Embed Size (px)

Citation preview

Capital Markets MalaysiaFINANCING THE FUTURE

COPYRIGHT© Securities Commission Malaysia 2015All rights reserved. No part of this publication may be reproduced, stored in or introduced into a retrieval system, or transmitted in any form or by any means (graphical, electronic, mechanical, photocopying, recording, taping or otherwise without the permission of the Capital Markets Promotion Council.

DISCLAIMERThis book aims to provide understanding of the subject and is not exhaustive write-up. It is not intended to be a substituted for legal advice nor does it diminish any duty (statutory or otherwise) that may be applicable to any person under existing laws.

CONTENTS

40 FREQUENTLY ASKED QUESTIONS 43 FOREIGN EXCHANGE ADMINISTRATION RULES APPLICABLE TO ISSUERS

44 FOREIGN EXCHANGE ADMINISTRATION RULES APPLICABLE TO INVESTORS

46 ABBREVIATIONS/ ACRONYMS

APPENDIXINTRODUCTIONMARKET

SEGMENTS

5 FINANCING THE FUTURE

6 CAPITAL MARKETS MALAYSIA (CM2) An ASEAN Asset An Open Market An Efficient Tax Regime A Strong Governance Structure Government Support

12 EQUITIES IPOs Quick Reference Guide

20 FIXED INCOME An ASEAN Product A Resilient Market Product Diversity Methods of Issuing Bonds International Recognition Range of Investors Liberalisation Efforts Quick Reference Guide 25 FUND MANAGEMENT Extraordinary Growth Potential Diversity of Market Segments Wide Market Base Government Support Open Regulation Islamic Asset Management Hub

30 ALTERNATIVE ASSETS Derivatives Venture Capital/Private Equity

33 ISLAMIC CAPITAL MARKET Overview Leader in Innovative Sukuk Established Islamic Fund Management Industry Notable Innovative Sukuk An ASEAN Market Strong Intermediation Capabilities Shariah Governance Facilitative Regulation Value Proposition

4

5

INTR

OD

UC

TIO

N

The future envisaged for the next generation is one that is sustainable, inclusive and innovative. Capital markets play an important role by ensuring that growth is not about maximisation, but optimisation of an economy. In 2013, Malaysia gained recognition as an Advanced Emerging market, with leading positions in regional bonds and global Islamic capital market. It has one of the largest unit trust industries in ASEAN, the third largest bond market in

Asia as a percentage of GDP and the largest sukuk market in the world. As such, Capital Markets Malaysia (CM2) is a prime platform for investors and issuers to finance their future growth plans. By promoting diversity, CM2 is a multi-faceted market with a wide range of conventional and Islamic products. A strong governance infrastructure coupled with intuitive government support, enables an efficient marketplace that will harness the vibrancy of the ASEAN potential. An ideal platform for small and medium sized companies to seek financing, investors in turn can be confident of stable long term investment returns.

FINANCING THE FUTURE

6

Source: IMF’s World Economic Outlook database, October 2014

*forecast starts from 2014

CAPITAL MARKETS MALAYSIA (CM2)

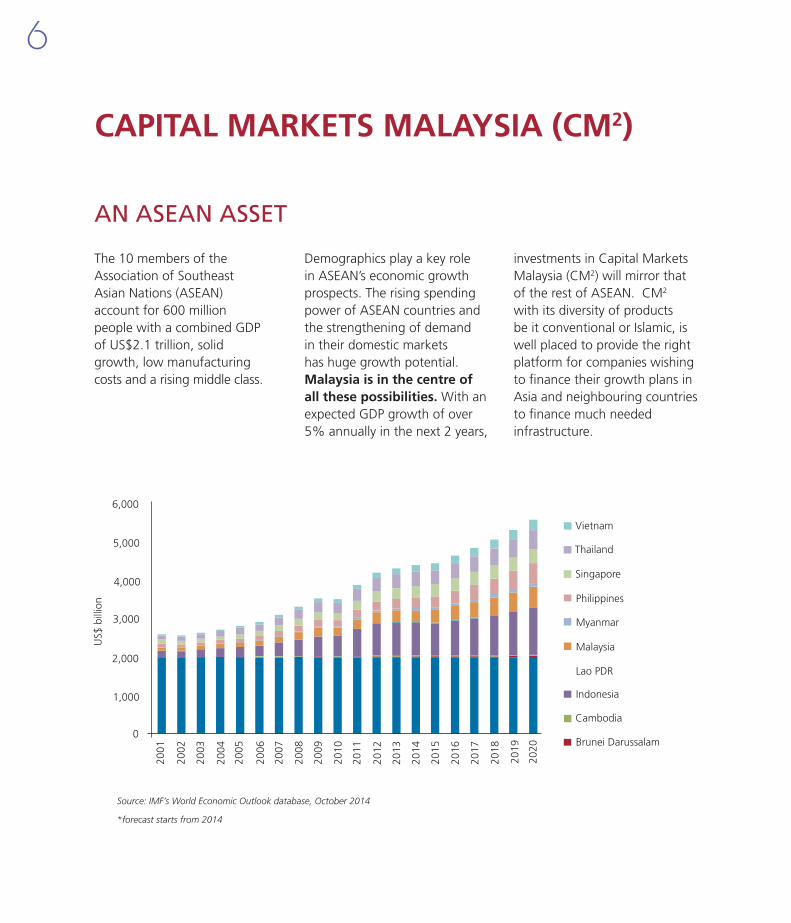

The 10 members of the Association of Southeast Asian Nations (ASEAN) account for 600 million people with a combined GDP of US$2.1 trillion, solid growth, low manufacturing costs and a rising middle class.

Demographics play a key role in ASEAN’s economic growth prospects. The rising spending power of ASEAN countries and the strengthening of demand in their domestic markets has huge growth potential. Malaysia is in the centre of all these possibilities. With an expected GDP growth of over 5% annually in the next 2 years,

AN ASEAN ASSET

6,000

2001

Brunei Darussalam

Cambodia

Indonesia

Lao PDR

Malaysia

Myanmar

Philippines

Singapore

Thailand

Vietnam

investments in Capital Markets Malaysia (CM2) will mirror that of the rest of ASEAN. CM2 with its diversity of products be it conventional or Islamic, is well placed to provide the right platform for companies wishing to finance their growth plans in Asia and neighbouring countries to finance much needed infrastructure.

5,000

4,000

3,000

2,000

1,000

0

US$

bill

ion

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

7

AN OPEN MARKET

There are no capital and exchange restrictions in Malaysia. Global investors are free to buy, sell and hedge RM and RM-denominated securities.

Malaysia’s liberalised foreign exchange administration (FEA) rules enhances Malaysia’s competitiveness and business efficiency, while promoting financial and economic stability.

The relaxation in rulings was made in tandem with the readiness of the Malaysian economy to support the country’s growth and competitiveness, while creating a conducive business environment for international financial institutions.

Apart from enhancing Malaysia’s competitiveness and business

efficiency, the liberal FEA rules enable greater trade in foreign currencies. With regards to sukuk issuances, the relaxed FEA rules enable foreign entities to raise ringgit and foreign currency-denominated funds from Malaysia. The international issuers can issue multi-currency sukuk and have the flexibility to swap domestic currency funding into other currencies.

Coupon/interest income derived by non-resident companies from:

• ringgit-denominatedIslamicsecuritiesanddebentures, other than convertible loan stocks,

• approvedbytheSecuritiesCommission;and

• securitiesissuedbytheGovernmentofMalaysia or Bank Negara Malaysia.

AN EFFICIENT TAX REGIME

Malaysia does not have Capital Gains Tax. No withholding tax on interest derived from the following:

INTEREST

Interest accruing to any resident or non-resident individual, unit trust and listed closed-end fund from:

• bondsorsecuritiesissuedorguaranteedbytheGovernmentofMalaysia;

• debentures,otherthanconvertibleloan stock, approved by the Securities Commission;and

• BonSimpananMalaysiaissuedbyBankNegara Malaysia.

COUPON/INTEREST INCOME

8

A STRONG GOVERNANCE STRUCTURE

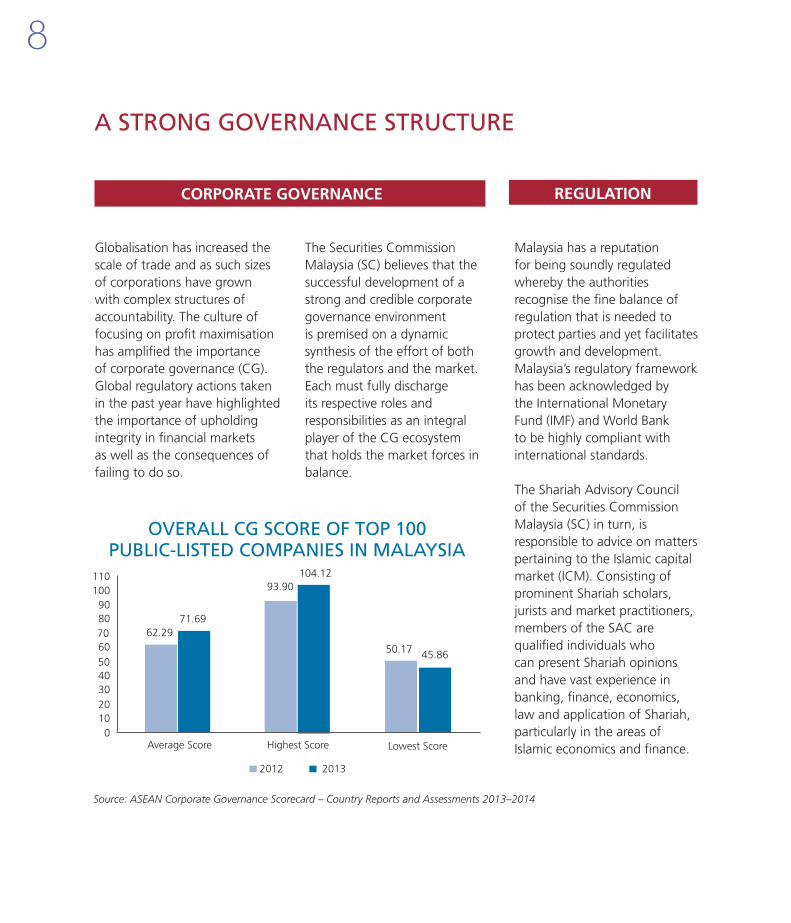

Globalisation has increased the scale of trade and as such sizes of corporations have grown with complex structures of accountability. The culture of focusing on profit maximisation has amplified the importance of corporate governance (CG). Global regulatory actions taken in the past year have highlighted the importance of upholding integrity in financial markets as well as the consequences of failing to do so.

The Securities Commission Malaysia (SC) believes that the successful development of a strong and credible corporate governance environment is premised on a dynamic synthesis of the effort of both the regulators and the market. Each must fully discharge its respective roles and responsibilities as an integral player of the CG ecosystem that holds the market forces in balance.

Malaysia has a reputation for being soundly regulated whereby the authorities recognise the fine balance of regulation that is needed to protect parties and yet facilitates growth and development. Malaysia’s regulatory framework has been acknowledged by the International Monetary Fund (IMF) and World Bank to be highly compliant with international standards.

The Shariah Advisory Council of the Securities Commission Malaysia (SC) in turn, is responsible to advice on matters pertaining to the Islamic capital market (ICM). Consisting of prominent Shariah scholars, jurists and market practitioners, members of the SAC are qualified individuals who can present Shariah opinions and have vast experience in banking, finance, economics, law and application of Shariah, particularly in the areas of Islamic economics and finance.

REGULATIONCORPORATE GOVERNANCE

2012 2013

62.2971.69

93.90104.12

50.17 45.86

Average Score Highest Score Lowest Score

OVERALL CG SCORE OF TOP 100 PUBLIC-LISTED COMPANIES IN MALAYSIA

0102030405060708090

100110

Source: ASEAN Corporate Governance Scorecard – Country Reports and Assessments 2013–2014

9

GOVERNMENT SUPPORT

To promote Malaysia as an international Islamic financial centre, the government has implemented measures such as tax exemptions, tax neutrality provisions and other incentives across the various Islamic finance market segments. One of the examples of tax neutrality is

ATTRACTIVE FISCAL

INCENTIVES AND TAX

NEUTRALITY

Islamic finance transactions are treated similarly to conventional financing transactions for tax purposes. In addition, sale or lease of any assets that is performed strictly to meet Shariah requirements would be ignored for tax purposes.

Malaysia’s facilitative environment encompasses a sound infrastructure platform, consisting of the Electronic Trading Platform (ETP) and the Real-time Electronic Transfer of Funds and Securities (RENTAS) system. These systems allow for an efficient platform for the trading of bonds, with a high level of post-trade transparency and market liquidity. For global investments, flexibility is also accorded to foreign investors to leverage on international clearing and settlement systems.

Malaysia provides a facilitative frameworkforsukukissuance;both for local and international issuers. In addition to issuing ringgit sukuk, the current issuance framework allows for issuers to issue a non-ringgit sukuk in Malaysia.

FACILITATIVE ENVIRONMENT

Moreover, Malaysia has an active secondary market, which gives investors the option to either hold investments until maturity or to take profit. The secondary market enables greater trading activity and attracts more investors including foreign-owned corporations, who are continuously tapping the market for funding.

This eventually augments the depth and liquidity of the sukuk market. Investors will benefit from the wide array and increasing size of sukuk transactions as they look towards diversifying their asset portfolios.

In this aspect, Malaysia offers well-developed value propositions, which enables a dynamic scenario that benefits both issuers and investors.

10

Malaysia’s diversity of market intermediaries consists of investment banks, local and foreign Islamic banks, brokers and fund managers who engage in a number of activities ranging from underwriting complex financial transactions to advising on sophisticated transaction structures.

In addition, most of these intermediaries have participated in Malaysia’s many notable sukuk issuances. As such, they possess a proven track record and in-depth experience. Capitalising on the

DIVERSITY OF FINANCIAL

INTERMEDIARIES

inherent strengths of Malaysia’s intermediaries enables issuers to benefit from a smoother issuance process while reducing costs. The reputation of these intermediaries adds further credibility to the issuance.

Malaysia’s market intermediaries are also internationally recognised for their innovative capability in structuring products, especially sukuk. This is attributed to their expert use of various Islamic principles or a combination of principles to produce truly customised sukuk offerings.

Malaysia’s legal framework caters for Islamic finance matters with a dedicated judge at the High Court level. The Kuala Lumpur Regional Centre for Arbitration (KLRCA) has specific capabilities to deal with Islamic contract matters. This legal framework enables the enforceability of Shariah-based contracts for Islamic finance while providing governance and legal redress for Islamic financial institutions. It also provides for strong investor protection.

In particular, the Capital Markets Services Act 2007 (CMSA) defines the parameters for permitted capital market activities

ADOPTION OF GLOBAL LEGAL

AND REGULATORY BEST PRACTICES

in Malaysia, while reinforcing the protection framework and promoting international best practices among financial institutions. These and other such regulatory guidelines have been instrumental in providing industry consistency and clarity for ICM in Malaysia. In addition, Malaysia’s regulatory guidelines have also set benchmarks for other countries in developing their own Islamic capital markets.

The legal and regulatory framework is constantly reviewed taking into consideration latest market, products and Shariah issues to ensure continuous development in ICM.

11

ISLAMIC CAPITAL

MARKET

Overview

Leader in Innovative SukukFacilitative RegulationsAn ASEAN

Market

Notable Innovative Sukuk

FIXED INCOME An ASEAN ProductA Resilient MarketProduct DiversityMethods of Issuing BondsInternational RecognitionRange of InvestorsLiberalisation EffortsQuick Reference Guide

EQU

ITIE

SIP

Os

Qui

ck R

efer

ence

Gui

de FUND MANAGEMENT Extraordinary Growth PotentialDiversity of Market Segments Wide Market BaseGovernment SupportOpen RegulationIslamic Asset Management HubAlternative AssetsVenture Capital/Private Equity

MA

RKET

SEG

MEN

TS

12

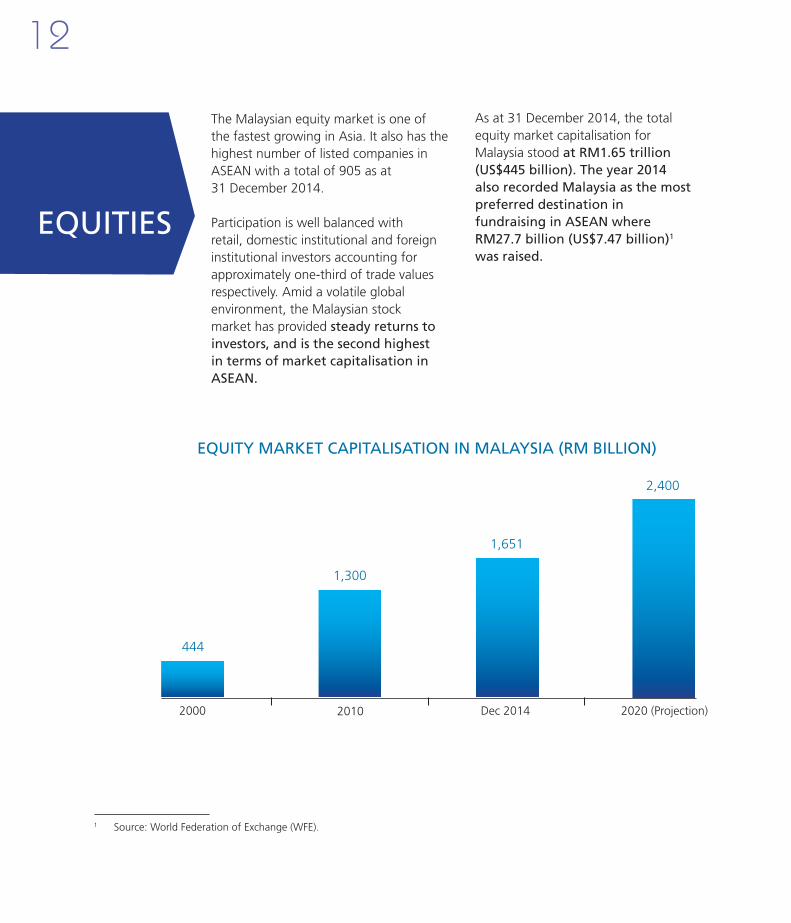

EQUITIES

The Malaysian equity market is one of the fastest growing in Asia. It also has the highest number of listed companies in ASEAN with a total of 905 as at 31 December 2014.

Participation is well balanced with retail, domestic institutional and foreign institutional investors accounting for approximately one-third of trade values respectively. Amid a volatile global environment, the Malaysian stock market has provided steady returns to investors, and is the second highest in terms of market capitalisation in ASEAN.

As at 31 December 2014, the total equity market capitalisation for Malaysia stood at RM1.65 trillion (US$445 billion). The year 2014 also recorded Malaysia as the most preferred destination in fundraising in ASEAN where RM27.7 billion (US$7.47 billion)1 was raised.

EQUITY MARKET CAPITALISATION IN MALAYSIA (RM BILLION)

444

1,300

1,651

2,400

2000 2010 Dec 2014 2020 (Projection)

1 Source: World Federation of Exchange (WFE).

13

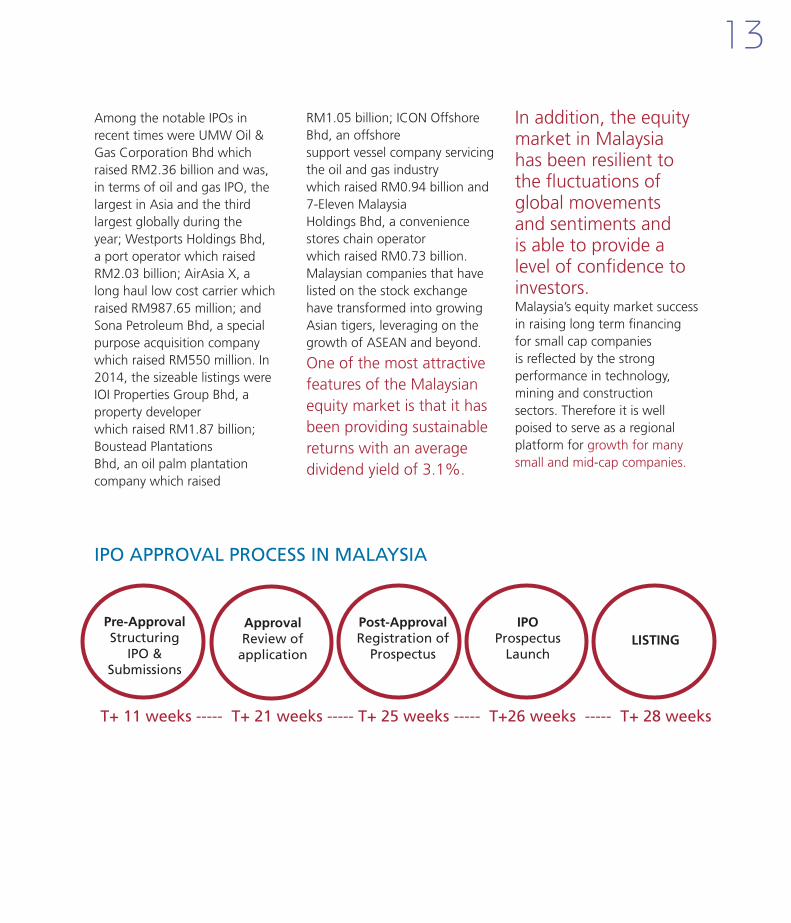

Among the notable IPOs in recent times were UMW Oil & Gas Corporation Bhd which raised RM2.36 billion and was, in terms of oil and gas IPO, the largest in Asia and the third largest globally during the year;WestportsHoldingsBhd,a port operator which raised RM2.03billion;AirAsiaX,along haul low cost carrier which raisedRM987.65million;andSona Petroleum Bhd, a special purpose acquisition company which raised RM550 million. In 2014, the sizeable listings were IOI Properties Group Bhd, a property developerwhichraisedRM1.87billion;Boustead PlantationsBhd, an oil palm plantation company which raised

IPO APPROVAL PROCESS IN MALAYSIA

RM1.05billion;ICONOffshoreBhd, an offshoresupport vessel company servicing the oil and gas industrywhich raised RM0.94 billion and 7-Eleven MalaysiaHoldings Bhd, a convenience stores chain operatorwhich raised RM0.73 billion. Malaysian companies that have listed on the stock exchange have transformed into growing Asian tigers, leveraging on the growth of ASEAN and beyond.

One of the most attractive features of the Malaysian equity market is that it has been providing sustainable returns with an average dividend yield of 3.1%.

In addition, the equity market in Malaysia has been resilient to the fluctuations of global movements and sentiments and is able to provide a level of confidence to investors.Malaysia’s equity market success in raising long term financing for small cap companies is reflected by the strong performance in technology, mining and construction sectors. Therefore it is well poised to serve as a regional platform for growth for many small and mid-cap companies.

Pre-ApprovalStructuring

IPO &Submissions

T+ 11 weeks ----- T+ 21 weeks ----- T+ 25 weeks ----- T+26 weeks ----- T+ 28 weeks

ApprovalReview of

application

Post-ApprovalRegistration of

Prospectus

IPOProspectus

LaunchLISTING

14

Malaysia benefits from a strong presence of domestic institutions and retail that provide the necessary stability and liquidity to keep the market vibrant. For example, in 2014, 50% of daily

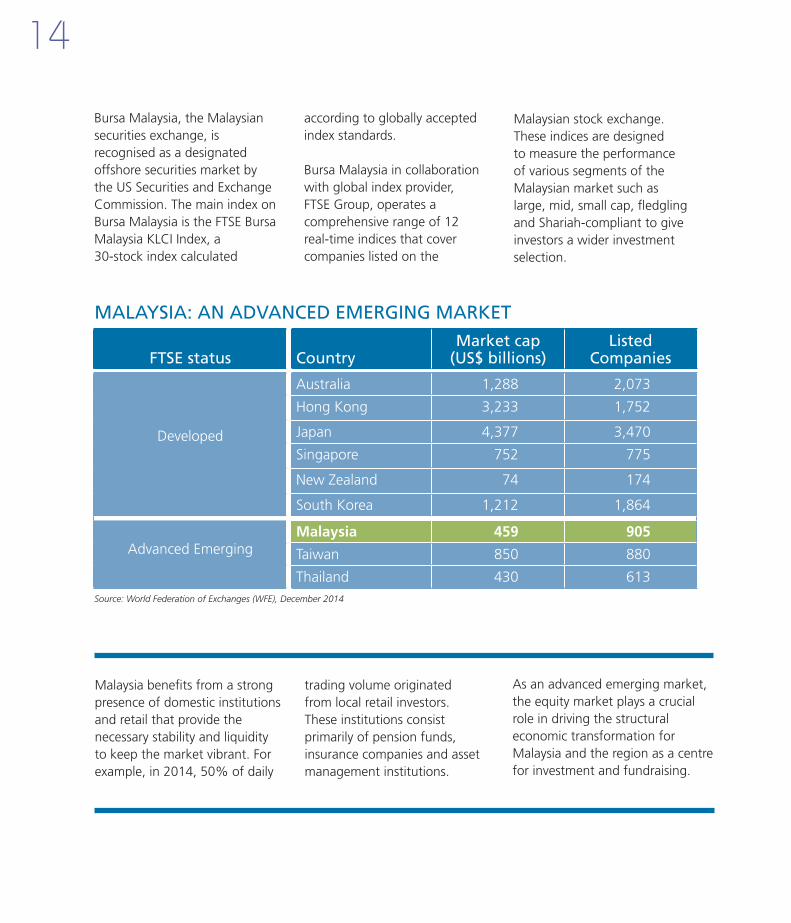

Bursa Malaysia, the Malaysian securities exchange, is recognised as a designated offshore securities market by the US Securities and Exchange Commission. The main index on Bursa Malaysia is the FTSE Bursa Malaysia KLCI Index, a 30-stock index calculated

according to globally accepted index standards.

Bursa Malaysia in collaboration with global index provider, FTSE Group, operates a comprehensive range of 12 real-time indices that cover companies listed on the

Source: World Federation of Exchanges (WFE), December 2014

MALAYSIA: AN ADVANCED EMERGING MARKET

FTSE status CountryMarket cap

(US$ billions)Listed

Companies

Developed

Australia 1,288 2,073

Hong Kong 3,233 1,752

Japan 4,377 3,470

Singapore 752 775

New Zealand 74 174

South Korea 1,212 1,864

Advanced EmergingMalaysia 459 905

Taiwan 850 880

Thailand 430 613

Malaysian stock exchange. These indices are designed to measure the performance of various segments of the Malaysian market such as large, mid, small cap, fledgling and Shariah-compliant to give investors a wider investment selection.

trading volume originated from local retail investors. These institutions consist primarily of pension funds, insurance companies and asset management institutions.

As an advanced emerging market, the equity market plays a crucial role in driving the structural economic transformation for Malaysia and the region as a centre for investment and fundraising.

15

Foreign investors are free to invest in Malaysia in either ringgit denominated or foreign currency denominated products. There is no restriction for foreign investors on repatriation of funds from divestment of ringgit assets or profits and dividends arising from investments.

16

For established companies with a profit track record of three to five full financial years or companies with a sizeable business

An alternative sponsor-driven market designed for companies of all business sectors that have excellent growth potential

Source: Bursa Malaysia

MAIN MARKET

ACE MARKET

GLOBAL RECOGNITION

17

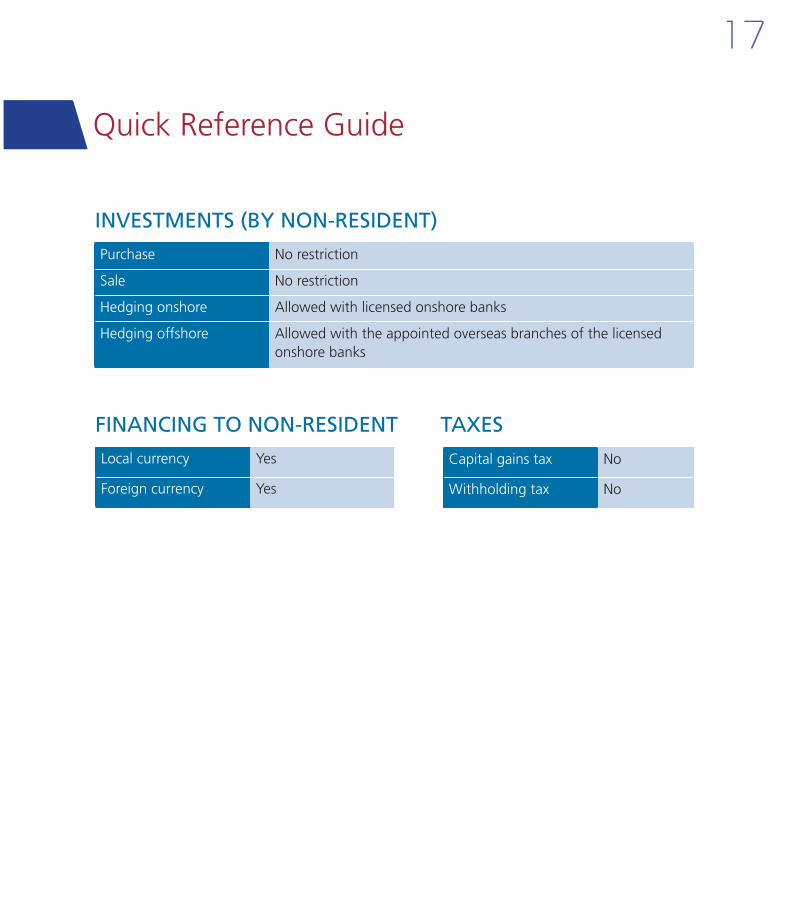

INVESTMENTS (BY NON-RESIDENT)

Purchase No restriction

Sale No restriction

Hedging onshore Allowed with licensed onshore banks

Hedging offshore Allowed with the appointed overseas branches of the licensed onshore banks

TAXES

Local currency Yes

Foreign currency Yes

FINANCING TO NON-RESIDENT

Quick Reference Guide

Capital gains tax No

Withholding tax No

18

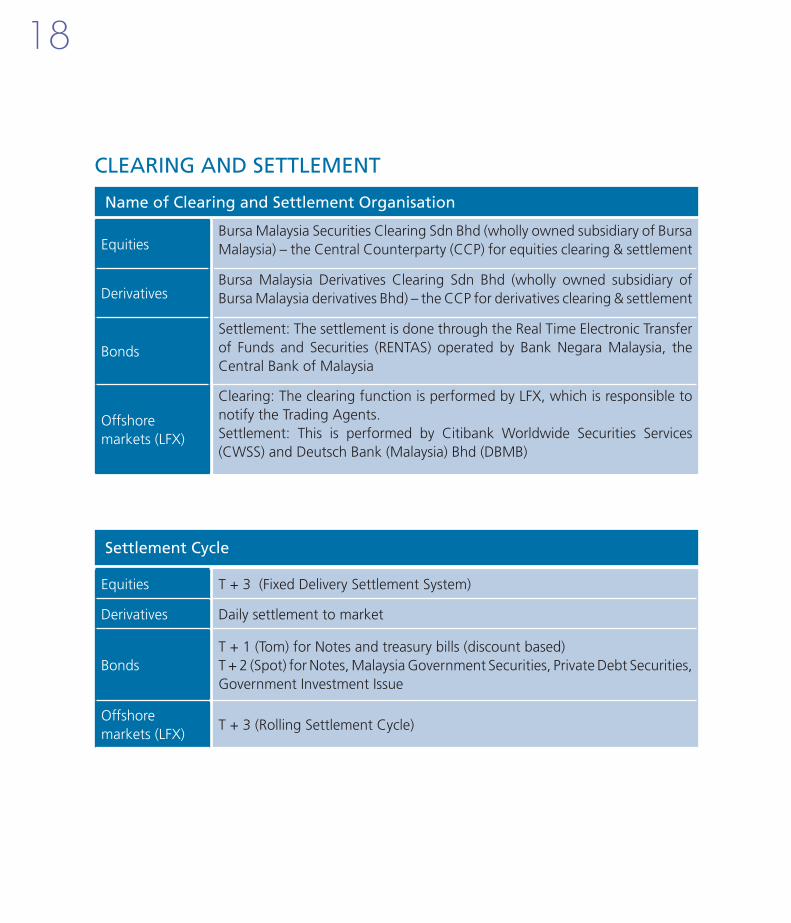

CLEARING AND SETTLEMENT

Name of Clearing and Settlement Organisation

EquitiesBursa Malaysia Securities Clearing Sdn Bhd (wholly owned subsidiary of Bursa Malaysia) – the Central Counterparty (CCP) for equities clearing & settlement

DerivativesBursa Malaysia Derivatives Clearing Sdn Bhd (wholly owned subsidiary of Bursa Malaysia derivatives Bhd) – the CCP for derivatives clearing & settlement

Bonds

Settlement: The settlement is done through the Real Time Electronic Transfer of Funds and Securities (RENTAS) operated by Bank Negara Malaysia, the Central Bank of Malaysia

Offshore markets(LFX)

Clearing:TheclearingfunctionisperformedbyLFX,whichisresponsibletonotify the Trading Agents.Settlement: This is performed by Citibank Worldwide Securities Services (CWSS) and Deutsch Bank (Malaysia) Bhd (DBMB)

Settlement Cycle

Equities T + 3 (Fixed Delivery Settlement System)

Derivatives Daily settlement to market

BondsT + 1 (Tom) for Notes and treasury bills (discount based)T + 2 (Spot) for Notes, Malaysia Government Securities, Private Debt Securities, Government Investment Issue

Offshore markets(LFX)

T + 3 (Rolling Settlement Cycle)

19

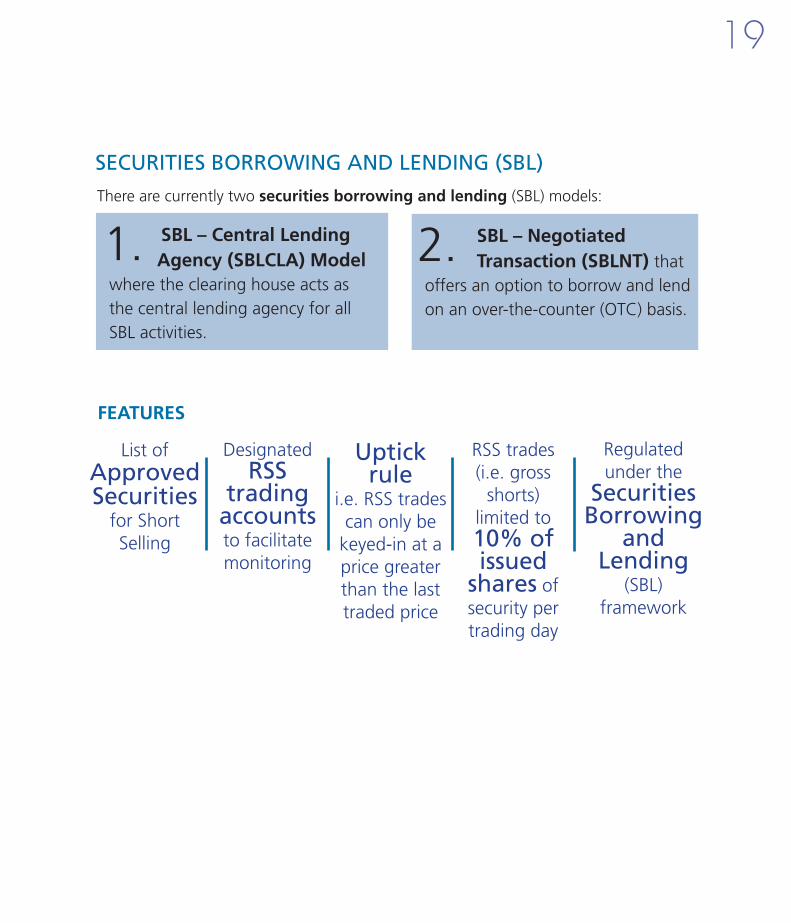

SECURITIES BORROWING AND LENDING (SBL)There are currently two securities borrowing and lending (SBL) models:

1. SBL – Central Lending Agency (SBLCLA) Model where the clearing house acts as the central lending agency for all SBL activities.

SBL – NegotiatedTransaction (SBLNT) that

offers an option to borrow and lend on an over-the-counter (OTC) basis.

2.

List of Approved Securities

for Short Selling

Designated RSS

trading accounts to facilitate monitoring

Uptick rule

i.e. RSS trades can only be

keyed-in at a price greater than the last traded price

RSS trades (i.e. gross

shorts) limited to 10% of issued

shares of security per trading day

Regulated under the

Securities Borrowing

and Lending

(SBL) framework

FEATURES

20

FIXED INCOME

The Malaysian fixed income market remains vibrant, supported by a strong demand from a global pool of steadfast investors. The bond market is an important source of funds as evidenced by the compounded annual growth rate (CAGR) of 11.3% over the last decade.

Infrastructure development has become a critical priority for developing Asia. There has been an observed shift from traditional means of financing through bank borrowings into capital market based financing. The fixed income market has provided a platform for accessing the significant savings in the region and enables issuers to raise financing at a competitive cost.

As at 31 December 2014, the Malaysian bond market stood at a value of RM1.1 trillion (US$299.7 billion). The bond market (including Shariah-compliant bonds) accounted for 40.2% of total corporate financing.

PRODUCT DIVERSITYThe range of debt securities issued has in part assisted in increasing the types of products available to cater to an increasing demand

for innovation and portfolio diversification from investors. The focus on product diversity forms part of the efforts by the

SC in deepening and developing their debt capital markets, and

in turn increasing liquidity. Some of these products include asset-

backed securities, perpetual bonds, agro sukuk, and stapled

securities among others.

RESILIENT MARKETMalaysia’s bond market is

resilient to volatile international capital flows. At RM1.1 trillion, it is the third largest in Asia relative to the size of the economy. The depth of the market provides absorptive capacity for portfolios to be rebalanced across maturities in an orderly manner. Hence, Malaysia is not significantly affected by the retreat of

foreign portfolio funds which other emerging bond markets

have experienced in recent times.

AN ASIAN PRODUCTThe Malaysian bond market is expected to grow to a value of RM2.1 trillion (US$684 billion)

by 2020 with an average annual growth rate of 11.3% (from year 2004 –2014). The growth opportunities in the

bond market are also expected to further escalate as the entry point projects under

the Malaysian Government’s Economic Transformation

Programme (ETP) progresses into implementation.

21

Methods of Issuing Bonds

AuctionBank Negara Malaysia (BNM) will issue government bonds through competitive auctions. Successful bidders are determined based on the lowest yields offered. The coupon rate is then fixed at the weighted average yield of the successful bids.

Principal Advisers can offer through auction BNM notes.

Direct Placement or TenderOther types of bonds are issued directly via direct placement or private tender.

Listed on Bursa MalaysiaBursa Malaysia’s “Exempt” Regime

Under an “Exempt” Regime, bonds and sukuk can be listed but will not be traded or quoted on the Exchange. To date, there are 20 sukuk issuers and seven conventional bond issuers listed under this Regime.

22

INTERNATIONAL RECOGNITION

The persistent demand for Malaysian fixed income is

indicative of the ease of access to the markets for offshore

investors. First, Malaysian fixed income is a part of developed market bond indices such as

the Citibank World Government Bond Index − Malaysia is notably one of the three

emerging markets in the index. This index has approximately

US$2 trillion of funds tracking it.

To subscribe or trade in debt securities or sukuk, investors must open an account with Authorised Depository institutions (ADIs).

ADIs offer protection to investors with regard to interest payments and redemption proceeds. Each ADI has to ensure separate accounts are maintained for each customer and their own holdings.

RANGE OF INVESTORS Malaysia as the largest fixed income

market in ASEAN is seeing a fair share of non-resident participation and investment

particularly from investors in advanced economics.

With the launch of the first Retail Sukuk in 2013, the bond market opened up to retail investors too1. The Malaysian

market mirrors growth potential of Asia which is extraordinary with the growing

middle class numbers, the naturally higher propensity to save for the future

and to invest in the capital markets.

LIBERALISATION EFFORTS As part of the comprehensive framework underlying the Malaysian fixed income market, the Bond Pricing Agency Malaysia (BPAM) was set up as part of efforts to increase

transparency. The Malaysian Government has also liberalised requirements for credit ratings by allowing international

credit rating agencies with full foreign ownership to operate in the Malaysian market from January 2017.

Furthermore, CM2 will provide a platform that will catalyse more cross-border and multi-currency bond and sukuk

issuances as well as explore potential new products such as high-yield bonds with a view to broaden the credit spectrum

of investable asset classes.

1 DanaInfra Nasional Bhd [Government entity set up to finance (Mass Rapid Transit) MRT Project] of RM300 million to retail investors, as part of a RM8 billion Islamic Commercial Papers/ Medium-Term Notes Programme. This retail sukuk is listed on the Loans and Bonds Board of Bursa Malaysia.

In 2014, SC announced the introduction of a new regulatory framework for the wholesale market with the objective of significantly reducing time to market for wholesale products. Under this framework, offerings for wholesale products are exempted from SC’s authorisation under section 212 of the CMSA, subject to lodgement of the requisite information and documents. This framework will come into effect in 2015.

INTRODUCTION OF LODGE AND LAUNCH FRAMEWORK

23

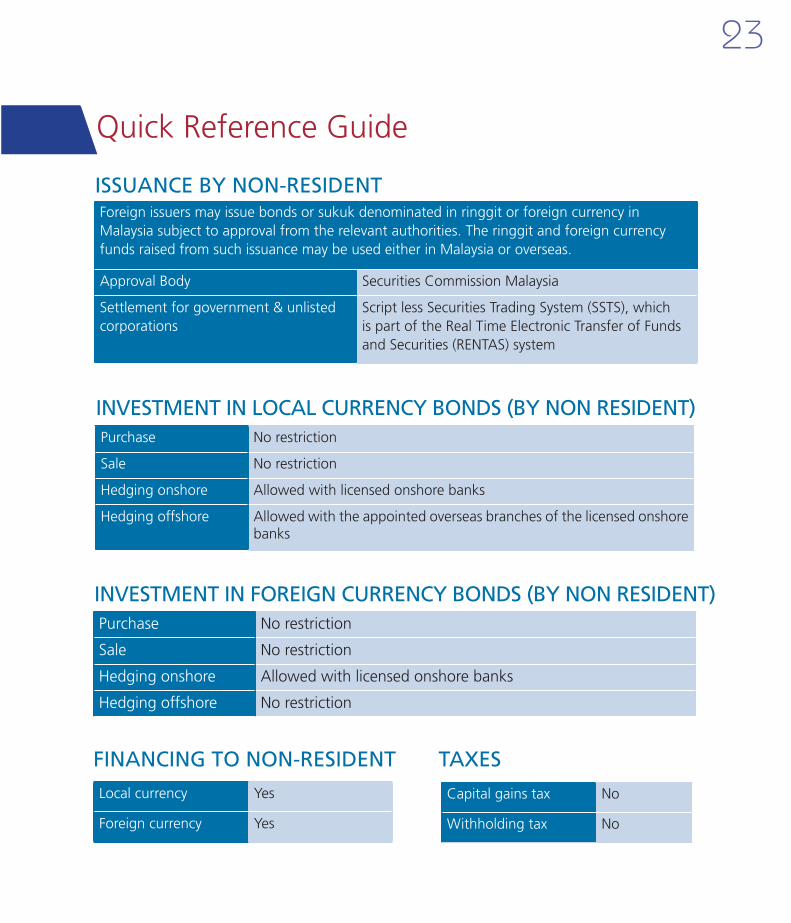

ISSUANCE BY NON-RESIDENTForeign issuers may issue bonds or sukuk denominated in ringgit or foreign currency in Malaysia subject to approval from the relevant authorities. The ringgit and foreign currency funds raised from such issuance may be used either in Malaysia or overseas.

Approval Body Securities Commission Malaysia

Settlement for government & unlisted corporations

Script less Securities Trading System (SSTS), which is part of the Real Time Electronic Transfer of Funds and Securities (RENTAS) system

INVESTMENT IN LOCAL CURRENCY BONDS (BY NON RESIDENT)Purchase No restriction

Sale No restriction

Hedging onshore Allowed with licensed onshore banks

Hedging offshore Allowed with the appointed overseas branches of the licensed onshore banks

INVESTMENT IN FOREIGN CURRENCY BONDS (BY NON RESIDENT)Purchase No restriction

Sale No restriction

Hedging onshore Allowed with licensed onshore banks

Hedging offshore No restriction

Quick Reference Guide

TAXES

Local currency Yes

Foreign currency Yes

FINANCING TO NON-RESIDENT

Capital gains tax No

Withholding tax No

24

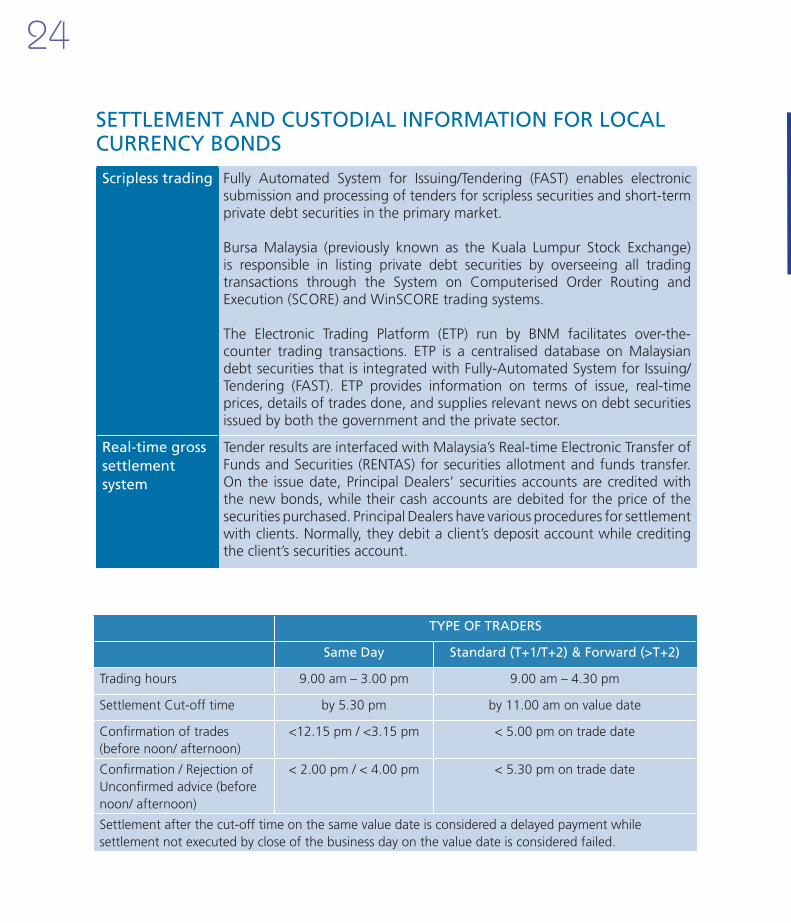

SETTLEMENT AND CUSTODIAL INFORMATION FOR LOCAL CURRENCY BONDS

Scripless trading Fully Automated System for Issuing/Tendering (FAST) enables electronic submission and processing of tenders for scripless securities and short-term private debt securities in the primary market.

Bursa Malaysia (previously known as the Kuala Lumpur Stock Exchange) is responsible in listing private debt securities by overseeing all trading transactions through the System on Computerised Order Routing and Execution (SCORE) and WinSCORE trading systems.

The Electronic Trading Platform (ETP) run by BNM facilitates over-the-counter trading transactions. ETP is a centralised database on Malaysian debt securities that is integrated with Fully-Automated System for Issuing/Tendering (FAST). ETP provides information on terms of issue, real-time prices, details of trades done, and supplies relevant news on debt securities issued by both the government and the private sector.

Real-time gross settlement system

Tender results are interfaced with Malaysia’s Real-time Electronic Transfer of Funds and Securities (RENTAS) for securities allotment and funds transfer. On the issue date, Principal Dealers’ securities accounts are credited with the new bonds, while their cash accounts are debited for the price of the securities purchased. Principal Dealers have various procedures for settlement with clients. Normally, they debit a client’s deposit account while crediting the client’s securities account.

TYPE OF TRADERS

Same Day Standard (T+1/T+2) & Forward (>T+2)

Trading hours 9.00 am – 3.00 pm 9.00 am – 4.30 pm

Settlement Cut-off time by 5.30 pm by 11.00 am on value date

Confirmation of trades (before noon/ afternoon)

<12.15 pm / <3.15 pm < 5.00 pm on trade date

Confirmation / Rejection of Unconfirmed advice (before noon/ afternoon)

< 2.00 pm / < 4.00 pm < 5.30 pm on trade date

Settlement after the cut-off time on the same value date is considered a delayed payment while settlement not executed by close of the business day on the value date is considered failed.

25

FUND MANAGEMENT

With its many advantages in geographical location, a growing pool of skilled talent and professional and legal services, Malaysia is well placed as a regional player for fund management.

The exponential growth in the fund management industry CAGR of 18.6% over 10 years has been largely underpinned by the strong growth in the unit trust industry. Over the same period, the net asset value (NAV) of unit trust funds (including Islamic unit trusts) grew from RM87.4 billion (US$23.58 billion) in 2004 to RM343.02 billion (US$ 92.53 billion) in 2014.

Fund management is the fastest

growing segment in Malaysia’s

capital market

EXTRAORDINARY GROWTH POTENTIAL The assets under management (AUM) is projected to rise from

RM377.4 billion in 2010 to RM1.6 trillion in 2020.With a penetration rate in Malaysia’s unit trust industry amounting to 18% as at end 2010, there are significant

opportunities within the industry as this rate is expected to almost double to a penetration rate of 34% by 2020. The

Malaysian market reflects a similar potential for growth in Asia with the growing middle-class numbers, the naturally higher propensity to save for the future and to invest in the capital

markets.

The development in the unit trust industry has been aided by several factors, including regulatory enhancements which

have facilitated product expansion, strengthened investor safeguards, improved time-to-market efficiencies and expanded the distribution channels. Since June 2010, unit trust funds can adopt multi-class structures which enable them to be tailored to

meet the needs of different investors.

DIVERSITY OF MARKET SEGMENTS

Besides the potential of institutional and retail fund products, Malaysia’s private retirement scheme industry is set to rise as a new and exciting segment given Malaysia’s growing young population. It is projected that assets under management

in the private retirement scheme (PRS) industry will grow to RM30.9 billion (US$10.3 billion) in the next

10 years. Developed in line with international best practices, this

industry which is still in its infancy is garnering significant support from the Government through incentives for young professionals to invest in

PRS products.

26

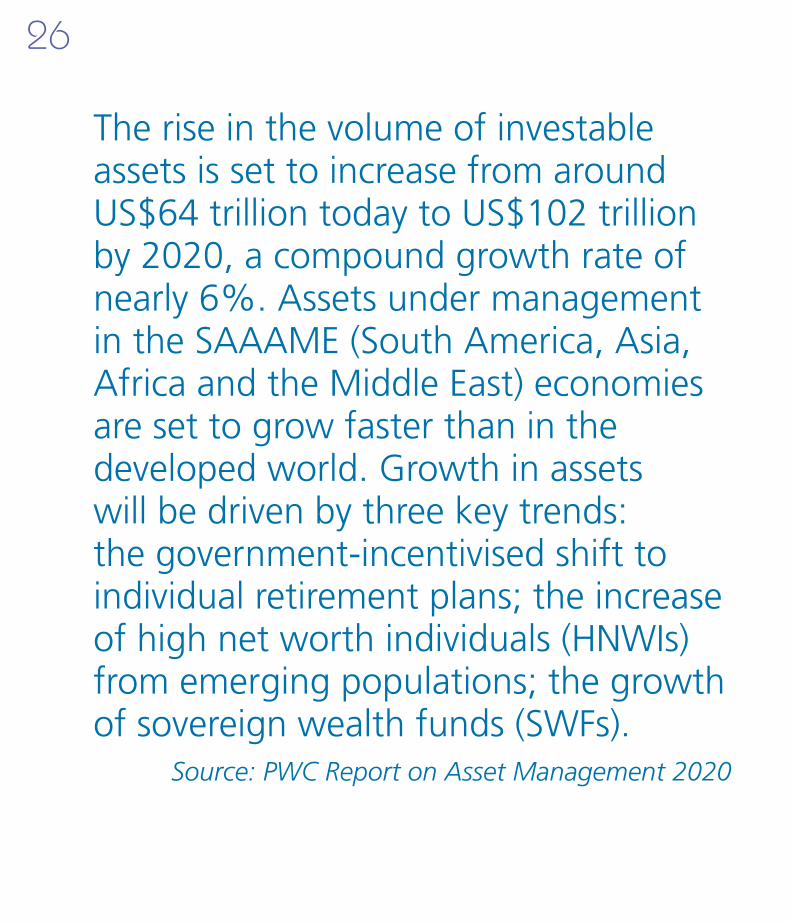

The rise in the volume of investable assets is set to increase from around US$64 trillion today to US$102 trillion by 2020, a compound growth rate of nearly 6%. Assets under management in the SAAAME (South America, Asia, Africa and the Middle East) economies are set to grow faster than in the developed world. Growth in assets will be driven by three key trends: the government-incentivised shift to individualretirementplans;theincreaseof high net worth individuals (HNWIs) fromemergingpopulations;thegrowthof sovereign wealth funds (SWFs).

Source: PWC Report on Asset Management 2020

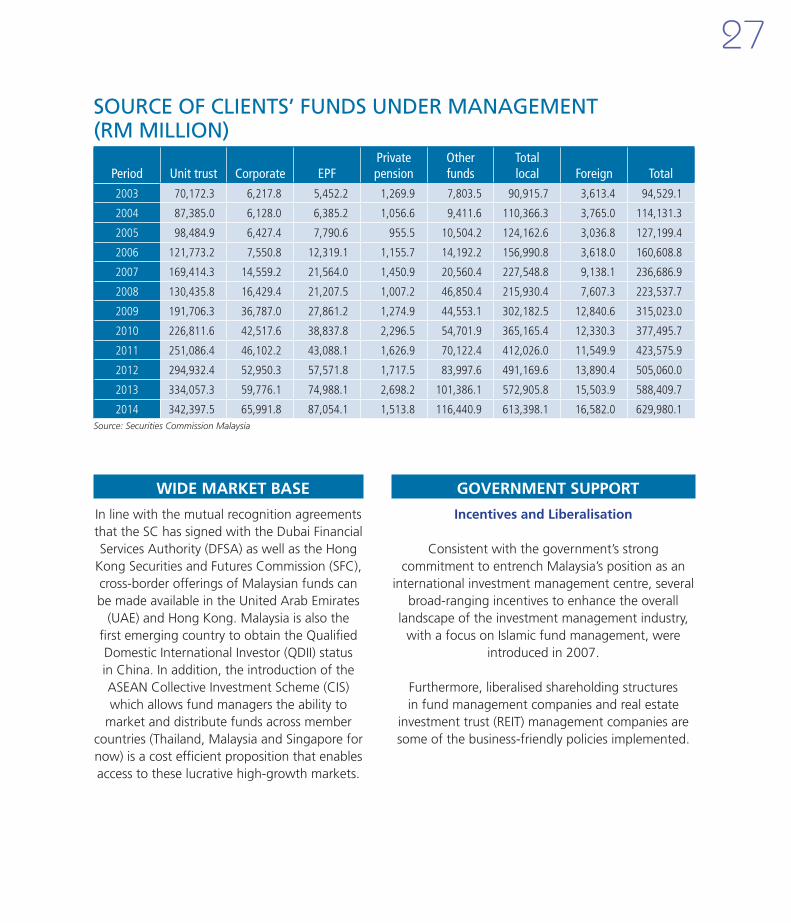

27

SOURCE OF CLIENTS’ FUNDS UNDER MANAGEMENT (RM MILLION)

Period Unit trust Corporate EPFPrivate pension

Other funds

Totallocal Foreign Total

2003 70,172.3 6,217.8 5,452.2 1,269.9 7,803.5 90,915.7 3,613.4 94,529.1

2004 87,385.0 6,128.0 6,385.2 1,056.6 9,411.6 110,366.3 3,765.0 114,131.3

2005 98,484.9 6,427.4 7,790.6 955.5 10,504.2 124,162.6 3,036.8 127,199.4

2006 121,773.2 7,550.8 12,319.1 1,155.7 14,192.2 156,990.8 3,618.0 160,608.8

2007 169,414.3 14,559.2 21,564.0 1,450.9 20,560.4 227,548.8 9,138.1 236,686.9

2008 130,435.8 16,429.4 21,207.5 1,007.2 46,850.4 215,930.4 7,607.3 223,537.7

2009 191,706.3 36,787.0 27,861.2 1,274.9 44,553.1 302,182.5 12,840.6 315,023.0

2010 226,811.6 42,517.6 38,837.8 2,296.5 54,701.9 365,165.4 12,330.3 377,495.7

2011 251,086.4 46,102.2 43,088.1 1,626.9 70,122.4 412,026.0 11,549.9 423,575.9

2012 294,932.4 52,950.3 57,571.8 1,717.5 83,997.6 491,169.6 13,890.4 505,060.0

2013 334,057.3 59,776.1 74,988.1 2,698.2 101,386.1 572,905.8 15,503.9 588,409.7

2014 342,397.5 65,991.8 87,054.1 1,513.8 116,440.9 613,398.1 16,582.0 629,980.1Source: Securities Commission Malaysia

WIDE MARKET BASE

In line with the mutual recognition agreements that the SC has signed with the Dubai Financial Services Authority (DFSA) as well as the Hong

Kong Securities and Futures Commission (SFC), cross-border offerings of Malaysian funds can be made available in the United Arab Emirates

(UAE) and Hong Kong. Malaysia is also the first emerging country to obtain the Qualified Domestic International Investor (QDII) status in China. In addition, the introduction of the ASEAN Collective Investment Scheme (CIS) which allows fund managers the ability to

market and distribute funds across member countries (Thailand, Malaysia and Singapore for now) is a cost efficient proposition that enables access to these lucrative high-growth markets.

GOVERNMENT SUPPORT

Incentives and Liberalisation

Consistent with the government’s strong commitment to entrench Malaysia’s position as an

international investment management centre, several broad-ranging incentives to enhance the overall

landscape of the investment management industry, with a focus on Islamic fund management, were

introduced in 2007.

Furthermore, liberalised shareholding structures in fund management companies and real estate

investment trust (REIT) management companies are some of the business-friendly policies implemented.

28

Tax IncentivesFor unit trust funds, interest income received by the fund from investments in fixed income securities / instruments aretaxexempt;

For real estate investment trusts (REITs):

Stamp duty exemption for sale of realestatetoaREIT;

Tax exemption at REIT level (tax transparency) provided that 90% ofitsincomeisdistributed;and

Lower income tax on income received from a REIT (i.e. 10% for individuals and institutions).

29

OPEN REGULATION

Apart from tax incentives, there has been a progressive shift from merit assessment

towards disclosure-based regulation for both fundraising and investment products. This has resulted in greater certainty and transparency for issuers and intermediaries to raise funds

and launch products in a timely and cost efficient manner. More importantly, this helps to promote product expansion and widening

of delivery channels which serve as catalysts for growth.

ISLAMIC ASSET MANAGEMENT HUB

Malaysia today has become a leading hub for Islamic Asset Management. Its position as a global Islamic financial centre has successfully attracted

local and international players to establish dedicated Islamic fund management operations. There are

20 Islamic fund management companies operating inMalaysiaatthemoment;theseincludeAberdeen

Islamic Asset Management, AmIslamic Fund Management, RHB Islamic Asset Management,

BNP Paribas Islamic Asset Management and Franklin Templeton Asset Management.

A noteworthy value proposition of the Malaysian capital market is that over 74% of Bursa Malaysia stocks are Shariah compliant, which includes blue chip companies from oil and gas, infrastructure,

consumer and industry-based sectors. As a result, there is a tremendous supply of investment avenues

that could benefit investors in the Islamic wealth management arena.

OTHER REGULATORY REQUIREMENTS

One-time approval of unit trustmanagement companies and trustees

A management company or trustee will only be required to seek a one-time approval for the purposes of section 289 of the CMSA

compared to the previous approach of ‘per-fund’ approval. Approved management

companies and trustees will be admitted into an ‘Approved List’ and shall be deemed approved for future issuances, offerings or

invitations to subscribe for or purchase of unit trusts. This will expedite the approval process

for the establishment of new funds.

Notification for outsourcing of material functions

SC removed the requirement for approval before an intermediary outsources a material function. Instead, licensed intermediaries only need to notify the SC within two weeks upon

signing the service level agreement for any material outsourcing arrangement. The shift from a pre-approval to a notification process

removes the prescriptive requirement and sets out guidance for intermediaries in assessing an

outsourcing arrangement.

INTRODUCTION OF LODGE ANDLAUNCH FRAMEWORK

In 2014, SC announced the introduction of a new regulatory framework for the wholesale market with the objective of significantly reducing time to market

for wholesale products. Under this framework, offerings for wholesale products are exempted from SC’s authorisation under section 212 of the CMSA, subject to lodgement of the requisite information and documents. This framework will come into

effect in 2015.

30

ALTERNATIVE ASSETS

Malaysia is the world’s second largest crude palm oil producer and exporter and serves as the global centre for price discovery vis-à-vis crude palm oil (CPO). Understandably, the Malaysian derivatives market is dominated by CPO futures contracts. In fact, Bursa Malaysia operates the most liquid and successful crude palm oil futures (FCPO) contract in the world.

Driven by FCPO, Malaysia’s derivative market has seen the notional value of derivatives traded at RM806.7 billion (US$219.7 billion) in 2014.

SC approved the reintroduction of two futures contracts to assist investors in broadening their trading and investment opportunities as well as provide suitable hedging instruments for physical trade users.Palm Olein Futures (FPOL), a commodity futures contract, was reintroduced to the market on 16 June. It was originally launched by the Kuala Lumpur Commodity Exchange in 1990 but not

Derivatives

traded. Its reintroduction is timely as there is a larger base of commodity players to support the contract and the Malaysian palm oil industry has evolved and experienced rapid growth over the past 20 years. FPOL will serve the palm olein community’s hedging and price discovery needs as well as broaden trading and investment opportunities for investors in commodity futures. It also complements existing crude palm oil futures contract, which has established itself as the pricing benchmark for palm oil globally.

The 5-Year Malaysian Government Securities Futures(FMG5) contract specifications were revised to ensure that the contract continues to serve as a good proxy for market participants to hedge and trade their exposures more effectively.

The derivatives market is projected to have a CAGR of 23.3% over the next years with notional value traded to reach RM4.2 trillion (US$1.4 trillion)

31

by 2020. Following a strategic partnership of Bursa Malaysia with the CME Group Inc. (CME), the world’s largest derivatives exchange, and the migration to CME’s trading platform in 2010, the derivative trade values is expected to grow even more rapidly.

With the strategic alliance with CME Group, the product range in Bursa Malaysia is anticipated to expand to provide hedging

and arbitraging activities across market segments. Trading of derivative products on Bursa Malaysia comprising commodity, financial and equity futures is carried out via multiple access globally on CME Globex, the electronic trading platform of the CME Group, which operates four other exchanges namely CME, Chicago Board of Trade (CBOT), New York MercantileExchange(NYMEX)and Commodity Exchange, Inc.

(COMEX).TheUSCommodityFutures Trading Commission (CFTC) allows Malaysian brokers to solicit and accept orders and customers’ funds directly from US customers to trade on Bursa Malaysia without being registered as a futures commission merchant with the CFTC. Bursa Malaysia’s Kuala Lumpur Composite Index Futures Contracts (FKLI) are also allowed to be offered and sold in the US.

With the strategic alliance with CME Group, the product range in Bursa Malaysia is anticipated to expand to provide hedging and arbitraging activities across market segments. Trading of derivative products on Bursa Malaysia comprising commodity, financial and equity futures is carried out via multiple access globally on CME Globex, the electronic trading platform of the CME Group... .

32

Malaysia’s venture capital industry recorded a total committed funds under management at RM6.2 billion (US$1.7 billion) in 2014. Venture capital investments were mainly in sectors such as electricity and power generation, storage, financial services, IT as well as communications. The rapid growth was attributed to the country’s commitment to develop venture capital as a source of financing to emerging high-growth companies.

The government has provided significant funding and tax incentives to promote the industry. For example, qualifying venture capital companies investing in venture companies are given full tax exemption on all sources of income for up to 10 years of assessment. Active steps have also been taken to expand the participation of investment management firms in venture capital and private equity by giving them the flexibility to invest in (a) unlisted securities and (b) wholesale funds that invest venture capital funds.Other measures include allowing collective investment schemes like unit trust funds and closed end funds to invest up to 10% of their net asset value (NAV) in unlisted securities.

Venture Capital/Private Equity

The SC has revised the Guidelines on Registration of Venture Capital and Private Equity Corporations and Management Corporations was developed to replace the Guidelines for the Registration of Venture Capital Corporations and Management Corporations, for release in early 2015. Feedback from the Malaysian Venture Capital and Private Equity Association (MVCA) as well as practitioners and professionals within the venture capital and privateequity industries was taken into consideration in formulating the revised Guidelines to ensure a smooth implementation process.

The revised Guidelines aims to spur the further development of the venture capital and private equity industries and address the limitations of the previousguidelines. Revisions encompass the inclusion of private equity activities, giving further flexibility to registered venture capital corporations to invest in listed securities subject to a certain threshold and enhancing the current reporting requirements to allow for better data capture for developmental and future policy making purposes.

In addition, Bursa Malaysia also offers the ACE Market for companies to raise equity based capital without the usual requirement of a profit track record. The sponsor-driven ACE Market has proven to be an ideal platform to nurture high growth companies.

The SC’s equity fund-raising framework also allows for the listing of special purpose acquisition companies (SPAC), which provides another vehicle for capital-raising by venture capital companies and private equity firms.

In order to help the industry to achieve sufficient critical mass to generate self-sustaining growth momentum, national initiatives have been streamlined to ensure more co-ordinated and effective public sector funding of the venture capital industry. In tandem with this, greater public-private sector collaboration has been promoted in the critical areas, namely at the start-up stage or in nurturing patents towards the commercialisation stage. Initiatives such as angel networks will assist in seeding the formation of innovation based companies.

Our doors are open to venture capital companies to capitalise on all the facilitative measures put in place, and to leverage on the opportunities that ensue.

33

ISLAMICCAPITAL MARKET

Islamic Capital Market’s (ICM) development stems from its foundation of ethical principles and strong corporate governance. The underlying principles that govern ICM, among others are, mutual risk and profit sharing between parties, the assurance of fairness for all and that transactions are based on an underlying business activity or asset.

The ICM are where activities are carried out in ways which do not conflict with Islamic principles, i.e. free from prohibited activities and elements such as gharar (ambiguity), riba (usury) and maisir (gambling).

In the last decade, there has been strong global awareness and interest in Islamic finance, not only among Muslims, but a wide range of investors who perceive Islamic financing as a fairer way of doing business. As such there is a growing view that the very framework of ICM may be a strong viable alternative to conventional finance.

The prospects for the Islamic capital markets remain positive. According to an industry report1, the size of global Islamic finance assets is projected to surpass the US$2 trillion-mark by the end of 2014 and the industry is expected

to continue to chart positive growth across all sectors. Within the Islamic capital market segment, the global sukuk market is set to maintain its upward trajectory, spurred by a number of sovereign issuances expected to take place this year. In June 2014, the UK became the first western country to issue a sovereign sukuk. Hong Kong issued its sukuk of US$1 billion in September 2014, the administrative region’s first. Luxembourg followed suit with a AAA-rated government sukuk, €200 million, in October 2014.

1 Islamic Finance Outlook 2014, KFH Research Limited, January 2014.

34

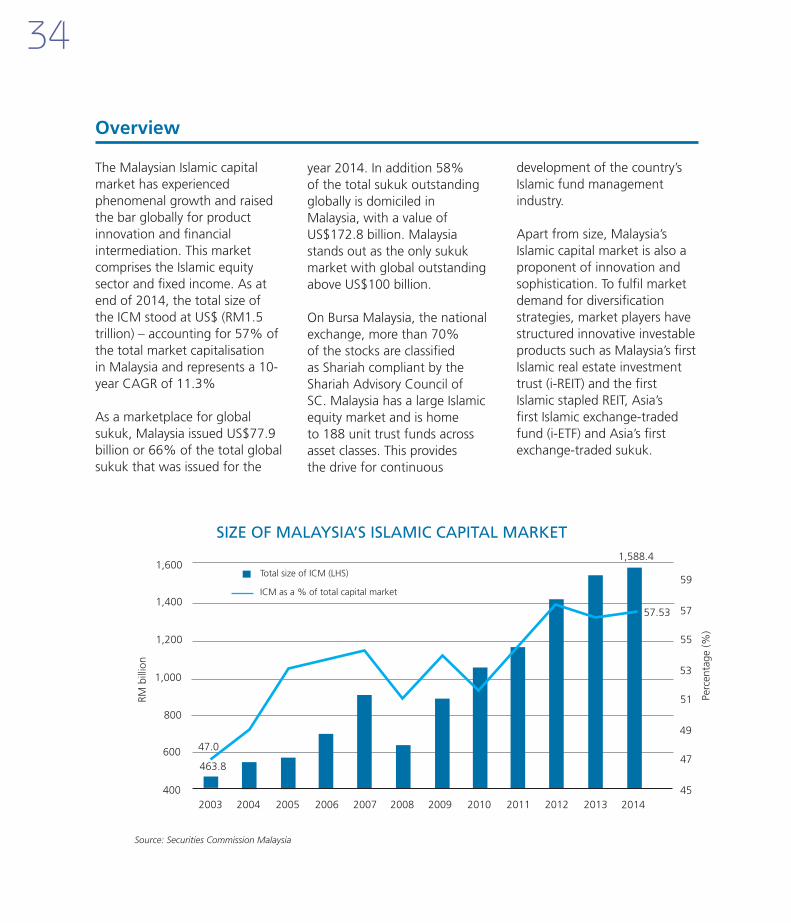

The Malaysian Islamic capital market has experienced phenomenal growth and raised the bar globally for product innovation and financial intermediation. This market comprises the Islamic equity sector and fixed income. As at end of 2014, the total size of the ICM stood at US$ (RM1.5 trillion) – accounting for 57% of the total market capitalisation in Malaysia and represents a 10-year CAGR of 11.3%

As a marketplace for global sukuk, Malaysia issued US$77.9 billion or 66% of the total global sukuk that was issued for the

year 2014. In addition 58% of the total sukuk outstanding globally is domiciled in Malaysia, with a value of US$172.8 billion. Malaysia stands out as the only sukuk market with global outstanding above US$100 billion.

On Bursa Malaysia, the national exchange, more than 70% of the stocks are classified as Shariah compliant by the Shariah Advisory Council of SC. Malaysia has a large Islamic equity market and is home to 188 unit trust funds across asset classes. This provides the drive for continuous

development of the country’s Islamic fund management industry.

Apart from size, Malaysia’s Islamic capital market is also a proponent of innovation and sophistication. To fulfil market demand for diversification strategies, market players have structured innovative investable products such as Malaysia’s first Islamic real estate investment trust (i-REIT) and the first Islamic stapled REIT, Asia’s first Islamic exchange-traded fund (i-ETF) and Asia’s first exchange-traded sukuk.

Overview

SIZE OF MALAYSIA’S ISLAMIC CAPITAL MARKET

1,600

1,400

1,200

1,000

800

600

4002003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Total size of ICM (LHS)

ICM as a % of total capital market59

57

55

53

51

49

47

45

47.0

463.8

Perc

enta

ge (%

)

RM b

illio

n

Source: Securities Commission Malaysia

1,588.4

57.53

2014

35

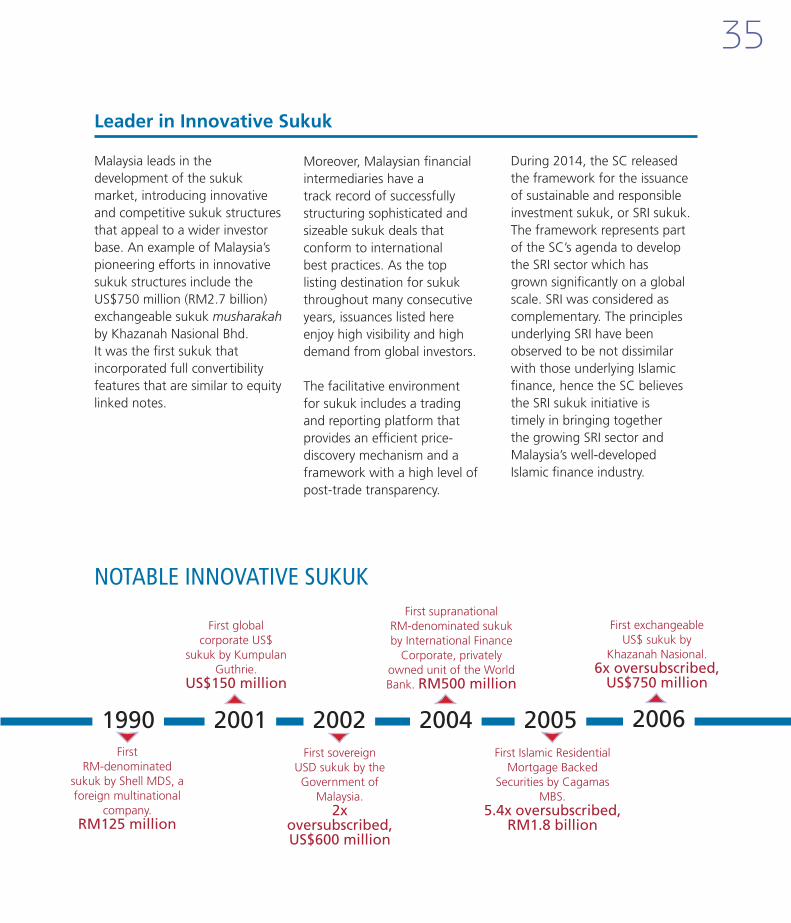

Malaysia leads in the development of the sukuk market, introducing innovative and competitive sukuk structures that appeal to a wider investor base. An example of Malaysia’s pioneering efforts in innovative sukuk structures include the US$750 million (RM2.7 billion) exchangeable sukuk musharakah by Khazanah Nasional Bhd. It was the first sukuk that incorporated full convertibility features that are similar to equity linked notes.

Moreover, Malaysian financial intermediaries have a track record of successfully structuring sophisticated and sizeable sukuk deals that conform to international best practices. As the top listing destination for sukuk throughout many consecutive years, issuances listed here enjoy high visibility and high demand from global investors.

The facilitative environment for sukuk includes a trading and reporting platform that provides an efficient price-discovery mechanism and a framework with a high level of post-trade transparency.

During 2014, the SC released the framework for the issuance of sustainable and responsible investment sukuk, or SRI sukuk. The framework represents part of the SC’s agenda to develop the SRI sector which has grown significantly on a global scale. SRI was considered as complementary. The principles underlying SRI have been observed to be not dissimilar with those underlying Islamic finance, hence the SC believes the SRI sukuk initiative is timely in bringing together the growing SRI sector and Malaysia’s well-developed Islamic finance industry.

Leader in Innovative Sukuk

NOTABLE INNOVATIVE SUKUK

1990First

RM-denominated sukuk by Shell MDS, a foreign multinational

company. RM125 million

2001

First global corporate US$

sukuk by Kumpulan Guthrie.

US$150 million

2002First sovereign

USD sukuk by the Government of

Malaysia. 2x

oversubscribed, US$600 million

2004

First supranational RM-denominated sukuk by International Finance

Corporate, privately owned unit of the World Bank. RM500 million

2005First Islamic Residential

Mortgage Backed Securities by Cagamas

MBS. 5.4x oversubscribed,

RM1.8 billion

2006

First exchangeable US$ sukuk by

Khazanah Nasional. 6x oversubscribed,

US$750 million

36

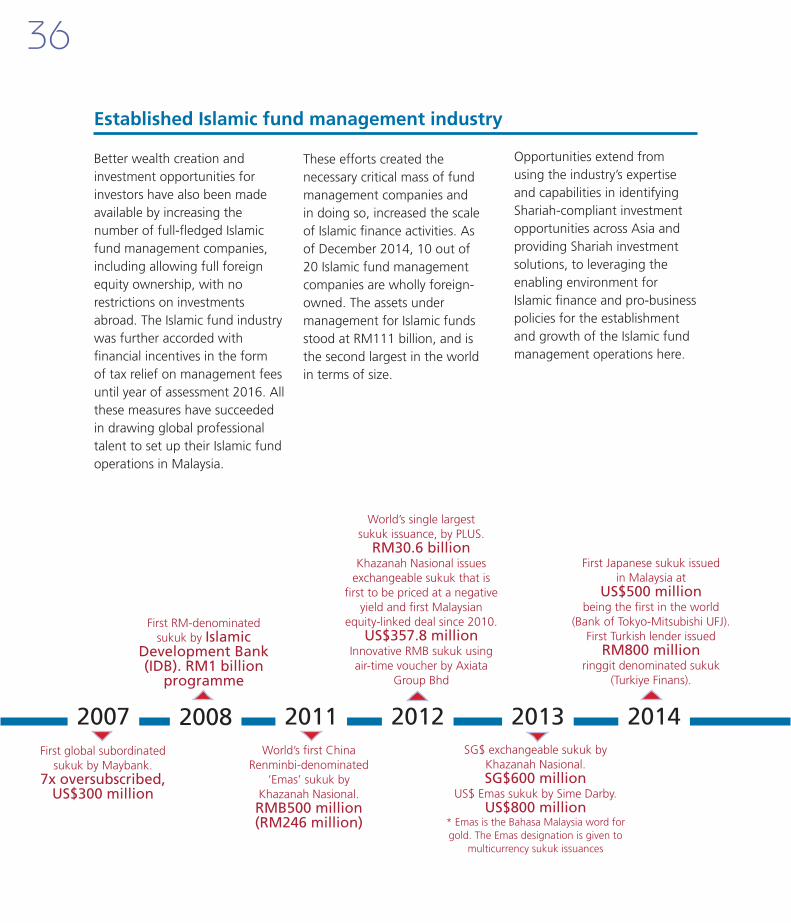

Better wealth creation and investment opportunities for investors have also been made available by increasing the number of full-fledged Islamic fund management companies, including allowing full foreign equity ownership, with no restrictions on investments abroad. The Islamic fund industry was further accorded with financial incentives in the form of tax relief on management fees until year of assessment 2016. All these measures have succeeded in drawing global professional talent to set up their Islamic fund operations in Malaysia.

These efforts created the necessary critical mass of fund management companies and in doing so, increased the scale of Islamic finance activities. As of December 2014, 10 out of 20 Islamic fund management companies are wholly foreign-owned. The assets under management for Islamic funds stood at RM111 billion, and is the second largest in the world in terms of size.

Established Islamic fund management industry

Opportunities extend from using the industry’s expertise and capabilities in identifying Shariah-compliant investment opportunities across Asia and providing Shariah investment solutions, to leveraging the enabling environment for Islamic finance and pro-business policies for the establishment and growth of the Islamic fund management operations here.

2007First global subordinated

sukuk by Maybank. 7x oversubscribed,

US$300 million

2008

First RM-denominated sukuk by Islamic

Development Bank (IDB). RM1 billion

programme

2011World’s first China

Renminbi-denominated ‘Emas’ sukuk by

Khazanah Nasional. RMB500 million (RM246 million)

2012

World’s single largest sukuk issuance, by PLUS.

RM30.6 billionKhazanah Nasional issues

exchangeable sukuk that is first to be priced at a negative

yield and first Malaysian equity-linked deal since 2010.

US$357.8 millionInnovative RMB sukuk using air-time voucher by Axiata

Group Bhd

2013SG$ exchangeable sukuk by

Khazanah Nasional. SG$600 million

US$ Emas sukuk by Sime Darby. US$800 million

* Emas is the Bahasa Malaysia word for gold. The Emas designation is given to

multicurrency sukuk issuances

2014

First Japanese sukuk issued in Malaysia at

US$500 millionbeing the first in the world

(Bank of Tokyo-Mitsubishi UFJ). First Turkish lender issued

RM800 millionringgit denominated sukuk

(Turkiye Finans).

37

The ASEAN Collective Investment Scheme (CIS) Framework became operational between Malaysia, Singapore and Thailand in 2014. This multilateral arrangement would also facilitate broader

distribution of Islamic funds across the member countries. Malaysia, having the largest Islamic unit trust fund market in ASEAN with total NAV of US$13 billion, can potentially

offer some of these funds in other member countries while fund managers in other countries can tap on the large investor base in Malaysia for Islamic fund products.

An ASEAN Market

The presence of large domestic intermediaries with regional footprint as well as numerous global intermediaries provides Malaysia with yet another competitive advantage. We also have investment banks and stockbroking companies licensed to carry out a broad spectrum

of capital market activities and a host of advisory companies licensed to carry out activities such as corporate finance, investment advisory, financial planning etc. Given the first mover advantage that our ICM has over markets in other countries, clearly the depth

of expertise including Islamic finance professionals in areas such as structuring, advisory, Shariah compliance, legal and accounting is also an important strength and reflects Malaysia’s growing significance as a centre of intermediation for the Islamic capital market.

Strong Intermediation Capabilities

In developing the Islamic capital market, a centralised Shariah governance framework was adopted as an effective mechanism to ensure adherence to, and the consistency of Shariah principles. In meeting

this need, the two-tier Shariah governance frameworks are implemented: the establishment of a Shariah Advisory Council for the capital market at the national level and the appointment of registered

Shariah advisers at the industry level. The governance framework promotes standardisation of Shariah practices within the industry and removes the possibilities of arbitrage and uncertainty within the system.

Shariah Governance

38

Investors in Malaysia’s ICM products are accorded the same legal and regulatory protection and recourse as conventional products. The Malaysian Government has ensured that disclosure, transparency and governance matters apply equally to both markets.These measures are anticipated to further enhance the vibrancy in Malaysia’s sukuk market which currently accounts for 58% of sukuk outstanding globally in 2014.

The SRI sukuk framework was thus launched on 28 August to facilitate the financing of sustainable and responsible investment initiatives. As the principles underlying SRI are similar to those underlying Islamic finance, the SRI sukuk initiative is timely as it bringstogether the growing SRI sector and Malaysia’s welldevelopedIslamic finance industry.The SRI sukuk framework capitalises on the existingsukuk framework set out in the Guidelines on Sukuk.

Additional requirements addressed in the frameworkfor the issuance of SRI sukuk include the utilisation ofproceeds, eligible SRI projects, disclosure requirements,appointment of independent party and reporting requirements. Eligible SRI projects as prescribed under the framework aim to preserve and protect the environment and natural resources, conserve use of energy, promote use of renewable energy, reduce greenhouse gas emission and improve the quality of life for society.

Facilitative Regulation

The ICM offers three main value propositions for investors. First are the greater diversification opportunities since the sector-profiles are typically different from conventional products. Second, it has enabled financial inclusion to those who have

been avoiding conventional investments due to ethical considerations. And third, in view of the growing affluence in Muslim-majority countries, ICM has created the opportunity for meeting this investment demand.

Malaysia’s ICM is thus able to offer a comprehensive infrastructure that supports competitiveness and innovation of product solutions and create a global marketplace conducive for capital market business and transactions.

Value Proposition

39

APPEN

DIX

Frequently Asked

Questions

Foreign ExchangeAdministration RulesApplicable to Issuers

Foreign ExchangeAdministration Rules

Applicable to Investors

Abbreviations/ Acronyms

40

Frequently Asked

Questions

How does Malaysia attract foreign investors to its local markets?Q:

We have embarked on extensive marketing efforts to attract foreign investors through roadshows, investment seminars and other speaking engagements. Our local markets benefit from a relatively strong primary demand for our capital markets products due to high domestic savings which we have successfully mobilised. We continue to create greater demand by developing the fund management business – including the private

pension fund industry and other investment conduits such as unit trusts and retail investment products.

Additionally, we ensure market dynamism by encouraging greater balance between long-term investors and short-term traders. All these will enhance Malaysia’s attractiveness to foreign investors.

Will Malaysia be fully liberalised?Q:

Foreign players can already have majority ownership in all segments of the Malaysian capital market and can buy over existing players. We do have an entry policy which is aimed at attracting

quality players who can contribute value add to the growth of the Malaysian capital market while managing prudential risks from competitive intensity.

41

How does Malaysia create new market opportunities?Q:

Malaysia is moving on several fronts to encourage quality foreign companies and products to list on our exchange, so that domestic investors can buy such products at their doorstep. We are also initiating more cross-border collaborative regulatory arrangements among ASEAN countries to create new market opportunities.

In line with the mutual recognition agreements that the SC has signed with the Dubai Financial Services Authority (DFSA) as well as the Hong

Kong Securities and Futures Commission (SFC), cross-border offerings of Malaysian funds can be made available in UAE and Hong Kong. Malaysia is also the first emerging country to obtain the Qualified Domestic International Investor (QDII) status in China. In addition, the introduction of the ASEAN Collective Investment Scheme (CIS) which allows fund managers the ability to market and distribute funds across member countries (Thailand, Malaysia and Singapore for now) is a cost efficient proposition that enables access to these lucrative high-growth markets.

Why would Malaysia be attractive to foreign shareholders?Q:

The Malaysian equity market is vibrant and offers unique value propositions and excellent investor protection. In addition, Bursa Malaysia is host to some of the world’s largest oil palm plantation companies and regional oil and gas sector

companies, which provides for capital flows into the commodity sector as well as ASEAN regional champions for banks and the GLCs. We are a good proxy to the ASEAN asset class growth.

42

Why is Malaysia moving from ‘Shariah-compliant’ to ‘Shariah-based’ approaches?Q:

The Shariah-compliant approach is premised largely on the adaptation of existing conventional products but with features prohibited under Shariah principles eliminated. The Shariah-based approach, on the other hand, looks into innovating new products that will finance real economic activities with a more direct risk-return trade-off model.

The shift from Shariah-compliant approach to Shariah-based approach will promote more product origination rather than product adaptation. This will in turn, strengthen the universality and acceptability of the Islamic capital market and giving it a distinctive value proposition, bringing along new opportunities and choices to investors and stakeholders alike.

How does Malaysia manage systemic risks in the capital market? Q:

As the regulator of the Malaysian capital market, the SC’s priority is to maintain market stability. The SC increasingly shares information and collaborate with other domestic and foreign market

supervisory authorities in managing systemic risks. The SC also has the powers to direct market intermediaries to take appropriate measures to monitor, mitigate or manage systemic risks.

43

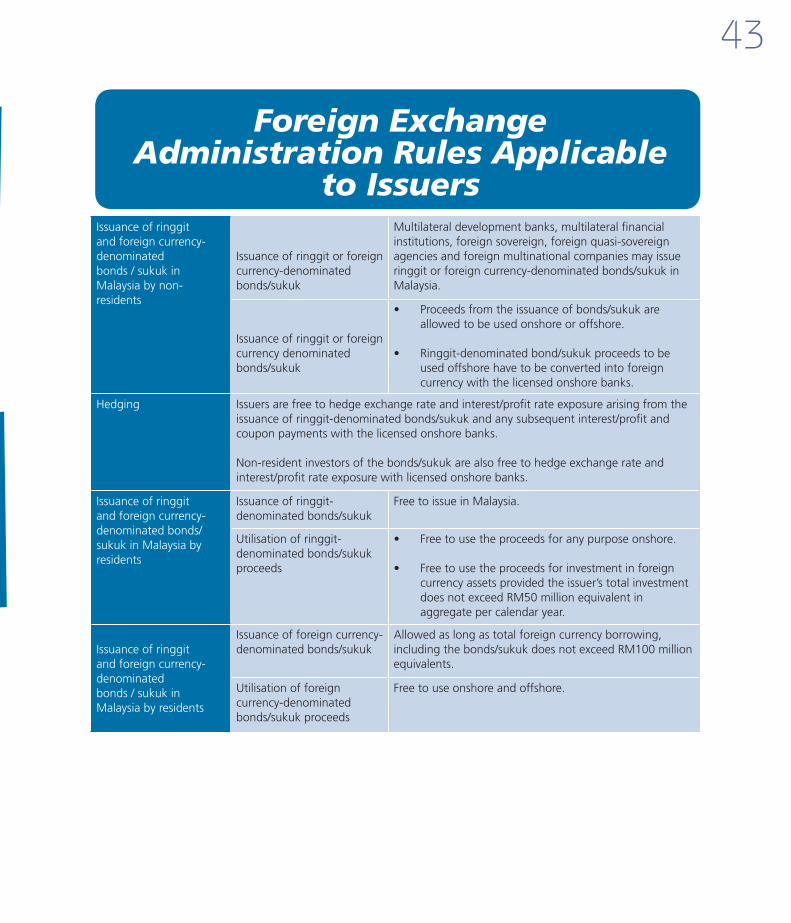

Foreign Exchange Administration Rules Applicable

to IssuersIssuance of ringgitand foreign currency-denominatedbonds / sukuk in Malaysia by non-residents

Issuance of ringgit or foreign currency-denominated bonds/sukuk

Multilateral development banks, multilateral financial institutions, foreign sovereign, foreign quasi-sovereign agencies and foreign multinational companies may issueringgit or foreign currency-denominated bonds/sukuk in Malaysia.

Issuance of ringgit or foreign currency denominated bonds/sukuk

• Proceedsfromtheissuanceofbonds/sukukareallowed to be used onshore or offshore.

• Ringgit-denominatedbond/sukukproceedstobeused offshore have to be converted into foreign currency with the licensed onshore banks.

Hedging Issuers are free to hedge exchange rate and interest/profit rate exposure arising from the issuance of ringgit-denominated bonds/sukuk and any subsequent interest/profit and coupon payments with the licensed onshore banks.

Non-resident investors of the bonds/sukuk are also free to hedge exchange rate and interest/profit rate exposure with licensed onshore banks.

Issuance of ringgit and foreign currency- denominated bonds/sukuk in Malaysia by residents

Issuance of ringgit- denominated bonds/sukuk

Free to issue in Malaysia.

Utilisation of ringgit- denominated bonds/sukuk proceeds

• Freetousetheproceedsforanypurposeonshore.

• Freetousetheproceedsforinvestmentinforeigncurrency assets provided the issuer’s total investment does not exceed RM50 million equivalent in aggregate per calendar year.

Issuance of ringgit and foreign currency- denominatedbonds / sukuk in Malaysia by residents

Issuance of foreign currency-denominated bonds/sukuk

Allowed as long as total foreign currency borrowing, including the bonds/sukuk does not exceed RM100 million equivalents.

Utilisation of foreigncurrency-denominatedbonds/sukuk proceeds

Free to use onshore and offshore.

44

Foreign Exchange Administration Rules Applicable

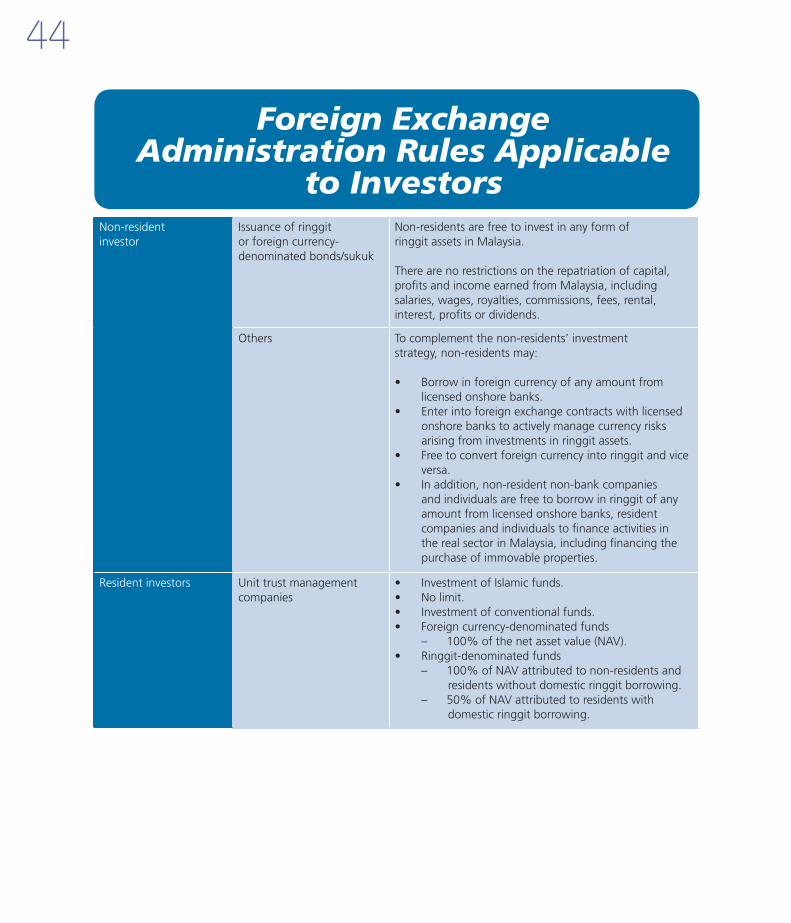

to InvestorsNon-residentinvestor

Issuance of ringgitor foreign currency-denominated bonds/sukuk

Non-residents are free to invest in any form ofringgit assets in Malaysia.

There are no restrictions on the repatriation of capital,profits and income earned from Malaysia, includingsalaries, wages, royalties, commissions, fees, rental,interest, profits or dividends.

Others To complement the non-residents’ investmentstrategy, non-residents may:

• Borrowinforeigncurrencyofanyamountfromlicensed onshore banks.

• Enterintoforeignexchangecontractswithlicensedonshore banks to actively manage currency risks arising from investments in ringgit assets.

• Freetoconvertforeigncurrencyintoringgitandviceversa.

• Inaddition,non-residentnon-bankcompaniesand individuals are free to borrow in ringgit of any amount from licensed onshore banks, resident companies and individuals to finance activities in the real sector in Malaysia, including financing the purchase of immovable properties.

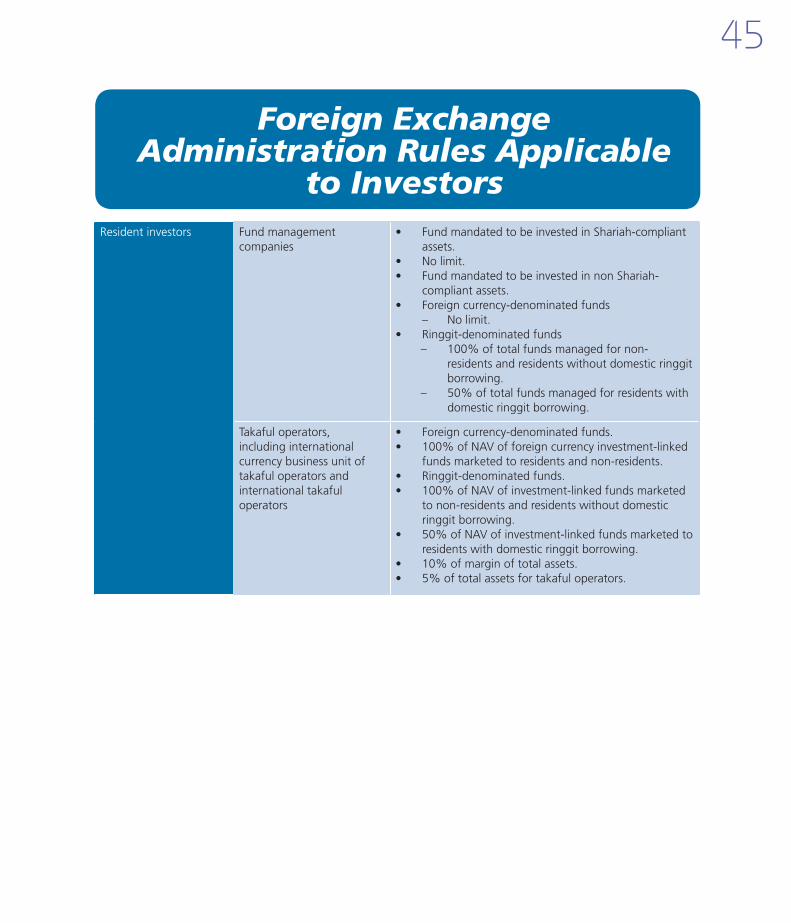

Resident investors Unit trust managementcompanies

• InvestmentofIslamicfunds.• Nolimit.• Investmentofconventionalfunds.• Foreigncurrency-denominatedfunds – 100% of the net asset value (NAV).• Ringgit-denominatedfunds

– 100% of NAV attributed to non-residents and residents without domestic ringgit borrowing.

– 50% of NAV attributed to residents with domestic ringgit borrowing.

45

Resident investors Fund managementcompanies

• FundmandatedtobeinvestedinShariah-compliantassets.

• Nolimit.• FundmandatedtobeinvestedinnonShariah-

compliant assets.• Foreigncurrency-denominatedfunds – No limit.• Ringgit-denominatedfunds

– 100% of total funds managed for non-residents and residents without domestic ringgit borrowing.

– 50% of total funds managed for residents with domestic ringgit borrowing.

Takaful operators,including internationalcurrency business unit of takaful operators andinternational takaful operators

• Foreigncurrency-denominatedfunds.• 100%ofNAVofforeigncurrencyinvestment-linked

funds marketed to residents and non-residents.• Ringgit-denominatedfunds.• 100%ofNAVofinvestment-linkedfundsmarketed

to non-residents and residents without domestic ringgit borrowing.

• 50%ofNAVofinvestment-linkedfundsmarketedtoresidents with domestic ringgit borrowing.

• 10%ofmarginoftotalassets.• 5%oftotalassetsfortakafuloperators.

Foreign Exchange Administration Rules Applicable

to Investors

46

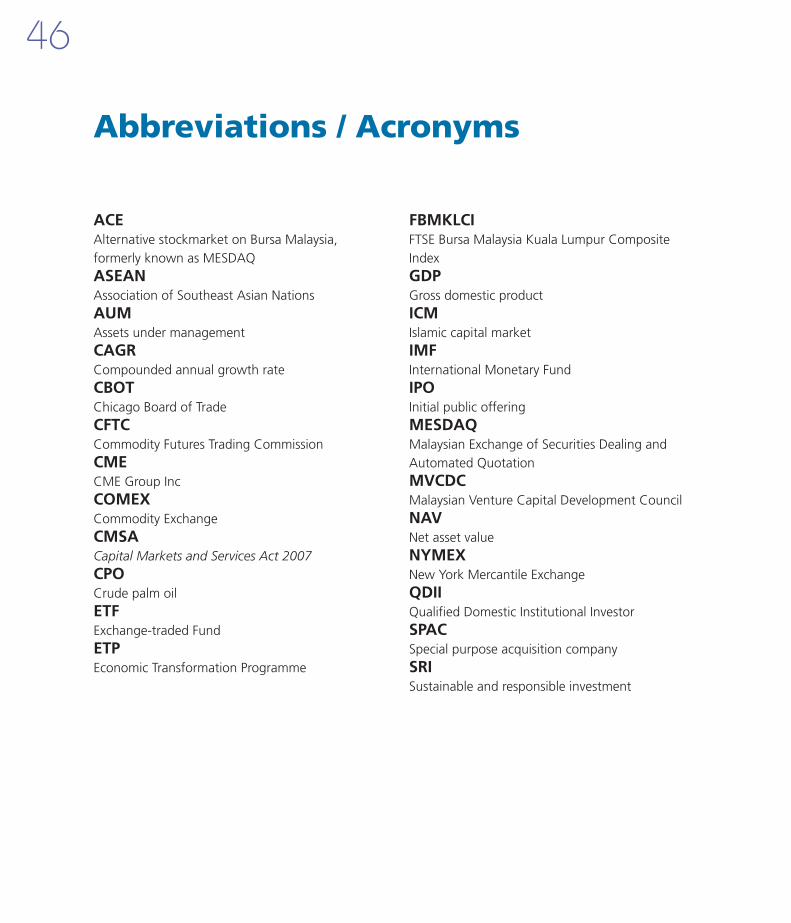

ACE Alternative stockmarket on Bursa Malaysia, formerly known as MESDAQ ASEAN Association of Southeast Asian NationsAUM Assets under management CAGR Compounded annual growth rateCBOT Chicago Board of TradeCFTC Commodity Futures Trading Commission CME CME Group IncCOMEX Commodity ExchangeCMSA Capital Markets and Services Act 2007 CPO Crude palm oil ETF Exchange-traded Fund ETP Economic Transformation Programme

Abbreviations / Acronyms

FBMKLCI FTSE Bursa Malaysia Kuala Lumpur Composite Index GDP Gross domestic product ICM Islamic capital market IMF International Monetary Fund IPO Initial public offering MESDAQ Malaysian Exchange of Securities Dealing and Automated QuotationMVCDC Malaysian Venture Capital Development CouncilNAV Net asset valueNYMEX New York Mercantile ExchangeQDIIQualified Domestic Institutional InvestorSPAC Special purpose acquisition companySRI Sustainable and responsible investment

47

NOTES

48

NOTES