Embed Size (px)

Citation preview

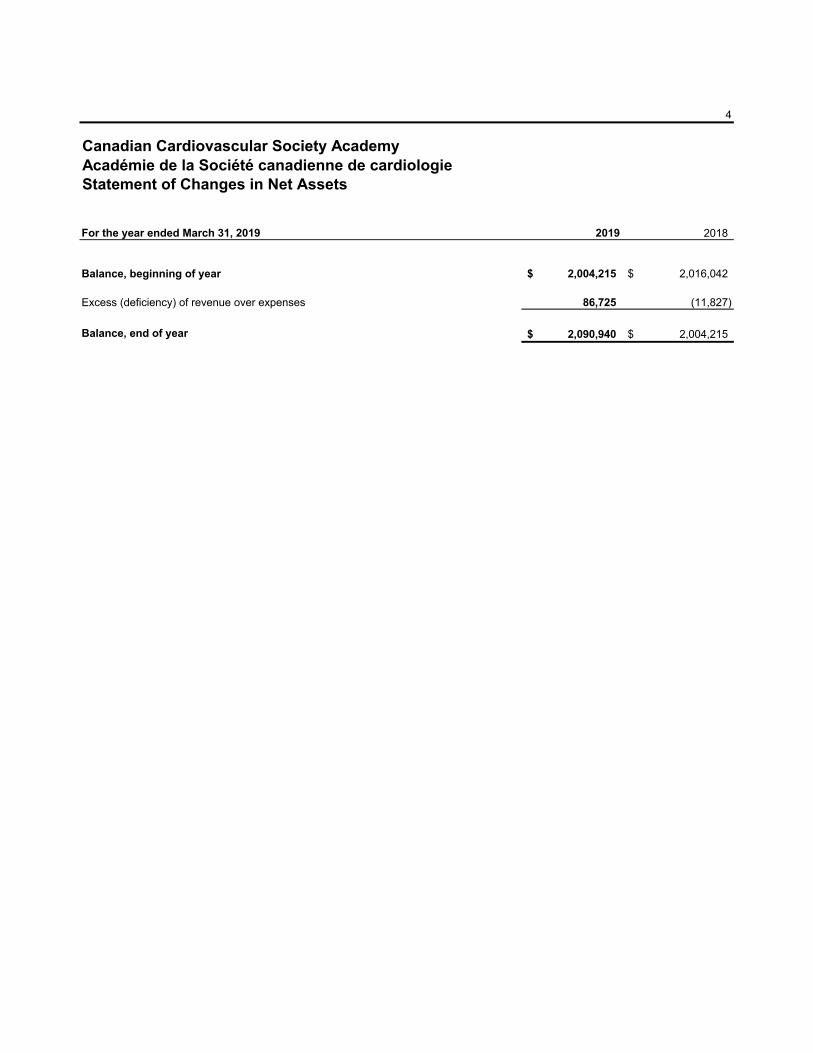

Canadian Cardiovascular Society Academy

Académie de la Société canadienne de cardiologie

Audited Financial Statements

March 31, 2019

Canadian Cardiovascular Society AcademyAcadémie de la Société canadienne de cardiologieFinancial Statements

For the year ended March 31, 2019

Contents

Independent Auditor's Report 1

Financial Statements

Statement of Financial Position 3

Statement of Changes in Net Assets 4

Statement of Operations 5

Statement of Cash Flows 6

Notes to the Financial Statements 7

1

To the Members ofCanadian Cardiovascular Society AcademyAcadémie de la Société canadienne de cardiologie

Qualified opinion

Basis for qualified opinion

Responsibilities of Management and Those Charged with Governance for the Financial Statements

Auditor's Responsibilities for the Audit of the Financial Statements

Those charged with governance are responsible for overseeing's the Academy's financial reporting process.

In preparing the financial statements, management is responsible for assessing's ability to continue as a going concern, disclosing, asapplicable, matters related to going concern and using the going concern basis of accounting unless management either intends toliquidate the Academy or to cease operations, or has no realistic alternative but to do so.

Management is responsible for the preparation and fair presentation of the financial statements in accordance with Canadianaccounting standards for not-for-profit organizations, and for such internal control as management determines is necessary to enablethe preparation of financial statements that are free from material misstatement, whether due to fraud or error.

Independent Auditor's Report

We conducted our audit in accordance with Canadian generally accepted auditing standards. Our responsibilities under thosestandards are further described in the Auditor's Responsibilities for the Audit of the Financial Statements section of our report. We areindependent of the Academy in accordance with the ethical requirements that are relevant to our audit of the financial statements inCanada, and we have fulfilled our other ethical responsibilities in accordance with these requirements. We believe that the auditevidence we have obtained sufficient and appropriate to provide a basis for our qualified opinion.

We have audited the financial statements of the Canadian Cardiovascular Society Academy / Académie de la Société canadienne decardiologie (the Academy), which comprise the statement of financial position as at March 31, 2019, and the statements of operationsand changes in net assets and cash flows for the year then ended, and notes to the financial statements, including a summary ofsignificant accounting policies.

In common with many charitable organizations, the Academy derives revenue from donations, the completeness of which is notsusceptible to satisfactory audit verification. Accordingly, our audit of these revenues was limited to the amounts recorded in therecords of the Academy. Therefore, we were not able to determine whether any adjustments might be necessary to revenue fromdonations, excess of revenue over expenses, and cash flows from operations for the years ended March 31, 2019 and 2018, currentassets as at March 31, 2019 and 2018, and net assets as at March 31, 2019, 2018 and 2017. Our audit opinion on the financialstatements for the year ended March 31, 2018 was also modified accordingly because of the possible effects of this limitation inscope.

Our objectives are to obtain reasonable assurance about whether the financial statements as a whole are free from materialmisstatement, whether due to fraud or error, and to issue an auditor's report that includes our opinion. Reasonable assurance is a highlevel of assurance, but is not a guarantee that an audit conducted in accordance with Canadian generally accepted auditing standardswill always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if,individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis ofthese financial statements.

In our opinion, except for the possible effects of the matter described in the Basis for Qualified Opinion section of our report, theaccompanying financial statements present fairly, in all material respects, the financial position of the Academy as at March 31, 2019,and the results of its operations and its cashflows for the year then ended, in accordance with Canadian accounting standards for not-for-profit organizations.

2

•

•

•

•

•

Chartered Professional Accountants, Licensed Public Accountants

Ottawa, Ontario

Identify and assess the risks of material misstatement of the financial statements, whether due to fraud or error, design andperform audit procedures responsive to those risks, and obtain audit evidence that is sufficient and appropriate to provide a basisfor our opinion. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, asfraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control.

Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in thecircumstances, but not for the purpose of expressing an opinion on the effectiveness of the Academy's internal control.

Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and related disclosuresmade by management.

Conclude on the appropriateness of management's use of the going concern basis of accounting and, based on the audit evidenceobtained, whether a material uncertainty exists related to events or conditions that may cast significant doubt on the Academy'sability to continue as a going concern. If we conclude that a material uncertainty exists, we are required to draw attention in ourauditor's report to the related disclosures in the financial statements or, if such disclosures are inadequate, to modify our opinion.Our conclusions are based on the audit evidence obtained up to the date of our auditor's report. However, future events orconditions may cause the Academy to cease to continue as a going concern.

Evaluate the overall presentation, structure and content of the financial statements, including the disclosures, and whether thefinancial statements represent the underlying transactions and events in a manner that achieves fair presentation.

As part of an audit in accordance with Canadian generally accepted auditing standards, we exercise professional judgment andmaintain professional skepticism throughout the audit. We also:

We communicate with those charged with governance regarding, among other matters, the planned scope and timing of the audit andsignificant audit findings, including any significant deficiencies in internal control that we identify during our audit.

June 26, 2019

3

March 31, 2019 2019 2018

Assets

CurrentCash 268,945$ 144,397$Sales tax receivable 1,996 1,306Receivable from Canadian Cardiovascular Society, without interest 4,033 4,943Current portion of promissory note receivable from the Canadian Cardiovascular Society (Note 6) 18,400 17,700

293,374 168,346

Investments (Note 3) 1,681,129 1,699,659

Promissory note receivable from the

117,691 136,210

1,798,820 1,835,869

2,092,194$ 2,004,215$

Liabilities and Net Assets

CurrentAccounts payable 1,254$ -$

Net AssetsUnrestricted 2,090,940 2,004,215

2,092,194$ 2,004,215$

On behalf of the Board:

Director

Director

Canadian Cardiovascular Society (Note 6)

Canadian Cardiovascular Society AcademyAcadémie de la Société canadienne de cardiologieStatement of Financial Position

4

Académie de la Société canadienne de cardiologie

For the year ended March 31, 2019 2019 2018

Balance, beginning of year 2,004,215$ 2,016,042$

Excess (deficiency) of revenue over expenses 86,725 (11,827)

Balance, end of year 2,090,940$ 2,004,215$

Statement of Changes in Net Assets

Canadian Cardiovascular Society Academy

5

Budget2019

For the year ended March 31, 2019 (Note 4) 2019 2018

RevenueDonations from members 109,000$ 139,131$ 103,520$ Donations from others 6,200 12,105 6,200 Grants from CIHR - ICRH 30,000 30,000 30,000 Interest on promissory note 5,861 5,906 6,555 Trainee day networking luncheon 4,000 5,150 3,925 Cardiac surgery TRP registration 6,375 12,475 10,175 Pediatric cardiology TRP registration 2,550 3,825 2,850 Adult TRP registration 24,300 25,500 27,570 Dividend and interest on investments 70,000 55,405 68,829 Bank interest 1,100 3,146 1,370

259,386 292,643 260,994

Expenses Trainee initiatives 38,800 38,660 34,800 CCS secretariat fees 75,000 75,000 75,000 Adult TRP 49,500 50,700 48,534 Have a Heart Bursary program 38,000 18,203 37,518 Cardiac surgery TRP 18,000 24,871 21,161 Investment management fees 10,465 14,633 14,297 Guideline development 10,000 10,000 10,000 Pediatric TRP 7,600 8,430 6,021 Publication/Reports 1,500 2,102 2,219 CCSA award recognition 1,500 1,196 162 Board meeting expenses 2,100 3,085 2,016 Miscellaneous 750 4,002 2,388 Directors and Officers liability insurance 1,200 1,107 1,107 Charles Kerr Award 5,100 6,447 3,846 Office expenses 1,500 2,317 1,398 Legal fees 500 - - Audit fees 4,600 4,781 429

266,115 265,534 260,896

(6,729) 27,109 98

Realized gains on investments - 2,944 2,120

Unrealized gains (losses) on investments - 56,672 (14,045)

Excess (deficiency) of revenue over expenses (6,729)$ 86,725$ (11,827)$

Canadian Cardiovascular Society AcademyAcadémie de la Société canadienne de cardiologieStatement of Operations

unrealized gains (losses) on investmentsOperating surplus (deficit) before realized and

6

For the year ended March 31, 2019 2019 2018

Operating Activities

Excess (deficiency) of revenue over expenses 86,725$ (11,827)$ Adjustment for:Unrealized (gain) loss on investments (56,672) 14,045

30,053 2,218

Net change in non-cash working capital items:Sales tax receivable (690) 4,991 Receivable from Canadian Cardiovascular Society 910 (2,996) Accounts payable and accrued liabilities 1,254 (7,805)

31,527 (3,592)

Investing Activities

Net change in investments 75,202 (58,268) Promissory note receipts 17,819 17,168

93,021 (41,100)

Increase (decrease) in cash and cash equivalents 124,548 (44,692)

Cash and cash equivalents, beginning of year 144,397 189,089

Cash and cash equivalents, end of year 268,945$ 144,397$

Cash and cash equivalents consist of cash.

Statement of Cash Flows

Canadian Cardiovascular Society AcademyAcadémie de la Société canadienne de cardiologie

7

Canadian Cardiovascular Society Academy

Académie de la Société canadienne de cardiologie

Notes to the Financial Statements

March 31, 2019

1. Statute and Nature of Organization

2. Significant Accounting Policies

Use of Estimates

Contribution Receivable

Revenue Recognition

Financial Instruments

Measurement of financial instruments

The Academy subsequently measures all its financial assets and financial liabilities at amortized cost, except for investments in

equity instruments that are quoted in an active market, which are measured at fair value. Changes in fair value are recognized in

operations.

The Academy initially measures its financial assets and financial liabilities at fair value, except for certain non-arm’s length

transactions.

The Academy applies Canadian accounting standards for not-for-profit organizations (ASNFPO) in accordance with Part III of

the CPA Canada Handbook - Accounting.

The Canadian Cardiovascular Society Academy / Académie de la Société canadienne de cardiologie's mandate is to advance

education, award scholarships, develop clinical practice guidelines, and carry out or support research in the field of

cardiovascular disease for the benefit of cardiovascular professionals and members of the general public.

The preparation of financial statements in compliance with the ASNFPO requires management to make estimates and

assumptions that affect the reported amounts of assets and liabilities and the reported amounts of revenues and expenses for

the periods covered.

Donations in cash are recognized as revenue when received or receivable if the amount to be received can be reasonably

estimated and collection is reasonably assured.

Donations in marketable securities are recorded when the Academy is notified by the investment broker that such a donation

has been received.

The Academy is incorporated as a not-for-profit organization without share capital under the Canada Not-for-Profit Corporations

Act. The Academy is a registered charity under the Income Tax Act and, as such, is exempt from income tax.

Registration fees are recognized once the program has occured.

Cash and cash equivalents

The Academy's policy is to disclose bank balances under cash and cash equivalents, including bank overdrafts with balances

that fluctuate frequently from being positive ot overdrawn.

Investment and other revenue is recognized when earned.

A contribution receivable is recognized as an asset when the amount to be received can be reasonably estimated and ultimate

collection is reasonably assured.

8

Canadian Cardiovascular Society Academy

Académie de la Société canadienne de cardiologie

Notes to the Financial Statements

March 31, 2019

2. Significant Accounting Policies (continued)

Financial Instruments (continued)

Impairment

Contributed Services

Financial assets measured at amortized cost include cash, sales tax receivable, receivable from Canadian Cardiovascular

Society and promissory note receivable.

Financial liabilities measured at amortized cost include accounts payable.

Financial assets measured at fair value include investments.

The hours that members and volunteers contribute over the year to assist the Academy in carrying out its service delivery

activities are not recognized in the financial statements.

Financial assets measured at amortized cost are tested for impairment when there are indicators of possible impairment. The

Academy determines whether a significant adverse change has occurred in the expected timing or amount of future cash flows

from the financial asset. If this is the case, the carrying amount of the asset is reduced directly to the higher of the present value

of the cash flows expected to be generated by holding the asset, and the amount that could be realized by selling the asset at

the balance sheet date. The amount of the write-down is recognized in operations. The previously recognized impairment loss

may be reversed to the extent of the improvement, provided it is no greater than the amount that would have been reported at

the date of the reversal had the impairment not been recognized previously. The amount of the reversal is recognized in

operations.

Transaction costs

The Academy recognizes its transaction costs in operations in the period incurred. However, transaction costs related to

financial instruments subsequently measured at amortized cost reduce the carrying amount of the financial asset or liability and

are accounted for in the statement of operations using the straight-line method.

9

Canadian Cardiovascular Society Academy

Académie de la Société canadienne de cardiologie

Notes to the Financial Statements

March 31, 2019

3. Investments

Book value Fair value Fair value

2019 2019 2018

International Equity 119,728$ 156,752$ 356,881$

Canadian Equity 1,014,837 1,046,227 853,127

Canadian Short-Term Bonds 275,863 278,669 304,958

Canadian Long-Term Bonds 194,463 199,481 184,693

1,604,891$ 1,681,129$ 1,699,659$

4. Budget

5. Financial Instruments

Market Risk

6. Related Party Transactions

2019 2018

Secretariat fees expense 75,000$ 75,000$

10,000$ -$

75,710$ 66,996$ Interest revenue charged on promissory note 5,906$ 6,555$

The budget figures presented in the financial statements have not been audited and consequently, no audit opinion is expressed

on these figures.

These transactions were concluded in the normal course of operations and are measured at the exchange amount, which is the

amount of consideration established and agreed to by the related parties.

The Academy signed a promissory note agreement with CCS. The note, maturing in 2025, is receivable in quarterly instalments

of $5,931, principal and interest at an annual rate of 4%. The note is secured by way of a general security agreement. Interest in

the amount of $5,906 (2018: $6,555) was received during the year.

The related party transactions with CCS presented in the financial statements are as follows:

Also, all revenue and expenses relating to Trainee initiatives, Cardiac surgery TRP, Adult TRP, Pediatric TRP and Guideline

development are processed through CCS.

Market risk is the risk that the fair value of future cash flows of a financial instrument will fluctuate because of changes in market

prices. The Academy's investments in bonds expose the Academy to market risk as such investments are subject to price

changes in the open market. The Academy does not use derivative financial instruments to alter the effects of this risk.

Guideline development expense

Program expenses

Canadian Cardiovascular Society (CCS) controls the Academy by virtue of its ability to appoint some of the members of the

Academy's Board of Directors.