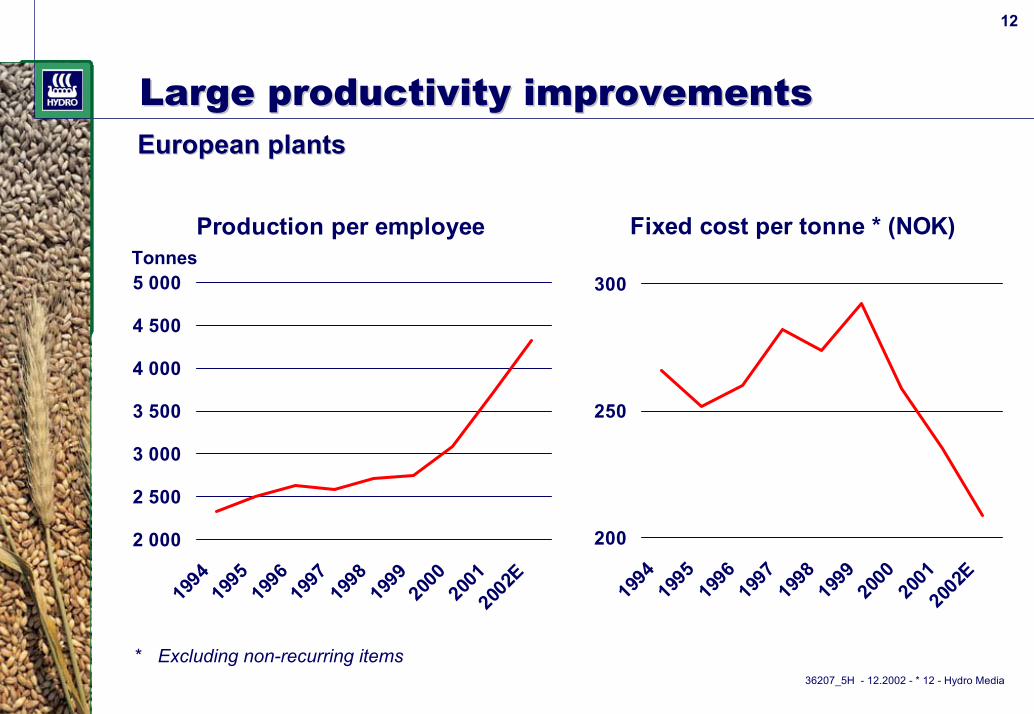

Large productivity improvementsLarge productivity improvements European plantsEuropean plants

Fixed cost per tonne * (NOK)

200

250

300

1994

1995

1996

1997

1998

1999

2000

2001

2002

E

Production per employee

2 000

2 500

3 000

3 500

4 000

4 500

5 000

1994

1995

1996

1997

1998

1999

2000

2001

2002

E

Tonnes

* Excluding non-recurring items

36207_5H - 12.2002 - * 13 - Hydro Media

13

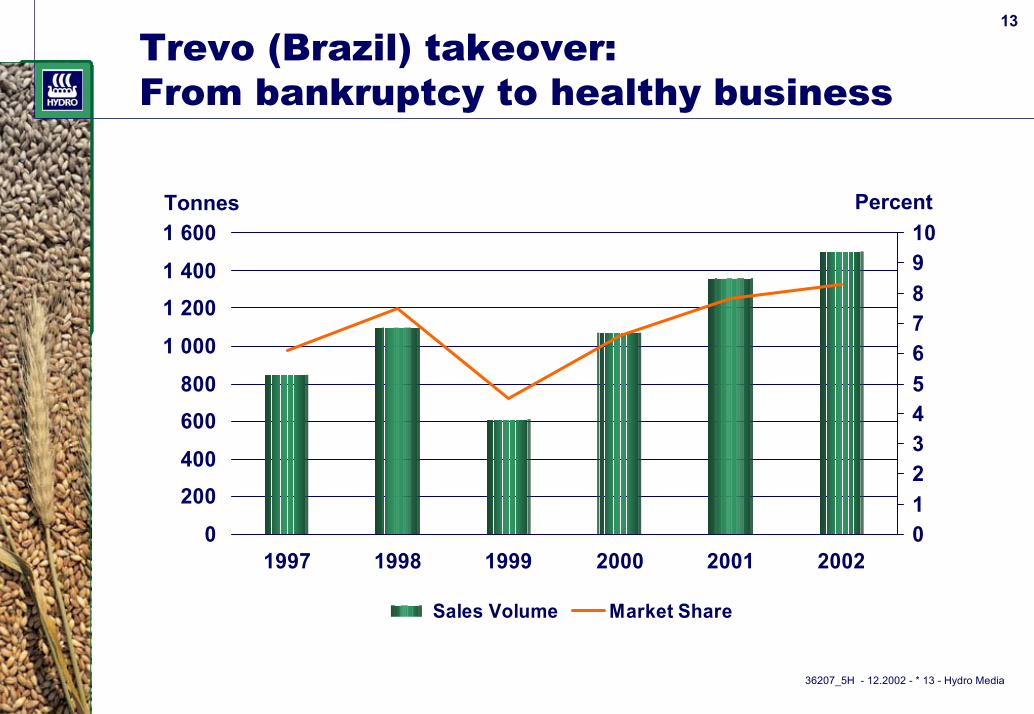

Trevo (Brazil) takeover:From bankruptcy to healthy business

0 200 400 600 800

1 0001 2001 4001 600

1997 1998 1999 2000 2001 2002012345678910

Sales Volume Market Share

Percent Tonnes

36207_5H - 12.2002 - * 14 - Hydro Media

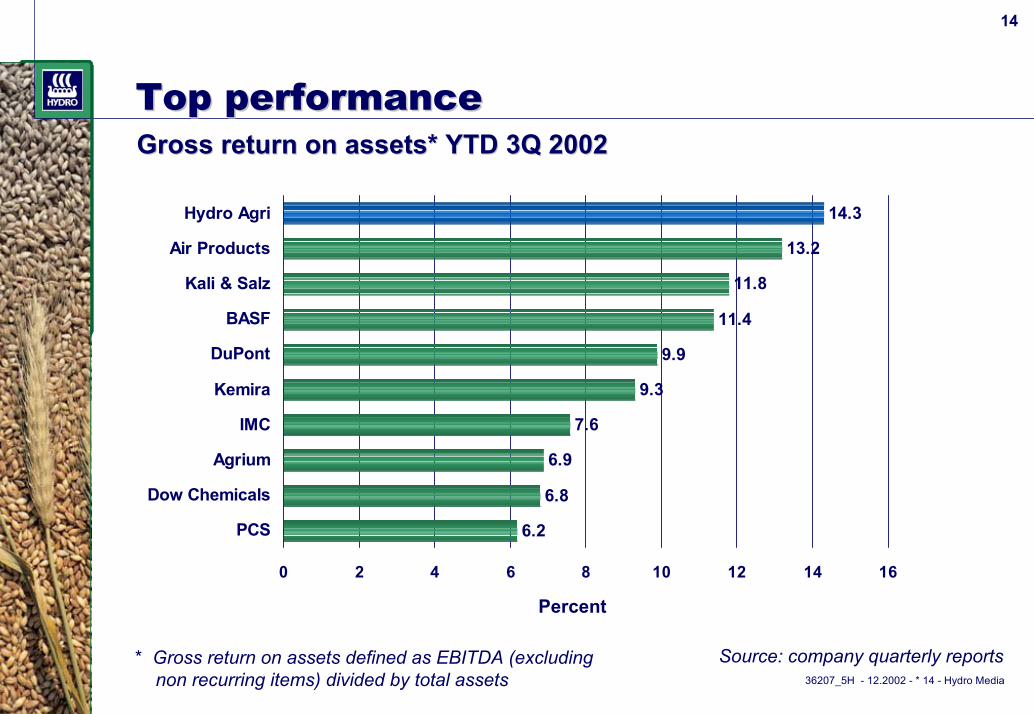

14

Top performanceTop performanceGross return on assets* YTD 3Q 2002Gross return on assets* YTD 3Q 2002

6.2

6.8

6.9

7.6

9.3

9.9

11.4

11.8

13.2

14.3

0 2 4 6 8 10 12 14 16

PCS

Dow Chemicals

Agrium

IMC

Kemira

DuPont

BASF

Kali & Salz

Air Products

Hydro Agri

Percent

Source: company quarterly reports* Gross return on assets defined as EBITDA (excludingnon recurring items) divided by total assets

36207_5H - 12.2002 - * 15 - Hydro Media

15

WeWe have a have a uniqueunique fertilizer positionfertilizer position

● The largest player

● The only truly global company

● Balanced product portfolio (N,P,K)

● Strong sourcing power

● Unique brands

36207_5H - 12.2002 - * 16 - Hydro Media

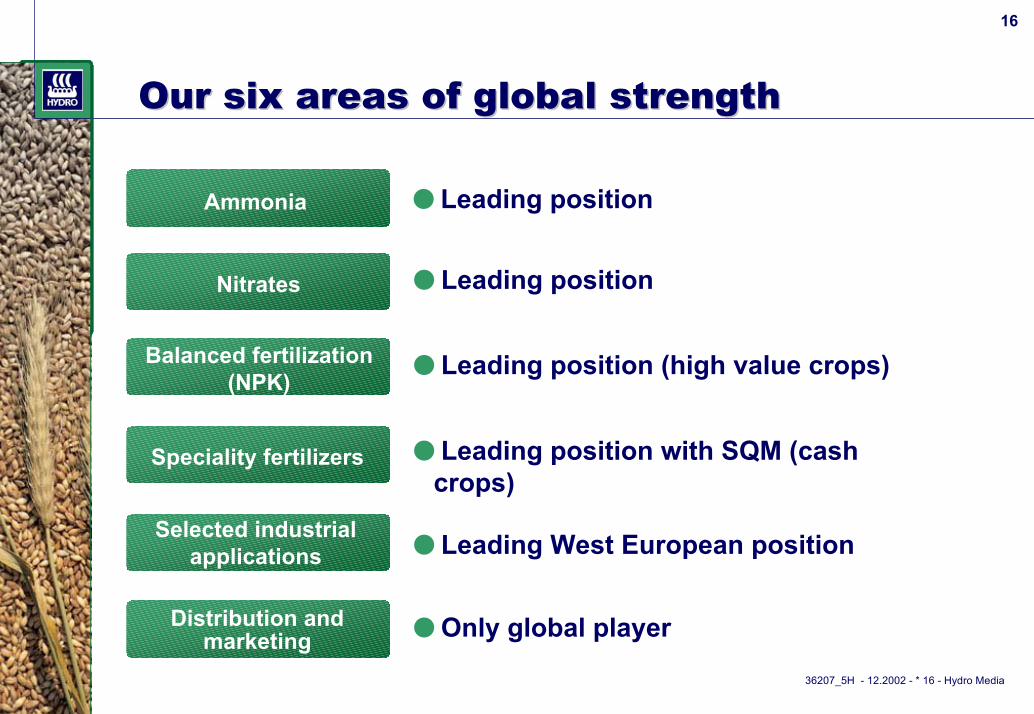

16

Our six areas of global strengthOur six areas of global strength

Ammonia ● Leading position

Nitrates ● Leading position

Balanced fertilization (NPK) ● Leading position (high value crops)

Speciality fertilizers ● Leading position with SQM (cash crops)

Selected industrialapplications ● Leading West European position

Distribution andmarketing ● Only global player

36207_5H - 12.2002 - * 17 - Hydro Media

17

Positive market outlookPositive market outlook

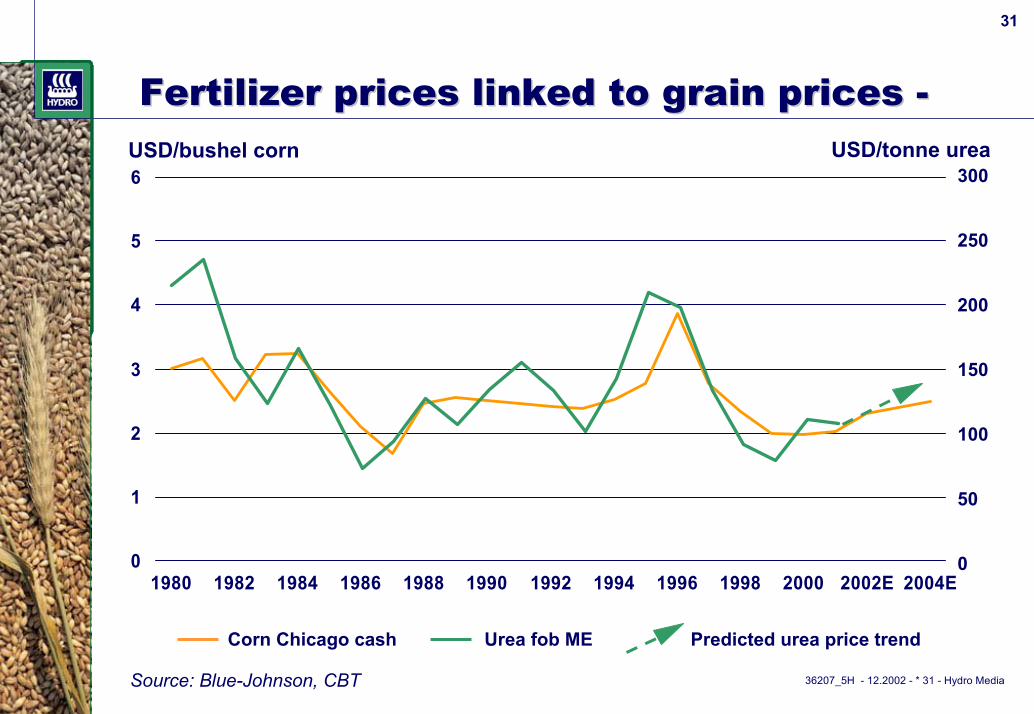

● Growth in fertilizer consumption■ Cereal stocks diminishing rapidly■ Increasing grain prices last months■ Historically, fertilizer prices correlate well with grain

prices

● Limited new capacity globally next 2-3 years

● Global supply/demand balance looks good

36207_5H - 12.2002 - * 18 - Hydro Media

18

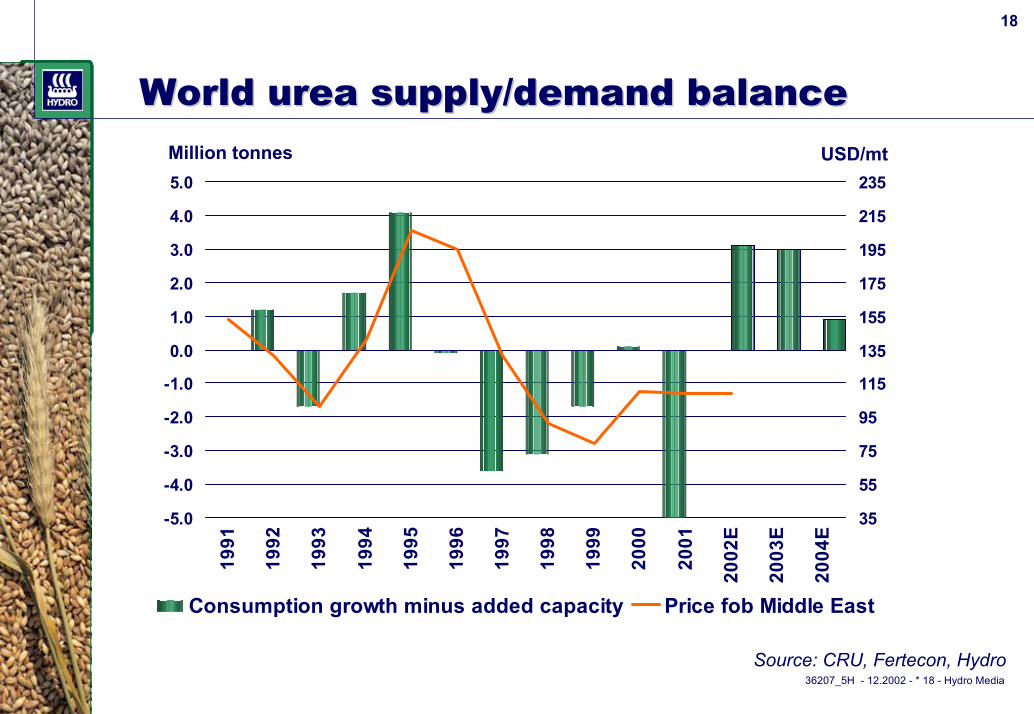

World urea supply/demand balanceWorld urea supply/demand balance

-5.0

-4.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

E

2003

E

2004

E

35

55

75

95

115

135

155

175

195

215

235

Consumption growth minus added capacity Price fob Middle East

Million tonnes USD/mt

Source: CRU, Fertecon, Hydro

36207_5H - 12.2002 - * 19 - Hydro Media

19

Possible opportunities and threatsPossible opportunities and threats

Opportunities● Increased exports to China and India● Russian WTO membership expected to establish gas

prices reflecting real costs■ Reduce Government impact■ Intermediate EU antidumping measures linked to gas price

Threats● Improved US cost position● Imports into Europe

36207_5H - 12.2002 - * 20 - Hydro Media

20

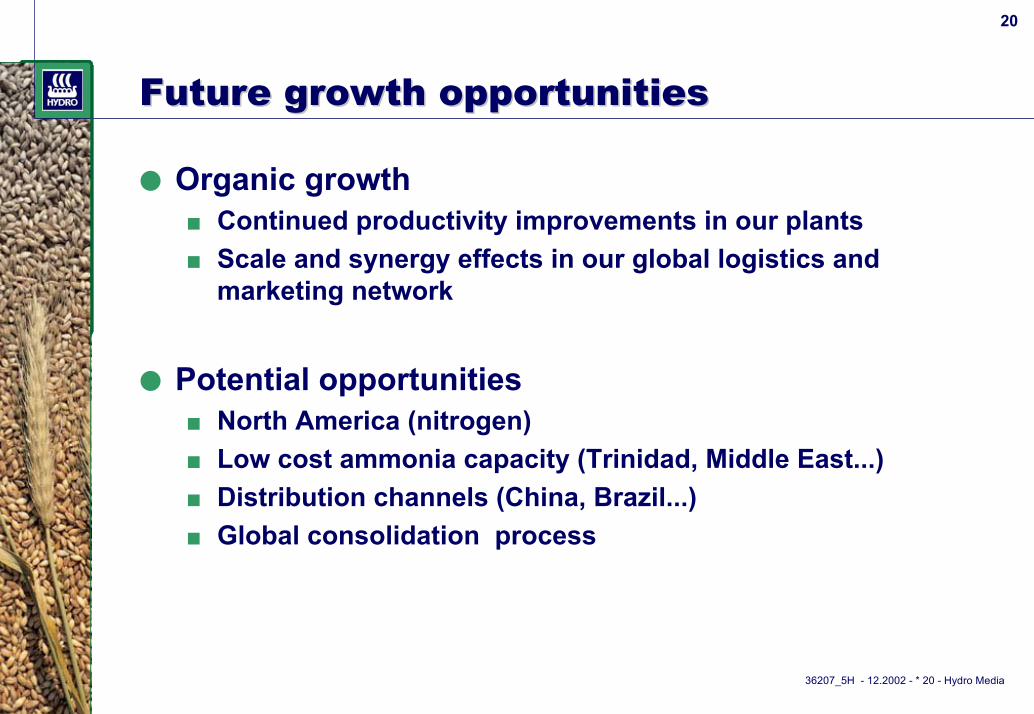

Future growth opportunitiesFuture growth opportunities

● Organic growth■ Continued productivity improvements in our plants■ Scale and synergy effects in our global logistics and

marketing network

● Potential opportunities■ North America (nitrogen)■ Low cost ammonia capacity (Trinidad, Middle East...)■ Distribution channels (China, Brazil...)■ Global consolidation process

36207_5H - 12.2002 - * 21 - Hydro Media

21

Key messagesKey messages

● Market outlook positive

● Unique business position

● Global leadership in key strategic areas

● Industry leadership after Turnaround

● Strong platform for profitable growth

Additional InformationAdditional InformationAdditional Information

36207_5H - 12.2002 - * 23 - Hydro Media

23

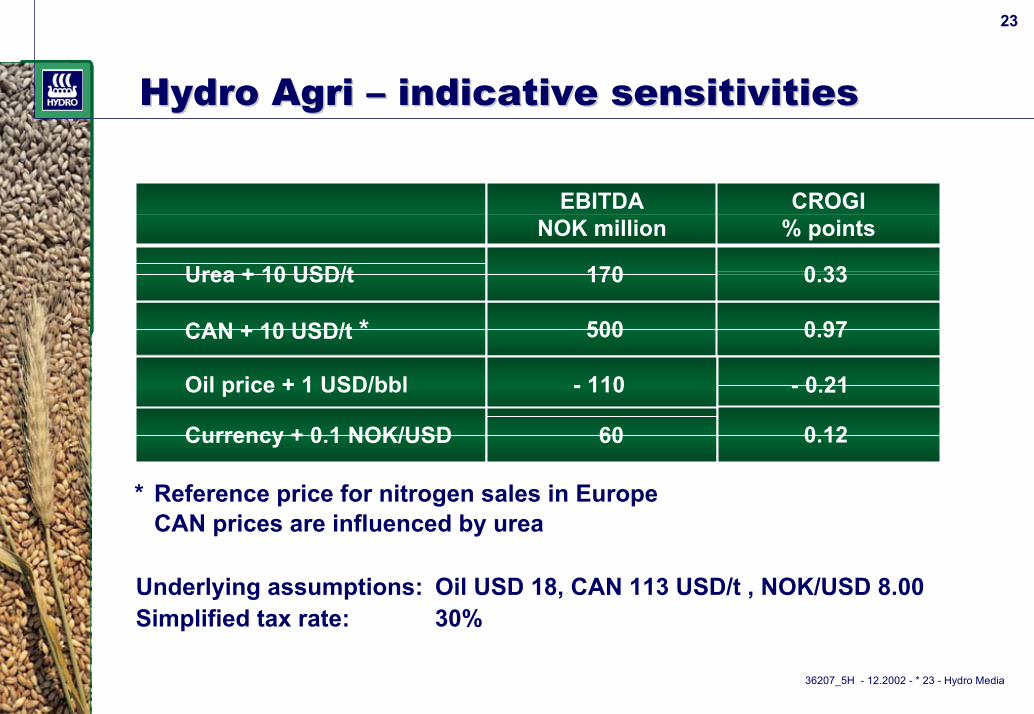

Hydro Hydro AgriAgri –– indicative sensitivitiesindicative sensitivities

EBITDANOK million

CROGI % points

Underlying assumptions: Oil USD 18, CAN 113 USD/t , NOK/USD 8.00Simplified tax rate: 30%

CAN + 10 USD/t * 500

Urea + 10 USD/t 170 0.33

0.97

Oil price + 1 USD/bbl - 110 - 0.21

0.12Currency + 0.1 NOK/USD 60

* Reference price for nitrogen sales in EuropeCAN prices are influenced by urea

36207_5H - 12.2002 - * 24 - Hydro Media

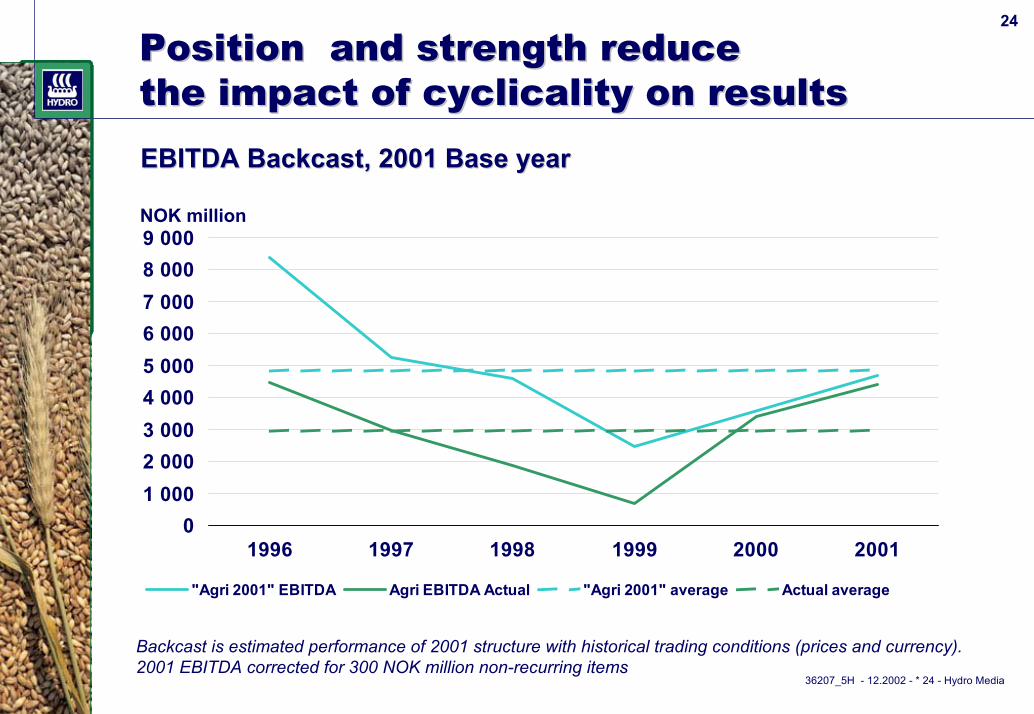

24

Position Position and and strength reduce strength reduce the impact of cyclicality on resultsthe impact of cyclicality on results EBITDA EBITDA BackcastBackcast, 2001 Base year, 2001 Base year

01 0002 0003 0004 0005 0006 0007 0008 0009 000

1996 1997 1998 1999 2000 2001

"Agri 2001" EBITDA Agri EBITDA Actual "Agri 2001" average Actual average

NOK million

Backcast is estimated performance of 2001 structure with historical trading conditions (prices and currency).2001 EBITDA corrected for 300 NOK million non-recurring items

36207_5H - 12.2002 - * 25 - Hydro Media

25

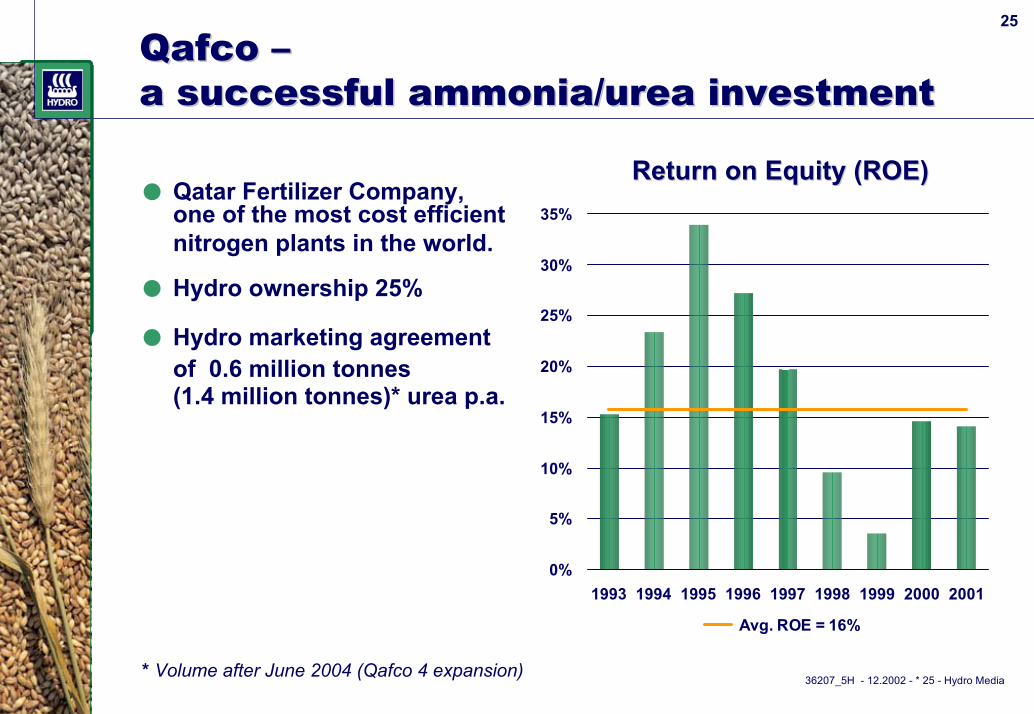

QafcoQafco ––a successful ammonia/urea investmenta successful ammonia/urea investment

0%

5%

10%

15%

20%

25%

30%

35%

1993 1994 1995 1996 1997 1998 1999 2000 2001

Avg. ROE = 16%

Return on Equity (ROE)Return on Equity (ROE)● Qatar Fertilizer Company,

one of the most cost efficientnitrogen plants in the world.

● Hydro ownership 25%

● Hydro marketing agreementof 0.6 million tonnes(1.4 million tonnes)* urea p.a.

* Volume after June 2004 (Qafco 4 expansion)

36207_5H - 12.2002 - * 26 - Hydro Media

26

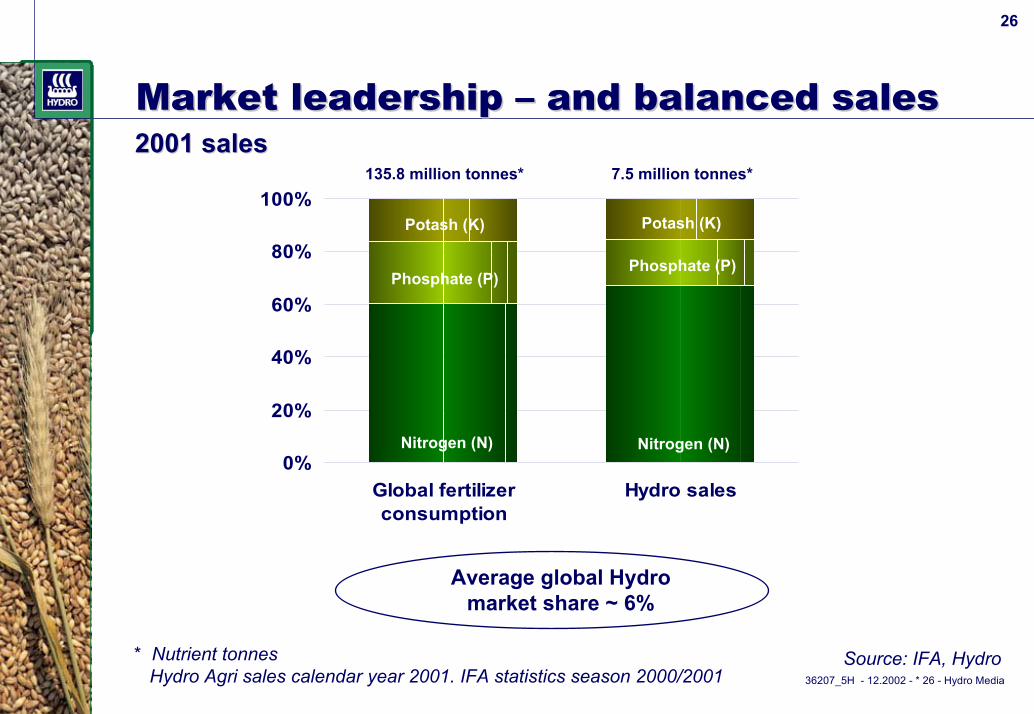

Market leadership Market leadership –– and balanced salesand balanced sales

0%

20%

40%

60%

80%

100%

Global fertilizerconsumption

Hydro sales

2001 sales2001 sales135.8 million tonnes*

Nitrogen (N)

Phosphate (P)

Potash (K)

7.5 million tonnes*

Nitrogen (N)

Phosphate (P)

Potash (K)

Average global Hydro market share ~ 6%

* Nutrient tonnesHydro Agri sales calendar year 2001. IFA statistics season 2000/2001

Source: IFA, Hydro

36207_5H - 12.2002 - * 27 - Hydro Media

27

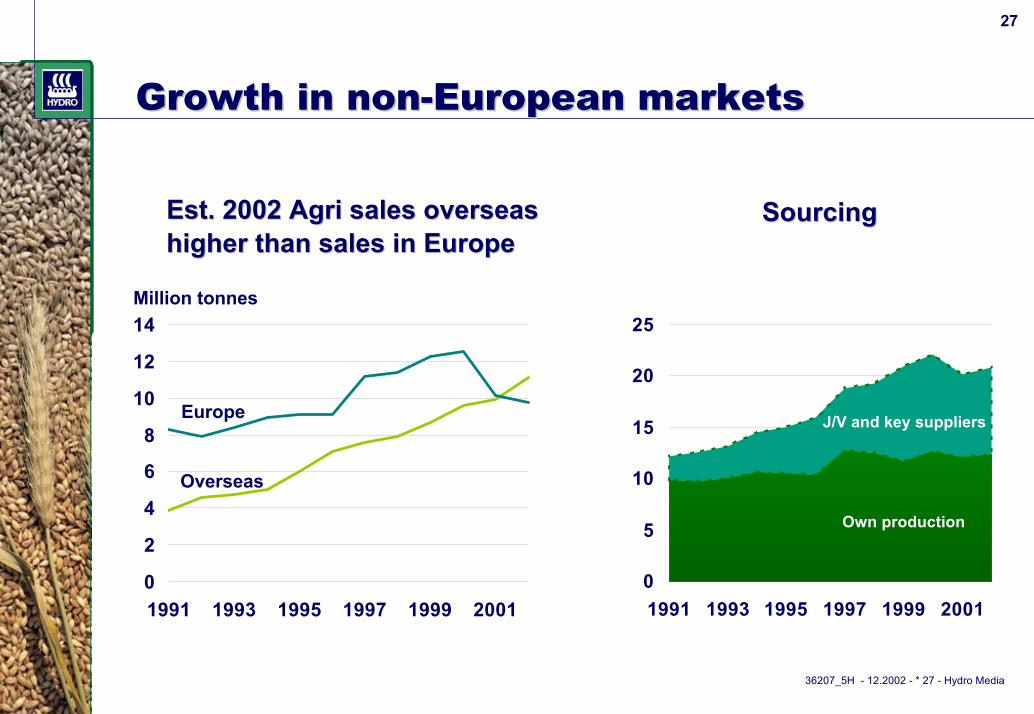

Growth in nonGrowth in non--European marketsEuropean markets

0

2

4

6

8

10

12

14

1991 1993 1995 1997 1999 2001

Million tonnes

Europe

Overseas

0

5

10

15

20

25

1991 1993 1995 1997 1999 2001

SourcingSourcingEst. 2002Est. 2002 AgriAgri sales overseassales overseashigher than sales in Europehigher than sales in Europe

Own production

J/V and key suppliers

36207_5H - 12.2002 - * 28 - Hydro Media

28

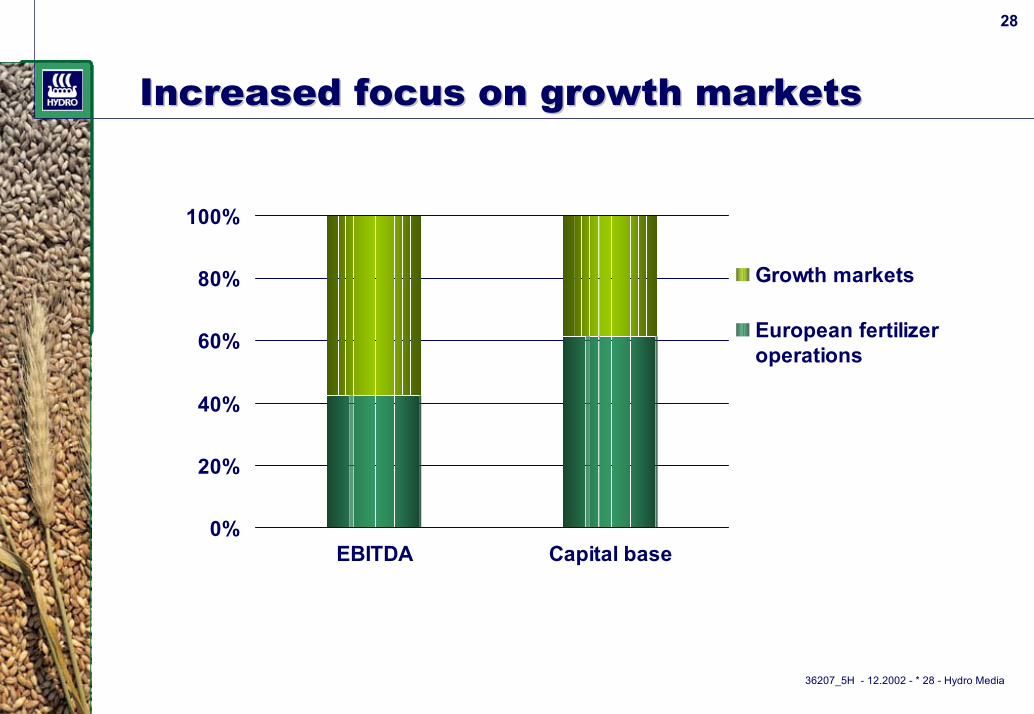

Increased focus on growth marketsIncreased focus on growth markets

0%

20%

40%

60%

80%

100%

EBITDA Capital base

Growth markets

European fertilizeroperations

36207_5H - 12.2002 - * 29 - Hydro Media

29

Historical and average fertilizer pricesHistorical and average fertilizer prices

0

50

100

150

200

250

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

USD/tonnes

Ammonia Fob Caribbean

UreaBulk fob Middle East

Source: Fertilizer Week, The Market for CAN

0

50

100

150

200

250

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

USD/tonnes

0

50

100

150

200

250

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

USD/tonnes

CAN GermanyBulk delivered warehouse

DAPBulk fob US Gulf

USD/tonnes 250

200

150

100

50

0 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

Average prices 1993 - 2001

36207_5H - 12.2002 - * 30 - Hydro Media

30

Jan

. -88

Jul

. -8

8 J

an. -

89 J

ul.

-89

Jan

. -90

Jul

. -9

0 J

an. -

91 J

ul.

-91

Jan

. -92

Jul

. -9

2 J

an. -

93 J

ul.

-93

Jan

. -94

Jul

. -9

4 J

an. -

95 J

ul.

-95

Jan

. -96

Jul

. -9

6 J

an. -

97 J

ul.

-97

Jan

. -98

Jul

. -9

8 J

an. -

99 J

ul.

-99

Jan

. -00

Jul

. -0

0 J

an. -

01 J

ul.

-01

Jan

. -02

Jul

. -0

2

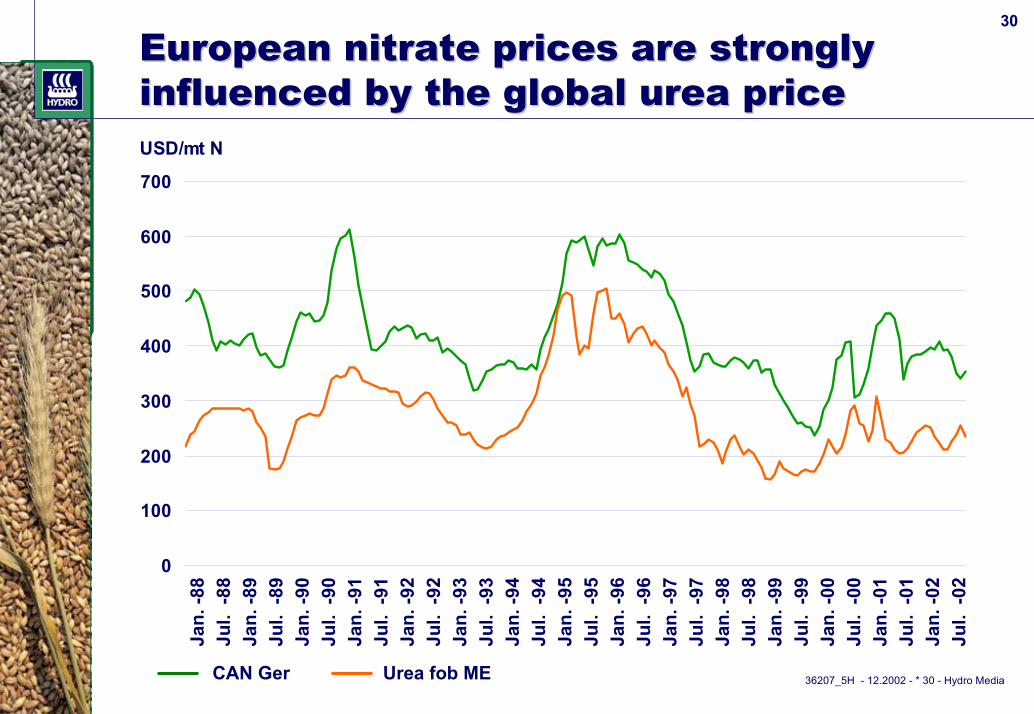

European nitrate prices are strongly European nitrate prices are strongly influenced by the global urea priceinfluenced by the global urea priceUSD/mt N

0

100

200

300

400

500

600

700

CAN Ger Urea fob ME

36207_5H - 12.2002 - * 31 - Hydro Media

31

Fertilizer prices linked to grain prices Fertilizer prices linked to grain prices --

0

1

2

3

4

5

6

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002E 2004E

USD/bushel corn USD/tonne urea 300

250

200

150

100

50

0

Corn Chicago cash Urea fob ME Predicted urea price trend

Source: Blue-Johnson, CBT

36207_5H - 12.2002 - * 32 - Hydro Media

32

-- grain prices increasinggrain prices increasing

0

50

100

150

200

250

Jul. 97 Jan 98 Jul. Jan 99 Jul. Jan 00 Jul. Jan 01 Jul. Jan 02 Jul.

USD/mt Wheat ( fob US Gulf ) Corn ( fob US Gulf )

Source: International Grain Council

36207_5H - 12.2002 - * 33 - Hydro Media

33

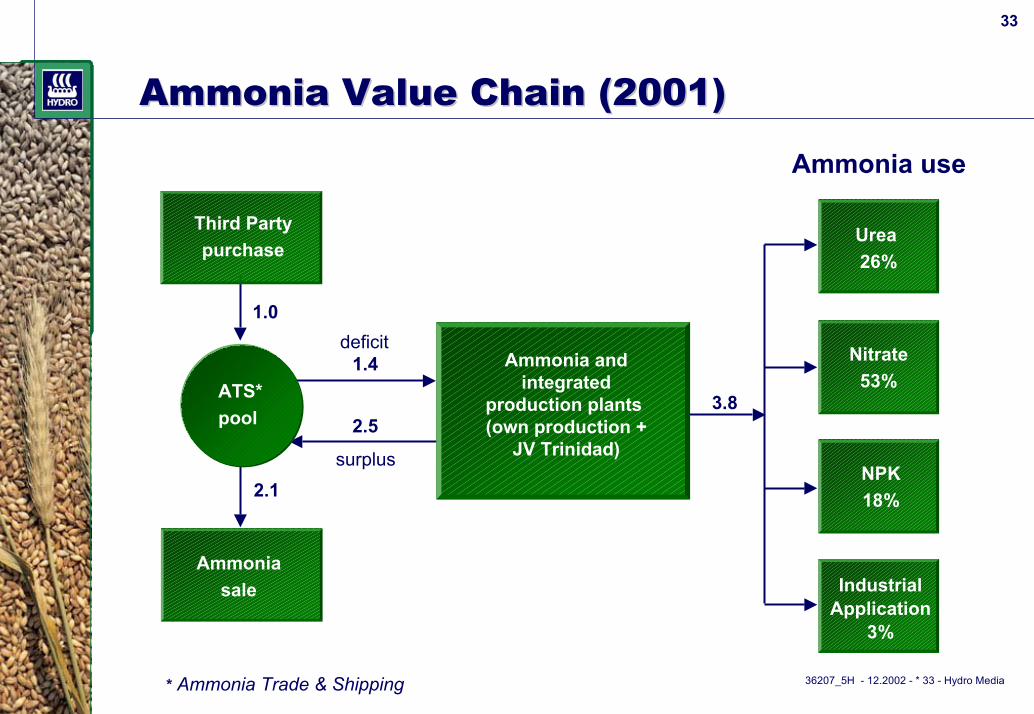

Ammonia Value Chain Ammonia Value Chain (2001)(2001)

ATS* pool

Third Party purchase

Ammonia sale

Urea 26%

Nitrate 53%

NPK 18%

Industrial Application

3%

deficit

surplus

1.4

2.5 3.8

2.1

Ammonia and integrated

production plants (own production +

JV Trinidad)

Ammonia use

1.0

* Ammonia Trade & Shipping

36207_5H - 12.2002 - * 34 - Hydro Media

34

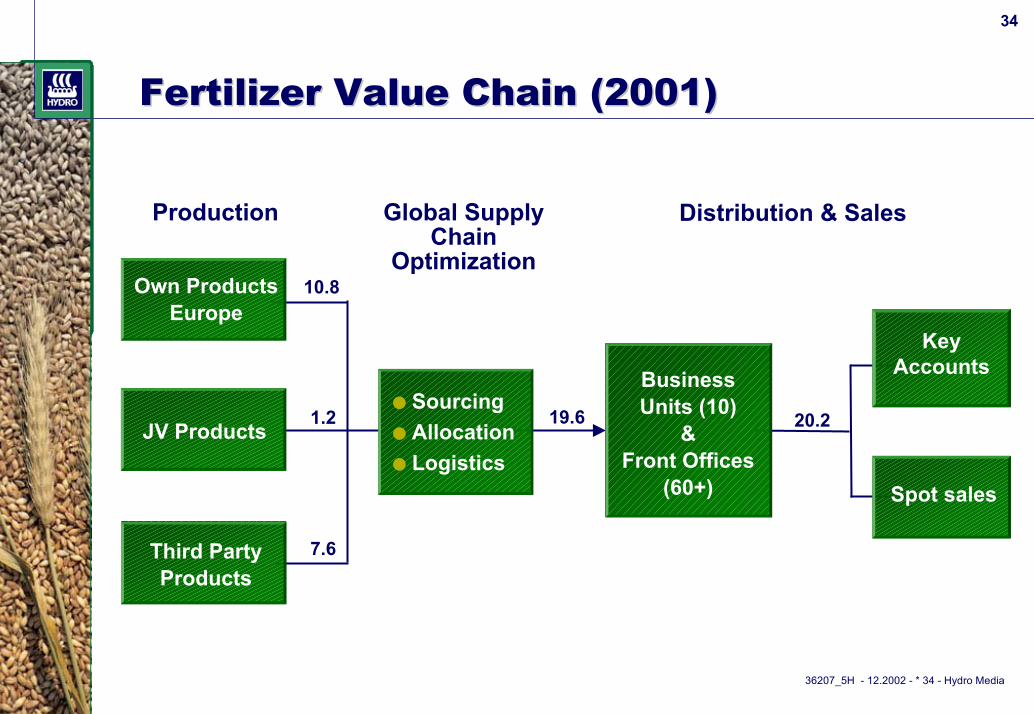

Fertilizer Value Chain Fertilizer Value Chain (2001)(2001)

Production Global Supply Chain

Optimization Own Products

Europe

JV Products

Third Party Products

● Sourcing● Allocation● Logistics

Business Units (10)

& Front Offices

(60+)

20.2

10.8

1.2

7.6

19.6

Key Accounts

Spot sales

Distribution & Sales

36207_5H - 12.2002 - * 35 - Hydro Media

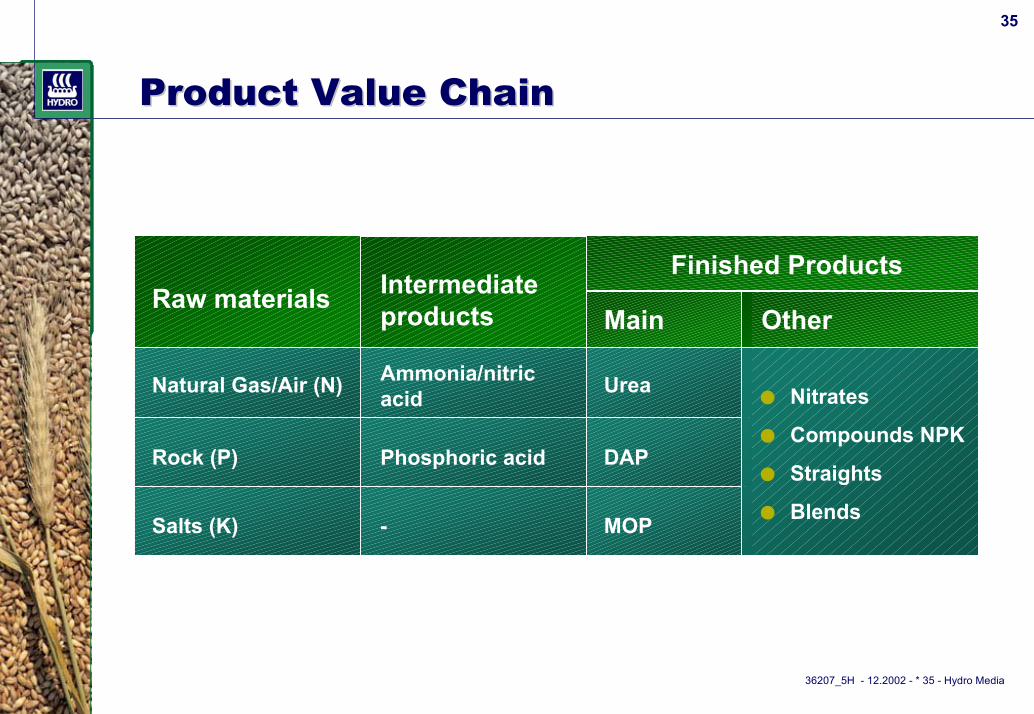

35

Product Value ChainProduct Value Chain

Raw materials

Natural Gas/Air (N)

Rock (P)

Salts (K)

Intermediate products

Ammonia/nitric acid

Phosphoric acid

-

Main

Urea

DAP

MOP

Other

● Nitrates

● Compounds NPK

● Straights

● Blends

Finished Products

36207_5H - 12.2002 - * 36 - Hydro Media

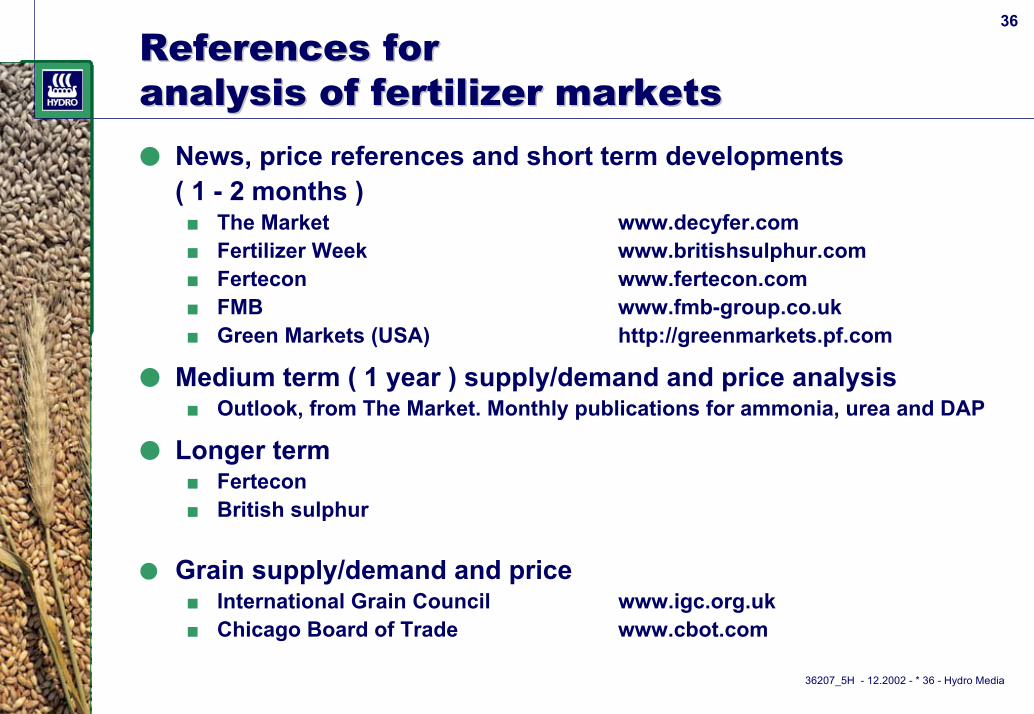

36

References forReferences foranalysis of fertilizer marketsanalysis of fertilizer markets● News, price references and short term developments

( 1 - 2 months )■ The Market www.decyfer.com■ Fertilizer Week www.britishsulphur.com■ Fertecon www.fertecon.com■ FMB www.fmb-group.co.uk■ Green Markets (USA) http://greenmarkets.pf.com

● Medium term ( 1 year ) supply/demand and price analysis■ Outlook, from The Market. Monthly publications for ammonia, urea and DAP

● Longer term■ Fertecon■ British sulphur

● Grain supply/demand and price■ International Grain Council www.igc.org.uk■ Chicago Board of Trade www.cbot.com

36207_5H - 12.2002 - * 37 - Hydro Media

37

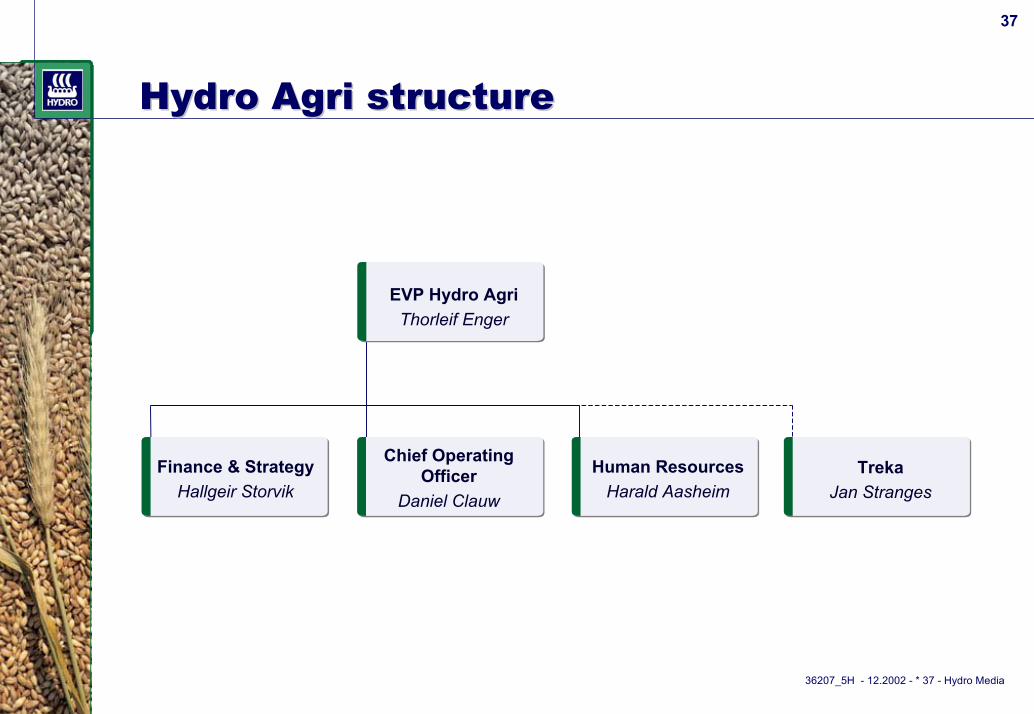

Hydro Agri structureHydro Agri structure

EVP Hydro AgriThorleif Enger

Finance & StrategyHallgeir Storvik

Chief Operating Officer

Daniel Clauw

Human ResourcesHarald Aasheim

TrekaJan Stranges