Embed Size (px)

Citation preview

HAZARDOUS TO YOUR WEALTH:SIX MISTAKES CANADIANS MAKE WITH THEIR FINANCES

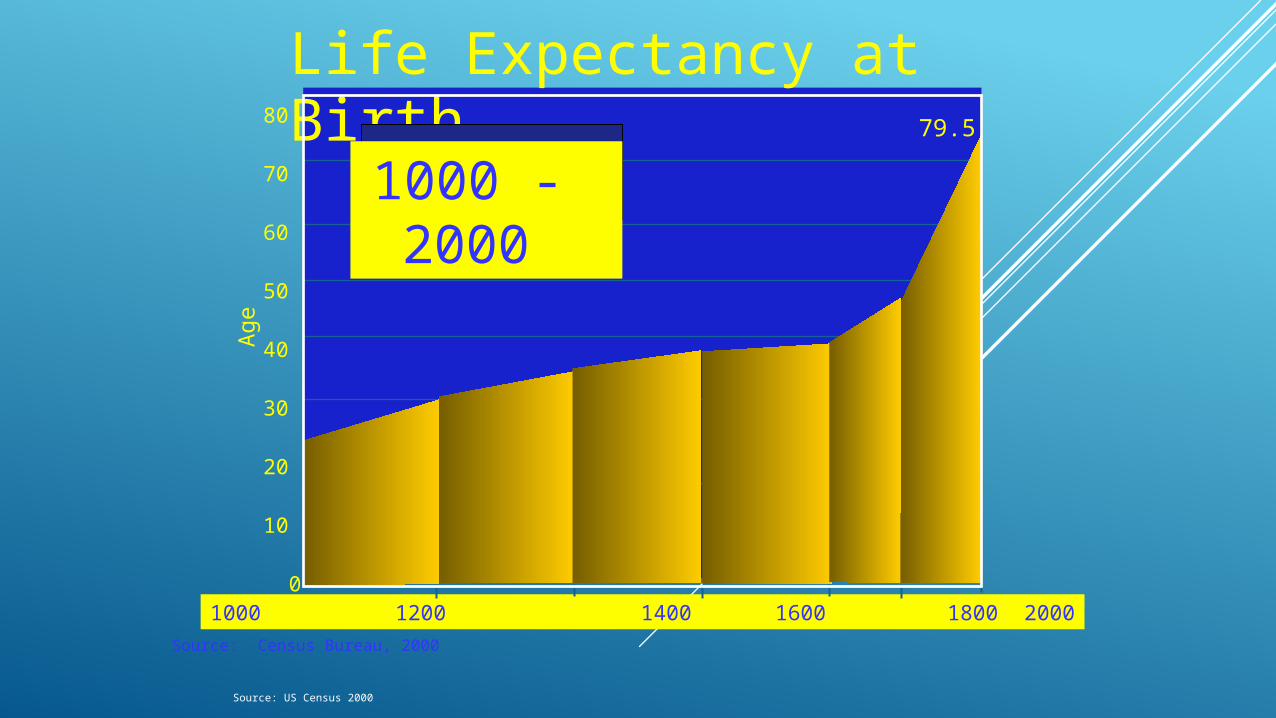

Life Expectancy at Birth79.5

Age

1000 1200 1400 1600 1800 2000

80

70

60

50

40

30

20

10

0

1000 - 2000

Source: Census Bureau, 2000

Source: US Census 2000

If clients can’t imagine living past age 100, tell them more than 50,000 people across North America already have, says Dan Anders.

What’s more, the number of centenarians (people aged 100 and older) in Canada is rising. Statistics Canada says that cohort grew 25.7% between 2006 and 2011 (the number of people aged 60 to 64 grew 29.1%). It’s also been one of the fastest-growing segments for nearly 40 years

Centenarians

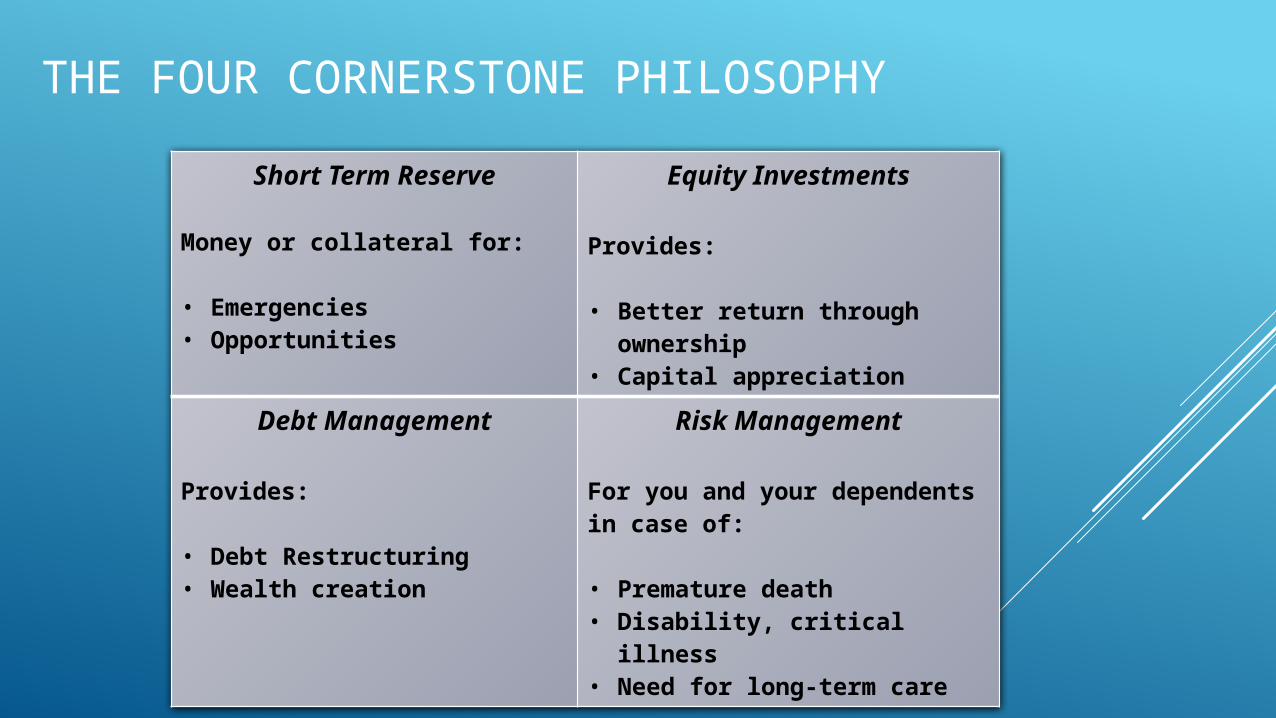

THE FOUR CORNERSTONE PHILOSOPHY

Short Term Reserve

Money or collateral for:

• Emergencies• Opportunities

Equity Investments

Provides:

• Better return through ownership

• Capital appreciation

Debt Management

Provides:

• Debt Restructuring• Wealth creation

Risk Management

For you and your dependents in case of:

• Premature death• Disability, critical illness• Need for long-term care

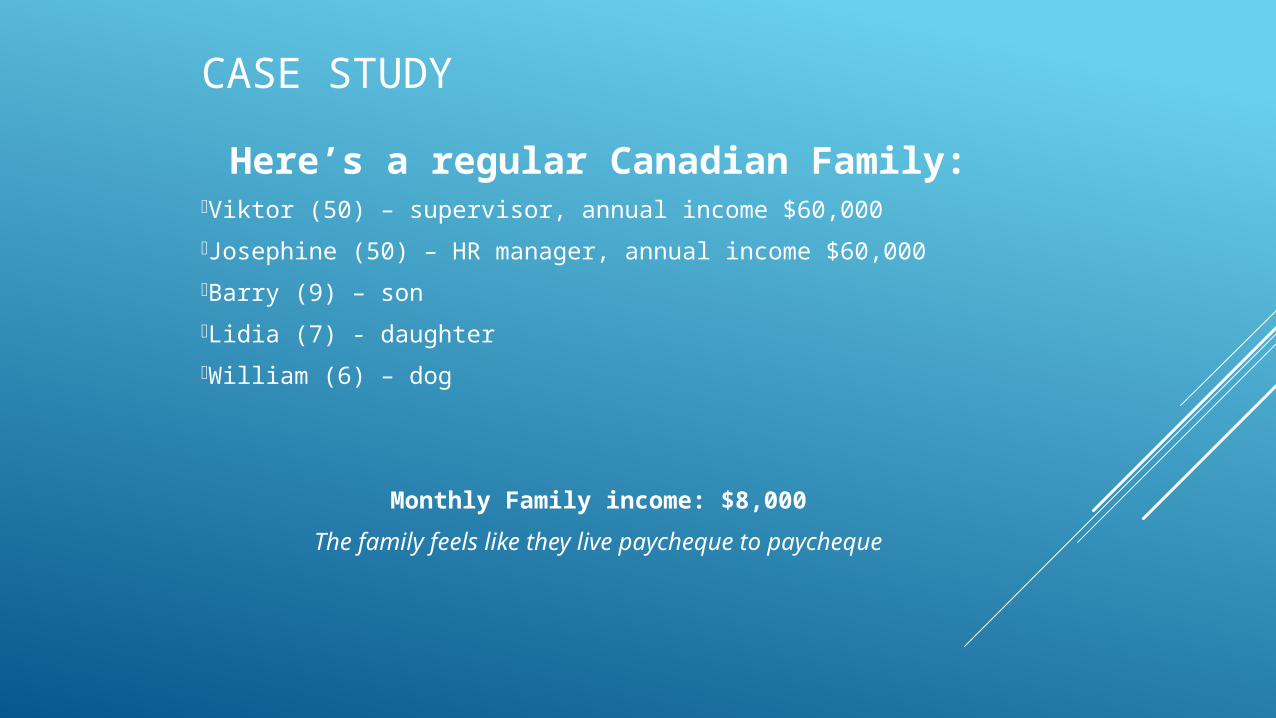

CASE STUDY

Here’s a regular Canadian Family:Viktor (50) – supervisor, annual income $60,000

Josephine (50) – HR manager, annual income $60,000

Barry (9) – son

Lidia (7) - daughter

William (6) – dog

Monthly Family income: $8,000

The family feels like they live paycheque to paycheque

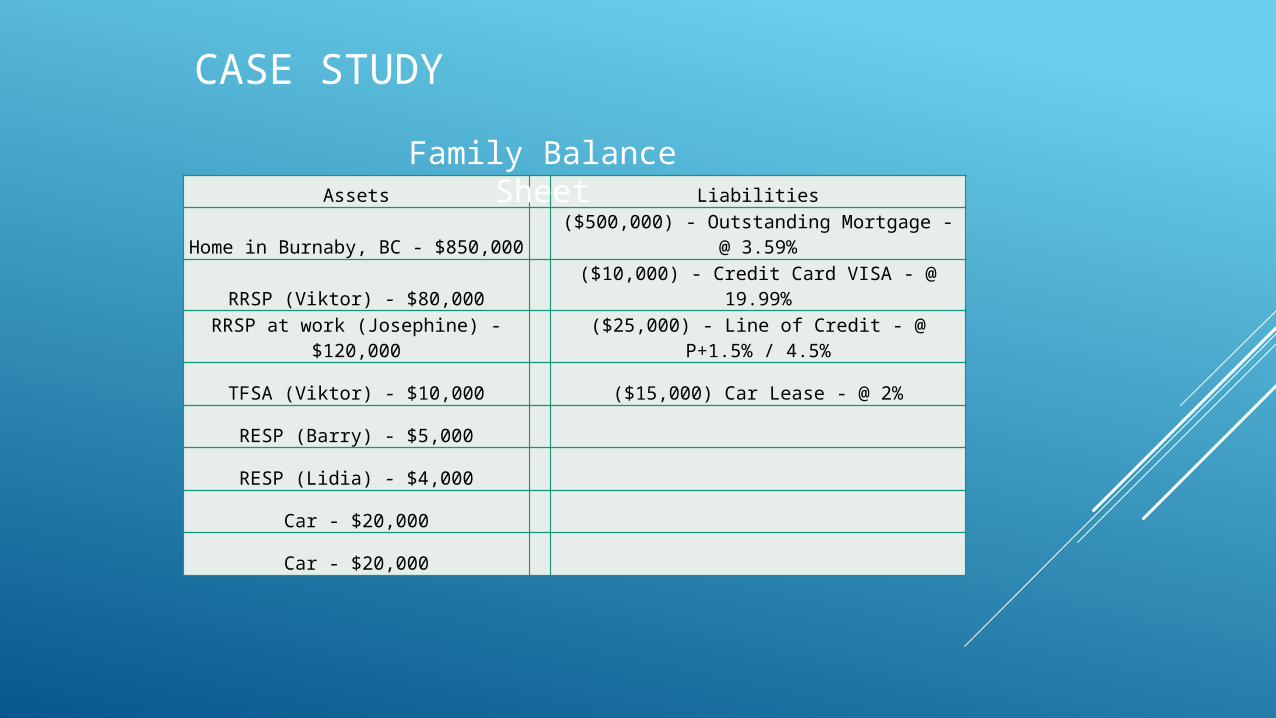

Assets Liabilities

Home in Burnaby, BC - $850,000($500,000) - Outstanding Mortgage - @

3.59%

RRSP (Viktor) - $80,000 ($10,000) - Credit Card VISA - @ 19.99%

RRSP at work (Josephine) - $120,000($25,000) - Line of Credit - @ P+1.5% /

4.5%

TFSA (Viktor) - $10,000 ($15,000) Car Lease - @ 2%

RESP (Barry) - $5,000

RESP (Lidia) - $4,000

Car - $20,000

Car - $20,000

CASE STUDY

Family Balance Sheet

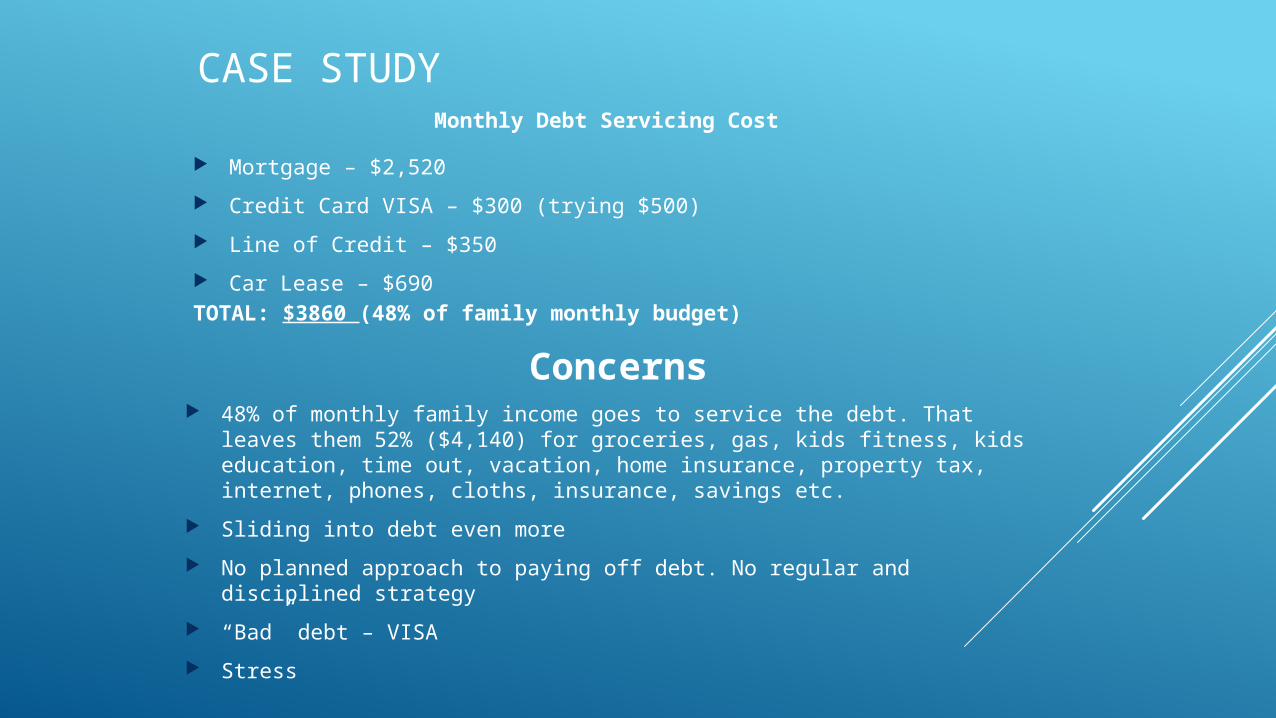

CASE STUDYMonthly Debt Servicing Cost

Mortgage – $2,520

Credit Card VISA – $300 (trying $500)

Line of Credit – $350

Car Lease – $690TOTAL: $3860 (48% of family monthly budget)

Concerns 48% of monthly family income goes to service the debt. That leaves them

52% ($4,140) for groceries, gas, kids fitness, kids education, time out, vacation, home insurance, property tax, internet, phones, cloths, insurance, savings etc.

Sliding into debt even more

No planned approach to paying off debt. No regular and disciplined strategy

“Bad” debt – VISA

Stress

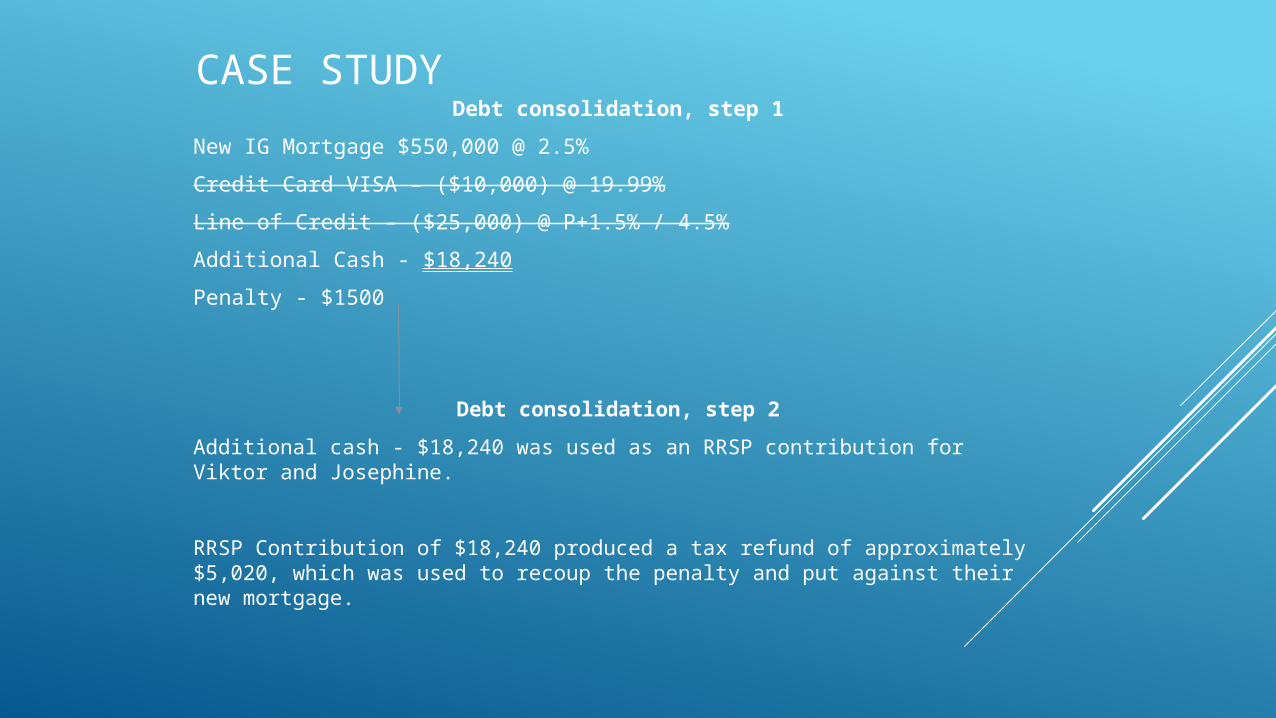

CASE STUDYDebt consolidation, step 1

New IG Mortgage $550,000 @ 2.5%

Credit Card VISA – ($10,000) @ 19.99%

Line of Credit – ($25,000) @ P+1.5% / 4.5%

Additional Cash - $18,240

Penalty - $1500

Debt consolidation, step 2

Additional cash - $18,240 was used as an RRSP contribution for Viktor and Josephine.

RRSP Contribution of $18,240 produced a tax refund of approximately $5,020, which was used to recoup the penalty and put against their new mortgage.

CASE STUDY

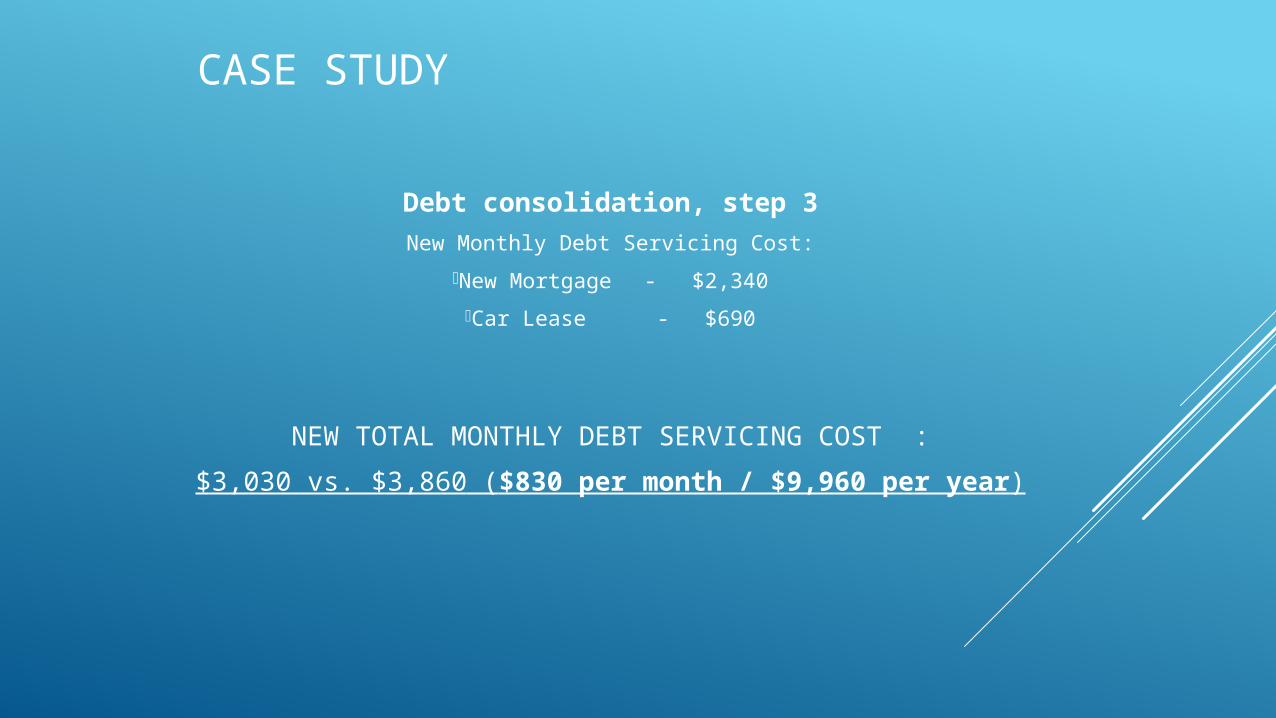

Debt consolidation, step 3

New Monthly Debt Servicing Cost:

New Mortgage - $2,340

Car Lease - $690

NEW TOTAL MONTHLY DEBT SERVICING COST :

$3,030 vs. $3,860 ($830 per month / $9,960 per year)

CASE STUDY

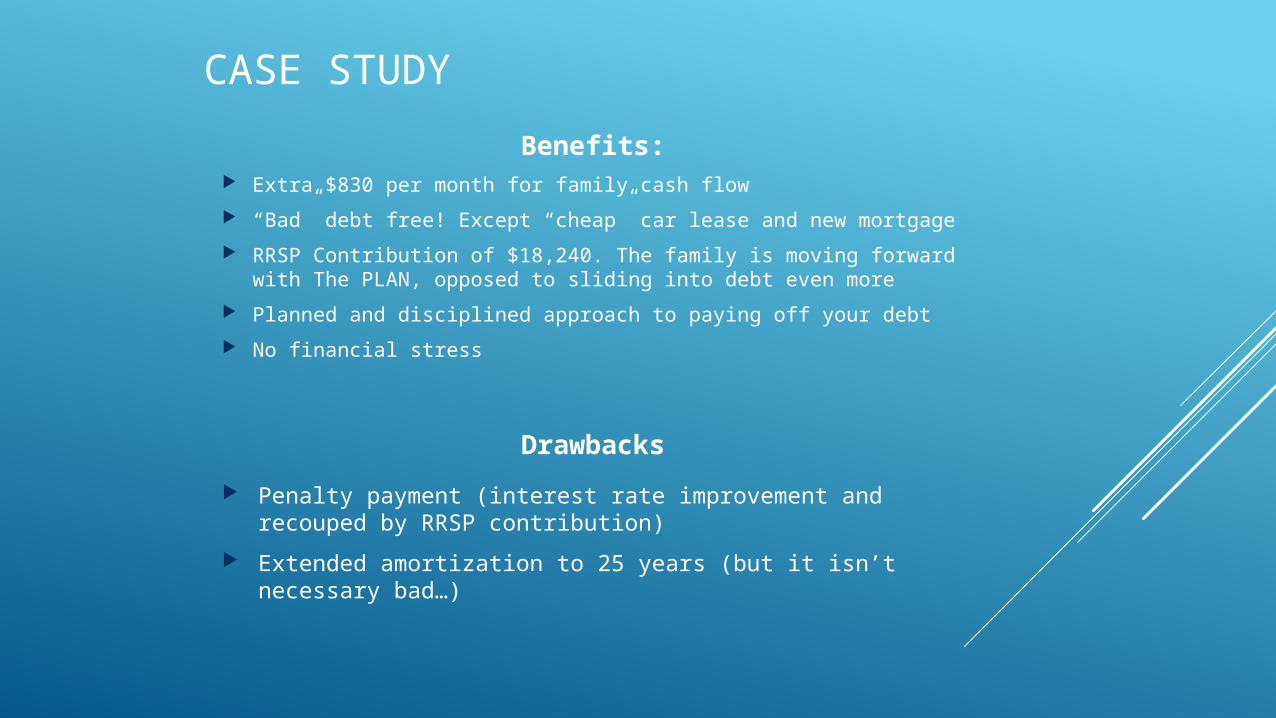

Drawbacks

Penalty payment (interest rate improvement and recouped by RRSP contribution)

Extended amortization to 25 years (but it isn’t necessary bad…)

Benefits: Extra $830 per month for family cash flow

“Bad” debt free! Except “cheap” car lease and new mortgage

RRSP Contribution of $18,240. The family is moving forward with The PLAN, opposed to sliding into debt even more

Planned and disciplined approach to paying off your debt

No financial stress

YOU NEED A PLAN

FINANCIAL ISSUES ARE COMPLEX

YOU NEED TO WORK WITH A PROFESSIONAL

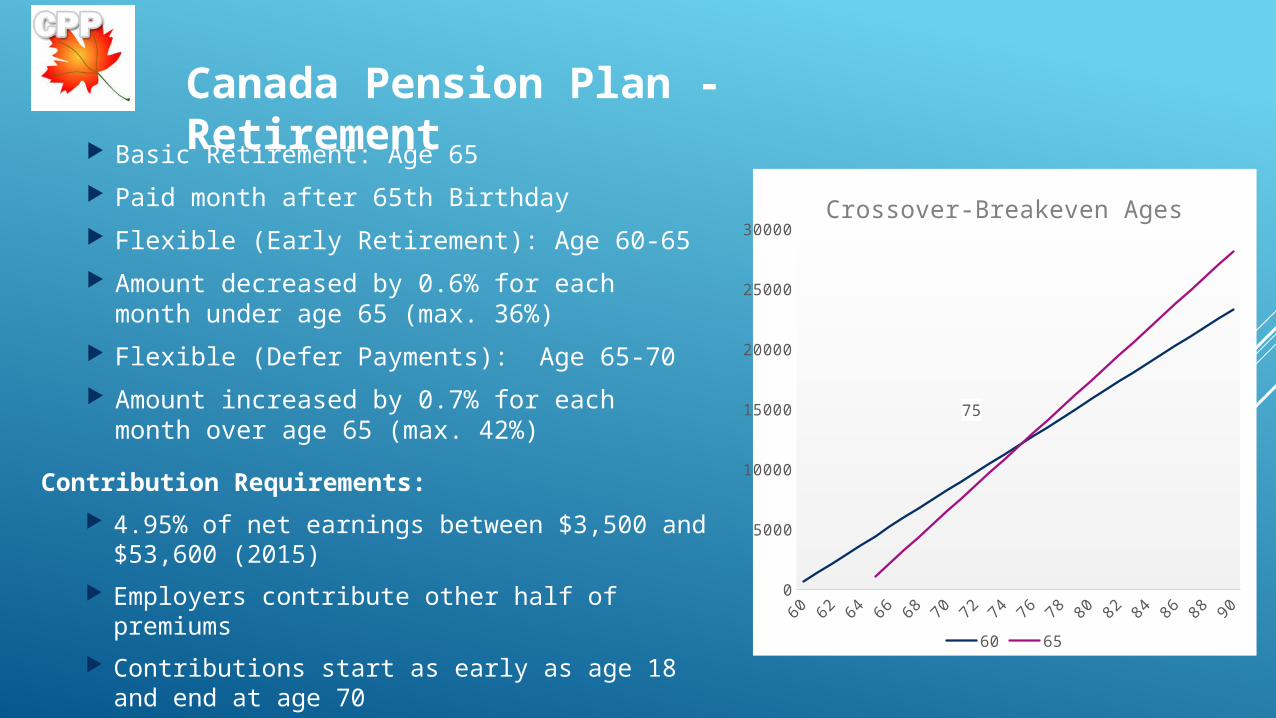

Basic Retirement: Age 65

Paid month after 65th Birthday

Flexible (Early Retirement): Age 60-65

Amount decreased by 0.6% for each month under age 65 (max. 36%)

Flexible (Defer Payments): Age 65-70

Amount increased by 0.7% for each month over age 65 (max. 42%)

Canada Pension Plan - Retirement

0

5000

10000

15000

20000

25000

30000

75

Crossover-Breakeven Ages

60 65

Contribution Requirements:

4.95% of net earnings between $3,500 and $53,600 (2015)

Employers contribute other half of premiums

Contributions start as early as age 18 and end at age 70

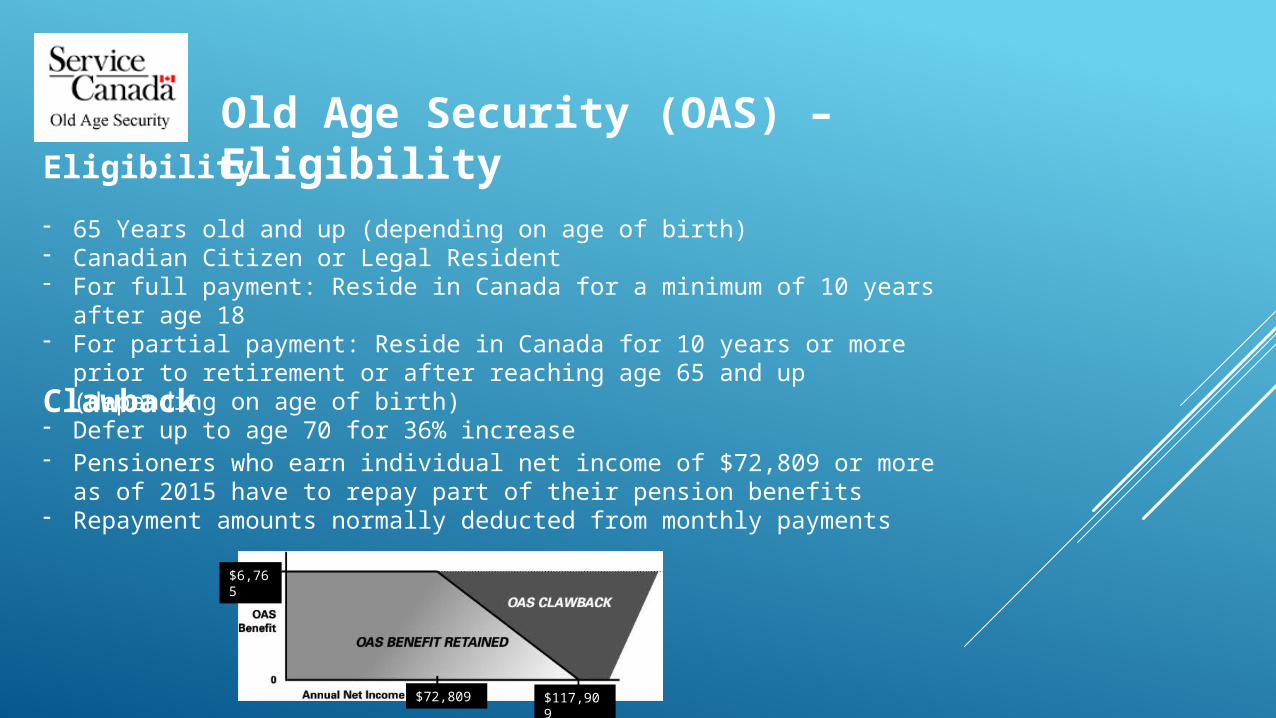

Old Age Security (OAS) – EligibilityEligibility

- 65 Years old and up (depending on age of birth) - Canadian Citizen or Legal Resident- For full payment: Reside in Canada for a minimum of 10 years after age

18- For partial payment: Reside in Canada for 10 years or more prior to

retirement or after reaching age 65 and up (depending on age of birth)- Defer up to age 70 for 36% increase Clawback

- Pensioners who earn individual net income of $72,809 or more as of 2015 have to repay part of their pension benefits

- Repayment amounts normally deducted from monthly payments

$72,809 $117,909

$6,765

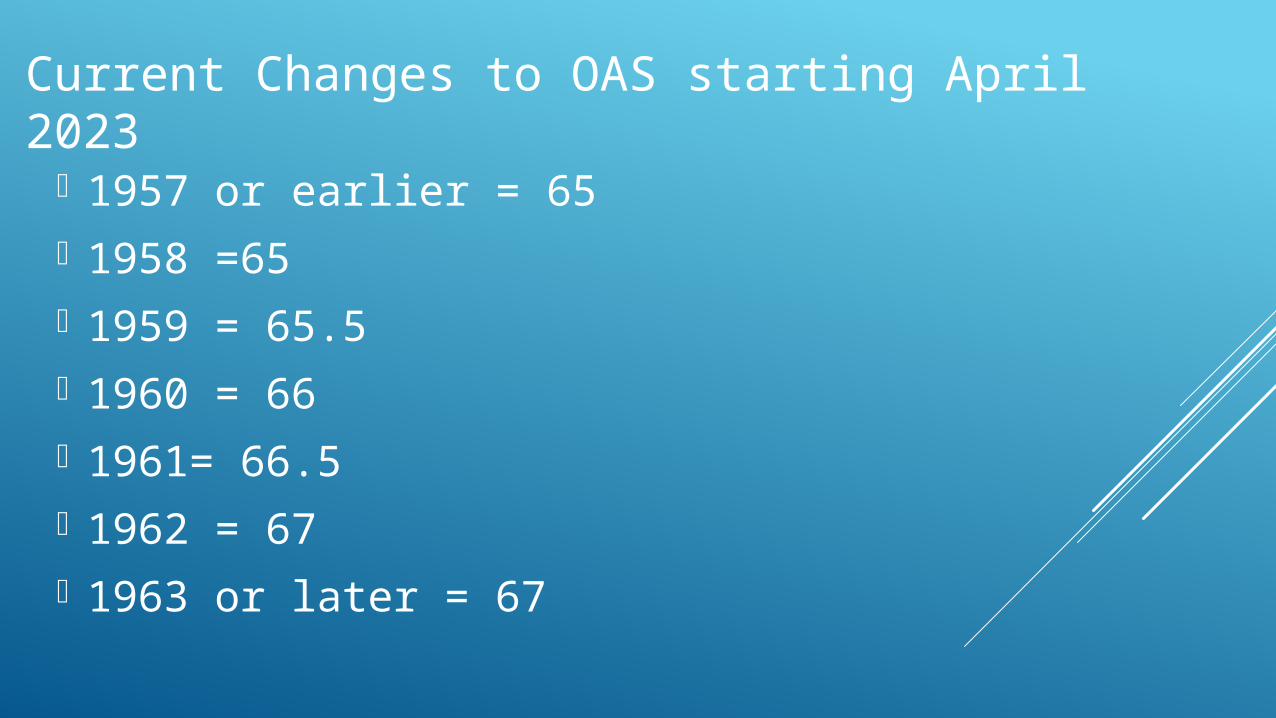

1957 or earlier = 65 1958 =65 1959 = 65.5 1960 = 66 1961= 66.5 1962 = 67 1963 or later = 67

Current Changes to OAS starting April 2023

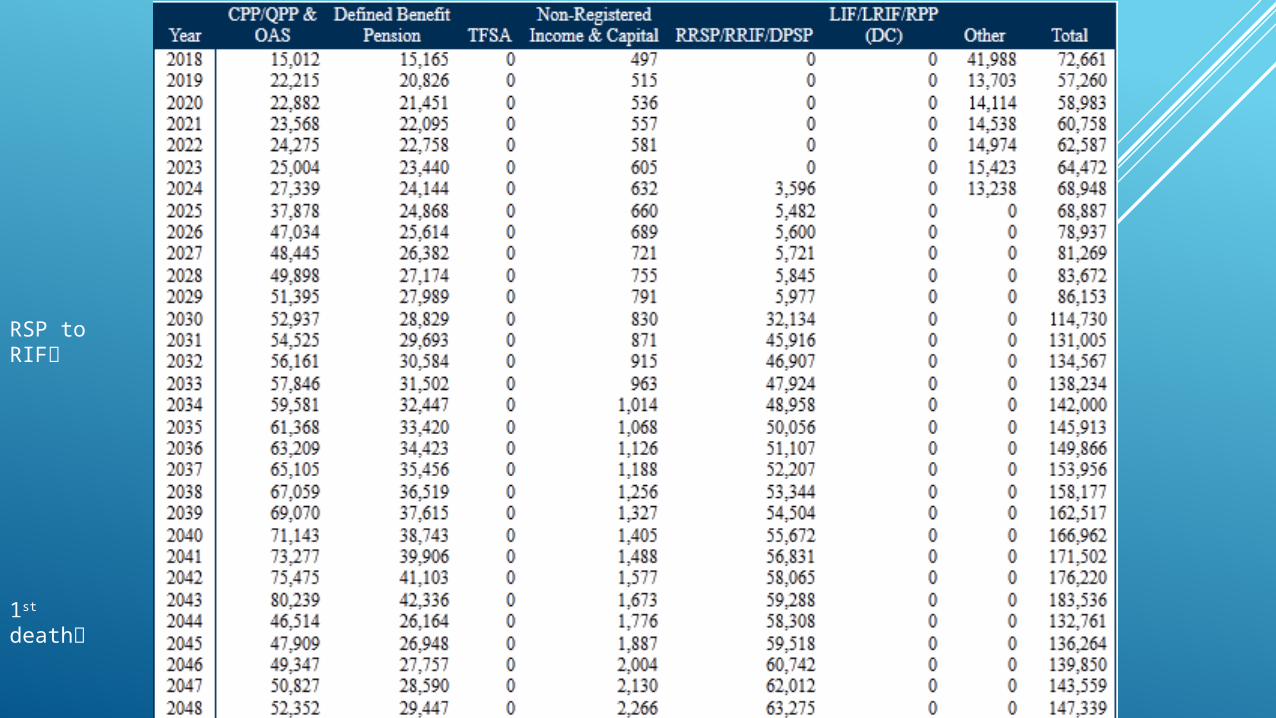

Retirement Paycheque

RSP to RIF

1st death

2nd death

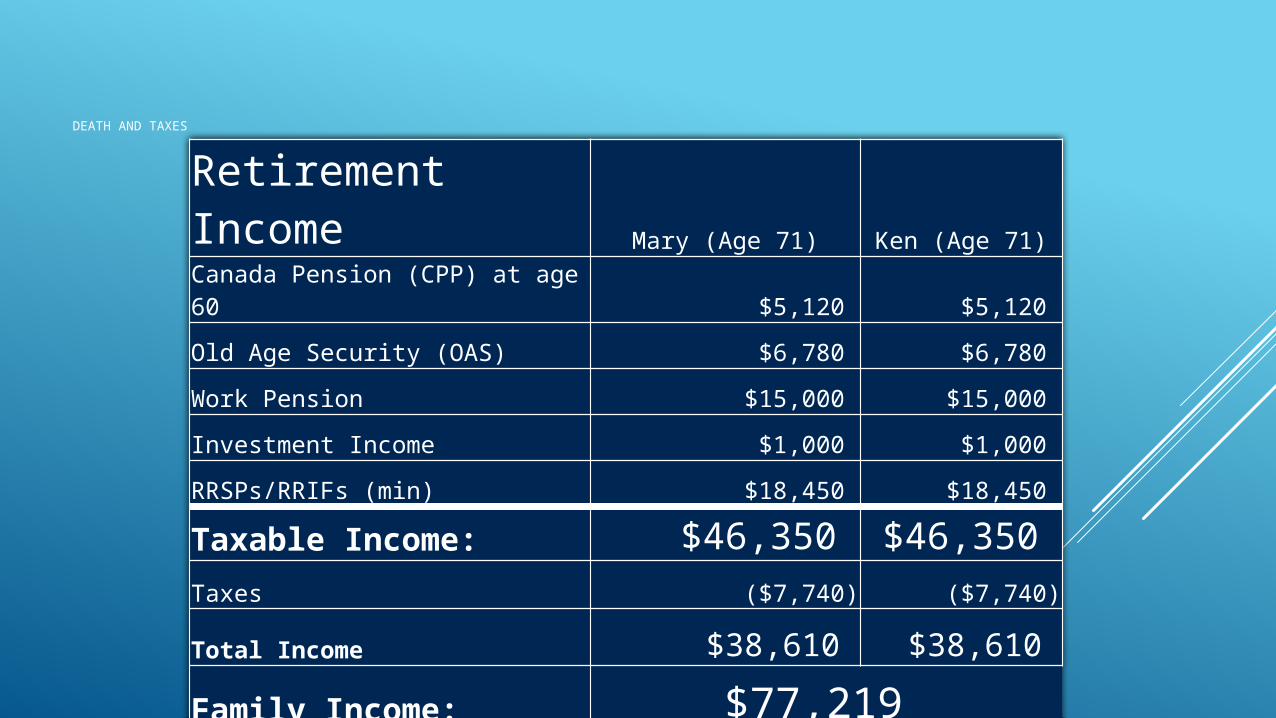

DEATH AND TAXES

Retirement Income Mary (Age 71) Ken (Age 71)

Canada Pension (CPP) at age 60 $5,120 $5,120

Old Age Security (OAS) $6,780 $6,780

Work Pension $15,000 $15,000

Investment Income $1,000 $1,000

RRSPs/RRIFs (min) $18,450 $18,450

Taxable Income: $46,350 $46,350 Taxes ($7,740) ($7,740)

Total Income $38,610 $38,610

Family Income: $77,219

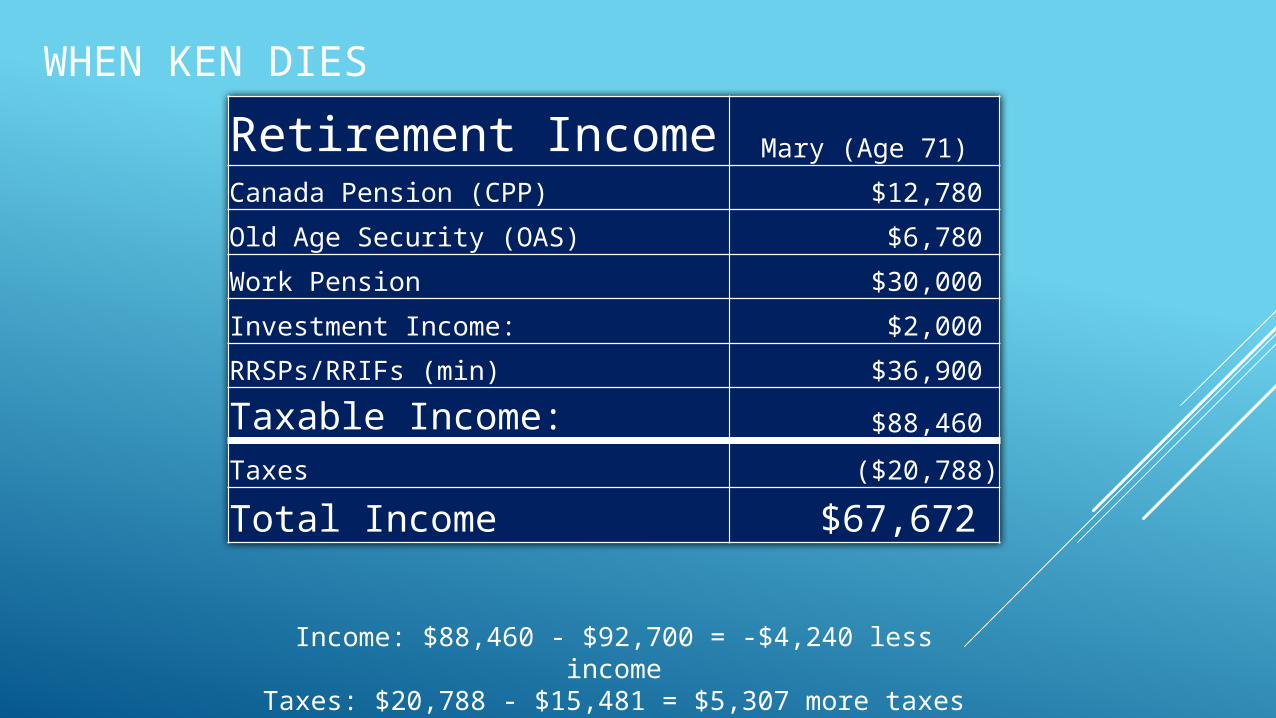

WHEN KEN DIES

Retirement Income Mary (Age 71)

Canada Pension (CPP) $12,780

Old Age Security (OAS) $6,780

Work Pension $30,000

Investment Income: $2,000

RRSPs/RRIFs (min) $36,900

Taxable Income: $88,460

Taxes ($20,788)

Total Income $67,672

Income: $88,460 - $92,700 = -$4,240 less incomeTaxes: $20,788 - $15,481 = $5,307 more taxes

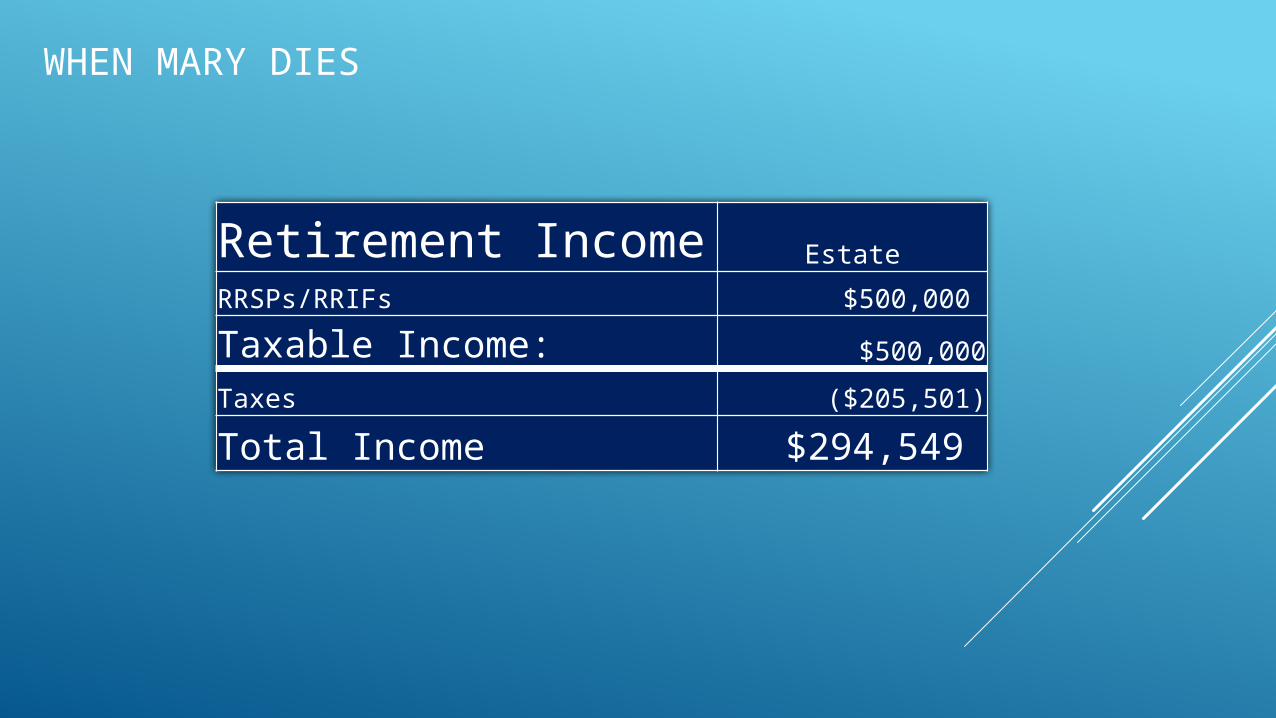

WHEN MARY DIES

Retirement Income Estate

RRSPs/RRIFs $500,000

Taxable Income: $500,000

Taxes ($205,501)

Total Income $294,549

YOU NEED A PLAN

FINANCIAL ISSUES ARE COMPLEX

YOU NEED TO WORK WITH A PROFESSIONAL

INVESTMENT MISTAKES

Wrong investments in the wrong accounts Unsuitable investments Don’t Understand Risk Questionable Source of Investment

Information

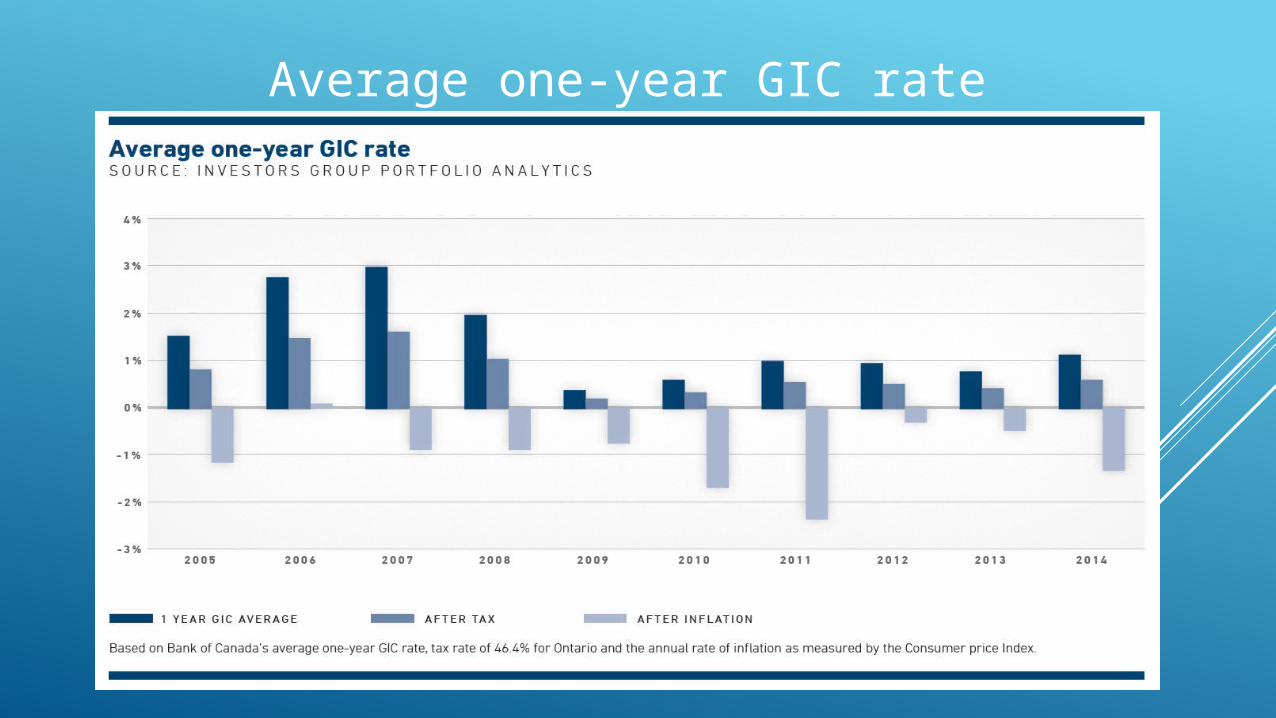

Average one-year GIC rate

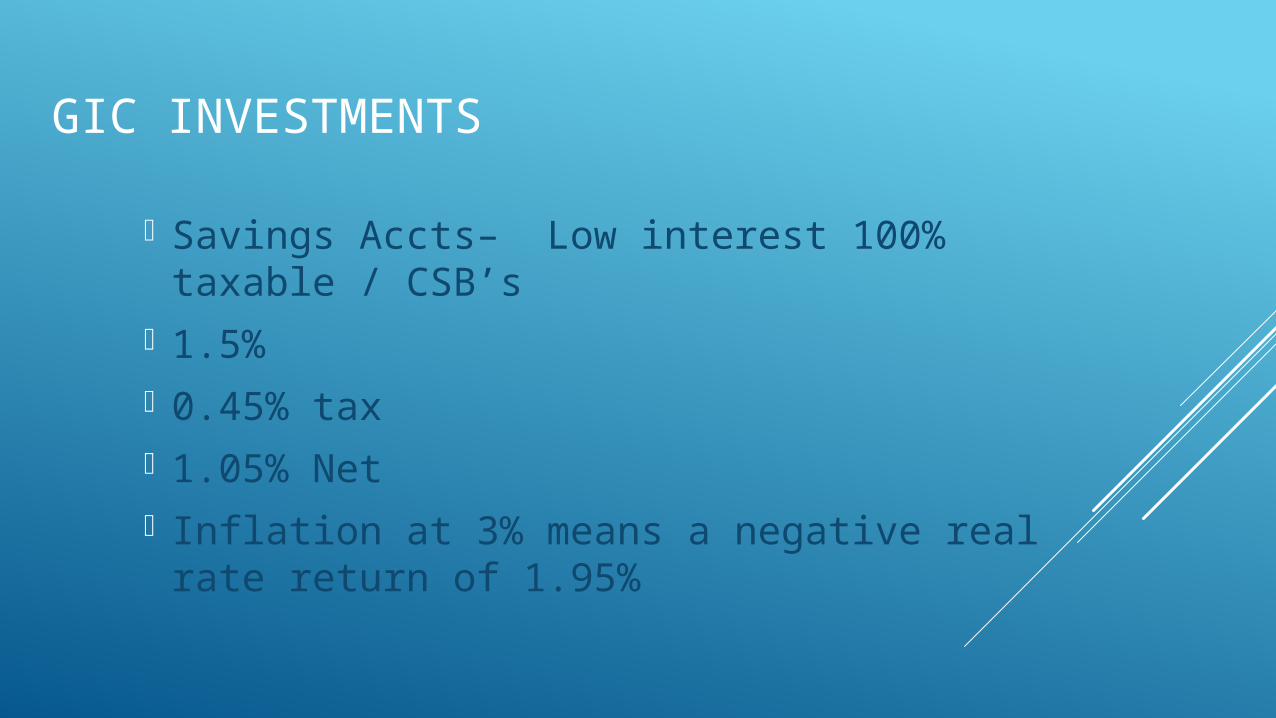

GIC INVESTMENTS

Savings Accts– Low interest 100% taxable / CSB’s

1.5% 0.45% tax 1.05% Net Inflation at 3% means a negative real rate

return of 1.95%

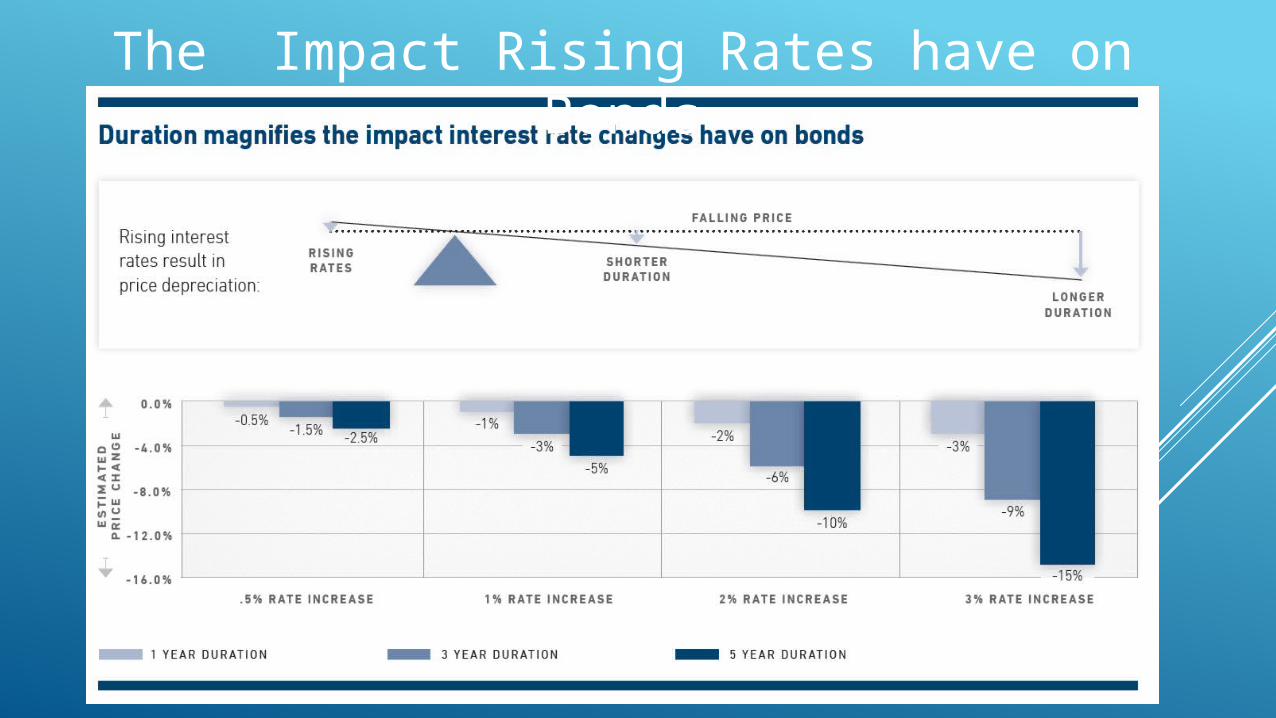

The Impact Rising Rates have on Bonds

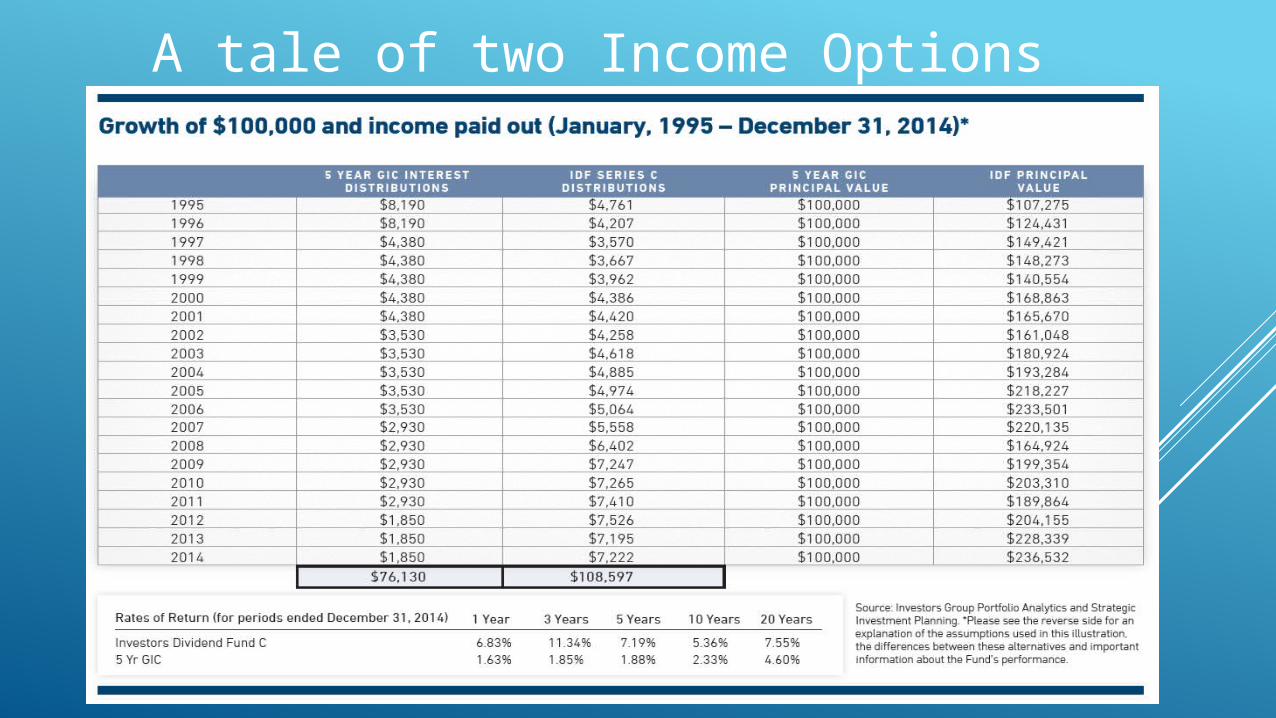

A tale of two Income Options

October 1999

June 2000 Sept. 1991

October 1987

Sept. 2001 June 2002

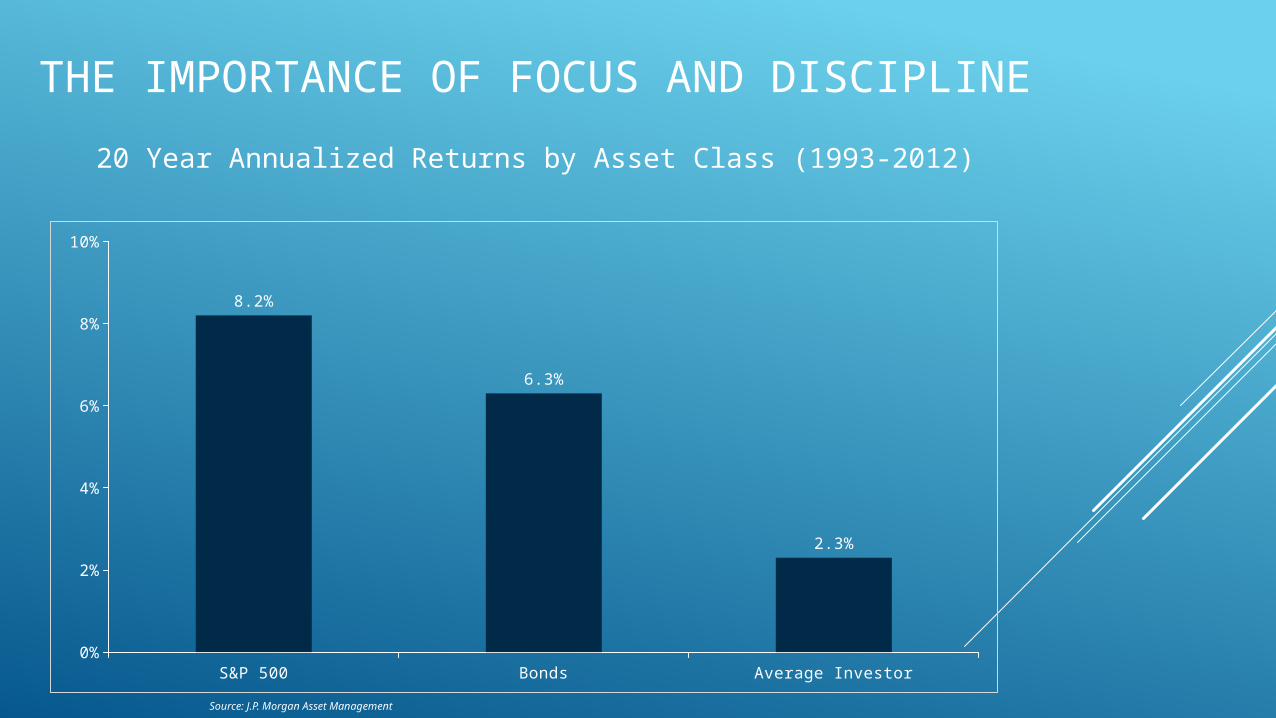

THE IMPORTANCE OF FOCUS AND DISCIPLINE

S&P 500 Bonds Average Investor0%

2%

4%

6%

8%

10%

8.2%

6.3%

2.3%

Source: J.P. Morgan Asset Management

20 Year Annualized Returns by Asset Class (1993-2012)

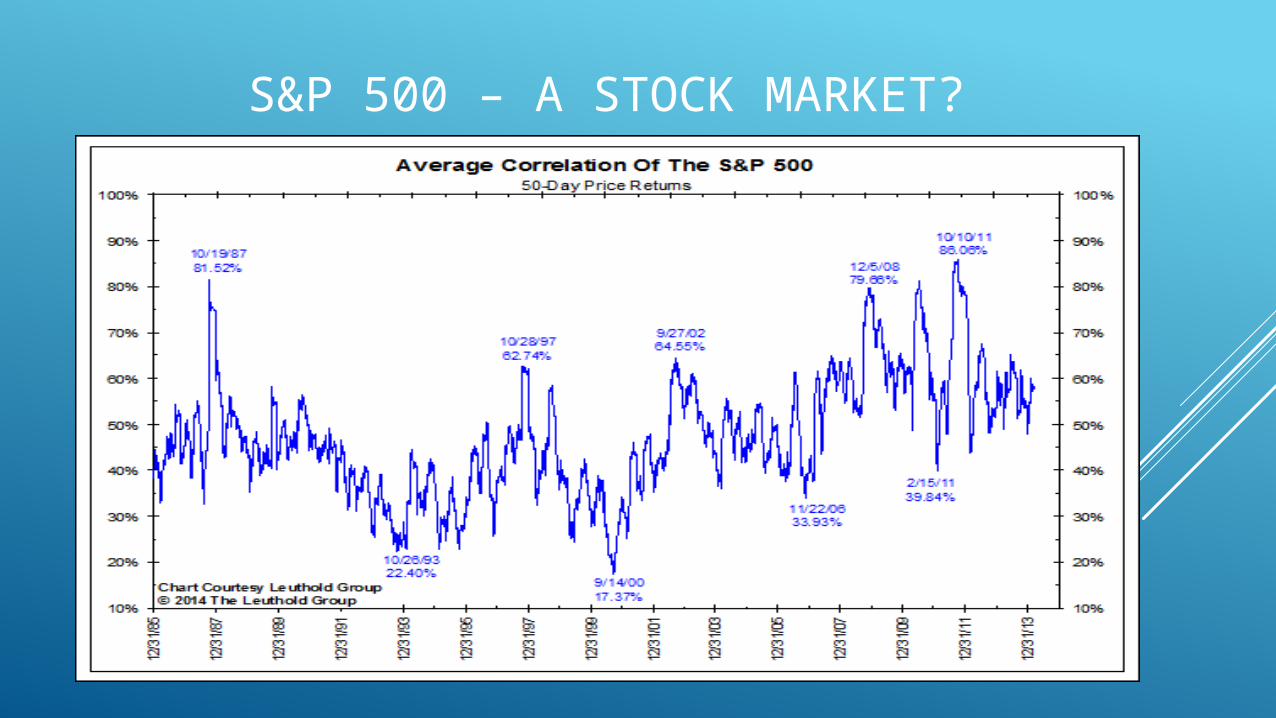

S&P 500 – A STOCK MARKET?

Technology Apple ($568 Billion) Google ($381 Billion) Microsoft ($340 Billion) Oracle ($190 Billion) IBM ($187 Billion) Facebook ($169 Billion) Amazon.com ($153 Billion) Intel ($141 Billion) Cisco ($128 Billion)

Consumer Staples Walmart ($247 Billion) Procter & Gamble ($217

Billion) Coca-Cola ($181 Billion) Pepsi ($134 Billion) Phillip Morris ($139 Billion)

Healthcare Johnson & Johnson ($295

Billion) Pfizer ($188 Billion) Merck ($171 Billion) Gilead ($122 Billion)

Industrials GE ($275 Billion) United Technologies ($110

Billion) Boeing ($100 Billion) 3M ($95 Billion) Union Pacific ($93 Billion)

Telecom AT&T ($181 Billion) Verizon ($205 Billion)

Consumer Discretionary Walt Disney ($147 Billion) Comcast ($137 Billion) McDonald’s ($100 Billion) Home Depot ($110 Billion)

Financials Berkshire Hathaway ($316

Billion) Wells Fargo ($277 Billion) JP Morgan ($219 Billion) Bank of America ($167 Billion) Citigroup ($150 Billion) Visa ($135 Billion) American Express ($101

Billion)

Energy Exxon ($436 Billion) Chevron ($239 Billion) Shlumberger ($139 Billion) Conoco Philips ($100 Billion)

All of these US companies would currently be the largest market cap in the Canadian equity market

Source: IGIM, Bloomberg

Or A Market of Stocks – (Global Business)

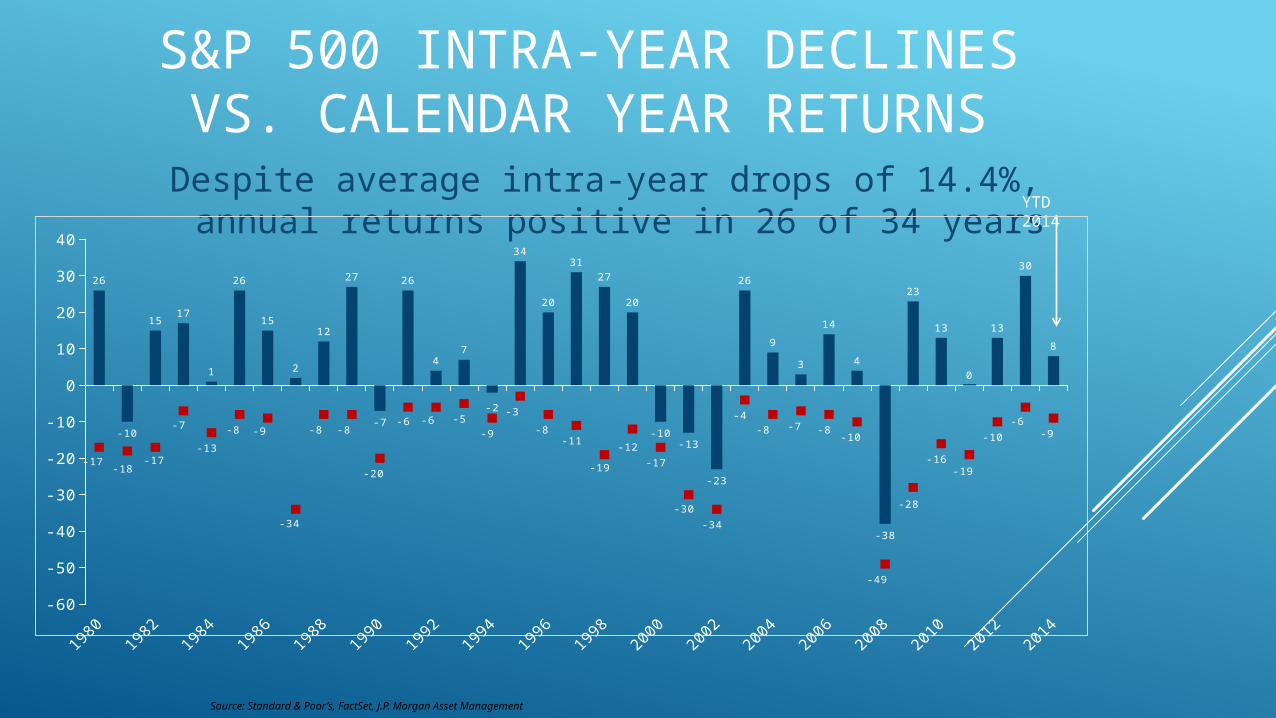

S&P 500 INTRA-YEAR DECLINES VS. CALENDAR YEAR RETURNS

Despite average intra-year drops of 14.4%, annual returns positive in 26 of 34 years

Source: Standard & Poor’s, FactSet, J.P. Morgan Asset Management

YTD 2014

-60

-50

-40

-30

-20

-10

0

10

20

30

40

26

-10

1517

1

26

15

2

12

27

-7

26

47

-2

34

20

3127

20

-10-13

-23

26

9

3

14

4

-38

23

13

0

13

30

8

-17-18

-17

-7

-13

-8 -9

-34

-8 -8

-20

-6 -6 -5-9

-3

-8-11

-19

-12

-17

-30

-34

-4-8 -7 -8

-10

-49

-28

-16-19

-10

-6-9

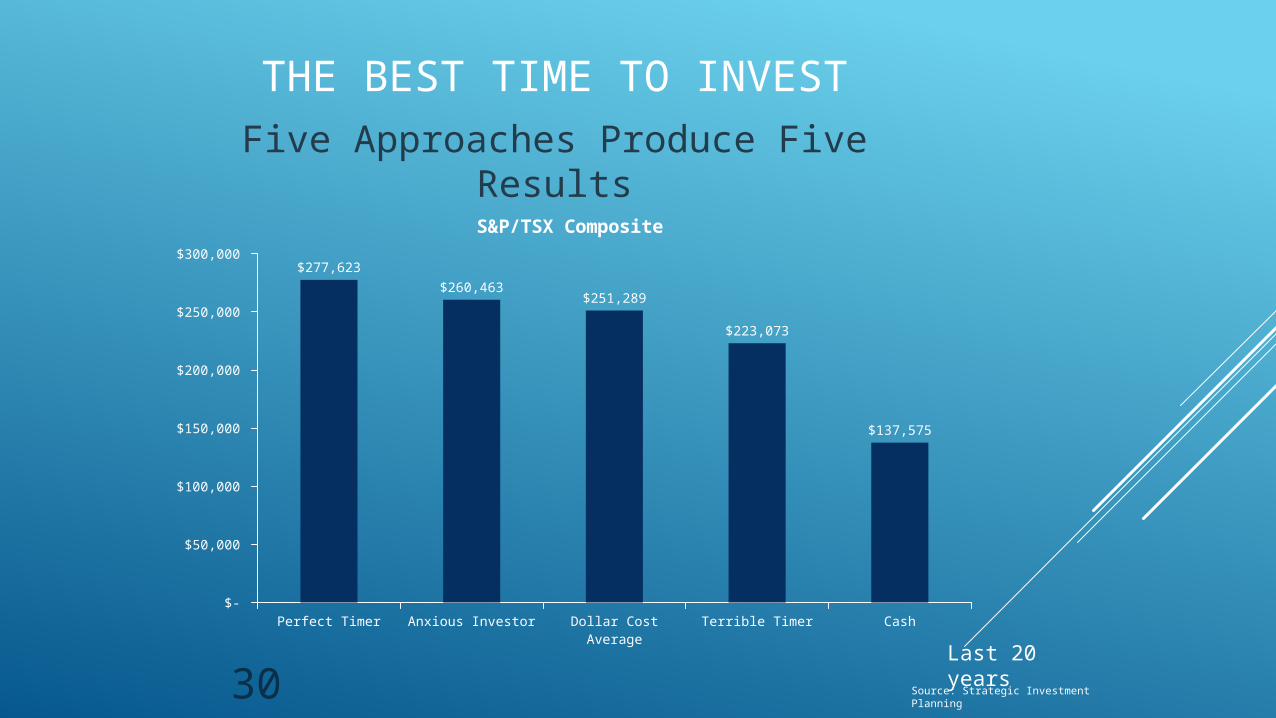

Five Approaches Produce Five Results

Source: Strategic Investment Planning

THE BEST TIME TO INVEST

30Perfect Timer Anxious Investor Dollar Cost Average Terrible Timer Cash

$-

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000 $277,623

$260,463$251,289

$223,073

$137,575

S&P/TSX Composite

Last 20 years

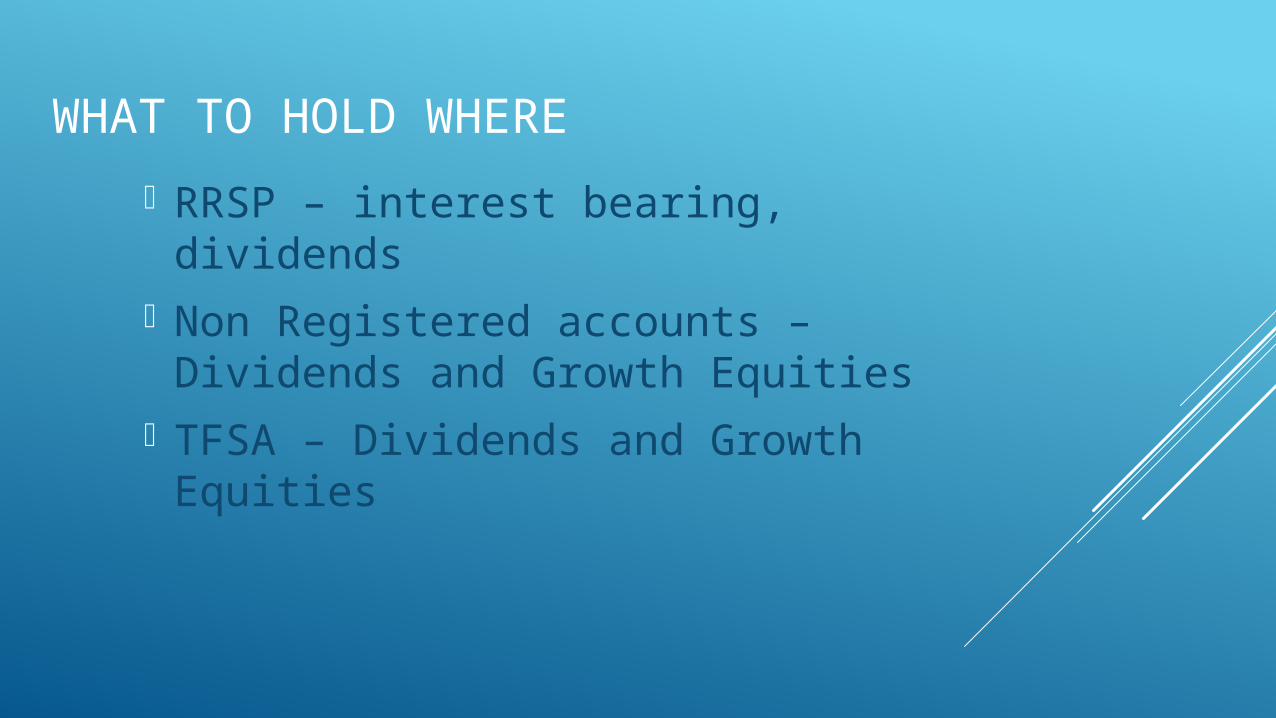

WHAT TO HOLD WHERE

RRSP – interest bearing, dividends Non Registered accounts – Dividends

and Growth Equities TFSA – Dividends and Growth Equities

YOU NEED A PLAN

FINANCIAL ISSUES ARE COMPLEX

YOU NEED TO WORK WITH A PROFESSIONAL

Sudden Death of a Loved One

YOU NEED A PLAN

FINANCIAL ISSUES ARE COMPLEX

YOU NEED TO WORK WITH A PROFESSIONAL

THANK YOU

![Slide 1 [S2001, Cap. 19] [GMJ91, Cap. 6] [R85, Cap. 6] Articoli citati in queste diapositive, e appunti u Generalità; verification & validation u Algoritmi](https://img.pdfslide.us/doc/110x75/5542eb4a497959361e8b62c9/slide-1-s2001-cap-19-gmj91-cap-6-r85-cap-6-articoli-citati-in-queste-diapositive-e-appunti-u-generalita-verification-validation-u-algoritmi.jpg)