Embed Size (px)

Citation preview

CanadaMiningInnovationCouncilValueProposition:TowardsZeroWasteMining

August4,2015

2

Documentcontext

DocumentPurpose

l DefineandfurtherrefineCMIC’sTowardsZeroWasteMiningstrategytotheminingindustry

– EmphasizetheimportanceofthisprojectandthenecessityforstepchangethroughCMICviaitsopeninnovationapproach

– CrystallizethedefinitionofTowardsZeroWasteMiningandidentifythekeyfocusareas

– DefinehowCMICwillcollaborateandpartneracrossstakeholders,reconcilepotentialIntellectualProperty(IP)issues,financelongterminitiatives,andgovern/reportactivitiesandoutcomes

l Serveasaninternalguidingdocument/strategytoalignkeystakeholdersandpotentiallyserveasmaterialfortheBusinessCasetoattractpartnersintheminingecosystem(e.g.,industryplayers,academiaandgovernment)

l Theminingindustrygenerallyagreesthatitisbehindtheinnovationcurveandthatafocusedeffortisrequiredtocreateaprofitableandresponsiblelongtermindustry

l TheCanadaMiningInnovationCouncil(CMIC)isfocusingitseffortsthroughtheTowardsZeroWasteMiningstrategywhichwilleliminateminewastebyfacilitatingcollaborationacrosspartnerswithinthebusinessecosystemtocollectivelytransformtheindustry

Background

Preamble

SourceData

l Thisdocumentcontainsinformationfromanumberofdifferentsources(CMICrepresentatives,externalserviceproviders,miningcompanies,governmentrepositories,andanalystinsights).ThisvaluepropositionattemptstoconsolidateallofthesewithinaninternalstrategyforCMIC

l ThepartnershipbetweenCMICandMonitorDeloitteisdefinedinaccordancewiththetermsofanagreementbetweentheparties

3

Tableofcontents

Contents Page

MininginCanada- CurrentStateofMining- CurrentStateofMiningInnovation

4

CMICOverview 9

StrategicChoiceCascadingFramework- Summary- GoalsandAspirations- WhereWillCMICPlay- HowWillCMICWin- HowWillCMICConfigure- PriorityInitiatives

10

CMICPortfolioImplementationApproach 20

Appendix- ListofAbbreviations

24

4

Increasedglobalcomplexityrequiressectoradaptationtonewrealities…

MininginCanada>CurrentStateofMining

Structuredlabourmarketforces,decliningresourcequality,andalegacyofinefficientcapitalallocationhaveledtodecliningproductivity

Source:(1)StatisticsCanada,CANSIMtable383-0012,2007to2014;(2)OntarioHydro– Ontario’sHistoricalRPPRates

Highenergyconsumption,elevatedoperatimg costs(e.g.,energy,infrastructure,labour,royalties,permittingfees,andcompliance),haveresultedindecreasingmarginsforexistingoperationsanddiminishingeconomicfeasibilityofnewminedevelopments

DecliningProductivity

IncreasingCosts

85

90

95

100

105

110

2007 2008 2009 2010 2011 2012 2013 201460

70

80

90

100

110

120

130

Labo

urProdu

ctivity

Index

Year

HourlyCom

pensation($CA

D)

LabourProductivityisDecliningwhileLabourCostsareRisingQuarrying,andOil&GasExtraction1

Totalcompensationperhourworked Labourproductivity

BlendedRPPOntarioHydroRateshavefaroutpacedAnnualInflationovertheyears2

Cents/KW

h

Year

RPPPriceInflation

5

…especiallycomplexitiesassociatedwiththelicensetooperateandthedeclineofcommodityprices

Volatilecommoditypriceshaveresultedinunpredictablemargins,forcingcompaniestoplanfortheunforeseeable,anddecreasingfinancingcapitalavailability

Concernsfrommultiplestakeholdersincludingconservationandthepotentialenvironmentalimpactsofmineraldevelopmentandmineclosurehaveresultedinincreasinggovernmentregulation anddemandforheightenedcorporatesocialresponsibilityandstakeholderengagement

MininginCanada>CurrentStateofMining

IncreasinglyComplexLicensetoOperate

OperatingwithUncertainty

Inordertomakeasignificantshifttowardsimprovement,theindustrymustcollectivelychallengeexistingwaysofthinkingbyrevisitinglong-standingpracticesandprocesses

6

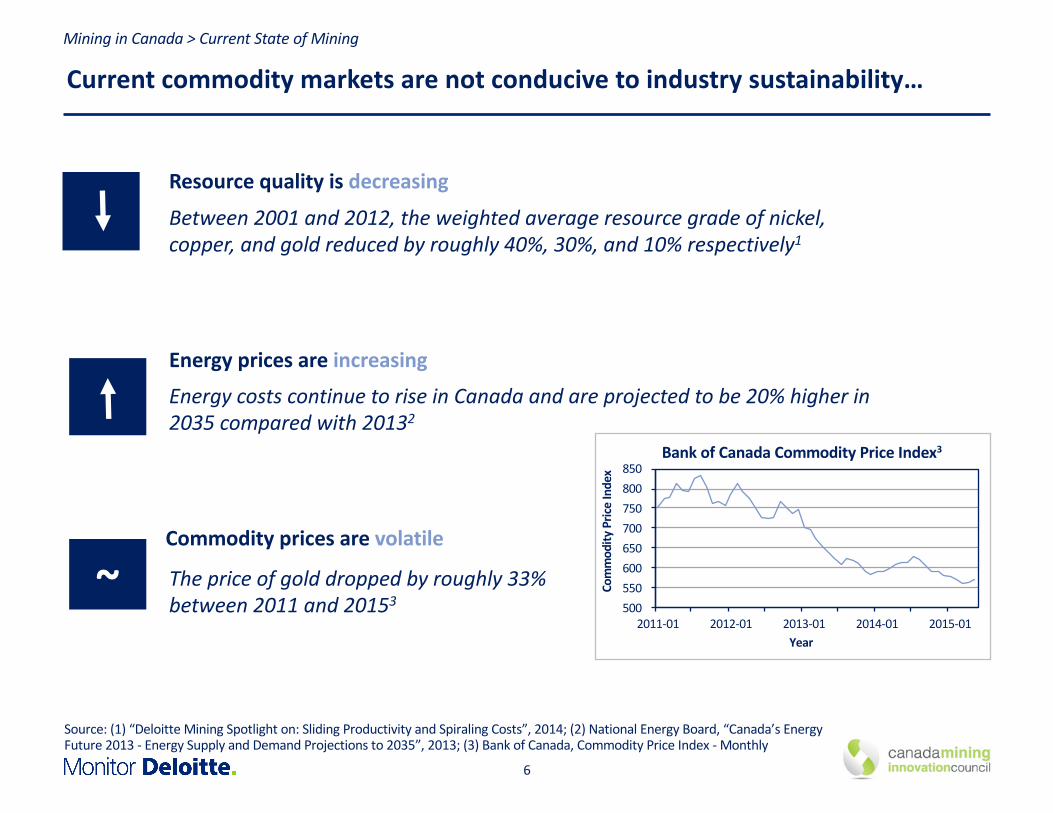

Currentcommoditymarketsarenotconducivetoindustrysustainability…

Resourcequalityisdecreasing

Between2001and2012,theweightedaverage resourcegradeofnickel,copper,andgoldreducedbyroughly40%,30%,and10%respectively1

Commoditypricesarevolatile

Thepriceofgolddroppedbyroughly33%between2011and20153

EnergypricesareincreasingEnergycostscontinuetoriseinCanadaandareprojectedtobe20%higherin2035comparedwith20132

~

Source:(1)“DeloitteMiningSpotlighton:SlidingProductivityandSpiralingCosts”,2014;(2)NationalEnergyBoard,“Canada’s EnergyFuture2013- EnergySupplyandDemandProjectionsto2035”,2013;(3)BankofCanada,CommodityPriceIndex- Monthly

MininginCanada>CurrentStateofMining

500550600650700750800850

2011-01 2012-01 2013-01 2014-01 2015-01Co

mmod

ityPriceIndex

Year

BankofCanadaCommodityPriceIndex3

7

…andisdecreasingtheviabilityofmininginCanadaasaneconomicforce

MiningandProcessing

G&AandExploration

NetInterestExp.

SustainingCapital

AvgGoldPrice($/oz)Year

$US

GoldIndustryMarginsAreDecreasing(all-insustainingcost$US/oz)1

TotalReturntoMiningShareholdersisUnderperformingOtherGlobalIndustries2

YearIndustrialsMining

Healthcare

TelecomsTechnologyAerospace&Defense

ConsumerGoodsBanks

TheNumberandValueofEquityIssuesinGlobalMining&MetalsisDecreasinginRecentYears2

YearNumberofIssues Proceeds($MUS)

Basedoncurrenttrendsandfutureprojections,costswilllikelycontinuetoincreaseovertime.Historicalcostcuttingexercises(e.g.,layoffs)arenotsustainableandwithoutasignificantshift,marginsmaydecreasetoapointwhereminingoperationsarenolongerprofitable

DecliningProfitability

Withmining’stotalreturntoshareholdersunderperformingothersectors,companiesareunder

mountingpressuretoboostshort-termprofits,oftenattheexpenseoflong-termplanning.Passingonlong-term,

possiblehighreturninvestments,resultsinfurtherdecreasinglongtermreturns

UnderperformingShareholderReturn

Significantpriceriskexposureduetovolatilecommoditypriceshasresultedindecliningequityfinancing and

scaledbackexplorationactivitybyjuniorsandmajors.Asaresult,thelong-termfuturesupplypipelinelooks

increasingunderrisk2

FutureofMiningProjectsIncreasinglyUnderRisk

Source:(1)Société Général,2013;(2)“Deloittetrackingthetrends2015– thetop10issuesminingcompanieswillfacethisyear”

MininginCanada> CurrentStateofMining

8

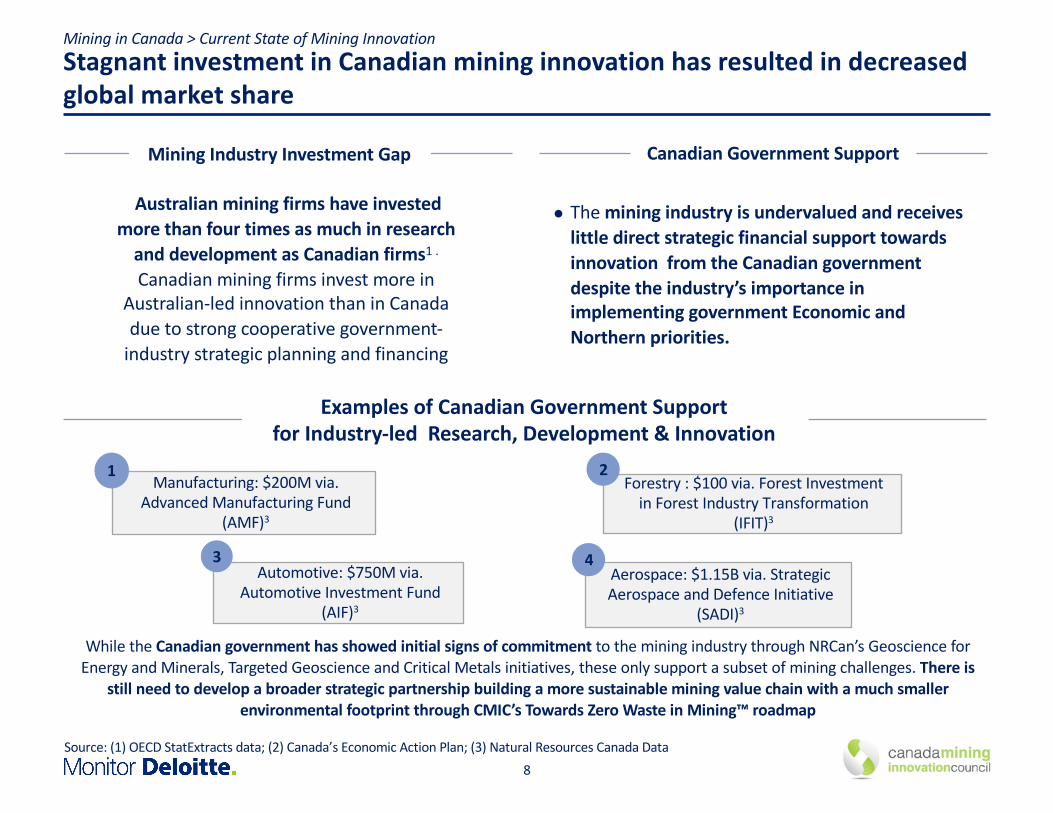

StagnantinvestmentinCanadianmininginnovationhasresultedindecreasedglobalmarketshare

Source:(1)OECDStatExtracts data;(2)Canada’sEconomicActionPlan;(3)NaturalResourcesCanadaData

AustralianminingfirmshaveinvestedmorethanfourtimesasmuchinresearchanddevelopmentasCanadianfirms1.Canadianminingfirmsinvestmorein

Australian-ledinnovationthaninCanadaduetostrongcooperativegovernment-industrystrategicplanningandfinancing

l TheminingindustryisundervaluedandreceiveslittledirectstrategicfinancialsupporttowardsinnovationfromtheCanadiangovernmentdespitetheindustry’simportanceinimplementinggovernmentEconomicandNorthernpriorities.

Manufacturing:$200Mvia.AdvancedManufacturingFund

(AMF)3

1Forestry:$100via.ForestInvestmentinForestIndustryTransformation

(IFIT)3

2

Automotive:$750Mvia.AutomotiveInvestmentFund

(AIF)3

3Aerospace:$1.15Bvia.StrategicAerospaceandDefenceInitiative

(SADI)3

4

CanadianGovernmentSupport

ExamplesofCanadianGovernmentSupportforIndustry-ledResearch,Development&Innovation

MiningIndustryInvestmentGap

WhiletheCanadiangovernmenthasshowedinitialsignsofcommitmenttotheminingindustrythroughNRCan’s GeoscienceforEnergyandMinerals,TargetedGeoscienceandCriticalMetalsinitiatives,theseonlysupportasubsetofminingchallenges.Thereis

stillneedtodevelopabroaderstrategicpartnershipbuildingamoresustainableminingvaluechainwithamuchsmallerenvironmentalfootprintthroughCMIC’sTowardsZeroWasteinMining™roadmap

MininginCanada> CurrentStateofMiningInnovation

9

CMICfacilitatesandfocusesthemininginnovationecosystemtocollaborativelyaddresspressingminingbusinesschallenges

l WhyCMICwascreated: formedtoprovideinnovationleadershiptotheCanadianminingindustry

l WhatCMICdoes:facilitatesanindustry-academic-governmentinnovationecosystemtofocusjointeffortsonaddressingCanadianminingcontinuedlicensetooperateprofitablychallengesinsupportofpublicpolicy

l CMIC’smission:enhancethecompetitivenessandsustainabilityoftheCanadianminingindustrybyensuringexcellenceinresearch,innovation,andcommercializationwiththeobjectiveofTowardsZeroWasteinMining™

l CMIC’svision:re-launchCanadaasagloballeaderinincreasingaresponsibleminingindustry’ssociallicensetooperate,therebyremainingastrongpillarintheCanadianlongtermeconomiclandscape

CMICOverview

AboutCMIC

10

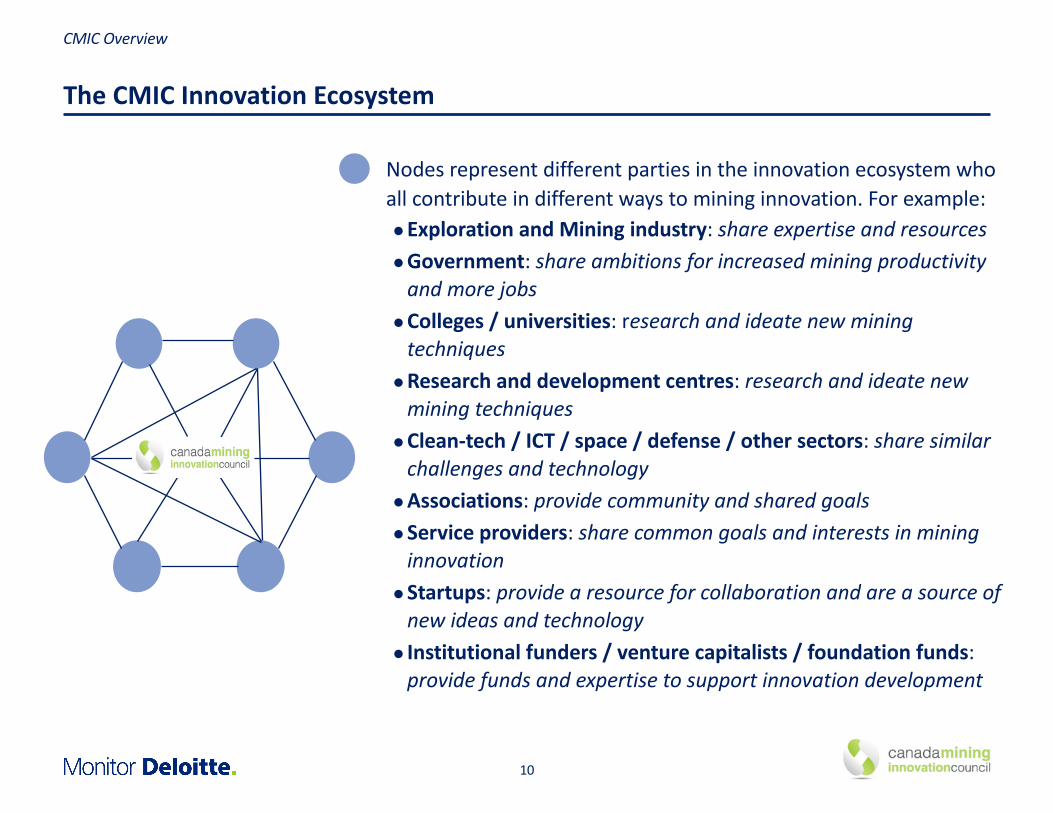

TheCMICInnovationEcosystem

Nodesrepresentdifferentpartiesintheinnovationecosystemwhoallcontributeindifferentwaystomininginnovation.Forexample:lExplorationandMiningindustry:shareexpertiseandresourceslGovernment:shareambitionsforincreasedminingproductivityandmorejobs

lColleges/universities:researchandideatenewminingtechniques

lResearchanddevelopmentcentres: researchandideatenewminingtechniques

lClean-tech/ICT/space/defense/othersectors:sharesimilarchallengesandtechnology

lAssociations:providecommunityandsharedgoalslServiceproviders:sharecommongoalsandinterestsinmininginnovation

lStartups:providearesourceforcollaborationandareasourceofnewideasandtechnology

l Institutionalfunders/venturecapitalists/foundationfunds:providefundsandexpertisetosupportinnovationdevelopment

CMICOverview

11

CMICbusinessecosystemframework

CMICBoardofDirectors

TechnicalWorkingGroupsonZeroWasteMiningFocusAreas

CMICMembership

CMICOfficeExecutiveDirector&CEO

GeneralPartners: CMICmembercompanyrepresentativeswho:l Determineandagreeuponanypre-competitiveissuesl Defineandprioritizebusinessissues/challengesandassociatedprogramsforCMICTechnicalWorkingGroups

l AreprivytoIPinonewayorformderivedfromprojectactivities,althoughnotimmediately

ProjectPartners:CMICmembercompanieswho:l Provide“in-kind”supportintheformofaccesstominingfacilitiesandequipmentforthetestingandimplementingoftechniquesortechnologies

l AreinvolvedaseitherProjectTestSiteLeaders,TechnicalExpertGroups,oroccasionallyintheProjectManagementOffice,andcontributetoactivitiesofprojectimplementationandtesting,ensuringadherencewiththeprojectroadmapandgovernmentregulations

StrategicChoiceCascadingFramework>HowWillCMICConfigure

12

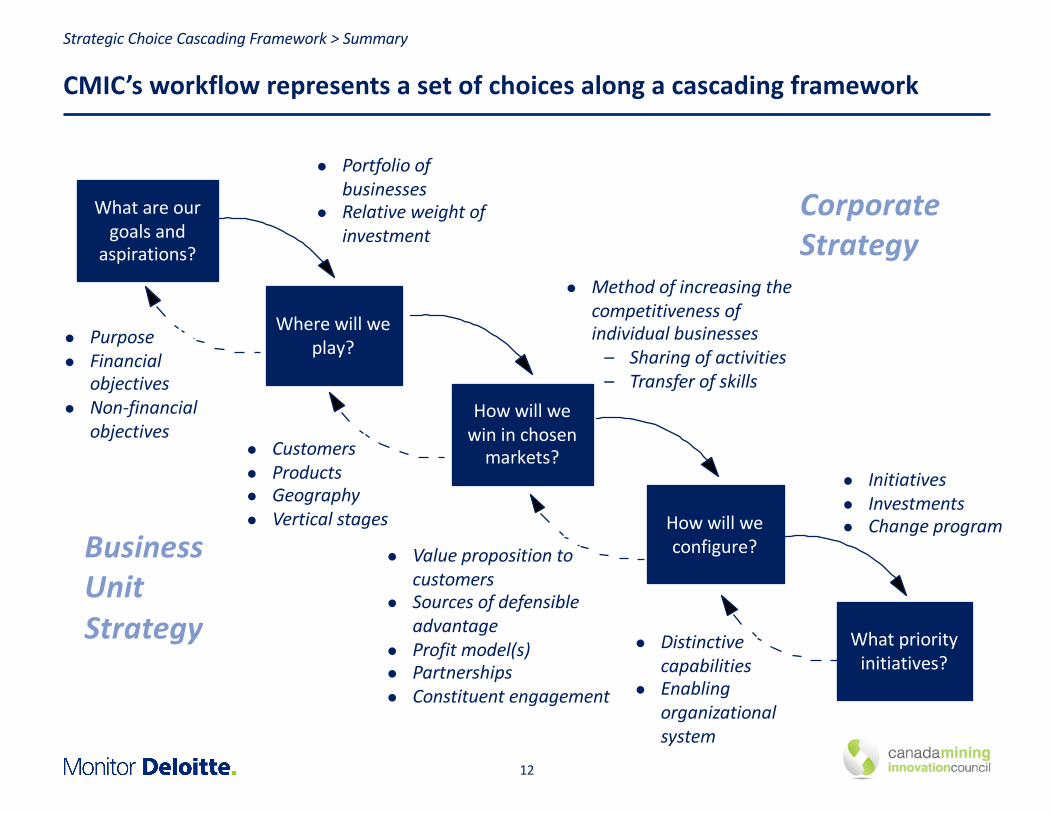

CMIC’sworkflowrepresentsasetofchoicesalongacascadingframework

Howwillwewininchosenmarkets?

Whatpriorityinitiatives?

Whatareourgoalsand

aspirations?

Howwillweconfigure?

Wherewillweplay?

l Initiativesl Investmentsl Changeprogram

l Customersl Productsl Geographyl Verticalstages

l Valuepropositiontocustomers

l Sourcesofdefensibleadvantage

l Profitmodel(s)l Partnershipsl Constituentengagement

l Distinctivecapabilities

l Enablingorganizationalsystem

l Purposel Financial

objectivesl Non-financial

objectives

BusinessUnitStrategy

l Portfolioofbusinesses

l Relativeweightofinvestment

l Methodofincreasingthecompetitivenessofindividualbusinesses– Sharingofactivities– Transferofskills

CorporateStrategy

StrategicChoiceCascadingFramework>Summary

13

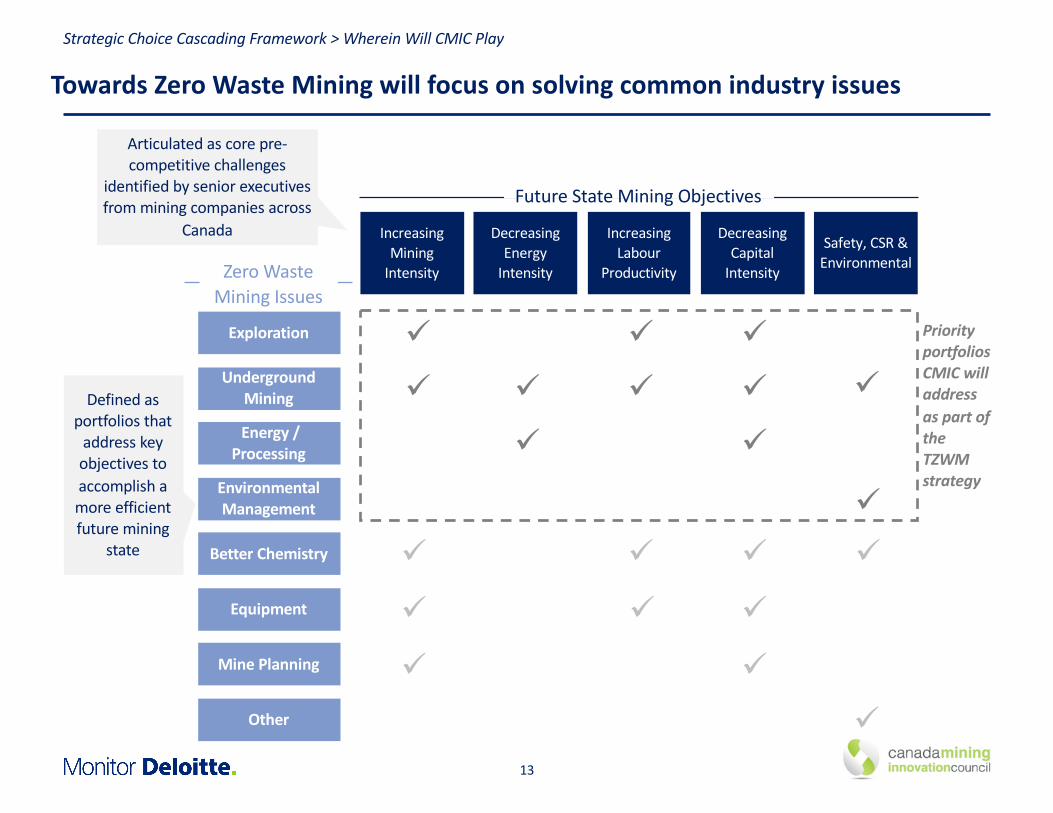

TowardsZeroWasteMiningwillfocusonsolvingcommonindustryissues

IncreasingMiningIntensity

FutureStateMiningObjectives

UndergroundMining

Energy/Processing

EnvironmentalManagement

BetterChemistry

Equipment

MinePlanning

ZeroWasteMiningIssues

DecreasingCapitalIntensity

Other

Exploration

DecreasingEnergyIntensity

IncreasingLabour

Productivity

ü

ü

ü

ü

ü

ü

ü

ü

ü

ü

ü

ü

ü

ü

ü

ü

ü

PriorityportfoliosCMICwilladdressaspartoftheTZWMstrategy

Safety,CSR&Environmental

ü

ü

ü

StrategicChoiceCascadingFramework>WhereinWillCMICPlay

Articulatedascorepre-competitivechallenges

identifiedbyseniorexecutivesfromminingcompaniesacross

Canada

Definedasportfoliosthataddresskeyobjectivestoaccomplishamoreefficientfuturemining

state

ü

14

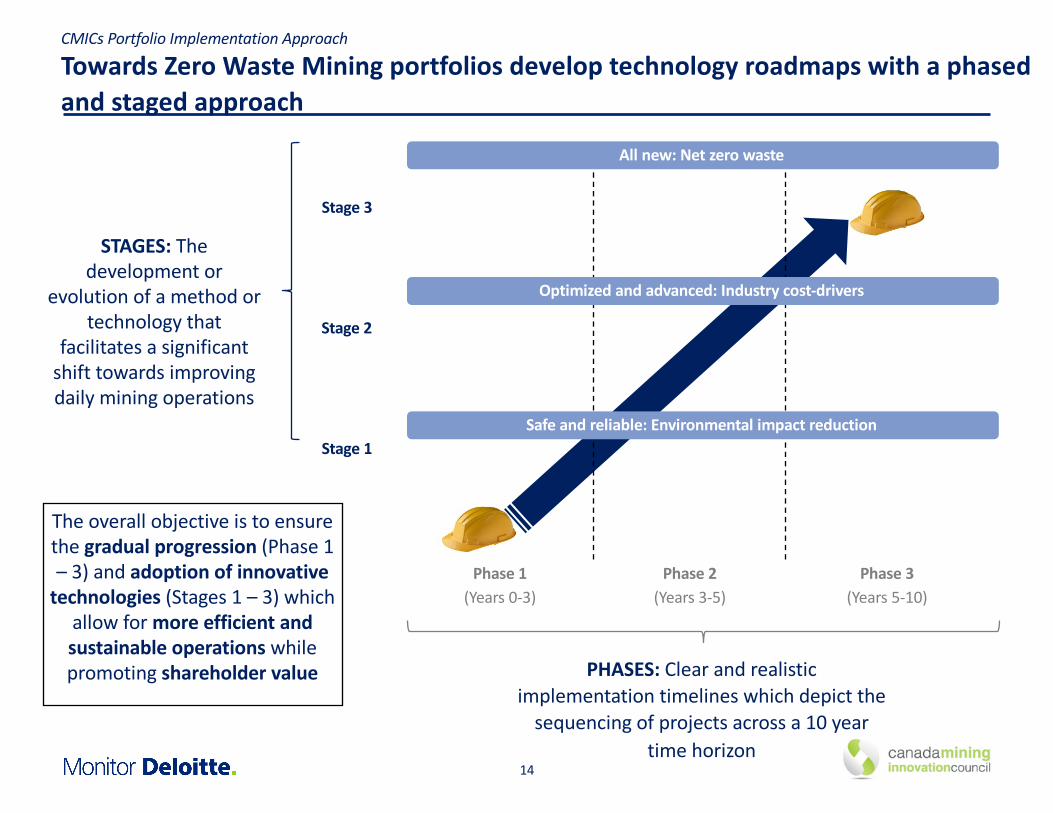

TowardsZeroWasteMiningportfoliosdeveloptechnologyroadmapswithaphasedandstagedapproach

CMICsPortfolioImplementationApproach

Stage1

Stage2

Stage3

STAGES:Thedevelopmentor

evolutionofamethodortechnologythat

facilitatesasignificantshifttowardsimprovingdailyminingoperations

PHASES:Clearandrealisticimplementationtimelineswhichdepictthesequencingofprojectsacrossa10year

timehorizon

Theoverallobjectiveistoensurethegradualprogression(Phase1– 3)andadoptionofinnovativetechnologies (Stages1– 3)which

allowformoreefficientandsustainableoperationswhilepromotingshareholdervalue

Phase1(Years0-3)

Phase2(Years3-5)

Phase3(Years5-10)

Allnew:Netzerowaste

Optimizedandadvanced:Industrycost-drivers

Safeandreliable:Environmentalimpactreduction

15

CMICwillcloselymonitorthetrajectoryofeachportfolio,againsttheroadmaptimelinesandstagegates

Phase1(Years0-3)

Phase2(Years3-5)

Phase3(Years5-10)

Stage3 Allnew:NetZeroWaste

Environmentalsustainabilitywillconstantlyshiftasthe

industryaddressesregulatory/complianceissues,thusStage3

mightnotoccur

Energy/Processingisahistoricalpainpointwithmining

companies,Stage3ispossiblethoughiftheindustrytacklesthemultipleissues

facingprocessinginaparallelmanner

Likelytomakesignificantstridesinstageswiththesmartmineand

efficiencydevelopments

UndergroundMining

Exploration

EnvironmentalStewardship

Energy/Processing

Legend:

ProgressthroughinnovationwillmoveindustrytowardsStage2;howeveritwillcontinuetobeachallengetofinddeeperdepositsandStage3mightnotoccur

CMICsPortfolioImplementationApproach

Stage1 Safeandreliable:Environmentalimpactreduction

Stage2 Optimizedandadvanced:Industrycost-drivers

Appendix

q ListofAbbreviations

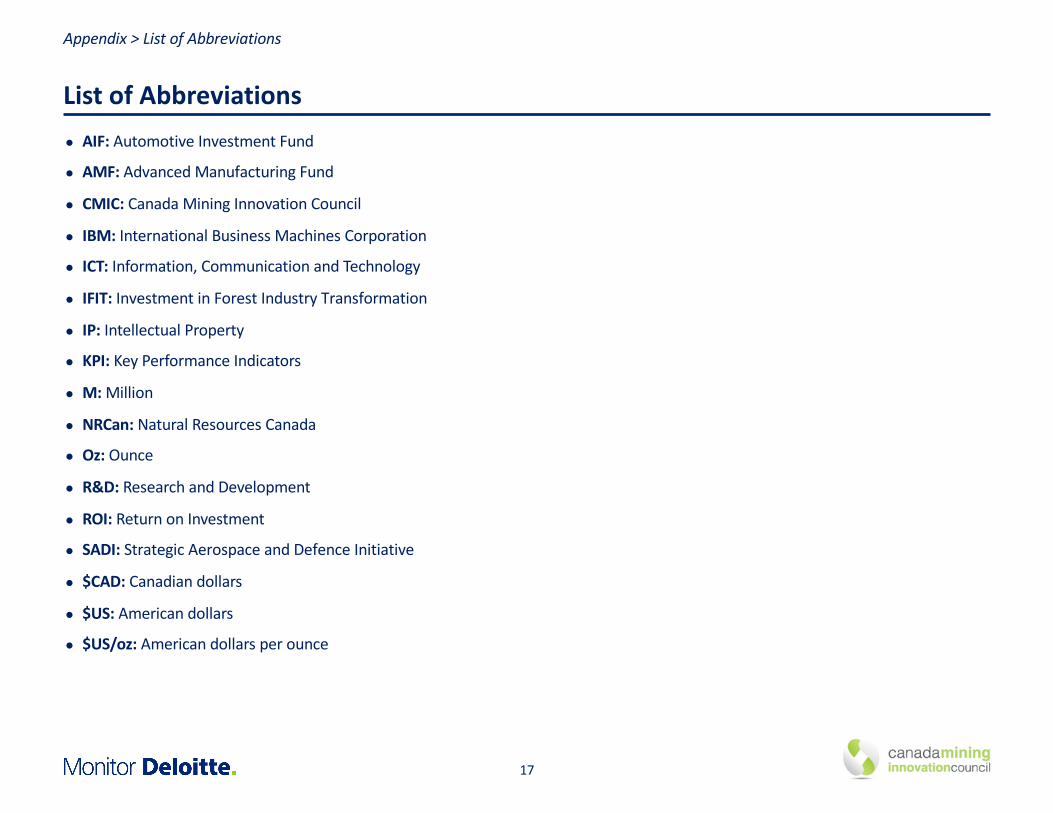

17

ListofAbbreviationsl AIF:AutomotiveInvestmentFund

l AMF:AdvancedManufacturingFund

l CMIC: CanadaMiningInnovationCouncil

l IBM:InternationalBusinessMachinesCorporation

l ICT:Information,CommunicationandTechnology

l IFIT:InvestmentinForestIndustryTransformation

l IP:IntellectualProperty

l KPI:KeyPerformanceIndicators

l M:Million

l NRCan:NaturalResourcesCanada

l Oz:Ounce

l R&D:ResearchandDevelopment

l ROI:ReturnonInvestment

l SADI:StrategicAerospaceandDefenceInitiative

l $CAD:Canadiandollars

l $US:Americandollars

l $US/oz:Americandollarsperounce

Appendix>ListofAbbreviations

18

CMICaimstoreviveCanada’sstatusasaglobalminingleaderbystimulatinginnovation,improvingtechnologyadoption,andpromotingculturalchange

StrategicChoiceCascadingFramework>GoalsandAspirations

Howwillweconfigure?

Whatpriorityinitiatives?

Howwillwewininchosenmarkets?

Whatareourgoalsand

aspirations?

Wherewillweplay?

l ReviveCanada’sstatusasaglobalminingleaderl DrivetheTowardsZeroWasteMiningstrategy- “Stimulate mining technologyinnovation inCanada to achieve zerowaste inminingandmineralprocessing within10-20 years, withafocusonthe environment,energy,andproductivity”by:– Fostercollaborationamongindustry,academia,government,andresearchfacilities,leveragingexpertiseandfundingtoarriveatimplementedsolutionsfasterandmorecosteffective

– Bridgegapbetweenindustrycomplexitiesandcapabilities,focusingonchallengesthatarecommontominingcompaniesl Decreasebarrierstotechnologyadoptionwithintheminingindustry:

– Providesharedcosts/benefitstoprojectparticipants,throughsharingofgenerateddata,freelicensesforsoftwaredeveloped,andnon-commercialaccesstodevelopedIP/patents

– Facilitatedevelopmentofdetailedtechnologyroadmapsandassistindustryinunderstandingthepositivefinancialimpactandreturnoninvestedcapital

l Promoteculturalchangeintheminingindustrytowardlongertermdecisionhorizons:

– ShiftmindsetfromannualKeyPerformanceIndicators(KPIs)to5-10yeartimeframeswhileprovidingincrementalvalueonanannualbasis

l Fosteraminingindustryinnovationbusinessecosystembasedontheprinciplesof:

– Simple,open,fair,andtransparentl Encouragesustainableminingpracticestoimprovethesector’slicensetooperate

19

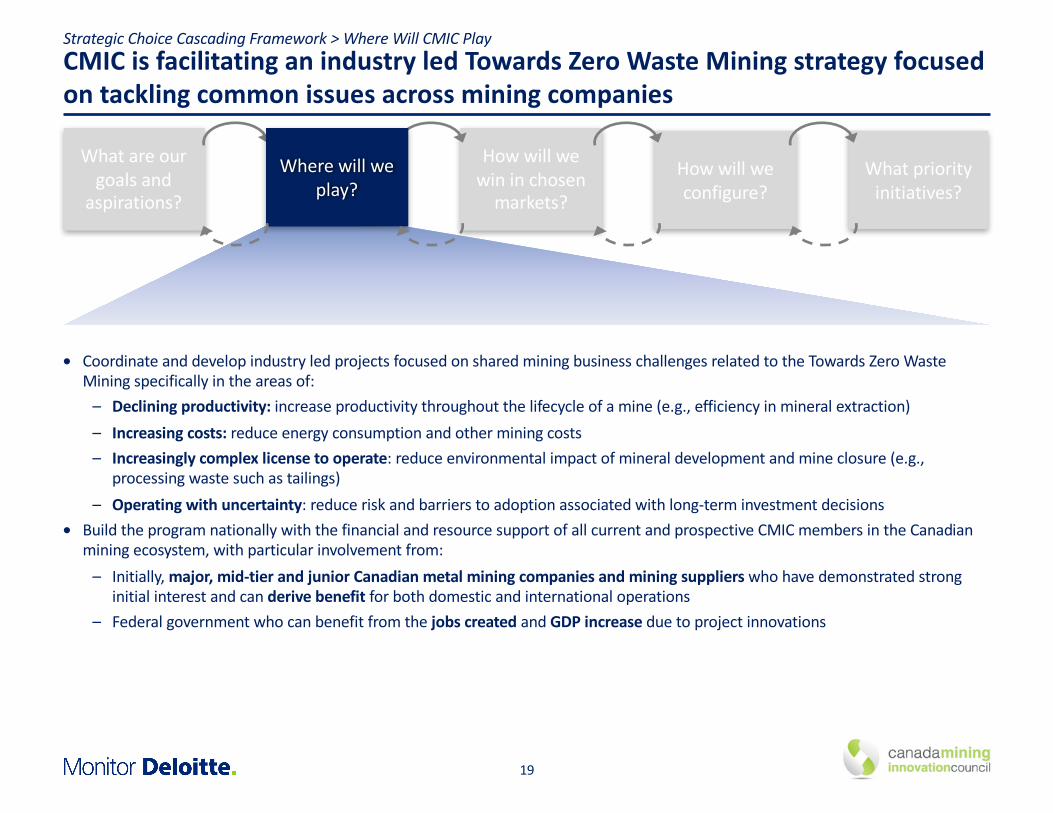

CMICisfacilitatinganindustryledTowardsZeroWasteMiningstrategyfocusedontacklingcommonissuesacrossminingcompanies

StrategicChoiceCascadingFramework>WhereWillCMICPlay

Howwillwewininchosenmarkets?

Whatareourgoalsand

aspirations?

Howwillweconfigure?

Whatpriorityinitiatives?

Wherewillweplay?

l CoordinateanddevelopindustryledprojectsfocusedonsharedminingbusinesschallengesrelatedtotheTowardsZeroWasteMiningspecificallyintheareasof:– Decliningproductivity:increaseproductivitythroughoutthelifecycleofamine(e.g.,efficiencyinmineralextraction)– Increasingcosts:reduceenergyconsumptionandotherminingcosts– Increasinglycomplexlicensetooperate:reduceenvironmentalimpactofmineraldevelopmentandmineclosure(e.g.,

processingwastesuchastailings)– Operatingwithuncertainty:reduceriskandbarrierstoadoptionassociatedwithlong-terminvestmentdecisions

l BuildtheprogramnationallywiththefinancialandresourcesupportofallcurrentandprospectiveCMICmembersintheCanadianminingecosystem,withparticularinvolvementfrom:– Initially,major,mid-tierandjuniorCanadianmetalminingcompaniesandminingsupplierswhohavedemonstratedstrong

initialinterestandcanderivebenefit forbothdomesticandinternationaloperations– Federalgovernmentwhocanbenefitfromthejobscreated andGDPincreaseduetoprojectinnovations

20

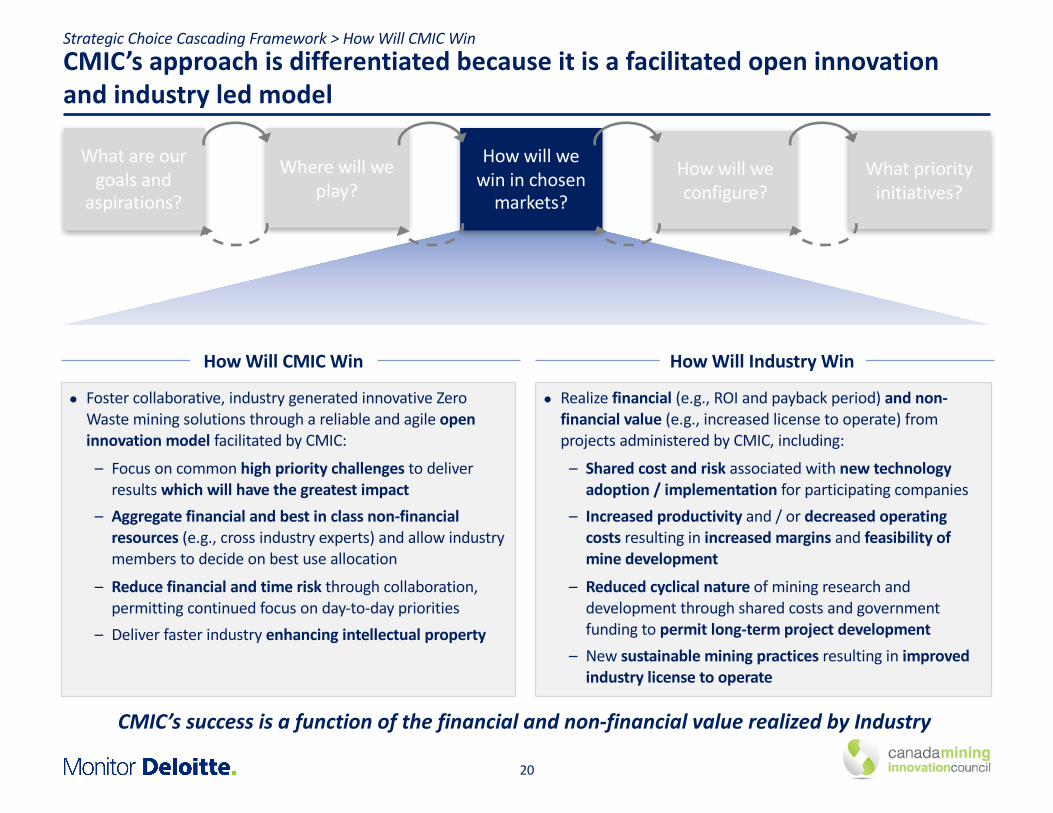

CMIC’sapproachisdifferentiatedbecauseitisafacilitatedopeninnovationandindustryledmodel

StrategicChoiceCascadingFramework>HowWillCMICWin

Howwillweconfigure?

Whatpriorityinitiatives?

Howwillwewininchosenmarkets?

Whatareourgoalsand

aspirations?

Wherewillweplay?

l Fostercollaborative,industrygeneratedinnovativeZeroWasteminingsolutionsthroughareliableandagileopeninnovationmodelfacilitatedbyCMIC:

– Focusoncommonhighprioritychallengestodeliverresultswhichwillhavethegreatestimpact

– Aggregatefinancialandbestinclassnon-financialresources(e.g.,crossindustryexperts)andallowindustrymemberstodecideonbestuseallocation

– Reducefinancialandtimeriskthroughcollaboration,permittingcontinuedfocusonday-to-daypriorities

– Deliverfasterindustryenhancingintellectualproperty

l Realizefinancial (e.g.,ROIandpaybackperiod)andnon-financialvalue(e.g.,increasedlicensetooperate)fromprojectsadministeredbyCMIC,including:

– Sharedcostandriskassociatedwithnewtechnologyadoption/implementation forparticipatingcompanies

– Increasedproductivityand/ordecreasedoperatingcostsresultinginincreasedmarginsandfeasibilityofminedevelopment

– Reducedcyclicalnature ofminingresearchanddevelopmentthroughsharedcostsandgovernmentfundingtopermitlong-termprojectdevelopment

– Newsustainableminingpracticesresultinginimprovedindustrylicensetooperate

CMIC’ssuccessisafunctionofthefinancialandnon-financialvaluerealizedbyIndustry

HowWillCMICWin HowWillIndustryWin

21

CMIChasatransparent,industryledgovernancestructurewithsupportingmechanismstopromoteinnovation

StrategicChoiceCascadingFramework>HowWillCMICConfigure

Howwillweconfigure?

Whatpriorityinitiatives?

Howwillwewininchosenmarkets?

Whatareourgoalsand

aspirations?

Wherewillweplay?

l Governance:

– Developingatransparent,industryledplatformthatwillfosteropeninnovationintheareasofhighestpriority

– Makinglinkagestootherpartieswithintheminingpartnerecosystemtoconnectideasandresources

– Establishingadecisionmakingstructurethatisdrivenbyindustryplayersinbothatopdown(e.g.,BoardofDirectorsiscomprisedofindustryexecutives)andbottomup(e.g.,MembersarecomprisedofnominatedrepresentativeswhoactivelyparticipateinCMICtomakedecisionsregardingprojectplanning,prioritization,execution,IPsharing,etc.onbehalfoftheircompany)approaches

– ProvidingsupporttotheindustryleddecisionmakingstructurethroughastreamlinedCMICProjectManagementOffice

– AstheTowardsZeroWasteStrategyexpands expands,encouragebroaderparticipationofdifferentminingplayersbyofferingtieredinvestmentopportunitiesforcompaniesofdifferentinvestmentcapacityandinterest(currentlythereare2levelsbut athirdlowerlevelmaybeconsidered)

l Supportingmechanisms:

– Definedprojectendgoalsandstagedtargets (e.g.,ROI)

– OpportunitiesforIP/patentownershipforGeneralPartnersandProjectPartners

– Repositoriesofshareddataandfullnon-commercialaccesstoallIP/PatentsdevelopedforCMICmembers

22

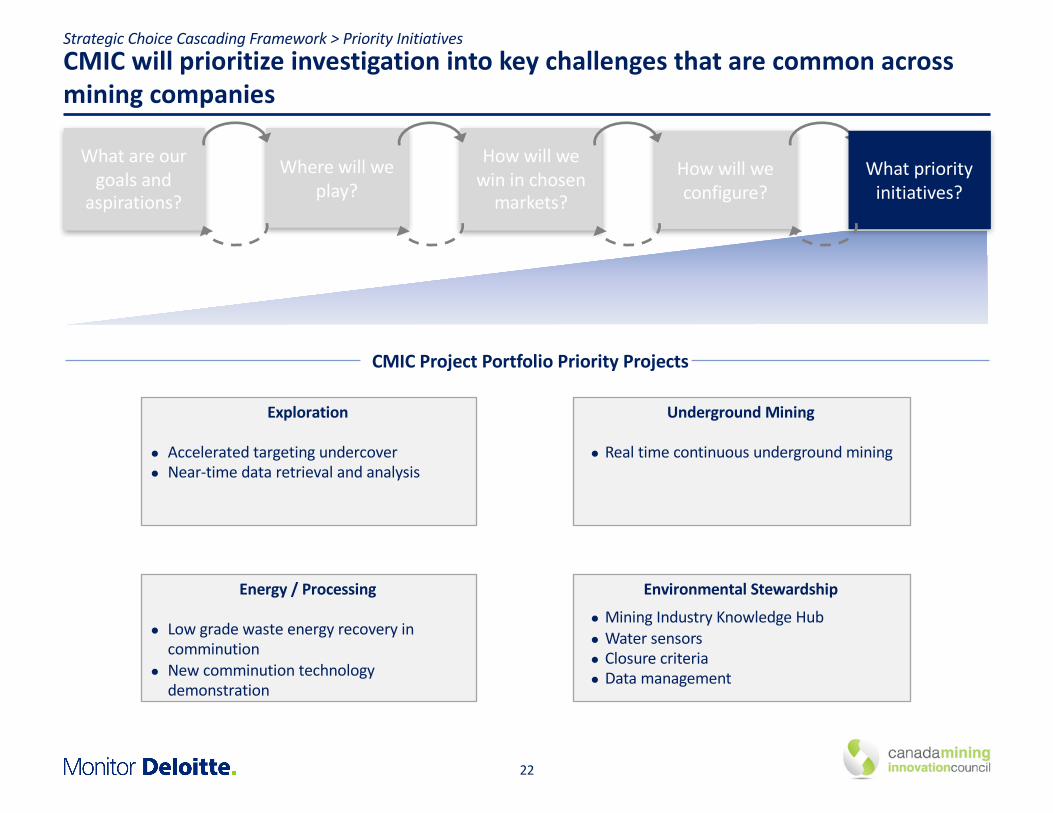

CMICwillprioritizeinvestigationintokeychallengesthatarecommonacrossminingcompanies

StrategicChoiceCascadingFramework>PriorityInitiatives

Howwillweconfigure?

Howwillwewininchosenmarkets?

Whatareourgoalsand

aspirations?

Wherewillweplay?

Whatpriorityinitiatives?

CMICProjectPortfolioPriorityProjects

Exploration

l Acceleratedtargetingundercoverl Near-timedataretrievalandanalysis

UndergroundMining

l Realtimecontinuousundergroundmining

Energy/Processing

l Lowgradewasteenergyrecoveryincomminution

l Newcomminutiontechnologydemonstration

EnvironmentalStewardship

l MiningIndustryKnowledgeHubl Watersensorsl Closurecriterial Datamanagement

23

ThestagedprojectobjectivesallowCMICtotrackthematurityoftechnologyadoptionwhilepromotingasignificantshiftinminingindustry…

Illustrative:WaterSensorProjectStagedTargets

StageGatesExplained

l Provideindustrymemberswithinsightsonhowtocustomizethetechnologytosuittheiroperations,asalignedtoroadmaptargets

Stage2(Optimizedand

advanced:Industrycost-

drivers)

l Begintoadaptexistingtechnologiesforremote,real-timeapplications

Stage1(Safeandreliable:

Environmentalimpactreduction)

l Aspecifiedobjective(e.g.,technology)isworkedon,forexample:– Technologyconceptualizationandtesting

l Tobeginaddressingthechallengeofremote,real-timesensorwaterqualitymonitoring,the3yeartargetofStage1istoestablishinnovationresearchanddevelopnetworks,direction,andinitiativeswithserviceprovidersandresearchfacilities

Stage3(Allnew:Netzero

waste)

l Developnewsensorsforheavymetalsandcontinuedplatformintegration

l Ultimately, thegoalistocommercializesensorpackages forindustryuse

l Allobjectivesoutlinedintheroadmapshavebeenachieved

l Technologieshavereachedimplementationmaturityandarebeingdeployedacrossindustriesparticipants

Progressiontothenextstageisdependentupontheattainmentofthecurrentstage’sobjectives.Forexample,ifnotmet,thepossibilityexiststostill

bebusywithStage1inPhase3

CMICsPortfolioImplementationApproach

24

…theseprioritieswillbephasedalongthefollowingtimelines,withsomereachingtheirroadmaptargetssoonerthanothers

l CMIChasprioritizedareasthatarehighestimpacttoindustrybylisteningtoindustryparticipants intheTechnicalWorkingGroups.Theseparticipantshavedeterminedwheretheywouldliketheinnovationfocustobe andthisisinfluencingthesequencingofevents

l TheprojectsCMIChaschosenfirstalsowillshow“quickwins”oftheopeninnovationmodel.This will helpbuildbrandandcreateacompellingcaseforadditionalfunding.ThisbrandbuildingeffortisimportantasCMIChasundergoneorganizationalchanges(e.g.,purelyresearchbasedprojectstoindustrychosenones).Thiseffortwillre-invigoratecredibilityandconfidencebyindustryandgovernment

l CMIChaschosentostartwithinitiativesinPhase1andaspartoftheinitialfundingrequest,companieswillbeaskedtoallocatefundstothefollowingProjectPortfolios:

Exploration EnvironmentalStewardship

Processing

Phase1(Years0-3)

Phase2(Years3-5)

Phase3(Years5-10)

l ProjectPortfolioinitiativeswhichcouldbedealtwithinthenextphaseinclude:BetterChemistry,Equipment,andMinePlanning

l Theplanningfortheseinitiativeswillbegin1-1.5yearspriortothestartofthisphase

l CMICwilldrivetheadvancementofinnovativetechnologies,throughindustryadoption,totheirnaturalendpoints

l Thefocusduringthisphasewillbetoensurethematurityofimplementation

l Aswithotherphases,thisonewillconsiderthenextplanningcyclesandwhatindustryprioritieswillneedtobeaddressedduringthenextphase

CMICsPortfolioImplementationApproach

UndergroundMining

25

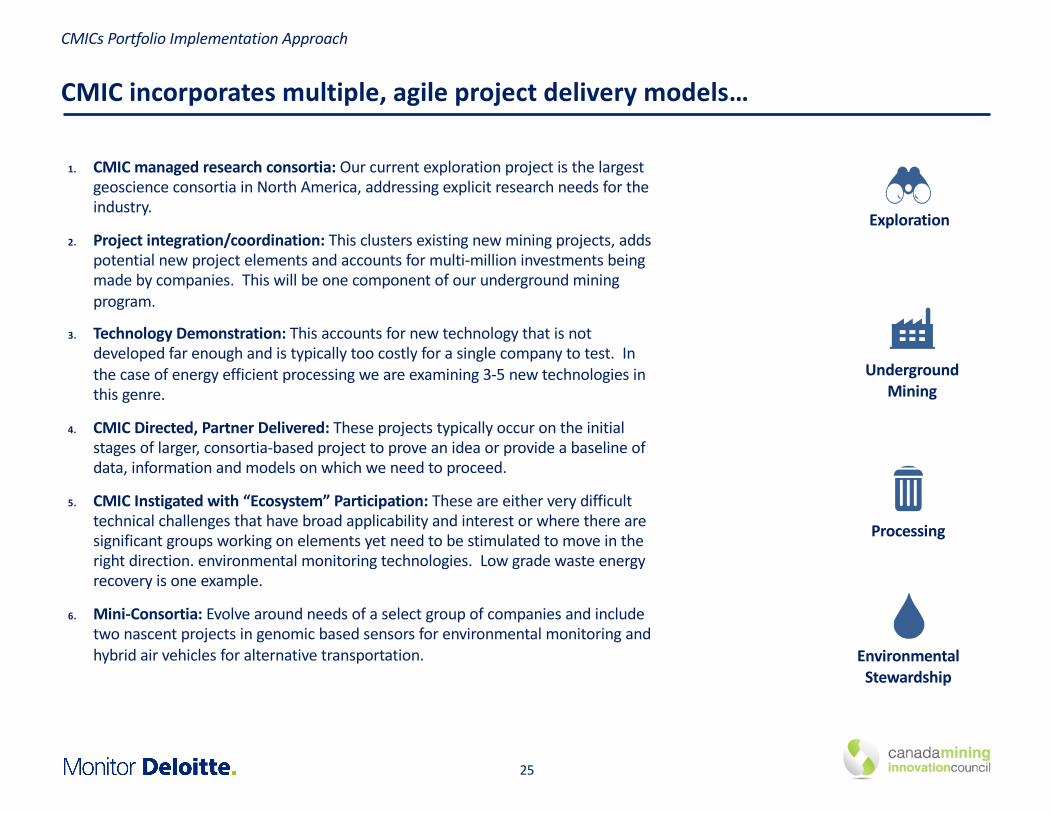

CMICincorporatesmultiple,agileprojectdeliverymodels…

1. CMICmanagedresearchconsortia:OurcurrentexplorationprojectisthelargestgeoscienceconsortiainNorthAmerica,addressingexplicitresearchneedsfortheindustry.

2. Projectintegration/coordination:Thisclustersexistingnewminingprojects,addspotentialnewprojectelementsandaccountsformulti-millioninvestmentsbeingmadebycompanies.Thiswillbeonecomponentofourundergroundminingprogram.

3. TechnologyDemonstration:Thisaccountsfornewtechnologythatisnotdevelopedfarenoughandistypicallytoocostlyforasinglecompanytotest.Inthecaseofenergyefficientprocessingweareexamining3-5newtechnologiesinthisgenre.

4. CMICDirected,PartnerDelivered:Theseprojectstypicallyoccurontheinitialstagesoflarger,consortia-basedprojecttoproveanideaorprovideabaselineofdata,informationandmodelsonwhichweneedtoproceed.

5. CMICInstigatedwith“Ecosystem”Participation:Theseareeitherverydifficulttechnicalchallengesthathavebroadapplicabilityandinterestorwheretherearesignificantgroupsworkingonelementsyetneedtobestimulatedtomoveintherightdirection.environmentalmonitoringtechnologies. Lowgradewasteenergyrecoveryisoneexample.

6. Mini-Consortia:Evolvearoundneedsofaselectgroupofcompaniesandincludetwonascentprojectsingenomicbasedsensorsforenvironmentalmonitoringandhybridairvehiclesforalternativetransportation.

Exploration

EnvironmentalStewardship

CMICsPortfolioImplementationApproach

UndergroundMining

Processing