Embed Size (px)

Citation preview

Capital management enhances shareholder value

Our unique value proposition• Integrated

The building blocks for collaboration

• Segment focus“Chunking”

• Business philosophyInnovation

Entrepreneurial

• Federal structureRun by owner-managers

Lots of little growth stories

Integrated

• Provides building blocks

• Leverages intellectual capital, client base,

brand, infrastructure, and balance sheet

• Facilitates collaboration

• Capital

Mobility of capital

Leverage benefit

Skills – actuarial & banking

Consistent growth strategy

Organic Collaboration Acquisitions Greenfields Capital management

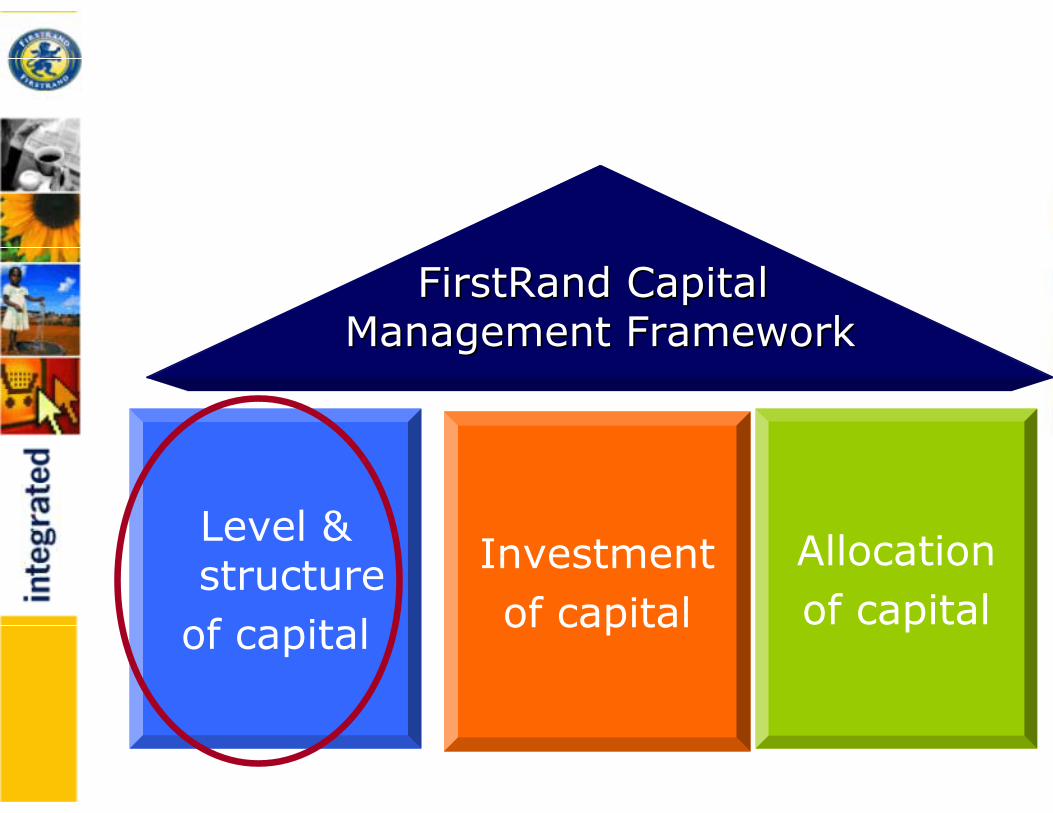

Level & structure

of capital

Investmentof capital

FirstRand Capital FirstRand Capital Management FrameworkManagement Framework

Allocation of capital

What is the optimal level of capital in the Bank?

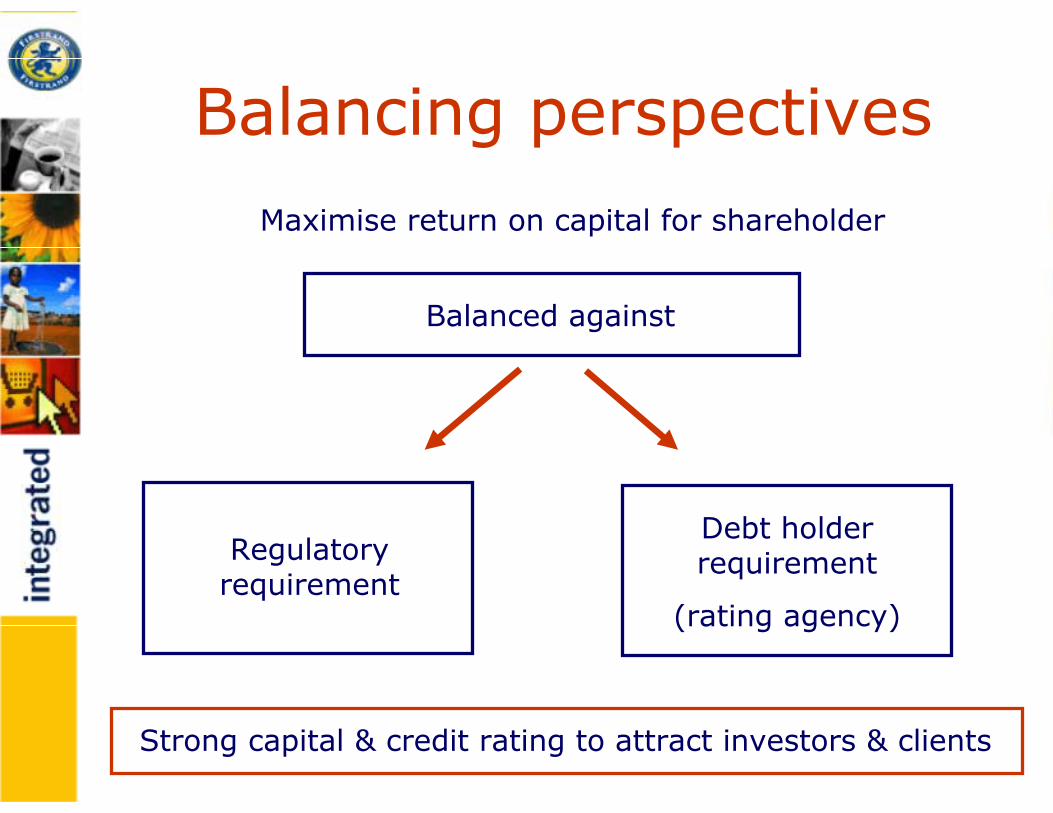

Balancing perspectivesMaximise return on capital for shareholder

Strong capital & credit rating to attract investors & clients

Balanced against

Regulatory requirement

Debt holder requirement

(rating agency)

Sound principles

• Maintain highest level of regulatory or

economic capital

• Maintain target counterparty credit rating

• Building blocks for buffer

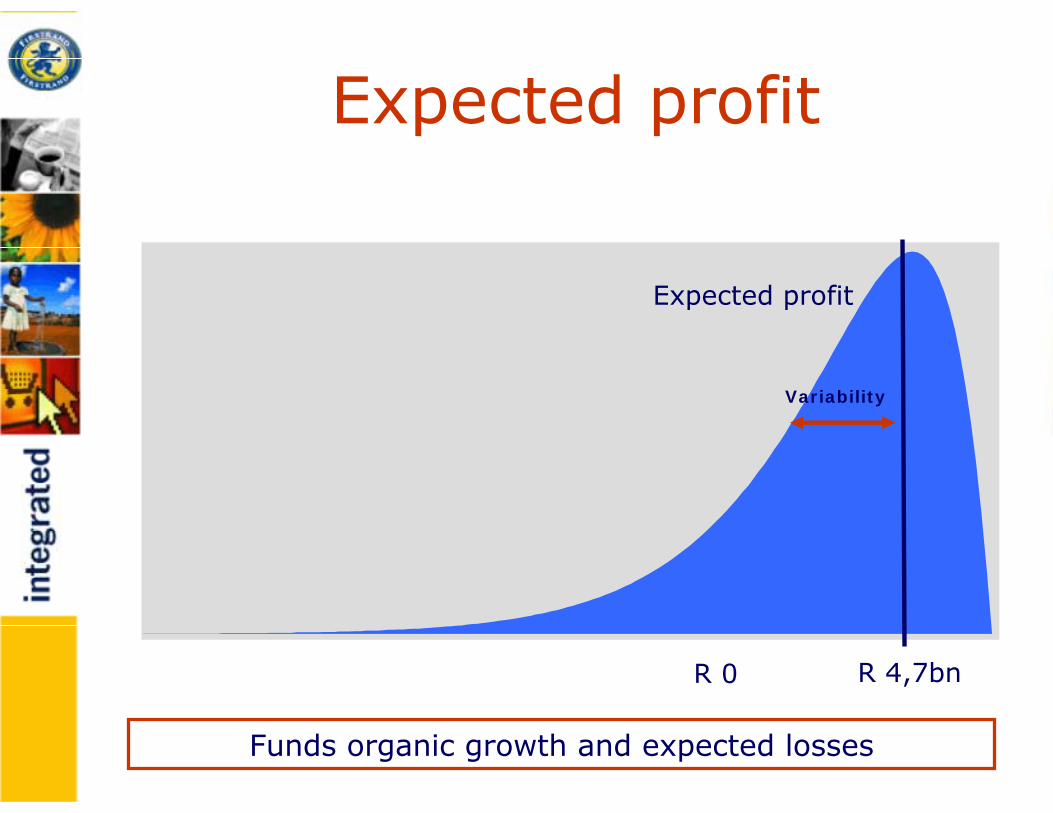

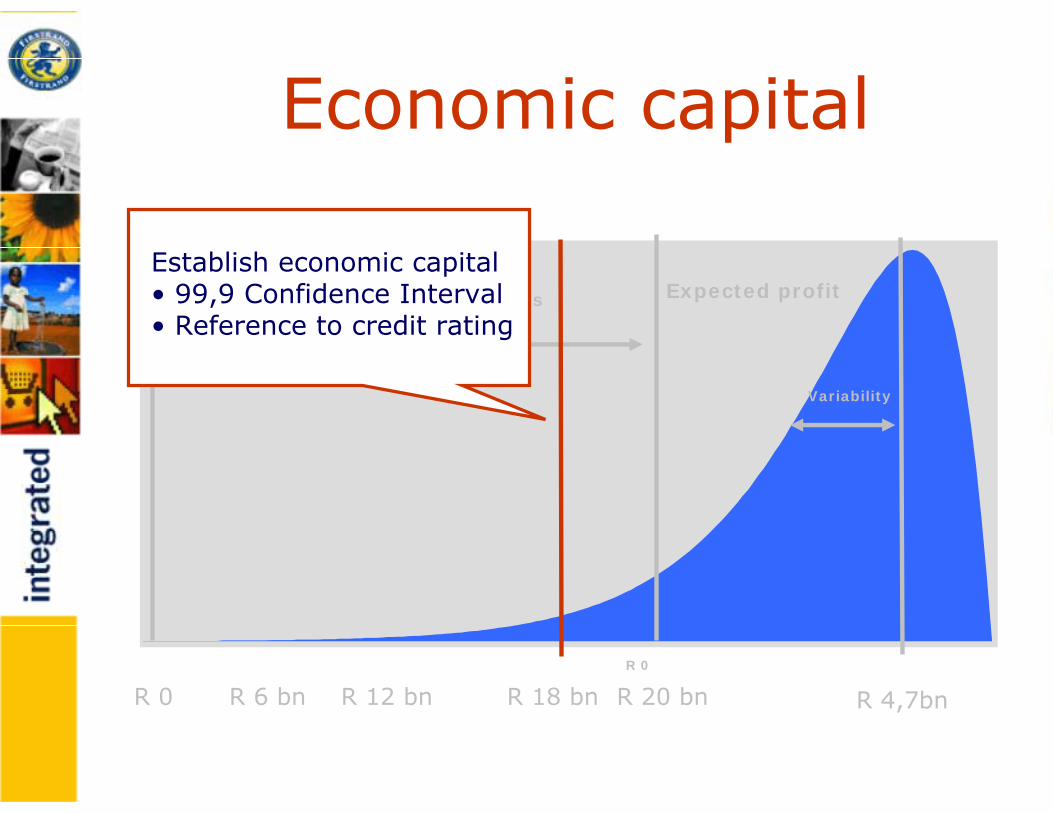

Expected profit

Economic capital

Economic cycles

Risk concentration

Expected profit

R 4,7bnR 0

Expected profit

Variability

Funds organic growth and expected losses

Economic capital

R 4,7bn

R 0

Expected profit

Variability

R 20 bnR 0 R 18 bnR 12 bnR 6 bn

Capital = unexpected losses

Establish economic capital• 99,9 Confidence Interval• Reference to credit rating

Building protection

R 4,7bnR 0

Expected profit

Variability

R 20 bnR 0 R 18 bnR 12 bnR 6 bn

Capital = unexpected losses

Establish buffer over regulatory capital

• Protect against business disruptions

• Volatility of earnings

• AC 133

• Internal capital generation for growth

• Economic downturns

• Interest rate shocks

• Exchange rate volatility

• Risk concentrations

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

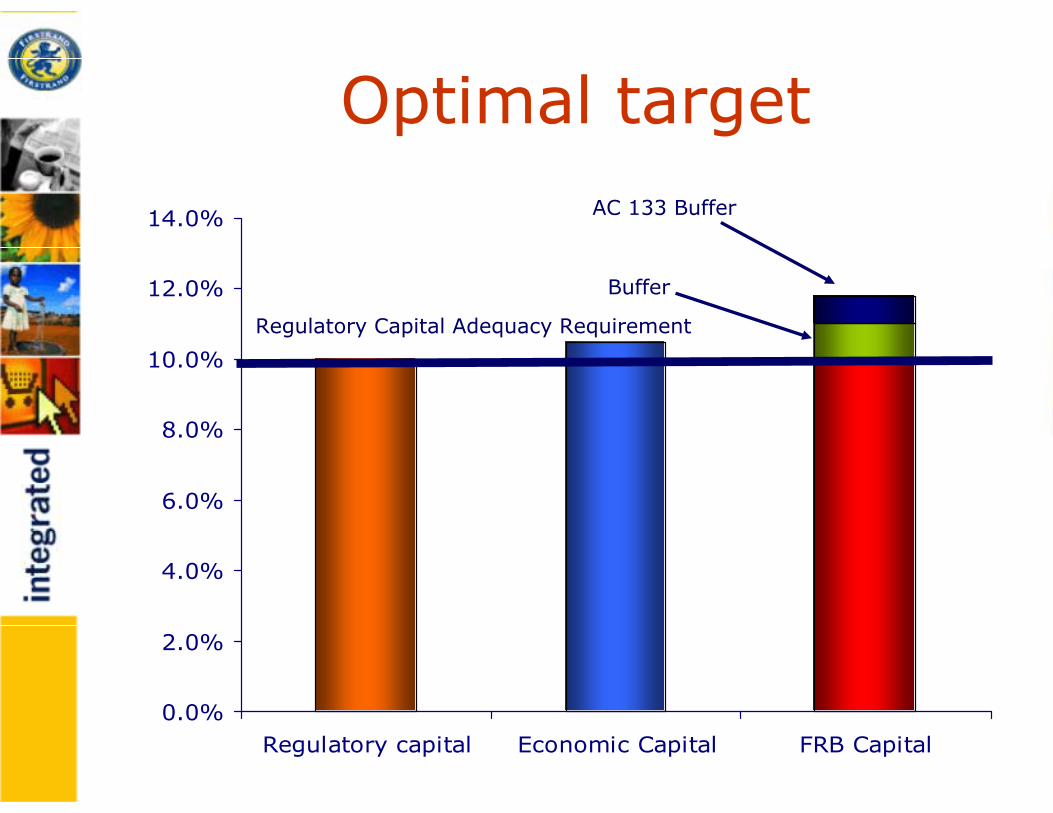

Regulatory capital Economic Capital FRB Capital

Regulatory Capital Adequacy Requirement

Buffer

AC 133 Buffer

Optimal target

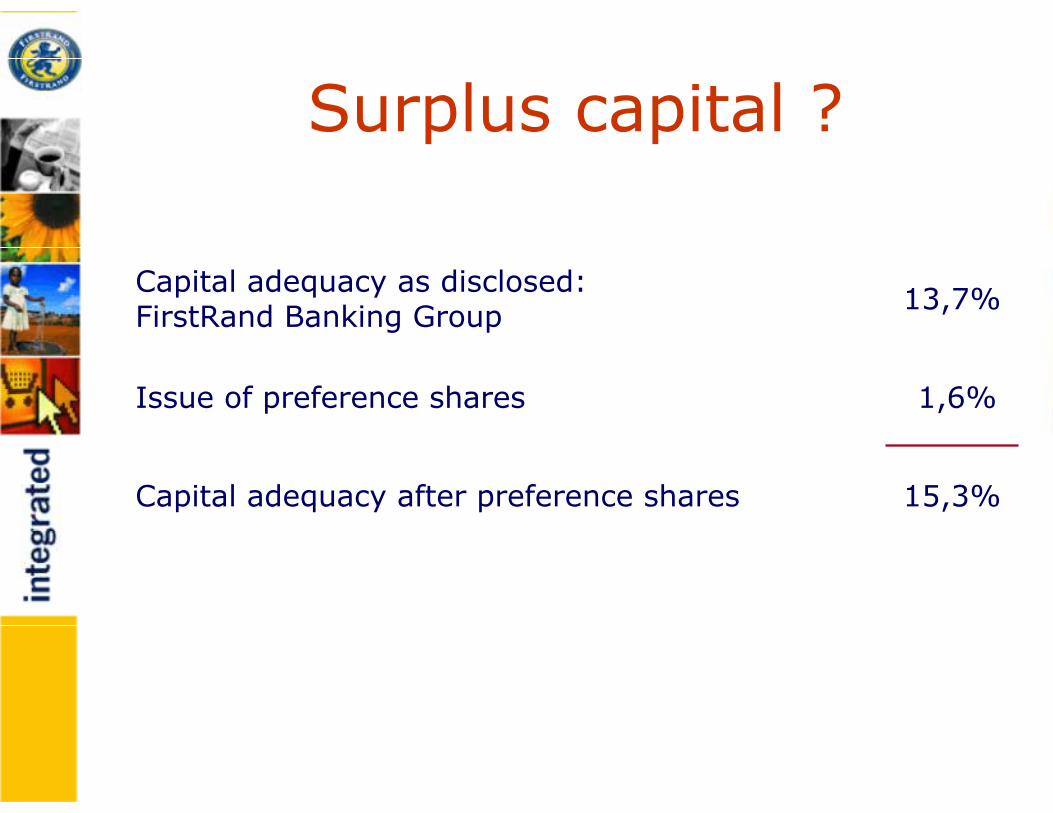

Surplus capital ?

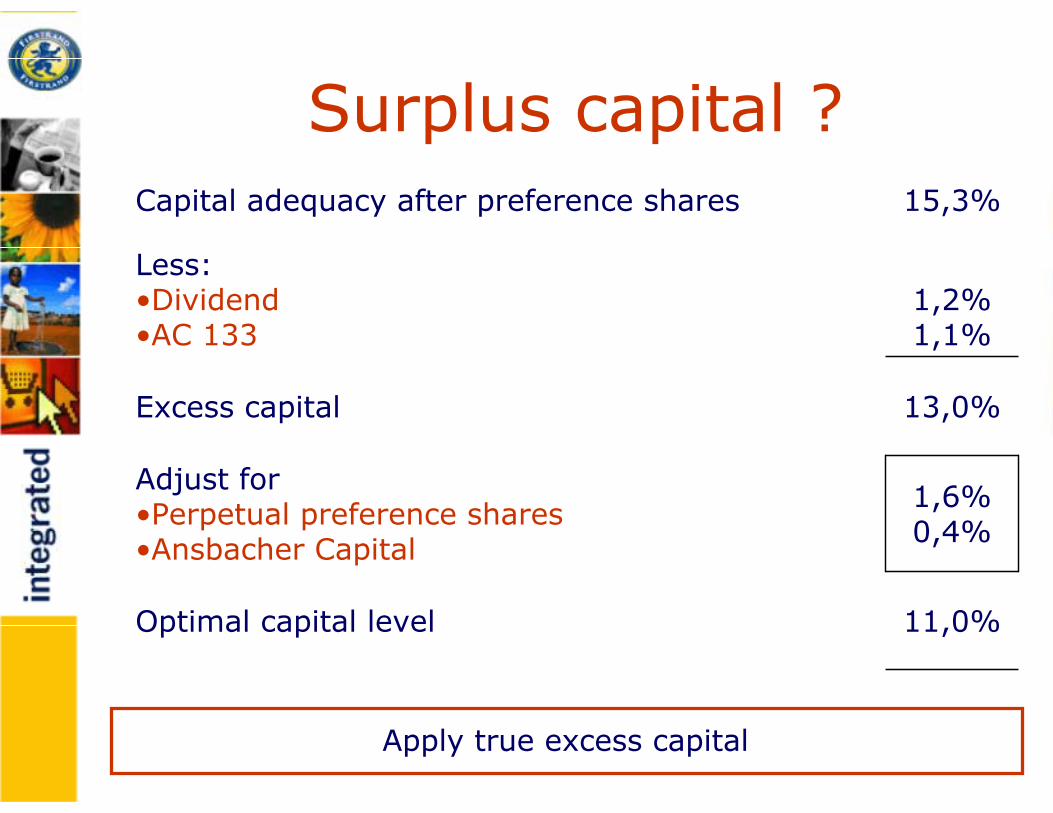

15,3%Capital adequacy after preference shares

1,6%Issue of preference shares

13,7%Capital adequacy as disclosed: FirstRand Banking Group

Surplus capital ?

11,0%Optimal capital level

1,6%0,4%

Adjust for•Perpetual preference shares•Ansbacher Capital

13,0%Excess capital

1,2%1,1%

Less:•Dividend•AC 133

15,3%Capital adequacy after preference shares

Apply true excess capital

What is the optimal capital structure for the Bank?

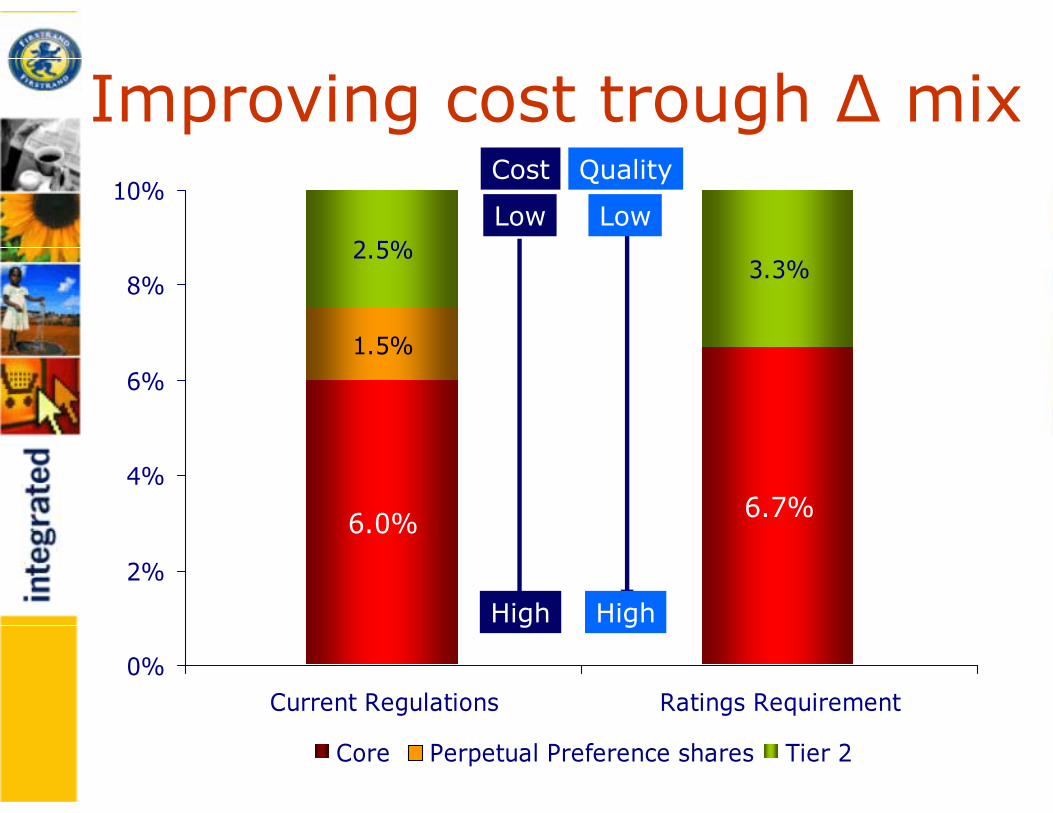

6.7%

3.3%

6.0%

1.5%

2.5%

0%

2%

4%

6%

8%

10%

Current Regulations Ratings Requirement

Core Perpetual Preference shares Tier 2

Improving cost trough ∆ mixQuality

Low

High

Cost

Low

High

• Rank capital instruments in order of cost

i.e. equity vs. subordinated term paper

• Issue capital instruments in order

• Capacity for the lowest cost

Improving cost through ∆ mix

FirstRand raises these instruments on a regular basis

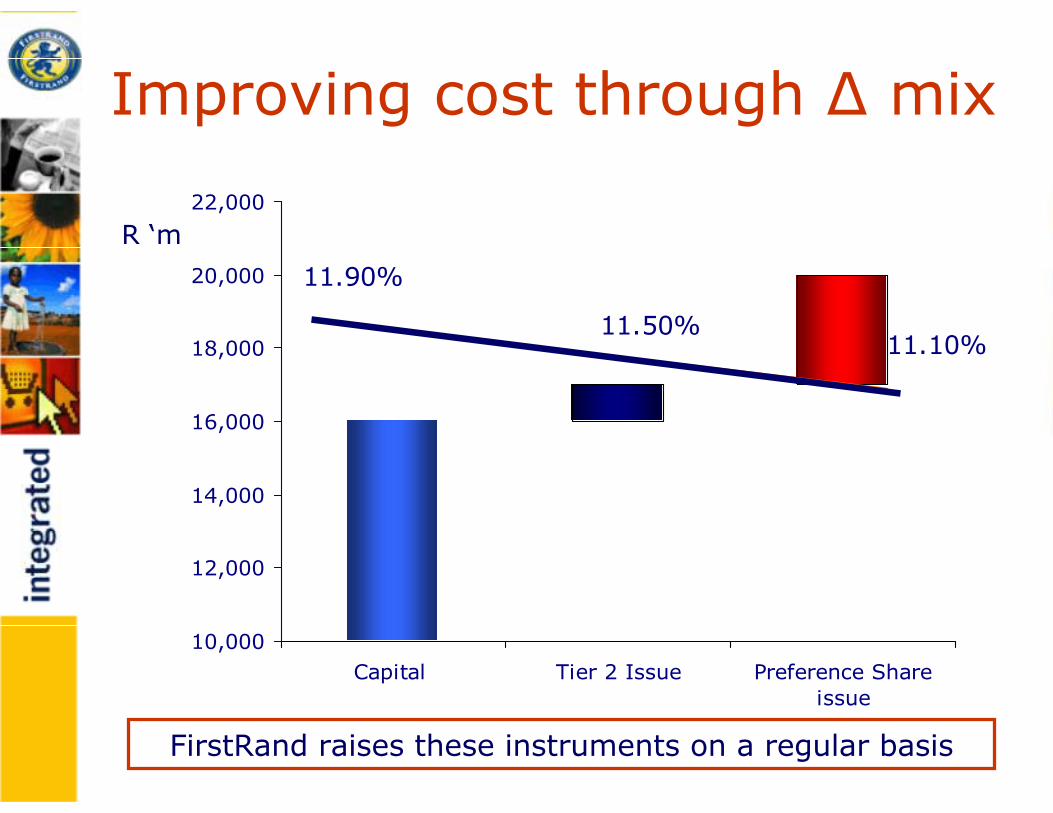

10,000

12,000

14,000

16,000

18,000

20,000

22,000

Capital Tier 2 Issue Preference Shareissue

11.10%

11.90%

11.50%

R ‘m

Improving cost through ∆ mix

FirstRand raises these instruments on a regular basis

What is the optimal level of capital for Momentum?

Balancing perspectivesMaximise return on capital for shareholder

Balanced against

Regulatory requirement

Policy holder requirement

0.50

1.00

1.50

2.00

2.50

Regulatory capital

Regulatory capital

Regulatory capital (1x)

• Do not cover credit risk

Tim

es

0.50

1.00

1.50

2.00

2.50

Regulatory capital

Informal regulatory capital

Informal regulatory capital (1,5x)

• Only 95% Confidence Interval

Tim

es

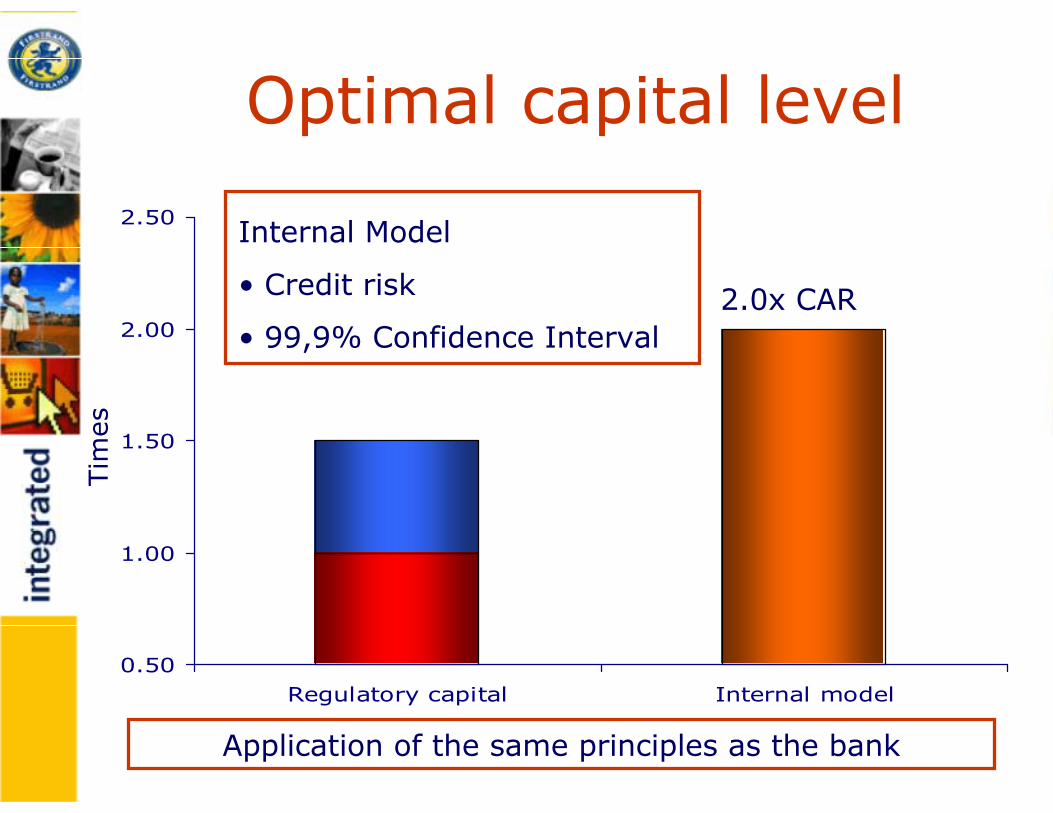

0.50

1.00

1.50

2.00

2.50

Regulatory capital Internal model

Optimal capital level

Internal Model

• Credit risk

• 99,9% Confidence Interval

Tim

es

2.0x CAR

Application of the same principles as the bank

Investmentof capital

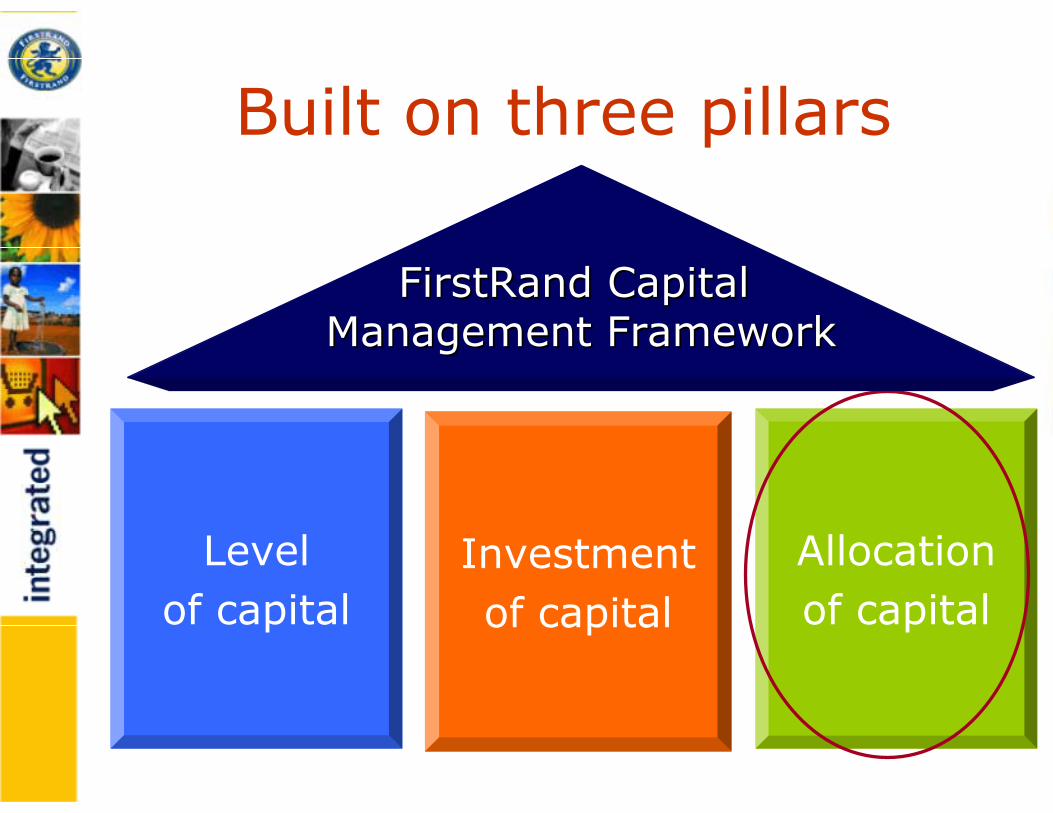

Built on three pillars

Level of capital

FirstRand Capital FirstRand Capital Management FrameworkManagement Framework

Allocation of capital

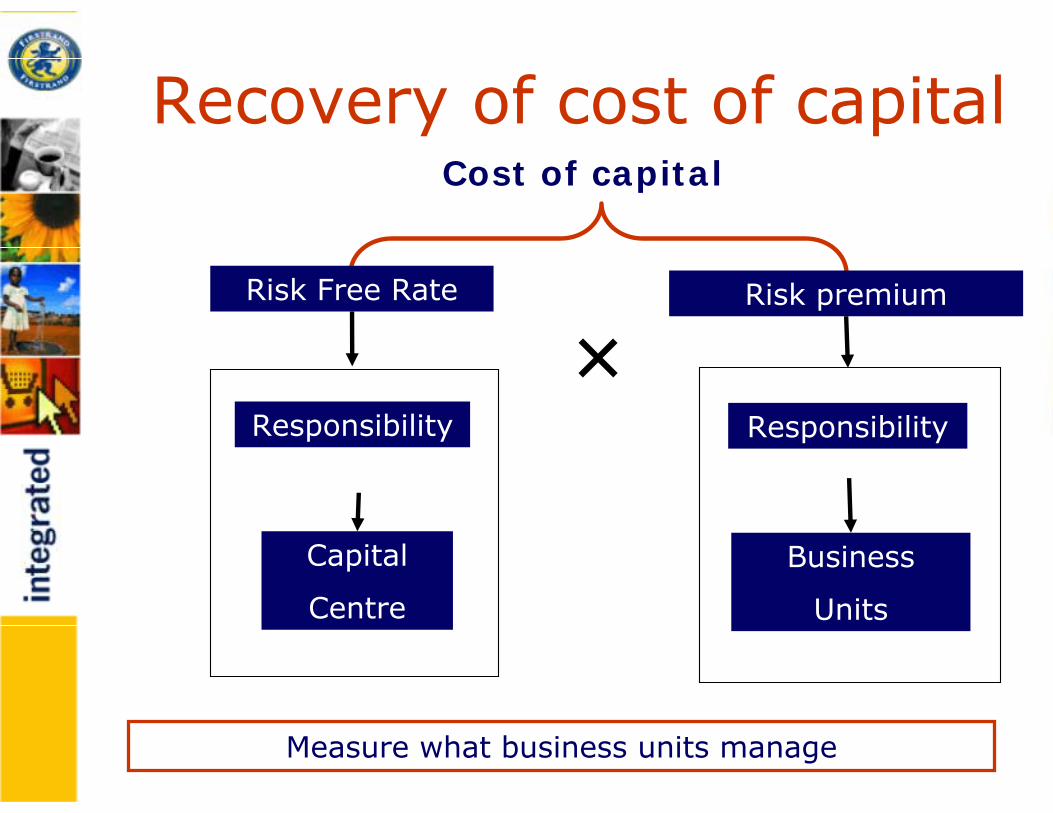

Recovery of cost of capitalCost of capital

Risk premiumRisk Free Rate

Capital

Centre

Business

Units

×Responsibility Responsibility

Measure what business units manage

How do we invest the

capital in the bank?

Recovery of risk free rate• Managed by Banking Group Treasury

• Invest in underlying currency

• No interest rate risk on issue of capital debt

instruments

• Cost is credit spread

• Invest along the yield curve to:

• Maximise and optimise the return

• Reduce volatility in the income statement

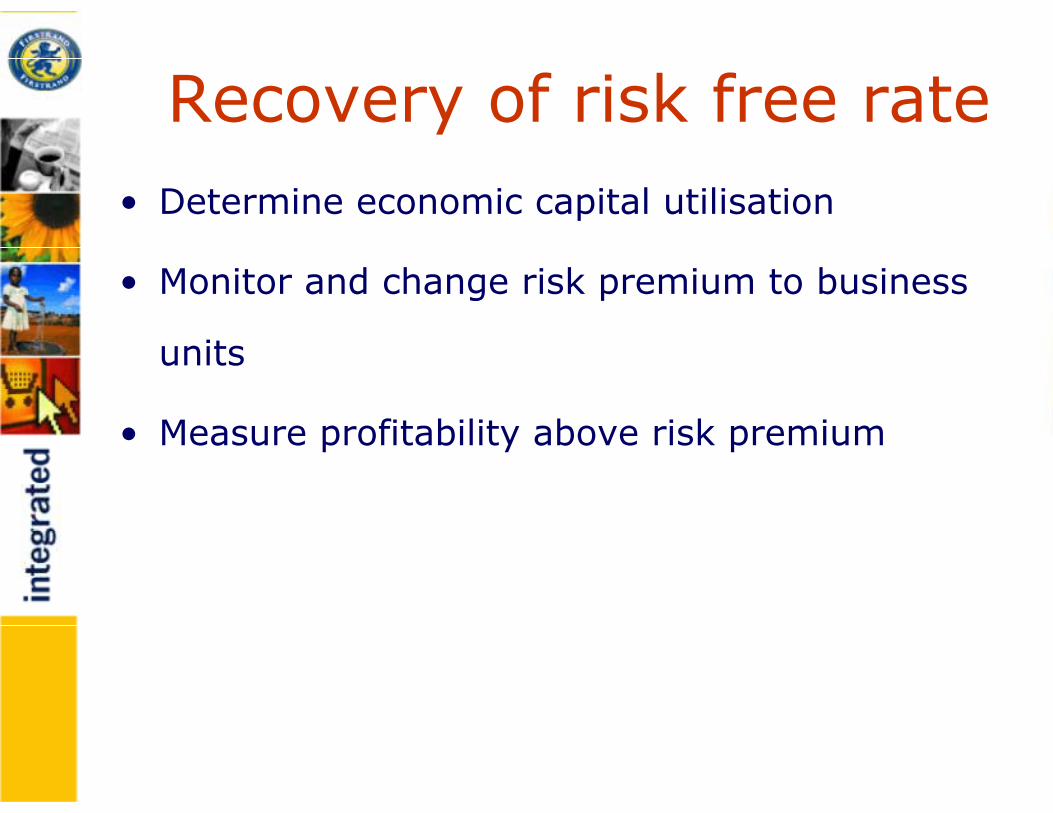

Recovery of risk free rate• Determine economic capital utilisation

• Monitor and change risk premium to business

units

• Measure profitability above risk premium

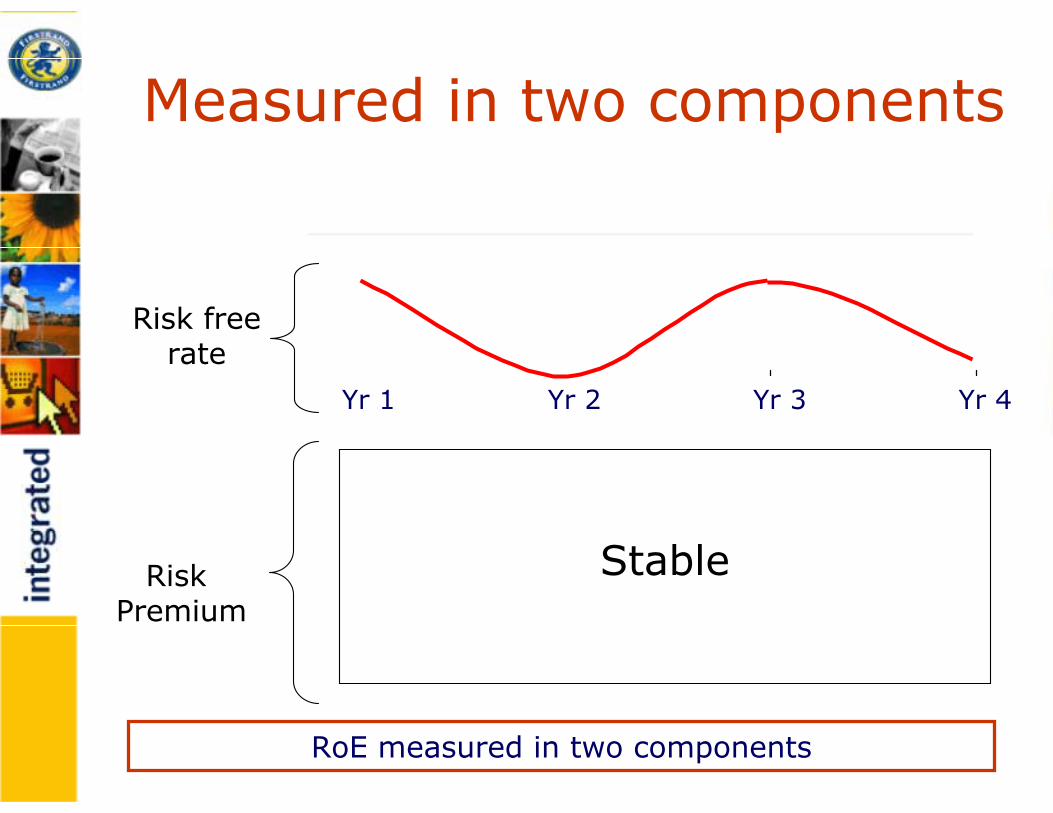

Measured in two components

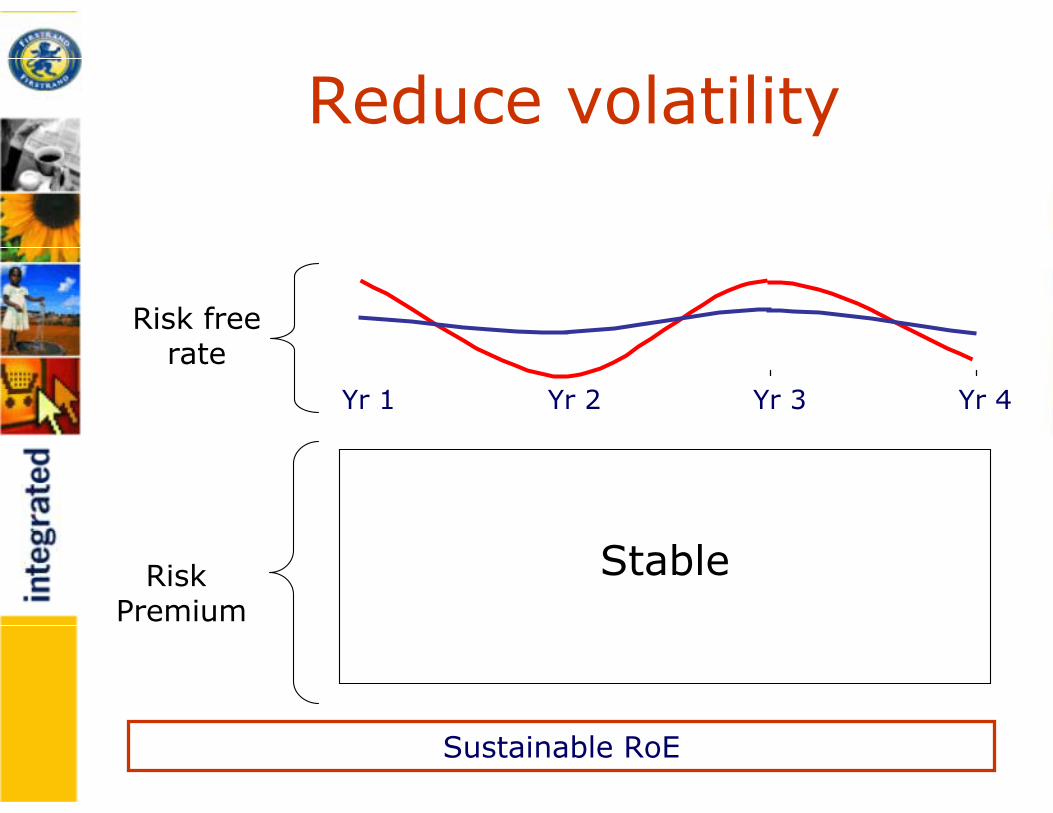

Yr 1 Yr 2 Yr 3 Yr 4

StableRisk Premium

Risk freerate

RoE measured in two components

Reduce volatility

Yr 1 Yr 2 Yr 3 Yr 4

Risk freerate

Sustainable RoE

StableRisk Premium

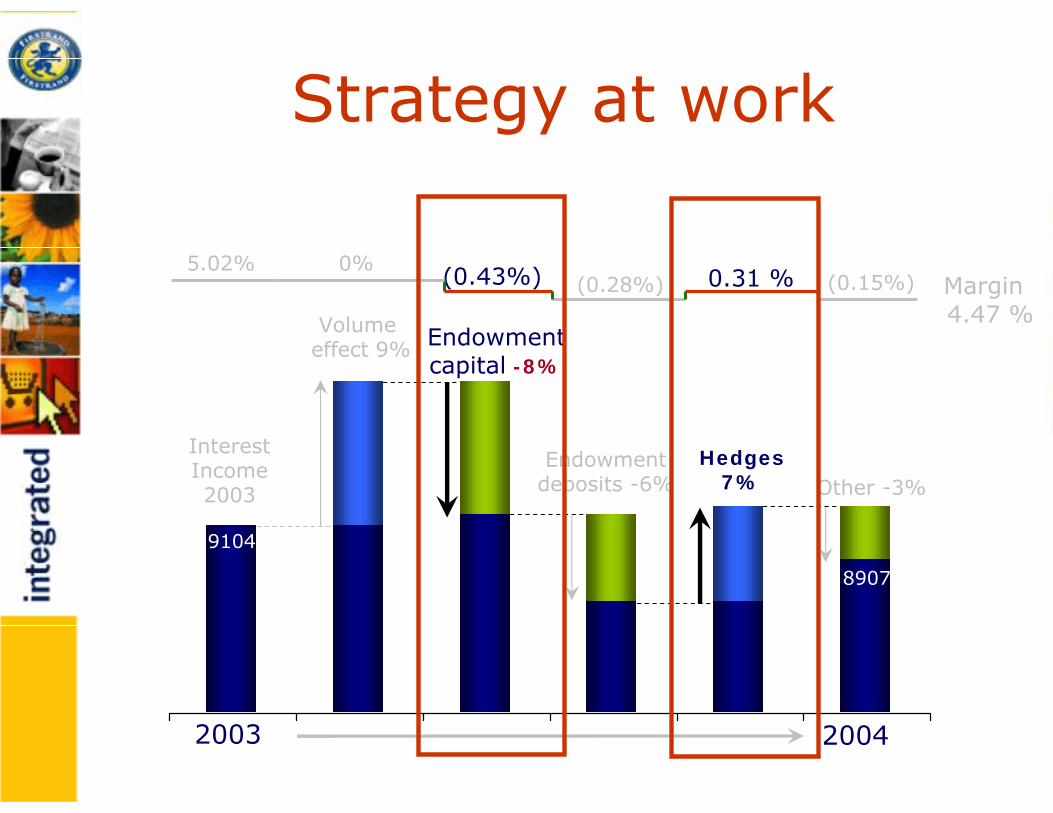

Strategy at work

2003 2004

Interest Income2003

Volumeeffect 9% Endowment

capital -8%

Endowmentdeposits -6%

5.02% 0%(0.43%) (0.28%)

4.47 %Margin

Hedges 7%

0.31 % (0.15%)

Other -3%

9104

8907

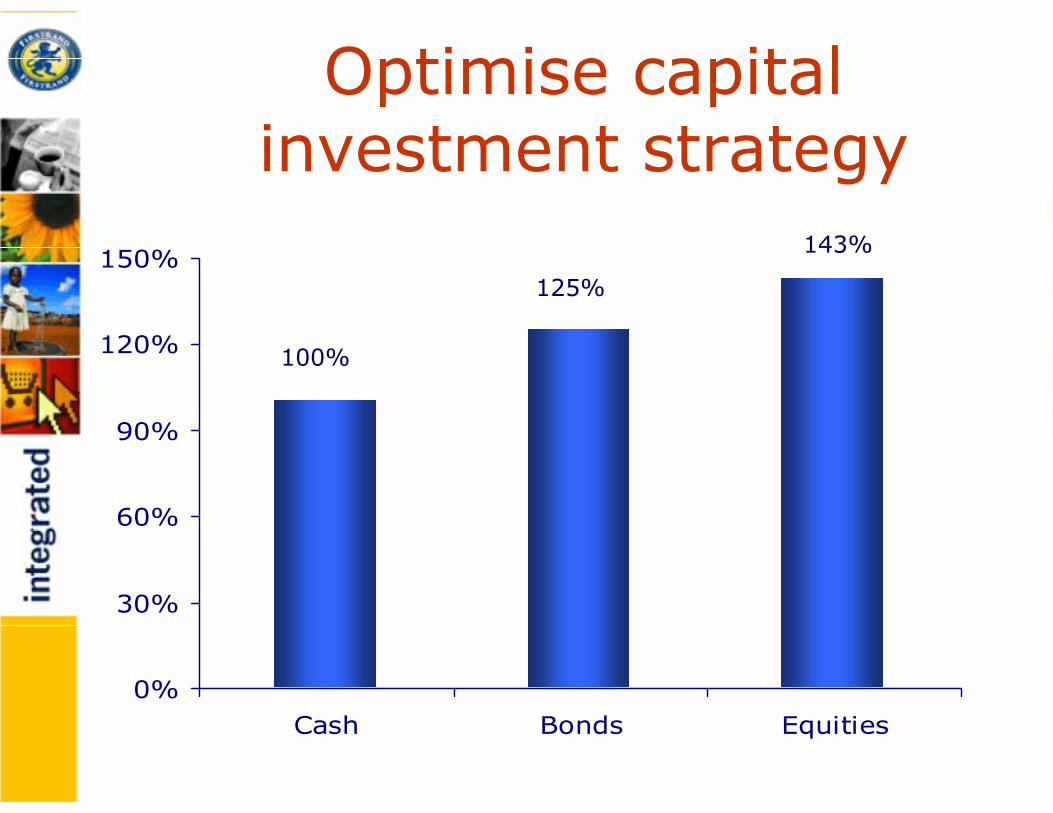

How does investment strategy affect level of capital in

Momentum?

Optimise capital investment strategy

0%

30%

60%

90%

120%

150%

Cash Bonds Equities

100%

125%

143%

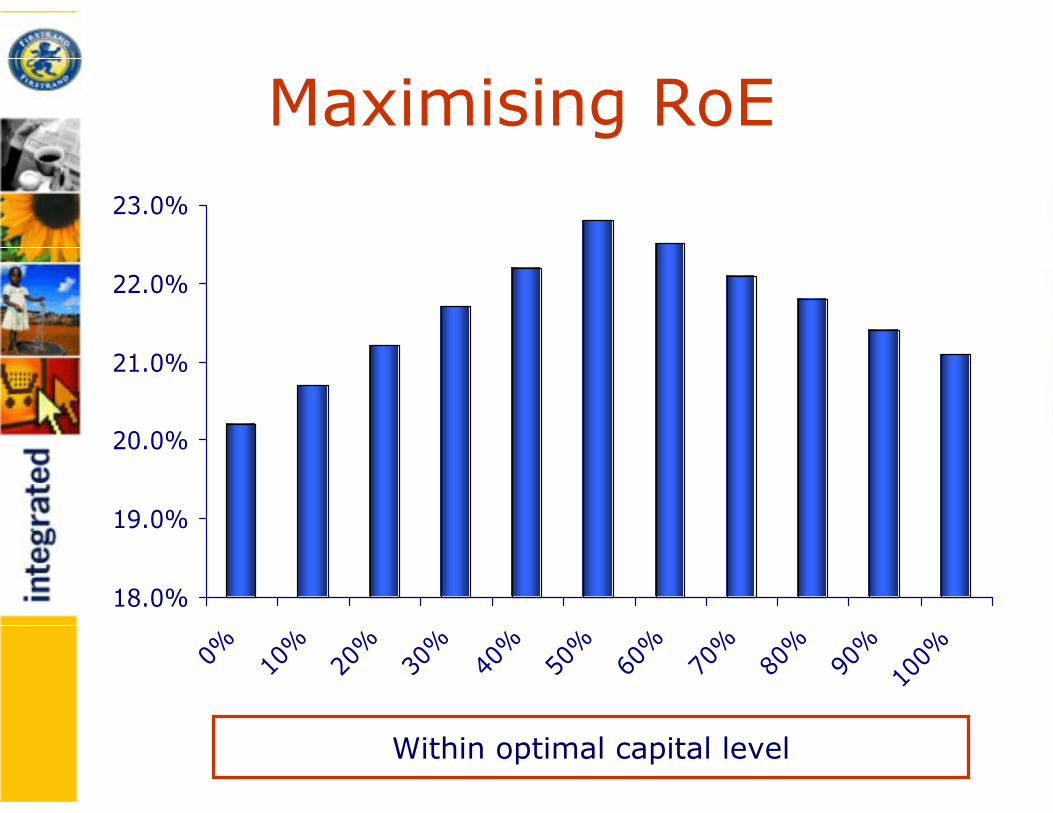

Maximising RoE

Within optimal capital level

18.0%

19.0%

20.0%

21.0%

22.0%

23.0%

0% 10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Integrated investment approach

• Cash & near cash

Managed by FirstRand Bank (Banking

Group Treasury)

• Actively managed equities

RMB Asset Management

Allocation of capital

Built on three pillars

Level of capital

Investmentof capital

FirstRand Capital FirstRand Capital Management FrameworkManagement Framework

Recovery of cost of capitalCost of capital

Risk premiumRisk Free Rate

Capital

Centre

Business

Units

×Responsibility Responsibility

Measure what business units manage

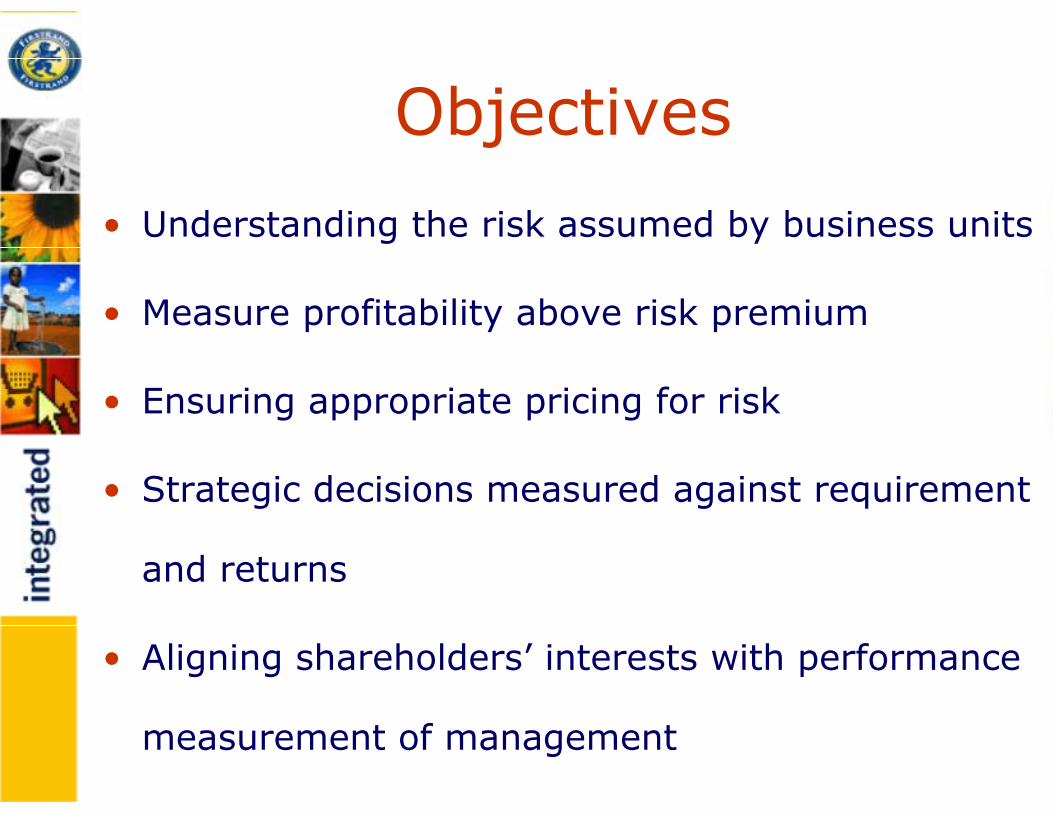

Objectives

• Understanding the risk assumed by business units

• Measure profitability above risk premium

• Ensuring appropriate pricing for risk

• Strategic decisions measured against requirement

and returns

• Aligning shareholders’ interests with performance

measurement of management

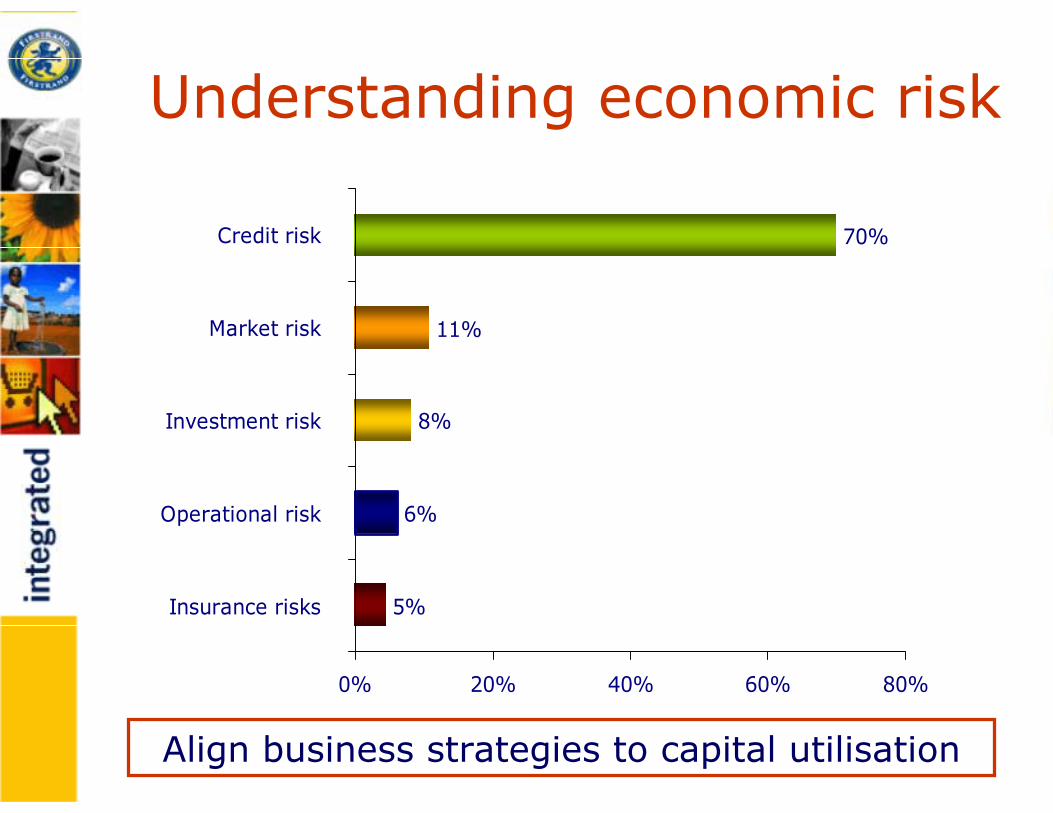

5%

6%

8%

11%

70%

0% 20% 40% 60% 80%

Insurance risks

Operational risk

Investment risk

Market risk

Credit risk

Understanding economic risk

Align business strategies to capital utilisation

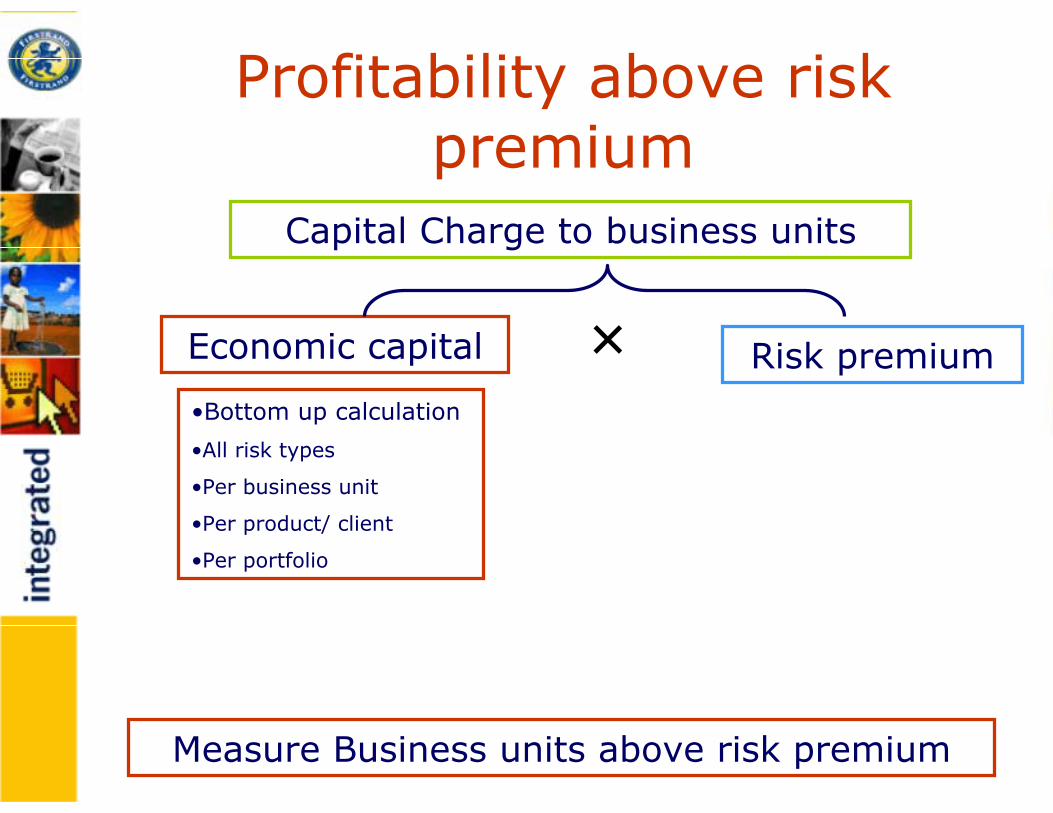

Profitability above risk premium

Capital Charge to business units

Economic capital וBottom up calculation

•All risk types

•Per business unit

•Per product/ client

•Per portfolio

Risk premium

Measure Business units above risk premium

Ensuring appropriate pricing

Statutory costs

Expected Loss (Credit)

Operational costs

Unexpected loss (capital)

MMTP

Ensure price for risk and pricing is dynamic

Regulatory costs

FR Internal Rating Assessment

Infrastructure costs & salaries

Interest & Liquidity risk (ALCO)

Economic Capital

Strategic decision making

Prerequisite

• Maintain credit rating

• Establish economic capital and risk/ reward

• Capital at risk

Probability of loss

Severity of loss

• Fund the capital required

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

AAA,AA,A BBB BB B CCC /D

CorporateRetail

Strategic decision making

Align with existing portfolio credit rating

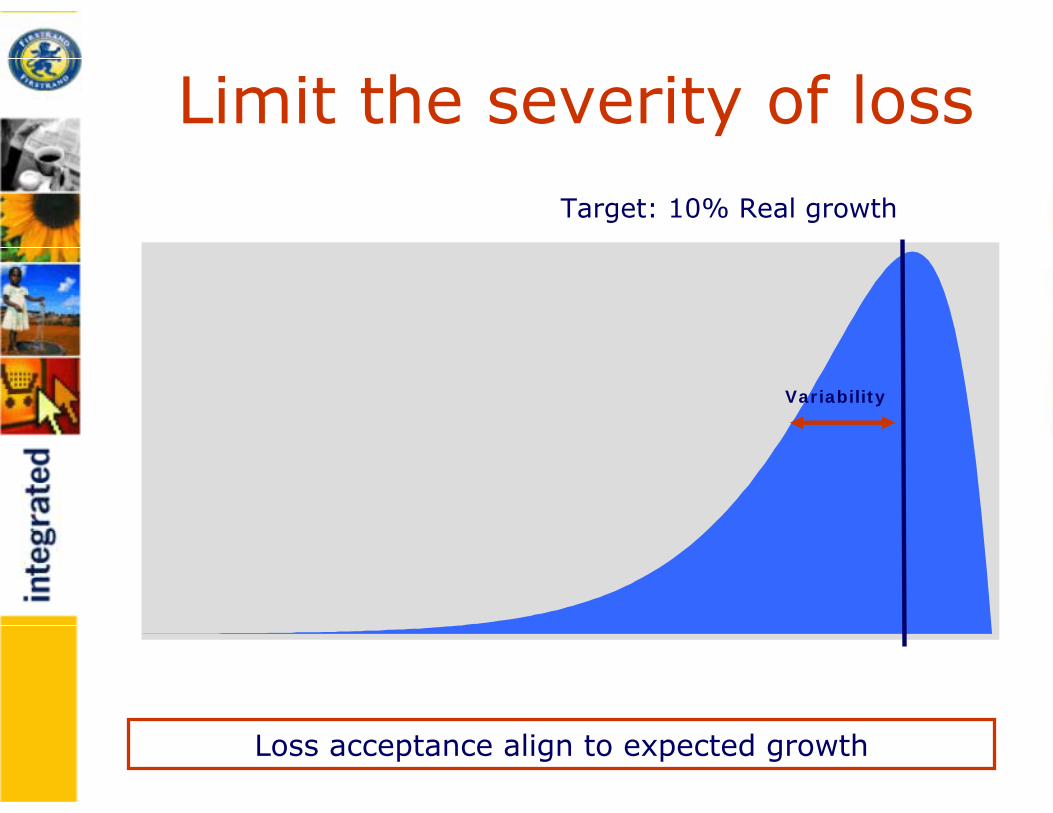

Limit the severity of lossTarget: 10% Real growth

Variability

Loss acceptance align to expected growth

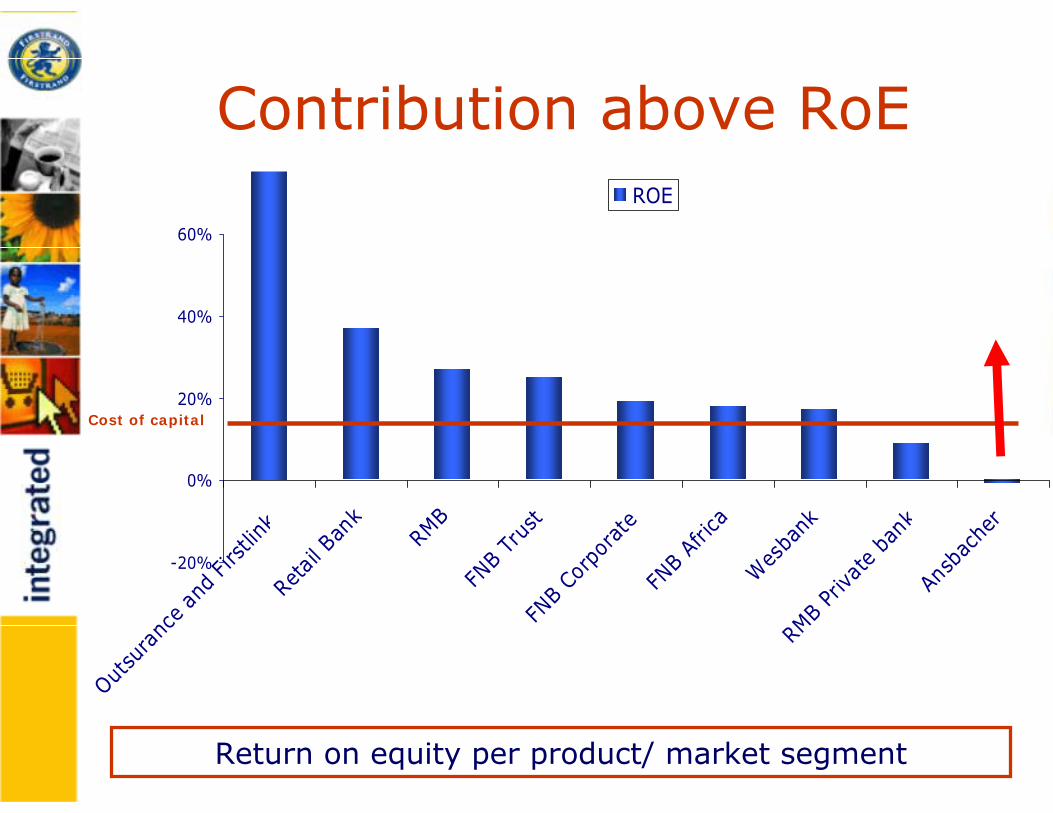

Contribution above RoE

-20%

0%

20%

40%

60%

Outsu

ranc

e an

d Fir

stlin

kRe

tail B

ank

RMB

FNB

Trus

tFN

B Co

rpor

ate

FNB

Afric

a

Wes

bank

RMB

Priva

te b

ank

Ansb

ache

r

ROE

Cost of capital

Return on equity per product/ market segment

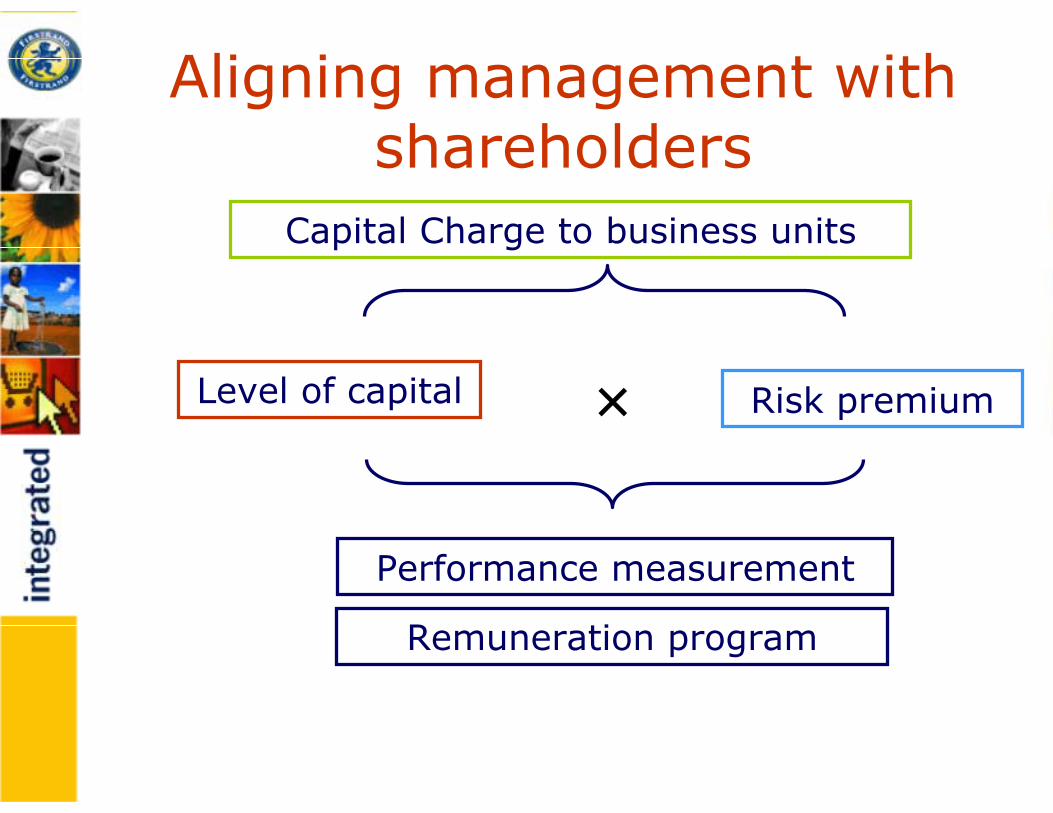

Aligning management with shareholders

Capital Charge to business units

Level of capital

Performance measurement

Remuneration program

× Risk premium

What does it all mean?

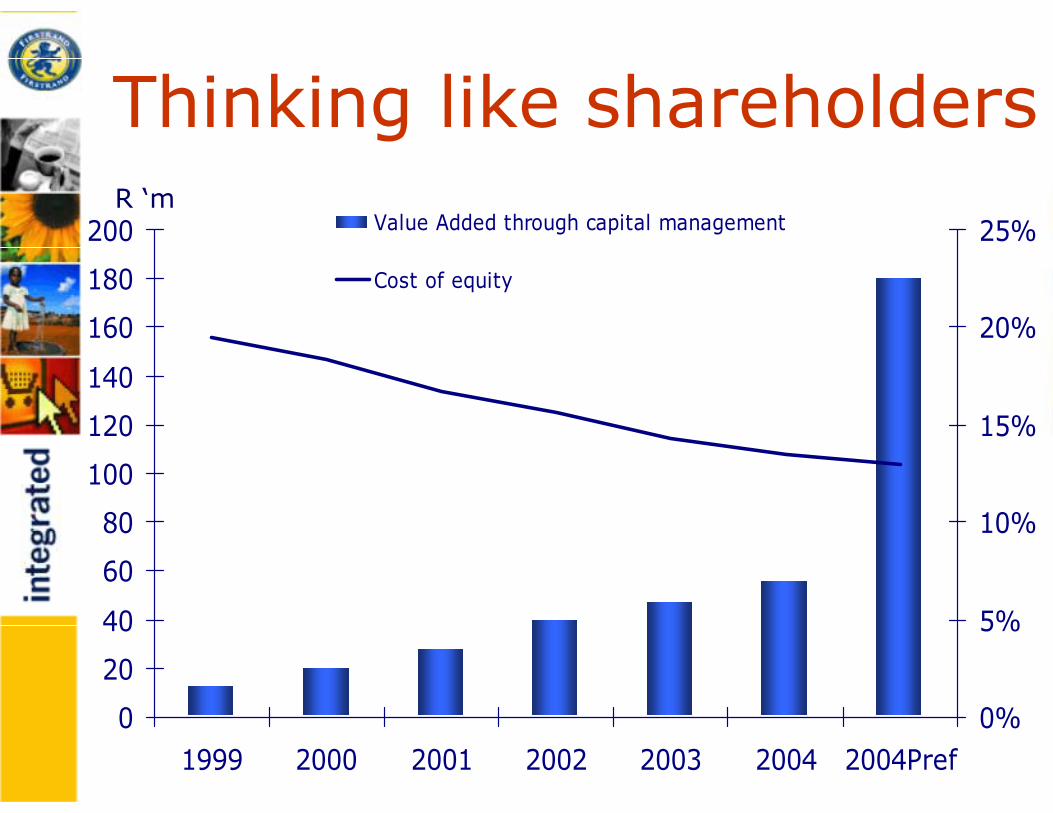

Thinking like shareholders

0

20

40

60

80

100

120

140

160

180

200

1999 2000 2001 2002 2003 2004 2004Pref0%

5%

10%

15%

20%

25%Value Added through capital management

Cost of equity

R ‘m

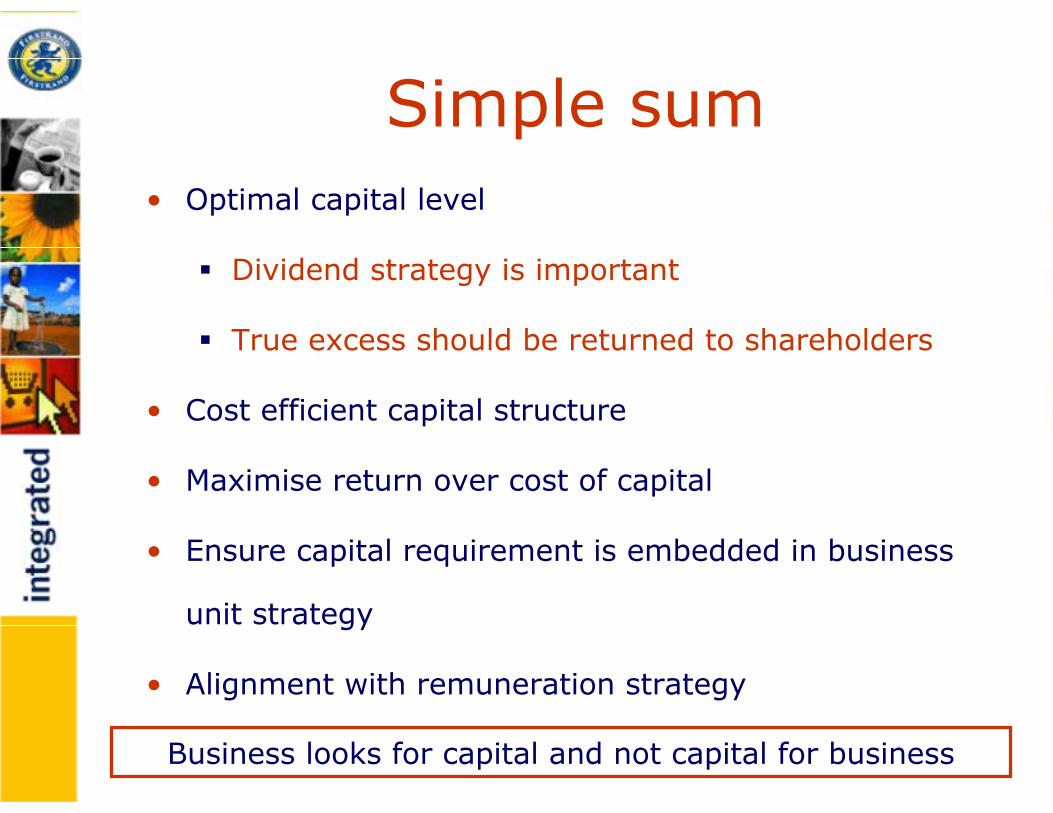

Simple sum• Optimal capital level

Dividend strategy is important

True excess should be returned to shareholders

• Cost efficient capital structure

• Maximise return over cost of capital

• Ensure capital requirement is embedded in business

unit strategy

• Alignment with remuneration strategy

Business looks for capital and not capital for business

What are the future challenges?

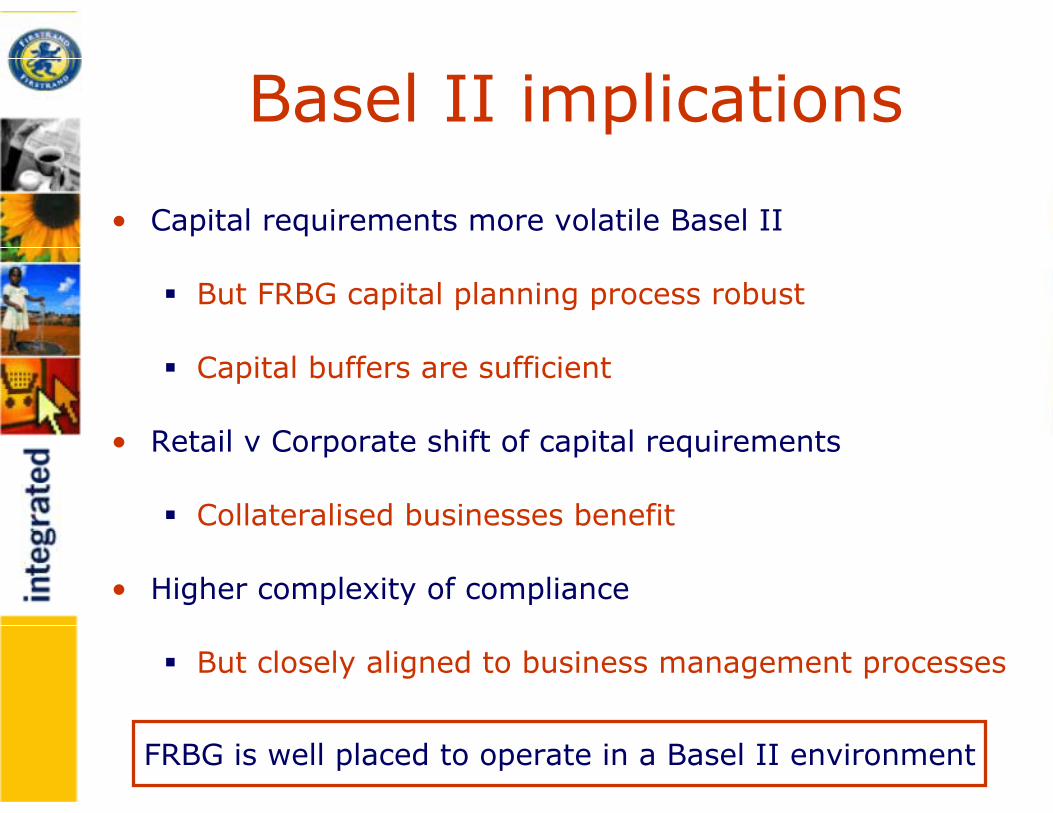

Basel II implications

• Capital requirements more volatile Basel II

But FRBG capital planning process robust

Capital buffers are sufficient

• Retail v Corporate shift of capital requirements

Collateralised businesses benefit

• Higher complexity of compliance

But closely aligned to business management processes

FRBG is well placed to operate in a Basel II environment

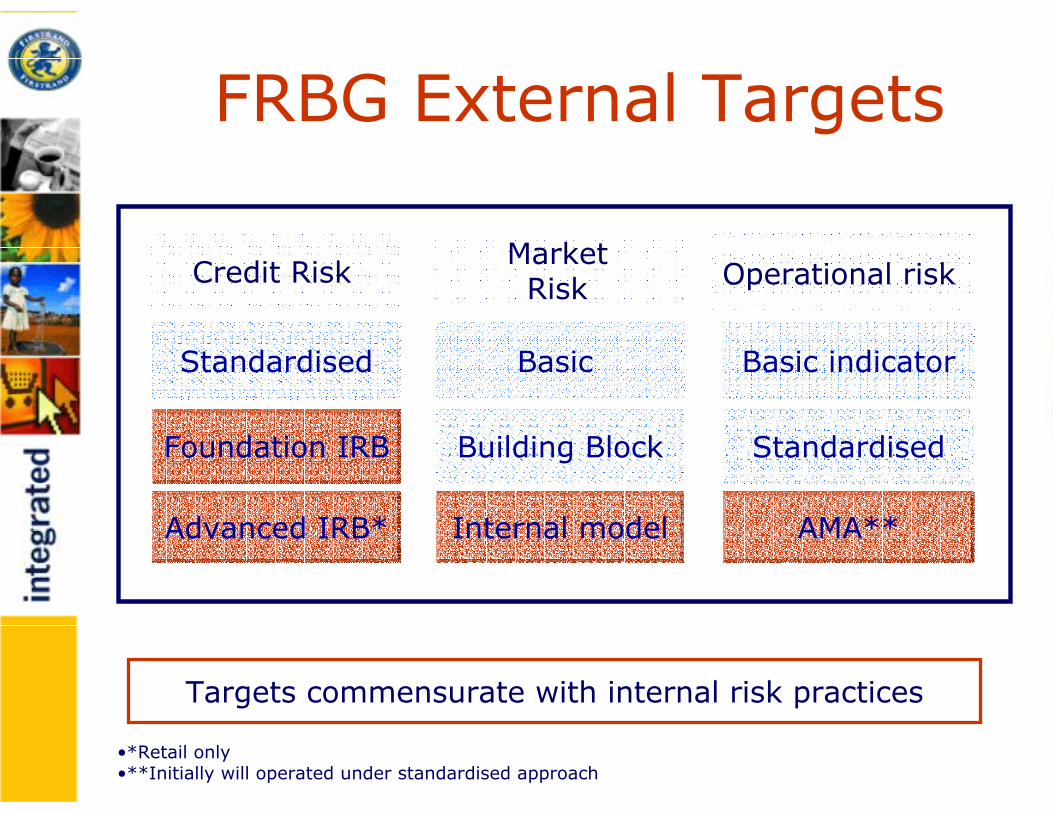

Advanced IRB*

Building Block

AMA**

Foundation IRB

FRBG External Targets

MarketRiskCredit Risk Operational risk

Standardised Basic

Internal model

Basic indicator

Standardised

•*Retail only•**Initially will operated under standardised approach

Targets commensurate with internal risk practices

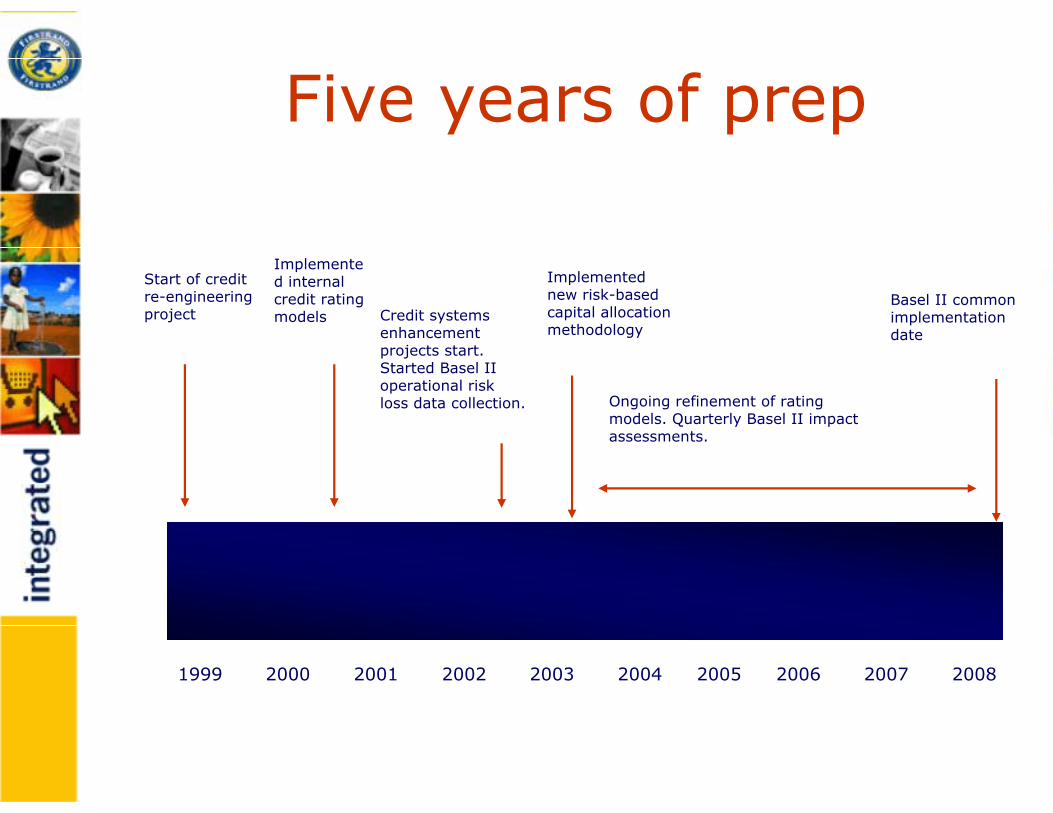

Five years of prep

Start of credit re-engineering project

Implemented internal credit rating models

Ongoing refinement of rating models. Quarterly Basel II impact assessments.

Basel II common implementation date

Implemented new risk-based capital allocation methodology

Credit systems enhancement projects start. Started Basel II operational risk loss data collection.

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

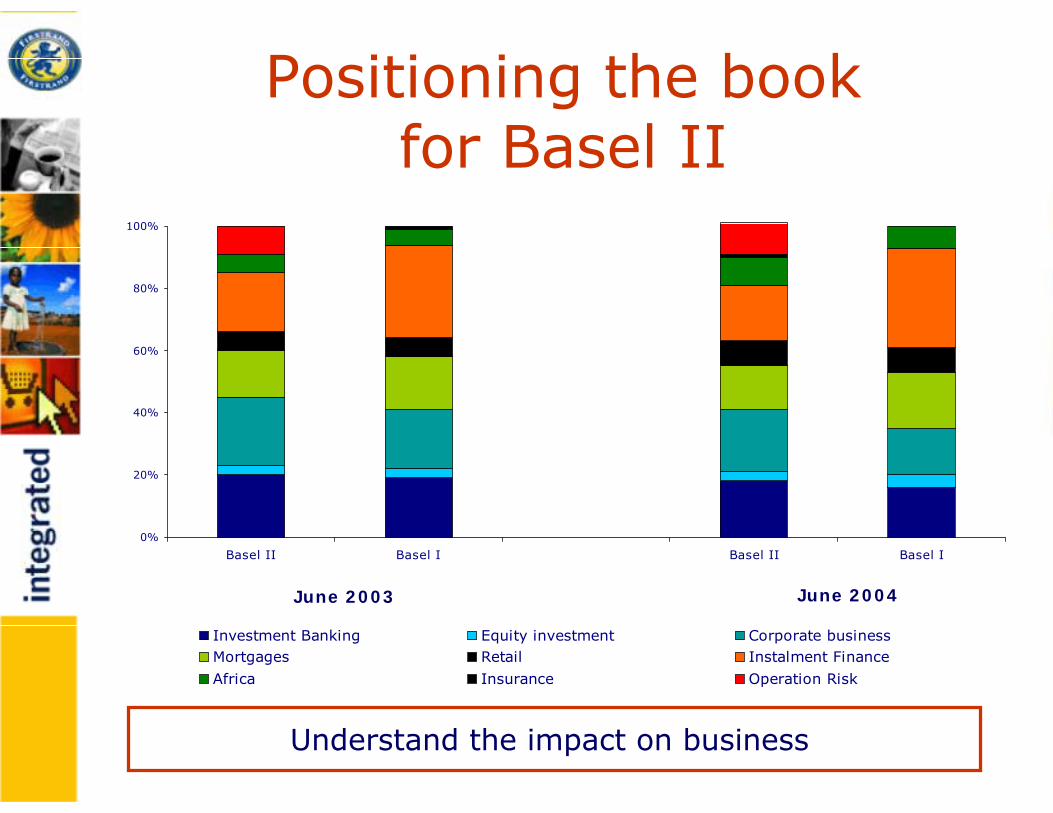

Positioning the book for Basel II

June 2003 June 2004

Understand the impact on business

0%

20%

40%

60%

80%

100%

Basel II Basel I Basel II Basel I

Investment Banking Equity investment Corporate businessMortgages Retail Instalment Finance

Africa Insurance Operation Risk

• Alignment between statutory & economic

capital

• Exploring the use of debt capital instruments

Insurance industry

![Raport Anual / Annual Report 2004 - Allianz-Tiriac · 2018-11-17 · ALTE INFORMA}II OTHER INFORMATION 2004 Varia]ie/Change 2003 2004/2003 Num`r angaja]i (medie anual`) 1.372 15,3%](https://img.pdfslide.us/doc/110x75/5fb9226cfc8b0e11cb28988a/raport-anual-annual-report-2004-allianz-tiriac-2018-11-17-alte-informaii.jpg)