Embed Size (px)

Citation preview

C M Clarke-Hill 1

Strategic Method Mergers and Acquisitions Theory Practice

C M Clarke-Hill 2

Strategic MethodStrategic Method

The The “ Method “ “ Method “ vector for corporate vector for corporate development can be adopted by the firm to development can be adopted by the firm to fulfill its strategy in any of the Ansoff quadrants. fulfill its strategy in any of the Ansoff quadrants.

The Method Vector can be sub-divided into :The Method Vector can be sub-divided into :– Internal DevelopmentInternal Development

– Joint DevelopmentJoint Development

– External Development - Acquisitions & MergersExternal Development - Acquisitions & Mergers

Lets consider each one

C M Clarke-Hill 3

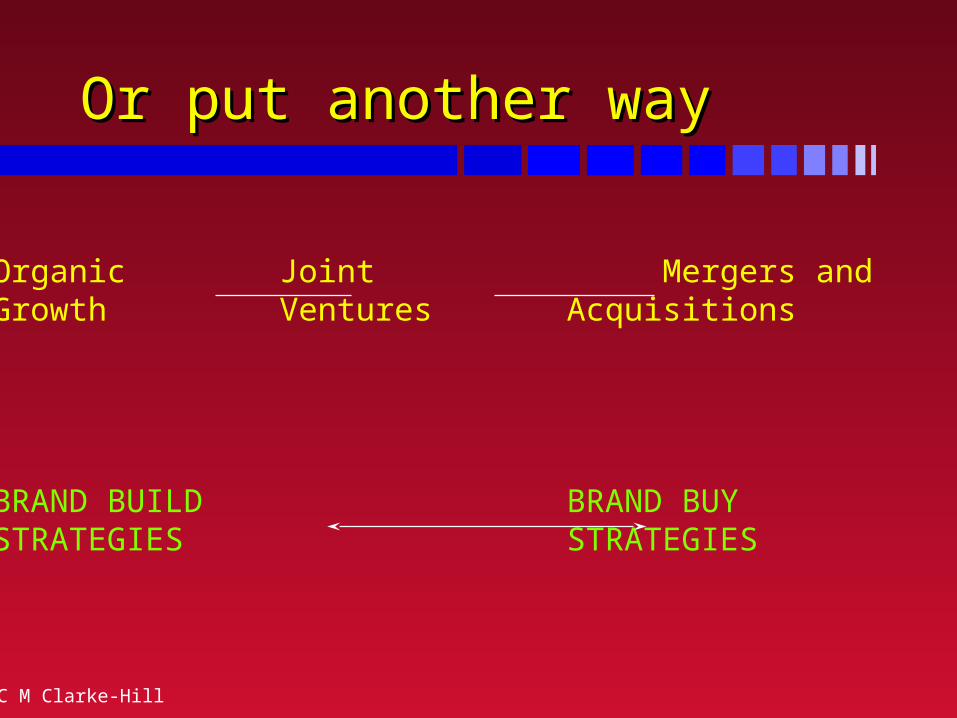

Or put another wayOr put another way

Organic Joint Mergers andGrowth Ventures Acquisitions

BRAND BUILD BRAND BUYSTRATEGIES STRATEGIES

C M Clarke-Hill 4

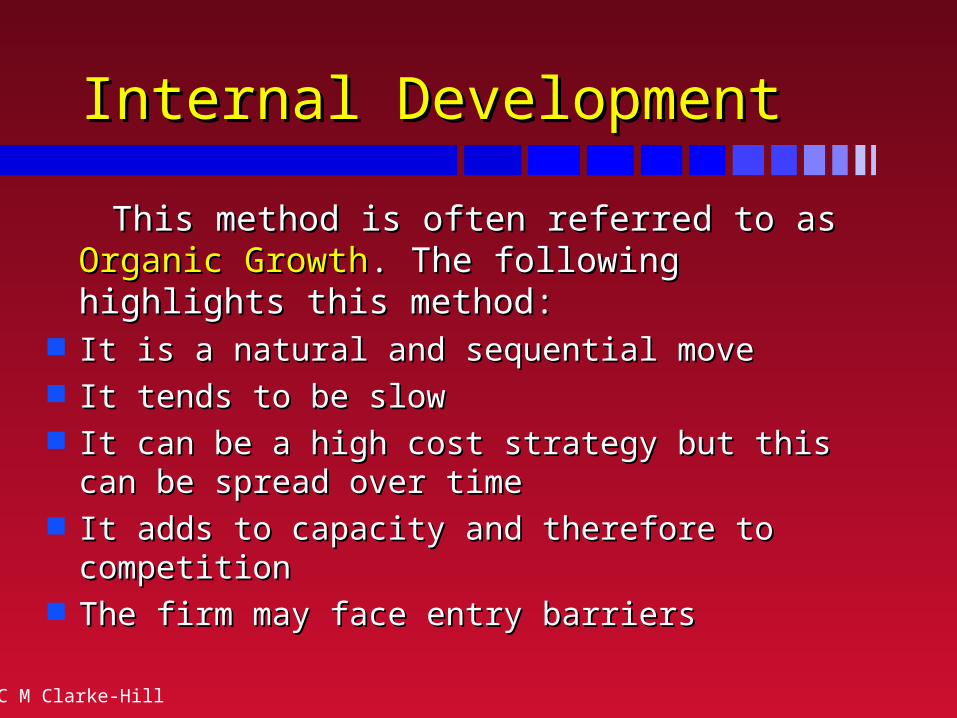

Internal DevelopmentInternal Development

This method is often referred to as This method is often referred to as Organic Organic GrowthGrowth. The following highlights this method:. The following highlights this method:

It is a natural and sequential move It is a natural and sequential move It tends to be slowIt tends to be slow It can be a high cost strategy but this can be spread It can be a high cost strategy but this can be spread

over timeover time It adds to capacity and therefore to competitionIt adds to capacity and therefore to competition The firm may face entry barriersThe firm may face entry barriers

C M Clarke-Hill 5

Joint DevelopmentJoint Development

This is a semi internal/external method of This is a semi internal/external method of development and is extensively used in many development and is extensively used in many forms and often for entry into foreign markets.forms and often for entry into foreign markets.

Joint VenturesJoint Ventures Strategic Alliances Strategic Alliances each of these each of these

hashas ConsortiaConsortia Franchising/LicensingFranchising/Licensing AgentsAgents

different elements of Risk, Profitability & Commitment

C M Clarke-Hill 6

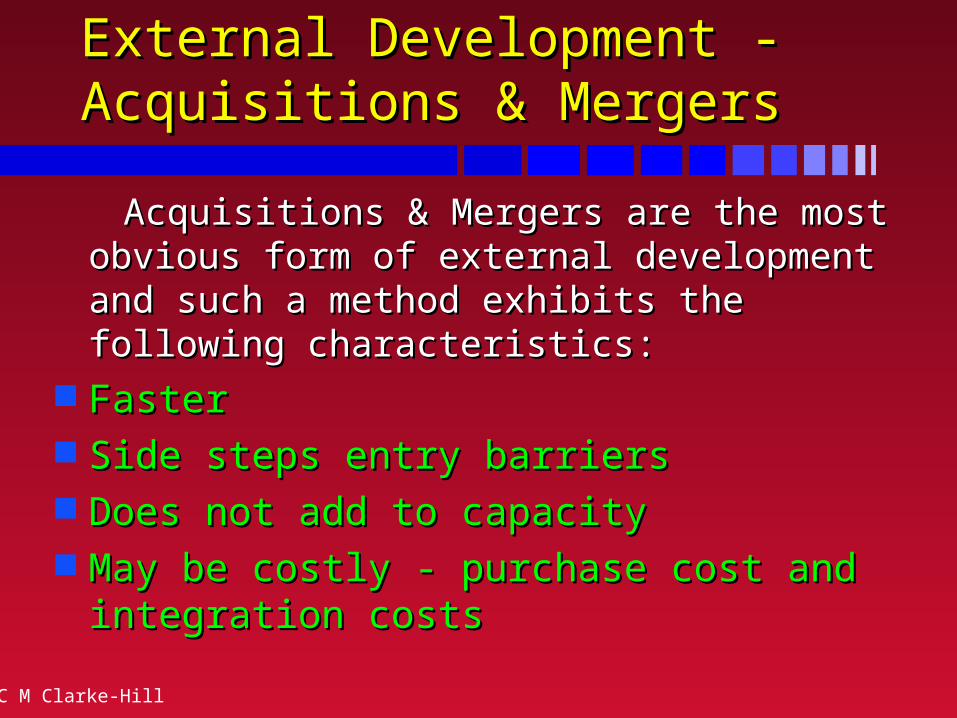

External Development - External Development - Acquisitions & MergersAcquisitions & Mergers

Acquisitions & Mergers are the most obvious Acquisitions & Mergers are the most obvious form of external development and such a form of external development and such a method exhibits the following characteristics:method exhibits the following characteristics:

FasterFaster Side steps entry barriersSide steps entry barriers Does not add to capacityDoes not add to capacity May be costly - purchase cost and May be costly - purchase cost and

integration costs integration costs

C M Clarke-Hill 7

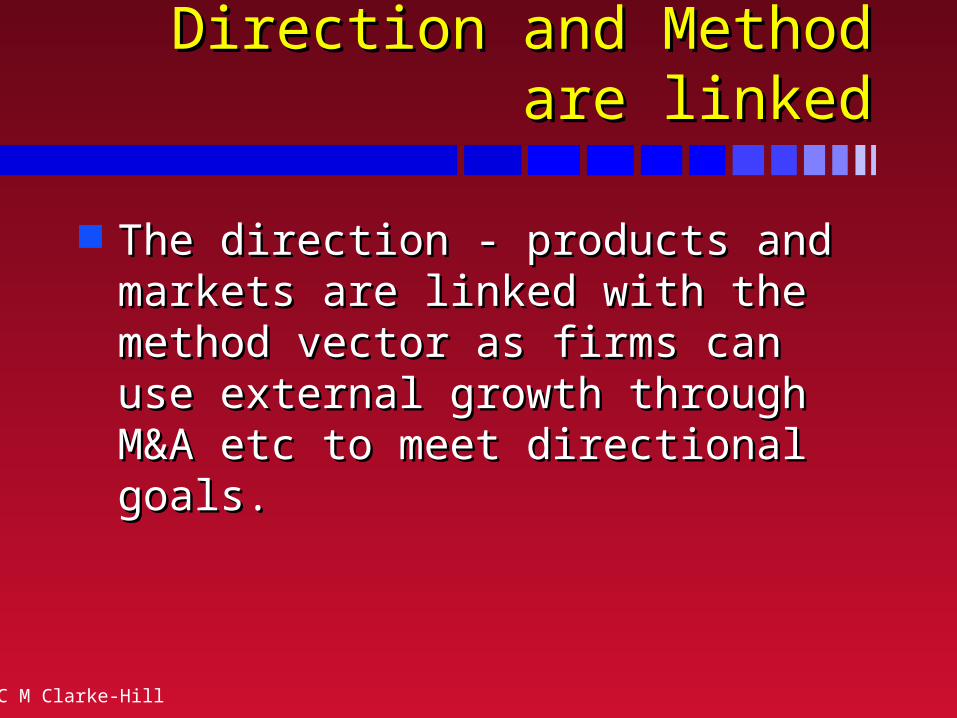

Direction and Method are linkedDirection and Method are linked

The direction - products and markets are The direction - products and markets are linked with the method vector as firms can linked with the method vector as firms can use external growth through M&A etc to use external growth through M&A etc to meet directional goals.meet directional goals.

C M Clarke-Hill 8

Mergers and AcquisitionsMergers and Acquisitions

Definitions Definitions

MotivationsMotivations

Selecting the targetSelecting the target

Paying for the targetPaying for the target

Fending off the bidFending off the bid

M&A in the UKM&A in the UK

C M Clarke-Hill 9

DefinitionsDefinitions

An acquisition is a combination of two or An acquisition is a combination of two or more businesses in which one firm acquires more businesses in which one firm acquires the assets and liabilities of the other (s). the assets and liabilities of the other (s). Acquisitions can be contested or agreed.Acquisitions can be contested or agreed.

A merger is similar, usually agreed. The A merger is similar, usually agreed. The process usually creates a new entity when process usually creates a new entity when the shares in the two companies are pooled the shares in the two companies are pooled to create the new firm through the creation to create the new firm through the creation of new stock in an agreed proportion.of new stock in an agreed proportion.

C M Clarke-Hill 10

Hamill’s Model (1991)Hamill’s Model (1991)

Strategic MotivesStrategic Motives Economic MotivesEconomic Motives Behavioural and Managerial MotivesBehavioural and Managerial Motives Financial MotivesFinancial Motives

Source- J Hamill, (1991), Journal of General ManagementVolume 17, 1, Autumn, pp 27-44

C M Clarke-Hill 11

Strategic Motivations Strategic Motivations

Instant growthInstant growth Buy rather than build market shareBuy rather than build market share DiversificationDiversification Competitive motivesCompetitive motives

– remove a competitorremove a competitor– market controlmarket control

Defensive motives - prevent a hostile bidDefensive motives - prevent a hostile bid

C M Clarke-Hill 12

Economic MotivationsEconomic Motivations

Economies of scaleEconomies of scale Synergy in the value chainSynergy in the value chain Improved efficiencyImproved efficiency Purchase of unique resourcesPurchase of unique resources Purchase of managerial skillsPurchase of managerial skills

C M Clarke-Hill 13

Behavioural/Managerial MotivesBehavioural/Managerial Motives

Increased sales growthIncreased sales growth Increased management utilityIncreased management utility Separation of ownership from controlSeparation of ownership from control Personal goals of senior managersPersonal goals of senior managers

These issues are covered in the managerial theory of the firm.See work by Cyert and March, Williamson, Marris, Simon etc.

C M Clarke-Hill 14

Financial MotivationsFinancial Motivations

Increased shareholder valueIncreased shareholder value Valuation gap theoryValuation gap theory Financial engineeringFinancial engineering The dealThe deal

C M Clarke-Hill 15

M&A and the AuthoritiesM&A and the Authorities

The authorities in the US, UK and EU make The authorities in the US, UK and EU make no distinction between the two forms as the no distinction between the two forms as the outcome often can create a dominant outcome often can create a dominant position. Authorities will regulate M&A position. Authorities will regulate M&A activity to protect the public interest.activity to protect the public interest.

In the EU context - articles 85 and 86 of the Treaty of RomeIn the UK context - Competition Commission & OFTIn the US context - various anti-trust laws apply

C M Clarke-Hill 16

For ExampleFor Example

In 2001 the proposed merger between GE In 2001 the proposed merger between GE of America and Honeywell failed because of America and Honeywell failed because the EU Competition Commissioner placed a the EU Competition Commissioner placed a number of key conditions on the merger number of key conditions on the merger that GE withdrew its bid.that GE withdrew its bid.

C M Clarke-Hill 17

Selecting an Acquisition TargetSelecting an Acquisition Target

In selecting a target the predator In selecting a target the predator company has to consider the following:company has to consider the following:– Strategic objectivesStrategic objectives

– Shareholder valueShareholder value

– Acquisition objectivesAcquisition objectives

C M Clarke-Hill 18

Selecting the TargetSelecting the Target

The predator company has to consider The predator company has to consider the following in terms of its target:the following in terms of its target:– Performance criteriaPerformance criteria

– Company characteristicsCompany characteristics

– ManagementManagement

– Industry sector dynamicsIndustry sector dynamics

C M Clarke-Hill 19

Target CriteriaTarget Criteria

Performance criteriaPerformance criteria

Company Company characteristicscharacteristics

ManagementManagement

Industry sector Industry sector characteristicscharacteristics

Return on capital employedReturn on capital employed Sales marginsSales margins Sales growthSales growth Market shareMarket share Net present valuesNet present values Size of companySize of company Geographical locationsGeographical locations Product range, R&D etc..Product range, R&D etc.. Quality of the managementQuality of the management Management styleManagement style Compatibility between the firmsCompatibility between the firms Stage of industry evolutionStage of industry evolution Competitive dynamicsCompetitive dynamics

C M Clarke-Hill 20

Portfolio Approach to AcquisitionsPortfolio Approach to Acquisitions

Look at sectorLook at sector Look at the dynamics of the industryLook at the dynamics of the industry Identify yourself and others strengths and Identify yourself and others strengths and

weaknesses and calculate shares and weaknesses and calculate shares and trajectoriestrajectories

Identify targets linked to acquisition Identify targets linked to acquisition strategy and corporate goalsstrategy and corporate goals

C M Clarke-Hill 21

Paying for the AcquisitionPaying for the Acquisition

Paying for the targetPaying for the target– Cash offer - may include ‘junk bonds’Cash offer - may include ‘junk bonds’– Cash and shares combinationCash and shares combination– Shares onlyShares only

How a firm pays for the target depends on its How a firm pays for the target depends on its share and its financial strengthshare and its financial strength

The role of the institutional fund manager is crucial in the The role of the institutional fund manager is crucial in the processprocess

In the UK it is rare for a target company to beat-off a predatorIn the UK it is rare for a target company to beat-off a predator

C M Clarke-Hill 22

Fending off a bid - the key 6 weeksFending off a bid - the key 6 weeks

Mass advertising - particularly to the small Mass advertising - particularly to the small shareholdershareholder

Mailings to all shareholders - paper and videoMailings to all shareholders - paper and video Press relations - keeping up the spin in the financial Press relations - keeping up the spin in the financial

presspress Investor relations - keeping the fund managers and Investor relations - keeping the fund managers and

the banks informedthe banks informed Public relations - shareholders and MPs etc..Public relations - shareholders and MPs etc.. Press conferences to ensure news coveragePress conferences to ensure news coverage

C M Clarke-Hill 23

Rise in takeover activity has many Rise in takeover activity has many factorsfactors

Short-term horizons of institutional fund managersShort-term horizons of institutional fund managers The rapid move away from the owner managed The rapid move away from the owner managed

firm to that of the professional managerfirm to that of the professional manager The rise in the power and influence of the The rise in the power and influence of the

merchant banksmerchant banks Internationalisation of capital markets Internationalisation of capital markets The financial sector willing to fund takeovers, The financial sector willing to fund takeovers,

often with ‘junk bonds’often with ‘junk bonds’

C M Clarke-Hill 24

Takeovers activity in recent yearsTakeovers activity in recent years

1986-1989 was the ‘golden era’ of the takeover 1986-1989 was the ‘golden era’ of the takeover where during that period takeovers were where during that period takeovers were running at around £ 10 billion a year.running at around £ 10 billion a year.

The recession of the early 1990s considerably The recession of the early 1990s considerably reduced the level of takeover activity in the reduced the level of takeover activity in the UK.UK.

1995 saw the return of the takeover era, with 1995 saw the return of the takeover era, with takeovers valued at over £ 40 bn.takeovers valued at over £ 40 bn.

Late 1990s this activity has been maintainedLate 1990s this activity has been maintained

C M Clarke-Hill 25

Takeovers in 1997Takeovers in 1997

In one week in October £ 100 bn worth of takeovers were announced. This became known as ‘Mad Monday’.

Most of these takeovers involved cross border mergers motivated by a need to create size and compete in an increasingly global world.

C M Clarke-Hill 26

1997-98 era1997-98 era

Stock market rises continually for two years in the Stock market rises continually for two years in the US and UK. OK some minor blips, but in 1998 the US and UK. OK some minor blips, but in 1998 the market is some 14% up on the year. In July ‘98 market is some 14% up on the year. In July ‘98 FTSE = 6195 FTSE = 6195 and in mid Jan ‘99 the and in mid Jan ‘99 the FTSE = 6100FTSE = 6100

Falling inflation Falling inflation Capital markets buoyed by American growth and Capital markets buoyed by American growth and

falling interest ratesfalling interest rates Banks willing to lend to companies - high degrees Banks willing to lend to companies - high degrees

of liquidity in the banking sectorof liquidity in the banking sector

C M Clarke-Hill 27

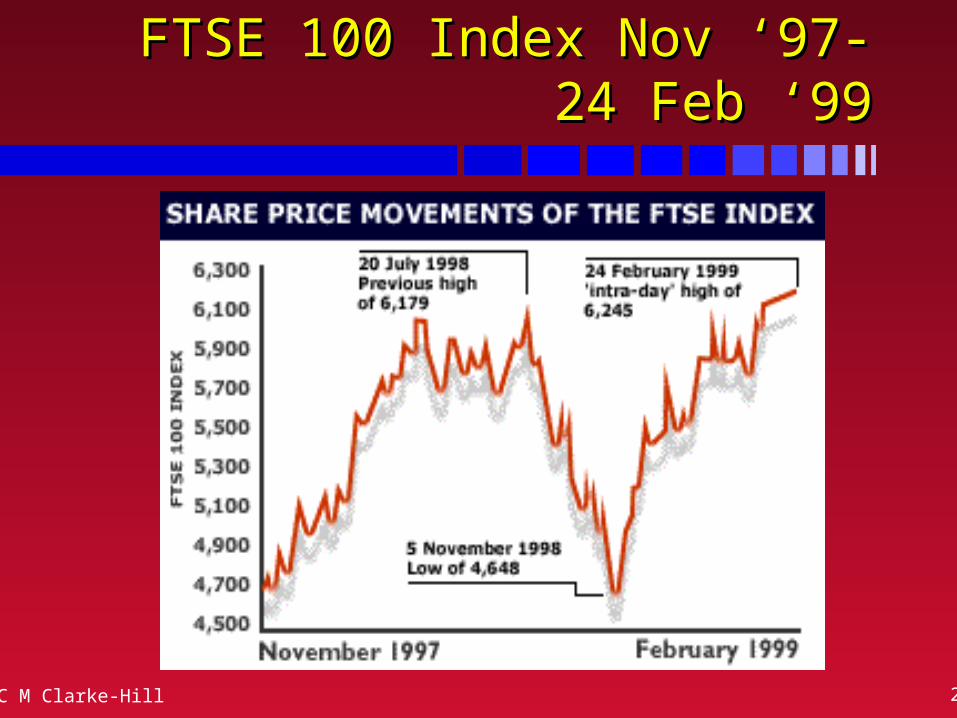

FTSE 100 Index Nov ‘97-24 Feb ‘99FTSE 100 Index Nov ‘97-24 Feb ‘99

C M Clarke-Hill 28

Takeovers and Mergers in 1998Takeovers and Mergers in 1998

Takeover activity has not slowed downTakeover activity has not slowed down Consolidation in many sectors continues to be a Consolidation in many sectors continues to be a

major motive:major motive:– ChemicalsChemicals

– Aerospace - both in the EU and US contextAerospace - both in the EU and US context

– PharmaceuticalsPharmaceuticals

– Banking and Financial ServicesBanking and Financial Services

Primarily cross border. Primarily cross border. In 1998, Cross border deals In 1998, Cross border deals made by UK firms amounted to £ 77bnmade by UK firms amounted to £ 77bn

Search for scaleSearch for scale

C M Clarke-Hill 29

Some memorable deals in 1998-early 99Some memorable deals in 1998-early 99

BP and Amoco - Oils sector - late 1998 merger largest BP and Amoco - Oils sector - late 1998 merger largest by UK firm - $61bnby UK firm - $61bn

Daimler Benz and Chrsyler - Auto sector - late 1998 Daimler Benz and Chrsyler - Auto sector - late 1998 merger to create new global firmmerger to create new global firm

Vodafone and Airtouch - Telecoms sector -takeover Vodafone and Airtouch - Telecoms sector -takeover now largest by UK firm - £36bn -Jan 1999now largest by UK firm - £36bn -Jan 1999

BAT merger with Rothmans - Tobacco sector - worth BAT merger with Rothmans - Tobacco sector - worth £15bn - Jan 1999£15bn - Jan 1999

BAe is set to acquire Marconi from GEC for around BAe is set to acquire Marconi from GEC for around £ 7 bn - mid Jan 1999 £ 7 bn - mid Jan 1999

C M Clarke-Hill 30

In many aspects, the 1990s takeover activity In many aspects, the 1990s takeover activity seems to follow the Hamill table of motives seems to follow the Hamill table of motives for mergers and acquisitions.for mergers and acquisitions.– Economic MotivesEconomic Motives– Financial MotivesFinancial Motives– Strategic motivesStrategic motives

However, will the new wave of acquisitions However, will the new wave of acquisitions result in a better and more competitive result in a better and more competitive economy ?economy ?

Some conclusions

C M Clarke-Hill 31

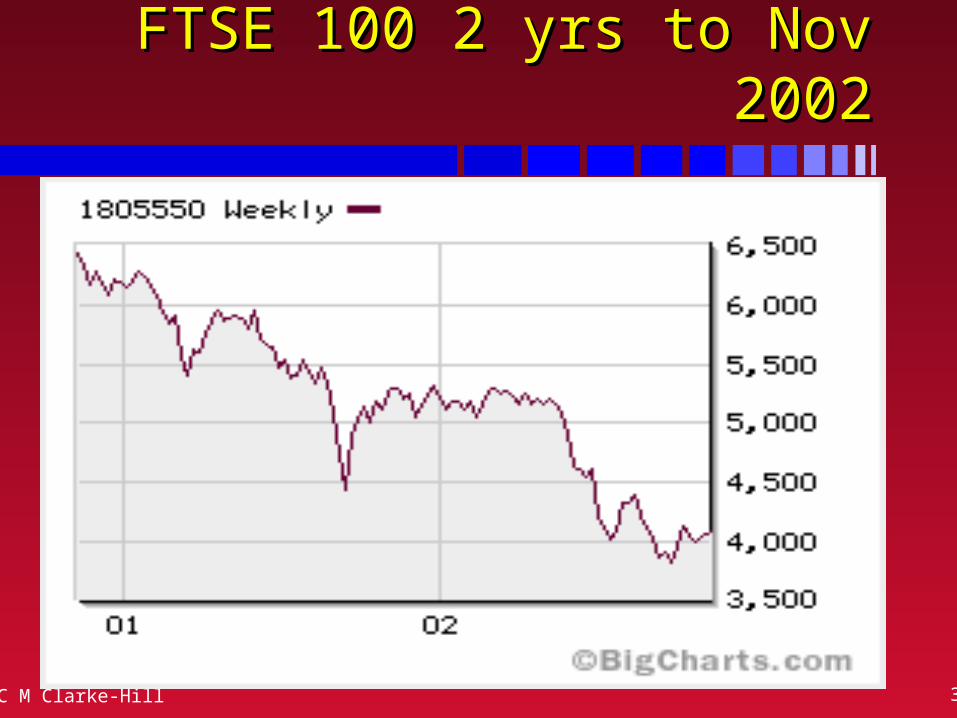

FTSE has FallenFTSE has Fallen

The dot.com bubble has burst – Tech Stocks have The dot.com bubble has burst – Tech Stocks have been affected very significantlybeen affected very significantly

The FTSE has actually fallen in the year to The FTSE has actually fallen in the year to November 2002 and so have M&A valuesNovember 2002 and so have M&A values

BUT takeovers are still fashionable but no BUT takeovers are still fashionable but no takeover wave of the late 1990s. HSBC - £10bn takeover wave of the late 1990s. HSBC - £10bn bid for Household International (US) announcedbid for Household International (US) announced

UK M&A StatisticsUK M&A Statistics

C M Clarke-Hill 32

FTSE 100 2 yrs to Nov 2002FTSE 100 2 yrs to Nov 2002