Embed Size (px)

Citation preview

0

Buyside Operational Efficiency and STP Workshop

Tel: 416.801.3450i t l h k

Robert Smythe

© Intelcheck Services Inc.

1

Workshop PurposeWorkshop Purpose

Di t it l k t t h l d l t d hDiscuss current capital markets technology developments and how they can enhance investment manager operational efficiency

Review and learn from some other Canadian and worldwide investment managers’ operational initiatives

Suggest ways to apply the learning within your organization

2

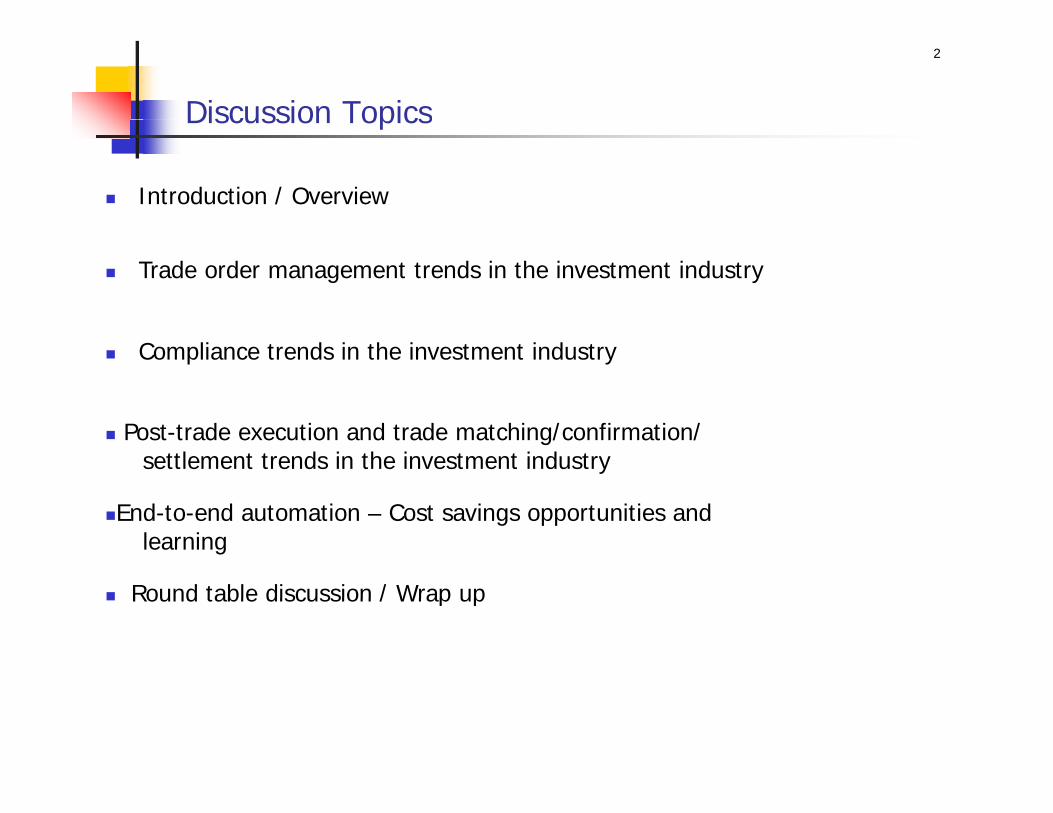

Discussion TopicsDiscussion Topics

Introduction / Overview

Trade order management trends in the investment industry

Compliance trends in the investment industry

Post-trade execution and trade matching/confirmation/ settlement trends in the investment industry

d d dEnd-to-end automation – Cost savings opportunities and learning

Round table discussion / Wrap upRound table discussion / Wrap up

3

“Matching on T” is Still ProceedingMatching on T is Still Proceeding

Canadian Securities Administrators continue to updating trade matching d t b d i d t f db kdates based on industry feedback

CCMA have established standards and best practices to facilitate STP and matching on Tmatching on T

Our research has found that investment managers have been focusing on enhancing internal operational efficiencyenhancing internal operational efficiency

Custodians have been automating their processes

4

Investment Manager ResearchInvestment Manager Research

Conducted in-depth interviews with operational executives of 23 i fi f V M linvestment management firms from Vancouver to Montreal

Research participants represent all major manager segments and collectively manage $600 billion in assets and make 9 million annual allocated trades

Reviewed 104 current and planned operational initiatives taken by firms

Examined firms’ STP status, operational pain, current system usage and future technology deployment strategies and plans

Found linkages between STP/operational efficiency and competitiveness, g / p y p ,and identified pertinent operational and technology trends

5

Key TakeawaysKey Takeaways

STP and Operational Efficiency….What’s In It For Me:

Firm management:- How STP enhances profitability and facilitates business development- How technology and integrated processes enhance business survival gy g p

Portfolio managers:- How technology and integrated processes enhance investment

performanceperformance

Traders:- How technology and integrated processes improve trading desk gy g p p g

efficiency

Accounting:H t h l d i t t d f ll- How technology and integrated processes can save me from manually correcting that same old error over and over again

Operations:- What is the ROI for the business case of my next system project

6

Trade Order Management Trends

7

Well Managed Trading Process Enhances PerformanceWell Managed Trading Process Enhances Performance

By Plexus Group measurement, a good trading desk enhances f f ll

Fi ’ I t t St l P f E h t

performance as follows:

Firm’s Investment Style Performance Enhancement

Growth 42 basis pointsGrowth 42 basis points

Diversified 62 basis points

Value 171 basis points

Source: Plexus Group/CFA Magazine March-April 2003

8

So What Makes or Breaks A Good Trading Desk ?So What Makes or Breaks A Good Trading Desk ?

Trading is not an isolated activity - It’s linked to portfolio decisions and external counter-parties

Plexus Group measurement indicates that most trading costs occurs outside the realm of the Brokeroutside the realm of the Broker

Best execution depends on how the Investment Manager manages money and progresses orders to the stage where they can bemoney and progresses orders to the stage where they can be executed, e.g.:- How the P.M. submits order to the trading desk ?

How the trading desk interacts with the broker ?- How the trading desk interacts with the broker ?- What the broker does with the order it receives ?

An automated trade order management system is key to:An automated trade order management system is key to:- Enhance timely information flows to the right people internally/externally- Eliminate manual re-keying errors

Capture trade interaction data points (shares and time stamps)- Capture trade interaction data points (shares and time stamps) associated with the flow of information

9

What The Others Are Doing with Order Management - 1What The Others Are Doing with Order Management 1

Our investment manager research found the following:

Operational Status:Order management is the second most frequently cited STP pain point- 39% of firms have experienced major operational pain in their order- 39% of firms have experienced major operational pain in their order

management activities

70%Data and data management

13%

4%

4%

35%

Portfolio management

Portfolio analytics

Risk management

Pre-trade compliance

Pre-trade

Trade26%

9%

39%

4%

Trade matching, confirmation & settlement

Trade execution

Trade communication / messaging

Order management

13%

17%

9%

0%Client reporting

Portfolio / Fund accounting

Reconciliation

Performance measurement & attribution

Post-trade

Total = 22 firms0%Client / advisor access

Total = 22 firms(Multiple responses accepted)

10

What The Others Are Doing with Order Management - 2What The Others Are Doing with Order Management 2

Actions Taken & Results:15% of firms have taken actions to address order management issuesOverall, these initiatives are producing good results:

Operational Efficiency Change Other Benefits Obtained

44%Major Increase

Operational Efficiency Change

44%

44%

78%

Improve connectivity

Reduce errors, exceptions &trade fails

Integrate internal processes

Other Benefits Obtained

22%

33%

Minor Increase

Major IncreaseExpected

22%

44%

44%

%

Reduce costs

Enhance investmentdecisions

Improve dataquality/integrity/accessibility

p y

0%No Increase11%

22%

Reduce settlemt time

Mitigate risk

Going forward:Order management is the #1 planned operational initiative:- 23% of firms planned additional order management projects, primarily

to implement a new trade order management system

11

What The Others Are Doing with Order Management - 3What The Others Are Doing with Order Management 3

System Usage:27%

14% 14% 14% 14%9% 9%

27%

18%

Order management

FMC In-house builtcustom apps.

ThomsonFinancial

Bloomberg MacGregor Excel & Access Charles River Manual paperbased

9% of firms use manual, paper-based processes

Excel spreadsheet and in-house systems are used by over 30% of firms

Remaining managers mostly use older trading systems such as FMC Vertex or portfolio accounting systems such as FMC Pacer and Thomson Portia for to manage trade orders

One in every four managers interviewed, however, already installed newer, more powerful TOMS (e.g. Charles River Trader and MacGregor MFTP) or are testing/piloting themMFTP), or are testing/piloting them

12

Current Development in Trade Order ManagementCurrent Development in Trade Order Management

Historically a buy-side Trade Order Management System (TOMS) is the trade blotter with electronic connectivity to the exchangey g

New and enhanced TOMS are emerging as integrated front/middle office systems as vendors expand their product functionality upstream and downstreamand downstream

The new generation of TOMS now incorporate:- Pre-trade compliance- Portfolio modeling - FIX connectivity- Matching utility interface

TOMS is evolving into open architecture environment to facilitate integration with portfolio accounting system

Trade blotters themselves are advancing beyond connectivity to incorporate internal or third-party information and applications

Convergence between TOMS and quote management systems on the g q g ysell-side is taking shape in the US

13

Some Key Buy-side TOMS Out ThereSome Key Buy side TOMS Out There

Vendor Product Name

Advent Software Moxy

Charles River DevelopmentCharles River Trader (CRTS)

Charles River Development(part of the Charles River IMS)

Eze Castle Software Traders Console

INDATA Precision Trading

Linedata The Longview Trading System

MacGregorThe MacGregor Financial Trading Platforms(MFTP)

SunGard Decalog TraderSunGard Decalog Trader

Thomson Financial Oneva Trade EQ(formerly Thomson Open Trader)

Source: Celent Communications

14

TOMS Ties Everything TogetherTOMS Ties Everything Together

Investment managers are moving from an initial link in the process chain towards being the hub that integrates all processes

Order Management System

ECNs BrokersNetwork

Investment Manager

Portfolio Management& Accounting

Compliance

TradingModeling & Analysis

DataSources

FIX FM

C

ClientsPortfolio accounting& Accounting

Post-trade

Reconcillation

Reference Data

SWIFT

INTE

RNET

g

MatchingUtilitiesCustodians

15

TOMS Needs to Accommodate Multiple InterfacesTOMS Needs to Accommodate Multiple Interfaces

Some examples of interfaces include, ECNs, ATS, aggregators, VMU

16

ECNs, ATS, Crossing and Aggregation PlatformsECNs, ATS, Crossing and Aggregation Platforms

Fixed IncomeM j b d t di l tf T d W b i d b Th- Major bond trading platform TradeWeb acquired by Thomson

- CanDeal owned by banks and TSX is major Canadian platform

- CollectiveBid recently entered into an arrangement with CIBCy g

Equity I i d A hi l- Instinet and Archipelago

- TSX POSIT, LiquidNet

- Bloomberg TradeBookg

Examples of aggregation solutions providing access to ECNs and other trading venuesother trading venues

- Belzberg Gateway, Lava

- MacGregor

17

Messaging Protocol ExamplesMessaging Protocol Examples

OTCDerivatives

FpML.org

Mutual Funds/Unit Trusts

F/X

ExchangeTradedDerivatives

Fixed Income

Equities

Pre-Trade Trade Post-Trade/Pre-Settlement Settlement Post Settlement

15022 15022 1502215022

18

Evolution of FIX and Industry Messaging Protocols - 1Evolution of FIX and Industry Messaging Protocols 1

ISO 15022 is becoming the standard data dictionary in the investment d i i i dmanagement and securities industry

Until recently, SWIFT was the most widely used protocol for post-trade electronic messaging, and FIX was the dominant protocol for pre-trade electronic messaging

Convergence of FIX and SWIFT following their incorporation into ISO 15022

Early signs indicate that FIX is emerging as the most widely adopted trade messaging protocol in the industry

The latest version FIX 4.4 enables bond trading

19

Evolution of FIX and Industry Messaging Protocols - 2Evolution of FIX and Industry Messaging Protocols 2

The XML version – FIXML makes it within reach of smaller and mid-size managers

For reference data, MDDL (Market Data Definition Language) is emerging as the preferred message language

ISINs are the preferred international securities identifier while CUSIPs pdominate in N.A.

20

What Does That Mean To Investment ManagersWhat Does That Mean To Investment Managers

The industry is moving a step closer to standardization of trade messaging l d k d lprotocols and market data languages

This will facilitate investment managers’ interface/connectivity with external counter-parties (custodians, brokers, etc.)

Custodians are considering charging their investment manager clients for non-electronic, manual interfaces to contain costs and reduce errors

Leading investment managers are forcing change at their brokers to provide electronic trading connectivity

4 out of 23 participants in the investment manager research ($150 p p g ($Billion+ in aggregate AUM) are already using FIX connectivity for Canadian trades

21

Selecting a TOMS – Case Study 1 (Part One)Selecting a TOMS Case Study 1 (Part One)

Firm Profile - Hotchkis and Wiley Capital Management:I i i l i i h US$4 billi iInstitutional equity manager with US$4 billion in assetsCurrently using MacGregor’s Predator, an older OMS Use FMC Pacer as portfolio accounting system, FMC Sylvan for performance measurement, and FMC Pages for client statements

Primary Objective:Gain better compliance functionality in the trading process

Products Selected:oducts Se ectedTwo components of the Charles River IMS –- Charles River Trading System (now called Charles River Trader)- Charles River Compliance Master (now called Charles River Compliance)- Charles River Compliance Master (now called Charles River Compliance)

Other Vendors Considered:Ad t E C tl S ft FMC Bl b d M GAdvent, Eze Castle Software, FMC, Bloomberg and MacGregor

22

Selecting a TOMS – Case Study 1 (Part Two)Selecting a TOMS Case Study 1 (Part Two)

Why Choose the Charles River IMS:Enhanced compliance functionalityAbility to interact with brokers using FIX which helps reduce failed trades and manual-exception processingSystem will now flow trades into FMC Pacer

Some Future Plans:Communicate with 15 of the firm’s 40 broker/dealers by yearendAutomate post-trade communication of allocation information to broker/dealers via Omgeobroker/dealers via Omgeo

Quote of the Day:“We did not choose the cheapest product but the one that fit us best ”We did not choose the cheapest product but the one that fit us best.

(Source: WST)

23

Selecting a TOMS – Case Study 2 (Part One)Selecting a TOMS Case Study 2 (Part One)

Firm Profile – M&I Investment Management:Investment management arm of a trust companyHas 1000’s of accountsCurrently using Linedata’s LongView portfolio management systemy g g p g y

Primary Objective:Trade fixed income and equities on the same platform

Product Selected:Four components of the MacGregor Financial Trading Platform (MFTP) –- MacGregor Portfolio Manager Workstation- MacGregor Advanced Fixed Income - MacGregor Compliance g p- MacGregor FIX Network

Other Vendors Considered:Charles River Development, and Linedata

24

Selecting a TOMS – Case Study 2 (Part Two)Selecting a TOMS Case Study 2 (Part Two)

Why Choose the MacGregor MFPT:Capable of doing fixed-income and equity trading, and compliance, on one single platform (current system Longview can’t)Scalable enough to handle the 1000’s of accounts that the firm interacts with as part of being in the trust business

Some Future Plans:Work with its trust accounting system provider, Metavante, to develop a link between the OMS and the accounting application

Quote of the Day:“When evaluating a potential system, it’s paramount to see the particular application at work in a financial institution that has similar functionality pp yand scalability requirements.”

(Source: WST)

25

Selecting a TOMS – Case Study 3 (Part One)Selecting a TOMS Case Study 3 (Part One)

Firm Profile – Harris Investment Management:Chicago-based institutional manager with US$20 billion in assetsWas using FMC Pivot for portfolio modeling and MacGregor’s Predator for order management

Primary Objective:Replace the existing portfolio modeling product which has become t h l i ll i ffi i ttechnologically insufficient(Upgrade path to the current vendor’s newest product FMC Model not suitable for the firm)

Products Selected:Indata’s Precision Trading

Other Vendors Considered:n/a

26

Selecting a TOMS – Case Study 3 (Part Two)Selecting a TOMS Case Study 3 (Part Two)

Why Choose Indata’s Precision Trading:Th i i d i f f li dThe system is an integrated suite of portfolio management system and order management system Already using the vendor’s portfolio attribution product and was happy with itwith itDoesn’t need MacGregor’s special features such as FIX connectivityVendor is willing to enhance products at the firm’s requestOpen architecture based on Microsoft access on an SQL server makesOpen architecture based on Microsoft access on an SQL server makes integration into the accounting system and price feeds simple

Some Future Plans:n/a

Quote of the Day:Q y“This solution has streamlined the process so that the portfolio managers [now] have better information and better control.”

(Source: WST)

27

Some Considerations When Buying a TOMS (1 of 2)Some Considerations When Buying a TOMS (1 of 2)

Learning from other managers:

Best fit vs. price tag

See the system in action at a shop that has similar functionality and scalability requirements

Integration with portfolio management/accounting system

Pre-trade compliance is critical

d f d d h l f ?Want to trade fixed income and equities on the same platform ?

28

Some Considerations When Buying a TOMS (2 of 2)Some Considerations When Buying a TOMS (2 of 2)

Learning from other managers:

Is FIX connectivity with counter-parties required ?

What other features are important to you? - E.g. Alternative trading system interface

Vendor’s implementation capability and willingness to enhance productp

Best-of-breed vs. integrated product suite

How long you want to be locked in with the vendor?- System’s useful life cycle (5-7 years)y y ( y )

29

Technology is Facilitating Trading Processes - 1Technology is Facilitating Trading Processes 1

Technology allows investment managers to control their trade ti th hexecutions through:

- FIX linkages with brokers

f- Integration with algorithmic platforms

- Connections to aggregators

- Transaction cost analysis models to measure and enhance trading efficiency

Technology also enables investment managers to:

- Process transaction volumes for a large number of accounts

- Provide electronic access to preferred sources of liquidity

- Unite various vendors, brokers, ECNs and ATS involved in their workflow onto a single platformworkflow onto a single platform

30

Technology is Facilitating Trading Processes - 2Technology is Facilitating Trading Processes 2

Evolving standards like FIX, SWIFT and VMUs are key to STP

Solutions need to address these components:

31

Buying a TOMS – A Process FrameworkBuying a TOMS A Process Framework

1. Model Business Processes

2. Determine Required Functionality

3. Determine the Long List of Vendors

5. Determine the Short List of Vendors

4. Create and Issue RFI

5. Determine the Short List of Vendors

6. Conduct Vendor Demonstration

7. Conduct Client References

8. Process RFPs

9. Final Negotiations

System Implementation

32

Compliance TrendsCompliance Trends

33

Compliance and Risk Management MatterCompliance and Risk Management Matter

Operational Efficiency

- Do it right the first time

B i D l t / Cli t R t tiBusiness Development / Client Retention

- Clients are comforted by modern risk management and mandate compliance without exceptionsp p

- Can we as investment manager afford to deviate from client mandates?

Regulatory Compliance

- OSC, IDA, OSFI are increasingly intolerant of exceptions

Business Survival / Avoid Reputational Risk

R l T t LTCM P t- Royal Trust, LTCM, Putnam

34

The Regulators are WatchingThe Regulators are Watching

Pressures like the Myners Report in the U.K. and the mutual fund regulatory reviews in the U.S. and Canada require that investment managers be able to demonstrate that they are acting in the best interest of their clients

Investors seeking better returns in more stable markets will increasingly look at execution and operational costs ad will holdincreasingly look at execution and operational costs ad will hold those managing their money accountable for deviations from the norm

35

Compliance Check – First GenerationCompliance Check First Generation

First generation = “Post-trade execution” complianceg p

Make Investment Decision

Construct Orders

Manage Orders

ExecuteOrders

Monitor Positions

ComplianceBreaches

- Check the positions after the trades are executed

- Rectify any breaches found “after the fact”

36

Compliance Check – Second GenerationCompliance Check Second Generation

Second generation = “At-trade” compliance

Make Investment Decision

Construct Orders

Manage Orders

ExecuteOrders

Monitor Positions

VerificationVerificationFailures

- Identify non-compliant orders after order generation and before execution

- Use constraints or compliance systems to check the order flow and rejectany non-compliant orders

37

Compliance Check – Third GenerationCompliance Check Third Generation

Third generation = “Pre-trade” compliance check

Make Investment Decision

Construct Orders

Manage Orders

ExecuteOrders

Monitor Positions

ConstructCompliant

Portfolio Model

- Avoid generating non-compliant orders in the first place

38

Data and “Real-time” Reporting are KeyData and Real time Reporting are Key

“Real-time” reporting is key to effective pre-trade compliancep g y p p

Even for “at trade” compliance check, the right data needs to be available at the point of the trade to run the compliance ruleavailable at the point of the trade to run the compliance rule

A truly “pre-trade” compliance check requires the right compliance d t t b i t t d i t tf li d li ti itidata to be integrated into portfolio modeling activities

39

What The Others Are Doing with Compliance - 1What The Others Are Doing with Compliance 1

The investment manager research found the following:

Operational Status:Pre-trade compliance is the third most frequently cited STP pain point- 35% of firms have experienced major operational pain in their pre-trade- 35% of firms have experienced major operational pain in their pre-trade

compliance activities

70%Data and data management

13%

4%

4%

35%

Portfolio management

Portfolio analytics

Risk management

Pre-trade compliance

Pre-trade

Trade26%

9%

39%

4%

Trade matching, confirmation & settlement

Trade execution

Trade communication / messaging

Order management

13%

17%

9%

0%Client reporting

Portfolio / Fund accounting

Reconciliation

Performance measurement & attribution

Post-trade

Total = 22 firms0%Client / advisor access

Total = 22 firms(Multiple responses accepted)

40

What The Others Are Doing with Compliance - 2What The Others Are Doing with Compliance 2

Inadequate Attention to Compliance / Risk Management a Cause for Concern:

Compliance and risk management were not one of investment managers’ top business priorities

What other business priorities does your firm have?What is your firm’s top business priority ?

48%

70%

39%

30%Reduce operational risk

Increase assets under management

Reduce costs

Increase operational efficiency

22%

43%

9%

9%Post-acquisiton integration

Maintain assets undermanagement

Increase assets undermanagement

Improve investment performance

Neither were they among the top technology challenges for most firms

Total = 23 firms

30%

17%Increase customer satisfaction

Reduce operational risk

4%Address system probems

q g

Neither were they among the top technology challenges for most firms

26%Integrate internal systems

What is your top technology or process challenge? What other technology and process challenges do you encounter in achieving your overall business priorities?

57%Data & data management

9%

9%

22%

22%

Trade Order Management Systems

Risk management

Data & data management

Re-design processes

Total = 23 firms

30%

39%

39%

P t d li

Reduce manual intervention

Integrate internal systems

External connectivity

9%Trade Order Management Systems Total 23 firms22%Pre-trade compliance

41

What The Others Are Doing with Compliance - 3What The Others Are Doing with Compliance 3

System Usage:

Pre-trade Compliance

18%9% 5% 5% 5% 5% 5%

23%36%

Excel & Manual In-house MacGregor FMC Charles Risk-based CRM RPMAccess built custom

apps.

gRiver rules system technology

for dealersystem

Excel spreadsheets, sometimes in combination with Access database or in-house systems, are the “application” the most frequently used by investment managers in pre-trade compliance- 36% of firms use Excel- 18% of firms use in-house systems

23% of firms said their compliance checks are entirely manual p y

Some firms who already installed automated TOMS perform pre-trade compliance checks through their TOMS (e.g. MacGregor, Charles River)

Th i f ( FRI R i CRM FMC)The rest use a variety of systems (e.g. FRI Raison, CRM systems, FMC)

42

What The Others Are Doing with Compliance - 4What The Others Are Doing with Compliance 4

Compliance Not Current Action Focus:

Only 7% of the current operational initiatives taken by investment managers addressed pre-trade compliance issues

Risk mitigation is the key benefit producedRisk mitigation is the key benefit produced

But Things are Gaining Momentum:

Going forward, 32% of investment managers said they planned to invest in automating pre-trade compliance

- as part of their TOM implementation project- or on a stand-alone basis

43

Pre-Trade Compliance Tools – What’s Out TherePre Trade Compliance Tools What s Out There

Many TOMS vendors claim their product incorporates pre-trade compliance functionality:compliance functionality:

TOMS Pre-Trade Compliance Module

Compliance testing at time of allocation √ √ √ √ √ √ √ √ √

Compliance testing at time of execution √ √ √ √ √ √ √ √

√ √ √ √ √ √ √ √ √Compliance testing at time of order √ √ √ √ √ √ √ √ √

Cover ERISA requirements √ √ √ √ √ √ √

Cover institutional client guidelines and restrictions √ √ √ √ √ √ √ √ √

C I t t C A t d t l f d t √ √ √ √ √ √ √ √Cover Investment Company Act and mutual fund prospectus √ √ √ √ √ √ √ √

Cover IRS requirements √ √ √ √ √ √ √

Pre-packaged compliance rules included √ √ √ √ √ √ √ √ √

Set up compliance rules √ √ √ √ √ √ √ √ √Set up compliance rules √ √ √ √ √ √ √ √ √

Violation notification for batch √ √ √ √ √ √ √ √ √

Violation notification for specific compliance violations √ √ √ √ √ √ √ √ √

Violation resolution and supervisory override √ √ √ √ √ √ √ √ √(Source: WST)

44

TOMS and Compliance – One System or Two Systems?TOMS and Compliance One System or Two Systems?

Question: Which one is the right answer ?Question: Which one is the right answer ?

A. Have one system for order management and pre-trade compliance

B Have two systems: a TOMS + a stand alone compliance systemB. Have two systems: a TOMS + a stand-alone compliance system

AnswerIt all depends on your circumstances…

45

Selecting a Compliance System – Case Study 1(Part One)g p y y ( )

Firm Profile – Britannic Asset Management:Glasgow, Scotland-based manager with GBP 14 billion under managementWas doing periodic manual compliance checkAlready using Linedata’s TOMS, LongView Trading System y g , g g y

Primary Objective:Minimize the risk of non-compliance to regulatory and client requirements(Current periodic manual checks inadequate to handle the firm’s trading volumes)

Product Selected:Product Selected:Latent Zero’s Sentinel pre- and post-trade compliance system

Other Vendors Considered:Other Vendors Considered:n/a

46

Selecting a Compliance System – Case Study 1 (Part Two)Selecting a Compliance System Case Study 1 (Part Two)

Why Choose Latent Zero Sentinel:Used by other similar investment firmsSaw examples of Sentinel integrating with the firm’s existing TOMSLiked the solution’s speed and scalabilityp yCurrent TOMS vendor didn’t have the right pre-trade compliance system

Implementation:Britannic has spent 18 months programming its own internal and client rules into the system, even though Latent Zero built rule libraries into Sentinel based on geographical areas.

Quote of the Day:“…clients will become more switched on to risk management, corporate

d li i h i [ d li t ]governance and compliance issues, so having [a good compliance system] really works in our favor.”

(Source: WST)(Source: WST)

47

Selecting a Compliance System – Case Study 2 (Part One)Selecting a Compliance System Case Study 2 (Part One)

Firm Profile – GE Asset Management:Large US manager based in Stamford, ConnecticutManagement recently put 3 money-management entities under one unitVarious fixed-income business entities running different vendor and in-ghouse platforms

Primary Objective:Standardize trading platform and workflow for all fixed-income entities Upgrade to pre-trade compliance to achieve STP capabilities

P d S l dProducts Selected:Latent Zero’s fixed-income applications - Tesseract for portfolio management, Minerva for trading and Sentinel for compliance

Other Vendors Considered:Bloomberg, MacGregor, Charles River Development

48

Selecting a Compliance System – Case Study 2 (Part Two)Selecting a Compliance System Case Study 2 (Part Two)

Why Choose Latent Zero:One of the superior fixed-income TOMSStrong pre-trade compliance engine with STP capabilitiesImpressed by its messaging technologyp y g g gyHas a virtual database that allows GE’s different locations to get the same performance as if they were in the Stamford head officeUltimately offered a reduced price point vs. original pricey p p g p

Some Future Plans:Expect the whole firm on the system by Q1/2005

Quote of the Day:“The key is moving data out of the accounting system and closer to the front office……[so that] it can be used by traders in real time.....to add new issues and perform a pre-trade compliance check on the fly.”

(S WST)(Source: WST)

49

Post-trade Execution and Trade Matching/Confirmation/Settlement TrendsMatching/Confirmation/Settlement Trends

50

Matching on T and Its ImplicationsMatching on T and Its Implications

Will require STP interfaces between counterpartiesTime for error correction virtually eliminatedSwiss can complete transactions in seconds

51

This Adds to Investment Managers’ ChallengesThis Adds to Investment Managers Challenges…

Multiple asset

Extensive compliance

Complex accounting &

reporting

Multiple asset classes

Straight- through processing

Disjointed internal s stems

Money Managers’ ChallengesFocus on core competencies

Complex portfolio & trading

systems

Focus on core competenciesImprove performance

Increase competitivenessReduce costs

Mitigate risk, etc

Data problemsg

strategies

Proliferatinginvestment

Multiplebusinesses

productsManual processes

businesses(pension, private,

mutual funds)High volumes (accounts, AUM,

trades)

Declining profit margins Increasing

operational risks

Haphazard external connectivity

52

End-to-end Electronic Processing Requires Industry-wide CollaborationIndustry wide Collaboration

I tit ti l S iti T dInstitutional Securities TradeHigh Level Transaction Process

Validate trades / monitor settlement status

Executes trades

Trade detailsMaintains record keeping for security positions in custodians’ omnibus accounts

TradeO df

Investment

Exchange DepositoryBroker / Dealer

Validate trade details and

Confirmation

Trade

Confirmation

OrderManages portfolio and initiates trades

Investment Manager

Validate trade details and account positions

Trade allocations to client accounts Settle trade on trade

date + 3 days

CustodianEntity Owning Security

Delegates investment

management

Delegates custody of securities

date 3 days

Manages security positions in client accountsaccounts

53

Costs of Manual Processes and Failed Trades – 1Costs of Manual Processes and Failed Trades 1

Financial Information Services Division (FISD) Research

- Lack of STP costs the industry about $12 billion annually

- 59% of instructions need repair

- 10% of transactions result in mismatches

- 15% of trades fail to settle on time

- A cross border trade involves up to 25 people, processes or systems

- 30% of trade failures are a direct result of inaccurate reference data

Tower Group Research

- Firms have multiple SMF systems (10-150 systems per firm)

- Average of 58 FTE to maintain SMF (some as high as 200 FTE)

- 30% of trade failures are caused by bad reference data

54

Costs of Manual Processes and Failed Trades - 2Costs of Manual Processes and Failed Trades 2

SWIFT research- 50% of transactions need repair ($6 per repair)

- 15% of trades fail to settle on time ($50 per settlement failure)

Omgeo research- Human error is the top reason for failed trades

F il d t d t i tit ti €182 f il d d ti t d d €388- Failed trades cost institutions €182 per failed domestic trade and €388 per failed cross-border trade

SmartStream Research- Exception management accounts for over 80% of all back office costs

55

On a Global Basis STP is Even More ChallengingOn a Global Basis STP is Even More Challenging

Automated central or local matching will be required

Exchanges

InstitutionalClient

Retail Client

Retailtrades

Retail &institutional

trades

Issuers

Broker/Dealer

Institutionalt d Institutional

Client

MoneyManager

Institutionaltrades

Retail Client Retail &institutional

trades

Retail & Institutionaltrades & settlesTransfer

A t

VMU

MutualFund

Distributor CentralDepository

trades Institutionaltrades

Institutionalt d

Institutionaltrades & settles

Agents

VMU

FundSERV

Concentrator

trades

Institutionaltrades

Institutionaltrades

Institutionaltrades & settles

Dematerialization

MutualFund

CompanyMoney

Manager

Institutionaltrades

MoneyManager

trades trades & settlesInstitutionaltrades & settles

CustodiansCorporateActions Securitiesg CustodiansActions Securities

Lending

56

Domestic Equities / Fixed Income with VMU (CCMA Model)Domestic Equities / Fixed Income with VMU (CCMA Model)

T T+18am 8am5:30pm

TCCMA MILESTONE: 100% Compliance with Industry Best Practices & Standards by June 2005

BrokerGenerate NOE(Full or Partial) Monitor Trades Receive Notice of

Settlement

1 11b 14Book Trades

Execute Order**

8b

Receive Order & Receive Order & Send Fills**

Reconcile and Resubmit NOE

Provide Matched InformationVMU* Receive NOE Match NOE and

Allocations

Standing

Receive Allocations/Blocks

Enrich with Standing Settlement

Instructions

24 5 7a 8a

Custodian

YES

NO6

Send MismatchinfoDetails

Match?

6

InvestmentManager

t

Update details in Blotter/Trading/ Portfolio Management System Send Block

All ti &

Standing Settlement

Instructions

3a

Place Order**

Matched Trade Details and Affirmed Trade Details

8c

Send block trades& Trade Allocations

3bReconcile and Resubmit

Allocations

Attach SSIAttach SSI

BrokerIM

Agree toTrade?

Agree toTrade?

NO

YES

Release Trades for

Allocations & Underlying client A/C

Receive Affirmed Trades

11a

12

(If not using SSI)

Add JITSettlement Instructions

(If not using SSI)

Receive All ti

Validate Details (Client Details Details YES

108d

ValidateTrades

ValidateTrades

YES

Custodian EP 2Resolve With Broker or IM

NO

IM Exception Process Reconcile with BD or

DK Trade

NO

Custodian

Settlement

Generate Affirmed Trades Settle Trades

Receive Notice ofSettlement

9 13

14

Depository & Clearing

Allocations (inventory, cash) Match?

Details Match?

Custodian EP 1Resolve With

IM

NO

57

The FMCNet2 is FMC’s Virtual Matching UtilityThe FMCNet2 is FMC s Virtual Matching Utility

VMU features are optionalSupport for multiple matching models

- CCMA and SIA models- External matching –g

30 minute matching cycle- Local matching- Matching criteria can differg

depending on counter-party- Matching criteria set by IM

58

CityIQ Proposed Use of FIX for ConfirmationsCityIQ Proposed Use of FIX for Confirmations

Major gap is that FIX does not accommodate standing settlement i t ti (SSI)instructions (SSI)

Fix OMS TL

NOE NOE

EngineOMS ETOrders Orders

Allocations Allocations

ConfirmationsAffirmations

Confirmations

Confirmation Confirmation ConfirmationConfirmationMatching

Engine

ConfirmsserviceET

L Confirmation Confirmation

Affirmation Affirmation

59

End-to-end Automation –Cost Saving Opportunities and LearningCost Saving Opportunities and Learning

60

End-to-end Automation Requires Clean DataEnd to end Automation Requires Clean Data

The need to achieve end-to-end automation, or STP, is a clear movement in the investment and securities industry

Every discussion about STP ends in a discussion of reference data

Data is the top enemy for STP, not technology

S iti M t Fil ( )- Securities Master File(s)- Securities identifiers- Broker identifiers- Client instructions- Settlement instructions…..

30% of trade fails due to bad data (TowerGroup research 2002)

61

Reference Data is At the Heart of Every SecurityTransactionTransaction

M d li S

ss Broker

Consolidate - Link - Enhance Reference Data

Disparate Data Modeling System

Trading System

Mas

ter D

etai

l

Ass

et C

lass

es Broker

Custodian

Disparate Data

Standardized Data

Portfolio Acct Sys

Secu

rity

M

Vario

us A

G/L System

Leveraged Data

Data Consolidation

DataEnhancement

S

Recon System

Data Consolidation

Data WarehousePerformanceSystem

Risk System

62

Data is Money Managers’ Biggest Operational Pain…Data is Money Managers Biggest Operational Pain…

70%Data and data management

13%

4%

35%

Portfolio anal tics

Risk management

Pre-trade compliance

Pre-trade

39%

4%

4%

Order management

Portfolio management

Portfolio analytics

Trade

26%

9%

4%

T d t hi fi ti & ttl t

Trade execution

Trade communication / messaging

13%

17%

26%

Reconciliation

Performance measurement & attribution

Trade matching, confirmation & settlement

Post-trade9%

0%

0%Cli t / d i

Client reporting

Portfolio / Fund accounting

Total = 22 firms(Multiple responses accepted)

0%Client / advisor access

63

… Because It’s Everywhere… Because It s Everywhere

DATA ELEMENTS

CUSIP, ISIN, SEDOL Trade Order Mgmt.

DATA USAGEREFERENCE DATA

Security Description

Country Codes

Trade Allocations

Matching & Settlement

SECURITIES MASTER

RECORDS

GICS Codes

Market Data Corp.Act./Entitlements

Compliance/Risk Mgmt

Asset Mix Targets

Reuters, Bloomberg Reconciliation

Portfolio Reporting

CLIENT INSTRUCTIONS

Trading Constraints Client Reporting

64

And Reference Data Covers So Many Things…And Reference Data Covers So Many Things

Transaction recordTransaction record

Transaction Reference #

Account Identification

CLIENT ACCOUNTPROFILES

DataBuy/Sell Indicator

Security Identifier

Number of Shares

Data

Transac

SECURITIES MASTER FILE(S)

ccy code + Principal Amount

ccy code + Commission

Trade Date

ctional

CURRENCY Settlement Date

Broker

Custodian/Clearing Agent

TABLES

Place of SettlementCOUNTER-PARTYDATABASE(S)

65

What Distinguishes Good Data from Bad Data ?What Distinguishes Good Data from Bad Data ?

Data Quality- Consistency of data across different systems and functional activities- Data concentration is required to “harmonize” data

=> Data hub/warehouse

Data Integrity- Accuracy and “cleanliness” of data in the systemAccuracy and cleanliness of data in the system- Data cleansing => Identify and automatically scrub mismatched data- Identify and correct the cause of data anomalies

Data Accessibility / Timeliness- Clean and harmonized data is transmitted to the right functions on a

timely basis to enhance the investment decision-making process

66

End-to-end Automation Also Requires Integrated Systems and ProcessesSystems and Processes

What is your top technology or process challenge resulting from your top business priority?

What other technology and process challenges do you encounter in achieving your overall business

i iti ?priorities?

26%Integrate internal systems 57%Data & data management

22%

22%

26%

Data & data management

Re-design processes

Integrate internal systems

22%

30%

39%

39%

Pre-trade compliance

Reduce manual intervention

Integrate internal systems

External connectivity

9%

9%

9%

CRM tools

Trade Order Management Systems

Risk management

17%

17%

17%

17%

TOMS

Reduce errors & trade fails

Upgrade internal systems

Re-design processes

N=23 (Multiple responses accepted) N=23

9%CRM tools13%Risk management

67

What Some Other Managers are Doing With Their Data ProblemsData Problems

Our investment manager research found that:

In the last 12 months:

Data management is the most frequent operational initiative takeng q p

52% of firms have actively pursued initiatives to alleviate data impediments to STP and operational efficiency

16 of the 60 current initiatives (or 27% of all initiatives) research participants described to us involved:

- Data cleansing, or

- Data consolidation and data hub/warehouse projects

68

Data and System/Process Integration Actions Pay OffData and System/Process Integration Actions Pay Off

O ti l Effi i Ch Oth B fit Obt i d

44%M j I

Operational Efficiency Change

94%Improve data

Other Benefits Obtained

44%

44%

Major IncreaseExpected

Major Increase

38%

50%

94%

Integrate internal processes

Improve connectivity

quality/integrity/accessibility

0%

6%

No Increase

Minor Increase

19%

31%

38%

Enhance investmentdecisions

Reduce settlement time

Reduce errors, exceptions &trade fails

6%Don't

Know/Refused13%

13%

Reduce settlemt time

Mitigate risk

69

Examples of Current Data Initiatives - 1Examples of Current Data Initiatives 1

Data Hubs/warehouse – Data consolidation:

“We implemented a data hub to address the lack of data sharing across business units identified in an STP audit two years ago. Now our SQL-based data hub is our central source of information. The benefits are the ability to query data and “plug and play” XML functionality. All in all, this initiative has resulted inand plug and play XML functionality. All in all, this initiative has resulted in much higher efficiency.” (Institutional asset manager)

“We use Excel and manual intervention a lot and we need to give our portfolio managers more flexibility We expect a major increase in efficiency from amanagers more flexibility. We expect a major increase in efficiency from a data hub that will resolve data quality problems caused by data coming from different sources being stored locally and used in different activities. We’re now in the RFP process for the implementation of a data hub”.

(Institutional asset manager)(Institutional asset manager)

“To alleviate STP challenges due to disjointed legacy systems, manual processes and widespread use of spreadsheets, we complemented our data warehouse initiatives with organizational redesign As a result we managed to reducedinitiatives with organizational redesign. As a result, we managed to reduced 1/3 of headcounts who were doing manual entries, etc. and re-direct the FTE to more critical analytical functions. We also improved our performance by 3 to 5 basis points by getting better, more accurate and more timely data.”

(Insurance company)(Insurance company)

70

Examples of Current Data Initiatives - 2Examples of Current Data Initiatives 2

Data Cleansing:

“With our custodian, we house our data in the custodian’s location. We then extract and normalize the data back to here, combine it with data from our brokers, and then bring it into our reconciliation system for automatedbrokers, and then bring it into our reconciliation system for automated reconciliation. This has resolved the data integrity problem we experienced due to multiple data sources and the resulting required reconciliation of data differences.” (Pension fund)

“We resolved our security identifier problems by mapping our internal CUSIP to actual industry CUSIP. We can now automatically match trades, and we now use a delivery instruction database This has resulted in a major increase inuse a delivery instruction database. This has resulted in a major increase in operational efficiency....Our STP rate has improved from 35% to 87% in the last year.” (Institutional asset manager)

“We cleaned up our security master file and centralized data management. We have gone through all our securities to ensure they are set up properly throughout the firm. This has resulted in some efficiency gains.”

(Institutional asset manager)

71

Going Forward…Going Forward…

Our investment manager research found that:

Going forward:68% of research participants planned further investments to address data management issuesg

“We plan to implement a data hub/warehouse. Going forward, for reporting, we plan to extract data into a central repository. The benefits we expect are p p y pbetter, more timely data, less operational risk with automated reporting. We expect the reports to be more granular and better for our portfolio managers to interpret the data.” (Pension fund)

“We will continue to invest in our data warehouse development to allow us to do things daily, including daily performance measurement and daily client reporting.” (Insurance company)

“We will re-architecture our existing data warehouse with a focus on [cleaning up] our security master file and reference data.” (Pension fund)

72

Investment Managers Will Also Benefit from Industry-wide Data HubsIndustry wide Data Hubs

Multiple capital market-specific common data hubs in Canada

Some of the likely candidates are:

- Corporate actions hub

· An initiative driven by the CCMA

· 77% of investment firms surveyed said they will consider an automated linkage to a future corporate action data hub

- Centralized security master fileCentralized security master file

- Securities classification database

- Common industry advisor database

73

Institutional vs. Private Wealth Management –What’s the Same, What’s Different in AutomationWhat s the Same, What s Different in Automation

Pre-Trade - 1:

Function Institutional Private

Detailed KYCSetup & Maintain Client & Account Profiles Less detailed KYC and

CRM requirements

Detailed KYC –Widespread use of

CRM functions

Very important (Di t d t d ft $Setup & Maintain Counterparty Profiles (Directed trades, soft $,

cumulative commissions etc.)

Not as important

M S it M t Fil ( )Very Important

Manage Security Master File(s)e y po ta t

(Data for all security types & many fund types)

Manage Investment Reference Data Very Important

Manage Portfolio PositionsVery Important

74

Institutional vs. Private Wealth Management –What’s the Same, What’s Different in AutomationWhat s the Same, What s Different in Automation

Pre-Trade - 2:

Function Institutional Private

Portfolio Risk/return Analytics Very Important

Model Target Portfolio, Rebalance Existing Very Important

Portfolio & Generate TradesVery Important

Pre-trade Compliance Checks Very Important

Cash Flow Monitoring & Short-term Cash Investments

More important (Large $ amounts)

Not As Important

75

Institutional vs. Private Wealth Management –What’s the Same, What’s Different in AutomationWhat s the Same, What s Different in Automation

Trade – Manage Trade Order Cycle:

Function Institutional Private

Order Creation based on Portfolio Decisions Very Important

Account Aggregation Very ImportantAccount Aggregation Very Important

Manage Trade Blotter Very Important

Order RoutingImportant

(Directed Trades)Less Important

Manage Trade Execution Processing Very Important

76

Institutional vs. Private Wealth Management –What’s the Same, What’s Different in AutomationWhat s the Same, What s Different in Automation

Post-Trade -1:

Function Institutional Private

Post-trade compliance checks Important

Trade Matching, Confirmation & Important

SettlementImportant

Corporate Actions Important

Reconciliation Important

77

Institutional vs. Private Wealth Management –What’s the Same, What’s Different in AutomationWhat s the Same, What s Different in Automation

Post-Trade - 2:

Function Institutional Private

Manage Portfolio Accounting Important

More sophisticatedLess sophisticated –

But requirePerformance Measurement & Attribution More sophisticated requirements

But require client/household aggregation, etc

Cli t R tiMore complex client &

l t Generally lessClient Reporting regulatory requirements

Generally less sophisticated

78

Applying the “Common” Operating Platform to Guardian – Some Areas of Potential Cost SavingsSome Areas of Potential Cost Savings

Some Probable Candidates for a “Common” Integrated Platform:- Reference data management (Data hub/warehouse)- Trade order management system- Post-trade back office processingPost trade back office processing - Portfolio accounting system

A F Q ti t A k O lA Few Questions to Ask Ourselves:- Do Institutional and Private need two overall platforms ? - Do we need two TOMS for the front/middle office?- Do we need two PMS for the back office ?- In what functions do Institutional and Private have major differences

in requirements ?q

Remember

“L i M ”“Less is More…”

79

Wrap up / Roundtable DiscussionWrap up / Roundtable Discussion