Embed Size (px)

Citation preview

capital markets day

2017

human forward.

london.

jacques van den broek, CEO

group strategy & vision

london | capital markets day | november 21 2017

|

agenda

our new brand positioning 6

strategic roadmap 7

ABFS 2018 9

tech as a differentiator 10

a structural growth industry 11

topline growth accelerating versus peers 12

14

conclusion 16

© Randstad 3

tech & touch initiatives by Randstad

| |

traditional authority via legacy.

personal. helpful. caring. relationship-focused.

innovative authority via change through data.

generic players

professional players tech players

more tech, algorithm driven.

our brand positioning tech-driven but human

© Randstad 4

| |

strategic roadmap best people, strong concepts, excellent execution & superior brands

© Randstad 5

our ultimate goal by 2030, we will touch the work life of 500 million people worldwide

grow to 5-6% ebita profitable growth improve margin increase productivity

| |

strategic roadmap best people, strong concepts, excellent execution & superior brands

© Randstad 6

• productivity (GP/FTE) up 3% YTD • prior cost savings programs on track • new cost savings of €90-100M

• inhouse growth 18% YTD 2017 • professionals growth 4% YTD 2017 • perm growth 9% YTD 2017 • SME growth 10% YTD 2017

• TTA -> enterprise clients • growth in MSP (+11%) & RPO (+30%) YTD 2017

• HR Tech opco initiatives

our ultimate goal by 2030, we will touch the work life of 500 million people worldwide

grow to 5-6% ebita profitable growth improve margin increase productivity

| |

ABFS 2018 integrated tech approach is crucial

© Randstad 7

| |

tech as a differentiator: higher barriers to entry, favouring big players in a fragmented market where scale and proximity matter

© Randstad 8

contingent w

ork

forc

e

perm

integrated talent management

talent engagement digital platforms

self-service platforms

tech touch tech touch

tech touch tech touch

SME clients large

| |

0,0%

0,3%

0,5%

0,8%

1,0%

1,3%

1,5%

1,8%

2,0%

2,3%

2,5%

2,8%

3,0%

3,3%

Belgium France Germany Netherlands Spain Japan US Italy

2007 2015

a structural growth industry staffing penetration rates rise over time

9 |

trends and growth drivers

globalization

technology

demographics

variety of work forms

governance of work

© Randstad

source: CIETT

| |

topline growth accelerating vs. peers powered by integrated tech

© Randstad 10

0%

5%

10%

15%

Randstad Peer 1 Peer 2

15%

20%

25%

30%

Randstad Peer 1 Peer 2

5%

10%

15%

Randstad Peer 1 Peer 2

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

2012 2013 2014 2015 2016 2017

Randstad Peer 1 Peer 2

organic revenue pwd growth by quarter, 2012-2017

france

italy

iberia

organic revenue pwd growth, 2017 YTD

| |

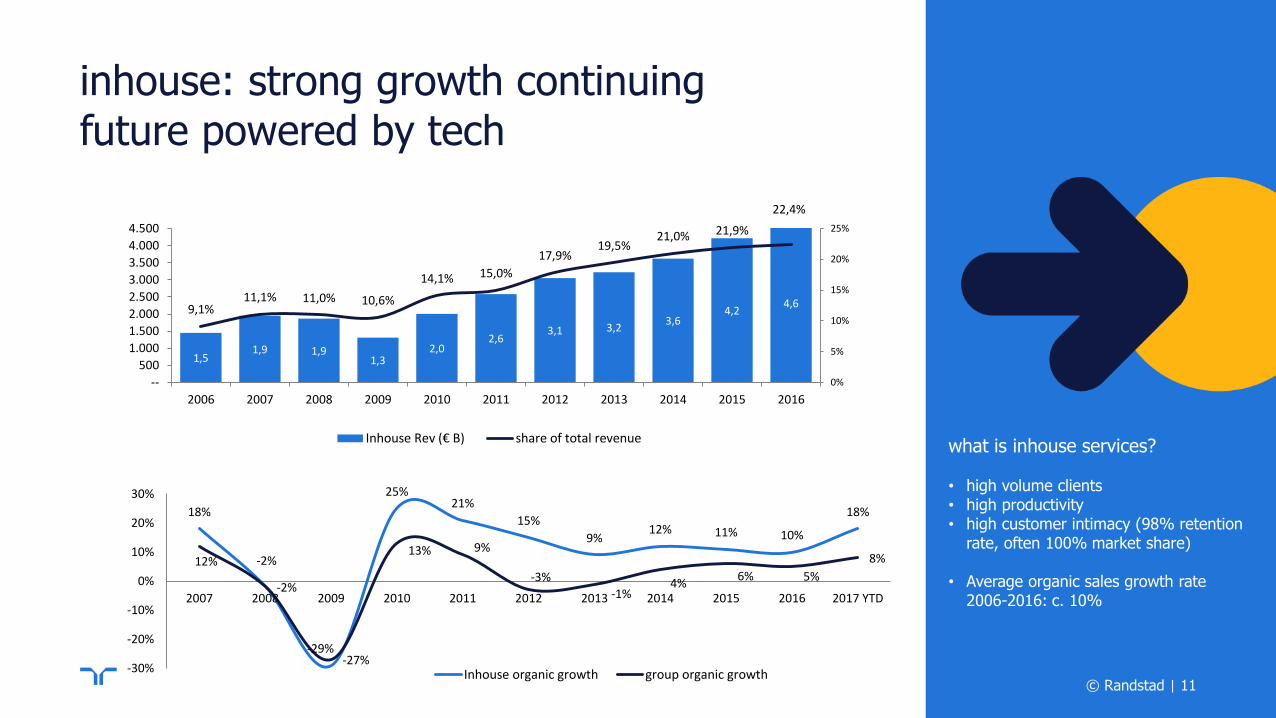

inhouse: strong growth continuing future powered by tech

© Randstad 11

1,5 1,9 1,9

1,3 2,0

2,6 3,1 3,2

3,6 4,2

4,6 9,1% 11,1% 11,0% 10,6%

14,1% 15,0%

17,9% 19,5%

21,0% 21,9%

22,4%

0%

5%

10%

15%

20%

25%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

--

500

1.000

1.500

2.000

2.500

3.000

3.500

4.000

4.500

Inhouse Rev (€ B) share of total revenuewhat is inhouse services? • high volume clients • high productivity • high customer intimacy (98% retention

rate, often 100% market share) • Average organic sales growth rate

2006-2016: c. 10%

18%

-2%

-29%

25% 21%

15%

9% 12% 11% 10%

18%

12%

-2%

-27%

13% 9%

-3%

-1% 4%

6% 5%

8%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 YTD

-30%

-20%

-10%

0%

10%

20%

30%

Inhouse organic growth group organic growth|

| 12

we are connecting the initiatives and scaling up successful concepts fast around the world.

|

tech & touch

RIF (15 investments) digital factory scale ups

data driven sales

workforce scheduling

external innovations via M&A

Capabilities (eg. SEO)

local innovations

Sales Navigator

Big Data France Ploy global concepts

SourceRight

RiseSmart

Global Clients Solutions

Horton (US)

© Randstad

| © Randstad 13

experiment, focus, proof, scale up validate business cases on hard data & leading KPIs

problem/solution fit product/market fit scale

pilot MVP roll-out

addressable market achievements so far growth potential

gro

up P

&L im

pact

tools

| © Randstad 14

conclusion

• integrated tech approach is crucial

• higher barriers to entry, in favour of big players

• riding the learning curve: experiment, focus, proof, scale up

• large addressable market size identified

ambition

gain further market share driven by our

differentiating tech & touch strategy

|

agenda

10.30 – 11.00 financial strategy & trading update

Robert Jan van de Kraats

11.00 – 11.30 Q&A

11.30 – 11.45 coffee break

11.45 – 12.15 US staffing/professionals & Monster

Linda Galipeau/Chris Kibarian

12.15 – 12.30 Q&A

12.30 – 13.30 buffet lunch

13.30 – 14.00 digital strategy: deep dive Jacques van

den Broek

© Randstad 15

14.00 – 15.00 data driven sales NL & France

Dominique Hermans & Sébastien Hélaine

15.00 – 15.15 coffee break

15.15 – 16.00 workforce scheduling François Béharel

16.00 – 16.30 enterprise clients Rebecca Henderson

16.30 – 16.45 wrap up

16.45 – 17.30 drinks and canapes

robert jan van de kraats, CFO

financial strategy & trading update

london | capital markets day | november 21 2017

|

agenda

current trading & outlook 21

revenue growth accelerating versus peers 22

perm: a major opportunity 24

cost savings update: consistent benchmarking 26

EBITA margin progression & outlook 27

M&A update & outlook 29

FCF stability through the cycle 31

capital allocation priorities 33

© Randstad 18

conclusion 34

| |

current trading

• revenue growth in October in line with

Q3 (+9%)

• volume trend in November so far appears

to be in line with October

• robust growth in Europe continued,

North America slightly improving

© Randstad 19

outlook

• there will be an adverse 2.4%

comparison in Q4

• gross margin in Q4 is expected to be

stable sequentially

• for Q4, operating expenses are expected

to be stable sequentially

• there will be an adverse 0.5 working day

impact in Q4 2017

|

| |

topline growth accelerating vs. peers driven by improving macro in europe and integrated tech

organic revenue growth by quarter, 2012-2017

© Randstad 20

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

2012 2013 2014 2015 2016 2017

Randstad Peer 1 Peer 2

• france still c.15% below 2007 peak • penetration rate in iberia (0.6%) and italy (1.2%)

markedly below european average • u.s. above peak and still growing

| |

further improving relative performance

france italy

0%

4%

8%

12%

16%

Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2015 2016 2017

Randstad Peer 1 Peer 2

-20%

-10%

0%

10%

20%

30%

40%

Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2015 2016 2017

Randstad Peer 1 Peer 2

-10%

-5%

0%

5%

Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2015 2016 2017

Randstad Peer 1 Peer 2

0%

10%

20%

30%

Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2015 2016 2017

Randstad Peer 1 Peer 2

north america iberia

© Randstad 21

organic revenue growth pwd organic revenue growth pwd

organic revenue growth pwd organic revenue growth pwd

| |

perm: a major opportunity

© Randstad 22

Chin

a

UK

AU

S

gro

up

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

FR

IT

NL

BE

ES

NAM

DE

IB

7%

9%

• In 2017 YTD perm made up 10% of

group GP (~12% in 2007)

• We have the potential to double in

established markets

• Strategic focus paying off as we outgrow

our peer group average

perm as % of GP, FY 2016

1 Competitors; Page group, Hays, Adecco, Manpower

& Robert Half

avg. growth competitors 1

2

2 Organic growth, excluding RPO

2017 YTD perm growth

previous group peak: 12%

|

| |

perm offers ample growth potential

perm growth 2017 YTD

© Randstad 23

0%

10%

20%

30%

40%

France Netherlands Germany Belgium

9% 4% 5% 3%

39%

16%

36%

24%

% of perm in country gross profit perm organic growth

| © Randstad 24

total upcoming cost savings 2018/19: € 90-100M

| |

adjusted EBITA margin progression in 2017: a balancing act adjusted for digital investments & working day effect

© Randstad 25

3,6% 3,8% 3,8%

4,7% 4,5%

5,0% 5,1% 4,9%

5,4%

3%

4%

5%

6%

Q1 2016 Q1 2017(reported)

Q1 2017(adjusted)

Q2 2016 Q2 2017(reported)

Q2 2017(adjusted)

Q3 2016 Q3 2017(reported)

Q3 2017(adjusted)

|

topline growth

business mix

digital opex

© Randstad 26

ebita margin outlook 2017/18

topline growth • consensus + 4.5%

sales growth 2018 • expected market

outperformance

business mix • focus on perm/profs/inhouse/SME;

pricing

digital • ongoing investments • early signs of additional

sales growth

opex • € 90-100M annual

savings by 2019

consensus FY 2017 EBITA margin: 4.6%

outlook 2018: further progression towards 5-6% EBITA margin

| |

acquired companies well on track

© randstad 27

aim to be top 3 in local Staffing

market

strengthen Professionals business

progress towards EVA after 3 years

accelerate digital strategy

in line

ahead

underway

ahead

underway

ahead

| © Randstad 28

M&A outlook 2018 and beyond

tech & touch strategy

• mainly organic through

digital factory

• repair Monster & global

roll-out

professionals

• acceleration through Ausy

(organic & bolt-on M&A)

• over time: small to mid-

sized M&A

staffing

• top position in most relevant

markets, ex-Japan, UK &

Australia

• no priority

• focus on value creation on the basis of current footprint

• no large transformational M&A going forward

• limited M&A in 2018

| |

FCF stability over the past 10 years

© Randstad 29

0,0

0,5

1,0

1,5

2,0

2,5

3,0

0

100

200

300

400

500

600

700

800

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

FCF ex-CICE (€ M) CICE (€ M) leverage ratio

| © Randstad 30

FCF outlook is consistent in various macro scenarios working capital movement is counter cyclical

-

500

1.000

1.500

2.000

2.500

3.000

FCF cumulative 2017to 2020

FCF outlook 2017 – 2020 tested against 6 macro scenarios: bandwidth is only 20%

FCF scenarios accumulated 2017-2020

1 2 3 4 5 6

for

illust

rative p

urp

ose

s, g

raph n

ot

to s

cale

| |

capital allocation priorities & dividend policy

© Randstad 31

investments in organic growth

including digital

maintain cash dividend policy with payout 40 – 50%

selective M&A

when leverage ratio < 1.0 ->

optional additional cash returns

to shareholders

sound FCF outlook

more details H1 2018

old new 1. investments in organic growth

2. M&A activity

3. dividend

4. share buybacks*

5. special dividend*

|

| © Randstad 32

long term value creation through tech & touch strategy optimizing EVA by steering on key levers

questions

& answers