Embed Size (px)

Citation preview

CLUB/SERVICE/ INCOMPLETE

CLUB ACCOUNTS

• A club is not a business. • Its ‘raison d'être’ is not profit. • It does not pay CPT on its profits.• Different set of words used to ‘flag’ this

difference.• Cash Book Receipts & Payments a/c• P & L Income & Expenditure a/c• Profit Excess of Income• Capital Accumulated Fund

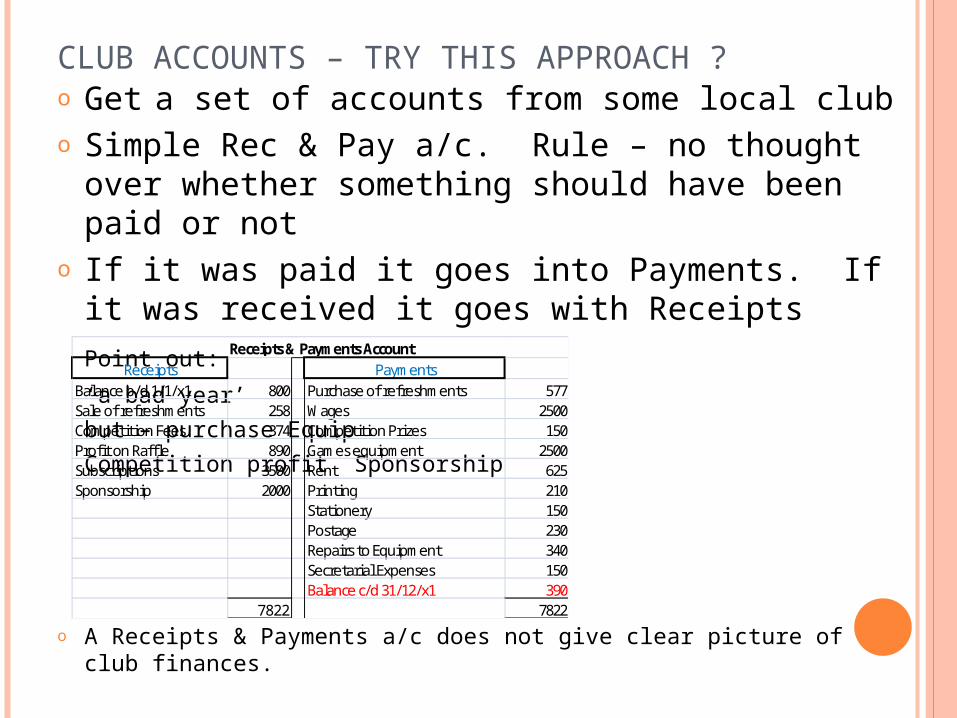

CLUB ACCOUNTS – TRY THIS APPROACH ?o Get a set of accounts from some local clubo Simple Rec & Pay a/c. Rule – no thought over

whether something should have been paid or not

o If it was paid it goes into Payments. If it was received it goes with Receipts

Point out:

‘a bad year’

but – purchase Equip

Competition profitSponsorship

o A Receipts & Payments a/c does not give clear picture of club finances.

Receipts PaymentsBalance b/d 1/1/x1 800 Purchase of refreshments 577Sale of refreshments 258 Wages 2500Competition Fees 374 Competition Prizes 150Profit on Raffl e 890 Games equipment 2500Subscriptions 3500 Rent 625Sponsorship 2000 Printing 210

Stationery 150Postage 230Repairs to Equipment 340Secretarial Expenses 150Balance c/d 31/12/x1 390

7822 7822

Receipts & Payments Account

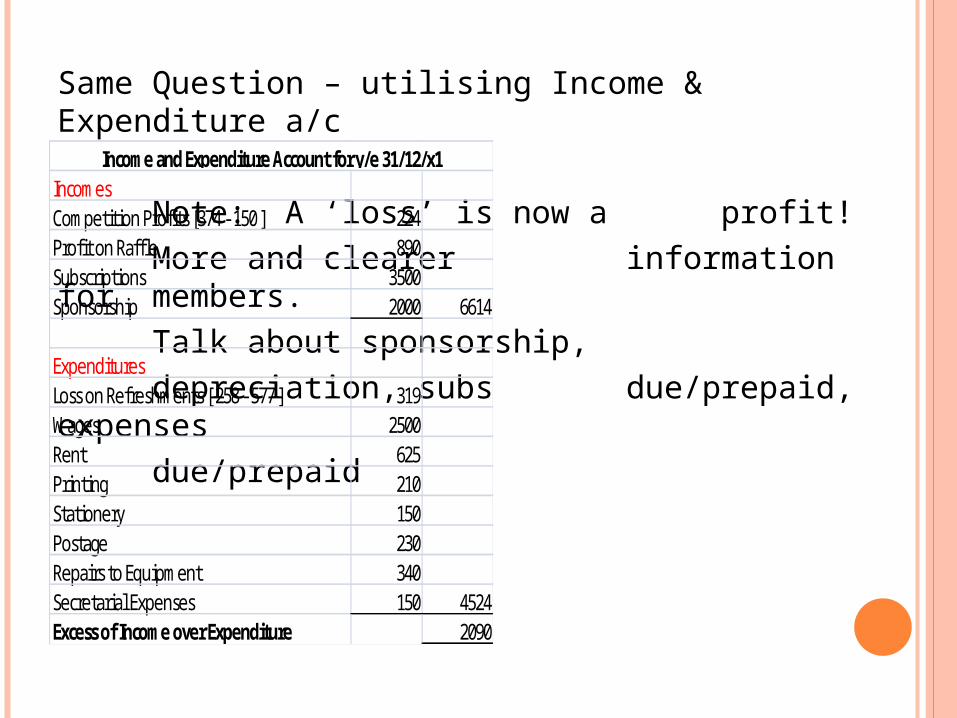

Same Question – utilising Income & Expenditure a/c

Note: A ‘loss’ is now a profit!

More and clearer information for members.Talk about

sponsorship, depreciation, subs

due/prepaid, expenses

due/prepaid

IncomesCompetition Profits [374 - 150 ] 224Profit on Raffl e 890Subscriptions 3500Sponsorship 2000 6614

ExpendituresLoss on Refreshments [ 258 - 577 ] 319Wages 2500Rent 625Printing 210Stationery 150Postage 230Repairs to Equipment 340Secretarial Expenses 150 4524Excess of Income over Expenditure 2090

Income and Expenditure Account for y/e 31/12/x1

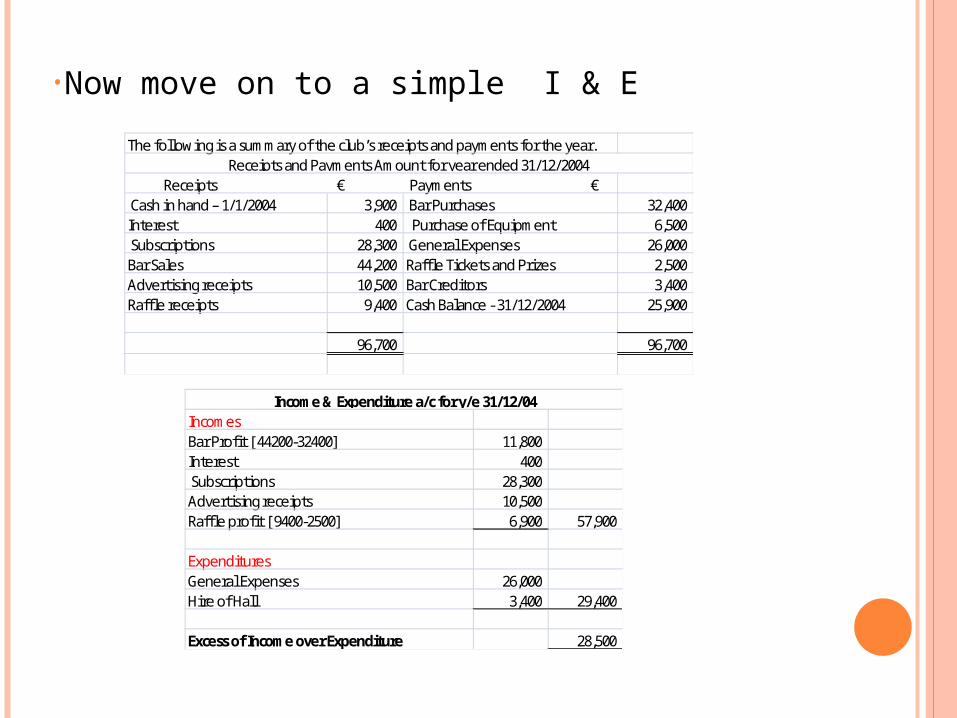

•Now move on to a simple I & E

The following is a summary of the club’s receipts and payments for the year.

Receipts € Payments € Cash in hand – 1/1/2004 3,900 Bar Purchases 32,400 Interest 400 Purchase of Equipment 6,500 Subscriptions 28,300 General Expenses 26,000 Bar Sales 44,200 Raffl e Tickets and Prizes 2,500 Advertising receipts 10,500 Bar Creditors 3,400 Raffl e receipts 9,400 Cash Balance - 31/12/2004 25,900

96,700 96,700

Receipts and Payments Amount for year ended 31/12/2004

IncomesBar Profit [ 44200-32400] 11,800 Interest 400 Subscriptions 28,300 Advertising receipts 10,500 Raffl e profit [ 9400-2500] 6,900 57,900

ExpendituresGeneral Expenses 26,000 Hire of Hall 3,400 29,400

Excess of Income over Expenditure 28,500

Income & Expenditure a/c for y/e 31/12/04

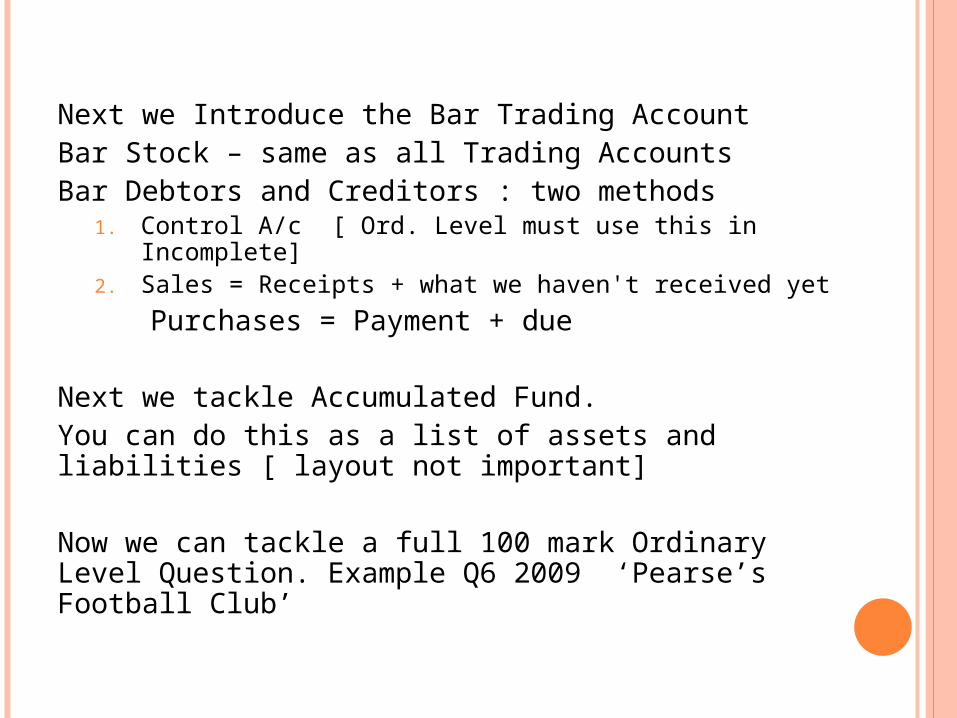

Next we Introduce the Bar Trading AccountBar Stock – same as all Trading AccountsBar Debtors and Creditors : two methods

1. Control A/c [ Ord. Level must use this in Incomplete]2. Sales = Receipts + what we haven't received yet

Purchases = Payment + due

Next we tackle Accumulated Fund.You can do this as a list of assets and liabilities [ layout not important]

Now we can tackle a full 100 mark Ordinary Level Question. Example Q6 2009 ‘Pearse’s Football Club’

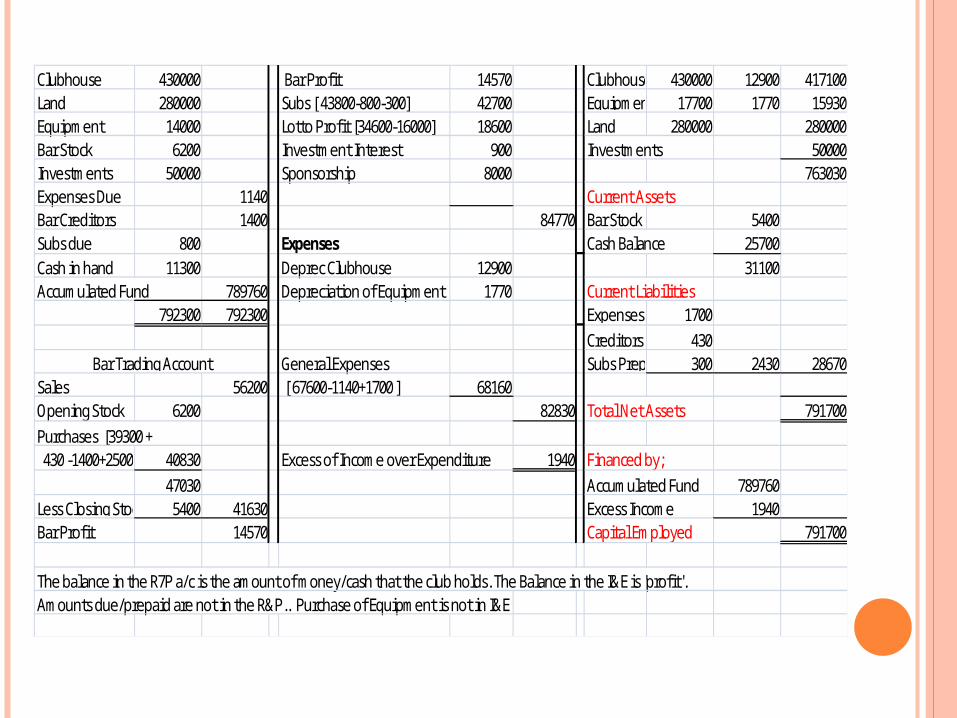

Clubhouse 430000 Bar Profit 14570 Clubhouse 430000 12900 417100Land 280000 Subs [ 43800-800-300] 42700 Equipment 17700 1770 15930Equipment 14000 Lotto Profit [34600-16000] 18600 Land 280000 280000Bar Stock 6200 Investment Interest 900 Investments 50000Investments 50000 Sponsorship 8000 763030Expenses Due 1140 Current AssetsBar Creditors 1400 84770 Bar Stock 5400Subs due 800 Expenses Cash Balance 25700Cash in hand 11300 Deprec Clubhouse 12900 31100Accumulated Fund 789760 Depreciation of Equipment 1770 Current Liabilities

792300 792300 Expenses Due 1700Creditors 430

General Expenses Subs Prepaid 300 2430 28670Sales 56200 [ 67600-1140+1700 ] 68160Opening Stock 6200 82830 Total Net Assets 791700Purchases [39300 + 430 -1400+2500] 40830 Excess of Income over Expenditure 1940 Financed by;

47030 Accumulated Fund 789760Less Closing Stock 5400 41630 Excess Income 1940Bar Profit 14570 Capital Employed 791700

The balance in the R7P a/c is the amount of money/cash that the club holds. The Balance in the I&E is 'profit'. Amounts due/prepaid are not in the R&P.. Purchase of Equipment is not in I&E

Bar Trading Account

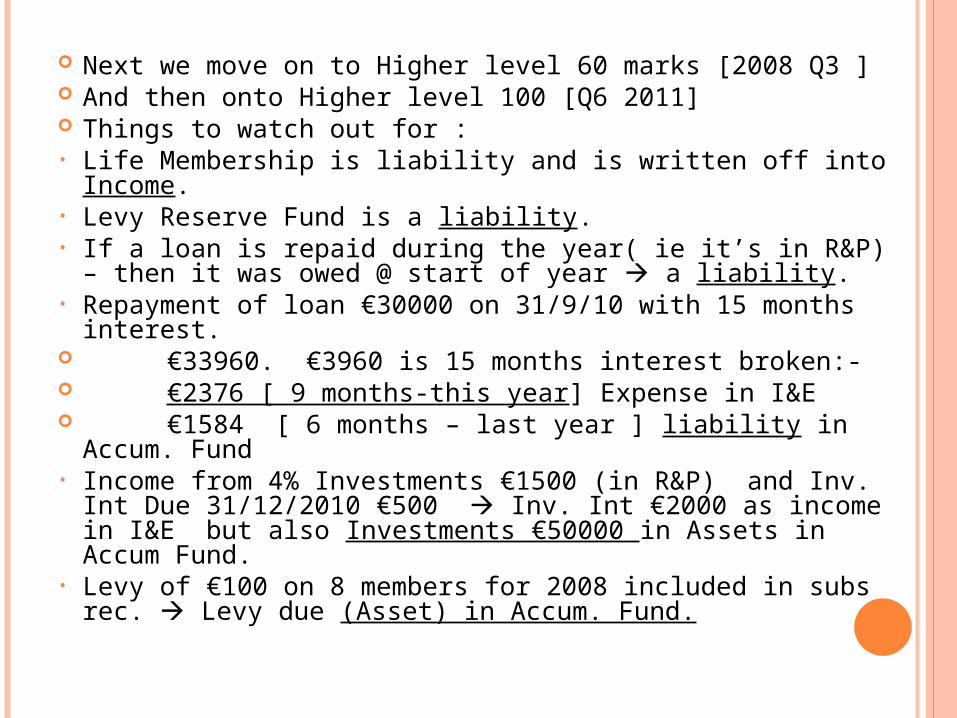

Next we move on to Higher level 60 marks [2008 Q3 ] And then onto Higher level 100 [Q6 2011] Things to watch out for :• Life Membership is liability and is written off into Income.• Levy Reserve Fund is a liability.• If a loan is repaid during the year( ie it’s in R&P) – then it

was owed @ start of year a liability.• Repayment of loan €30000 on 31/9/10 with 15 months

interest. €33960. €3960 is 15 months interest broken:- €2376 [ 9 months-this year] Expense in I&E €1584 [ 6 months – last year ] liability in Accum.

Fund• Income from 4% Investments €1500 (in R&P) and Inv. Int

Due 31/12/2010 €500 Inv. Int €2000 as income in I&E but also Investments €50000 in Assets in Accum Fund.

• Levy of €100 on 8 members for 2008 included in subs rec. Levy due (Asset) in Accum. Fund.

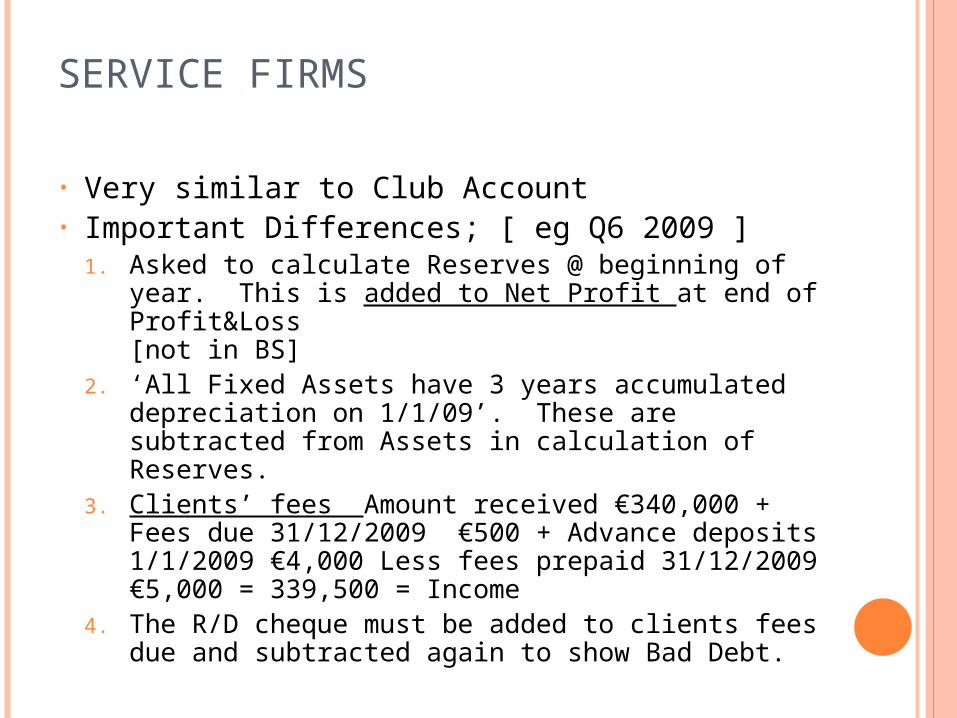

SERVICE FIRMS

• Very similar to Club Account• Important Differences; [ eg Q6 2009 ]

1. Asked to calculate Reserves @ beginning of year. This is added to Net Profit at end of Profit&Loss [not in BS]

2. ‘All Fixed Assets have 3 years accumulated depreciation on 1/1/09’. These are subtracted from Assets in calculation of Reserves.

3. Clients’ fees Amount received €340,000 + Fees due 31/12/2009 €500 + Advance deposits 1/1/2009 €4,000 Less fees prepaid 31/12/2009 €5,000 = 339,500 = Income

4. The R/D cheque must be added to clients fees due and subtracted again to show Bad Debt.

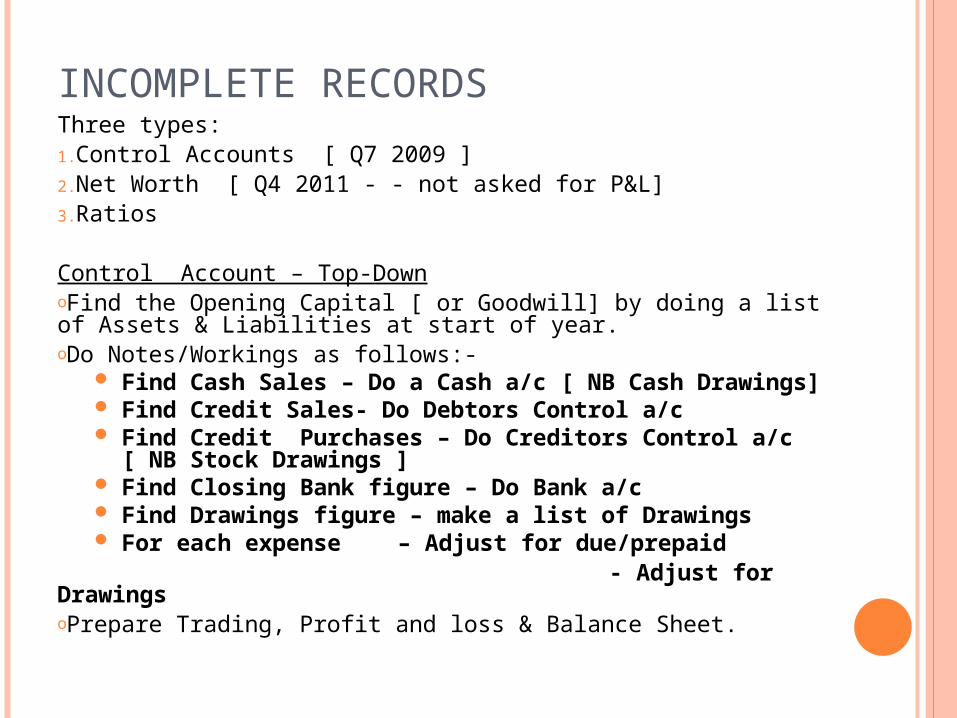

INCOMPLETE RECORDSThree types: 1.Control Accounts [ Q7 2009 ] 2.Net Worth [ Q4 2011 - - not asked for P&L]3.Ratios

Control Account – Top-DownoFind the Opening Capital [ or Goodwill] by doing a list of Assets & Liabilities at start of year.oDo Notes/Workings as follows:-

Find Cash Sales – Do a Cash a/c [ NB Cash Drawings] Find Credit Sales- Do Debtors Control a/c Find Credit Purchases – Do Creditors Control a/c

[ NB Stock Drawings ] Find Closing Bank figure – Do Bank a/c Find Drawings figure – make a list of Drawings For each expense – Adjust for due/prepaid

- Adjust for DrawingsoPrepare Trading, Profit and loss & Balance Sheet.

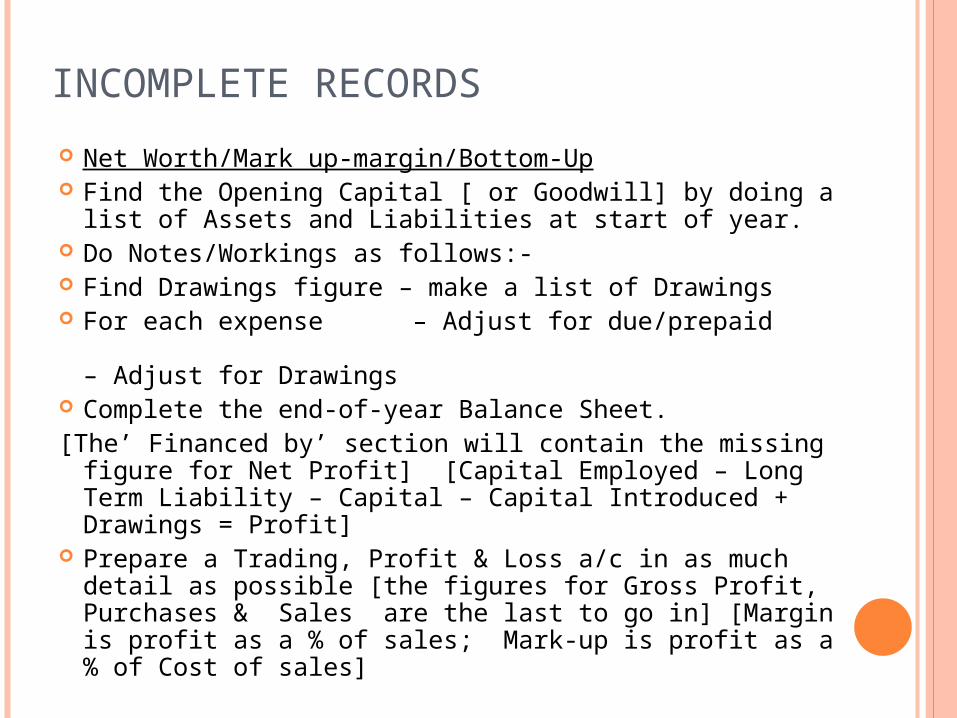

INCOMPLETE RECORDS

Net Worth/Mark up-margin/Bottom-Up Find the Opening Capital [ or Goodwill] by doing a

list of Assets and Liabilities at start of year. Do Notes/Workings as follows:- Find Drawings figure – make a list of Drawings For each expense – Adjust for due/prepaid

– Adjust for Drawings

Complete the end-of-year Balance Sheet.[The’ Financed by’ section will contain the missing

figure for Net Profit] [Capital Employed – Long Term Liability – Capital – Capital Introduced + Drawings = Profit]

Prepare a Trading, Profit & Loss a/c in as much detail as possible [the figures for Gross Profit, Purchases & Sales are the last to go in] [Margin is profit as a % of sales; Mark-up is profit as a % of Cost of sales]

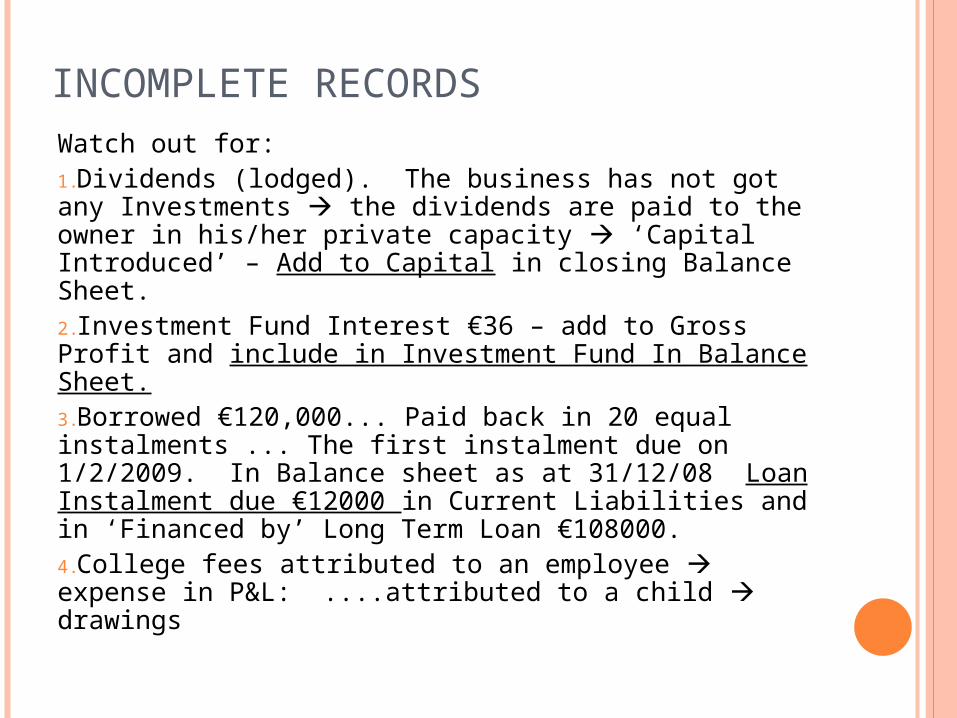

INCOMPLETE RECORDS

Watch out for:1.Dividends (lodged). The business has not got any Investments the dividends are paid to the owner in his/her private capacity ‘Capital Introduced’ – Add to Capital in closing Balance Sheet.2.Investment Fund Interest €36 – add to Gross Profit and include in Investment Fund In Balance Sheet.3.Borrowed €120,000... Paid back in 20 equal instalments ... The first instalment due on 1/2/2009. In Balance sheet as at 31/12/08 Loan Instalment due €12000 in Current Liabilities and in ‘Financed by’ Long Term Loan €108000.4.College fees attributed to an employee expense in P&L: ....attributed to a child drawings

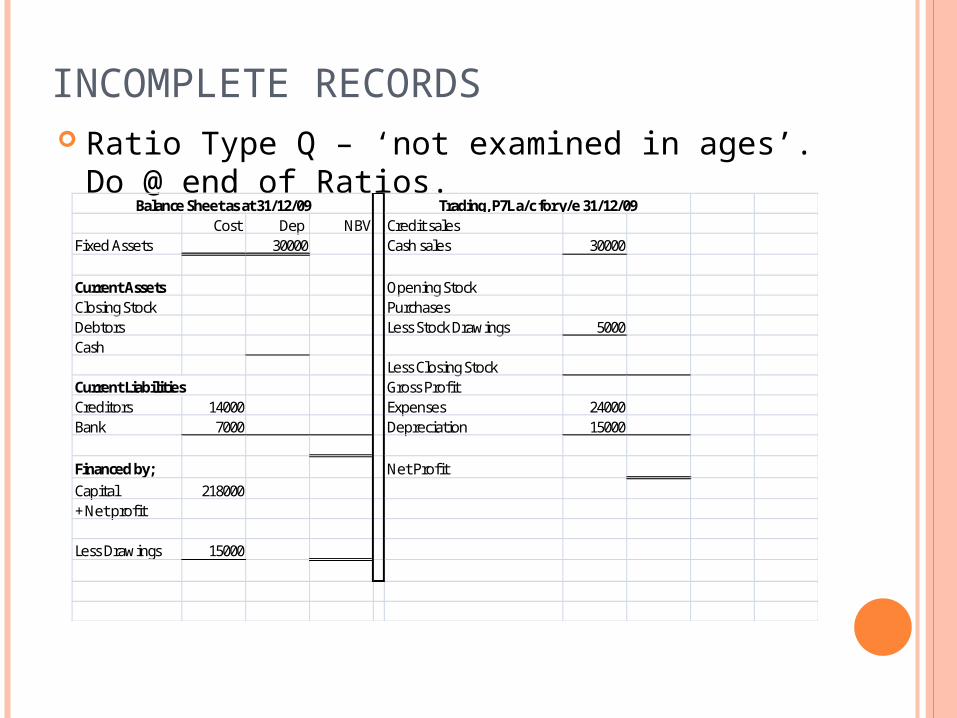

INCOMPLETE RECORDS Ratio Type Q – ‘not examined in ages’. Do @

end of Ratios.Cost Dep NBV Credit sales

Fixed Assets 30000 Cash sales 30000

Current Assets Opening StockClosing Stock PurchasesDebtors Less Stock Drawings 5000Cash

Less Closing StockCurrent Liabilities Gross ProfitCreditors 14000 Expenses 24000Bank 7000 Depreciation 15000

Financed by; Net ProfitCapital 218000+ Net profit

Less Drawings 15000

Balance Sheet as at 31/12/09 Trading, P7L a/c for y/e 31/12/09

THEORY

• Answer the question that is asked! The answer is in the question.

• Incomplete has had the same theory question for years!

• Club & Service: Always quantify your comments. Do not mix assets with liabilities in one sentence If asked to give advice – give financial advice