Embed Size (px)

Citation preview

F i n a n c i a l

S t a t e m e n t s

September2 0 1 1

3

Message from the CEO

The external environment has been evolving amida context of increasing risk perception associatedwith the financial instability that has deepened overthe first nine months of 2011. The delicate fiscalsituation of the Eurozone’s peripheral countries,the debate over raising the debt ceiling in the UnitedStates that ended up with the downgrade of theAmerican rating, the increase in the inflation riskin emerging economies and the uncertaintiesregarding the global economy’s ability to recoverhave also contributed to the worsening of tensionsin international markets.Backed by the stability of the labor market and thecredit evolution, together with a significant in-flowof foreign capital, the strong growth observed inBrazil in the beginning of the year produced apicture of inflationary pressures exacerbated byrising commodity prices, a scenario that wasmanaged through increasing interest rates andfiscal control measures that reduced the economicactivity and reversed the contraction cycle in August2011, in face of the deepening global instabi lity.Given Rio Grande do Sul’s exporting profile, theindustry performance reflected the dynamics of theglobal economy; however, infrastructureinvestments such as roads duplication, the use ofalternative energy sources and the development ofthe technological pole, among others, are signs offavorable prospects for the development of theregional environment, also supported by the goodperformance of the agricultural sector, aided byproductivity gains and appropriate climaticconditions.The high degree of integration among the local,domestic and international economies and thedynamics of the banking sector, extremely linkedto the movements of business cycles, have requiredplanning efforts and constant review of businessesstrategies.After six months of managing Banrisul, manyevents, actions, relevant facts have enabled us tobetter understand the nuances of the business

environment, as well as to improve the diagnosisof a financial institution that celebrated inSeptember its 83rd anniversary.In the last three months, the preparation of the2011-2015 strategic plans can be safely cited as akey process on which we have focused. Variousmeetings addressing all Banrisul’s employees wereheld in July and August, for the purpose ofpromoting a broad discussion about thealternatives that will ensure the growth andsustainability of the Bank’s business.Several are the challenges within the bankingindustry. Changes in the economic environment andin the regulatory framework, such as the recentalignment of the Central Bank of Brazil to Basel III,aiming at preparing the banking system to supportsystemic crises, and changes in the competitiveand technological environments, that ultimatelyrespond for innovation in the financial sector,illustrate our point.And many have being the changes wrought in thesocial environment in recent years. The lifeexpectancy of Brazilians has increased, the habitsare different, and the entry of new classes in theconsumer market demands new approaches tosales and information management related todifferent customer profiles.Hence we have defined, in our planning efforts, theimprovement of customer service as one of themain pillars of the current administration.Banrisul’s other strategic guidelines are groundedin the ( i) expansion of the credit and fundingportfolios, (ii) increase and consolidation of ourmarket share in banking services, (iii ) ongoingimprovements of internal controls and corporaterisk mitigation mechanisms, and ( iv) training,retention and qualification of employees, all basedon sound principles of sustainability andefficiency-focused management.The improvement of customer service covers notonly the branch network, planned to expandespecially to towns lacking financial services, to

4 FINANCIAL STATEMENTSSEPTEMBER 2011

Túlio Luiz ZaminCEO

promote local development in coordinated effortsjointly with the State Government, but also toincrease the quality of services and accessibilityconditions in the different customer channels,including home and office banking, mobile bankingand correspondent banking network.With respect to services provided at branches, inthe last quarter, business hours of local offices in25 municipalities was expanded, the opening of89 new branches in the Southern Region approved,the purchase of equipment for technology upgradeand furniture for standardizing branch layouttriggered, procedures to review and improve thesizing and allocation of human and materialresources at the Head Office initiated, andprocedures for the integration of internalcommunication mechanisms defined.The strengthening and consolidation ofBanricompras network as an acquiring channel tocapture cards other than those of Banrisul’s issueand the back office automation are part of actionsaimed at increasing levels of operating efficiencyand deepening customer loyalty and therelationship with and users of the institution, withinmarket guidelines and the continuous improvementof processes.And finally, to make a difference in service tocustomers, improvements related to processes ofdealing with people must be reached. As much astechnology incorporates agility and comfort tobanking transactions, the delivery of high servicestandards, characterized by warmth, attention,knowledge and efficiency, implies employeequalification and the ability to retain a talented,

skilled workforce aware of developments in theircareer possibilities.By integrating technology, processes and people,we have maintained the consistent trend ofpositive results. Banrisul’s net income of R$678million in the first nine months of was 32.52%higher than that of the same period last year.Net income of R$239 million in 3Q11 was 15.89%higher than 3Q10 and 5.28% higher than that of2Q11.With R$37 billion in assets, of which R$20 billionin loans, Banrisul’s credit portfolio grew 21.05%in the last twelve months. Total funding, includingthird party assets under managed, reached R$28billion in September 2011, an increase of 14.15%over the same month last year. Shareholders’ equitytotaled R$4 billion at the end of September, withan ROAE of 22.76%.Banrisul recently figured in the third position inrelation to customer satisfaction level in theranking of standard banks, and was highly notedin the item of banking safety as perceived bycustomers. Recently, the Bank was included in TheBest Companies list published by IstoÉ Dinheiro,with special emphasis on indicators of financialsustainabi lity, social responsibi lity andenvironmental and human resources. Banrisul hasbeen repeatedly highlighted by the value of itsbrand, the reputation achieved in the local marketand the return of its shares in the stock exchange.And all this has been achieved obtained frompeople’s work. One has no reason to doubt that wecan be one of the best financial institutions inBrazil when it comes to tending customers.

5

IndexMessage from the CEO........................................................................................... 3

Press Release ............................................................................................................. 11Management Report .................................................................................................. 19

Economic Scenario ................................................................................................. 21Consolidated Performance .................................................................................... 23

Net Income ............................................................................................................. 23Shareholders' Equity .............................................................................................. 23Total Assets............................................................................................................. 24Taxes and Contributions ........................................................................................ 24

Operational Performance ...................................................................................... 25Funds Raised and Under Management .................................................................. 25Securities ................................................................................................................ 25

Loan Operations .................................................................................................... 27Products, Services and Channels ............................................................................ 30

Banricompras.......................................................................................................... 30Banrisul's Correspondent Banks ............................................................................ 30Virtual Branch - Home and Office Banking ........................................................... 31Banrifone and Branch Call Center ......................................................................... 31Credit Cards ............................................................................................................ 31Insurances, Private Pension and Capitalization.................................................... 32Eletronic Bidding.................................................................................................... 32

Public Sector Activities .......................................................................................... 32Banrisul's Customer Service Network .................................................................... 33Subsidiaries ........................................................................................................... 34Corporate Governance........................................................................................... 35

Overview ................................................................................................................ 35Shareholding Structure .......................................................................................... 35Investor Relations and Communication Policy ..................................................... 36Interest on Equity and Dividends Payout Policy................................................... 37

Internal Controls and Compliance .......................................................................... 38Risk Management .................................................................................................. 38Basel Ratio .............................................................................................................. 41

Technological Modernization ................................................................................. 42Marketing .............................................................................................................. 43Human Resources .................................................................................................. 44Corporate Responsibility ....................................................................................... 44

Awards.................................................................................................................... 45 Acknowledgements................................................................................................. 48

6 FINANCIAL STATEMENTSSEPTEMBER 2011

Index of GraphsGraph 1: Net Income ................................................................................................... 23Graph 2: Shareholders' Equity Growth ....................................................................... 23Graph 3: Total Assets Growth...................................................................................... 24Graph 4: Growth of Funds Raised and Under Management ....................................... 25Graph 5: Securities Growth ......................................................................................... 26Graph 6: Loan Operations Growth .............................................................................. 27Graph 7: Commercial Credit Growth - Individuals and Companies........................... 28Graph 8: Banricompras ................................................................................................ 30Graph 9: Shareholding Structure ................................................................................ 36Graph 10: Market Value X Shareholders' Equity......................................................... 36Graph 11: Pay Out - Quartely Payments - R$ Million ................................................. 37

Financial Statements .................................................................................................. 49Balance Sheet ........................................................................................................ 51Statement of Income ............................................................................................. 55Cash Flow............................................................................................................... 56Statement of Value Added..................................................................................... 57Statement of Changes on Shareholders' Equity ..................................................... 58Contents of the Notes to Financial Statements ..................................................... 59

Note 01 - Operations.............................................................................................. 61Note 02 - Presentation of the Financial Statements ............................................ 61Note 03 - Significant Accounting Practices............................................................ 62Note 04 - Interbank Investments........................................................................... 66Note 05 - Securities and Derivatives ..................................................................... 66Note 06 - Restricted Deposits ................................................................................ 68Note 07 - Loans, Lease Operations and Other Credit-like Receivables ............... 69Note 08 - Other Receivables.................................................................................. 71Note 09 - Permanent Assets .................................................................................. 72Note 10 - Deposits and Money Market Funding ................................................... 73Note 11 - Borrowings ............................................................................................. 73Note 12- Onlendings ............................................................................................. 74Note 13 - Other Payables....................................................................................... 74Note 14 - Reserves, Contingent Assets and Liabilities ........................................ 75Note 15 - Income from Services Rendered ........................................................... 76Note 16 - Income from Bank Fees ......................................................................... 77Note 17 - Other Administrative Expenses ............................................................ 77Note 18 - Other Operating Income ....................................................................... 77Note 19 - Other Operating Expenses..................................................................... 78Note 20 - Shareholders' Equity - Banrisul ............................................................. 78Note 21 - Commitments, Guarantees and Other .................................................. 79Note 22 - Income and Social Contribution Taxes .................................................. 80Note 23 - Fundação Banrisul de Seguridade Social and Cabergs - Caixa de

Assistência dos Empregados do Banco do Estado do Rio Grande do Sul ......... 82Note 24 - Financial Instruments and Financial Risks Management...................... 83Note 25 - Transactions With Related Parties ........................................................ 87

7

Note 26 - Impact from the Adoption of the InternacionalFinancial Reporting Standards (IFRS) ................................................................ 92

Note 27 - Authorization for Completion of the Financial Statements ................. 92Report ...................................................................................................................... 93Analysis of Performance ............................................................................................. 97

Banco do Estado do Rio Grande do Sul S.A. ............................................................ 99Banking Industry and Competitive Environment.................................................... 100Economic and Financial Indicators.......................................................................... 101

Assets and Earnings Structure ................................................................................. 102Financial Performance ........................................................................................... 102Capital Expenditure Policy .................................................................................... 103Margin Analysis ...................................................................................................... 104Variations in Interest Income and Expenses: Volumes and Rates ....................... 106

Banrisul's Stock Market Performance .................................................................... 107Evolution of Balance Sheet Accounts ..................................................................... 110

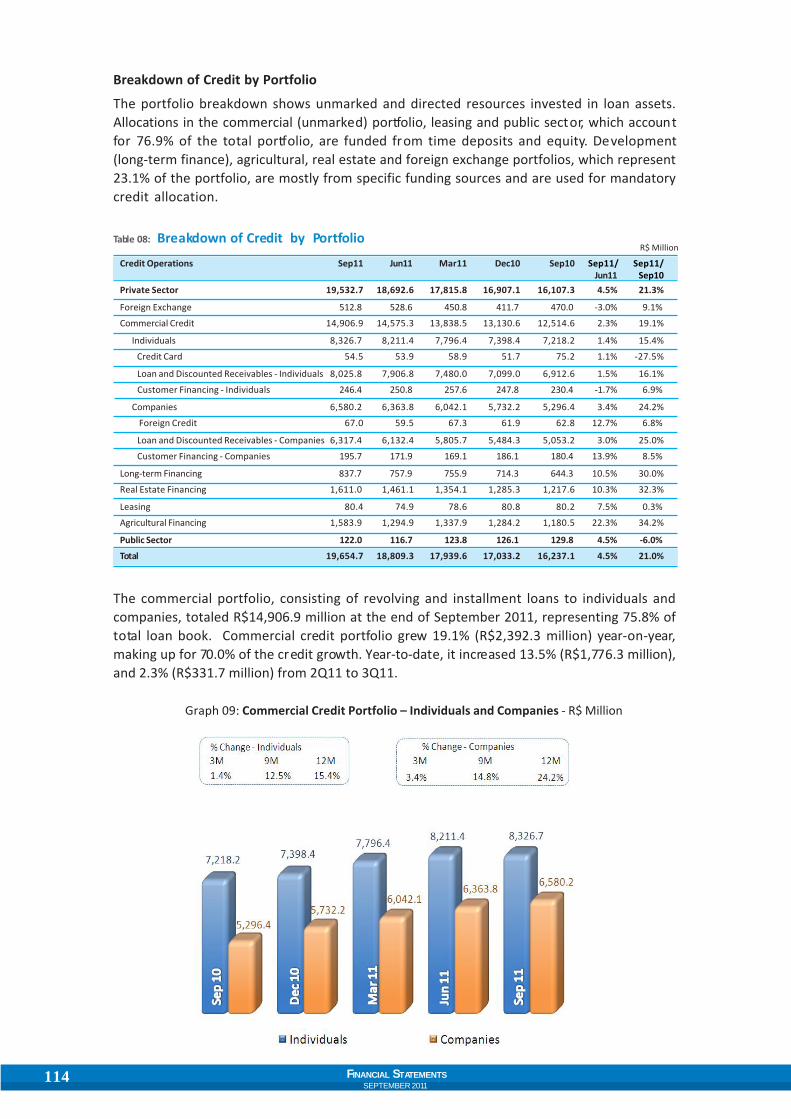

Total Assets ....................................................................................................... 110Securities ................................................................................................................ 111Interbank and Interbranch Transactions ............................................................... 112Credit Operation ............................................................................................... 112Breakdown of Credit by Company Size ................................................................. 113Breakdown of Credit by Sector .............................................................................. 113Breakdown of Credit by Portfolio ......................................................................... 114Breakdown of Credit Disbursement...................................................................... 115Commercial Credit ............................................................................................ 116Breakdown of Credit by Rating .............................................................................. 117Allowance for Loan Losses..................................................................................... 118Cover Ratio ............................................................................................................. 119Default Ratio .......................................................................................................... 119Funds Raised and Under Management .............................................................. 120Demand Deposits ................................................................................................... 120Savings Accounts.................................................................................................... 120Time Deposits ........................................................................................................ 121Assets under Management.................................................................................... 121Cost of Funding ...................................................................................................... 121Shareholders' Equity ......................................................................................... 122Return on Average Shareholders' Equity .............................................................. 123Basel Ratio .............................................................................................................. 123Pace of Growth ....................................................................................................... 124

Evolution of Income Statement Accounts .............................................................. 125Net Income ............................................................................................................. 125Financial Income .................................................................................................... 125Revenue from Treasury Operations ...................................................................... 126Revenues from Credit and Leasing Operations .................................................... 126Revenues from Commercial Credit - Individuals and Companies ....................... 127Financial Expenses ................................................................................................. 129

8 FINANCIAL STATEMENTSSEPTEMBER 2011

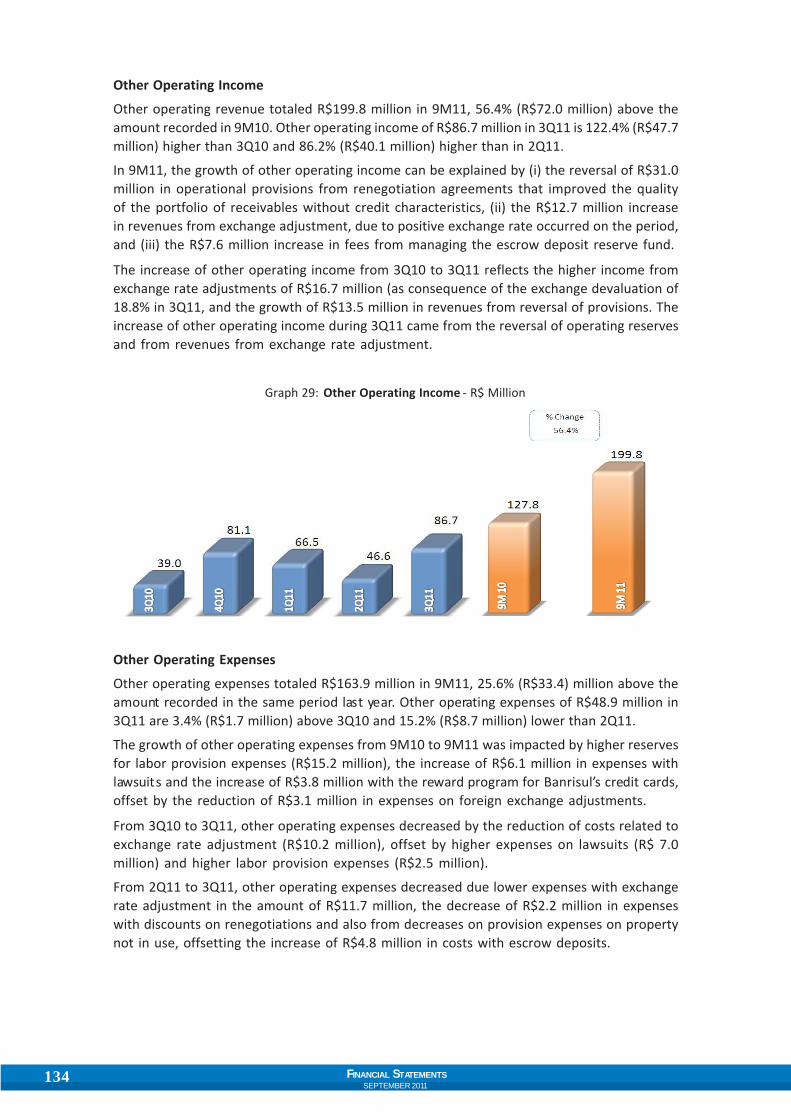

Expenses with Market Funding Operations .......................................................... 130Expenses with Borrowings and Onlendings ......................................................... 131Allowance for Loan Losses..................................................................................... 131Financial Margin..................................................................................................... 132Revenue from Services Rendered ......................................................................... 132Administrative Expenses....................................................................................... 133Other Operating Income ........................................................................................ 134Other Operating Expenses .................................................................................... 134

Economic Indicators ............................................................................................... 136Leverage Ratio ....................................................................................................... 136Operating Cost ....................................................................................................... 136Debt-Equity Ratio................................................................................................... 136Employee Productivity .......................................................................................... 137Efficiency Ratio ...................................................................................................... 137

Consolidated Pro Forma Balance Sheet ................................................................. 138Pro Forma Income Statement ................................................................................ 139

Index of GraphsGraph 01: Banrisul PNB Performance vs. Brazilian Stock Market Indexes ................ 107Graph 02: Average Financial Volume, Number of Trades and Number of Shares .... 108Graph 03: Banrisul´s Shares - Geographic Distribution .............................................. 108Graph 04: Total Assets ................................................................................................. 110Graph 05: Composition of Assets................................................................................ 111Graph 06: Securities and Liquid Interbank Transaction.............................................. 111Graph 07: Interbank and Interbranch Transactions .................................................... 112Graph 08: Credit Operations ....................................................................................... 112Graph 09: Commercial Credit Portfolio - Individuals and Companies ...................... 114Graph 10: Credit Portfolio by Risk Levels ................................................................... 117Graph 11: Breakdown of Allowance for Loan Losses ................................................. 118Graph 12: Cover Ratio.................................................................................................. 119Graph 13: Default Ratio ............................................................................................... 119Graph 14: Funds Raised and Under Management ...................................................... 120Graph 15: Cost of Funding as % of Selic Rate ............................................................. 122Graph 16: Shareholders' Equity................................................................................... 122Graph 17: Return on Average Shareholders' Equity................................................... 123Graph 18: Basel Ratio .................................................................................................. 124Graph 19: Pace of Growth - Credit and Funding......................................................... 124Graph 20: Net Income ................................................................................................. 125Graph 21: Financial Income......................................................................................... 126Graph 22: Revenues from Credit and Leasing Operations......................................... 127Graph 23: Financial Expenses ..................................................................................... 130Graph 24: Expenses with Market Funding Operations .............................................. 130Graph 25: Allowance for Loan Losses ......................................................................... 131Graph 26: Financial Margin ......................................................................................... 132

9

Graph 27: Revenue from Services Rendered ............................................................. 133Graph 28: Personnel and Other Administrative Expenses ........................................ 133Graph 29: Other Operating Income ............................................................................ 134Graph 30: Other Operating Expenses ......................................................................... 135Graph 31: Leverage Ratio ............................................................................................ 136Graph 32: Operating Cost ............................................................................................ 136Graph 33: Debt-Equity Ratio ....................................................................................... 136Graph 34: Employee Productivity ............................................................................... 137Graph 35: Efficiency Ratio ........................................................................................... 137

Index of TablesTable 01: Competitive Environment ........................................................................... 100Table 02: Economic and Financial Indicators .............................................................. 101Table 03: Margin Analysis ............................................................................................ 104Table 04: Variations in Interest Income and Expenses: Volumes and Rate .............. 106Table 05: Communication and Relationship Efforts................................................... 107Table 06: Breakdown of Credit to Companies by Company Size ............................... 113Table 07: Breakdown of Credit by Sector ................................................................... 113Table 08: Breakdown of Credit by Portfolio ............................................................... 114Table 09: Breakdown of Credit Disbursement ........................................................... 116Table 10: Composition of General Credit - Individuals and Companies ................... 117Table 11: Balance of Allowance for Losses ................................................................. 118Table 12: Funding Composition .................................................................................. 121Table 13: Cost of Funding ............................................................................................ 122Table 14: Revenues from Commercial Credit - Individuals and Companies ............. 128Table 15: Monthly Average Commercial Credit Rates - Individuals

and Companies ............................................................................................. 129Table 16: Consolidated Pro Forma Balance Sheet ...................................................... 138Table 17: Pro Forma Income Statement ..................................................................... 139

10 FINANCIAL STATEMENTSSEPTEMBER 2011

11

PressRelease

12 FINANCIAL STATEMENTSSEPTEMBER 2011

13

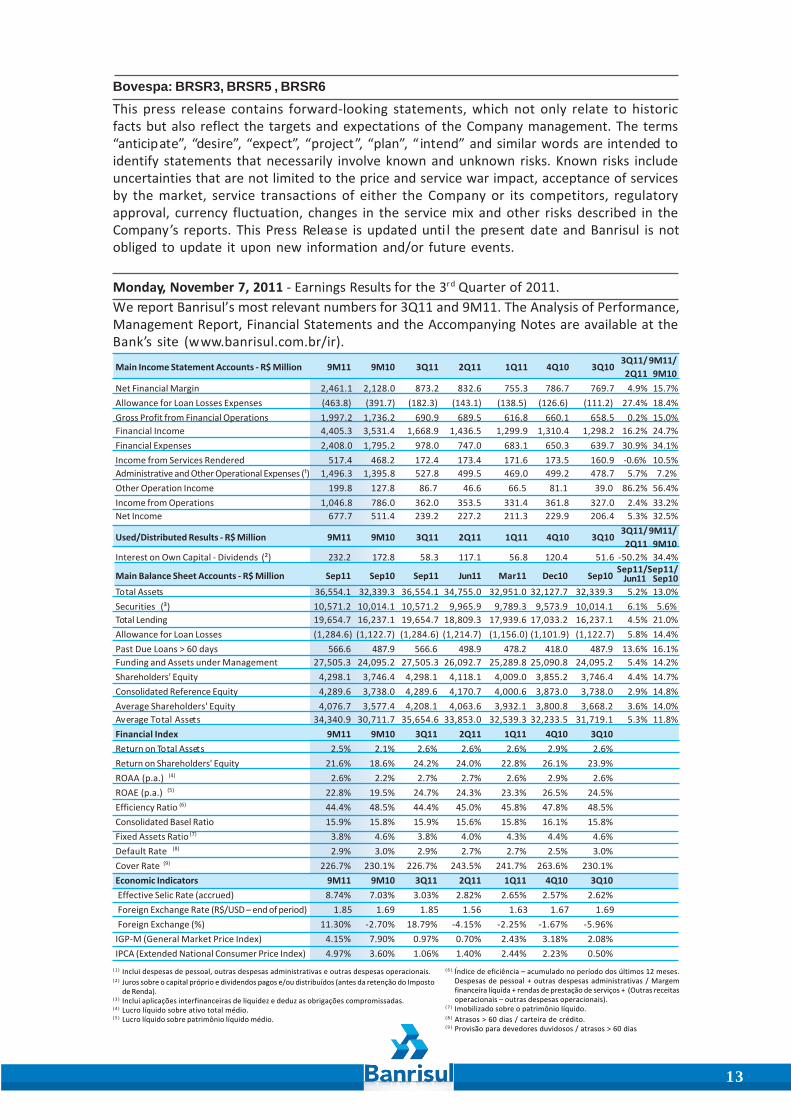

Monday, November 7, 2011 - Earnings Results for the 3r d Quarter of 2011.We report Banrisul’s most relevant numbers for 3Q11 and 9M11. The Analysis of Performance,Management Report, Financial Statements and the Accompanying Notes are available at theBank’s site (www.banrisul.com.br/ir).

Bovespa: BRSR3, BRSR5 , BRSR6This press release contains forward-looking statements, which not only relate to historicfacts but also reflect the targets and expectations of the Company management. The terms“anticipate”, “desire”, “expect”, “project”, “plan”, “ intend” and similar words are intended toidentify statements that necessarily involve known and unknown risks. Known risks includeuncertainties that are not limited to the price and service war impact, acceptance of servicesby the market, service transactions of either the Company or its competitors, regulatoryapproval, currency fluctuation, changes in the service mix and other risks described in theCompany’s reports. This Press Release is updated unti l the present date and Banrisul is notobliged to update it upon new information and/or future events.

( 1 ) Inclui despesas de pessoal, outras despesas administrativas e outras despesas operacionais.( 2 ) Juros sobre o capital próprio e dividendos pagos e/ou distribuídos (antes da retenção do Imposto

de Renda).( 3 ) Inclui aplicações interfinanceiras de liquidez e deduz as obrigações compromissadas.( 4 ) Lucro líquido sobre ativo total médio.( 5 ) Lucro líquido sobre patrimônio líquido médio.

( 6 ) Índice de eficiência – acumulado no período dos últimos 12 meses.Despesas de pessoal + outras despesas administrativas / Margemfinanceira líquida + rendas de prestação de serviços + (Outras receitasoperacionais – outras despesas operacionais).

( 7 ) Imobilizado sobre o patrimônio líquido.( 8 ) Atrasos > 60 dias / carteira de crédito.( 9 ) Provisão para devedores duvidosos / atrasos > 60 dias

Main Income Statement Accounts - R$ Million 9M11 9M10 3Q11 2Q11 1Q11 4Q10 3Q103Q11/ 9M11/2Q11 9M10

Net Financial Margin 2,461.1 2,128.0 873.2 832.6 755.3 786.7 769.7 4.9% 15.7%Allowance for Loan Losses Expenses (463.8) (391.7) (182.3) (143.1) (138.5) (126.6) (111.2) 27.4% 18.4%Gross Profit from Financial Operations 1,997.2 1,736.2 690.9 689.5 616.8 660.1 658.5 0.2% 15.0%Financial Income 4,405.3 3,531.4 1,668.9 1,436.5 1,299.9 1,310.4 1,298.2 16.2% 24.7%Financial Expenses 2,408.0 1,795.2 978.0 747.0 683.1 650.3 639.7 30.9% 34.1%Income from Services Rendered 517.4 468.2 172.4 173.4 171.6 173.5 160.9 -0.6% 10.5%Administrative and Other Operational Expenses (¹) 1,496.3 1,395.8 527.8 499.5 469.0 499.2 478.7 5.7% 7.2%Other Operation Income 199.8 127.8 86.7 46.6 66.5 81.1 39.0 86.2% 56.4%Income from Operations 1,046.8 786.0 362.0 353.5 331.4 361.8 327.0 2.4% 33.2%Net Income 677.7 511.4 239.2 227.2 211.3 229.9 206.4 5.3% 32.5%

Used/Distributed Results - R$ Million 9M11 9M10 3Q11 2Q11 1Q11 4Q10 3Q103Q11/ 9M11/2Q11 9M10

Interest on Own Capital - Dividends (²) 232.2 172.8 58.3 117.1 56.8 120.4 51.6 -50.2% 34.4%

Main Balance Sheet Accounts - R$ Million Sep11 Sep10 Sep11 Jun11 Mar11 Dec10 Sep10Sep11/Sep11/

Jun11 Sep10Total Assets 36,554.1 32,339.3 36,554.1 34,755.0 32,951.0 32,127.7 32,339.3 5.2% 13.0%Securities (³) 10,571.2 10,014.1 10,571.2 9,965.9 9,789.3 9,573.9 10,014.1 6.1% 5.6%Total Lending 19,654.7 16,237.1 19,654.7 18,809.3 17,939.6 17,033.2 16,237.1 4.5% 21.0%Allowance for Loan Losses (1,284.6) (1,122.7) (1,284.6) (1,214.7) (1,156.0) (1,101.9) (1,122.7) 5.8% 14.4%Past Due Loans > 60 days 566.6 487.9 566.6 498.9 478.2 418.0 487.9 13.6% 16.1%Funding and Assets under Management 27,505.3 24,095.2 27,505.3 26,092.7 25,289.8 25,090.8 24,095.2 5.4% 14.2%Shareholders' Equity 4,298.1 3,746.4 4,298.1 4,118.1 4,009.0 3,855.2 3,746.4 4.4% 14.7%Consolidated Reference Equity 4,289.6 3,738.0 4,289.6 4,170.7 4,000.6 3,873.0 3,738.0 2.9% 14.8%Average Shareholders' Equity 4,076.7 3,577.4 4,208.1 4,063.6 3,932.1 3,800.8 3,668.2 3.6% 14.0%Average Total Assets 34,340.9 30,711.7 35,654.6 33,853.0 32,539.3 32,233.5 31,719.1 5.3% 11.8%Financial Index 9M11 9M10 3Q11 2Q11 1Q11 4Q10 3Q10Return on Total Assets 2.5% 2.1% 2.6% 2.6% 2.6% 2.9% 2.6%Return on Shareholders' Equity 21.6% 18.6% 24.2% 24.0% 22.8% 26.1% 23.9%ROAA (p.a.) (4) 2.6% 2.2% 2.7% 2.7% 2.6% 2.9% 2.6%ROAE (p.a.) (5) 22.8% 19.5% 24.7% 24.3% 23.3% 26.5% 24.5%Efficiency Ratio (6) 44.4% 48.5% 44.4% 45.0% 45.8% 47.8% 48.5%Consolidated Basel Ratio 15.9% 15.8% 15.9% 15.6% 15.8% 16.1% 15.8%Fixed Assets Ratio (7) 3.8% 4.6% 3.8% 4.0% 4.3% 4.4% 4.6%Default Rate (8) 2.9% 3.0% 2.9% 2.7% 2.7% 2.5% 3.0%Cover Rate (9) 226.7% 230.1% 226.7% 243.5% 241.7% 263.6% 230.1%Economic Indicators 9M11 9M10 3Q11 2Q11 1Q11 4Q10 3Q10 Effective Selic Rate (accrued) 8.74% 7.03% 3.03% 2.82% 2.65% 2.57% 2.62% Foreign Exchange Rate (R$/USD – end of period) 1.85 1.69 1.85 1.56 1.63 1.67 1.69 Foreign Exchange (%) 11.30% -2.70% 18.79% -4.15% -2.25% -1.67% -5.96%IGP-M (General Market Price Index) 4.15% 7.90% 0.97% 0.70% 2.43% 3.18% 2.08%IPCA (Extended National Consumer Price Index) 4.97% 3.60% 1.06% 1.40% 2.44% 2.23% 0.50%

14 FINANCIAL STATEMENTSSEPTEMBER 2011

Operational Highlights

In 9M11, Banrisul presented ascendant creditrates. Default indicators and credit qualityremained stable, in spite of the riskierenvironment due to the effects of macro-prudential measures issued in December2010 and high interest rates, reverted at theend of 3Q11 due to the foreign economiesenvironment instability. The increase ofcredit, treasury and foreign Exchangerevenues contributed to the growth of thenet interest income.Six months after the Management change,Banrisul has maintained its market-orientedbusiness strategies focused on returns to

public and private shareholders.A mature organization, and by adopting thebest practices of corporate governance,Banrisul ensures that reshuffles in theBoard of Administration and its ExecutiveBody, a natural process within a state-controlled bank, reinforces the continuityof business management and operationalprocesses.The focus on efficiency is also compatiblewith maintaining, by the third consecutivequarter, the Company’s guidance released,despite the changing circumstances of theeconomy.

Financial Performance

Net income registered in 9M11 was R$677.7million, 32.5% or R$166.3 million above thenet income reached in the same period of2010. In 3Q11, net income was R$239.2million, 15.9% or R$32.8 million higher thanin 3Q10.

From 3Q10 to 3Q11, the Bank’s performancepositively reflects the increase of 23.3% orR$217.5 mill ion in credit revenues, ofR$44.3 million in treasury income andservices fees and of R$95.2 mill ion inforeign exchange revenues, howeveroffset by growing financial, market fundingand onlendings expenses.

From 2Q10 to 3Q11, the performancepositively was impacted by the increaseof 8 .9% (R$94.0 mi l l ion) in cred i trevenues and the increase of 6 .4%(R$20.2 mill ion) in treasury revenues,negatively offset by higher f inancial ,market funding and onlending expenses

and administrative costs.

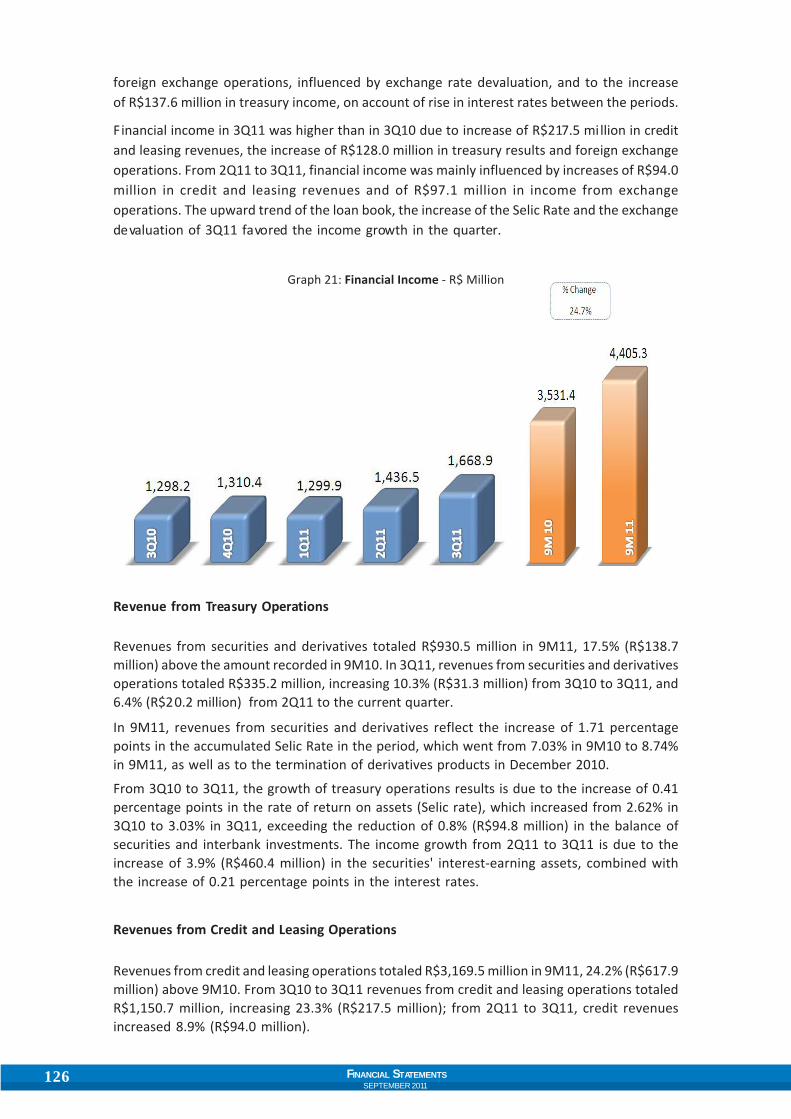

The net interest margin totaled R$2,461.1million at the end of 9M11, a 15.7% (R$333.1million) increase over that of 9M10. NIMwas positively affected by the growth ofrevenues from credit, treasury, restricteddeposits and foreign exchange, whilenegatively impacted by increasingfinancial, market funding and onlendingexpenses.

3Q11’s NIM of R$873.2 million is 13.4%(R$103.5 million) above 3Q10’s, on accountof higher income from credit, treasury andforeign exchange that offset increasesrecorded on financial and market fundingexpenses.

NIM increase in from 2Q11 to 3Q11 isexplained by higher credit and treasury andforeign exchange income in comparison toincreases seen on financial expenses.

15

Evolution of Assets

Total assets at the end of September 2011were R$36,554.1 million, 13.0% (R$4,214.8million) higher than in September 2010. Incomparison to December 2010, assetsincreased 13.8% (R$4,426.4 million), whileexpanding 5.2% (R$1,799.1 million) from2Q11 to 3Q11.

The year-on-year asset growth of R$2,956.0million comes from the expansion of thefunding portfolio and the increase of R$616.2million in escrow deposits. In the last twelvemonths, the growth of credit (in R$3,417.6million) and interbank transactions (inR$812.9 million) were the main drivers ofasset allocation.

Banrisul‘s credit portfolio totaled R$19,654.7million in September 2011, exceeding by21.0% the balance as of September 2010, by15.4% the amount as of December 2010 andby 4.5% the balance as of June 2011.

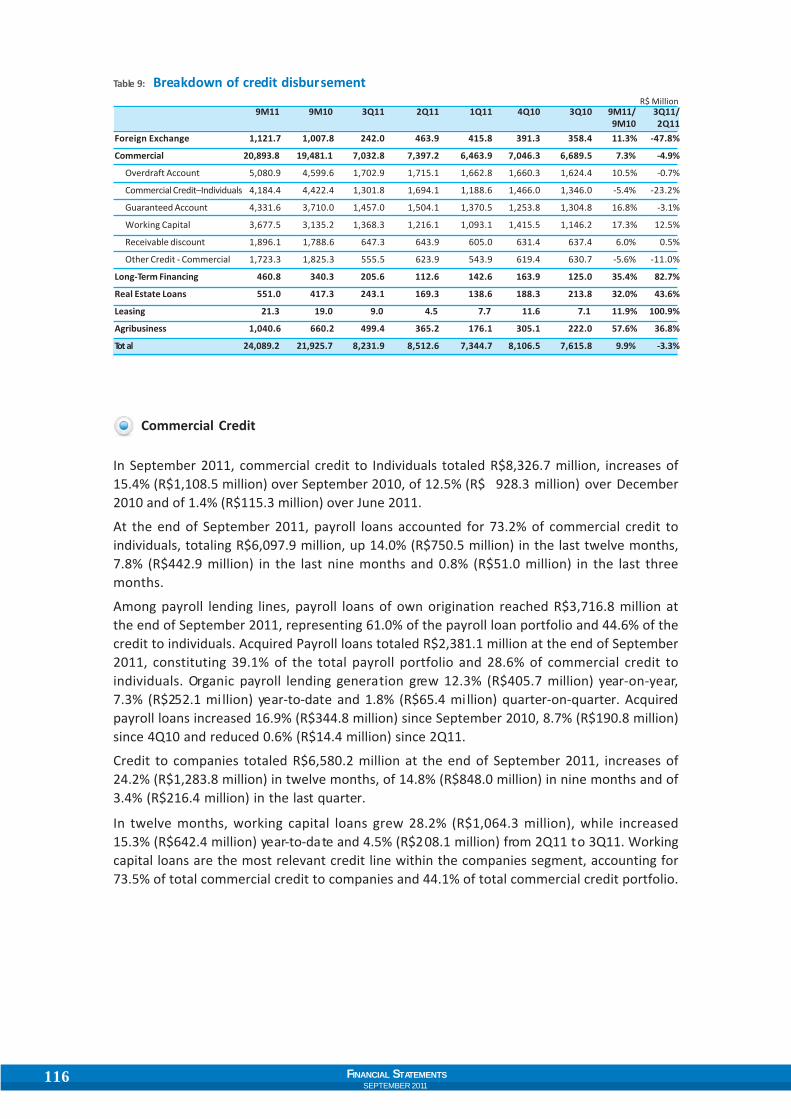

In September 2011, commercial credit toIndividuals totaled R$8,326.7 mill ion,15.4% (R$1,108.5 million) over September2010, increasing 12.5% (R$928.3 million)

over December 2010 and 1.4% (R$115.3mill ion) from 2Q10. Payroll loansconsolidated as important tool in theexpansion of operations in the last twelvemonths. Credit to companies totaledR$6,580.2 million at the end of September2011, increasing 24.2% (R$1,283.8 million)in twelve months, 14.8% (R$848.0 million)year-to-date and 3.4% (R$216.4 million)from 2Q10 to 3Q10.

Non-performing loans over 60 days, 2.9% ofthe loan book, reduced 10 basis points fromSeptember 2010 to 2.9% of total loans inSeptember 2011. NPL over 90 days was 2.4%in September 2011, below market ratios.Total provisions remain at a level sufficientto cover loans in arrears.

Securities totaled R$10,571.2 million at theend of September 2011, amount 5.6%(R$557.1 million) above that of 3Q10. Year-to-date, securities increased 10.4% (R$997.2million) and rose 6.1% (R$605.2 million) from2Q11 to 3Q11. This amount includes liquidinterbank transactions but excludes total

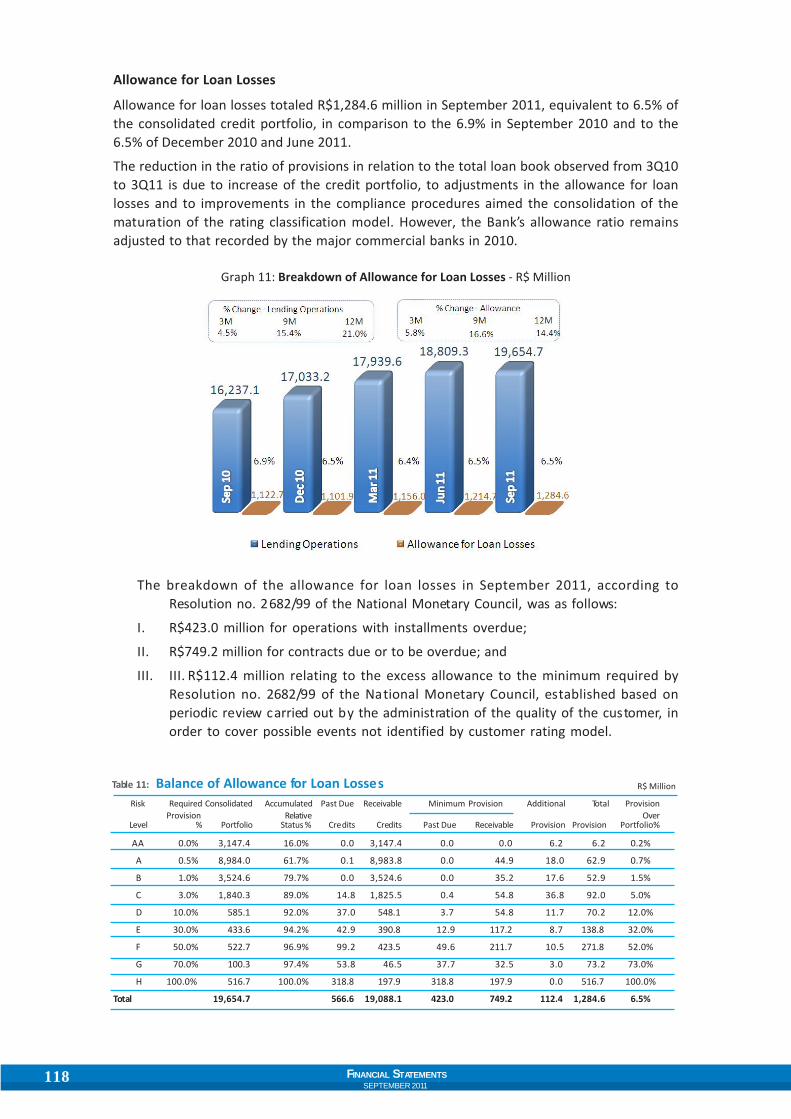

At the end of 3Q11, expenses with loan lossesallowance totaled R$463.8 million, 18.4%(R$72.1 million) higher than that recordedon 9M10, reflecting the growth of the loanportfolio and also of loans past due over 60

days. From 2Q11 to 3Q11, provision expensestotaled R$182.3 million, increasing 63.9%(R$71.1 million) in twelve months and 27.4%(R$39.2 million) quarter-on-quarter.

9M11 9M10 3Q11 2Q11 1Q11 4Q10 3Q10

Financial Margin 2,461.1 2,128.0 873.2 832.6 755.3 786.7 769.7

Gross Profit from Financial Operations 1,997.2 1,736.2 690.9 689.5 616.8 660.1 658.5

Average Profitable Assets (1) 31,178.4 28,433.1 32,140.6 31,475.5 29,919.1 29,563.8 29,291.2

Net Financial Margin(2) 10.7% 10.1% 11.3% 11.0% 10.5% 11.1% 10.9%

Gross Profit from Financial Operations(3) 8.6% 8.2% 8.9% 9.1% 8.5% 9.2% 9.3%(1) Average Interest-Earning Assets of the Period(2) Net Financial Margin / Average Profitable Assets (Annualized)(3) Gross Profit from Financial Operations / Average Profitable Assets (Annualized)

Financial Margin R$ Million

16 FINANCIAL STATEMENTSSEPTEMBER 2011

The efficiency ratio reached 44.4% in the pasttwelve months ended in September 2011.The consistent reduction in efficiency ratioreflects the capacity of the financial margin,sustained by the growth in revenue fromcredit, treasury and favored by reduction offinancial expenses, to absorb the increase inadministrative and operating expenses.

Operating cost indicator ended September2011 at 4.9% for the past twelve months.Asset expansion, leveraged by the growthin credit operations helped to absorb theincrease of administrative expenses,reflecting in the reduction of costs inproportion to the assets in twelve months.

Sep/11 Jun/11 Mar/11 Dec/10 Sep/10

Total Assets 36,554.1 34,755.0 32,951.0 32,127.7 32,339.3

Tot al Credit O perations 19,654.7 18,809.3 17,939.6 17,033.2 16,237.1

Securities (1) 10,571.2 9,965.9 9,789.3 9,573.9 10,014.1

Funds raised and under management 27,505.3 26,092.7 25,289.8 25,090.8 24,095.2

Shareholders' Equity 4,298.1 4,118.1 4,009.0 3,855.2 3,746.4(1) Securities + In terbank Investiments - Matched Transactions

Highlights R$ Million

liabilities from matched transactions. Thelower securities balance year-on-yearreflects the Bank’s policy of migrating tohigher yield assets.

Funds raised and under management totaledR$27,505.3 million in September 2011,growing 14.2% (R$3,410.2 million) overSeptember 2010, 9.6% (R$2,414.5 million)year-to-date and 5.4% (R$1,412.6 million)quarter-on-quarter.

The growth in the last twelve months camemainly from the expansion of time anddemand deposits. Ye ar-to-dat e, the

increase of time deposits and third-partyassets under management exceeded thereduction of demand and savings deposits,indicating migration of funding. Similartrend was also observed in the last quarter.

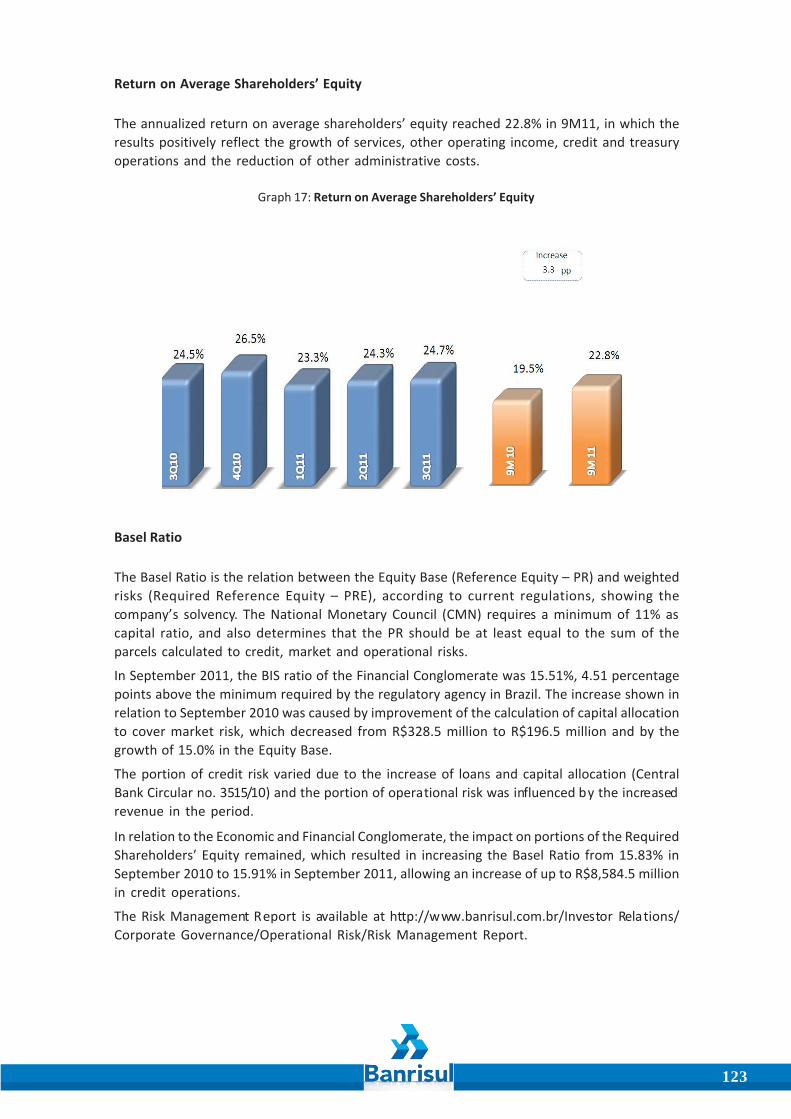

At the end of September 2011,shareholders’ equity totaled R$4,298.1million, with increases of 14.7% in twelvemonths, 11.5% year-to-date and 4.4% from2Q11 to 3Q11, on account of profitsaccounted net of dividends and interest oncapital paid and provisioned. In 9M11, ROEreached 22.8%, and Basel ratio was 15.9%.

Guidance

Banrisul’s strategic guidelines established forthe period 2011-2014 are grounded on theexpansion of loan and funding portfolios, onthe consolidation of market share in services,especially through Banricompras Network,on ongoing improvements of customerservices, on preserving investment ininnovation and reinforcing mechanisms ofinternal controls and risk mitigation and on

employees’ retention and qualification,based on sound, efficiency orientedprinciples of sustainability and management.

In the short term, the special attention tobusiness continuity and the Bank’scommitment to its 2011 guidance has beenreflected in the results achieved in the 9M11,in line to expectations from when it was firstreleased and the reason as to why business

17

Estimate Banrisul Year 2011 Not Altered

CREDIT PORTFOLIO 15% to 20%

Commercial Credit - Individuals 12% to 17%

Commercial Credit - Companies 16% to 21%

Real Estate Loans 18% to 23%

Provision Cost / Average Credit Portfolio 3% to 4%

Allowance for loan Losses / Average Credit Portfolio 6% to 8%

FUNDING 15% to 20%

Time Deposits 35% to 40%

Return on Average Shareholders' Equity 19% to 23%

Efficiency Ratio 44% to 48%

Net Financial Margin / Interest-Earning Assets 10% to 11%

* No altered in 3Q11

and indicators forecasts have beenmaintained ever since.Credit evolution confirms the expecteddeceleration in response to measuresadopted by the Central Bank of Brazil at the

end of December 2010, with a view tomaintaining monetary stabi lity. Otherassumptions included in the guidance reflectthe priority to preserve asset quality and tomanage costs.

Awards

January 2011. Banrisul Brand is featured in world ranking.

January 2011. Banrisul is one of the best reputed companies in Rio Grande do Sul.

March 2011. Banrisul is highlighted in the study Brands of Who Decides.

April/2011. Banrisul’s shares presented the best performance.

April/2011. Banrisul, one of the largest companies in the world.

May/2011. Banrisul’s shares listed in Bovespa’s new index.

May/2011. Banrisul, one of Brazil’s most valuable brands.

June/2011. Banrisul among Brazi l’s most valuable brands.

June/2011. Banrisul is the most remembered brand of Rio Grande do Sul in the bankcategory.

June /2011. Banrisul receives Government and Society Sustainability Certificate.

18 FINANCIAL STATEMENTSSEPTEMBER 2011

July/2011. Banrisul is one of Brazi l’s 100 largest companies.

July/2011. Projeto Pescar Banrisul is awarded as Best Educational Practice.

August/2011. Banrisul is recognized as the Sports’ Best Friend.

August/2011. Bank is featured in national ranking.

August/2011. Banrisul is among the 500 best companies in the country.

August/2011. Banrisul is featured on the socio-environmental area.

August/2011. Banrisul is awarded the Luiz Henrique Roessler Environmental Merit.

September/2011. Banrisul featured in the ranking of customer satisfaction.

Porto Alegre, November 7, 2011.

19

Management ReportWE PRESENT THE MANAGEMENT REPORT AND FINANCIAL STATEMENTS OF BANCODO ESTADO DO RIO GRANDE DO SUL S.A. IN THE 3 RD QUARTER OF 2011 ANDBETWEEN JANUARY AND SEPTEMBER 2011, PREPARED IN ACCORDANCE WITH THERULES OF THE BRAZILIAN SECURITIES AND EXCHANGE COMMISSION (COMISSÃODE VALORES MOBILIÁRIOS – CVM) AND THE CENTRAL BANK OF BRAZIL.

20 FINANCIAL STATEMENTSSEPTEMBER 2011

21

Economic Scenario

During the first semester and the beginning of the secondhalf of 2011, the international economic scenario wascharacterized by the deepening of the global financialinstability, directly associated with the worsening of fiscalproblems in developed economies and the increasing riskof inflation, especially in emerging economies, anduncertainties regarding the recovery of the world’seconomic activity. The protracted stalemate on raising thedebt ceiling as well as the unfavorable prospects for theperformance of the economy in the USA led to thedowngrading of the world’s largest economy rating, withrelevant consequences in the deterioration of consumerand business confidence and in the almost stagnation ofthe economic activity. In Europe, high unemployment

rates, high public debt and low economic growth contributed to increasing global risk aversionand the demand for liquid, low risk assets, and promoted, more recently, the recovery of theUS Dollar in world markets.

The domestic environment, although housed in a highly uncertain international environment,presented a firm economic growth, albeit moderate when compared to the same period lastyear, driven by household consumption which, in turn, was supported by the stability of thelabor market, with historically low unemployment rates and high real wages, as well as bythe consistent evolution of credit in Brazil. In combination with high levels of installed capacityutilization, such a situation led to the gap between the demand and supply growth rates,culminating at inflationary pressures aggravated by the boom of commodity pricesinternationally. Stubbornly such pressures kept market expectations pessimist throughoutthe year, signaling further deterioration of the inflation picture and lower growth rate,nevertheless being partially attenuated by the appreciation of the Brazilian Real in the sameperiod, largely stemming from excess of liquidity in international markets and from theattractiveness of the local economy.

In contrast, the monetary authority has implemented adjustments in monetary policy, raisingthe Selic rate by 175 basis points from January to July, reaching 12.50% per year, besides othermacro prudential measures such as lifting bank reserve requirements and increasing tax onfinancial operations and capital requirement for banks. However, against the backdrop ofincreased uncertainty and pessimism about the evolution of the global economy, monetarypolicy was promptly reversed by starting, in late August, a new setting cycle for the Selic rate,with a drop of 50 points base to the level of 12.00% per year, in order to preserve adequateconditions for the Brazilian economy.

As for the State of Rio Grande do Sul, economic activity showed moderate performance fromJanuary to September 2011 in comparison to the first nine months of 2010, following the

22 FINANCIAL STATEMENTSSEPTEMBER 2011

dynamics of the rest of the country. This moderate scenario reflected fundamentally thestagnation of industrial activity, despite the positive performance of retail sales supported bysolid labor market and the exports of primary products as a result, mainly, of the appreciationof commodities. According to data released by the Federation of Industries of Rio Grande doSul – FIERGS -, the Industrial Performance Index stalled in the first eight months of this year,revealing difficulties to overcome restrictions and resume growth. Among the restrictivefactors to the expansion of the industrial sector, exchange valuation stood out, with directeffects on the trade balance of manufactured products and on the domestic demand, as itmakes local products less attractive abroad and favors the supply of internal market withimported goods, in combination with the apathy of international economic activity. It is worthmentioning that, despite this scenario, the level of installed capacity utilization remained athigh peaks and the variables associated with labor market still showed no significantdeterioration.

Regarding the agricultural sector, the estimate for the total grain harvest in the State of RioGrande do Sul for 2010/2011 already surpasses by 13.5% the effective 2009/2010 harvest, thehighest growth in the Southern Region of Brazil which, coupled with rising prices, guaranteesthe performance of the primary sector in the State. According to Conab’s (Companhia Nacionalde Abastecimento - National Supply Company) September survey, grain production is expectedto surpass 28 million tons, driven by productivity increases and suitable climatic conditions.

As for the State’s trade balance, the result of foreign sales from January to September 2011recorded significant growth driven mainly on higher prices. In the period, exports totaledUSD15 billion, 30.03% higher than that of 9M10. With these figures, Rio Grande do Sul hasreturned to be listed among the largest Brazilian exporting states, contributing now to 7.89%of Brazil’s total exports. On the other hand, imports remained high, supported by favorableexchange rate and the expansion of the internal market, recording, in 9M11, an increase of18.26%. Thus, the State’s trade balance had a surplus of USD3 bi llion, representing an increaseof 95.08% on accumulated numbers in the first nine months of 2011.

In this scenario, it is worth noting also that the evolution of prices from January to Septemberthis year remained dynamic similar to that observed nationally, with major impacts on Food,Housing and Education. Based on IPCA - Extended Consumer Price Index for the MetropolitanRegion of Porto Alegre, accumulated inflation in period was 4.68%.

23

Consolidated Performance

Net Income

Banrisul’s net income totaled R$678 million between January and September 2011, R$166million or 32.52% above the result recorded in the same period in 2010, due to the growth ofcredit and treasury revenues and services fees, and lower administrative costs (exceptpersonnel expenses).

Graph 1: Net Income - R$ Million

Shareholders’ Equity

At the end of September 2011, Banrisul’s shareholders’ equity totaled R$4,298 million, growing14.73% in twelve months as the result of the incorporation of net income net and the deductionof dividend and interest on equity payments and provisions. Return on average shareholders’equity in 9M11 reached 22.76% per annum.

Graph 2: Shareholders’ Equity Growth - R$ Million

24 FINANCIAL STATEMENTSSEPTEMBER 2011

Total Assets

Total assets amounted to R$36,554 million at the end of September 2011, a 13.03% increase inrelation to the R$32,339 million recorded in the same period of 2010, coming from creditexpansion leveraged by the growth of the commercial credit to individuals and companies.

Graph 3: Total Assets Growth - R$ Million

Taxes and Contributions

In 9M11, Banrisul collected and provisioned R$582 million in taxes and contributions. Thetaxes retained and passed through levied directly on financial intermediation and otherpayments amounted to R$370 million.

25

Operational Performance

Funds Raised and Under Management

Funds Raised and Under Management totaled R$27,505 million in September 2011, up 14.15%or R$3,410 million in twelve months. Banrisul has maintained its retail funding policy.

The balance of time deposits reached R$13,269 million, a 39.19% or R$3,736 million increaseover September 2010, and make up for 48.24% of total funding. Savings deposits reduced19.43% or R$1,223 million, ending 9M11 with a balance of R$5,072 million, and account for18.44% of the total funds raised and under management. Demand deposits, which accountfor 9.29% of total funding, increased 21.20% or R$447 million year-over-year and reached thebalance of R$2,556 million. Assets under management, which account for 23.98% of totalfunding, totaled R$6,595 million at the end of 9M11, increasing R$454 million or 7.4% overSeptember 2010.

Graph 4: Growth of Funds Raised and Under Management - R$ Million

Securities

The balance of securities stood at R$10,571 million in September 2011, a year-on-year increaseof 5.56% or R$557 million. This balance includes interbank investments net of resale andrepurchase agreement liabilities.

As confirmed by internal technical studies, Banrisul has a strong financial capacity and intendsto hold securities classified as “held-to-maturity” pursuant to Article 8 of the Central Bank ofBrazil Circular Letter no. 3068 of November 8, 2001.

26 FINANCIAL STATEMENTSSEPTEMBER 2011

Graph 5: Securities Growth* - R$ Million

*Net of Matched transactions

27

Loan Operations

In September, 2011, Banrisul’s loan portfolio totaledR$19,655 million, 21.05% or R$3,418 million above theR$16,237 million recorded in the same month of 2010.Accounting for 70.00% of such growth, the commercialcredit portfolio increased from R$12,515 million toR$14,907 million, rising 19.12% or R$2,392 million intwelve months.

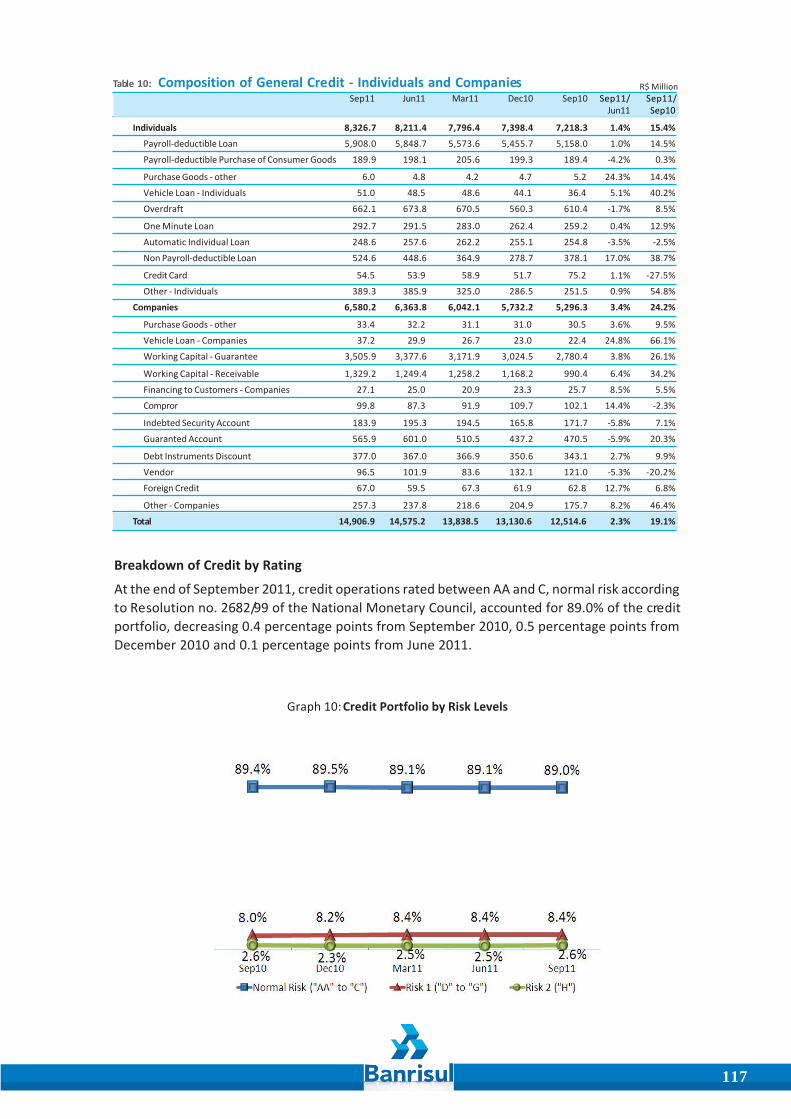

At the end of September 2011, credit operations of AAto C ratings, representative of normal risk according to

Resolution no. 2682/99 of Conselho Monetário Nacional, accounted for 89.02% of the creditportfolio, with a balance of R$17,496 million. Credit operations rated D to G (risk level 1),amounted to R$1,642 million, equivalent to 8.35% of the loan portfolio. Risk level 2, composedsolely by operations rated H that require provisions of 100%, represented 2.63% or R$517million of the total loan portfolio.

Graph 6: Loan Operations Growth - R$ Million

At the end September 2011, commercial loan operations (non ear-marked credit) to individualstotaled R$8,327 million, accounting for 55.86% of the commercial portfolio and 42.37% of allloan operations. The 15.36% or R$1,108 million year-on-year increase is particularly due tothe growth of payroll loans.

Own payroll loan portfolio amounted to R$3,717 million in September 2011, 12.25% abovethe balance recorded in the same month of 2010. Acquired payroll loan portfolio amountedto R$2,381 million in September 2011, a year-on-year increase of 16.93%.

Commercial loan operations targeted to Companies increased R$1,284 million or 24.24%,totaling R$6,580 million at the end of September 2011, and accounted for 44.14% of the

28 FINANCIAL STATEMENTSSEPTEMBER 2011

commercial credit portfolio and for 33.48% of the loan book. Working capital lines increased28.23% year-on-year, reaching a balance of R$4,835 million in September 2011.

Graph 7: Commercial Credit Growth – Individuals and Companies - R$ Million

The balance of real estate loans reached R$1,611 million in September 2011, an increase ofR$393 million or 32.31% in twelve months. In 2011, Banrisul held events in various locations topromote the lines of credit and financing conditions offered by the Bank to real estatecompanies and brokers, to real estate loans correspondents, to developers and otherprofessionals engaged in real estate business. Since September 2011, and looking to addbenefits to the portfolio, the customer who was has a real estate finance at Banrisul has thebenefit of opting to include in the loan the amount due as ITBI (tax transfer of immovableproperty) and other fees, and may also choose for a grace period of up to 3 (three) months forthe payment of amortization.

At the end of September 2011, rural lending amounted to R$1,584 million, an increase ofR$403 million or 34.18% in twelve months. In order to stimulate the productive sector ofagribusiness and to expand Banrisul’s market share in rural lending, the Bank has attendedagricultural fairs, created new products for the sector and provided training to employees.The Bank’s participation at the 34th Expointer, held between August 27 and September 04,2011, increased the amount of agricultural credit proposals in the amount of R$47 million, anincrease of 138% over 2010. In their implementation phase and expected to begin operationsin the fourth quarter of 2011, programs were created, such as the Banriagro Simplified Credit,for cooperatives and agribusinesses, and the Rice in the Mercantile Exchange, a partnershipwith Banrisul’s Brokerage Company. During this period, 330 branch employees participated intraining courses to efficiently and effectively operate the demand for rural credit.

29

The long-term finance portfolio totaled R$838 million in the end of 9M11, an increase ofR$193million or 30.00% over the balance recorded in 9M10.

ACC and ACE (pre- and post-shipment export financing operations) totaled R$513 million atthe end September 2011.

It is the aim of Banrisul to align public policy with social and economic development toexpand the supply of credit for formal and informal businesses. Given this purpose, in July2011 microcredit ’s project and risk policy were approved. In August, the launch of GauchoMicrocredit program by the State Government was the highlight, and microcredit operationsstarted at Banrisul.

30 FINANCIAL STATEMENTSSEPTEMBER 2011

Graph 8: Banricompras

Financial Transactions - R$ Million Transactions - Million

Products, Services and Channels

Banricompras

Banrisul customer’s unique product, Banricompras conducted 56 millionoperations from January to September 2011, totaling R$3,909 million in

financial turnover, numbers that are 9.67% and 15.66%, respectively,higher to the same period last year. The strengthening of the

Banricompras Network is part of the Bank’s business strategy, whichincluded entering into accrediting new merchant stores, providingshop owners and customers various payment options on a singleterminal.

Banrisul has established agreement to offer the SafetyPay system in Brazil,through operations to be carried out online by the store Amazon.com and

settled through Banrisul's Internet Banking. Initially, the launch of the International SafetyPayBanricompras is available only to Banrisul's employees for subsequent use by customers.

In July 2011, the Bank and the Verde Administradora de Cartões de Crédito (VerdeCard – CreditCard Issuing Company) entered into a partnership that will allow Banricompras network tocapture debit and credit transactions other than Banrisul’s debit card directly at terminals andPOS, providing new business opportunities for both companies.

Partnerships with other card brands allow the increase of Banrisul own network, which isbecoming a multibrand one. This diversity of payment options offered by BanricomprasNetwork enables business expansion to the Bank and brings convenience, safety and state-of-the-art benefits to its affiliated stores and customers.

Banrisul’s Correspondent Banks

From January to September 2011, Banrisul had approximately 2,000 correspondent banks,with an average of 5 million transactions per month. At the end of this quarter, 43 milliontransactions were recorded with a financial turnover of R$10.865 million, an increase of 8.08%over 9M10.

31

Virtual Branch – Home and Office Banking

From January to September 2011, 76 million operations totaling R$65,664 million were carriedout through Agência Virtual Banrisul (Banrisul Virtual Branch). In relation to the same periodin 2010, the number of transactions grew 4.11% and the financial turnover, 15.91%.

Banrifone and Branch Call Center

Through Banrifone, customers can obtain account statements and balances, request bankingservices and carry out banking transactions, all these over the phone. During the first ninemonths of 2011, Banrifone electronic service had 4 million accesses, 420.000 of them operatorassisted, and presented a financial turnover of R$166 million, information services aside.Over the same period, 987.000 phone calls with a financial turnover of R$17 million weremade to the Branch Call Center, designed to capture calls from individual customers that aremade to branches that are part of such service.

Credit Cards

At the end of September 2011, Banrisul had a base of 403,000 Visa and MasterCard creditcardholders, 42.18% up over the same period in 2010. During the same period, credit cardcustomers were responsible for a financial turnover of R$759 million in 10 million transactions,an increase of 39.88% and 34.32%, respectively, over 9M10.

In Banrisul’s own acquiring network, Banricompras Network, a wide variety of transactionscan be carried out: with Banricompras and MasterCard cards, Meal Food, Benefits, Presentand Fuel cards, and IPE’s (Instituto de Previdência do Estado – Social Security Institute of theState of Rio Grande do Sul) Health Care. As a result from the strategy of entering into theacquiring business, Banricompras network has started a multibrand expansion since 2010and, from March 2011 on, has gained notoriety with the capture of debit and credit cardstransactions with the MasterCard brand. Recently, the Bank has also prepared the network tocapture credit card transactions with the VerdeCard label. The technological advances offeredby the network include modern solutions that meet the needs of commercial trade.

As issuer of Visa and MasterCard cards, Banrisul has promoted internal campaigns to increasesales. Beside the BanriClube de Vantagens (Banrisul’s reward program), released at the end of2010, commercial campaigns conducted during 3Q11 ended up with sales of more than 50,000credit cards.

These actions to broaden and improve the card base and has brought in recognition. Recentsurvey conducted by the consulting company CVA Solutions demonstrated that Banrisul’scustomers are satisfied with the interest rates charged in the revolving credit facilities andwith the outreach of its network in the State. The survey indicated that the Bank is the secondbest institution according to how customers perceive the cost-benefit perceived of plasticmoney.

32 FINANCIAL STATEMENTSSEPTEMBER 2011

Insurance, Private Pension and Capitalization

The expansion of the Brazilian economy and improved income distribution have brought intothe insurance market new customers, especially from the classes C and D. In this scenario,following the rapid growth of the insurance industry, Banrisul has sought to better repositionits products and establish actions and campaigns to increase synergy among customers, pointof sale and brand value, which strengthens Banrisul’s identity as a provider of insurancesolutions.

In the third quarter of 2011, the Bank launched three new insurance products: EngineeringRisk, Civil Liability and Miscellaneous Equipment Risks. In the same period, the marketing oflife and automotive insurance products was encouraged, through campaigns named Auto andLife SuperAção, with the participation of more than 3,000 employees.

Electronic Bidding

The Electronic Auction is a modern shopping portal on the Internet directed at public companiesindirectly controlled by the State Government, municipal governments and other public andprivate entities. By September 2011, R$608 million in purchases of goods and the hiring ofservices were carried out, in 34,000 trading sessions of bidding contests. Banrisul, in the sameperiod, while user of the Procurement System, held 298 trading sessions, with a total of R$24million in purchases of goods and contracting of services, which represented a reduction ofR$12 million over the R$36 million initially offered for the purchases, an economy of 33.33%.

Public Sector ActivitiesBanrisul continuously strives to strengthen customerservice and collaborate with the economic and socialdevelopment of Rio Grande do Sul. Focused on thatmission, it establishes partnerships with the governmentat the municipal, state and federal levels.

In order to reduce operating costs for the municipalities,the Bank has maintained the focus of providing productsand services, particularly the fleet managementsolutions and the management of electronic purchases. During the 9M11, through placingtelephone calls and sending illustrative e-mails to local government representatives, thedisposition of credit lines to anticipate year-end bonus (the 13th salary) to municipal civilservants was made available. Among the banking services offered from January to September2011, a total of R$814 million was raised from municipal taxes and fees upon the collection ofmore than four million documents. In relation to managing assets from the public sector,marketing actions addressing the social security system related to the civil servants wererestructured, in order to expand the attractiveness of Banrisul’s products. Also noteworthy isthe Bank’s participation in FAMURS 31 st General Congress with the theme Agriculture:Sustainable Growth and Economic Relevance.

33

Eletronic Service Station - Brasília Passo da Areia Branch - Bourbon Shopping - Porto Alegre

Trindade Branch - Florianópolis

To service the state public sector, in conjunction with the Court of the State and the StateDepartment of Finance, Banrisul launched the Automated State Debt Security, a new systemof transferring information between the Court of Justice of the State of Rio Grande do Sul andBanrisul, which enables the deposit of amounts in all of the Bank’s branches, eliminating theneed for going in person to the State Debt Security Agency in Porto Alegre.

Responsible for payments to policyholders/beneficiaries of Social Security, Banrisul mademore than 254,000 payments to new beneficiaries of the Social Security during the first ninemonths of 2011, consolidating its position as the bank of choice in the state of Rio Grande doSul in the providing benefits payment on behalf of the Institute.

Banrisul´s Customer Service NetworkBy the end of September 2011, Banrisulserved its customers in 1,272 points,distributed in 440 branches (399 in RioGrande do Sul, 25 in Santa Catarina, 14 inother Brazilian states, one in New Yorkand one in Grand Cayman), 279 bankingservice stations and 553 electronicservice stations. In Rio Grande do Sul, theBank is present in 414 municipalities,covering 98.31% of the population andthe GDP of the state.

The focus of expansion of the service network is in the Southern Region of the country. Thecurrent expansion project encompasses the opening of 35 branches in places where Banrisulis already present, 21 new branches in cities that lack banking presence and to transform 48service stations into full small size branches in the State of Rio Grande do Sul, besides the 7new branches to be opened in the State of Santa Catarina, totaling 111 branches.

34 FINANCIAL STATEMENTSSEPTEMBER 2011

99.6% ON70.5% PNA13.0% PNB57.0% Total

0.4% ON29.5% PNA87.0% PNB43.0% Tot al

State of RioGrande do Sul Market

Banco do Estadodo Rio Grande do Sul S.A.

Banrisul S.A.Adm. Consórcios

Banrisul S.A.CVMC

Banrisul ArmazénsGerais S.A

Banrisul ServiçosLtda.

99.6% Total 98.7% Total 99.5% Total 99.8% Total

Subsidiaries

Banrisul S.A. Administradora de Consórcios –The Company ended September 2011 with 24,983active groups and with a loan portfolio of R$762 million. In the first nine months of 2011, 3,403letters of credit were granted to customers, equivalent to R$83 million for the purchase ofgoods. Net income in 9M11 totaled R$11 million.

Banrisul S.A. Corretora de Valores Mobiliários e Câmbio – By the end of September 2011, theCompany brokered R$843 million in the stock market, of which 65.30% through Home Broker.Net income for the first nine months of 2011 totaled R$3 million.

Banrisul Armazéns Gerais S.A. – Banrisul Armazéns Gerais S.A. accumulated until September2011 a net income of R$1 million. The company’s strategy to expand its participation in thelogistics market is to invest in technology, process automation, increase of workforce andsearch for new market niches.

Banrisul Serviços Ltda. – Banrisul Serviços Ltda. operates in the southern region of Brazil inthe segments of meal and food vouchers, fuel, gifts, private label and benefit cards. On adaily basis, more than 410,000 individual customers and 5,500 companies use its products inmore than 50,000 affiliated stores. Regarding the lines sponsored by the Federal Governmentwithin the Programa de Alimentação ao Trabalhador (PAT - Workers' Nourishment Program),Refeisul is responsible to make payments under PAT program to about 35% of the totalbeneficiaries in Rio Grande do Sul. By September 2011, the company's net income was R$15million.

35

Corporate Governance

Overview

Since July 2007 listed on BM&FBovespa SA‘sCorporate Governance Level 1, Banrisul meetsthe requirements of this level of listing and alsorequirements of other levels of corporategovernance, in line with best market practices,on behalf of greater transparency, fairness andproper accountabi lity, whi le enhancingcredibility and the interest of investors andcustomers.

Corporate governance practices create incentives and monitoring mechanisms, ensuring thatthe Banrisul’s behavior is market oriented. They also confirm the interest in improving andstrengthening relations with its controlling shareholders, the Board of Administration, FiscalCouncil, Board of executive Officers, independent auditors, oversight bodies and other relatedparties and stakeholders.

Such practices are important, especially in times of administrative changes such as occurredduring the first semester of this year, yet without significant changes in Banrisul’s businessmanagement, reinforcing its role as a state-controlled, market-oriented publicly held company.

It is also worth noting that, in the first quarter of 2011, Deloitte Touche Tohmatsu, independentauditors, was replaced by Ernst & Young Terco Auditores Independentes S/S upon terminationof contract. The hiring was done through a bidding process (Public Competition 97/2010), asestablishing by the Law No. 8666 of June 21, 1993 (Public Procurement Law), which sets forthrules forbidding and contracts within the Public Administration area, to which Banrisul has toabide for being a public capital company controlled directly by the State of Rio Grande do Sul.

The participation of the Boards of Administration and Fiscal Council in the decision-makingstructure, the management model focused on profitability and quality of operations and theadoption of corporate governance policies give Banrisul strength and recognition, as reflectedin the proper performance within the banking industry.

Shareholding Structure

The Government of the State of Rio Grande do Sul, as the main shareholder, have control overthe election of the Board of Administration and, therefore, over Banrisul’s management andoperations. However, the Bank’s free float is above the minimum of 25% required by CorporateGovernance Level 1: 42.8% of its total shares are held by shareholders without any connectionwith the Institution. Banrisul’s shareholding structure is presented in the following graph.

36 FINANCIAL STATEMENTSSEPTEMBER 2011

Investor Relations and Communication Policy

A transparent relationship with clients and investors is built through the disclosure of dataand information to the market, communication that allows broader and timely knowledge ofthe Bank’s business.

Banrisul’s Investor Relations website, available in Portuguese and English, provides clear,detai led and timely information for the Bank’s shareholders, institutional investors,individuals, market analysts and other interested stakeholders.

The significance of these events is reflected on Banrisul’s trading volume. At the end ofSeptember 2011, the Bank’s PNB stock (BRSR6) ranked 94th among the 100 most-traded stockson BM&F Bovespa (78th in twelve months).

Banrisul’s market value in September 2011, represented by the total number of outstandingshares multiplied by the closing price of its PNB stock, was 52% higher than shareholders’equity in the same period.

Graph 10: Market Value X Shareholders’ Equity - R$ Mi llion

37

The table below shows the geographic distribution of shareholders by number and numberof Banrisul’s shares held.

REGION SHAREHOLDERS % SHARES %

BRAZIL 55,500 98.96% 242,276,301 59.24%

NORTH AMERICA 263 0.47% 57,451,426 14.05%

CENTRAL AMERICA 15 0.03% 1,528,485 0.37%

SOUTH AMERICA (Except Brazil) 8 0.01% 1,162,443 0.28%

EUROPE 218 0.39% 85,992,065 21.03%

AFRICA 1 0.00% 95,000 0.02%

ASIA 67 0.12% 18,354,238 4.49%

OCEANIA 14 0.02% 2,114,519 0.52%

TOTAL 56,086 100% 408,974,477 100%

Interest on Equity and Dividends Payout Policy

Since early 2008, Banrisul has maintained the policy of paying interest on equity on a quarterlybasis and, historically, has remunerated its shareholders by paying interest on capital anddividends above the minimum level required.

From January to September 2011, R$221 million net of income taxes were paid/provisionedas interest on own equity and dividends.

Graph 11: Pay Out – Quarterly Payments - R$ Million

38 FINANCIAL STATEMENTSSEPTEMBER 2011

Internal Controls and Compliance

To strengthen the system of internal controls, Banrisul hasadopted policies aimed at spreading the culture of internalcontrols, ensuring compliance with rules, procedures andstandards established by law and enforcement agencies.

The internal controls policy establishes guidelines that seek toperiodically reinforce the alignment of internal controls withthe goals related to global business strategies and otherinstitutional policies set by the management.

The area in charge of internal control monitors activities in order to ensure compliance withregulations, the use and the effectiveness of controls in the many processes of the institution,to prevent and reduce risks inherent to business.

The spread of a controlling culture and the maintenance of an ethical environment areguaranteed by a set of rules, regulations and codes that guide employees in their activities toincorporate the values and ethical principles of the Organization.

Money Laundering Prevention - MLP

The Bank has established specific prevention processes and systems in order to ensure thatits activities are conducted in an environment of adequate controls to prevent risks related tothe crime of money laundering.

In this context, Banrisul maintains dedicated staff devoted to the execution of tasks focusedon the prevention of money laundering, which is responsible for reviewing legislation andprocedures and developing training programs for all employees.

The “Know Your Customer” process is continually reviewed and disseminated, emphasizingthe importance of timely, qualified customer information gathered at the beginning of eachand every business relationship, mitigating the risks of having the Bank’s services and productsused to legitimize illicit activities.

Risk Management

The risk management is embedded and continuously monitored in Banrisul’s strategicplanning. Management is performed on a consolidated basis and is added to the managementstructures dealing with credit, market, liquidity and operational risk, which contributes toexpedite processes, to decision making and to the alignment to the provisions of best practicesand standards defined by the Central Bank of Brazil, in accordance with the guidelines of theBasel Committee.

39

Credit Risk

The institutional policy for the management of credit risk at Banrisul aims to identify, measure,monitor and mitigate exposure to credit risk within the loan portfolio; to act towardsconsolidating a culture of best practices in credit risk management; to enhance ongoingmanagement of credit risk in all types of assets; to ensure adequate levels of risk and avoidlosses not covered; to ensure impartial and segregation of function in the process of managingcredit risk.

In the process of identifying, evaluating and monitoring credit risk, Banrisul adopts CreditScore and Behavior Score models when dealing with Individuals, defining pre-approved creditlimits based on risk classifications provided for in statistical models. The analysis of adherenceto the model is assessed every six months by the Board of Executive Officers and the BankingManagement Committee. For the Companies segment, the Automated Credit Risk Modelwas established in February 2011, also based on models of Credit and Behavior Scores. At thisstage of implementation, the current policy model in use by the Bank, through credit scopeand credit grant by the Branches Credit Committees, remains as it is. For the Corporatesegment, Banrisul has adopted technical studies performed by the internal area of risk analysis,which evaluates companies from the financial, management, marketing and productionperspectives, with periodic review, considering economic scenarios, simulating the economicsituation of companies in these environments.

As for the credit operations not covered by scoring models and onlendings operations throughfinancial agents, Banrisul assesses the probability of default of counterparties individually,through classification tools designed for the different categories of counterparties. Regularly,the Administration validates the performance of the classification and its predictive powerwith respect to events of default.