Embed Size (px)

Citation preview

C1 - 1

Learning Objectives

1. Nature of a Business

2. The Role of Accounting in Business

3. Business Ethics

4. Profession of Accounting

5. Generally Accepted Accounting Principles

6. Assets, Liabilities, and Owner’s Equity

7. Business Transactions

8. Financial Statements

9. Financial Analysis and Interpretation.

Power Notes Introduction to Accounting and Business Introduction to Accounting and Business

Chapter F1

C1

C1 - 2 Note: To select a topic, type the slide # and press Enter.

• Accounting – An Information Process• Users of Accounting Information• Profession of Accounting• The Accounting Equation• Business Transactions• Financial Statements• Ratio of Liabilities to Stockholders Equity

Slide # Power Note Topics

Power Notes Introduction to Accounting and Business Introduction to Accounting and Business

Chapter F1

39

1116195369

C1 - 3

Accounting — An Information Process Accounting — An Information Process

Accounting — An Information Process Accounting — An Information Process

Identificationof Users

C1 - 4

UserInformation

Needs

Accounting — An Information Process Accounting — An Information Process

Accounting — An Information Process Accounting — An Information Process

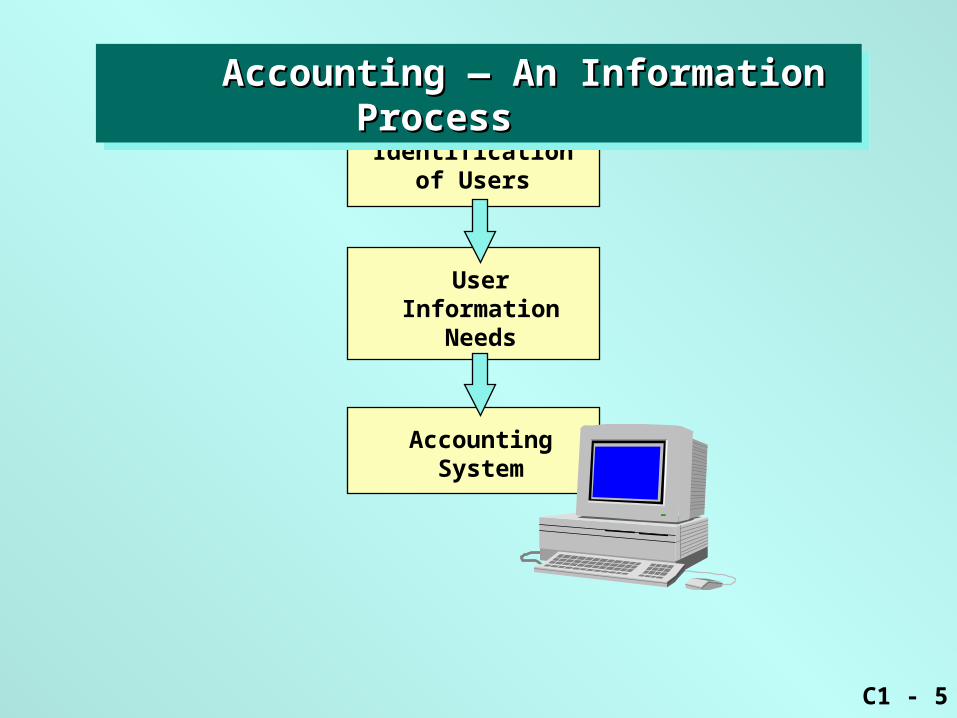

Identificationof Users

C1 - 5

Identificationof Users

UserInformation

Needs

AccountingSystem

Accounting — An Information Process Accounting — An Information Process

Accounting — An Information Process Accounting — An Information Process

C1 - 6

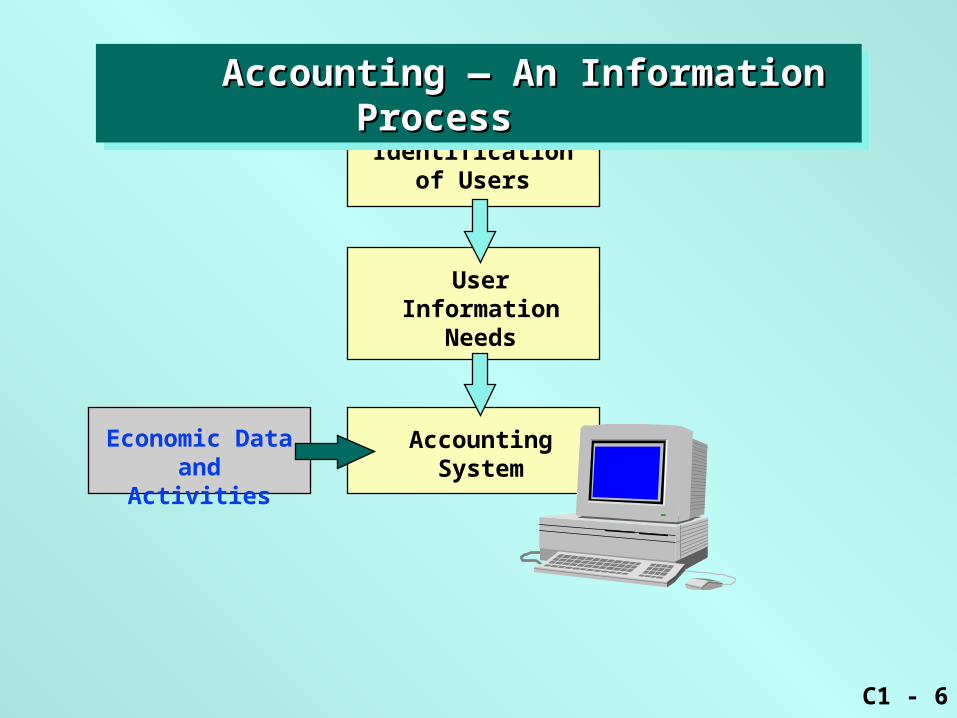

Identificationof Users

UserInformation

Needs

AccountingSystem

Economic Dataand Activities

Accounting — An Information Process Accounting — An Information Process

Accounting — An Information Process Accounting — An Information Process

C1 - 7

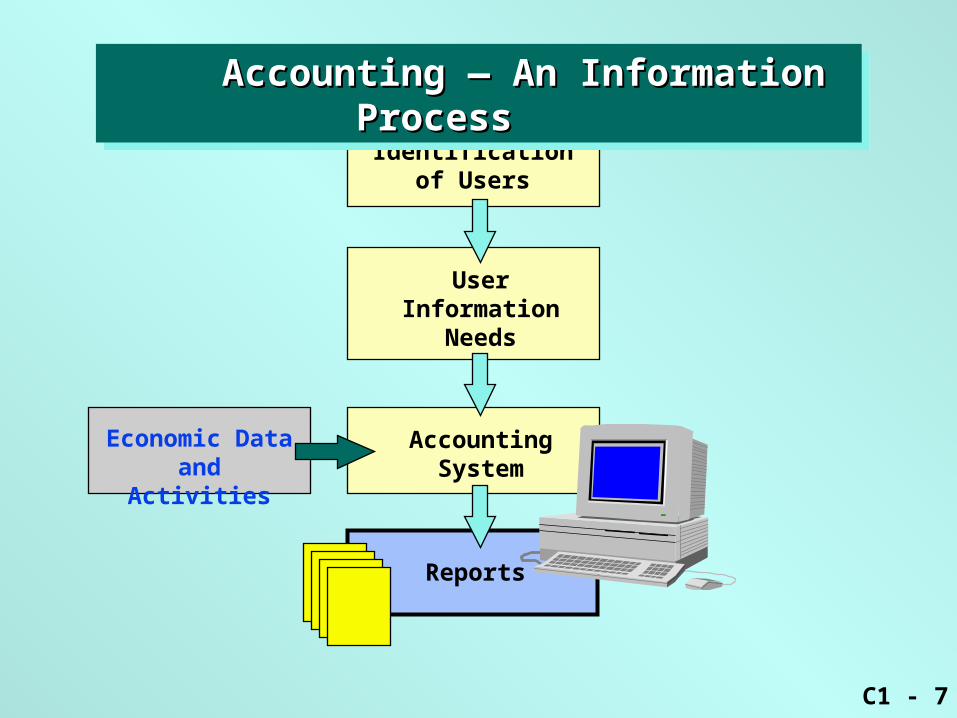

Identificationof Users

UserInformation

Needs

AccountingSystem

Economic Dataand Activities

Reports

Accounting — An Information Process Accounting — An Information Process

Accounting — An Information Process Accounting — An Information Process

C1 - 8

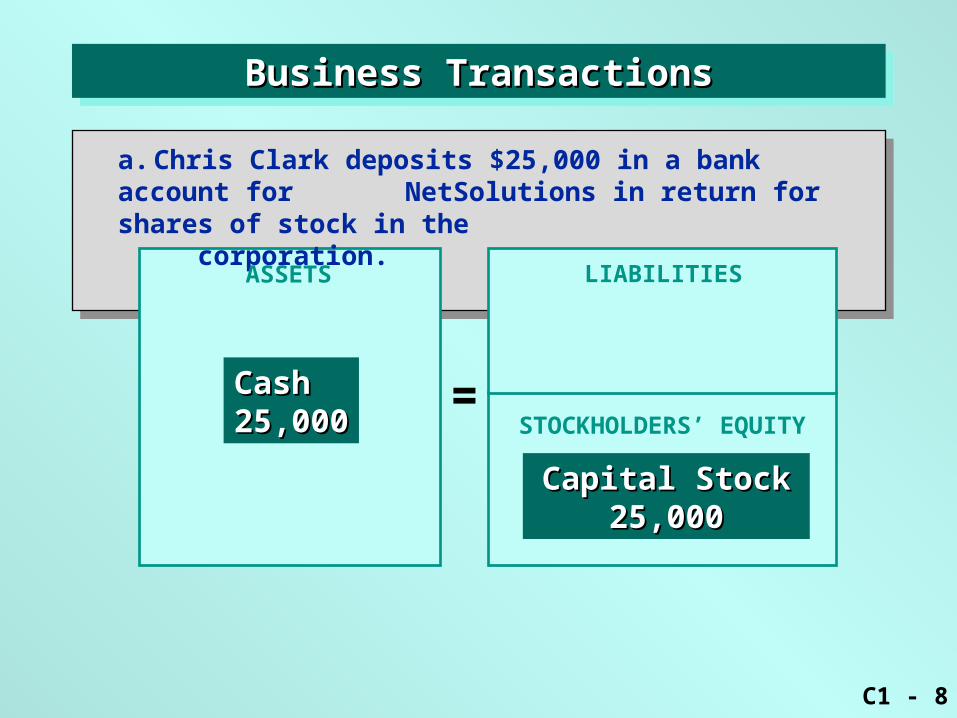

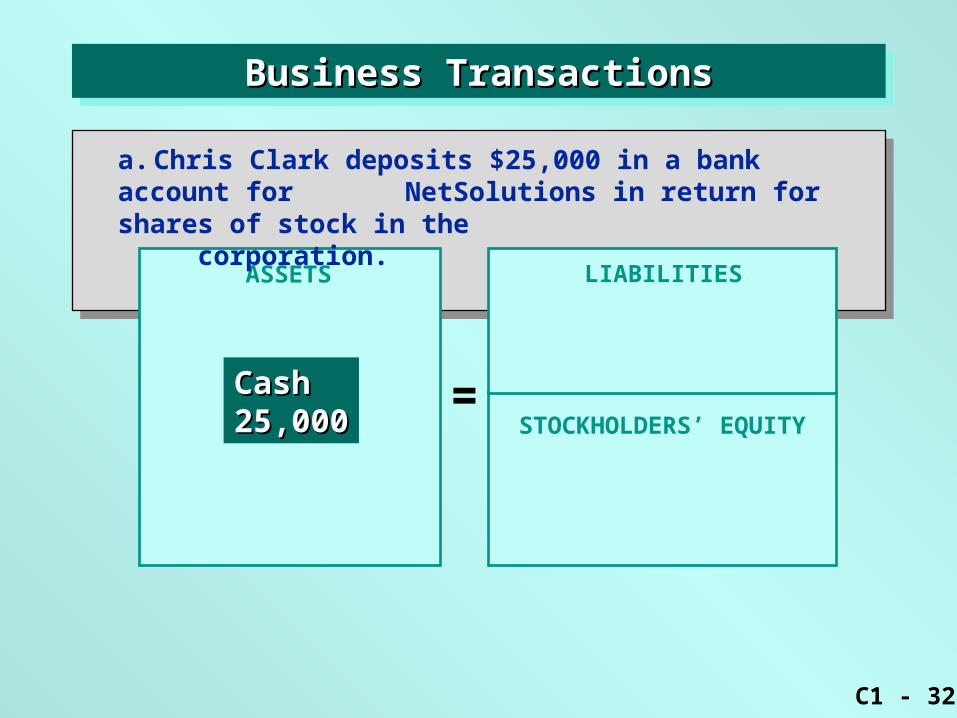

a. Chris Clark deposits $25,000 in a bank account for NetSolutions in return for shares of stock in the

corporation.

ASSETS

=

Business TransactionsBusiness TransactionsBusiness TransactionsBusiness Transactions

Cash Cash 25,00025,000

LIABILITIES

Capital Stock Capital Stock 25,00025,000

STOCKHOLDERS’ EQUITY

C1 - 9

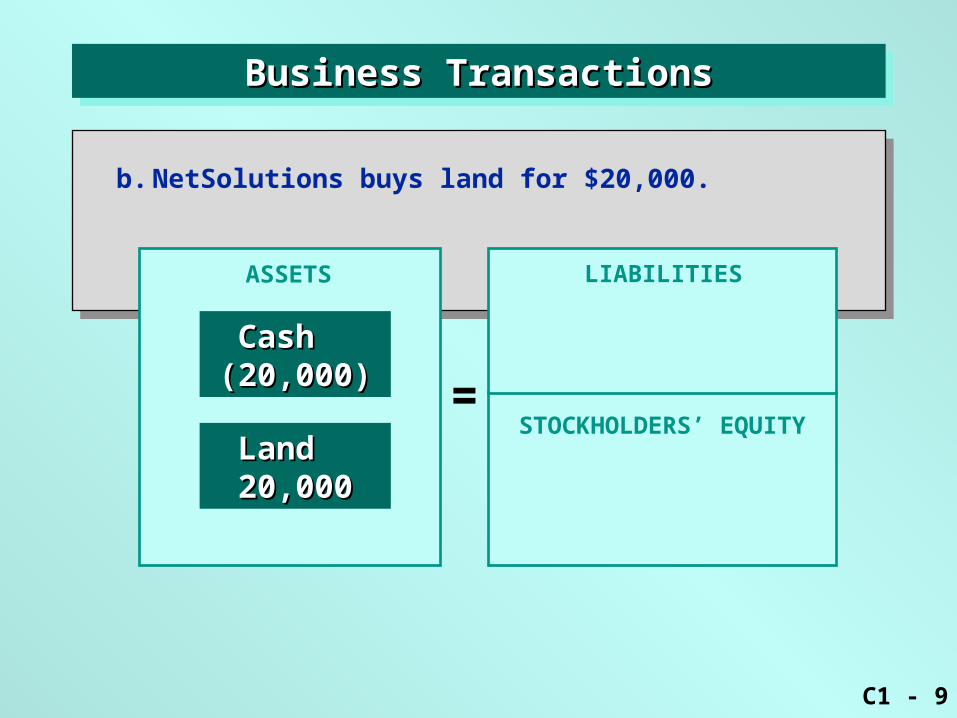

Business TransactionsBusiness TransactionsBusiness TransactionsBusiness Transactions

b. NetSolutions buys land for $20,000.

ASSETS

=

LIABILITIES

Cash Cash (20,000)(20,000)

Land Land 20,00020,000

STOCKHOLDERS’ EQUITY

C1 - 10

Business TransactionsBusiness TransactionsBusiness TransactionsBusiness Transactions

ASSETS

=

LIABILITIES

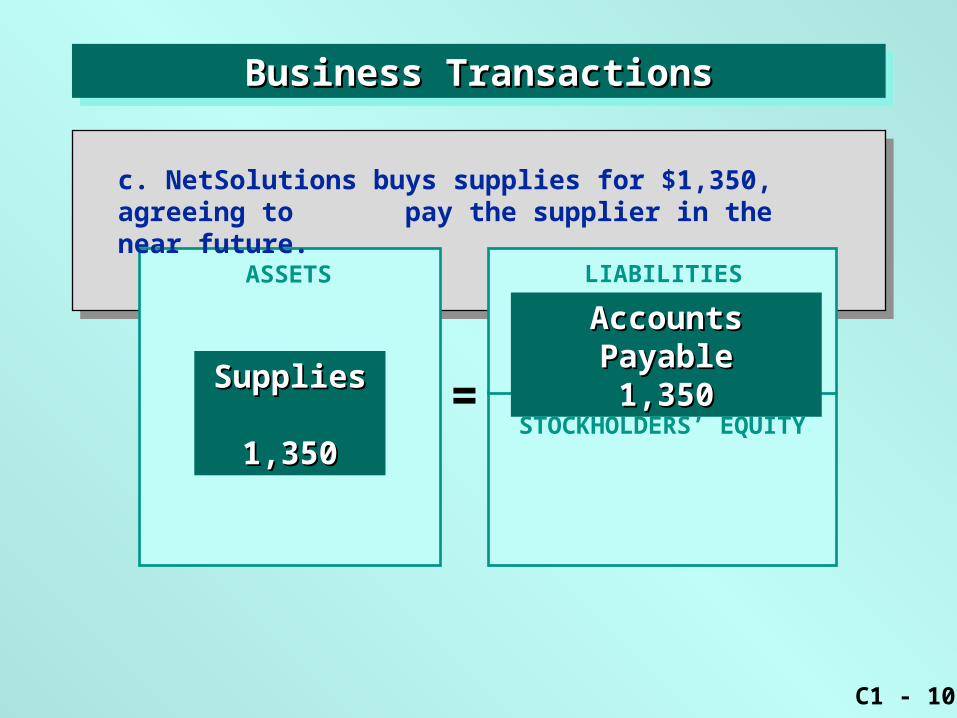

c. NetSolutions buys supplies for $1,350, agreeing to pay the supplier in the near future.

Accounts PayableAccounts Payable1,3501,350

Supplies Supplies 1,3501,350 STOCKHOLDERS’ EQUITY

C1 - 11

Business TransactionsBusiness TransactionsBusiness TransactionsBusiness Transactions

ASSETS

=

LIABILITIES

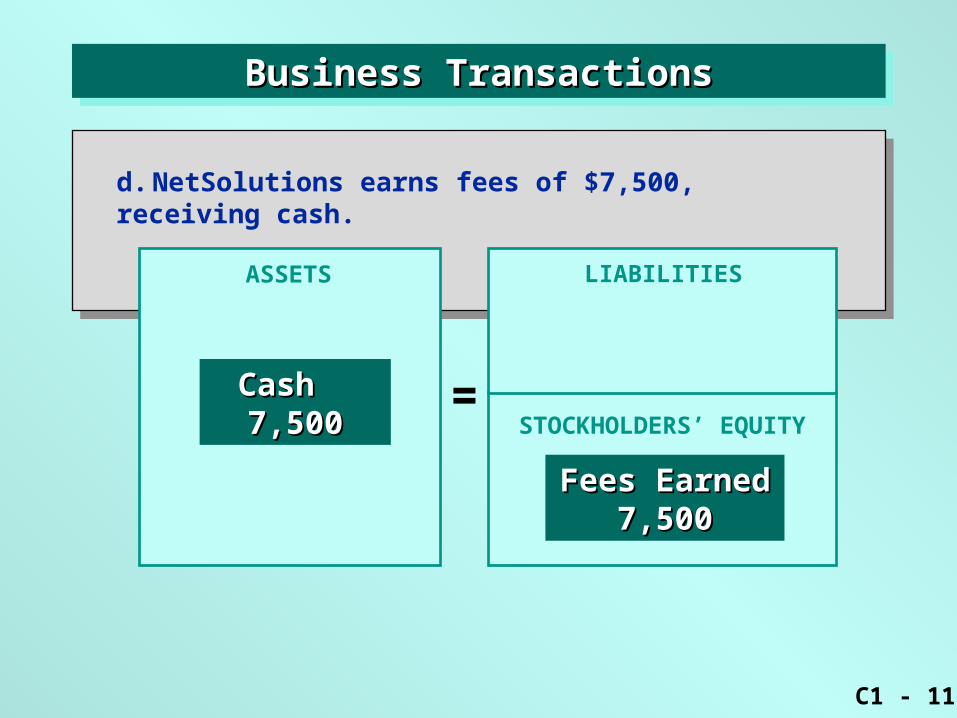

Cash Cash 7,5007,500

Fees Earned Fees Earned 7,5007,500

d. NetSolutions earns fees of $7,500, receiving cash.

STOCKHOLDERS’ EQUITY

C1 - 12

Business TransactionsBusiness TransactionsBusiness TransactionsBusiness Transactions

ASSETS

=

LIABILITIES

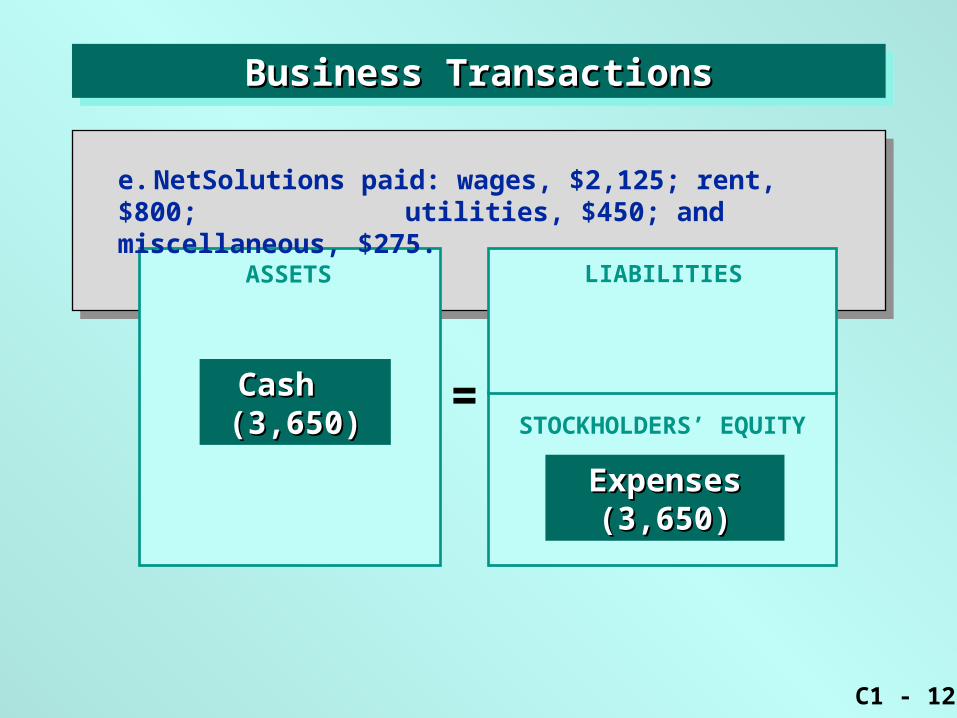

Cash Cash (3,650)(3,650)

ExpensesExpenses(3,650)(3,650)

e. NetSolutions paid: wages, $2,125; rent, $800; utilities, $450; and miscellaneous, $275.

STOCKHOLDERS’ EQUITY

C1 - 13

Business TransactionsBusiness TransactionsBusiness TransactionsBusiness Transactions

ASSETS

=

LIABILITIES

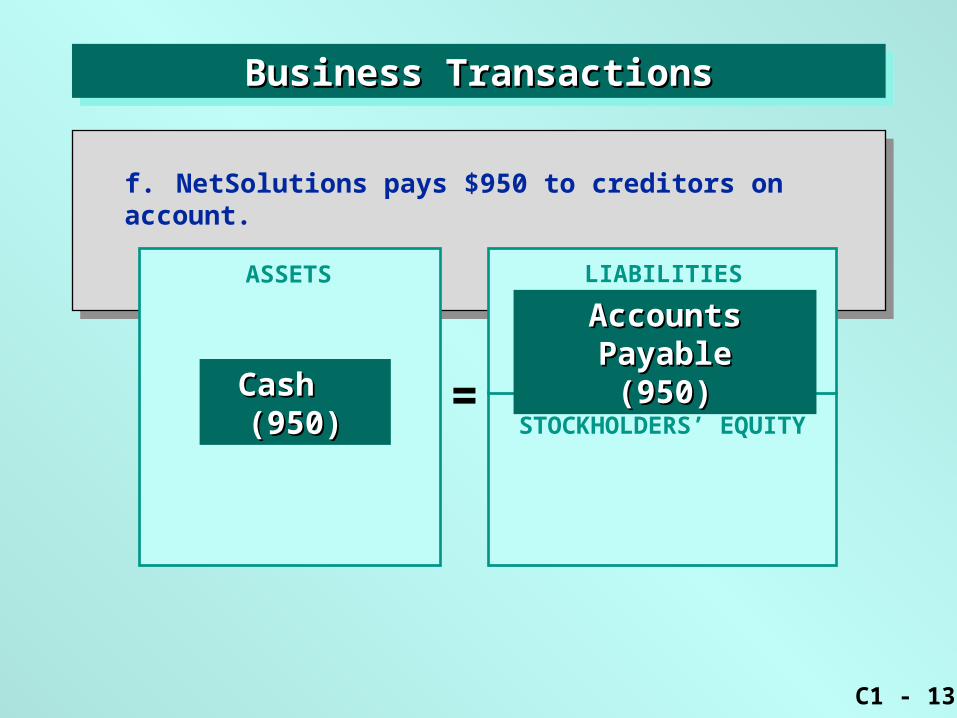

Cash Cash (950)(950)

Accounts PayableAccounts Payable(950)(950)

f. NetSolutions pays $950 to creditors on account.

STOCKHOLDERS’ EQUITY

C1 - 14

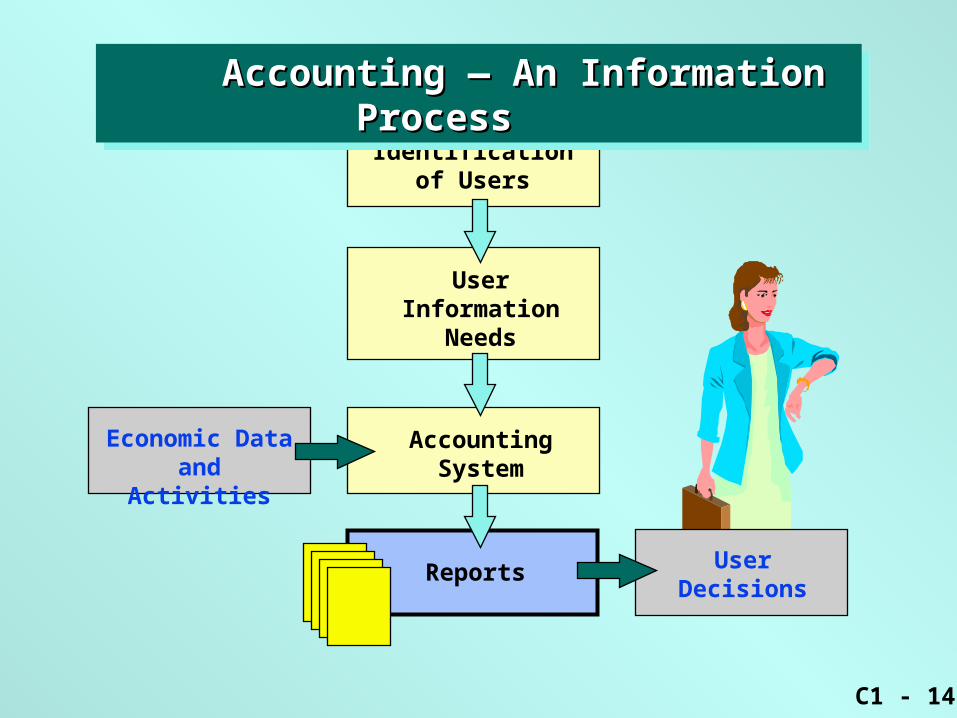

Identificationof Users

UserInformation

Needs

AccountingSystem

Reports

Economic Dataand Activities

UserDecisions

Accounting — An Information Process Accounting — An Information Process

Accounting — An Information Process Accounting — An Information Process

C1 - 15

Business TransactionsBusiness TransactionsBusiness TransactionsBusiness Transactions

ASSETS

=

LIABILITIES

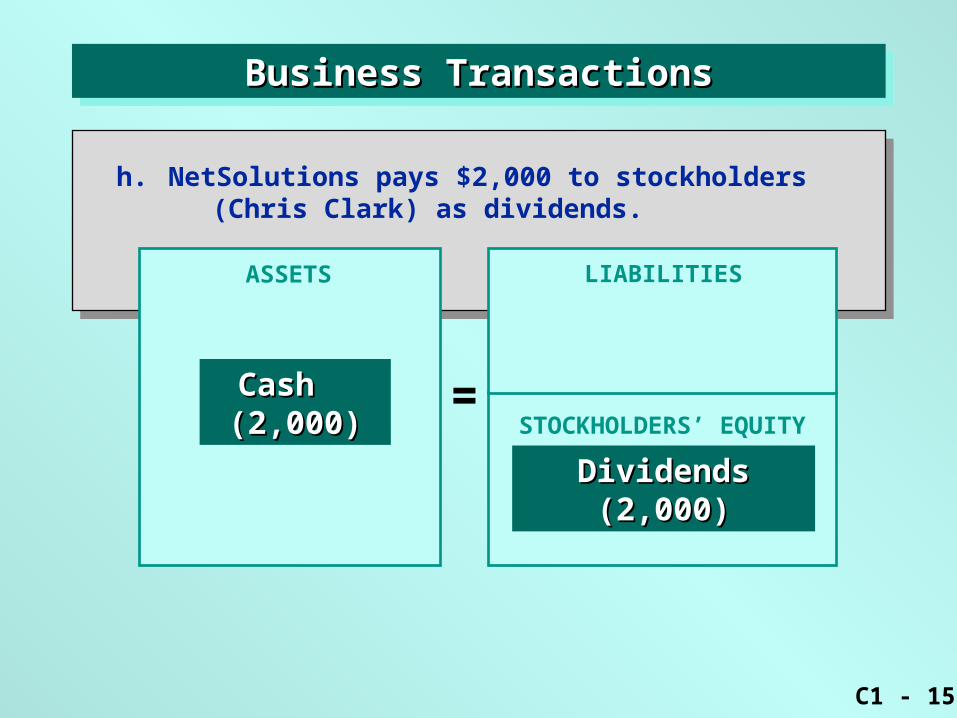

Cash Cash (2,000)(2,000)

DividendsDividends(2,000)(2,000)

h. NetSolutions pays $2,000 to stockholders (Chris Clark) as dividends.

STOCKHOLDERS’ EQUITY

C1 - 16

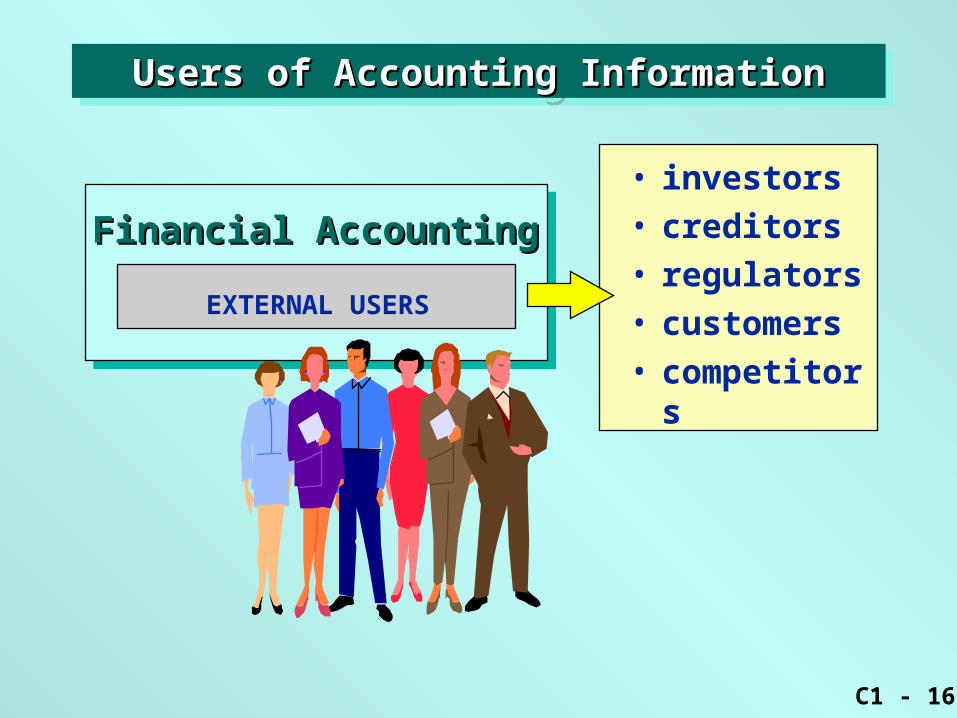

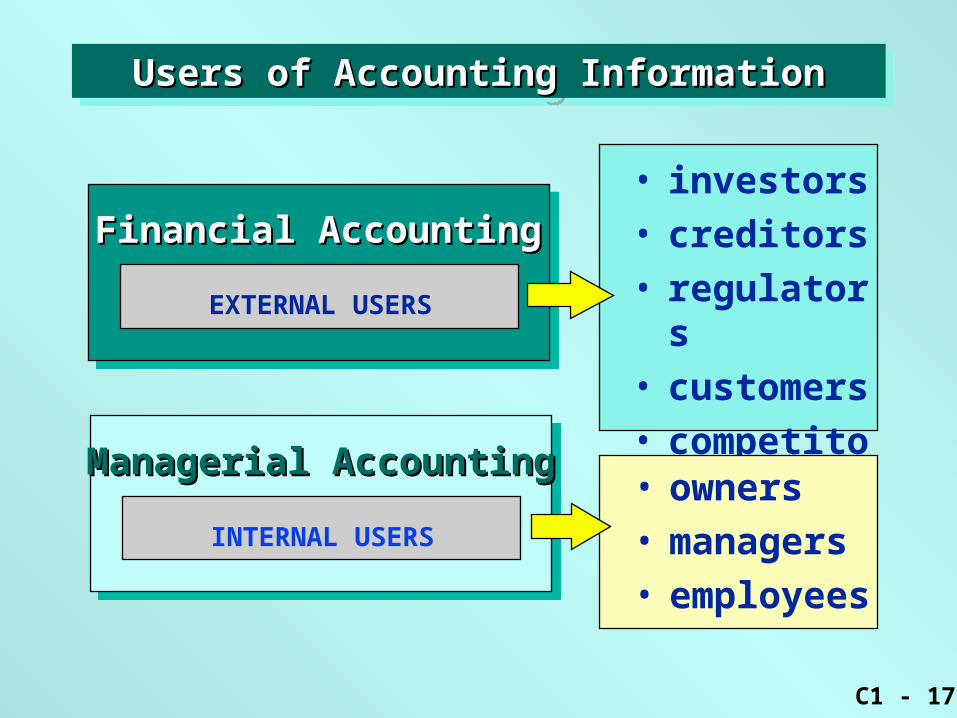

EXTERNAL USERS

Financial AccountingFinancial Accounting

• investors• creditors• regulators• customers• competitors

Users of Accounting InformationUsers of Accounting InformationUsers of Accounting InformationUsers of Accounting Information

C1 - 17

EXTERNAL USERS

Financial AccountingFinancial Accounting

• investors• creditors• regulators• customers• competitors

• owners• managers• employees

INTERNAL USERS

ManagerialManagerial AccountingAccounting

Users of Accounting InformationUsers of Accounting InformationUsers of Accounting InformationUsers of Accounting Information

C1 - 18

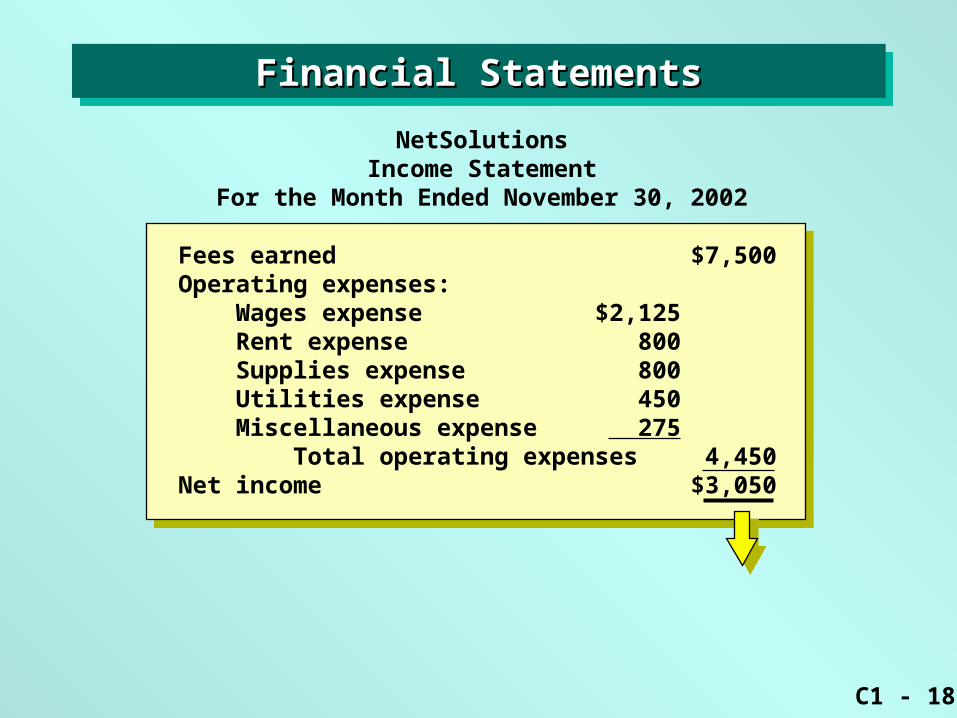

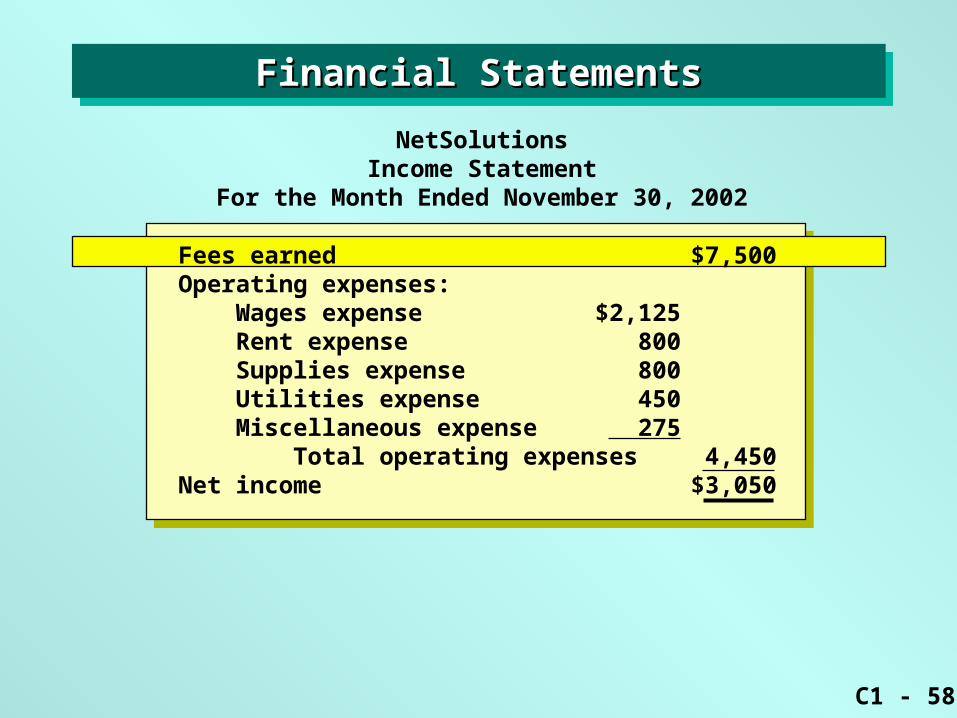

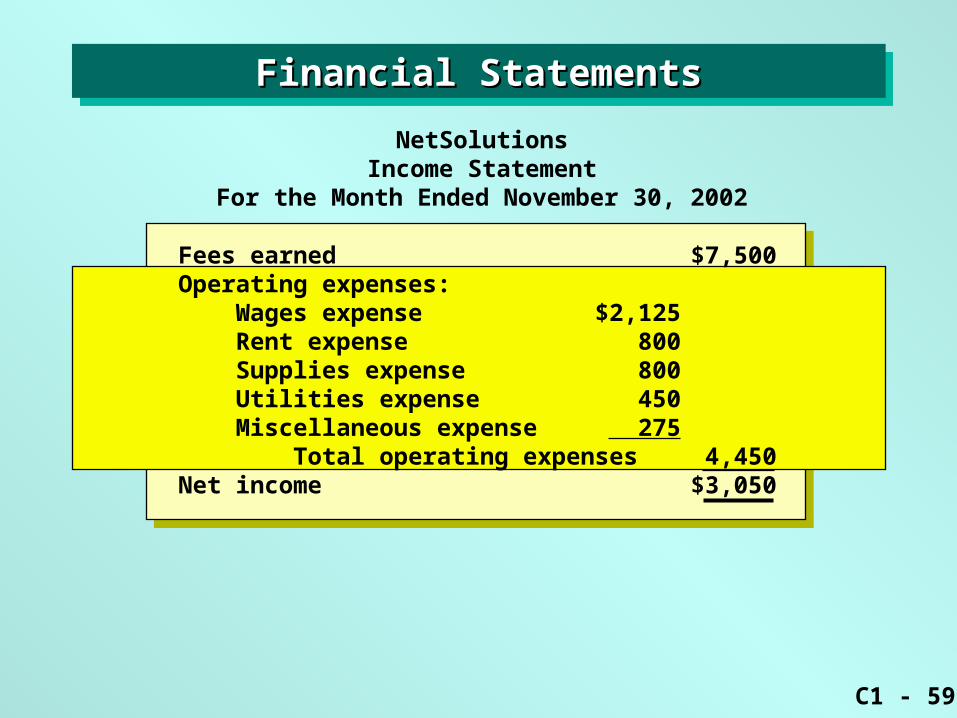

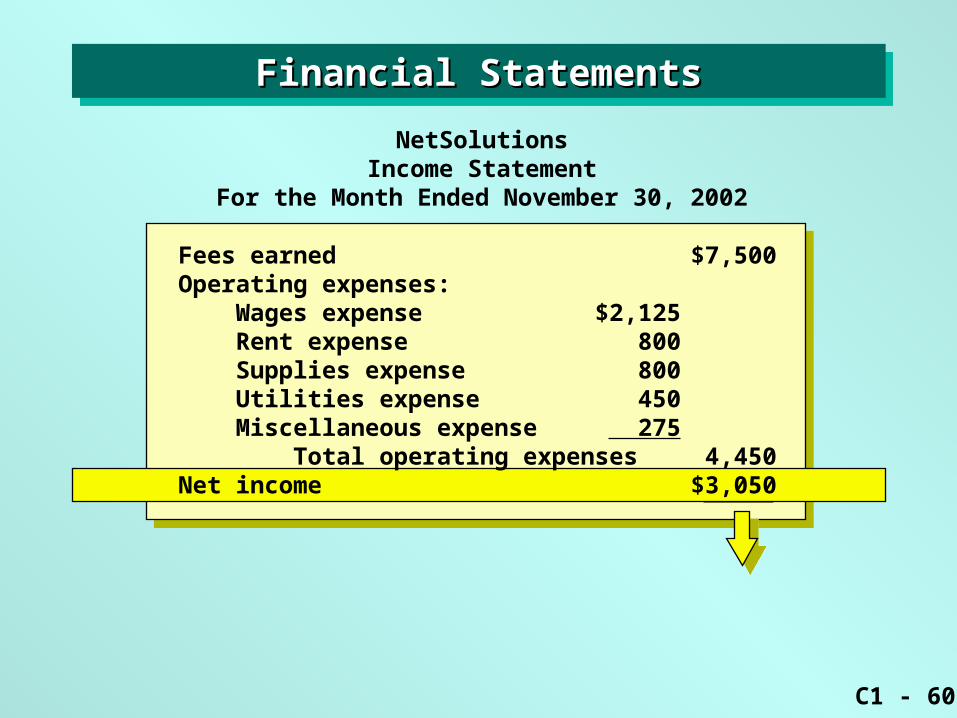

Financial StatementsFinancial StatementsFinancial StatementsFinancial Statements

NetSolutionsIncome Statement

For the Month Ended November 30, 2002

Fees earned $7,500Operating expenses: Wages expense $2,125 Rent expense 800 Supplies expense 800 Utilities expense 450 Miscellaneous expense 275 Total operating expenses 4,450Net income $3,050

C1 - 19

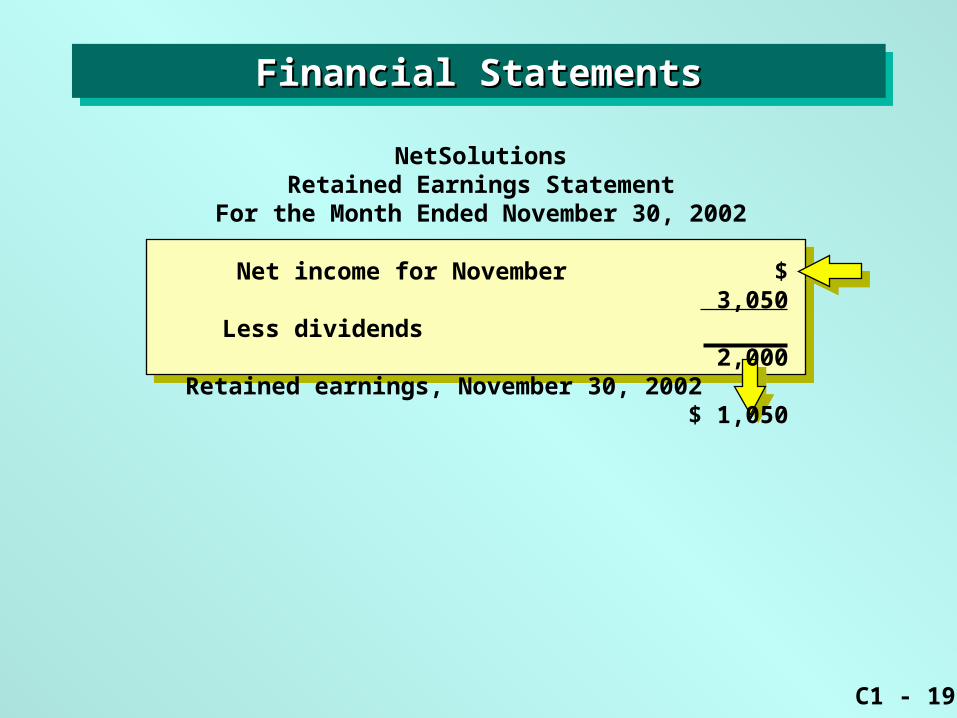

NetSolutionsRetained Earnings Statement

For the Month Ended November 30, 2002

Financial StatementsFinancial StatementsFinancial StatementsFinancial Statements

Net income for November $ 3,050Less dividends 2,000Retained earnings, November 30, 2002 $ 1,050

C1 - 20

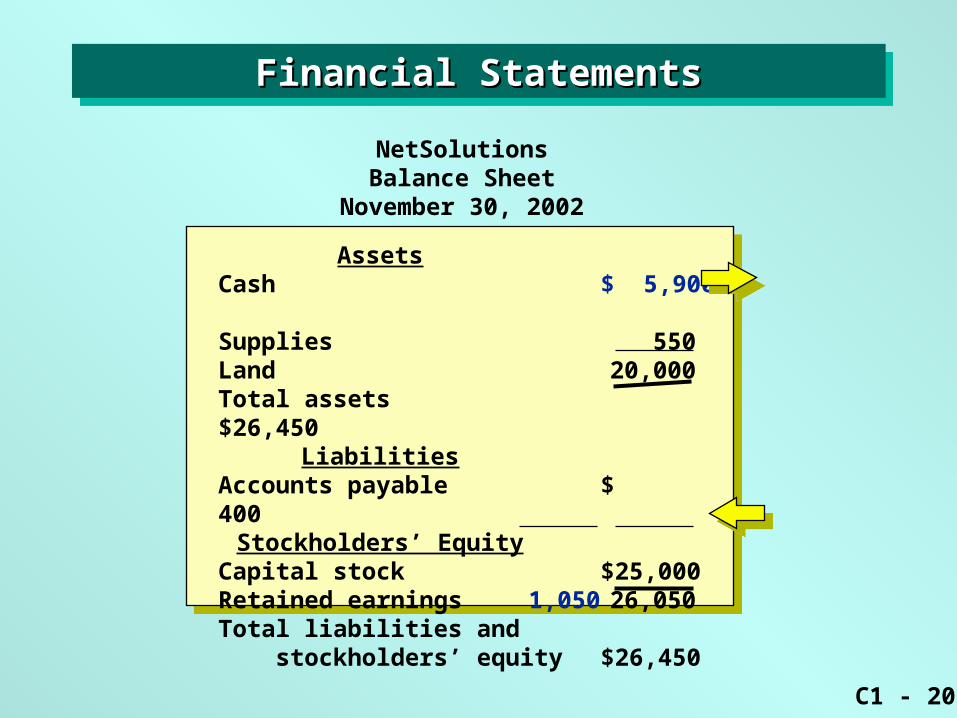

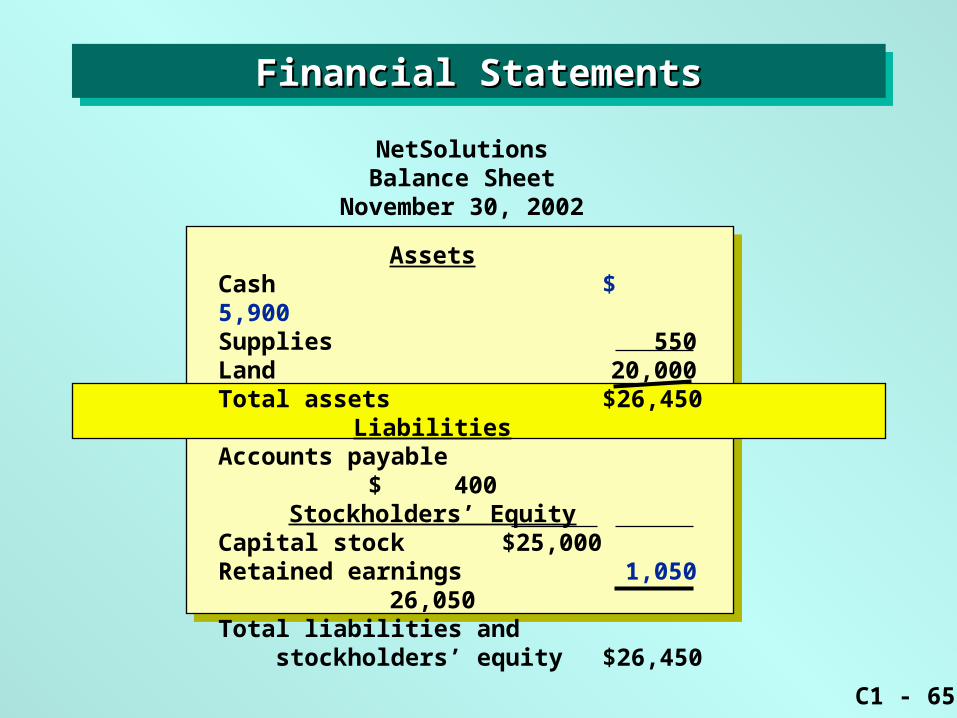

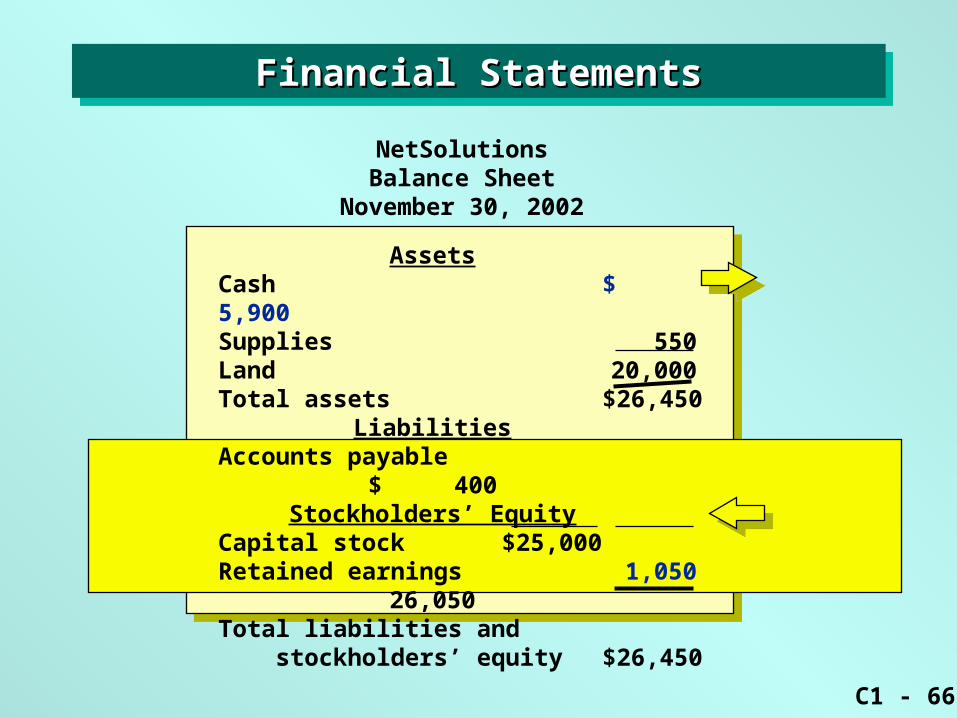

NetSolutionsBalance Sheet

November 30, 2002

AssetsCash $ 5,900Supplies 550Land 20,000Total assets $26,450

LiabilitiesAccounts payable $ 400

Stockholders’ EquityCapital stock $25,000Retained earnings 1,050 26,050Total liabilities and stockholders’ equity $26,450

Financial StatementsFinancial StatementsFinancial StatementsFinancial Statements

C1 - 21

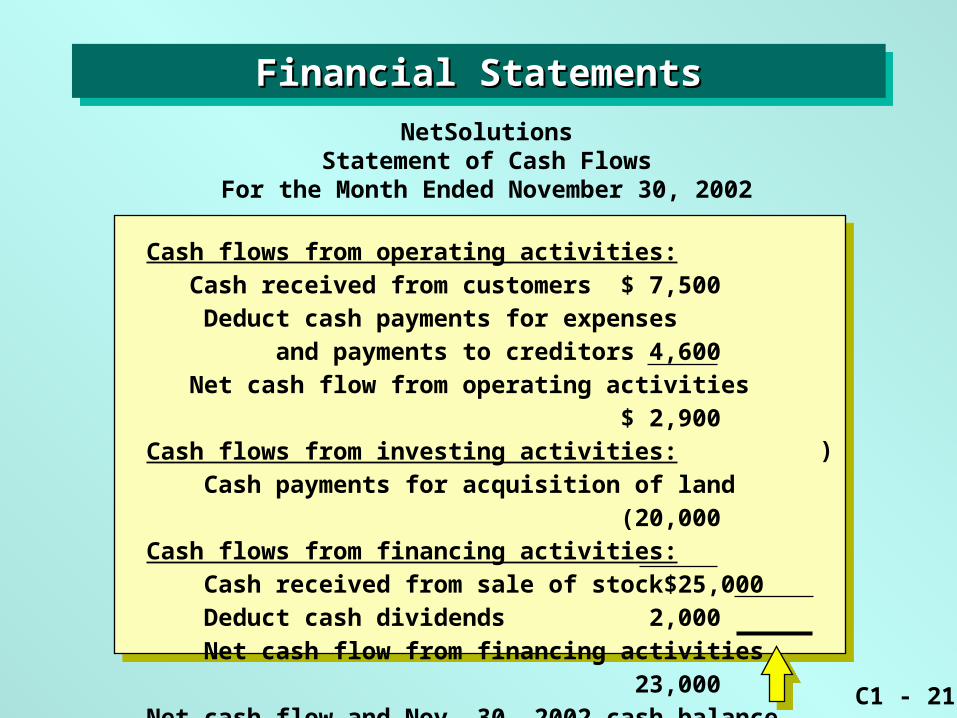

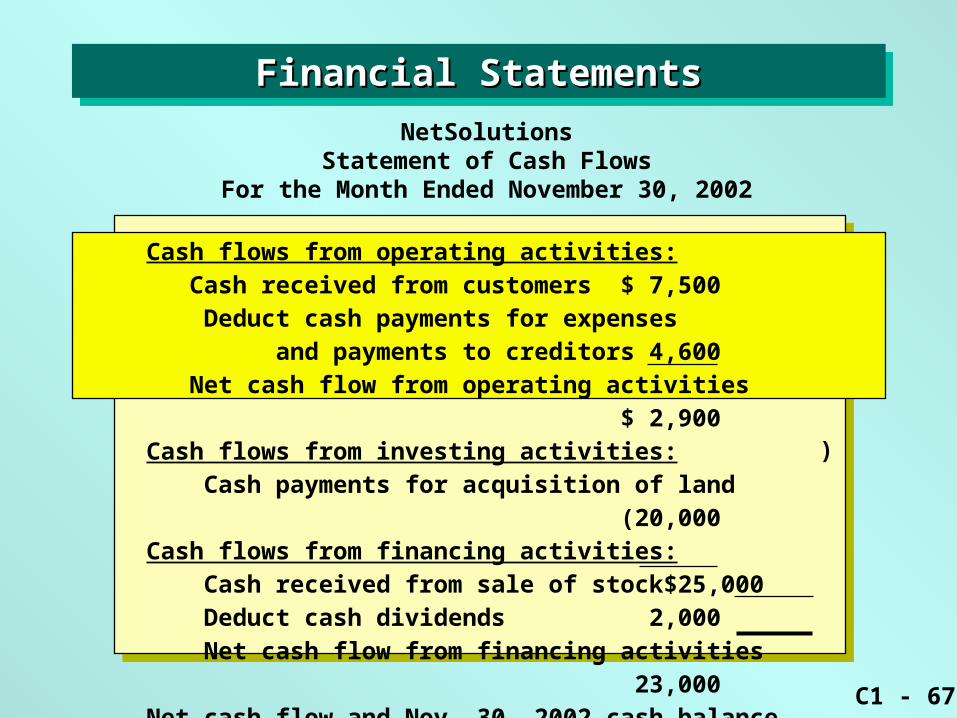

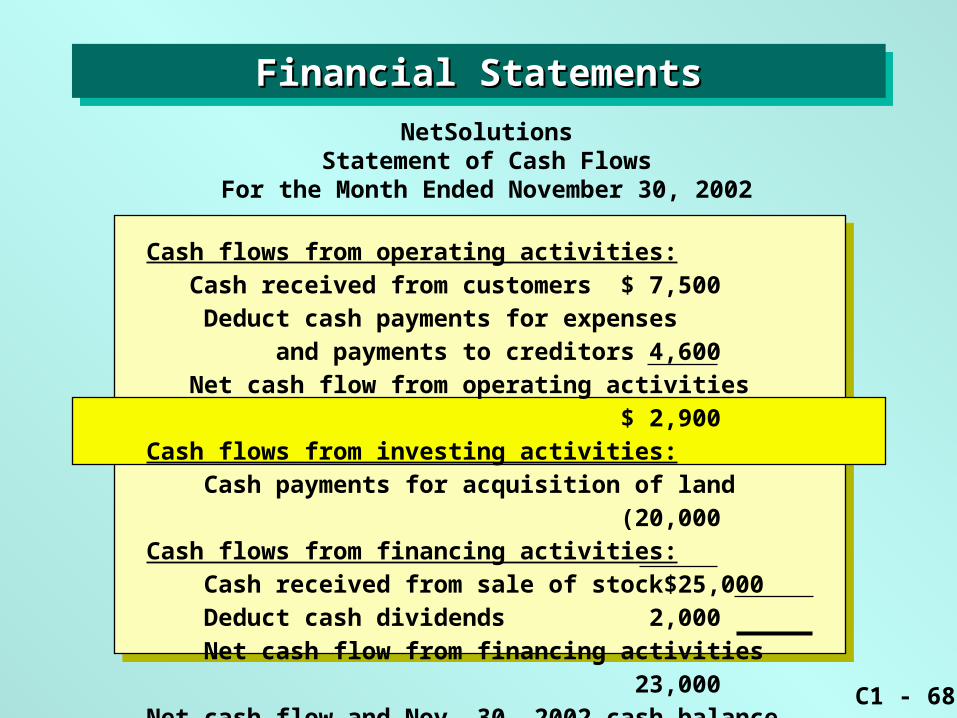

NetSolutionsStatement of Cash Flows

For the Month Ended November 30, 2002

Cash flows from operating activities: Cash received from customers $ 7,500 Deduct cash payments for expenses and payments to creditors 4,600 Net cash flow from operating activities $ 2,900Cash flows from investing activities: Cash payments for acquisition of land (20,000Cash flows from financing activities: Cash received from sale of stock $25,000 Deduct cash dividends 2,000 Net cash flow from financing activities 23,000Net cash flow and Nov. 30, 2002 cash balance $5,900

)

Financial StatementsFinancial StatementsFinancial StatementsFinancial Statements

C1 - 22

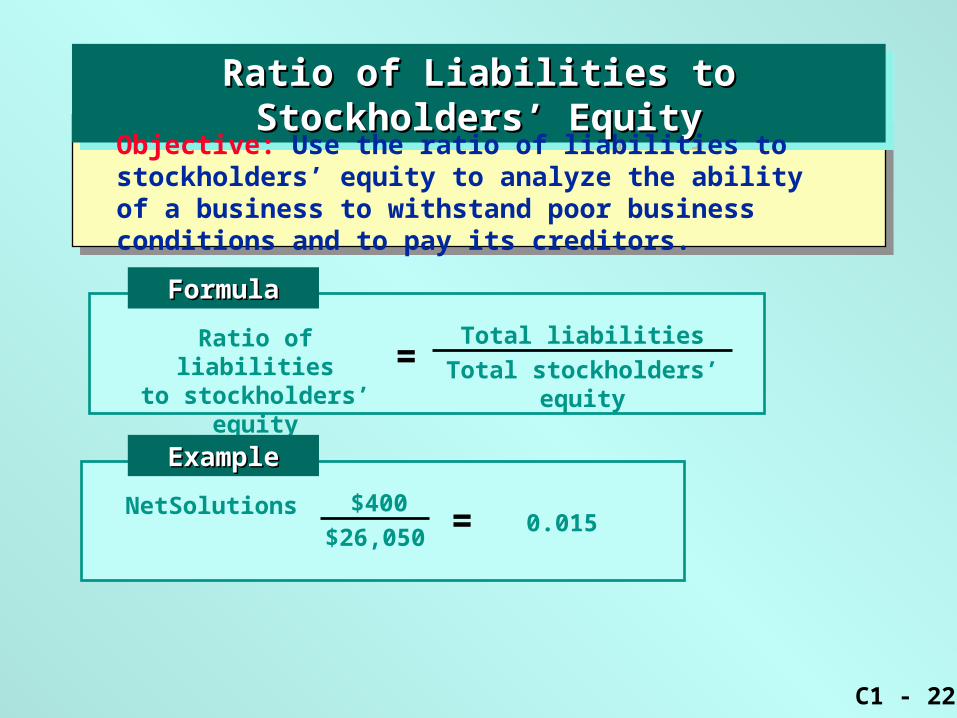

Ratio of Liabilities to Stockholders’ EquityRatio of Liabilities to Stockholders’ EquityRatio of Liabilities to Stockholders’ EquityRatio of Liabilities to Stockholders’ Equity

Ratio of liabilitiesto stockholders’ equity =

FormulaFormula

Objective: Use the ratio of liabilities to stockholders’ equity to analyze the ability of a business to withstand poor business conditions and to pay its creditors.

Total liabilities

Total stockholders’ equity

NetSolutions =

ExampleExample

$400

$26,0500.015

C1 - 23

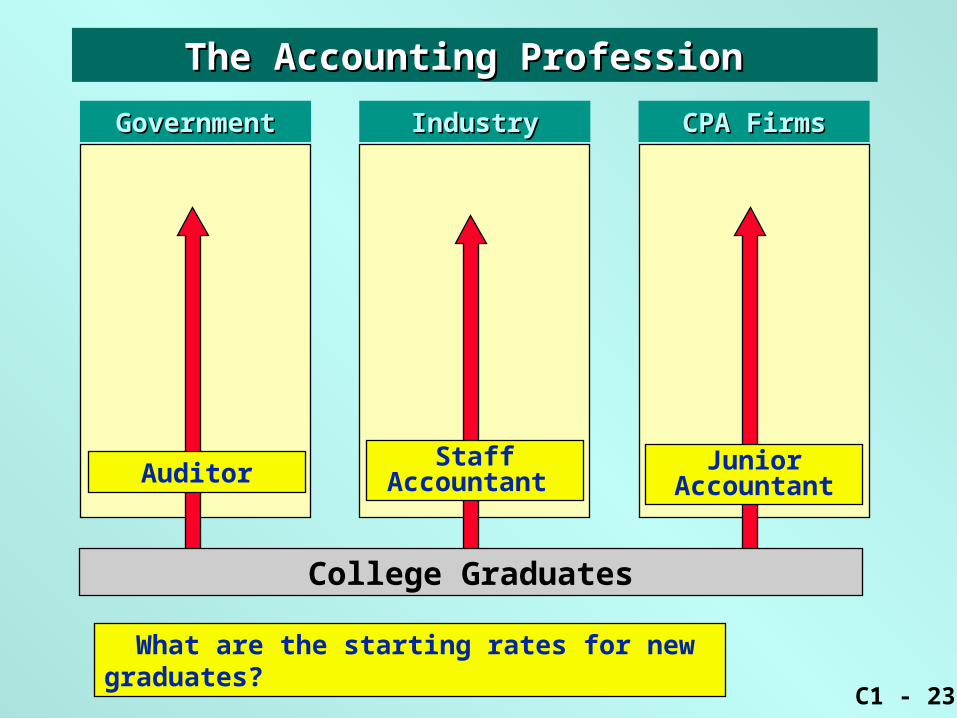

What are the starting rates for new graduates?

GovernmentGovernment IndustryIndustry CPA FirmsCPA Firms

College Graduates

The Accounting Profession The Accounting Profession

AuditorStaff

Accountant Junior

Accountant

C1 - 24

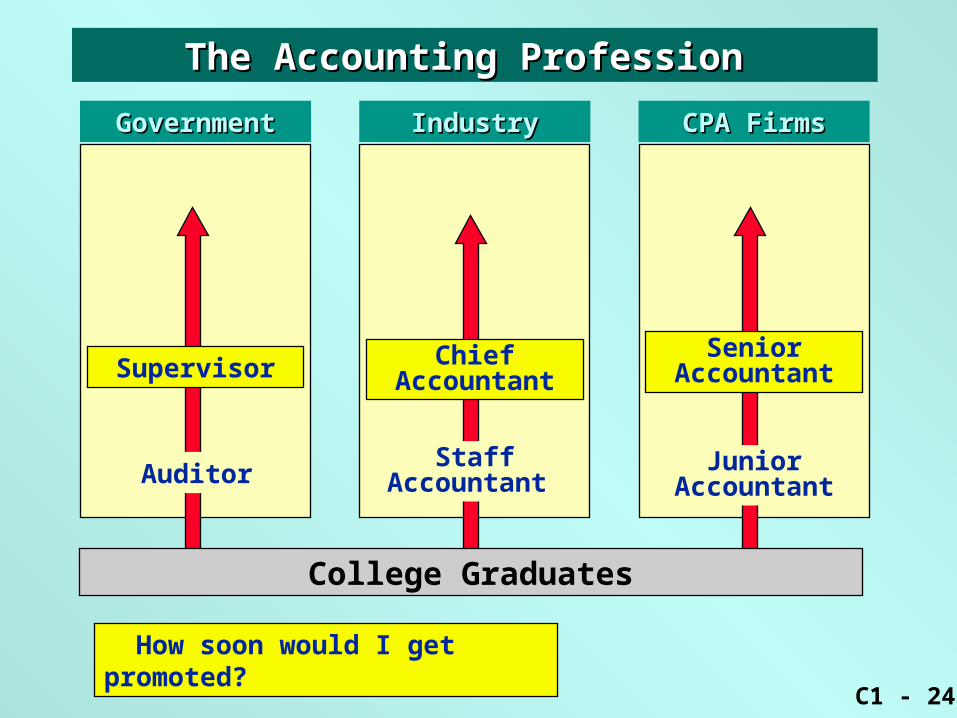

GovernmentGovernment IndustryIndustry CPA FirmsCPA Firms

StaffAccountant

JuniorAccountantAuditor

College Graduates

How soon would I get promoted?

The Accounting Profession The Accounting Profession

SeniorAccountantSupervisor Chief

Accountant

C1 - 25

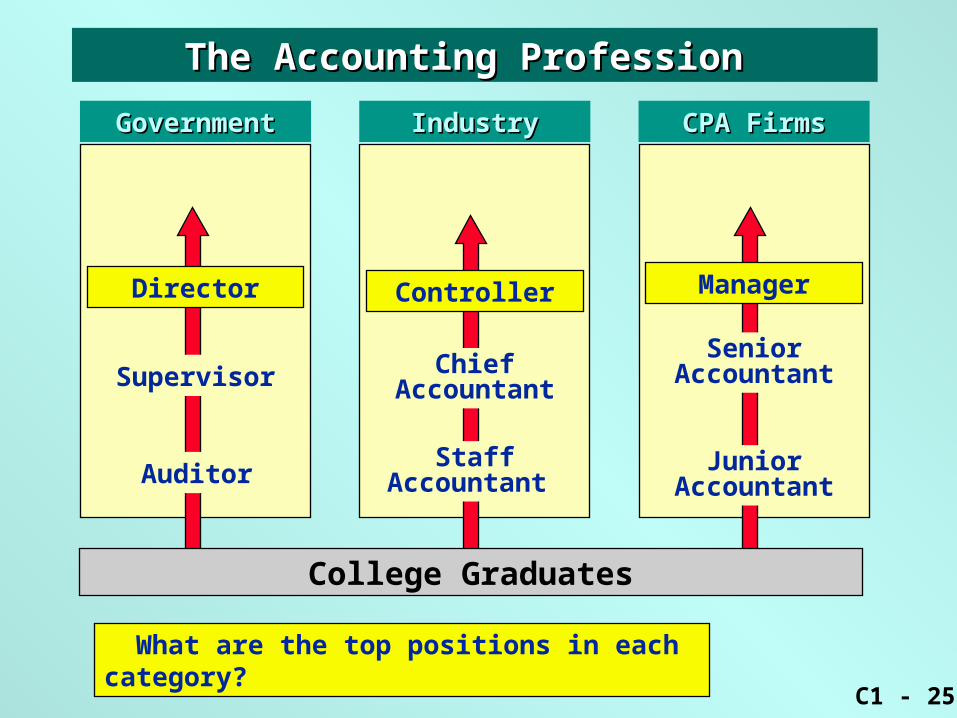

What are the top positions in each category?

GovernmentGovernment IndustryIndustry CPA FirmsCPA Firms

ChiefAccountant

StaffAccountant

SeniorAccountant

JuniorAccountant

Supervisor

Auditor

College Graduates

The Accounting Profession The Accounting Profession

Controller ManagerDirector

C1 - 26

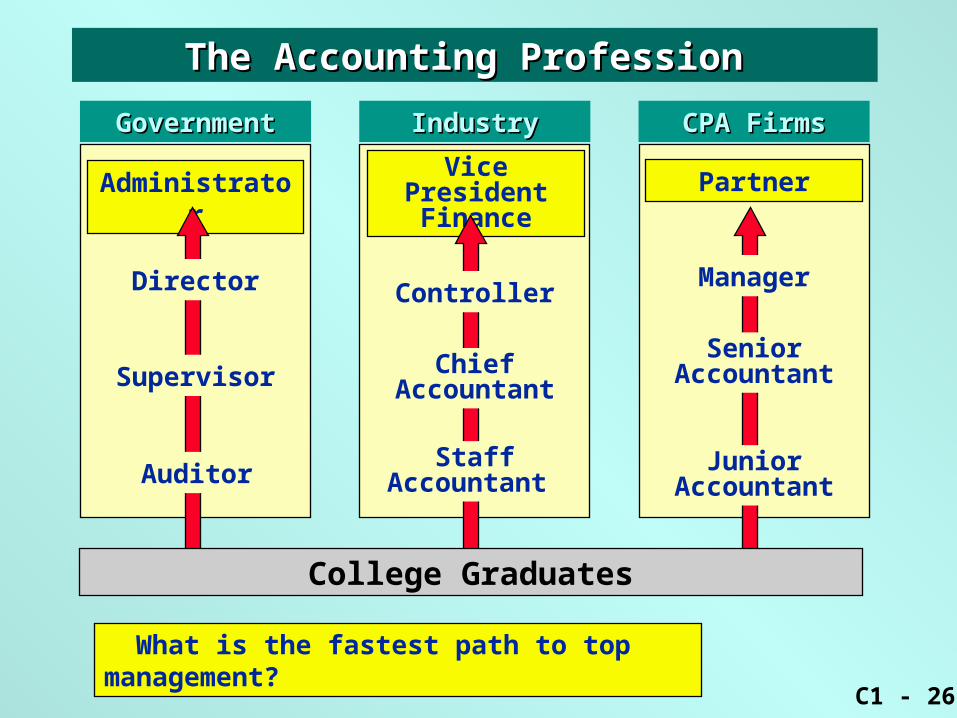

What is the fastest path to top management?

GovernmentGovernment

Administrator

IndustryIndustry

Vice PresidentFinance

CPA FirmsCPA Firms

ChiefAccountant

StaffAccountant

Controller

Partner

Manager

SeniorAccountant

JuniorAccountant

Director

Supervisor

Auditor

College Graduates

The Accounting Profession The Accounting Profession

C1 - 27

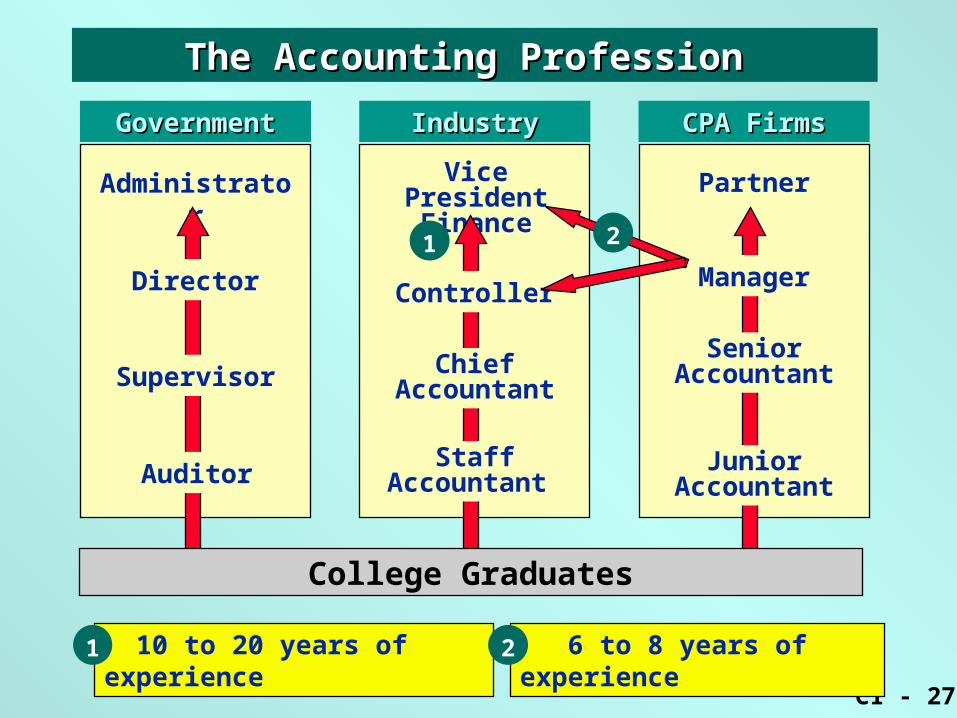

10 to 20 years of experience1

GovernmentGovernment

The Accounting Profession The Accounting Profession

Administrator

IndustryIndustry

Vice PresidentFinance

CPA FirmsCPA Firms

1

6 to 8 years of experience2

ChiefAccountant

StaffAccountant

Controller

Partner

Manager

SeniorAccountant

JuniorAccountant

2

Director

Supervisor

Auditor

College Graduates

C1 - 28

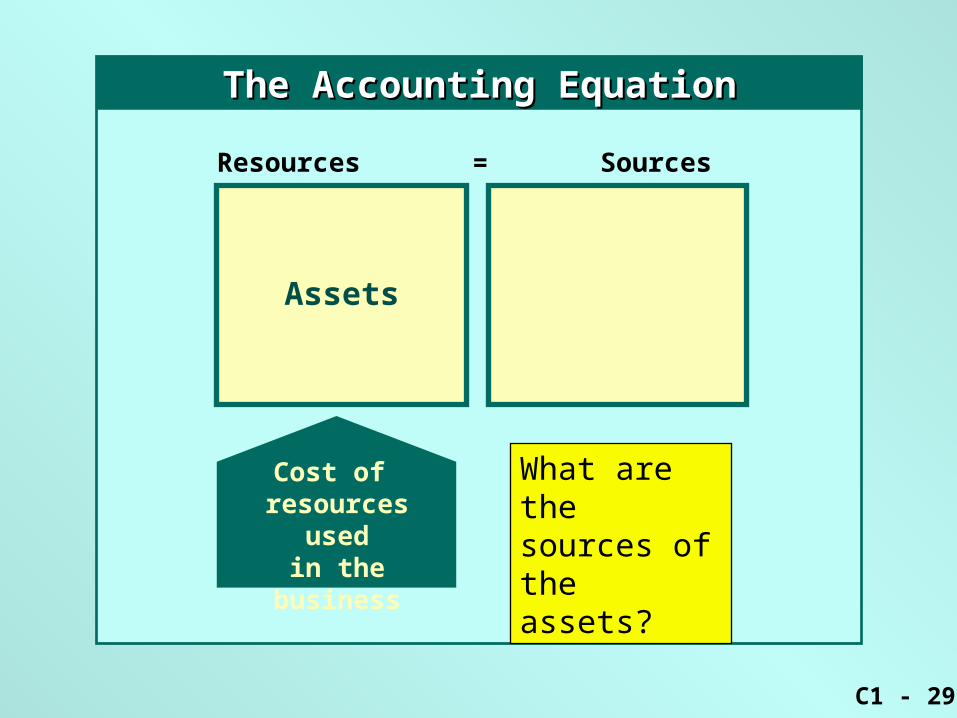

Resources

The Accounting EquationThe Accounting Equation

What are an organization’s resources called?

C1 - 29

Assets

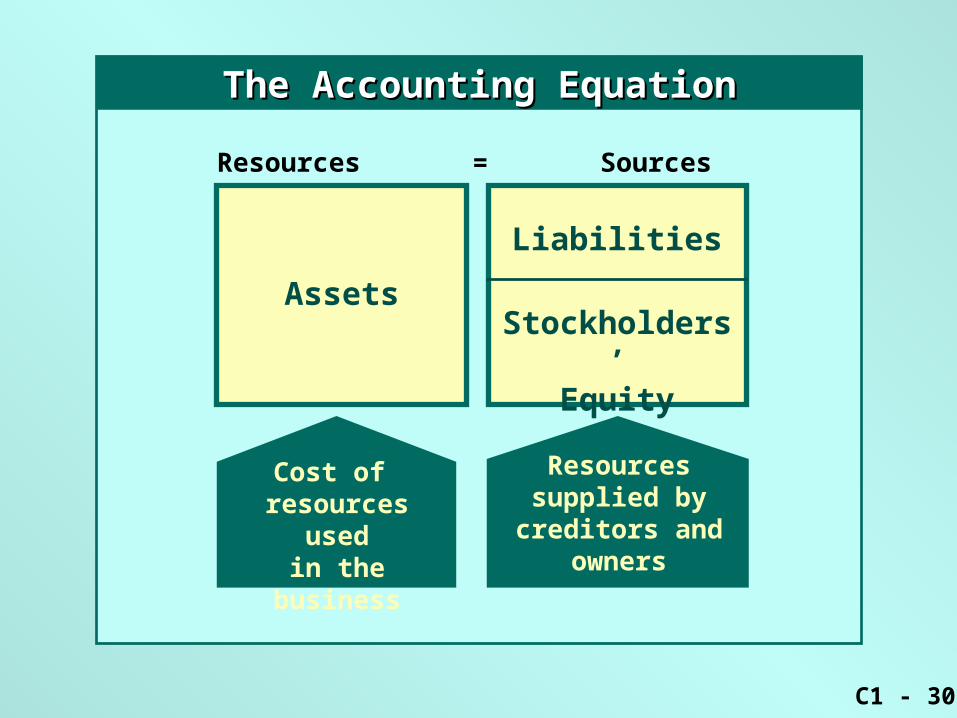

Resources = Sources

The Accounting EquationThe Accounting Equation

What are the sources of the assets?

Cost of resources usedin the business

C1 - 30

Assets

Liabilities

Stockholders’Equity

Resources = Sources

Cost of resources usedin the business

Resources supplied by

creditors and owners

The Accounting EquationThe Accounting Equation

C1 - 31

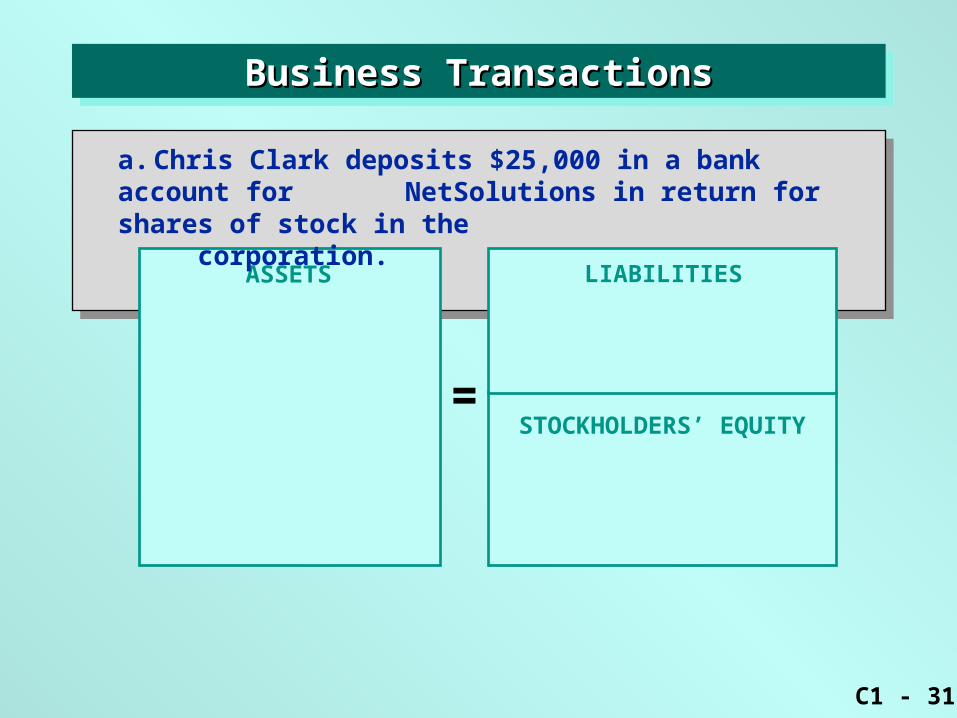

ASSETS

=

Business TransactionsBusiness TransactionsBusiness TransactionsBusiness Transactions

STOCKHOLDERS’ EQUITY

LIABILITIES

a. Chris Clark deposits $25,000 in a bank account for NetSolutions in return for shares of stock in the

corporation.

C1 - 32

ASSETS

=

Business TransactionsBusiness TransactionsBusiness TransactionsBusiness Transactions

Cash Cash 25,00025,000

LIABILITIES

a. Chris Clark deposits $25,000 in a bank account for NetSolutions in return for shares of stock in the

corporation.

STOCKHOLDERS’ EQUITY

C1 - 33

Business TransactionsBusiness TransactionsBusiness TransactionsBusiness Transactions

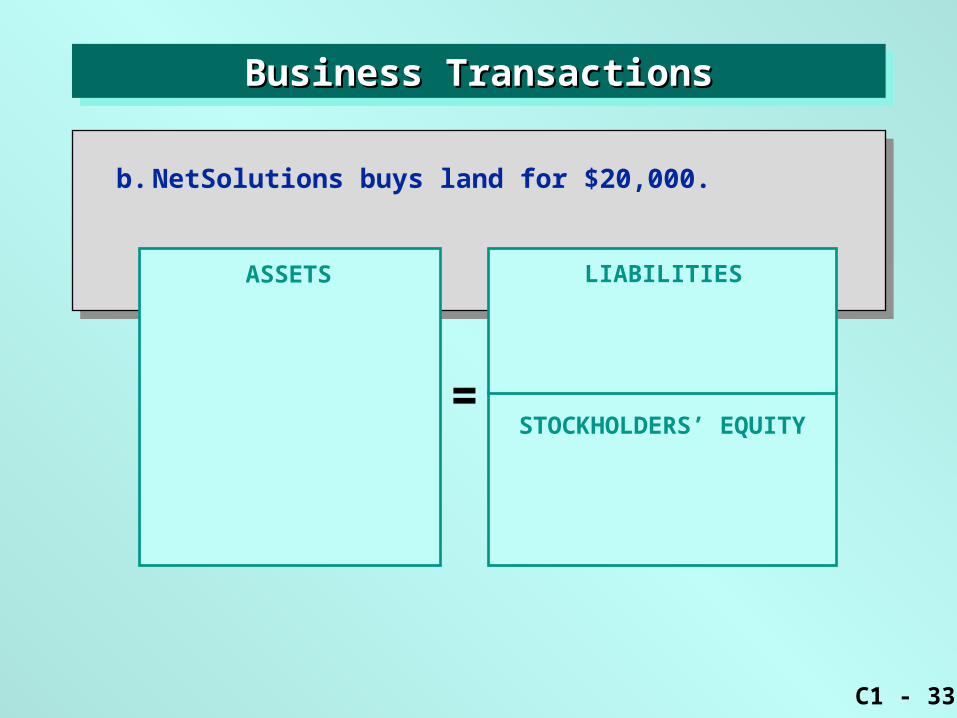

b. NetSolutions buys land for $20,000.

ASSETS

=

LIABILITIES

STOCKHOLDERS’ EQUITY

C1 - 34

Business TransactionsBusiness TransactionsBusiness TransactionsBusiness Transactions

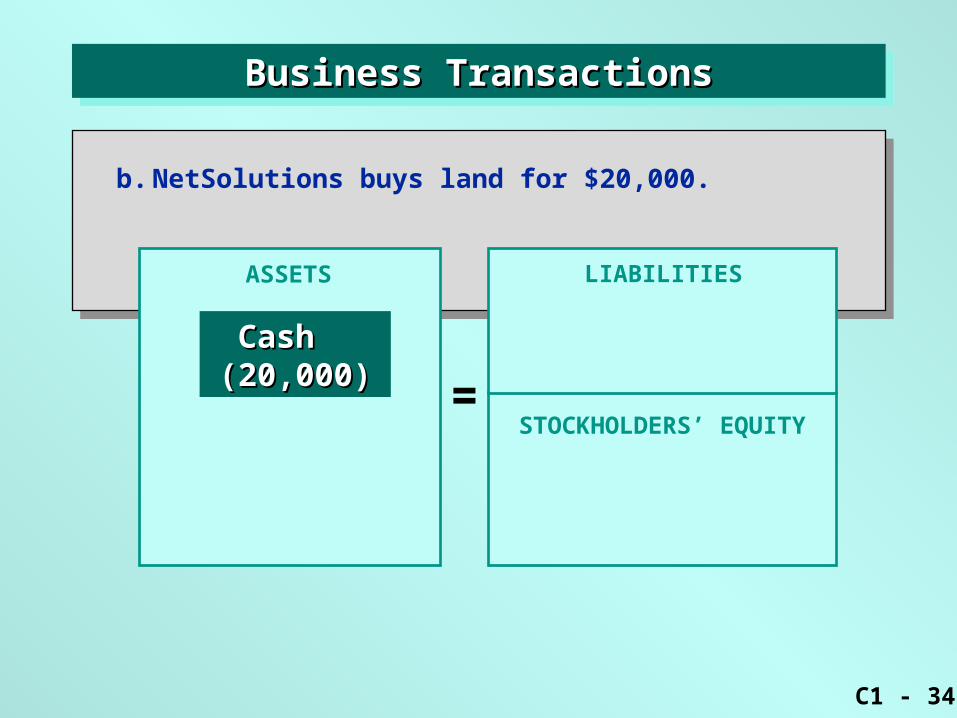

b. NetSolutions buys land for $20,000.

ASSETS

=

LIABILITIES

Cash Cash (20,000)(20,000)

STOCKHOLDERS’ EQUITY

C1 - 35

Business TransactionsBusiness TransactionsBusiness TransactionsBusiness Transactions

ASSETS

=

LIABILITIES

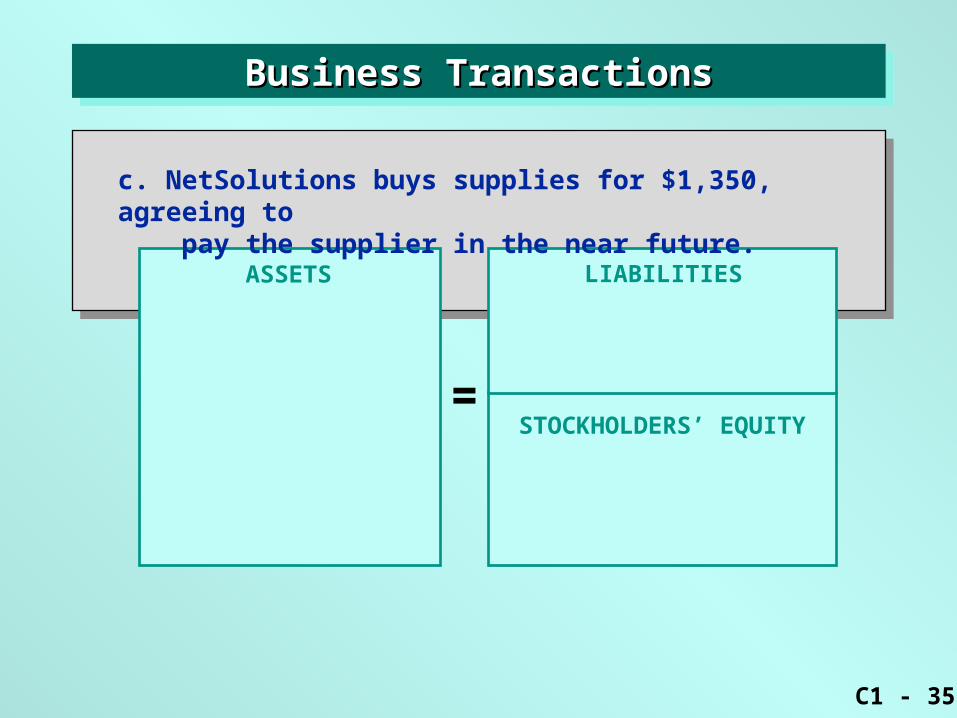

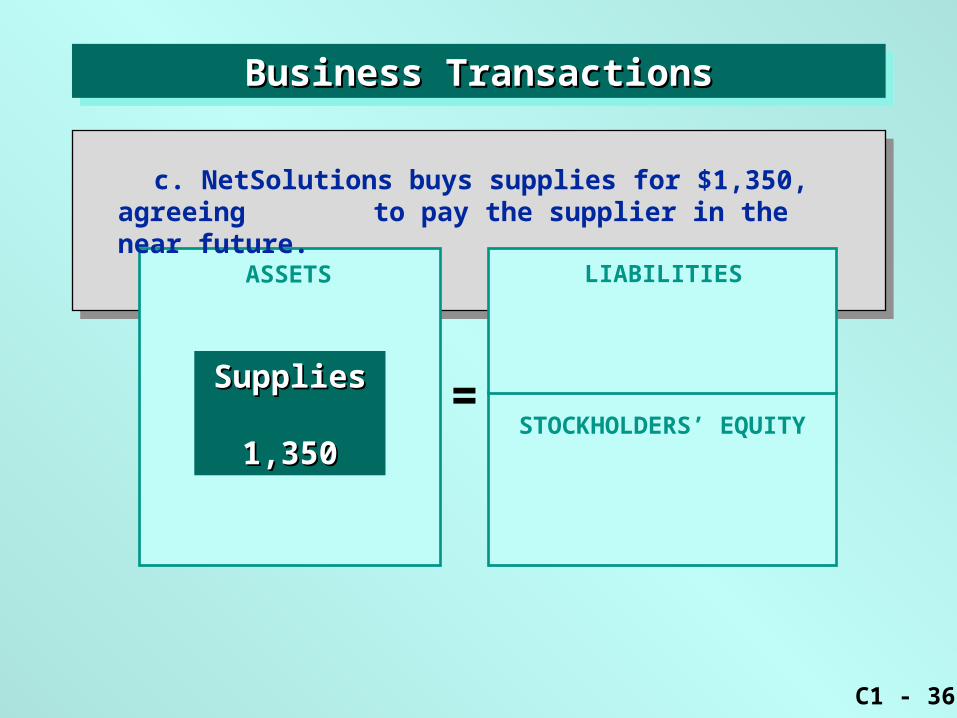

c. NetSolutions buys supplies for $1,350, agreeing to pay the supplier in the near future.

STOCKHOLDERS’ EQUITY

C1 - 36

Business TransactionsBusiness TransactionsBusiness TransactionsBusiness Transactions

ASSETS

=

LIABILITIES

Supplies Supplies 1,3501,350

c. NetSolutions buys supplies for $1,350, agreeing to pay the supplier in the near future.

STOCKHOLDERS’ EQUITY

C1 - 37

Business TransactionsBusiness TransactionsBusiness TransactionsBusiness Transactions

ASSETS

=

LIABILITIES

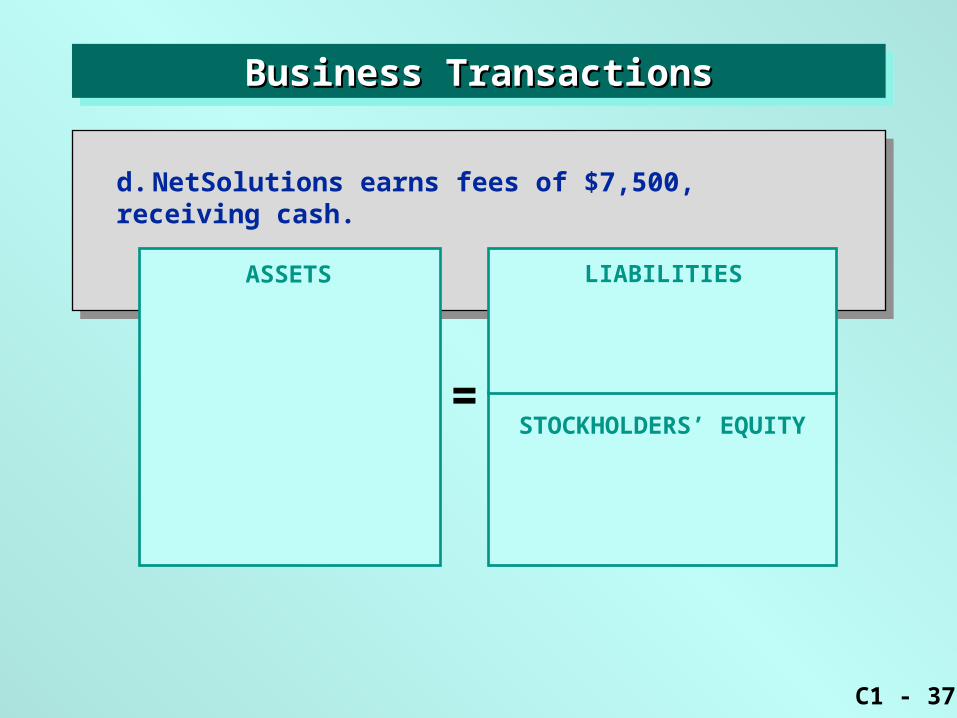

d. NetSolutions earns fees of $7,500, receiving cash.

STOCKHOLDERS’ EQUITY

C1 - 38

Business TransactionsBusiness TransactionsBusiness TransactionsBusiness Transactions

ASSETS

=

LIABILITIES

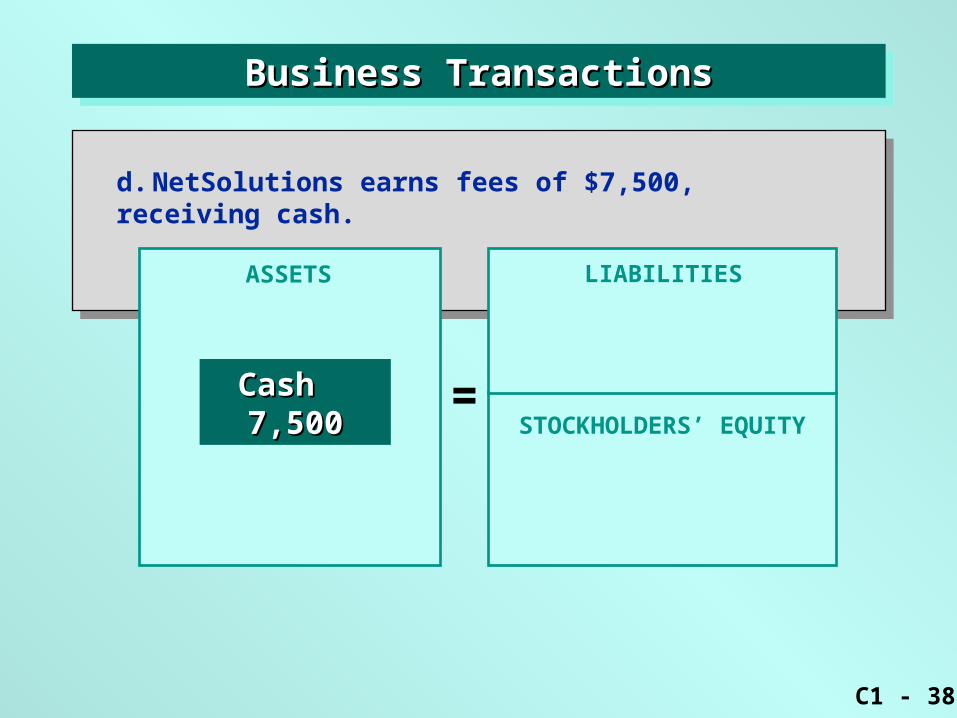

Cash Cash 7,5007,500

d. NetSolutions earns fees of $7,500, receiving cash.

STOCKHOLDERS’ EQUITY

C1 - 39

Business TransactionsBusiness TransactionsBusiness TransactionsBusiness Transactions

ASSETS

=

LIABILITIES

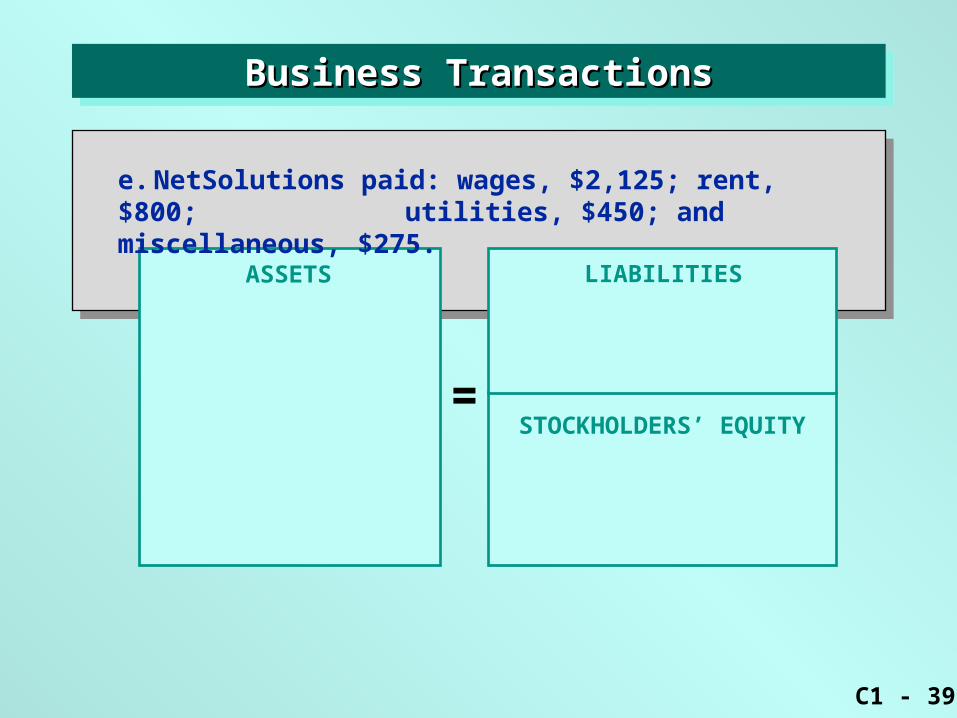

e. NetSolutions paid: wages, $2,125; rent, $800; utilities, $450; and miscellaneous, $275.

STOCKHOLDERS’ EQUITY

C1 - 40

Business TransactionsBusiness TransactionsBusiness TransactionsBusiness Transactions

ASSETS

=

LIABILITIES

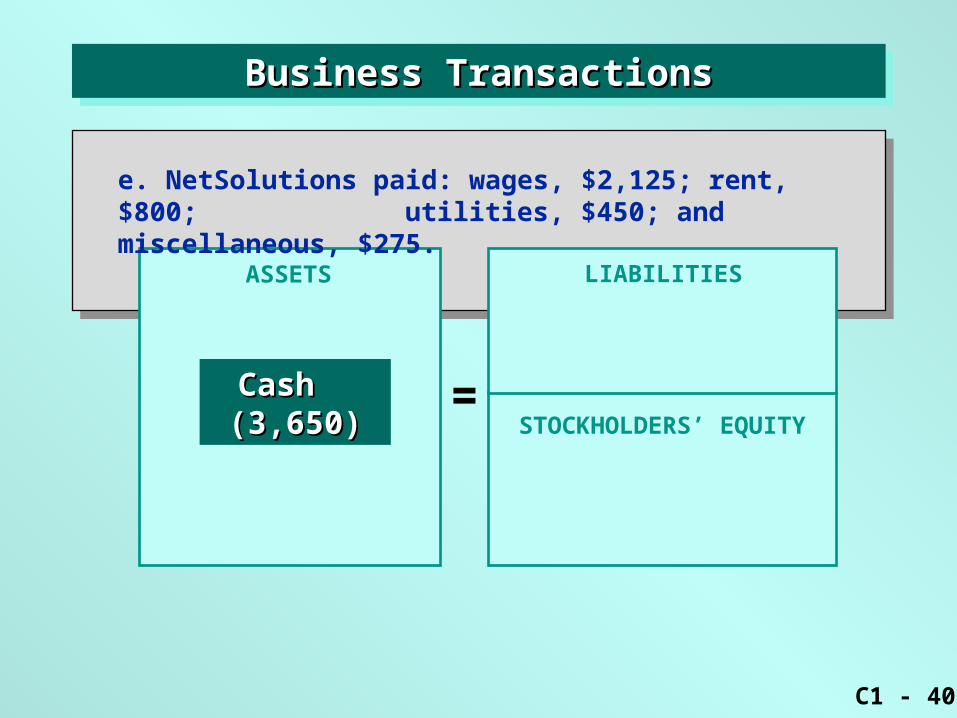

Cash Cash (3,650)(3,650)

e. NetSolutions paid: wages, $2,125; rent, $800; utilities, $450; and miscellaneous, $275.

STOCKHOLDERS’ EQUITY

C1 - 41

Business TransactionsBusiness TransactionsBusiness TransactionsBusiness Transactions

ASSETS

=

LIABILITIES

f. NetSolutions pays $950 to creditors on account.

STOCKHOLDERS’ EQUITY

C1 - 42

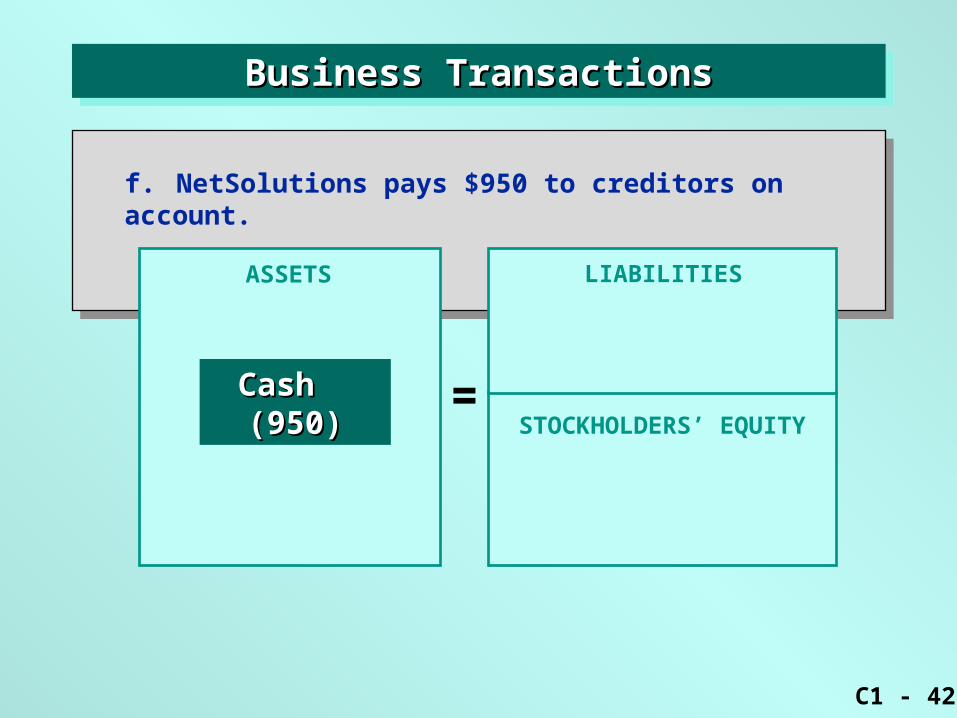

Business TransactionsBusiness TransactionsBusiness TransactionsBusiness Transactions

ASSETS

=

LIABILITIES

Cash Cash (950)(950)

f. NetSolutions pays $950 to creditors on account.

STOCKHOLDERS’ EQUITY

C1 - 43

Business TransactionsBusiness TransactionsBusiness TransactionsBusiness Transactions

ASSETS

=

LIABILITIES

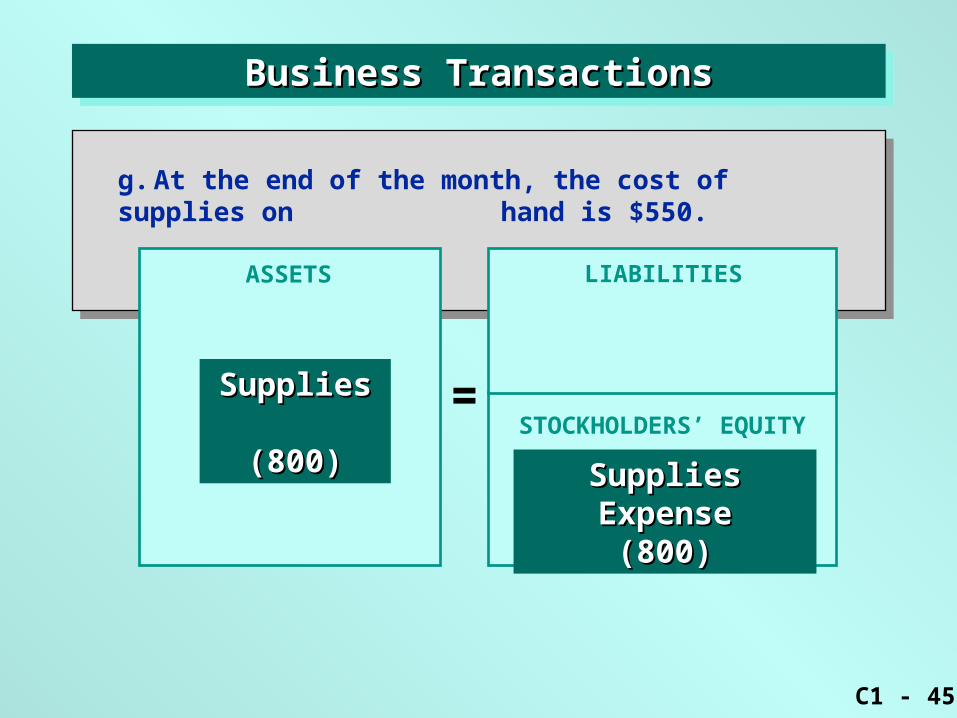

g. At the end of the month, the cost of supplies on hand is $550.

STOCKHOLDERS’ EQUITY

C1 - 44

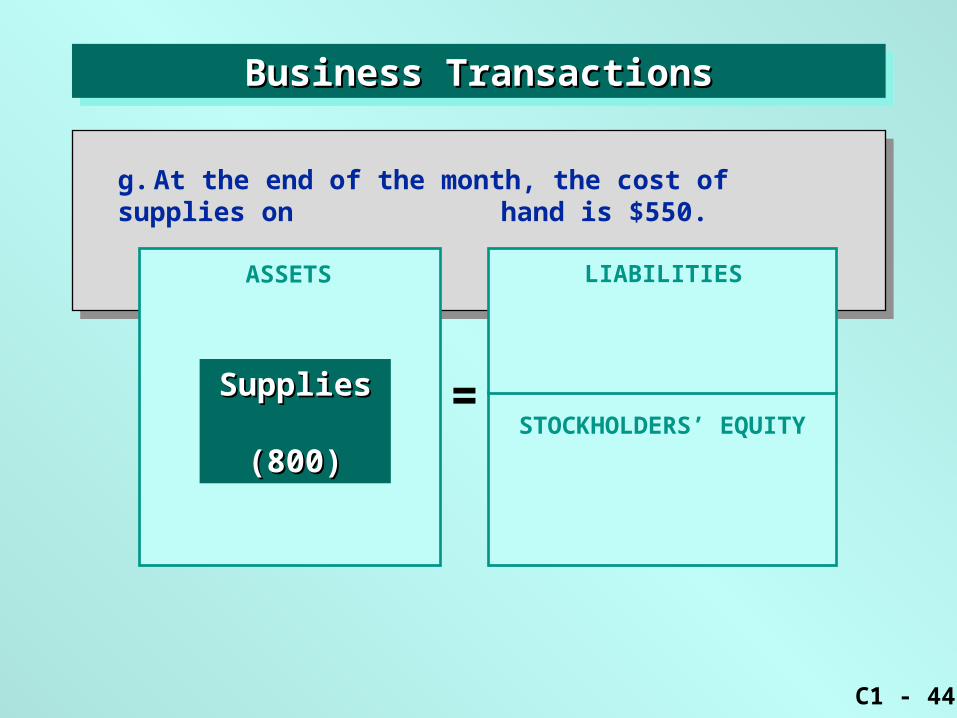

Business TransactionsBusiness TransactionsBusiness TransactionsBusiness Transactions

ASSETS

=

LIABILITIES

Supplies Supplies (800)(800)

g. At the end of the month, the cost of supplies on hand is $550.

STOCKHOLDERS’ EQUITY

C1 - 45

Business TransactionsBusiness TransactionsBusiness TransactionsBusiness Transactions

ASSETS

=

LIABILITIES

Supplies Supplies (800)(800)

Supplies ExpenseSupplies Expense(800)(800)

g. At the end of the month, the cost of supplies on hand is $550.

STOCKHOLDERS’ EQUITY

C1 - 46

Business TransactionsBusiness TransactionsBusiness TransactionsBusiness Transactions

ASSETS

=

LIABILITIES

h. NetSolutions pays $2,000 to stockholders (Chris Clark) as dividends.

STOCKHOLDERS’ EQUITY

C1 - 47

Business TransactionsBusiness TransactionsBusiness TransactionsBusiness Transactions

ASSETS

=

LIABILITIES

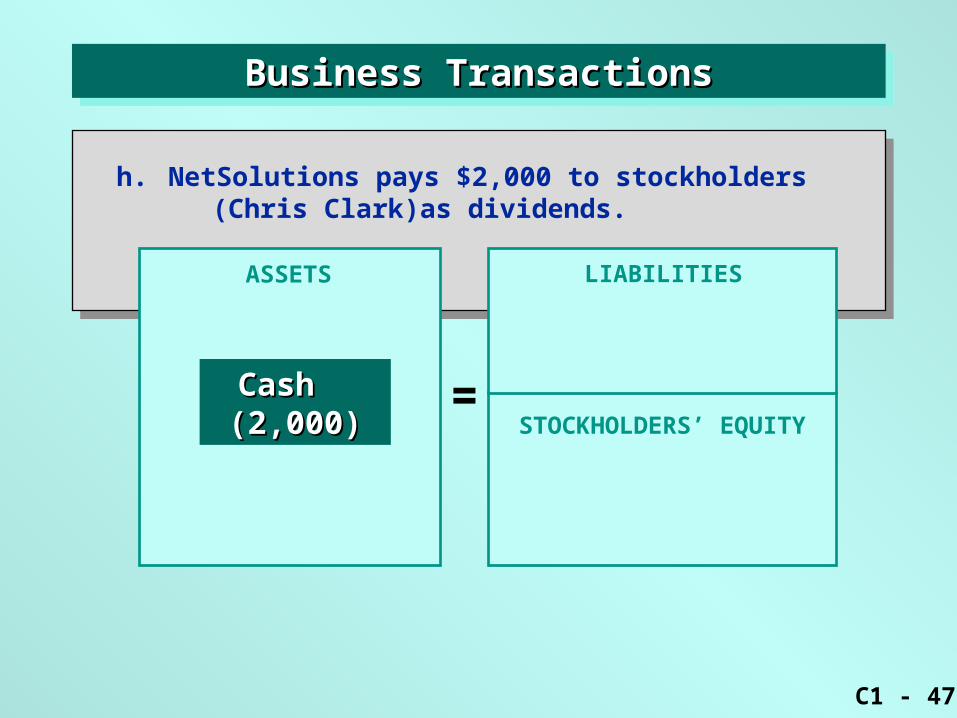

Cash Cash (2,000)(2,000)

h. NetSolutions pays $2,000 to stockholders (Chris Clark)as dividends.

STOCKHOLDERS’ EQUITY

C1 - 48

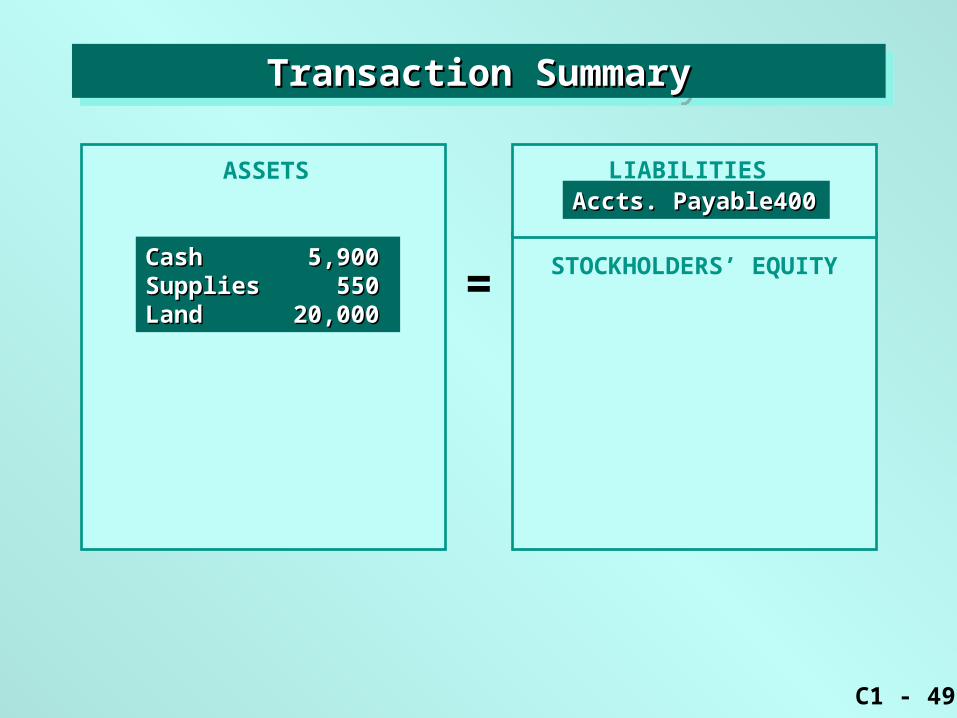

Transaction SummaryTransaction SummaryTransaction SummaryTransaction Summary

ASSETS

=

LIABILITIES

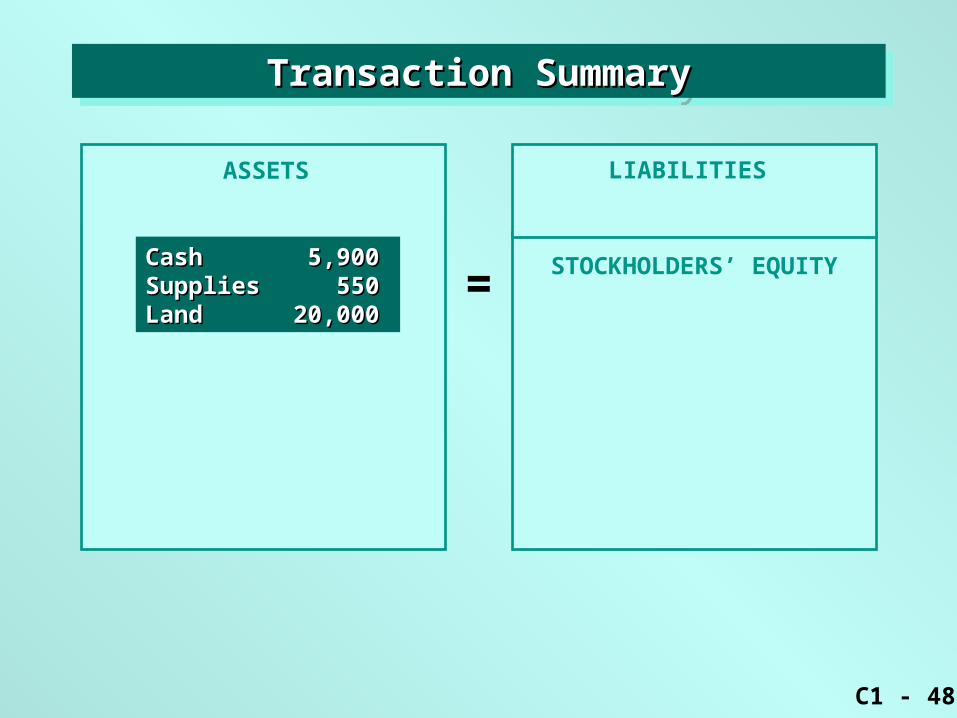

CashCash 5,9005,900SuppliesSupplies 550550LandLand 20,00020,000

STOCKHOLDERS’ EQUITY

C1 - 49

Transaction SummaryTransaction SummaryTransaction SummaryTransaction Summary

ASSETS

=

LIABILITIES

CashCash 5,9005,900SuppliesSupplies 550550LandLand 20,00020,000

Accts. PayableAccts. Payable 400400

STOCKHOLDERS’ EQUITY

C1 - 50

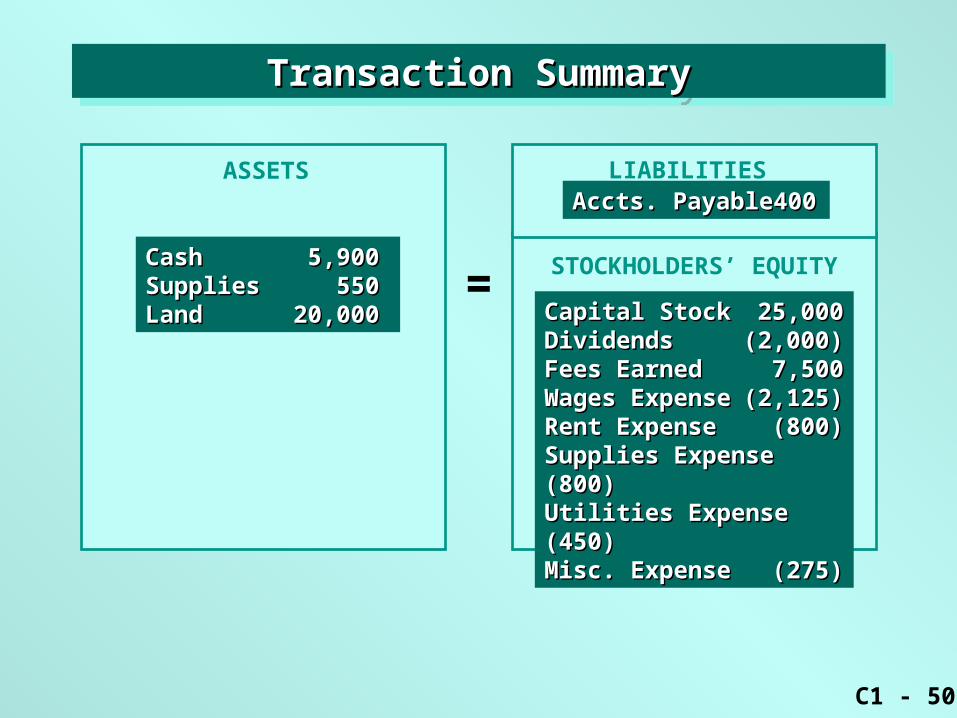

Transaction SummaryTransaction SummaryTransaction SummaryTransaction Summary

ASSETS

=

LIABILITIES

CashCash 5,9005,900SuppliesSupplies 550550LandLand 20,00020,000

Accts. PayableAccts. Payable 400400

Capital StockCapital Stock 25,00025,000DividendsDividends (2,000)(2,000)Fees EarnedFees Earned 7,5007,500Wages ExpenseWages Expense (2,125)(2,125)Rent ExpenseRent Expense (800)(800)Supplies ExpenseSupplies Expense (800)(800)Utilities ExpenseUtilities Expense (450)(450)Misc. ExpenseMisc. Expense (275)(275)

STOCKHOLDERS’ EQUITY

C1 - 51

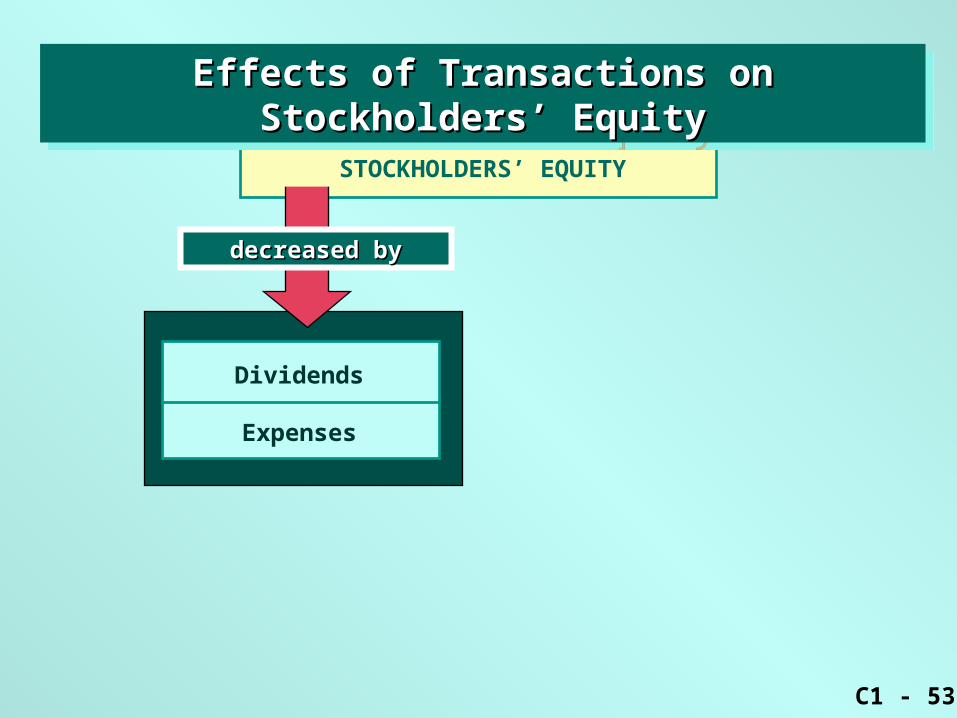

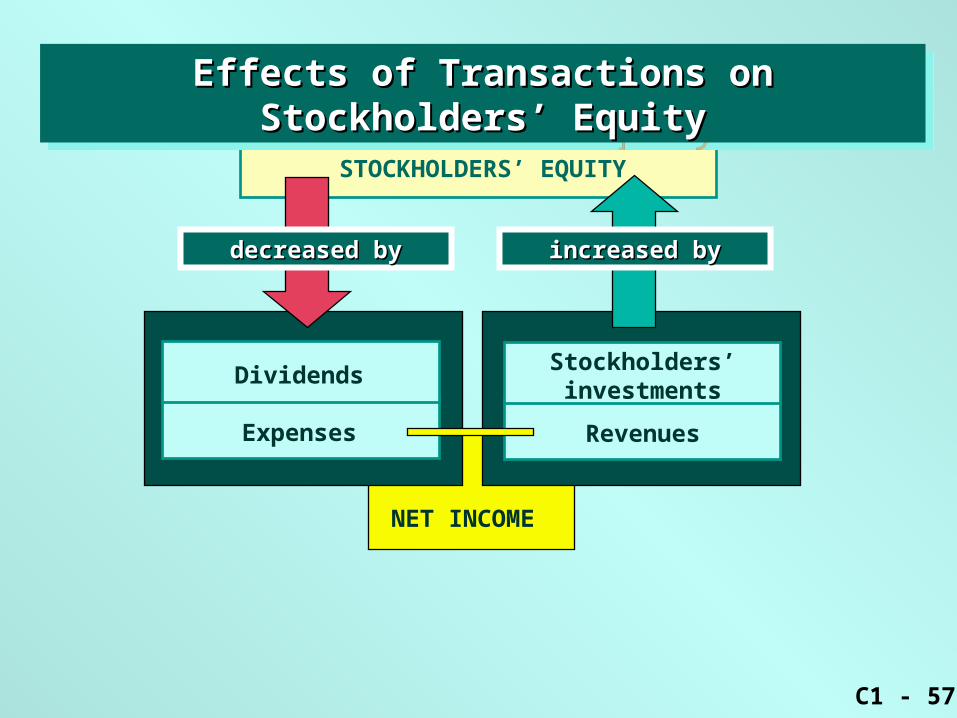

STOCKHOLDERS’ EQUITY

Effects of Transactions on Stockholders’ EquityEffects of Transactions on Stockholders’ EquityEffects of Transactions on Stockholders’ EquityEffects of Transactions on Stockholders’ Equity

C1 - 52

decreased bydecreased by

STOCKHOLDERS’ EQUITY

Effects of Transactions on Stockholders’ EquityEffects of Transactions on Stockholders’ EquityEffects of Transactions on Stockholders’ EquityEffects of Transactions on Stockholders’ Equity

C1 - 53

decreased bydecreased by

STOCKHOLDERS’ EQUITY

Dividends

Expenses

Effects of Transactions on Stockholders’ EquityEffects of Transactions on Stockholders’ EquityEffects of Transactions on Stockholders’ EquityEffects of Transactions on Stockholders’ Equity

C1 - 54

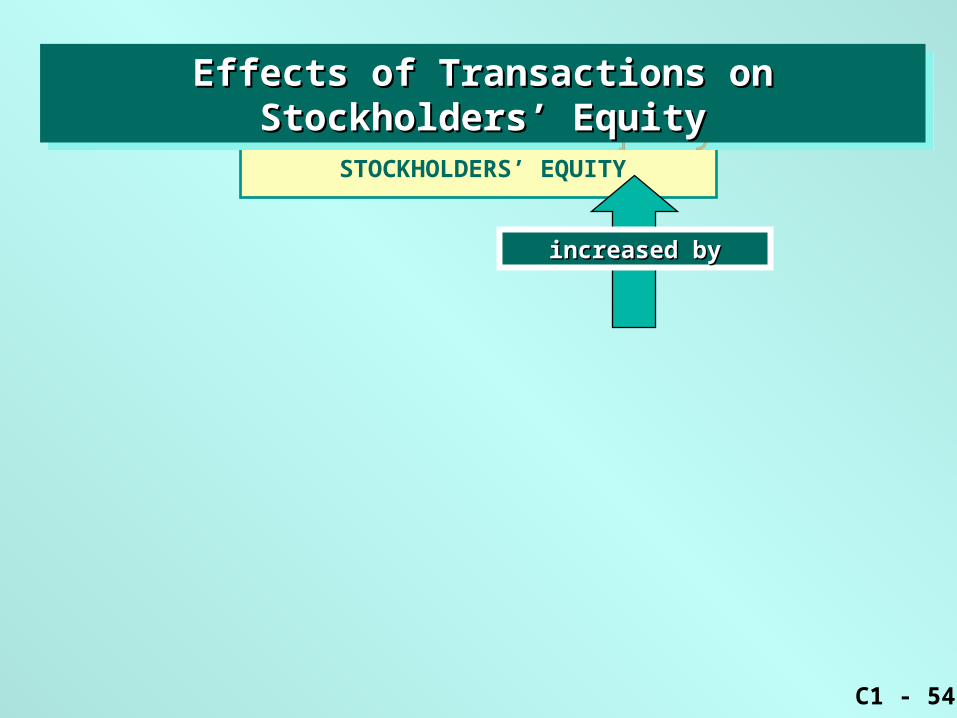

STOCKHOLDERS’ EQUITY

increased byincreased by

Effects of Transactions on Stockholders’ EquityEffects of Transactions on Stockholders’ EquityEffects of Transactions on Stockholders’ EquityEffects of Transactions on Stockholders’ Equity

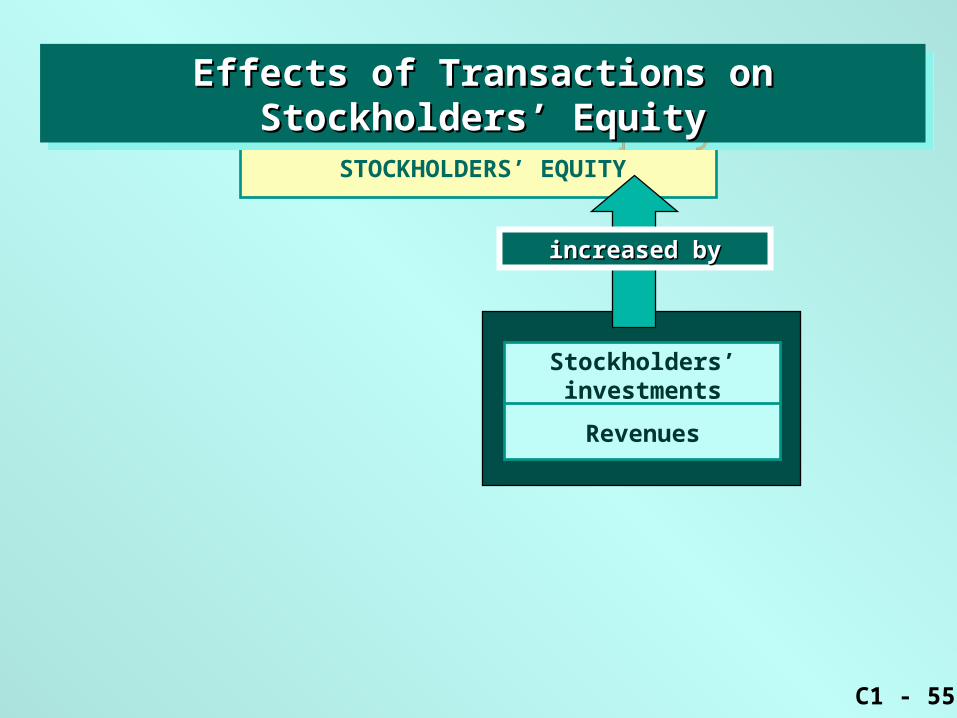

C1 - 55

STOCKHOLDERS’ EQUITY

increased byincreased by

Stockholders’ investments

Revenues

Effects of Transactions on Stockholders’ EquityEffects of Transactions on Stockholders’ EquityEffects of Transactions on Stockholders’ EquityEffects of Transactions on Stockholders’ Equity

C1 - 56

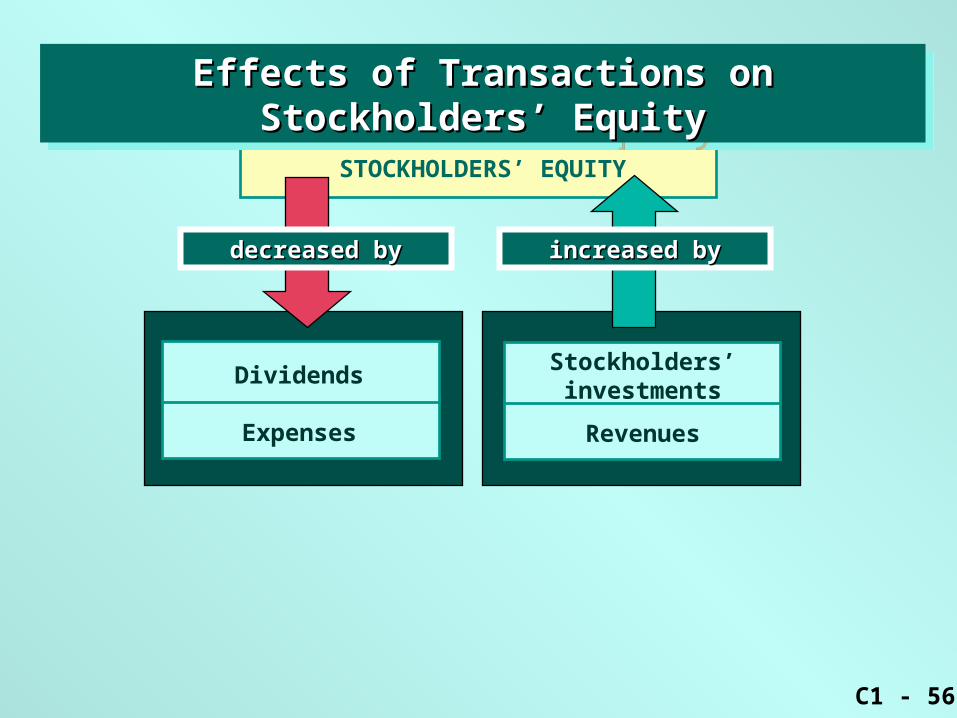

STOCKHOLDERS’ EQUITY

Dividends

Expenses

decreased bydecreased by increased byincreased by

Stockholders’ investments

Revenues

Effects of Transactions on Stockholders’ EquityEffects of Transactions on Stockholders’ EquityEffects of Transactions on Stockholders’ EquityEffects of Transactions on Stockholders’ Equity

C1 - 57

STOCKHOLDERS’ EQUITY

decreased bydecreased by increased byincreased by

NET INCOME

Dividends

Expenses

Stockholders’ investments

Revenues

Effects of Transactions on Stockholders’ EquityEffects of Transactions on Stockholders’ EquityEffects of Transactions on Stockholders’ EquityEffects of Transactions on Stockholders’ Equity

C1 - 58

Financial StatementsFinancial StatementsFinancial StatementsFinancial Statements

NetSolutionsIncome Statement

For the Month Ended November 30, 2002

Fees earned $7,500Operating expenses: Wages expense $2,125 Rent expense 800 Supplies expense 800 Utilities expense 450 Miscellaneous expense 275 Total operating expenses 4,450Net income $3,050

C1 - 59

Financial StatementsFinancial StatementsFinancial StatementsFinancial Statements

NetSolutionsIncome Statement

For the Month Ended November 30, 2002

Fees earned $7,500Operating expenses: Wages expense $2,125 Rent expense 800 Supplies expense 800 Utilities expense 450 Miscellaneous expense 275 Total operating expenses 4,450Net income $3,050

C1 - 60

Financial StatementsFinancial StatementsFinancial StatementsFinancial Statements

NetSolutionsIncome Statement

For the Month Ended November 30, 2002

Fees earned $7,500Operating expenses: Wages expense $2,125 Rent expense 800 Supplies expense 800 Utilities expense 450 Miscellaneous expense 275 Total operating expenses 4,450Net income $3,050

C1 - 61

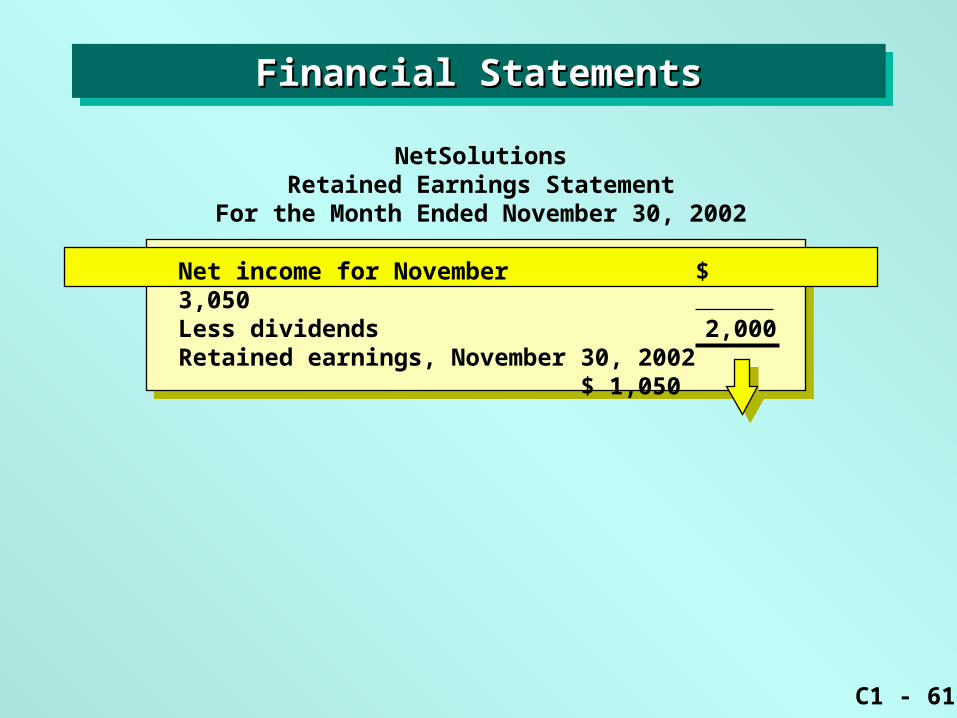

Net income for November $ 3,050Less dividends 2,000Retained earnings, November 30, 2002 $ 1,050

NetSolutionsRetained Earnings Statement

For the Month Ended November 30, 2002

Financial StatementsFinancial StatementsFinancial StatementsFinancial Statements

C1 - 62

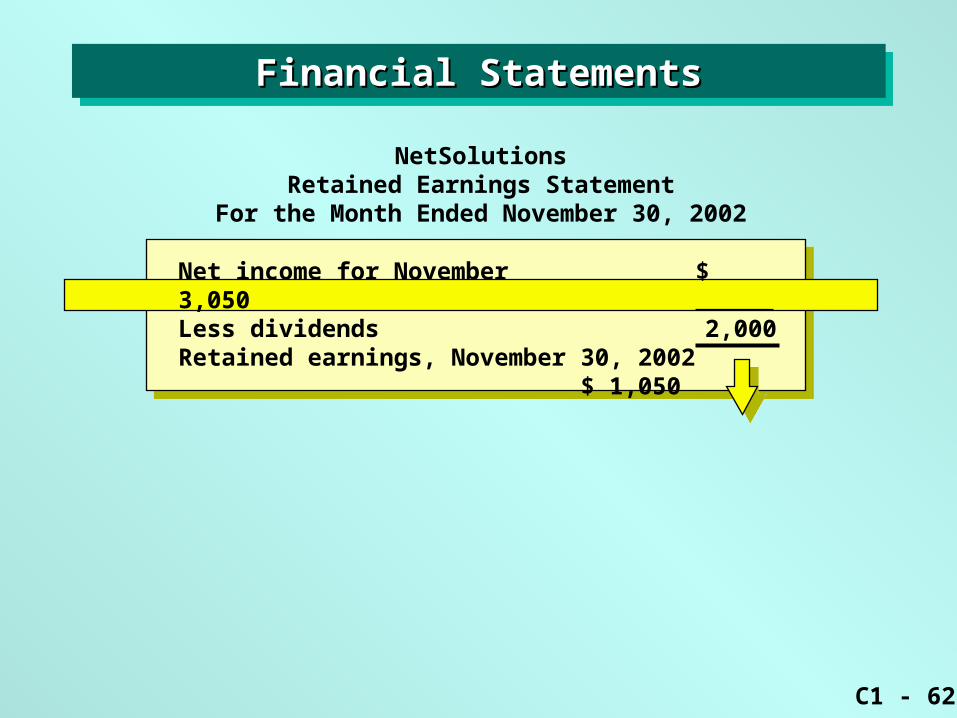

Net income for November $ 3,050Less dividends 2,000Retained earnings, November 30, 2002 $ 1,050

NetSolutionsRetained Earnings Statement

For the Month Ended November 30, 2002

Financial StatementsFinancial StatementsFinancial StatementsFinancial Statements

C1 - 63

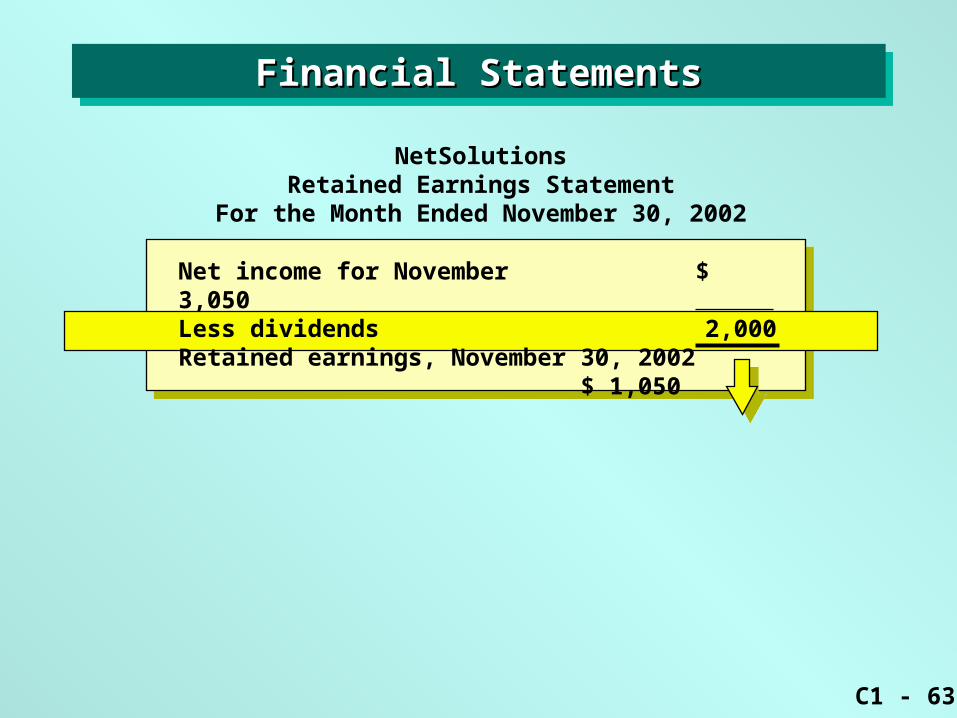

Net income for November $ 3,050Less dividends 2,000Retained earnings, November 30, 2002 $ 1,050

NetSolutionsRetained Earnings Statement

For the Month Ended November 30, 2002

Financial StatementsFinancial StatementsFinancial StatementsFinancial Statements

C1 - 64

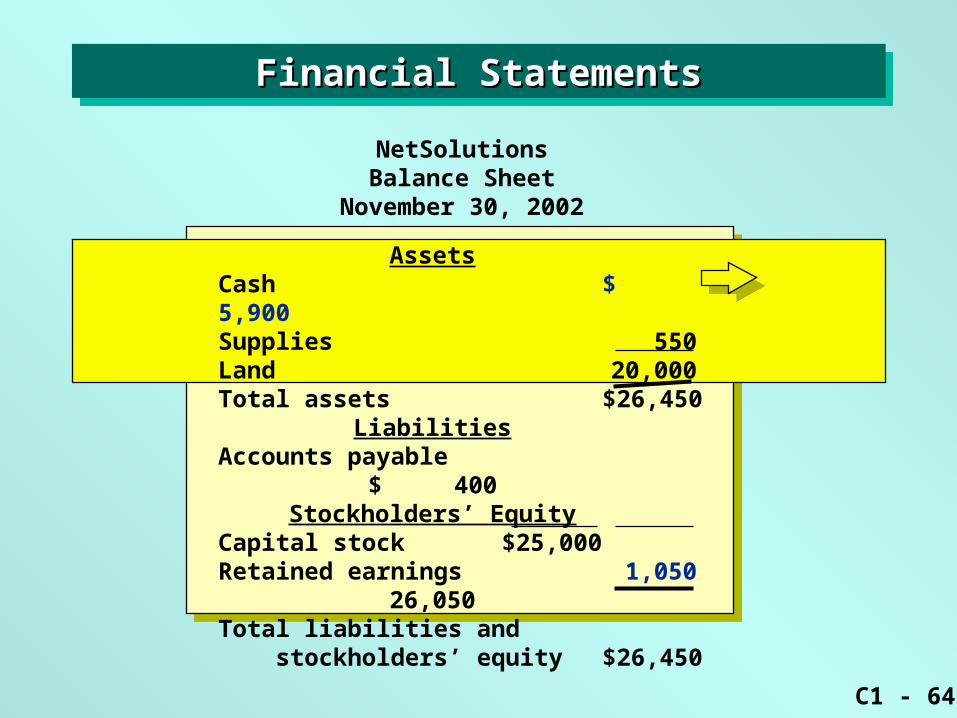

AssetsCash $ 5,900Supplies 550Land 20,000Total assets $26,450

LiabilitiesAccounts payable $ 400

Stockholders’ EquityCapital stock $25,000Retained earnings 1,050 26,050Total liabilities and stockholders’ equity $26,450

NetSolutionsBalance Sheet

November 30, 2002

Financial StatementsFinancial StatementsFinancial StatementsFinancial Statements

C1 - 65

AssetsCash $ 5,900Supplies 550Land 20,000Total assets $26,450

LiabilitiesAccounts payable $ 400

Stockholders’ EquityCapital stock $25,000Retained earnings 1,050 26,050Total liabilities and stockholders’ equity $26,450

NetSolutionsBalance Sheet

November 30, 2002

Financial StatementsFinancial StatementsFinancial StatementsFinancial Statements

C1 - 66

AssetsCash $ 5,900Supplies 550Land 20,000Total assets $26,450

LiabilitiesAccounts payable $ 400

Stockholders’ EquityCapital stock $25,000Retained earnings 1,050 26,050Total liabilities and stockholders’ equity $26,450

NetSolutionsBalance Sheet

November 30, 2002

Financial StatementsFinancial StatementsFinancial StatementsFinancial Statements

C1 - 67

NetSolutionsStatement of Cash Flows

For the Month Ended November 30, 2002

)

Financial StatementsFinancial StatementsFinancial StatementsFinancial Statements

Cash flows from operating activities: Cash received from customers $ 7,500 Deduct cash payments for expenses and payments to creditors 4,600 Net cash flow from operating activities $ 2,900Cash flows from investing activities: Cash payments for acquisition of land (20,000Cash flows from financing activities: Cash received from sale of stock $25,000 Deduct cash dividends 2,000 Net cash flow from financing activities 23,000Net cash flow and Nov. 30, 2002 cash balance $5,900

C1 - 68

NetSolutionsStatement of Cash Flows

For the Month Ended November 30, 2002

)

Financial StatementsFinancial StatementsFinancial StatementsFinancial Statements

Cash flows from operating activities: Cash received from customers $ 7,500 Deduct cash payments for expenses and payments to creditors 4,600 Net cash flow from operating activities $ 2,900Cash flows from investing activities: Cash payments for acquisition of land (20,000Cash flows from financing activities: Cash received from sale of stock $25,000 Deduct cash dividends 2,000 Net cash flow from financing activities 23,000Net cash flow and Nov. 30, 2002 cash balance $5,900

C1 - 69

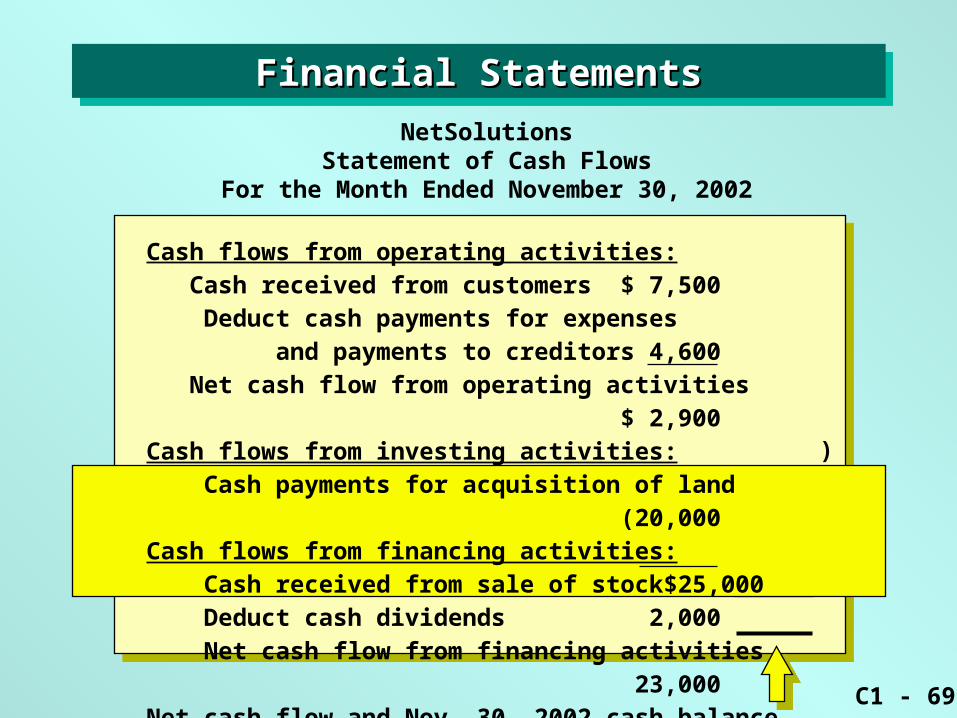

NetSolutionsStatement of Cash Flows

For the Month Ended November 30, 2002

Financial StatementsFinancial StatementsFinancial StatementsFinancial Statements

Cash flows from operating activities: Cash received from customers $ 7,500 Deduct cash payments for expenses and payments to creditors 4,600 Net cash flow from operating activities $ 2,900Cash flows from investing activities: Cash payments for acquisition of land (20,000Cash flows from financing activities: Cash received from sale of stock $25,000 Deduct cash dividends 2,000 Net cash flow from financing activities 23,000Net cash flow and Nov. 30, 2002 cash balance $5,900

)

C1 - 70

Note: To see the topic slide, type 2 and press Enter.

This is the last slide in Chapter F1. This is the last slide in Chapter F1.

Power NotesChapter F1

Introduction to Accounting and Business Introduction to Accounting and Business