Embed Size (px)

Citation preview

Please refer to page 19 for important disclosures and analyst certification, or on our website

www.macquarie.com/research/disclosures .

CANADA/UNITED STATES

BEP-U CN/BEP US Outperform

Price (at 04:38, 01 Feb 2017 GMT)C$39.20/US$30.22

Valuation C$ 43.00/US$33.00 - EV/2018E EBITDA and Dividend Yield 12-month target C$ 43.00/US$33.00

12-month TSR % +16.8

Volatility Index Low

GICS sector Utilities

Market cap C$m 11,619

Market cap US$m 8,912

30-day avg turnover C$m 5.1

Number shares on issue m 296.4

Investment fundamentals Year end 31 Dec 2015A 2016E 2017E 2018E

EBITDA m 1,088.0 1,585.4 1,529.8 1,560.7 Total DPS US$ 1.66 1.78 1.90 2.04 Total div y ield % 5.5 5.9 6.3 6.8 EV/EBITDA x 12.6 9.1 9.5 9.4

BEP-U CN vs TSX, & rec history

Note: Recommendation timeline - if not a continuous line, then there was no Macquarie coverage at the time or there was an embargo period.

Source: FactSet, Macquarie Capital (USA), February 2017

(all f igures in USD unless noted, TP in CAD)

Analyst(s) Dav id Noseworthy, P.Eng +1 212 231 6681 [email protected]

1 February 2017 Macquarie Capital (USA) Inc.

Brookfield Renewable Potential TERP & GLBL Acquisition Event

In our opinion, the potential acquisition of TerraForm Power Inc. and Terraform

Global Inc. by Brookfield Asset Management (Brookfield) is increasingly likely and

proximate. On Jan. 23/17 Brookfield, manager and sponsor of Brookfield

Renewable (BEP), brought this acquisition closer to reality by entering an

agreement to negotiate exclusively with these two parties. Herein we provide a

detailed analysis, summary of key events, and our perspective on frequently

asked questions regarding the potential acquisition.

Impact

In our view, TERP’s and GLBL’s lack of management and operational capability,

large size, and geographically diverse asset base make them difficult to acquire.

We view the fact that TERP and GLBL entered into exclusive agreements to work

with Brookfield as evidence that there were no superior bids to that of Brookfield’s.

We believe, BEP is well situated to acquire TERP and GLBL due to its large

overlapping operating footprint, relatively low cost of capital, and ready access to

large pools of capital from its sponsor and private equity partners.

We estimate, absent any cost synergies, acquiring 100% of TERP and GLBL on

the terms proposed would be $0.07 accretive to our 2017E DCPS on a full year

basis. However, we believe the elimination of public issuer costs, capital

efficiencies, and operating efficiencies would likely result in $20M of cost savings

net to BEP’s ownership interest. Including these savings we estimate $0.13 DCPS

accretion. For a more fulsome accretion analysis see Fig 10-18.

Depending on which of BEP’s four proposals is ultimately successful, we estimate

BEP will require between $320M - $850M to finance the equity portion of such a

transaction. Also, we expect BEP retain a 40% stake in whatever the Brookfield

consortium ultimately acquires, consistent with other recent transactions.

BEP reports Q4/16 result on Feb. 2/17. We expect AFFOPS of $0.41, above

consensus of $0.35, and Adj. EBITDA of $407M above consensus of $397M.

Earnings and target price revision

Our revised estimates reflect the transition to a new model.

Price catalyst

12-month price target: C$43.00 based on a combination of 13.75x EV/2018E

EBITDA and a 5.75% target yield on our 2018E dividend of $2.04/sh.

methodology.

Catalyst: Acquisition of TERP, GLBL, or other portfolios of renewable assets.

Action and recommendation

We maintain our Outperform rating. As one of the world’s largest publicly -traded,

pure play renewable power businesses, we believe BEP is a core holding in the

global independent power producer space.

Macquarie Research Brookfield Renewable

1 February 2017 2

Source: Company data, Macquarie Capital (USA), February 2017

Macquarie Research Brookfield Renewable

1 February 2017 3

What happened most recently?

On Jan. 23/17 Brookfield Asset Management (Brookfield), manager and sponsor of Brookfield

Renewable, entered into two separate agreements to negotiate a takeover on an exclusive basis with

both TerraForm Power (TERP US, US$11.87, Outperform, TP: US$14.00, Angie Storozynski) and

TerraForm Global (GLBL US, US$4.40, Outperform, TP: US$4.00, Angie Storozynski). This is the

most recent event in a series of efforts made by Brookfield to acquire TERP (see Fig. 1 for a summary

of key events). Brookfield has provided four alternative proposals to acquire TERP and GLBL. These

offers include acquiring: (1) 100% of TERP for $11.50/class A share; (2) 100% of TERP and GLBL for

$12.50 and $4.35 per share, respectively; (3) 50.1% of TERP and replace SunEdison, Inc. (SUNE) as

sponsor for $11.50/share; and (4) 50.1% of TERP and GLBL and replace SUNE as sponsor for $12.50

and $4.25, respectively. We have conducted a detailed analysis of Brookfield’s offers based on our

examination of Brookfield’s, TERP’s, and GLBL’s filings.

Fig 1 TERP Class A Share Price and Volume with Select Key Events Rela ted to Brookfield’s Acquisition Efforts

Source: company reports, Bloomberg, Macquarie Capital (USA)

Why are TERP & GLBL potentially available?

TERP and GLBL are potentially available for acquisition because its manger and sponsor,

SUNE, has filed for bankruptcy, creating doubt in the minds of investors as to the long term

sustainability of the yieldco model for these companies. Recall, on April 21, 2016 SUNE, manager and

sponsor of both TERP and GLBL, filed for protection under Chapter 11 of the U.S. Bankruptcy Code.

TERP and GLBL were not part of this filing and have no plans to file for bankruptcy. However, absent

SUNE, they would lack an operator, asset manager, and sponsor. Consequently, on September 19,

2016 TERP announced that its Board of Directors has initiated a process to explore and evaluate

potential strategic alternatives to maximize shareholder value, including a merger or sale of its entire

business.

Source: Company Releases, Bloomberg

(1) Dec 02/15 Appaloosa LP (ALP) disclosed its 8.7M Class A share position in TerraForm Power, Inc.

(2) Jun 20/16 Brookfield announces its 11.1M Class A share stake in TERP and total return swap for 11.6M notional Class A TERP shares

(3) Jul 22/16 Brookfield and ALP disclose that they have formed a group under the Exchange Act with a combined 22.5% economic interest TERP Class A shares.

(4) Nov 09/16 Brookfield offers $12/Class A share for TERP

(5) Nov 17/16 Brookfield offers a $13/Class A share for TERP and says it is prepared to make an offer for GLBL as well

(6) Dec 01/16 Brookfield extends the expiration date of its total return swaps agreement for 9M notional Class A TERP shares from April 17/17 to April 17/18

(7) Dec 03/16 Brookfield enters confidentiality agreement with TERP to participate in TERP's strategic review process

(8) Jan 09/17 Brookfield offers $11.50 - $12.50 per Class A TERP share, and $4.25 - $4.35 per Class A GLBL share

(9) Jan 23/17 Brookfield enters agreement to negotiate acquisition of TERP and GLBL on a exclusive basis

0

5

10

15

20

25

30

35

40

45

50

$0

$5

$10

$15

$20

$25

$30

$35

Jul 10

/15

Nov 1

2/1

5

Ma

r 16/1

6

Jul 19

/16

Nov 2

1/1

6

Avg

Da

ily V

olu

me

(M

illi

on

s)

Sh

are

Pri

ce

($/s

ha

re)

Major Events Price Volume (RHS)

2

4

83 5 9

6, 7

1

July 22/16 - Brookfield and ALP form a legal "group " with a combined 19.8M

Class A TERP shares

Jan 9/17 -Brookfield

offers

$11.50 -$12.50 for

TERP

Dec 3/16 - Appaloosa LP discloses 8.7M Class A share position in TERP

June 2/16 - Brookfield discloses 11.1M Class A

share position in TERP

and 11.5M Notional Class A Total Return swap

Nov 17/16 -Brookfield

offers

$13/share for TERP

Dec 3/16 -Brookfield gains access to TERP's

data room

Nov 9/16 - Brookfield offers $12/share for

TERP

Jan 23/17 - Brookfield enters agreement to negotiate the acquisition of TERP and GLBL on an exclusive basis -

Brookfield offers $4.25 - $4.35 for GLBL

Macquarie Research Brookfield Renewable

1 February 2017 4

Why is BEP a strong candidate to acquire TERP & GLBL?

We believe BEP is uniquely capable of acquiring TERP and GLBL because BEP has: (1) a strong

global operating footprint overlapping in many of the areas that TERP’s and GLBL’s assets reside; (2)

a relatively low cost of capital compared to the US yieldcos; and (3) access to significant pools of

capital through its affiliation with Brookfield Asset Management (Brookfield). The lack of other potential

suitors with these characteristics has in our view, severely diminished the pool of potential bidders for

these otherwise top-tier renewable assets. We discuss each factor in further detail below.

BEP has a strong global operating footprint overlapping in many of the areas that TERP and

GLBL have assets. We believe an acquirer of TERP and GLBL will need operating, maintenance,

and back office capability to replace those functions currently being provided by SUNE. As sponsored

yieldcos, TERP and GLBL, are financial constructs that lack internal operations, maintenance, and

asset management capability. The TerraForm Companies currently receive these services under a

management agreement with SunEdison, which has filed for protection under Chapter 11. In our view,

most financial buyers, like pension funds and private equity funds, have likely been eliminated from

the process due to the uncertainty regarding operating personnel and the difficulty to mitigate such a

risk. In contrast, BEP as one of the largest renewable power operators in the world could likely

assume operating control from SUNE in relatively short order.

BEP a significant cost of capital advantage over other strategic acquirers. BEP trades at a 2.3x

EV/2017E premium to the US yieldco average of 9.5 x (see Fig 2). Furthermore, BEP trades at a 0.7x

premium to its Canadian Independent Power Producers (IPP) average of 11.1x. In our view, the

relative weak valuations for US yieldcos and Canadian IPP make a competitive bid from strategics

less likely.

Fig 2 US and Canadian Comparables

Source: Factset, Macquarie Capital (USA), February 2017

Macquarie Research Brookfield Renewable

1 February 2017 5

BEP has access to significant pools of capital. BEP has demonstrated an ability to access public

equity and preferred equity markets on a regular basis over the last several years. For example in

2016, BEP raised C$860M of common equity, C$500M of medium term notes, and C$200M of

preferred equity. Beyond the public capital markets, BEP has access, through its partners and

sponsor, to private capital markets as well. Recall, in July 2016 Brookfield raised $14B for its

Brookfield Infrastructure Fund III. BEP has been regularly investing alongside the Brookfield private

equity funds over the last couple of years, typically taking a 40% interest. We would expect this to

continue with the potential acquisition of TERP and GLBL.

Despite indications of interest from other bidders, TERP decided to enter an exclusivity

agreement with BEP, which we believe is indicative that BEP made the best offer. Since

December 6th, 2016 when TERP let BEP’s expedited buy-out offer fall through, there have been a

couple of other bidders whom have shown interest.

D.E. Shaw: On Dec. 15th D.E. Shaw, entered into a confidentiality pact with TERP according to the

13D/A filing. The company owns a 6.7% stake in TERP. Prior to this announcement, Reuters

published an article on August 28th stating that D.E Shaw had expressed interest in TERP and on

October 25, 2016 D.E. Shaw made an offer for SunEdison’s stake in TERP.

AES Corp: in December AES Corp emerged as a potential bidder as well. According to

SparkSpread AES had intentions to make a formal bid for 100% of TERP.

Why is BEP interested in TERP?

In our view, TERP owns a premiere portfolio of North American renewable generation assets

(see Fig 3). The 3.0 GW portfolio has an average asset life of three years. The portfolio is diversified,

with no single project representing more than 10% of the overall capacity, and no one jurisdiction

representing more than 25% of capacity (see Fig 4). In addition, the portfolio has an average

remaining power purchase agreement (PPA) life of 15 years and 90% of the contracted capacity is for

six years or longer (see Fig 5). Finally, 86% of the PPAs are with investment-grade counterparties

(see Fig. 5). We note that on January 6, 2017 TERP sold a 365MW portfolio of UK solar assets to the

private equity arm of EFG Hermes for $580M, including $370M of assumed debt. TERP estimates that

these assets generate about $35M of annual EBITDA.

BEP, as one of the world’s largest operators of renewable assets, may be able to achieve operations

and maintenance cost saving relative to the costs incurred by TERP under its management agreement

with SUNE. Furthermore, we believe there may also be refinancing opportunities that would ultimately

reduce interest expense. We estimate $10M cost savings (assuming Brookfield acquires a 100%

interest) increases cash flow accretion by $0.04/share.

Macquarie Research Brookfield Renewable

1 February 2017 6

Fig 3 TERP Asset Map As At October 31, 2016

Note (1) : On January 6, 2017 TERP announced the sales of 365MW of solar in the UK for $580M. The transaction is expected to close in H1/17.

Source: Company data, January 2017

Fig 4 TERP’s Asset Portfolio Breakdown by Project / by Power Market

Source: Company data, January 2017

Macquarie Research Brookfield Renewable

1 February 2017 7

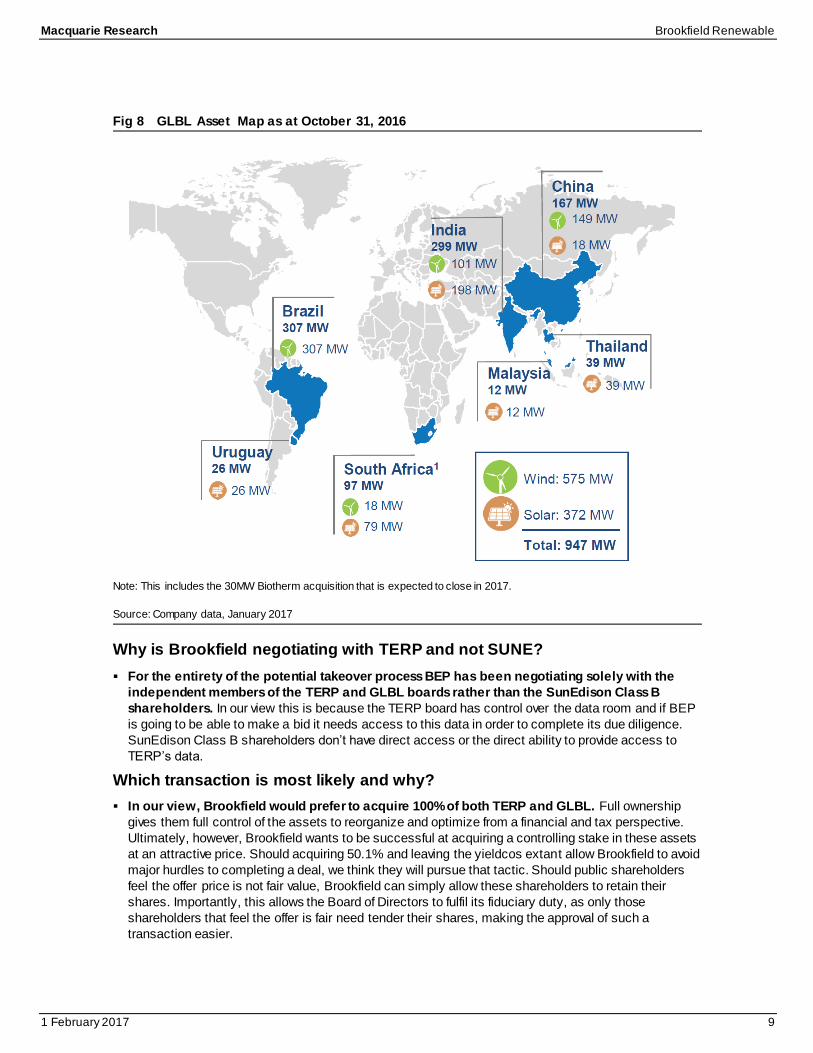

Why is BEP interested in GLBL?

We believe Brookfield’s interest in GLBL is motivate by a few considerations. First, at

Brookfield’s offer price, it is materially-accretive. Second, to the extent the sale of both TERP and

GLBL is desirable for stakeholders like SUNE and the TERP and GLBL Board of Directors, this could

differentiate Brookfield’s bid from other potential bids. Finally, GLBL’s assets are located primarily in

markets Brookfield is targeting. We discuss each consideration in further detail below.

We estimate the acquisition of 100% of GLBL for $4.35/share is $0.09 accretive to BEP’s 2017

cash flow, assuming a full year contribution. This is materially more accretive than TERP. We

believe Brookfield requires the higher cash-on-cash returns that the higher accretion signifies to bear

the higher risk profile of the countries in which GLBL operates (see Fig 6 – GLBL’s Assets by

Geography and Risk) and the credit-risk of their PPA counter parties.

Fig 5 TERP’s Asset Portfolio Breakdown by PPA Duration/ by Counterparty Credit Quality

Source: Company data, January 2017

Fig 6 GLBL’s Assets by Geography and by Risk

Source: Company data, Bureau of Diplomatic Security, CIA, January 2017

Macquarie Research Brookfield Renewable

1 February 2017 8

On January 27, 2017, Knighthead Capital, owner of a 7.2% stake in GLBL, indicated that based on a

recent acquisition in Brazil that GLBL would be worth $7.21/share. We estimate at this acquisition

price GLBL would still be $0.02 accretive to BEP’s 2017E AFFOPS. We believe the lack of an

alternative bid makes a higher bid from Brookfield challenging to justify.

BEP may be interested in GLBL as a way to differentiate its bid for TERP. Acquiring GLBL at the

same time as TERP may be attractive to: (1) SUNE, as it allows them to monetize their equity position

in both companies perhaps more quickly than would be the case if GLBL were to seek an acquirer

separately. Also, as structured, Brookfield is offering a premium for both TERP and GLBL together.

Any premium is likely desirable for SUNE; (2) there are six overlapping directors on the board of GLBL

and TERP (see Fig 7 – TERP & GLBL Board of Directors). To the extent that Brookfield’s offer allows

these directors to responsibly discharge their fiduciary duty to shareholders of both companies, we

believe a combined offer for TERP and GLBL may be more appealing than an offer for TERP alone,

especially if an acquisition of TERP by itself leaves GLBL orphaned.

Fig 7 TERP and GLBL Board of Directors

Source: Company data, Macquarie Capital (USA), February 2017

Two-thirds of GLBL’s assets are in markets that BEP either currently operates or intends to

operate (see Fig 8 – GLBL Asset Map). About 1/3 of GLBL’s assets are in Brazil, a historically

important market for BEP. Another 1/3 of GLBL’s assets are in India. BEP has recently identified India

as a potential market for expansion. However, the positive exposure to these markets may be

somewhat offset by exposure to potentially unattractive markets like South Africa, Malaysia, and

Uruguay.

Macquarie Research Brookfield Renewable

1 February 2017 9

Fig 8 GLBL Asset Map as at October 31, 2016

Note: This includes the 30MW Biotherm acquisition that is expected to close in 2017.

Source: Company data, January 2017

Why is Brookfield negotiating with TERP and not SUNE?

For the entirety of the potential takeover process BEP has been negotiating solely with the

independent members of the TERP and GLBL boards rather than the SunEdison Class B

shareholders. In our view this is because the TERP board has control over the data room and if BEP

is going to be able to make a bid it needs access to this data in order to complete its due diligence.

SunEdison Class B shareholders don’t have direct access or the direct ability to provide access to

TERP’s data.

Which transaction is most likely and why?

In our view, Brookfield would prefer to acquire 100% of both TERP and GLBL. Full ownership

gives them full control of the assets to reorganize and optimize from a financial and tax perspective.

Ultimately, however, Brookfield wants to be successful at acquiring a controlling stake in these assets

at an attractive price. Should acquiring 50.1% and leaving the yieldcos extant allow Brookfield to avoid

major hurdles to completing a deal, we think they will pursue that tactic. Should public shareholders

feel the offer price is not fair value, Brookfield can simply allow these shareholders to retain their

shares. Importantly, this allows the Board of Directors to fulfil its fiduciary duty, as only those

shareholders that feel the offer is fair need tender their shares, making the approval of such a

transaction easier.

Macquarie Research Brookfield Renewable

1 February 2017 10

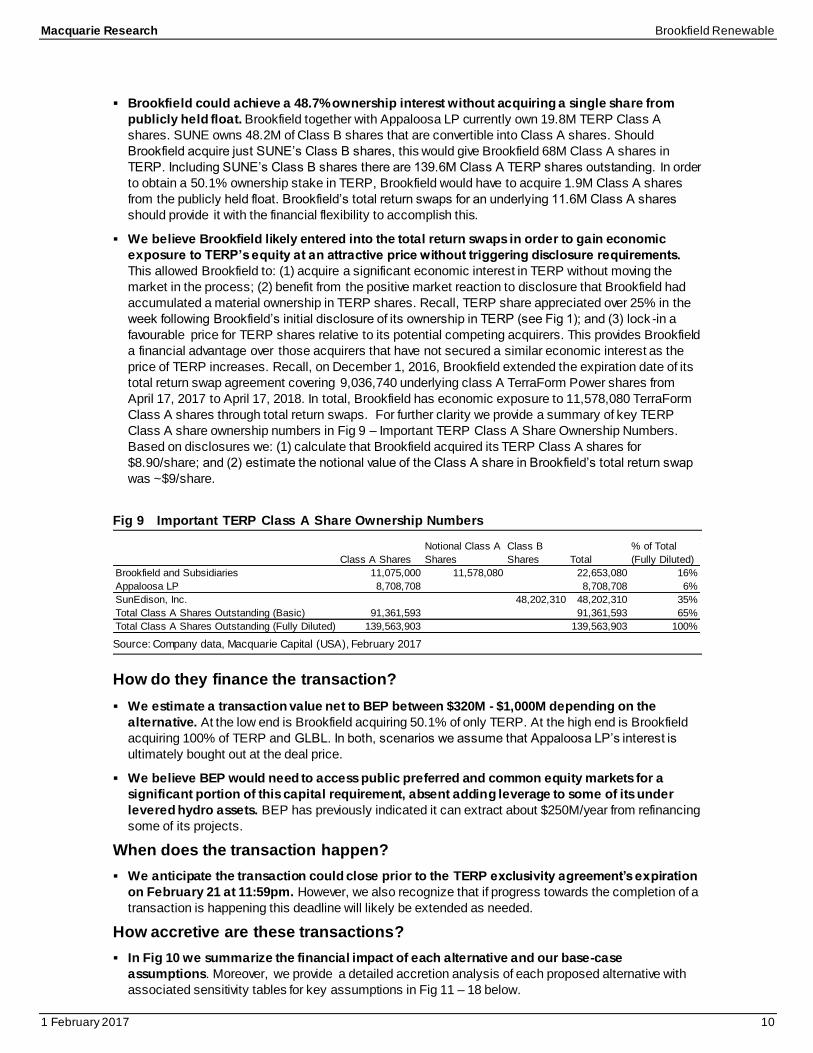

Brookfield could achieve a 48.7% ownership interest without acquiring a single share from

publicly held float. Brookfield together with Appaloosa LP currently own 19.8M TERP Class A

shares. SUNE owns 48.2M of Class B shares that are convertible into Class A shares. Should

Brookfield acquire just SUNE’s Class B shares, this would give Brookfield 68M Class A shares in

TERP. Including SUNE’s Class B shares there are 139.6M Class A TERP shares outstanding. In order

to obtain a 50.1% ownership stake in TERP, Brookfield would have to acquire 1.9M Class A shares

from the publicly held float. Brookfield’s total return swaps for an underlying 11.6M Class A shares

should provide it with the financial flexibility to accomplish this.

We believe Brookfield likely entered into the total return swaps in order to gain economic

exposure to TERP’s equity at an attractive price without triggering disclosure requirements.

This allowed Brookfield to: (1) acquire a significant economic interest in TERP without moving the

market in the process; (2) benefit from the positive market reaction to disclosure that Brookfield had

accumulated a material ownership in TERP shares. Recall, TERP share appreciated over 25% in the

week following Brookfield’s initial disclosure of its ownership in TERP (see Fig 1); and (3) lock -in a

favourable price for TERP shares relative to its potential competing acquirers. This provides Brookfield

a financial advantage over those acquirers that have not secured a similar economic interest as the

price of TERP increases. Recall, on December 1, 2016, Brookfield extended the expiration date of its

total return swap agreement covering 9,036,740 underlying class A TerraForm Power shares from

April 17, 2017 to April 17, 2018. In total, Brookfield has economic exposure to 11,578,080 TerraForm

Class A shares through total return swaps. For further clarity we provide a summary of key TERP

Class A share ownership numbers in Fig 9 – Important TERP Class A Share Ownership Numbers.

Based on disclosures we: (1) calculate that Brookfield acquired its TERP Class A shares for

$8.90/share; and (2) estimate the notional value of the Class A share in Brookfield’s total return swap

was ~$9/share.

Fig 9 Important TERP Class A Share Ownership Numbers

Source: Company data, Macquarie Capital (USA), February 2017

How do they finance the transaction?

We estimate a transaction value net to BEP between $320M - $1,000M depending on the

alternative. At the low end is Brookfield acquiring 50.1% of only TERP. At the high end is Brookfield

acquiring 100% of TERP and GLBL. In both, scenarios we assume that Appaloosa LP’s interest is

ultimately bought out at the deal price.

We believe BEP would need to access public preferred and common equity markets for a

significant portion of this capital requirement, absent adding leverage to some of its under

levered hydro assets. BEP has previously indicated it can extract about $250M/year from refinancing

some of its projects.

When does the transaction happen?

We anticipate the transaction could close prior to the TERP exclusivity agreement’s expiration

on February 21 at 11:59pm. However, we also recognize that if progress towards the completion of a

transaction is happening this deadline will likely be extended as needed.

How accretive are these transactions?

In Fig 10 we summarize the financial impact of each alternative and our base-case

assumptions. Moreover, we provide a detailed accretion analysis of each proposed alternative with

associated sensitivity tables for key assumptions in Fig 11 – 18 below.

Class A Shares

Notional Class A

Shares

Class B

Shares Total

% of Total

(Fully Diluted)

Brookfield and Subsidiaries 11,075,000 11,578,080 22,653,080 16%

Appaloosa LP 8,708,708 8,708,708 6%

SunEdison, Inc. 48,202,310 48,202,310 35%

Total Class A Shares Outstanding (Basic) 91,361,593 91,361,593 65%

Total Class A Shares Outstanding (Fully Diluted) 139,563,903 139,563,903 100%

Macquarie Research Brookfield Renewable

1 February 2017 11

Fig 10 Summary of Proposed Acquisition Alternatives by Brookfield Under Base Case Assumptions

Source: Company Reports, Macquarie Capital (USA), February 2017

Summary of Proposal

Alternatives (using base case

assumptions) (2) - (6)

Transaction Cost

(mlns USD)

Equity Funding

(mlns USD)

DCPS Accretion

($)

DCPS Accretion

(%)

EBITDA/share

Accretion ($)

EBITDA/share

Accretion (%)

BEP 2017E

EBITDA (mlns

USD) (1)

100% of TERP - $11.50/share $2,690 $642 $0.04 2.0% $0.21 3.7% $1,937

100% of TERP and GLBL for

$12.50 and $4.35 per share

respectively $3,409 $852 $0.13 5.7% $0.32 5.5% $2,013

50.1% of TERP and replace

SunEdison, Inc. (SUNE) as

sponsor for $11.50/share $1,347 $322 $0.01 0.6% $0.10 1.8% $1,838

50.1% of TERP and GLBL and

replace SUNE as sponsor for

$12.50 and $4.25

respectively. $1,704 $426 $0.05 2.2% $0.15 2.6% $1,873

(1) This combines BEP's EBITDA with that of the acquired assets and assumes the potenital transaction is effective as at January 1, 2017

(2) maximum 25% equity financing after assumption of debt(3) All cash on hand is used to reduce debt before close of the transaction

(4) For 100% acquired entities the removal of public issuer costs results in $15M/company

(5) For all transactions operating, finance, and tax efficiencies will result in $10M/company of savings

(6) Per share transaction price will equal price disclosed in each alternative (ie. No adjustment made post due diligence)

(7) We have adjusted estimates to reflect the announced agreement to sell TERP's 365MW portfolio of UK solar assets for $580M

Macquarie Research Brookfield Renewable

1 February 2017 12

Fig 11 BEP-TERP 100% Takeover Analysis (USD$ mlns., except where otherwise indicated)

Source: Company reports, Bloomberg, Macquarie Capital (USA), February 2017

Fig 12 Sensitivity Analysis (shaded areas represent scenarios that are not accretive)

Source: Company reports, Bloomberg, Macquarie Capital (USA), February 2017

Transaction Assumptions

Year 2017 Assumed equity component 25%

Interest rate - debt 4.0%

Tax rate 38%

BEP Ownership Percentage 40%

Percentage Of Target Acquired 100%

Transaction BEP TERP Comment Adjust Proforma

Stock Price (USD$/share) 30.22 11.50 30.22

Shares O/S (#M) 299 56

Current market cap 9,036 642

Takeout premium 0% Cash on hand 0

Purchase price 642 New Equity 642 9,678

Preferred shares 578 - 578

NCI 5,194 690 5,884

Net Debt 9,564 1,357 New net debt - 10,921

EV 24,372 2,690 27,061

Acretion Analysis

2017E Distributable Cash 686 52 Cost synergies 10 748

2017E Shares outstanding 304 56 (higher)/lower debt costs - 325

2017E DCPS 2.25 0.94 New shares issued (# M) 21.24 2.30

2017E EBITDA 1,746 181 1,937

2017E EBITDA per share 5.74 3.24 5.95

(1) The stock price for TERP is BEP's offer price. BEP's stock price is as of the close January 31st, 2017.

DCPS Accretion Cash on Hand EBITDAPS Accretion Cash on Hand

0.04 $0 $100 $200 $300 0.21 $0 $100 $200 $300

$0 $0.013 $0.021 $0.028 $0.036 $0 $0.182 $0.182 $0.182 $0.182

$5 $0.029 $0.036 $0.044 $0.051 $5 $0.197 $0.197 $0.197 $0.197

$10 $0.044 $0.052 $0.059 $0.067 $10 $0.212 $0.212 $0.212 $0.212

$15 $0.059 $0.067 $0.075 $0.082 $15 $0.228 $0.228 $0.228 $0.228

$20 $0.075 $0.082 $0.090 $0.098 $20 $0.243 $0.243 $0.243 $0.243

DCPS Accretion Takeout Premium EBITDAPS Accretion Takeout Premium

0.04 0% 5% 10% 20.0% 0.21 0% 5% 10% 20.0%

15% $0.082 $0.079 $0.076 $0.069 15% $0.360 $0.357 $0.354 $0.348

20% $0.061 $0.057 $0.054 $0.047 20% $0.276 $0.272 $0.268 $0.260

25% $0.044 $0.036 $0.032 $0.024 25% $0.212 $0.193 $0.184 $0.175

30% $0.044 $0.036 $0.029 $0.014 30% $0.212 $0.193 $0.174 $0.136

35% $0.044 $0.036 $0.029 $0.014 35% $0.212 $0.193 $0.174 $0.136

Co

st

Syn

erg

ies

Co

st

Syn

erg

ies

Eq

uit

y

Fin

an

cin

g

Eq

uit

y

Fin

an

cin

g

Macquarie Research Brookfield Renewable

1 February 2017 13

Fig 13 BEP-TERP-GLBL 100% Takeover Analysis (USD$ mlns., except where otherwise indicated)

Source: Company reports, Bloomberg, Macquarie Capital (USA), February 2017

Fig 14 Sensitivity Analysis (shaded areas represent scenarios that are not accretive)

Source: Company reports, Bloomberg, Macquarie Capital (USA), February 2017

Transaction Assumptions

Year 2017 Assumed equity component 25%

Interest rate - debt 4.0%

Tax rate 38%

BEP Ownership Percentage 40%

Percentage Of Target Acquired 100%

Transaction BEP TERP GLBL TERP & GLBL Comment Adjust Proforma

Stock Price (USD$/share) (1) 30.22 12.50 4.35 30.22

Shares O/S (#M) 299 56 70

Current market cap 9,036 698 304

Takeout premium 0% 0% Cash on hand 0

Purchase price 698 304 1,001 New Equity 852 9,888

Preferred shares 578 - - - 578

NCI 5,194 690 189 880 6,074

Net Debt 9,564 1,357 170 1,527 New net debt 149 11,240

EV 24,372 2,745 663 3,409 27,780

Acretion Analysis

2017E Distributable Cash 686 52 38 90 Cost synergies 20 792

2017E Shares outstanding 304 56 70 (higher)/lower debt costs (4) 332

2017E DCPS 2.25 0.94 0.54 New shares issued (# M) 28.20 2.38

2017E EBITDA 1,746 181 66 247 2,013

2017E EBITDA per share 5.74 3.24 0.95 6.054

(1) The stock price for TERP and GLBL is BEP's offer price. BEP's stock price is as of the close January 31st, 2017.

DCPS Accretion Cash on Hand EBITDAPS Accretion Cash on Hand

0.13 $0 $100 $200 $300 0.32 $0 $100 $200 $300

$0 $0.069 $0.076 $0.084 $0.091 $0 $0.256 $0.256 $0.256 $0.256

$5 $0.084 $0.091 $0.099 $0.106 $5 $0.271 $0.271 $0.271 $0.271

$10 $0.099 $0.107 $0.114 $0.121 $10 $0.286 $0.286 $0.286 $0.286

$15 $0.114 $0.122 $0.129 $0.136 $15 $0.301 $0.301 $0.301 $0.301

$20 $0.129 $0.137 $0.144 $0.152 $20 $0.317 $0.317 $0.317 $0.317

DCPS Accretion Takeout Premium EBITDAPS Accretion Takeout Premium

0.13 0% 5% 10% 20% 0.32 0% 5% 10% 20%

15% $0.187 $0.181 $0.176 $0.166 15% $0.529 $0.524 $0.519 $0.510

20% $0.157 $0.152 $0.146 $0.135 20% $0.421 $0.415 $0.409 $0.396

25% $0.129 $0.123 $0.118 $0.106 25% $0.317 $0.309 $0.301 $0.286

30% $0.105 $0.096 $0.090 $0.078 30% $0.228 $0.207 $0.198 $0.181

35% $0.105 $0.094 $0.082 $0.060 35% $0.228 $0.199 $0.170 $0.113

Co

st

Syn

erg

ies

Co

st

Syn

erg

ies

Eq

uit

y

Fin

an

cin

g

Eq

uit

y

Fin

an

cin

g

Macquarie Research Brookfield Renewable

1 February 2017 14

Fig 15 BEP-TERP 50.1% Takeover Analysis (USD$ mlns., except where otherwise indicated)

Source: Company reports, Bloomberg, Macquarie Capital (USA), February 2017

Fig 16 Sensitivity Analysis (shaded areas represent scenarios that are not accretive)

Source: Company reports, Bloomberg, Macquarie Capital (USA), February 2017

Transaction Assumptions

Year 2017 Assumed equity component 25%

Interest rate - debt 4.0%

Tax rate 38%

BEP Ownership Percentage 40%

Percentage Of Target Acquired 50.1%

Transaction BEP TERP Comment Adjust Proforma

Stock Price (USD$/share) 30.22 11.50 30.22

Shares O/S (#M) 299 28

Current market cap 9,036 322

Takeout premium 0% Cash on hand 0

Purchase price 322 New Equity 321.61 9,358

Preferred shares 578 - 578

NCI 5,194 345.9 5,540

Net Debt 9,564 680 New net debt - 10,244

EV 24,372 1,347 25,719

Acretion Analysis

2017E Distributable Cash 686 26 Cost synergies 2 714.07

2017E Shares outstanding 304 28 (higher)/lower debt costs - 315

2017E DCPS 2.25 0.94 New shares issued (# M) 10.64 2.27

2017E EBITDA 1,746 91 1,838

2017E EBITDA per share 5.74 3.24 5.84

(1) The stock price for TERP is BEP's offer price. BEP's stock price is as of the close January 31st, 2017.

DCPS Accretion Cash on Hand EBITDAPS Accretion Cash on Hand

0.01 $0 $50 $100 $150 0.10 $0 $50 $100 $150

$0 $0.007 $0.011 $0.015 $0.019 $0 $0.094 $0.094 $0.094 $0.094

$2 $0.013 $0.017 $0.021 $0.025 $2 $0.100 $0.100 $0.100 $0.100

$4 $0.020 $0.023 $0.027 $0.031 $4 $0.107 $0.107 $0.107 $0.107

$6 $0.026 $0.030 $0.034 $0.038 $6 $0.113 $0.113 $0.113 $0.113

$10 $0.039 $0.043 $0.046 $0.050 $10 $0.126 $0.126 $0.126 $0.126

DCPS Accretion Takeout Premium EBITDAPS Accretion Takeout Premium

0.01 0% 5% 10% 20% 0.10 0% 5% 10% 20%

15% $0.033 $0.031 $0.029 $0.026 15% $0.175 $0.173 $0.172 $0.169

20% $0.022 $0.020 $0.018 $0.014 20% $0.133 $0.131 $0.129 $0.125

25% $0.013 $0.009 $0.007 $0.003 25% $0.100 $0.091 $0.086 $0.081

30% $0.013 $0.009 $0.006 -$0.002 30% $0.100 $0.091 $0.081 $0.061

35% $0.013 $0.009 $0.006 -$0.002 35% $0.100 $0.091 $0.081 $0.061

Co

st

Syn

erg

ies

Co

st

Syn

erg

ies

Eq

uit

y

Fin

an

cin

g

Eq

uit

y

Fin

an

cin

g

Macquarie Research Brookfield Renewable

1 February 2017 15

Fig 17 BEP-TERP-GLBL 50.1% Takeover Analysis (USD$ mlns., except where otherwise indicated)

Source: Company reports, Bloomberg, Macquarie Capital (USA), February 2017

Fig 18 Sensitivity Analysis (shaded areas represent scenarios that are not accretive)

Source: Company reports, Bloomberg, Macquarie Capital (USA), February 2017

Transaction Assumptions

Year 2017 Assumed equity component 25%

Interest rate - debt 4.0%

Tax rate 38%

BEP Ownership Percentage 40%

Percentage Of Target Acquired 50.1%

Transaction BEP TERP GLBL TERP & GLBL Comment Adjust Proforma

Stock Price (USD$/share) 30.22 12.50 4.25 30.22

Shares O/S (#M) 299 28 35

Current market cap 9,036 350 149

Takeout premium 0% 0% Cash on hand 0

Purchase price 350 149 498 New Equity 426 9,462

Preferred shares 578 - - - 578

NCI 5,194 346 95 441 5,635

Net Debt 9,564 680 85 765 New net debt 72 10,401

EV 24,372 1,375 329 1,704 26,076

Acretion Analysis

2017E Distributable Cash 686 26 19 45 Cost synergies 4 733.32

2017E Shares outstanding 304 28 35 (higher)/lower debt costs (2) 318

2017E DCPS 2.25 0.94 0.54 New shares issued (# M) 14.10 2.30

2017E EBITDA 1,746 91 33 124 1,873

2017E EBITDA per share 5.74 3.24 0.95 5.88

DCPS Accretion Cash on Hand EBITDAPS Accretion Cash on Hand

0.05 $0 $50 $100 $150 0.15 $0 $50 $100 $150

$0 $0.036 $0.040 $0.044 $0.048 $0 $0.135 $0.135 $0.135 $0.135

$2 $0.043 $0.047 $0.051 $0.054 $2 $0.141 $0.141 $0.141 $0.141

$4 $0.049 $0.053 $0.057 $0.061 $4 $0.147 $0.147 $0.147 $0.147

$6 $0.055 $0.059 $0.063 $0.067 $6 $0.153 $0.153 $0.153 $0.153

$10 $0.068 $0.072 $0.076 $0.080 $10 $0.166 $0.166 $0.166 $0.166

DCPS Accretion Takeout Premium EBITDAPS Accretion Takeout Premium

0.05 0% 5% 10% 20% 0.15 0% 5% 10% 20%

15% $0.077 $0.076 $0.076 $0.074 15% $0.253 $0.253 $0.252 $0.251

20% $0.063 $0.062 $0.061 $0.060 20% $0.200 $0.199 $0.198 $0.196

25% $0.049 $0.048 $0.047 $0.046 25% $0.147 $0.146 $0.145 $0.143

30% $0.038 $0.036 $0.034 $0.032 30% $0.103 $0.099 $0.094 $0.090

35% $0.038 $0.036 $0.034 $0.030 35% $0.103 $0.099 $0.094 $0.086

Co

st

Syn

erg

ies

Co

st

Syn

erg

ies

Eq

uit

y

Fin

an

cin

g

Eq

uit

y

Fin

an

cin

g

Macquarie Research Brookfield Renewable

1 February 2017 16

Q4 Preview

Q4/16 Outlook: We forecast Q4/16 fund AFFOPU of $0.41, above consensus of $0.35 and Q4/15

AFFOPU of $0.27. Higher distributable cash Y/Y is largely due to cash flow contributions from the

1) stronger merchant power prices in the US and Ireland; 2) the full quarter contribution of Isagen; and

3) the increased contribution of the 151MW of wind assets in Ireland due to recent acquisitions; and

4) increased overall generation; partially offset by 1) weaker merchant power prices in Brazil and 2) a

stronger US dollar relative to other currencies where BEP operates.

See Fig 19 for a full summary of our Q4/16 estimates.

What to Expect in Q4

Acquisition and Development Pipeline: We expect management to provide colour on the progress

of these developments: (1) 127 MW of hydro and biomass development in Brazil (72 hydro, 55

biomass); (2) the full quarter contribution of Isagen; (3) the 43MW Ireland wind project development,

including the 19MW added in Q3/16; and (4) 100MW of hydro development projects in Brazil in early

stage development.

Recent Developments:

TERP and GLBL: The potential for BEP to acquire TERP and GLBL has been BEP’s most material

update this quarter. As we have outlined, this acquisition would be accretive if it were to go through.

See above for more detail.

Macquarie Research Brookfield Renewable

1 February 2017 17

Fig 19 Q4/2016 Expectations

Source: Company reports, and Macquarie

Macquarie Research Brookfield Renewable

1 February 2017 18

Macquarie Quant View

The quant model currently holds a marginally positive view on Brookfield

Renewable. The strongest style exposure is Valuations, indicating this stock

is under-priced in the market relative to its peers. The weakest style

exposure is Price Momentum, indicating this stock has had weak medium to

long term returns which often persist into the future.

Displays where the

company’s ranked based on

the fundamental consensus

Price Target and

Macquarie’s Quantitative

Alpha model.

Two rankings: Local market

(Canada) and Global sector

(Util ities)

194/433 Global rank in

Utilities % of BUY recommendations 60% (6/10)

Number of Price Target downgrades 0

Number of Price Target upgrades 5

Macquarie Alpha Model ranking Factors driving the Alpha Model

A list of comparable companies and their Macquarie Alpha model score

(higher is better).

For the comparable firms this chart shows the key underlying styles and their contribution

to the current overall Alpha score.

Macquarie Earnings Sentiment Indicator Drivers of Stock Return

The Macquarie Sentiment Indicator is an enhanced earnings revisions

signal that favours analysts who have more timely and higher conviction

revisions. Current score shown below.

Breakdown of 1 year total return (local currency) into returns from dividends, changes in

forward earnings estimates and the resulting change in earnings multiple.

What drove this Company in the last 5 years How it looks on the Alpha model

Which factor score has had the greatest correlation with the company’s

returns over the last 5 years.

A more granular view of the underlying style scores that drive the alpha (higher is better)

and the percentile rank relative to the sector and market.

Source (all charts): FactSet, Thomson Reuters, and Macquarie Research. For more details on the Macquarie Alpha model or for m ore customised analysis and screens, please contact the Macquarie Global Quantitative/Custom Products Group ([email protected])

Fu

nd

am

en

tals

Quant

Local market rank Global sector rank

Attractive

0.3

0.4

0.5

0.5

0.6

0.7

0.7

-3.0 -2.0 -1.0 0.0 1.0 2.0 3.0

Brookfield Renewable

SCANA Corporation

Aqua America

AES

American Water Works

Alliant Energy

CMS Energy

-100% -80% -60% -40% -20% 0% 20% 40% 60% 80% 100%

Brookfield Renewable

SCANA Corporation

Aqua America

AES

American Water Works

Alliant Energy

CMS Energy

Valuations Growth Profitability Earnings

Momentum

Price

Momentum

Quality

-0.7

0.5

0.5

-0.9

0.6

-1.2

0.3

-3.0 -2.0 -1.0 0.0 1.0 2.0 3.0

Brookfield Renewable

SCANA Corporation

Aqua America

AES

American Water Works

Alliant Energy

CMS Energy

-90% -40% 10% 60%

Brookfield Renewable

SCANA Corporation

Aqua America

AES

American Water Works

Alliant Energy

CMS Energy

Dividend Return Multiple Return Earnings Outlook 1Yr Total Return

-25%

-25%

-23%

-16%

19%

22%

23%

30%

-40% -20% 0% 20% 40%

⇐ Negatives Positives ⇒

Earnings Stability

3m Recom. Revisions

Return on Assets NTM

BPS Growth FY1

IRR Dividend Disc. Model

Piotroski Score

Price to Book NTM

Price to Book FY1

0 1

Technicals & TradingRisk

LiquidityCapital & Funding

QualityPrice Momentum

Earnings MomentumProfitability

Growth

ValuationAlpha Model Score

-0.56-0.28

-1.03 0.28

-0.22-0.26

0.00-0.15 0.07

0.18 0.29

0 1

Normalized

Score

0 50 100

Percentile relative

to sector(/433)

0 50 100

Percentile relative

to market(/430)

Macquarie Research Brookfield Renewable

1 February 2017 19

Important disclosures:

Recommendation definitions

Macquarie - Australia/New Zealand Outperf orm – return >3% in excess of benchmark return

Neutral – return within 3% of benchmark return Underperf orm – return >3% below benchmark return

Benchmark return is determined by long term nominal GDP growth plus 12 month f orward market div idend y ield

Macquarie – Asia/Europe Outperf orm – expected return >+10%

Neutral – expected return f rom -10% to +10% Underperf orm – expected return <-10%

Macquarie – South Africa Outperf orm – expected return >+10%

Neutral – expected return f rom -10% to +10% Underperf orm – expected return <-10%

Macquarie - Canada Outperf orm – return >5% in excess of benchmark return

Neutral – return within 5% of benchmark return Underperf orm – return >5% below benchmark return

Macquarie - USA Outperf orm (Buy ) – return >5% in excess of Russell 3000 index return

Neutral (Hold) – return within 5% of Russell 3000 index

return

Underperf orm (Sell)– return >5% below Russell 3000 index return

Volatility index definition*

This is calculated f rom the v olatility of historical price

mov ements.

Very high–highest risk – Stock should be expected

to mov e up or down 60–100% in a y ear – inv estors

should be aware this stock is highly speculativ e.

High – stock should be expected to mov e up or

down at least 40–60% in a y ear – inv estors should

be aware this stock could be speculativ e.

Medium – stock should be expected to mov e up or

down at least 30–40% in a y ear.

Low–medium – stock should be expected to mov e

up or down at least 25–30% in a y ear.

Low – stock should be expected to mov e up or down at least 15–25% in a y ear.

* Applicable to Asia/Australian/NZ/Canada stocks

only

Recommendations – 12 months

Note: Quant recommendations may dif f er from

Fundamental Analy st recommendations

Financial definitions

All "Adjusted" data items hav e had the f ollowing

adjustments made:

Added back: goodwill amortisation, prov ision f or catastrophe reserv es, IFRS deriv ativ es & hedging, IFRS

impairments & IFRS interest expense

Excluded: non recurring items, asset rev als, property rev als, appraisal v alue uplif t, pref erence div idends &

minority interests

EPS = adjusted net prof it / ef powa* ROA = adjusted ebit / av erage total assets

ROA Banks/Insurance = adjusted net prof it /av erage

total assets

ROE = adjusted net prof it / av erage shareholders f unds Gross cashflow = adjusted net prof it + depreciation

*equiv alent f ully paid ordinary weighted av erage number

of shares

All Reported numbers f or Australian/NZ listed stocks are

modelled under IFRS (International Financial Reporting

Standards).

Recommendation proportions – For quarter ending 31 December 2016

AU/NZ Asia RSA USA CA EUR Outperf orm 57.53% 50.72% 45.57% 42.28% 60.58% 52.79% (for global coverage by Macquarie, 8.71% of stocks followed are investment banking clients)

Neutral 33.90% 33.97% 43.04% 50.11% 37.23% 35.62% (for global coverage by Macquarie, 8.05% of stocks followed are investment banking clients) Underperf orm 8.56% 15.30% 11.39% 7.61% 2.19% 11.59% (for global coverage by Macquarie, 4.63% of stocks followed are investment banking clients)

BEP-U CN vs TSX, & rec history

(all f igures in CAD currency unless noted)

BEP US vs S&P 500, & rec history

(all f igures in USD currency unless noted)

TERP US vs S&P 500, & rec history

(all f igures in USD currency unless noted)

GLBL US vs S&P 500, & rec history

(all f igures in USD currency unless noted)

Note: Recommendation timeline – if not a continuous line, then there was no Macquarie coverage at the time or there was an embargo period.

Source: FactSet, Macquarie Capital (USA), February 2017

12-month target price methodology

BEP-U CN: C$43.00 based on a combination of 13.75x EV/2018E EBITDA and a 5.75% target yield on our 2018E dividend of $2.04/sh. methodology

BEP US: US$33.00 based on a DDM methodology

TERP US: US$14.00 based on a NAV methodology

GLBL US: US$4.00 based on a NAV methodology

Company-specific disclosures: TERP US: Macquarie Capital (USA) Inc. or one of its aff iliates, expects to receive or intends to seek compensation for investment banking services from Terraform Pow er Inc in the next three months. MACQUARIE CAPITAL (USA) INC or one of its aff iliates managed or co-managed a public offering of securities of TerraForm Pow er Inc in the past 24 months, for w hich it received compensation.

Macquarie Research Brookfield Renewable

1 February 2017 20

SUNE US: Macquarie Capital (USA) Inc. or one of its aff iliates, expects to receive or intends to seek compensation for investment banking services from Sunedison Inc in the next three months. MACQUARIE CAPITAL (USA) INC or one of its aff iliates managed or co-managed a public offering of securities of Sunedison Inc in the past 24 months, for w hich it received compensation. MACQUARIE CAPITAL (USA) INC or one of its aff iliates managed or co-managed a public offering of securities of SunEdison Inc in the past 24 months, for w hich it received compensation. TERP US: Macquarie Capital (USA) Inc. or one of its aff iliates, expects to receive or intends to seek compensation for investment banking services f rom Terraform Pow er Inc in the next three months. MACQUARIE CAPITAL (USA) INC or one of its aff iliates managed or co-managed a public offering of securities of TerraForm Pow er Inc in the past 24 months, for w hich it received compensation. Important disclosure information regarding the subject companies covered in this report is available at w ww.macquarie.com/research/disclosures.

Date Stock Code (BBG code) Recommendation Target Price 08-Aug-2016 BEP-U CN Outperform C$43.00 25-Jan-2016 BEP-U CN Outperform C$40.00

23-Feb-2015 BEP-U CN Outperform C$42.00 18-Sep-2014 BEP-U CN Outperform C$39.00

Target price risk disclosures: BEP-U CN: Risks to the dow nside include higher market interest rates, diff iculties in achieving increased eff iciencies, inflation of the value of potential M&A targets. Risks to the upside include low er market interest rates, increased pace of acquisitions driving faster growth in div idends. BEP US: Our US$33 TP is based on our DDM model w hich assumes a 6% discount rate and a 2% terminal grow th rate. Risks to the dow nside include higher market interest rates, diff iculties in achieving increased eff iciencies, inflation of the value of potential M&A targets. Risks to the upside include low er market interest rates, increased pace of acquisitions driving faster growth in dividends. TERP US: Our US$14.00 TP is based on run-rate CAFD of US$180m and a w ind-based multiple of 11x. Risks to the dow nside include inability to get a new sponsor and delever the balance sheet. GLBL US: GLBL's ongoing operations are vulnerable to w eaker than expected solar/wind/hydro resources in its operating geographies, as w ell as political/regulatory risk w ith regards to its contracts, and foreign exchange/inflation risk. GLBL's grow th is very capital intensive and is entirely dependent on the cost of and access to debt and equity f inancing.

Analyst certification: We hereby certify that all of the view s expressed in this report accurately reflect our personal views about the subject company or companies and its or their securities. We also certify that no part of our compensation w as, is or w ill be, directly or indirectly, related to the spec if ic recommendations or views

expressed in this report. The Analysts responsible for preparing this report receive compensation from Macquarie that is based upon various factors including Macquarie Group Ltd total revenues, a portion of w hich are generated by Macquarie Group’s Investment Banking activities. General disclaimers: Macquarie Securities (Australia) Ltd; Macquarie Capital (Europe) Ltd; Macquarie Capital Markets Canada Ltd; Macquarie Capital Markets North America Ltd;

Macquarie Capital (USA) Inc; Macquarie Capital Limited and Macquarie Capital Limited, Taiw an Securities Branch; Macquarie Capital Securities (Singapore) Pte Ltd; Macquarie Securities (NZ) Ltd; Macquarie Equities South Africa (Pty) Ltd; Macquarie Capital Securities (India) Pvt Ltd; Macquarie Capital Securities (Malaysia) Sdn Bhd; Macquarie Securities Korea Limited and Macquarie Securities (Thailand) Ltd are not authorized deposit-taking institutions for the purposes of the Banking Act 1959 (Commonw ealth of Australia), and their obligations do not represent deposits or other liabilities of Macquarie Bank Limited

ABN 46 008 583 542 (MBL) or MGL. MBL does not guarantee or otherw ise provide assurance in respect of the obligations of any of the above mentioned entities. MGL provides a guarantee to the Monetary Authority of Singapore in respect of the obligations and liabilities of Macquarie Capital Securities (Singapore) Pte Ltd for up to SGD 35 million. This research has been prepared for the general use of the w holesale clients of the Macquarie Group and must not be copied, either in w hole or in part, or distributed to any other person. If you are not the intended recipient you must not use or disclose the

information in this research in any w ay. If you received it in error, please tell us immediately by return e-mail and delete the document. We do not guarantee the integrity of any e-mails or attached files and are not responsible for any changes made to them by any other person. MGL has established and implemented a conflicts policy at group level (w hich may be revised and updated from time to time) (the "Conflicts Policy") pursuant to regulatory

requirements (including the FCA Rules) w hich sets out how we must seek to identify and manage all material conflicts of interest. Nothing in this research shall be construed as a solicitation to buy or sell any security or product, or to engage in or refrain from engaging in any transaction. In preparing this research, we did not take into account your investment objectives, f inancial situation or particular needs. Macquarie salespeople, traders and other professionals may provide oral or w ritten market commentary or trading strategies to our clients that reflect opinions w hich are contrary to the opinions

expressed in this research. Macquarie Research produces a variety of research products including, but not limited to, fundamental analysis, macro-economic analysis, quantitative analysis, and trade ideas. Recommendations contained in one type of research product may differ from r ecommendations contained in other types of research, whether as a result of differing time horizons, methodologies, or otherw ise. Before making an investment decision on the basis of this research, you need to consider, w ith or without the assistance of an adviser, whether the advice is appropriate in light of your particular investment

needs, objectives and f inancial circumstances. There are risks involved in securities trading. The price of securities can and does f luctuate, and an individual security may even become valueless. International investors are reminded of the additional risks inherent in international investments, such as currency f luctuations and international stock market or economic conditions, w hich may adversely affect the value of the investment. This research is based on information obtained from sources believed to be reliable but w e do not make any representation or w arranty that it is accurate, complete or up to date. We

accept no obligation to correct or update the information or opinions in it. Opinions expressed are subject to change w ithout notice. No member of the Macquarie Group accepts any liability w hatsoever for any direct, indirect, consequential or other loss arising from any use of this research and/or further communication in relation to this research. Clients should contact analysts at, and execute transactions through, a Macquarie Group entity in their home jurisdiction unless governing law permits otherw ise. The date and timestamp for above share price and market cap is the closed price of the price date.

#CLOSE is the f inal price at w hich the security is traded in the relevant exchange on the date indicated. Country-specific disclaimers: Australia: In Australia, research is issued and distributed by Macquarie Securities (Australia) Ltd (AFSL No. 238947), a participating organisation of the

Australian Securities Exchange. New Zealand: In New Zealand, research is issued and distributed by Macquarie Securities (NZ) Ltd, a NZX Firm. Canada: In Canada, research is prepared, approved and distributed by Macquarie Capital Markets Canada Ltd, a participating organisation of the Toronto Stock Exchange, TSX Venture Exchange & Montréal Exchange. Macquarie Capital Markets North America Ltd., w hich is a registered broker-dealer and member of FINRA, accepts responsibility for the contents of reports issued by Macquarie Capital Markets Canada Ltd in the United States and sent to US persons. Any

US person w ishing to effect transactions in the securities described in the reports issued by Macquarie Capital Markets Canada Ltd should do so w ith Macquarie Capital Markets North America Ltd. The Research Distribution Policy of Macquarie Capital Markets Canada Ltd is to allow all clients that are entitled to have equal access to our research. United Kingdom: In the United Kingdom, research is issued and distributed by Macquarie Capital (Europe) Ltd, w hich is authorised and regulated by the Financial Conduct Authority (No. 193905). Germany: In Germany, this research is issued and/or distributed by

Macquarie Capital (Europe) Limited, Niederlassung Deutschland, w hich is authorised and regulated by the UK Financial Conduct Authority (No. 193905). and in Germany by BaFin. France : In France, research is issued and distributed by Macquarie Capital (Europe) Ltd, w hich is authorised and regulated in the United Kingdom by the Financial Conduct Authority (No. 193905). Hong Kong & Mainland China: In Hong Kong, research is issued and distributed by Macquarie Capital Limited, w hich is licensed and regulated by the Securities and Futures Commission. In Mainland China, Macquarie Securities (Australia)

Limited Shanghai Representative Office only engages in non-business operational activities excluding issuing and distributing research. Only non-A share research is distributed into Mainland China by Macquarie Capital Limited. Japan: In Japan, research is Issued and distributed by Macquarie Capital Securities (Japan) Limited, a member of the Tokyo Stock Exchange, Inc. and Osaka Exchange, Inc. (Financial Instruments Firm, Kanto Financial Bureau

(kin-sho) No. 231, a member of Japan Securities Dealers Association). India: In India, research is issued and distributed by Macquarie Capital Securities (India) Pvt. Ltd. (CIN: U65920MH1995PTC090696), 92, Level 9, 2 North Avenue, Maker Maxity, Bandra Kurla Complex, Bandra (East), Mumbai – 400 051, India, w hich is a SEBI registered Research Analyst having registration no. INH000000545. Malaysia: In Malaysia, research is issued and distributed by Macquarie Capital Securities (Malaysia) Sdn. Bhd. (Company registration number: 463469-W) w hich is a Participating Organisation of Bursa Malaysia

Macquarie Research Brookfield Renewable

1 February 2017 21

Berhad and a holder of Capital Markets Services License issued by the Securities Commission. Taiwan: In Taiw an, research is issued and distributed by

Macquarie Capital Limited, Taiw an Securities Branch, w hich is licensed and regulated by the Financial Supervisory Commission. No portion of the report may be reproduced or quoted by the press or any other person w ithout authorisation from Macquarie. Nothing in this research shall be construed as a solicitation to buy or sell any security or product. The recipient of this report shall not engage in any activities w hich may give rise to potential conflicts of interest to the report. Research Associate(s) in this report w ho are registered as Clerks only assist in the preparation of research and are not engaged in

w riting the research. Thailand: In Thailand, research is produced, issued and distributed by Macquarie Securities (Thailand) Ltd. Macquarie Securities (Thailand) Ltd. is a licensed securities company that is authorized by the Ministry of Finance, regulated by the Securities and Exchange Commission of Thailand and is an exchange member of the Stock Exchange of Thailand. The Thai Institute of Directors Association has disclosed the Corporate

Governance Report of Thai Listed Companies made pursuant to the policy of the Securities and Exchange Commission of Thailand. Macquarie Securities (Thailand) Ltd does not endorse the result of the Corporate Governance Report of Thai Listed Companies but this Report can be accessed at: http://www.thai-iod.com/en/publications.asp?type=4. South Korea: In South Korea, unless otherw ise stated, research is prepared, issued and distributed by Macquarie Securities Korea Limited, w hich is regulated by the Financial Supervisory Services. Information on analysts in MSKL is disclosed at

http://dis.kofia.or.kr/websquare/index.jsp?w2xPath=/wq/fundMgr/DISFundMgrAnalystStut.xml&divisionId=MDIS03002001000000&serviceId=SDIS03002001000. South Africa: In South Africa, research is issued and distributed by Macquarie Equities South Africa (Pty) Ltd, a member of the JSE Limited. Singapore: In Singapore, research is issued and distributed by Macquarie Capital Securities (Singapore) Pte Ltd (Company Registration Number: 198702912C), a Capital Markets Services license holder under the Securities and Futures Act to deal in securities and provide custodial services in

Singapore. Pursuant to the Financial Advisers (Amendment) Regulations 2005, Macquarie Capital Securities (Singapore) Pte Ltd is exempt from complying w ith sections 25, 27 and 36 of the Financial Advisers Act. All Singapore-based recipients of research produced by Macquarie Capital (Europe) Limited, Macquarie Capital Markets Canada Ltd, Macquarie Equities South Africa (Pty) Ltd and Macquarie Capital (USA) Inc. represent and w arrant that they are institutional investors as defined in the Securities and Futures Act. United States: In the United States, research is issued and distributed by Macquarie

Capital (USA) Inc., w hich is a registered broker-dealer and member of FINRA. Macquarie Capital (USA) Inc, accepts responsibility for the content of each research report prepared by one of its non-US aff iliates when the research report is distributed in the United States by Macquarie Capital (USA) Inc. Macquarie Capital (USA) Inc.’s aff iliate’s analysts are not registered as research analysts with FINRA, may not be associated persons of Macquarie Capital

(USA) Inc., and therefore may not be subject to FINRA rule restrictions on communications w ith a subject company, public appearances, and trading securities held by a research analyst account. Information regarding futures is provided for reference purposes only and is not a solicitation for purchases or sales of futures. Any persons receiving this report directly from Macquarie Capital (USA) Inc. and w ishing to effect a transaction in any security described herein should do so w ith Macquarie Capital (USA) Inc. Important disclosure information regarding the subject companies covered in this report is available

at www.macquarie.com/research/disclosures, or contact your registered representative at 1-888-MAC-STOCK, or w rite to the Supervisory Analysts, Research Department, Macquarie Securities, 125 W.55th Street, New York, NY 10019. © Macquarie Group

Research Heads of Equity Research

Peter Redhead (Global - Head) (852) 3922 4836 Christine Farkas (US) (1 212) 231 6668 Greg MacDonald (Canada) (1 416) 628 3934

Consumer

Chad Beynon (Head of US Consumer) (1 212) 231 2634 Bob Summers (New York) (1 212) 231 1072 Laurent Vasilescu (New York) (1 212) 231 8046

Emerging Leaders – Consumer Discretionary

Matthew Brooks (New York) (1 212) 231 1585

Autos

Takuo Katayama (New York) (1 212) 231 1757

Energy

Oil & Gas

Vikas Dwivedi (Head of Oil & Gas, Global Energy Strategist) (1 713) 275 6352 Iain Reid (London) (44 20) 3037 2119

US Exploration & Production

Paul Grigel (Denver) (1 303) 952 2754

US Refining

Vikas Dwivedi (Head of Oil & Gas, Global Energy Strategist) (1 713) 275 6352

Oilfield Services

Walt Chancellor (Houston) (1 713) 275 6230

International/Canadian Oil & Gas Producers

Brian Bagnell (Calgary) (1 403) 539 8540 Brian Kristjansen (Calgary) (1 403) 539 8508 Tom Hems (Calgary) (1 403) 218 6666

Energy Infrastructure

David Noseworthy (New York) (1 212) 231 6681

Financials

Banks/Trust Banks

David Konrad (New York) (1 212) 231 0525 John Moran (Denver) (1 212) 231 0662 Jason Bilodeau (Toronto) (1 416) 848 3687

Regional Brokerage/Debt Collection

Hugh Miller (New York) (1 212) 231 2323

Financials

Property & Casualty Insurance

Amit Kumar (New York) (1 212) 231 8013

Industrials

Building Products

Adam Baumgarten (New York) (1 212) 231 0633

Business Services

Hamzah Mazari (New York) (1 212) 231 2442

Chemicals

Cooley May (Head of US Basics & Industrials) (1 212) 231 2586

Diversified Industrials

Jamie Clement (New York) (1 212) 231 0452 Michael Glen (Montreal) (1 514) 905 3636

Construction & Engineering/Machinery

Sameer Rathod (San Francisco) (1 415) 762 5034 John D’Angelo (Boca Raton) (1 415) 732 5038

Paper & Packaging

Danny Moran (New York) (1 212) 231 0698

Transports

Konark Gupta (Toronto) (1 416) 848 3539

Materials

Steel & Metals

Aldo Mazzaferro (New York) (1 212) 231 0693

Emerging Leaders – Basic Materials

Anthony Young (Boca Raton) (1 212) 231 2612

Global Metals & Mining

Michael Siperco (Toronto) (1 416) 848 3520 Matt Murphy (Toronto) (1 416) 848 3541 Michael Gray (Vancouver) (1 604) 639 6372

Technology

Gus Papageorgiou (Toronto) (1 416) 848 3512

TMET

Telecommunications

Amy Yong (New York) (1 212) 231 2624 Greg MacDonald (Toronto) (1 416) 628 3934

Cable, Satellite & Entertainment

Amy Yong (New York) (1 212) 231 2624 Andrew DeGasperi (New York) (1 212) 231 0649

Internet

Ben Schachter (New York) (1 212) 231 0644 Tom White (New York) (1 212) 231 0643

Media & Entertainment

Tim Nollen (New York) (1 212) 231 0635

Software

Sarah Hindlian (New York) (1 212) 231 1371

Utilities & Alternative Energy

Angie Storozynski (Head of US Utilities & Alternative Energy) (1 212) 231 2569 Andrew Weisel (New York) (1 212) 231 1159 James Ward (New York) (1 212) 231 0707 David Noseworthy (New York) (1 212) 231 6681

Commodities & Precious Metals

Colin Hamilton (Global) (44 20) 3037 4061 Jim Lennon (London) (44 20) 3037 4271

Economics and Strategy

David Doyle (Toronto) (1 416) 848 3663

Quantitative Analysis

Gurvinder Brar (Mumbai) (9197) 8055 5902 Steve Gao (London) (44 20) 3037 2765 Giuliano De Rossi (London) (44 20) 3037 1997

Find our research at

Macquarie: www.macquarieresearch.com/ideas/

Thomson: www.thomson.com/financial

Reuters: www.knowledge.reuters.com

Bloomberg: MAC GO

Factset: http://www.factset.com/home.aspx

CapitalIQ www.capitaliq.com

Contact [email protected] for access requests.

Email addresses

Equities Head of Global Cash Equities

Mark Duncan (852) 3922 5888

Head of US Equities

Robert Ansell (New York) (1 212) 231 0888

Head of Canadian Equities

David Washburn (Toronto) (1 416) 848 3631

Sales US Sales

Khristina McLaughlin (New York) (1 212) 231 8012 Jeff Evans (Boston) (1 617) 598 2508 Lisa Sowell (Atlanta) (1 212) 231 1787 Simon Barrington (London) (44 20) 3037 4927 Troy Pilalas (San Francisco) (1 415) 762 5025

Canada Sales

David Ricciardelli (Toronto) (1 416) 572 7150

Trading US Sales Trading

J.T. Cacciabaudo (New York) (1 212) 231 6381

Canada Trading

Perry Catellier (Co-head, Toronto) (1 416) 848 3619

Michael O'Rourke (Co-head, Toronto) (1 416) 848 3633

International Sales Trading

Mike Gray (New York) (1 212) 231 0928

This publication was disseminated on 01 February 2017 at 16:19 UTC.