Embed Size (px)

Citation preview

Canada Research Published by Raymond James Ltd.

Please read domestic and foreign disclosure/risk information beginning on page 27 and Analyst Certification on page 26. Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Sleep Country Canada Holdings Inc. August 20, 2015 ZZZ-TSX Company Report - Initiation of Coverage Kenric S. Tyghe MBA | 416.777.7188 | [email protected]

Krisztina Katai (Associate) | 416.777.7060 | [email protected]

Consumer & Retail

(Mattress) Size Matters; (Massive) Sheet Margins

Recommendation We are initiating coverage of Sleep Country Canada Holdings (Sleep Country) with a Market Perform rating and a $16.00 target price. While recent performance has been impressive (underpinned by strong SSS growth, higher gross margins and improved SG&A leverage), and long-term industry fundamentals appear attractive, we are mindful of a number of key headwinds through our forecast window. While the long-term mattress industry fundamentals are at face value supportive of a more positive bias (and the economics of the model are particularly attractive), the nature of the business (big ticket and infrequent purchase) gives us pause (on tough comps and a weak macro backdrop). The 2014 SSS increase of 8.3% was a on a weak 2013 comp of 1.0%, for 2-year stacked SSS growth of 4.7%. The 4.5% midpoint (long-term guidance is 3.0%-6.0%) imputes a further moderation (versus the 2-year comp) of SSS momentum through our forecast. The new store format rollout and strong (higher margin) bedding accessories traction, while broadly positive, are not without risk in our opinion, as key competitors (most notably in the accessories category) are going to try to steal back the duvet.

Analysis While industry fundamentals are solid, and Sleep Country is the leading specialty

bedding Retailer with a 23% national share, traffic remains a little challenged. An improvement in SSS growth attribution would be incrementally positive.

The attractive economics of the model impute few barriers to entry, however as many a new entrant has discovered, Sleep Country is an adept competitor. The revamped advertising strategy delivered compelling SSS improvements through 2Q15.

We are conservatively modelling 2016E SSS growth of 4.3% (long-term guidance is 3.0%-6.0%) for 2016E EBITDA of $67.3 mln, to which we apply a 10.0x multiple. Our EBITDA estimates are based on sales of $468.7 mln, modest further gross margin expansion to 27.3% and improved SG&A leverage on margins to 12.9%.

Valuation

We are initiating coverage of Sleep Country with a Market Perform rating and $16.00 target price. Our target price of $16.00 is based on the average of our EV/EBITDA and DCF valuation, for an implied value of $16.37. We apply a target EV/EBITDA multiple of 10.0x to our 2016E EBITDA of $67.3 mln, which is essentially in-line with the US mattress peer group average of 9.6x, and below US leading specialty mattress retailer Mattress Firm’s 3-year average of 12.0x. See our Valuation & Recommendation section for details.

EPS 1Q 2Q 3Q 4Q Full Revenues EBITDA Mar Jun Sep Dec Year (mln) (mln)

2014A C$0.03 C$0.10 C$0.26 C$0.30 C$0.58 C$396 C$51

2015E 0.13A 0.20A 0.23 0.36 0.92 433 62

2016E 0.14 0.19 0.26 0.39 0.99 469 67

2017E 0.16 0.21 0.28 0.43 1.08 504 73

Source: Raymond James Ltd., Thomson ONE

Market Perform 3 C$16.00 target price

Current Price ( Aug-18-15 ) C$15.02 Total Return to Target 7% 52-Week Range C$17.20 - C$14.76 Suitability Total Return

Market Data Market Capitalization (mln) C$564 Current Net Debt (mln) C$133 Enterprise Value (mln) C$697 Shares Outstanding (mln, f.d.) 38.0 Dividend/Yield C$0.44/2.9% 10 Day Avg Daily Volume (000s) 104

Key Financial Metrics 2014A 2015E 2016E 2017E

P/E 25.9x 16.3x 15.2x 13.9x

EV/EBITDA 13.8x 11.3x 10.4x 9.6x

Company Description Sleep Country is Canada's leading mattress retailer with a national footprint, commanding an estimated 23% national market share, under the Sleep Country and Dormez-vous? Retail banners.

Canada Research | Page 2 of 31 Sleep Country Canada Holdings Inc.

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Table of Contents

Sleep Country Canada Tear Sheet........................................................................................................................ 3

Executive Summary ............................................................................................................................................. 4

Company Overview .............................................................................................................................................. 5

Investment Thesis ................................................................................................................................................ 7

Financial Analysis & Outlook................................................................................................................................ 16

Valuation & Recommendation ............................................................................................................................ 18

Appendix A: Financial Statements ....................................................................................................................... 20

Appendix B: Management & Board of Directors ................................................................................................. 23

Risks ..................................................................................................................................................................... 24

Sleep Country Canada Holdings Inc. Canada Research | Page 3 of 31

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

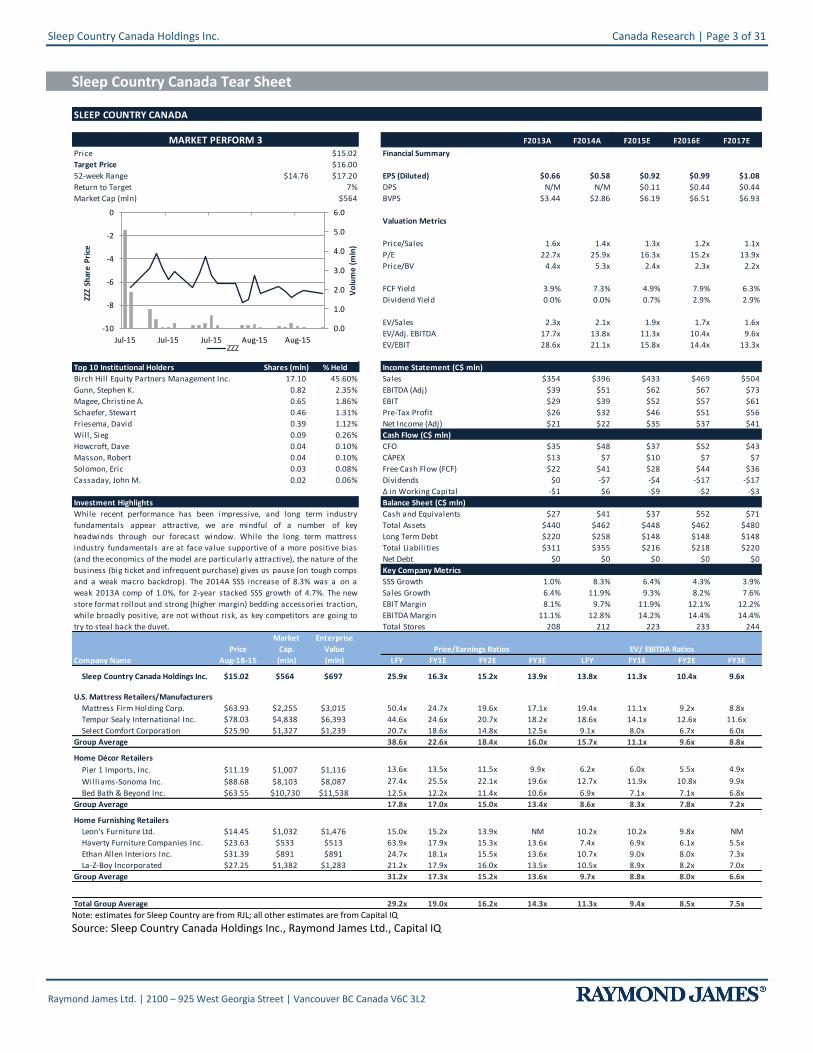

Sleep Country Canada Tear Sheet

SLEEP COUNTRY CANADA TSX:ZZZ

F2013A F2014A F2015E F2016E F2017E

Price $15.02 Financial Summary 12/31/2011 12/31/2013 12/31/2014 12/31/2015 12/30/2016 12/30/2017

Target Price $16.00

52-week Range $14.76 $17.20 EPS (Diluted) $0.66 $0.58 $0.92 $0.99 $1.08

Return to Target 7% DPS N/M N/M $0.11 $0.44 $0.44

Market Cap (mln) $564 BVPS $3.44 $2.86 $6.19 $6.51 $6.93

Valuation Metrics

Price/Sales 1.6x 1.4x 1.3x 1.2x 1.1x

P/E 22.7x 25.9x 16.3x 15.2x 13.9x

Price/BV 4.4x 5.3x 2.4x 2.3x 2.2x

FCF Yield 3.9% 7.3% 4.9% 7.9% 6.3%

Dividend Yield 0.0% 0.0% 0.7% 2.9% 2.9%

EV/Sales 2.3x 2.1x 1.9x 1.7x 1.6x

EV/Adj. EBITDA 17.7x 13.8x 11.3x 10.4x 9.6x

EV/EBIT 28.6x 21.1x 15.8x 14.4x 13.3x

37.5 37.5 37.5 37.5 37.5

Top 10 Institutional Holders Shares (mln) % Held Income Statement (C$ mln)

Birch Hill Equity Partners Management Inc. 17.10 45.60% Sales $354 $396 $433 $469 $504

Gunn, Stephen K. 0.82 2.35% EBITDA (Adj) $39 $51 $62 $67 $73

Magee, Christine A. 0.65 1.86% EBIT $29 $39 $52 $57 $61

Schaefer, Stewart 0.46 1.31% Pre-Tax Profit $26 $32 $46 $51 $56

Friesema, David 0.39 1.12% Net Income (Adj) $21 $22 $35 $37 $41

Will, Sieg 0.09 0.26% Cash Flow (C$ mln)

Howcroft, Dave 0.04 0.10% CFO $35 $48 $37 $52 $43

Masson, Robert 0.04 0.10% CAPEX $13 $7 $10 $7 $7

Solomon, Eric 0.03 0.08% Free Cash Flow (FCF) $22 $41 $28 $44 $36

Cassaday, John M. 0.02 0.06% Dividends $0 -$7 -$4 -$17 -$17

Δ in Working Capital -$1 $6 -$9 -$2 -$3

Investment Highlights Balance Sheet (C$ mln)

Cash and Equivalents $27 $41 $37 $52 $71

Total Assets $440 $462 $448 $462 $480

Long Term Debt $220 $258 $148 $148 $148

Total Liabilities $311 $355 $216 $218 $220

Net Debt $0 $0 $0 $0 $0

Key Company Metrics

SSS Growth 1.0% 8.3% 6.4% 4.3% 3.9%

Sales Growth 6.4% 11.9% 9.3% 8.2% 7.6%

EBIT Margin 8.1% 9.7% 11.9% 12.1% 12.2%

EBITDA Margin 11.1% 12.8% 14.2% 14.4% 14.4%

Total Stores 208 212 223 233 244

Market

Price Cap.

Company Name Aug-18-15 (mln) LFY FY1E FY2E FY3E LFY FY1E FY2E FY3E1000 1001 1002 1003 1002 1000 1001 1002

Sleep Country Canada Holdings Inc. $15.02 $564 $697 TSX:ZZZ 25.9x 16.3x 15.2x 13.9x 13.8x 11.3x 10.4x 9.6x

U.S. Mattress Retailers/Manufacturers

Mattress Firm Holding Corp. $63.93 $2,255 $3,015 MFRM 50.4x 24.7x 19.6x 17.1x 19.4x 11.1x 9.2x 8.8x

Tempur Sealy International Inc. $78.03 $4,838 $6,393 TPX 44.6x 24.6x 20.7x 18.2x 18.6x 14.1x 12.6x 11.6x

Select Comfort Corporation $25.90 $1,327 $1,239 SCSS 20.7x 18.6x 14.8x 12.5x 9.1x 8.0x 6.7x 6.0x

Group Average 38.6x 22.6x 18.4x 16.0x 15.7x 11.1x 9.6x 8.8x

Home Décor Retailers

Pier 1 Imports, Inc. $11.19 $1,007 $1,116 PIR 13.6x 13.5x 11.5x 9.9x 6.2x 6.0x 5.5x 4.9x

Williams-Sonoma Inc. $88.68 $8,103 $8,087 WSM 27.4x 25.5x 22.1x 19.6x 12.7x 11.9x 10.8x 9.9x

Bed Bath & Beyond Inc. $63.55 $10,730 $11,538 BBBY 12.5x 12.2x 11.4x 10.6x 6.9x 7.1x 7.1x 6.8x

Group Average 17.8x 17.0x 15.0x 13.4x 8.6x 8.3x 7.8x 7.2x

Home Furnishing Retailers

Leon's Furniture Ltd. $14.45 $1,032 $1,476 TSX: LNF 15.0x 15.2x 13.9x NM 10.2x 10.2x 9.8x NM

Haverty Furniture Companies Inc. $23.63 $533 $513 HVT 63.9x 17.9x 15.3x 13.6x 7.4x 6.9x 6.1x 5.5x

Ethan Allen Interiors Inc. $31.39 $891 $891 ETH 24.7x 18.1x 15.5x 13.6x 10.7x 9.0x 8.0x 7.3x

La-Z-Boy Incorporated $27.25 $1,382 $1,283 LZB 21.2x 17.9x 16.0x 13.5x 10.5x 8.9x 8.2x 7.0x

Group Average 31.2x 17.3x 15.2x 13.6x 9.7x 8.8x 8.0x 6.6x

Total Group Average 29.2x 19.0x 16.2x 14.3x 11.3x 9.4x 8.5x 7.5x

Price/Earnings Ratios EV/ EBITDA Ratios

MARKET PERFORM 3

Enterprise

Value

(mln)

While recent performance has been impressive, and long term industry

fundamentals appear attractive, we are mindful of a number of key

headwinds through our forecast window. While the long term mattress

industry fundamentals are at face value supportive of a more positive bias

(and the economics of the model are particularly attractive), the nature of the

business (big ticket and infrequent purchase) gives us pause (on tough comps

and a weak macro backdrop). The 2014A SSS increase of 8.3% was a on a

weak 2013A comp of 1.0%, for 2-year stacked SSS growth of 4.7%. The new

store format rollout and strong (higher margin) bedding accessories traction,

while broadly positive, are not without risk, as key competitors are going to

try to steal back the duvet.

0.0

1.0

2.0

3.0

4.0

5.0

6.0

-10

-8

-6

-4

-2

0

Jul-15 Jul-15 Jul-15 Aug-15 Aug-15

Vo

lum

e (

mln

)

ZZZ

Shar

e P

rice

ZZZ

Note: estimates for Sleep Country are from RJL; all other estimates are from Capital IQ

Source: Sleep Country Canada Holdings Inc., Raymond James Ltd., Capital IQ

Canada Research | Page 4 of 31 Sleep Country Canada Holdings Inc.

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Executive Summary

Mattress Retailing’s Attractive Economics

The essentially blind mattress purchase affords retailers both relatively high product gross margins and conversion (shopper to buyer conversion is approximately 59% at Sleep Country). In addition to the attractive gross margins, the just in time relationship with suppliers supports a negative working capital model, which helps fund growth. The reality is that the combination of the simplicity of the business, the ease with which the model can be replicated, and the benefit of the working capital of the model impute few barriers to entry (although size does matter in terms of advertising support and volume rebates from suppliers). However, while tickets to the game are cheap and plentiful, the incumbents are pretty adept players. As such, while the majors on balance do a good job of defending share, they have struggled to increase share (other than through consolidation). In terms of market concentration, the top 3 retailers in Canada command an approximate 55% market share (Sleep Country is the largest with an estimated 23% national market share). In comparison, the top 3 retailers in the US command a 33% share (Mattress Firm is the largest with an estimated 17%).

Momentum to Moderate

The strong (relative to management’s 5-7 year guidance of 3.0%-6.0%) 2014 performance, with SSS growth of 8.3%, is unlikely to see a repeat anytime soon, in our view. Sleep Country’s 2-year stacked SSS growth is 4.7% (1.7% on a stacked 3-year basis). While our 2015 estimates are based on SSS growth of 6.4% (above long-term guidance), our respective 2016 and 2017 estimates of 4.3% and 3.9% are both more consistent with the 2-year stacked performance (and at the lower end of management’s guidance). We believe that our conservative SSS estimates reflect the nature (infrequent) and cost (big ticket) of bedding purchases. Mattress purchases are impacted by the macro backdrop, as consumers can (if necessary) defer the purchase of a replacement mattress (which accounts for approximately 75% of industry volume, with life cycle events largely representing the balance of the market). We are also mindful that competitors will respond to Sleep Country’s revamped advertising strategy (and increased advertising spend), potentially increasing competitive intensity. While the increased advertising spend in market could increase competitive intensity, a mitigating factor is the reality that a number of key competitors have either curtailed (or scaled back) their planned bedding retail expansions.

Macro and Industry Growth

The Canadian market, despite its relative size, concentration and competitive intensity at Retail, exhibits very similar characteristics to the US and, as such (given the granularity of the available US versus Canadian data), we have largely referenced US data for the purposes of this report. While bedding industry units and sales have a strong positive correlation with a number of key economic variables, specifically, GDP, Consumer Confidence, and Housing, the replacement cycle nature of bedding purchases has made the industry generally resistant to deep or protracted declines.

According to the International Sleep Products Association (ISPA), during the past 20 years, bedding dollar sales have only decreased (on a year-over-year basis) in three years (2001, 2008, and 2009), though unit volumes have decreased seven times. In addition to its steady long-term dollar sales growth (with 20-year and 10-year US CAGRs of 6.0% and 4.3%, respectively), mattress (or bedding) retail (as detailed above) boasts attractive economics due to relatively high gross margins, lean inventory and meaningful support from manufacturers (in the form of both volume based rebates and advertising dollars). Average Unit Selling Price (AUSP) dynamics are of particular reference, with increases driven by a number of factors including larger mattress sizes (neither houses nor the inhabitants have been getting any smaller), changing consumer preferences (pillow tops and higher profile beds), and subsequent to the great recession (and the bifurcation of consumer) market share gains by premium-priced specialty sleep (non-innerspring) beds.

Mattress Store Density

Sleep Country’s sales per average store in 2014 were $1.9 mln (versus $2.0 mln in 2009). While sales per store have decreased, despite Sleep Country focusing its store openings on in-fill markets, its store density (162,000 people per store) is relatively low. Management is targeting growth in existing, satellite and new markets. The target growth of 50 to 70 net new stores over the next 5-7 years appears reasonable (perhaps even conservative) against the above backdrop, as it imputes exit density of 140,000 per store (versus US density of 84,000) across all markets. In a mature Retail landscape, the new store growth opportunity is attractive.

Sleep Country Canada Holdings Inc. Canada Research | Page 5 of 31

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Company Overview

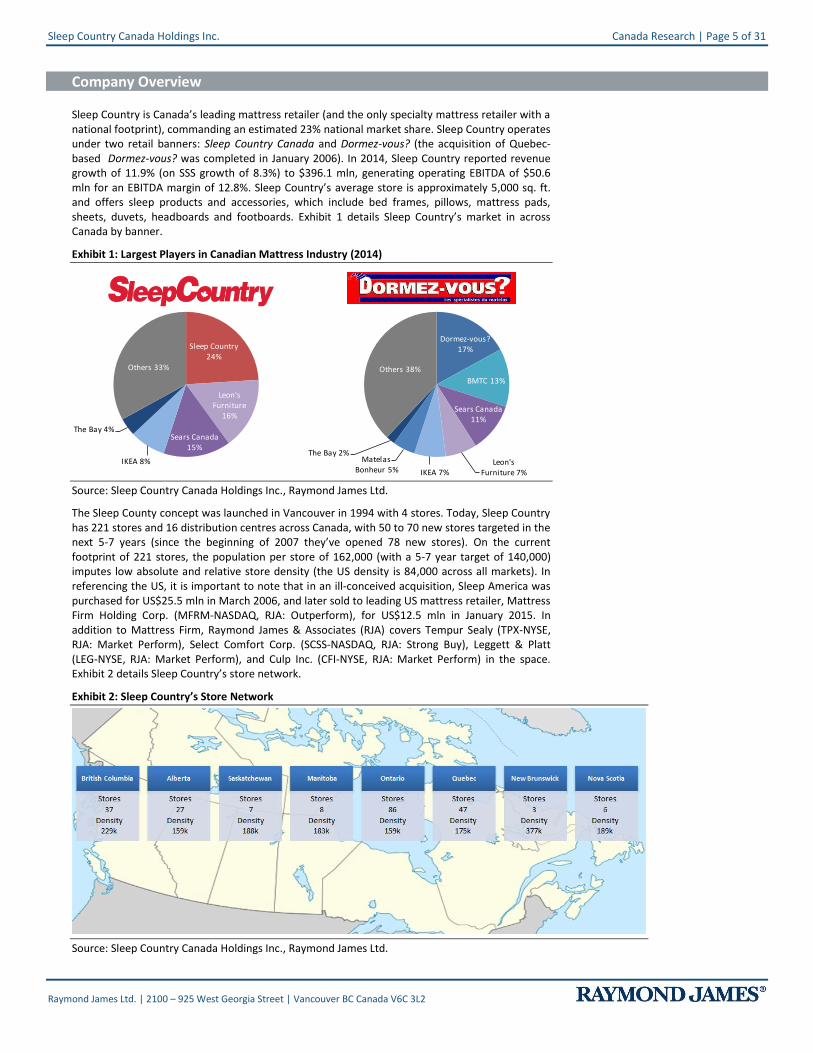

Sleep Country is Canada’s leading mattress retailer (and the only specialty mattress retailer with a national footprint), commanding an estimated 23% national market share. Sleep Country operates under two retail banners: Sleep Country Canada and Dormez-vous? (the acquisition of Quebec-based Dormez-vous? was completed in January 2006). In 2014, Sleep Country reported revenue growth of 11.9% (on SSS growth of 8.3%) to $396.1 mln, generating operating EBITDA of $50.6 mln for an EBITDA margin of 12.8%. Sleep Country’s average store is approximately 5,000 sq. ft. and offers sleep products and accessories, which include bed frames, pillows, mattress pads, sheets, duvets, headboards and footboards. Exhibit 1 details Sleep Country’s market in across Canada by banner.

Exhibit 1: Largest Players in Canadian Mattress Industry (2014)

Sleep Country 24%

Leon's Furniture

16%

Sears Canada 15%

IKEA 8%

The Bay 4%

Others 33%

Dormez-vous? 17%

BMTC 13%

Sears Canada 11%

Leon's Furniture 7%IKEA 7%

Matelas Bonheur 5%

The Bay 2%

Others 38%

Source: Sleep Country Canada Holdings Inc., Raymond James Ltd.

The Sleep County concept was launched in Vancouver in 1994 with 4 stores. Today, Sleep Country has 221 stores and 16 distribution centres across Canada, with 50 to 70 new stores targeted in the next 5-7 years (since the beginning of 2007 they’ve opened 78 new stores). On the current footprint of 221 stores, the population per store of 162,000 (with a 5-7 year target of 140,000) imputes low absolute and relative store density (the US density is 84,000 across all markets). In referencing the US, it is important to note that in an ill-conceived acquisition, Sleep America was purchased for US$25.5 mln in March 2006, and later sold to leading US mattress retailer, Mattress Firm Holding Corp. (MFRM-NASDAQ, RJA: Outperform), for US$12.5 mln in January 2015. In addition to Mattress Firm, Raymond James & Associates (RJA) covers Tempur Sealy (TPX-NYSE, RJA: Market Perform), Select Comfort Corp. (SCSS-NASDAQ, RJA: Strong Buy), Leggett & Platt (LEG-NYSE, RJA: Market Perform), and Culp Inc. (CFI-NYSE, RJA: Market Perform) in the space. Exhibit 2 details Sleep Country’s store network.

Exhibit 2: Sleep Country’s Store Network

Source: Sleep Country Canada Holdings Inc., Raymond James Ltd.

Canada Research | Page 6 of 31 Sleep Country Canada Holdings Inc.

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Sleep Country was listed on the TSX (as an income fund) between 2003 and 2008, when it was taken private at $22.00 per unit (a 37.1% premium to the trading price on August 13, 2008) by a group led by Birch Hill Equity Partners for $356.0 mln (which equated to a 8.2x EBITDA multiple). On July 16, 2015, Birch Hill Equity Partners and the co-investors again brought Sleep Country public through an IPO of 47% of the outstanding shares at $17.00 per share, for total gross proceeds of $300.0 mln (and a 11.8x EBITDA multiple). In connection with the offering, Sleep Country Canada Holdings Inc. also completed the acquisition of Sleep Country Canada Inc. and certain of its affiliates for an aggregate purchase price of $461.7 mln. The net proceeds of the offering were used by the company to satisfy a portion of the purchase price (the balance was satisfied by the issuance of shares and acquisition notes to certain of the shareholders of the acquired entities).

Mattresses represented approximately 80% of 2014 revenues, and bedding accessories, which include bedframes, pillows, mattress pad sheets, duvets, and headboards, accounted for 18%. Bedding accessories revenue has more than doubled in the last 8-years, with Sleep Country generating in excess of $73.0 mln in 2014, in what the company believes to be approximately an $830 mln market in Canada. While Sleep Country’s market share is essentially unchanged from when it was taken private in 2008 (an issue which we explore in the Investment Thesis section), the share gains in accessories (which boast a higher gross margin) are an incremental positive.

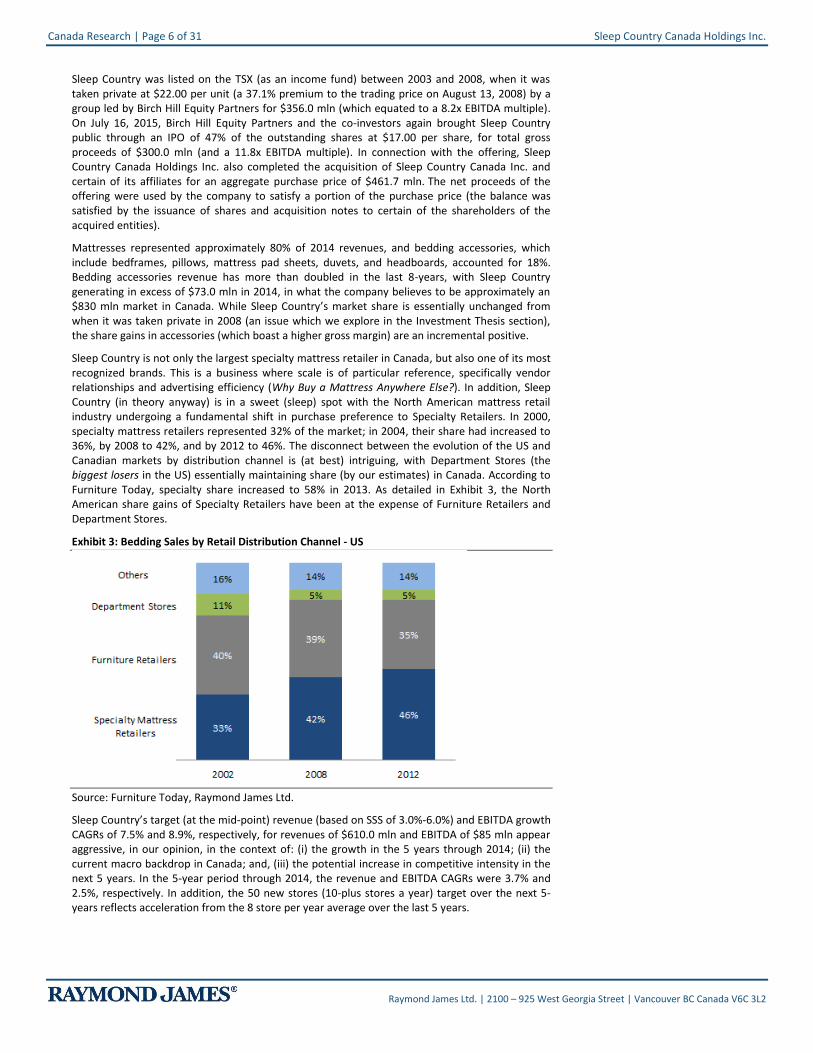

Sleep Country is not only the largest specialty mattress retailer in Canada, but also one of its most recognized brands. This is a business where scale is of particular reference, specifically vendor relationships and advertising efficiency (Why Buy a Mattress Anywhere Else?). In addition, Sleep Country (in theory anyway) is in a sweet (sleep) spot with the North American mattress retail industry undergoing a fundamental shift in purchase preference to Specialty Retailers. In 2000, specialty mattress retailers represented 32% of the market; in 2004, their share had increased to 36%, by 2008 to 42%, and by 2012 to 46%. The disconnect between the evolution of the US and Canadian markets by distribution channel is (at best) intriguing, with Department Stores (the biggest losers in the US) essentially maintaining share (by our estimates) in Canada. According to Furniture Today, specialty share increased to 58% in 2013. As detailed in Exhibit 3, the North American share gains of Specialty Retailers have been at the expense of Furniture Retailers and Department Stores.

Exhibit 3: Bedding Sales by Retail Distribution Channel - US

Source: Furniture Today, Raymond James Ltd.

Sleep Country’s target (at the mid-point) revenue (based on SSS of 3.0%-6.0%) and EBITDA growth CAGRs of 7.5% and 8.9%, respectively, for revenues of $610.0 mln and EBITDA of $85 mln appear aggressive, in our opinion, in the context of: (i) the growth in the 5 years through 2014; (ii) the current macro backdrop in Canada; and, (iii) the potential increase in competitive intensity in the next 5 years. In the 5-year period through 2014, the revenue and EBITDA CAGRs were 3.7% and 2.5%, respectively. In addition, the 50 new stores (10-plus stores a year) target over the next 5-years reflects acceleration from the 8 store per year average over the last 5 years.

Sleep Country Canada Holdings Inc. Canada Research | Page 7 of 31

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Investment Thesis

Sizing and Economic Sensitivity

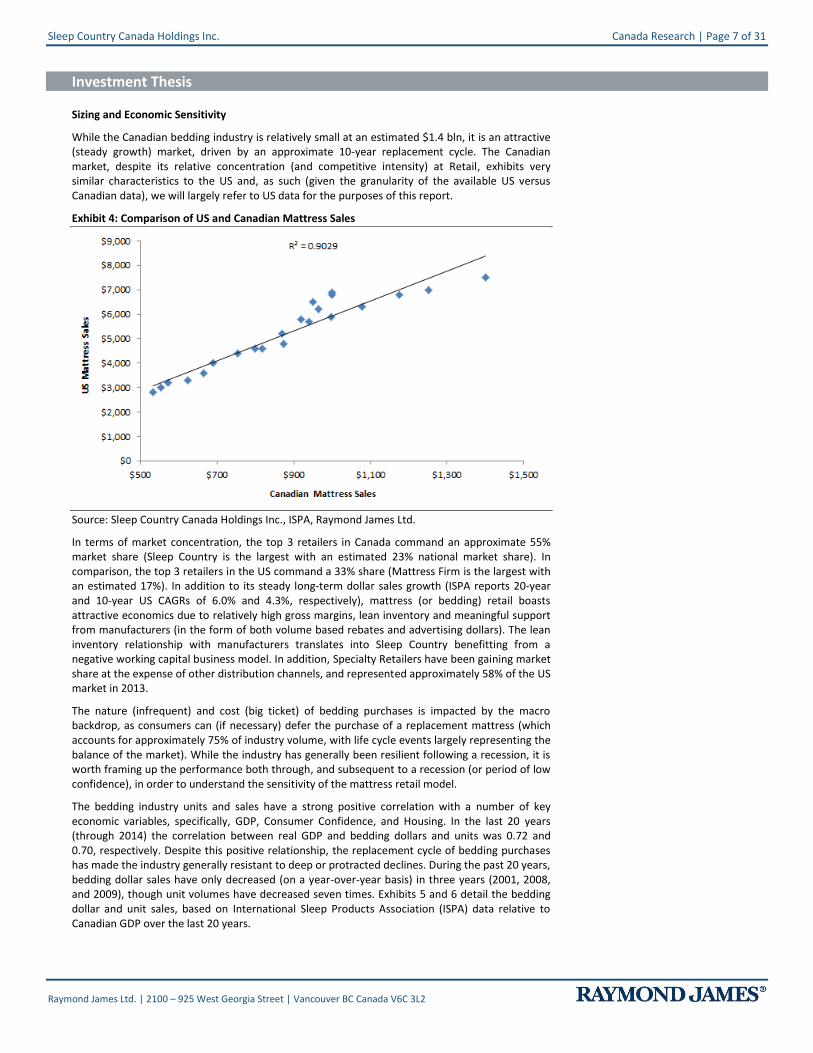

While the Canadian bedding industry is relatively small at an estimated $1.4 bln, it is an attractive (steady growth) market, driven by an approximate 10-year replacement cycle. The Canadian market, despite its relative concentration (and competitive intensity) at Retail, exhibits very similar characteristics to the US and, as such (given the granularity of the available US versus Canadian data), we will largely refer to US data for the purposes of this report.

Exhibit 4: Comparison of US and Canadian Mattress Sales

Source: Sleep Country Canada Holdings Inc., ISPA, Raymond James Ltd.

In terms of market concentration, the top 3 retailers in Canada command an approximate 55% market share (Sleep Country is the largest with an estimated 23% national market share). In comparison, the top 3 retailers in the US command a 33% share (Mattress Firm is the largest with an estimated 17%). In addition to its steady long-term dollar sales growth (ISPA reports 20-year and 10-year US CAGRs of 6.0% and 4.3%, respectively), mattress (or bedding) retail boasts attractive economics due to relatively high gross margins, lean inventory and meaningful support from manufacturers (in the form of both volume based rebates and advertising dollars). The lean inventory relationship with manufacturers translates into Sleep Country benefitting from a negative working capital business model. In addition, Specialty Retailers have been gaining market share at the expense of other distribution channels, and represented approximately 58% of the US market in 2013.

The nature (infrequent) and cost (big ticket) of bedding purchases is impacted by the macro backdrop, as consumers can (if necessary) defer the purchase of a replacement mattress (which accounts for approximately 75% of industry volume, with life cycle events largely representing the balance of the market). While the industry has generally been resilient following a recession, it is worth framing up the performance both through, and subsequent to a recession (or period of low confidence), in order to understand the sensitivity of the mattress retail model.

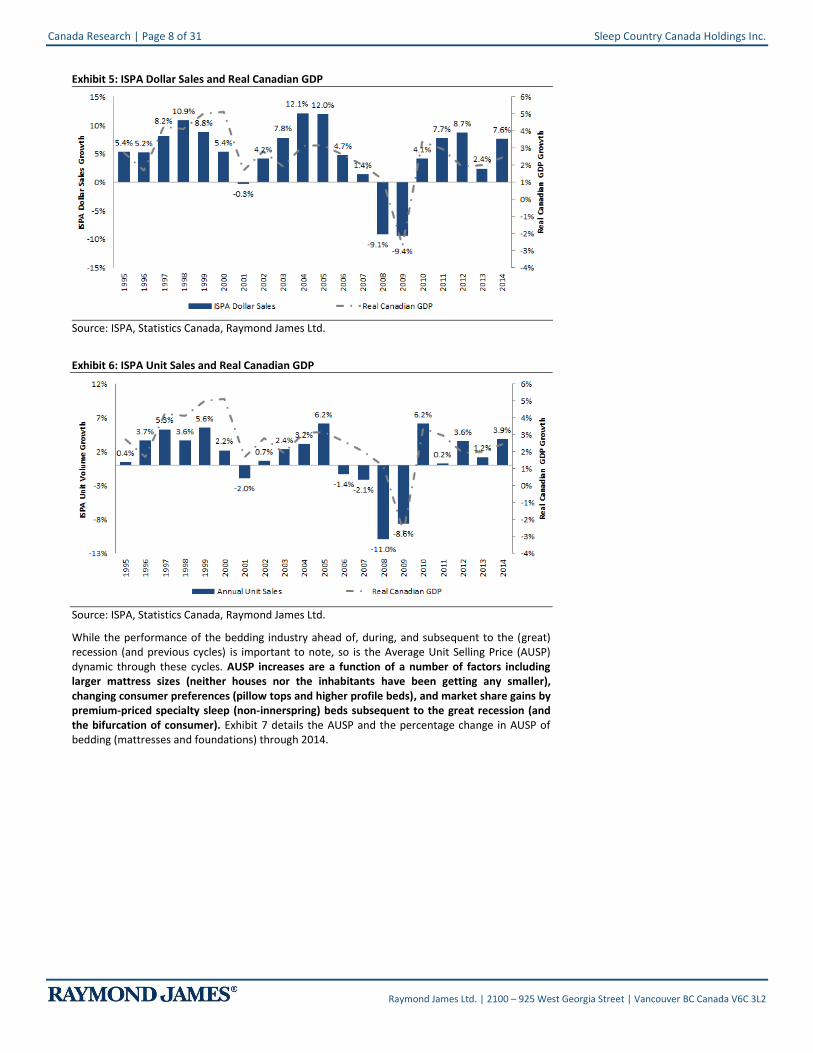

The bedding industry units and sales have a strong positive correlation with a number of key economic variables, specifically, GDP, Consumer Confidence, and Housing. In the last 20 years (through 2014) the correlation between real GDP and bedding dollars and units was 0.72 and 0.70, respectively. Despite this positive relationship, the replacement cycle of bedding purchases has made the industry generally resistant to deep or protracted declines. During the past 20 years, bedding dollar sales have only decreased (on a year-over-year basis) in three years (2001, 2008, and 2009), though unit volumes have decreased seven times. Exhibits 5 and 6 detail the bedding dollar and unit sales, based on International Sleep Products Association (ISPA) data relative to Canadian GDP over the last 20 years.

Canada Research | Page 8 of 31 Sleep Country Canada Holdings Inc.

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Exhibit 5: ISPA Dollar Sales and Real Canadian GDP

Source: ISPA, Statistics Canada, Raymond James Ltd.

Exhibit 6: ISPA Unit Sales and Real Canadian GDP

Source: ISPA, Statistics Canada, Raymond James Ltd.

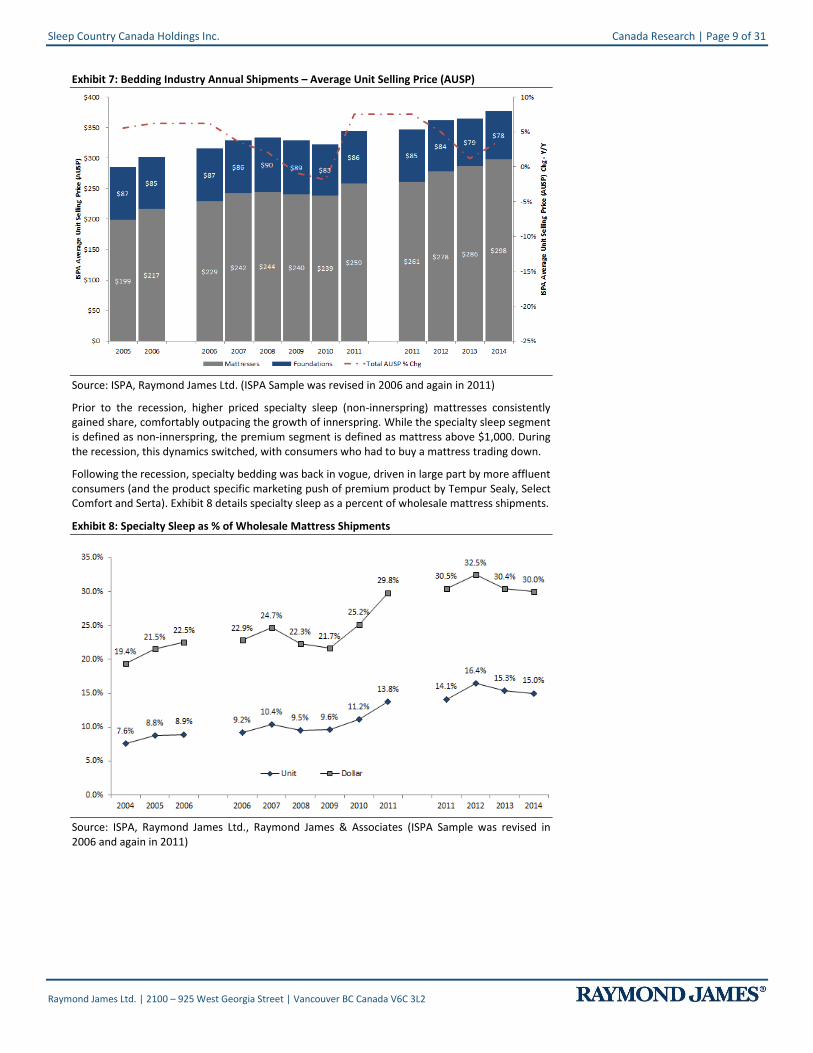

While the performance of the bedding industry ahead of, during, and subsequent to the (great) recession (and previous cycles) is important to note, so is the Average Unit Selling Price (AUSP) dynamic through these cycles. AUSP increases are a function of a number of factors including larger mattress sizes (neither houses nor the inhabitants have been getting any smaller), changing consumer preferences (pillow tops and higher profile beds), and market share gains by premium-priced specialty sleep (non-innerspring) beds subsequent to the great recession (and the bifurcation of consumer). Exhibit 7 details the AUSP and the percentage change in AUSP of bedding (mattresses and foundations) through 2014.

Sleep Country Canada Holdings Inc. Canada Research | Page 9 of 31

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Exhibit 7: Bedding Industry Annual Shipments – Average Unit Selling Price (AUSP)

Source: ISPA, Raymond James Ltd. (ISPA Sample was revised in 2006 and again in 2011)

Prior to the recession, higher priced specialty sleep (non-innerspring) mattresses consistently gained share, comfortably outpacing the growth of innerspring. While the specialty sleep segment is defined as non-innerspring, the premium segment is defined as mattress above $1,000. During the recession, this dynamics switched, with consumers who had to buy a mattress trading down.

Following the recession, specialty bedding was back in vogue, driven in large part by more affluent consumers (and the product specific marketing push of premium product by Tempur Sealy, Select Comfort and Serta). Exhibit 8 details specialty sleep as a percent of wholesale mattress shipments.

Exhibit 8: Specialty Sleep as % of Wholesale Mattress Shipments

Source: ISPA, Raymond James Ltd., Raymond James & Associates (ISPA Sample was revised in 2006 and again in 2011)

Canada Research | Page 10 of 31 Sleep Country Canada Holdings Inc.

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

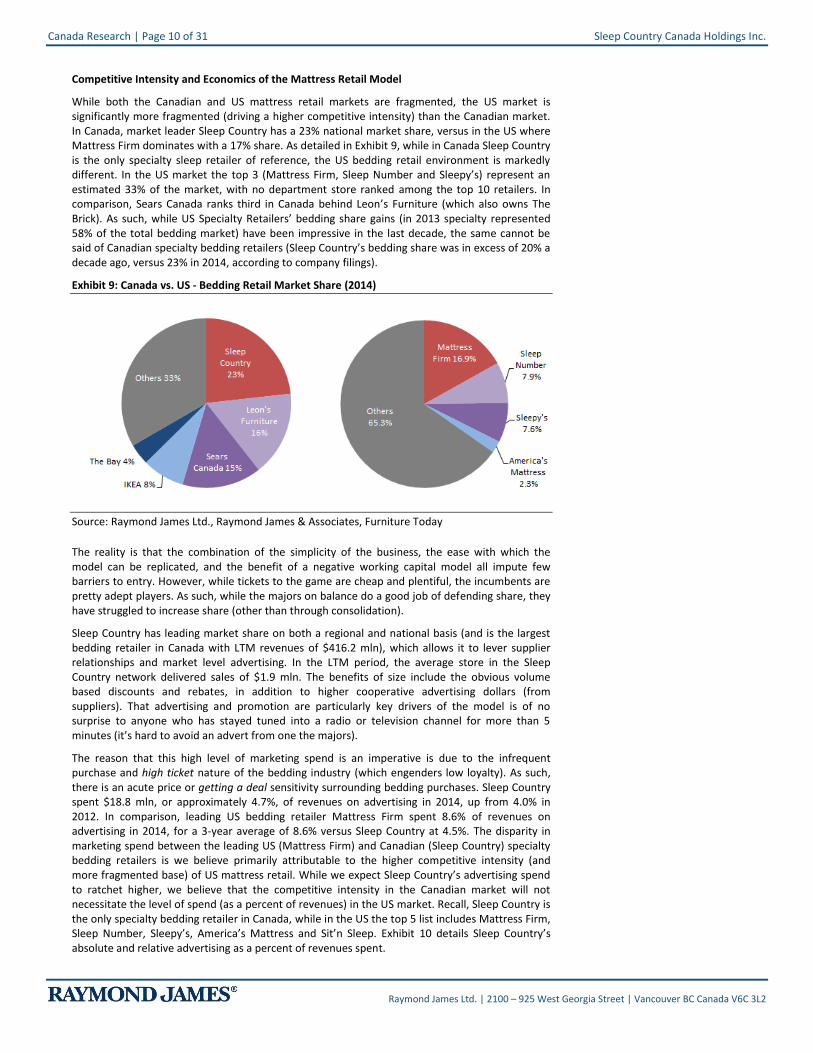

Competitive Intensity and Economics of the Mattress Retail Model

While both the Canadian and US mattress retail markets are fragmented, the US market is significantly more fragmented (driving a higher competitive intensity) than the Canadian market. In Canada, market leader Sleep Country has a 23% national market share, versus in the US where Mattress Firm dominates with a 17% share. As detailed in Exhibit 9, while in Canada Sleep Country is the only specialty sleep retailer of reference, the US bedding retail environment is markedly different. In the US market the top 3 (Mattress Firm, Sleep Number and Sleepy’s) represent an estimated 33% of the market, with no department store ranked among the top 10 retailers. In comparison, Sears Canada ranks third in Canada behind Leon’s Furniture (which also owns The Brick). As such, while US Specialty Retailers’ bedding share gains (in 2013 specialty represented 58% of the total bedding market) have been impressive in the last decade, the same cannot be said of Canadian specialty bedding retailers (Sleep Country’s bedding share was in excess of 20% a decade ago, versus 23% in 2014, according to company filings).

Exhibit 9: Canada vs. US - Bedding Retail Market Share (2014)

Source: Raymond James Ltd., Raymond James & Associates, Furniture Today

The reality is that the combination of the simplicity of the business, the ease with which the model can be replicated, and the benefit of a negative working capital model all impute few barriers to entry. However, while tickets to the game are cheap and plentiful, the incumbents are pretty adept players. As such, while the majors on balance do a good job of defending share, they have struggled to increase share (other than through consolidation).

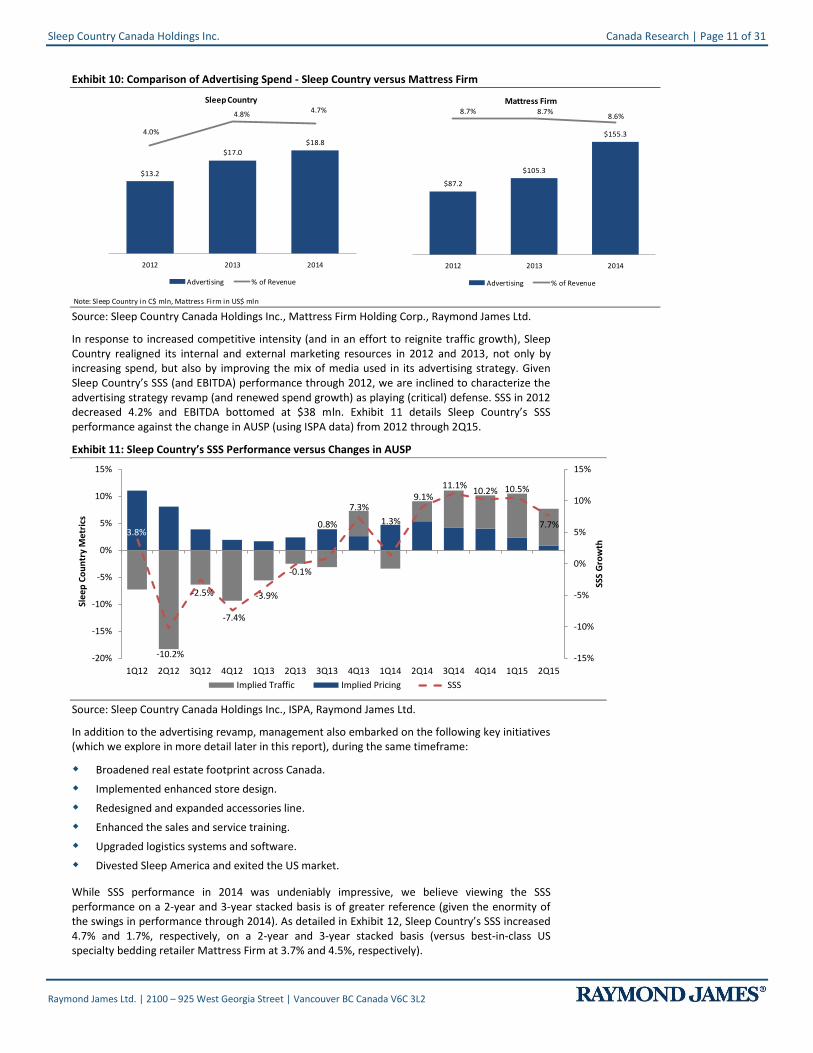

Sleep Country has leading market share on both a regional and national basis (and is the largest bedding retailer in Canada with LTM revenues of $416.2 mln), which allows it to lever supplier relationships and market level advertising. In the LTM period, the average store in the Sleep Country network delivered sales of $1.9 mln. The benefits of size include the obvious volume based discounts and rebates, in addition to higher cooperative advertising dollars (from suppliers). That advertising and promotion are particularly key drivers of the model is of no surprise to anyone who has stayed tuned into a radio or television channel for more than 5 minutes (it’s hard to avoid an advert from one the majors).

The reason that this high level of marketing spend is an imperative is due to the infrequent purchase and high ticket nature of the bedding industry (which engenders low loyalty). As such, there is an acute price or getting a deal sensitivity surrounding bedding purchases. Sleep Country spent $18.8 mln, or approximately 4.7%, of revenues on advertising in 2014, up from 4.0% in 2012. In comparison, leading US bedding retailer Mattress Firm spent 8.6% of revenues on advertising in 2014, for a 3-year average of 8.6% versus Sleep Country at 4.5%. The disparity in marketing spend between the leading US (Mattress Firm) and Canadian (Sleep Country) specialty bedding retailers is we believe primarily attributable to the higher competitive intensity (and more fragmented base) of US mattress retail. While we expect Sleep Country’s advertising spend to ratchet higher, we believe that the competitive intensity in the Canadian market will not necessitate the level of spend (as a percent of revenues) in the US market. Recall, Sleep Country is the only specialty bedding retailer in Canada, while in the US the top 5 list includes Mattress Firm, Sleep Number, Sleepy’s, America’s Mattress and Sit’n Sleep. Exhibit 10 details Sleep Country’s absolute and relative advertising as a percent of revenues spent.

Sleep Country Canada Holdings Inc. Canada Research | Page 11 of 31

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Exhibit 10: Comparison of Advertising Spend - Sleep Country versus Mattress Firm

Note: Sleep Country in C$ mln, Mattress Firm in US$ mln

$13.2

$17.0

$18.8

4.0%

4.8%4.7%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

$0.0

$5.0

$10.0

$15.0

$20.0

$25.0

2012 2013 2014

Sleep Country

Advertising % of Revenue

$87.2

$105.3

$155.3

8.7% 8.7%8.6%

7.0%

7.2%

7.4%

7.6%

7.8%

8.0%

8.2%

8.4%

8.6%

-$10.0

$10.0

$30.0

$50.0

$70.0

$90.0

$110.0

$130.0

$150.0

$170.0

$190.0

2012 2013 2014

Mattress Firm

Advertising % of Revenue

Source: Sleep Country Canada Holdings Inc., Mattress Firm Holding Corp., Raymond James Ltd.

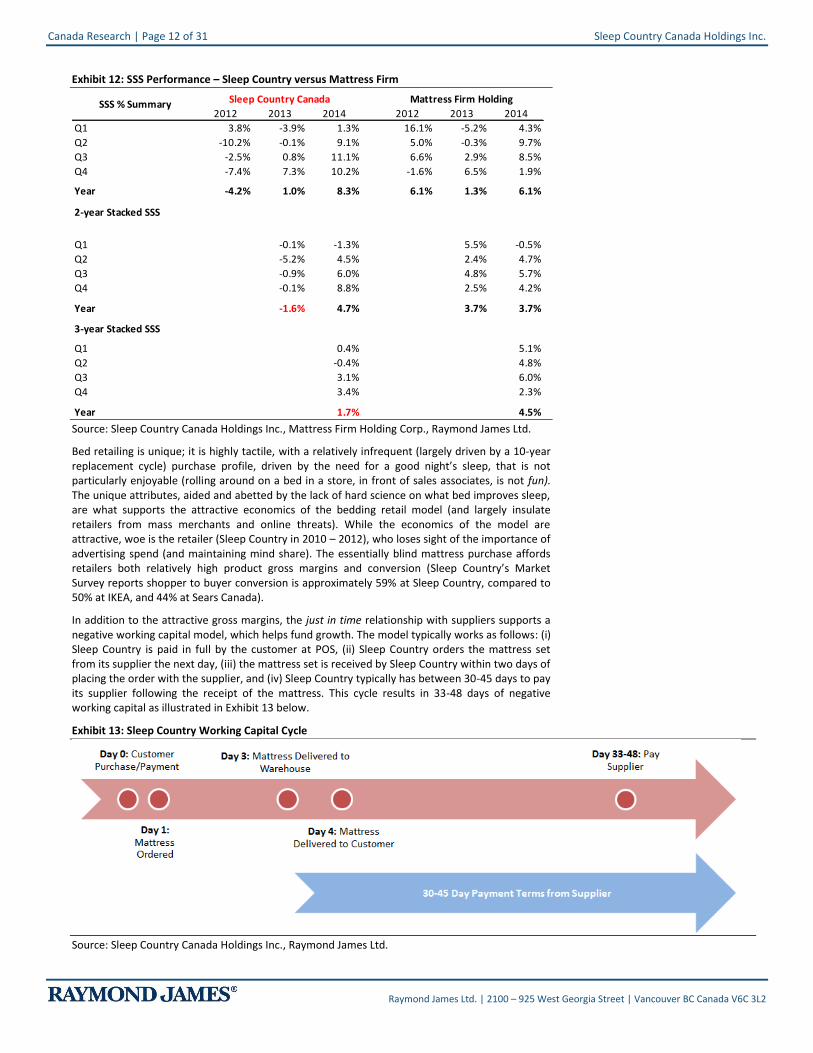

In response to increased competitive intensity (and in an effort to reignite traffic growth), Sleep Country realigned its internal and external marketing resources in 2012 and 2013, not only by increasing spend, but also by improving the mix of media used in its advertising strategy. Given Sleep Country’s SSS (and EBITDA) performance through 2012, we are inclined to characterize the advertising strategy revamp (and renewed spend growth) as playing (critical) defense. SSS in 2012 decreased 4.2% and EBITDA bottomed at $38 mln. Exhibit 11 details Sleep Country’s SSS performance against the change in AUSP (using ISPA data) from 2012 through 2Q15.

Exhibit 11: Sleep Country’s SSS Performance versus Changes in AUSP

3.8%

-10.2%

-2.5%

-7.4%

-3.9%

-0.1%

0.8%

7.3%

1.3%

9.1%11.1%

10.2% 10.5%

7.7%

-15%

-10%

-5%

0%

5%

10%

15%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15

SSS

Gro

wth

Sle

ep

Co

un

try

Me

tric

s

Implied Traffic Implied Pricing SSS

Source: Sleep Country Canada Holdings Inc., ISPA, Raymond James Ltd.

In addition to the advertising revamp, management also embarked on the following key initiatives (which we explore in more detail later in this report), during the same timeframe:

Broadened real estate footprint across Canada.

Implemented enhanced store design.

Redesigned and expanded accessories line.

Enhanced the sales and service training.

Upgraded logistics systems and software.

Divested Sleep America and exited the US market.

While SSS performance in 2014 was undeniably impressive, we believe viewing the SSS performance on a 2-year and 3-year stacked basis is of greater reference (given the enormity of the swings in performance through 2014). As detailed in Exhibit 12, Sleep Country’s SSS increased 4.7% and 1.7%, respectively, on a 2-year and 3-year stacked basis (versus best-in-class US specialty bedding retailer Mattress Firm at 3.7% and 4.5%, respectively).

Canada Research | Page 12 of 31 Sleep Country Canada Holdings Inc.

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Exhibit 12: SSS Performance – Sleep Country versus Mattress Firm

2012 2013 2014 2012 2013 2014

Q1 3.8% -3.9% 1.3% 16.1% -5.2% 4.3%

Q2 -10.2% -0.1% 9.1% 5.0% -0.3% 9.7%

Q3 -2.5% 0.8% 11.1% 6.6% 2.9% 8.5%

Q4 -7.4% 7.3% 10.2% -1.6% 6.5% 1.9%

Year -4.2% 1.0% 8.3% 6.1% 1.3% 6.1%

2-year Stacked SSS

Q1 -0.1% -1.3% 5.5% -0.5%

Q2 -5.2% 4.5% 2.4% 4.7%

Q3 -0.9% 6.0% 4.8% 5.7%

Q4 -0.1% 8.8% 2.5% 4.2%

Year -1.6% 4.7% 3.7% 3.7%

3-year Stacked SSS

Q1 0.4% 5.1%

Q2 -0.4% 4.8%

Q3 3.1% 6.0%

Q4 3.4% 2.3%

Year 1.7% 4.5%

Sleep Country Canada Mattress Firm HoldingSSS % Summary

Source: Sleep Country Canada Holdings Inc., Mattress Firm Holding Corp., Raymond James Ltd.

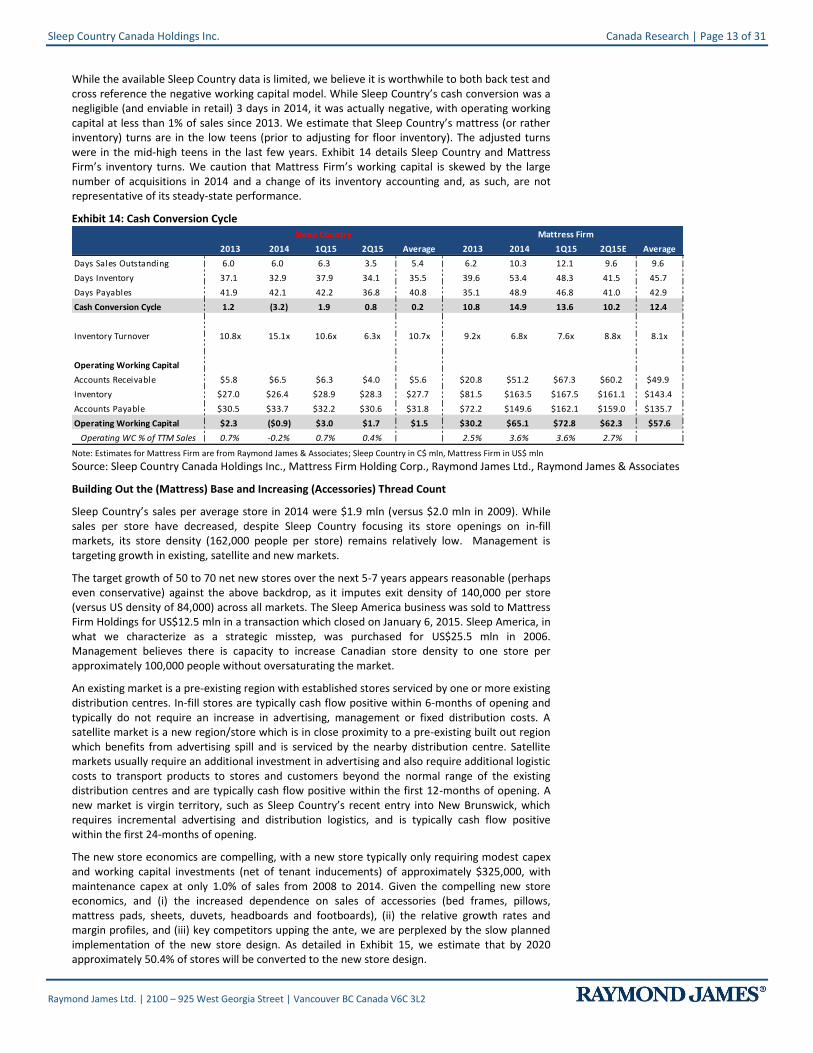

Bed retailing is unique; it is highly tactile, with a relatively infrequent (largely driven by a 10-year replacement cycle) purchase profile, driven by the need for a good night’s sleep, that is not particularly enjoyable (rolling around on a bed in a store, in front of sales associates, is not fun). The unique attributes, aided and abetted by the lack of hard science on what bed improves sleep, are what supports the attractive economics of the bedding retail model (and largely insulate retailers from mass merchants and online threats). While the economics of the model are attractive, woe is the retailer (Sleep Country in 2010 – 2012), who loses sight of the importance of advertising spend (and maintaining mind share). The essentially blind mattress purchase affords retailers both relatively high product gross margins and conversion (Sleep Country’s Market Survey reports shopper to buyer conversion is approximately 59% at Sleep Country, compared to 50% at IKEA, and 44% at Sears Canada).

In addition to the attractive gross margins, the just in time relationship with suppliers supports a negative working capital model, which helps fund growth. The model typically works as follows: (i) Sleep Country is paid in full by the customer at POS, (ii) Sleep Country orders the mattress set from its supplier the next day, (iii) the mattress set is received by Sleep Country within two days of placing the order with the supplier, and (iv) Sleep Country typically has between 30-45 days to pay its supplier following the receipt of the mattress. This cycle results in 33-48 days of negative working capital as illustrated in Exhibit 13 below.

Exhibit 13: Sleep Country Working Capital Cycle

Source: Sleep Country Canada Holdings Inc., Raymond James Ltd.

Sleep Country Canada Holdings Inc. Canada Research | Page 13 of 31

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

While the available Sleep Country data is limited, we believe it is worthwhile to both back test and cross reference the negative working capital model. While Sleep Country’s cash conversion was a negligible (and enviable in retail) 3 days in 2014, it was actually negative, with operating working capital at less than 1% of sales since 2013. We estimate that Sleep Country’s mattress (or rather inventory) turns are in the low teens (prior to adjusting for floor inventory). The adjusted turns were in the mid-high teens in the last few years. Exhibit 14 details Sleep Country and Mattress Firm’s inventory turns. We caution that Mattress Firm’s working capital is skewed by the large number of acquisitions in 2014 and a change of its inventory accounting and, as such, are not representative of its steady-state performance.

Exhibit 14: Cash Conversion Cycle

2013 2014 1Q15 2Q15 Average 2013 2014 1Q15 2Q15E Average

Days Sales Outstanding 6.0 6.0 6.3 3.5 5.4 6.2 10.3 12.1 9.6 9.6

Days Inventory 37.1 32.9 37.9 34.1 35.5 39.6 53.4 48.3 41.5 45.7

Days Payables 41.9 42.1 42.2 36.8 40.8 35.1 48.9 46.8 41.0 42.9

Cash Conversion Cycle 1.2 (3.2) 1.9 0.8 0.2 10.8 14.9 13.6 10.2 12.4

Inventory Turnover 10.8x 15.1x 10.6x 6.3x 10.7x 9.2x 6.8x 7.6x 8.8x 8.1x

Operating Working Capital

Accounts Receivable $5.8 $6.5 $6.3 $4.0 $5.6 $20.8 $51.2 $67.3 $60.2 $49.9

Inventory $27.0 $26.4 $28.9 $28.3 $27.7 $81.5 $163.5 $167.5 $161.1 $143.4

Accounts Payable $30.5 $33.7 $32.2 $30.6 $31.8 $72.2 $149.6 $162.1 $159.0 $135.7

Operating Working Capital $2.3 ($0.9) $3.0 $1.7 $1.5 $30.2 $65.1 $72.8 $62.3 $57.6

Operating WC % of TTM Sales 0.7% -0.2% 0.7% 0.4% 2.5% 3.6% 3.6% 2.7%

Note: Sleep Country in C$ mln, Mattress Firm in US$ mln

Sleep Country Mattress Firm

Note: Estimates for Mattress Firm are from Raymond James & Associates; Sleep Country in C$ mln, Mattress Firm in US$ mln

Source: Sleep Country Canada Holdings Inc., Mattress Firm Holding Corp., Raymond James Ltd., Raymond James & Associates

Building Out the (Mattress) Base and Increasing (Accessories) Thread Count

Sleep Country’s sales per average store in 2014 were $1.9 mln (versus $2.0 mln in 2009). While sales per store have decreased, despite Sleep Country focusing its store openings on in-fill markets, its store density (162,000 people per store) remains relatively low. Management is targeting growth in existing, satellite and new markets.

The target growth of 50 to 70 net new stores over the next 5-7 years appears reasonable (perhaps even conservative) against the above backdrop, as it imputes exit density of 140,000 per store (versus US density of 84,000) across all markets. The Sleep America business was sold to Mattress Firm Holdings for US$12.5 mln in a transaction which closed on January 6, 2015. Sleep America, in what we characterize as a strategic misstep, was purchased for US$25.5 mln in 2006. Management believes there is capacity to increase Canadian store density to one store per approximately 100,000 people without oversaturating the market.

An existing market is a pre-existing region with established stores serviced by one or more existing distribution centres. In-fill stores are typically cash flow positive within 6-months of opening and typically do not require an increase in advertising, management or fixed distribution costs. A satellite market is a new region/store which is in close proximity to a pre-existing built out region which benefits from advertising spill and is serviced by the nearby distribution centre. Satellite markets usually require an additional investment in advertising and also require additional logistic costs to transport products to stores and customers beyond the normal range of the existing distribution centres and are typically cash flow positive within the first 12-months of opening. A new market is virgin territory, such as Sleep Country’s recent entry into New Brunswick, which requires incremental advertising and distribution logistics, and is typically cash flow positive within the first 24-months of opening.

The new store economics are compelling, with a new store typically only requiring modest capex and working capital investments (net of tenant inducements) of approximately $325,000, with maintenance capex at only 1.0% of sales from 2008 to 2014. Given the compelling new store economics, and (i) the increased dependence on sales of accessories (bed frames, pillows, mattress pads, sheets, duvets, headboards and footboards), (ii) the relative growth rates and margin profiles, and (iii) key competitors upping the ante, we are perplexed by the slow planned implementation of the new store design. As detailed in Exhibit 15, we estimate that by 2020 approximately 50.4% of stores will be converted to the new store design.

Canada Research | Page 14 of 31 Sleep Country Canada Holdings Inc.

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Exhibit 15: Sleep Country New Store Format – 2014 to 2020E

2014A 2015E 2016E 2017E 2018E 2019E 2020E

Beginning Store Count 208 212 223 233 244 256 266

New Stores (New Format) 11 10 11 12 10 10

New Format Conversions 3 12 12 12 12 12 12

Total Stores 212 223 233 244 256 266 276

Total New Format Stores 3 26 48 71 95 117 139

New Format as a % of Total Stores 1.4% 11.7% 20.6% 29.1% 37.1% 44.0% 50.4%

Source: Sleep Country Canada Holdings Inc., Raymond James Ltd.

In the last 5 years, Sleep Country’s bedding sales CAGR was a relatively paltry 2.4% versus its bedding accessories sales CAGR of 7.5%. The CAGR in the AUSP in the same period was 3.2% (on a 2.6% CAGR in unit volumes), according to ISPA data. In addition, the accessories category carries an even more attractive margin, at an estimated 10% higher than mattresses. While Sleep Country, on approximately $73 mln in accessories sales, has a modest 8.8% market share, neither its growth rate nor its share gains have gone unnoticed by the market leaders. The bedding accessories sections of key competitors have undergone (or are undergoing) the biggest refresh in a generation based on our channel checks.

The experience is of particular reference in bedding accessories shopping, as linens, pillows and duvets are seldom (if ever) on an average consumer’s fun day of shopping list. While the new store design is competitive (and worlds removed from the old store design), it is not especially compelling relative to offerings (and redesigns) by key bedding accessories competitors. As such, we believe that Sleep Country is going to need to further refine its accessories model in order to maintain growth trajectory (and share gains). Exhibit 16 depicts a typical Sleep Country store in 2006 and one of the 9 new format stores.

Exhibit 16: Sleep Country Store – Base 2006 Store versus Enhanced 2014 Store

Source: Raymond James Ltd., Sleep Country Canada Holdings Inc. (National Post)

Sleep Country prides itself on its highly-trained and dedicated workforce. Sleep Country provides extensive initial and ongoing employee training and development in order to deliver a superior in-store experience. The combination of Sleep Country’s enhanced employee training and competitive compensation program (base salary and commission earned on gross margins) is the driver behind its impressive average employee turnover rate of 16%, which is approximately a third of the Retail industry average of 44% (according to a recent Mercer survey). The enhanced sales and service training (which we suspect dovetails with tougher performance criteria) has, however, resulted in a marked increase from the unsustainably low mid-single digit levels of 10 years ago.

The investments made in its sales teams enables Sleep Country to deliver a superior in-store experience that results in high conversion of sales (59%), repeat business and superior sales per associate metrics. Given that a mattress is an infrequent (and big ticket) purchase item with highly personalized tastes, preferences, needs, budgets, and is a difficult product to compare (not to mention the complex and constantly evolving product landscape), knowledgeable sales staff are key. In addition, by offering 60-day price and comfort guarantees, Sleep Country strives to take the worry out of the purchase decision.

Sleep Country Canada Holdings Inc. Canada Research | Page 15 of 31

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

While the conventional wisdom posits that Bricks have (and will continue) to dominate Clicks in mattress retailing, with limited traction gained from online sales given the challenges in gaining an understanding of the differences, falling asleep at your mouse doesn’t result in a good night’s sleep (or growing share). While the Canadian mattress retail market is at a lower risk from online cannibalization and showrooming than other retail categories, Sleep Country can ill afford to become complacent about the threat.

Given that Sleep Country is the leading specialty bedding retailer in Canada, and has recently revamped its advertising strategy (to bolster its traditional and online marketing strategies the company increased its total expenditures on advertising and improved the mix of media that it deployed in its advertising strategy), we decided it would be instructive to do a little online shopping. The results of this exercise were disappointing. Our search of “mattress” generated some surprising results. While we expected new entrants (and online-only players the likes of Endy Sleep) to rank highly, we did not expect Sleep Country to rank below the line. The highest ranking non-sponsored link was by The Brick. In terms of sponsored links, startup Endy Sleep was top ranked, with both Sears Canada and Walmart Canada hard to miss.

Despite an online advertising presence (and website that appears designed to either frustrate consumers into a Sleep Country store or the arms of a competitor), both Sleep Country Canada’s banners enjoy market leading unaided brand awareness and share of traffic. We are of the opinion that significant opportunity (from either a risk mitigation or share gain perspective) exists in Sleep Country’s online capabilities, and we would look to see it become a leader (versus a laggard), in terms of its online capabilities.

Exhibit 17: Consumers’ Brand Awareness

Source: Sleep Country Canada Holdings Inc., Raymond James Ltd.

Canada Research | Page 16 of 31 Sleep Country Canada Holdings Inc.

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Financial Analysis & Outlook

2Q15 Results Summary

Sleep Country’s revenue increased 10.6% from $92.7 mln to $102.5 mln, driven by mattress sales growth of 9.8% to $83.1 mln and accessory sales growth of 14.5% to $19.4 mln. The combination of continued store refreshes (Sleep Country has converted 9 stores thus far to its new enhanced design) and focus on improved merchandizing and sleep-related accessories is facilitating particularly solid performance. In addition, the renovated stores have delivered a 22% increase in SSS since their reopening.

Sleep Country’s revenue increased a strong 10.6% from $92.7 mln to $102.5 mln, reflecting SSS growth of 7.7% (on a tough 9.1% comp). The particularly strong SSS increase marked the 8

th consecutive quarterly SSS increase, reflecting the continued momentum of its strategic

initiatives.

Gross margin performance was also noteworthy, increasing a strong 188 bp from 24.5% to 26.3% (gross profit dollars increased 19.2% from $22.7 mln to $27.0 mln), driven by improved mix, distribution efficiencies and leveraging of certain fixed costs.

Adjusted EBITDA came in at $13.4 mln, for an EBITDA margin of 13.0% versus 9.5% in the prior-year quarter. The particularly strong 356 bp margin expansion reflects higher gross margins and improved SG&A leverage (SG&A margins of 13.7% versus 16.3% in 2Q14).

Revenue

Sleep Country’s revenue increased a strong 10.6% from $92.7 mln to $102.5 mln, on mattress sales growth of 9.8% to $83.1 mln and accessory sales growth of 14.5% to $19.4 mln. The revenue growth reflects a particularly 7.7% increase in SSS (against a tough 9.1% comp), and the addition of 6 new stores in 1H15.

Gross Profit

Gross profit increased 19.2% from $22.7 mln to $27.0 mln, for a gross margin of 26.3%. The strong 188 bp margin increase reflects a more favourable product mix, distribution efficiencies, and leveraging of fixed costs. The improved mix reflects a higher proportion of (i) accessories and (ii) specialty mattress in the mix, in addition to improved promotional efficiency. Sleep Country saw further improvements in logistics costs, on improved communication stores and its distribution centres.

EBITDA

Operating EBITDA increased 52.2% from $8.8 mln to $13.4 mln, for an EBITDA margin of 13.0% (versus 9.5% in the year-ago quarter). The particularly strong 356 bp margin improvement reflects the twin tailwinds of higher gross margins and better SG&A leverage (SG&A margins were 13.7% versus 16.3% in 2Q14).

EPS

Adjusted EPS was $0.20, on adjusted net income of $7.5 mln.

Sleep Country Canada Holdings Inc. Canada Research | Page 17 of 31

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Model and Estimates

We are initiating 2015E EPS of $0.92, 2016E EPS of $0.99 and 2017E EPS of $1.08. The combination of continued store conversions (Sleep Country is expected to convert 10 to 15 stores annually to its new enhanced design), and focus on improved product mix and higher-margin sleep-related accessories, is expected to facilitate continued solid performance through our forecast window. Our earnings forecasts are based on the following assumptions:

2015 Estimates

Revenue of $433.1 mln reflects a 9.3% increase from the prior year, driven by SSS growth of 6.4% and the opening of 11 net new stores. We expect total store count of 223 versus 212 at the end of 2014.

Gross margin of 27.1%, for a gross margin expansion of 103 bp, reflecting our expectations of improved product mix (higher proportion of accessories sales), distribution efficiencies, and leveraging of fixed costs.

Operating EBITDA margin improvement of 146 bp to 14.2% (EBITDA of $61.7 mln), reflecting our expectations of higher gross margins dovetailing with improved SG&A leverage. We expect SG&A margins of 12.9% versus 13.9% in 2014.

EPS growth of 58.7% to $0.92, on net income of $34.6 mln and an expected effective tax rate of 27.0%.

2016 Estimates

Revenue growth of 8.2% to $468.7 mln, which is primarily predicated on a 4.3% increase in SSS and 10 net new stores (for a total store base of 233).

We expect a more modest gross margin expansion of 14 bp to 27.3%, on a tough 103 bp expected increase in 2015. While favourable mix impacts are feasible through 2016E, they are not explicitly baked into our assumptions.

An 11 bp increase in Operating EBITDA margin to 14.4% (EBITDA of $67.3 mln), on our expectations of a 14 bp in gross margin increase and essentially unchanged SG&A leverage (very modest 3 bp increase in SG&A margins of 12.9%).

EPS of $0.99, for a 7.2% increase from the prior year, on our expectations of net income of $37.1 mln and an unchanged effective tax rate of 27.0%.

2017 Estimates

Revenue of $504.4 mln, for a 7.6% increase from the prior year, is predicated on a 3.9% growth in SSS and 11 net new stores (bringing Sleep Country’s total store base to 244 by year-end 2017E).

Gross margin of 27.3%, for a very modest 7 bp gross margin increase. While more favourable product mix impacts are possible through 2017E, they are not explicitly baked into our assumptions.

Operating EBITDA of $72.6 mln, for an EBITDA margin of 14.4%. The very modest 3 bp EBITDA margin increase reflects our expectations of a 7 bp gross margin expansion, and essentially unchanged SG&A leverage. We expect SG&A margins of 13.0% versus 12.9% in the prior year.

EPS growth of 9.7% to $1.08, which is predicated on our $40.6 mln net income expectation and unchanged effective tax rate of 27.0%.

Canada Research | Page 18 of 31 Sleep Country Canada Holdings Inc.

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

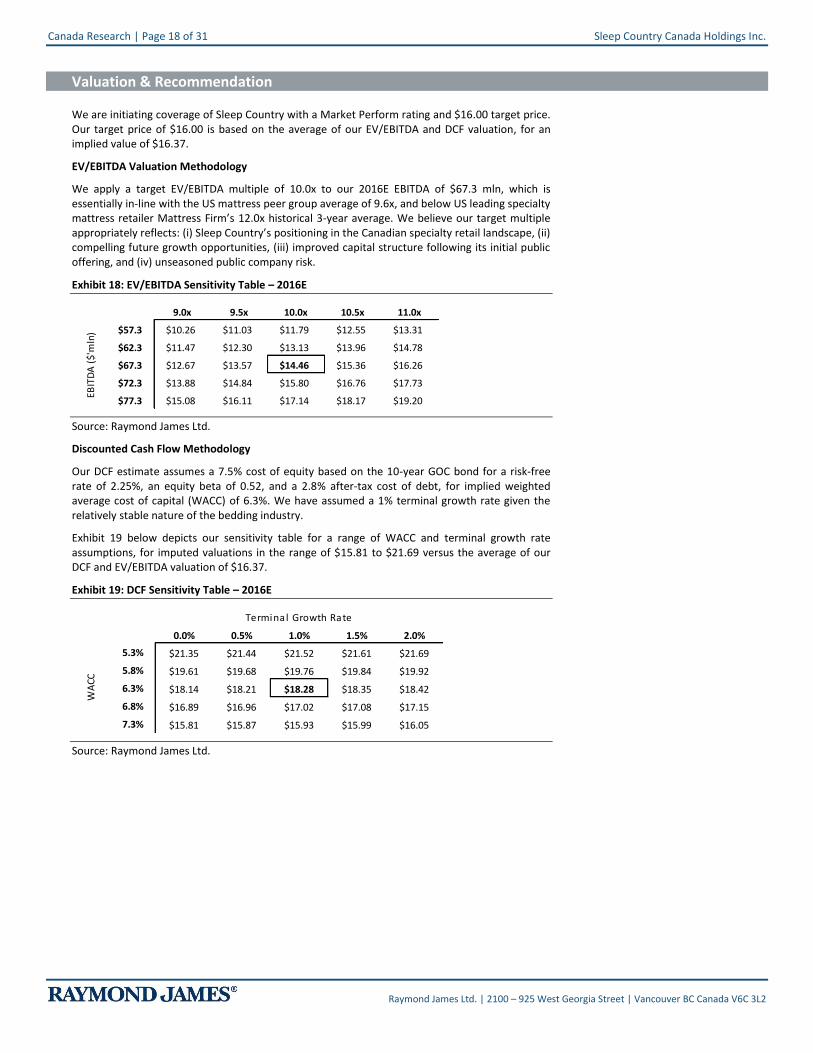

Valuation & Recommendation

We are initiating coverage of Sleep Country with a Market Perform rating and $16.00 target price. Our target price of $16.00 is based on the average of our EV/EBITDA and DCF valuation, for an implied value of $16.37.

EV/EBITDA Valuation Methodology

We apply a target EV/EBITDA multiple of 10.0x to our 2016E EBITDA of $67.3 mln, which is essentially in-line with the US mattress peer group average of 9.6x, and below US leading specialty mattress retailer Mattress Firm’s 12.0x historical 3-year average. We believe our target multiple appropriately reflects: (i) Sleep Country’s positioning in the Canadian specialty retail landscape, (ii) compelling future growth opportunities, (iii) improved capital structure following its initial public offering, and (iv) unseasoned public company risk.

Exhibit 18: EV/EBITDA Sensitivity Table – 2016E

14.46$ 9.0x 9.5x 10.0x 10.5x 11.0x

$57.3 $10.26 $11.03 $11.79 $12.55 $13.31

$62.3 $11.47 $12.30 $13.13 $13.96 $14.78

$67.3 $12.67 $13.57 $14.46 $15.36 $16.26

$72.3 $13.88 $14.84 $15.80 $16.76 $17.73

$77.3 $15.08 $16.11 $17.14 $18.17 $19.20

EBIT

DA

($'

mln

)

Source: Raymond James Ltd.

Discounted Cash Flow Methodology

Our DCF estimate assumes a 7.5% cost of equity based on the 10-year GOC bond for a risk-free rate of 2.25%, an equity beta of 0.52, and a 2.8% after-tax cost of debt, for implied weighted average cost of capital (WACC) of 6.3%. We have assumed a 1% terminal growth rate given the relatively stable nature of the bedding industry.

Exhibit 19 below depicts our sensitivity table for a range of WACC and terminal growth rate assumptions, for imputed valuations in the range of $15.81 to $21.69 versus the average of our DCF and EV/EBITDA valuation of $16.37.

Exhibit 19: DCF Sensitivity Table – 2016E

1,828% 0.0% 0.5% 1.0% 1.5% 2.0%

5.3% $21.35 $21.44 $21.52 $21.61 $21.69

5.8% $19.61 $19.68 $19.76 $19.84 $19.92

6.3% $18.14 $18.21 $18.28 $18.35 $18.42

6.8% $16.89 $16.96 $17.02 $17.08 $17.15

7.3% $15.81 $15.87 $15.93 $15.99 $16.05

Terminal Growth Rate

WA

CC

Source: Raymond James Ltd.

Sleep Country Canada Holdings Inc. Canada Research | Page 19 of 31

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

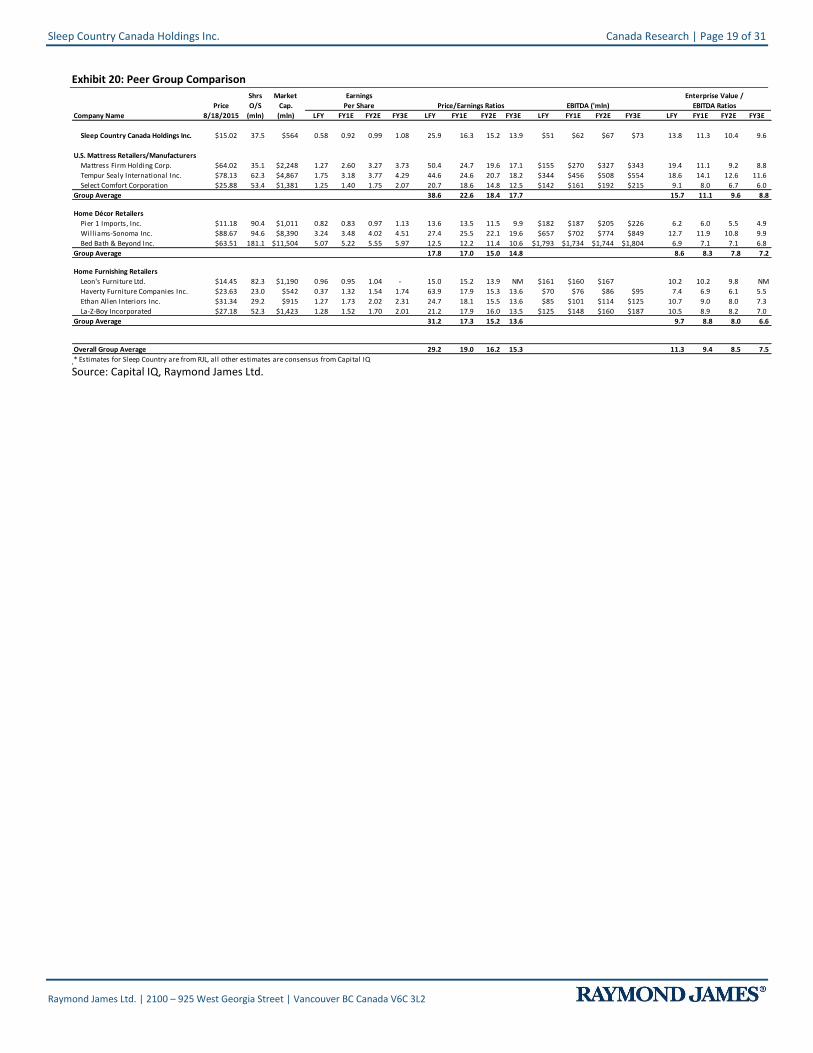

Exhibit 20: Peer Group Comparison

Shrs Market 1000 1001 1002 1003

Price O/S Cap.

Company Name 8/18/2015 (mln) (mln) LFY FY1E FY2E FY3E LFY FY1E FY2E FY3E LFY FY1E FY2E FY3E LFY FY1E FY2E FY3E

Sleep Country Canada Holdings Inc. $15.02 37.5 $564 0.58 0.92 0.99 1.08 25.9 16.3 15.2 13.9 $51 $62 $67 $73 13.8 11.3 10.4 9.6

U.S. Mattress Retailers/Manufacturers LAST 1000 1001 1002 1003

Mattress Firm Holding Corp. $64.02 35.1 $2,248 1.27 2.60 3.27 3.73 50.4 24.7 19.6 17.1 $155 $270 $327 $343 19.4 11.1 9.2 8.8

Tempur Sealy International Inc. $78.13 62.3 $4,867 1.75 3.18 3.77 4.29 44.6 24.6 20.7 18.2 $344 $456 $508 $554 18.6 14.1 12.6 11.6

Select Comfort Corporation $25.88 53.4 $1,381 1.25 1.40 1.75 2.07 20.7 18.6 14.8 12.5 $142 $161 $192 $215 9.1 8.0 6.7 6.0

Group Average 38.6 22.6 18.4 17.7 15.7 11.1 9.6 8.8

Home Décor Retailers LAST 1000 1001 1002 1003

Pier 1 Imports, Inc. $11.18 90.4 $1,011 0.82 0.83 0.97 1.13 13.6 13.5 11.5 9.9 $182 $187 $205 $226 6.2 6.0 5.5 4.9

Williams-Sonoma Inc. $88.67 94.6 $8,390 3.24 3.48 4.02 4.51 27.4 25.5 22.1 19.6 $657 $702 $774 $849 12.7 11.9 10.8 9.9

Bed Bath & Beyond Inc. $63.51 181.1 $11,504 5.07 5.22 5.55 5.97 12.5 12.2 11.4 10.6 $1,793 $1,734 $1,744 $1,804 6.9 7.1 7.1 6.8

Group Average 17.8 17.0 15.0 14.8 8.6 8.3 7.8 7.2

Home Furnishing Retailers LAST 1000 1001 1002 1003

Leon's Furniture Ltd. $14.45 82.3 $1,190 0.96 0.95 1.04 - 15.0 15.2 13.9 NM $161 $160 $167 $0 10.2 10.2 9.8 NM

Haverty Furniture Companies Inc. $23.63 23.0 $542 0.37 1.32 1.54 1.74 63.9 17.9 15.3 13.6 $70 $76 $86 $95 7.4 6.9 6.1 5.5

Ethan Allen Interiors Inc. $31.34 29.2 $915 1.27 1.73 2.02 2.31 24.7 18.1 15.5 13.6 $85 $101 $114 $125 10.7 9.0 8.0 7.3

La-Z-Boy Incorporated $27.18 52.3 $1,423 1.28 1.52 1.70 2.01 21.2 17.9 16.0 13.5 $125 $148 $160 $187 10.5 8.9 8.2 7.0

Group Average 31.2 17.3 15.2 13.6 9.7 8.8 8.0 6.6

Overall Group Average 29.2 19.0 16.2 15.3 11.3 9.4 8.5 7.5

* Estimates for Sleep Country are from RJL, all other estimates are consensus from Capital IQ

Earnings

Per Share Price/Earnings Ratios EBITDA ('mln)

Enterprise Value /

EBITDA Ratios

Source: Capital IQ, Raymond James Ltd.

Canada Research | Page 20 of 31 Sleep Country Canada Holdings Inc.

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

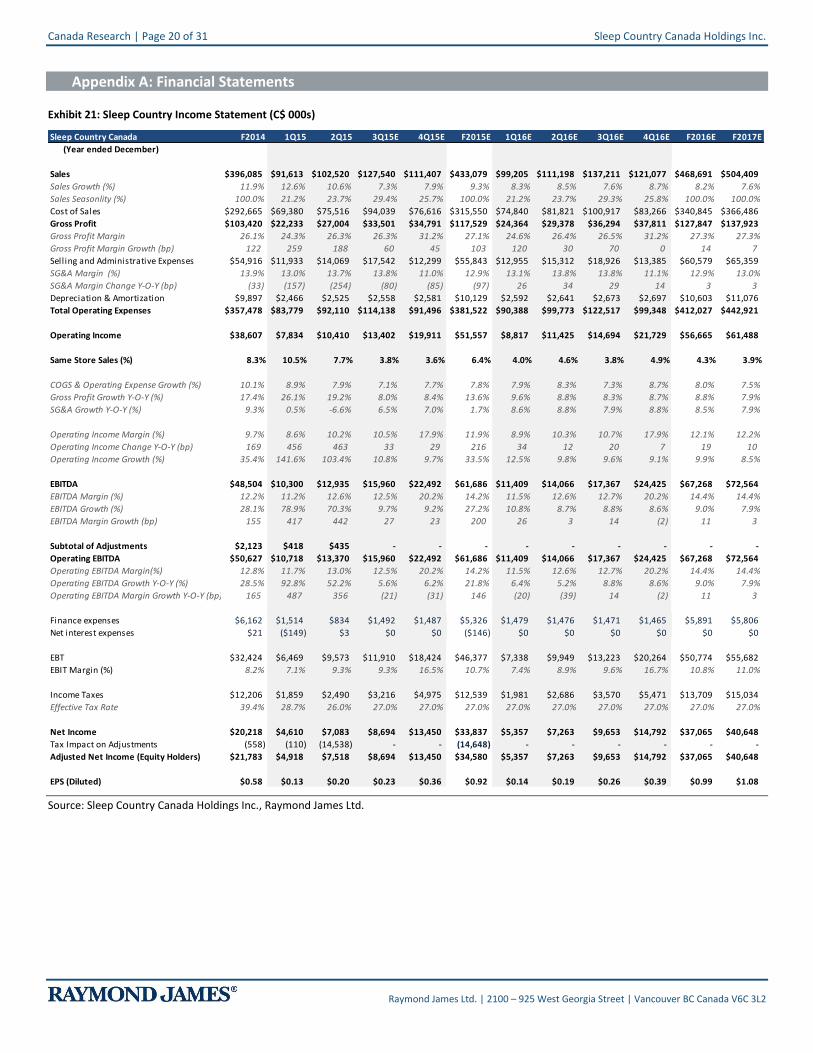

Appendix A: Financial Statements

Exhibit 21: Sleep Country Income Statement (C$ 000s)

Sleep Country Canada F2014 1Q15 2Q15 3Q15E 4Q15E F2015E 1Q16E 2Q16E 3Q16E 4Q16E F2016E F2017E

(Year ended December)

Sales $396,085 $91,613 $102,520 $127,540 $111,407 $433,079 $99,205 $111,198 $137,211 $121,077 $468,691 $504,409

Sales Growth (%) 11.9% 12.6% 10.6% 7.3% 7.9% 9.3% 8.3% 8.5% 7.6% 8.7% 8.2% 7.6%

Sales Seasonlity (%) 100.0% 21.2% 23.7% 29.4% 25.7% 100.0% 21.2% 23.7% 29.3% 25.8% 100.0% 100.0%

Cost of Sales $292,665 $69,380 $75,516 $94,039 $76,616 $315,550 $74,840 $81,821 $100,917 $83,266 $340,845 $366,486

Gross Profit $103,420 $22,233 $27,004 $33,501 $34,791 $117,529 $24,364 $29,378 $36,294 $37,811 $127,847 $137,923

Gross Profit Margin 26.1% 24.3% 26.3% 26.3% 31.2% 27.1% 24.6% 26.4% 26.5% 31.2% 27.3% 27.3%

Gross Profit Margin Growth (bp) 122 259 188 60 45 103 120 30 70 0 14 7

Selling and Administrative Expenses $54,916 $11,933 $14,069 $17,542 $12,299 $55,843 $12,955 $15,312 $18,926 $13,385 $60,579 $65,359

SG&A Margin (%) 13.9% 13.0% 13.7% 13.8% 11.0% 12.9% 13.1% 13.8% 13.8% 11.1% 12.9% 13.0%

SG&A Margin Change Y-O-Y (bp) (33) (157) (254) (80) (85) (97) 26 34 29 14 3 3

Depreciation & Amortization $9,897 $2,466 $2,525 $2,558 $2,581 $10,129 $2,592 $2,641 $2,673 $2,697 $10,603 $11,076

Total Operating Expenses $357,478 $83,779 $92,110 $114,138 $91,496 $381,522 $90,388 $99,773 $122,517 $99,348 $412,027 $442,921

Operating Income $38,607 $7,834 $10,410 $13,402 $19,911 $51,557 $8,817 $11,425 $14,694 $21,729 $56,665 $61,488

Same Store Sales (%) 8.3% 10.5% 7.7% 3.8% 3.6% 6.4% 4.0% 4.6% 3.8% 4.9% 4.3% 3.9%

COGS & Operating Expense Growth (%) 10.1% 8.9% 7.9% 7.1% 7.7% 7.8% 7.9% 8.3% 7.3% 8.7% 8.0% 7.5%

Gross Profit Growth Y-O-Y (%) 17.4% 26.1% 19.2% 8.0% 8.4% 13.6% 9.6% 8.8% 8.3% 8.7% 8.8% 7.9%

SG&A Growth Y-O-Y (%) 9.3% 0.5% -6.6% 6.5% 7.0% 1.7% 8.6% 8.8% 7.9% 8.8% 8.5% 7.9%

Operating Income Margin (%) 9.7% 8.6% 10.2% 10.5% 17.9% 11.9% 8.9% 10.3% 10.7% 17.9% 12.1% 12.2%

Operating Income Change Y-O-Y (bp) 169 456 463 33 29 216 34 12 20 7 19 10

Operating Income Growth (%) 35.4% 141.6% 103.4% 10.8% 9.7% 33.5% 12.5% 9.8% 9.6% 9.1% 9.9% 8.5%

EBITDA $48,504 $10,300 $12,935 $15,960 $22,492 $61,686 $11,409 $14,066 $17,367 $24,425 $67,268 $72,564

EBITDA Margin (%) 12.2% 11.2% 12.6% 12.5% 20.2% 14.2% 11.5% 12.6% 12.7% 20.2% 14.4% 14.4%

EBITDA Growth (%) 28.1% 78.9% 70.3% 9.7% 9.2% 27.2% 10.8% 8.7% 8.8% 8.6% 9.0% 7.9%

EBITDA Margin Growth (bp) 155 417 442 27 23 200 26 3 14 (2) 11 3

Subtotal of Adjustments $2,123 $418 $435 - - - - - - - - -

Operating EBITDA $50,627 $10,718 $13,370 $15,960 $22,492 $61,686 $11,409 $14,066 $17,367 $24,425 $67,268 $72,564

Operating EBITDA Margin(%) 12.8% 11.7% 13.0% 12.5% 20.2% 14.2% 11.5% 12.6% 12.7% 20.2% 14.4% 14.4%

Operating EBITDA Growth Y-O-Y (%) 28.5% 92.8% 52.2% 5.6% 6.2% 21.8% 6.4% 5.2% 8.8% 8.6% 9.0% 7.9%

Operating EBITDA Margin Growth Y-O-Y (bp) 165 487 356 (21) (31) 146 (20) (39) 14 (2) 11 3

Finance expenses $6,162 $1,514 $834 $1,492 $1,487 $5,326 $1,479 $1,476 $1,471 $1,465 $5,891 $5,806

Net interest expenses $21 ($149) $3 $0 $0 ($146) $0 $0 $0 $0 $0 $0

EBT $32,424 $6,469 $9,573 $11,910 $18,424 $46,377 $7,338 $9,949 $13,223 $20,264 $50,774 $55,682

EBIT Margin (%) 8.2% 7.1% 9.3% 9.3% 16.5% 10.7% 7.4% 8.9% 9.6% 16.7% 10.8% 11.0%

Income Taxes $12,206 $1,859 $2,490 $3,216 $4,975 $12,539 $1,981 $2,686 $3,570 $5,471 $13,709 $15,034

Effective Tax Rate 39.4% 28.7% 26.0% 27.0% 27.0% 27.0% 27.0% 27.0% 27.0% 27.0% 27.0% 27.0%

Net Income $20,218 $4,610 $7,083 $8,694 $13,450 $33,837 $5,357 $7,263 $9,653 $14,792 $37,065 $40,648

Tax Impact on Adjustments (558) (110) (14,538) - - (14,648) - - - - - -

Adjusted Net Income (Equity Holders) $21,783 $4,918 $7,518 $8,694 $13,450 $34,580 $5,357 $7,263 $9,653 $14,792 $37,065 $40,648

EPS (Diluted) $0.58 $0.13 $0.20 $0.23 $0.36 $0.92 $0.14 $0.19 $0.26 $0.39 $0.99 $1.08

Source: Sleep Country Canada Holdings Inc., Raymond James Ltd.

Sleep Country Canada Holdings Inc. Canada Research | Page 21 of 31

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Exhibit 22: Sleep Country Balance Sheet (C$ 000s) Sleep Country Canada 2013 2014 2015E 2016E 2017E

(Year ended December)

Assets:

Current Assets:

Cash & Equivalents 27,401 41,331 37,045 52,450 71,003

Trade & Other Receivables 5,808 6,477 4,897 5,322 5,734

Due from Related Parties 11 16 1,194 - -

Inventories 27,046 26,369 31,151 33,855 36,372

Prepaid Expenses 1,482 2,475 2,287 2,287 2,287

Assets for Disposal/Held for Sale - 14,086 - - -

Non-Current Assets:

Property & Equipment 30,455 24,948 25,242 21,839 17,962

Other Assets 419 480 431 431 431

Intangibles 105,006 104,042 103,845 103,845 103,845

Goodwill 242,595 242,146 242,146 242,146 242,146

Total Assets 440,223 462,370 448,238 462,175 479,780

Liabilities & Shareholder's Equity

Current Liabilities:

Trade & Other Payables 30,546 33,729 31,151 33,855 36,372

Customer Deposits 10,093 12,116 10,811 10,811 10,811

Current Portion of Long-term Debt 885 7,367 6,928 6,208 5,488

Liabilities of Disposal Group Held for Sale - 5,210 - - -

Total Current Liabilities 41,524 58,422 48,890 50,874 52,671

Other Liabilities 7,078 6,965 6,985 6,985 6,985

Deferred Tax Liabilities 42,541 31,820 11,429 11,429 11,429

Long-term Debt 220,115 257,838 148,487 148,487 148,487

Total Liabilities 311,258 355,045 215,791 217,775 219,572

Shareholders' Equity

Share Capital 123,994 123,603 207,583 205,102 205,102

Retained Earnings/Deficit (28,234) (63,693) 24,863 39,297 55,105

Currency Translation Reserve 80 428 - - -

Total Shareholders' Equity 95,840 60,338 232,446 244,400 260,208

Non-controlling Interest 33,125 46,987 - - -

Total Liabilities & Shareholder's Equity 440,223 462,370 448,238 462,175 479,780 Source: Sleep Country Canada Holdings Inc., Raymond James Ltd.

Canada Research | Page 22 of 31 Sleep Country Canada Holdings Inc.

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

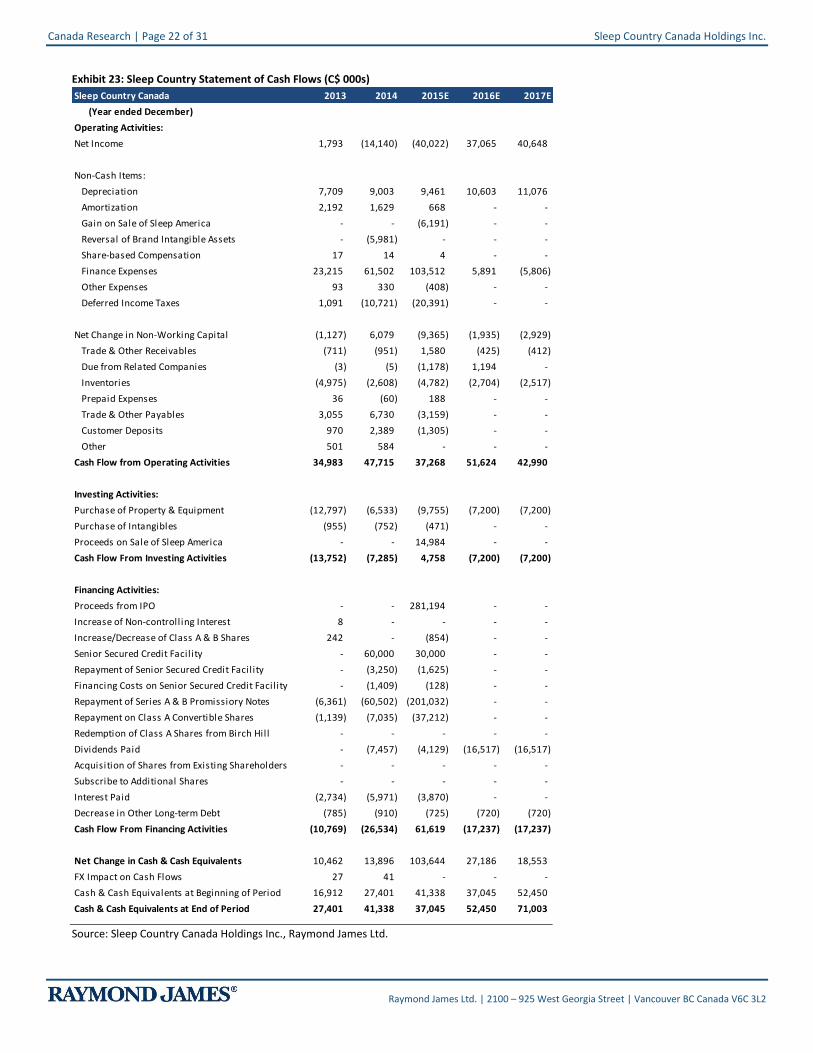

Exhibit 23: Sleep Country Statement of Cash Flows (C$ 000s)

Sleep Country Canada 2013 2014 2015E 2016E 2017E

(Year ended December)

Operating Activities:

Net Income 1,793 (14,140) (40,022) 37,065 40,648

Non-Cash Items:

Depreciation 7,709 9,003 9,461 10,603 11,076

Amortization 2,192 1,629 668 - -

Gain on Sale of Sleep America - - (6,191) - -

Reversal of Brand Intangible Assets - (5,981) - - -

Share-based Compensation 17 14 4 - -

Finance Expenses 23,215 61,502 103,512 5,891 (5,806)

Other Expenses 93 330 (408) - -

Deferred Income Taxes 1,091 (10,721) (20,391) - -

Net Change in Non-Working Capital (1,127) 6,079 (9,365) (1,935) (2,929)

Trade & Other Receivables (711) (951) 1,580 (425) (412)

Due from Related Companies (3) (5) (1,178) 1,194 -

Inventories (4,975) (2,608) (4,782) (2,704) (2,517)

Prepaid Expenses 36 (60) 188 - -

Trade & Other Payables 3,055 6,730 (3,159) - -

Customer Deposits 970 2,389 (1,305) - -

Other 501 584 - - -

Cash Flow from Operating Activities 34,983 47,715 37,268 51,624 42,990

Investing Activities:

Purchase of Property & Equipment (12,797) (6,533) (9,755) (7,200) (7,200)

Purchase of Intangibles (955) (752) (471) - -

Proceeds on Sale of Sleep America - - 14,984 - -

Cash Flow From Investing Activities (13,752) (7,285) 4,758 (7,200) (7,200)

Financing Activities:

Proceeds from IPO - - 281,194 - -

Increase of Non-controlling Interest 8 - - - -

Increase/Decrease of Class A & B Shares 242 - (854) - -

Senior Secured Credit Facil ity - 60,000 30,000 - -

Repayment of Senior Secured Credit Facil ity - (3,250) (1,625) - -

Financing Costs on Senior Secured Credit Facil ity - (1,409) (128) - -

Repayment of Series A & B Promissiory Notes (6,361) (60,502) (201,032) - -

Repayment on Class A Convertible Shares (1,139) (7,035) (37,212) - -

Redemption of Class A Shares from Birch Hill - - - - -

Dividends Paid - (7,457) (4,129) (16,517) (16,517)

Acquisition of Shares from Existing Shareholders - - - - -

Subscribe to Additional Shares - - - - -

Interest Paid (2,734) (5,971) (3,870) - -

Decrease in Other Long-term Debt (785) (910) (725) (720) (720)

Cash Flow From Financing Activities (10,769) (26,534) 61,619 (17,237) (17,237)

Net Change in Cash & Cash Equivalents 10,462 13,896 103,644 27,186 18,553

FX Impact on Cash Flows 27 41 - - -

Cash & Cash Equivalents at Beginning of Period 16,912 27,401 41,338 37,045 52,450

Cash & Cash Equivalents at End of Period 27,401 41,338 37,045 52,450 71,003

Source: Sleep Country Canada Holdings Inc., Raymond James Ltd.

Sleep Country Canada Holdings Inc. Canada Research | Page 23 of 31

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Appendix B: Management & Board of Directors

Stephen K. Gunn, Executive Co-Chair Mr. Gunn co-founded Sleep Country in 1994 and served as its Chief Executive Officer from 1997 to 2014. Prior to co-founding Sleep Country, Mr. Gunn held management consulting positions at McKinsey from 1981 to 1987, after which he co-founded Kenrick Capital. Mr. Gunn also serves on the Board of Directors at Dollarama, Golfsmith International, Cara, and Mastermind Toys. Mr. Gunn holds an MBA from University of Western Ontario, and a B.Sc. degree from Queen’s University. Christine Magee, Executive Co-Chair Ms. Magee co-founded Sleep Country in 1994 and served as its President until 2014. Prior to co-founding Sleep Country, Ms. Magee held various senior positions at Continental Bank and National Bank between 1982 and 1994. Ms. Magee also serves on the Board of Directors of SiriusXM Canada and Trillium Health Partners. In addition, Ms. Magee also serves on the Advisory Board of the Ivey School of Business and the Women’s President Organization. Ms. Magee holds an HBA from the University of Western Ontario. David Friesema, Director and Chief Executive Officer Mr. Friesema has served as Sleep Country’s Chief Executive Officer since November 2014. Mr. Friesema joined Sleep Country in 1995, during which he held various senior positions such as Head of Sales, General Manager and Chief Operating Officer. During his 20 year tenure at Sleep Country, Mr. Friesema has led the company through various strategic initiatives, such as developing sales training programs and creative marketing campaigns. Previously, Mr. Friesema worked in the mattress industry in the United States. Mr. Friesema is the Chairman of the Better Sleep Council of Canada. He attended the University of Detroit Business School and the University of Missouri-St. Louis School of Psychology. Stewart Schaefer, President of Dourmez-vous? and Chief Business Development Officer Mr. Schaefer founded Dourmez-vous? in 1994 and managed the company until it was acquired by Sleep Country in 2006. Prior to founding Dourmez-vous?, Mr. Schaefer co-founded Heritage Classic Beds, a manufacturer and distributor of iron and brass beds. Prior to entering the bedding industry, Mr. Schaefer worked as a commodity broker in Chicago, and at Dean Witter Reynolds and Refco Futures in Montreal. Mr. Schaefer studied Finance and Marketing at Concordia University in Montreal. Robert Masson, Chief Financial Officer and Corporate Secretary Mr. Masson has served in his current role since July 2013, when he joined Sleep Country. Previously, he held the position of Chief Financial Officer at Second Cup, in addition to various senior roles at IBM Canada, Manchuwok, Ernst & Young, Deloitte & Touche, and Sappi. Mr. Masson holds a Bachelor of Commerce and a Post Graduate Diploma of Accounting from the University of Kwa-Zulu Natal in South Africa. In addition, Mr. Masson holds the Chartered Accountant designation and is a member of the Chartered Professional Accountants of Ontario. David Howcroft, Senior Vice President of Sales Mr. Howcroft joined Sleep Country in 1996 and has served in his current role since 2012. During his tenure at Sleep Country, Mr. Howcroft has created various sales training programs and played an integral role in the development and implementation of sales workshops, training programs and sales processes. Mr. Howcroft has in excess of 20 years of retail sales experience, with the ability to conceive new sales strategies and a well-recognized ability to mentor and motivate. Sieg Will, Senior Vice President of Operations Mr. Will joined Sleep Country in 2002 and has served in his current role since 2012. During his tenure at Sleep Country, he has held various senior positions and played an integral role in the development and implementation of standard operating policies and procedures across the company. Previously, Mr. Will held senior positions in sales, operations and account management at Canadian Tire and PepsiCo. He serves on the Humber College Supply Chain Advisory Board, is a Team Leader for Sleeping Children Around the World and an Ambassador for the Pinehurst Club Breakfast. Mr. Will holds a B.A. (Honours) from the University of Guelph, and a Master’s Certificate in Supply Chain Management from the Schulich School of Business. He also has a Professional Logistics Designation from the Logistics Institute.

Canada Research | Page 24 of 31 Sleep Country Canada Holdings Inc.

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Eric Solomon, Senior Vice President of Merchandising and Marketing Mr. Solomon joined Sleep Country in 1996 and has served in his current role since 2012. During his tenure at Sleep Country, Mr. Solomon played an integral part of increasing the company’s brand awareness and diversifying Sleep Country’s product lineup with exclusive offerings. Mr. Solomon also led the sales and operating functions of Sleep Country. Mr. Solomon attended McMaster University.

Risks

General Economic Conditions The company’s business and operating performance may be adversely affected by economic forces beyond its control. Rising consumer debt levels and changes in consumer preferences and buying patterns, as well as changes in unemployment rate and labour costs could negatively impact the company’s performance. External factors that affect global and/or regional economies, interest rates, exchange rates, or major segments of the economy could alter investor confidence and investment prospects; an increase in minimum wage could have an adverse impact on operating costs and earnings. Competitive Landscape The Canadian retail landscape is highly competitive and continues to attract new entrants. The industry has been undergoing significant changes over the years, with both US and international players entering the Canadian retail market. In addition, with the increasing prevalence of e-commerce, existing competitors may start offering mattresses online and new competitors with an online presence may enter the bedding market. An increase in competition, both in-store and online, may result in price wars, market share loss, and reduced sales and profitability. Seasonality and Weather Retail mattress sales are subject to seasonal patterns, with the highest level of sales occurring in the second half of the year. Variable costs, such as certain selling costs and employee wages, can be managed to match seasonal fluctuations. A large portion of retail costs, such as ret, are fixed and cannot be adjusted to match seasonal demand. Unseasonable weather can result in lower traffic to Sleep Country and Dourmez-vous? stores and deter consumer spending. Supply Chain Disruption Disruptions or delays in store inventory replenishment could negatively impact operations and profitability. Factors resulting in disruptions of supply chain could include, but are not limited to, shipping slowdown or disruption due to extreme weather conditions. Product Cost and Inflation The company’s operating results may be adversely affected by the prices of the components used in the manufacture of the mattress and complementary sleep related products and accessories it sells. These prices may fluctuate based on a number of factors outside the company’s control, such as the price of oil, changes in supply and demand, general economic conditions and consumer spending, labour costs, competition, import duties and tariffs. Foreign Currency A portion of the company’s merchandize purchases are denominated in USD. As a portion of the company’s purchases are made in US dollars, unfavourable currency fluctuations relative to the Canadian dollar may adversely impact the company’s profitability. Sleep Country currently has no hedging instruments in place to mitigate the impact of fluctuating foreign exchange rates.

Sleep Country Canada Holdings Inc. Canada Research | Page 25 of 31

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

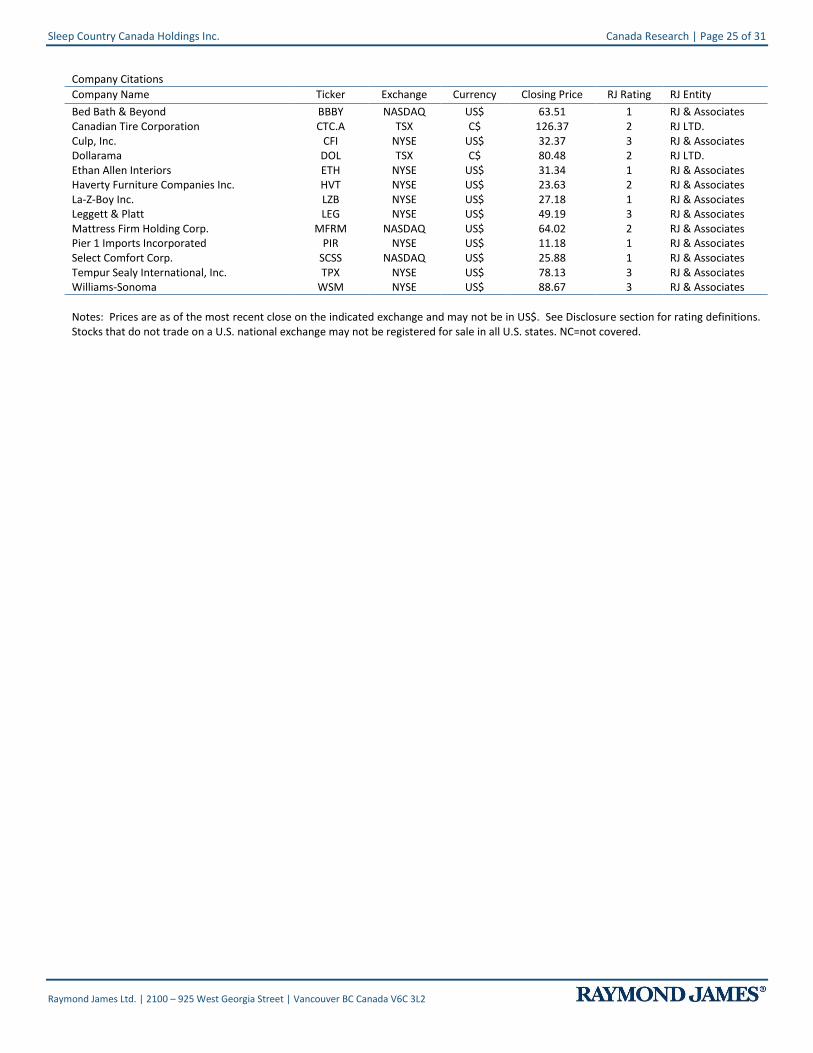

Company Citations

Company Name Ticker Exchange Currency Closing Price RJ Rating RJ Entity

Bed Bath & Beyond BBBY NASDAQ US$ 63.51 1 RJ & Associates Canadian Tire Corporation CTC.A TSX C$ 126.37 2 RJ LTD. Culp, Inc. CFI NYSE US$ 32.37 3 RJ & Associates Dollarama DOL TSX C$ 80.48 2 RJ LTD. Ethan Allen Interiors ETH NYSE US$ 31.34 1 RJ & Associates Haverty Furniture Companies Inc. HVT NYSE US$ 23.63 2 RJ & Associates La-Z-Boy Inc. LZB NYSE US$ 27.18 1 RJ & Associates Leggett & Platt LEG NYSE US$ 49.19 3 RJ & Associates Mattress Firm Holding Corp. MFRM NASDAQ US$ 64.02 2 RJ & Associates Pier 1 Imports Incorporated PIR NYSE US$ 11.18 1 RJ & Associates Select Comfort Corp. SCSS NASDAQ US$ 25.88 1 RJ & Associates Tempur Sealy International, Inc. TPX NYSE US$ 78.13 3 RJ & Associates Williams-Sonoma WSM NYSE US$ 88.67 3 RJ & Associates

Notes: Prices are as of the most recent close on the indicated exchange and may not be in US$. See Disclosure section for rating definitions. Stocks that do not trade on a U.S. national exchange may not be registered for sale in all U.S. states. NC=not covered.

Canada Research | Page 26 of 31 Sleep Country Canada Holdings Inc.

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

IMPORTANT INVESTOR DISCLOSURES Raymond James & Associates (RJA) is a FINRA member firm and is responsible for the preparation and distribution of research created in the United States. Raymond James & Associates is located at The Raymond James Financial Center, 880 Carillon Parkway, St. Petersburg, FL 33716, (727) 567-1000. Non-U.S. affiliates, which are not FINRA member firms, include the following entities which are responsible for the creation and distribution of research in their respective areas; In Canada, Raymond James Ltd., Suite 2100, 925 West Georgia Street, Vancouver, BC V6C 3L2, (604) 659-8200; In Latin America, Raymond James Latin America, Ruta 8, km 17, 500, 91600 Montevideo, Uruguay, 00598 2 518 2033; In Europe, Raymond James Euro Equities, SAS, 40, rue La Boetie, 75008, Paris, France, +33 1 45 61 64 90, and Raymond James Financial International Ltd., Broadwalk House, 5 Appold Street, London, England EC2A 2AG, +44 203 798 5600.