Embed Size (px)

Citation preview

By

Glenn R. Mueller, Ph.D. – Professor

Kyle Cascioli – Adjunct Professor

U.S. Commercial Debt Markets

Evolution

&

Dislocation

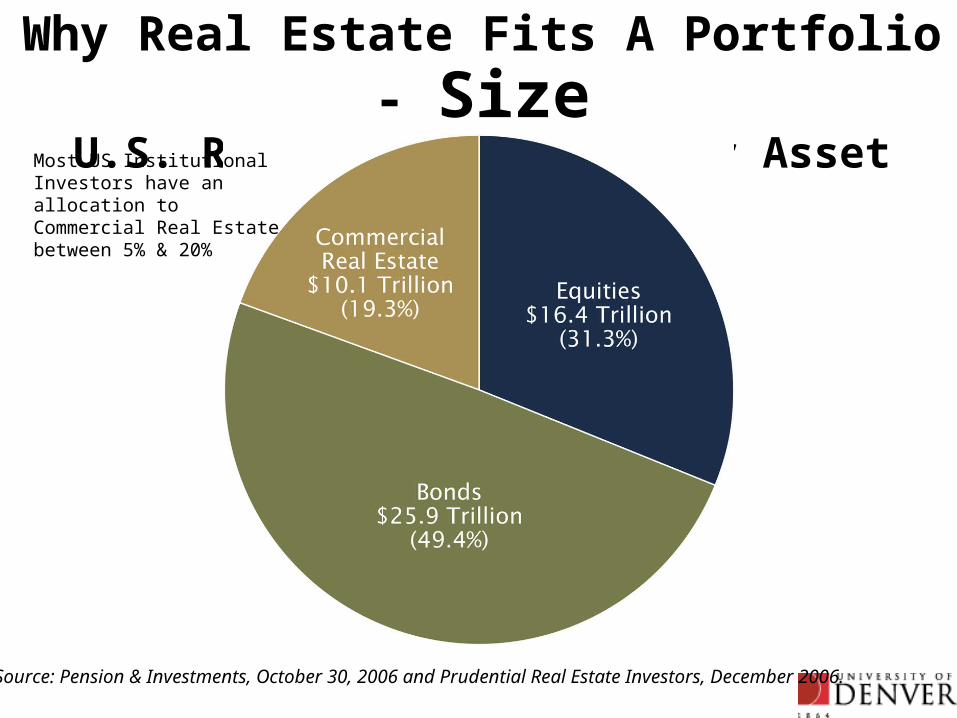

Why Real Estate Fits A Portfolio - SizeU.S. Real Estate vs. Other Asset Classes - 12/06

Source: Pension & Investments, October 30, 2006 and Prudential Real Estate Investors, December 2006.

Most US Institutional Investors have an allocation to Commercial Real Estate between 5% & 20%

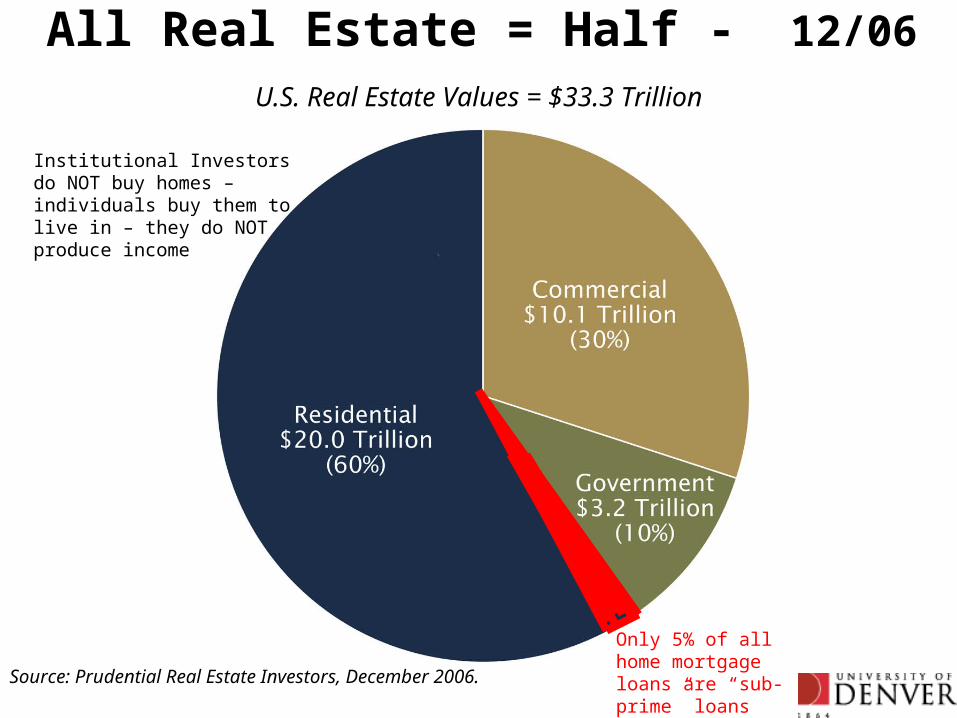

All Real Estate = Half - 12/06

Source: Prudential Real Estate Investors, December 2006.

U.S. Real Estate Values = $33.3 Trillion

Institutional Investors do NOT buy homes – individuals buy them to live in – they do NOT produce income

Only 5% of all home mortgage loans are “sub-prime” loans

$ CAPITAL $•DEBT is Major component of Real Estate

•Historically private loan sources (Banks, Ins Co’s)

•Major access to public CMBS markets in 1990s

•Cross boarder investing grows in 2000s

•Size and health of markets drives future values

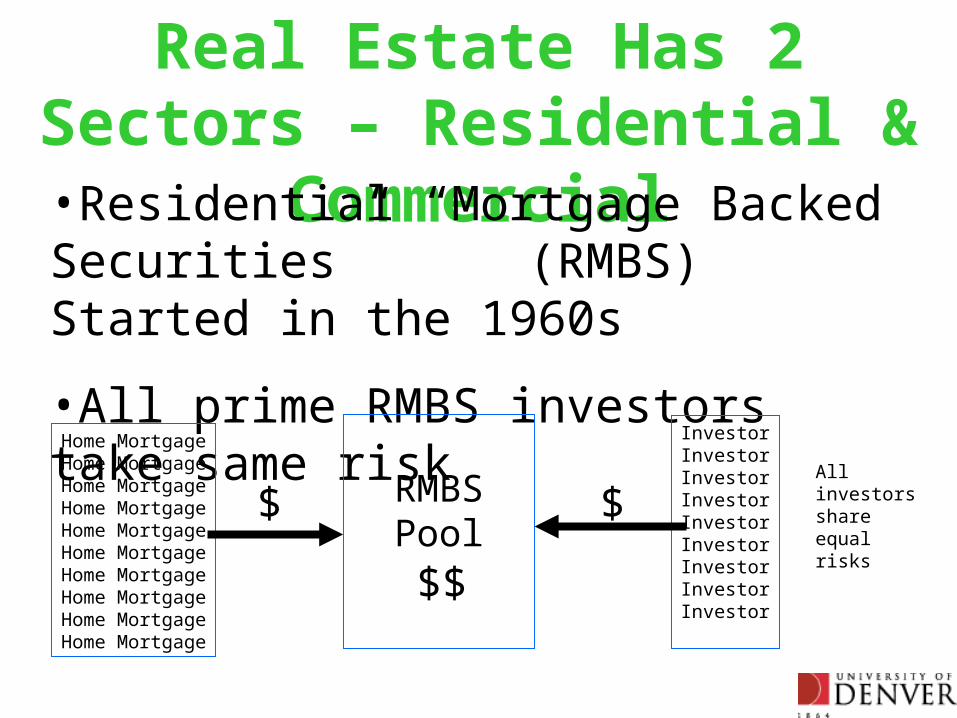

Real Estate Has 2 Sectors – Residential & Commercial

•Residential “Mortgage Backed Securities” (RMBS) Started in the 1960s

•All prime RMBS investors take same risk

Home MortgageHome MortgageHome MortgageHome MortgageHome MortgageHome MortgageHome MortgageHome MortgageHome MortgageHome Mortgage

RMBSPool

InvestorInvestorInvestorInvestorInvestorInvestorInvestorInvestorInvestor

$$

$$

All investors share equal risks

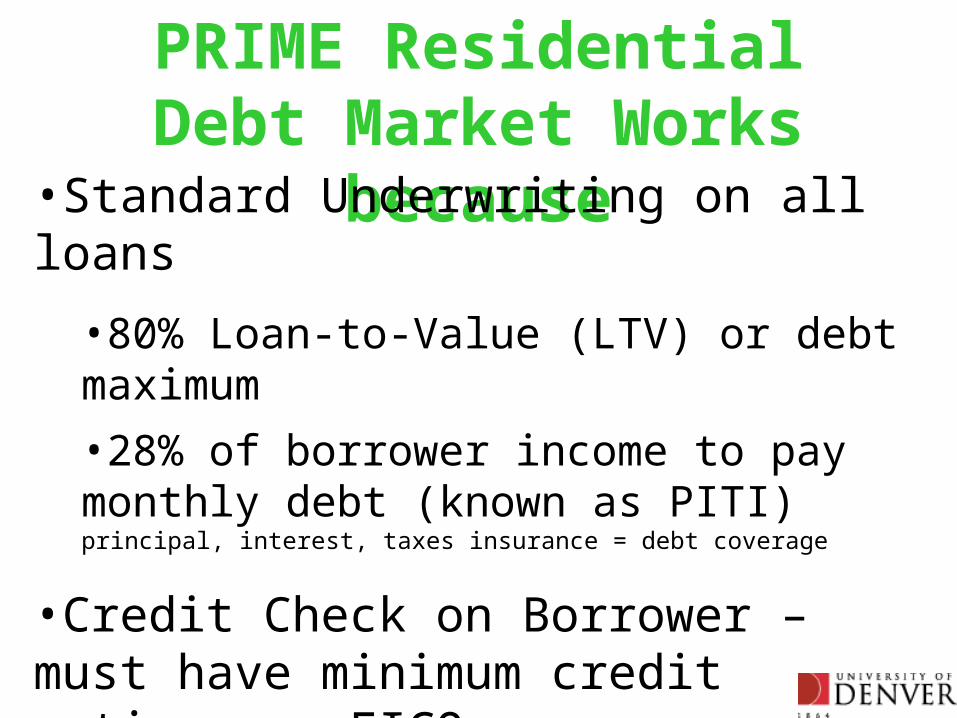

PRIME ResidentialDebt Market Works because

•Standard Underwriting on all loans

•80% Loan-to-Value (LTV) or debt maximum

•28% of borrower income to pay monthly debt (known as PITI) principal, interest, taxes insurance = debt coverage

•Credit Check on Borrower – must have minimum credit rating- or FICO score

•64% of U.S. population meets prime criteria

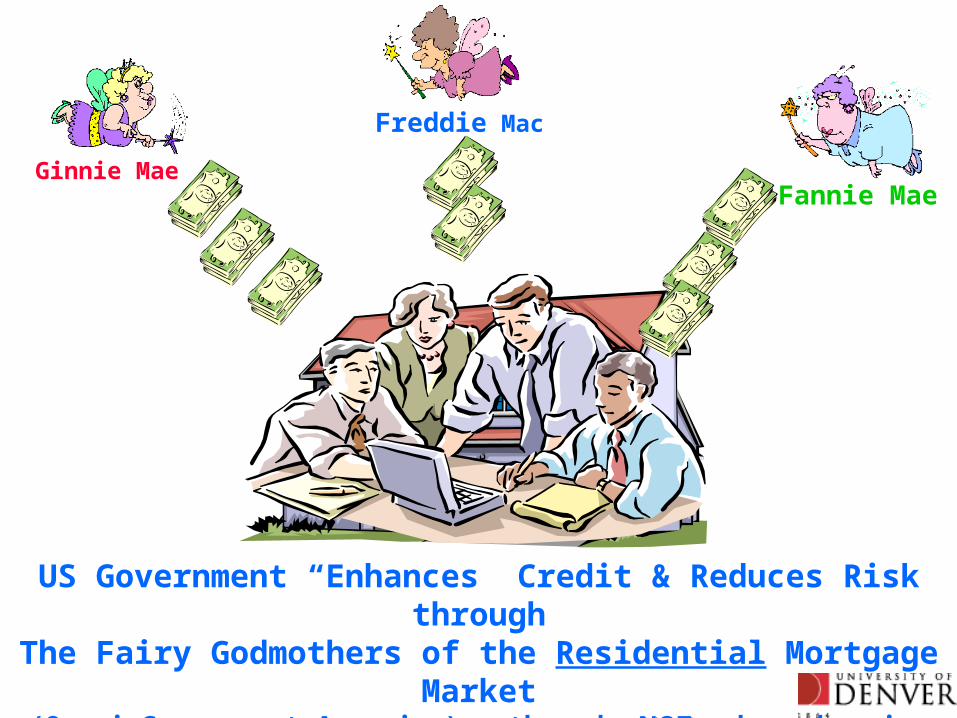

US Government “Enhances” Credit & Reduces Risk through

The Fairy Godmothers of the Residential Mortgage Market

(Quasi-Government Agencies) – they do NOTNOT make sub-prime loans

Freddie Mac

Fannie MaeGinnie Mae

SO – How did sub-prime loans start?

• A LONG story– Starts with CMBS in 1989– CMBS evolves or “mutates” to CDOs in 1999– Was function of cheap $ circa 2005

http://yegsz.com/Yieldsz/index2.html

– Creative Wall Street Bankers figure out how to put junk into CDOs and get part of the CDO traunche rated as AAA, AA, & A bonds

COMMERCIAL CMBS is DifferentMany Types of Commercial Loans in CMBS

• Multifamily Housing

• Retail

• Office

• Industrial / Warehouse

• Hospitality

• Health Care

• Self-Storage

• Mobile Home Parks

• Credit Tenant Leases

• Mixed-Use

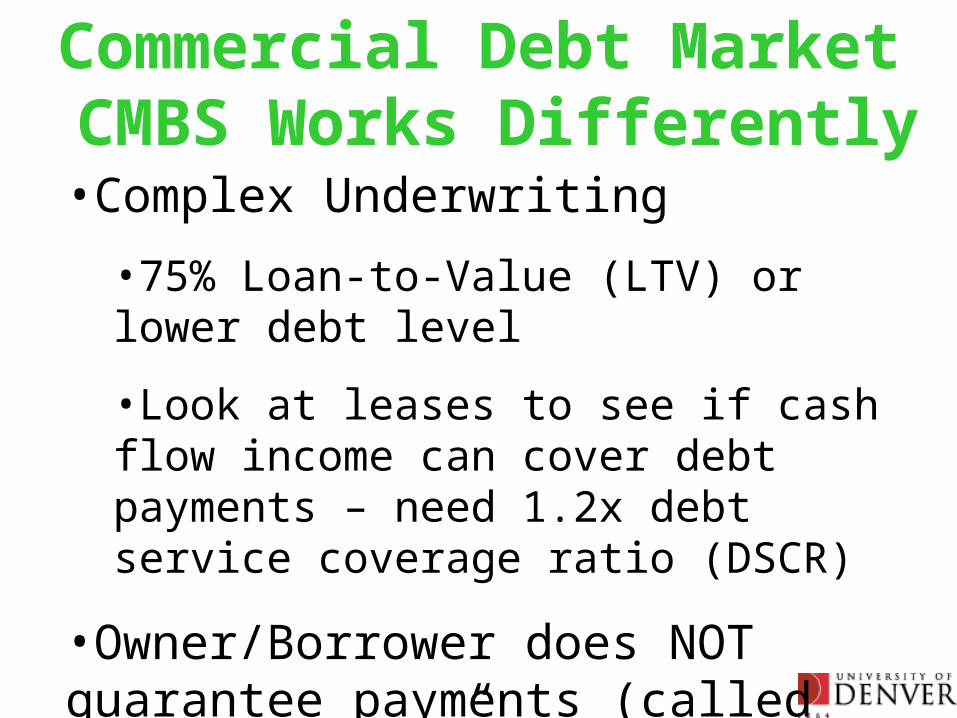

Commercial Debt Market CMBS Works Differently

•Complex Underwriting

•75% Loan-to-Value (LTV) or lower debt level

•Look at leases to see if cash flow income can cover debt payments – need 1.2x debt service coverage ratio (DSCR)

•Owner/Borrower does NOT guarantee payments (called “non-recourse” lending)

•Local market knowledge important

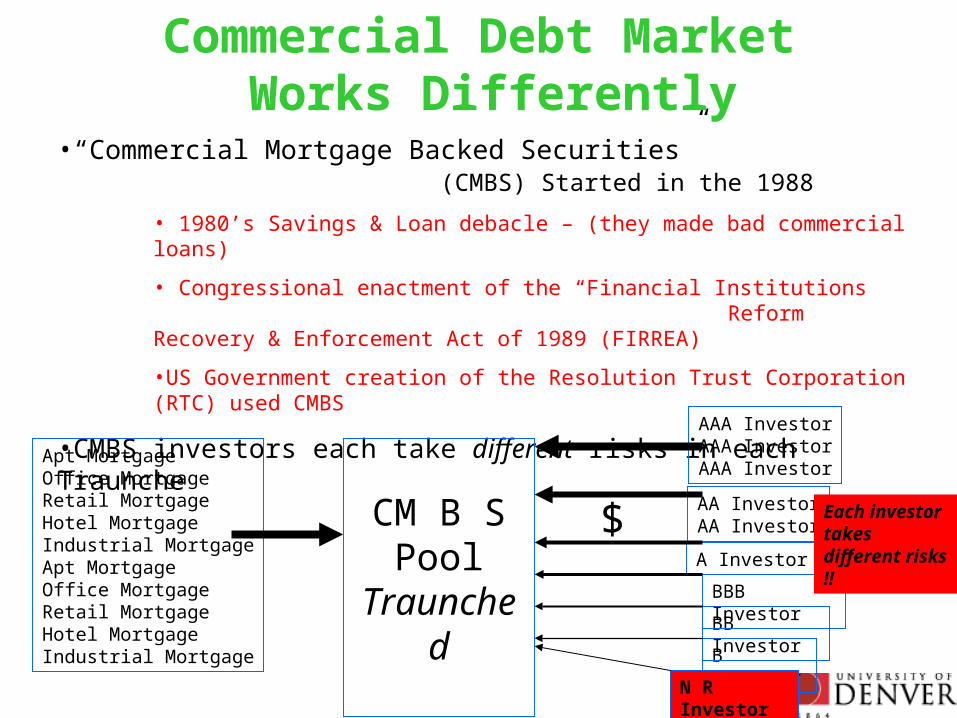

•“Commercial Mortgage Backed Securities” (CMBS) Started in the 1988

• 1980’s Savings & Loan debacle – (they made bad commercial loans)

• Congressional enactment of the “Financial Institutions Reform Recovery & Enforcement Act of 1989 (FIRREA)

•US Government creation of the Resolution Trust Corporation (RTC) used CMBS

•CMBS investors each take different risks in each Traunche

Apt MortgageOffice MortgageRetail MortgageHotel MortgageIndustrial MortgageApt MortgageOffice MortgageRetail MortgageHotel MortgageIndustrial Mortgage

CM B SPool

Traunched

AAA InvestorAAA InvestorAAA Investor

$AA InvestorAA Investor

A Investor

B Investor

N R Investor

BB Investor

BBB Investor

Commercial Debt Market Works Differently

Each investor takes different risks !!

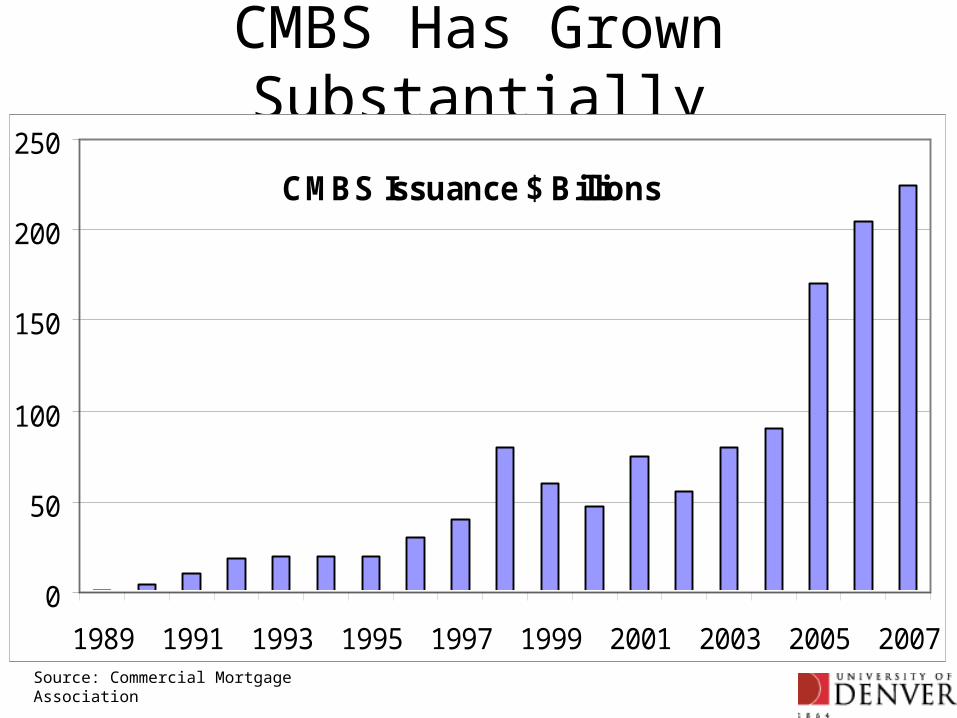

CMBS Has Grown Substantially

CMBS Issuance $ Billions

0

50

100

150

200

250

1989 1991 1993 1995 1997 1999 2001 2003 2005 2007Source: Commercial Mortgage Association

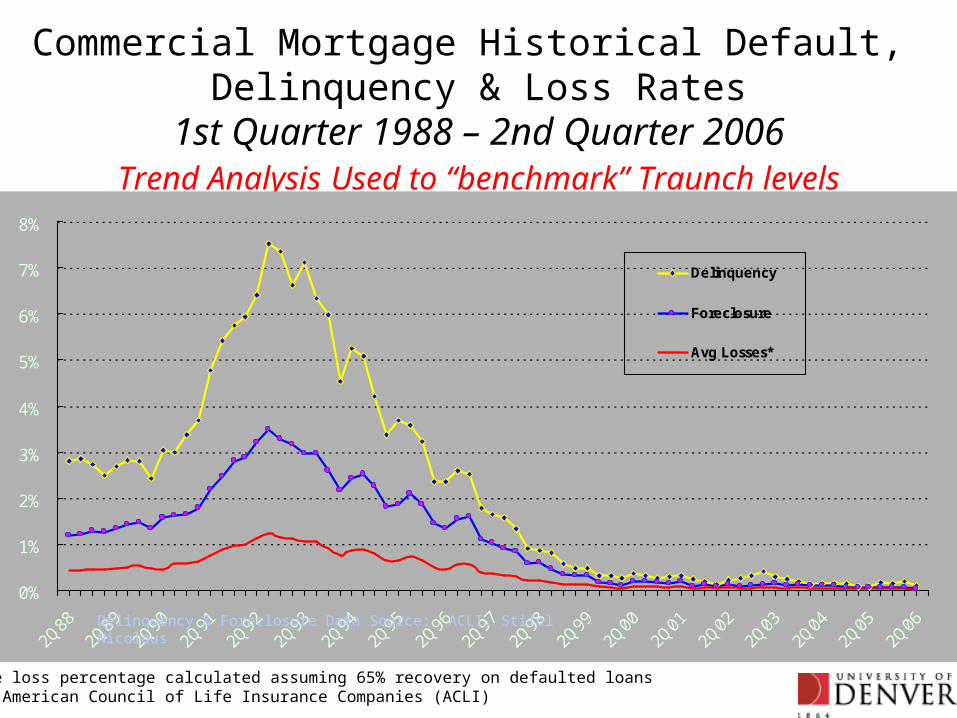

Commercial Mortgage Historical Default, Delinquency & Loss Rates

1st Quarter 1988 – 2nd Quarter 2006Trend Analysis Used to “benchmark” Traunch levels

0%

1%

2%

3%

4%

5%

6%

7%

8%

Delinquency

Foreclosure

Avg Losses*

Delinquency & Foreclosure Data Source: ACLI, Stifel Nicolaus

*Average loss percentage calculated assuming 65% recovery on defaulted loansSource: American Council of Life Insurance Companies (ACLI)

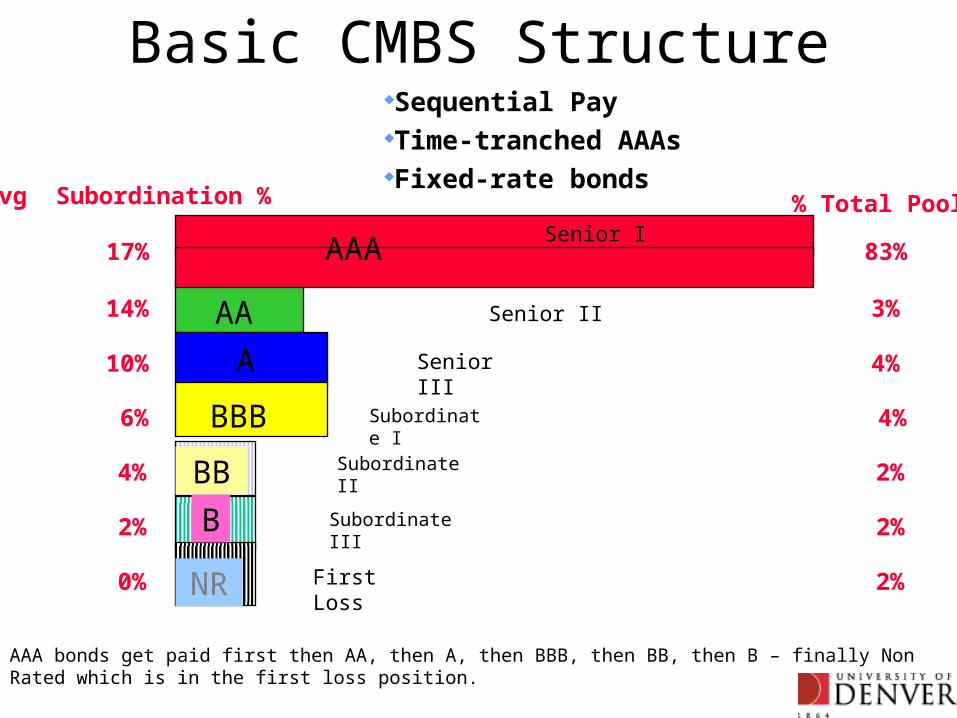

Basic CMBS StructureSequential PayTime-tranched

AAAs Fixed-rate bonds

AAA

A

BBB

BB

B

NR

IO

Avg Subordination %

17%

14%

10%

6%

4%

2%

0%

Senior I

Senior II

Senior III

Subordinate I

Subordinate II

Subordinate III

First Loss

AA

AAA

AAA bonds get paid first then AA, then A, then BBB, then BB, then B – finally Non Rated which is in the first loss position.

% Total Pool

83%

3%

4%

4%

2%

2%

2%

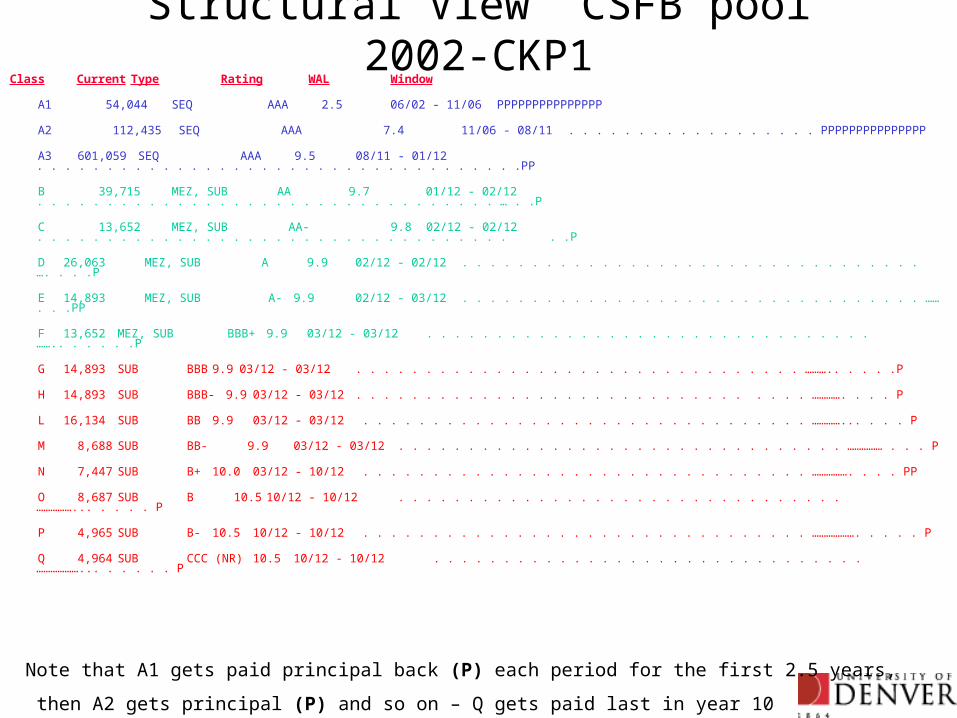

Structural View CSFB pool 2002-CKP1Class Current Type Rating WAL Window A1 54,044 SEQ AAA 2.5 06/02 - 11/06 PPPPPPPPPPPPPPP A2 112,435 SEQ AAA 7.4 11/06 - 08/11 . . . . . . . . . . . . . . . . . . PPPPPPPPPPPPPPP A3 601,059 SEQ AAA 9.5 08/11 - 01/12 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .PP B 39,715 MEZ, SUB AA 9.7 01/12 - 02/12 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . … . .P C 13,652 MEZ, SUB AA- 9.8 02/12 - 02/12 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .P D 26,063 MEZ, SUB A 9.9 02/12 - 02/12 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . …. . . .P

E 14,893 MEZ, SUB A- 9.9 02/12 - 03/12 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . …… . . .PP F 13,652 MEZ, SUB BBB+ 9.9 03/12 - 03/12 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . …….. . . . . .P G 14,893 SUB BBB 9.9 03/12 - 03/12 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ……….. . . . .P H 14,893 SUB BBB- 9.9 03/12 - 03/12 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . …………. . . . P L 16,134 SUB BB 9.9 03/12 - 03/12 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . …………... . . . P M 8,688 SUB BB- 9.9 03/12 - 03/12 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . …………… . . . P N 7,447 SUB B+ 10.0 03/12 - 10/12 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ……………. . . . PP O 8,687 SUB B 10.5 10/12 - 10/12 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ……………... . . . . P P 4,965 SUB B- 10.5 10/12 - 10/12 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ………………. . . . .

P

Q 4,964 SUB CCC (NR) 10.5 10/12 - 10/12 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ………………... . . . . . P

Note that A1 gets paid principal back (P) each period for the first 2.5 years,

then A2 gets principal (P) and so on – Q gets paid last in year 10

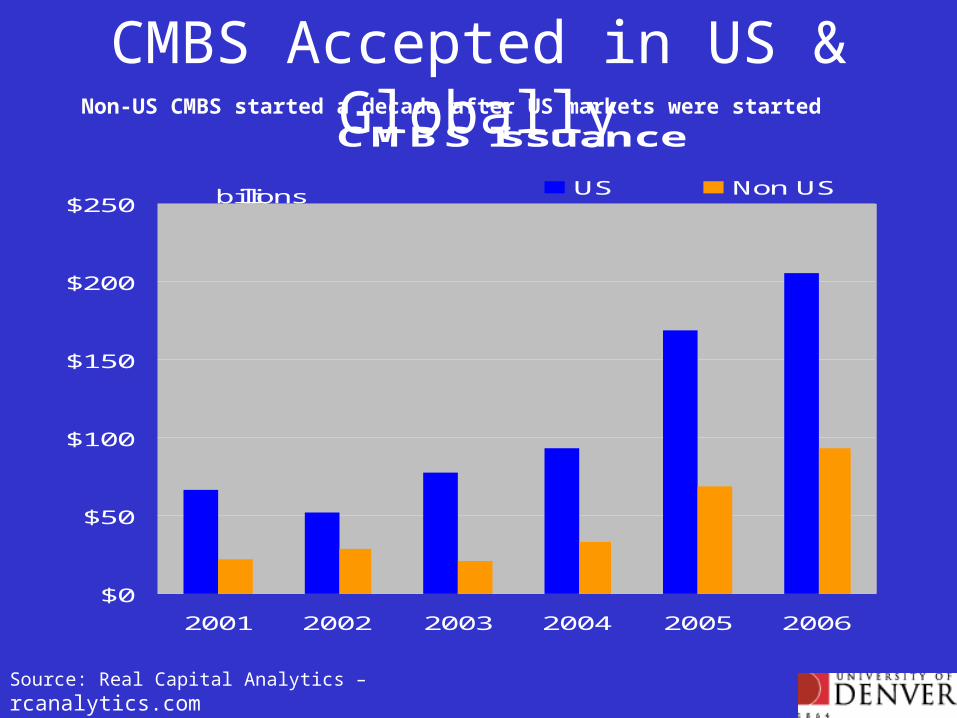

CMBS Issuance

$0

$50

$100

$150

$200

$250

2001 2002 2003 2004 2005 2006

billions US Non US

CMBS Accepted in US & Globally

Source: Real Capital Analytics – rcanalytics.com

Non-US CMBS started a decade after US markets were started

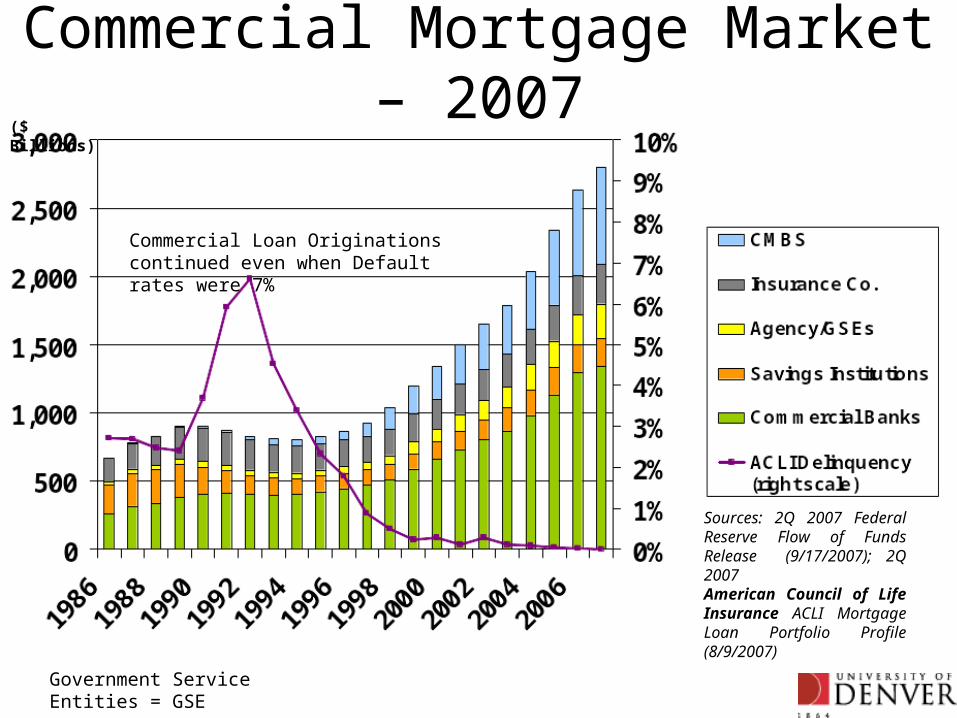

Commercial Mortgage Market – 2007

Sources: 2Q 2007 Federal Reserve Flow of Funds Release (9/17/2007); 2Q 2007American Council of Life Insurance ACLI Mortgage Loan Portfolio Profile (8/9/2007)

($ Billions)

Commercial Loan Originations continued even when Default rates were 7%

Government Service Entities = GSE

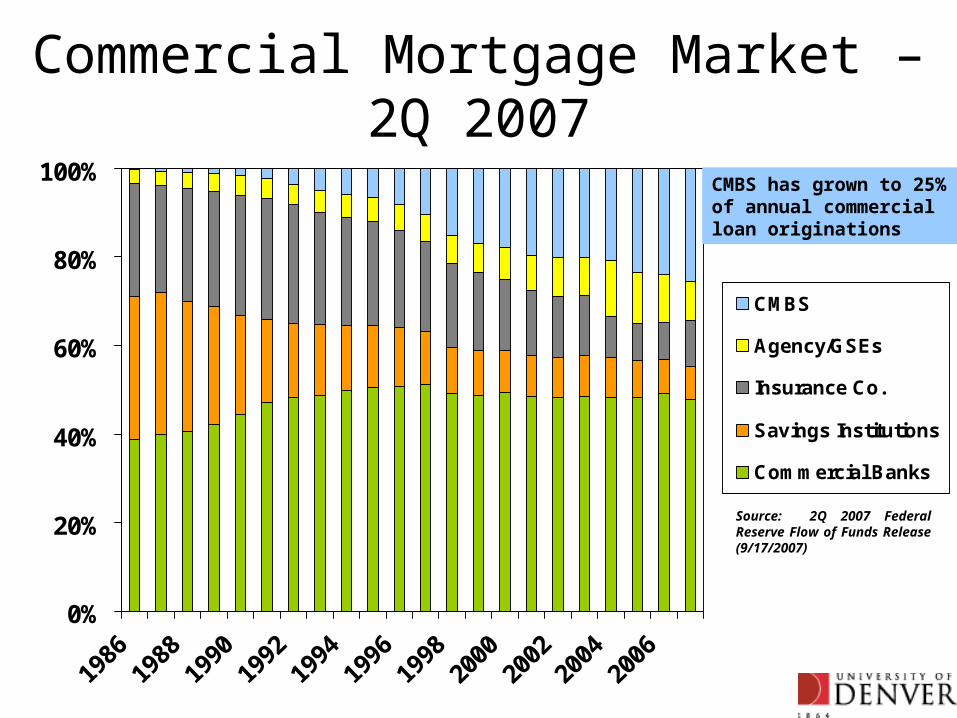

Commercial Mortgage Market – 2Q 2007

0%

20%

40%

60%

80%

100%

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

CMBS

Agency/GSEs

Insurance Co.

Savings Institutions

Commercial Banks

Source: 2Q 2007 Federal Reserve Flow of Funds Release (9/17/2007)

CMBS has grown to 25% of annual commercial loan originations

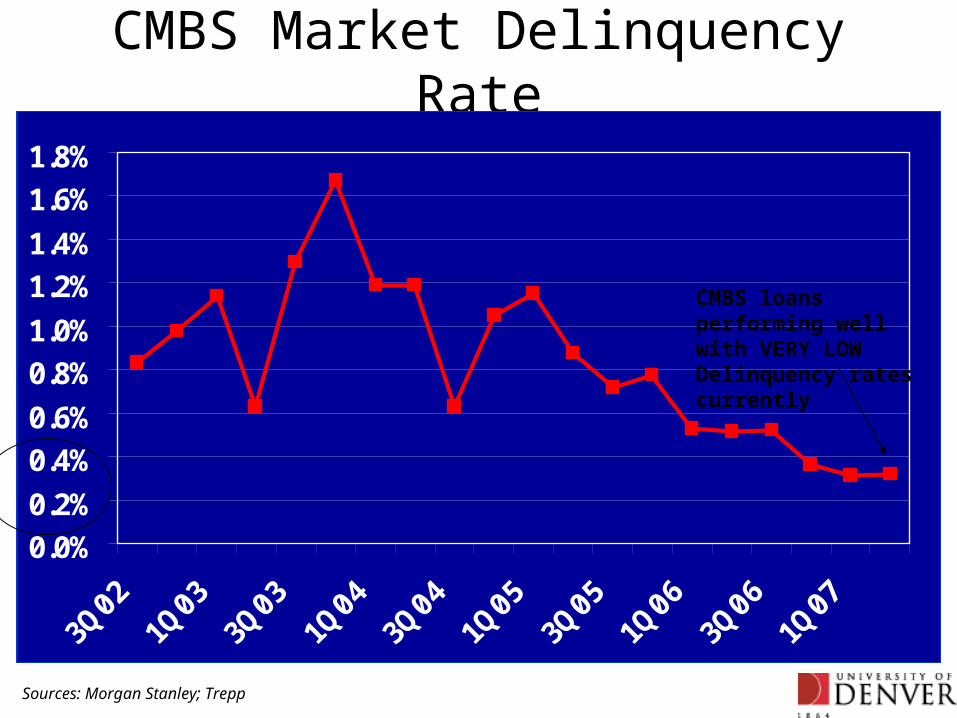

CMBS Market Delinquency Rate

Sources: Morgan Stanley; Trepp

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

1.4%

1.6%

1.8%

3Q02

1Q03

3Q03

1Q04

3Q04

1Q05

3Q05

1Q06

3Q06

1Q07

CMBS loans performing well with VERY LOW Delinquency rates currently

0%

5%

10%

15%

20%

25%

30%

35%

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

1Q20

07

Source: Merrill Lynch

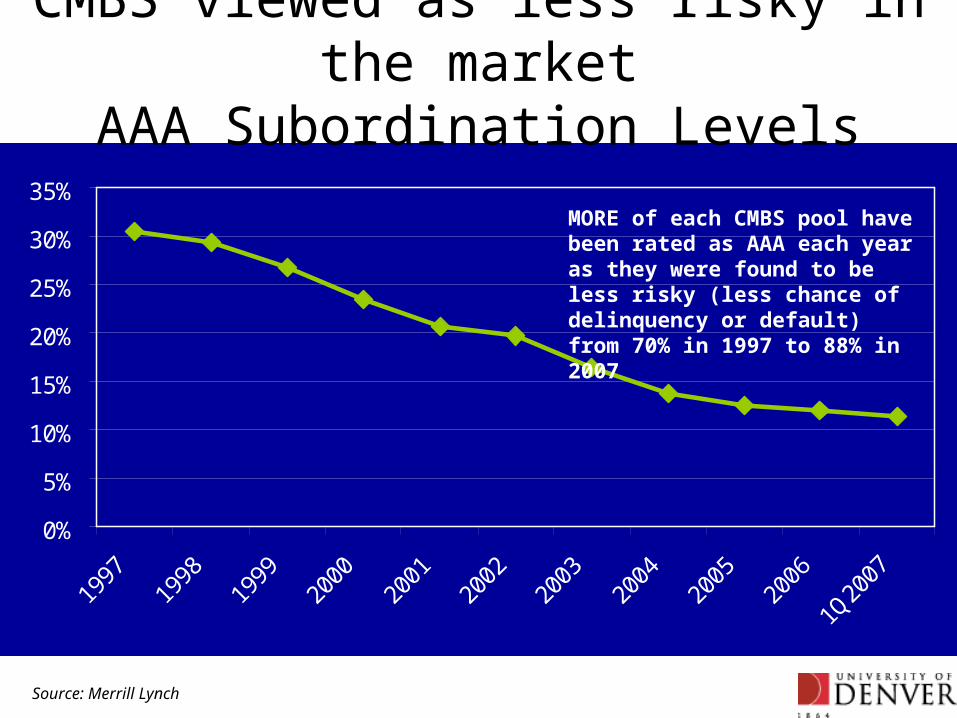

CMBS viewed as less risky in the marketAAA Subordination Levels

MORE of each CMBS pool have been rated as AAA each year as they were found to be less risky (less chance of delinquency or default) from 70% in 1997 to 88% in 2007

0%10%20%30%40%50%60%70%80%90%

Partial Term IO

Full Term IO

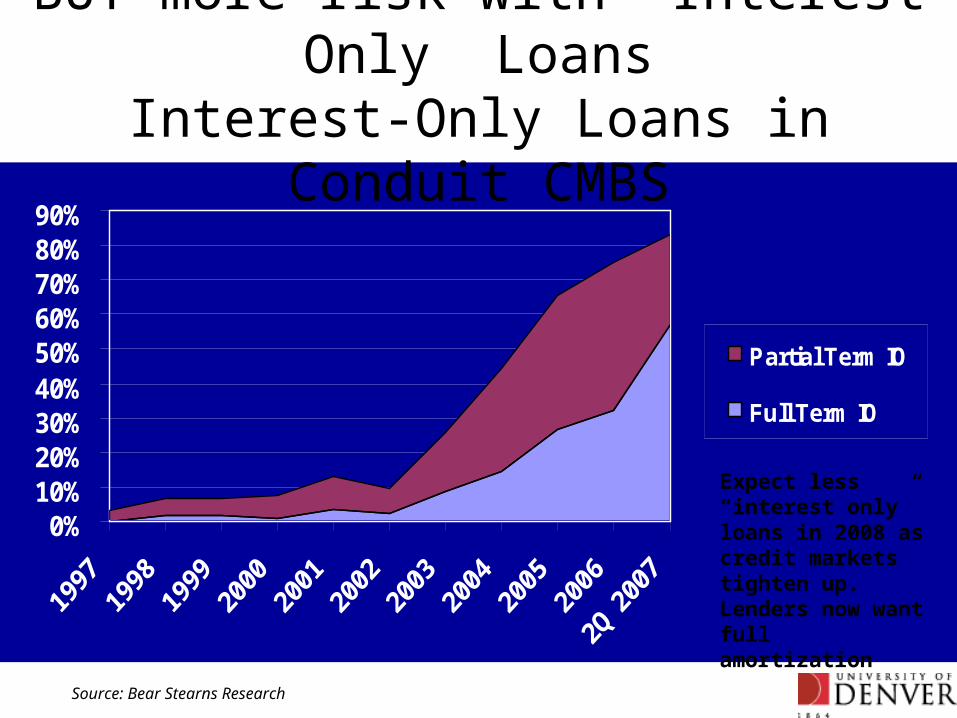

BUT more risk with “Interest Only” LoansInterest-Only Loans in Conduit CMBS

Source: Bear Stearns Research

Expect less “interest only” loans in 2008 as credit markets tighten up. Lenders now want full amortization

0

100

200

300

400

500

600

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

AAA - 10Yr

BBB

BBB-

Sub-Prim

e

Mel

tdown!

BUT Markets don’t know how to price“new” risks

CMBS Spreads to Treasury

Source: Citigroup Global Markets

Russia

n

Debt C

risis

CMBS AAA risks

– not very high

AAA rates jump from 75 to 200

BBB- jump from 125 to 400

AAA rates jump from 75 to 125

BBB- jump from 150 to 525 !!

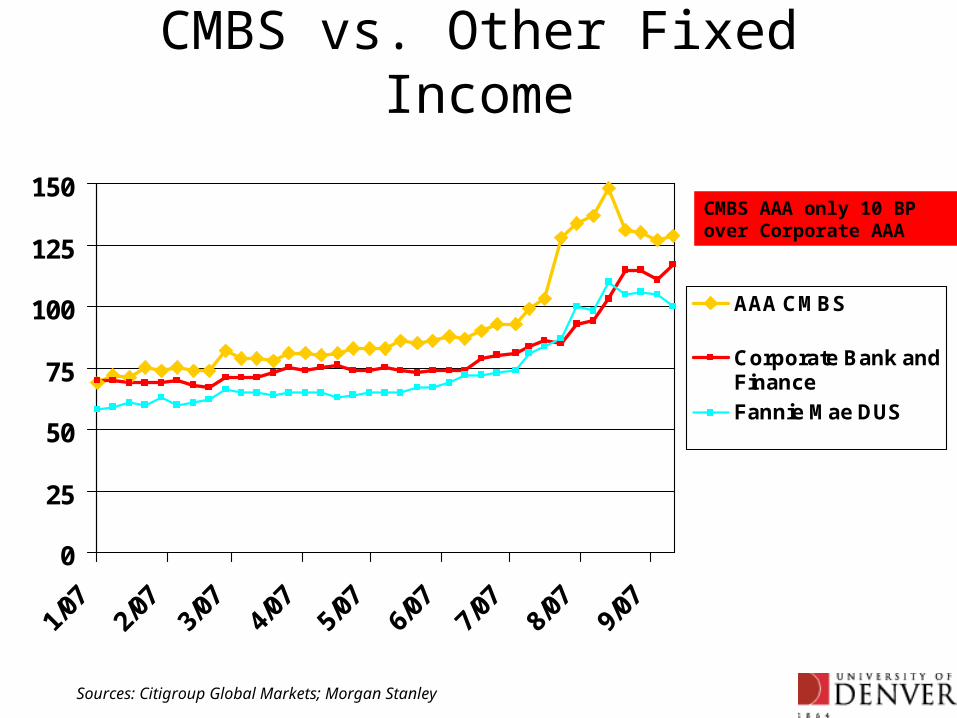

CMBS vs. Other Fixed Income

0

25

50

75

100

125

150

1/07

2/07

3/07

4/07

5/07

6/07

7/07

8/07

9/07

AAA CMBS

Corporate Bank andFinance

Fannie Mae DUS

Sources: Citigroup Global Markets; Morgan Stanley

CMBS AAA only 10 BP over Corporate AAA

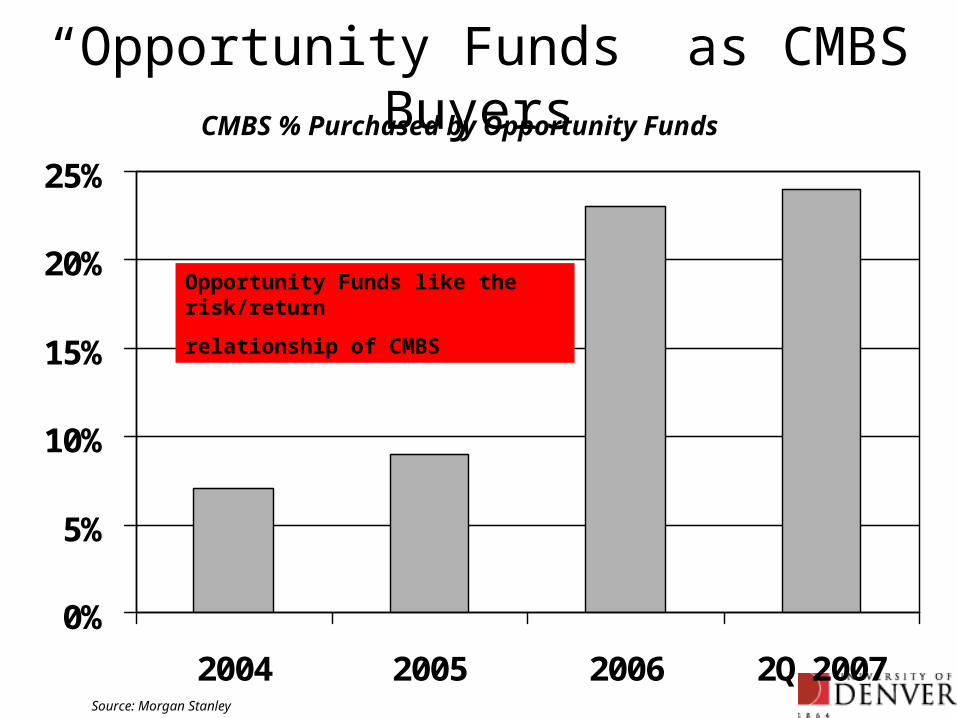

“Opportunity Funds” as CMBS Buyers

0%

5%

10%

15%

20%

25%

2004 2005 2006 2Q 2007Source: Morgan Stanley

CMBS % Purchased by Opportunity Funds

Opportunity Funds like the risk/return

relationship of CMBS

CMBS has worked for 20 years• The risk in the NR traunch was underwritten by Crimmie Mae a mortgage REIT for

the first 10 years - 1988 to 1998

• Crimmie Mae bought all NR traunches, but they reviewed and approved all loans and also took the special servicer position & fee – thus Outside / Independent oversight worked well

• When REIT prices declined in 1998 Crimme Mae stopped purchasing and Wall Street Banks were stuck with the NR traunches

• In 1999 a Wall Street Bank invented CMO (Collateralized Mortgage Obligations) and placed all their NR traunches of CMBS into the CMO. (CMOs investing in securities NOT real estate)

• They convinced rating agencies that not all the NR traunches could go bad – so some of the CMO could be rated AAA, AA and A (and sold to low risk investors)

•The CMO idea was so popular that CDOs (Collateralized Debt Obligations) were created to put other risky debt investments into a traunched security. CDOs can have credit card debt and other high risk / high loss debt in them

•Looking for more high risk investments – the Wall Street Banks created “Sub-Prime” Mortgages and started selling them through unregulated mortgage brokers, home builder mortgage companies and residential home brokers mortgage subsidiaries

•They worked to enlarge the AAA traunch of the high risk CDOs by purchasing bond insurance to improve traunch ratings

•Without a NR traunche buyer – the Wall Steet Banks kept the NR traunche on their books – Banks currently taking all their losses

•NO PROBLEMS while the residential market was going UP – but bad now that the market is going down

CDO created to securitize JUNK

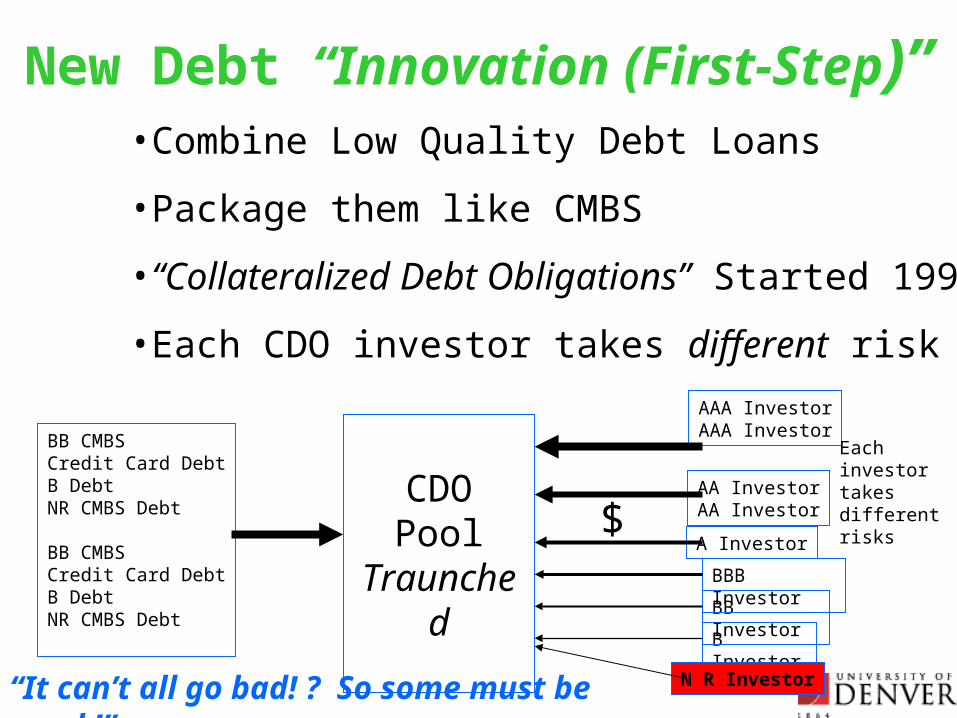

New Debt “Innovation (First-Step)”•Combine Low Quality Debt Loans

•Package them like CMBS

•“Collateralized Debt Obligations” Started 1999

•Each CDO investor takes different risk

BB CMBSCredit Card DebtB DebtNR CMBS Debt

BB CMBSCredit Card DebtB DebtNR CMBS Debt

CDOPool

Traunched

AAA InvestorAAA Investor

$AA InvestorAA Investor

A Investor

B Investor

N R Investor

BB Investor

BBB Investor

“It can’t all go bad! ? So some must be good !”

Each investor takes different risks

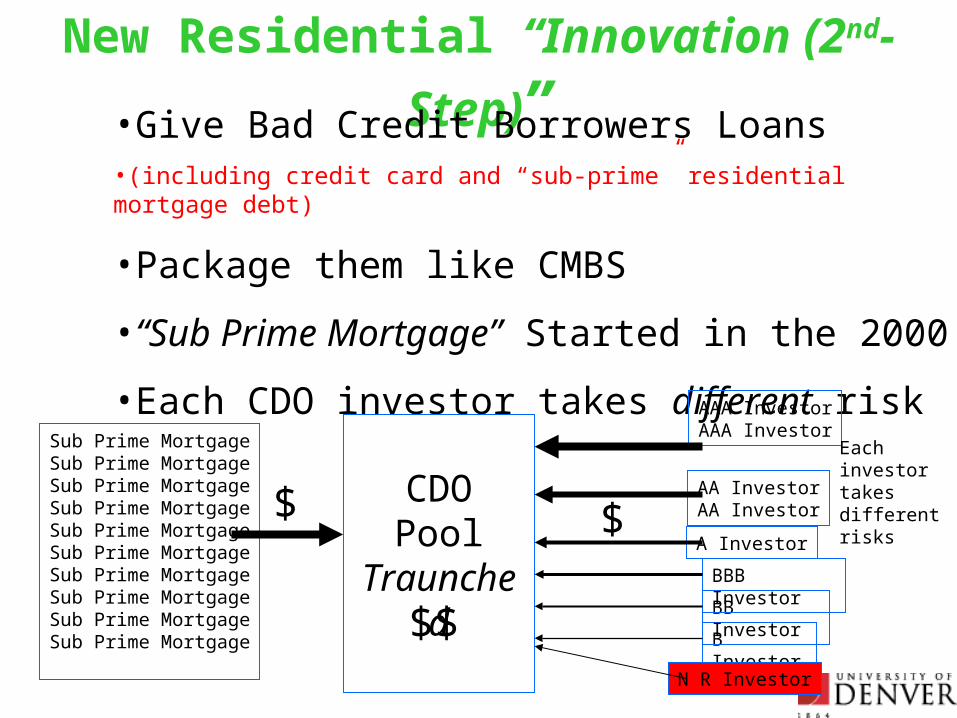

New Residential “Innovation (2nd-Step)”•Give Bad Credit Borrowers Loans•(including credit card and “sub-prime” residential mortgage debt)

•Package them like CMBS

•“Sub Prime Mortgage” Started in the 2000

•Each CDO investor takes different risk

Sub Prime MortgageSub Prime MortgageSub Prime MortgageSub Prime MortgageSub Prime MortgageSub Prime MortgageSub Prime MortgageSub Prime MortgageSub Prime MortgageSub Prime Mortgage

CDOPool

Traunched

AAA InvestorAAA Investor

$AA InvestorAA Investor

A Investor

B Investor

N R Investor

BB Investor

BBB Investor

$$

$

Each investor takes different risks

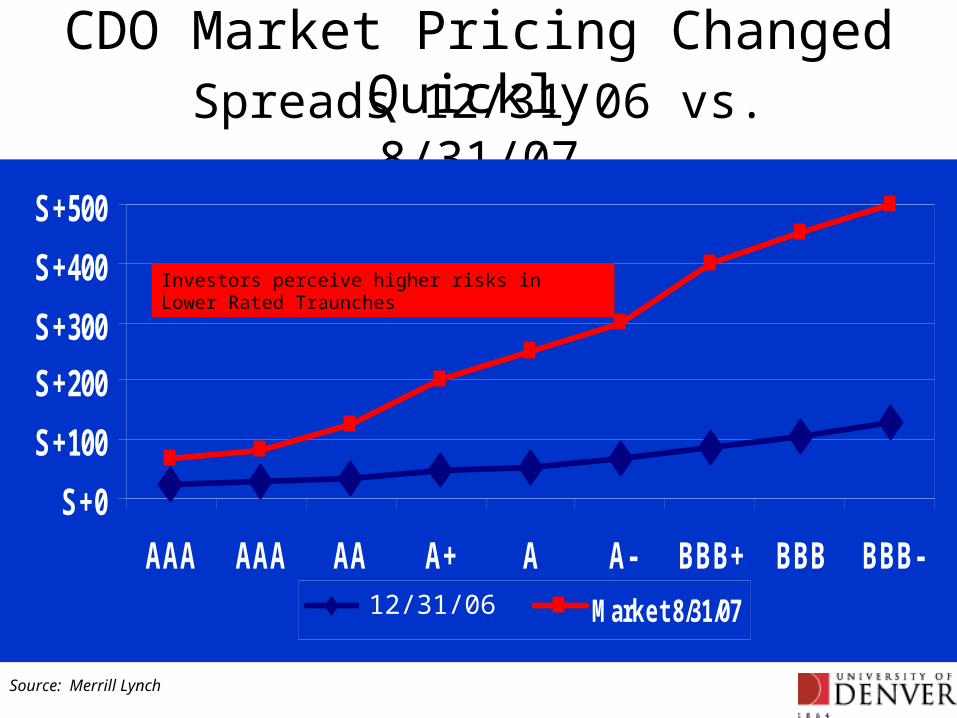

CDO Market Pricing Changed QuicklySpreads 12/31/06 vs. 8/31/07

S+0

S+100

S+200

S+300

S+400

S+500

AAA AAA AA A+ A A- BBB+ BBB BBB-

Market 12/31/07 Market 8/31/07

Source: Merrill Lynch

12/31/06

Investors perceive higher risks in Lower Rated Traunches

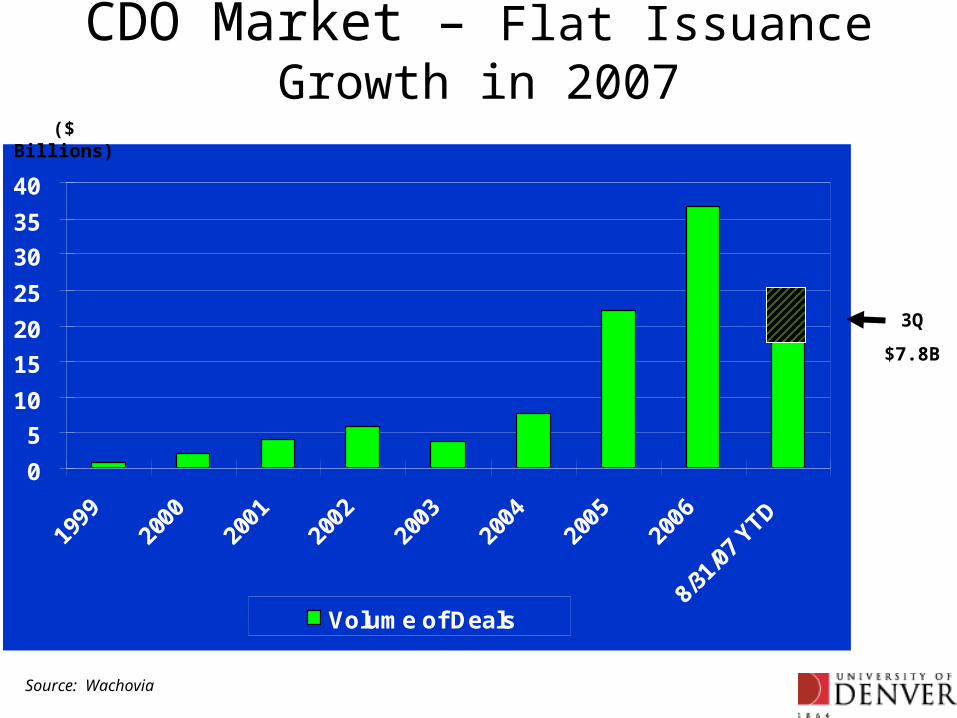

CDO Market – Flat Issuance Growth in 2007

0

5

10

15

20

25

30

35

40

1999

2000

2001

2002

2003

2004

2005

2006

8/31

/07

YTD

Volume of Deals

Source: Wachovia

3Q

$7.8B

($ Billions)

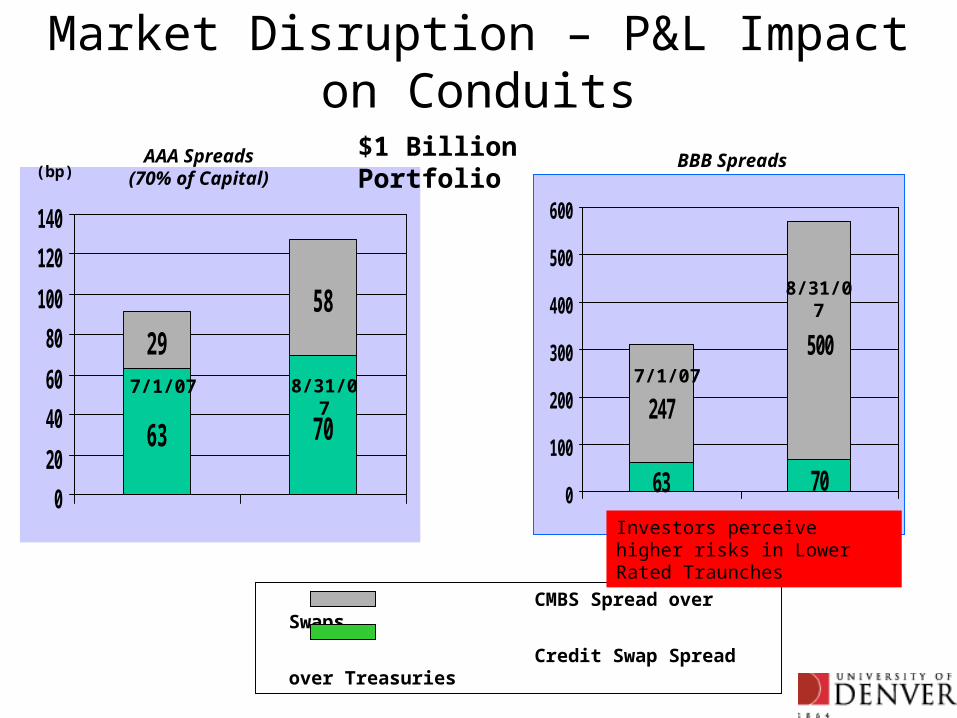

Market Disruption – P&L Impact on Conduits

63 70

2958

0

20

40

60

80

100

120

140

AAA Spreads(70% of Capital)

63 70

247

500

0

100

200

300

400

500

600

BBB Spreads

CMBS Spread over Swaps

Credit Swap Spread over Treasuries

7/1/07 8/31/07 7/1/07

8/31/07

$1 Billion Portfolio(bp)

Investors perceive higher risks in Lower Rated Traunches

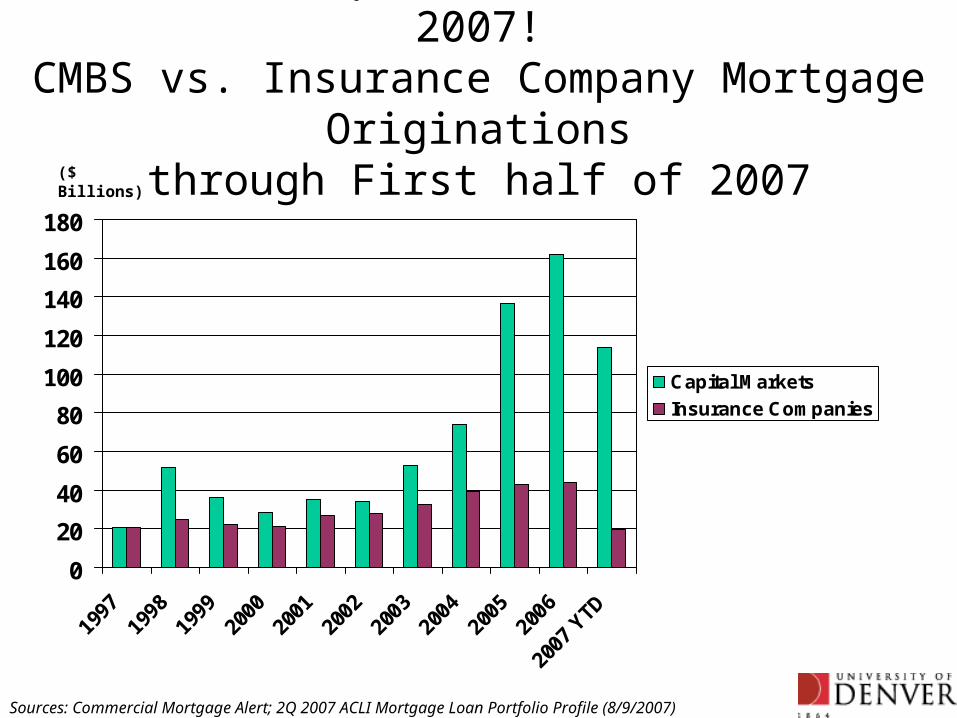

Insurance Companies saw more Risk in 2007!CMBS vs. Insurance Company Mortgage Originations

through First half of 2007

0

20

40

60

80

100

120

140

160

180

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

YTD

Capital Markets

Insurance Companies

($ Billions)

Sources: Commercial Mortgage Alert; 2Q 2007 ACLI Mortgage Loan Portfolio Profile (8/9/2007)

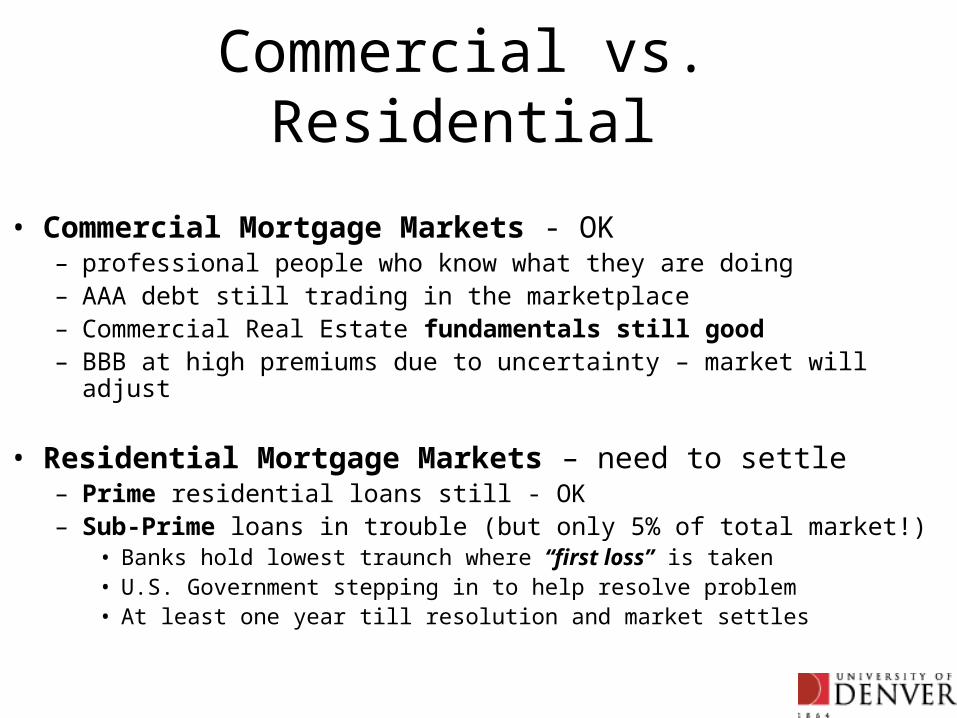

Commercial vs. Residential

• Commercial Mortgage Markets - OK – professional people who know what they are doing– AAA debt still trading in the marketplace– Commercial Real Estate fundamentals still good– BBB at high premiums due to uncertainty – market will adjust

• Residential Mortgage Markets – need to settle– Prime residential loans still - OK– Sub-Prime loans in trouble (but only 5% of total market!)

• Banks hold lowest traunch where “first loss” is taken• U.S. Government stepping in to help resolve problem• At least one year till resolution and market settles

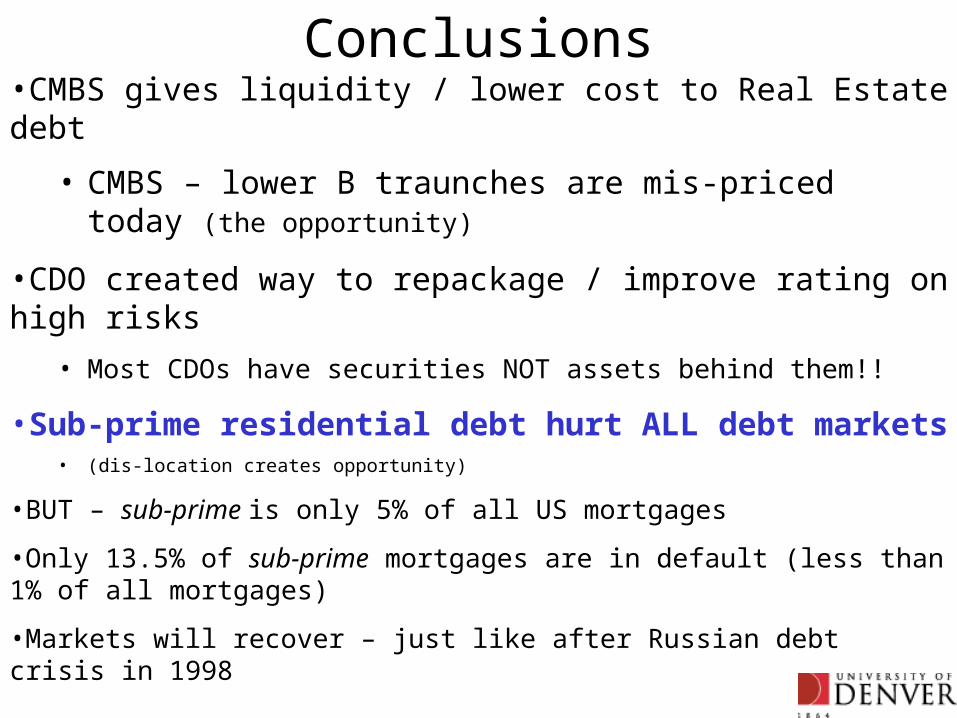

Conclusions•CMBS gives liquidity / lower cost to Real Estate debt

• CMBS – lower B traunches are mis-priced today (the opportunity)

•CDO created way to repackage / improve rating on high risks

• Most CDOs have securities NOT assets behind them!!

•Sub-prime residential debt hurt ALL debt markets • (dis-location creates opportunity)

•BUT – sub-prime is only 5% of all US mortgages

•Only 13.5% of sub-prime mortgages are in default (less than 1% of all mortgages)

•Markets will recover – just like after Russian debt crisis in 1998

• Rational long term investment focus can take advantage of dislocation!

• Markets are TRANSPARENT – lots of information available – good decisions can be made