Embed Size (px)

Citation preview

Canada Market Access Briefing

3

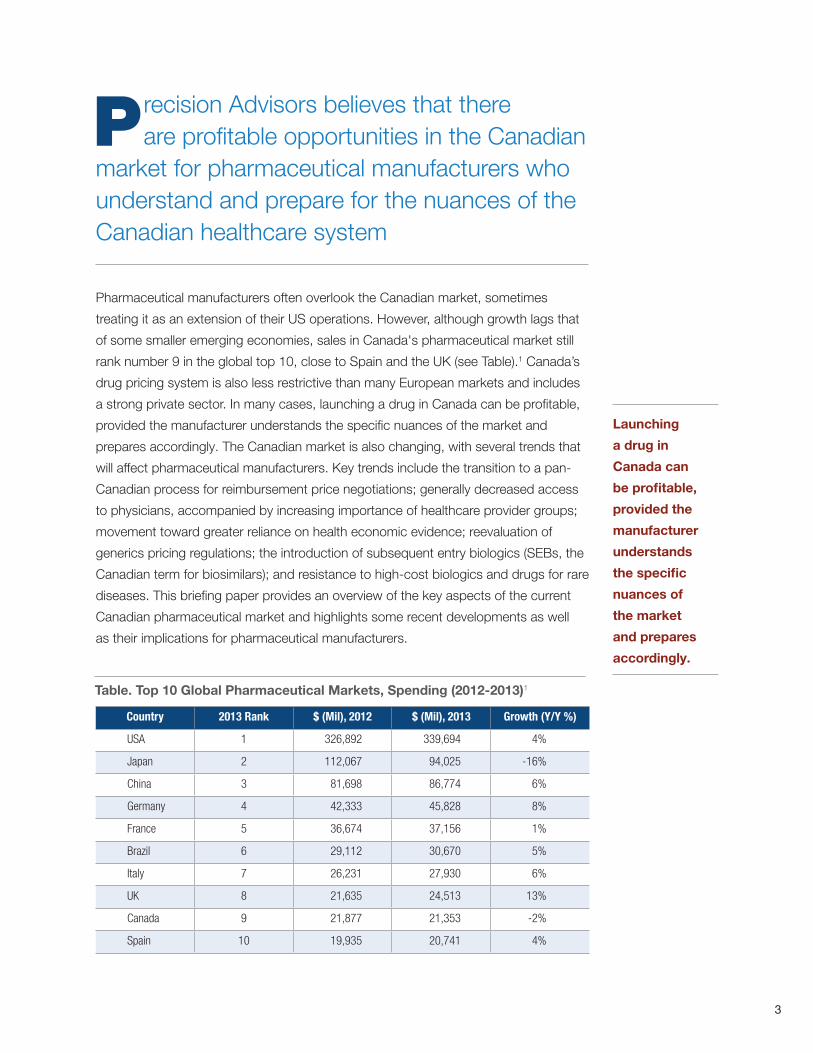

Pharmaceutical manufacturers often overlook the Canadian market, sometimes

treating it as an extension of their US operations. However, although growth lags that

of some smaller emerging economies, sales in Canada's pharmaceutical market still

rank number 9 in the global top 10, close to Spain and the UK (see Table).1 Canada’s

drug pricing system is also less restrictive than many European markets and includes

a strong private sector. In many cases, launching a drug in Canada can be profitable,

provided the manufacturer understands the specific nuances of the market and

prepares accordingly. The Canadian market is also changing, with several trends that

will affect pharmaceutical manufacturers. Key trends include the transition to a pan-

Canadian process for reimbursement price negotiations; generally decreased access

to physicians, accompanied by increasing importance of healthcare provider groups;

movement toward greater reliance on health economic evidence; reevaluation of

generics pricing regulations; the introduction of subsequent entry biologics (SEBs, the

Canadian term for biosimilars); and resistance to high-cost biologics and drugs for rare

diseases. This briefing paper provides an overview of the key aspects of the current

Canadian pharmaceutical market and highlights some recent developments as well

as their implications for pharmaceutical manufacturers.

Country 2013 Rank $ (Mil), 2012 $ (Mil), 2013 Growth (Y/Y %)

USA 1 326,892 339,694 4%

Japan 2 112,067 94,025 -16%

China 3 81,698 86,774 6%

Germany 4 42,333 45,828 8%

France 5 36,674 37,156 1%

Brazil 6 29,112 30,670 5%

Italy 7 26,231 27,930 6%

UK 8 21,635 24,513 13%

Canada 9 21,877 21,353 -2%

Spain 10 19,935 20,741 4%

Table. Top 10 Global Pharmaceutical Markets, Spending (2012-2013)1

recision Advisors believes that there are profitable opportunities in the Canadian market for pharmaceutical manufacturers who understand and prepare for the nuances of the Canadian healthcare system

P

Launching

a drug in

Canada can

be profitable,

provided the

manufacturer

understands

the specific

nuances of

the market

and prepares

accordingly.

4

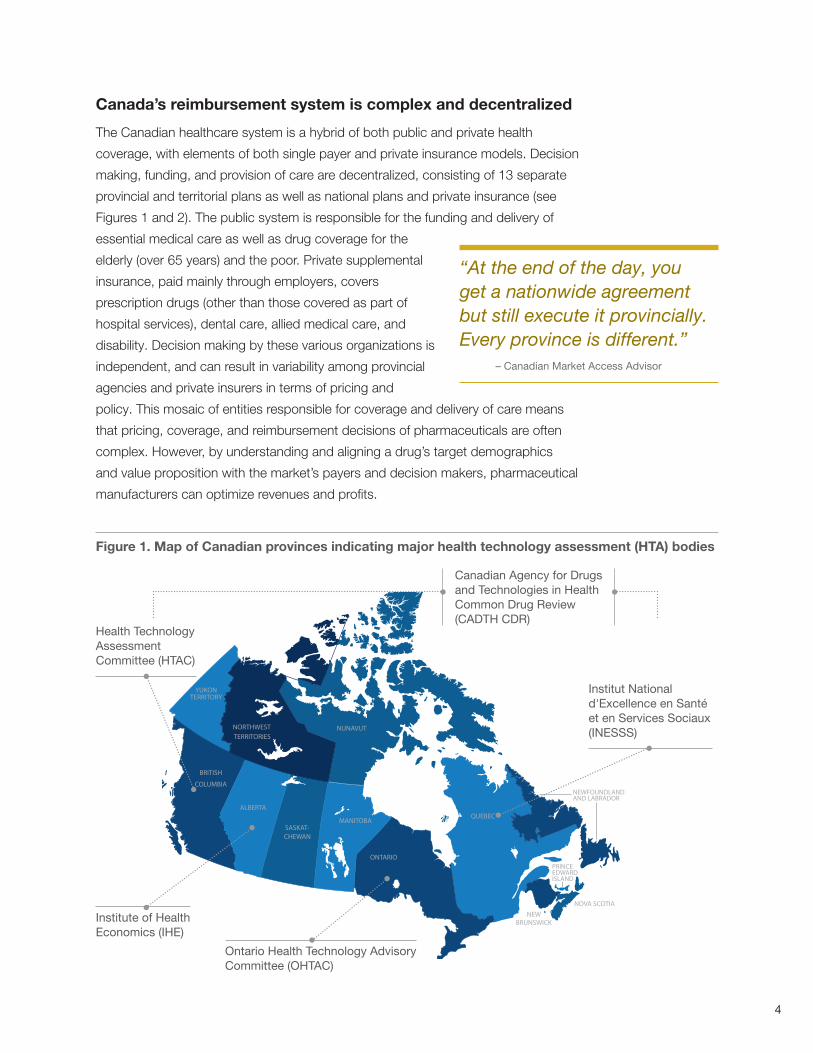

Canada’s reimbursement system is complex and decentralized

The Canadian healthcare system is a hybrid of both public and private health

coverage, with elements of both single payer and private insurance models. Decision

making, funding, and provision of care are decentralized, consisting of 13 separate

provincial and territorial plans as well as national plans and private insurance (see

Figures 1 and 2). The public system is responsible for the funding and delivery of

essential medical care as well as drug coverage for the

elderly (over 65 years) and the poor. Private supplemental

insurance, paid mainly through employers, covers

prescription drugs (other than those covered as part of

hospital services), dental care, allied medical care, and

disability. Decision making by these various organizations is

independent, and can result in variability among provincial

agencies and private insurers in terms of pricing and

policy. This mosaic of entities responsible for coverage and delivery of care means

that pricing, coverage, and reimbursement decisions of pharmaceuticals are often

complex. However, by understanding and aligning a drug’s target demographics

and value proposition with the market’s payers and decision makers, pharmaceutical

manufacturers can optimize revenues and profits.

“At the end of the day, you get a nationwide agreement but still execute it provincially. Every province is different.”

– Canadian Market Access Advisor

NEWFOUNDLANDAND LABRADOR

PRINCEEDWARDISLAND

Figure 1. Map of Canadian provinces indicating major health technology assessment (HTA) bodies

Institute of Health Economics (IHE)

Canadian Agency for Drugs and Technologies in Health Common Drug Review (CADTH CDR)

Institut National d'Excellence en Santé et en Services Sociaux (INESSS)

Ontario Health Technology Advisory Committee (OHTAC)

Health Technology Assessment Committee (HTAC)

5

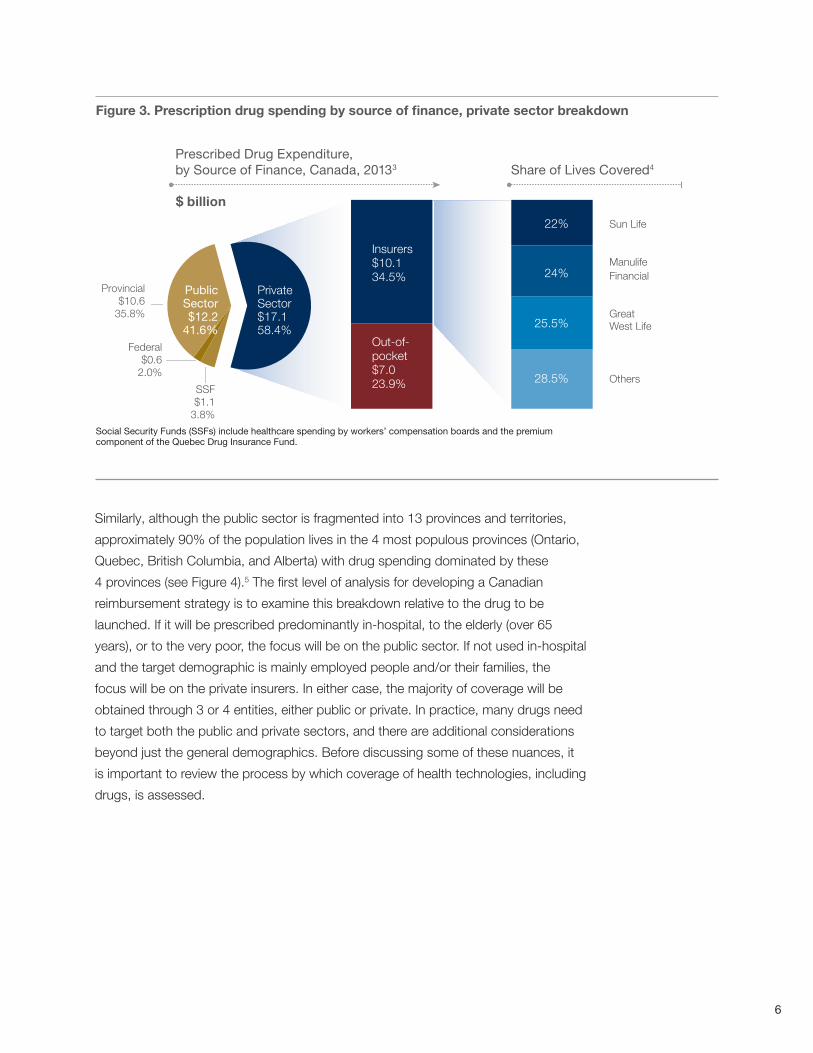

Private sector drug coverage comprises nearly 60% of prescription drug spending

Although public sector coverage comprises approximately 70% of overall Canadian

health spending,2 nearly 60% of prescription drug spending comes from the private

sector, including both private insurance and out-of-pocket spending by consumers

(see Figure 3).3 Furthermore, more than two-thirds of private insurance coverage is

managed by 3 insurers. In addition, within private insurance plans, approximately

70%-75% of these are “open access,” ie, have few coverage restriction.4 A number

of open plans use prior authorizations and copays to manage some cost impact;

however, access to these plans is generally quick and without price negotiations or

contracting. The remaining plans are “managed care.” These plan designs typically

use a more comprehensive clinical and economic review, use tiering and formularies,

and sometimes match funding decisions by the provinces. Moreover, some of the

managed plans are now considering price contracting as a means to control program

costs. Private, open insurance plans are particularly attractive for pharmaceutical

manufacturers due to their relatively free pricing and speed to access the benefit

plan. This is especially the case if their product is used in a therapeutic area that is

predominantly prescribed to a younger, employed demographic.

Figure 2. Overview of Canadian public sector healthcare governance and responsibilities

n National level: Health Canada is responsible for national public health (eg, Public Health Agency, National Microbiology Laboratory, compliance and enforcement). The Department of Finance is responsible for overseeing federal transfer payments to the provinces and territories

n Provincial level: Provinces administer funds, define provincial priorities (in alignment with national priorities), and set fee schedules for healthcare services

n Regional level: Local healthcare financing and administration ensure that provincial priorities are met. Healthcare delivery is coordinated by regional health authorities

n Local level: Primary care clinics and office-based specialists are privately owned facilities that are reimbursed based on fee schedules set by the provincial Ministry of Health

– Hospitals are not-for-profit, publicly owned corporations

– Hospital outpatient clinics are funded as part of the hospital budget and may receive supplemental funding from the region or provincial Ministry of Health

Federal Government

Determines national policies/priorities/budget

Provincial Government

Applies federal policies/priorities/budget and prescribes health services

Regional Health Authority

Allocates resources and assigns services

Local Healthcare Providers

Delivers healthcare services in alignment with policy, priorities, and annual budget

Patient Outcomes

6

Figure 3. Prescription drug spending by source of finance, private sector breakdown

SSF$1.1

3.8%

Federal$0.6

2.0%

Provincial$10.6

35.8%

Insurers$10.134.5%

Out-of-pocket$7.023.9%

Private Sector $17.158.4%

Prescribed Drug Expenditure, by Source of Finance, Canada, 20133

PublicSector$12.2

41.6%

28.5%

25.5%

24%

22%

Others

Great West Life

ManulifeFinancial

Sun Life

Share of Lives Covered4

$ billion

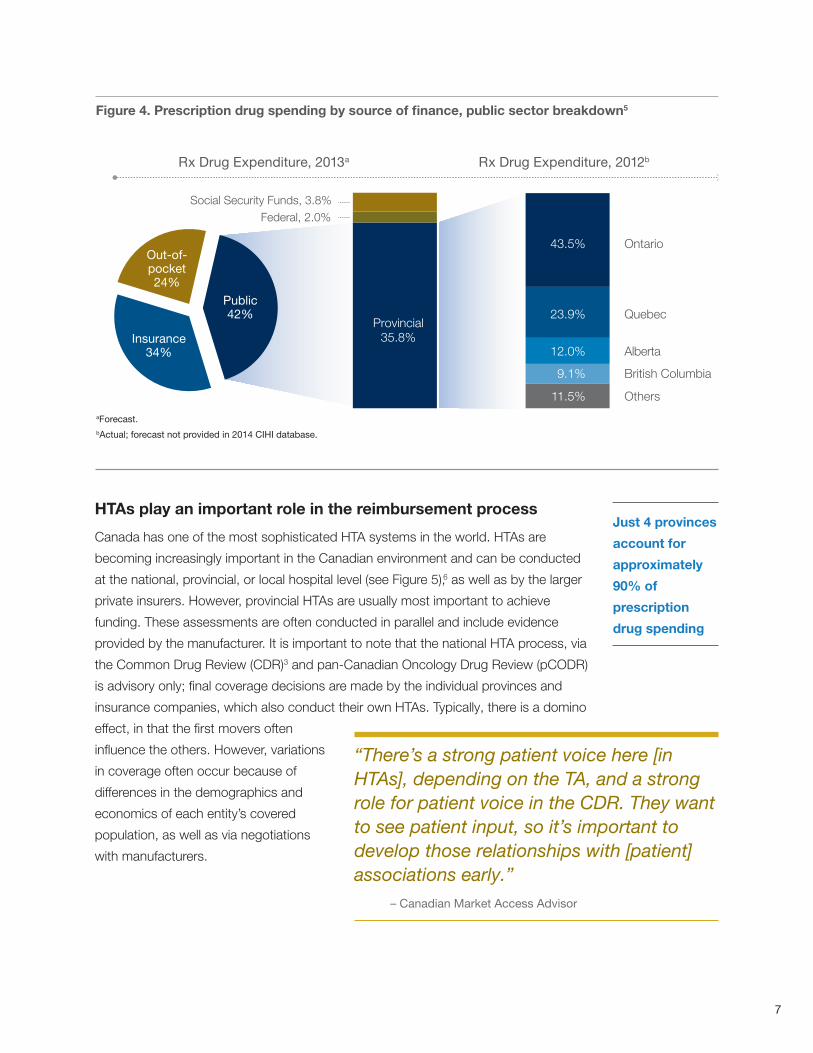

Similarly, although the public sector is fragmented into 13 provinces and territories,

approximately 90% of the population lives in the 4 most populous provinces (Ontario,

Quebec, British Columbia, and Alberta) with drug spending dominated by these

4 provinces (see Figure 4).5 The first level of analysis for developing a Canadian

reimbursement strategy is to examine this breakdown relative to the drug to be

launched. If it will be prescribed predominantly in-hospital, to the elderly (over 65

years), or to the very poor, the focus will be on the public sector. If not used in-hospital

and the target demographic is mainly employed people and/or their families, the

focus will be on the private insurers. In either case, the majority of coverage will be

obtained through 3 or 4 entities, either public or private. In practice, many drugs need

to target both the public and private sectors, and there are additional considerations

beyond just the general demographics. Before discussing some of these nuances, it

is important to review the process by which coverage of health technologies, including

drugs, is assessed.

Social Security Funds (SSFs) include healthcare spending by workers’ compensation boards and the premium component of the Quebec Drug Insurance Fund.

7

Figure 4. Prescription drug spending by source of finance, public sector breakdown5

Rx Drug Expenditure, 2013a Rx Drug Expenditure, 2012b

Out-of-pocket24%

Insurance34%

Public42%

British Columbia

Others

Alberta

Quebec

Ontario

Social Security Funds, 3.8%Federal, 2.0%

Provincial35.8%

11.5%

9.1%

12.0%

23.9%

43.5%

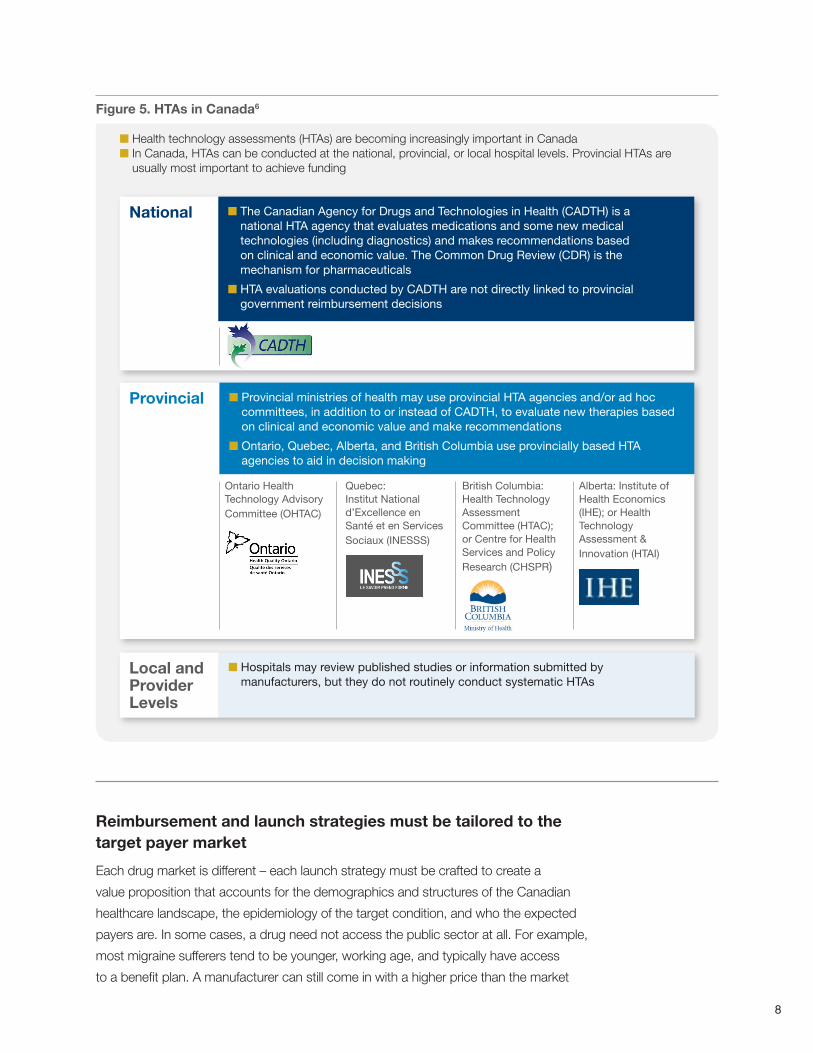

HTAs play an important role in the reimbursement process

Canada has one of the most sophisticated HTA systems in the world. HTAs are

becoming increasingly important in the Canadian environment and can be conducted

at the national, provincial, or local hospital level (see Figure 5),6 as well as by the larger

private insurers. However, provincial HTAs are usually most important to achieve

funding. These assessments are often conducted in parallel and include evidence

provided by the manufacturer. It is important to note that the national HTA process, via

the Common Drug Review (CDR)3 and pan-Canadian Oncology Drug Review (pCODR)

is advisory only; final coverage decisions are made by the individual provinces and

insurance companies, which also conduct their own HTAs. Typically, there is a domino

effect, in that the first movers often

influence the others. However, variations

in coverage often occur because of

differences in the demographics and

economics of each entity’s covered

population, as well as via negotiations

with manufacturers.

Just 4 provinces

account for

approximately

90% of

prescription

drug spending

“There’s a strong patient voice here [in HTAs], depending on the TA, and a strong role for patient voice in the CDR. They want to see patient input, so it’s important to develop those relationships with [patient] associations early.”

– Canadian Market Access Advisor

aForecast.bActual; forecast not provided in 2014 CIHI database.

8

Figure 5. HTAs in Canada6

Reimbursement and launch strategies must be tailored to the target payer market

Each drug market is different – each launch strategy must be crafted to create a

value proposition that accounts for the demographics and structures of the Canadian

healthcare landscape, the epidemiology of the target condition, and who the expected

payers are. In some cases, a drug need not access the public sector at all. For example,

most migraine sufferers tend to be younger, working age, and typically have access

to a benefit plan. A manufacturer can still come in with a higher price than the market

National n The Canadian Agency for Drugs and Technologies in Health (CADTH) is a national HTA agency that evaluates medications and some new medical technologies (including diagnostics) and makes recommendations based on clinical and economic value. The Common Drug Review (CDR) is the mechanism for pharmaceuticals

n HTA evaluations conducted by CADTH are not directly linked to provincial government reimbursement decisions

Local and Provider Levels

n Hospitals may review published studies or information submitted by manufacturers, but they do not routinely conduct systematic HTAs

Provincial n Provincial ministries of health may use provincial HTA agencies and/or ad hoc committees, in addition to or instead of CADTH, to evaluate new therapies based on clinical and economic value and make recommendations

n Ontario, Quebec, Alberta, and British Columbia use provincially based HTA agencies to aid in decision making

Ontario Health Technology Advisory Committee (OHTAC)

Quebec: Institut National d’Excellence en Santé et en Services Sociaux (INESSS)

British Columbia: Health Technology Assessment Committee (HTAC); or Centre for Health Services and Policy Research (CHSPR)

Alberta: Institute of Health Economics (IHE); or Health Technology Assessment & Innovation (HTAI)

n Health technology assessments (HTAs) are becoming increasingly important in Canada n In Canada, HTAs can be conducted at the national, provincial, or local hospital levels. Provincial HTAs are

usually most important to achieve funding

9

and get the open plans to cover 70%-75% of the 19.5 million people with access to

private insurance. Marketing can help. Biogen IDEC’s Amevive®, a biologic treatment for

psoriasis, did relatively poorly in the United States but did well in Canada. It targeted a

population of mostly younger, privately insured patients via a strong marketing campaign

to dermatologists. Canadian sales were 25% of those in the United States, which has

nearly 10 times the population. The remaining privately insured managed plans use

a variety of methodologies similar to those in the United States to control drug costs.

One approach private insurers (eg, Sun Life) are starting to use as an affordable third

tier option for their customers is a hyper-managed/generics-first plan, outsourced (or

subcontracted) to the Reformulary Group.7 Reformulary offers generics as first tier and

then approaches pharmaceutical manufacturers directly to negotiate a price deal, get a

better listing, or get more favorable criteria.

In the public sector, value outside the drug can be influential. The Inspired COPD

Outreach Program is a good example of how a manufacturer has been able to gain

favorable coverage and maintain premium pricing by adding value beyond the drug

itself. Boehringer Ingelheim (BI), following a pilot program with a clinic in Nova Scotia,

partnered with the Canadian Foundation for Healthcare Improvement (CFHI) to

provide funding and support to enable providers to implement an approach to reduce

emergency room visits, hospital admissions, and days in hospital among participating

patients with chronic obstructive pulmonary disease (COPD).8 BI’s support for this

program has enabled it to maintain premium pricing of its COPD medications along

with favorable marketing and PR.

For public and private payers alike, the value proposition should also include incentives

for providers. These generally fall into 2 categories – quality of care and financial.

As Canadian providers are private businesses, they are motivated to make money

(increased revenues or cost savings). They are also evaluated on quality performance

metrics, which affects them financially. Overall, the more the manufacturer is able to

create a value proposition that addresses all stakeholders – patients, payers, and

providers – the better able they will be to gain favorable coverage and pricing. Effective

marketing can help, of course, but unless key stakeholder relationships are developed

early on and informed by a deeper understanding of each stakeholder’s economics,

marketing can be an uphill battle. This understanding starts with health economics.

For public and

private payers

alike, the value

proposition

should also

include

incentives for

providers.

10

Health economics is becoming increasingly important to marketing, market access, pricing, and contracting

As in other markets, access to individual physicians is becoming increasingly

restricted. Marketing and sales are moving to a B2B model as physicians are

accessed via group purchasing organizations (GPOs) and integrated HCP groups

rather than individually via sales reps. These groups are looking directly at their

budget, finances, and quality performance metrics (which affect how they are paid).

Similarly, payers examine budget impact

and cost savings when negotiating

contracts and pricing. The key to

avoiding downward pricing pressure, or

maintaining premium or parity pricing, is

to develop a value proposition in terms of

overall budget impact or cost savings. As

discussed in the BI example, that value

may be outside the drug. Preparing a

drug for launch today requires developing

some level of health economic modeling

with consideration of stakeholder

impacts, as well as developing key stakeholder relationships in advance, whether

the primary target payer is in the public sector, private insurer, or both. For the public

sector, health economic analysis is becoming particularly important as pricing and

contracting is moving toward a national process.

Contract negotiation processes are changing

In the past, public sector contract negotiations were conducted separately and

confidentially with each province. The only exception was Quebec, which has had

a requirement that all contracted pricing decisions be disclosed publicly. With the

exception of Quebec, this has meant that manufacturers needed to conduct multiple

simultaneous negotiations, but also that it was possible to secure favorable deals.

A new agreement among the provinces has resulted in the establishment of a pan-

Canadian pricing negotiation process, the pan-Canadian Pharmaceutical Alliance

(pCPA), formerly known as the pan-Canadian Pricing Alliance.9 Soon to be based in

Ontario, the pCPA conducts joint provincial/territorial negotiations for brand name

drugs in Canada. All brand name drugs coming forward for funding through the

national review processes CDR or pCODR are now considered for negotiation through

the pCPA. The current structure is that one province will negotiate on behalf of all

the others. Effectively, there will be one negotiation rather than several, with certain

provinces taking the lead in certain areas of specialty (eg, oncology in Ontario and

British Columbia, rare diseases in Alberta and Ontario).

“There is a move to health economics, to bring stakeholder discussions and influence earlier…health economics is becoming far more aggressive, with the biggest growth on the market access side, and less on government relations…whereas commercial sales teams have shrunk.”

– Manager, Canadian Market Access, Pharmaceutical Company

11

The pCPA is still in the process of being established, with little clarity yet on rules

and procedures. Furthermore, Quebec has announced that it will join in the national

negotiation scheme. Historically, Quebec has followed a separate review and funding

process and it still remains unclear how its participation in the pCPA will affect the

national process in practice. It is also important to note that each province executes the

national agreement separately, including aspects such as formulary access, utilization

agreements, volume discounts, claims adjudication, handling of expensive drugs,

distribution, and time to listing. These

pathways need to be mapped out for

each province, at least for more complex

agreements.

In other respects, negotiation processes

remain the same. The goal in negotiation

with payers is to avoid restrictions and

negative price pressure by showing

value to the overall budget. With HCP

formularies and the retail channel, the

goal is to get a listing and, if possible,

a preferential listing (eg, with volume

rebates). With HCPs, the key in

negotiations is to show 1 of 2 things: either make/save money or improve quality. The top

quality metrics are wait times, length of stay, readmission, and infection rates. With retail,

a typical negotiation tool is to use rebates along with some other value-add, such as a

pharmacist education program.

Biosimilars (SEBs) are just beginning to enter the market

One of the more recent developments in the Canadian market, as in other markets,

is the introduction of biosimilars – known as SEBs in Canada.10 These are new

biologic drugs designed to be similar to their branded original reference drugs, also

known as bio-originals, or reference biologics. In 2010, Health Canada unveiled its

regulatory guidance for the entry of SEBs into the Canadian market (see Figure 6).11 The

introduction of SEBs presents unique regulatory and reimbursement challenges. Unlike

the more common, small-molecule drugs, biologics generally exhibit high molecular

complexity and are sensitive to changes in manufacturing practices. Since SEBs are

not considered to be therapeutically or pharmaceutically equivalent to the reference

biologic drug, Health Canada does not support the automatic substitution of an SEB for

its reference product.

“It’s all changing now…traditionally, it was a price negotiation, but is now evolving where manufacturers spend more resources building their value proposition with stakeholders – patient advocacy groups, physicians – to demonstrate why payers should keep prices at a premium, or not restrict access.”

– Manager, Canadian Market Access, Pharmaceutical Company

12

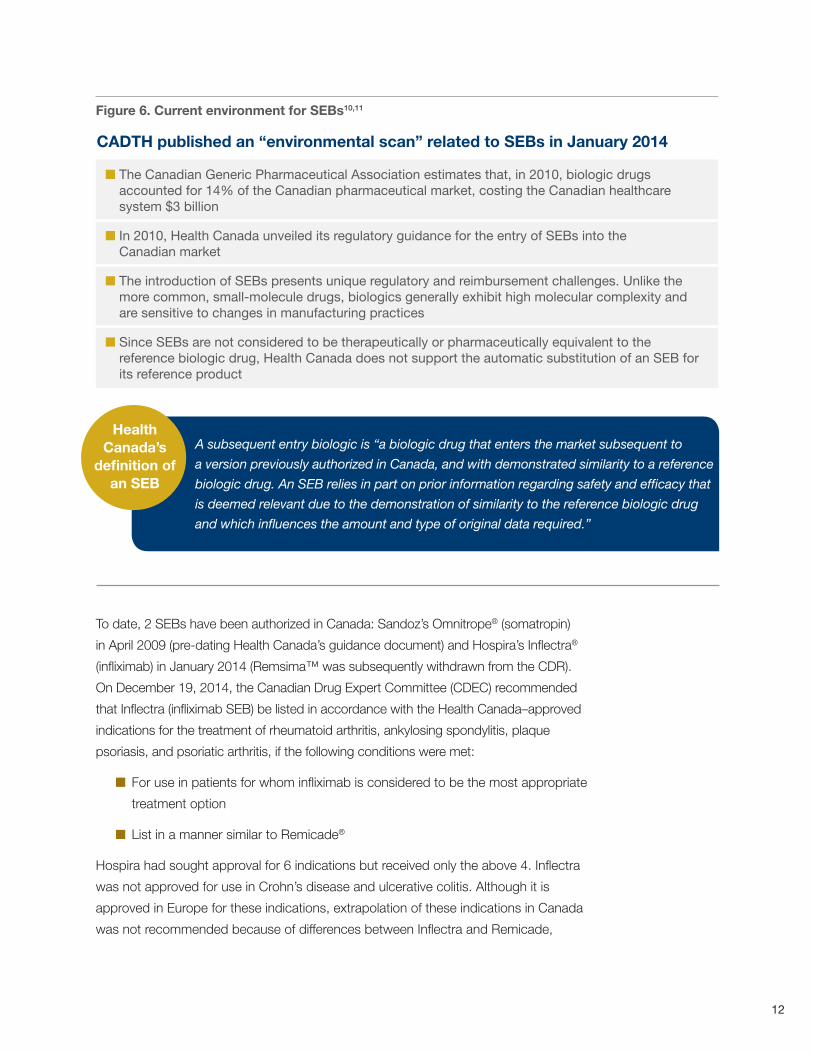

Figure 6. Current environment for SEBs10,11

To date, 2 SEBs have been authorized in Canada: Sandoz’s Omnitrope® (somatropin)

in April 2009 (pre-dating Health Canada’s guidance document) and Hospira’s Inflectra®

(infliximab) in January 2014 (Remsima™ was subsequently withdrawn from the CDR).

On December 19, 2014, the Canadian Drug Expert Committee (CDEC) recommended

that Inflectra (infliximab SEB) be listed in accordance with the Health Canada–approved

indications for the treatment of rheumatoid arthritis, ankylosing spondylitis, plaque

psoriasis, and psoriatic arthritis, if the following conditions were met:

n For use in patients for whom infliximab is considered to be the most appropriate

treatment option

n List in a manner similar to Remicade®

Hospira had sought approval for 6 indications but received only the above 4. Inflectra

was not approved for use in Crohn’s disease and ulcerative colitis. Although it is

approved in Europe for these indications, extrapolation of these indications in Canada

was not recommended because of differences between Inflectra and Remicade,

n The Canadian Generic Pharmaceutical Association estimates that, in 2010, biologic drugs accounted for 14% of the Canadian pharmaceutical market, costing the Canadian healthcare system $3 billion

n In 2010, Health Canada unveiled its regulatory guidance for the entry of SEBs into the Canadian market

n The introduction of SEBs presents unique regulatory and reimbursement challenges. Unlike the more common, small-molecule drugs, biologics generally exhibit high molecular complexity and are sensitive to changes in manufacturing practices

n Since SEBs are not considered to be therapeutically or pharmaceutically equivalent to the reference biologic drug, Health Canada does not support the automatic substitution of an SEB for its reference product

CADTH published an “environmental scan” related to SEBs in January 2014

Health Canada’s

definition of an SEB

A subsequent entry biologic is “a biologic drug that enters the market subsequent to

a version previously authorized in Canada, and with demonstrated similarity to a reference

biologic drug. An SEB relies in part on prior information regarding safety and efficacy that

is deemed relevant due to the demonstration of similarity to the reference biologic drug

and which influences the amount and type of original data required.”

13

the reference product. Once granted marketing authorization for one or more of

the reference indications, an SEB may seek a formulary listing and coverage by the

provincial and private insurance plans.

The introduction of SEBs offers the

potential to reduce healthcare costs

by introducing competition into the

biologic drugs market. Although this

is likely to be true in the long run, the

cost savings in the short-term may

be limited because of slow uptake

by physicians and lack of interchangeability (prescriptions are still filled as written).

Currently, Canadian payers expect discounts to be in the range of 20%-25% off the

price of the branded products.12 Slow uptake by physicians reflects strong familiarity

and comfort with the branded products and poor understanding among physicians

about SEBs reinforced by marketing messages from the manufacturers of the branded

products. Over the next several years, as more SEBs enter the market and physicians

become familiar with and educated about SEBs, overall costs to the system should

decrease. Nevertheless, payers are approaching SEBs somewhat cautiously as they

do not want to move too far ahead of their constituents (physicians and patients). As

they put processes in place, most payers are in reactive mode, handling submissions

on a case-by-case basis and developing their processes as they do so. With the

introduction of Inflectra and a pipeline of other SEBs, we expect most Canadian HTAs

and payers to have established processes in place over the next 1-2 years.

Conclusions

To compete in the Canadian market, pharmaceutical manufacturers need to do their

homework, develop key relationships early, and build their value proposition with key

stakeholders. Understanding target demographics in relation to the payer landscape

is a first step in tailoring a payer strategy. In some cases, it is possible to enter the

market successfully even with no public coverage and without negotiations (such as by

targeting the under 65 and employed population with open plans). In addition, health

economic modeling and stakeholder mapping is important as part of developing the

value proposition. That value proposition may entail showing benefits outside the drug

itself, and for providers (physicians and pharmacists) as well as payers, it’s not just

about price. Finally, forge key relationships early. It’s not sufficient to “bring in some

medical science liaisons from the United States.” It’s necessary to develop relationships

with key stakeholders, whether these are payers, physicians, or patient advocacy

groups, via representatives who know the Canadian market.

“SEBs are in early development in Canada and require acceptance from physicians and patients, and the degree of cost savings remains to be determined.”

– Canadian PBM

14

Precision Advisors supports pharmaceutical manufacturers in their strategic decisions, product launch planning, and market access needs

Precision Advisors is a full-service consulting and advisory firm. Capabilities to assist

pharmaceutical, device, and diagnostics manufacturers include

n Corporate and business/franchise strategy

n Product and portfolio strategy

n Launch preparation, planning, and execution support

n Market access expertise

n Health economic assessment support, including HEOR and payer value

proposition development

n Advanced analytics

Contact

For more information, contact

Michael D. Jacobson, PhD

Principal, Strategy

Precision Advisors

55 Cambridge Parkway, 300E

Cambridge, MA 02142

Tel: 617-299-3010

Larry Blandford, PharmD

Executive Vice President, Managing Partner

Precision Advisors

55 Cambridge Parkway, 300E

Cambridge, MA 02142

Tel: 502-939-9862

15

1. IMS, accessed via statista.com.

2. Canadian Institute for Health Information: Healthcare Cost Drivers: The Facts, 2011. https://secure.cihi.ca/free_products/health_care_cost_drivers_the_facts_en.pdf. Accessed January 22, 2015.

3. National Health Expenditure Database, 2013, Canadian Institute for Health Information.

4. Patient Access Solutions Inc.; Equitus Consulting.

5. National Health Expenditure Database, 2014, Canadian Institute for Health Information. Guidelines for the economic evaluation of health technologies: Canada [3rd Edition]. Ottawa: Canadian Agency for Drugs and Technologies in Health; 2006.

6. Canadian Institute for Health Information. Exploring the 70/30 Split: How Canada’s Health System Is Financed, 2006. https://secure.cihi.ca/free_products/FundRep_EN.pdf. Accessed January 22, 2015.

7. Reformulary Group. http://www.reformulary.com/index_en.php. Accessed January 22, 2015.

8. Canadian Foundation for Healthcare Improvement. INSPIRED Approaches to COPD: Improving Care and Creating Value. http://www.cfhi-fcass.ca/Elearning/spreading-healthcare-innovations-initiative/inspired-approaches-to-copd. Accessed January 22, 2015.

9. The pan-Canadian Pharmaceutical Alliance. http://www.conseildelafederation.ca/en/initiatives/358-pan-canadian-pricing-alliance. Accessed January 22, 2015.

10. Ndegwa S, Quansah K. Subsequent Entry Biologics — Emerging Trends in Regulatory and Health Technology Assessment Frameworks [Environmental Scan, Issue 43, ES0284]. Ottawa: Canadian Agency for Drugs and Technologies in Health; 2014. www.cadth.ca/media/pdf/ES0284_SEBs_es_e.pdf. Accessed January 22, 2015.

11. Guidance for Sponsors: Information and Submission Requirements for Subsequent Entry Biologics (SEBs). Ottawa: Health Canada; 2010.

12. Precision Advisors payer interviews. Conducted October-December 2014.

References

Acknowledgment

The authors wish to acknowledge contributions from the following individuals who assisted in preparing the content for this paper: Larry Arshoff, Stephen Hull, and Matt Reifenberger of Hull Associates LLC; and Robert Kulik of Patient Access Solutions Inc.

2 Bethesda Metro Center, Suite 850

Bethesda, MD 20814

+1 240.654.0730 office

precisionformedicine.com

© 2015. All rights reserved.