Embed Size (px)

Citation preview

(c) Grant Thornton Japan. All rights reserved.

Japan Real Estate Taxation(Individuals Purchasing Real Estate in Japan)

Grant Thornton Japan / ASG Tax Corporation

(c) Grant Thornton Japan. All rights reserved.

Japan Real Estate TaxationAgenda

1. Resident Status

2. Taxes on Acquisition and Holding

3. Rental Income

4. Capital Gains

5. Case Study

(c) Grant Thornton Japan. All rights reserved.

Japan Real Estate TaxationResident Status - Classifications

Resident

Non-permanent

Permanent

Non-Resident

Lived in Japan for 5 years or less of past 10 years

Lived in Japan for more than 5 of past 10 years

Domicile in Japan or resided in Japan for at least 1 year up to current date

(c) Grant Thornton Japan. All rights reserved.

Japan Real Estate TaxationResident Status - Scope of Income

• Permanent Resident– Worldwide income

• Non-permanent resident– Japan source income and income remitted into

Japan

• Non-Resident– Japan source income only

(c) Grant Thornton Japan. All rights reserved.

Japan Real Estate Taxation Acquisition Taxes

Taxes paid on acquisition of propertyReal Estate Acquisition Tax 4% of valuation

Registration and License Tax 2% of valuation

Consumption Tax 5% of building value

Stamp Tax JPY80,000 (JPY100M - JPY500M contract)

Total as % of Purchase Price 5% - 8%

(c) Grant Thornton Japan. All rights reserved.

Japan Real Estate TaxationAcquisition Taxes - Client Case

Purchase Price JPY130M; Valuation JPY93M

Real Estate Acquisition Tax 3.7M

Registration & License Tax 1.8M

Consumption Tax 4.2M

Stamp Tax 0.08M

Total 9.8M

Total as % of Purchase Price 7.5%

Calculation of Acquisition Taxes

(c) Grant Thornton Japan. All rights reserved.

Japan Real Estate TaxationHolding Taxes

Taxes paid through the period of ownershipFixed Assets Tax 1.4% of valuation

City Planning Tax 0.3% of valuation

Total as % of Property Value 1% - 3%

(c) Grant Thornton Japan. All rights reserved.

Japan Real Estate TaxationHolding Taxes - Client Case

Purchase Price JPY130M; Valuation JPY93M

Fixed Assets Tax 1.3M

City Planning Tax 0.3M

Total 1.6M

Total as % of Purchase Price 1.2%

Calculation of Holding Taxes

(c) Grant Thornton Japan. All rights reserved.

Japan Real Estate TaxationRental Income - Treatment

• How does Japan treat rental income?

– Treated as “lease” or “business” income on your tax return

– Taxed with other income at progressive rate

(c) Grant Thornton Japan. All rights reserved.

Japan Real Estate TaxationRental Income – Expenses

• Claim expenses against your income:

– Depreciation

– Repairs

– Interest

– Management fees

(c) Grant Thornton Japan. All rights reserved.

Japan Real Estate TaxationRental Income - Depreciation

• Purchase cost of the building can be recovered as an expense – depreciated over useful life

• Only buildings can be depreciated

(c) Grant Thornton Japan. All rights reserved.

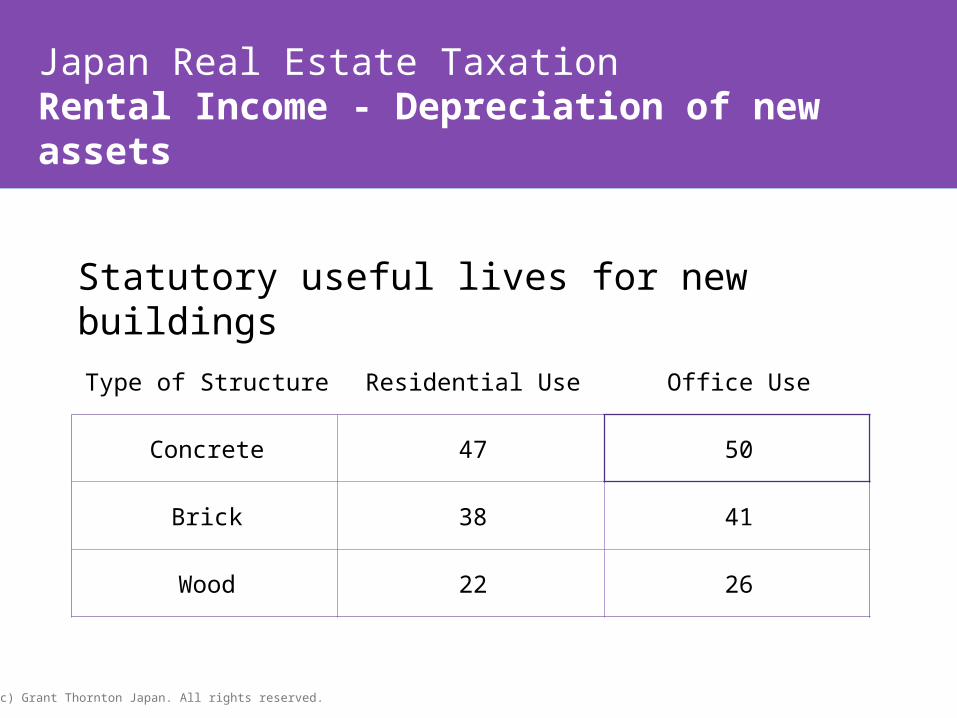

Japan Real Estate TaxationRental Income - Depreciation of new assets

Statutory useful lives for new buildings

Type of Structure Residential Use Office Use

Concrete 47 50

Brick 38 41

Wood 22 26

(c) Grant Thornton Japan. All rights reserved.

Japan Real Estate TaxationRental Income - Depreciation of used assets

• If older than statutory useful life …

– Depreciated over period equal to 20% of statutory useful life

– 30-year old wooden house depreciated over 4 yrs.

(c) Grant Thornton Japan. All rights reserved.

Japan Real Estate TaxationRental Income - Repairs and Renovations

• Repairs– Treated as an expense

– Taxable deduction

• Renovations– Increase value of building

– Costs added to the price paid for the house and depreciated

(c) Grant Thornton Japan. All rights reserved.

Japan Real Estate TaxationRental Income - Interest

• Interest on a loan deductible

– Building / land value ratio required

– All of building portion deductible

– Land portion may be deductible

(c) Grant Thornton Japan. All rights reserved.

Japan Real Estate TaxationCapital Gains

Niseko Property

Buy in 2001 9M

Sell in 2008 62M

Capital Gain 53M

(c) Grant Thornton Japan. All rights reserved.

Japan Real Estate TaxationCapital Gains - Short term vs. Long term

Non-residents pay national component only

Capital Gains Tax RatesTime Property held National Local

More than 5 years 15% 5%

5 years or less 30% 9%

(c) Grant Thornton Japan. All rights reserved.

Japan Real Estate TaxationCapital Gains - Owner-occupier discount

• JPY30M discount on gains

• Must reside in the property at time of sale

• Joint-owners can each claim discount … gift tax

(c) Grant Thornton Japan. All rights reserved.

Japan Real Estate TaxationClient Case (Jack)

• Jack is from the USA• Single• Annual salary JPY32M• Lives in Tokyo• Considering property purchase

and wants to know tax implications

(c) Grant Thornton Japan. All rights reserved.

Japan Real Estate TaxationClient Case (Jack) – Investment Property

Jack's InvestmentProperty (type/use/construction date) Wood/Residential/1987

Year of purchase 2008

Purchase price JPY80M

Loan, Interest 60M, 5%

Repairs JPY15M over 5 years

Renovations None

Estimated rental income JPY3M per year

Sell date/Estimated price 2014/JPY100M

(c) Grant Thornton Japan. All rights reserved.

Japan Real Estate TaxationClient Case (Jack) - Calculation

Before investment

Employment Income 32M

Deductions 2M

Taxable income 30M

Income Tax 9.2M

After investment

Rental Income 3M

ExpensesInterestRepairsDepreciation

(2.25M)(3M)

(12M)

Taxable Income (Prop.) (14.25M)

Taxable Income (E) 30M

Taxable income 15.75M

Income Tax 3.7M

Annual Income Tax Savings: JPY5.5M(5-year: JPY27.5M)

(c) Grant Thornton Japan. All rights reserved.

Japan Real Estate TaxationClient Case (Jack) – Capital Gain

Sell in 2014 for JPY100MCost base (purchase price + depreciation) 20

Amount of gain (sale price – cost base) 80

Long-term / Non-resident CG tax payable (15%) 12

Long-term / Resident CG tax payable (20%) 16

Long-term / Resident CG tax payable (20%) with JPY30M deduction

10