Embed Size (px)

Citation preview

Bypasses for a Billion: improving healthcare availability for allLearnings from India

Bypasses for a Billion: improving healthcare availability for allLearnings from India

Managing DirectorHealthBridge Advisors Pvt. Ltd, India

Dr. Adheet Gogate

Learnings from IndiaLearnings from India

CONTENTS

Overview of healthcare in India

The Indian hospital free market

Winning strategies

Implications for South Africa

Overall Healthcare market

In Billion US $; 2012E

Total

80

Others

13

Pharma

10

Health delivery

57

THOUGH INDIA IS LARGE, ITS HOSPITAL INDUSTRY IS RELATIVELY SMALL…

The 2nd populous country in the world with the 7th largest area

• Population: 1.21 billion• Population growth rate: 1.3%• Sex ratio: 943• Population density: 382 per sq.km

2011

GEOGRAPHICAL AREA - 3, 287, 263 sq.km

DEMOGRAPHICS

delivery

Care delivery sector

In Billion US $

2020(E)

160

2012

57

2002

18

Source: Census india 2011, : IDFC Securities Hospital Sector November 2010, Hospital Market – India by Research on India, Aranca Research; World Bank data 2012; HBA Analysis

• GDP – 1.842 trillion US $• GDP/ Capita – 1489.24 US $• Purchasing Power Parity adjusted per

Capita – 3876 US $

• Population density: 382 per sq.km

2012ECONOMYHBA estimates

THE GROWTH IN INDIA’S HOSPITAL INDUSTRY IS DRIVEN BY STRONG, RESILIENT FACTORS

GDP growth

Trillion US $ 5.6

2020(E)2011

1.7

2001

0.5

Rise in NCDs

Multiple drivers creating a positive tide….

Prevalence rate as percentage of population

3.3

5

2.8

3.72005

2015(E)

Growing middle class

Income group in percent

6%

13%

34%

2009-10

2020(E)

Too little capacity

Beds per 10,000 population

China

36

S.Africa

28

USA

30

13

35

India WHO std

Source: Census india 2011, Macro economic outlook 2020, KPMG report, McKinsey report, IDFC Securities Hospital Sector November 2010, Hospital Market – India by Research on India, Aranca Research; PWC report; HBA Analysis;

India will have to build between 1.5 – 3

million beds in the next decade

India will have to build between 1.5 – 3

million beds in the next decade

CHD Diabtetes

3.32.8

0.20

Cancer

0.18

2015(E)

2001-02

2010

UNUSUAL FOR A COUNTRY OF THIS SIZE AND DIVERSITY, HEALTHCARE IS LARGELY PAID FOR OUT OF POCKET

Total healthcare spend very low…

% of GDP

17.9

9.7

Public

Private

2011

… with most people uninsured

13%

2%

Private insurance

Uninsured

Public insuranceImpact

% of Services delivered by value

80%

Public

Private

Percent; 2012

100% = 1.2 Billion people

Source: World Bank data, PWC report, Economic & Political Weekly 2004, HBA analysis, Centrum Healthcare sector October, 2010, KPMG analysis

USA China

1.2

India

3.95.2

2.3

2.92.7

8.2

85%2012

20%

Ability to access & consume Healthcare

dependant on the ability to pay

Ability to access & consume Healthcare

dependant on the ability to pay

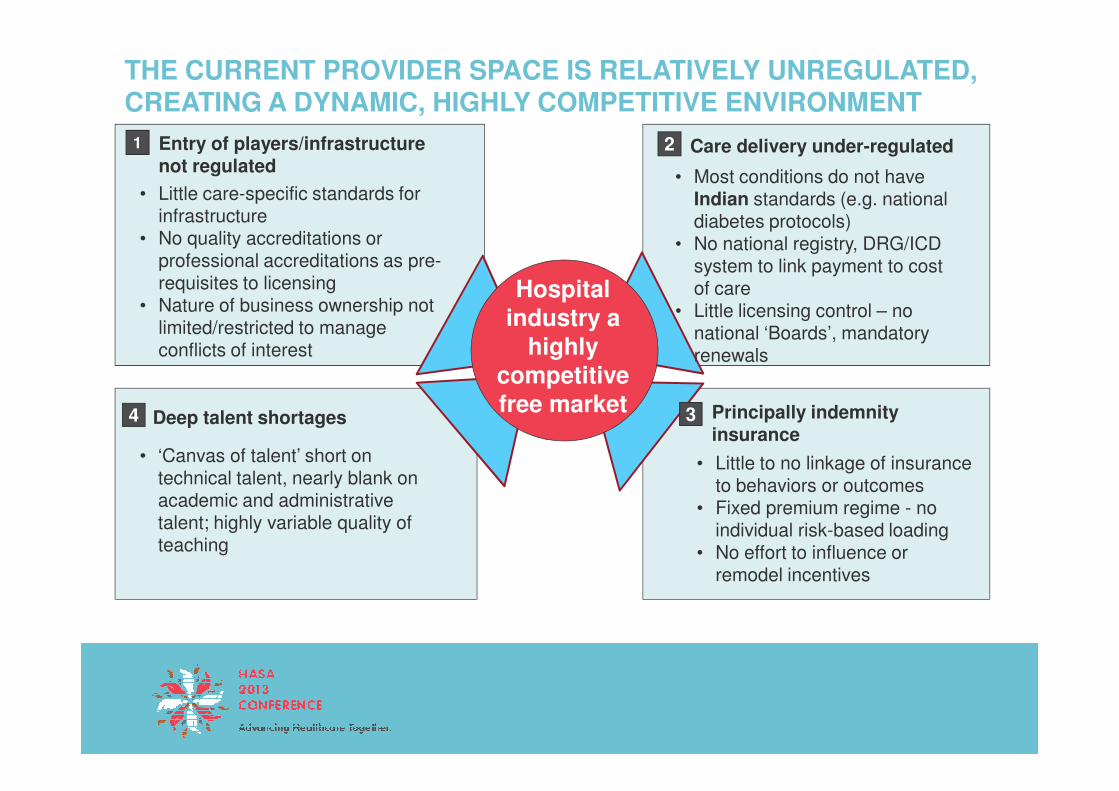

THE CURRENT PROVIDER SPACE IS RELATIVELY UNREGULATED, CREATING A DYNAMIC, HIGHLY COMPETITIVE ENVIRONMENT

Hospital industry a

highly competitive free market

Entry of players/infrastructure not regulated

1

• Little care-specific standards for infrastructure

• No quality accreditations or professional accreditations as pre-requisites to licensing

• Nature of business ownership not limited/restricted to manage conflicts of interest

Care delivery under-regulated2

• Most conditions do not have Indian standards (e.g. national diabetes protocols)

• No national registry, DRG/ICD system to link payment to cost of care

• Little licensing control – no national ‘Boards’, mandatory renewals

free market Principally indemnity insurance

3

• Little to no linkage of insurance to behaviors or outcomes

• Fixed premium regime - no individual risk-based loading

• No effort to influence or remodel incentives

Deep talent shortages4

• ‘Canvas of talent’ short on technical talent, nearly blank on academic and administrative talent; highly variable quality of teaching

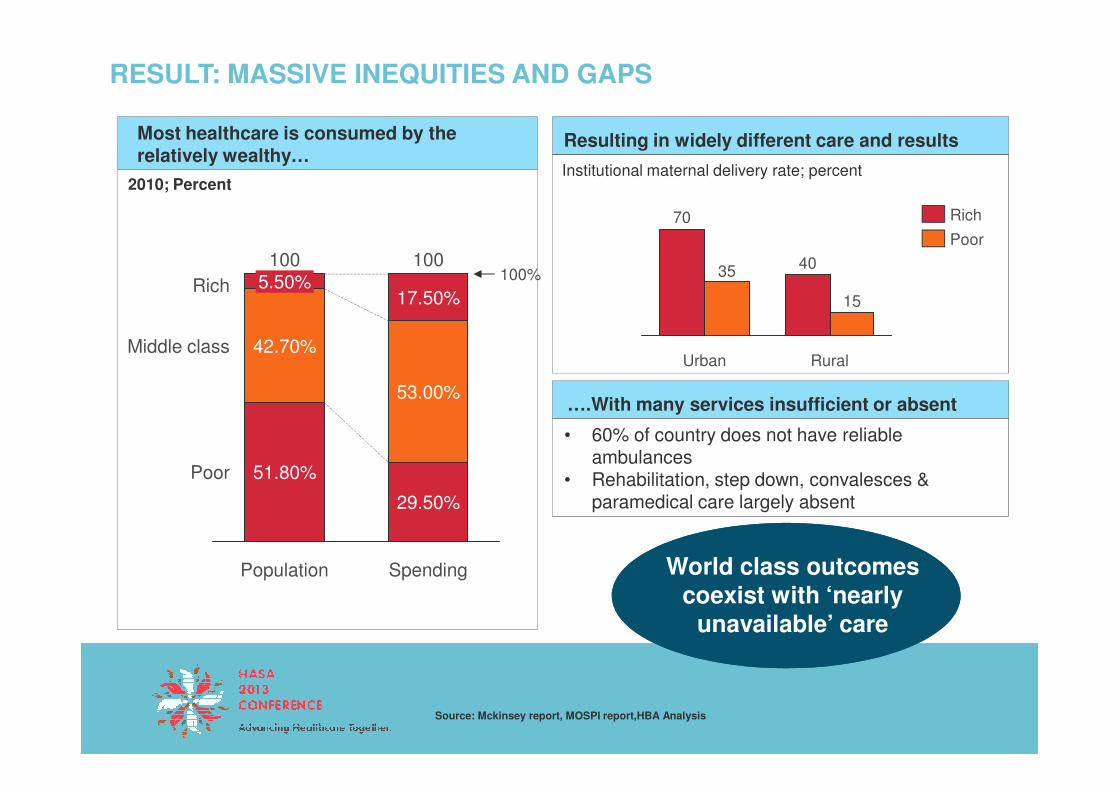

RESULT: MASSIVE INEQUITIES AND GAPS

….With many services insufficient or absent

Most healthcare is consumed by the relatively wealthy…

2010; Percent

Resulting in widely different care and results

Rural

15

40

Urban

35

70

Poor

Rich

Institutional maternal delivery rate; percent

Rich

Middle class 42.70%

5.50%100

100%100

17.50%

53.00%

Source: Mckinsey report, MOSPI report,HBA Analysis

….With many services insufficient or absent

• 60% of country does not have reliable ambulances

• Rehabilitation, step down, convalesces & paramedical care largely absent

World class outcomes coexist with ‘nearly

unavailable’ care

Population Spending

Poor 51.80%

29.50%

53.00%

CONTENTS

Overview of healthcare in India

The Indian hospital free market

Winning strategies

Implications for South Africa

DESPITE THESE PROBLEMS, THE INDIAN HEALTHCARE SYSTEM IS AN EXTRAORDINARY FREE-MARKET…

Opportunity

Segment

Competitive, diverse provider landscape• Plethora of business philosophies & business models - both

private & public• Variety of players competing in overlapping segments

Providers at (nearly) all price points• Premier hospitals (JCI standards) to low cost players in same

market – even in same neighborhood!• Variety of scale and capabilities

Competitive response

Pop. In Millions

Private spend (US$ Bn)

Poor 624

Year 2010

14.7

• Variety of scale and capabilities• Multiple price-service-quality alternatives at most price points

(‘middle class upwards’)

Supported by made in (and for) India suppliers and business models• Deep bench of domestic providers and manufacturers in all

areas• Innovative business models to keep prices low (e.g. reagent

rental)

Low, middle & upper middle

512 26.5

Rich 66 8.7

Source: McKinsey report, MOSPI report; HBA Analysis

EYE CARE : AS A RESULT, A RICH DIVERSITY OF PLAYERS HAS EMERGED…

Premium / upscale play

• Smaller, boutique

“For the poor” play

Expertise play

Mid-market+ SCALE play

Eye care system

• Mid to large • Large scale • Standardized • Comprehensive Configu-

Examples

• Smaller, boutique with 3-5 doctors

• Focused capabilities

• Luxury experience

• Mid to large scale with younger doctors

• Varied

• Basic

• Large scale with heavy technology

• World class

• Budget

• Standardized centers

• Focused on profitability

• Budget

• Comprehensive system

• Comprehensive

• Margin on all patients

• Socialized • Cross subsidy • Volume play • Cross subsidy

Configu-ration

Capabilities & Experience

Model

AS AN INDUSTRY, THESE PLAYERS HAVE ACHIEVED VERY IMPRESSIVE RESULTS

Cost at all price points…

… using innovative new techniques

With world-class results

Cataract surgery price; US$

SE/ Aravindfolding

300

SE/ Aravind Conventional

100

• Lowest cost surgeries done indigenously developed SICS techniques that have a far shorter learning curve

% complication rates for senior surgeons

Conventional Low cost SICS

1.0 1.1

USA 3500

TypicalNHS

1200

Vasan ’package’

550

curve

• Ability to do truly difficult surgeries. eg: vitrectomies, oculoplasties, prematurity retinopathy

Source: International federation of health plans, comparative price report; British Journal of Ophthalmology; Web reportsBr J Ophthalmol 2005;89:1073–1074. doi: 10.1136/bjo.2005.068213J Cataract Refract Surg 2012; 38:1360–1369 Q 2012 ASCRS and ESCRS

Conventional phaco

Low cost SICS technique

• SICS failure rates for younger surgeons less than a third for phaco – due to far shorter learning curve

• Very low infection rates, over 95% restoration of visual acuity to 6/18 or above

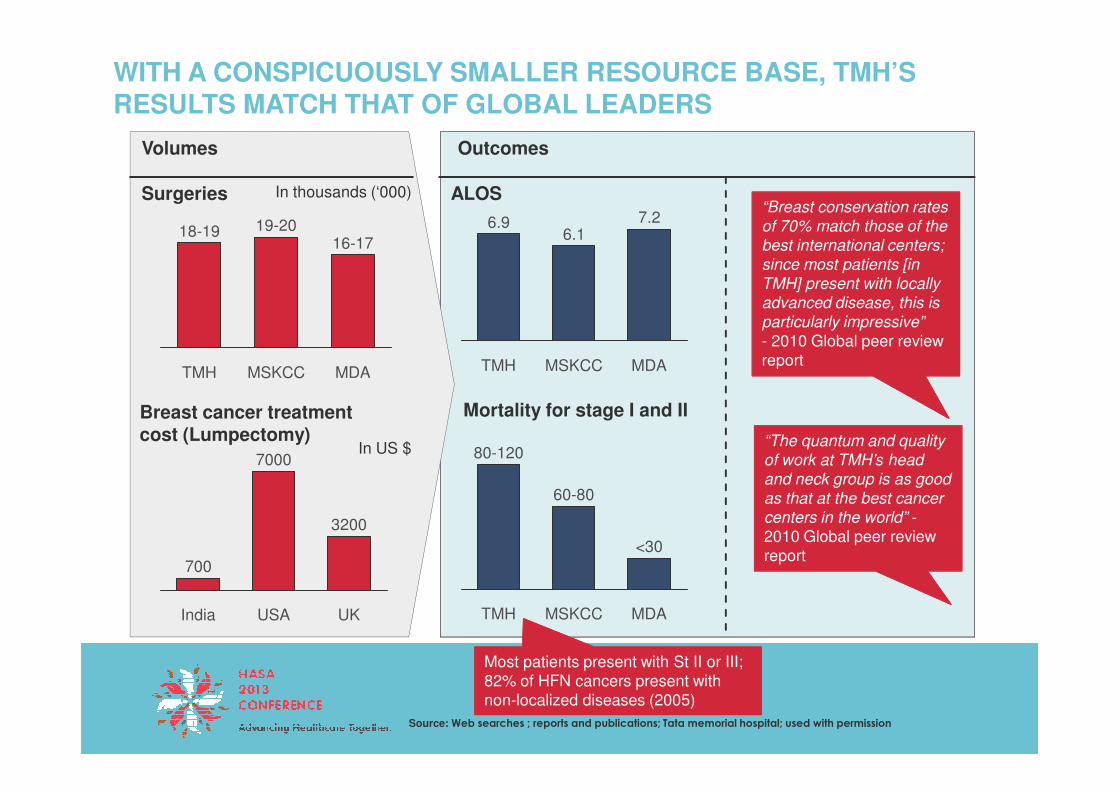

CENTERS OF EXCELLENCE SUCH AS TATA MEMORIAL(CANCER) CENTER ALSO EXIST IN THE PUBLIC SECTOR

Tata Memorial Centre: a first among equals

A unique business model

• 60 year old, 550 bedded cancer treatment & research hospital

• Among the first hospitals to move to a Disease Management Group(DMG) approach for treatment

• Provides own teaching, research

• Patients in higher payment classes subsidize poorer ones; telescopic pricing used to spread benefits in all departments

• “Business + economy” OPD with shared ICU/ OT’s keeps operating costs low

Source: TMH Annual Report

• Provides own teaching, research and care opportunities with full-suite, in-house services

• Pioneer in the field of tissue banking in India & is the only hospital in India to have an ISO 9001:2000 certified tissue bank .

• Part socialized – part paid/; staff + capex government paid; consumables charged

• Rigorous cost control (e.g. re-using consumables)

Nearly 70% of patients are

treated totally for free or at

subsidized prices

Nearly 70% of patients are

treated totally for free or at

subsidized prices

WITH A CONSPICUOUSLY SMALLER RESOURCE BASE, TMH’S RESULTS MATCH THAT OF GLOBAL LEADERS

Volumes

Surgeries

Outcomes

ALOS

16-17

MSKCC

19-20

TMH

18-19

MDA MDA

7.2

MSKCC

6.1

TMH

6.9

In thousands (‘000)“Breast conservation rates

of 70% match those of the

best international centers;

since most patients [in

TMH] present with locally

advanced disease, this is

particularly impressive”

- 2010 Global peer review report

Breast cancer treatment cost (Lumpectomy)

Mortality for stage I and II

700

7000

USA

3200

UKIndia

In US $

Source: Web searches ; reports and publications; Tata memorial hospital; used with permission

MDA

<30

MSKCC

60-80

TMH

80-120

Most patients present with St II or III; 82% of HFN cancers present with non-localized diseases (2005)

“The quantum and quality

of work at TMH’s head

and neck group is as good

as that at the best cancer

centers in the world” -2010 Global peer review report

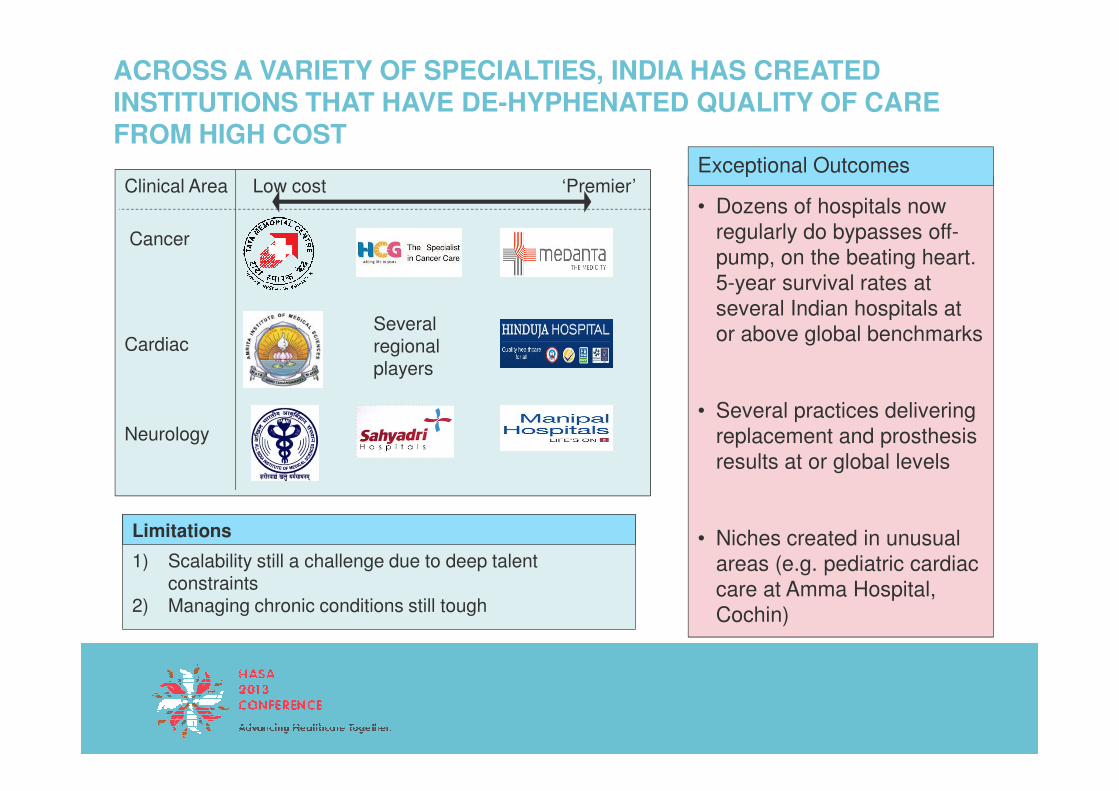

ACROSS A VARIETY OF SPECIALTIES, INDIA HAS CREATED INSTITUTIONS THAT HAVE DE-HYPHENATED QUALITY OF CARE FROM HIGH COST

Clinical Area

Cancer

Cardiac

Low cost ‘Premier’

Several regional players

Exceptional Outcomes

• Dozens of hospitals now regularly do bypasses off-pump, on the beating heart. 5-year survival rates at several Indian hospitals at or above global benchmarks

Neurology

Limitations

1) Scalability still a challenge due to deep talent constraints

2) Managing chronic conditions still tough

• Several practices delivering replacement and prosthesis results at or global levels

• Niches created in unusual areas (e.g. pediatric cardiac care at Amma Hospital, Cochin)

CONTENTS

Overview of healthcare in India

The Indian hospital free market

Winning strategies

Implications for South Africa

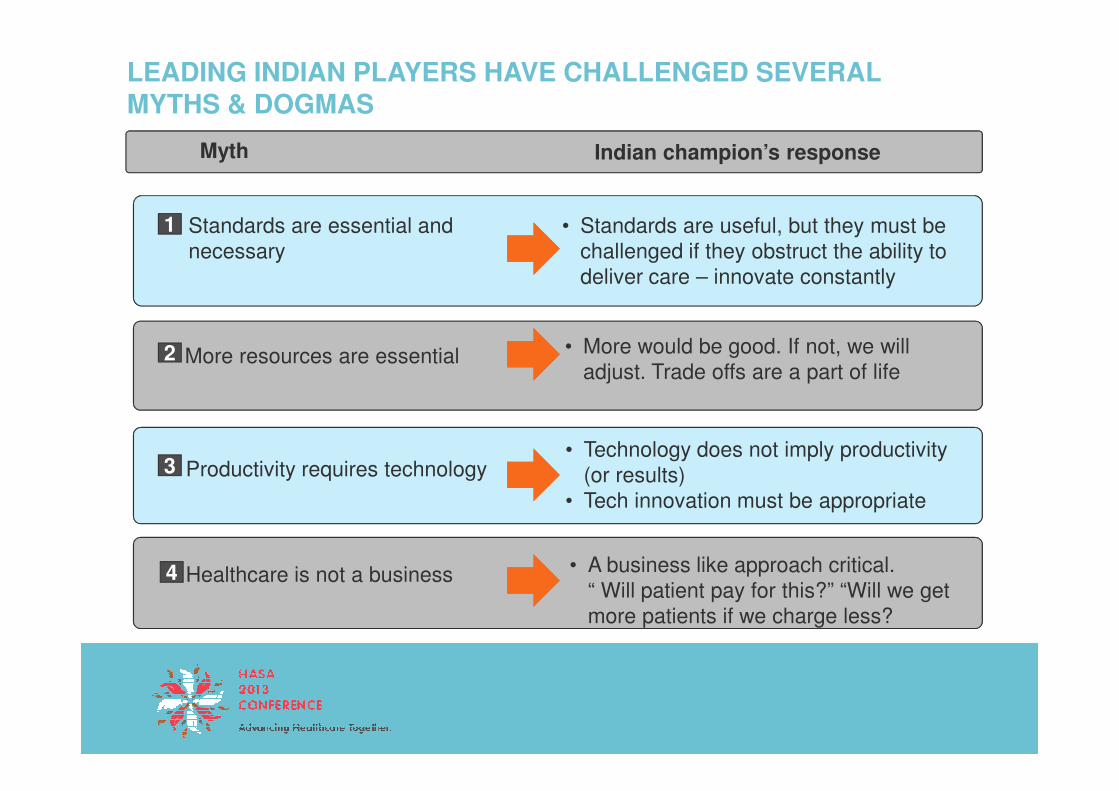

LEADING INDIAN PLAYERS HAVE CHALLENGED SEVERAL MYTHS & DOGMAS

• Standards are useful, but they must be challenged if they obstruct the ability to deliver care – innovate constantly

More resources are essential

1

2

Standards are essential and necessary

• More would be good. If not, we will adjust. Trade offs are a part of life

Myth Indian champion’s response

Productivity requires technology3• Technology does not imply productivity

(or results)• Tech innovation must be appropriate

Healthcare is not a business4 • A business like approach critical.“ Will patient pay for this?” “Will we get more patients if we charge less?

INDIAN PLAYERS HAVE INNOVATED RELENTLESSLY, CONSTANTLY CHALLENGING DOGMA AND NORMS

…leading to a service at any price point

Economy

Low costMaternityproviders

83

Price of normal labour; US$

Hospitals at all sizes Calibrated infrastructure

Sq ft per bed

Small200

Nursinghome

120

$ per patient bed

$150

1

Economynursing

home417

1,250

1,667"Birthing

suite"

SuperiorTrust

hospital

Luxuryhospital

1500

Majorhospital

600

Smallhospital

200

Source: Web Reports; client studies

$3500

INDIAN PROVIDERS HAVE TORN DOWN AND REDESIGNED CARE, FOCUSING ON PRODUCTIVITY OVER MARGINS

Physician productivityThe challenge : Deliver a Cataract Surgery for under 100 US $

Raise physician productivity

• Developed new small incision technique which requires less than 5 minutes to remove old lens

• Used Lean processes to raise productivity

Cataract surgeries per day per surgeon

Client A >60

2

CLIENT EXAMPLE

Source: Web Reports

• Create “continuous flow” of patients

Control capital costs

• Developed domestic low cost microscope with 20% fewer features for only 40% of price

• Developed domestic foldable lenses at a fraction of cost

Client B ~40

<20Typical global

number

THEY HAVE SHOWN THAT MUCH CAN BE DONE WITH JUDICIOUS USE OF TECHNOLOGY

The challenge

The plan : ADT @ global standards

Results

• 60 year old Trust hospital facing competitive pressure

• 10 year old basic HIS system

• Rigorously studied total process

• Devised paper & people solutions for all drivers of discharge process

• Piloted, tested, rolled out

From

• 0% planned discharges• 0% e-discharge cards• 5 hours to discharge

CLIENT EXAMPLE

3

• No EMR• No RFID/bar coding• No vacuum tubes

system

• Shallow talent pool

• Used minimal HIS/ IT fixes for electronic discharge summaries

• CEO-led, nurse driven 6 month program

• 80% pre-planned discharges

• 100% e-discharge cards• 45 min “sign to vacate”

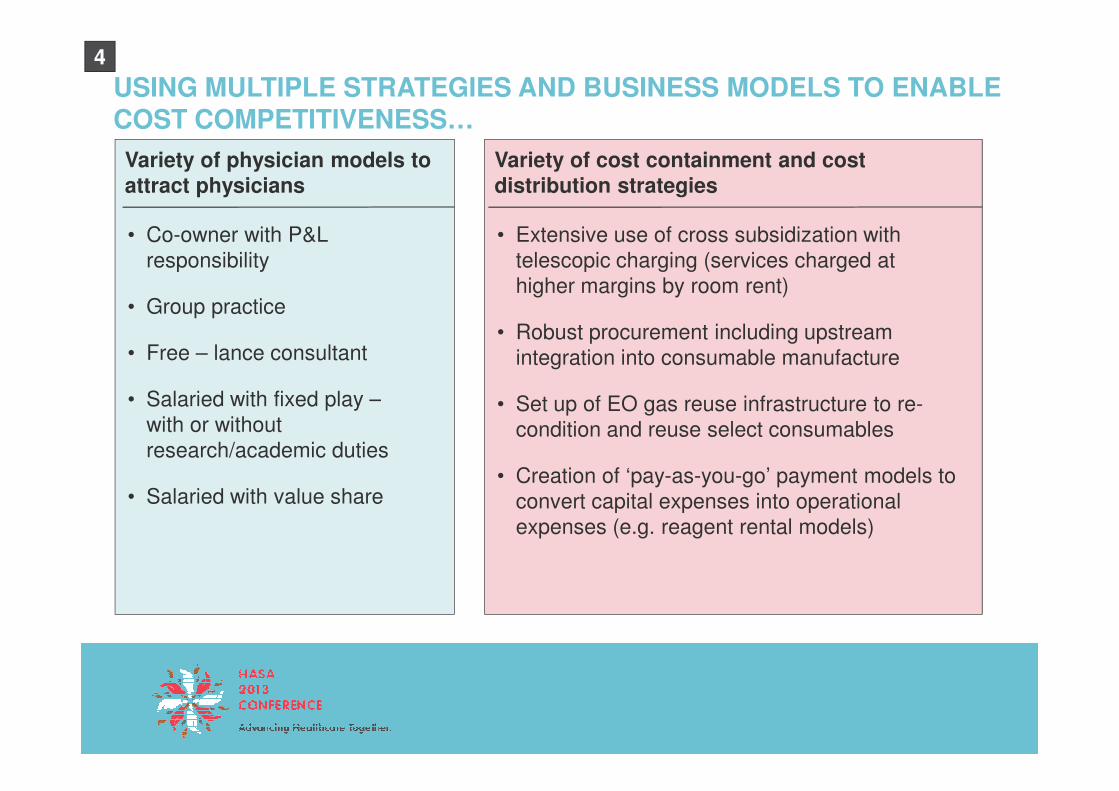

USING MULTIPLE STRATEGIES AND BUSINESS MODELS TO ENABLE COST COMPETITIVENESS…

Variety of physician models to attract physicians

• Co-owner with P&L responsibility

• Group practice

• Free – lance consultant

• Salaried with fixed play –

Variety of cost containment and cost distribution strategies

• Extensive use of cross subsidization with telescopic charging (services charged at higher margins by room rent)

• Robust procurement including upstream integration into consumable manufacture

• Set up of EO gas reuse infrastructure to re-

4

• Salaried with fixed play –with or without research/academic duties

• Salaried with value share

• Set up of EO gas reuse infrastructure to re-condition and reuse select consumables

• Creation of ‘pay-as-you-go’ payment models to convert capital expenses into operational expenses (e.g. reagent rental models)

CONTENTS

Overview of healthcare in India

The Indian hospital free market

Winning strategies

Implications for South Africa

IMPLICATIONS FOR SOUTH AFRICA

Expensive Healthcare ≠ Good Healthcare

Go from using price to determine the market to using the market to set the price

1

2

Don’t make the ‘best’ the enemy of the ‘better’

If you want to change the game, change the rules

3

4

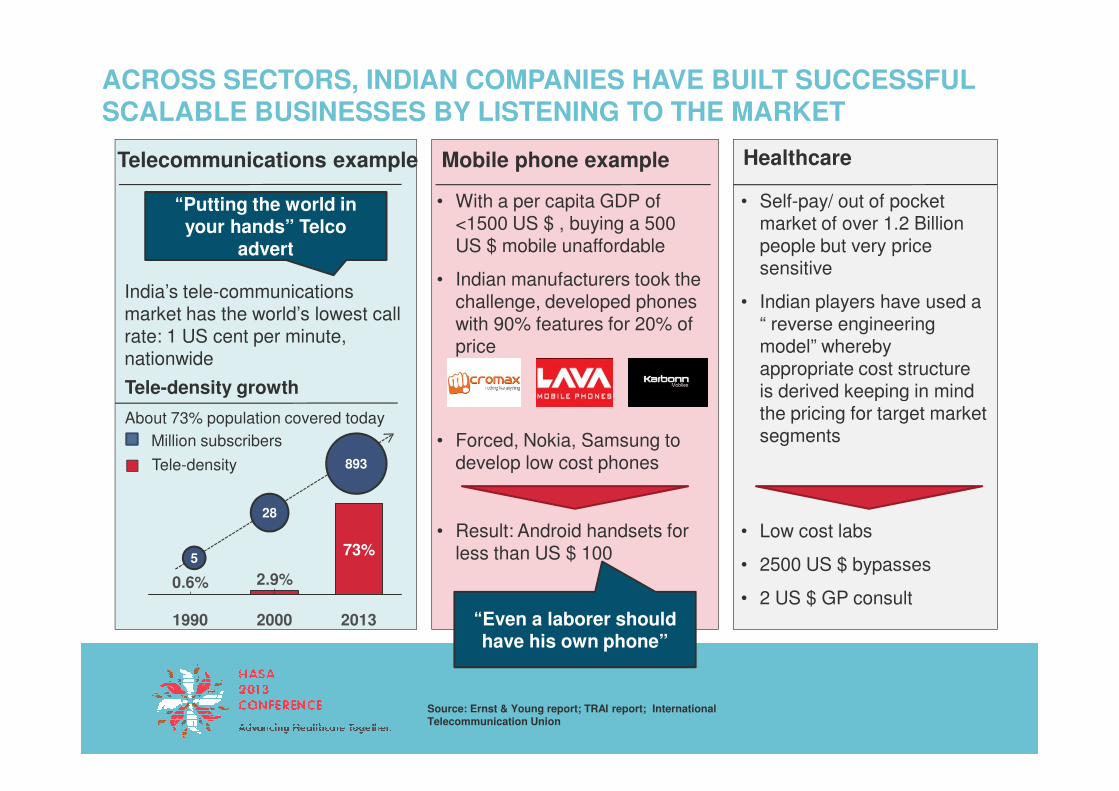

ACROSS SECTORS, INDIAN COMPANIES HAVE BUILT SUCCESSFUL SCALABLE BUSINESSES BY LISTENING TO THE MARKET

Telecommunications example Mobile phone example

• With a per capita GDP of <1500 US $ , buying a 500 US $ mobile unaffordable

• Indian manufacturers took the challenge, developed phones with 90% features for 20% of price

India’s tele-communications market has the world’s lowest call rate: 1 US cent per minute, nationwide

Tele-density growth

“Putting the world in your hands” Telco

advert

Healthcare

• Self-pay/ out of pocket market of over 1.2 Billion people but very price sensitive

• Indian players have used a “ reverse engineering model” whereby appropriate cost structure is derived keeping in mind Tele-density growth

About 73% population covered today

• Forced, Nokia, Samsung to develop low cost phones

• Result: Android handsets for less than US $ 100

“Even a laborer should have his own phone”

is derived keeping in mind the pricing for target market segments

• Low cost labs

• 2500 US $ bypasses

• 2 US $ GP consult2.9%

73%

0.6%

201320001990

Source: Ernst & Young report; TRAI report; International Telecommunication Union

Million subscribers

Tele-density

5

28

893

THE TATA NANO EXAMPLE: NOT MAKING THE BEST THE ENEMY OF THE BETTER

The challenge The NANO story

• The vision: A family car for 4 at under (US $ 2,000) “ One lakh”

• Small 2 cylinder engine

• Light, low cost chassis

• Basic equipment, single wiper

The result

• A car for INR 1,20,000

• With low running cost of less than 4 cents per mile

• Providing safe, dignified, affordable transportation to a family of 4

wiper

• Top speed 80 km/hr

• Costly, luxury features removed

• Several sophisticated safety system removed (ABS, ESP, Airbag, Sensor)

• Safe transport for 4

India has over 100,000 road

fatalities annually

Won’t survive on the

Autobahn but better than a

motorbike

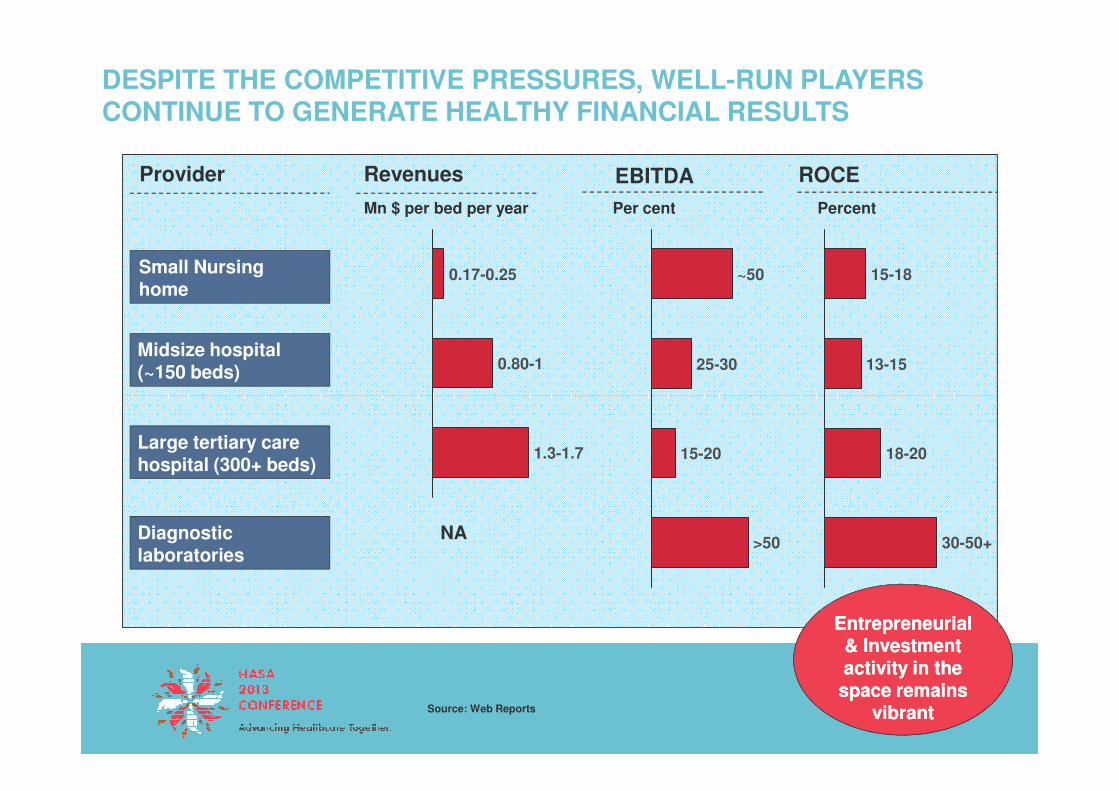

DESPITE THE COMPETITIVE PRESSURES, WELL-RUN PLAYERS CONTINUE TO GENERATE HEALTHY FINANCIAL RESULTS

ROCE

15-18

13-15

Provider Revenues

Small Nursing home

0.80-1

0.17-0.25

PercentMn $ per bed per year

Midsize hospital (~150 beds)

EBITDA

25-30

~50

Per cent

18-20

30-50+

1.3-1.7

Source: Web Reports

Large tertiary care hospital (300+ beds)

Diagnostic laboratories

>50

15-20

NA

Entrepreneurial & Investment activity in the

space remains vibrant

Entrepreneurial & Investment activity in the

space remains vibrant

IN SUMMARY

Policy and incentives have had profound implications for healthcare in India

Several challenges are similar: reducing variability in care outcomes in a nation with a huge spread in the ability to pay

Exposed to the cold-face of payment insecurity and Exposed to the cold-face of payment insecurity and competition, players have risen to the challenge and delivered exceptional performance

Changing the rules to change the game is essential; but the route adopted is as important as the destination

THANK YOU!

AS A RESULT, HEALTH CARE OUTCOMES IN INDIA ARE HIGHLY VARIABLE

• CABG results in several institutions that meet or exceed global outcomes

• >95% off-pump rates• > 90% RIMA/LIMA usage

• Presence of large transplant programs –with over 5,000 patients – in the not for profit sector!

….co exist with brillianceDismal healthcare outcome….

1648

5

17

Infant Mortality rate/ 1000 live births

20056

Maternal Mortality rate/ 100000 live births

profit sector!

• Pool of benchmark eye care institutions with deep skill base, benchmark outcomes at low prices

56

1237

15

10825647

TB Prevalence/ 100000 population

India U.K. China Brazil

Source: WHO Health statistics, 2010

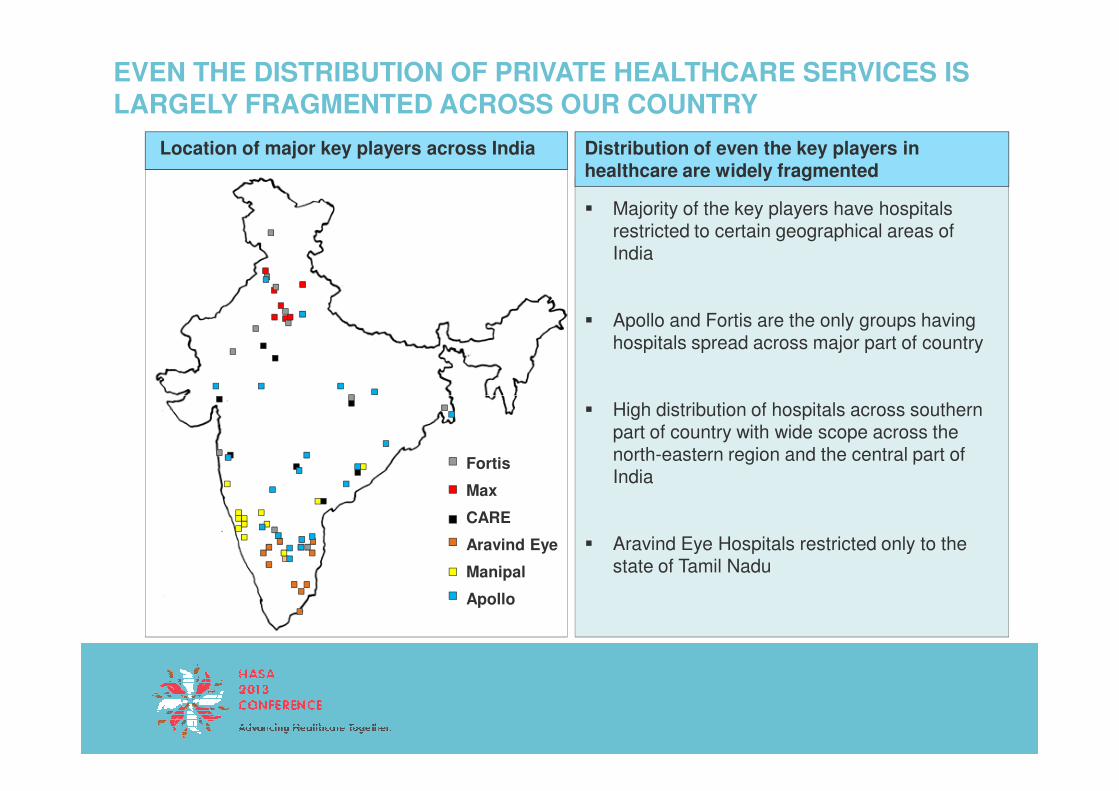

EVEN THE DISTRIBUTION OF PRIVATE HEALTHCARE SERVICES IS LARGELY FRAGMENTED ACROSS OUR COUNTRY

� Majority of the key players have hospitals restricted to certain geographical areas of India

� Apollo and Fortis are the only groups having hospitals spread across major part of country

Distribution of even the key players in healthcare are widely fragmented

Location of major key players across India

Fortis

Max

CARE

Aravind Eye

Manipal

Apollo

� High distribution of hospitals across southern part of country with wide scope across the north-eastern region and the central part of India

� Aravind Eye Hospitals restricted only to the state of Tamil Nadu