Embed Size (px)

Citation preview

Business Valuation of

Erin’s Fitness Gear, Inc.

As of June 30, 2013

Prepared for:

Erin K. O’Donnell

President

Erin’s Fitness Gear

100 Erskine Plaza

South Bend, IN 46614-3244

Report Date:

July 30, 2013

Prepared by:

Patrick Keszei, CPA, CFP, CVA, EA, MBA

Manager of Business Valuation Services

Business ValueCalc

1456 Lincolnway East

South Bend, IN 46613-3249

July 30, 2013

Patrick Keszei, CPA, CFP, CVA, EA, MBA

Manager of Business Valuation Services

Business ValueCalc

1456 Lincolnway East

South Bend, IN 46613-3249

Erin K. O’Donnell

President

Erin’s Fitness Gear, Inc.

100 Erskine Plaza

South Bend, IN 46614-3244

RE: Erin’s Fitness Gear, Inc.

Dear Erin K. O’Donnell:

At your request, we have performed a valuation engagement, as defined in the Statement on Standards for

Valuation Services (SSVS) of the American Institute of Certified Public Accountants. This valuation was

performed solely to assist in the matter of establishing the fair market value of 80% of Erin’s Fitness Gear,

Inc’s non-voting common shares as of June 30, 2013. This value should not be used for any other purpose or

by any other party for any purpose. This valuation engagement was conducted in accordance with the

SSVS. The estimate of value that results from a valuation engagement is expressed as a conclusion of

value.

We have estimated the Fair Market Value on a minority interest, non-marketable basis for 80.00% of Erin’s

Fitness Gear, Inc.'s non-voting common shares as of June 30, 2013 as described within the valuation report.

Our conclusion is $1,990,000.00 or 1.31718 per share. This conclusion is subject to the Statement of

Assumptions and Limiting Conditions and the Representations presented in the following report. We have

no obligation to update this report or our conclusion of value for information that comes to our attention

after the date of this report.

In arriving at this opinion of value, we relied on a “value in use” or going-concern premise. This premise

assumes that the Company is an ongoing business enterprise with management operating in a rational way

with a goal of maximizing shareholder value.

Sincerely,

________________________

(Signature)

July 30, 2013

(Date)

— Table of Contents —

VALUATION OBJECTIVE AND SUMMARY ...................................................................................................... 1

EXTERNAL SOURCES OF INFORMATION ........................................................................................................ 3

INTERNAL SOURCES OF INFORMATION ......................................................................................................... 3

ASSUMPTIONS AND LIMITING CONDITIONS ......................................... ERROR! BOOKMARK NOT DEFINED.

COMPANY BACKGROUND ............................................................................................................................. 6

Company Identification .......................................................................................................................... 6

Nature and History of the Company ....................................................................................................... 6

Stock Classes and Ownership ................................................................................................................. 7

Management Team ................................................................................................................................. 7

Product and Service Information ............................................................................................................ 7

Market Data and Analysis/Competition ................................................................................................. 8

Governmental or Regulatory Environment ............................................................................................ 8

Key Customers and Suppliers ................................................................................................................ 8

Marketing Strategy ................................................................................................................................. 8

Business Risks ........................................................................................................................................ 8

Current Operations ................................................................................................................................. 8

Company Expectations ........................................................................................................................... 9

Other Observations ................................................................................................................................. 9

NATIONAL ECONOMIC AND INDUSTRY CONDITIONS .................................................................................. 10

General Economic Conditions and Outlook ......................................................................................... 10

Industry Conditions and Outlook ......................................................................................................... 10

HISTORICAL AND NORMALIZED FINANCIAL STATEMENTS......................................................................... 11

Summary Historical Income Statements .............................................................................................. 11

Income Statement Adjustments ............................................................................................................ 11

Normalized Historical Income Statements ........................................................................................... 12

Summary Historical Balance Sheets .................................................................................................... 12

Balance Sheet Adjustments .................................................................................................................. 13

Normalized Historical Balance Sheets ................................................................................................. 14

Summary Historical Statements of Cash Flows ................................................................................... 14

Normalized Earnings and Net Cash Flow Summary ............................................................................ 15

Normalized Earnings ..................................................................................................................... 15

Normalized Equity Net Cash Flows (FCF-Equity) ........................................................................ 15

Normalized Invested Capital Net Cash Flows (FCF-TIC) ............................................................. 16

Normalized Interim Financial Statements ............................................................................................ 16

ANALYSIS OF HISTORIC FINANCIAL STATEMENTS ..................................................................................... 18

Common-Size (Percentage) Financial Statements ............................................................................... 19

Integra Industry Data, Common-Size Statement Comparison ....................................................... 22

RMA Industry Data, Common-Size Statement Comparison ......................................................... 27

Financial Ratio Analysis....................................................................................................................... 30

Integra Industry Data, Ratio Comparison ...................................................................................... 34

RMA Industry Data, Ratio Comparison ........................................................................................ 39

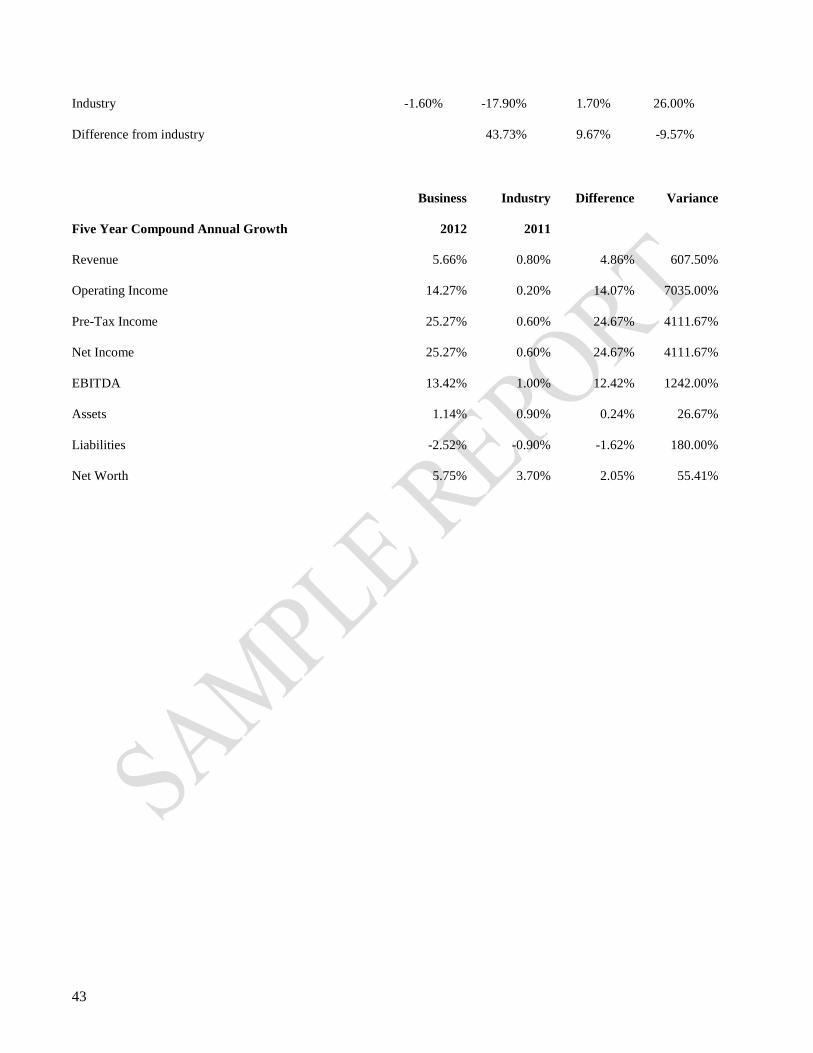

Integra Industry Data, Growth Comparison ................................................................................... 41

VALUATION OF ERIN’S FITNESS GEAR, INC. ......................................................................................... 44

Overview of Valuation Approaches and Methods ............................................................................... 46

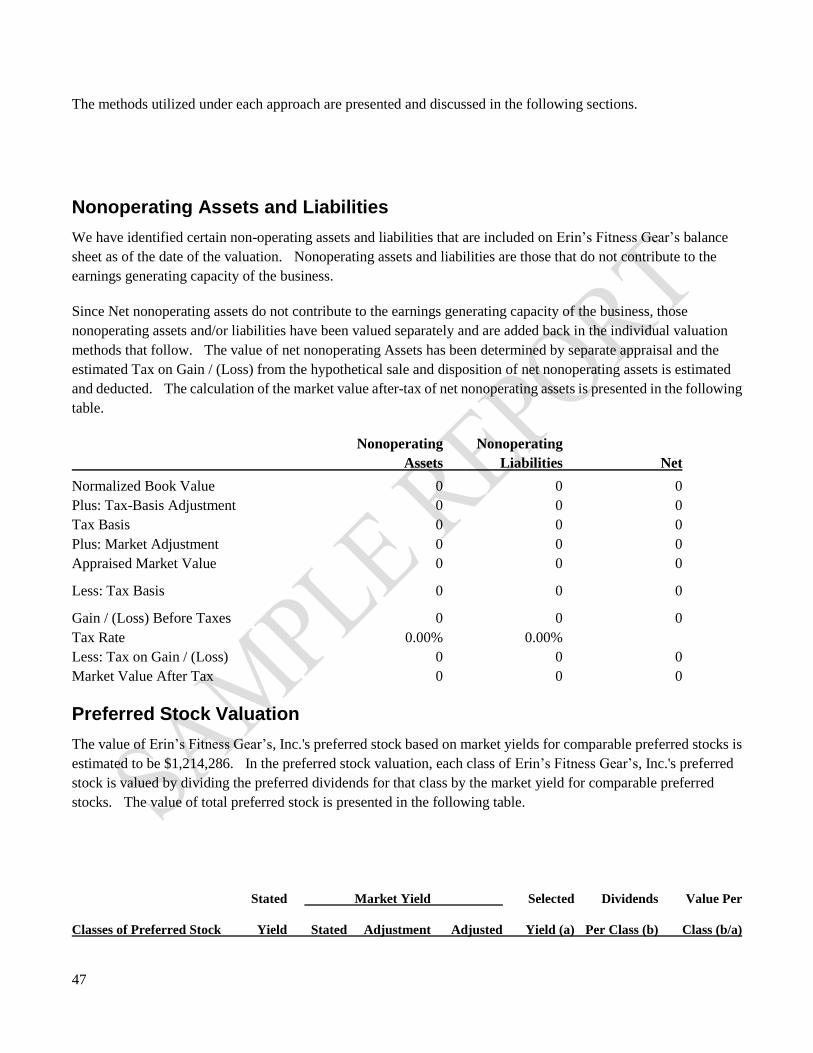

Nonoperating Assets and Liabilities ..................................................................................................... 47

Preferred Stock Valuation .................................................................................................................... 47

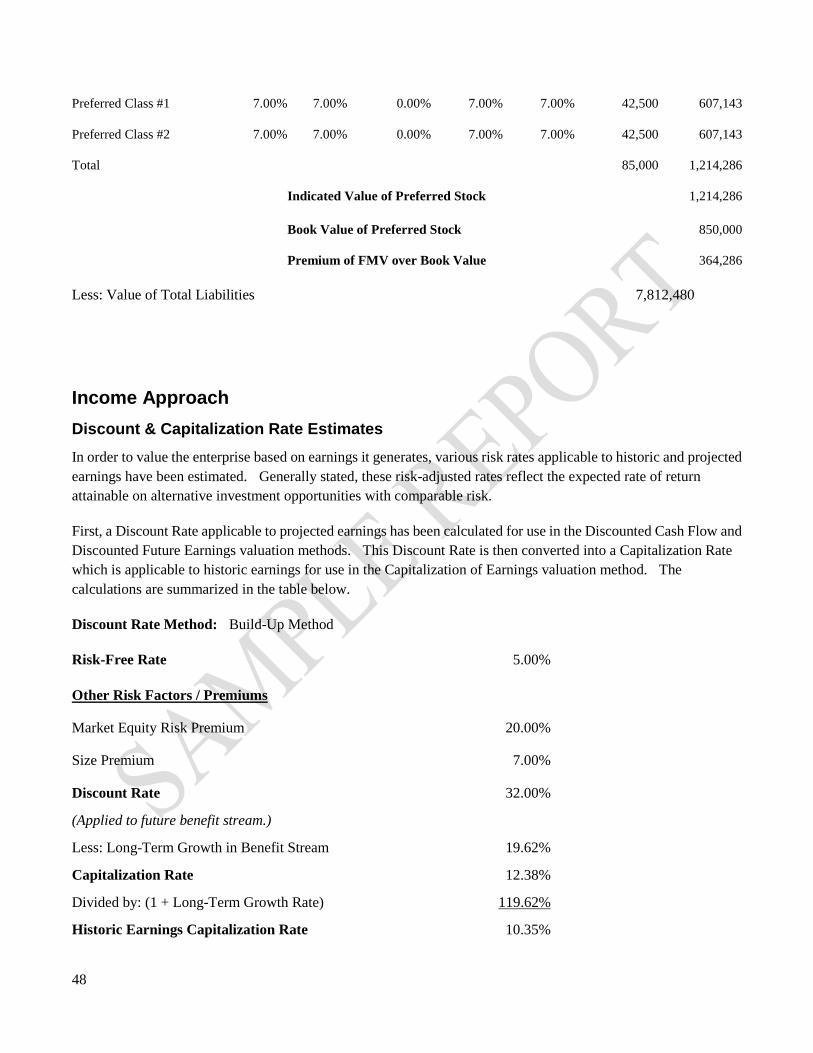

Income Approach ................................................................................................................................. 48

Discount & Capitalization Rate Estimates ..................................................................................... 48

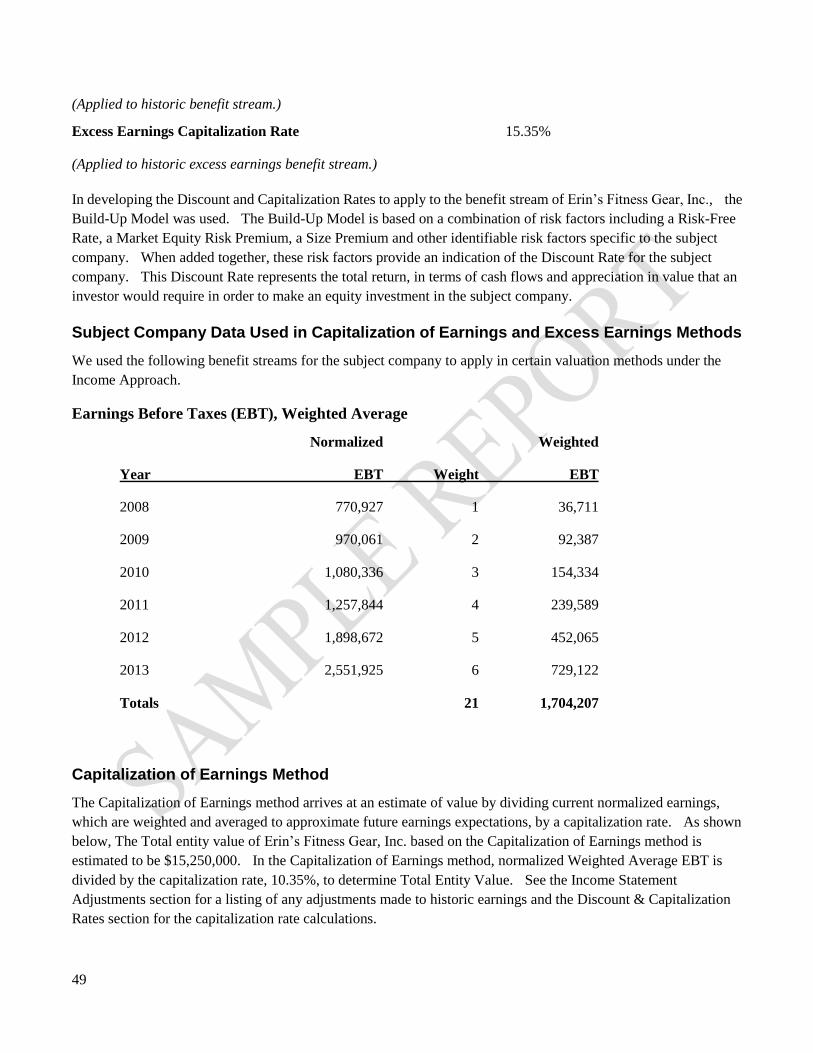

Subject Company Data Used in Capitalization of Earnings and Excess Earnings Methods ......... 49

Capitalization of Earnings Method ................................................................................................ 49

Capitalization of Excess Earnings ................................................................................................. 50

Discounted Future Earnings ........................................................................................................... 52

Market Approach .................................................................................................................................. 54

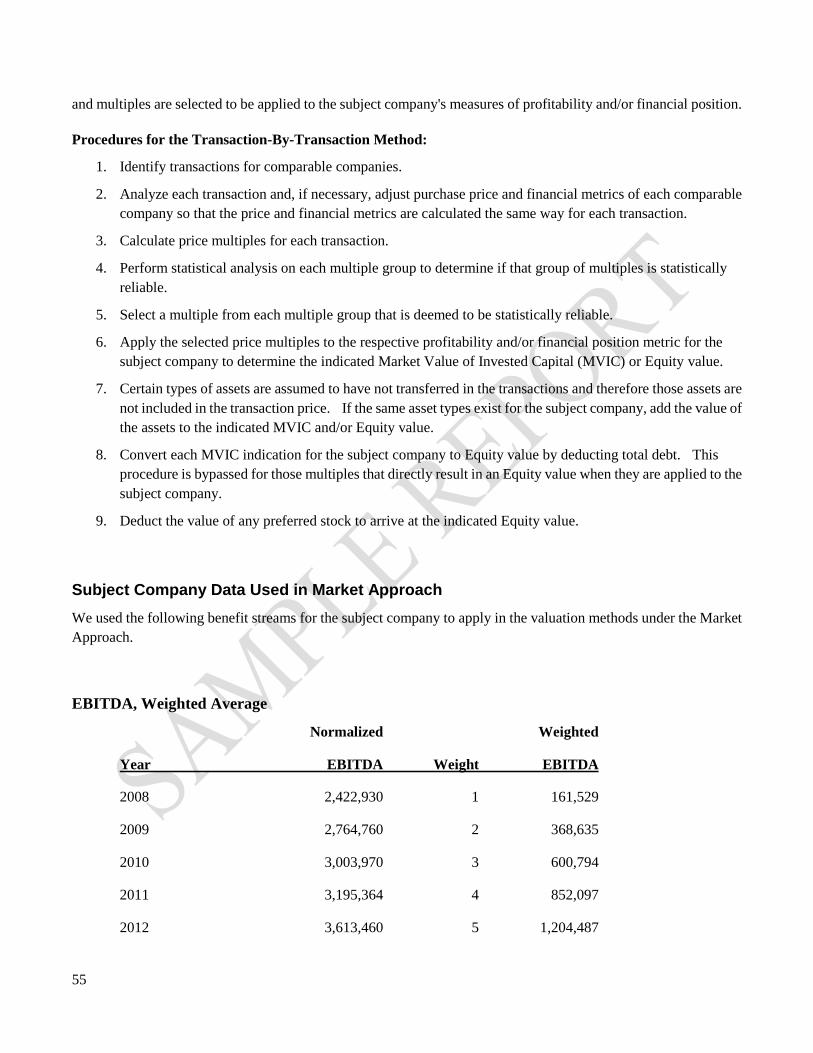

Subject Company Data Used in Market Approach ........................................................................ 55

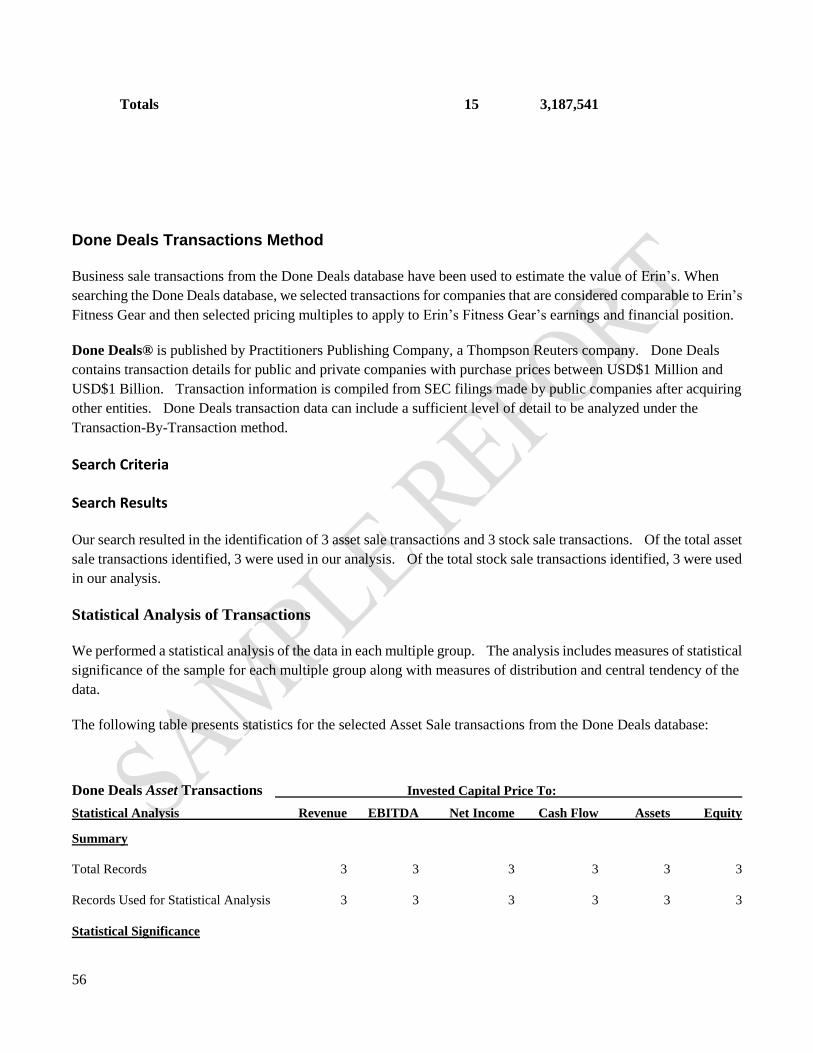

Done Deals Transactions Method .................................................................................................. 56

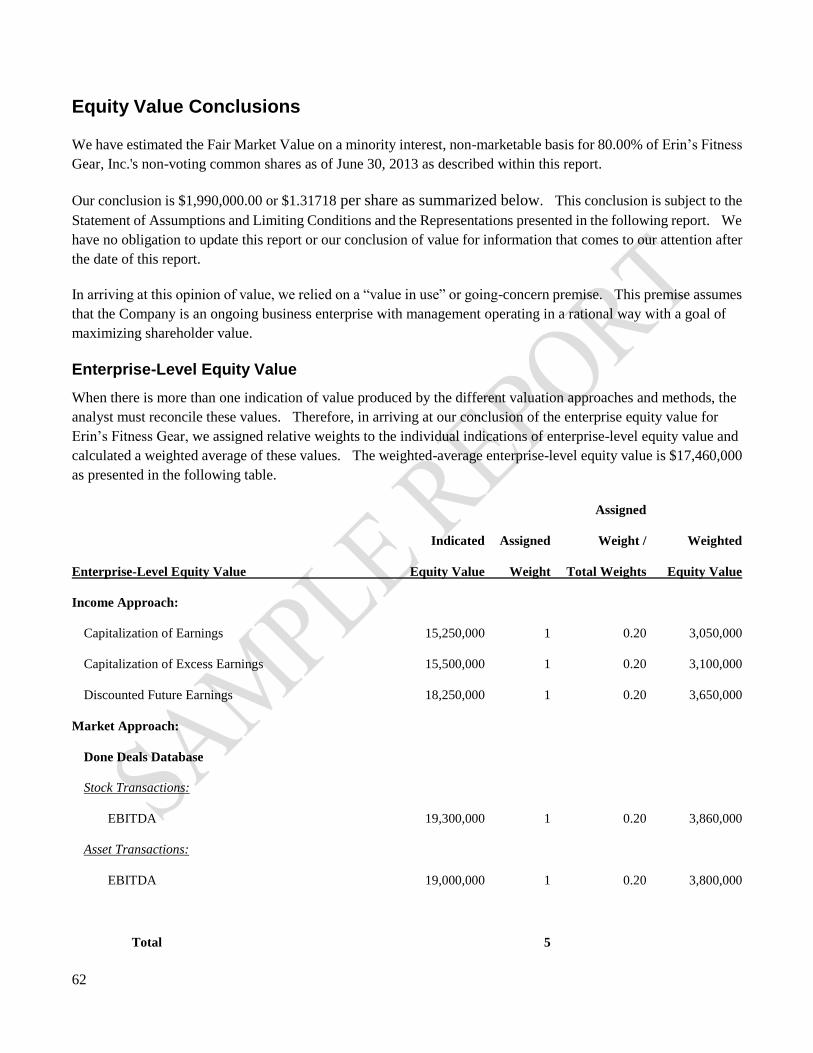

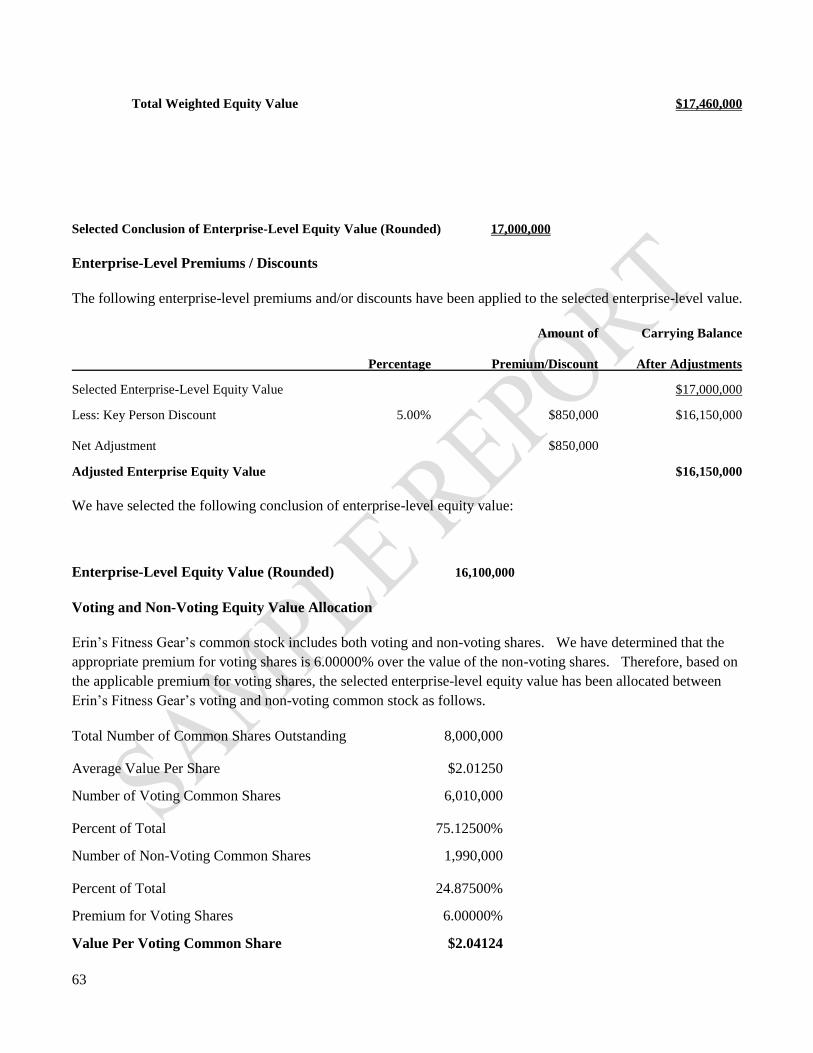

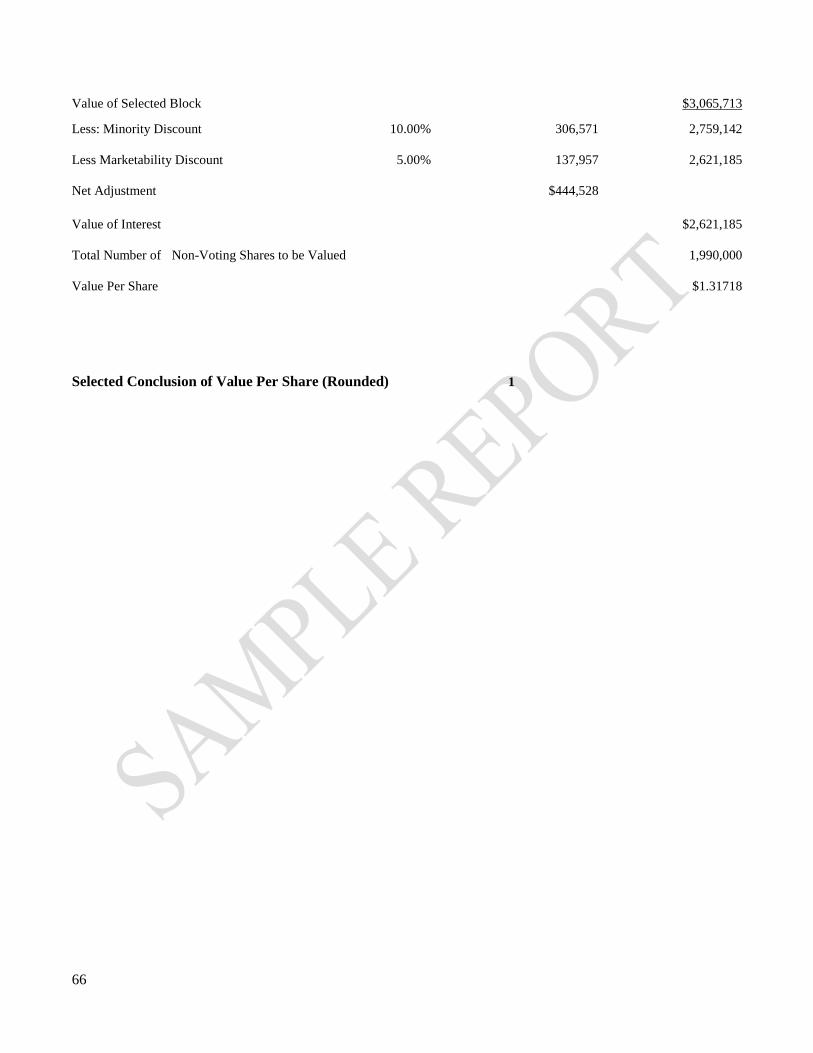

Equity Value Conclusions .................................................................................................................... 62

Enterprise-Level Equity Value ...................................................................................................... 62

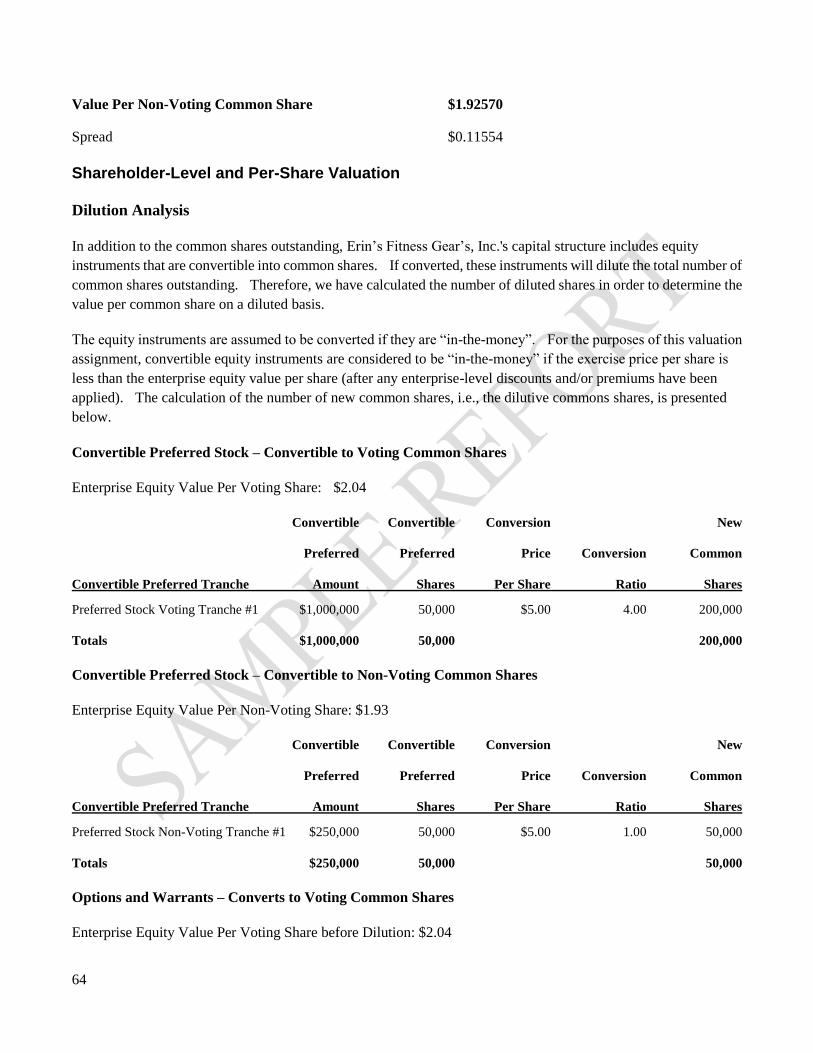

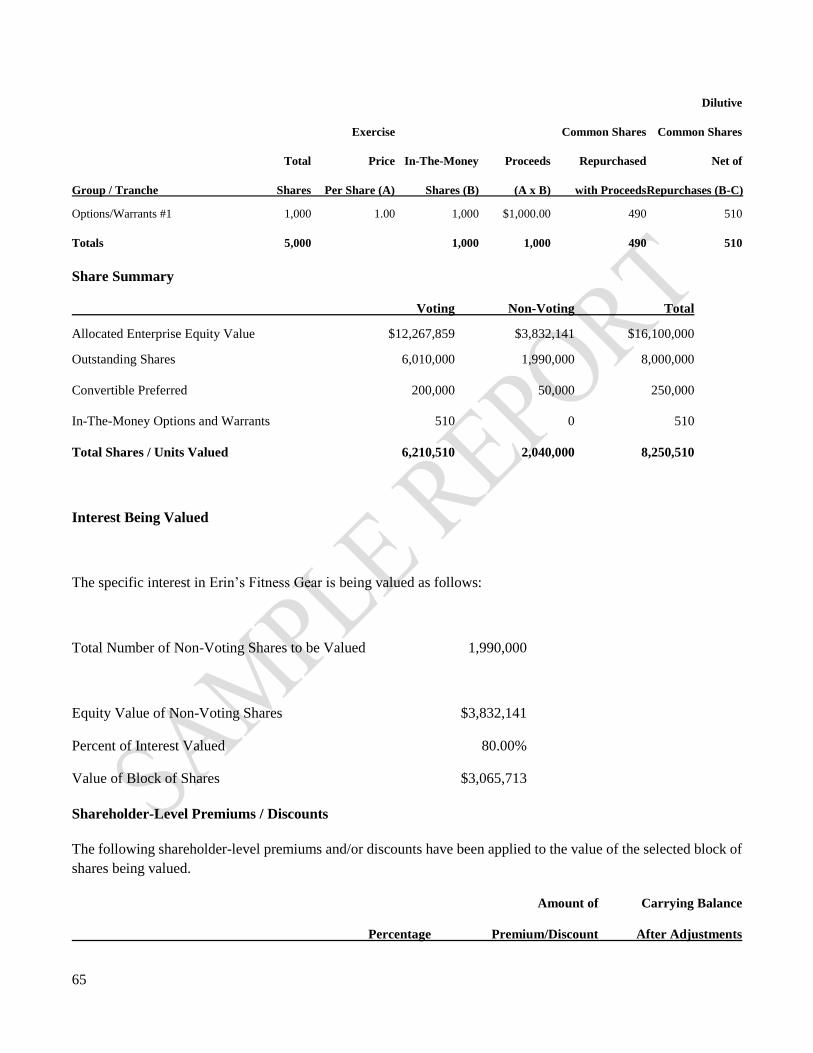

Shareholder-Level and Per-Share Valuation .................................................................................. 64

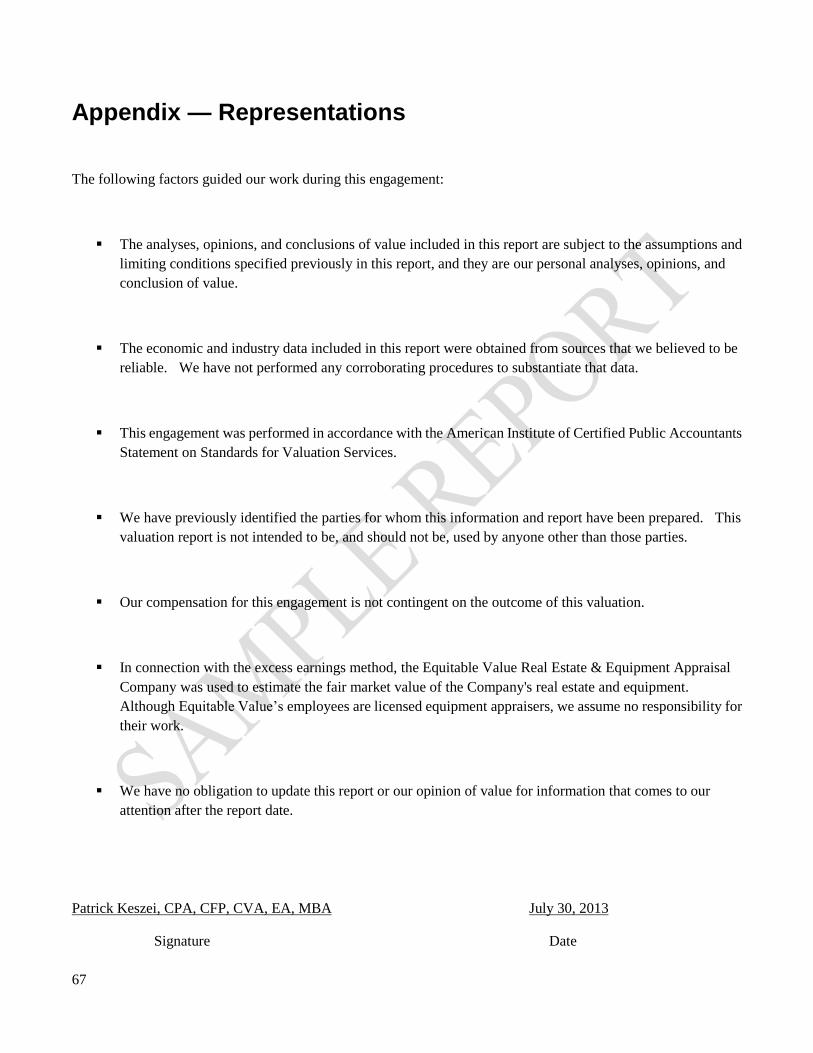

APPENDIX — REPRESENTATIONS ............................................................................................................... 67

APPENDIX — QUALIFICATIONS .................................................................................................................. 68

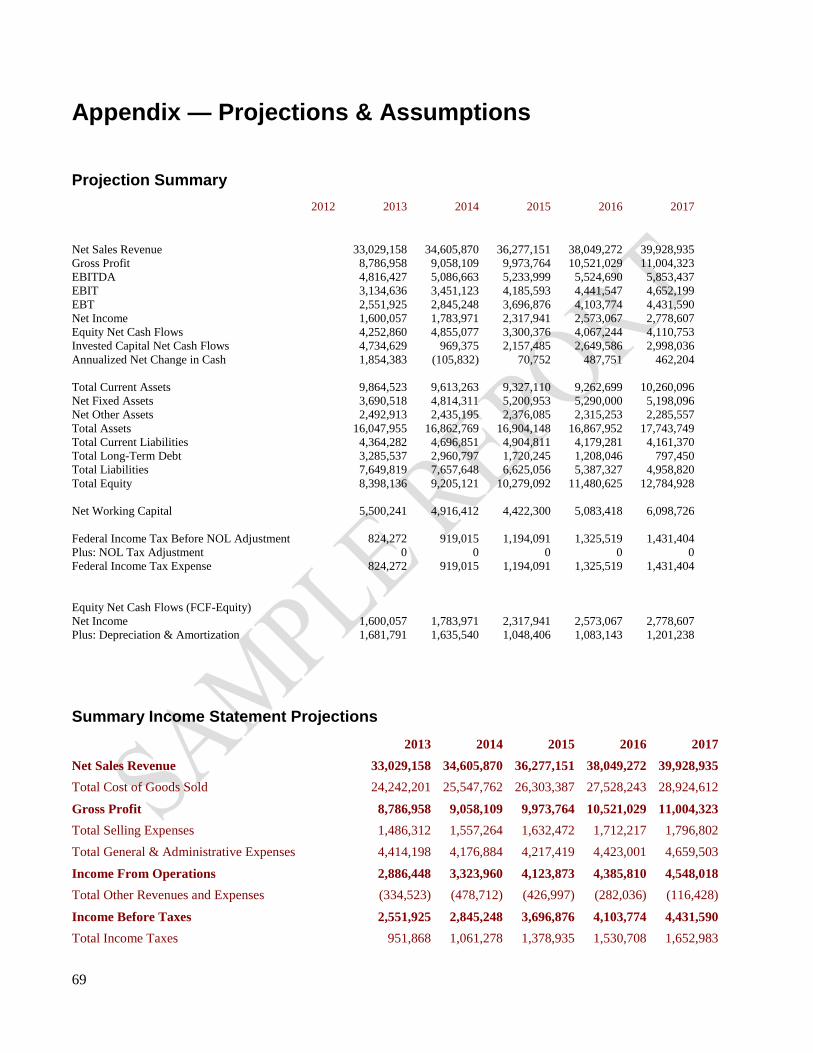

APPENDIX — PROJECTIONS & ASSUMPTIONS ............................................................................................ 69

Projection Summary....................................................................................................................... 69

Summary Income Statement Projections ....................................................................................... 69

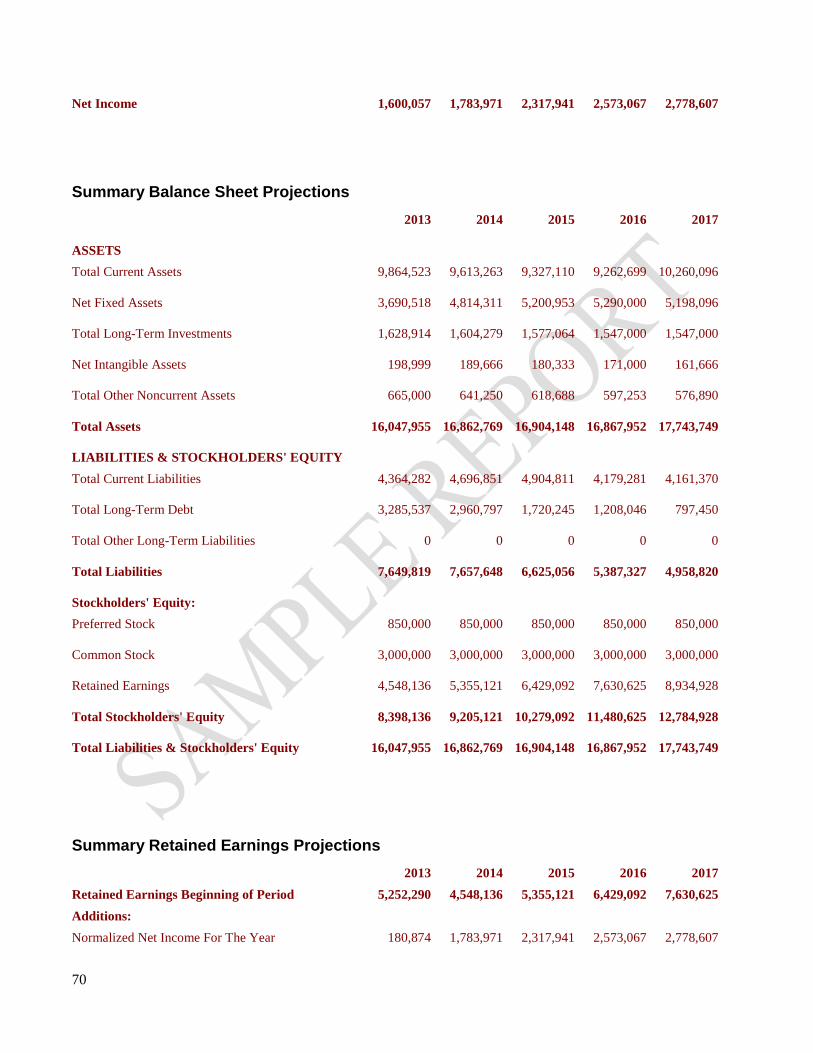

Summary Balance Sheet Projections ............................................................................................. 70

Summary Retained Earnings Projections ....................................................................................... 70

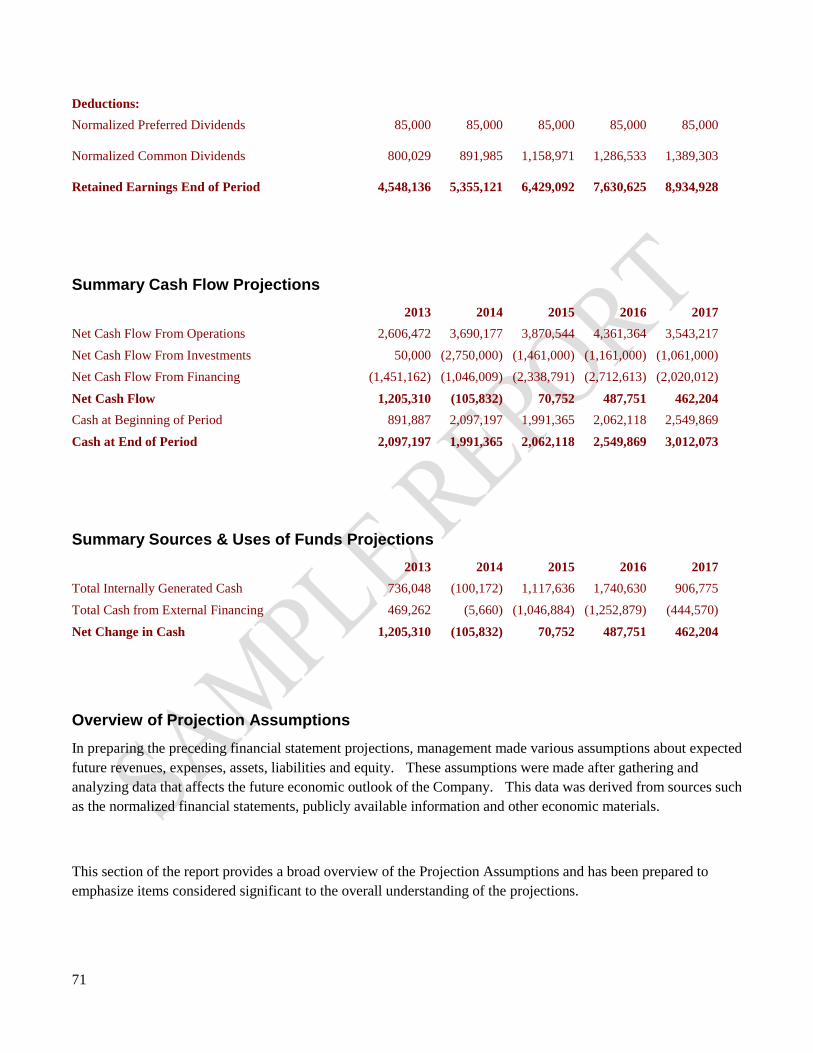

Summary Cash Flow Projections ................................................................................................... 71

Summary Sources & Uses of Funds Projections ........................................................................... 71

Overview of Projection Assumptions ............................................................................................ 71

Revenue & Expense Assumptions ................................................................................................. 72

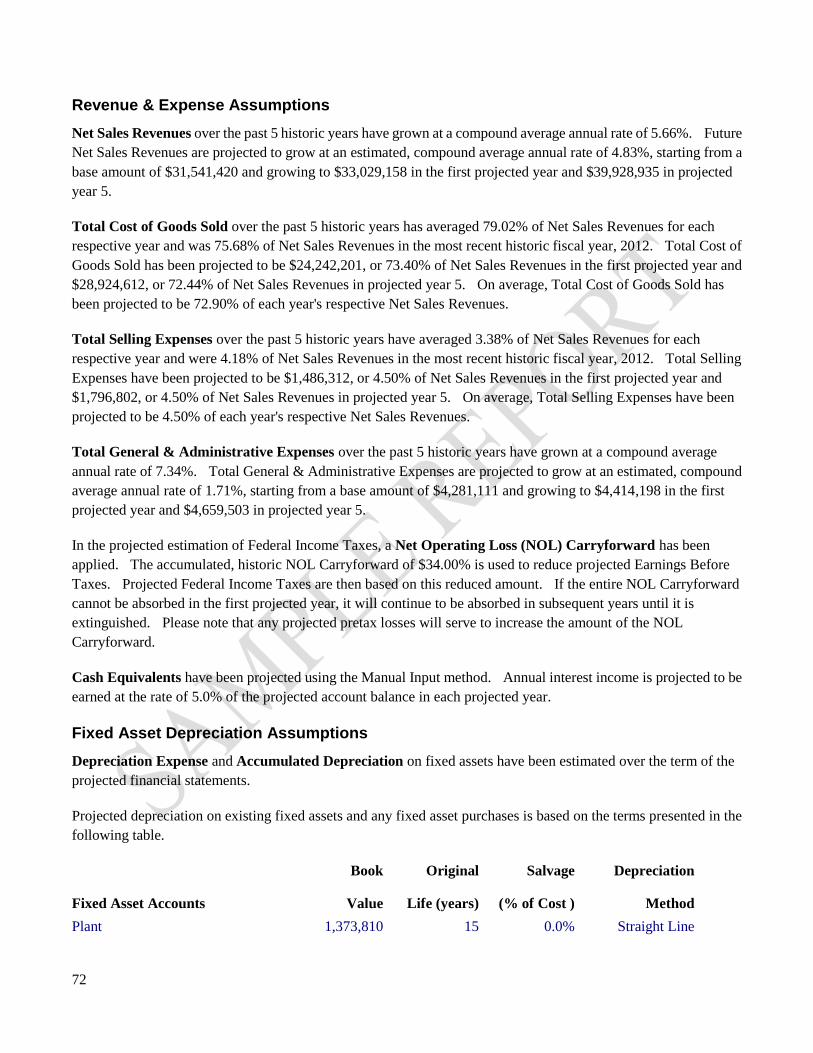

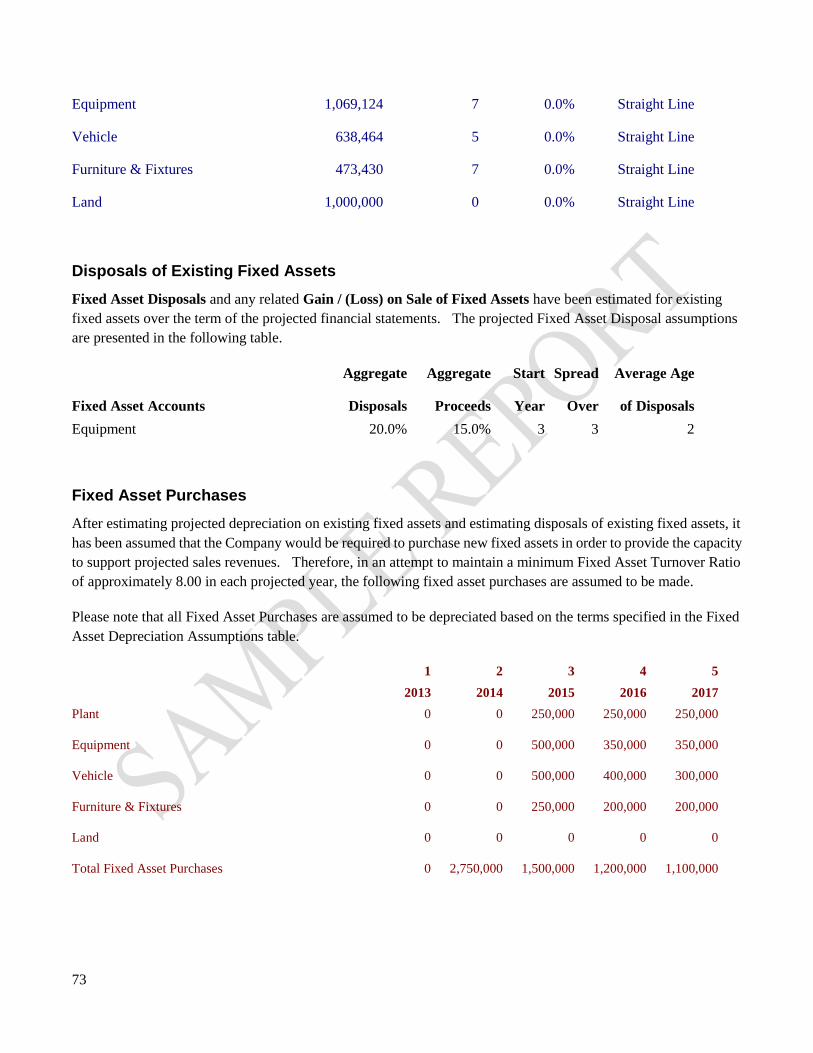

Fixed Asset Depreciation Assumptions ......................................................................................... 72

Disposals of Existing Fixed Assets ................................................................................................ 73

Fixed Asset Purchases.................................................................................................................... 73

Existing Notes Receivable Assumptions ....................................................................................... 74

Amortization of Intangible Assets ................................................................................................. 74

Existing Notes Payable Assumptions ............................................................................................ 74

Fixed Asset Purchase Financing Assumptions .............................................................................. 74

Dividends Assumptions ................................................................................................................. 75

1

Valuation Objective and Summary

Assignment Objective

We were engaged by Erin K. O’Donnell, President of Erin’s Fitness Gear, Inc., to issue a business valuation report.

Our objective was to estimate the Fair Market Value of 80.00% of Erin’s Fitness Gear, Inc.'s non-voting common

shares as of June 30, 2013.

Company Description

Erin’s Fitness Gear, Inc. is a C-Corporation and is organized under the laws of Indiana. The Company is primarily

engaged in the business of manufacturing and wholesaling of fitness gear, supplies, clothing and equipment. The

Company is doing business as Erin’s Fitness Gear.

Qualifications of Appraiser

This report was prepared by Patrick Keszei, Manager of Business Valuation Services of Business ValueCalc.

Patrick Keszei holds the following professional designations and certifications: CPA, CFP, CVA, EA, MBA.

Please refer to the appendix – qualifications for his curriculum vitae.

Purpose of Valuation

The purpose of this valuation is to determine the fair market value of 80.00% of Erin’s Fitness Gear, Inc.’s

non-voting common shares as of June 30, 2013. This report is prepared for Erin K. O’Donnell, President, and

should not be used by others. This report is dated July 30, 2013.

Standard of Value

The standard of value used in our valuation of Erin’s Fitness Gear, Inc. is Fair Market Value. Fair Market Value is

defined in IRS Revenue Ruling 59-60 as: “The price at which the property would change hands between a willing

buyer and a willing seller when the former is not under any compulsion to buy and the latter is not under any

compulsion to sell, both parties having reasonable knowledge of relevant facts. Court decisions frequently state in

addition that the hypothetical buyer and seller are assumed to be able, as well as willing, to trade and to be well

informed about the property and concerning the market for such property.”

Premise of Value

Our opinion of value relied on a “value in use” or going-concern premise. This premise assumes that the Company

is an ongoing business enterprise with management operating in a rational way with a goal of maximizing

shareholder value.

Scope of Work

Our analysis considers those facts and circumstances present at the Company at the valuation date. Our opinion

would most likely be different if another valuation date was used. There were no restrictions or limitations in the

scope of our work or in the data available for analysis, and no hypothetical assumptions were used.

The factors we considered include the history of the business, economic outlook, financial condition of the business,

earnings and dividend paying capacity, book value of the stock and the size of the block being valued, prior sales of

2

the Company's stock, goodwill and intangible value, and the market prices for publicly traded and privately held

companies in the same or similar line of business.

Valuation Procedures

To arrive at our conclusion of value, we performed the following procedures:

Identified the nature of the business and reviewed the history of the Company since its inception.

Researched the general economic outlook and the outlook for the specific industry at the date of the valuation.

Collected the Company's relevant historic financial statements.

Analyzed the historic financial statements by calculating financial ratios and common-size financial statements

for each historic year in order to identify trends.

Compared the Company's financial ratios and common-size financial statements to industry guideline data to

identify any significant variances.

Assisted management in preparing a five year projection of the financial statements based on management's

assumptions as to the Company's future outlook.

Analyzed Goodwill and other intangible value.

Identified and analyzed prior sales of the Company's stock.

Developed risk-adjusted Capitalization and Discount Rates to apply to the Company's historic and projected

earnings, respectively.

Collected and analyzed transactional data from comparable companies within the same industry.

Adjusted historic earnings to eliminate the effects of excess and discretionary expenses, nonoperating revenues

and expenses, and non-transferable revenue streams.

In reaching the conclusion of value, we considered the asset, income, and market valuation approaches and the

following methods under each approach.

1. Asset Approach

Net Asset Value

Liquidation Value.

2. Income Approach

Capitalization of Earnings

Capitalization of Excess Earnings

Multiple of Discretionary Earnings

Discounted Future Earnings/Discounted Cash Flow.

3

3. Market Approach

Price multiples from sales of comparable businesses from the following data sources:

BIZCOMPS

IBA Database

Done Deals

Pratt's Stats

Other Data Source

FactSet Mergerstat Review

Guideline Public Company Data

Selected the most reasonable enterprise-level equity value from the range of values established in the valuation

methods

Applied any appropriate enterprise-level discounts and/or premiums to arrive at an enterprise-level equity

value.

Allocated the conclusion of enterprise-level equity value between voting and non-voting shares based on a

premium assigned to the voting shares.

Calculated the total number of shares assuming dilution from convertible preferred stock and the in-the-money

options and warrants.

Calculated the shareholder-level value of the 80.00% interest.

Applied any appropriate shareholder-level discounts and/or premiums to arrive at our conclusion of value for

the specific block of shares.

External Sources of Information

To aid us in our analysis of the Company, we searched a number of publicly available sources of information.

Numerous financial publications and databases were consulted including Business Statistics, Standard & Poor's

Industry Surveys, Ibbotson Associates' Stocks, Bonds, Bills and Inflation 200X Yearbook, Mergerstat Review, U.S.

Financial Data, Standard & Poor's Register of Corporations, Directors, and Executives, Disclosure, Inc. on-line

database, and Value Line Investment Survey. Integra Industry Data and RMA Industry Data were used for ratio

analysis and comparative industry data.

Internal Sources of Information

To aid us in our analysis of the Company, we interviewed the following personnel:

Erin K. O’Donnell: President

4

Izaak Katz: Vice President

Albert Johnson: Chief Operations Officer

Victor J. Spaniolo, CPA: Chief Financial Officer

Joey Husband: Chief Information Officer

We conducted a complete tour of the facilities and spoke with numerous company personnel.

We collected the following source data:

Five years of audited financial statements

Interim financial statements

Five years of corporate tax returns.

Company bylaws & minutes

Assumptions and Limiting Conditions

This valuation is subject to the following assumptions and limiting conditions:

1. Public, industry, statistical, and other information furnished by others, upon which all or portions of this

analysis is based, is believed to be reliable. However, we make no representation as to the accuracy or

completeness of such information and have performed no procedures to corroborate the information.

2. The Company and its representatives warranted to us that the information they supplied was complete and

accurate to the best of their knowledge and that the financial statement information reflects the Company's

results of operations and financial and business condition in accordance with generally accepted accounting

principles, unless otherwise noted. The financial statements and other related information supplied by

management has been accepted as correct without further verification. We have not audited, reviewed, or

compiled the financial information provided to us and, accordingly, we express no audit opinion or any

other form of assurance on this information.

3. This report and conclusion of value is restricted to the internal use of the management of the Company for

the sole and specific purpose as noted herein, and shall not be used to obtain credit or for any other purpose

or by any other party for any purpose. Neither our work product nor any portions thereof, including any

conclusions or the identity of our firm, any individuals signing or associated with this report, or the

professional associations or organizations with which they are affiliated, shall be disseminated to third

parties other than the Company, its financial accounting firm and attorneys, and governmental agencies by

any means without our prior written consent and approval.

4. We or any individual associated with this assignment are not required to provide future services regarding

the subject matter of this report, including but not limited to providing further consultation, providing

testimony, or appearing in court or other legal proceedings unless specific arrangements have been made.

5

5. The conclusion of value is valid only for the stated purpose as of the valuation date indicated. We take no

responsibility for changes in market conditions and assume no obligation to revise our conclusion of value

to reflect events or conditions which occur subsequent to the valuation date.

6. Full compliance by the Company with all applicable federal, state, and local zoning and use, occupancy,

environmental, and similar laws and regulations is assumed, unless otherwise stated. Furthermore, no effort

has been made to determine the possible effect, if any, on the Company due to future Federal, state, or local

legislation including any environmental or ecological matters or interpretations thereof, unless otherwise

stated.

7. This report and the conclusion of value arrived at herein are not intended by the author and should not be

construed by the reader to be investment advice in any manner whatsoever. The conclusion of value

represents the considered opinion of Business ValueCalc based on information furnished to them by the

Company and other sources.

8. We do not provide assurance on the achievability of the results forecasted by the Company because events

and circumstances frequently do not occur as expected; differences between actual and expected results

may be material; and achievement of the forecasted results is dependent on actions, plans, and assumptions

of management.

9. For the prospective financial information approved by management that was used in our engagement, we

have not examined or compiled the prospective financial information and therefore, do not express an audit

opinion or any other form of assurance on the prospective financial information or the related assumptions.

Events and circumstances frequently do not occur as expected and there will usually be differences between

prospective financial information and actual results, and those differences may be material.

10. We are not environmental consultants or auditors, and we take no responsibility for any actual or potential

environmental liabilities. Any person entitled to rely on this report, wishing to know whether such liabilities

exist, or the scope and their effect on the value of the property, is encouraged to obtain a professional

environmental assessment. We do not conduct or provide environmental assessments and have not

performed one for the subject property.

11. We have not determined independently whether the Company is subject to any present or future liability

relating to environmental matters, including but not limited to CERCLA/Superfund liability, nor the scope

of any such liabilities. Our valuation takes no such liabilities into account, except as they have been

reported to us by the Company or by an environmental consultant working for the Company, and then only

to the extent that the liability was reported to us in an actual or estimated dollar amount. Such matters, if

any, are noted in the report. To the extent such information has been reported to us, we relied on it without

verification and offer no warranty or representation as to its accuracy or completeness.

12. Except as noted, we have relied on the representations of the owners, management, and other third parties

concerning the value and useful condition of all equipment, real estate, and any other assets or liabilities,

except as specifically stated to the contrary in this report. We have not attempted to confirm whether all

assets of the business are free and clear of liens and encumbrances or that the Company has good title to all

assets.

13. Neither all nor any part of the contents of this report (including the conclusion of value, the identity of any

6

valuation specialist(s), the firm with which such valuation specialists are connected, or any reference to any

of their professional designations) should be disseminated to the public through advertising media, public

relations, news media, sales media, mail, direct transmittal, or any other means of communication without

our prior written consent and approval.

14. We have not made a specific compliance survey or analysis of the subject property to determine whether it

is subject to, or in compliance with, the American Disabilities Act of 1990, and this valuation does not

consider the effect, if any, of noncompliance.

15. No change of any item in this valuation report shall be made by anyone other than, and we shall have no

responsibility for any such unauthorized change.

16. We have conducted interviews with the current management of the Company concerning the past, present,

and future operating results of the Company.

17. This conclusion of value assumes that the Company will continue to operate as a going concern, and that the

character and integrity of the Company through any sale, reorganization, exchange, or diminution of the

owners' participation would not be materially or significantly changed. It also assumes that the current level

of management expertise and effectiveness would continue to be maintained.

Company Background

Company Identification

Erin’s Fitness Gear, Inc. is a C-Corporation organized under the laws of Indiana and is located at 100 Erskine Plaza,

South Bend, IN 46614-3244.

Nature and History of the Company

Erin’s Fitness Gear, Inc. was established in 2001 and operates under the trade name of Erin’s Fitness Gear.

The following table describes the business activities in which Erin’s Fitness Gear, Inc. is engaged and lists the

NAICS/SIC Codes for the industry associated with each business activity:

Business Activity Description NAICS SIC

7

Primary Business Activity Fitness Products Manufacturing 339920 3949

Secondary Business Activity Fitness Product Wholesale 421910 5091

Erin’s Fitness Gear, Inc. commenced operations in January of 2001. The company started with one wholesale

location and quickly grew to five outlets. In 2005, the company built a manufacturing facility. This vertical

integration enabled Erin’s to custom-design their products and control costs. The Company offers a full line of

fitness gear. Please refer to the Company’s website: www.erinsfitnessgear.com for a full listing of all their

products.

Stock Classes and Ownership

The following table lists the owners of Erin’s Fitness Gear, Inc.’s commons stock as of the valuation date, June 30,

2013. The number of shares, equity class and other details are presented for each owner.

Number Percent Equity Active in Number

Classes of Common Stock of Shares Ownership Class Business of Votes Preemptive Dividends

Izaak Katz 3,000,000 37.50% A Yes 3,000,000 0

Erin K. O’Donnell 4,000,000 50.00% A Yes 4,000,000 0

Other Shareholders 1,000,000 12.50% No 0 0

Total 8,000,000 100.00%

Management

Outlined below is a list of the Company’s managerial staff:

Erin K. O’Donnell: President

Izaak Katz: Vice President

Albert Johnson: Chief Operations Officer

Victor J. Spaniolo, CPA: Chief Financial Officer

Joey Husband: Chief Information Officer.

Product and Service Information

The Company is a manufacturer and wholesaler of fitness goods, primarily exercise equipment. The products are

of exquisite quality. Erin’s products compete with mid to high-end fitness gear manufacturers and wholesalers.

Erin’s niche is the “selective customer” who needs the best and most durable fitness equipment, supplies and gear

8

available. Please refer to Erin’s website for a full product catalog at www.erinsfitnessgear.com

Market Data and Analysis/Competition

Brunswick Corporation (Life Fitness) and Johnson Health Tech. Co., Ltd, are the major players in this industry.

Competitive rivalry in the industry is high. The existing players continuously try to maintain their market shares

and drive growth by entering new regions and introducing technologically advanced products and product

innovations. Right now, this market represents stiff competition. The players are established and the economy is

well below par and exercise equipment is not a recession proof product. In the future, as the world economy grows

and more foreign countries vie for fitness center, long-term growth potential exists.

Governmental or Regulatory Environment

Erin’s Fitness Gear, Inc. has a capable quality control, accounting, legal and human resource departments. The

Company has adhered to all governmental and regularity laws and rules. We visualize that the company will

continue its record of excellence and will continue to place a material emphasis on this topic.

Key Customers and Suppliers

The Company sells their fitness gear to numerous fitness clubs, sporting goods stores and large merchandise

retailers. It also purchases their inventory, material and supplies from numerous vendors. The company views this

diversification as a strength because it is does not rely on a few customers or a few vendors. The list of customers

and vendors would be impractical to list here. In summary, the company’s customers and vendors are diversified.

Marketing Strategy

Erin’s current marketing strategy is to develop the foreign markets. The company will concentrate their efforts on

the countries with the most growth potential, such as China and India. The domestic market is somewhat saturated

and growth lies with the developing economies of the world. All else remains the same. Erin’s will continue to

market to the mid-level to high-end customer.

Business Risks

The top business risk for Erin’s is the oversaturation of the market with physical fitness equipment. Numerous

companies manufacture and market physical fitness gear. The domestic market is mature. This can create an

abundant supply and place downward pressure on pricing, thus reducing net profit. The company’s strategy is to

maintain our domestic presence and pursue the growing foreign markets.

Current Operations

The corporate office of Erin’s Fitness Gear is headquartered in South Bend, Indiana. The company owns two

manufacturing facilities, one in South Bend and the other in Clarion, Pennsylvania. Eight retail stores are scattered

through the Midwest. The Company has an excellent logistic system. Upon product completion, the goods are

transported by truck to the various retail stores. A “just in time” inventory system is used to maintain cost controls.

The company recently passed their ISO 9000 audit. The company undergoes an annual financial statement audit by

their CPA firm each year and is in full compliance.

9

Company Expectations

The Company expects sales to grow by about three to four percent per year. Profitability is important, however,

the current plan is to invest profits into the company, reduce debt and pursue the foreign markets. The company

expects that this strategy will provide long-term growth and profitability.

Other Observations

None

10

National Economic and Industry Conditions

General Economic Conditions and Outlook

The United States economy slowed in the second quarter amid weak consumer spending, government cuts and a rise

in imports from foreign countries. As of June 30, 2013, the Gross Domestic Product (GDP) of the United States

grew at an annual rate of 1.7%, from April to June. That’s significantly down from a forty year average growth rate

of 3.23%%.

US inflation rose 1.8 percent over the last year ending June 30, 2013. The nation’s unemployment rate was slightly

down at 7.6 % for the second consecutive month, the Labor Department reported. The economic forecast is not

great and not gloomy, but rather unpredictable. The best bet is the economy will be rather stable with no extreme

ups or downs. The world’s best economists and investors predict that the upcoming twelve month period will be a

year of volatility and uncertainty for the markets and global economy, as a whole.

Industry Conditions and Outlook

The global fitness equipment industry is forecast to grow with a compound annual growth rate of 3.5% over the next

five years (2013 – 2018) and reach an approximate 10.6 billion by 2018. Rising concern and awareness for healthful

living, physical benefits and exercise are among the major drivers for fitness equipment demand around the world.

Several drivers are anticipated to fuel the market during the next five years. Among these are the rapid

modernization of economies with increasing spending capacity; the opening of new fitness centers & clubs and

expansion of existing players in emerging economies: the World Health Organizations’s physical activity

recommendations and governmental efforts to promote the benefits of exercise. The industry is expected to

expand its presence in India and China, as they possess good growth opportunities with expanding, new upper class

populations and increasing purchasing power

11

Historical and Normalized Financial Statements

A summary of the historic Income Statements, Balance Sheet, and Cash Flows for Erin’s Fitness Gear, Inc. is

presented in the following section.

Financial statement data is necessary in order to analyze the historic performance of the business and how that

performance compares to its peers in the industry. Prior revenues, expenses and earnings provide a baseline for

estimating future earnings and cash flows.

Summary Historical Income Statements

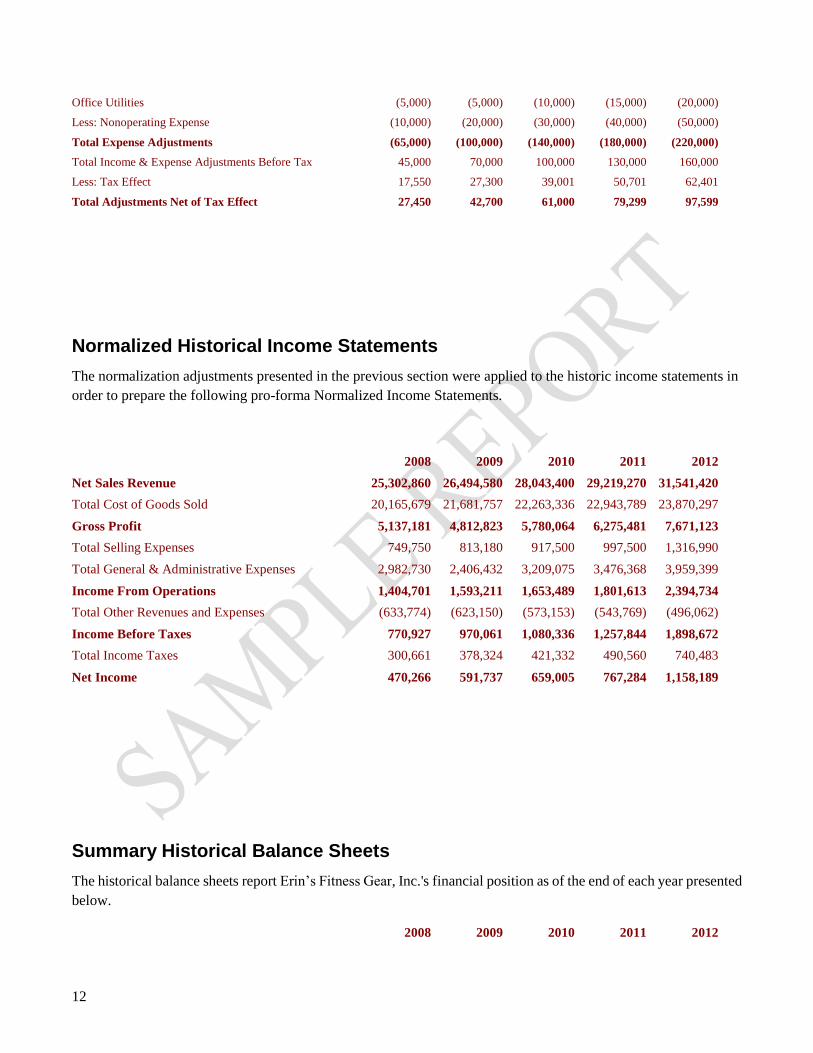

The following tables provide a summary of Erin’s Fitness Gear, Inc.'s Income Statements.

2008 2009 2010 2011 2012

Net Sales Revenue 25,302,860 26,494,580 28,043,400 29,219,270 31,541,420

Total Cost of Goods Sold 20,165,679 21,681,757 22,263,336 22,943,789 23,870,297

Gross Profit 5,137,181 4,812,823 5,780,064 6,275,481 7,671,123

Total Selling Expenses 749,750 813,180 917,500 997,500 1,316,990

Total General & Administrative Expenses 3,037,730 2,486,432 3,319,075 3,616,368 4,129,399

Income From Operations 1,349,701 1,513,211 1,543,489 1,661,613 2,224,734

Total Other Revenues and Expenses (623,774) (613,150) (563,153) (533,769) (486,062)

Income Before Taxes 725,927 900,061 980,336 1,127,844 1,738,672

Total Income Taxes 283,111 351,024 382,331 439,859 678,082

Net Income 442,816 549,037 598,005 687,985 1,060,590

Income Statement Adjustments

In order to estimate the value of Erin’s Fitness Gear, Inc., it was necessary to make certain normalization

adjustments to the Income Statements. Normalization adjustments are made to reflect the Company's true

economic earnings by eliminating excessive, nonoperating, non-recurring and/or unusual items. The following

table presents a summary of the adjustments that were made to Erin’s Fitness Gear, Inc.'s earnings.

2008 2009 2010 2011 2012

Add/(Deduct) Income Adjustments:

Nonoperating Income (20,000) (30,000) (40,000) (50,000) (60,000)

Total Income Adjustments (20,000) (30,000) (40,000) (50,000) (60,000)

Add/(Deduct) Expense Adjustments:

Officer/Owner's Compensation (50,000) (75,000) (100,000) (125,000) (150,000)

12

Office Utilities (5,000) (5,000) (10,000) (15,000) (20,000)

Less: Nonoperating Expense (10,000) (20,000) (30,000) (40,000) (50,000)

Total Expense Adjustments (65,000) (100,000) (140,000) (180,000) (220,000)

Total Income & Expense Adjustments Before Tax 45,000 70,000 100,000 130,000 160,000

Less: Tax Effect 17,550 27,300 39,001 50,701 62,401

Total Adjustments Net of Tax Effect 27,450 42,700 61,000 79,299 97,599

Normalized Historical Income Statements

The normalization adjustments presented in the previous section were applied to the historic income statements in

order to prepare the following pro-forma Normalized Income Statements.

2008 2009 2010 2011 2012

Net Sales Revenue 25,302,860 26,494,580 28,043,400 29,219,270 31,541,420

Total Cost of Goods Sold 20,165,679 21,681,757 22,263,336 22,943,789 23,870,297

Gross Profit 5,137,181 4,812,823 5,780,064 6,275,481 7,671,123

Total Selling Expenses 749,750 813,180 917,500 997,500 1,316,990

Total General & Administrative Expenses 2,982,730 2,406,432 3,209,075 3,476,368 3,959,399

Income From Operations 1,404,701 1,593,211 1,653,489 1,801,613 2,394,734

Total Other Revenues and Expenses (633,774) (623,150) (573,153) (543,769) (496,062)

Income Before Taxes 770,927 970,061 1,080,336 1,257,844 1,898,672

Total Income Taxes 300,661 378,324 421,332 490,560 740,483

Net Income 470,266 591,737 659,005 767,284 1,158,189

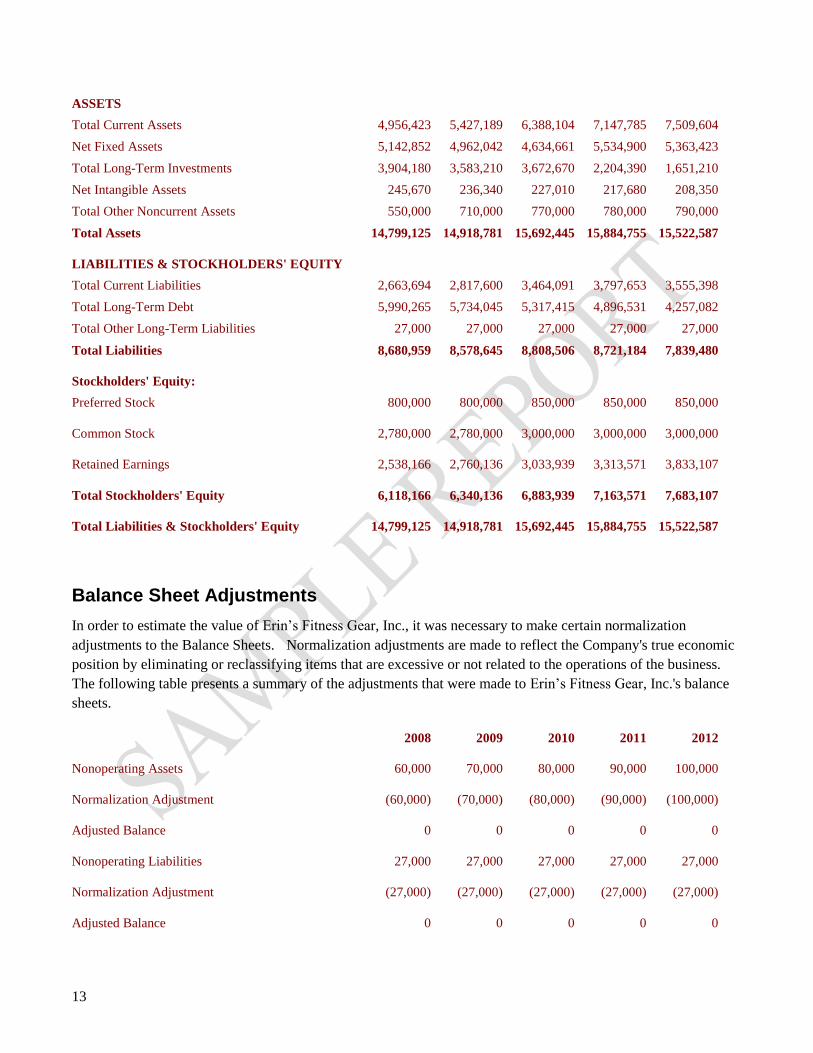

Summary Historical Balance Sheets

The historical balance sheets report Erin’s Fitness Gear, Inc.'s financial position as of the end of each year presented

below.

2008 2009 2010 2011 2012

13

ASSETS

Total Current Assets 4,956,423 5,427,189 6,388,104 7,147,785 7,509,604

Net Fixed Assets 5,142,852 4,962,042 4,634,661 5,534,900 5,363,423

Total Long-Term Investments 3,904,180 3,583,210 3,672,670 2,204,390 1,651,210

Net Intangible Assets 245,670 236,340 227,010 217,680 208,350

Total Other Noncurrent Assets 550,000 710,000 770,000 780,000 790,000

Total Assets 14,799,125 14,918,781 15,692,445 15,884,755 15,522,587

LIABILITIES & STOCKHOLDERS' EQUITY

Total Current Liabilities 2,663,694 2,817,600 3,464,091 3,797,653 3,555,398

Total Long-Term Debt 5,990,265 5,734,045 5,317,415 4,896,531 4,257,082

Total Other Long-Term Liabilities 27,000 27,000 27,000 27,000 27,000

Total Liabilities 8,680,959 8,578,645 8,808,506 8,721,184 7,839,480

Stockholders' Equity:

Preferred Stock 800,000 800,000 850,000 850,000 850,000

Common Stock 2,780,000 2,780,000 3,000,000 3,000,000 3,000,000

Retained Earnings 2,538,166 2,760,136 3,033,939 3,313,571 3,833,107

Total Stockholders' Equity 6,118,166 6,340,136 6,883,939 7,163,571 7,683,107

Total Liabilities & Stockholders' Equity 14,799,125 14,918,781 15,692,445 15,884,755 15,522,587

Balance Sheet Adjustments

In order to estimate the value of Erin’s Fitness Gear, Inc., it was necessary to make certain normalization

adjustments to the Balance Sheets. Normalization adjustments are made to reflect the Company's true economic

position by eliminating or reclassifying items that are excessive or not related to the operations of the business.

The following table presents a summary of the adjustments that were made to Erin’s Fitness Gear, Inc.'s balance

sheets.

2008 2009 2010 2011 2012

Nonoperating Assets 60,000 70,000 80,000 90,000 100,000

Normalization Adjustment (60,000) (70,000) (80,000) (90,000) (100,000)

Adjusted Balance 0 0 0 0 0

Nonoperating Liabilities 27,000 27,000 27,000 27,000 27,000

Normalization Adjustment (27,000) (27,000) (27,000) (27,000) (27,000)

Adjusted Balance 0 0 0 0 0

14

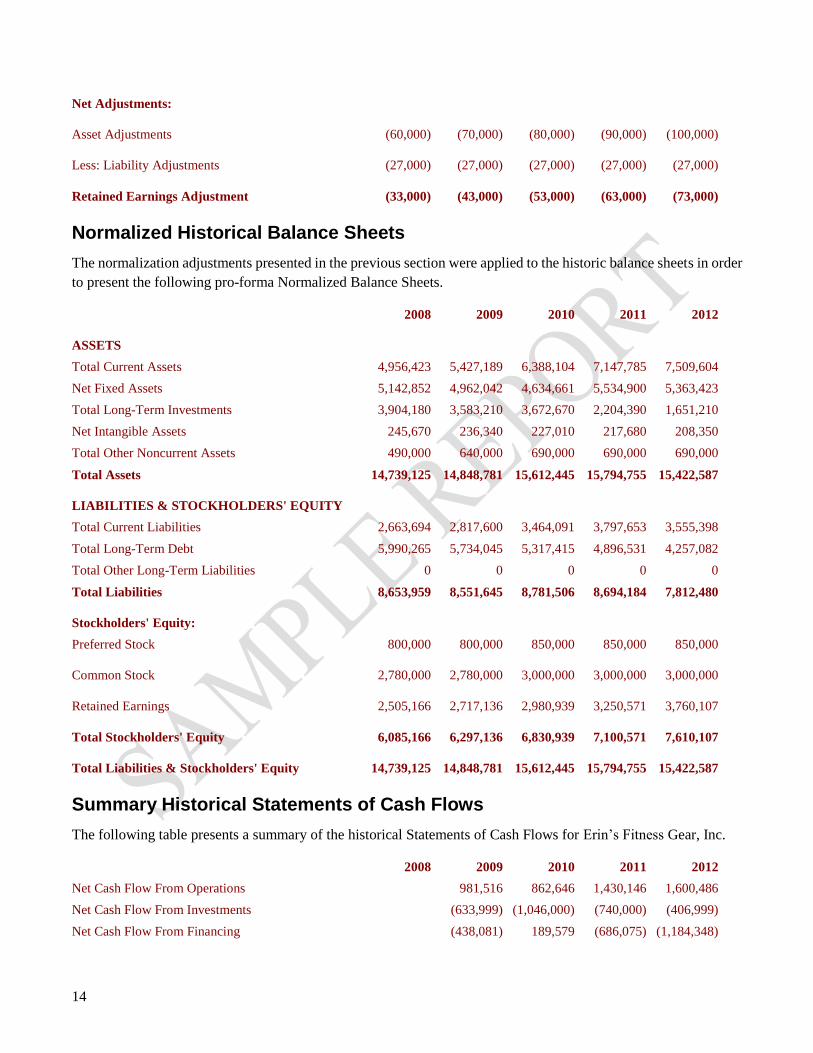

Net Adjustments:

Asset Adjustments (60,000) (70,000) (80,000) (90,000) (100,000)

Less: Liability Adjustments (27,000) (27,000) (27,000) (27,000) (27,000)

Retained Earnings Adjustment (33,000) (43,000) (53,000) (63,000) (73,000)

Normalized Historical Balance Sheets

The normalization adjustments presented in the previous section were applied to the historic balance sheets in order

to present the following pro-forma Normalized Balance Sheets.

2008 2009 2010 2011 2012

ASSETS

Total Current Assets 4,956,423 5,427,189 6,388,104 7,147,785 7,509,604

Net Fixed Assets 5,142,852 4,962,042 4,634,661 5,534,900 5,363,423

Total Long-Term Investments 3,904,180 3,583,210 3,672,670 2,204,390 1,651,210

Net Intangible Assets 245,670 236,340 227,010 217,680 208,350

Total Other Noncurrent Assets 490,000 640,000 690,000 690,000 690,000

Total Assets 14,739,125 14,848,781 15,612,445 15,794,755 15,422,587

LIABILITIES & STOCKHOLDERS' EQUITY

Total Current Liabilities 2,663,694 2,817,600 3,464,091 3,797,653 3,555,398

Total Long-Term Debt 5,990,265 5,734,045 5,317,415 4,896,531 4,257,082

Total Other Long-Term Liabilities 0 0 0 0 0

Total Liabilities 8,653,959 8,551,645 8,781,506 8,694,184 7,812,480

Stockholders' Equity:

Preferred Stock 800,000 800,000 850,000 850,000 850,000

Common Stock 2,780,000 2,780,000 3,000,000 3,000,000 3,000,000

Retained Earnings 2,505,166 2,717,136 2,980,939 3,250,571 3,760,107

Total Stockholders' Equity 6,085,166 6,297,136 6,830,939 7,100,571 7,610,107

Total Liabilities & Stockholders' Equity 14,739,125 14,848,781 15,612,445 15,794,755 15,422,587

Summary Historical Statements of Cash Flows

The following table presents a summary of the historical Statements of Cash Flows for Erin’s Fitness Gear, Inc.

2008 2009 2010 2011 2012

Net Cash Flow From Operations 981,516 862,646 1,430,146 1,600,486

Net Cash Flow From Investments (633,999) (1,046,000) (740,000) (406,999)

Net Cash Flow From Financing (438,081) 189,579 (686,075) (1,184,348)

15

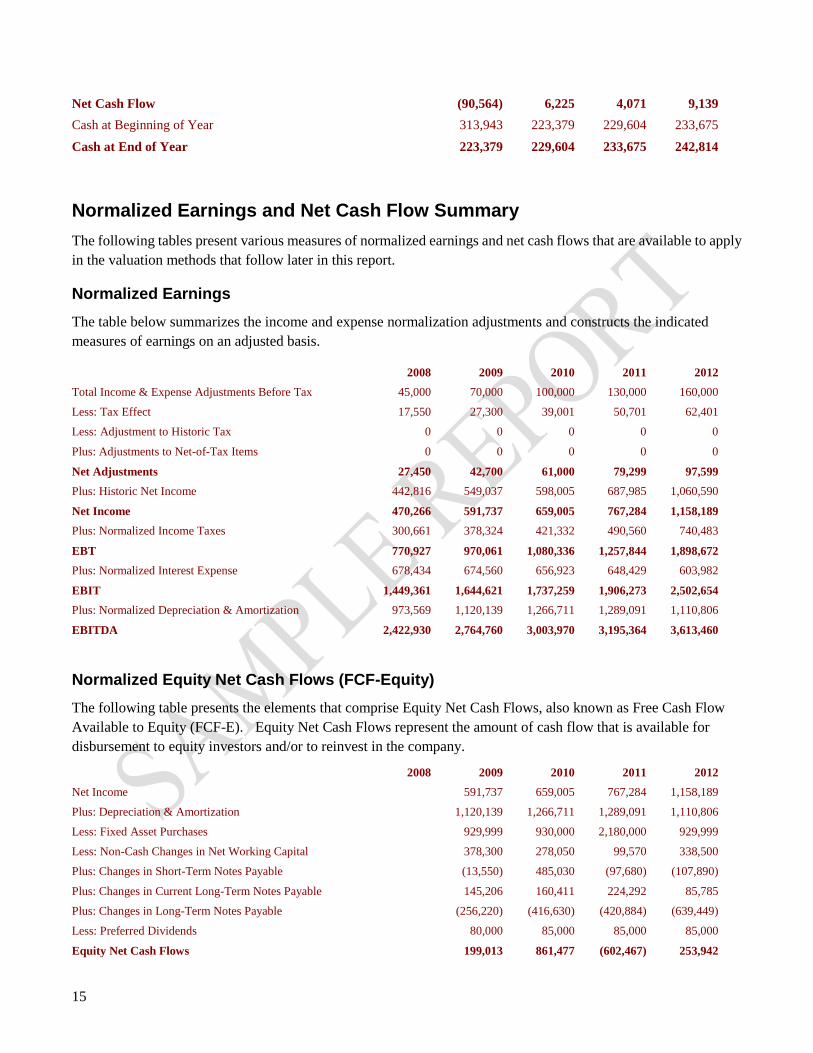

Net Cash Flow (90,564) 6,225 4,071 9,139

Cash at Beginning of Year 313,943 223,379 229,604 233,675

Cash at End of Year 223,379 229,604 233,675 242,814

Normalized Earnings and Net Cash Flow Summary

The following tables present various measures of normalized earnings and net cash flows that are available to apply

in the valuation methods that follow later in this report.

Normalized Earnings

The table below summarizes the income and expense normalization adjustments and constructs the indicated

measures of earnings on an adjusted basis.

2008 2009 2010 2011 2012

Total Income & Expense Adjustments Before Tax 45,000 70,000 100,000 130,000 160,000

Less: Tax Effect 17,550 27,300 39,001 50,701 62,401

Less: Adjustment to Historic Tax 0 0 0 0 0

Plus: Adjustments to Net-of-Tax Items 0 0 0 0 0

Net Adjustments 27,450 42,700 61,000 79,299 97,599

Plus: Historic Net Income 442,816 549,037 598,005 687,985 1,060,590

Net Income 470,266 591,737 659,005 767,284 1,158,189

Plus: Normalized Income Taxes 300,661 378,324 421,332 490,560 740,483

EBT 770,927 970,061 1,080,336 1,257,844 1,898,672

Plus: Normalized Interest Expense 678,434 674,560 656,923 648,429 603,982

EBIT 1,449,361 1,644,621 1,737,259 1,906,273 2,502,654

Plus: Normalized Depreciation & Amortization 973,569 1,120,139 1,266,711 1,289,091 1,110,806

EBITDA 2,422,930 2,764,760 3,003,970 3,195,364 3,613,460

Normalized Equity Net Cash Flows (FCF-Equity)

The following table presents the elements that comprise Equity Net Cash Flows, also known as Free Cash Flow

Available to Equity (FCF-E). Equity Net Cash Flows represent the amount of cash flow that is available for

disbursement to equity investors and/or to reinvest in the company.

2008 2009 2010 2011 2012

Net Income 591,737 659,005 767,284 1,158,189

Plus: Depreciation & Amortization 1,120,139 1,266,711 1,289,091 1,110,806

Less: Fixed Asset Purchases 929,999 930,000 2,180,000 929,999

Less: Non-Cash Changes in Net Working Capital 378,300 278,050 99,570 338,500

Plus: Changes in Short-Term Notes Payable (13,550) 485,030 (97,680) (107,890)

Plus: Changes in Current Long-Term Notes Payable 145,206 160,411 224,292 85,785

Plus: Changes in Long-Term Notes Payable (256,220) (416,630) (420,884) (639,449)

Less: Preferred Dividends 80,000 85,000 85,000 85,000

Equity Net Cash Flows 199,013 861,477 (602,467) 253,942

16

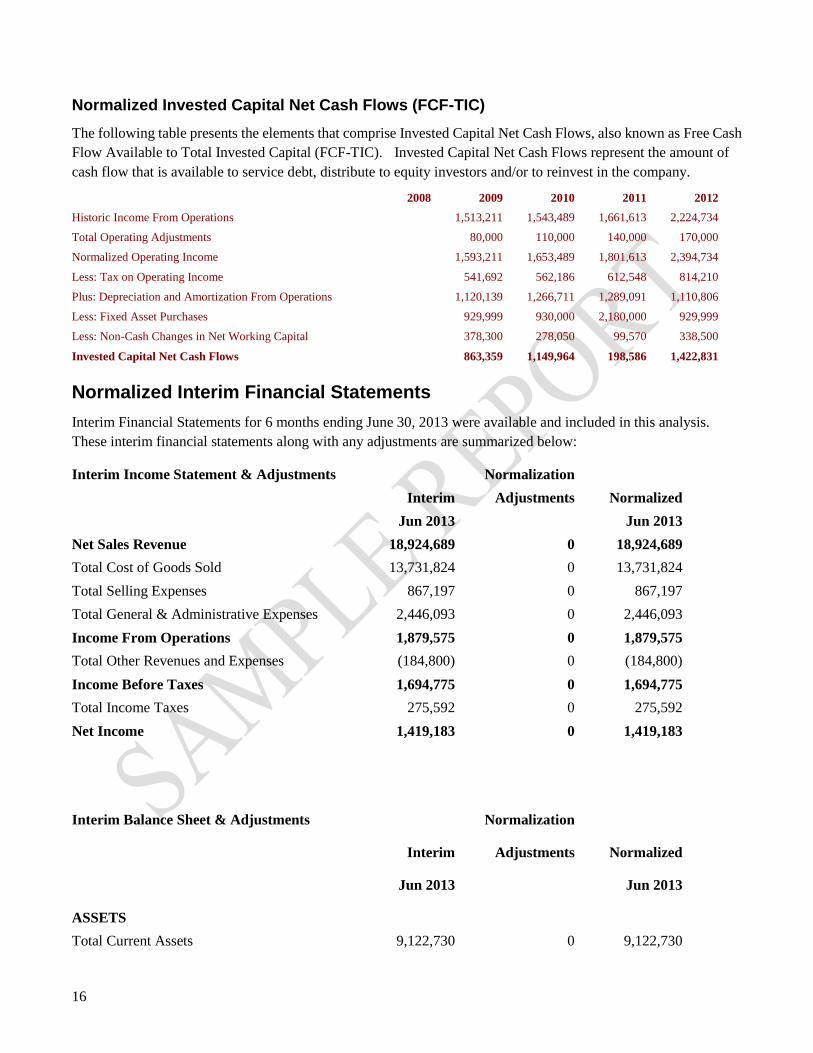

Normalized Invested Capital Net Cash Flows (FCF-TIC)

The following table presents the elements that comprise Invested Capital Net Cash Flows, also known as Free Cash

Flow Available to Total Invested Capital (FCF-TIC). Invested Capital Net Cash Flows represent the amount of

cash flow that is available to service debt, distribute to equity investors and/or to reinvest in the company.

2008 2009 2010 2011 2012

Historic Income From Operations 1,513,211 1,543,489 1,661,613 2,224,734

Total Operating Adjustments 80,000 110,000 140,000 170,000

Normalized Operating Income 1,593,211 1,653,489 1,801,613 2,394,734

Less: Tax on Operating Income 541,692 562,186 612,548 814,210

Plus: Depreciation and Amortization From Operations 1,120,139 1,266,711 1,289,091 1,110,806

Less: Fixed Asset Purchases 929,999 930,000 2,180,000 929,999

Less: Non-Cash Changes in Net Working Capital 378,300 278,050 99,570 338,500

Invested Capital Net Cash Flows 863,359 1,149,964 198,586 1,422,831

Normalized Interim Financial Statements

Interim Financial Statements for 6 months ending June 30, 2013 were available and included in this analysis.

These interim financial statements along with any adjustments are summarized below:

Interim Income Statement & Adjustments Normalization

Interim Adjustments Normalized

Jun 2013 Jun 2013

Net Sales Revenue 18,924,689 0 18,924,689

Total Cost of Goods Sold 13,731,824 0 13,731,824

Total Selling Expenses 867,197 0 867,197

Total General & Administrative Expenses 2,446,093 0 2,446,093

Income From Operations 1,879,575 0 1,879,575

Total Other Revenues and Expenses (184,800) 0 (184,800)

Income Before Taxes 1,694,775 0 1,694,775

Total Income Taxes 275,592 0 275,592

Net Income 1,419,183 0 1,419,183

Interim Balance Sheet & Adjustments Normalization

Interim Adjustments Normalized

Jun 2013 Jun 2013

ASSETS

Total Current Assets 9,122,730 0 9,122,730

17

Net Fixed Assets 4,554,828 0 4,554,828

Total Long-Term Investments 1,640,341 0 1,640,341

Net Intangible Assets 203,666 0 203,666

Total Other Noncurrent Assets 790,000 0 790,000

Total Assets 16,311,565 0 16,311,565

LIABILITIES & STOCKHOLDERS' EQUITY

Total Current Liabilities 3,303,998 0 3,303,998

Total Long-Term Debt 3,855,277 0 3,855,277

Total Other Long-Term Liabilities 50,000 0 50,000

Total Liabilities 7,209,275 0 7,209,275

Stockholders' Equity:

Preferred Stock 850,000 0 850,000

Common Stock 3,000,000 0 3,000,000

Retained Earnings 5,252,290 0 5,252,290

Total Stockholders' Equity 9,102,290 0 9,102,290

Total Liabilities & Stockholders' Equity 16,311,565 0 16,311,565

18

Analysis of Historic Financial Statements

We have performed an analysis of the Company's historic financial statements by calculating common-size

financial statements on a percentage basis and traditional financial ratios. The common-size income statement

items are presented as percentages of Total Sales and the balance sheet items a percentages of Total Assets in order

to compare the relative composition of line items from year to year. The calculated financial ratios measure areas

such as liquidity, leverage, profitability, etc. for each historic year.

In addition, the Company's common-size financial statements and financial ratios have been compared to aggregate

industry data in order to provide a benchmark against other peer companies in the selected industry.

The industry data used in this analysis is described below.

Although industry statistics are a useful source of general analytical data, there can be significant variation in the

reporting practices and operational methods of companies within a given industry. Therefore, industry statistics as

used throughout this report should not be regarded as absolute norms or standards.

Comparative Industry Data:

Source: RMA Annual Statement Studies

Industry Description: Sporting and Athletic Goods Manufacturing

Industry NAICS code: 339920

Sample categorized by: Sales

Category size: $10MM to $25MM

Industry Quartile (for ratios): Median Quartile

Number of companies in sample: 47

Date of industry information: 2012

Source: Integra - Financial Statement Analysis

Industry Description: Sporting and Athletic Goods Manufacturing

Industry NAICS code: 339920

Sales Range: $10,000,000 - $24,999,999

Number of companies in sample: 94

Detailed industry description: This industry comprises establishments primarily engaged in

manufacturing sporting and athletic goods (except apparel and footwear).

19

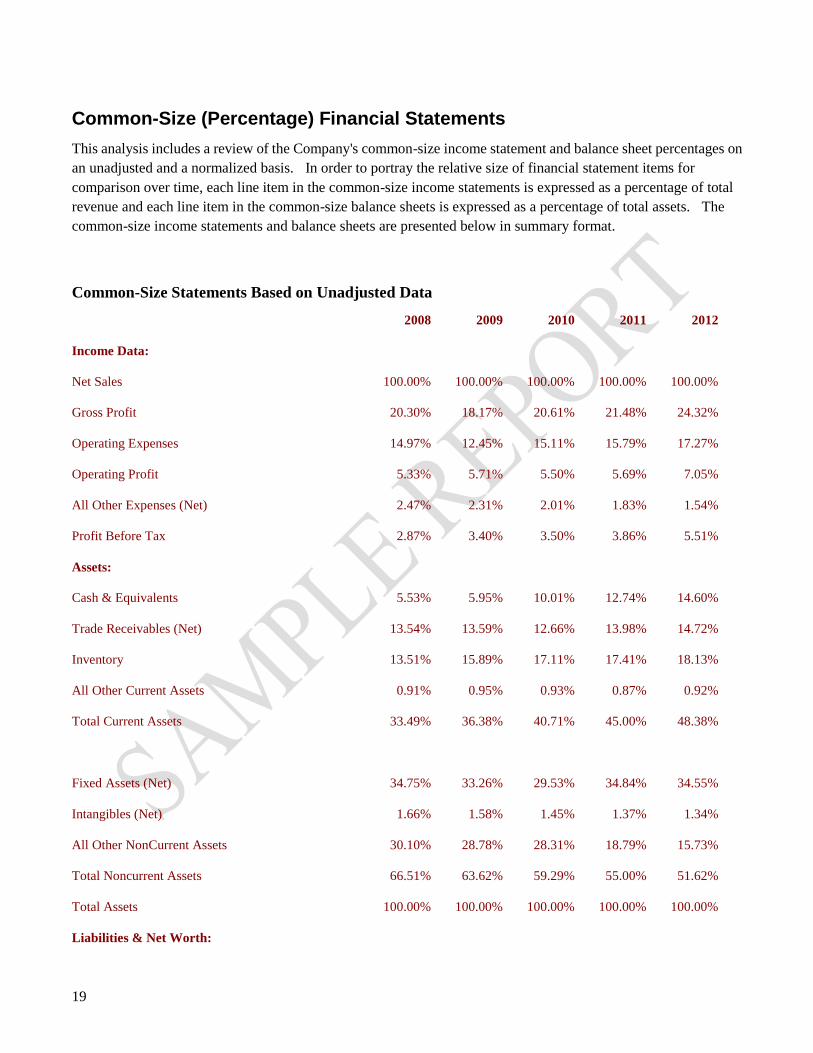

Common-Size (Percentage) Financial Statements

This analysis includes a review of the Company's common-size income statement and balance sheet percentages on

an unadjusted and a normalized basis. In order to portray the relative size of financial statement items for

comparison over time, each line item in the common-size income statements is expressed as a percentage of total

revenue and each line item in the common-size balance sheets is expressed as a percentage of total assets. The

common-size income statements and balance sheets are presented below in summary format.

Common-Size Statements Based on Unadjusted Data

2008 2009 2010 2011 2012

Income Data:

Net Sales 100.00% 100.00% 100.00% 100.00% 100.00%

Gross Profit 20.30% 18.17% 20.61% 21.48% 24.32%

Operating Expenses 14.97% 12.45% 15.11% 15.79% 17.27%

Operating Profit 5.33% 5.71% 5.50% 5.69% 7.05%

All Other Expenses (Net) 2.47% 2.31% 2.01% 1.83% 1.54%

Profit Before Tax 2.87% 3.40% 3.50% 3.86% 5.51%

Assets:

Cash & Equivalents 5.53% 5.95% 10.01% 12.74% 14.60%

Trade Receivables (Net) 13.54% 13.59% 12.66% 13.98% 14.72%

Inventory 13.51% 15.89% 17.11% 17.41% 18.13%

All Other Current Assets 0.91% 0.95% 0.93% 0.87% 0.92%

Total Current Assets 33.49% 36.38% 40.71% 45.00% 48.38%

Fixed Assets (Net) 34.75% 33.26% 29.53% 34.84% 34.55%

Intangibles (Net) 1.66% 1.58% 1.45% 1.37% 1.34%

All Other NonCurrent Assets 30.10% 28.78% 28.31% 18.79% 15.73%

Total Noncurrent Assets 66.51% 63.62% 59.29% 55.00% 51.62%

Total Assets 100.00% 100.00% 100.00% 100.00% 100.00%

Liabilities & Net Worth:

20

Notes Payable Short-Term 1.27% 1.17% 4.20% 3.54% 2.92%

Current Maturity of Long-Term Debt 3.58% 4.53% 5.33% 6.67% 7.38%

Trade Payables 8.33% 8.32% 7.83% 8.37% 8.34%

Income Taxes Payable 2.19% 2.25% 2.13% 2.45% 1.73%

All Other Current Liabilities 2.62% 2.62% 2.59% 2.88% 2.53%

Total Current Liabilities 18.00% 18.89% 22.07% 23.91% 22.90%

Long-Term Debt 40.48% 38.44% 33.89% 30.83% 27.43%

Deferred Taxes 0.00% 0.00% 0.00% 0.00% 0.00%

All Other NonCurrent Liabilities 0.18% 0.18% 0.17% 0.17% 0.17%

Net worth 41.34% 42.50% 43.87% 45.10% 49.50%

Total Liabilities & Net Worth 100.00% 100.00% 100.00% 100.00% 100.00%

Common-Size Statements Based on Normalized Data

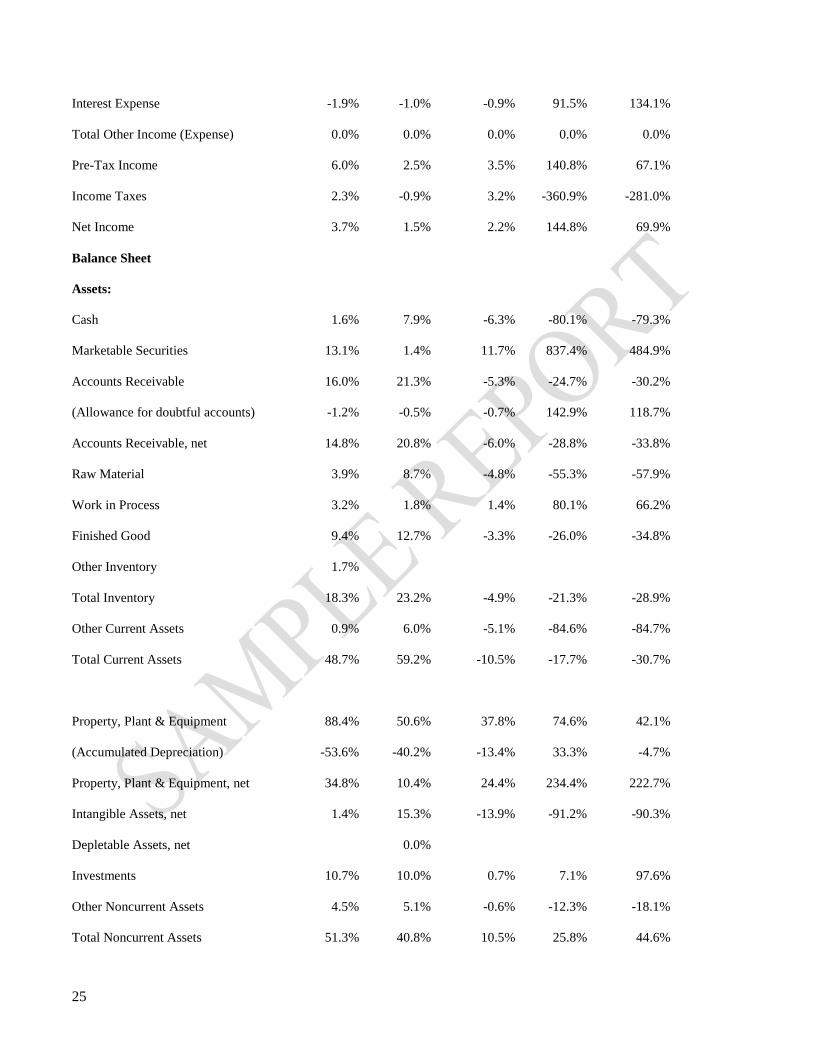

2008 2009 2010 2011 2012

Income Data:

Net Sales 100.00% 100.00% 100.00% 100.00% 100.00%

Gross Profit 20.30% 18.17% 20.61% 21.48% 24.32%

Operating Expenses 14.75% 12.15% 14.71% 15.31% 16.73%

Operating Profit 5.55% 6.01% 5.90% 6.17% 7.59%

All Other Expenses (Net) 2.50% 2.35% 2.04% 1.86% 1.57%

Profit Before Tax 3.05% 3.66% 3.85% 4.30% 6.02%

Assets:

Cash & Equivalents 5.55% 5.98% 10.06% 12.81% 14.70%

Trade Receivables (Net) 13.60% 13.65% 12.73% 14.06% 14.82%

Inventory 13.57% 15.96% 17.20% 17.51% 18.25%

All Other Current Assets 0.91% 0.95% 0.93% 0.88% 0.92%

Total Current Assets 33.63% 36.55% 40.92% 45.25% 48.69%

21

Fixed Assets (Net) 34.89% 33.42% 29.69% 35.04% 34.78%

Intangibles (Net) 1.67% 1.59% 1.45% 1.38% 1.35%

All Other NonCurrent Assets 29.81% 28.44% 27.94% 18.33% 15.18%

Total Noncurrent Assets 66.37% 63.45% 59.08% 54.75% 51.31%

Total Assets 100.00% 100.00% 100.00% 100.00% 100.00%

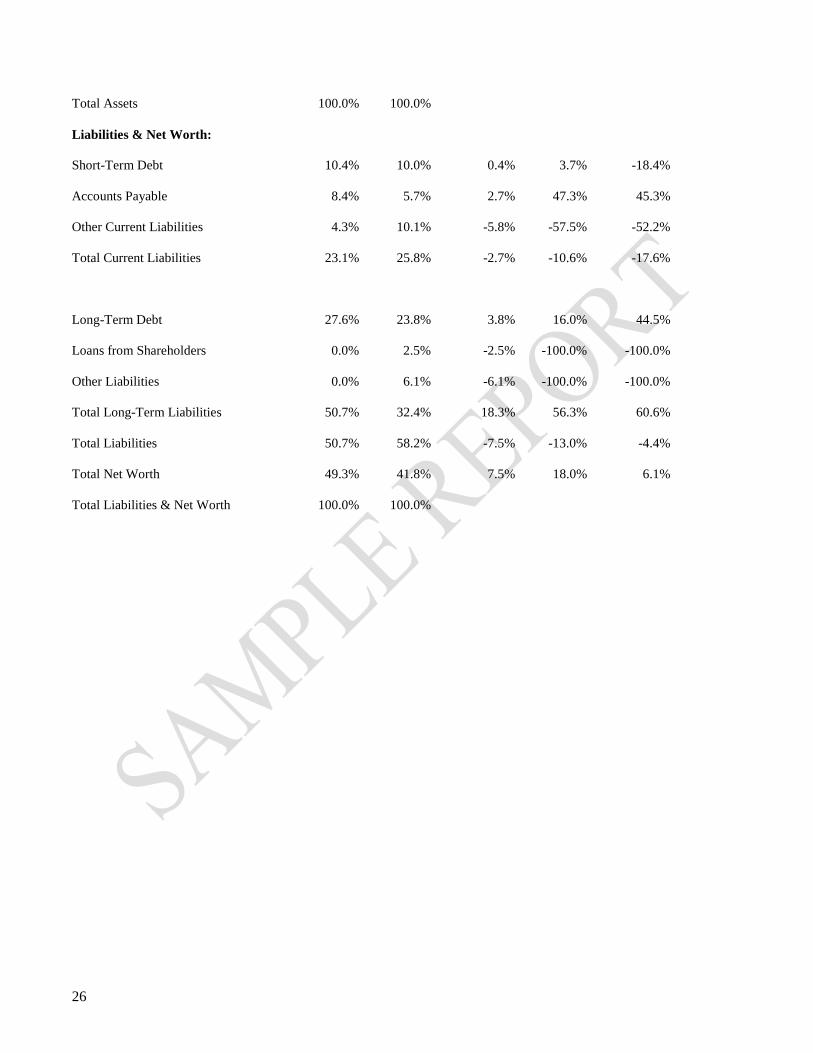

Liabilities & Net Worth:

Notes Payable Short-Term 1.27% 1.17% 4.22% 3.56% 2.94%

Current Maturity of Long-Term Debt 3.60% 4.55% 5.35% 6.71% 7.43%

Trade Payables 8.37% 8.36% 7.87% 8.42% 8.39%

Income Taxes Payable 2.20% 2.26% 2.14% 2.47% 1.74%

All Other Current Liabilities 2.63% 2.64% 2.60% 2.89% 2.55%

Total Current Liabilities 18.07% 18.98% 22.19% 24.04% 23.05%

Long-Term Debt 40.64% 38.62% 34.06% 31.00% 27.60%

Deferred Taxes 0.00% 0.00% 0.00% 0.00% 0.00%

All Other NonCurrent Liabilities 0.00% 0.00% 0.00% 0.00% 0.00%

Net worth 41.29% 42.41% 43.75% 44.96% 49.34%

Total Liabilities & Net Worth 100.00% 100.00% 100.00% 100.00% 100.00%

22

Integra Industry Data, Common-Size Statement Comparison

The Company's common-size financial statements are calculated from both the unadjusted and normalized financial

statements and compared here to the selected Integra industry data. For each line item, the business vs. industry

difference, variance and average variance are calculated and presented in the table below. A multi-year

comparison is available as an attachment to this report.

Integra Common-Size Comparison to Unadjusted Company Financials

Integra - Business vs. Industry

Common-Size Statements, Current Year 5 Yr Average

Business Industry Difference Variance Variance

2012 2011

Income Statement

Revenue 100.0% 100.0% 0.0% 0.0% 0.0%

Cost of Sales 73.1% 66.3% 6.8% 10.2% 14.6%

Gross Margin 26.9% 33.7% -6.8% -20.1% -37.8%

Selling, General & Administrative 12.0% 18.6% -6.6% -35.5% -49.3%

Officer Compensation 1.7% 2.1% -0.4% -17.0% -24.3%

Pension & Benefits 0.0% 2.1% -2.1% -100.0% -100.0%

Advertising & Sales 0.0% 1.9% -1.9% -100.0% -100.0%

Bad Debts 0.0% 0.2% -0.2% -100.0% -100.0%

Rents Paid 0.0% 2.1% -2.1% -100.0% -100.0%

Depreciation & Amortization 3.5% 3.2% 0.3% 10.1% 28.3%

Operating expenses 17.3% 30.3% -13.0% -43.0% -50.1%

Operating Income 7.1% 3.5% 3.6% 101.5% 67.4%

Interest Income 0.3% 0.1% 0.2% 242.2% 173.9%

Interest Expense -1.9% -1.0% -0.9% 91.5% 134.1%

Total Other Income (Expense) 0.0% 0.0% 0.0% 0.0% 0.0%

Pre-Tax Income 5.5% 2.5% 3.0% 120.5% 53.1%

Income Taxes 2.1% -0.9% 3.0% -338.9% -265.8%

Net Income 3.4% 1.5% 1.9% 124.2% 55.6%

23

Balance Sheet

Assets:

Cash 1.6% 7.9% -6.3% -80.2% -79.5%

Marketable Securities 13.0% 1.4% 11.6% 831.4% 481.6%

Accounts Receivable 15.9% 21.3% -5.4% -25.2% -30.6%

(Allowance for doubtful accounts) -1.2% -0.5% -0.7% 141.3% 117.6%

Accounts Receivable, net 14.7% 20.8% -6.1% -29.2% -34.1%

Raw Material 3.9% 8.7% -4.8% -55.6% -58.1%

Work in Process 3.2% 1.8% 1.4% 79.0% 65.4%

Finished Good 9.3% 12.7% -3.4% -26.4% -35.1%

Other Inventory 1.7%

Total Inventory 18.1% 23.2% -5.1% -21.8% -29.3%

Other Current Assets 0.9% 6.0% -5.1% -84.7% -84.8%

Total Current Assets 48.4% 59.2% -10.8% -18.3% -31.1%

Property, Plant & Equipment 87.8% 50.6% 37.2% 73.5% 41.3%

(Accumulated Depreciation) -53.2% -40.2% -13.0% 32.4% -5.2%

Property, Plant & Equipment, net 34.6% 10.4% 24.2% 232.2% 221.0%

Intangible Assets, net 1.3% 15.3% -14.0% -91.2% -90.3%

Depletable Assets, net 0.0%

Investments 10.6% 10.0% 0.6% 6.4% 96.6%

Other Noncurrent Assets 5.1% 5.1% 0.0% -0.2% -8.3%

Total Noncurrent Assets 51.6% 40.8% 10.8% 26.5% 45.1%

Total Assets 100.0% 100.0%

Liabilities & Net Worth:

Short-Term Debt 10.3% 10.0% 0.3% 3.0% -18.8%

Accounts Payable 8.3% 5.7% 2.6% 46.3% 44.5%

Other Current Liabilities 4.3% 10.1% -5.8% -57.8% -52.5%

24

Total Current Liabilities 22.9% 25.8% -2.9% -11.2% -18.0%

Long-Term Debt 27.4% 23.8% 3.6% 15.2% 43.7%

Loans from Shareholders 0.0% 2.5% -2.5% -100.0% -100.0%

Other Liabilities 0.2% 6.1% -5.9% -97.1% -97.1%

Total Long-Term Liabilities 50.5% 32.4% 18.1% 55.9% 60.3%

Total Liabilities 50.5% 58.2% -7.7% -13.2% -4.6%

Total Net Worth 49.5% 41.8% 7.7% 18.4% 6.4%

Total Liabilities & Net Worth 100.0% 100.0%

Integra Common-Size Comparison to Normalized Company Financials

Integra - Business vs. Industry

Common-Size Statements, Current Year 5 Yr Average

Business Industry Difference Variance Variance

2012 2011

Income Statement

Revenue 100.0% 100.0% 0.0% 0.0% 0.0%

Cost of Sales 73.1% 66.3% 6.8% 10.2% 14.6%

Gross Margin 26.9% 33.7% -6.8% -20.1% -37.8%

Selling, General & Administrative 11.9% 18.6% -6.7% -35.8% -49.5%

Officer Compensation 1.3% 2.1% -0.8% -39.6% -40.8%

Pension & Benefits 0.0% 2.1% -2.1% -100.0% -100.0%

Advertising & Sales 0.0% 1.9% -1.9% -100.0% -100.0%

Bad Debts 0.0% 0.2% -0.2% -100.0% -100.0%

Rents Paid 0.0% 2.1% -2.1% -100.0% -100.0%

Depreciation & Amortization 3.5% 3.2% 0.3% 10.1% 28.3%

Operating expenses 16.7% 30.3% -13.6% -44.8% -51.4%

Operating Income 7.6% 3.5% 4.1% 116.9% 78.4%

Interest Income 0.3% 0.1% 0.2% 242.2% 173.9%

25

Interest Expense -1.9% -1.0% -0.9% 91.5% 134.1%

Total Other Income (Expense) 0.0% 0.0% 0.0% 0.0% 0.0%

Pre-Tax Income 6.0% 2.5% 3.5% 140.8% 67.1%

Income Taxes 2.3% -0.9% 3.2% -360.9% -281.0%

Net Income 3.7% 1.5% 2.2% 144.8% 69.9%

Balance Sheet

Assets:

Cash 1.6% 7.9% -6.3% -80.1% -79.3%

Marketable Securities 13.1% 1.4% 11.7% 837.4% 484.9%

Accounts Receivable 16.0% 21.3% -5.3% -24.7% -30.2%

(Allowance for doubtful accounts) -1.2% -0.5% -0.7% 142.9% 118.7%

Accounts Receivable, net 14.8% 20.8% -6.0% -28.8% -33.8%

Raw Material 3.9% 8.7% -4.8% -55.3% -57.9%

Work in Process 3.2% 1.8% 1.4% 80.1% 66.2%

Finished Good 9.4% 12.7% -3.3% -26.0% -34.8%

Other Inventory 1.7%

Total Inventory 18.3% 23.2% -4.9% -21.3% -28.9%

Other Current Assets 0.9% 6.0% -5.1% -84.6% -84.7%

Total Current Assets 48.7% 59.2% -10.5% -17.7% -30.7%

Property, Plant & Equipment 88.4% 50.6% 37.8% 74.6% 42.1%

(Accumulated Depreciation) -53.6% -40.2% -13.4% 33.3% -4.7%

Property, Plant & Equipment, net 34.8% 10.4% 24.4% 234.4% 222.7%

Intangible Assets, net 1.4% 15.3% -13.9% -91.2% -90.3%

Depletable Assets, net 0.0%

Investments 10.7% 10.0% 0.7% 7.1% 97.6%

Other Noncurrent Assets 4.5% 5.1% -0.6% -12.3% -18.1%

Total Noncurrent Assets 51.3% 40.8% 10.5% 25.8% 44.6%

26

Total Assets 100.0% 100.0%

Liabilities & Net Worth:

Short-Term Debt 10.4% 10.0% 0.4% 3.7% -18.4%

Accounts Payable 8.4% 5.7% 2.7% 47.3% 45.3%

Other Current Liabilities 4.3% 10.1% -5.8% -57.5% -52.2%

Total Current Liabilities 23.1% 25.8% -2.7% -10.6% -17.6%

Long-Term Debt 27.6% 23.8% 3.8% 16.0% 44.5%

Loans from Shareholders 0.0% 2.5% -2.5% -100.0% -100.0%

Other Liabilities 0.0% 6.1% -6.1% -100.0% -100.0%

Total Long-Term Liabilities 50.7% 32.4% 18.3% 56.3% 60.6%

Total Liabilities 50.7% 58.2% -7.5% -13.0% -4.4%

Total Net Worth 49.3% 41.8% 7.5% 18.0% 6.1%

Total Liabilities & Net Worth 100.0% 100.0%

27

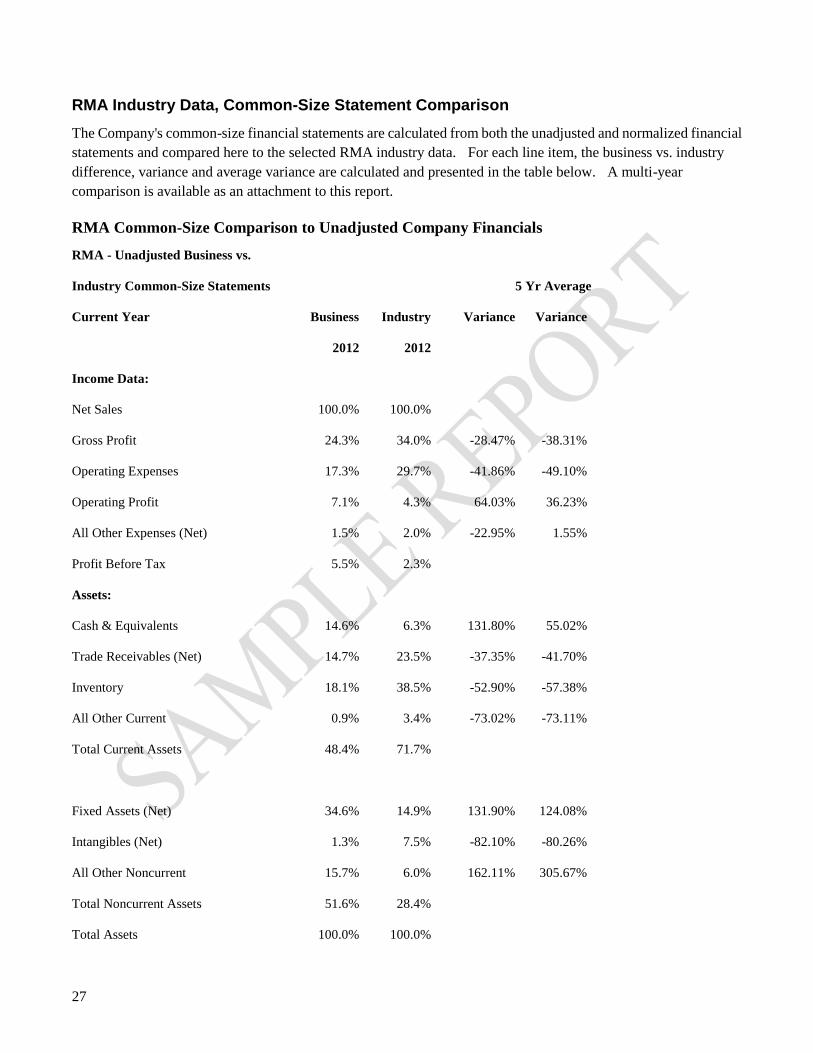

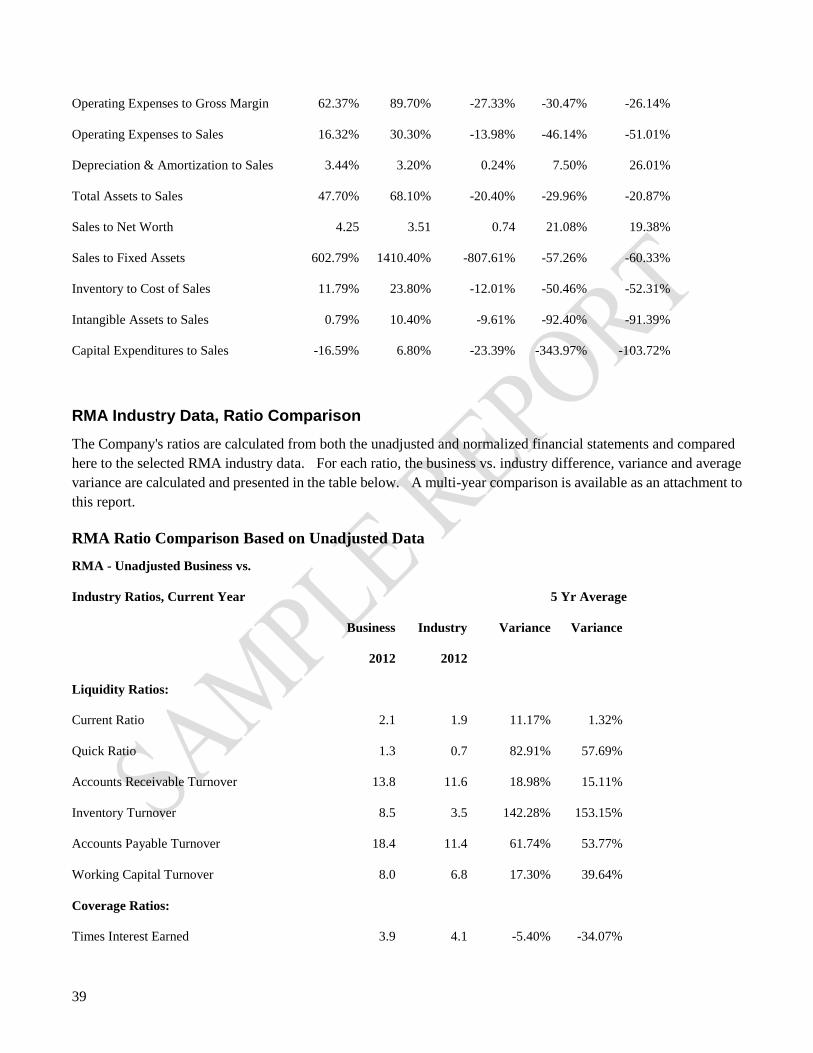

RMA Industry Data, Common-Size Statement Comparison

The Company's common-size financial statements are calculated from both the unadjusted and normalized financial

statements and compared here to the selected RMA industry data. For each line item, the business vs. industry

difference, variance and average variance are calculated and presented in the table below. A multi-year

comparison is available as an attachment to this report.

RMA Common-Size Comparison to Unadjusted Company Financials

RMA - Unadjusted Business vs.

Industry Common-Size Statements 5 Yr Average

Current Year Business Industry Variance Variance

2012 2012

Income Data:

Net Sales 100.0% 100.0%

Gross Profit 24.3% 34.0% -28.47% -38.31%

Operating Expenses 17.3% 29.7% -41.86% -49.10%

Operating Profit 7.1% 4.3% 64.03% 36.23%

All Other Expenses (Net) 1.5% 2.0% -22.95% 1.55%

Profit Before Tax 5.5% 2.3%

Assets:

Cash & Equivalents 14.6% 6.3% 131.80% 55.02%

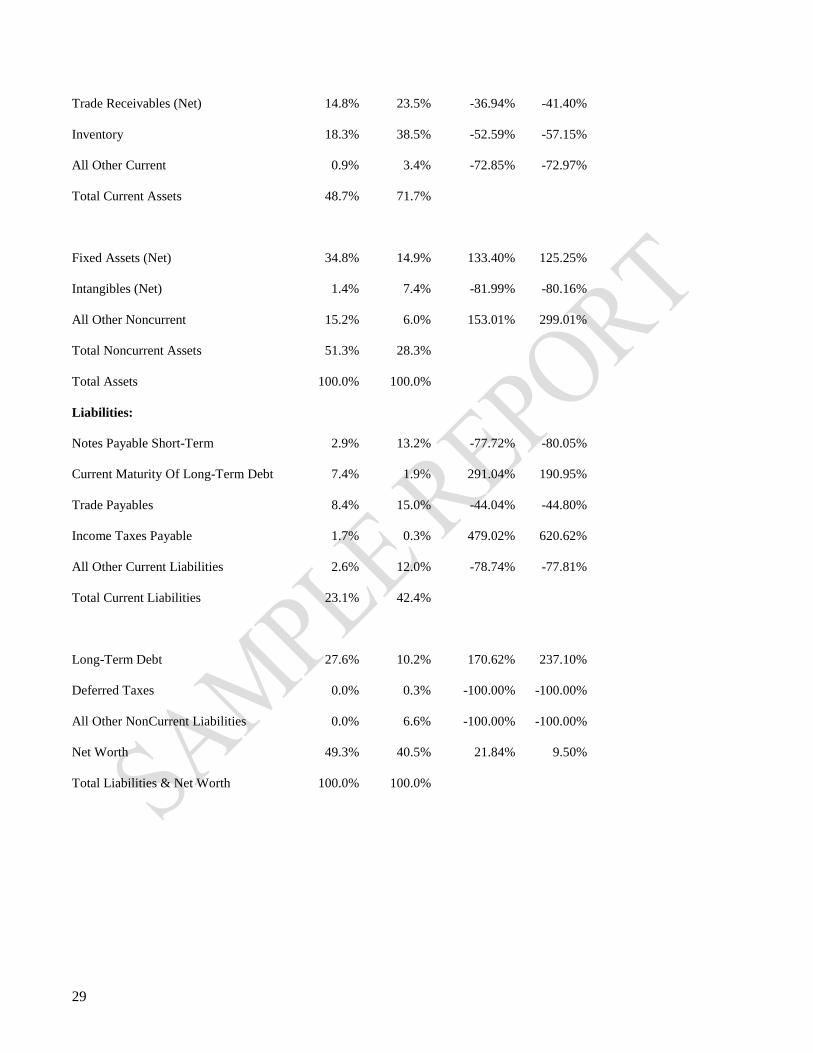

Trade Receivables (Net) 14.7% 23.5% -37.35% -41.70%

Inventory 18.1% 38.5% -52.90% -57.38%

All Other Current 0.9% 3.4% -73.02% -73.11%

Total Current Assets 48.4% 71.7%

Fixed Assets (Net) 34.6% 14.9% 131.90% 124.08%

Intangibles (Net) 1.3% 7.5% -82.10% -80.26%

All Other Noncurrent 15.7% 6.0% 162.11% 305.67%

Total Noncurrent Assets 51.6% 28.4%

Total Assets 100.0% 100.0%

28

Liabilities:

Notes Payable Short-Term 2.9% 13.2% -77.86% -80.16%

Current Maturity Of Long-Term Debt 7.4% 1.9% 288.52% 189.38%

Trade Payables 8.3% 15.0% -44.40% -45.08%

Income Taxes Payable 1.7% 0.3% 475.29% 616.91%

All Other Current Liabilities 2.5% 12.0% -78.88% -77.92%

Total Current Liabilities 22.9% 42.4%

Long-Term Debt 27.4% 10.1% 168.87% 235.39%

Deferred Taxes 0.0% 0.4% -100.00% -100.00%

All Other NonCurrent Liabilities 0.2% 6.6% -97.36% -97.34%

Net Worth 49.5% 40.5% 22.21% 9.78%

Total Liabilities & Net Worth 100.0% 100.0%

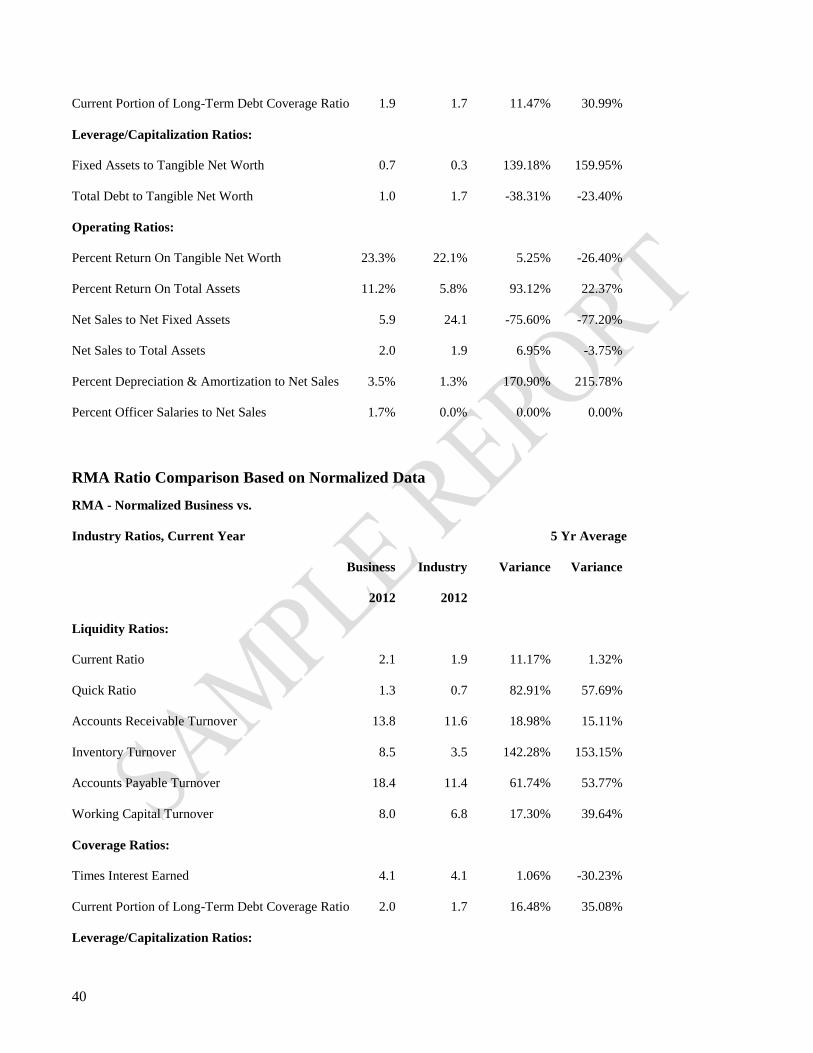

RMA Common-Size Comparison to Normalized Company Financials

RMA - Normalized Business vs.

Industry Common-Size Statements 5 Yr Average

Current Year Business Industry Variance Variance

2012 2012

Income Data:

Net Sales 100.0% 100.0%

Gross Profit 24.3% 34.0% -28.47% -38.31%

Operating Expenses 16.7% 29.7% -43.68% -50.40%

Operating Profit 7.6% 4.3% 76.57% 45.21%

All Other Expenses (Net) 1.6% 2.0% -21.36% 3.34%

Profit Before Tax 6.0% 2.3%

Assets:

Cash & Equivalents 14.7% 6.3% 133.30% 55.87%

29

Trade Receivables (Net) 14.8% 23.5% -36.94% -41.40%

Inventory 18.3% 38.5% -52.59% -57.15%

All Other Current 0.9% 3.4% -72.85% -72.97%

Total Current Assets 48.7% 71.7%

Fixed Assets (Net) 34.8% 14.9% 133.40% 125.25%

Intangibles (Net) 1.4% 7.4% -81.99% -80.16%

All Other Noncurrent 15.2% 6.0% 153.01% 299.01%

Total Noncurrent Assets 51.3% 28.3%

Total Assets 100.0% 100.0%

Liabilities:

Notes Payable Short-Term 2.9% 13.2% -77.72% -80.05%

Current Maturity Of Long-Term Debt 7.4% 1.9% 291.04% 190.95%

Trade Payables 8.4% 15.0% -44.04% -44.80%

Income Taxes Payable 1.7% 0.3% 479.02% 620.62%

All Other Current Liabilities 2.6% 12.0% -78.74% -77.81%

Total Current Liabilities 23.1% 42.4%

Long-Term Debt 27.6% 10.2% 170.62% 237.10%

Deferred Taxes 0.0% 0.3% -100.00% -100.00%

All Other NonCurrent Liabilities 0.0% 6.6% -100.00% -100.00%

Net Worth 49.3% 40.5% 21.84% 9.50%

Total Liabilities & Net Worth 100.0% 100.0%

30

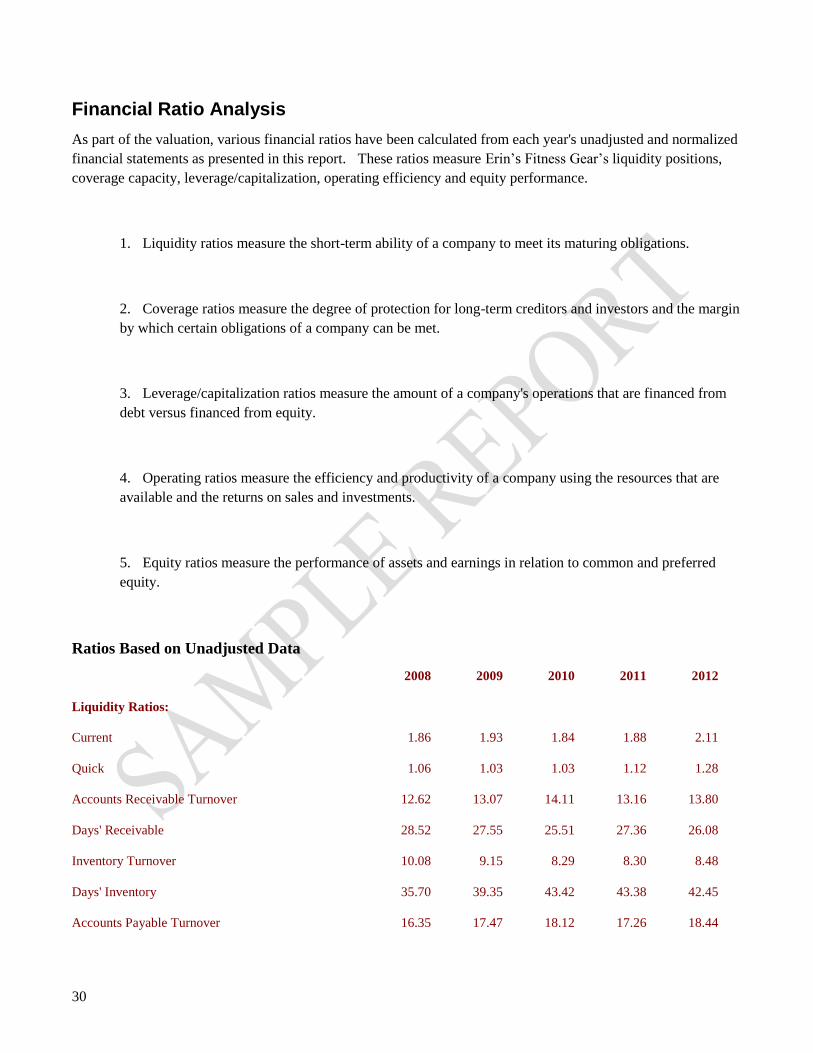

Financial Ratio Analysis

As part of the valuation, various financial ratios have been calculated from each year's unadjusted and normalized

financial statements as presented in this report. These ratios measure Erin’s Fitness Gear’s liquidity positions,

coverage capacity, leverage/capitalization, operating efficiency and equity performance.

1. Liquidity ratios measure the short-term ability of a company to meet its maturing obligations.

2. Coverage ratios measure the degree of protection for long-term creditors and investors and the margin

by which certain obligations of a company can be met.

3. Leverage/capitalization ratios measure the amount of a company's operations that are financed from

debt versus financed from equity.

4. Operating ratios measure the efficiency and productivity of a company using the resources that are

available and the returns on sales and investments.

5. Equity ratios measure the performance of assets and earnings in relation to common and preferred

equity.

Ratios Based on Unadjusted Data

2008 2009 2010 2011 2012

Liquidity Ratios:

Current 1.86 1.93 1.84 1.88 2.11

Quick 1.06 1.03 1.03 1.12 1.28

Accounts Receivable Turnover 12.62 13.07 14.11 13.16 13.80

Days' Receivable 28.52 27.55 25.51 27.36 26.08

Inventory Turnover 10.08 9.15 8.29 8.30 8.48

Days' Inventory 35.70 39.35 43.42 43.38 42.45

Accounts Payable Turnover 16.35 17.47 18.12 17.26 18.44

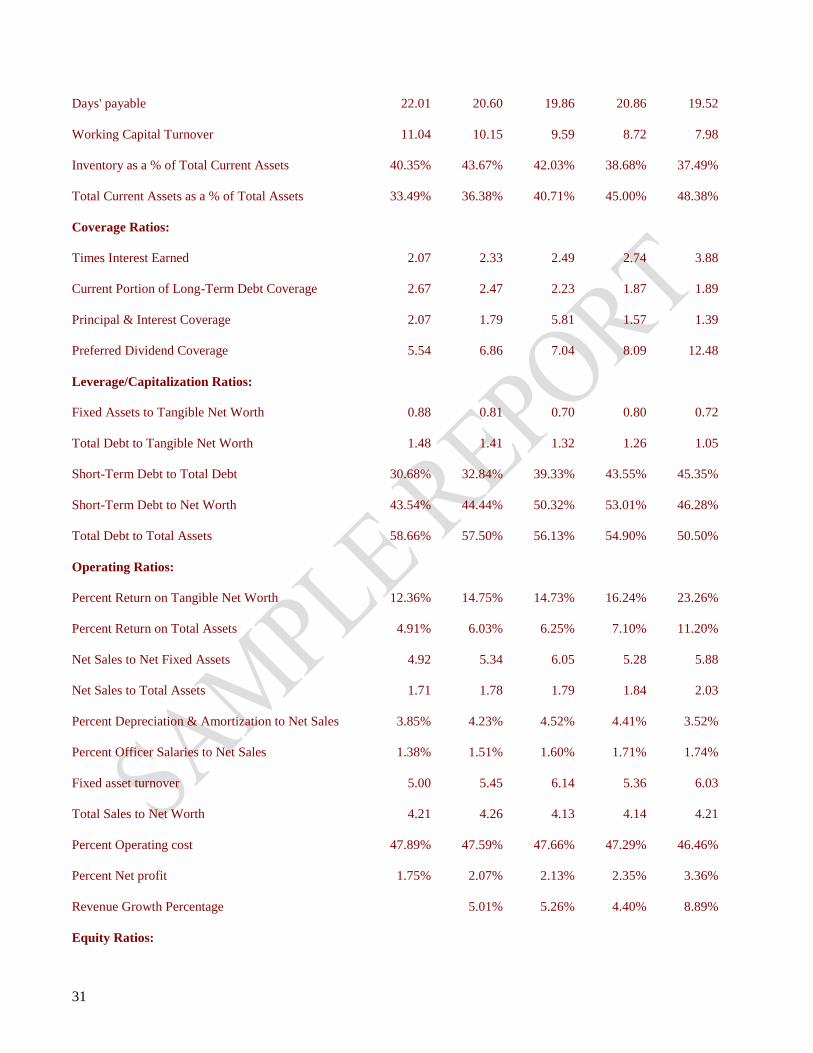

31

Days' payable 22.01 20.60 19.86 20.86 19.52

Working Capital Turnover 11.04 10.15 9.59 8.72 7.98

Inventory as a % of Total Current Assets 40.35% 43.67% 42.03% 38.68% 37.49%

Total Current Assets as a % of Total Assets 33.49% 36.38% 40.71% 45.00% 48.38%

Coverage Ratios:

Times Interest Earned 2.07 2.33 2.49 2.74 3.88

Current Portion of Long-Term Debt Coverage 2.67 2.47 2.23 1.87 1.89

Principal & Interest Coverage 2.07 1.79 5.81 1.57 1.39

Preferred Dividend Coverage 5.54 6.86 7.04 8.09 12.48

Leverage/Capitalization Ratios:

Fixed Assets to Tangible Net Worth 0.88 0.81 0.70 0.80 0.72

Total Debt to Tangible Net Worth 1.48 1.41 1.32 1.26 1.05

Short-Term Debt to Total Debt 30.68% 32.84% 39.33% 43.55% 45.35%

Short-Term Debt to Net Worth 43.54% 44.44% 50.32% 53.01% 46.28%

Total Debt to Total Assets 58.66% 57.50% 56.13% 54.90% 50.50%

Operating Ratios:

Percent Return on Tangible Net Worth 12.36% 14.75% 14.73% 16.24% 23.26%

Percent Return on Total Assets 4.91% 6.03% 6.25% 7.10% 11.20%

Net Sales to Net Fixed Assets 4.92 5.34 6.05 5.28 5.88

Net Sales to Total Assets 1.71 1.78 1.79 1.84 2.03

Percent Depreciation & Amortization to Net Sales 3.85% 4.23% 4.52% 4.41% 3.52%

Percent Officer Salaries to Net Sales 1.38% 1.51% 1.60% 1.71% 1.74%

Fixed asset turnover 5.00 5.45 6.14 5.36 6.03

Total Sales to Net Worth 4.21 4.26 4.13 4.14 4.21

Percent Operating cost 47.89% 47.59% 47.66% 47.29% 46.46%

Percent Net profit 1.75% 2.07% 2.13% 2.35% 3.36%

Revenue Growth Percentage 5.01% 5.26% 4.40% 8.89%

Equity Ratios:

32

Net Book Value Per Share of Preferred Stock 5.87 6.10 6.66 6.95 7.47

Net Book Value Per Share of Common Stock 0.63 0.66 0.73 0.76 0.83

Percent Earnings Payout 62.69% 52.68% 46.63% 53.63% 46.75%

Percent Earnings Retention 37.31% 47.32% 53.37% 46.37% 53.25%

Dividends Per Common Share 0.03 0.03 0.03 0.04 0.06

Simple Earnings Per Share 0.05 0.06 0.06 0.08 0.12

Ratios Based on Normalized Data

2008 2009 2010 2011 2012

Liquidity Ratios:

Current 1.86 1.93 1.84 1.88 2.11

Quick 1.06 1.03 1.03 1.12 1.28

Accounts Receivable Turnover 12.62 13.07 14.11 13.16 13.80

Days' Receivable 28.52 27.55 25.51 27.36 26.08

Inventory Turnover 10.08 9.15 8.29 8.30 8.48

Days' Inventory 35.70 39.35 43.42 43.38 42.45

Accounts Payable Turnover 16.35 17.47 18.12 17.26 18.44

Days' Payable 22.01 20.60 19.86 20.86 19.52

Working Capital Turnover 11.04 10.15 9.59 8.72 7.98

Inventory as a % of Total Current Assets 40.35% 43.67% 42.03% 38.68% 37.49%

Total Current Assets as a % of Total Assets 33.63% 36.55% 40.92% 45.25% 48.69%

Coverage Ratios:

Times Interest Earned 2.14 2.44 2.64 2.94 4.14

Current Portion of Long-Term Debt Coverage 2.72 2.53 2.30 1.94 1.98

Principal & Interest Coverage 2.14 1.87 6.16 1.69 1.48

Preferred Dividend Coverage 5.88 7.40 7.75 9.03 13.63

Leverage/Capitalization Ratios:

Fixed Assets to Tangible Net Worth 0.88 0.82 0.70 0.80 0.72

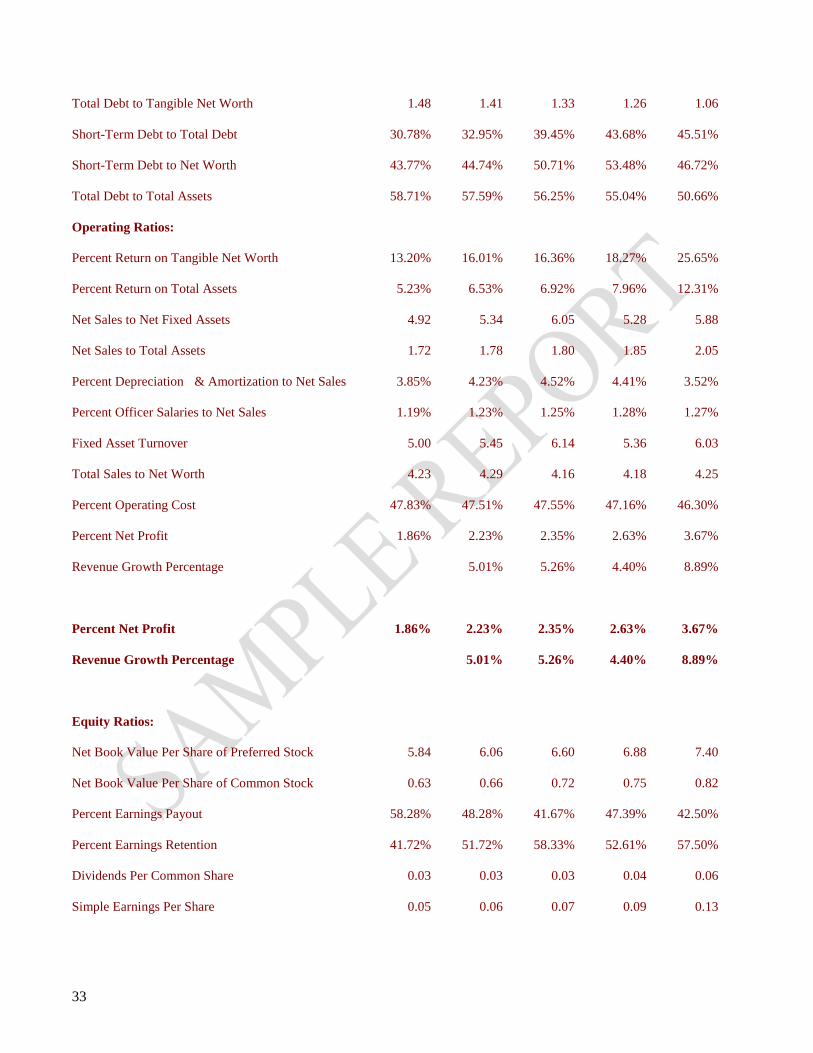

33

Total Debt to Tangible Net Worth 1.48 1.41 1.33 1.26 1.06

Short-Term Debt to Total Debt 30.78% 32.95% 39.45% 43.68% 45.51%

Short-Term Debt to Net Worth 43.77% 44.74% 50.71% 53.48% 46.72%

Total Debt to Total Assets 58.71% 57.59% 56.25% 55.04% 50.66%

Operating Ratios:

Percent Return on Tangible Net Worth 13.20% 16.01% 16.36% 18.27% 25.65%

Percent Return on Total Assets 5.23% 6.53% 6.92% 7.96% 12.31%

Net Sales to Net Fixed Assets 4.92 5.34 6.05 5.28 5.88

Net Sales to Total Assets 1.72 1.78 1.80 1.85 2.05

Percent Depreciation & Amortization to Net Sales 3.85% 4.23% 4.52% 4.41% 3.52%

Percent Officer Salaries to Net Sales 1.19% 1.23% 1.25% 1.28% 1.27%

Fixed Asset Turnover 5.00 5.45 6.14 5.36 6.03

Total Sales to Net Worth 4.23 4.29 4.16 4.18 4.25

Percent Operating Cost 47.83% 47.51% 47.55% 47.16% 46.30%

Percent Net Profit 1.86% 2.23% 2.35% 2.63% 3.67%

Revenue Growth Percentage 5.01% 5.26% 4.40% 8.89%

Percent Net Profit 1.86% 2.23% 2.35% 2.63% 3.67%

Revenue Growth Percentage 5.01% 5.26% 4.40% 8.89%

Equity Ratios:

Net Book Value Per Share of Preferred Stock 5.84 6.06 6.60 6.88 7.40

Net Book Value Per Share of Common Stock 0.63 0.66 0.72 0.75 0.82

Percent Earnings Payout 58.28% 48.28% 41.67% 47.39% 42.50%

Percent Earnings Retention 41.72% 51.72% 58.33% 52.61% 57.50%

Dividends Per Common Share 0.03 0.03 0.03 0.04 0.06

Simple Earnings Per Share 0.05 0.06 0.07 0.09 0.13

34

Sustainable Growth Rate 2.68% 4.20% 4.90% 5.05% 8.11%

Z-Score 2.89 3.06 3.12 3.28 3.81

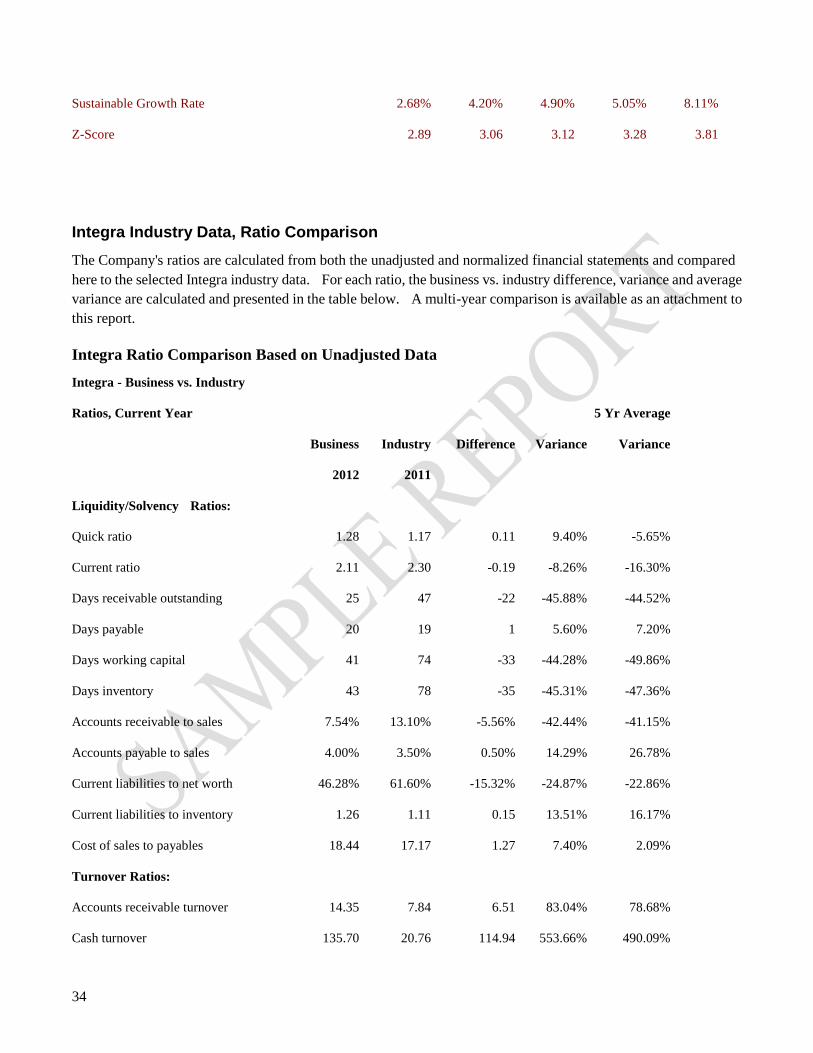

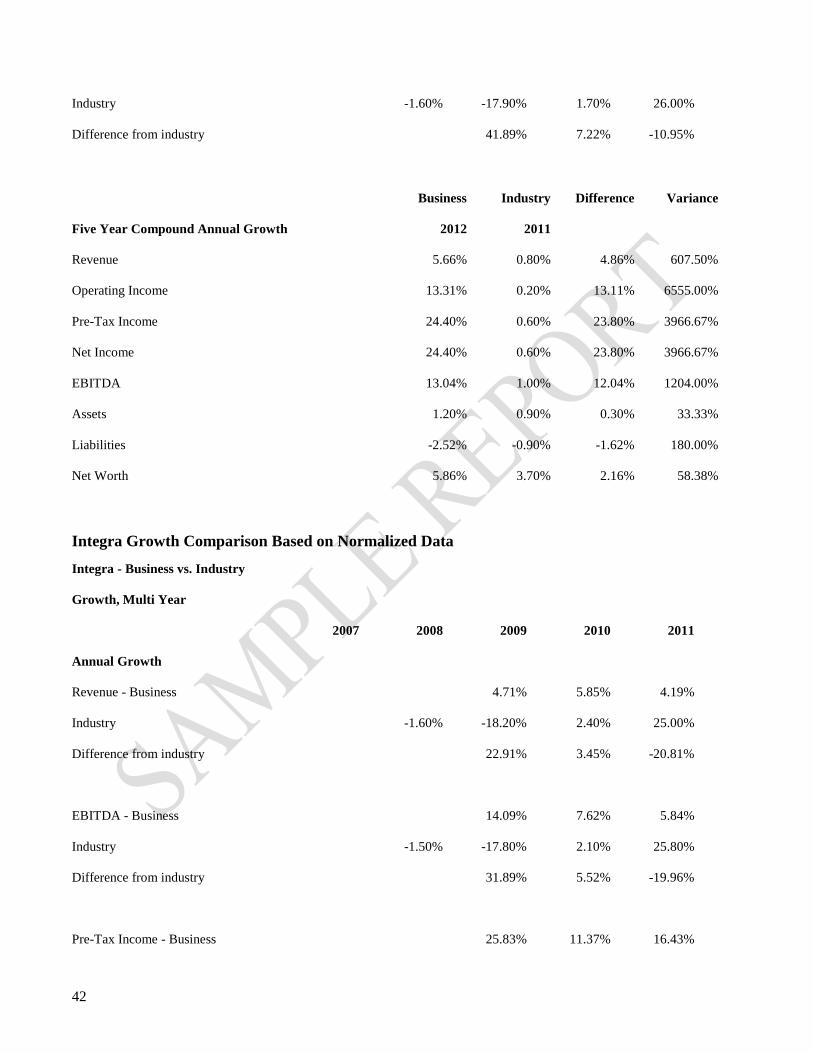

Integra Industry Data, Ratio Comparison

The Company's ratios are calculated from both the unadjusted and normalized financial statements and compared

here to the selected Integra industry data. For each ratio, the business vs. industry difference, variance and average

variance are calculated and presented in the table below. A multi-year comparison is available as an attachment to

this report.

Integra Ratio Comparison Based on Unadjusted Data

Integra - Business vs. Industry

Ratios, Current Year 5 Yr Average

Business Industry Difference Variance Variance

2012 2011

Liquidity/Solvency Ratios:

Quick ratio 1.28 1.17 0.11 9.40% -5.65%

Current ratio 2.11 2.30 -0.19 -8.26% -16.30%

Days receivable outstanding 25 47 -22 -45.88% -44.52%

Days payable 20 19 1 5.60% 7.20%

Days working capital 41 74 -33 -44.28% -49.86%

Days inventory 43 78 -35 -45.31% -47.36%

Accounts receivable to sales 7.54% 13.10% -5.56% -42.44% -41.15%

Accounts payable to sales 4.00% 3.50% 0.50% 14.29% 26.78%

Current liabilities to net worth 46.28% 61.60% -15.32% -24.87% -22.86%

Current liabilities to inventory 1.26 1.11 0.15 13.51% 16.17%

Cost of sales to payables 18.44 17.17 1.27 7.40% 2.09%

Turnover Ratios:

Accounts receivable turnover 14.35 7.84 6.51 83.04% 78.68%

Cash turnover 135.70 20.76 114.94 553.66% 490.09%

35

Inventory turnover 8.56 4.66 3.90 83.69% 91.56%

Current asset turnover 4.41 2.76 1.65 59.78% 70.44%

Working capital turnover 8.85 4.91 3.94 80.24% 101.73%

Fixed asset turnover -14.28 15.65 -29.93 -191.25% -211.68%

Total asset turnover 2.06 1.63 0.43 26.38% 16.81%

Debt Ratios:

Debt service coverage EBITDA 1.50 1.02 0.48 47.06% 62.55%

Debt service coverage Pre-tax 1.50 1.03 0.47 45.63% 60.97%

Debt service coverage After-tax 1.19 0.89 0.30 33.71% 57.76%

Interest coverage 3.68 3.30 0.38 11.52% -22.25%

Current assets to short term debt 4.69 5.91 -1.22 -20.64% -9.75%

Accounts payable to total debt 16.51% 9.70% 6.81% 70.21% 53.35%

Short term debt to total debt 20.40% 17.20% 3.20% 18.60% -13.79%

Long term debt to total assets 27.60% 23.80% 3.80% 15.97% 44.48%

ST debt plus LT debt to net worth 76.58% 80.90% -4.32% -5.34% 19.07%

Total debt to assets 50.50% 58.20% -7.70% -13.23% -4.57%

Total debt to inventory 2.78 2.51 0.27 10.76% 36.89%

Total debt to net worth 1.02 1.39 -0.37 -26.62% -9.51%

Risk Ratios:

Z-Score Manufacturing 2.93 2.52 0.41 16.27% 0.94%

Z-Score Non-manufacturing 5.28 2.52 2.76 109.52% 70.93%

Fixed assets to Net worth -0.38 0.25 -0.63 -252.00% -137.32%

Profitability Ratios:

Gross Margin % 26.17% 33.70% -7.53% -22.34% -33.54%

EBITDA to Sales 10.68% 6.70% 3.98% 59.40% 50.54%

Operating Margin 6.88% 3.50% 3.38% 96.57% 64.29%

Operating Cash Flow to Sales 4.95% 0.00% 4.95% 0.00% 0.00%

Pre-Tax Return on Assets 11.20% 3.70% 7.50% 202.70% 91.82%

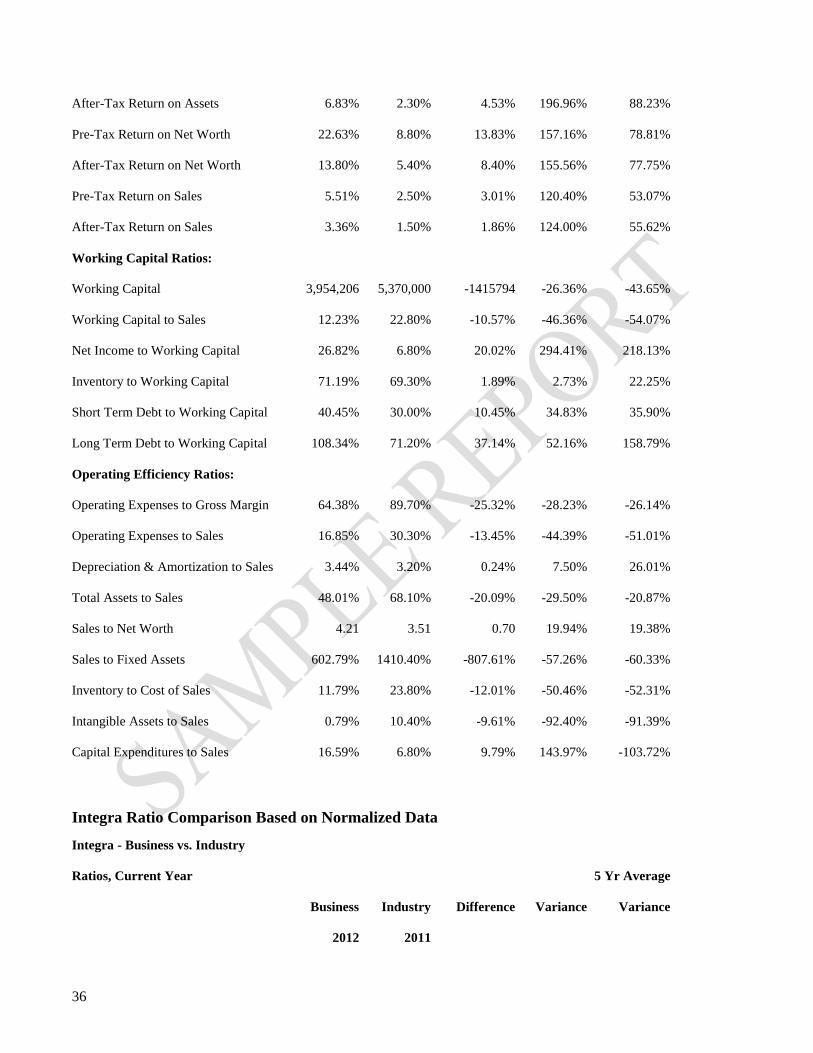

36

After-Tax Return on Assets 6.83% 2.30% 4.53% 196.96% 88.23%

Pre-Tax Return on Net Worth 22.63% 8.80% 13.83% 157.16% 78.81%

After-Tax Return on Net Worth 13.80% 5.40% 8.40% 155.56% 77.75%

Pre-Tax Return on Sales 5.51% 2.50% 3.01% 120.40% 53.07%

After-Tax Return on Sales 3.36% 1.50% 1.86% 124.00% 55.62%

Working Capital Ratios:

Working Capital 3,954,206 5,370,000 -1415794 -26.36% -43.65%

Working Capital to Sales 12.23% 22.80% -10.57% -46.36% -54.07%

Net Income to Working Capital 26.82% 6.80% 20.02% 294.41% 218.13%

Inventory to Working Capital 71.19% 69.30% 1.89% 2.73% 22.25%

Short Term Debt to Working Capital 40.45% 30.00% 10.45% 34.83% 35.90%

Long Term Debt to Working Capital 108.34% 71.20% 37.14% 52.16% 158.79%

Operating Efficiency Ratios:

Operating Expenses to Gross Margin 64.38% 89.70% -25.32% -28.23% -26.14%

Operating Expenses to Sales 16.85% 30.30% -13.45% -44.39% -51.01%

Depreciation & Amortization to Sales 3.44% 3.20% 0.24% 7.50% 26.01%

Total Assets to Sales 48.01% 68.10% -20.09% -29.50% -20.87%

Sales to Net Worth 4.21 3.51 0.70 19.94% 19.38%

Sales to Fixed Assets 602.79% 1410.40% -807.61% -57.26% -60.33%

Inventory to Cost of Sales 11.79% 23.80% -12.01% -50.46% -52.31%

Intangible Assets to Sales 0.79% 10.40% -9.61% -92.40% -91.39%

Capital Expenditures to Sales 16.59% 6.80% 9.79% 143.97% -103.72%

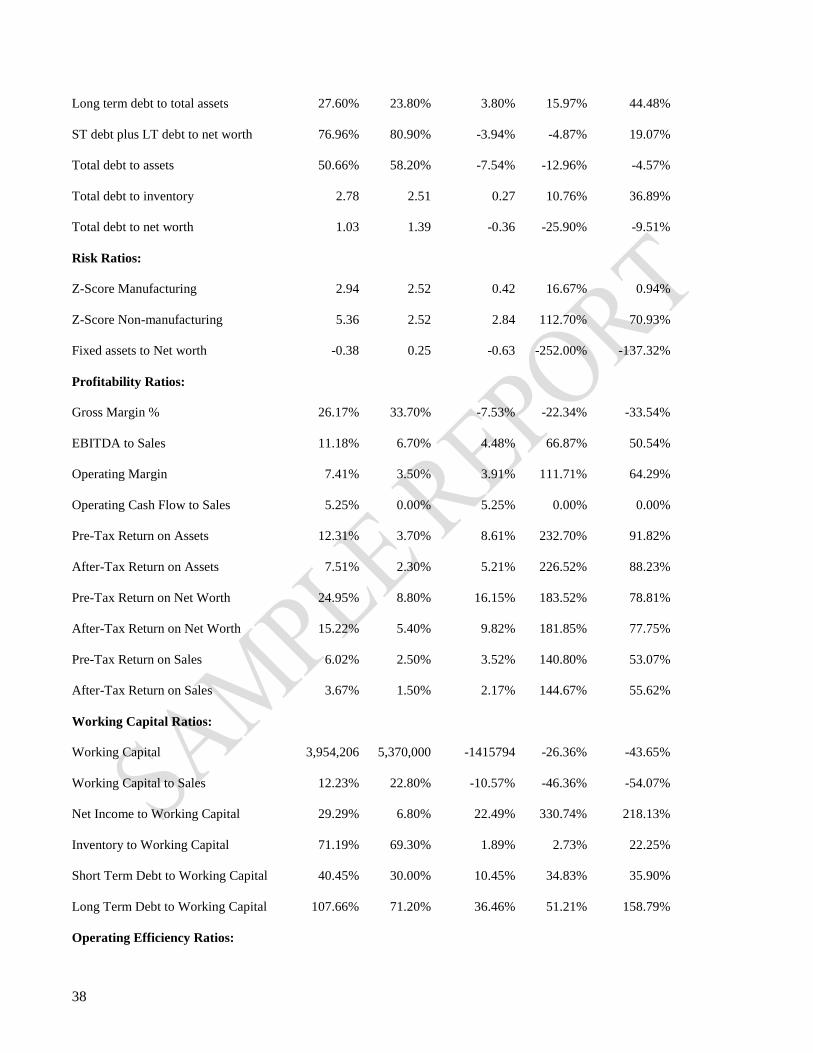

Integra Ratio Comparison Based on Normalized Data

Integra - Business vs. Industry

Ratios, Current Year 5 Yr Average

Business Industry Difference Variance Variance

2012 2011

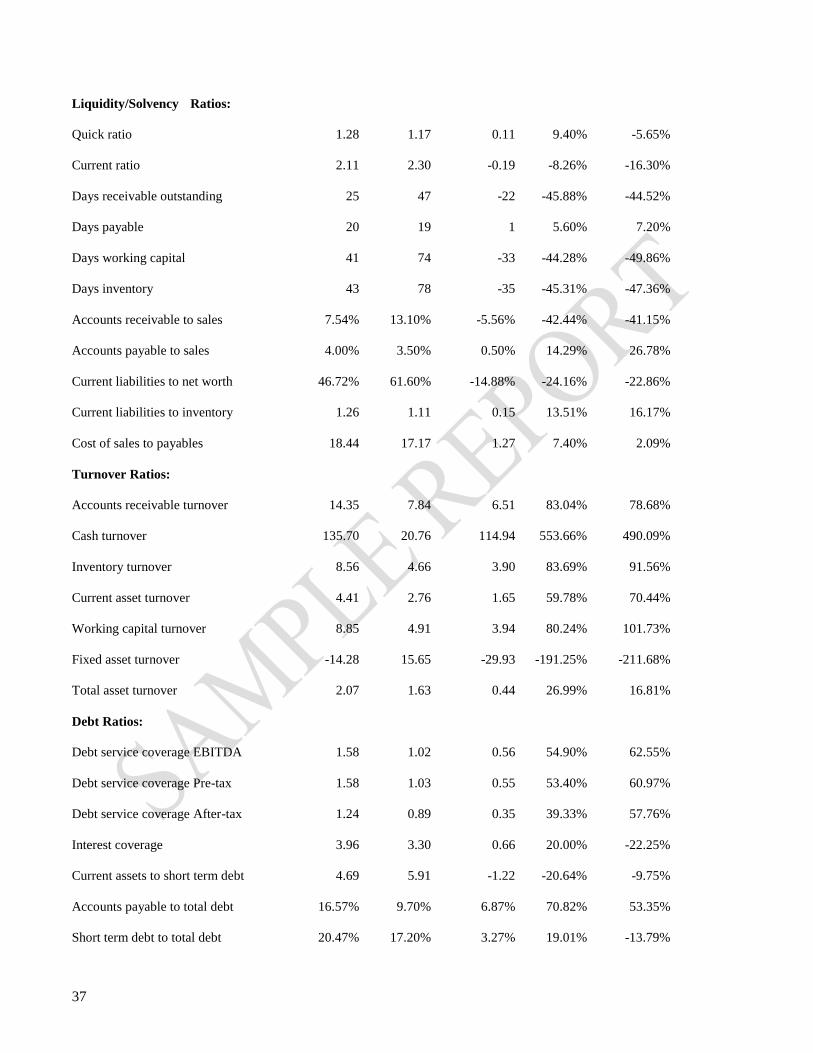

37

Liquidity/Solvency Ratios:

Quick ratio 1.28 1.17 0.11 9.40% -5.65%

Current ratio 2.11 2.30 -0.19 -8.26% -16.30%

Days receivable outstanding 25 47 -22 -45.88% -44.52%

Days payable 20 19 1 5.60% 7.20%

Days working capital 41 74 -33 -44.28% -49.86%

Days inventory 43 78 -35 -45.31% -47.36%

Accounts receivable to sales 7.54% 13.10% -5.56% -42.44% -41.15%

Accounts payable to sales 4.00% 3.50% 0.50% 14.29% 26.78%

Current liabilities to net worth 46.72% 61.60% -14.88% -24.16% -22.86%

Current liabilities to inventory 1.26 1.11 0.15 13.51% 16.17%

Cost of sales to payables 18.44 17.17 1.27 7.40% 2.09%

Turnover Ratios:

Accounts receivable turnover 14.35 7.84 6.51 83.04% 78.68%

Cash turnover 135.70 20.76 114.94 553.66% 490.09%

Inventory turnover 8.56 4.66 3.90 83.69% 91.56%

Current asset turnover 4.41 2.76 1.65 59.78% 70.44%

Working capital turnover 8.85 4.91 3.94 80.24% 101.73%

Fixed asset turnover -14.28 15.65 -29.93 -191.25% -211.68%

Total asset turnover 2.07 1.63 0.44 26.99% 16.81%

Debt Ratios:

Debt service coverage EBITDA 1.58 1.02 0.56 54.90% 62.55%

Debt service coverage Pre-tax 1.58 1.03 0.55 53.40% 60.97%

Debt service coverage After-tax 1.24 0.89 0.35 39.33% 57.76%

Interest coverage 3.96 3.30 0.66 20.00% -22.25%

Current assets to short term debt 4.69 5.91 -1.22 -20.64% -9.75%

Accounts payable to total debt 16.57% 9.70% 6.87% 70.82% 53.35%

Short term debt to total debt 20.47% 17.20% 3.27% 19.01% -13.79%

38

Long term debt to total assets 27.60% 23.80% 3.80% 15.97% 44.48%

ST debt plus LT debt to net worth 76.96% 80.90% -3.94% -4.87% 19.07%

Total debt to assets 50.66% 58.20% -7.54% -12.96% -4.57%

Total debt to inventory 2.78 2.51 0.27 10.76% 36.89%

Total debt to net worth 1.03 1.39 -0.36 -25.90% -9.51%

Risk Ratios:

Z-Score Manufacturing 2.94 2.52 0.42 16.67% 0.94%