Embed Size (px)

Citation preview

No 252– March 2017

Capital flow surges and economic growth in sub-Saharan

Africa: Any role for capital controls?

Ibrahim Alley

Editorial Committee

Shimeles, Abebe (Chair) Anyanwu, John C. Faye, Issa Ngaruko, Floribert Simpasa, Anthony Salami, Adeleke O. Verdier-Chouchane, Audrey

Coordinator

Salami, Adeleke O.

Copyright © 2017 African Development Bank Headquarter Building Rue Joseph Anoma 01 BP 1387, Abidjan 01 Côte d'Ivoire E-mail: [email protected]

Rights and Permissions

All rights reserved.

The text and data in this publication may be

reproduced as long as the source is cited.

Reproduction for commercial purposes is

forbidden.

The Working Paper Series (WPS) is produced by the

Macroeconomics Policy, Forecasting and Research

Department of the African Development Bank. The

WPS disseminates the findings of work in progress,

preliminary research results, and development

experience and lessons, to encourage the exchange

of ideas and innovative thinking among

researchers, development practitioners, policy

makers, and donors. The findings, interpretations,

and conclusions expressed in the Bank’s WPS are

entirely those of the author(s) and do not

necessarily represent the view of the African

Development Bank, its Board of Directors, or the

countries they represent.

Working Papers are available online at

http:/www.afdb.org/

Correct citation: Alley, Ibrahim (2017), Capital flow surges and economic growth in sub-Saharan Africa: Any role for capital

controls?, Working Paper Series N° 252, African Development Bank, Abidjan, Côte d’Ivoire.

Capital flow surges and economic growth in sub-Saharan Africa: Any role for capital controls?

Ibrahim Alleya

a The author would like to express gratitude for valuable comments and suggestions from Jacob Oduor. Other

members of the Macroeconomics Policy, Forecasting and Research Department, African Development Bank,

especially John Anyanwu, Momoudu Sy, Adeleke Salami, Anthony Simpasa and Qingwei Meng are well

appreciated for useful information ans support. Many thanks to Andres Fernandez of Inter-American Development

Bank (IADB) for providing the IMF AREAR documents and technical guidelines used in extending FKRU capital

control dataset for this research.

AFRICAN DEVELOPMENT BANK GROUP

Working Paper No. 252

March 2017

Office of the Chief Economist

Abstract

This study provides explanation for weak

linkage between private capital flows and

economic growth of the sub-Saharan

African region and offers policy

recommendations for stronger linkage

and growth optimization. Estimation of a

simple growth equation shows, in

support of stylized facts, that the flows do

not significantly affect growth. Further

analyses controlling for surge

components of these flows and the effects

of capital controls provides useful

insights. Risk-sharing private capital

(foreign direct investment and equity

capital) proved beneficial in terms of

growth contribution and improved

credit supply while risk-apathetic capital

(bond) harmed growth and weakened

competitiveness. Surges to these flows

imposed costs in terms of growth loss,

reduced credit supply and poor capital

formation. These costs detracted from

the benefits and resulted in the weak

linkage. Capital controls were more

effective at containing surges to risk-

sharing capital and when selectively

targeted. Financial institutions (national

and regional) should be encouraged to

attract more of risk-sharing private

capital to finance the region while

governments should appropriately

target controls to optimise benefits from

the flows.

Keywords: Private capital flows, Shocks, Capita controls, Economic growth

JEL classifications: F21, F32, F36, F38, F41, F43

5

1. Introduction

International capital flows not only offer a great deal of benefits to financially integrated

countries, they also pose numerous macroeconomic challenges (Reinhart and Reinhart, 2008;

Furceri, Guichard and Rusticelli, 2011). While countries with some degrees of financial

openness are able to share income risks with rest of the world, smooth their consumption path

and bridge saving-investment and foreign exchange gaps (Prasad et al., 2003; Chenery and

Strout, 1966; Taylor, 1991; Akinboade, Siebrits and Roussot, 2006), they also face the risks of

having their economies exposed to exogenous shocks transmitted through capital flow

volatility which, in turn, induce domestic instability (Kaminsky, 2005; Fernandez et al., 2015)

and weaken economic growth (Cavallo, 2005).

Capital flows, gross and net, have been generally volatile (Broner et al., 2012; IMF, 2012; Lee,

Park and Byun, 2012) and subject to overshootings, brutal reversal and sudden stops (Boudias,

2014; Broner et al., 2012; Calderon and Kubota, 2011; Agosin and Huaita, 2010; Calvo and

Reinhart, 2000). Financial flows to sub-Saharan Africa (SSA) have not been exceptional:

capital flows to the SSA region are very volatile, and in addition very stupendous relative to

economic sizes of recipients (IMF, 2011). The large inflows of capital into the region are not

unconnected with performance of frontier market in the region. These market have attracted

considerable private capital (bond, equity and direct investment)2 from the rest of the world

(IMF, 2011), especially the advanced countries (Boudias, 2014), due to so many factors. They

are attractive to international investors because relevant financial indicators - e.g. real interest

rates and interest rate spread - in these economies are impressive. With respect to these

indicators, seven selected representative frontier markets (FM73) outperform the major

advanced economies4 (the G7) throughout 1980-2014 period. The rate of inflows of these

private external finances to the FM7 has been explicably larger than to the G75 for the foregoing

reasons.

While these inflows of the private capital should be beneficial to the region from the theoretical

perspective, data suggest a weak linkage between these flows and economic growth6 (Figures

1-4) in the SSA. The figures, which plot the average real GDP growth for each of the FM7

against their inflows of aggregate private capital, foreign direct investment, equity capital and

bond capital respectively in 2003-2008 (pre-financial crisis) and 2009-2013 (post-financial

crisis) periods show that equity capital and bond capital flows are negatively correlated with

growth while FDI and aggregate private capital’s positive correlation with growth are weak

and statistically insignificant.

This study thus re-examines the nexus to unravel the weak linkage between the flows and

economic growth, as well as the disconnect between the theory and empirical evidence, by

controlling for the flow characteristics of private capital in terms of surges to these flows. This

research perspective is informed by the fact that private capital flows are volatile and transmit

disturbances in the origin economies to recipient countries. This perspective is important

because the role of recipient economies’ characteristics such as the absorptive characteristics

2 These capital flows, unlike the official capital flows, are market based in nature and responsive to market

(economic) fundamentals; thus they are our main focus in this study. 3 These frontier markets identified by IMF (2011) are important in terms of size and geographical

representativeness of the sub-Saharan Africa economy, and are covered for analysis in this study. They include

Nigeria Mauritius, Mozambique, Senegal, Tanzania, Uganda and Zambia. 4 See Figure 1 in the section 2 of this article. 5 See figures 2-5 in section 2. 6 See figures 1A-4A in the apendix

6

(IMF, 2011), financial market depth (Klein and Olivei, 2008), and level of economic and

financial sector development (Bailliu, 2000; Edwards, 2001; Arteta et al., 2003) only matter

when the flow patterns of private capital in terms of magnitude and timing are not consistent

with the need and size of the recipient economy7. By controlling for surges to these flows, it

will be possible to determine the true effects of the flows. Then, policy directive regarding what

recipient countries should do in terms of designing and targeting capital controls would be

clear. If a flow is beneficial but its surges are harmful, then, the control should target the surges,

and vice versa. Specifically, this study analyses the effects of the private flows and their surges

(positive and negative) on economic growth directly, and indirectly through capital formation,

credit supply and exchange rate transmission mechanisms. It also assesses the effectiveness of

capital controls in the SSA with respect to managing the surges and any negative growth effects

of capital flows.

The study estimated extended Blanchard et al.’s (2016) growth equations8 for a panel of 25

SSA countries in 2003-2013 period with a System Generalized Methods of Moment

(Sys.GMM) and established that private capital flows had insignificant effects on economic

growth when the effects of surges were not controlled for. Once the surges were accounted for,

equity capital and foreign direct investment (known to share income risks of recipient

economies) had positive effects on economic growth while bond flows (risk-apathetic capital)

exerted negative impact on the economies. Further investigations into these effects show that

risk-sharing capital (equity and direct investment) support credit supply and did not conduce

to loss of international competitiveness by not appreciating the real effective exchange rate

(REER). Bond flows, on the other hand, neither supported capital formation nor credit supply;

rather, they contributed to weakening trade competitiveness by engendering REER

appreciation. Surges to these capital flows negatively affected economic growth and detract

from the positive effects of the flows. This detraction explains the weak linkage between capital

flows and economic growth observed in reality. Capital control measures are found to be

effective in stemming shocks to capital flows and their negative growth effects when carefully

targeted.

This study contributes to the literature in two main ways. It presents evidence on the effects of

surges to capital inflows (measured using methodologies for measuring surges in capital flows

literature) on economic growth of sub-Saharan Africa. Most studies in this strand of literature

rarely focus on the SSA, perhaps due to data issues; and their best shot at the region is to include

one or two SSA countries in their samples (Cardarelli et al., 2010 [South Africa, non-SSA-

Egypt, Morocco, Tunisia]; Gosh et. 2014 [Mauritius, non SSA – Egypt]; Benigno et al, 2015

[Mauritius and South Africa, non-SSA – Egypt, Morroco and Tunisia]). Most others totally

exclude SSA (e.g. Forbes and Warnock, 2012). Thus, this study is a major contribution to

literature on capital flow surges. It is close to Cardarelli et al. (2010) and Caballero (2014) in

that it focuses on surges of private capital flows, and Caballero (2014) and Benigno et. al (2015)

in their measurement of surges. It differs from Caballero (2014) in not examining the effect of

the surges/shocks to private capital on likelihood of banking crises, from Benigno et al. (2015)

7 Felices and Orskaug (2005) note that international capital markets, rather the forces of demand and supply,

arbitrarily allocate capital in ways that may not match with the quantity and timing of capital need of domestic,

capital recipient economy. 8 Simple partial-equilibrium growth equations not derived from optimisation of general equilibrium model was

adopted on the basis cost-benefit comparison. While derived equations estimated in micro-foundation general

equilibrium (GE) models (e. g. Gabaix and Maggiori, 2015) are not significantly different from the simple partial

equilibrium analyses (e. g. Blanchard et al. 2016; Alley, 2015). Besides the latter are more transparent and obviate

the need for calibrations and simulation requisite in many GE models (Korinek, 2014) which rely on many

assumptions about parameters and structural relationships that are difficult to verify (Chetty, 2009).

7

in not examining surges to aggregate capital flows proxied by adjusted current account balance,

and from Forbes and Warnock (2012) and Ghosh et al. (2014) in that it does not focus on

determinants of surges or their probability of occurrence.

Secondly, this study presents evidence on effectiveness of capital controls in managing capital

flows problems facing small open economies, which most SSA countries are. In addition, it

contributes to the literature on capital flows management by extending the Fernandez et al.

(2015) datasets on capital controls to cover 14 additional SSA countries. While this study is

similar to many previous studies on effectiveness of capital control in reducing volume of

surges and composition of flows, it differs from them in use of capital control index that draws

information from individual capital controls.

The rest of the paper is organised as follows. Section 2 presents stylised facts while section 3

briefly reviews related literature. Section 4 discuses methodology and preliminary analyses are

conducted in section 5. Empirical evidence is discussed in section 6 while section 7 offers

concluding remarks and policy lessons.

2. Stylized Facts

The financial performance of SSA, from the perspectives of international investors, has been

impressive. Real interest rates and interest rate spread in the SSA, especially the FM7 are far

higher than in the G79. Many factors are responsible for this differential. Capital stock in

developed economies, the G7 for examples, is far larger than in developing economies like the

SSA10. Hence, the return on capital would be far higher in the latter than in the former. Given

the diminishing return of factor inputs to which production functions are generally subject to,

larger capital stock in the G7, 7

2

Gk , engenders lower return )( 7

2

Gkr because it produces, in

autarky, output 7

2

Gy which is lower than optimal output 7

1

Gy , (figure 11A) 11. On the other

hand, lower capital stock in the FM7 corresponds to higher return on capital )( 7

1

FMkr in figure

10A (appendix).

With financial globalisation, international investors arbitrage and reallocate more capital from

the G7 to the FM7, leading to convergence of interest rates to )( GLOkr which is less than

)( 7

1

FMkr and higher than )( 7

2

Gkr in figure 10. This is expected to lead to growth in both the G7

and FM7 as more capital in the latter leads to higher output level 7

2

FMy (figure 9A) 12 and the

interest income on exported capital (flows to the FM7 from GM7) increase the gross national

income of the former to7

3

Gy on a new income function/path )()( 7

2

7

2

GG kkf .

Evidence on interest rate convergence can be seen in figure 6A (appendix). Though the world

real interest rate data is not available on World Bank WDI database, it is obvious from figure

6A that the gap (divergence) between the real interest rate in FM7 and G7 fell over time. The

rate in both country groups albeit declined in absolute terms, perhaps due to several factors

such as global liquidity, the gap between the real interest rate in FM7 and G7 decline from

about 8.6 in 2002 to about 4.4 in 2014.

9 See figures 5A-7A in the appendix. 10 See figures 8A in the appendix. 11 See appendix 12 See appendix

8

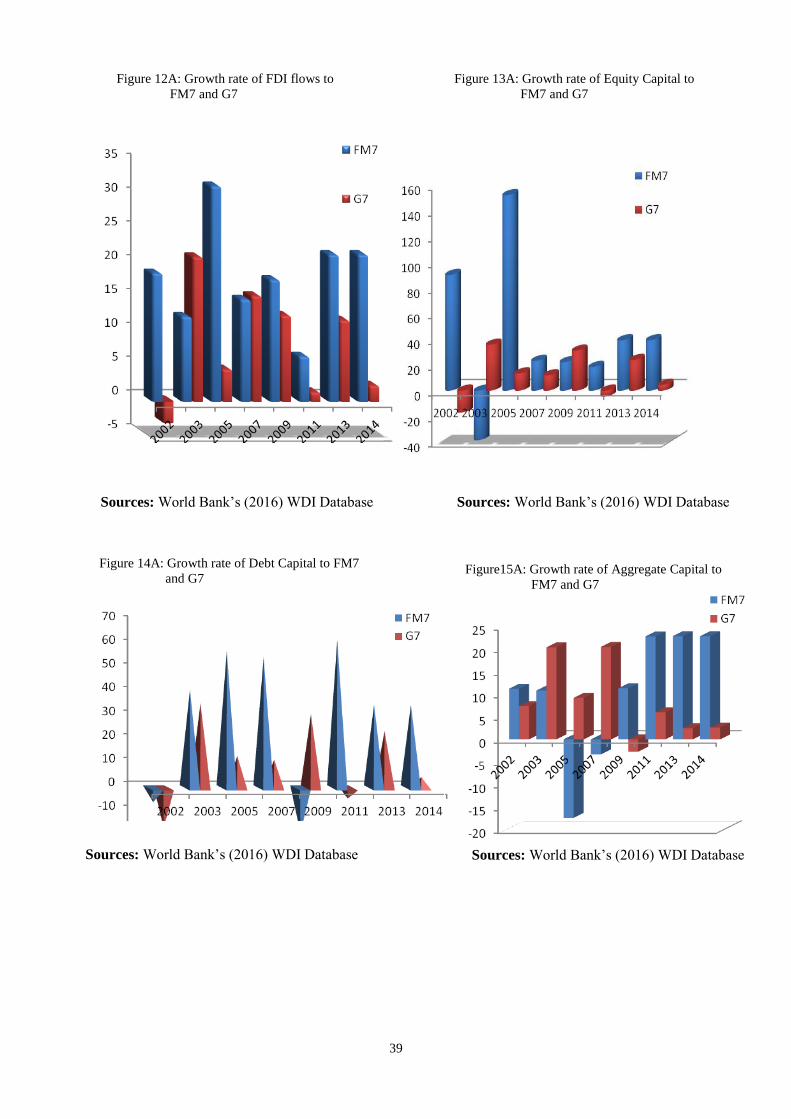

Evidence on reallocation of private capital from the G7 to the FM7 is presented below. Figures

12A-15A (see appendix) highlight the growth rate of FDI, equity capital, debt capital and

aggregate capital inflows to the FM7 and G7 respectively. The figures support the theoretical

prediction in figures 6A-8A in the appendix. The rate at which private capital flows to the FM7

has been higher than to the G7. Though the rate generally fell for both country groups around

2007-2009 global financial crisis, the rate of flow to the FM7 has been larger than to the G7 in

post-crises period. During the crises, the rate of flow to the FM7 is visibly less than to G7 and

this is evident of flight to safety which describes the herd behaviour of international investors

who repatriate their investment from developing, perceptibly riskier, economies to the

developed, perceptibly less risky economies during the crises.

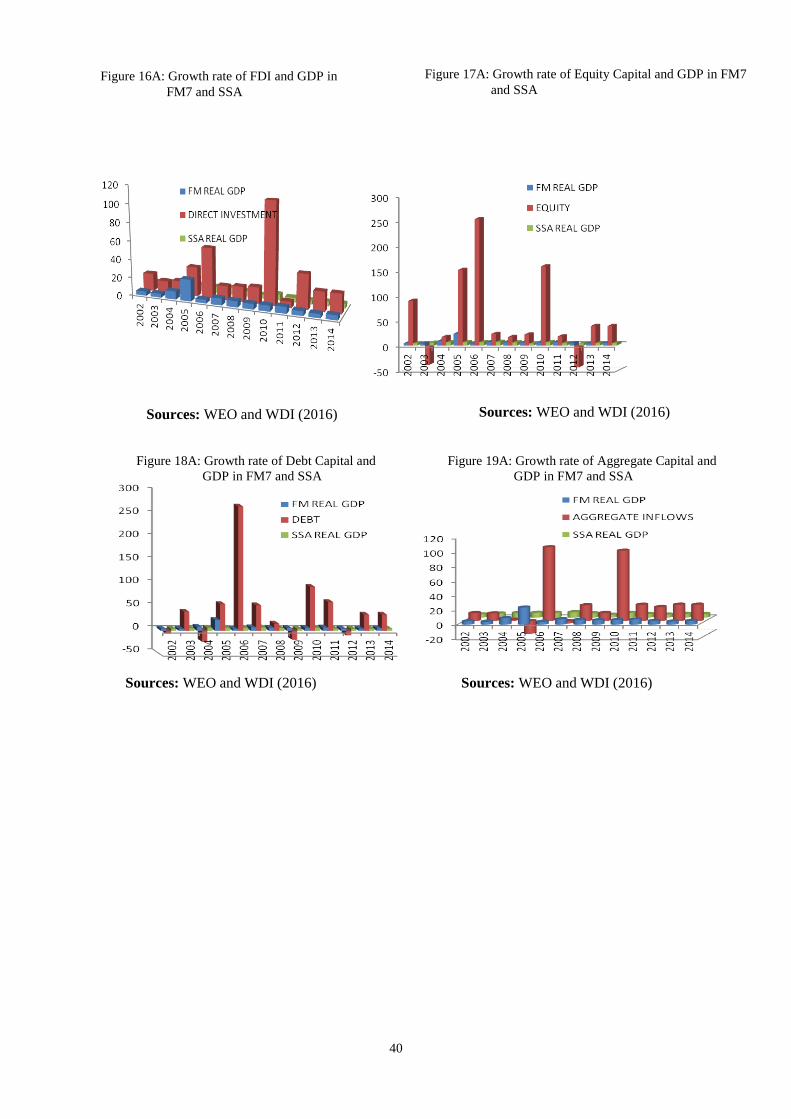

Though capital flows to the SSA (especially the FM7) have been on the rise, neither the region

nor the group appear to achieve growth gains from the flows. This is evident in figures 1A-4A

and figures 16A-19A (see appendix) below.

Figures 16A-19A suggest a weak linkage between growth of private capital inflows to the FM7

and GDP growth in FM7 and the region. While the rate of inflows has been very huge, real

GDP growth rates have been very small. Both the rate of flows and the real GDP growth rates

were affected however by the global financial crises. The weak linkage between the private

capital flows and the real GDP in the region is supported by the correlation matrix in table 1

below. While the correlations between the flows are mostly high, private flows are weakly

correlated with GDP.

Table 1: Correlation Matrix on Private Capital Flows and GDP in FM7 and SSA

FDI EQUITY BOND AGG.

FLOWS

FM7

GDP

SSA

GDP

FDI 1.000

EQUITY 0.610 1.000

BOND 0.467 0.781 1.000

AGG. FLOWS 0.781 0.631 0.739 1.000

FMGDP -0.008 0.257 -0.055 0.423 1.000

SSAGDP 0.282 0.440 0.474 0.161 0.387 1.000

Source: WEO and WDI (2016)

3. Literature Review

This section reviews the literature on capital flows, their effects on the economy and the role

of capital controls in addressing the challenges that accompany international capital flows.

3.1 Capital Flows and Economic Growth

Many of the empirical studies on capital flows and economic growth kick off their analyses

with the assumptions of the neoclassical growth theory13, which they test against empirical

reality. Relying on the assumption of diminishing marginal productivity of capital, the theory

predicts that (developed) countries with large capital stock would pay low return on capital 13 As developed in Solow (1956) and Swan (1956) growth model.

9

while the reverse holds for (developing) countries with lower capital stock (Barro and Salai-

Martin, 1996, Romer, 2012). Thus, in a scenario of financial integration, capital should flow

from developed countries (in the North) to developing countries (in the south), and both

categories of countries benefit as productivity rise in developed countries and developing

countries use the inflow of capital to augment the domestic resources for higher growth. Alley

(2014) provides a graphical analysis of neoclassical theoretic explanation of how capital would

naturally flow from capital surplus country to a capital-deficit one, and how both gain from the

flows. Prasad, Rogoff, Wei and Kose (2003) describe the direct and indirect channels by which

capital flows, in theory, enhance growth of recipient economies.

Testing this prediction has been the main focus of empirical studies. The literature is replete

with many inconclusive findings. Many find evidence in support of the prediction, some no

evidence, while a host of studies find evidence disproving the theory. The bulk of the arguments

in the empirical literature centres around explanations for the contradictory evidences on the

nexus between capital flows and economic growth. Prasad et al (2003) documents how data on

countries’ growth and capital level of financial integration (capital inflows) provide a platform

for mixed evidences reported in several studies. As against the theory’s prediction that capital

flows more to fast-growing economies, less financially integrated14 countries like Mauritius

and Botswana have high per capita GDP growth while more financially integrated countries

like South Africa and Jordan have negative per capita GDP growth. In support of the theory,

on the other hand, more financially integrated countries like Korea, Singapore and Thailand

record super economic growth while economic performance of less financially integrated

countries like Haiti, Niger and Nicaragua is appalling.

Capital flows have been noted to benefit recipient economies by augmenting domestic savings,

lowering the cost of capital owing to better risks allocation, enhancing transfer of technology,

developing the financial sector and inducing better policy formulation (Prasad et al., 2003) as

well as improving welfare by supporting consumption smoothing (Bekeart et. al., 2005). Given

the inherent benefits, capital flows enable the recipient economy to improve its economic

growth. Many other studies (Aizenman, Jinjarak and Park, 2013; Alfaro, Kalemli-Ozcan and

Volosovych, 2011; Kose, Prasad and Terrones, 2009) also agree that international capital flows

positively affect economic growth. For a survey of literature on studies that found positive

evidence for capital flows-growth nexus, see Bunmann, Hermes and Lensink (2013).

Some studies however posit that the positive effects of capital flows are only conditional. Klein

and Olivei’s (2008) show that that the positive effects of capital account liberalisation and the

associated flows on economic growth depend on financial depth. Edwards (2001) and Arteta,

Eichengreen and Wyplosz (2003) find that, conditional upon a significant level of economic

development - specifically financial - capital account openness (and the associated flows)

positively affects growth. In the same vein, Bailliu (2000), on examination of the role of capital

flows on economic growth using data on 40 developing countries, finds that the impact of

capital flows on the economy depends on the level of financial market development: capital

inflows have positive (negative) effect on growth when the country is financially developed

(underdeveloped).

In variance to the foregoing, some studies establish that capital flows do not positively affect

economic growth. Prasad, Rajan and Subramanian (2007) show that capital flows negatively

correlate with growth. The study finds that countries with lower inflows of capital grow more

14 Degree of financial integration is associated with level of capital flows.

10

than those with larger inflows. Gourinchas and Jeanne (2011) also noted that capital flows

correlates with growth, as countries with slower growth attract more flows that faster growth

counterparts. In separate studies, Edison et al. (2002) and Kraay (1998) find that capital flows

do not affect growth at all. A comprehensive survey of literature on similar evidence is

available in Bunmann, Hermes and Lensink (2013).

The divergence between the findings of the studies above may result from the type of flows

analysed. Some studies find that different components of capital flows have different effects

on economic growth. Choong et al’s (2010) show that FDI positively affects growth while

foreign debt and portfolio investment do not. In the same vein, Kose, Prasad and Terrones

(2009) had found that both FDI and portfolio flows enhance total factor productivity growth

(TFP) but foreign debts do not. In their analysis of the impact of capital flows on the economic

growth of one hundred countries over the period of twenty years (1990-2010), Aizenman,

Jinjarak and Park (2013) find that FDI positively influence growth while non-FDI flows

(portfolio investment, debt and equity) do not have significant positive effects on economic

growth other than provision of access to foreign savings.

3.2 Capital Flow Volatility and Economic Growth

Capital flows have been noted to very volatile, and subject to over-shootings, brutal reversal

or sudden stops15 (Broner et al., 2012; Calderon and Kubota, 2011). However, some

components are more volatile than others (Becker and Noone, 2009). Portfolio flows and

foreign debt are generally considered to be the more volatile than FDI (Ferreira and Laux, 2008;

Becker and Noone (2009).

Volatility of capital flows has been noted to have significant negative effects on the economy.

Surges in gross and net capital flows have been associated with exchange rate appreciation,

macroeconomic overheating and inflation assets bubbles, which in turn exacerbates financial

fragilities and credit risks (Ostry et al., 2010). Broner and Rigobon (2004) find that capital

flows volatility is negatively correlated with level of GDP, institutional quality and financial

development. Alfaro, Kalemli-Ozcan and Volosovych (2007) also show that capital flows

volatility is negatively correlated with sound macroeconomic policies and institutional quality.

Broto, Diaz-Cassou and Erce-Dominguez (2008) find that volatility of portfolio flows is

negatively correlated with GDP per capita, its growth, bank sector development and trade

openness. In the same vein, Aizenman and Sushko (2011) as well as Mody and Murshid (2005)

report that portfolio flows have less beneficial effects on the economy than FDI flows because

the former is more volatile. In a panel regression using data on 15 emerging countries from

1991-2011, Converse (2012) finds that while portfolio flow positively affects output but its

volatility reduces output via its dampening effect on investment. Ferreira and Laux (2008)

however disagree. On the basis of their analysis of data on 50 countries including 14 developed

countries between 1988 to 2001, this study show that openness to portfolio flows is conducive

to growth, and that the volatility associated with the flows does not hurt economic growth

because the results are statistical insignificant.

Similarly, capital flow shocks have been established to negatively correlate with economic

growth. Using data on fourteen sub-Saharan African counties in a vector Autoregressive (VAR)

model, Alley and Poloamina (2015) show that shocks to portfolio investment and foreign debt

(bank lending flows) reduce economic growth. The study however finds that shocks to FDI, a 15A sudden stop is conceived in literature as unexpected, persistent and significant reversal of net inflows of

capital.

11

more stable flow with longer maturity, do not. In this same vein, Alley (2014) using Devereux

and Sutherland’s (2011) definition of capital flow shocks, find that shocks to capital flows

detract from economic growth of sub-Saharan African countries.

3.3 Capital Flows Shocks and Capital Controls

Several studies have examined capital flow shocks and capital controls from different

perspectives. While some studies attempt to examine the effectiveness of capital controls in

curbing capital flows shocks - surges, stops, retrenchment and flight - and their probability of

occurrence (Forbes and Warnock, 2012; Ghosh et al., 2014), others seek to analyse the

determinants capital controls deployment (Fratzscher, 2012).

Estimating data on 58 countries in a logistic regression, Forbes and Warnock (2012), find that

capital controls, as well as other domestic factors, do not significantly affect probability that a

country experiences capital flows shocks. The study however finds that global factors, such as

global economic risk (measured by VIX index), global growth increases and regional

contagion, increase the probability that a country experiences capital flow shocks.

Similarly, Ghosh et al. (2014) analysed data on 56 emerging economies to estimate the effects

of global push factors and domestic pull factors on likelihood and magnitude of capital flow

surges. The study finds that both global factors and domestic factors matter for capital flow

surges. Unlike Forbes and Warnock (2012), Ghosh et al. (2014) find that capital controls reduce

the probability and the magnitude of capital flow shocks that a country experiences.

Ostry et al. (2011) examined the effects of capital controls (measured with Schindler (2009)

index) on composition of capital flow, credit boom and foreign exchange lending. The study

finds that capital control measures are effective against credit boom, debt composition and FX

lending. It also finds that maturity composition of capital flows affects growth resilience. While

nonfinancial FDI enhances resilience, debt and financial FDI negatively do because they are

associated with credit booms and growth vulnerabilities (decline in output growth). Ostry, et

al. (2010) however note that the effectiveness of controls in regulating inflows thus depends

on how extensive they are, whether the country maintains the necessary administrative and

institutional infrastructure to enforce the controls, and whether investors have incentives

circumventing them. The study also finds that capital controls negatively correlate with growth

decline and crisis. The study finds that capital controls on total flows, equity investment and

bond inflow reduce probability of growth crises.

Fratzscher (2012) estimated data on 79 countries from 1984 to 2009 to analyse factors that

influence the probability that a country imposes capita controls. The study finds that the

probability is significantly influenced by exchange rate regime, exchange rate volatility and

interest rate differentials. Countries with higher volatility of real effective exchange rate,

undervalued currency, fixed/pegged exchange rate regimes, favourable interest rates

differentials and equity returns volatility are more likely to impose capital controls than others;

while countries that are open to trade, and have well developed financial sector are less likely

to impose controls.

4. Methodology

This section presents the methods employed in analysing the effects of private capital inflows

on the economic growth of SSA, the role of surges to the flows in the growth nexus and the

effectiveness of capital control measures in managing the growth effects of the flows and the

related surges. Data description, measurement and sources are also highlighted.

12

4.1 Theoretical Framework and Model Specification

The neoclassical growth model extended by Alley (2015) to analyze the effects of shocks to

private capital flows on growth of 14 SSA countries provides the theoretical framework. Within

this framework, the Blanchard et al.’s (2016) growth equation (which analyzed the role of bond

and non-bond inflows on growth of 19 emerging economies) was extended to incorporate the

effects of surges to inflows of bond, equity, direct investment and aggregate private capital

flows on economic growth of 25 SSA countries. The effects of capital controls in the growth

nexus are also examined within the extended model.

Equation 1 presents the baseline growth model16. Equations 2 highlights the Blanchard et al.’s

(2016) growth equation, testing the effects of bond inflows, equity inflows and direct

investment inflows on growth rate of real gross domestic products of the SSA countries. The

extended Blanchard et al.’s (2016) growth equations where the effects of surges to these flows

are tested and where the effectiveness of relevant capital control measures is examined are

respectively presented by equations 3-4. Equation 5 is a modified version of equation 4.

19

1

'1 it

k

itkitit Xyy

(1)

23

1

'9

1

'1 it

l

itl

k

itkitit ZXyy

)2(

36

1

'3

1

'9

1

'1 it

p

itp

l

itl

k

itkitit SZXyy

)3(

46

1

'6

1

'3

1

'9

1

'1 )*( it

q

ititq

p

itp

l

itl

k

itkitit SCSZXyy

(4)

5

1

''

1

'6

1

'3

1

'9

1

'1 )*()*( it

n

r

ititr

n

q

ititp

p

itp

l

itl

k

itkitit SZSCSZXyy

(5)

where

y = growth rate real gross domestic product (GDP).

X = 9x1 vector of explanatory variables which serve as control in subsequent growth

equations. These variables are (average) real government expenditures in percentage

of GDP, real gross capital formation in percentage of GDP (RCF), secondary school

enrolment rate population growth rate, institutional quality, change in terms of trade,

trade openness and real GDP growth rate of trading partners.

Z = 3x1 vector of surges to private capital inflows in percentage of GDP: bond capital

inflows, equity capital, and direct investment, respectively.

S

= 6x1 vector of surges to private capital inflows: positive surges to bond capital

inflows, equity capital, and direct investment, respectively; ( DIIEQUIBDI ,, )

and negative surges to these flows ( DIIEQUIBDI ,, ).

16 The explanatory variables in this baseline growth model are those widely employed in the empirical growth

literature (See Ostry et al., 2010; Barro (2003); Kroft and Lloyd-Ellis (2002); Fatas (2001); and Ramey and

Ramey (1995) for a survey).

13

C =6x1 vector of capital controls on positive surges ),,( DIIEQUIBDI ContrlContrlContrl

and negative surges ),,( DIIEQUIBDI ContrlContrlContrl

= error terms, as captured in the equations.

Equations 6-9 below replicate equations 2-5 for aggregate capital inflows. The equations are

the only but representation of the nexus between real economic growth rate, aggregate inflows,

related surges and capital controls.

6'9

1

'1 ititl

k

itkitit KXyy

)6(

72

1

''9

1

'1 it

p

itpitl

k

itkitit GSKXyy

)7(

82

1

'2

1

''9

1

'1 )*( it

q

ititqq

p

itpitl

k

itkitit GSLGSKXyy

)8(

9

1

'2

1

'2

1

''9

1

'1 )*()*( it

n

r

ititr

q

ititqq

p

itpitl

k

itkitit GSKGSLGSKXyy

)9(

where

y = as earlier denoted.

X = as earlier denoted.

K = aggregate private capital inflows (KAI).

GS = 2x1 vector of surges to aggregate private capital inflows: positive surges and negative

surges to these flows KAI and KAI respectively. L =2x1 vector of capital controls on positive surges and negative surges respectively

KAIContrl and KAIContrl .

= error terms, as captured in the equations

To probe the effects of the capital flows on GDP, this study examines three main transmission

mechanisms: the investment, finance and trade (international competitiveness). Analyzing

these transmission mechanisms entails estimating the effects of the private capital inflows on

real capital formation (investment), credit to the private sector by the financial industry and

real effective exchange rate.

A simple accelerator model (equation 10) was specified as the baseline model for investment

transmission mechanism. This model was then extended to analyse the effects of the private

capital flows on investment in equation (11). Further extensions (equations 12 and 13) examine

the role of surges to these flows and effectiveness of relevant capital control measures in the

nexus between investment, private capital flows and related surges.

103

1

'1 it

k

itkitit PRCFRCF

)10(

113

1

3

1

'1 it

k

itl

k

itkitit ZPRCFRCF

)11(

14

126

1

'3

1

3

1

'1 it

p

itp

k

itl

k

itkitit SZPRCFRCF

)12(

136

1

'1

6

1

'3

1

3

1

'1 )*( it

q

ititq

p

itp

k

itl

k

itkitit SCSZPRCFRCF

)13(

where

RCF = real capital formation in percentage of GDP

P = 3x1 vector of explanatory variables which serve as control in subsequent capital

formation equations. These variables are change in the natural logarithm of real GDP,

real interest rate and domestic credit availed to the private sector.

= error terms, as captured in the equations

Others = as earlier defined.

The financial transmission mechanism is exploited by estimating equations 14-17 below, with

equation 14 being the baseline equation. Equations 15-17 are extensions where the effects of

capital flows, related surges and capital controls measures are respectively tested.

144

1

'1 itit

k

itkitit IQMDCRDCR

)14(

153

1

4

1

'1 it

k

itl

k

itkitit ZMDCRDCR

)15(

166

1

'3

1

4

1

'1 it

p

itp

k

itl

k

itkitit SZMDCRDCR

)16(

176

1

'1

6

1

'3

1

4

1

'1 )*( it

q

ititq

p

itp

k

itl

k

itkitit SCSZMDCRDCR

)17(

where

DCR = credit availed to the private sector in percentage of GDP

M = 4x1 vector of explanatory variables which serve as control in subsequent capital

formation equations. These variables are change in the natural logarithm of real

GDP, real interest rate and real capital formation and institutional quality. Both real

GDP real capital formation drive the demand for credit availed by the financial

sector. Real interest rate is the real price of credit (and serves as both demand and

supply factor). Institutional quality may also affect credit availed by the financial

sector as this variable affect the property right and other factors affecting credit

expansion.

= error terms, as captured in the equations

Others = as earlier defined.

A rearranged current account equation used in Alley (2016) to explain exchange rate in Nigeria

was extended, using the optimal current account deficit equation of Ghosh et al.’s (2014). This

extended equation (18) serves as the baseline model, and further extensions (equations 19-21)

were employed to capture the effects of capital flows, surges to these flows and capital flow

controls on the real effective exchange rate in the SSA countries.

189

1

'1 it

k

itkitit WREERREER

)18(

15

193

1

'9

1

'1 it

l

itl

k

itkitit ZWREERREER

)19(

206

1

'3

1

'9

1

'1 it

p

itp

l

itl

k

itkitit SZWREERREER

)20(

216

1

''6

1

'9

1

'1 )*( it

q

ititq

p

itp

k

itkitit SCSWREERREER

)21(

where:

REER = real effective exchange rate

W = 9x1 vector of explanatory variables which serve as control in subsequent growth

equations. These variables are natural logarithms of real GDP, real government

expenditures, real capital formation, change in terms of trade, trade openness and

trade partners’ growth rate.

= error terms, as captured in the equations

Others = as earlier defined.

The effectiveness of capital control measures in curtailing surges to private capital flows was

analysed using equations 22-25 below

nitititp

k

itkitit cxRxx

)*( '6

1

'1 )22(

where

x = each member of the vector S above.

R = 6x1 vector of explanatory variables which serve as control in subsequent growth

equations. These variables are real GDP growth rate, real interest rate institutional

qualities (all three being domestic variables) foreign interest rates, VIX and trade

partners growth rate (foreign variables).

Z = 3x1 vector of surges to private capital inflows in percentage of GDP: bond capital inflows,

equity capital, and direct investment, respectively.

c = each member of the vector C above that corresponds to x above

= error terms, as captured in the equations

4.2 Data

Data on relevant variables for 25 SSA countries from 2003 to 2013 were employed, based on

data availability. Data on private capital flows (bond capital, equity and direct) were collected

from the International Monetary Fund’s (IMF) International Financial Statistics (IFS) and

Balance of Payment (BoP) statistics databases. Surges to capital flows were calculated

following Benigno et al. (2015). This method is standard in determination and measurement of

surges in the literature on capital flows surges. Data on capital flows were scaled by the GDP

and detrended using the Hodrick-Prescott filter. The divergence between the detrended capital

flow series from one standard deviation represents the capital flows surges, which were then

sieved into the positive and the negative. Positive surges occur when the detrended series in

excess of one standard deviation of same series, while negative surges represents the magnitude

by which the detrended series fall short of one standard deviation.

Capital control variables were created for 14 SSA countries, in additions to 11 SSA countries

in our sample which Fernandez et al.’s (2015) dataset covers. The technical guidelines by

16

Fernandez et al. (2015) were followed in creating these capital control data17, using the

comprehensive Annual Report on Exchange Arrangements and Exchange Restrictions

(AREAER) by the IMF. Data on real gross domestic product (RGDP), government

expenditure, capital formation, terms of trade and RGDP of trade partners were obtained from

the World Bank’s database on World Development Indicators. These variables, with exception

of RGDP, terms of trade and RGDP of trade partners are scaled by the GDP, like the capital

flows. Real economic growth rate of the SSA countries and their trade partners and were

calculated as percentage growth of the RGDP. Change in terms of trade variable is calculated

as first difference of the variable.

Data on real growth rate of trade partners were calculated as trade weighted average of real

economic growth of the partners with which trade is a least five percent of total trade. Trade

weights were calculated as the percentage of the aggregated trade with the partners with which

trade is a least five percent of total trade. Data on real effective exchange rates and trade

volumes (used in calculating trade weights) were collected from the United Nations for

Cooperation on Trade Agreement’s (UNCTAD) database. Institutional quality variable used

are average of the five governance indicators from World Bank’s database on World

Governance Indicators, in line with Moody and Murshid (2005) and Keefer and Keefer (1995).

Data on VIX were collected from the Bloomberg and Chicago Board of Exchange (CBOE)

databases while data on total capital stock used in the stylized facts were collected from

Knoema database of which declared origin is the IMF database.

4.3 Estimation Techniques

Blanchard et al.’s (2016) growth equation and its extensions are naturally a dynamic panel,

subject to two sources of persistence over time: autocorrelation due to inclusions of lagged

values of the dependent variables in the list of regressors (endogeneity problem) and the

presence of individual effects characterising the heterogeneity of the panel (Baltagi, 2005). To

efficiently estimate the growth equations and other dynamic panel models in study, a System

Generalised Method of Moment (Sys.GMM) technique by Blundel and Bond (1998) was

deployed. This method outperforms other class of dynamic panel estimation techniques such

as first difference GMM by Arellano and Bond (1991) and Arellano and Bover (1995) in that

it not only instruments with lagged values of dependent variable due to its orthogonality with

the error components, like these other estimation techniques, it also instruments with lagged

differences of dependent variable. Justified by Ahn and Smith (1995) stationarity condition,

this additional instrumentation increases efficiency of the dynamic panel estimators, especially

when time period T is short and persistence (autoregressive coefficient) is large (close to

untity).

The smaller T period of panel used in this study appeals to the application of the SysGMM over

other methods, even both the restricted and the unrestricted vector autogressive (VAR) models.

The Sys.GMM also takes cares all endogeneity concerns that both the two/the three stage least

squares (2SLS/3SLS) address, but with a better advantage that it is more suitable for dynamic

panel estimation in terms of efficiency gains (Baltagi, 2005).

17 Categorical data (Yes/No for restriction/unrestricted transaction) on each of aggregate capital, FDI, equity and

bond were collected from AREAR and were coded 1/0 respectively. There are two inflow transactions for each

private capital: purchase locally by non-residents (pilbn) and sale or issue abroad by residents (siar). Categorical

data on these transactions are averaged for each of the FDI, equity and bond capital. For aggregate capital data,

the categorical data on transaction with FDI, equity and bond are averaged.

17

5. Preliminary Analyses

The statistical properties of the data are examined with a view to understanding their behaviour,

requirement for any possible transformation and making an appropriate choice of analytical

techniques for accurate estimation and reliable research findings. Since the time length of the

panels is small, the time series properties such as the unit roots and their cointegrational

properties are of little consequence and are not presented here18.

5.1 Descriptive Analyses and Statistics

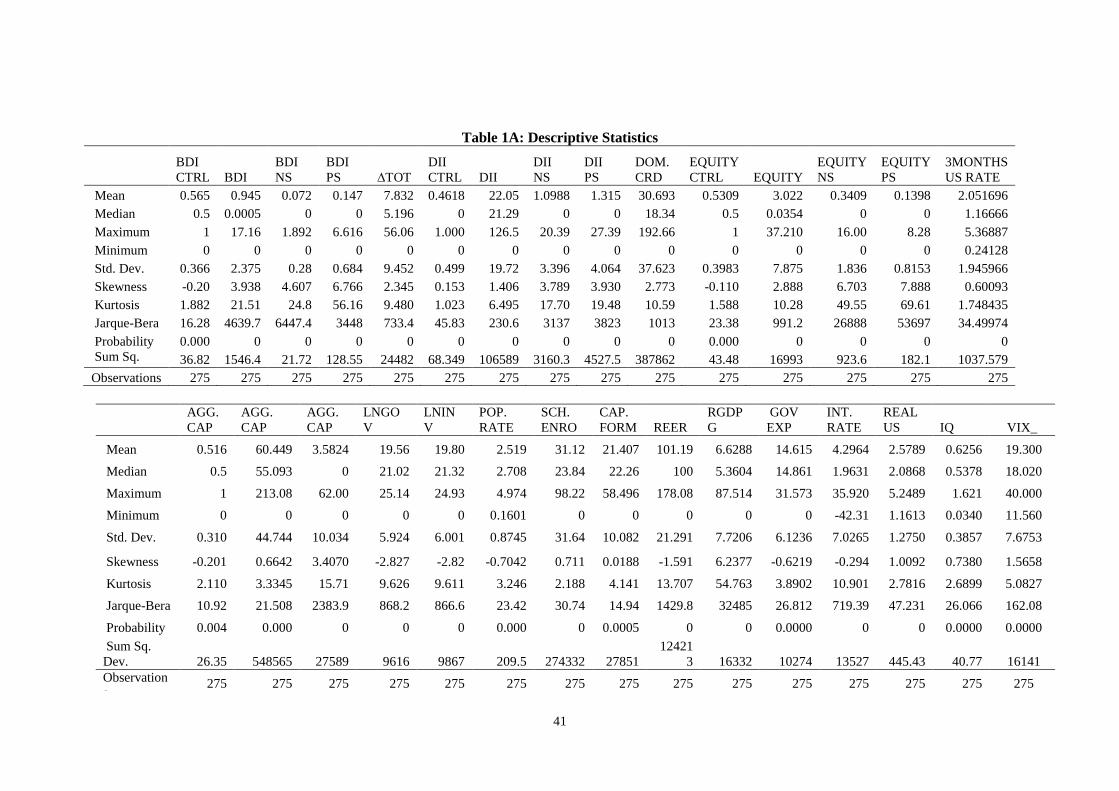

Table 1A in the appendix presents the descriptive statistics of the data. The skewness statistics

show that most of the series are positively skewed. This suggests that there are larger than

average countries in the sample, and this is reflected in the Jacque-Bera statistics which show

non-normal distribution. The Kurtosis statistics show that most of the series are platykurtic,

with exception of a few cases. This indicates that the countries are within a small range and are

fairly close to each other in terms of variables’ magnitude. Hence, the effects of non-normal

distribution on pooling for panel estimation are limited.

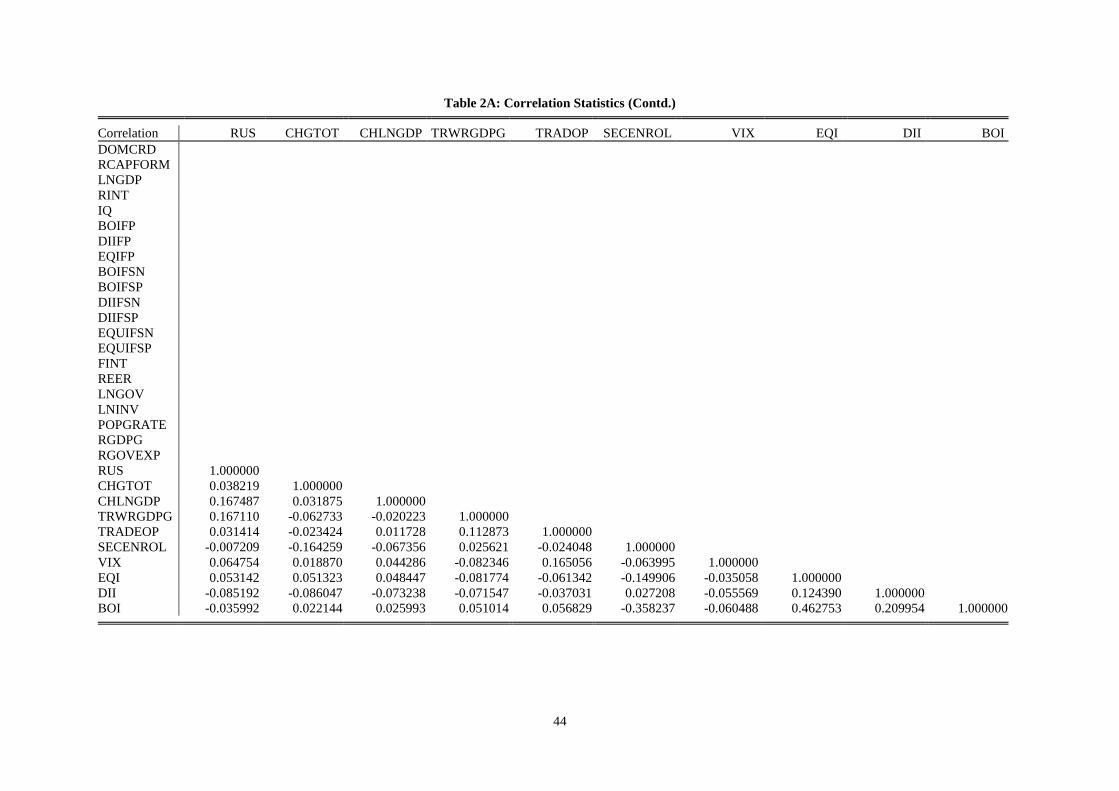

5.2 Correlation Analyses

Correlation matrix in table 2A of the appendix shows that most of the series are weakly

correlated. Some exceptions such as correlation between government expenditures and capital

formation are due to their own individual correlation with GDP. This is not a problem as these

three series feature simultaneously in equations 1-9 where GDP growth is the dependent

variable: the endogeneity resulting from the correlation of each of the government expenditures

and capital formation with GDP (growth) which underlies correlation between the two

explanatory series is taken care of by the estimation technique. Only bond capital and equity

are moderately correlated and this is due to both being portfolio capital. Neither of the two is

correlated with the FDI. Besides these very few exceptions, virtually all series are weakly

correlated. Hence, likelihood of multicollinearity problem is remote.

6. Empirical Evidence

Evidence on the effects of private capital flows on economic growth and related economic

indicators from a panel of 25 sub-Saharan Africa are presented and discussed in terms of their

economic implications and requirement for policy reactions. The results discussed relate to

various estimation scenarios: when the surges components of the private capital surges are

controlled for, when they are not, when the effects of capital control measures are taken into

consideration, and when not. These results emanate from GMM estimation of equations

specified in the preceding section. The estimations were such that the variances of the equations

are robust to many types of mis-specification. The Arellano-Bond test show that the error are

not correlated and the Sargan tests were not necessary (obtainable) once the variances are

robust. Section 6.1 provides empirical evidence of the growth nexus while sections 6.2, 6.3 and

6.4 highlight the dynamics on capital formation nexus, credit supply nexus, and exchange rate

nexus respectively. Evidence on the effects on capital controls on surges to capital flows is

presented in section 6.5.

18 They are however available and be supplied on request.

18

6.1 Private Capital Related Surges, Capital Controls and Economic Growth

Findings from the baseline regression (equation 1) in table 4 show that lags of real economic

growth rate and institutional quality significantly enhanced growth while capital formation did

not. These results are consistent with findings in Alley (2015) on the effects of lagged values

of economic growth, capital formation and institution quality on current economic growth.

Significance of lagged values of growth to current economic growth indicates persistence and

growth inertia in the region. The fundamentals supporting growth in the previous period still

remained effective in spurring current economic growth. Improvement in institution quality

coming from reduction in corruption, reduction in political instability and improvement in rule

of law, accountability and government effectiveness all bear positively on the region’s

economic growth. The negative effects of capital formation suggest low capital productivity or

poor allocation of investment resources. These results are consistent with findings in Korinek

(2014) and Blanchard et al. (2016). Equity capital had no significant effects.

These results suggest that the surge components of private capital dampened the effects of

private capital inflows on economic growth and explain why they do not have significant

effects in the growth equation 2. These two growth equations 2 and 3 may explain the reality

of the nexus between capital flows and economic growth in the SSA (as shown in figures 1A-

4A and 16A-19A in the appendix); that is, why the region has not really fared well despite large

inflows of private capital. The significance of determinants and other variables in the baseline

equation is preserved in all other growth equations.

All private capital flows - bond capital, equity capital and direct investment capital - had

insignificant effects on economic growth in equation 2 where the effects of surges components

to these flows were not controlled for. Once these surges were accounted for in growth equation

3, bond capital had significantly negative effects while direct investment capital had

significantly positive effects on economic growth.

19

Table 4: Inflows of Bond, Equity and Direct Investment and Real GDP Growth rate in SSA Dependent Variable: Real GDP growth rate (RGDPG)

Series 1 2 3 4 5

lag(RGDPG) 0.203***

(0.000)

0.198***

(0.000)

0.202***

(0.000)

0.187***

(0.000)

0.196***

(0.001)

School enrolment 0.008

(0.672)

0.011

(0.557)

0.001

(0.945)

0.004

(0.850)

0.006

(0.763)

Real govt. expenditure 0.052

(0.683)

0.046

(0.688)

0.049

(0.709)

0.026

(0.842)

0.036

(0.787)

Real capital formation -0.144**

(0.012)

-0.147**

(0.013)

-0.169***

(0.004)

-0.162***

(0.006)

-0.158***

(0.008)

Population growth 1.619

(0.123)

1.185*

(0.091)

2.351**

(0.041)

2.701**

(0.026)

2.805**

(0.019)

Institutional quality 17.738***

(0.000)

17.981***

(0.000)

14.352***

(0.000)

15.917***

(0.000)

15.507***

(0.000)

Change in terms of trade -0.058

(0.127)

-0.061

(0.112)

-0.057

(0.140)

-0.046

(0.266)

-0.044

(0.269)

Trade openness -0.000

(0.893)

-0.000

(0.890)

-0.000

(0.953)

0.000

(0.905)

0.000

(0.933)

Domestic credit -0.027

(0.588)

-0.019

(0.725)

-0.028

(0.591)

-0.021

(0.708)

-0.019

(0.708)

Trade Partners growth rate -0.098

(0.479)

-0.095

(0.499)

-0.131

(0.355)

-0.068

(0.642)

-0.085

(0.560)

Bond inflows (BDI)

-0.368

(0.246)

-1.567***

(0.001)

-1.346***

(0.006)

-1.510*

(0.066)

Equity inflows (EQI)

0.021

(0.844)

-0.079

(0.652)

-0.064

(0.732)

-0.060

(0.739)

Foreign Direct investment (FDI)

-0.007

(0.827)

0.129***

(0.003)

0.129***

(0.004)

0.127***

(0.004)

Positive shocks to BDI (BDI+)

1.580**

(0.018)

1.430

(0.388)

1.516**

(0.026)

Positive shocks to Equity inflows

(EQI+)

-0.181

(0.628)

-0.241

(0.706)

-0.284

(0.706)

Positive shocks to FDI (FDI+) -0.290***

(0.001)

-0.177

(0.117)

-0.166

(0.125)

Negative shocks to BDI 0.420

(0.709)

-0.714

(0.728)

0.493

(0.668)

Negative shocks to Equity inflows

(EQI+)

-0.556*

(0.099)

-1.199

(0.161)

-1.060

(0.208)

Negative shocks to FDI(FDI-)

0.137

(0.113)

0.090

(0.485)

0.090

(0.485)

BDI+ *Control BDI

-1.089

(0.971)

EQI+ *Control EQI

-0.006

(0.996)

DII+ *Control DDI

-0.216

(0.134)

-0.234*

(0.081)

BDI- *Control BDI

3.446

(0.474)

EQI-*Control EQI

0.819

(0.390)

0.648

(0.390)

DII+*Control FDI

0.076

(0.649)

BDI *Control BDI

0.114

(0.937)

Constant 6.173

(0.163)

6.630

(0.145)

-5.876

(0.227)

-8.475

(0.108)

-8.475

(0.108)

Wald Stat 174.57***

177.14***

207.59***

209.86***

207.73***

Arellano-Bond Test 1st Order

2nd Order

-1.215

-0.552

-1.483

-0.680

-1.392

-0.734

-1.526

-0.726

-1.502

-0.626

*, **, *** indicate 10%, 5% and 1% degree of statistical significance respectively, Control** = capital control on flow **

Source: Author’s computation

20

The significant effects of the bond capital and FDI on economic growth may be explained and

understood from two related perspectives: tenure and risk. Bond capital and equity capital are

short term flows while foreign direct investment is of much longer term. Bond capital is a debt

flow, sharing no risk in terms of dependence on states of economic performance. Equity capital

and direct investment capital are however risk-sharing flows whose performance in terms of

total return hinges on states of the economy. The short term riskless flow (bond capital)

negatively affects the economy while the long term risk-sharing flow (FDI) significantly

enhances growth. Equity capital belongs to both classes of flows; hence, the negative aspect of

the short terminal characteristics neutralises the positive effects of the risk-sharing capacities.

It thus has no significant effect on growth.

Positive and negative surges to inflows of private capital have divergent effects on economic

growth. Positive surges to foreign direct investment have negative effects. This may be

explained with the fact that foreign direct investment inflows are large relative to other inflows;

hence positive surges to this capital are correspondingly large and may not be effectively

absorbed and efficiently allocated to the best uses. The surge thus negatively affects on

economic growth. Positive surges to equity capital had no impact on economic growth, possibly

for reason that the regular flows had no significant effect as well. Negative surges to bond

capital and direct investment capital had no effects while negative surges to equity had negative

significant effects on the economy. Sharp declines in equity (denoted by negative surges) may

undermine the optimal finance mix of equity-financed business investments in the region and

this, in turn, negatively affects their profitability and hence economic performance.

When capital controls are selectively targeted at the surges (equation 5, table 4), surges to risk-

sharing capital no longer affect the economy. To this extent, the controls may be said to be

effective. However, the effects of regular flows seem not be affected by capital control. When

the controls are interacted with the flows (equation 5) they don’t change the impacts of the

regular flows on economic growth. Specifically, capital control did not change the negative

effects of bond flows on growth. This suggests that controls targeted at risk-sharing capital,

especially their surges, are more effective than those targeted at bond flows.

Findings on the effects of aggregate flows of capital on economic growth are presented in table

5 below. The effects and statistical significance of growth determinants in growth equations

testing the aggregate flows effects on growth are the same as in baseline equation, as they in

the growth equations involving individual components of private capital flows.

21

Table 5: Aggregate Private Capital Inflows and Real GDP Growth rate in SSA

Dependent Variable: Real GDP growth rate (RGDPG)

Series 1 6 7 8 9

lag(RGDPG) 0.203***

(0.000)

0.203***

(0.000)

0.189***

(0.000)

0.183***

(0.000)

0.188***

(0.001)

School enrolment 0.008

(0.672)

0.008

(0.663)

0.004

(0.828)

0.006

(0.770)

0.007

(0.725)

Real govt. expenditure 0.052

(0.683)

0.054

(0.670)

0.062

(0.627)

0.035

(0.785)

0.037

(0.776)

Real capital formation -0.144**

(0.012)

-0.146**

(0.011)

-0.149***

(0.010)

-0.131**

(0.025)

-0.132**

(0.023)

Population growth 1.619

(0.123)

1.664

(0.120)

1.074

(0.041)

1.198

(0.276)

1.177

(0.284)

Institutional quality 17.738***

(0.000)

17.884***

(0.000)

16.360***

(0.000)

16.984***

(0.000)

17.011***

(0.000)

Change in terms of trade -0.058

(0.127)

-0.067

(0.129)

-0.059

(0.154)

-0.052

(0.181)

-0.048

(0.209)

Trade openness -0.000

(0.893)

-0.000

(0.890)

-0.000

(0.789)

0.000

(0.813)

0.000

(0.805)

Domestic credit -0.027

(0.588)

-0.022

(0.684)

-0.051

(0.353)

-0.042

(0.443)

-0.045

(0.406)

Trade Partners growth rate -0.098

(0.479)

-0.097

(0.487)

-0.082

(0.560)

-0.066

(0.641)

-0.074

(0.142)

Aggregate capital inflows

(KAI)

-0.004

(0.758)

0.042**

(0.037)

0.037*

(0.062)

0.038*

(0.059)

Positive surges to KAI (KAI+)

-0.047

(0.164)

0.053

(0.414)

0.062

(0.437)

Negative surges to KAI (KAI-)

0.108***

(0.004)

0.054

(0.527)

0.102***

(0.007)

KAI + *Control KAI

-0.164

(0.178)

-0.181

(0.413)

KAI- *Control KAI

-0.077

(0.515)

Constant 6.173

(0.163)

6.321

(0.157)

-6.581

(0.143)

-6.748

(0.139)

-6.691

(0.142)

Wald Stat 174.57*** 177.14*** 182.07***

184.75*** 184.01***

Arellano-Bond Test 1st order

2nd order

-1.112

-0.331

-1.247

-0.422

-1.418

-0.490

-1.453

-0.503

-1.486

-0.456

*, **, *** indicate 10%, 5% and 1% degree of statistical significance respectively.

Source: Author’s computation

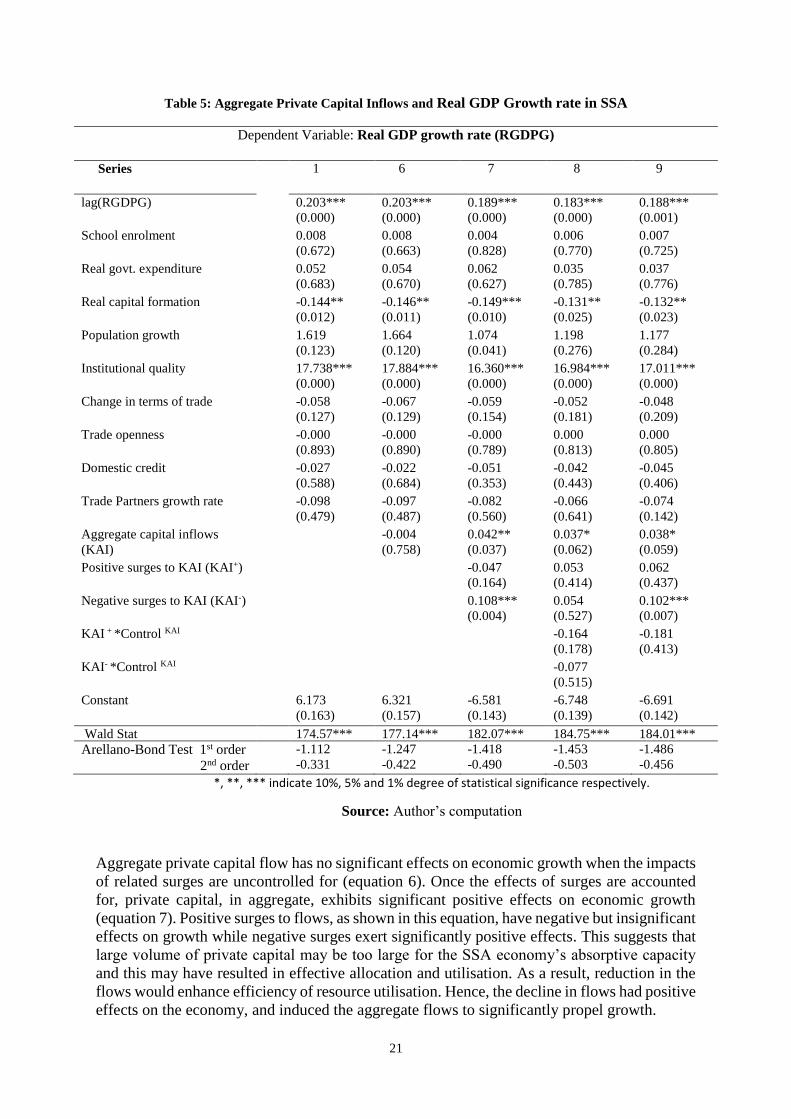

Aggregate private capital flow has no significant effects on economic growth when the impacts

of related surges are uncontrolled for (equation 6). Once the effects of surges are accounted

for, private capital, in aggregate, exhibits significant positive effects on economic growth

(equation 7). Positive surges to flows, as shown in this equation, have negative but insignificant

effects on growth while negative surges exert significantly positive effects. This suggests that

large volume of private capital may be too large for the SSA economy’s absorptive capacity

and this may have resulted in effective allocation and utilisation. As a result, reduction in the

flows would enhance efficiency of resource utilisation. Hence, the decline in flows had positive

effects on the economy, and induced the aggregate flows to significantly propel growth.

22

Since the surges to aggregate capital inflows have no significant negative effect on the

economy, there is less worry on the control. However, the insignificant negative effects of

positive surges turned positive with capital controls while the significant positive effects of

negative surges disappeared (equation 8). This means that unfiltered application of capital

control may not be efficient. When selectively applied to check positive surges alone (equation

9), the negative effects of positive surge in equation 7 turn positive while the positive effects

of negative surges to aggregate flows remain.

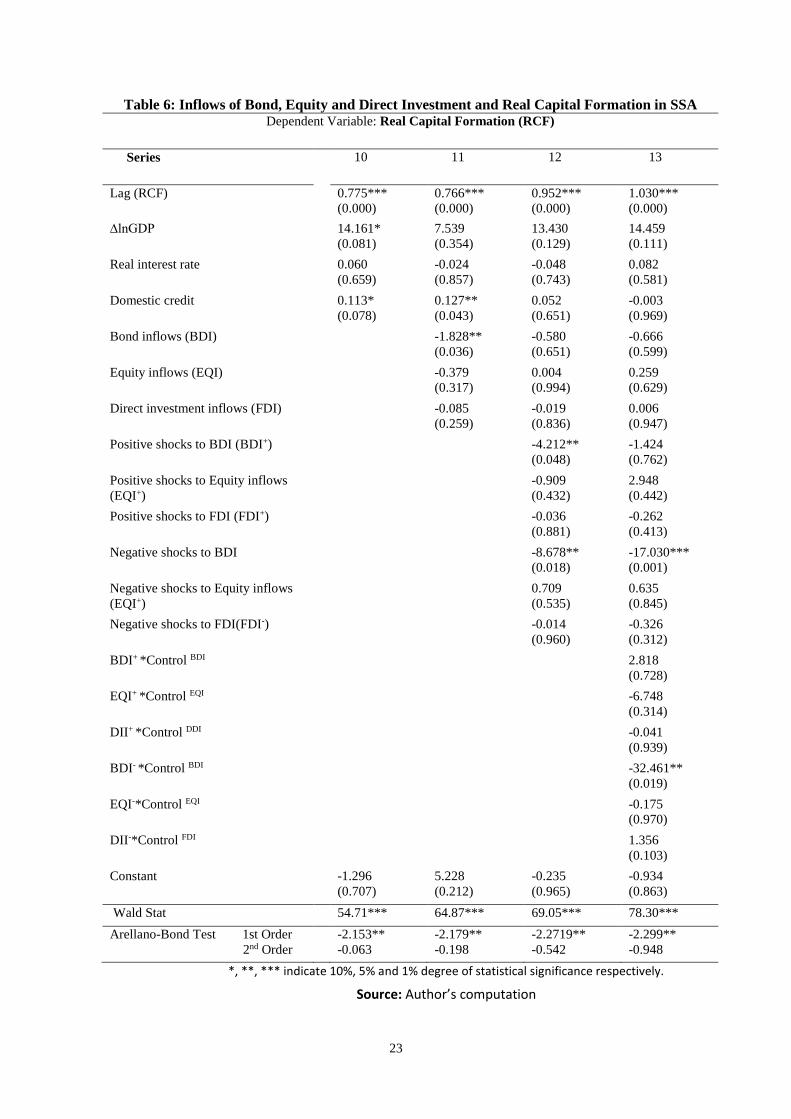

6.2 Private capital flows, related surges, capital controls and Capital Formation

To probe the effects of private capital flows on economic growth, three transmission

mechanisms or pathways were analysed: the capital formation link, the credit growth pathway

and international competitiveness mechanisms. Table 6 below presents the effects of private

flows on capital formation in the SSA.

Besides the persistence in real capita formation - suggesting that fundamental driving capital

formation in the last period are still effective in the current period - difference of natural log of

real GDP and domestic credit exert strongly significant positive effects on real capital

formation in the baseline equation. These results lend credence to the validity of the simple

accelerator model of investment in the SSA. Economic growth and supply of credits are shown

to be supportive for capital formation (investment). The effects of change in real GDP and

domestic credit fade in many other capital formation equations where the effects of private

capital flows are tested. This suggests that private capital flows exert powerful, perhaps

overriding, influence on capital formation.

Equity capital and foreign direct investment bear no significant effects on capital formation in

all the equations, whether or not the surges and capital control effects are accounted for. Bond

flows, on the other hand, had strong significant negative effects on capital formation when the

effects of surges were not controlled for (equation 11). The flow no longer had significant

negative effects on capital formation once the surges were controlled for (equation 12). Both

positive and negative surges to bond capital significantly detract from capital formation.

Capital control measures were only effective in curtailing the negative effects of positive

surges; they were not in case of negative surges (equation 13). This suggests that more controls

are needed against the negative surges of bond capital flows.

23

Table 6: Inflows of Bond, Equity and Direct Investment and Real Capital Formation in SSA Dependent Variable: Real Capital Formation (RCF)

Series 10 11 12 13

Lag (RCF) 0.775***

(0.000)

0.766***

(0.000)

0.952***

(0.000)

1.030***

(0.000)

∆lnGDP 14.161*

(0.081)

7.539

(0.354)

13.430

(0.129)

14.459

(0.111)

Real interest rate 0.060

(0.659)

-0.024

(0.857)

-0.048

(0.743)

0.082

(0.581)

Domestic credit 0.113*

(0.078)

0.127**

(0.043)

0.052

(0.651)

-0.003

(0.969)

Bond inflows (BDI) -1.828**

(0.036)

-0.580

(0.651)

-0.666

(0.599)

Equity inflows (EQI) -0.379

(0.317)

0.004

(0.994)

0.259

(0.629)

Direct investment inflows (FDI) -0.085

(0.259)

-0.019

(0.836)

0.006

(0.947)

Positive shocks to BDI (BDI+) -4.212**

(0.048)

-1.424

(0.762)

Positive shocks to Equity inflows

(EQI+)

-0.909

(0.432)

2.948

(0.442)

Positive shocks to FDI (FDI+) -0.036

(0.881)

-0.262

(0.413)

Negative shocks to BDI

-8.678**

(0.018)

-17.030***

(0.001)

Negative shocks to Equity inflows

(EQI+)

0.709

(0.535)

0.635

(0.845)

Negative shocks to FDI(FDI-)

-0.014

(0.960)

-0.326

(0.312)

BDI+ *Control BDI

2.818

(0.728)

EQI+ *Control EQI

-6.748

(0.314)

DII+ *Control DDI

-0.041

(0.939)

BDI- *Control BDI

-32.461**

(0.019)

EQI-*Control EQI

-0.175

(0.970)

DII-*Control FDI

1.356

(0.103)

Constant -1.296

(0.707)

5.228

(0.212)

-0.235

(0.965)

-0.934

(0.863)

Wald Stat 54.71***

64.87***

69.05***

78.30***

Arellano-Bond Test 1st Order

2nd Order

-2.153**

-0.063

-2.179**

-0.198

-2.2719**

-0.542

-2.299**

-0.948

*, **, *** indicate 10%, 5% and 1% degree of statistical significance respectively.

Source: Author’s computation

24

6.3 Private capital flows, related surges, capital controls and Domestic Credit

Evidence on the effects of determinants of domestic credit supply in the SSA in presented in

table 7 below. The previous value of domestic credit and interest rate are significant in all the

credit equation including the baseline, and these results show that credit formation was

persistent due to the enduring fundamentals and that price of capital (payment on borrowing)

was a critical supply factor in the credit supply nexus.

Table 7: Inflows of Bond, Equity and Direct Investment and Domestic Credit in SSA

Dependent Variable: Domestic Credit (DCRD)

Series 14 15 16 17

Lag (DCRD ) 1.101***

(0.000)

0.930***

(0.000)

0.985***

(0.000)

0.996***

(0.000)

Real capital formation -0.019

(0.799)

0.024

(0.731)

0.013

(0.843)

0.003

(0.953)

∆lnGDP 1.660*

(0.082)

-1.192

(0.220)

-1.124

(0.224)

-1.636*

(0.2069)

Real interest rate 0.291***

(0.000)

0.311***

(0.000)

0.292***

(0.000)

0.291***

(0.000)

Institutional quality -9.761

(0.129)

-11.050*

(0.067)

-8.893

(0.110)

-8.548

(0.118)

Bond inflows (BDI) -0.179

(0.646)

-0.662

(0.201)

-0.876*

(0.079)

Equity inflows (EQI) 0.526**

(0.011)

0.514**

(0.029)

0.445**

(0.051)

Foreign Direct investment (FDI) 0.026

(0.612)

0.014

(0.806)

0.050

(0.345)

Positive shocks to BDI (BDI+) 1.573

(0.154)

1.794

(0.525)

Positive shocks to Equity inflows (EQI+) -2.057***

(0.001)

0.065

(0.974)

Positive shocks to FDI (FDI+)

-0.233

(0.106)

-0.123

(0.488)

Negative shocks to BDI

0.468

(0.814)

3.613

(0.168)

Negative shocks to Equity inflows

(EQI+)

-2.714***

(0.188)

-6.446***

(0.000)

Negative shocks to FDI(FDI-)

0.229

(0.188)

0.026

(0.883)

BDI+ *Control BDI

2.593

(0.266)

EQI+ *Control EQI

-4.114

(0.252)

DII+ *Control DDI

-0.249

(0.401)

BDI- *Control BDI

-9.609

(0.196)

EQI-*Control EQI

6.292**

(0.011)

DII-*Control FDI

-0.207

(0.657)

Constant -34.02

(0.106)

-21.33

(0.319)

-21.68

(0.300)

-35.33*

(0.084)

Wald Stat 2640.95***

(0.000)

3086.79***

(0.000)

3701.67***

(0.000)

4154.74***

(0.000) Arellano-Bond Test 1st Order

2nd Order

-2.114**

-0.709

-2.670***

-0.735

-2.927***

0.747

-2.929***

1.024

*, **, *** indicate 10%, 5% and 1% degree of statistical significance respectively.

Source: Author’s computation

25

Only equity capital had positive and significant effects on domestic credits in all the relevant

credit equations, whether or not the effects of surges and capital controls were controlled for

(equations 15 and 16). Other private capital flows play no significant roles in all the domestic

credit equations except in equation (17) where bond flows had significant negative effect.

These results are consistent with Blanchard et al. (2016) who find that bond flows did not

significantly affect credit formation. In contrast, they find that portfolio equity had insignificant

effects. While we find that FDI did not significantly affect credit formation, Blanchard et al.

(2016) finds that it negatively affects credit supply, with an explanation that some of the

intermediation which would have taken place through banks is now replaced by FDI financing.

The short term nature and the risk-sharing capacity of equity flows may have made the flows

amenable to lending. Compared to bond flow, it is more stable due to risk-sharing nature; and

compared to direct investment, it is of shorter term in nature. Moreover, equity capital flows

through the stock exchange market and end up in banking system as deposit, unlike the direct

investment flows which are expeditiously used up in some business directly by its foreign

owners. These make equity flows more amenable for lending and credit supply.

Both positive and negative surges to equity negatively affect credit supply, and this suggests

that the banking system are not sophisticated enough to handle the surges. While the negative

effects of negative surges to the flows on credit could be explained in terms of supply effects,

the negative effects of positive surges may be due to balance sheet pressure, leading to poor

credit, risk asses losses and reactive caution on credit expansion. With capital controls in place,

the negative effects of the positive surges disappear but those of the negative surges did not:

the negative effects of negative surges to equity capital were so large that capital controls could

not wipe them out completely.

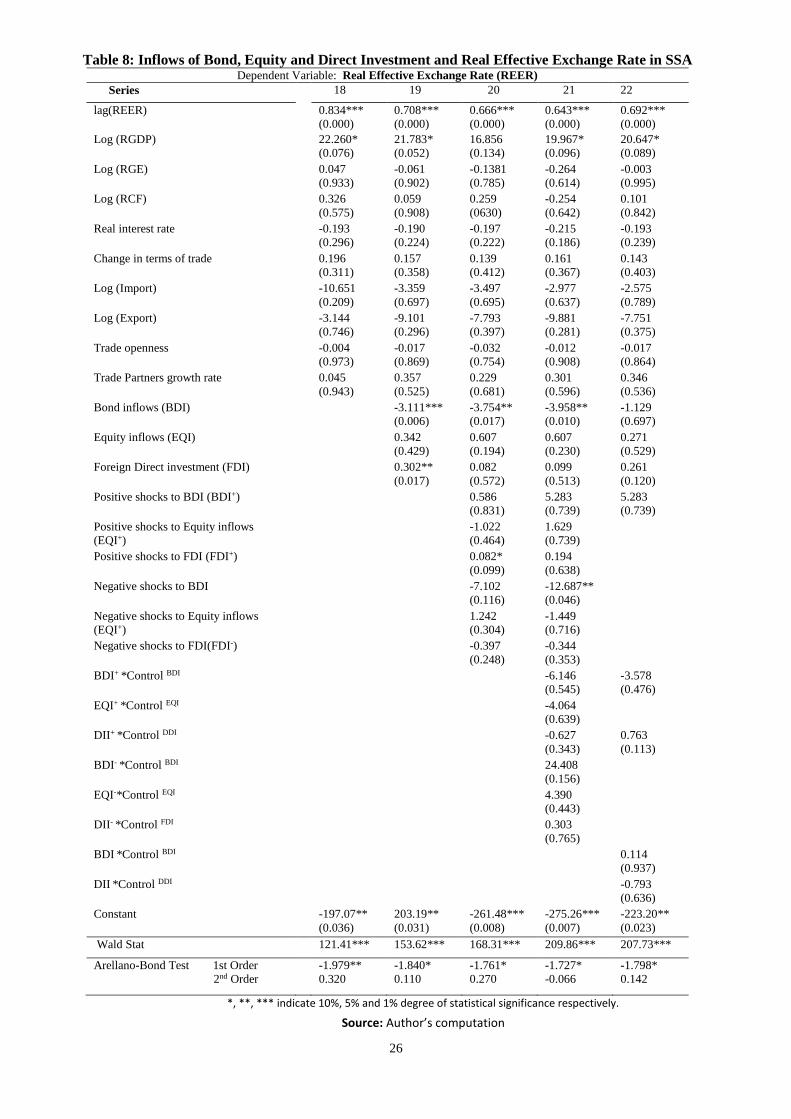

6.4 Private capital flows, related surges, capital controls and real effective exchange

rate

Apart from the previous values of the real exchange rate, only real GDP had positive effects

on real exchange rate in the baseline equation (18). Given the definition of exchange rate as

the trade weighted average price of foreign currency (of trade partners) in domestic currency

in real terms, a positive coefficient denotes that an explanatory variable leads to currency

depreciation while a negative coefficient indicates currency appreciation. The currency

depreciation effects of real GDP can be explained in terms of income effects on import, its

effect on current account balance, and implication for relatively higher demand for foreign

currency; hence, domestic currency depreciates relative to the foreign currencies as real GDP

rises. The effects of real GDP remain significant in all the equations except equation 20. Bond

capital inflows have significant negative effects, showing that real exchange rate significantly

appreciates with inflows of bond capital (equation 19). These effects endured whether or not

surges to these flows were controlled for: bond inflows led to appreciation of domestic currency

when surges were controlled for (equation 20) and when the roles of capital control measures

were accounted for (equation 21). The currency appreciation effect of the bond inflows is

explicable in terms of the financial flows effects (relative currency demand) leading to nominal

exchange rate appreciation, real sector effects and the engendered inflation effects.

26

Table 8: Inflows of Bond, Equity and Direct Investment and Real Effective Exchange Rate in SSA Dependent Variable: Real Effective Exchange Rate (REER)

Series 18 19 20 21 22

lag(REER) 0.834***

(0.000)

0.708***

(0.000)

0.666***

(0.000)

0.643***

(0.000)

0.692***

(0.000)

Log (RGDP) 22.260*

(0.076)

21.783*

(0.052)

16.856

(0.134)

19.967*

(0.096)

20.647*

(0.089)

Log (RGE) 0.047

(0.933)

-0.061

(0.902)

-0.1381

(0.785)

-0.264

(0.614)

-0.003

(0.995)

Log (RCF) 0.326

(0.575)

0.059

(0.908)

0.259

(0630)

-0.254

(0.642)

0.101

(0.842)

Real interest rate -0.193

(0.296)

-0.190

(0.224)

-0.197

(0.222)

-0.215

(0.186)

-0.193

(0.239)

Change in terms of trade 0.196

(0.311)

0.157

(0.358)

0.139

(0.412)

0.161

(0.367)

0.143

(0.403)

Log (Import) -10.651

(0.209)

-3.359

(0.697)

-3.497

(0.695)

-2.977

(0.637)

-2.575

(0.789)

Log (Export) -3.144

(0.746)

-9.101

(0.296)

-7.793

(0.397)

-9.881

(0.281)

-7.751

(0.375)

Trade openness -0.004

(0.973)

-0.017

(0.869)

-0.032

(0.754)

-0.012

(0.908)

-0.017

(0.864)

Trade Partners growth rate 0.045

(0.943)

0.357

(0.525)

0.229

(0.681)

0.301

(0.596)

0.346

(0.536)

Bond inflows (BDI)

-3.111***

(0.006)

-3.754**

(0.017)

-3.958**

(0.010)

-1.129

(0.697)

Equity inflows (EQI)

0.342

(0.429)

0.607

(0.194)

0.607

(0.230)

0.271

(0.529)

Foreign Direct investment (FDI)

0.302**

(0.017)

0.082

(0.572)

0.099

(0.513)

0.261

(0.120)

Positive shocks to BDI (BDI+)

0.586

(0.831)

5.283

(0.739)

5.283

(0.739)

Positive shocks to Equity inflows

(EQI+)

-1.022

(0.464)

1.629

(0.739)

Positive shocks to FDI (FDI+) 0.082*

(0.099)

0.194

(0.638)

Negative shocks to BDI -7.102

(0.116)

-12.687**

(0.046)

Negative shocks to Equity inflows

(EQI+)