Embed Size (px)

Citation preview

Toronto Region Economic Summit

Presented byy

BUSINESS TAKES THE LEAD:COLLABORATE TO COMPETE

Summit Report

Toronto Region Economic Summit

Presented byy

The Summit was clear in its ambitions —

the time for thinking and talking about regional

competitiveness was over. It is now time for action.

2 |

4 EXECUTIVE SUMMARY

7 ToRoNTo BoARD of TRADE’S ToRoNTo REgIoN ECoNoMIC SUMMIT, PRESENTED BY KPMg: A PIVoTAL MoMENT

9 BUSINESS TAKES THE LEAD: MoBILIzINg foR ACTIoN

10 TowARDS A REgIoNAL STRATEgY AND VISIoN

11 LEADINg THE THINKINg oN REgIoNAL CoMPETITIVENESS AND CLUSTERS

14 BEgINNINg THE CLUSTER DIALogUE

15 ADVANCED MANUfACTURINg

16 ENERgY

17 fooD & BEVERAgE

18 INfoRMATIoN AND CoMMUNICATIoN TECHNoLogY (ICT) & CREATIVE INDUSTRIES

19 LIfE SCIENCES

20 TRANSPoRTATIoN & LogISTICS

22 NoTHINg BUT oPTIMISM: TogETHER, wE wILL MAKE THIS HAPPEN

CoNTENTS

| 3

ToronTo Board of Trade’s ToronTo region economic summiT 2012 – PRESENTED BY KPMG

Toronto Region Economic Summit

Presented byy

EXECUTIVE SUMMARY

Toronto Board Of Trade’s Toronto Region Economic Summit, Presented by KPMG: A Pivotal Moment

A Region to be Proud Of

Toronto Board of Trade hosted the landmark Toronto Region Economic Summit, presented by KPMG, on March 29, 2012.

The Summit was clear in its ambitions — the time for thinking and talking about regional competitiveness was over.

It was time for action.

Action, in building a business-led regional economic strategy that increased the competitiveness of the Toronto Region’s key industry clusters — our critical mass of linked businesses and institutions, from suppliers to postsecondary institutions to government.

The Summit program was simple: bring together business leaders give each of them a clear understanding of the potential of their clusters and let the dialogue begin on generating effective cluster strategies for the Toronto Region.

As the Region’s best roadmap, the Financial Service’s cluster’s success was based on collaboration through the Toronto Financial Services Alliance, which brought together competitors and turned them into productive allies. An early win for the cluster was getting agreement on a “burning platform” as well as establishing specific objectives and metrics that showed progress and maintained momentum.

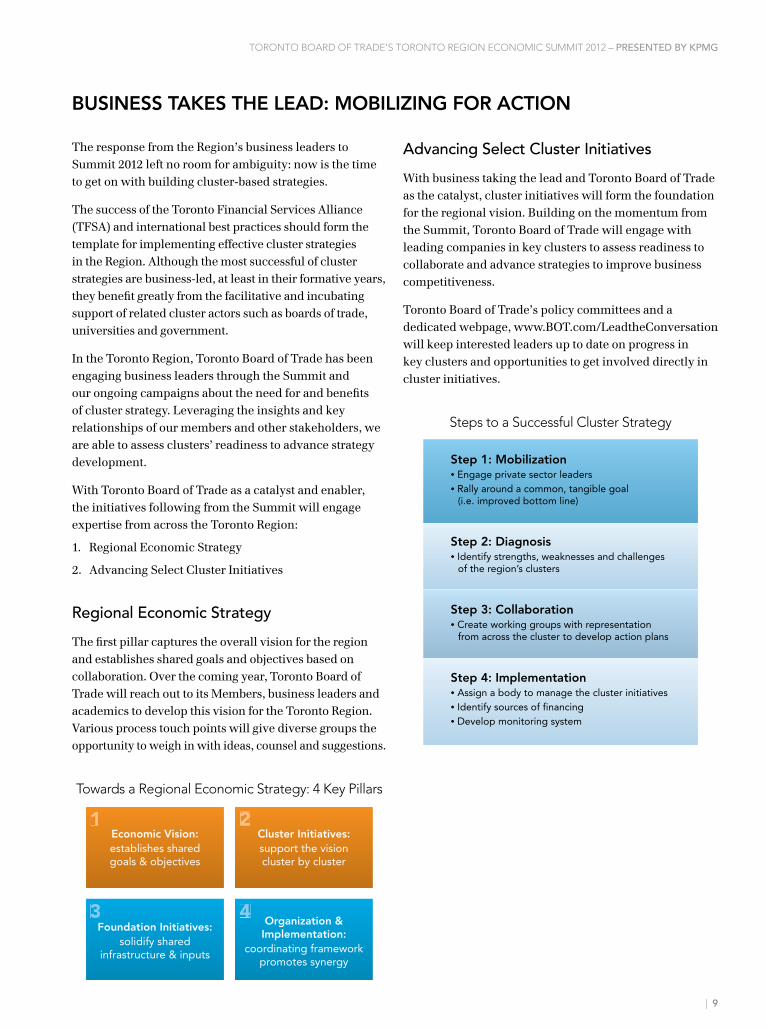

The response from the Region’s business leaders to Summit 2012 left no room for ambiguity: now is the time to get on with building cluster-based strategies.

With Toronto Board of Trade as a catalyst and enabler, the initiatives following from the Summit will engage expertise from across the Toronto Region:

1. Regional Economic Strategy

The strategy captures the overall vision for the region and establishes shared goals and objectives based on collaboration. Over the coming year, Toronto Board of Trade will reach out to its Members, business leaders, academics, government representatives, labour and other key stakeholders to draft this vision for the Toronto Region. Various touch points will give diverse groups the opportunity

to weigh in with ideas, counsel and suggestions.

2. Advancing Select Cluster Initiatives

With business taking the lead and Toronto Board of Trade as the catalyst, cluster initiatives will form the foundation for the regional vision. Building on the momentum from the Summit, Toronto Board of Trade will engage with leading companies in key clusters to assess their readiness to collaborate and advance business strategies to improve business competitiveness.

Toronto Board of Trade’s policy committees and a dedicated webpage, www.BOT.com/LeadtheConversation will keep interested leaders up to date on progress in key clusters and opportunities to get involved directly in cluster initiatives.

Dr. Michael Porter: “Collaborating to Compete”The Summit’s keynote speaker argued that the fate of the Region’s firms’ and economy was inexorably linked to the power of its key industry clusters. Porter described how the business community could help nurture those clusters best placed to compete internationally. Specifically, business needed to build upon their industry’s competitive advantages, understand what is distinctive and unique about the Toronto Region, and in so doing, help create a world beating economy.

In Dr. Porter’s view, the Toronto Region was on the right track. It was making the conversation more about what business can do to promote growth and competitiveness versus waiting for government to take action. If business started acting with one voice, examples of collaborative cluster-based success would make it “irresistibly uncomfortable” for government to maintain the status-quo of regional disunity. Dr. Porter emphasized the notion of “collaborating to compete”. While recognizing businesses must be competitors on one level, businesses also needed to work together on tackling common challenges which held back their clusters from realizing their full potential.

Business Takes the Lead: Mobilizing for Action

4 |

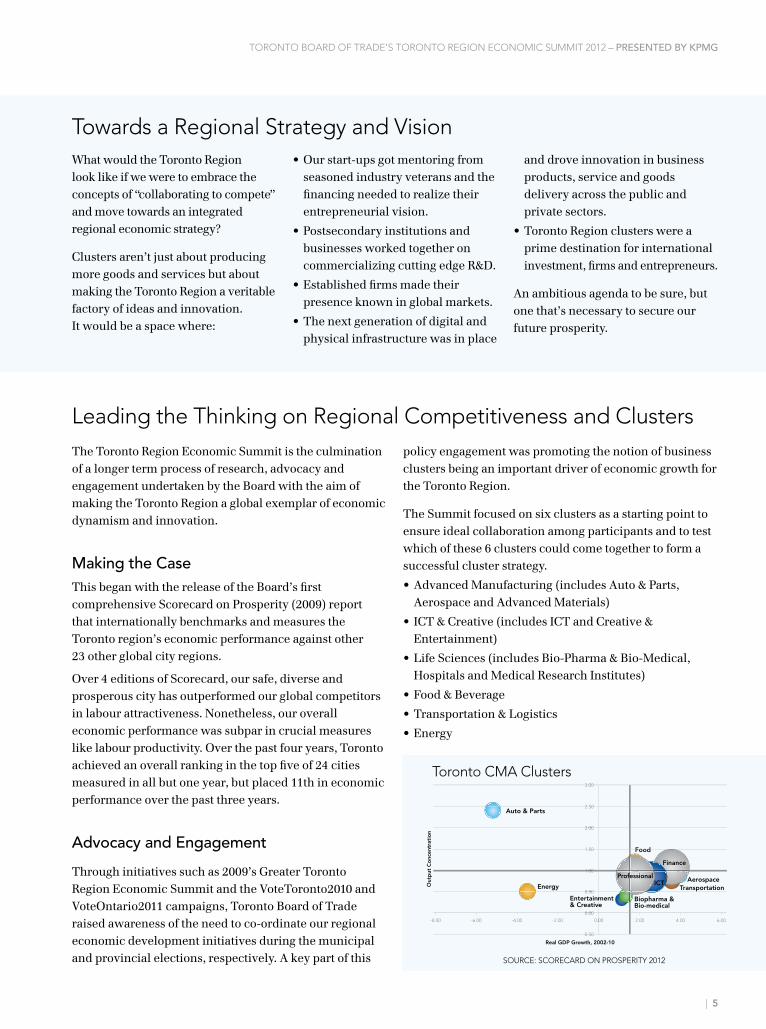

The Toronto Region Economic Summit is the culmination of a longer term process of research, advocacy and engagement undertaken by the Board with the aim of making the Toronto Region a global exemplar of economic dynamism and innovation.

Making the CaseThis began with the release of the Board’s first comprehensive Scorecard on Prosperity (2009) report that internationally benchmarks and measures the Toronto region’s economic performance against other 23 other global city regions.

Over 4 editions of Scorecard, our safe, diverse and prosperous city has outperformed our global competitors in labour attractiveness. Nonetheless, our overall economic performance was subpar in crucial measures like labour productivity. Over the past four years, Toronto achieved an overall ranking in the top five of 24 cities measured in all but one year, but placed 11th in economic performance over the past three years.

Advocacy and Engagement

Through initiatives such as 2009’s Greater Toronto Region Economic Summit and the VoteToronto2010 and VoteOntario2011 campaigns, Toronto Board of Trade raised awareness of the need to co-ordinate our regional economic development initiatives during the municipal and provincial elections, respectively. A key part of this

policy engagement was promoting the notion of business clusters being an important driver of economic growth for the Toronto Region.

The Summit focused on six clusters as a starting point to ensure ideal collaboration among participants and to test which of these 6 clusters could come together to form a successful cluster strategy.

•Advanced Manufacturing (includes Auto & Parts, Aerospace and Advanced Materials)

• ICT & Creative (includes ICT and Creative & Entertainment)

•Life Sciences (includes Bio-Pharma & Bio-Medical, Hospitals and Medical Research Institutes)

•Food & Beverage

•Transportation & Logistics

•Energy

Auto & Parts

3.00

2.50

2.00

1.50

1.00

0.50

0.00

-0.50

0.00-2.00 2.00 4.00 6.00-4.00-6.00-8.00

Energy

Real GDP Growth, 2002-10

Out

put

Co

ncen

trat

ion

Food

Finance

AerospaceTransportation

Biopharma & Bio-medical

ProfessionalICT

Entertainment & Creative

1 00

0 50

0 00

0 50

2 00

Food1 50

2 50

3 00

fe

0

me

Toronto CMA Clusters

Leading the Thinking on Regional Competitiveness and Clusters

What would the Toronto Region look like if we were to embrace the concepts of “collaborating to compete” and move towards an integrated regional economic strategy?

Clusters aren’t just about producing more goods and services but about making the Toronto Region a veritable factory of ideas and innovation. It would be a space where:

•Our start-ups got mentoring from seasoned industry veterans and the financing needed to realize their entrepreneurial vision.

•Postsecondary institutions and businesses worked together on commercializing cutting edge R&D.

•Established firms made their presence known in global markets.

•The next generation of digital and physical infrastructure was in place

and drove innovation in business products, service and goods delivery across the public and private sectors.

•Toronto Region clusters were a prime destination for international investment, firms and entrepreneurs.

An ambitious agenda to be sure, but one that’s necessary to secure our future prosperity.

Towards a Regional Strategy and Vision

SOURCE: SCORECARD ON PROSPERITY 2012

| 5

ToronTo Board of Trade’s ToronTo region economic summiT 2012 – PRESENTED BY KPMG

Toronto Region Economic Summit

Presented byy

Advanced Manufacturing Energy food & Beverage

Strengths• Talented workforce

• Diversity of industry

• Internationally competitive

• Opportunity for new exportable elements

• Diversity of technologies

• Strong electrical generating infrastructure

• Great endowments

• Proximity to micro-clusters

• Stable demand and growth

Challenges

• Poor cross-industry collaboration

• Inadequate access to captial

• Lack of commercialization of R & D

• Inconsistent governance

• Need to attract innovation/ R & D related investment

• Human capital gap

• Municipal zoning and regulations impede expansion

• No strategy to access emerging markets

• Lack of cohesive taxation policy

Possible Solutions

• Encourage green initiatives

• Improve support of entrepreneurs

• Create new funding vehicles to support high-growth potential firms

• Build consistent long term energy strategy

• Export growing green and nuclear energy know how

• Improve smart grid applications

• Involve post secondary educational institutions to grow industry leaders

• Create competitive commercial property taxes across the GTA

• Improve talent attraction

ICT & Creative Life Sciences Transportation & Logistics

Strengths• Single industry association

• Critical mass of traded industries

• Strength of education system

• Diversity of global connections

• Strong talent management

• Diverse hospital network

• Strong inter-modality across all modes of transportation

• Emerging West-East Lakeshore transit hub

• Large land capacity near GTAA

Challenges• Lack of industry mentorship

• Need to build stronger brand

• Inadequate broadband access

• Broad geography impedes collaboration

• Procurement system needs to better manage new R & D opportunities

• Better management of labour market needs

• Skill & apprenticeship shortage at trade skill level

• Lack of long-term infrastructure financing

• Poor use of ICT to enhance productivity

Possible Solutions

• Broaden ICT curriculum

• Increase industry apprenticeships

• Create growth-oriented tax incentives

• Leverage purchasing/procurement power to drive greater innovation

• Develop sustained long-term vision (10 yrs +)

• Develop value proposiiton in medical devices and diagnostics

• Leverage domestic procurement expertise to develop exportable knowledge and products

• Expand Provincial Nominee program to fill skills gap

• Better align industry needs with educational institutions

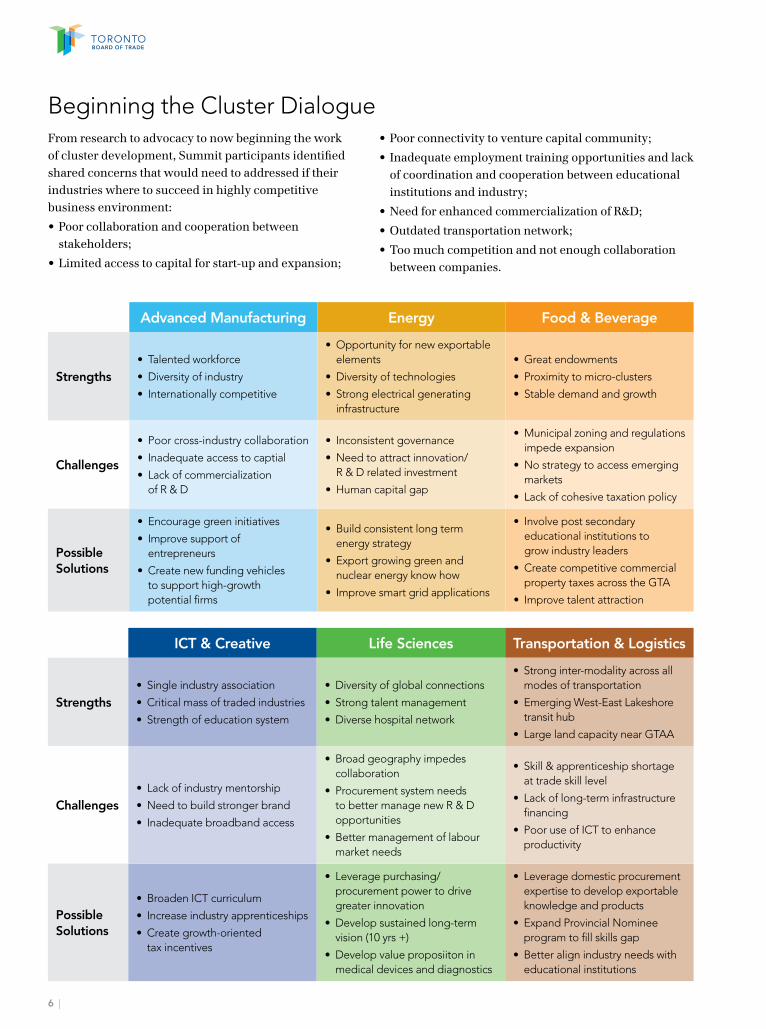

From research to advocacy to now beginning the work of cluster development, Summit participants identified shared concerns that would need to addressed if their industries where to succeed in highly competitive business environment:

•Poor collaboration and cooperation between stakeholders;

•Limited access to capital for start-up and expansion;

•Poor connectivity to venture capital community;

• Inadequate employment training opportunities and lack of coordination and cooperation between educational institutions and industry;

•Need for enhanced commercialization of R&D;

•Outdated transportation network;

•Too much competition and not enough collaboration between companies.

Beginning the Cluster Dialogue

6 |

ToRoNTo BoARD of TRADE’S ToRoNTo REgIoN ECoNoMIC SUMMIT, PRESENTED BY KPMg: A PIVoTAL MoMENT

A Region to be Proud Of

Few would dispute the Toronto Region’s assets: an enviable quality of life, world class educational institutions, a diverse and highly educated workforce and a wealth of leading industry clusters such as advanced manufacturing, food and beverage, financial services and life-sciences. The Toronto Region exudes cultural sophistication through the Toronto International Film Festival and economic heft through being home to what the World Economic Forum described as the soundest financial system in the world. Innovation and creativity sparkle through groundbreaking public and private sector collaborations such as MaRs and one-of-a kind urban spaces like the Distillery District. Make no mistake — the Toronto Region’s a perennial top-10 performer across a range of international rankings from the Economist’s “Most Liveable Cities in the World” to KPMG’s “Competitive Alternatives” for good reason. This year’s Scorecard on Prosperity was no exception, the Region finished 5th ahead of such world renowned competition as New York, Tokyo and Barcelona; impressive of course, but certainly no cause for complacency. Indeed city regions are no different from businesses. They compete globally for investment, talent and new ways of transforming their business environment. As headlines from the business news demonstrate, without a clear commitment to continuous improvement and innovation, once great firms can whither and disappear from the economic landscape.

Against a competitive backdrop that continuously raises the bar, we also have to address the areas where we lag. Regardless of the indicator, whether it’s GDP and productivity growth or the unemployment rate, our long-term economic performance puts us near the bottom of North American league tables. Improving these indicators would remove the limits to raising our standard of living and ability to invest in those things that make the Toronto Region so liveable and desirable.

Toronto Board of Trade hosted the landmark Toronto Region Economic Summit, presented by KPMG, on March 29, 2012.

The Summit was clear in its ambitions — the time for thinking and talking about regional competitiveness was over.

It was time for action.

Action, in building a business-led regional economic strategy that increased the competitiveness of the Toronto Region’s key industry clusters - our critical mass of linked businesses and institutions, from suppliers to postsecondary institutions to government.

The Summit program was simple: bring together business leaders from across clusters, give each of them a clear understanding of the potential of cluster strategy and begin the dialogue to develop cluster strategies for the Toronto Region.

Regional CooRdination is needed

For Dr. Anne Golden, President and CEO of the Conference Board

of Canada, city-regions are the drivers of economic prosperity and the Toronto Region and its

constituent municipalities comprise an integrated single economy. A

long-time advocate of the need for better integrated Toronto Region

governance, Dr. Golden noted that while the city-region had many

advantages, it was undermined by a failure “to think and act like a region”. She pointed out that over $1 billion could be saved annually (in direct and indirect costs to government)

simply by undertaking infrastructure development as a region versus multiple entities. Dr. Golden also outlined how the Toronto Region, unlike many competitor regions,

did not have a well-funded regional partnership capable of building a strong regional brand, to attract

business and investment.

$1 billion +Estimated annual amount in lost revenue from Canadian

companies employing strategies to lower their taxes.

$62,500Average Canadian family income.

$23.56Average hourly wage.

SOURCE: TRANSFORMING CANADA’S INTERNATIONAL TAX SYSTEM BY

BRIAN J. ARNOLD. STATISTICS CANADA.

| 7

ToronTo Board of Trade’s ToronTo region economic summiT 2012 – PRESENTED BY KPMG

Learning from Business Leaders and the Region’s Most Established Cluster

Leaders from all of the Toronto Region’s key industry clusters including Financial Services, Life Sciences, Transportation and Logistics, Advanced Manufacturing, Food and Beverage, Energy and ICT and Creative shared their insights from their own clusters.

Kevan Cowan, President of TSX Markets, and Group Head of Equities at the TMX Group, recounted the success of the established Financial Services cluster. The Cluster’s success was based on collaboration through the Toronto Financial Services Alliance, which brought together competitors and turned them into productive allies. This was not an overnight success. It was victory built on a long structured path of mobilizing key constituencies, getting buy-in on a shared understanding of the challenges facing the cluster and having the right implementation infrastructure in place. An early win for the cluster was getting agreement on a “burning platform” as well as establishing specific objectives and metrics that showed progress and maintained momentum.

Ted Lyman, IHS Managing Director, has successfully implemented cluster initiatives in San Francisco, Austin and Seattle, and moderated a lively Summit panel discussion with senior business leaders on the key opportunities and challenges facing the Toronto Region’s main industry clusters. Lyman indicated how in Seattle and Boston, cluster-driven strategies rewarded these regions with enhanced economic growth, increased innovation and productivity.

The panel included key cluster leaders:

•John Helou, President, Pfizer Canada;

•Jonathan Bamberger, President, Redpath Sugar;

•Mike Andrade, Senior Vice President, Diversified Markets, Celestica;

•Doug McCuaig, President, CGI Canada;

•Charles Rate, President, SNC Lavalin;

•David McFadden, Partner, Gowlings.

Highlighted were some of the most vital elements necessary to achieve the goals of a cluster strategy for the Toronto Region:

•A general consensus that effective clustering was all about collaboration and as a first step industrial and sector networks need to be enhanced in such areas as supply chain management.

•Underlining the importance of clusters in making business decisions was John Helou, the President of Pfizer, Canada, who explained how a recent move of its UK operations to the Boston region was driven by that city’s dense and well organized cluster of life-sciences related firms, research bodies and educational institutions.

• In a similar vein, Mike Andrade Senior Vice President, Diversified Markets for Celestica noted how improving the competitiveness of the local business environment, including clusters, was a core component of his firm’s business strategy.

dR. MiChael PoRteR: “CollaboRating to CoMPete”

Masterfully tying together the elements of regional governance and business strategy

was the Summit’s keynote speaker, Dr. Michael Porter of Harvard Business School. Dr. Porter argued that the fate of the Region’s firms’ and economy was inexorably linked to the power of its key industry clusters. Porter described

how the business community could help nurture those clusters best placed to compete

internationally. Business knows how to build on strengths based on what is distinctive and

unique in the Region’s environment.

Toronto’s mix of multiple and related clusters such as aerospace and metal manufacturing offered great opportunities for synergies in

such areas as R&D, education and workforce training. Cultural factors such as a greater

openness to immigration than many competing regions, including the U.S, positioned the

region’s prospects well in the race to attract the world’s best talent and entrepreneurs.

In Dr. Porter’s view, the Toronto Region was on the right track in making the conversation more about what business can do to promote

growth and competitiveness versus waiting for government to take action. If business

started acting with one voice, then examples of collaborative cluster-based success would make it “irresistibly uncomfortable” for government to maintain the status-quo of regional disunity. He stated that intra-regional bickering among

local governments was one of the major barriers to competitiveness and growth. He maintained that a shared vision and strategy was still a vital element in the Toronto region

realizing its full economic potential.

Dr. Porter emphasized the notion of “collaborating to compete”. Although

counterintuitive for businesses to want to encourage growth and competition in their

particular clusters, his research made the case that new businesses were more apt to be profitable and stood a better chance of

surviving over the longer-term within clusters.

BUSINESS TAKES THE LEAD: MoBILIzINg foR ACTIoN

The response from the Region’s business leaders to Summit 2012 left no room for ambiguity: now is the time to get on with building cluster-based strategies.

The success of the Toronto Financial Services Alliance (TFSA) and international best practices should form the template for implementing effective cluster strategies in the Region. Although the most successful of cluster strategies are business-led, at least in their formative years, they benefit greatly from the facilitative and incubating support of related cluster actors such as boards of trade, universities and government.

In the Toronto Region, Toronto Board of Trade has been engaging business leaders through the Summit and our ongoing campaigns about the need for and benefits of cluster strategy. Leveraging the insights and key relationships of our members and other stakeholders, we are able to assess clusters’ readiness to advance strategy development.

With Toronto Board of Trade as a catalyst and enabler, the initiatives following from the Summit will engage expertise from across the Toronto Region:

1. Regional Economic Strategy

2. Advancing Select Cluster Initiatives

Regional Economic Strategy

The first pillar captures the overall vision for the region and establishes shared goals and objectives based on collaboration. Over the coming year, Toronto Board of Trade will reach out to its Members, business leaders and academics to develop this vision for the Toronto Region. Various process touch points will give diverse groups the opportunity to weigh in with ideas, counsel and suggestions.

Towards a Regional Economic Strategy: 4 Key Pillars

Economic Vision:establishes shared goals & objectives

1 2

3 4

Cluster Initiatives:support the vision cluster by cluster

Foundation Initiatives:solidify shared

infrastructure & inputs

Organization & Implementation:

coordinating framework promotes synergy

Advancing Select Cluster Initiatives

With business taking the lead and Toronto Board of Trade as the catalyst, cluster initiatives will form the foundation for the regional vision. Building on the momentum from the Summit, Toronto Board of Trade will engage with leading companies in key clusters to assess readiness to collaborate and advance strategies to improve business competitiveness.

Toronto Board of Trade’s policy committees and a dedicated webpage, www.BOT.com/LeadtheConversation will keep interested leaders up to date on progress in key clusters and opportunities to get involved directly in cluster initiatives.

Steps to a Successful Cluster Strategy

Step 1: Mobilization• Engage private sector leaders• Rally around a common, tangible goal (i.e. improved bottom line)

Step 2: Diagnosis• Identify strengths, weaknesses and challenges of the region’s clusters

Step 3: Collaboration• Create working groups with representation from across the cluster to develop action plans

Step 4: Implementation• Assign a body to manage the cluster initiatives• Identify sources of financing• Develop monitoring system

| 9

ToronTo Board of Trade’s ToronTo region economic summiT 2012 – PRESENTED BY KPMG

Toronto Region Economic Summit

Presented byy

So, what’s next?

What would the Toronto Region look like if we were to embrace the concept of “collaborating to compete” and move towards an integrated regional economic strategy?

Clusters aren’t just about producing more goods and services but about making the Toronto Region a veritable factory of ideas and innovation. It would be a space where:

•Our start-ups got mentoring from seasoned industry veterans and the financing needed to realize their entrepreneurial vision.

•Postsecondary institutions and businesses worked together on commercializing cutting edge R&D.

•Established firms made their presence known in global markets.

•The next generation of digital and physical infrastructure was in place and drove innovation in business products, service and goods delivery across the public and private sectors.

•Toronto Region clusters were a prime destination for international investment, firms and entrepreneurs.

Driving this vision would be a new partnership that brought together our firms big and small, government, labour and academia with a singular objective in mind: making the Toronto Region the most innovative, creative and fastest growing regional economy in North America.

The partnership would be driven by a strategy that would create the optimal conditions and business environment for the Toronto Region’s powerful economy to thrive. Our partnership’s leaders would act as advocates for the Toronto Region, speaking up for our workforce and businesses and making the case for continued investment in our critical infrastructure.

Bringing this together would be a transformed regional governance structure that would encourage businesses and organizations to work together and to pool resources toward common goals, such as the promotion of the Toronto Region’s clusters overseas. It would maintain and enhance the conditions that allow our people and firms to use the creativity and initiative that have contributed so much to the growth of our clusters.

An ambitious agenda to be sure, but one that’s necessary to secure our future prosperity.

TowARDS A REgIoNAL STRATEgY AND VISIoN

The Toronto Region’s catchment area includes 120 million people within an 800 kilometre radius and other leading city regions such as Montreal, New York, Chicago and Boston.

10 |

The Toronto Region Economic Summit is the culmination of a longer term process of research, advocacy and engagement undertaken by the Board with the singular objective of making the Toronto Region a global exemplar of economic dynamism and innovation.

Making the Case

Responding to the shock waves of economic upheaval associated with the global recession at the end of the last decade, Toronto Board of Trade launched an ambitious research and policy campaign to focus attention on the global competitiveness of the Toronto region. This

campaign was inaugurated with the release of the Board’s first comprehensive Scorecard on Prosperity (2009) report, an international benchmarking study designed to measure the Toronto Region’s economic performance against 23 other global city regions.

Our core mandate is to elevate the quality of life and improve the global competitiveness of the Toronto Region. The Board has lived by the mantra “what gets measured gets managed” at the regional level. Our findings on the economy domain confirmed a consistent message from year to year — Toronto was ranked in the middle of the pack compared to its leading competitor regions such as San Francisco, Boston and Seattle.

LEADINg THE THINKINg oN REgIoNAL CoMPETITIVENESS AND CLUSTERS

Toronto Region Scorecard 2012

overall

Rank Metro Area

1 Paris

2 San Francisco

3 London

4 Calgary

5 Toronto

6 Seattle

7 Boston

8 Oslo

9 Madrid

10 Barcelona

11 Tokyo

12 Sydney

13 Dallas

14 New York

15 Stockholm

16 Vancouver

17 Hong Kong

18 Montréal

19 Halifax

20 Chicago

21 Los Angeles

22 Milan

23 Shanghai

24 Berlin

Economy

Rank Metro Area grade

1 San Francisco A

2 Boston A

3 Seattle A

4 Dallas B

5 Paris B

6 New York B

7 Tokyo B

8 Calgary B

9 Oslo C

10 Hong Kong C

11 Toronto C

12 Chicago C

13 Stockholm C

14 Madrid C

15 Sydney C

16 Los Angeles C

17 London C

18 Milan C

19 Vancouver C

20 Halifax C

21 Barcelona D

22 Montréal D

23 Shanghai D

24 Berlin D

Labour Attractiveness

Rank Metro Area grade

1 Paris A

2 London A

3 Barcelona A

4 Calgary A

5 Toronto B

6 Madrid B

7 Oslo B

8 Sydney B

9 Montréal C

10 Tokyo C

11 Vancouver C

12 Halifax C

13 Stockholm C

14 New York D

15 Dallas D

16 Seattle D

17 Berlin D

18 Hong Kong D

19 San Francisco D

20 Shanghai D

21 Boston D

22 Chicago D

23 Los Angeles D

24 Milan D

| 11

ToronTo Board of Trade’s ToronTo region economic summiT 2012 – PRESENTED BY KPMG

Toronto Region Economic Summit

Presented byy

Advocacy and Engagement

In conjunction with this robust platform of research and analysis, the Greater Toronto Region Economic Summit mobilized in the Spring of 2009 business leaders and entrepreneurs to think and market ourselves as a region. Its No. 1 recommendation was to establish a co-ordinating “war cabinet” composed of all mayors, regional chairs, and municipal economic development to work directly with Ontario’s Minister of Economic Development and Trade. This priority responded to the realization that economic development leadership was fractured across too many organizations, noting that “instead of competing as a unit in the global economy, we appeared to the world as a disorganized group of entities.”

Through its VoteToronto2010 and VoteOntario2011 campaigns, Toronto Board of Trade raised awareness of the need to co-ordinate our regional economic development initiatives during the municipal and provincial elections, respectively. A key part of this policy engagement was promoting the notion of business clusters being an important driver of economic growth for the Toronto Region.

Talking about Clusters 2012

A natural evolution from the Board’s focus on the governance dimension of economic competitiveness was to begin a more deep-dive into the comparative performance of our Region’s firms and business environment. This year’s Scorecard laid the foundation of understanding that cluster-based strategies are an important element in securing the Toronto Region’s future prosperity. In fact, following Dr. Porter’s research on clusters, the Board contended that robust cluster strategies were the best way of fostering innovation, improving productivity and international competitiveness.

Its analysis of economic clusters identified five key indicators upon which to benchmark the breadth and depth of 10 clusters across 12 North American regions:

•Aerospace

•Auto & Parts

•Creative & Entertainment

•Energy

•Finance

•Food & Beverage

•Bio-Pharma & Bio-Medical

• Information & Communication Technology (ICT)

•Professional Services

•Transportation & Logistics

These 10 clusters of economic activity formed a representative sample of manufacturing and service industries rather than a comprehensive inventory of total economic activity. They comprise roughly 37% of economic activity in the Toronto Region and accounted for substantial employment in Toronto.

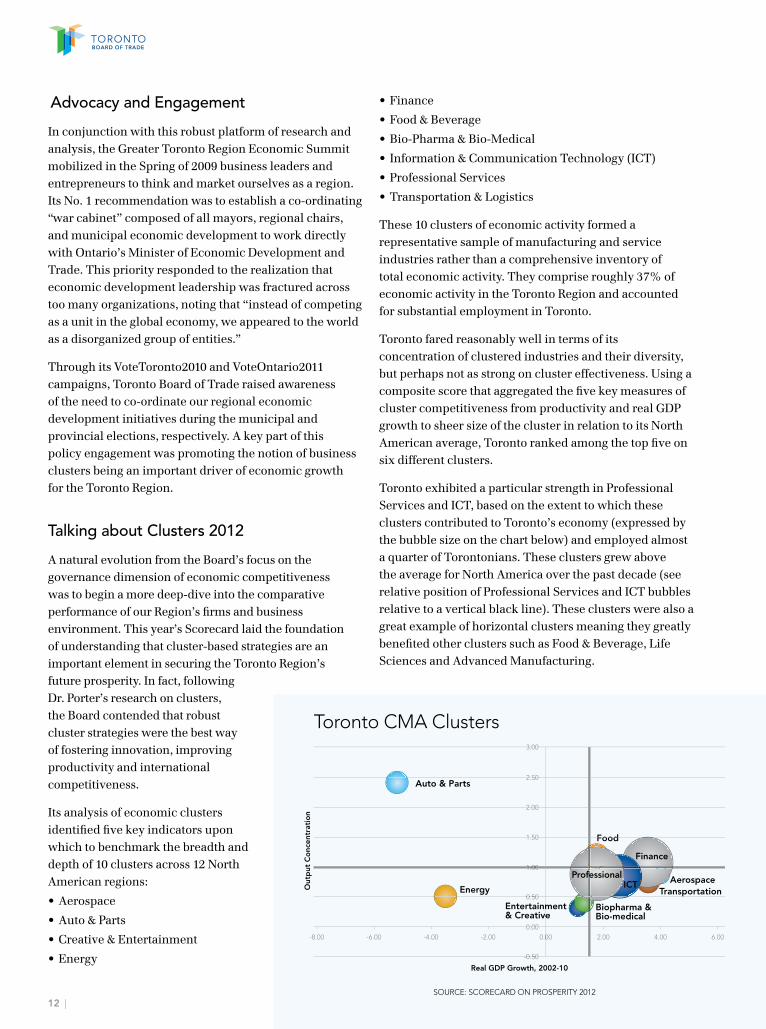

Toronto fared reasonably well in terms of its concentration of clustered industries and their diversity, but perhaps not as strong on cluster effectiveness. Using a composite score that aggregated the five key measures of cluster competitiveness from productivity and real GDP growth to sheer size of the cluster in relation to its North American average, Toronto ranked among the top five on six different clusters.

Toronto exhibited a particular strength in Professional Services and ICT, based on the extent to which these clusters contributed to Toronto’s economy (expressed by the bubble size on the chart below) and employed almost a quarter of Torontonians. These clusters grew above the average for North America over the past decade (see relative position of Professional Services and ICT bubbles relative to a vertical black line). These clusters were also a great example of horizontal clusters meaning they greatly benefited other clusters such as Food & Beverage, Life Sciences and Advanced Manufacturing.

Auto & Parts

3.00

2.50

2.00

1.50

1.00

0.50

0.00

-0.50

0.00-2.00 2.00 4.00 6.00-4.00-6.00-8.00

Energy

Real GDP Growth, 2002-10

Out

put

Co

ncen

trat

ion

Food

Finance

AerospaceTransportation

Biopharma & Bio-medical

ProfessionalICT

Entertainment & Creative

1 00

0 50

0 00

0 50

2 00

Food1 50

2 50

3 00

fe

0

me

Toronto CMA Clusters

SOURCE: SCORECARD ON PROSPERITY 201212 |

CLUSTER SUCCESS SToRY

Financial Services and the Toronto Financial Services Alliance (TFSA)The TFSA convened key industry, government and educational sector stakeholders to develop a comprehensive cluster strategy for Toronto’s financial services cluster.

The strategy identified several emerging sub-clusters, such as risk and retirement management, and support to mining, gas and oil companies, where Toronto can compete on a global scale.

The efforts of the TFSA members are recognized internationally, with Toronto ranked among the top 10 financial centres in the world, according to the Global Financial Centers Index. Importantly, the reputation of Canada’s banking system soared in the wake of the recent recession further positioning Toronto as a strong global financial centre. When Forbes named Canada as the No. 1 country to do business in 2011, the banking sector was showered with praise: “Canada’s major banks, however, emerged from the financial crisis of 2008-09 among the strongest in the world, owing to the financial sector’s tradition of conservative lending practices and strong capitalization”.

“Canada’s four largest public pension funds manage $640 billion of combined assets and are seen as global best-in-class for sound long-term strategy, governance and compensation practices in the world, owing to the financial sector’s tradition of conservative lending practices and strong capitalization,” Forbes wrote.

Toronto is also the leading global hub for mining, metals, and energy financing activity, creating sizeable spinoff effects for professional services sector. The future of financial and professional services clusters, at least in Toronto’s context, is inextricably linked to natural resource sectors. According to TFSA, the activity associated with these sectors is the source of an estimated 7,000 financial services jobs in Canada, including investment bankers, research analysts, traders, corporate lenders and other support and professional occupations. While Toronto’s current position is strong, there is a significant opportunity to proactively promote the Region’s expertise through a more concerted effort among political leaders and industry.

SIX clusters

The Summit focused on six clusters as a starting point to ensure ideal collaboration among participants

and to test which of these 6 clusters could come together to form a

successful cluster strategy.

advanced Manufacturing

(includes Auto & Parts, Aerospace and Advanced Materials)

energy

Food & beverage

iCt & Creative (includes ICT and Creative &

Entertainment)

life sciences (includes Bio-Pharma &

Bio-Medical, Hospitals and Medical Research Institutes)

transportation & logistics

| 13

ToronTo Board of Trade’s ToronTo region economic summiT 2012 – PRESENTED BY KPMG

Toronto Region Economic Summit

Presented byy

Energized by the keynote address of Dr. Michael Porter, the Toronto Region’s leaders in Transportation & Logistics, ICT & Creative Industries, Food & Beverage, Life Sciences, Energy and Advanced Manufacturing met to discuss issues and opportunities to enhance their cluster’s competitive position.

Shared concerns surfaced including:

•Poor collaboration and cooperation between stakeholders;

•Limited access to capital for start-up and expansion;

•Poor connectivity to venture capital community;

• Inadequate employment training opportunities and lack of coordination and cooperation between educational institutions and industry;

•Need for enhanced commercialization of R&D;

•Outdated transportation network;

•Too much competition and not enough collaboration between companies.

BEgINNINg THE CLUSTER DIALogUE

3 #1 Toronto ranks first in Auto & Parts

#5 Toronto ranks fifth in Financebehind New York

#2 Toronto ranks secondin Transportation & Logistics behind Vancouver

#5Toronto ranks fifth in Bio-pharma & Bio-medical behind San Francisco

#3Toronto ranks third in Food & Beverage Manufacturingbehind Calgary

#5 Toronto ranks fifth in Aerospace behind Seattle

A

A

B

B

c

B

How Toronto ranks and grades

14 |

the initial discussion: Key Points

stRengths• Large, experienced & talented workforce

• Internationally competitive companies in Toronto

• Important part of the economy (15% of GDP)

• High value-added products

• Diversity of industry (e.g. aerospace, nuclear, food

• & beverage mfg.)

Challenges• Not much collaboration amongst industry organizations.

Too much focus on government advocacy. Cluster focus can help to increase collaboration

• Increase in training in supply chain & logistics to help competitiveness

• Poor cross-industry collaboration

• Inadequate access to capital for start-up & expansion

• Municipal zoning can impact expansion plans and loss of employment lands

• Lack of commercialization of R&D

Possible solUtions• Take advantage of green initiatives (Celestica)

• Work with government to introduce minor changes in the tax system to encourage risktaking

• Improve business support for young entrepreneurs (i.e. great ideas but not investor ready)

• Improve technology transfer in universities and businesses

• Create new funding vehicles (e.g. Sobey’s/McCains VC fund)

• Increase training in supply chain management programs

After some uncertainty, the outlook for advanced manufacturing in the Toronto Region and North America is brightening. The Canadian manufacturing sector has been enjoying a cyclical rebound from the recession with increasing consumer demand both in Canada and the U.S. helping to drive growth. Machinery and transportation manufacturing output is up by 30% and 40%, respectively, across Canada.

While the sector is forecast to recover, we can’t ignore the competitive challenges that were weighing on the sector prior to the recession. Manufacturers must step up their game in order to thrive in Toronto’s (and the world’s) changing economy.

Investing in innovative practices and technologies to increase productivity and contain unit labour costs is vital to improve competitiveness. As well, moving away from a reliance on U.S. markets to tap into other faster growing markets will increase the pool of potential buyers of Canadian-made goods.

Taking a closer look at the advanced manufacturing sector, the Board sees solid opportunities for growth in the Aerospace and Auto & Parts sectors, important contributors to the Toronto Region’s Advanced Manufacturing cluster. Unique challenges facing each of cluster sub-sectors will require creative business strategies to keep ahead of strong global competitors.

ADVANCED MANUfACTURINg

AUTo & PARTSOVERALL RANK: AREAL GDP GROWTH: BPRODUCTIVITY GROWTH: AOUTPUT CONCENTRATION: AEMPLOYMENT CONCENTRATION: AFIRM DENSITY: A

AERoSPACEOVERALL RANK: CREAL GDP GROWTH: BPRODUCTIVITY GROWTH: AOUTPUT CONCENTRATION: DEMPLOYMENT CONCENTRATION: DFIRM DENSITY: C

| 15

ToronTo Board of Trade’s ToronTo region economic summiT 2012 – PRESENTED BY KPMG

Toronto Region Economic Summit

Presented byy

the initial discussion: Key Points

stRengths• Strong and diverse electrical infrastructure development

and asset management across variety of technologies (e.g., nuclear, wind, solar)

• Potential for : » Nuclear plant development and refurbishment

• Opportunities to create new exportable elements: » Excellent project management /development

expertise (e.g., legal/financing, consulting, construction project management experience, regulatory compliance)

Challenges• Poor energy governance and inconsistent policies

• Significant need to update energy technology/infrastructure (e.g., 3rd line to Toronto)

• Can improve on the smart grid cluster system

• Looming human capital gap & challenges » Retiring workers » Education/Training » Skilled worker shortages

• Inadequate access to capital for new energy technologies

• Challenge to attract innovation/R&D deficit

• Too many LDC’s – makes it difficult to execute necessary system reforms

Possible solUtions• Build consistent long-term energy strategy which

drives development of low carbon energy with lower marginal costs – help facilitate electrification of rail, electric cars etc.

• Opportunities for development of energy/electrical storage systems

• Create strategy to better export our growing green and nuclear energy expertise and knowledge base (e.g. refurbishment of nuclear facilities)

• Better balance energy generation base with business needs to have reliable and affordable electricity

• Improved smart grid applications and integration of renewable technologies into supply mix , using innovation to match demand with supply – better base-load management

As the Board argued in its VoteOntario2011 paper Shifting Into High Gear, a successful regional economic development strategy must be supported by a competitive pro-business environment. We know successful economies are built on the foundations of a strong business environment and robust institutional infrastructure. While many factors shape a region’s ability to attract businesses and investors, having a reliable, secure and cost-competitive energy supply is undoubtedly one key precondition for success. Additionally, having a strong energy cluster supports the creation of export oriented energy and infrastructure related firms which can compete globally.

With the release of the Green Energy Act in 2009, the Long-Term Energy Plan in 2010, the Drummond Commission’s recommendations for the Ontario’s energy sector, and the recent review of the province’s feed-in-tariff strategy for renewable energy supply, this cluster has experienced considerable change in recent years.

Nevertheless, big challenges remain, including:

•Meeting the government’s target of 10,700 megawatts of alternative energy (wind, solar, biomass) by 2030;

•Replacing the generating capacity (approximately 4,484 megawatts) lost due to the phase-out of coal by 2014;

•Paying for almost $90 billion worth of investment needed to achieve the long- term energy plan, including transmission and generating infrastructure upgrades in the Toronto region;

•Achieving the government’s target of 50,000 new green energy industry jobs by 2013.

At the same-time these market and regulatory challenges open-up new business opportunities, nationally and internationally for energy-related firms in the Toronto Region, with expertise in such areas as nuclear plant development and refurbishment, project management, regulatory compliance and green energy technology.

ENERgY

OVERALL RANK: DREAL GDP GROWTH: DPRODUCTIVITY GROWTH: DOUTPUT CONCENTRATION: DEMPLOYMENT CONCENTRATION: DFIRM DENSITY: D

16 |

the initial discussion: Key Points

stRengths• Great endowments (water, agriculture, land)

• Access to large customer base (120 million)

• Proximity to micro-clusters (Niagara-on-the-lake, Prince Edward County and Guelph)

• Transportation: highways, water and rail

• Major food headquarters are close to food manufacturing, food processors, retailers

• Diversity of population, links to international markets

• Diversity of skill sets

• Stable demand and stable growth

• Access to better quality educational institutions

• Safety of food/ great quality

Challenges• Gap in medium size quality food product inhibits

smaller firms who want to grow; medium players can’t compete with large

• Limited access to capital for start-up & expansion

• Lacking cluster conscience and need more collaboration

• Lack of innovation because of small margins/small scale and no opportunity to expand

• TR doesn’t have a strategy to access emerging markets

• Municipal zoning and regulations impede expansion

• Water and sewage costs are increasing

• Rising costs to build food facilities

• GTA transportation due to congestion & challenges getting in and out; supply management

• Universities do not cooperate/coordinate and don’t coordinate with industry for employment training

• Lack of cohesive taxation policy

• Need to access foreign capital to invest in food infrastructure

Possible solUtions• Industry to work with colleges and universities to develop

the next generation of food leaders

• Improve access to capital opportunities for start-up & expansion

• Encourage talent attraction (inward investment agencies) and develop specific programs to attract foreign talent

• Unify competitive property taxes across the GTA on commercial properties

• Encourage more government support/tax credit for innovation

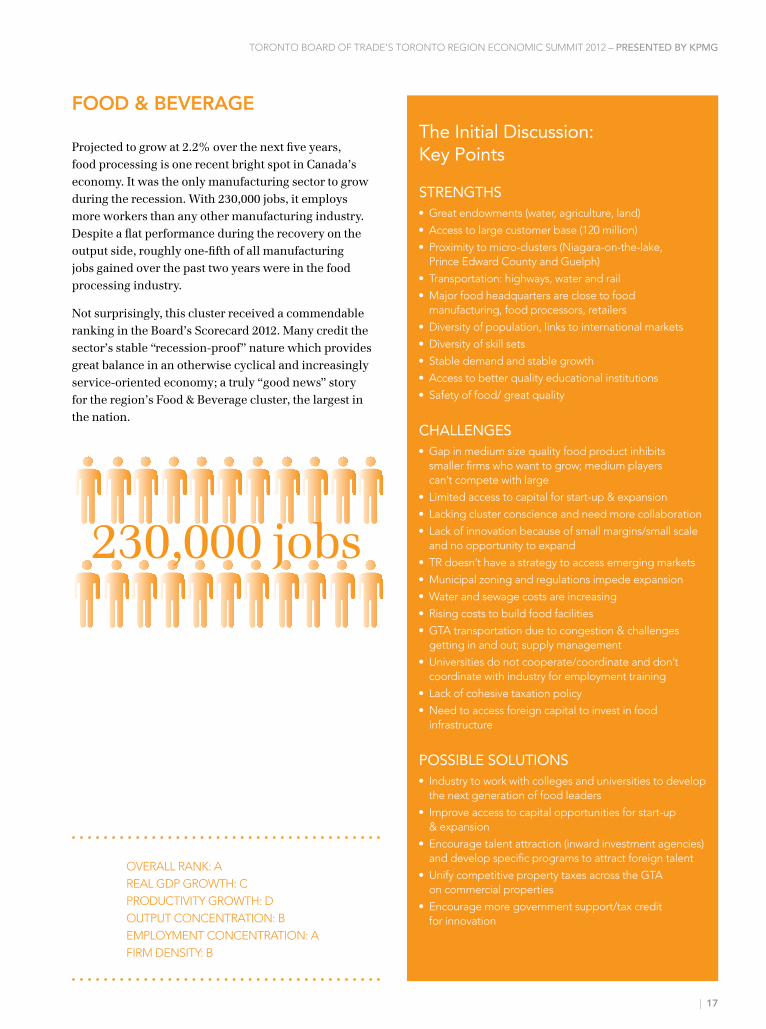

Projected to grow at 2.2% over the next five years, food processing is one recent bright spot in Canada’s economy. It was the only manufacturing sector to grow during the recession. With 230,000 jobs, it employs more workers than any other manufacturing industry. Despite a flat performance during the recovery on the output side, roughly one-fifth of all manufacturing jobs gained over the past two years were in the food processing industry.

Not surprisingly, this cluster received a commendable ranking in the Board’s Scorecard 2012. Many credit the sector’s stable “recession-proof” nature which provides great balance in an otherwise cyclical and increasingly service-oriented economy; a truly “good news” story for the region’s Food & Beverage cluster, the largest in the nation.

fooD & BEVERAgE

230,000 jobs

OVERALL RANK: AREAL GDP GROWTH: CPRODUCTIVITY GROWTH: DOUTPUT CONCENTRATION: BEMPLOYMENT CONCENTRATION: AFIRM DENSITY: B

| 17

ToronTo Board of Trade’s ToronTo region economic summiT 2012 – PRESENTED BY KPMG

Toronto Region Economic Summit

Presented byy

the initial discussion: Key Points

stRengths• One single industry association (e.g. ITAC)

• Critical mass of traded industries

• Proximity to large customer base (~120 mil)

• Strength of education system (e.g. elementary & secondary)

• Large artistic creative community helps foster innovation through collaboration between industries

• Potential to leverage our post-secondary assets

Challenges• Poor collaboration between different stakeholders

• Poor connectivity to venture capital community

• Mentality to sell out early vs. to grow business

• Lack of industry mentorship

• Need broadening of ICT curriculum as there is little entrepreneurial culture

• Quality of life vs. cost of living (costs increase benfits due to increased congestion and lack of affordable housing)

• Lacking multiple co-location/incubator space

• Poor transportation network

• Lack of success stories (e.g. RIM)

• Inadequate broadband access

• Need to build brand to attract investment and people

• Inadequate access to capital for entire ecosystem of companies

• Increase talent pool and need for apprenticeships/internships

Possible solUtions• Improve access to capital across the entire finance

ecosystem

• Broaden ICT curriculum

• Increase industry apprenticeships

• Work with government to create growth-oriented tax incentives

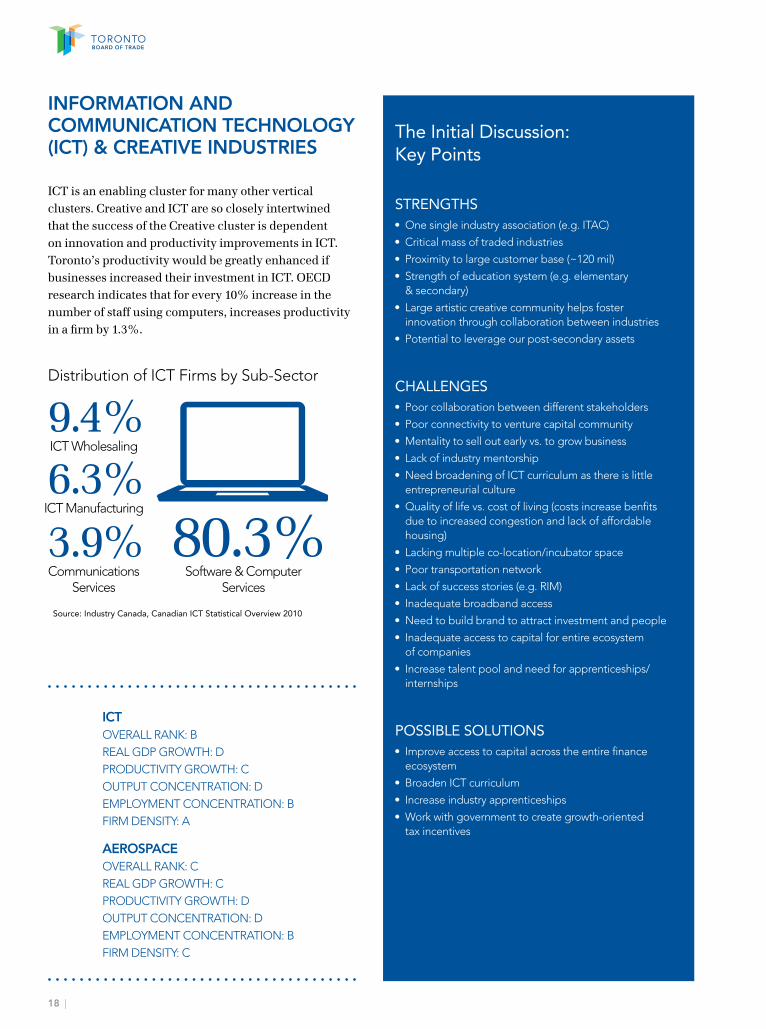

ICT is an enabling cluster for many other vertical clusters. Creative and ICT are so closely intertwined that the success of the Creative cluster is dependent on innovation and productivity improvements in ICT. Toronto’s productivity would be greatly enhanced if businesses increased their investment in ICT. OECD research indicates that for every 10% increase in the number of staff using computers, increases productivity in a firm by 1.3%.

Distribution of ICT Firms by Sub-Sector

INfoRMATIoN AND CoMMUNICATIoN TECHNoLogY (ICT) & CREATIVE INDUSTRIES

9.4%ICT Wholesaling

6.3%ICT Manufacturing

80.3%Software & Computer

Services

3.9%Communications

Services

Source: Industry Canada, Canadian ICT Statistical Overview 2010

ICTOVERALL RANK: BREAL GDP GROWTH: DPRODUCTIVITY GROWTH: COUTPUT CONCENTRATION: DEMPLOYMENT CONCENTRATION: BFIRM DENSITY: A

AERoSPACEOVERALL RANK: CREAL GDP GROWTH: CPRODUCTIVITY GROWTH: DOUTPUT CONCENTRATION: DEMPLOYMENT CONCENTRATION: BFIRM DENSITY: C

18 |

the initial discussion: Key Points

stRengths• Diversity of global connections

• Good quality of life/labour attractiveness

• Strong talent management

• Linkages to strong clinical trial system

• Diverse hospital network

• Synergy of Quebec/Ontario corridor for R&D

Challenges• Poor transportation infrastructure

• Limited access to capital for start-up & expansion

• Organizations compete more than collaborate (e.g. research centres, hospitals)

• Fragmented system operating in silo (e.g. LHINS)

• Procurement system not used to leverage new R&D opportunities

• Broad geography of cluster prevents collaboration

• Excess talent (better management of talent supply and demand needed )

• Industry not aligned with educational institutions (e.g. pharma)

Possible solUtions• Leverage purchasing/procurement power to drive

greater innovation

• Improve access to capital opportunities for start-up & expansion (e.g. Boston)

• Stronger collaboration among hospitals & broader healthcare system

• Develop sustained vision (10 years +)

• Government cannot provide this, must originate from private sector

• Develop value proposition in medical devices and diagnostics

• Better access to health records across the entire system (e.g. E-health)

• Opportunities to build-on work of OBIO initiative – Ontario Bioscience Economic Strategy Team (OBEST)

Bio-Medical and Bio-Pharma have strong ties to fundamental research in biology and medicine, and have great implications on the Life Sciences cluster overall. Hospitals are also a dominant part of this cluster’s supply chain. Hospitals typically put pressure on pharmaceutical and medical device manufacturers requiring them to produce top-quality goods and services to minimize cost. Therefore, hospitals can be thought of as very demanding consumers requiring highly sophisticated medications and medical devices, putting a lot of pressure on pharma and medical-device manufacturers to innovate. In addition, there is an opportunity for ongoing innovation through creative procurement practices that typically benefit both local and export-oriented segments of the cluster.

Major global demographic, economic, technological and political factors have created increasing demand for health- and life-science products over the recessionary period, including aging populations, rising affluence in emerging markets (with the accompanying “diseases of wealth”), and advances in medical techniques and technology. According to IHS Global Insight’s most recent North American industry forecast, the Bio-Pharma & Bio-Medical sectors will grow at a brisk rate over the next five years to accommodate this demand.

LIfE SCIENCES

OVERALL RANK: BREAL GDP GROWTH: CPRODUCTIVITY GROWTH: BOUTPUT CONCENTRATION: CEMPLOYMENT CONCENTRATION: BFIRM DENSITY: B

| 19

ToronTo Board of Trade’s ToronTo region economic summiT 2012 – PRESENTED BY KPMG

Toronto Region Economic Summit

Presented byy

the initial discussion: Key Points

stRengths• Strong inter-modality across all modes of

transportation including air, rail, trucking, etc.

• Emerging West-East Lakeshore transit hub

• Strong geographical endowment (e.g. location)

• Large land capacity near GTAA

• Opportunity to expand distribution logistics firms » On Pearson property itself » Opportunity to develop additional hub (e.g. Hamilton)

Challenges• Long commute times due to gridlock

• Poor infrastructure

• Long-term infrastructure financing

• Skill and apprenticeship shortage at trade skill level

• Poor use of ICT to drive innovation & productivity

Possible solUtions• Leverage domestic procurement expertise to develop

exportable knowledge and products (e.g. trolling)

• Expand Provincial Nominee program to fill skills gap

• Better align industry needs with educational institutions

Transportation and logistics (T&L) is one of the world’s largest industries. Its sectors range from trucking firms to airlines, rail transport, courier services, shipping, warehousing/distribution centres and logistics services. With the fragmentation of manufacturing activities and growing international and intra-firm trade, T&L activities have become more global, complex and sophisticated. An unprecedented array of products are crossing borders using different modes and generating a multitude of interconnected logistics activities across various sectors, including natural resources, manufacturing, and services. Like the ICT & Creative Industries cluster, this sector is both an important enabler of economic activity in other sectors and a source of economic activity in its own right.

Future Opportunities & Threats

The sector must be mindful of several potential threats to its long-term position:

•Rising energy costs/low carbon compliance requirements;

• Inadequate transportation infrastructure for road and rail;

•Skill shortages across T&L sub-sectors like trucking;

•External and macro economic factors such as a strong Canadian currency, global trade disruptions, and the volatile world economy.

To cope with these diverse challenges, cluster stakeholders and economic leaders should focus on implementing creative IT solutions, identifying efficiencies in work processes, and having effective talent development and management strategies.

TRANSPoRTATIoN & LogISTICS

OVERALL RANK: AREAL GDP GROWTH: APRODUCTIVITY GROWTH: COUTPUT CONCENTRATION: DEMPLOYMENT CONCENTRATION: CFIRM DENSITY: A

20 |

A promising candidate for early cluster success could be the Food & Beverage cluster. According to Scorecard 2012, the Food & Beverage cluster was ranked among the top three in North America on the back of strong output, employment concentration and firm density measure. The scale cluster became even more clear when other parts of the cluster supply chain were included (i.e. farming, primary production, packaging, distribution and logistics, retail and related food service, research centres, and colleges and universities that offer training programs).

In local terms, the economic benefits of the entire Food & Beverage cluster were seen to be huge. Nearly 75% of what was grown in the rural area surrounding Toronto was processed locally. This generated positive spin-offs for the rest of the province through the so-called ‘multiplier’ effect, which was especially strong for this cluster. It also employed a wide range of professionals from food scientists to plant managers to line supervisors; positions that were knowledge-intensive, well-paid and comparable to those in advanced manufacturing clusters like Auto & Parts.

In addition, many cluster specialists pointed to the stable, “recession-proof” nature of this sector, reflected in its steady growth over the past decade. At this time, it is unquestionably an important part of Toronto’s mix of industries, adding a measure of balance in what is otherwise an increasingly service-oriented economy.

Another selling point is this cluster’s solid export potential with easy access to foreign markets. Toronto is already recognized as a hub for specialty foods. Indeed, many food processing companies located in the GTA supply a myriad of retailers in the U.S. and other countries with private label items. With more than 80% of Toronto’s food processors employing less than 50 people, many argue that the quality, safety and innovation of our products are second to none.

That said, where Toronto’s Food & Beverage cluster was seen to be lagging in Scorecard 2012 was in the levels of investment in productivity-enhancing machinery and equipment. One report obtained by the Board estimated that for every dollar invested per worker in this cluster in the U.S., Canadian facilities invested only 62 cents.

It is evident that with the right kind of support, strategic planning and collaboration between the private sector and government, this cluster has the potential to grow and succeed globally.

Boston leverages its intellectual capital to great effect reinforcing the region as a hub of scientific research and innovation. Biotechnology is a particular strength. Boston managed to attract close to 280 biotech companies employing 30,000 people, with industry leaders like Pfizer, Genzyme, Novartis AG and Wyeth Pharmaceuticals located in Cambridge. Thus, it is not a surprise that nearly ten per cent of the world’s total pipeline of new drugs comes from companies headquartered in Cambridge alone.

Physical proximity to the medical R&D community in Massachusetts is designed to encourage frequent and meaningful relationships with leading biomedical research institutions, according to Rod MacKenzie, senior vice president of Pfizer PharmaTherapeutics. Indeed, this is a key reason behind Pfizer’s recent decision to substantially boost its presence in Cambridge making it the second largest biopharmaceutical company in Massachusetts.

Boston’s businesses, academic institutions and all levels of government have demonstrated an understanding of the value of a multi-sector, common-vision approach forming the Massachusetts Life Sciences Center, a quasi-public agency. Federal grants to Massachusetts (principally Boston) trail only California in terms of funds received. Furthermore, Massachusetts government has offered the life sciences industry $1 billion worth of incentives over the next decade to support development of innovative medical technology.

CASE STUDY

Boston – Brains and Biotech Make a Winning Combination

Food & Beverage: Growth Potential

Massachusetts government has offered the life sciences industry $1 billion worth of incentives over the next decade75%

NEARLY of what was grown in the rural area surrounding Toronto was processed locally.

| 21

ToronTo Board of Trade’s ToronTo region economic summiT 2012 – PRESENTED BY KPMG

Toronto Region Economic Summit

Presented byy

NoTHINg BUT oPTIMISM: TogETHER, wE wILL MAKE THIS HAPPEN

The Toronto Region Economic Summit 2012 left few questions about where the future of the Toronto Region’s economy lies.

No silver bullets or quick-fixes, but instead the shared work of building regional competitiveness based on strengthening our leading industry clusters. As Dr. Porter contended, many things go into making competitive city regions, but it’s people and businesses that drive and sustain economies in conjunction with sound governance. Unless we get these disparate elements working better together the Toronto Region will never quite be the sum of its parts.

Two big challenges lie before us.

First getting our clusters to optimize all of their growth opportunities in both national and international markets and second, building the momentum for the adoption of a regional economic vision and strategy.

There’s much for us to learn from places such as Seattle, a perennial high performer. Seattle experienced its tipping point that brought together business leadership to play a prominent role in driving long-term economic prosperity. At the core of this success story was the central role clusters played in galvanizing the region’s competitiveness and getting other stakeholders to rally around a common narrative, vision and strategy for regional growth.

The Toronto Region is now primed to do the same. With the business community organizing to take on a leadership role and Toronto Board of Trade helping to bring the influencers together, we are building the foundation for success.

Seattle City-Region – “Prosperity Partnership” In 2004, the Central Puget Sound Region, which refers to the greater Seattle area, embarked on a unique journey of urban economic renewal with the development and implementation of an integrated strategy to tackle the Region’s economic challenges.

Under the banner of the “Prosperity Partnership”, the Region’s business, labour, government, academia and community leaders agreed on a shared set of objectives and actions to achieve long-term economic prosperity and the creation of 100,000 new jobs. Driving the plan was a concern about how to ensure the Region maintained its strong competitive position in key industry clusters such as aerospace and life sciences.

Coordinated by the Puget Sound Regional Council (a regional governance body), the Partnership’s strategy encompassed not only business led cluster initiatives, but also actions by government and other public sector partners in such areas education and infrastructure.

22 |

The Summit was clear in its ambitions —

the time for thinking and talking about regional

competitiveness was over. It is now time for action.

| 23

ToronTo Board of Trade’s ToronTo region economic summiT 2012 – PRESENTED BY KPMG

Toronto Region Economic Summit

Presented byy

Toronto Region Economic Summit

Presented byy

Toronto Board of Trade1 First Canadian Place, P.O. Box 60Toronto, Ontario, Canada MX5 1C1

Phone: 416.366.6811www.bot.com/leadtheconversation

would not have been possible without the generous support of: