Embed Size (px)

Citation preview

Business Method Update and Briefingfor the

Patent Lawyers Club of Washington

April 21, 2009

by

Wynn Coggins Group Director, Technology Center 3600

What is a “ Business Method”?

The term “Business Method” is a generic term that has been used to describe many types of process and apparatus claims.

There has been confusion regarding business method claims vs. other process claims.

Not all “business method”- type claims are classified in Class 705. Only computer-implemented processes related to e-commerce, the Internet and data processing involving finance, business practices, management or cost/price determination are classified in Class 705. Other process claims are classified and examined according to their structure or field of use. For example, gaming methods and teaching

methods are classified elsewhere.

What is a “ Business Method”?

Class 705

Title:Data processing: Financial, Business Practice, Management, or Cost/Price Determination

Definition:Machines and methods for performing data processing or calculation operations in the:• Practice, administration or management of an

enterprise, or

• Processing of financial data, or

• Determination of the charge for goods or services

Class 705 Comprises:

A collection of 20+ financial and business data processing areas.

Its four largest categories are:

The Four Categories….

1. Determining Who Your Customers Are, and the Products/Services They Need/Want. Operations Research

- Market Analysis

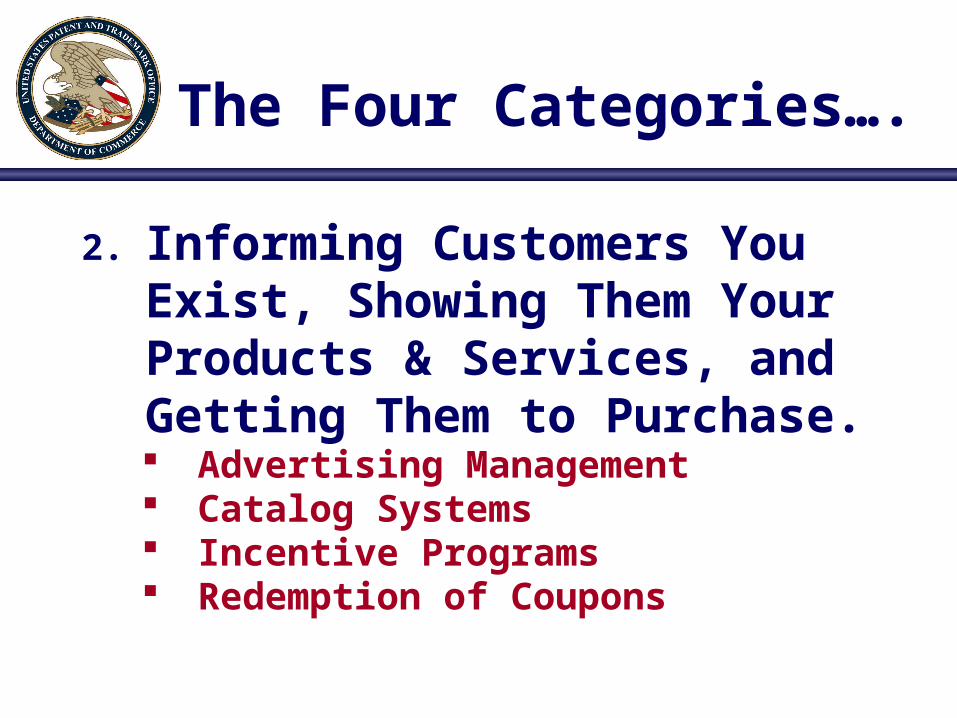

2. Informing Customers You Exist, Showing Them Your Products & Services, and Getting Them to Purchase. Advertising Management Catalog Systems Incentive Programs Redemption of Coupons

The Four Categories….

3. Exchanging Money and Credit Before, During, and After the Business Transaction.

The Four Categories….

Credit and Loan Processing

Point of Sale Systems

Billing

Funds Transfer

Banking

Clearinghouses

Tax Processing

Investment Planning

4. Tracking Resources, Money, And Products. Human Resource Management Scheduling Accounting Inventory Monitoring

The Four Categories….

Class 705 Workgroups3620, 3680, 3690

3620 Workgroup

¨ AU 3621 - Business Cryptography, Andrew Fischer, SPE ¨ AU 3622 - Incentive Programs/Coupons, Eric Stamber, SPE¨ AU 3623 - Operations Research/Voting, Beth Van Doren, Acting SPE¨ AU 3625 - E-shopping, Jeffrey Smith, SPE¨ AU 3626 - Health Care/Insurance, Christopher (Luke) Gilligan¨ AU 3627 - Point-of-Sale/Inventory/Accounting, F. Ryan Zeender, SPE¨ AU 3628 - Cost/Price, Reservations, Transportation John Hayes, SPE¨ AU 3629 – Business Processing, John Weiss, SPE

3680 Workgroup

¨ AU 3685 – Business Cryptography, Calvin Hewitt, SPE

¨ AU 3686 – Health Care/Insurance, Jerry O’Conner, SPE

¨ AU 3687 - Point-of-Sale/Inventory/Accounting, Matthew Gart, SPE

¨ AU 3688 - Incentive Programs/Coupons, James Myhre, SPE

¨ AU 3689 - Business Processing, Janice Mooneyham, SPE

Class 705 Workgroups3620, 3680, 3690

Class 705 Workgroups3620, 3680, 3690

3690 Workgroup (Finance and Banking)

¨ AU 3691 - Finance & Banking, Alexander Kalinowski, SPE¨ AU 3692 - Finance & Banking, Kambiz Abdi, SPE¨ AU 3693 - Finance & Banking, James (Jay) Kramer, SPE¨ AU 3694 - Finance & Banking, James Trammell, SPE¨ AU 3695 – Finance & Banking, Charles Kyle, SPE¨ AU 3696 – Finance & Banking, Tom Dixon, SPE

Filing Trends in Class 705

Business Methods Filing History

0

2000

4000

6000

8000

10000

12000

14000

1998 1999 2000 2001 2001 2003 2004 2005 2006 2007 2008

Fiscal Year

Ap

pli

cati

on

s F

iled

Pendency in Class 705 (At Mid-year 2009)

Current Pendency to First Action = 31.6 months

• Down from 41.4 months at the mid year 2008.• For comparison, corps-wide current pendency to first action = 26.9 months

Current Pendency to Issue/Abandonment = 46.1 months

• Down from 56.3 months at mid year 2008• For comparison, corps-wide current pendency to issue/abandonment = 33.7 months

Assignees for Patent Grants in Class 705 (2003-2007)

IBM = 259

PITNEY-BOWES = 95

FUJITSU = 66

SONY = 59

HP = 58

MICROSOFT = 55

NCR =49

HITACHI = 46

CONTENTGUARD = 43

WALKER DIGITAL = 39

FIRST DATA = 36

MATSUSHITA ELECTRONICS = 34

Examiner Growth

Year FY ‘01 FY ’02 FY ’03 FY ‘04 FY ’05 FY ’06_ FY’07 FY ’08 FY ‘09

Number of

Examiners 77 125 110 116 133 147 260 300 328

Patents 433 492 495 289 711 1,191 1,330 1,643 **

Issued ** End of year Data Not Yet Available.

Business Methods Web Site http://www.uspto.gov/web/menu/pbmethod/

Filings and Issue Data (1997 – 2008)• Updated annually

Business methods Allowance Checklist• Very helpful for applicants• Indicates what examiners must verify prior to allowing an

application Guidelines on when an electronic document is considered prior

art. 103 rejection examples Class 705 core databases and classification definitions Revised MPEP 2106 – Examination guidelines for business

methods• Guidance for Examining Process Claims in view of In re Bilski,

signed January 7, 2009 The paper “Successfully Preparing and Prosecuting a Business

Method Patent Application”

Examples of what is posted:

Prior Art

The USPTO is always looking for ways to ensure that examiners have the best prior art as early as possible in the examination process. Our data shows that when examiners have the right art in front of them, they make the right decisions.

Reaching Out to Our Industry Partners

We have successfully partnered with industry to gain valuable input on prior art resources. They have shared: Databases; Books, Technical Reports, and

Conference Proceedings, Journals; and

Web-based Resources

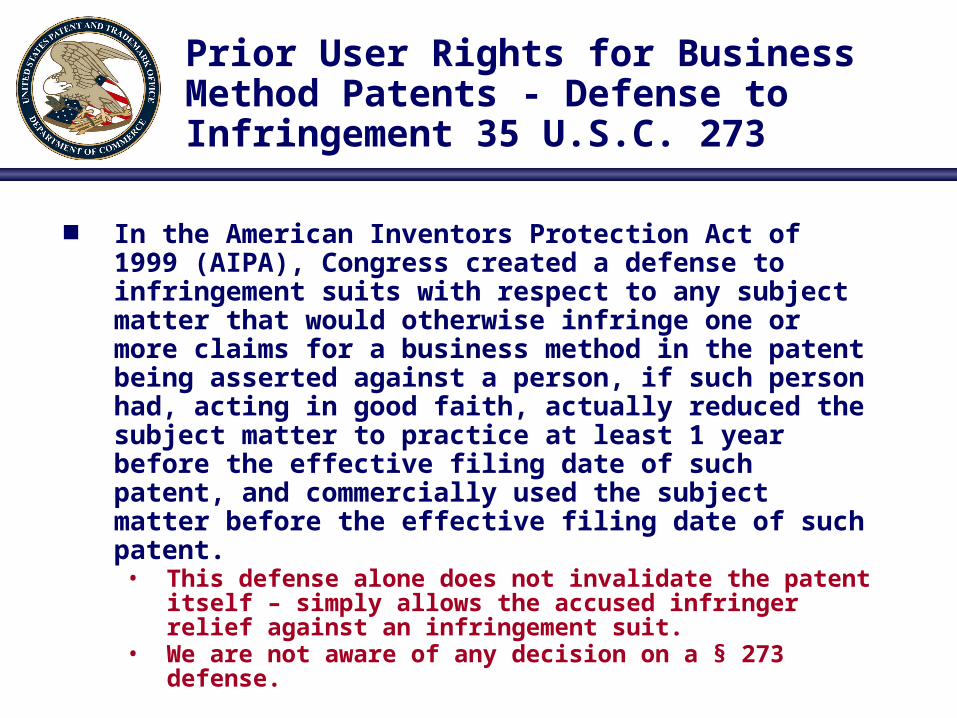

Prior User Rights for Business Method Patents - Defense to Infringement 35 U.S.C. 273

In the American Inventors Protection Act of 1999 (AIPA), Congress created a defense to infringement suits with respect to any subject matter that would otherwise infringe one or more claims for a business method in the patent being asserted against a person, if such person had, acting in good faith, actually reduced the subject matter to practice at least 1 year before the effective filing date of such patent, and commercially used the subject matter before the effective filing date of such patent. • This defense alone does not invalidate the patent

itself – simply allows the accused infringer relief against an infringement suit.

• We are not aware of any decision on a § 273 defense.

Legal Update

• In re Bilski • U.S. Court of Appeals for the Federal

Circuit (CAFC) issued the en banc ruling 10/30/08.

• The court’s opinion clarified the standards applicable in determining whether a claimed method constitutes a statutory “process” under 35 U.S.C. 101.

Legal Update

• In view of the Bilski decision, the USPTO’s Interim Guidelines for Examination of Patent Applications for Patent Subject Matter Eligibility are being redrafted to reflect the most current standards for subject matter eligibility.

• Until those guidelines are completed, examiners have been instructed to follow the current patent subject matter eligibility guidelines appearing in MPEP 2106, with the modification set forth in the January 7, 2009 memorandum entitled “Guidance for Examining Process Claims in view of In re Bilski”.

Legal Update

The January 7, 2009 memorandum has been provided to assist examiners in determining whether a method claim qualifies as a patent eligible process under 35 USC § 101. A method claim must meet a specialized,

limited meaning to qualify as a patent-eligible process claim. As clarified in Bilski, the test for a method claim is whether the claimed method is (1) tied to a particular machine or apparatus, or (2) transforms a particular article to a different state or thing. This is called the “machine-or-transformation test.”

If neither of these requirements is met by the claim, the method is not a patent eligible process under § 101 and should be rejected as being directed to non-statutory subject matter.

Legal Update

An example of a method claim that would not qualify as a statutory process would be a claim that recites purely mental steps.

Thank You

![Wynn Macau [1128.HK] · Wynn Resorts of the US owns 72.29% of the Company, ... Wynn Macau Encore Wynn Cotai Opening September 2006 April 2010 2015 or 2016 (planned)](https://img.pdfslide.us/doc/110x75/5b16bcbe7f8b9a5e6d8d7055/wynn-macau-1128hk-wynn-resorts-of-the-us-owns-7229-of-the-company-.jpg)