Embed Size (px)

Citation preview

Calgary Toronto Moscow Almaty Caracas Rio de Janeiro

MINE PERU: Dual-Listed Companies on the TSX/TSX-V and the BLV (Lima Stock

Exchange)

Presenters: Janne Duncan Patricia Prato CasadoPartner, Macleod Dixon LLP Associate, Macleod Dixon LLP

Tel.: (416) 202-6715 +58 212 276 0059Email: [email protected]@macleoddixon.com

MAY 27, 2010

The Toronto Stock Exchange

2

Overview The Toronto Stock Exchange http:/ / www.tsx.com Toronto Stock Exchange

Exchange I nformation

Established: Constituent Countries:

1852 Canada

Total Market Cap (Equity):

$1.1K

Primary Country: Number of Domestic IPOs ():

TSX, Inc. operates as a senior equities market in Canada.TSX, Inc. was formerly known as Toronto Stock Exchange, Inc. and changed its name to TSX, Inc. in 2002. The company was founded in 1852 and is based in Toronto, Canada. TSX, Inc. operates as a subsidiary of TSX Group, Inc.

Headquarters: P.O. Box 450 3rd Floor 130 King Street W. Toronto, ON M5X 1J2 Phone: 416-947-4670

Listings

Bolsa de Valores de Lima

3

Overview Bolsa de Valores de Lima (Lima Stock Exchange) http:/ / www.bvl.com.pe/ Bolsa de Valores de Lima

Exchange I nformation

Established: Constituent Countries:

1860 Peru

Total Market Cap (Equity):

$41.6

Primary Country: Number of Domestic IPOs ():

Bolsa de Valores de Lima S.A. offers securities trading services in Peru. Founded in 1860, Bolsa de Valores de Lima (BVL) is the stock exchange of Peru, situated in the capital Lima.

Headquarters: Pasaje Acuña 106 Lima 100 Phone: 51 1 619 3333

Listings

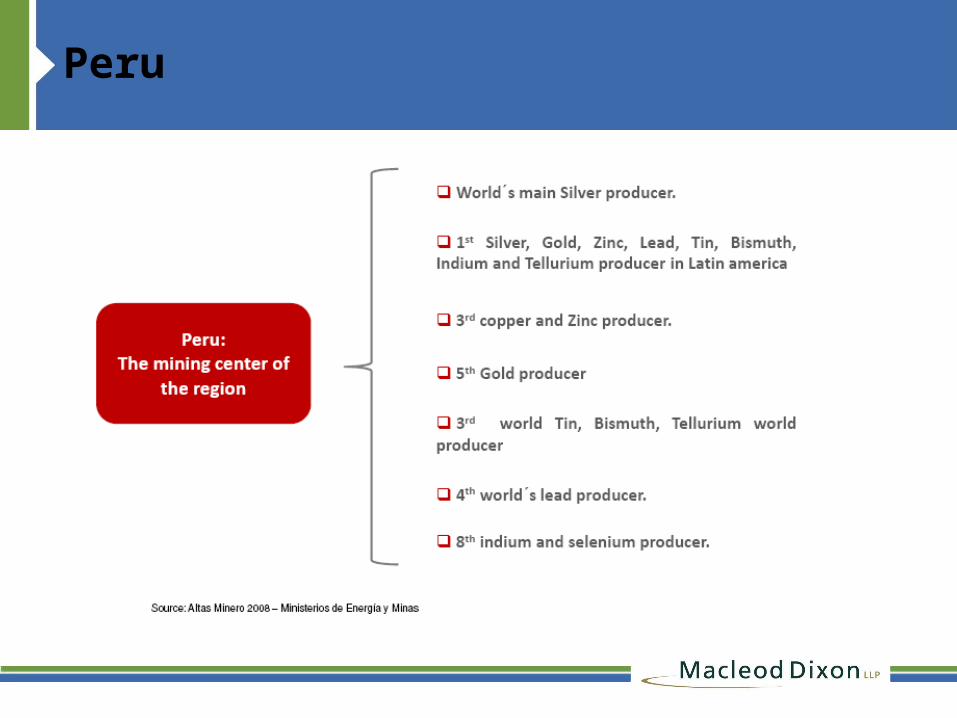

Peru

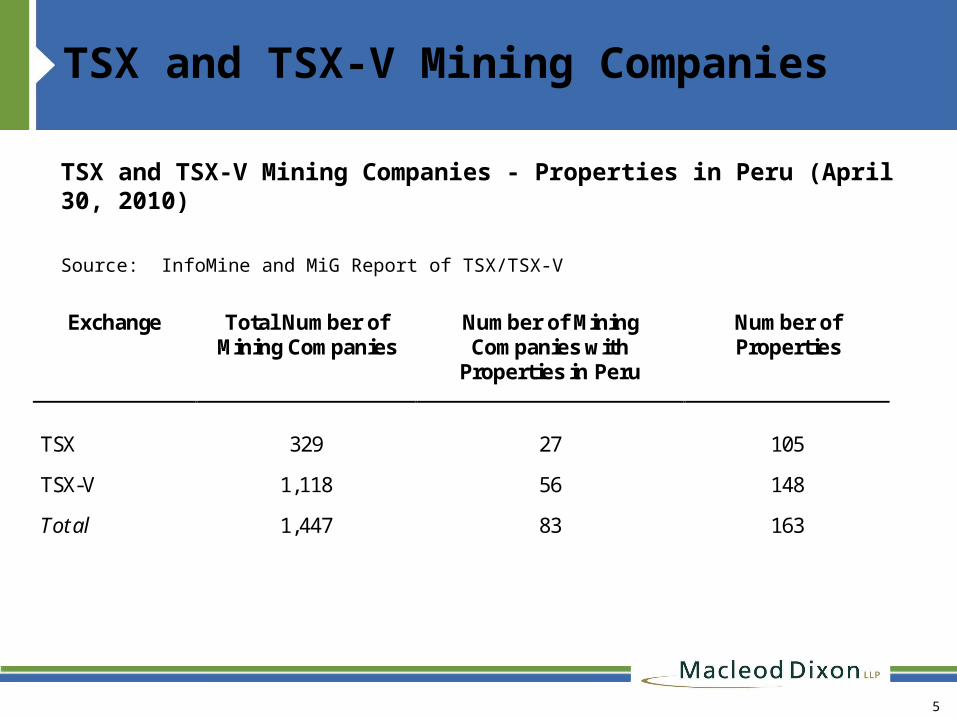

TSX and TSX-V Mining Companies

TSX and TSX-V Mining Companies - Properties in Peru (April 30, 2010)

Source: InfoMine and MiG Report of TSX/TSX-V

5

Exchange Total Number of Mining Companies

Number of Mining Companies with

Properties in Peru

Number of Properties

TSX 329 27 105

TSX-V 1,118 56 148

Total 1,447 83 163

Interlisted Mining Companies – TSX - BVC

6

Company Name Quoted Market Value (April 20, 2010)

Mineral IRL Limited $90M

Candente Copper Corp. $42M

Norsemont Mining Inc. $198M

Vena Resources Inc. $31M

Fortuna Silver Mines Inc. $251M

Interlisted Mining Companies – TSX-V - BVC

7

Company Name Quoted Market Value (April 20, 2010)

Alturas Minerals Corp. $10M

Apoquindo Minerals Inc. $51M

Inca Pacific Resources Inc. $11M

Panoro Minerals Ltd. $26M

Rio Alto Mining Limited $68M

Lima Mining Companies

Lima Mining Companies (April 30, 2010)

There are 256 companies in total listed in the Lima Stock Exchange. 27 of them correspond to regular mining companies, and 8 to junior mining companies.

8

Mining Companies

Mining Companies currently listed: a) Regular Mining Companies:

9

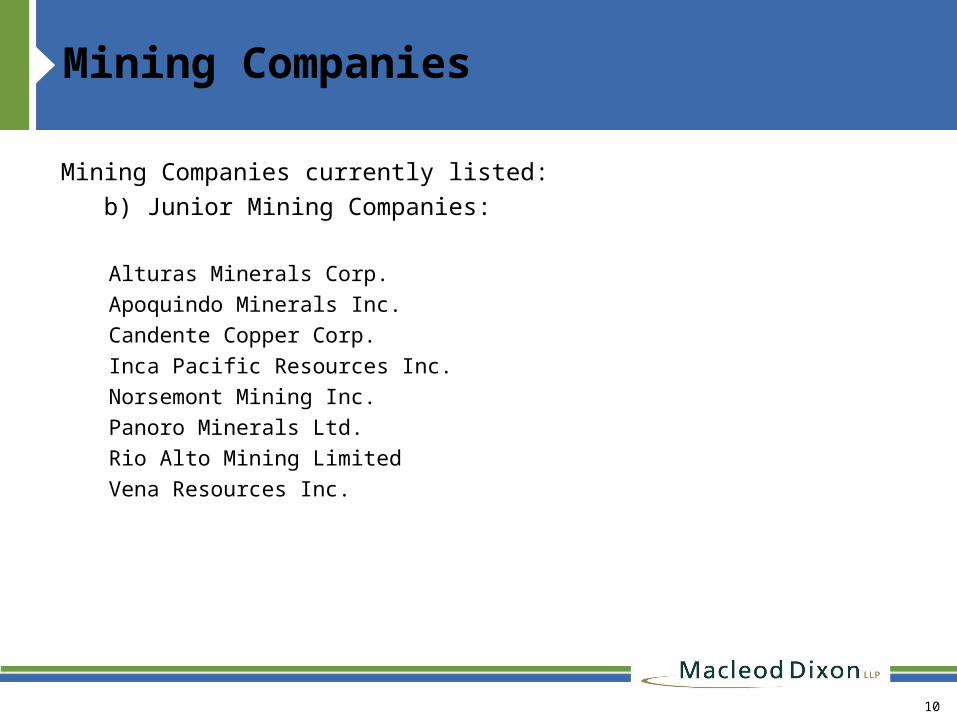

Mining Companies

Mining Companies currently listed: b) Junior Mining Companies:

Alturas Minerals Corp. Apoquindo Minerals Inc. Candente Copper Corp. Inca Pacific Resources Inc. Norsemont Mining Inc. Panoro Minerals Ltd. Rio Alto Mining Limited Vena Resources Inc.

10

11

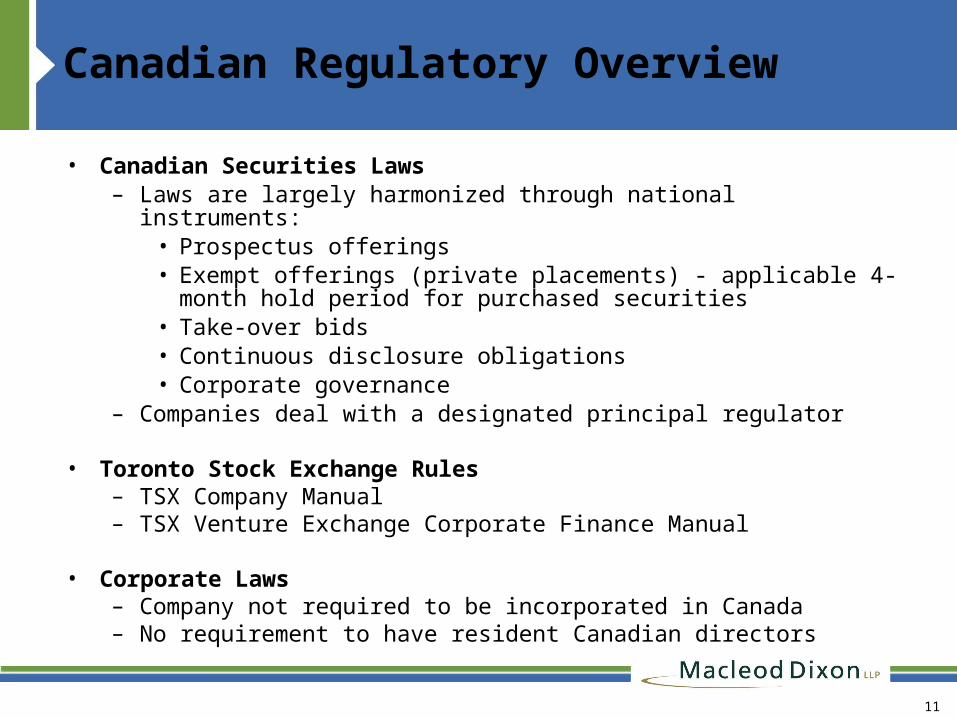

Canadian Regulatory Overview

• Canadian Securities Laws – Laws are largely harmonized through national instruments:

• Prospectus offerings• Exempt offerings (private placements) - applicable 4-

month hold period for purchased securities• Take-over bids• Continuous disclosure obligations• Corporate governance

– Companies deal with a designated principal regulator

• Toronto Stock Exchange Rules – TSX Company Manual– TSX Venture Exchange Corporate Finance Manual

• Corporate Laws – Company not required to be incorporated in Canada– No requirement to have resident Canadian directors

12

Peru Regulatory Overview

• The General Mining Law No.28327 is the main Mining Statute in Peru. There is also the Law of Mining Royalties, No.28258

• There is a Rule regarding the Environmental Protection on Mining Activities, D.S.No. 016-93-EM

Important Links

• Rules on the High Risk Capital of the Lima Stock Exchange Stock:

• http://www.bvl.com.pe/Juniors/ReglamentoMod2005.pdf• Law that regulates the Peruvian Stock Market:

http://www.bvl.com.pe/decreto_legis1.jsp?idioma=E• Rules of Important Acts, Privileged Information and

other Publications:• http://www.bvl.com.pe/reglamento_hechos_imp.html• Companies currently listed in the Lima Stock Exchange• http://www.bvl.com.pe/emp_listado_todas.jsp

Bolsa de Valores de Lima

14

• BVL is the only stock exchange in Peru. Moreover, is the only one in the region which has a mining Venture Exchange

• The BVL is regulated by the Comision Nacional Supervisora de Empresas y Valores – CONASEV.

• The BVL is a public company and its shares are traded on the Peruvian equity market.

• Trading is made by electronic system, which guarantees a transparent and efficient market. IT IS THE ONLY STOCK EXCHANGE LINKED TO CDS, which makes for easy clearing and settlement for dual-listed companies

• SEC recognizes BVL as designated offshore securities market under “S” regulations.

Peru Regulatory Environment

15

• Peru markets itself as having a friendly market environment for business

• There are no taxes or restrictions to short term or long term capital flows in or out of the Country.

• The exchange rate is market driven and there are no taxes or restrictions to buying/selling foreign currency in Peru.

• Canada and Peru have signed 3 agreements effective August 1, 2009:

– Canada-Peru Free Trade Agreement– Labour Coooperation Agreement– Agreement on the Environment

16

Advantages to listing on TSX

• Market sentiment: Certain North American investors may be more attracted to a company with a "local" listing

• Access to capital for growth: BLV does not provide access to the levels of investment capital that are available on TSX

• Heightened company profile: Increased press coverage and analyst's reports, helping to maintain liquidity of shares

• Objective market value: Potential re-rating or revaluation of the company

• Increased liquidity

• New market for shares

Advantages to Listing on the BVL

• Peruvian investors have an appetite for locally-listed companies, particularly large producers

• BVL has streamlined its processes to match the TSX TSX-V more than other international exchanges (AIM, ASE, Johannesburg)

18

Doubling Up: BLV and TSX

• On-going expenses - underwriting, legal (all applicable jurisdictions), audit, registrar and transfer fees, fees to stock exchanges, fees to securities regulators

• Corporate governance more complicated since issuer is listed in multiple jurisdictions

• Continuous disclosure obligations

• Regulatory compliance

• Check to see if there are exemptions under various rules for foreign issuers

19

Practical differences for BLV companies

• Liman companies undertaking TSX listing or capital raising should prepare for a greater volume and complexity of legal documentation

• TSX listings and Canadian capital raisings involve lawyers to far greater degree than in Lima (even for routine placements) as transactions are "lawyer driven"

• Differences in documentation between TSX and BLV listings

• TSX requires that the Board must contain independent directors, and directors with experience in Canadian capital markets

• Increased costs associated with management time, frequent travel to Canada, and additional resources to list as TSX entity

20

Comparison of Continuous Obligations for Maintaining Listing on TSX/TSX-V vs. PSE

Requirement

TSX/TSX-V PSE/CONASEV

Material Change Report File within 10 days of a material change File as soon as the change takes place, at least 1 business day after the change has been agreed upon

Early Warning Reports Shareholder to immediately notify market when shareholdings reach 10% and thereafter every time an additional 2% is acquired

Company must notify within 5 days of the transaction when: (i) when a company’s director or manager, and their family, acquire 1% or more of the stocks issued; and (ii) a person acquires 10% or more of the stock issued

Significant Acquisition Report

Business acquisition report filed within 75 days of acquisition if pass one of three tests for significant acquisition

The person who intends to acquire a significant participation -direct or indirect, through 1 or more acts- must do it through a Public Offer, which would require to notify CONASEV

Communications withShareholders

Management information circular and form of proxy to be filed and delivered to shareholders in connection with shareholder meetings

5% of the shares with right to vote of the total capital stock of the Company can call on shareholders´ meetings. Requirement to published an information circular to call on shareholders´ meetings with at least 25 days prior the celebration date of such meeting

21

Comparison of Continuous Obligations for Maintaining Listing on TSX/TSX-V vs. PSE

Requirement

TSX/TSX-V PSE/CONASEV

Annual Information Form

TSX: File within 90 days of financial year end, accompanied by material contractsTSX-V: Not required; if prepared, file within 120 days of financial year end

As requested by the Peruvian Exchange CommissionIf failed to comply with the information requested, the Commission can perform an inspection in the offices of the Company

CEO & CFO Certification

Concurrently with annual and quarterly filings

CEOs and CFOs required to certify that the financial statements, together with other financial information included in their company’s filings “fairly present” in all material respects the financial condition, results of operations and cash flows of the issuer

Legal Representative and Licensed External Auditor must certify the Financial Statements submitted

Interim Financial Statements

File interim financials and related MD&A on or before earlier of (i) 45 days (60 days for TSX-V) from end of the interim period, and (ii) date of filing in foreign jurisdiction

Audited Financial Statements must be filed quarterly, no later than 1 month of been approved

22

Comparison of Continuous Obligations for Maintaining Listing on TSX/TSX-V vs. PSERequirement TSX/TSX-V PSE/CONASEV

Annual Financials File financial statements and MD&A on or before earlier of (i) 90 days (120 days for TSX-V) from end of financial year (concurrent with AIF for TSX), and (ii) date of filing in foreign jurisdiction

Audited Financial Statements must be filed yearly, no later than 1 month of been approved

Insider Reporting Insiders (directors, officers and 10% shareholders) to file insider report within 10 calendar days of becoming an insider and within 10 calendar days of any subsequent transaction; reporting deadline to be shortened to 5 calendar days as of April 30, 2010

N/A

Insider Trading Prohibition against trading with knowledge of undisclosed material fact or material change; restrictions on trading by persons in “special relationships”

Directors, Managers and Shareholders, and their family, are forbidden to: (i) reveal privileged information to third parties, (ii) Recommend/advise third parties to on transactions they have knowledge of, (iii) Use privileged information on for their own benefit or third parties connected to them

23

Comparison of Continuous Obligations for Maintaining Listing on TSX/TSX-V vs. PSERequireme

ntTSX/TSX-V PSE/CONASEV

Audit Committee TSX requires fully independent audit committee, TSX-V does notAn independent director is a person who: (i) is not a member of management and is free from any interest and any business or other relationship which could reasonably be perceived to materially interfere with the director's ability to act in the best interest of the issuer; and (ii) holds 10% or less of the votes attaching to all issued and outstanding securities of the issuer

External Audit Committees are required and they must perform at least 1 annual audit. The External Auditors must be registered before the Sole Auditory Registry of Companies

Technical Reports Form 43-101F1 technical report required to be filed upon becoming a reporting issuer in Canada; an issuer incorporated or organized in a foreign jurisdiction may file a technical report that utilizes the mineral resource and mineral reserve categories of the JORC Code if a reconciliation to the mineral resource and mineral reserve categories in NI 43-101 is disclosed in the technical report

Obligation to submit a Geological Report of the property where the resources obtained from the issuance would be invested (for High Risk Capital Companies)

24

Comparison of Continuous Obligations for Maintaining Listing on TSX/TSX-V vs. PSERequiremen

tTSX/TSX-V PSE/CONASEV

Share Compensation Plan Disclosure

Annually disclosed and shareholder approval required for plan and/or amendments to plan

Obligation to submit annually the Principles of Good Corporate Governance to be applied

Notice and Approval of New Issuances

For all new issuances of securities; TSX issuers exempt for issuances of unlisted, non-voting, non-participating securities

CONASEV must approve all new issuances of shares and securities

Security Holder Approval

TSX: Required if the transaction materially affects control of the issuer or provides consideration to insiders in aggregate of 10% or more of the market capitalization of the issuer and has not been negotiated at arm's length; TSX will also consider effect transaction may have on the quality of the marketplaceTSX-V: Required in connection with certain specified transactions (e.g. RTOs), including any transaction that results in the creation of a new "control person"; approval also required for various matters related to the approval of or amendments to an issuer's stock option plan

CONASEV must approve any acquisition done with the intention of acquiring a significant participation – direct or indirect, through 1 or more acts

Comparison of Continuous Obligations for Maintaining Listing on TSX/TSX-V vs. PSERequiremen

tTSX/TSX-V PSE/CONASEV

Other Company must have: 1 of the Director and a Management Team with Mining experience

Company must be the owner of the mining property or at least have an option contract granting an exclusive right to explore such property

25

26

Exemptions for Foreign Issuers

• National Instrument 71-102 – Continuous Disclosure and Other Exemptions Relating to Foreign Issuers – An issuer that qualifies as a Designated Foreign Issuer (a "DFI") will receive

relief from certain Canadian disclosure requirements

– If there are de minimus securities owned, directly or indirectly, by Canadian residents (<10%), and the issuer is subject to foreign disclosure requirements in a designated foreign jurisdiction (such as Lima), the issuer will qualify as a DFI

- Exempt from requirement to prepare Canadian forms of: Material Change Reports; financial statements and MD&A; AIFs; Business Acquisition Reports; Management Information Circulars; and Early Warning Reports, provided, among other things, that the issuer (i) complies with its foreign disclosure requirements relating to such documents, and (ii) complies with applicable Canadian filing obligations and shareholder delivery requirements

- DFI status does not relieve issuer from all Canadian securities law obligations (e.g. qualification of auditors, certification of financial statements, obligation to notify of change in corporate structure)

27

Exemptions for Foreign Issuers

• Issuer required to disclose to its shareholders, at least once a year, that it is a DFI subject to the requirements of a foreign regulatory authority

• Determinations on DFI status are made as at the start of each financial year (i.e. the exemption lasts for one year)

• Interlisted issuers with 75% of trading value and volume on an exchange other than the TSX will be exempt from certain requirements concerning securityholder approvals, private placements and security-based compensation arrangements

28

National Instrument 43-101 - Standards of Disclosure for Mineral Projects• Requirement to file technical report triggered by (i) new previously

undisclosed scientific or technical material information about any of the issuer's material properties prior to the filing of a document listed below, or (ii) a material change to information contained in a previously issued technical report is discovered between the filing of a preliminary prospectus and the filing of the final prospectus

• A technical report must be filed at the same time an issuer (i) becomes a reporting issuer, (ii) files a short form or long form prospectus, (iii) files an information circular in relation to the acquisition of a mineral property, (iv) or files an AIF in that includes previously undisclosed scientific or technical material information

• Technical report must also be filed within 45 days following the issuance of a news release that includes previously undisclosed scientific or technical material information which represents a material change

29

National Instrument 43-101 - Standards of Disclosure for Mineral Projects• Scientific and technical data must be prepared by a “qualified

person” (as defined in NI 43-101)

• Technical report must be prepared in format required by NI 43-101 and must use definition standards from the Canadian Institute of Mining & Metallurgy ("CIM") to report quantities and grades of “mineral resources” – inferred; indicated; measured – and “mineral reserves” – probable; proven

• Issuer may make disclosure and file a technical report the utilizes the mineral resource and mineral reserve categories of the JORC Code if such disclosure includes statement that the report was prepared in using the guidelines of the JORC Code, and that the categories used are directly comparable with the classifications of the CIM

• NI 43-101 does not permit inferred mineral resources to be added to other categories of mineral resources

30

Technical Reports – TSX and TSX-V Requirements

TSX Company Manual• Appendix B: Disclosure Standards for Companies Engaged in

Mineral Exploration, Development and Production

TSX Venture Exchange Corporate Finance Manual• Appendix 3F Mining Standards Guidelines• Appendix 3E News Release Guidelines

Peru Mining Companies

• Must submit a list containing the identified mineral substances on the qualified property.

• Must submit a Geological Report of the property where the resources obtained from the issuance would be invested. Such report must contain the recommendations for exploration and development of the project. It also must be elaborated in accordance with the Code of Standards to Inform regarding Mineral Resources and Mine Reserves, approved by the Lima Stock Exchange.

• Must be the owner of the mining property or at least have an option contract granting an exclusive right to explore such property.

43-101 – Standards v. Peruvian Code of Standards

Requirement

TSX/TSX-V PSE/CONASEV

Type of Report Technical Report Geological Report

Preparation of the Report

Technical report must be prepared in format required by NI 43-101 and must use definition standards from the Canadian Institute of Mining & Metallurgy ("CIM")

Geological Report must be prepared in the format required by the Code of Standards to Inform regarding Mineral Resources and Mine Reserves, approved by the Lima Stock Exchange

What must be reported

Quantities and grades of “mineral resources” – inferred; indicated; measured – and “mineral reserves” – probable; proven

List identifying the mineral substances

LIMA Stock Exchange

Mining Companies must submit the following requirements before the Peruvian Ministry of Mines:

• Consolidated Annual Declaration informing the Ministry about the mining activities performed the previous year. This declaration would be used to classify the mining company as Big and Medium Size Mines, Small Size Mines, and Crafted Mines; evaluating its impact on the national economy. If the Company fails to comply with this requirement, a fine valued between 1 and 6 applicable tax unit.

• Monthly Reports of: (i) Production and (ii) Statistics of Accidents must be submitted before the Ministry. Such reports must be submitted 10 days after the month has concluded.

• Declarations of: (i) planned and (ii) executed investments per month. Such declarations must be submitted 10 days after the month has concluded.

• Obligation to pay the annually “derecho de vigencia”, which grants the right to exploit the mine.

33

LIMA Stock Exchange

• Comply with the assigned minimum production. E.g.: a Small Size Mine shall produce: S$50.00 yearly by acre; while a Crafted Mine shall produce US$ 25.00 yearly by acre.

• The General Mining Law No.28327 is the main Mining Statute in Peru. There is also the Law of Mining Royalties, No.28258. There is a Rule regarding the Environmental Protection on Mining Activities, D.S.No. 016-93-EM.

• It is required for mining companies to present/submit environmental assessments or environmental impact statements, but I wasn't able to find how often. I know for sure at the beginning of the project companies must submit one.

34

Macleod Dixon’s Offices

Calgary, TorontoCaracas

Moscow

Macleod Dixon LLP is a global law firm with offices in six key centers of the energy industry: Canada (Calgary and Toronto), Venezuela, Brazil, Russian Federation and Kazakhstan. Nine lawyers from Macleod Dixon have just been ranked as leading practitioners by Who's Who Legal, Mining 2010 - the highest number of any Canadian-based firm. PLC Which Lawyer has also just ranked Macleod Dixon as the #1 Energy firm in Canada and Venezuela for 2010.

Macleod Dixon LLP is a global law firm with offices in six key centers of the energy industry: Canada (Calgary and Toronto), Venezuela, Brazil, Russian Federation and Kazakhstan. Nine lawyers from Macleod Dixon have just been ranked as leading practitioners by Who's Who Legal, Mining 2010 - the highest number of any Canadian-based firm. PLC Which Lawyer has also just ranked Macleod Dixon as the #1 Energy firm in Canada and Venezuela for 2010.

AlmatyRio de Janeiro

35