Embed Size (px)

Citation preview

BUSINESS REPORT 2004

Imprint: Medium Ownership : POLYTEC HOLDING AG, Austria;Responsible for content: Mag. Wolf-Dieter Gabriel, Controlling Group, Ing. Karl Heinz Solly, Vice president/Director New Business Development;Conception: eigen)art werbegesellschaft mbH & Co KGPhotography: Edwin Enzlmüller, archive POLYTEC HOLDING AG, Austria; Lithography: G2; Print: Gutenberg, Linz

POLYTEC AUTOMOTIVE

POLYTEC AUTOMOTIVE GmbH & Co KGMeyerfelder Weg 45D-49393 LohneGERMANYTel: +49-4442-950-0Fax: [email protected]

Office southDieselweg 10D-82538 GeretsriedGERMANYTel: +49-8171-381-0Fax: +49-8171-381-206

POLYTEC RIESSELMANN

POLYTEC RIESSELMANN GmbH & Co KGMeyerfelder Weg 45D-49393 LohneGERMANYTel: +49-4442-950-0Fax: [email protected]

LOHNER LACKIERWERK

Lohner Lackierwerk GmbHIm Schlatt 7D-49393 LohneGERMANYTel: +49-4442-950-0Fax: [email protected]

POLYTEC THERMOPLAST

POLYTEC THERMOPLAST GmbH & Co KG Black & Decker Strasse 25D-65510 IdsteinGERMANYTel: +49-6126-582-0Fax: [email protected]

POLYTEC RENTROP

POLYTEC RENTROP GmbH & Co KGAm Flugplatz 3D-29693 HodenhagenGERMANYTel: +49-5164-9856-0Fax: [email protected]

POLYTEC PLASTICS

POLYTEC PLASTICS Wolmirstedt GmbH & Co KGPolytec Strasse 1D-39326 WolmirstedtGERMANYTel: +49-39201-282-500Fax: [email protected]

POLYTEC INTERIOR GERMANY

POLYTEC INTERIOR GmbHHead office / Plant GeretsriedDieselweg 10D-82538 GeretsriedGERMANYTel: +49-8171-381-0Fax: [email protected]

POLYTEC INTERIOR GmbHPlant EbersdorfEmpestrasse 1D-07929 Saalburg-EbersdorfGERMANYTel: +49-36651-73-0Fax: [email protected]

POLYTEC INTERIOR GmbHPlant Nordhalben Langenrain 2D-96365 NordhalbenGERMANYTel: +49-9267-89-0Fax: [email protected]

POLYTEC INTERIOR GmbHPlant Wackersdorf Oskar-von-Miller-Strasse 23D-92442 WackersdorfGERMANYTel: +49-9431-7486-0Fax: [email protected]

POLYTEC INTERIOR GREAT BRITAIN

POLYTEC INTERIOR UK Ltd.Unit 6, Gravelly Industrial ParkBirminghamB24 8HZGREAT BRITAINTel: +44-121-328-7667Fax: [email protected]

POLYTEC INTERIOR SPAIN

POLYTEC INTERIOR Zaragoza S.L.Poligono LogisticoCtra. De Logrono, km 27,5E-50639 Figueruelas (Zaragoza)SPAINTel: +34-976-656-285Fax: [email protected]

POLYTEC INTERIOR POLAND

POLYTEC INTERIOR Polska Sp.z.o.o.UI. Piaskowa 120PL-97 200 Tomaszow / MazowieckiPOLANDTel: +48-44-7233-960Fax: [email protected]

POLYTEC INTERIOR SOUTH AFRICA

POLYTEC INTERIOR South Africa (Pty) Ltd.P.O. Box 911-456Rosslyn0200 South AfricaSOUTH AFRICATel: +27-12541-1878Fax: [email protected]

POLYTEC FOR

POLYTEC FOR Car Styling GmbH & Co KGLinzer Strasse 50 A-4063 HörschingAUSTRIATel: +43-7221-701-0Fax: [email protected]

POLYTEC FOHA

POLYTEC FOHA Corp. 75 Shields Court, Unit 1Markham Ontario L3R 9T4CANADATel: +1-905-940-5006-0Fax: [email protected]

POLYTEC FOHA Inc. 7020 Murtham Ave. Warren, MI 48092 USATel: +1-586-978-9386Fax: [email protected]

POLYTEC HOLDEN

POLYTEC HOLDEN Ltd. Porthouse Industrial EstateBromyard Herefordshire HR7 4NSGREAT BRITAINTel: +44-1885-483-000Fax: [email protected]

POLYTEC AVO

POLYTEC AVO NVMetropoolstraat 8B-2900 SchotenBELGIUMTel: +32-3-680-18-20Fax: [email protected]

04.0

5.0,

5D.0

,5E

POLYTEC COMPOSITES ITALIA

POLYTEC COMPOSITES ITALIA Srl.Corso Milano 3I-12084 Mondovi ( Cuneo )ITALYTel: +39-0174-562-511Fax: [email protected]

POLYTEC COMPOSITES SWEDEN

POLYTEC COMPOSITES SWEDEN ABBox 302S-34126 LjungbySWEDENTel: +46-372-67-500Fax: [email protected]

SVENSK KOMPOSITUTVECKLING

SVENSK KOMPOSITUTVECKLING ABVästgötavägen 30S-451 34 UddevallaSWEDENTel: +46-522-657760Fax: [email protected]

POLYTEC ELASTOFORM

POLYTEC ELASTOFORM GmbH & Co KGKiesstrasse 12A-4614 MarchtrenkAUSTRIATel: +43-7243-53451Fax: [email protected]

POLYTEC THELEN

POLYTEC THELEN GmbHAm Vorort 24D-44894 BochumGERMANYTel: +49-234-89368-0Fax: [email protected]

POLYTEC EMC

POLYTEC EMC Eng. GmbH & Co KGKiesstrasse 12A-4614 MarchtrenkAUSTRIATel: +43-7243-53952Fax: [email protected]

POLYTEC GROUP

POLYTEC HOLDING AG HeadquarterLinzer Strasse 50 A-4063 HörschingAUSTRIATel: +43-7221-701-0Fax: [email protected]

www.polytec-group.com

3

22 LOCATIONS WORLDWIDE22 locations; average number of employees: 2 840; Turnover EUR 392,1 Mio., of which 95,8 % in automobile supply and 4,2 % in industrial applications.

POLYTEC GROUP CUSTOMERS Passenger Cars: BMW Group: BMW, Mini, Rolls-Royce • Daimler Chrysler Group: Daimler Chrysler, Dodge, Hyundai, Jeep, NedCar, Mercedes McLaren, Mitsubishi • GM Group: Buick, Cadillac, Chevrolet, Corvette, GMC, GM, Holden, HSV, Hummer, Isuzu, Opel, Pontiac, Saab, Subaru, Suzuki, Vauxhall • Fiat Group: Alfa Romeo, Ferrari, Fiat, Lancia • Ford Group: Aston Martin, Ford, FPV, Land Rover, Lincoln, Mazda, Mercury, Volvo Car, Jaguar • Renault, Nissan • PSA: Peugeot-Citroen • Toyota, Daihatsu, Lexus • VW Group: Audi, Bentley, Seat, Skoda, VW • Honda, London Taxis, Lotus, Pininfarina, Porsche, Think

Trucks & Commercial Vehicles: Daimler Chrysler Trucks, Iveco, MAN, Paccar, Scania, Volvo Trucks

TIER 1 customers: Bing, Decoma, Delphi, Edscha, Faurecia, Heywinkel, IBS, Johnson Controls, Kloth Senking, Lear Corporation, Leoni, Magna Steyr, Peguform, Pierburg, Seeber, Siemens VDO, ThyssenKrupp

Other Customers: Caterpillar, CNH, Dynapac, Reformwerke, Swoboda

The whole technology and product range of the POLYTEC GROUP – from the development to the production – is the result of a consequent quality management. Certifications like VDA 6.1, ISO 9001, QS 9001, ISO TS 16949: 2002 and ISO 14001 have become standard in the POLYTEC GROUP.

Letter of the Chairman of the Supervisory BoardLetter of the CEOThe shareholder structureThe divisions and subsidiariesThe core competence: plastic technologiesThe strategy The genetic codeManagement report and consolidated management report POLYTEC HOLDING AGConsolidated notes for the financial year 2004, of POLYTEC HOLDING AG, HörschingAuditor’s Report

CONTENTS 04 .............. 05 ..............06 ..............08 .............. 10 .............. 12 .............. 14 .............. 16 .............. 21 .............. 39 ..............

PASSION CREATES INNOVATION

TO TURN GROWTH INTO SUCESS – TO FURTHER FUELL SUCESS BY GROWTH The year 2004 was another important milestone in the history of POLYTEC, which main characteristic was growth, on its way to become a globally pre-sent automotive supplier, who according to our goals and visions envisages a sales volume of 1 billion EUR.

By integrating „Findlay Industries Europe“, today well known as POLYTEC IN-TERIOR, consolidated sales of POLYTEC GROUP of the year 2003 of 265,5 Mio. EUR increased to 392,1 Mio. EUR in the year 2004, which means a growth rate of 48 %. However the integration of the Findlay-Group was only accomplished July 1st 2004 so economically POLYTEC GROUP at the end of the fiscal year 2004 represents a sales volume of 500 Mio. EUR, which is made possible by 3.500 employees. By organic growth, which is based on the start of production of new important projects, the sales in the year 2005 will increase to 530,0 Mio. EUR according to the plans of the group. Taking this sales figure into consideration group sales will have grown more than six times compared to the year 2000.

Also the development of the results was satisfactory for POLYTEC GROUP. An operating income (EBITA) of 27,77 Mio. EUR was accomplished, which means a growth of 30,5 % compared to the previous year. Because of extraordinary impairment of goodwill EBIT and EBT have dropped slightly, but this should not qualify the successful year POLYTEC can look back on. The average work-force was 2.840 during the year. POLYTEC manufactured in 22 production sites worldwide.

A balance sheet that can help as a long-term protection against crisis is at least as important as P&L results for POLYTEC. With a clearly improved equity ratio during the fiscal year 2004 POLYTEC is well prepared for the challenges of the market as well as for further acquisitions, which are monitored con-stantly. The equity ratio of POLYEC, which rose to 32,9 % of balance sheet to-tal in 2004 (compared to 21,5 % in 2003) enables the group to appear on the market accordingly, as today it is increasingly complicated for an automotive supplier to raise the necessary funds for financing bigger projects.

The short- and medium-term analysis of the market however also shows that the next years, especially 2005, will not be easy for POLYTEC. The still pre-vailing economic downturn, overcapacities at our customers leading to high cost-pressure on suppliers as well as increasing raw material prices are pro-blems that POLYTEC cannot completely avoid. In total a big challenge which I, believing in the innovative capacity, the total commitment and the strategic potential of the company, look at with optimism.

Since the founding of POLYTEC GROUP in the year 1986 growth was THE extraordinary characteristic of this group of companies. With prudence but consequently the spectrum of strategically important markets, customers, technologies and products, which are served by POLYTEC, was enlarged. Standstill means regress in a world becoming ever more dynamic. Especially

FRIEDRICH HUEMER, 47, lives in Wallern, Upper Austria, is married and has one son. He studied at the Poly-technic for Chemical Production Technology and finished his studies there in 1976. Following a range of functions in national and international companies, the engineer Friedrich Huemer, together with his wife and a partner, foun-ded the POLYTEC GROUP in 1986, which he currently heads as co-owner and CEO and represents the driving force in terms of the strategy and acquisitions of the group. The successfully run group currently includes 22 locations in Europe, USA, Canada und South Africa.

thereof the route for which POLYTEC in the past was prominent must be followed further. Growth, mainly by acquisitions, for POLYTEC never was an end in itself, but always focused on consolidating or improving the long-term position of POLYTEC on the market. In this I see my very personal responsi-bility as a manager. It is a task which I always liked to tackle and also today and tomorrow will with all my knowledge, my experience and the help of the other management. For me it is extremely important that I control this company not only as the CEO, but that I also have a long-term commitment as a core shareholder in this group. This aggregation of management- and shareholder-interest can assure that conflicting goals between these to sta-keholders can be widely avoided.

The track for the further development of POLYTEC GROUP must be set today to enable further growth of what was accomplished already, so that also in the future „motion“ can be the principle of POLYTEC GROUP.

Sincere thanks to all our customers, business partners, suppliers and of course my employees, for the confidence in our group and for the work performed, which for me sets the basis for a positive future development.

Friedrich HuemerChairman and CEOPOLYTEC HOLDING AG

First and foremost, we must express our thanks to both our customers and suppliers for the great trust they have shown in us and which we hope will be proved to be well founded. This would not have been possible without the daily commitment of the around 3.500 POLYTEC employees worldwide, who through their support of our business goals and their determination to continuously prove themselves worthy of the “best-in-class” distinction, have shown that they really are the most valuable asset of POLYTEC. They deserve our most special thanks. It is precisely due to our trust in this strength that we can look to the future in 2005 with optimism, in spite of difficult econo-mic conditions.

Dr. Yves DudliChairman of the supervisory boardPOLYTEC Holding AG

THE SUPERVISORY BOARD OF POLYTEC HOLDING AG: Dr. Yves Dudli Chairman of the Supervisory BoardPartner of Capvis Equity Partners AG Engineer Gerald AichingerDeputy ChairmanChairman of Supervisory Board of Artax AG

Ulrike HuemerMember of BoardDivision Head Polytec Industrial Division

Dr. Alexander KrebsMember of BoardPartner of Capvis Equity Partners AG

YVES DUDLI, 50 years old, lives in Zürich, Switzerland, is married with two children. He studied Economics in Vienna, where he did his doctorate. He received an MBA in Leuven, Belgium and is a partner at CapVis Equity Partners. Dr. Yves Dudli has been actively involved in Private Equity since 1995. His broad range of experience was the result of the structuring and financing of MBOs. Pior to this he was actively involved in Corporate Finance/ Investment Banking at Citibank and the Schweizerischen Bankverein and SBC Warburg and his last position was that of the Head of Investment Banking Austria.

DEAR LADIES AND GENTLEMEN!

Once again, the POLYTEC GROUP can look back on an eventful year in 2004. Without a doubt, the aquisition of the European division of the US-American Findlay-Group (Findlay-Europe) was the most significant event of the past business year. The newly-acquired business group, with its base in Geretsried, Bavaria and specialising in interior modules such as door panels, headliners and trunk panels based on natural fibres, is a long-standing and well-recog-nised partner enterprise in the automobile industry, first and foremost in connection with the German manufacturer, BMW.

The take-over of Findlay-Europe was initiated by Capvis Fund II, with Capvis Equity Partners AG, Zurich acting as advisors. The synergy potential of this investment with POLYTEC GROUP, in which our Capvis Fund I has been inves-ted since 2000, was quickly recognised as being of great importance. For this reason, the necessary steps for the merger with POLYTEC were taken imme-diately following the takeover and together with our partner shareholders at POLYTEC, this was rapidly implemented.The financial strength of POLYTEC, combined with the product competence of Findlay-Europe, now integrated into the Interior Automotive Division, puts POLYTEC into the position of being able to present itself as a leading provider of complete automotive solutions. POLYTEC would like to offer a medium-scale alternative to the so-called mega-suppliers.

POLYTEC today represents a business group with a turnover of around 500 million Euros and with an impressive growth in 2004 that is not only due to this major acquisition. With an organic growth of approximately 6 %, the ‘old’ POLYTEC was able to produce very good results, even in the face of the continuing difficult overall economic developments in the past economic year.

Of course, the development of POLYTEC is not completed with the strate-gies coordinated by the management and board of directors. In addition to long-term customer satisfaction based on organic growth, acquisitions will continue to be a core element of the strategic development of POLYTEC, with the goal of achieving a turnover of approximately 1 billion Euros, as set out in the long-term plans of the group. Acquisitions alone, however, in no way serve to merely ‘buy’ added turnover but must rather bring a real increase in value for the operative business and thereby also for the shareholders, as has been the case in the past. Since its formation in 1986, POLYTEC has shown that this ambitious goal can be achieved, and therefore in the future we will not deviate from this path.

Due to the strong growth in the past year, POLYTEC has also achieved the size and the earning potential required for it to take the step of becoming a public company and thereby ensures the continuation of this ambitious growth trend into the future. For this reason, the board of directors will incorporate this attractive option within the framework of evaluation of further strategic steps in the development of POLYTEC.

LETTER OF THE CHAIRMAN OF THE SUPERVISORY BOARD LETTER OF THE CEO

6 7

1986

1990

1993

1995

1995

1995

1995

1996

1997

1997

2001

2001

2001

2002

2002

2003

2003

2004

2004

2004

HU

EMER

BET

EILI

GU

NG

S G

mbH

CA

PVIS

FU

ND

I

CA

PVIS

FU

ND

II

INVE

ST U

nter

nehm

ensb

etei

ligun

gs A

G

FRIE

DR

ICH

HU

EMER

(IM

C)

ULR

IKE

HU

EMER

Gm

bH

WIE

SLEI

TNER

HO

F Pr

ivat

stif

tung

POLY

TEC

Man

agem

ent

POLY

TEC

IM

MO

BIL

IEN

GR

UPP

E

POLY

TEC

HO

LDIN

G A

G

32,5

%

53,2

%

13,5

%

17,7

%

15,6

%

100

%

2,6

%

37,6

%

27,3

%

MOVEMENT AS PRINCIPLEA Tradition of innovation. The aim of the POLYTEC GROUP is to be a global development partner for all aspects of engineered plastic- and natural fibre parts for industrial and automotive applications. As a certified partner, the POLYTEC GROUP manages the supply of modules and systems to automobile manufacturers and system suppliers and makes every effort to provide the tools for more motion. POLYTEC meets this challenge by deploying a wide va-riety of technologies with the use of all the synergies within the group across an activity spectrum, which encompasses the complete process chain.

THE SHAREHOLDER STRUCTURECapvis Fund I + II 64,9 %. The financial partner with the right understan-ding of what the POLYTEC GROUP does .Huemer Beteiligungs GmbH 32,5 %. The POLYTEC founding family and its partners. Strategy is of primary importance and successful implementation is guaranteed. The future is clearly set out and customers and employees are of vital importance. Social responsibility is a main focus in daily business operations. By taking over 2,6 % of the shares the management proved its confidence in the “own“ company.

THE HISTORYIn 1986, Friedrich Huemer founded POLYTEC ELASTOFORM GmbH, the first company in the present-day POLYTEC GROUP. The company was founded with the goal of producing industrial parts from PUR elastomers. This was the starting signal for the development of a global enterprise. The expansion was driven by internal growth, active acquisitions of companies in the fields of plastics technology, “industrial plastic parts” and “automotive plastic parts”. In 2000, Capvis (C.I.) Limited, took over two thirds of the shares. One third was transferred to the Huemer Holding Company by the founders of the company. Today, the POLYTEC GROUP is part of a renowned network of businesses operating at a high technical level, which includes 22 locations in Europe, the USA, Canada and South Africa.

THE FAMILY: POLYTEC is backed by a strong family. As a personified and tangible enterprise, it is important for us to stand apart from the rest. In concrete terms, this means recognising potential faster, actively structuring growth and the more efficient use of synergies. As a family, it is in our blood to think in terms of networks and act accordingly. Being nimble, the ability to work as a team, lean management, shorter decision-making paths and flat hierarchies are characteristics of our organisation. The shared sense of enjoyment drives us forward to continue our history of success in a persistent way. Our aim is to further develop the value of POLYTEC and be an attractive partner in the world market. The intense partnership with our customers and harmonious cooperation of all our family members make our solutions faster, more efficient and more personal.

POLYTEC ELASTOFORM, Austria

POLYTEC EMC, Austria

POLYTEC ROTOFORM, Austria

POLYTEC THELEN, Germany

POLYTEC FOR, Austria

POLYTEC FOHA, Canada

RATIPUR, Hungary

POLYTEC RENTROP, Germany

POLYTEC HOLDEN, Great Britain

POLYTEC FOHA, USA

POLYTEC COMPOSITES, Sweden

POLYTEC COMPOSITES, Italy

POLYTEC AVO, Belgium

POLYTEC THERMOPLAST, Germany

POLYTEC RIESSELMANN, Germany

POLYTEC AUTOMOTIVE, Germany

SVENSK KOMPOSITUTVECKLING, Sweden

LOHNER LACKIERWERK, Germany

POLYTEC PLASTICS, Germany

POLYTEC INTERIOR, Germany (4 plants),Great Britain, Spain, Poland, South Africa

THE SHAREHOLDER STRUCTURE

Mar

chtr

enk,

Aus

tria

Hör

schi

ng, A

ustr

ia

Jers

ey, G

reat

Bri

tain

Jers

ey, G

reat

Bri

tain

Mar

chtr

enk,

Aus

tria

Aus

tria

, Ger

man

y, B

elgi

um,

Swed

en, S

pain

, Pol

and

Shareholder structure

8 9

High Volume Division 62,1 %

Industrial Division 4,2 %

Low & Medium Volume Division 17,1 %

Composites Division 16,6 %

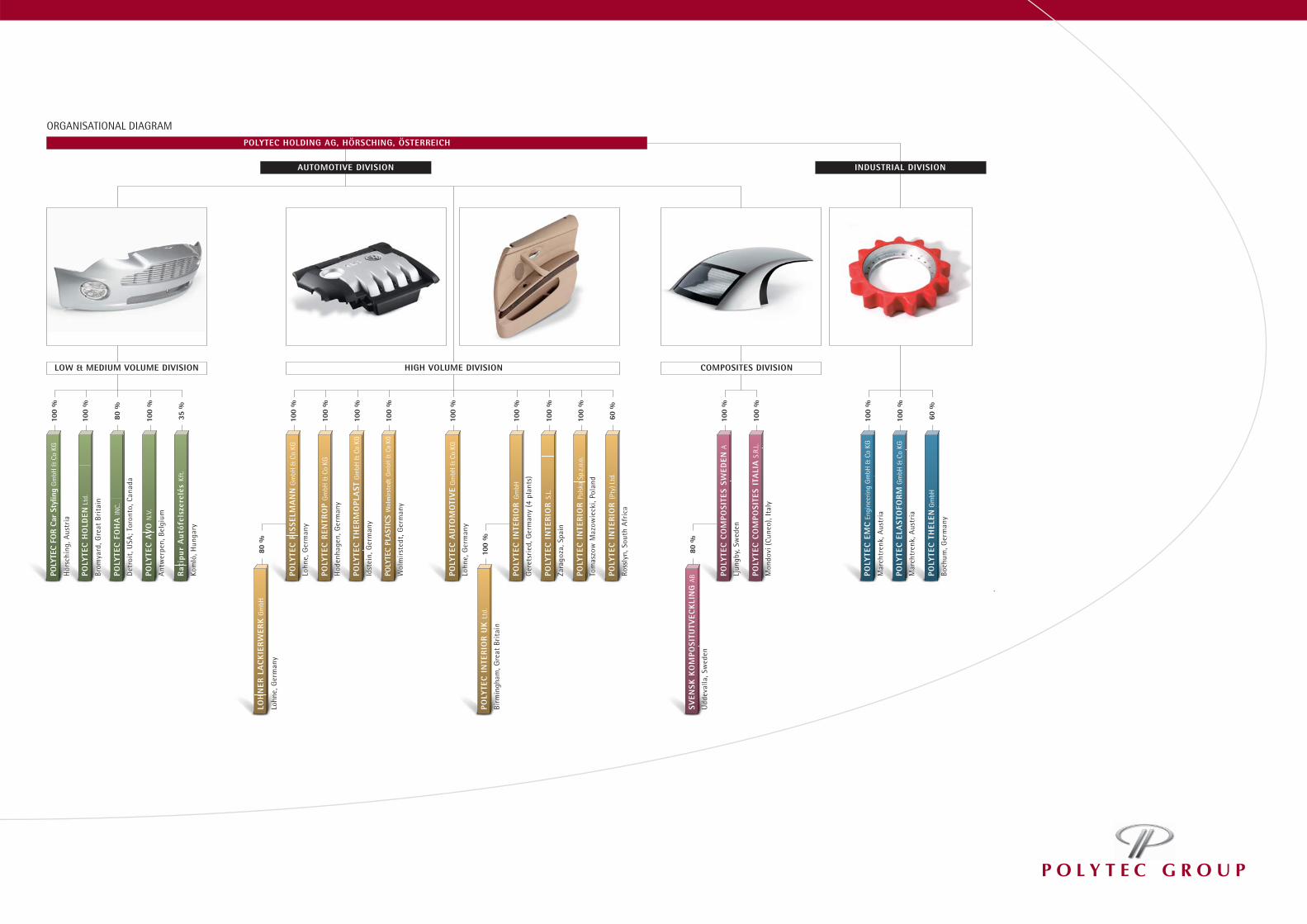

SUBSIDIARIES AND HOLDINGSOur goal is to work towards synergies and use them to their full advan-tage on a daily basis, in the interest of each individual customer and project. Nevertheless, our subsidiaries still serve their customers and markets inde-pendently. Information flows from the respective division to the HOLDING Organisation and from there back to the operational units. Communication is one factor that guarantees success, as is mutual support in order to find the optimal process for the customer. The decisive factor is not where POLYTEC produces something, but far more the correct process chain and technology, prices of parts that are in line with market requirements and quality and reliability that satisfy the customer’s expectations.

HIGH VOLUME DIVISIONThe HIGH VOLUME DIVISION represents itself to the customers of the auto-motive industry though the POLYTEC AUTOMOTIVE GMBH & Co KG, based in Lohne and Geretsried, Germany. At these locations, parts for the interior, trunk and engine compartment area as well as functional parts are acquired and developed. Products of plastics and natural fibre composites are made in 12 production plants of the POLYTEC HIGH VOLUME DIVISION. Our range of activities comprises the complete process chain, from the concept phase, development and design, production of prototypes and test tools to pre-se-ries and series production including logistics and just-in-sequence delivery. This division comprises the business units injection moulding and natural fibre composites.

LOW & MEDIUM VOLUME DIVISIONThe LOW & MEDIUM VOLUME DIVISION produces plastic and metal parts for interior and exterior applications, which are primarily developed for “Genuine Accessory Parts” together with the automobile industry. Supply can be made from of any of the six locations of the LOW & MEDIUM VOLUME DIVISION. The activity range offered includes: design, CAD engineering, model and tool making, production and logistics. If required, parts can be painted in body colour. Exterior parts for cars produced in the low and medium volume series is an additional area of our product range. These parts are supplied to the assembly lines of the car manufacturers.

COMPOSITES DIVISION The COMPOSITES DIVISION develops and produces composite parts in dif-ferent technologies at three locations. Exterior, functional and structural parts are used by customers in the passenger car and heavy truck production sectors. All parts are delivered to the assembly lines of the vehicle manufac-turers. The production of carbon fibre parts is a new and interesting field for the COMPOSITES DIVISION. Sports and luxury cars offer especially interesting future prospects for this application.

INDUSTRIAL DIVISIONThe INDUSTRIAL DIVISION with its 2 locations was the stepping stone which brought the founder family to the Automobile Industry. In the INDUSTRIAL DIVISION elastomeres and other plastics for industrial use are formed through moulding, casting and spraying. The activitiy spectrum is rounded off by POLYTEC EMC which is renowned worldwide for the manufacturing of multi-component, low pressure machines for the processing of liquid resins.

THE TURNOVER IN 2004

CONTINUITY: However the pace may increase, there are always values that remain important: Reliability, loy-alty and responsibility. We take these values seriously in every respect. Each one of our customers can rely on us. Continuity – this is what we understand by close customer relations. Continuity through actively thinking ahead and showing initiative. Flexibility is our trump card in a highly competitive market. We can provide solutions to almost all of our cutomers’ problems. Why? Because our teams react quickly and efficiently. There are no long de-cision-making processes, but rather rapid solutions. This high level of flexibility in the way we think and deal with problems is a living philosophy in our divisions – giving the customer the advantage.

THE DIVIS IONS AND SUBSIDIARIES

Photos: Copyright GM, Porsche, Mercedes; Austria

High Volume Division 62.1 %

Industrial Division 4.2 %

Low & Medium Volume Division 17.1 %

Composites Division 16.6 %

POLYTEC HOLDING AG, HÖRSCHING, ÖSTERREICH

AUTOMOTIVE DIVISION

LOW & MEDIUM VOLUME DIVISION COMPOSITES DIVISION

POLY

TEC

FOR

Car

Styl

ing

Gm

bH &

Co

KG

POLY

TEC

HO

LDEN

Ltd

.

POLY

TEC

FO

HA

INC.

POLY

TEC

AV

O N

.V.

Rat

ipur

Aut

ófel

szer

elés

Kft

.

POLY

TEC

CO

MPO

SITE

S IT

ALI

A S

.R.L

.

POLY

TEC

CO

MPO

SITE

S SW

EDEN

A

B

SVEN

SK K

OM

POSI

TUTV

ECK

LIN

G A

B

100

%

100

%

80 %

100

%

35 %

HIGH VOLUME DIVISION

POLY

TEC

REN

TRO

P G

mbH

& C

o KG

100

%

POLY

TEC

TH

ERM

OPL

AST

Gm

bH &

Co

KG10

0 %

POLY

TEC

PLAS

TICS

Wol

mirs

tedt

Gm

bH &

Co

KG10

0 %

POLY

TEC

AU

TOM

OTI

VE

Gm

bH &

Co

KG10

0 %

POLY

TEC

IN

TER

IOR

Gm

bH10

0 %

POLY

TEC

IN

TER

IOR

S.L

.10

0 %

POLY

TEC

IN

TER

IOR

Pol

ska

Sp.z

.o.o

.10

0 %

POLY

TEC

IN

TER

IOR

(Pty

) Ltd

.60

%

POLY

TEC

RIS

SELM

AN

N G

mbH

& C

o KG

100

%

LOH

NER

LA

CK

IER

WER

K G

mbH

80 %

POLY

TEC

IN

TER

IOR

UK

Ltd

.10

0 %

100

%

100

%

INDUSTRIAL DIVISION

POLY

TEC

ELA

STO

FOR

M G

mbH

& C

o KG

POLY

TEC

EM

C E

ngin

eerin

g G

mbH

& C

o KG

POLY

TEC

TH

ELEN

Gm

bH

100

%

100

%

60 %

80 %

Hör

schi

ng, A

ustr

ia

Brom

yard

, Gre

at B

rita

in

Det

roit

, USA

; To

ront

o, C

anad

a

Ant

wer

pen,

Bel

gium

Kom

ló, H

unga

ry

Mon

dovi

(Cu

neo)

, Ita

ly

Ljun

gby,

Sw

eden

B

Udd

eval

la, S

wed

en

Hod

enha

gen,

Ger

man

y

Idst

ein,

Ger

man

y

Wol

mir

sted

t, G

erm

any

Lohn

e, G

erm

any

Ger

etsr

ied,

Ger

man

y (4

pla

nts)

Zara

goza

, Spa

in

Tom

aszo

w M

azow

ieck

i, Po

land

Ross

lyn,

Sou

th A

fric

a

Lohn

e, G

erm

any

Lohn

e, G

erm

any

Birm

ingh

am, G

reat

Bri

tain

Mar

chtr

enk,

Aus

tria

Mar

chtr

enk,

Aus

tria

Boch

um, G

erm

any

ORGANISATIONAL DIAGRAM

10 11

• trunk organizers • luggage trunk trims • lock covers • cargo trays • trunk lid locks and lid pillar trims ADVANCED COMPOSITE PARTS: parts for the automobile- and aviation industry, mobile communication, robotics, medical technology and military sectors METAL PARTS: entrance sills • light guards • dog- and cargo guards • styling bars • front and rear bumper parts • side bars ENGINE PARTS: oil scrapers • cylinder head covers • engine covers • gearing control boxes • toothed belt protection / closing parts • electronic boxes • cable channels • battery trays • under body & gear box shields TRUCK PARTS: valve covers • oil pans • cabins and cab corners • complete cabin roofs • side deflectors • A-, B-, C-, D-spoilers • bumpers • front grills • fenders

OFF-ROAD PARTS:OFF-ROAD PARTS: front guards • running boards • fog lamp bezels • skid plates • side claddings • fender extensions • wind deflectors • bumper protections EXTERIOR PARTS: front and rear bumpers • front grills • grill surrounds • number plate surrounds • side sills • fender extensions • spoi-lers • side mouldings • mud flaps • bumper protections • gas caps • fuel tank shields • hard tops • tonneau covers • trunk lid parts INTERIOR PARTS: centre consoles • arm rests • tray mats • sun glass holders • mobile phone holders • glove boxes • attachment parts for instrument pa-nels • seat back panels • door panels • door pockets • headliners • armrests and skibag units • clutch pedals • air vents • trunk trim covers and parcel shelves TRUNK COMPARTMENT PARTS: window trim frames / tailgate trims

A KNOW-HOW COMPANY: In terms of taking over technologies, building machines and training employ-ees, we can be compared to others. Regarding being a leader in terms of technology, the situation becomes more complex. For us the magic formula for the future is competence. We invest our full passion and zeal in this intel-lectual and creative performance. Expertise is the most valuable resource. For our engineers, the job is a way of life. Finding solutions is an obsession for them and they are driven by an inner desire to develop improved solutions. At POLYTEC, the person is the focus and takes over responsibility.

STYL

ING

, DES

IGN

• CAD DEVELOPMENT • ENGINEERING

•PRO

TOTYPING

•

MODELMAKING•TOOLMAKIN

G•

PUR

FOA

MIN

GT E

CHN

OLO

GY•

PUR RIGID • PUR SEMI-RIGID • PURRIM

•PU

RR

- RIM

•PU

RS-RIM

•

BLOWMOULDING•DCPD•INJECTIO

NM

OULD

ING

•2K

INJE

CTIO

NM

OULD

ING

• MULTI COMPONENT INJECTION MOULDING•

TEXTIL EI N

JECTION

MO

ULDING•

GASASSISTEDINJECTIONMOULDING•WIT

•M

UCEL

L•

SMC

•BM

C•

GM

T•

LFT

•VA

RI • RTM• PRIMING • PAINTING • PRINTING

•FLOCKIN

G•

1-CO

AT

AN

D2-CO

AT

PAINTING

•

METAL-ANDPREMIUMSTEELPROCESSING•PURLO

WPR

ESSU

REPR

OC

ESS

•PU

RCO

ATIN

GW

ITH

ELASTO

MERES • PUR CASTING OF ELASTOMERES •PUR

SPRAYING

OF

ELAST O

MERES

•EN

GIN

EERINGAND

ASSEMBLYOFMULTI-COMPONENTLOWPRESSUREM

ACHINES

•PR

OD

UCT

ION

OF

TRIM

PART

S(T

HER

MOP

LAST

ICAND DUROPLASTIC NATURAL FIBRE COMPOSITE MATERIALS) •

INMO

ULD

GRA

ININ

G•

BAC

KSID

EFO

AMING

•LEATHERPROCESSING•LAMINATING•JOINING

THE CORE COMPETENCE: PLASTIC TECHNOLOGIES

12 13

86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04

550

500

450

400

350

300

250

200

150

100

50

0

GROWTH THROUGH DEVELOPMENTEnhancement of group capabilities is the central strategy – through selective acquisition into new fields of production possibilities with already existing and related technologies and also to be represented in important geographi-cal supply areas. The vision of the POLYTEC GROUP is to be a leading group in the plastics processing industry with its main focus on automotive supply. Its technologies, products, locations and stringent cost management make the POLYTEC GROUP a very attractive Tier 1 und Tier 2 supplier to our costumers. Organic growth and acquisitions will eventually enable the group as an auto-nomous company to achieve its target of total sales of one billion EUR and to be an interesting partner for larger strategic alliances in the future.

THE POLYTEC GROUP SEES ITS MISSION THROUGH THE FOLLOWING FACTORS: Living PartnershipThe mission of the POLYTEC GROUP is to supply high-quality plastic parts to customers within a living partnership and also to provide professional know-how and expertise for the development of these parts.

Organic DevelopmentAccording to the international company structure and the strategic aims, the POLYTEC GROUP will develop further towards the “Global Market” – through organic growth as well as through the aquisition of companies within the core competences.

Technology-leadershipIn the field of plastics, the technology leadership has to be positioned on a broad basis, in order to offer optimal solutions for the customers. The certi-fied, integrated management system of the POLYTEC GROUP serves as a basis for this.

ExpertiseThe core competence of the POLYTEC GROUP is the wide variety of technolo-gies for the production of plastic parts, this applies primarily to the automo-tive division. The group is using this core competence as a problem-solver to the advantage of the customers in order to reach interesting and innovative solutions with particular attention to feasibility, costs and quality.

PASSION CREATES INNOVATION: At POLYTEC, working means more than merely making a profit. Stand-ing one’s own is a way of life at POLYTEC – an essential part of one’s outlook. POLYTEC is a name with aspirations, overtaking the competition. Technology is interchangeable – people are not. The fire in our eyes, the unquenchable desire to be among the best. The fire of this passion is the pulse behind every production model, in every detail and in every respect to the customer. Success is only possible through the combined brainwork of each team. We are convinced of the fact that only people can make POLYTEC what it is and our products and our customer services unmistakeable. Passion creates Innovation! This is what we stand for!

SALES DEVELOPMENT

Turnover in million Euro

THE STRATEGY

14 15

86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04

5500

5000

4500

4000

3500

3000

2500

2000

1500

1000

500

0

PASSION CREATES INNOVATION The genetic code of the POLYTEC GROUP is reflected in the passion with which the company acts, inspiring its customers as well as itself, creating something new and improving what already exists.

THE CREED OF THE POLYTEC GROUP: Think passionately.Work passionately.Live passionately. Because: Ultimately, technologies are not the decisive factor – people are. People with passion, who express this through innovation, ideas, develop-ments and products for the prosperity of the POLYTEC GROUP and to the advantage of the customer.

The dedicated, qualified and loyal employees of the POLYTEC GROUP together with a determined management represent the value of the company and assure the way into the future. The skills and efforts of the employees have to be fully developed and utilised in order to underline and enhance the reputa-tion of the POLYTEC GROUP and also to improve our competitiveness in the market. A continuous improvement of the results of the activities should help to ensure the growth and the success of the group. The environment and the social responsibility are obligations, wherever the POLYTEC GROUP is active. The future of the POLYTEC GROUP is based on these values and on the search for possibilities to become even better.

There is an ethical responsibility in every job and every kind of business with respect and confidence on the one side and social value on the other. The aim of the POLYTEC GROUP is to create consistent values for customers, emp-loyees and shareholders. All contact with the public, the authorities, other organisations and the media, should reflect this social resposibility whilst complying with all the environmental and legal regulations.

SUCCESS STORY: The future is not the extension of the present, but rather the realisation of fantasy and inventiveness. This is the focus of our work. We are proud of the fact that we have an important role to play in the automotive industry. We have a responsibility to make an inspirational contribution to the development of the automotive industry, actively participating in the changes and enriching life. We are committed to making our slogan “Passion creates Innovation“ a living reality.

Average number of employees

EMPLOYEE DEVELOPMENT THE GENETIC CODE

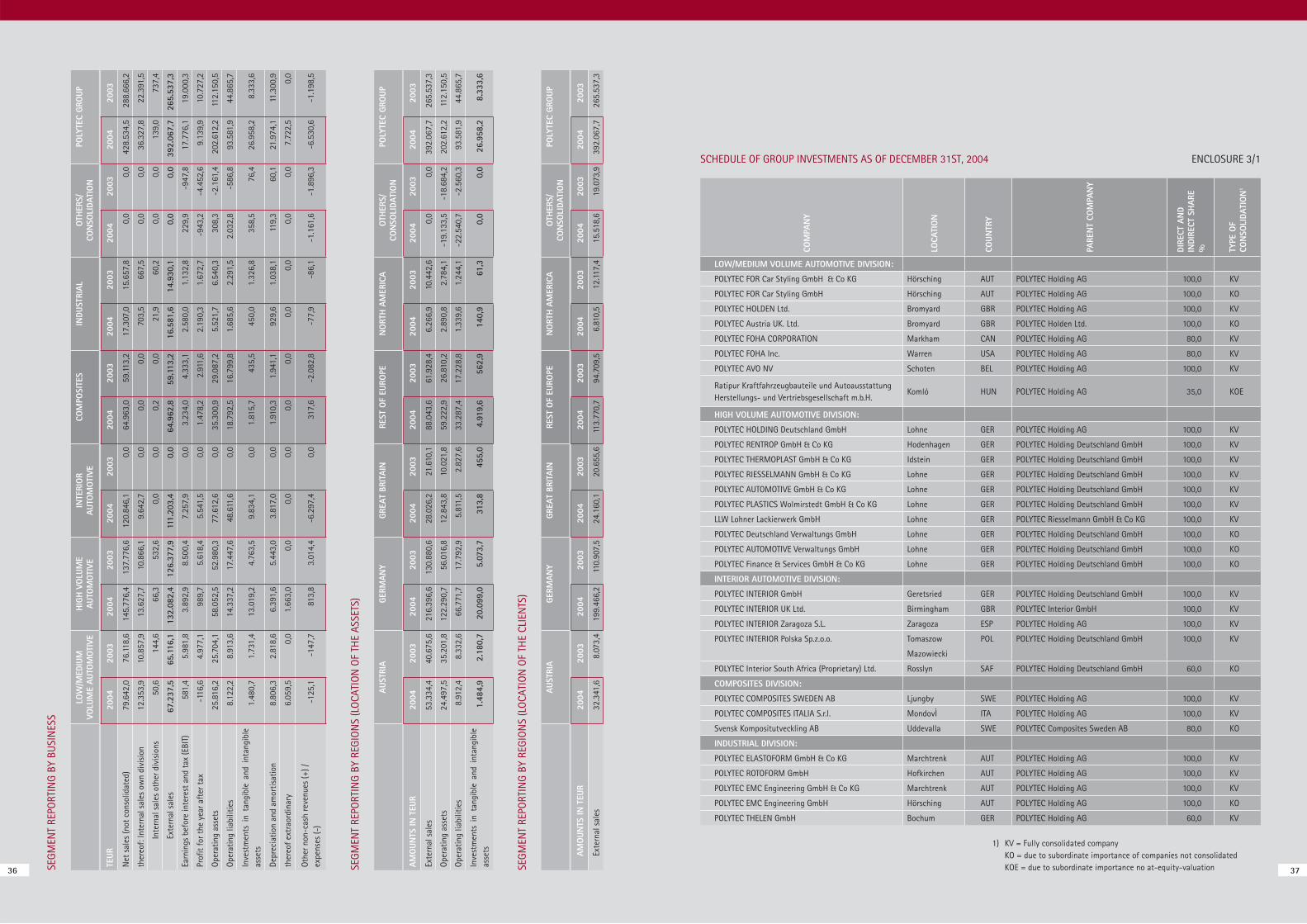

2. EXPECTED DEVELOPMENT OF THE GROUP:As a result of the acquisitions made during the financial year 2004 the imme-diate dependence of POLYTEC GROUP on the economic cycle of the automo-tive industry will increase. The success of single models, for which POLYTEC functions as a supplier, is also increasingly important for the success of the Group. The following table shows the development of the percentage portion of the single divisions as of group sales:

The budgeted net sales for the business year 2005 amount to EUR 530 m. This target is heavily based on booked business. A distinctive change in the custo-mer structure is a result of the newly acquired INTERIOR DIVISION. BMW will be the most important customer of the Group. The start of production of the door panels for the new „3 series“ class, which is scheduled to be launched in spring, will be a big challenge for the Group in 2005.

Despite the pleasing development in the previous year and the projected growth in net sales for 2005, the market situation can still be described as difficult. Even though the forecast of the automotive industrial society (VDA) for 2005 is cautiously optimistic, slightly lower sales figures are expected on the core market Germany despite an old average vehicle age of 93 months. The forecasted growth is therefore based on export chances.

In particular, Germany, the most important market for the Group, is characte-rised by overcapacities of the OEMs, which led to the problems at important customers as Opel and VW as reported by the media. Also the recent increase in quality problems of the OEMs can affect the suppliers negatively. Because of the strong bargaining power of the customer it will be almost impossible to pass on the full extent of the price increases, caused by the oil price situation, to the customer.

The generally dissatisfactory market situation in Germany and in Western Europe in general is only partially compensated for by the market growth in the CEE-countries and Asia. POLYTEC will not be able to disregard the big challenge China presents. Promising talks with potential Chinese partners are ongoing at this time.

Due to the facts stated above the net income of 2005 will increase in abso-lute numbers based on the increase in net sales, yet the margins will drop. Nevertheless based on the budgetary numbers, a result clearly above industry average is expected for 2005. The earnings report of the first quarter of 2005 gives rise to the hope that this goal will be met.

MANAGEMENT REPORT AND CONSOLIDATED MANAGEMENT REPORT POLYTEC HOLDING AG, HÖRSCHING, FOR THE FINANCIAL YEAR 2004

1. BUSINESS DEVELOPMENT AND STATE OF AFFAIRSThe finished business year marked an important milestone for POLYTEC GROUP towards becoming a global supplier of the automotive industry, for parts as well as modules. With the acquisition of the European business of the Findlay USA GROUP (now INTERIOR AUTOMOTIVE DIVISION) POLYTEC finally completed the step of becoming a supplier of complete modules. Products like door panels, headliners and trunk panels can almost be manufactured 100 % within the Group. Here the injection moulding businesses of the HIGH VOLUME AUTOMOTIVE DIVISION can function as a supplier for the INTERI-OR DIVISION. At the same time extensive new industrialisation and logistical competence (JIT/JIS) were brought into the Group through this acquisition, which can also be utilised by other divisions.

Due to the acquisitions, as well as organic growth, the consolidated net sa-les increased 47,7 % to EUR 392.1 m. This net sales figure, however, is only provisional though, since the first consolidation of the INTERIOR DIVISION dated July 1st Economically the POLYTEC GROUP represents today a net sales volume of EUR 500.0 m.

The operating income (EBITA) rose in comparison to the previous year by 30.5 % to EUR 27.8 m. Due to the extraordinary amortisation of goodwill included in the consolidated financial statements EBIT decreased slightly.

The financial situation of the Group as of 31.12.2004 has clearly shifted to-wards self-financing because of the capital increases carried out. Equity re-presents 32.9 % (Previous year: 21.5 %) of the balance sheet total. The small portion of outside financing of POLYTEC GROUP is also an important argu-ment in project acquisition, because the ability to pre-finance tooling- and project expenses can be a crucial competitive advantage.

3. RISK REPORTING:Within its business operations POLYTEC GROUP is exposed to a great number of risks that are directly connected to business activities. Risk management is an integral part of all business processes for POLYTEC. The required certifica-tions for an automotive supplier (e.g. TS ISO/16409:2002) also regulate this and are externally monitored by audits. Based on the organisation of POLYTEC risks are decentrally managed and controlled during the ongoing business processes; the management of financial risks is, however, primarily accom-plished by group headquarters. The following areas of risk can be identified:

Market risk: The industry of automotive supplies is known as a market with high competition and a fast rate of consolidation. Sales results depend heavily on the signing of new contracts, which is normally done 4 to 5 years ahead of start of production. In this phase of acquisition every supplier is exposed to a high level of competition. During serial production a supplier also depends on the sales of the vehicle for which parts are supplied, without being able to control its success. Furthermore the OEMs benchmark the suppliers after series production has started, which can cause price demands or in extreme cases, a loss of a contract. POLYTEC tries through a balanced mix of custo-mers and contracts to reduce its dependence on single contracts as much as possible.

Supply risk: Crucial risks include the fluctuation of raw material costs, which in the case of the POLYTEC GROUP as a plastic processing corporation de-pends heavily on the price of oil. On the supply side this problem is dealt with through long term supply contracts, on the customer side through adjust-ments in the disclosed calculations. Prices of raw materials and supplied parts are partly directly negotiated between our customer and the supplier.

Credit risk: Because of the customer structure, 90 % of net sales are achieved with OEMs or big system suppliers, POLYTEC is exposed to almost no credit risk at all. Overdue receivables are, however, critically pursued and contractual payment is ensured.

Financial risk: A big portion of the sales of POLYTEC GROUP is invoiced in EURO, therefore the Group is exposed to exchange rate risk only at a mini-mum. The purchase of supplies is partly made in the same currency as the later sales, so that the exchange rate risk is hedged naturally. The interest rate risk is managed by POLYTEC GROUP through a diversified portfolio of means of finance which bear fixed and variable interest rates. When needed such exchange and interest rate risk can be hedged by derivatives.

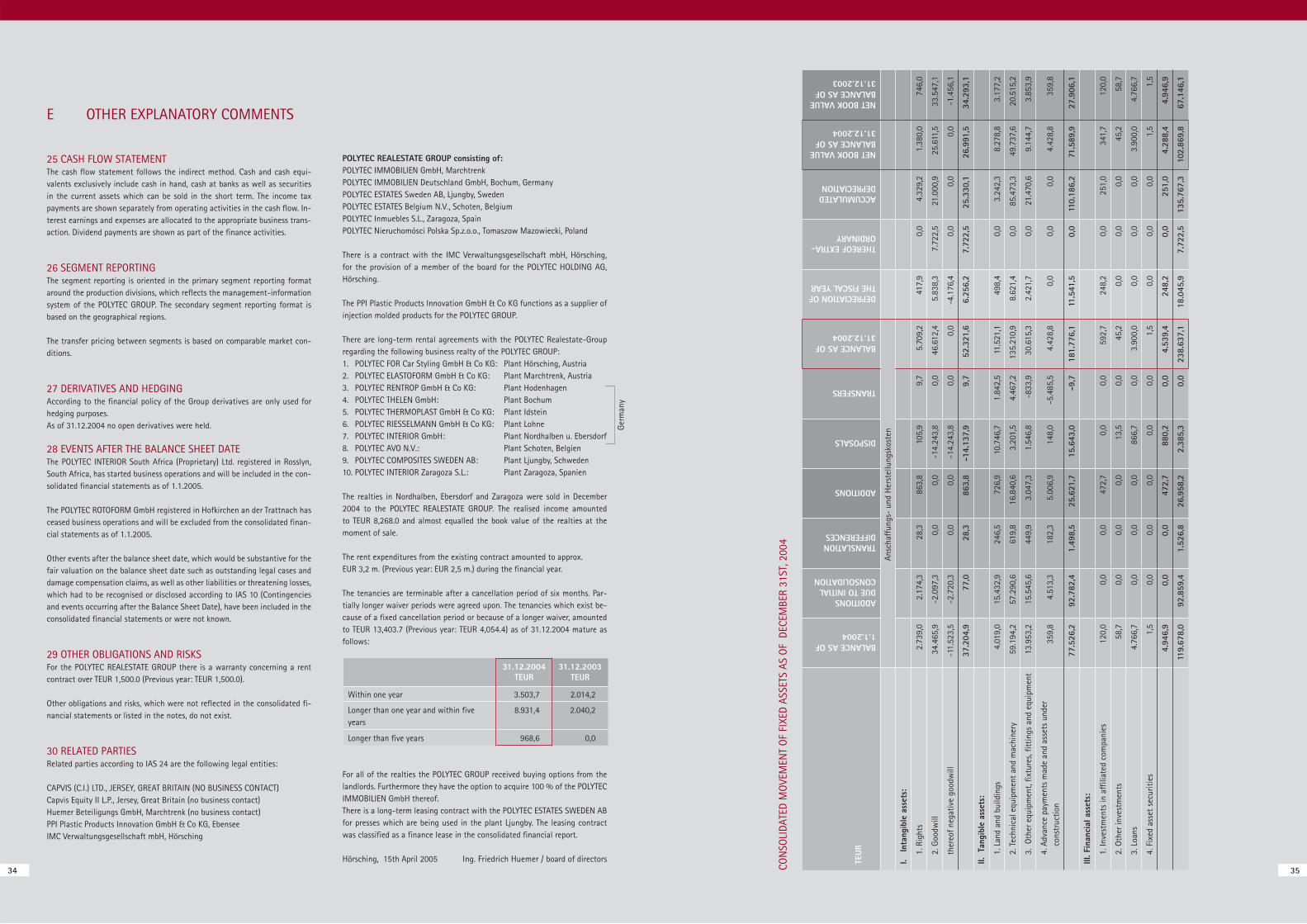

4. OTHER DETAILS:Regarding extraordinary events after the balance sheet date and the financial instruments used by the corporation we would refer you to the consolidated notes.

Research and development of the corporation relates, in particular, to ongoing improvements and the rationalisation of the existing production processes, technical improvements of vehicles in cooperation with our customers, as well as improvements of the environmental standard. The contract related development is charged to the client separately or paid of as part of the price per unit.

Hörsching, 15th April 2005

Ing. Friedrich Huemer / board of directors

16 17

DIVISION ACTUAL2001

ACTUAL2002

ACTUAL2003

ACTUAL2004

BUDGET2005

LOW & MEDIUM AUTOMOTIVE

41,7 31,7 24,5 17,1 12,9

HIGH VOLUMEAUTOMOTIVE

8,6 32,0 47,6 33,7 23,7

INTERIOR AUTO-MOTIVE DIVISION

— — — 28,4 48,2

COMPOSITES 38,9 28,3 22,3 16,6 12,4

INDUSTRIAL(NON AUTOMOTIVE)

10,8 8,0 5,6 4,2 2,8

WW

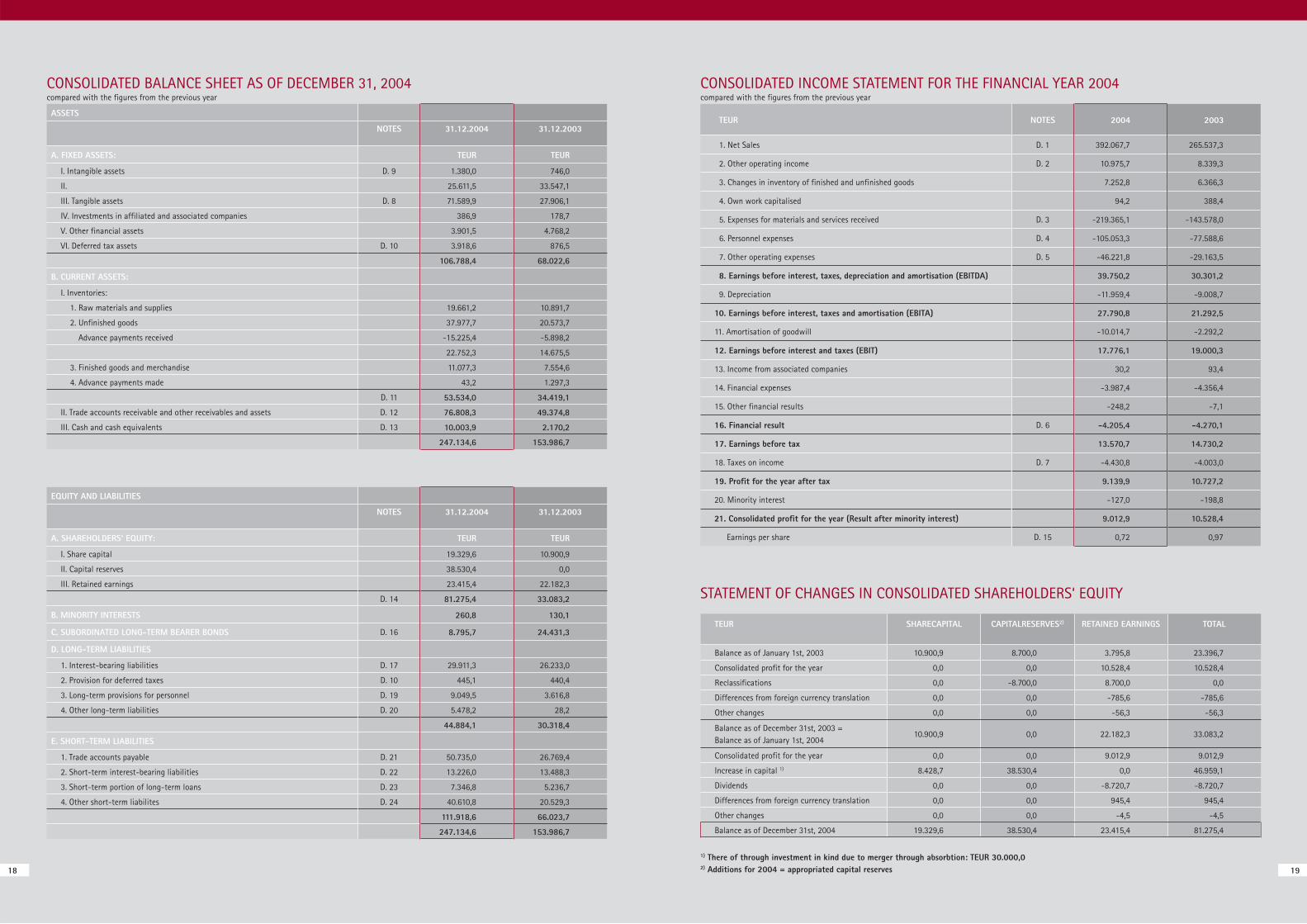

CONSOLIDATED BALANCE SHEET AS OF DECEMBER 31, 2004compared with the figures from the previous year

CONSOLIDATED INCOME STATEMENT FOR THE FINANCIAL YEAR 2004 compared with the figures from the previous year

STATEMENT OF CHANGES IN CONSOLIDATED SHAREHOLDERS‘ EQUITY

1) There of through investment in kind due to merger through absorbtion: TEUR 30.000,02) Additions for 2004 = appropriated capital reserves18 19

EQUITY AND LIABILITIES

NOTES 31.12.2004 31.12.2003

A. SHAREHOLDERS‘ EQUITY: TEUR TEUR

I. Share capital 19.329,6 10.900,9

II. Capital reserves 38.530,4 0,0

III. Retained earnings 23.415,4 22.182,3

D. 14 81.275,4 33.083,2

B. MINORITY INTERESTS 260,8 130,1

C. SUBORDINATED LONG-TERM BEARER BONDS D. 16 8.795,7 24.431,3

D. LONG-TERM LIABILITIES

1. Interest-bearing liabilities D. 17 29.911,3 26.233,0

2. Provision for deferred taxes D. 10 445,1 440,4

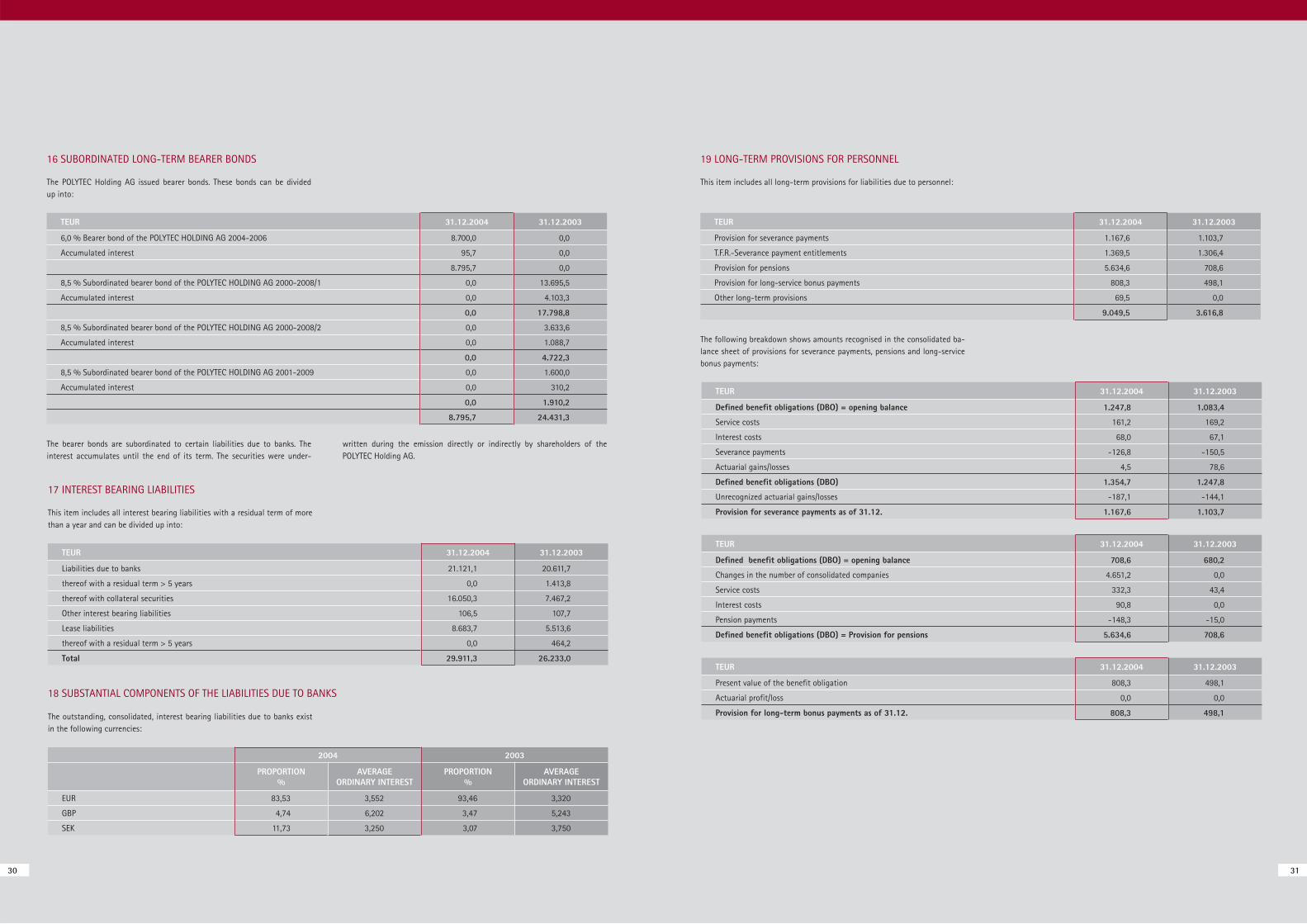

3. Long-term provisions for personnel D. 19 9.049,5 3.616,8

4. Other long-term liabilities D. 20 5.478,2 28,2

44.884,1 30.318,4

E. SHORT-TERM LIABILITIES

1. Trade accounts payable D. 21 50.735,0 26.769,4

2. Short-term interest-bearing liabilities D. 22 13.226,0 13.488,3

3. Short-term portion of long-term loans D. 23 7.346,8 5.236,7

4. Other short-term liabilites D. 24 40.610,8 20.529,3

111.918,6 66.023,7

247.134,6 153.986,7

ASSETS

NOTES 31.12.2004 31.12.2003

A. FIXED ASSETS: TEUR TEUR

I. Intangible assets D. 9 1.380,0 746,0

II. 25.611,5 33.547,1

III. Tangible assets D. 8 71.589,9 27.906,1

IV. Investments in affiliated and associated companies 386,9 178,7

V. Other financial assets 3.901,5 4.768,2

VI. Deferred tax assets D. 10 3.918,6 876,5

106.788,4 68.022,6

B. CURRENT ASSETS:

I. Inventories:

1. Raw materials and supplies 19.661,2 10.891,7

2. Unfinished goods 37.977,7 20.573,7

Advance payments received -15.225,4 -5.898,2

22.752,3 14.675,5

3. Finished goods and merchandise 11.077,3 7.554,6

4. Advance payments made 43,2 1.297,3

D. 11 53.534,0 34.419,1

II. Trade accounts receivable and other receivables and assets D. 12 76.808,3 49.374,8

III. Cash and cash equivalents D. 13 10.003,9 2.170,2

247.134,6 153.986,7

TEUR NOTES 2004 2003

1. Net Sales D. 1 392.067,7 265.537,3

2. Other operating income D. 2 10.975,7 8.339,3

3. Changes in inventory of finished and unfinished goods 7.252,8 6.366,3

4. Own work capitalised 94,2 388,4

5. Expenses for materials and services received D. 3 -219.365,1 -143.578,0

6. Personnel expenses D. 4 -105.053,3 -77.588,6

7. Other operating expenses D. 5 -46.221,8 -29.163,5

8. Earnings before interest, taxes, depreciation and amortisation (EBITDA) 39.750,2 30.301,2

9. Depreciation -11.959,4 -9.008,7

10. Earnings before interest, taxes and amortisation (EBITA) 27.790,8 21.292,5

11. Amortisation of goodwill -10.014,7 -2.292,2

12. Earnings before interest and taxes (EBIT) 17.776,1 19.000,3

13. Income from associated companies 30,2 93,4

14. Financial expenses -3.987,4 -4.356,4

15. Other financial results -248,2 -7,1

16. Financial result D. 6 -4.205,4 -4.270,1

17. Earnings before tax 13.570,7 14.730,2

18. Taxes on income D. 7 -4.430,8 -4.003,0

19. Profit for the year after tax 9.139,9 10.727,2

20. Minority interest -127,0 -198,8

21. Consolidated profit for the year (Result after minority interest) 9.012,9 10.528,4

Earnings per share D. 15 0,72 0,97

TEUR SHARECAPITAL CAPITALRESERVES2) RETAINED EARNINGS TOTAL

Balance as of January 1st, 2003 10.900,9 8.700,0 3.795,8 23.396,7

Consolidated profit for the year 0,0 0,0 10.528,4 10.528,4

Reclassifications 0,0 -8.700,0 8.700,0 0,0

Differences from foreign currency translation 0,0 0,0 -785,6 -785,6

Other changes 0,0 0,0 -56,3 -56,3

Balance as of December 31st, 2003 = Balance as of January 1st, 2004

10.900,9 0,0 22.182,3 33.083,2

Consolidated profit for the year 0,0 0,0 9.012,9 9.012,9

Increase in capital 1) 8.428,7 38.530,4 0,0 46.959,1

Dividends 0,0 0,0 -8.720,7 -8.720,7

Differences from foreign currency translation 0,0 0,0 945,4 945,4

Other changes 0,0 0,0 -4,5 -4,5

Balance as of December 31st, 2004 19.329,6 38.530,4 23.415,4 81.275,4

CONSOLIDATED NOTES FOR THE FINANCIAL YEAR 2004OF POLYTEC HOLDING AG, HÖRSCHING

FINANCE LEASEWhen all significant risks and chances associated with rented or leased goods transfer to the POLYTEC GROUP (finance lease), these goods will be stated in the balance sheet as a tangible asset. At conclusion date of a contract the valuation of the good is derived from the lower value of the present market value or the cash value of the minimum future payment stated. At the same time the cash value of the minimum future payment of the contract will be shown as a financial liability in the consolidated balance sheet.

DEFERRED TAXESFollowing Austrian financial reporting standards deferred tax liabilities only have to be calculated for temporary differences that affect the income state-ment, while for deferred tax assets there is the option to capitalise items or not. Prevailing opinion dictates that a creation of deferred tax asset based on losses carried forward is not allowed. According to the rules of IFRS deferred taxes have to be calculated for all temporary differences, taking into account the expected tax rate (at the time of usage). This also applies to tax losses carried forward, as long as they can be consumed by expected future tax profits.

FOREIGN CURRENCY TRANSLATIONAccording to Austrian financial reporting standards non-realised capital gains from the valuation of foreign currency items may not be taken into account, while according to IFRS both capital gains and losses from the translation of foreign currency items on balance sheet date are included in the income statement.

PROVISIONS FOR SEVERANCE AND PENSION PAYMENTSAccording to the Austrian financial reporting standards such provisions have to be calculated using actuarial principles (discount value method). Following IFRS these provisions are calculated with the projected-unit-credit-method.

OTHER PROVISIONSAccording to IFRS provisions are to be made for liabilities towards third par-ties, whose occurrence has to be expected more likely than not and whose amount can be reliably determined. On the other hand Austrian financial reporting standards (öHGB) follows the principle of prudence according to which provisions for future expenses can also be provided.

The consolidated financial statements for the financial year 2004 of the POLYTEC HOLDING AG („the Company“) and its subsidiaries (together with the Company designated as „the Group“) were prepared in accordance with the guidelines of the International Financial Reporting Standards (IFRS).

Based in Austria, the POLYTEC GROUP is a globally acting corporate group based in the plastics industry; the Group is a component supplier of injection molded parts for serial production in the automotive industry (HIGH VOLUME AUTOMOTIVE DIVISION) and a supplier of original accessories and parts for small automotive series (LOW-MEDIUM-VOLUME AUTOMOTIVE DIVISION). THE COMPOSITES DIVISION functions as a supplier of the automotive and commercial vehicle industries. Beyond that plastic components and machines for their production are sold to other industries (INDUSTRIAL DIVISION). In the financial year 2004 the new INTERIOR AUTOMOTIVE DIVISION was created through the acquisition of the European business of the FINDLAY GROUP USA. It functions as a supplier of car interior modules (e.g. door and trunk panels, headliners) especially for suppliers in the premium segment.

The consolidated financial statements are compiled in thousand Euro (TEUR).

The present consolidated financial statements replace, in accordance with § 245a HGB, the consolidated financial statements which would otherwise be drawn up in accordance with § 244 ff HGB. The significant differences between Austrian financial reporting standards and the IFRS are:

GOODWILL AN NEGATIVE GOODWILL FROM CAPITAL CONSO-LIDATIONThe Austrian accounting standards provide several options for the treatment of goodwill. It can be absorbed directly by any reserve the Company might have, or it can be capitalised and amortised ordinarily. The treatment of ne-gative goodwill depends on the cause of its creation. According to IFRS good-will has to be capitalised and ordinarily amortised for the last time in 2004, whereby the expected useful life is often estimated as longer. From 2005 the ordinary amortisation will be replaced by an annual impairment-test.

Negative goodwill, caused by acquisitions until the 31st of March 2004, has to be allocated as ordinary revenue over the weighted average useful life of the asset, in as far as it cannot be allocated to an identifiable future loss. The amount that exceeds the fair market value of the non-cash assets has to be immediately designated as a revenue. For acquisitions after the 31st of March 2004 any remaining negative goodwill has to be recognised as a revenue in the financial year of the acquisition after asset depreciation and any contin-gent liabilities have been taken into account.

A GENERAL INFORMATION

CONSOLIDATED CASH FLOW STATEMENT FOR THE FINANCIAL YEAR 2004compared with the figures from the previous year

20 21

TEUR 2004 2003

Earnings before tax 13.570,7 14.730,2

- Income taxes -6.069,9 -987,6

+(-) Depreciation (appreciation) of fixed assets 22.222,3 11.300,9

- Dissolution of negative goodwill -4.176,4 -3.600,1

+ Book value of asset disposals 8.688,1 2.492,6

+ Retained bond interest 1.456,7 1.914,0

+(-) Increase (decrease) in long-term provisions 562,2 392,0

= Consolidated financial Cash flow 36.253,7 26.242,0

-(+) Profit (Loss) from asset disposals -627,3 -1.677,0

- Book value of asset disposals -8.688,1 -2.492,6

= Consolidated Cash flow from earnings 26.938,3 22.072,4

-(+) Increase (decrease) in inventories, advance payments made -929,7 -6.291,3

-(+) Increase (decrease) in trade and other receivables 8.023,5 -628,1

+(-) Increase (decrease) in trade and other payables 3.078,5 -1.752,2

+(-) Increase (decrease) in short-term provisions -4.845,2 176,2

= Consolidated Cash flow from operating activities 32.265,4 13.577,0

TEUR 2004 2003

- Investments in fixed assets -26.958,2 -8.333,6

- Acquisition of consolidated subsidiaries (Purchase price less the acquired cash and cash equivalents)

8.526,1 0,0

+(-) Profit (Loss) from asset disposals 627,3 1.677,0

+ Translation differences -741,9 432,6

+ Book value of asset disposals 8.688,1 2.492,6

= Consolidated Cash flow from investing activities -9.858,6 -3.731,4

TEUR 2004 2003

+(-) Increase (decrease) in interest-bearing loans and liabilities to banks -7.530,5 6.576,7

- Repayment of bearer bonds (less grant) -17.092,3 -10.477,3

+(-) Grant of long-term loans (less repayment) 866,7 -4.766,7

- Dividends -8.720,7 -72,3

+ Capital increase for cash 16.959,1 0,0

+(-) Other changes in equity 944,6 -816,5

= Consolidated Cash flow from financing activities -14.573,1 -9.556,1

TEUR 2004 2003

+(-) Consolidated Cash flow from operating activities 32.265,4 13.577,0

+(-) Consolidated Cash flow from investing activities -9.858,6 -3.731,4

+(-) Consolidated Cash flow from financing activities -14.573,1 -9.556,1

= Changes in cash and cash equivalents 7.833,7 289,5

+ Opening balance of cash and cash equivalents 2.170,2 1.880,7

= Closing balance of cash and cash equivalents 10.003,9 2.170,2

C METHODS OF ACCOUNTING AND VALUATION

B CONSOLIDATION PRINCIPLES

3. FOREIGN CURRENCY TRANSLATIONIn the single companies of the Group all transactions in foreign currencies were valued at the exchange rate of the transaction date. Monetary assets and lia-bilities in foreign currency are converted at the exchange rate of the balance sheet date. Resulting exchange rate differences are stated in the consolidated income statement. Non monetary assets and liabilities in foreign currency are converted using the exchange rate of the transaction date. Exchange rate differences for monetary items that partly belong to a foreign company, as for example long-term receivables and loans, are offset against the consolidated shareholder‘s equity without affecting the income statement.

Assets and liabilities of foreign subsidiaries were converted at the average exchange rate on the balance sheet date. Items in the consolidated income statement were converted using the average exchange rate of the financial year.

With uniform guidelines for all consolidated companies the principle of con-sistent accounting and valuation has been taken into account.

NON-CURRENT ASSETSTangible assets are valued at the purchase or production cost less the sche-duled depreciation, or the lower fair market value. The scheduled depreciation is determined according to the straight-line method.

For consumable tangible assets the following rates of scheduled depreciation apply:

Impairment losses that exceed the scheduled depreciation are taken into ac-count by the extraordinary depreciation. If the reason for an extraordinary depreciation ceases to exist, a respective write-up will be carried out.

Leased fixed assets for which all the essential risks and opportunites of ownership of the asset are transferred (Finance lease) are valued at their mar-ket value or the lower cash value according to IAS 17 (Leases - revised 1997). They are depreciated over the useful life of the asset or the shorter term of the lease contract. Payment obligations resulting from future lease instalments are discounted and carried as liabilities.

Maintenance expenses are recorded in the income statement of the financial year of their incurrence.

Borrowing costs for tangible assets are not capitalised if production or purchase exceeds a longer period of time.

Intangible assets are valued at their purchase costs and amortised using the straight-line method. Amortisation rates vary between 10,0 % and 66,7 %. Research expenses are recognised as an expense in the year of their incur-rence. Development costs also generally represent period expenses. These costs may only be capitalised if development activity will lead with sufficient probability to future revenues that not only covers the regular costs but also the relating development costs.

Other investments and loans are included in other financial assets. They are valued at the purchase costs or the lower market value on the balance sheet date.

1. SCOPE OF CONSOLIDATED COMPANIESThe stipulation of the companies included in consolidation follows the prin-ciples of IAS 27 (Consolidated Financial Statements and Accounting for In-vestments in Subsidiaries). Accordingly 4 (Previous year: 4) domestic and 18 (Previous year: 13) foreign subsidiaries are included, which all are under the legal or actual control of the POLYTEC GROUP. The eight companies not inclu-ded are in total immaterial.

According to IFRS 3 the first consolidation of a subsidiary in principle has to take place when control over assets and business of this company is actually transferred to the parent company.

The number of consolidated companies changed during the reporting year. In the financial year six companies were consolidated for the first time. In detail the following dates were selected as the dates of initial consolidation:

The acquisition of the INTERIOR AUTOMOTIVE DIVISION resulted through the merger of the Caprice Holding GmbH, Hörsching, with the POLYTEC HOLDING AG, Hörsching. In the course of this merger a capital increase amounting to TEUR 30,000 in the POLYTEC HOLDING AG, Hörsching, was carried out. The emitted equity capital instruments reflect the acquisition costs of the subsi-diary as suggested by IFRS 3.

From the time of first consolidation in the POLYTEC GROUP the newly ac-quired (founded) companies realised net sales with third parties amounting to TEUR 111,203.4 and employed a yearly average of 1,483 people. The newly acquired (founded) companies contributed TEUR 4,178.9 to the consolidated profit for the year 2004. For further details we would refer you to enclosure 4 in the notes.

During the financial year one company was no longer included in the conso-lidated financial statements due to a intragroup reorganisation. The following date of final consolidation was chosen:

2. METHODS OF CONSOLIDATIONThe capital consolidation for acquisitions until 31.3.2004 was made with the book value method by offsetting the acquisition costs of the participa-tion with its portion of equity capital at the date of acquisition. A resulting positive goodwill is allocated to its respective assets whenever possible.

Remaining differences were capitalised as goodwill in previous years, in ac-cordance with IAS 22 (Business Combinations), and as a rule amortised over a time frame not exceeding 20 years. The comparison of the acquisition costs, the fair market value of the identifiable assets and the liabilities of the subsi-diaries resulted in an original goodwill of TEUR 46,612.4. The net book value on the balance sheet date amounts to TEUR 25,611.5 (Previous year: TEUR 34,913.2).

In the previous years an arising negative goodwill was analysed according to the cause of its occurrence, and if relating to a future loss or expense it was registered as revenue in that respective year. From the comparison of acquisition costs, market values of the identifiable assets and the liabilities of the subsidiary resulted in a negative goodwill, originally amounting to TEUR 11,523.5. The net book value on the 1.1.2004 of TEUR 1,456.1 was completely released during the financial year.

For acquisitions after the 31.3.2004 the IFRS 3 provides a different method. The capital consolidation has to be carried out using only the purchase me-thod. Here the value of the investment is compared with the revalued equity of the subsidiary (purchase accounting). Any remaining goodwill is capitalised and subject to an impairment-test in the future. Accordingly this goodwill will not be ordinarily amortised. Any remaining negative goodwill after reassess-ment of the assets, while taking into account any contingent liabilities, has to be completly released in the year of the acquisition Contingent liabilities from acquisitions after the 31.3.2004 amounting to TEUR 3,951.1 were stated in the balance sheet. The remaining negative goodwill amounting to TEUR 2,720.3 was recognised as revenue in the income statement for 2004.

Minority interests in the equity and the net profit of the companies controlled by the parent company are shown separately in the consolidated financial statements.

All receivables and payables, revenues and expenses resulting from trans-actions within the consolidated companies were eliminated. Intercompany results arising from intragroup transactions were also consolidated as far as they are not of subordinated significance.

22 23

COMPANY INITIAL CONSOLIDATION

POLYTEC PLASTICS Wolmirstedt GmbH & Co KG, Lohne, Germany

Start-up 27.1.2004

LLW Lohner Lackierwerk GmbH, Lohne, Germany 1.1.2004

The POLYTEC INTERIOR AUTOMOTIVE DIVISION consisting of:

POLYTEC INTERIOR GmbH, Geretsried, Germany 1.7.2004

POLYTEC INTERIOR UK Ltd., Birmingham, Great Britain 1.7.2004

POLYTEC INTERIOR Zaragoza S.L., Zaragoza, Spain 1.7.2004

POLYTEC INTERIOR Polska Sp.z.o.o., Tomaszow Mazowiecki, Poland

1.7.2004

COMPANY FINAL CONSOLIDATION

POLYTEC AUSTRIA UK Ltd., Bromyard, Great Britain 1.1.2004

%

Buildings and leasehold improvements 4,0-20,0

Technical equipment and machinery 6,7-50,0

Other equipment, fixtures, fittings and equipment 10,0-50,0

Low value items 100,0

D EXPLANATORY COMMENTS TO THE CONSOLIDATED INCOME STATEMENT AND BALANCE SHEET

1 NET SALES

As to the composition of the net sales we would refer you to the segment reporting.

Deferred taxes are calculated, in particular, for temporary differences in valuation between the tax and commercial balance sheet of the individual companies, as well as for consolidation items. They are computed according to IAS 12 (Income Taxes - revised 1996) using the balance-sheet-liability me-thod. Deferred tax assets on losses carried forward are calculated only when consumption is expected within a foreseeable period. The calculation of the deferred taxes is based on the customary national income tax rate at the time the temporary difference will be reversed.

CURRENT ASSETSThe inventories are valued at the purchase or production costs, or the lower recoverable amount on the balance sheet date. The purchase and production costs for similar assets are determined by applying the weighted average price method or similar methods. Production costs includes only direct expenses and allocated overheads.

Trade account receivables and other receivables and assets are recorded at cost. Recognizable risks are reflected in appropriate valuation adjustments.

LONG-TERM LIABILITIESProvision for severance paymentsBased on statutory obligations employees of an Austrian group company are entitled to receive a one-time severance payment upon redundancy or at re-tirement. The amount of the severance payment depends on the number of years of service and the relevant salary/wage at the end of employment.

The provisions for severance payments are calculated uniformly on the balan-ce sheet date according to the projected-unit-credit method, using an inte-rest rate of 4.75 % p.a. (Previous year: 5.0 % p.a.) and future salary increases of 2.5 % p.a. A fluctuation reduction based on the length of service is also included in the calculation.

The corridor method is used for actuarial gains/losses. If the actuarial gains/losses exceed the defined benefit obligation by more than 10 % at the begin-ning of the financial year, then they are distributed over the expected average remaining working period of the employees participating and recognised as a profit or loss. Service costs and actuarial profits and losses are shown in the consolidated income statement as part of the personnel expenses. Interest expenses resulting from severance payments provisions are shown in the fi-nancial result.

T.F.R. - Severance payment entitlementsBased on legal obligations employees of Italian group companies can receive, in case of dismissal or other legally defined events, a one-time payment. The payment depends on the years of service as well as the benefits applicable at the time of severance.

Provision for pensions A pension is obligatory for specific employees of German group companies. The provision for pension payments is calculated according to the projected-unit-credit method, whereas depending on the distribution between entitle-ments and liquid pensions an interest rate of 4.5 % to 5.0 % and an augmen-tation rate of 0.5 % to 2.0 % is used. The actuarial calculation refers to the guideline table 1998 - Dr. Klaus Heubeck. The corridor method following IAS 19.22 is not utilised.

OTHER LONG- AND SHORT-TERM LIABILITIESThe other provisions that are disclosed under the other long- and short-term liabilities cover all foreseeable risks and uncertain obligations. The amounts reflect the most probable amount based on careful assessment of the circum-stances. Provisions for future expenses are not stated in the balance sheet. Liabilities are valued at their redemption amount. Contingent liabilities in accordance with IFRS 3 are also shown under this item.

REVENUE RECOGNITIONRevenue from the sale of products and goods is recognised when risk and opportunity are transferred to the buyer.

Interest income is recognised on a pro rata basis in accordance with the ef-fective return on asset. Income from dividends is recorded when a legal claim arises.

ESTIMATESTo a certain extent estimates have to be made in the consolidated financial statements, which affect the assets, liabilities and other obligations on the balance sheet date, as well as the revenue and expenses for the reporting period. Actual amounts arising in the future may differ from these estimates.

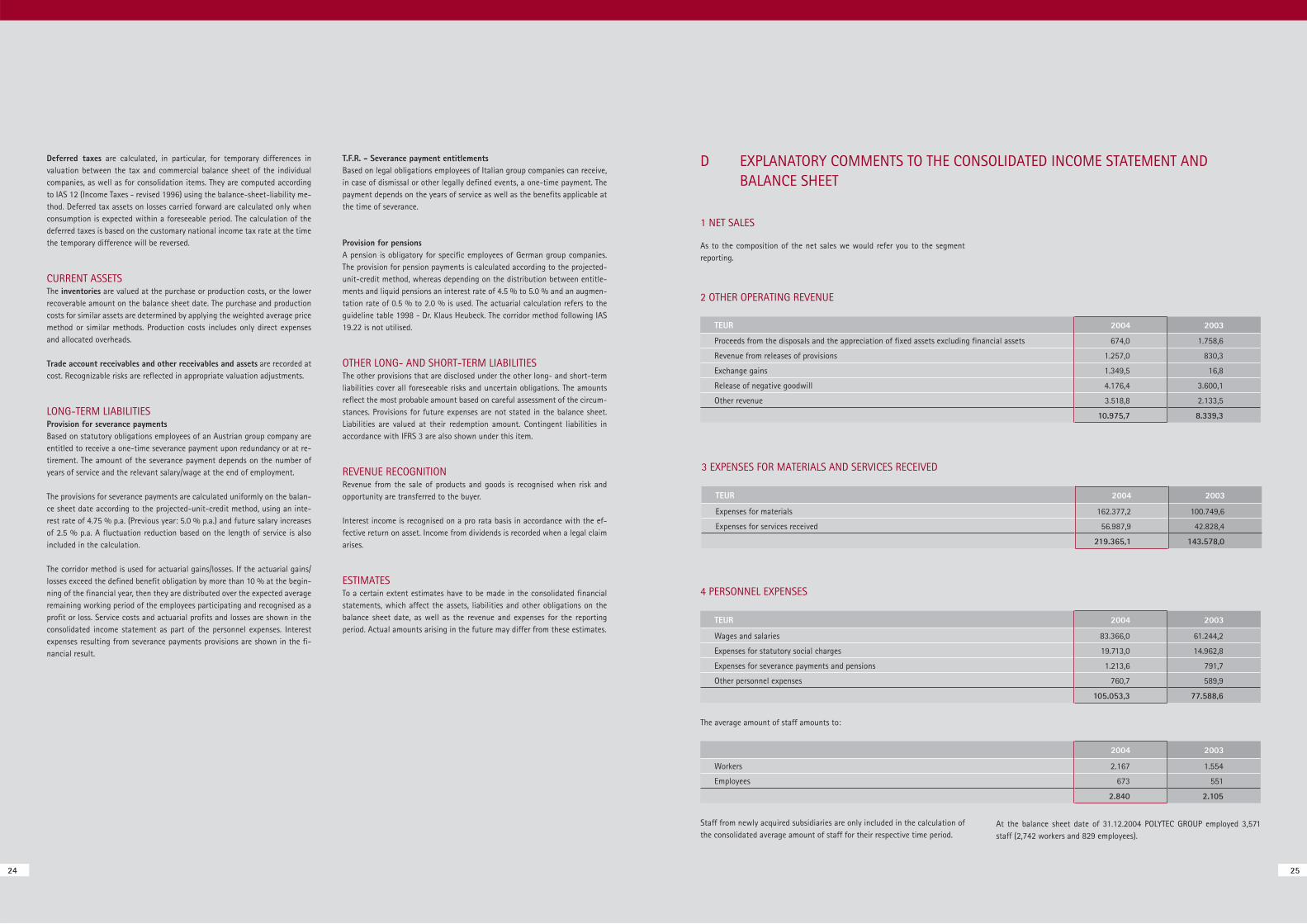

2 OTHER OPERATING REVENUE

3 EXPENSES FOR MATERIALS AND SERVICES RECEIVED

The average amount of staff amounts to:

At the balance sheet date of 31.12.2004 POLYTEC GROUP employed 3,571 staff (2,742 workers and 829 employees).

Staff from newly acquired subsidiaries are only included in the calculation of the consolidated average amount of staff for their respective time period.

4 PERSONNEL EXPENSES

24 25

TEUR 2004 2003

Proceeds from the disposals and the appreciation of fixed assets excluding financial assets 674,0 1.758,6

Revenue from releases of provisions 1.257,0 830,3

Exchange gains 1.349,5 16,8

Release of negative goodwill 4.176,4 3.600,1

Other revenue 3.518,8 2.133,5

10.975,7 8.339,3

TEUR 2004 2003

Expenses for materials 162.377,2 100.749,6

Expenses for services received 56.987,9 42.828,4

219.365,1 143.578,0

TEUR 2004 2003

Wages and salaries 83.366,0 61.244,2

Expenses for statutory social charges 19.713,0 14.962,8

Expenses for severance payments and pensions 1.213,6 791,7

Other personnel expenses 760,7 589,9

105.053,3 77.588,6

2004 2003

Workers 2.167 1.554

Employees 673 551

2.840 2.105

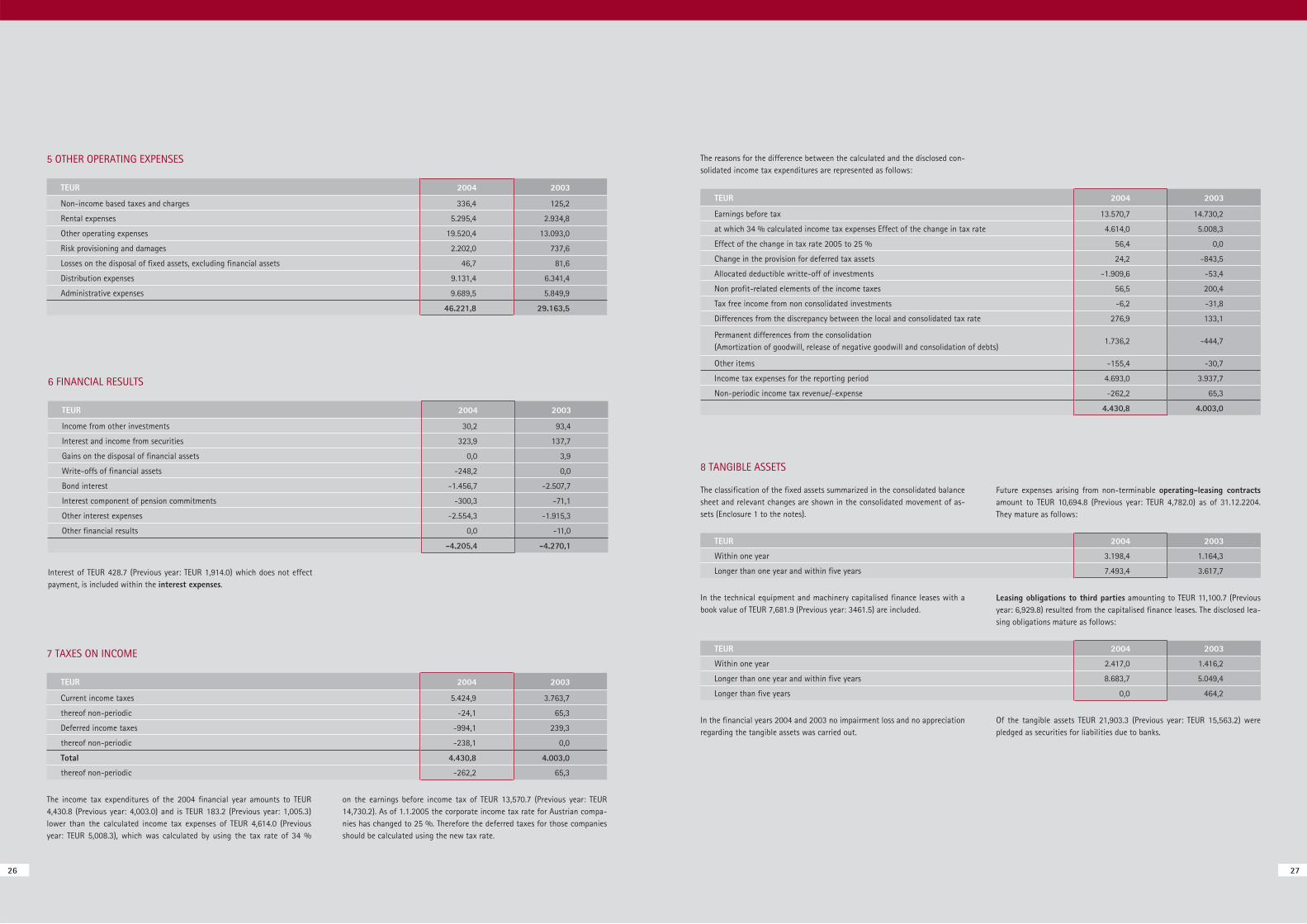

In the financial years 2004 and 2003 no impairment loss and no appreciation regarding the tangible assets was carried out.

Of the tangible assets TEUR 21,903.3 (Previous year: TEUR 15,563.2) were pledged as securities for liabilities due to banks.

8 TANGIBLE ASSETS

The classification of the fixed assets summarized in the consolidated balance sheet and relevant changes are shown in the consolidated movement of as-sets (Enclosure 1 to the notes).

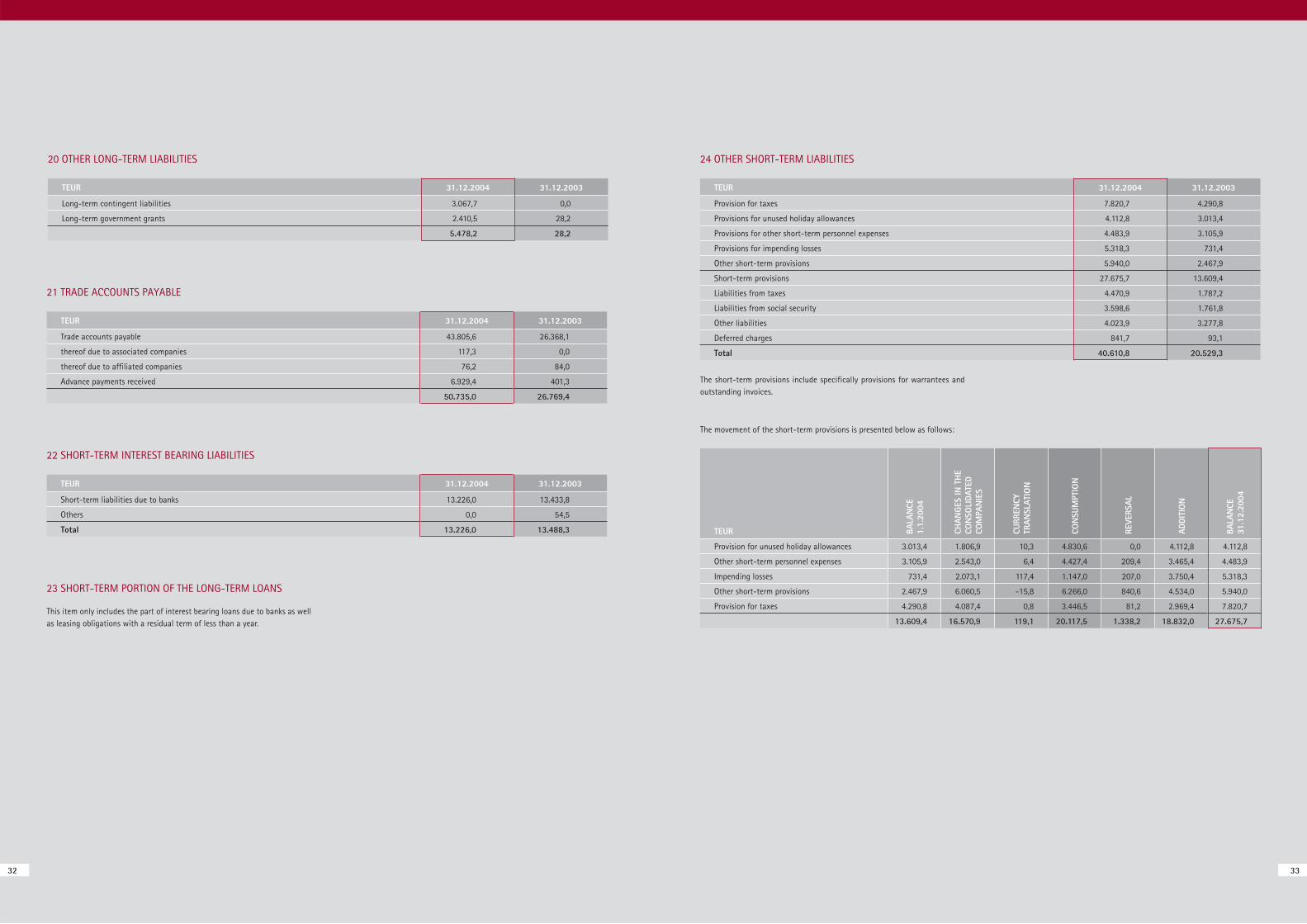

Future expenses arising from non-terminable operating-leasing contracts amount to TEUR 10,694.8 (Previous year: TEUR 4,782.0) as of 31.12.2204. They mature as follows:

In the technical equipment and machinery capitalised finance leases with a book value of TEUR 7,681.9 (Previous year: 3461.5) are included.

Leasing obligations to third parties amounting to TEUR 11,100.7 (Previous year: 6,929.8) resulted from the capitalised finance leases. The disclosed lea-sing obligations mature as follows:

The reasons for the difference between the calculated and the disclosed con-solidated income tax expenditures are represented as follows:

7 TAXES ON INCOME

on the earnings before income tax of TEUR 13,570.7 (Previous year: TEUR 14,730.2). As of 1.1.2005 the corporate income tax rate for Austrian compa-nies has changed to 25 %. Therefore the deferred taxes for those companies should be calculated using the new tax rate.

The income tax expenditures of the 2004 financial year amounts to TEUR 4,430.8 (Previous year: 4,003.0) and is TEUR 183.2 (Previous year: 1,005.3) lower than the calculated income tax expenses of TEUR 4,614.0 (Previous year: TEUR 5,008.3), which was calculated by using the tax rate of 34 %

5 OTHER OPERATING EXPENSES

6 FINANCIAL RESULTS

Interest of TEUR 428.7 (Previous year: TEUR 1,914.0) which does not effect payment, is included within the interest expenses.

26 27

TEUR 2004 2003

Within one year 3.198,4 1.164,3

Longer than one year and within five years 7.493,4 3.617,7

TEUR 2004 2003

Within one year 2.417,0 1.416,2

Longer than one year and within five years 8.683,7 5.049,4

Longer than five years 0,0 464,2

TEUR 2004 2003

Earnings before tax 13.570,7 14.730,2

at which 34 % calculated income tax expenses Effect of the change in tax rate 4.614,0 5.008,3

Effect of the change in tax rate 2005 to 25 % 56,4 0,0

Change in the provision for deferred tax assets 24,2 -843,5

Allocated deductible writte-off of investments -1.909,6 -53,4

Non profit-related elements of the income taxes 56,5 200,4

Tax free income from non consolidated investments -6,2 -31,8

Differences from the discrepancy between the local and consolidated tax rate 276,9 133,1

Permanent differences from the consolidation (Amortization of goodwill, release of negative goodwill and consolidation of debts)

1.736,2 -444,7

Other items -155,4 -30,7

Income tax expenses for the reporting period 4.693,0 3.937,7

Non-periodic income tax revenue/-expense -262,2 65,3

4.430,8 4.003,0

TEUR 2004 2003

Current income taxes 5.424,9 3.763,7

thereof non-periodic -24,1 65,3

Deferred income taxes -994,1 239,3

thereof non-periodic -238,1 0,0

Total 4.430,8 4.003,0

thereof non-periodic -262,2 65,3

TEUR 2004 2003

Non-income based taxes and charges 336,4 125,2

Rental expenses 5.295,4 2.934,8

Other operating expenses 19.520,4 13.093,0

Risk provisioning and damages 2.202,0 737,6

Losses on the disposal of fixed assets, excluding financial assets 46,7 81,6

Distribution expenses 9.131,4 6.341,4

Administrative expenses 9.689,5 5.849,9

46.221,8 29.163,5

TEUR 2004 2003

Income from other investments 30,2 93,4

Interest and income from securities 323,9 137,7

Gains on the disposal of financial assets 0,0 3,9

Write-offs of financial assets -248,2 0,0

Bond interest -1.456,7 -2.507,7

Interest component of pension commitments -300,3 -71,1

Other interest expenses -2.554,3 -1.915,3

Other financial results 0,0 -11,0

-4.205,4 -4.270,1

9 INTANGIBLE ASSETS

The classification of the fixed assets summarized in the consolidated balance sheet and relevant changes are shown in the consolidated movement of assets

(Enclosure 1 to the notes). No intangible assets are pledged as a security for liabilities due to banks.

There were no restraints on disposal of the amounts included in this item at the balance sheet date.

13 CASH AND CASH EQUIVALENTS

12 TRADE ACCOUNTS RECEIVABLE AND OTHER RECEIVABLES AND ASSETS

15 EARNINGS PER SHARE

According to IAS 33 (Earnings per share) the basic earnings per share are deri-ved by dividing the periodic result allocated to the ordinary shareholder (Profit

for the year after minority interest) by the weighted average of outstanding shares during the reporting period.

14 CONSOLIDATED SHAREHOLDER‘S EQUITY

The share capital of the POLYTEC HOLDING AG amounts to TEUR 19,329.6 (Previous year: TEUR 10,900.9) on the balance sheet date, and is divided into 19,329,585 ordinary shares with a nominal value of EUR 1.00 per share. The shares are registered.The board of directors was authorised by a resolution of the shareholders‘ meeting on 27.10.2004, with the approval of the board of supervisors, to in-

crease the share capital through the issue of new shares up to an amount of TEUR 4,500.0 within 12 months after registration of the authorised capital at latest.

For details we would refer you to the development of the consolidated shareholder‘s equity.

A reversal of write-downs in accordance with IAS 2.31 (Disclosure of Accoun-ting Policies - revised 1994) was not undertaken.

Of the inventories TEUR 7,750.9 (Previous year: TEUR 5,940.9) are pledged as a security for liabilities due to banks.

11 INVENTORIES

The classification of the inventories is represented as follows:

Deferred taxes from losses carried forward amounting to TEUR 188.7 (Pre-vious year: TEUR 107.6) were not capitalised.

Deferred taxes were not included in the consolidated financial statement re-sulting from investments in subsidiaries in accordance with IAS 12.39 (Income Taxes - revised 1993).

10 ALLOCATION OF DEFERRED TAXES

Temporary differences between the tax base and the carrying amount in the IFRS financial statements resulted from the following amounts / had the fol-lowing impact on deferred taxes:

28 29

TEUR 31.12.2004 31.12.2003

Cash in hand, checks, cash at banks 10.003,9 2.170,2

TEUR 31.12.2004 31.12.2003

Trade accounts receivable 70.873,7 46.223,6

thereof with a residual term > 1 year 792,2 595,6

thereof from affiliated companies 1.407,3 37,2

thereof from associated companies 0,0 757,7