Embed Size (px)

Citation preview

BUSINESS IN AMERICA I l l u s t r at e d

A V I S U A L G U I D E T O B U S I N E S S , T A X E S , A N D T H E E C O N O M Y

PART OF THE P U T T I N G A FAC E SERIES

i

Business in America IllustratedA V I S U A L G U I D E T O B U S I N E S S , T A X E S , A N D T H E E C O N O M Y

ii

iii

Copyright © 2014 Tax Foundation

ISBN: 978-0-9887183-8

National Press Building529 14th Street, NW, Suite 420 • Washington, DC 20045 • (202) 464-6200

taxfoundation.org

iv

v

Americans often look at businesses impersonally. We think of them as lifeless entities that earn profits and don’t do much else. When we think of businesses this way, it becomes very easy to think that business taxes are somehow different than other taxes.

But the reality is that businesses are simply groups of people; they are workers, consumers, and shareholders.

This means that when we tax businesses, we actually tax people; workers through lower wages, consumers through higher prices, and shareholders through lower returns. Furthermore, the majority of businesses are, in fact, a person that the tax code treats as a business.

In the United States, we place a heavy tax burden on businesses. Our corporations face the highest tax rate and the most burdensome international tax rules in the developed world. Our non-corporate businesses face high tax rates, too, reaching above 50 percent in some states. Furthermore, our tax code actively discourages investment by double taxing that investment at high rates.

America’s high-tax environment stifles the economy and makes work and investment more expensive. This is bad for long-term prosperity.

The good news is that there is a solution. Tax reform that lowers taxes on businesses and investment can create jobs, increase incomes, and lead to higher living standards.

This book is your visual guide to business taxes in America. It discusses the vast array of business types and sizes, the sectors of the economy they serve, and the effects of taxes on U.S. businesses and the people who build, create, and maintain them.

Introduction

vi

Chapter 1: The U.S. Economy Is Treading Water 1Economic Growth Has Slowed Since 2000 2The U.S. Economy Is Recovering Too Slowly From the Last Recession 3The U.S. Labor Force Is Smaller Today Than in the Past 30 Year 4Household Incomes Have Stagnated in the Last Decade 5Saving and Investment Are In Long-Term Decline 6The Financial Crisis Hurt All Investment, Not Just Housing 7

Chapter 2: Who Are America’s Businesses? 895 Percent of Businesses Are Pass-through Entities 9Pass-throughs Now Earn More Business Income Than Corporations 10Corporations Make Up 5 Percent of Businesses but Earn 62 Percent of Revenues 11Less Than One Percent of Businesses Employ Half of the Private Sector Workforce 12C Corporations Pay the Highest Private Sector Wages 13Service Industries Are the Largest Segment of the U.S. Economy 14Government Employs More Workers Than Any Other Industry 15

Chapter 3: Pass-through Businesses in the United States 16The Basics of the Taxes on Pass-through Businesses 17Sole Proprietorships Are Three-Quarters of All Pass-through Businesses 18Pass-through Businesses Employ Most of the Private Sector Workforce 19High-Income Earners Make Three-Quarters of Pass-through Business Income 20Pass-through Businesses Face Marginal Tax Rates over 50 Percent in Some States 21

Table of Contents

vii

Chapter 4: The U.S. Corporate Tax System Is Uncompetitive 22The U.S. Corporate Tax Rate Is Out of Line with Our Trading Partners 23The U.S. Has the Least Competitive Corporate Tax Rate in the OECD 24Corporate Tax Rates Throughout the World Have Declined Over the Past Decade 25The U.S. Places a High Tax Burden on Personal Dividend Income 26The U.S. Capital Gains Tax Rate Is Higher Than the OECD Average 27The Combined Tax on Corporate Profits Is High in the U.S. 28The Total Tax Burden on Corporate Investment Is High in the U.S. 29

Chapter 5: U.S. Corporations Pay a Lot in Taxes 30Corporations Pay Over $700 Billion in Total Taxes Per Year 31Large Companies Pay Nearly 90 Percent of Corporate Income Taxes 32Corporations Face High Effective Tax Rates Across All Industries 33Depreciation Requires Businesses to Pay Tax on Income That Doesn’t Exist 34Corporations Receive Only 13 Percent of All Tax Expenditures 3517 U.S. States Have a Combined Corporate Tax Rate Over 40 Percent 36

Chapter 6: The International Corporate Tax System Is Outdated 3795 Percent of the World’s Population Is Outside the U.S. Borders 38U.S. Corporations Are Earning More Money and Paying More Taxes Overseas 39The U.S. Tax Code Puts U.S. Multinationals at a Disadvantage 40The Number of Worldwide Tax Systems Has Declined Over the Last Century 41The Effective Tax Rate on U.S. Foreign Corporate Earnings Has Averaged Above 25 Percent 42Most Foreign Corporate Income Is Earned in Europe and Asia 43The Effective Tax Rate on Foreign Earnings Varies by Region 44Effective Tax Rates on Foreign Income Vary Substantially by Industry 45

viii

Chapter 7: What Would Happen If We Fixed the Tax Code? 46Lowering the Corporate Tax Rate Would Increase GDP Without Reducing Revenue 47Eliminating the Corporate Income Tax Is Self-Financing 48Individual Tax Rate Cuts Would Grow the Economy, but Don’t Pay for Themselves 49Lowering Investment Taxes Would Grow the Economy and Increase Revenues 50Full Expensing Would Grow the Economy by $870 Billion 51Tax Reform Could Grow the Economy by $2.5 Trillion 52

CHAPTER 1 | 1

The global recession was tough on the U.S. economy, and many Americans are still feeling the effects. Five years into the recovery, economic growth has remained persistently sluggish. Median household incomes are below the levels seen in 2000, and the percent of people employed is at its lowest level in over 30 years. To make matter worse, U.S. saving and investment are in a long-term decline, and businesses are barely investing enough to keep pace with the wearing out of equipment and structures. The U.S. economy is treading water. A big reason for the economic malaise in the United States is how the tax code treats businesses and private business owners. For starters, the U.S. has one of the least competitive tax codes in the developed world. U.S. corporations face the third highest tax rate in the entire world, behind only Chad and the United Arab Emirates. They also face rules on foreign-earned income that discourage corporations from reinvesting in the United States.

The tax code isn’t any better for non-corporate businesses. Pass-through businesses face an overly complex and burdensome tax code with small businesses reporting compliance costs of $19 billion per year. To make matters worse, a 2012 tax increase raised tax rates on some pass-through businesses to over 50 percent in some states. It also increased tax rates on investment by nearly 60 percent. Our increasingly burdensome tax code makes it more and more difficult to build and grow a business. This has a real impact on real people. If we want our economy to achieve its potential, we need to better understand the problem so we can find the solution.

The U.S. Economy Is Treading WaterCHAPTER 1

2 | BUSINESS IN AMERICA ILLUSTRATED

Economic Growth Has Slowed Since 2000Real Annual GDP Growth Rate and Average, 1970–2013

Since 2000, GDP growth in the U.S. has been persistently low, averaging about 2 percent. Between 1970 and 2000, GDP growth averaged above 3 percent. There is a recent trend toward slower growth in the U.S., a trend that needs to be mitigated or reversed with better economic policy.

Source: Bureau of Economic Analysis.

0.2

3.3

5.2 5.6

-0.5 -0.2

5.4

4.6

5.6

3.2

-0.2

2.6

-1.9

4.6

7.3

4.2

3.5 3.5

4.2 3.7

1.9

-0.1

3.6

2.7

4.0

2.7

3.8

4.5 4.4 4.8

4.1

1.0

1.8

2.8

3.8 3.4

2.7

1.8

-0.3

-2.8

2.5 1.8

2.8 1.9

-3

-2

-1

0

1

2

3

4

5

6

7

8%

1970 1975 1980 1985 1990 1995 2000 2005 2010

CHAPTER 1 | 3

The U.S. Economy Is Recovering Too Slowly From the Last Recession U.S. Real GDP 2000–2025 (Projected), CBO Projected vs. Pre-Recession Trend (2014 Dollars)

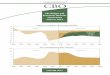

The global financial crisis dramatically harmed the U.S. economy, reducing overall output by $455 billion in real terms. Typically after recessions, the economy quickly recovers. However, this recovery has not been quick. While the U.S. economy has been growing for the past couple of years, it has been slow—too slow to fully recover from the crisis. In fact, the Congressional Budget Office (CBO) projects that the U.S. economy will permanently remain below the pre-recession trend. This permanent gap due to the recession means that the economy will still be $4.5 trillion below its previous trend by 2020.

Source: Congressional Budget Office; Tax Foundation calculations.

5

10

15

20

25

$30

2000 2005 2010 2015 2020 2025

Actual

Trend

CBO Projected

Trill

ions

of D

olla

rs

4 | BUSINESS IN AMERICA ILLUSTRATED

The U.S. Labor Force Is Smaller Today Than in the Past 30 Years Civilian Employment to Population Ratio, Seasonally Adjusted 1960–2014

The global financial crisis also impacted the U.S. labor force. The U.S. employment-to-population ratio, which reflects the number of working-age individuals who are employed, declined from 63 percent in 2007 to about 58 percent in 2009, the largest decline in the past 50 years. Even as the economy has slowly recovered, the labor market has not. The employment-to-population ratio remains below 60 percent, levels we have not seen since the late 1970s and early 1980s.

Source: Federal Reserve Bank of St. Louis.

54 55 56 57 58 59 60 61 62 63 64 65%

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010

Employment to Population Ratio

CHAPTER 1 | 5

Household Incomes Have Stagnated in the Last Decade U.S. Median Household Income, 1980–2013 (2013 Dollars)

Household incomes have stagnated in recent years. From 1980 to 2000, when the economy was growing at a higher rate, real household income increased from $47,668 to $56,800, where it peaked. But since 2000, and after two recessions, median household income in the United States has declined. In 2013, median household income was $51,939, the lowest it has been since 1995.

Source: U.S. Census Bureau.

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

1980 1985 1990 1995 2000 2005 2010

Median Household Income

6 | BUSINESS IN AMERICA ILLUSTRATED

Saving and Investment Are In Long-Term Decline Net National Saving and Net Investment as a Percentage of GDP, 1969–2013

One reason for slow economic growth is that saving and investment have been declining in the U.S. for nearly a half century. Investment is important, because it provides American workers with the means to be more productive. Saving is important, because it provides the money needed for investment, which explains the close correlation between the two trends. Tax policy is one of the many factors contributing to the long-term decline in saving and investment.

Source: Bureau of Economic Analysis, Investment Accounts, Table 5.1.

-3

-1

1

3

5

7

9

11

13%

1969 1974 1979 1984 1989 1994 1999 2004 2009

Investment

Saving

CHAPTER 1 | 7

The Financial Crisis Hurt All Investment, Not Just Housing Net Investment by Sector, 1990–2013 (Billions of 2009 Dollars)

The financial crisis was most disastrous for housing, but it was terrible for all kinds of investment. After accounting for the wearing out of equipment and buildings, most sectors of the U.S. capital stock are barely being replenished fast enough to make up for depreciation. The U.S. is doing little to expand its capital stock and is instead mostly just holding on to what it has. The low investment in corporate structures and equipment helps explain why wage growth has been so sluggish. Tax reform, which lowers the cost of capital, could increase investment and grow the economy.

Source: Bureau of Economic Analysis, Investment Accounts, Table 5.2.6.

-100

0

100

200

300

400

500

$600

1990 1995 2000 2005 2010

Commercial Structures Equipment

Intellectual Property

Residential Structures

Net investment is all investment in physical capital minus the lost value of previously purchased physical capital due to wear and tear.

8 | BUSINESS IN AMERICA ILLUSTRATED

Businesses serve nearly every need of our daily lives and come in all shapes and sizes. Small businesses, large businesses, and international businesses, we have them all in America. There are companies with hundreds of thousands of employees, millions of shareholders, and tens of millions of customers, and there are companies with one person—who is both the worker and the shareholder—and a handful of clients. In total, the United States is home to over 32.5 million businesses, nearly 150 million workers, and trillions of dollars of productivity. Ninety-five percent of businesses are pass-through entities. These businesses pay taxes on individual tax returns and are organized as sole proprietorships, partnerships, and S corporations. We often think of pass-throughs as small businesses. While this is generally true, some pass-through businesses can be very large and rival large C corporations in terms of size.

On average, though, C corporations are 30 times larger than pass-throughs in terms of revenue. Their employees often tend to receive higher incomes than pass-through businesses and, despite there being far fewer C corporations relative to pass-through businesses, C corporations earn about 40 percent of all business income in the U.S.

The comparable economic footprint of C corporations and pass-through businesses means tax reform must fix the entire tax code, as both types of businesses are crucial to the future economic success of the United States.

Who Are America’s Businesses?CHAPTER 2

CHAPTER 2 | 9

Sole Proprietorships

0

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

35,000,000

1958 1963 1968 1973 1978 1983 1988 1993 1998 2003 2008

C Corps S Corps

Partnerships

95 Percent of Businesses Are Pass-through EntitiesPass-through Entities and C Corporations by Number of Tax Returns, 1958–2011

In number of firms, pass-throughs are the dominant business type, with over 30 million tax returns in 2011. Over the last 30 years, the number of pass-throughs has increased substantially. Much of this growth comes from the doubling in number of sole proprietorships since the 1980s. The number of S corporations has also increased, particularly since the Tax Reform Act of 1986 lowered individual tax rates. Since then, the number of S corporations has grown from 800,000 to over 4 million returns.

Source: IRS.

S corporations became part of the tax code in 1958 and have grown to become the second most common type of business, behind sole proprietorships. C corporations are now outnumbered by all three types of pass-throughs.

10 | BUSINESS IN AMERICA ILLUSTRATED

Pass-throughs Now Earn More Business Income Than CorporationsShare of Net Income for Pass-throughs and C Corporations, 1958–2011

Much of the growth in business income since 1980 has come from pass-through businesses. Pass-throughs now earn over 60 percent of all net business income. In 2011, pass-throughs earned $1.3 trillion in business income compared to around $800 billion earned by corporations.

Source: IRS.

Corporations saw a huge collapse in their income following the financial market crash, falling from nearly $1.3 trillion in 2007 to $450 billion in 2008.

0

10

20

30

40

50

60

70

80

90

100%

1958 1963 1968 1973 1978 1983 1988 1993 1998 2003 2008

C Corporation Net Income

All Pass-through Net Income

CHAPTER 2 | 11

Corporations Make Up 5 Percent of Businesses but Earn 62 Percent of Revenues Share of Firms and Share of Gross Receipts by Firm Type, 2011

While there are significantly more pass-through entities than C corporations, corporations still earn the largest portion of total gross receipts. In 2011, corporations earned 62 percent of the $30.9 trillion in total business receipts. Meanwhile, pass-throughs make up nearly 95 percent of all firms and account for the remaining 38 percent of gross receipts with $11.8 trillion.

Note: This includes all active returns both with and without income. Source: IRS.

Despite earning $8 trillion less in total gross receipts, pass-throughs earned more net income (over $1.3 trillion) than corporations (over $800 billion) in 2011.

5.1%

94.9%

61.8%

38.2%

0

10

20

30

40

50

60

70

80

90

100%

Corporate Pass-through

Share of ReturnsShare of Receipts

12 | BUSINESS IN AMERICA ILLUSTRATED

Less Than One Percent of Businesses Employ Half of the Private Sector Workforce Share of Firms and Share of Employment by Firm Size and Form, 2011

While over 90 percent of all firms have between 0 and 20 employees, these firms only employ 19.2 percent of all private sector workers. These firms can be anything from coffee shops to small car dealerships and are organized as pass-throughs and C corporations. On the other hand, while only 0.4 percent of all firms have over 500 employees, this small group of businesses employs 50.6 percent of the nation’s private sector workforce, with most of those employees working for C corporations.

Note: Only includes firms with employees. Source: U.S. Census Bureau.

Some of the world’s largest companies employ nearly a quarter of a million people each.

Number of Employees

Share of EmploymentShare of Firms

0

10

20

30

40

50

60

70

80

90

100%

Less than 20

20 to 99 100 to 499

500 and Up

90.1%

19.2%

8.2%

17.1%

1.3%

13.0%

0.4%

50.6%

CHAPTER 2 | 13

C Corporations Pay the Highest Private Sector Wages Average Employee Pay by Type of Organization, 2011

Corporations pay employees a higher average annual wage than pass-through entities. Average pay at corporations is $53,444 a year, while average pay for pass-through entities is about $38,000 a year. While corporations come close, they don’t match the annual average pay for government employees of $53,661. The average pay across the entire private sector is $46,458.

Note: Only includes firms with employees. Source: U.S. Census Bureau.

$53,444

$46,458

$37,987

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$53,661

Government Corporate Private Sector Average

Pass-through

14 | BUSINESS IN AMERICA ILLUSTRATED

Service Industries Are the Largest Segment of the U.S. Economy Gross Domestic Product by Industry in 2013 (Billions of Dollars)

The U.S. economy is largely service focused. Service industries—including government—make up four of the five largest individual sectors of the economy. The largest sector of the economy in 2013 was the financial and real estate sector at $3.3 trillion, followed by government ($2.2 trillion) and manufacturing ($2.1 trillion).

Source: Bureau of Economic Analysis.

$269

$287

$361

$449

$490

$611

$623

$802

$956

$999

$1,388

$2,005

$2,080

$2,186

$3,293

Agriculture, forestry, fishing, and hunting

Utilities

Other services, except government

Mining

Transportation and warehousing

Construction

Arts, entertainment, food services, etc.

Information

Retail

Wholesale

Educational services, health care, etc.

Professional and business services

Manufacturing

Government

Finance, insurance, real estate, etc.

Service IndustryProduction Industry

Since 1997, the service industry has expanded from 64.2 percent of the economy to 66.7 percent, while the production sector has dropped from 22.5 percent of the economy to 20.3 percent.

CHAPTER 2 | 15

Government Employs More Workers Than Any Other Industry

Governments at all levels employ more people than any other single industry

with 24.4 million people, or over 17 percent of all employees.

Combined, the service industry accounts for 68 percent of all employees. Goods-

producing industries, such as manufacturing and mining, only account for about

19 million jobs (14 percent), with the most coming from manufacturing with 11.9

million. Source: Bureau of Economic Analysis.

Service IndustryProduction Industry0.6

0.8

1.3

2.7

4.4

5.7

5.8

6.8

7.9

11.9

13.9

15.0

18.1

20.4

24.4

Utilities

Mining

Agriculture, forestry, fishing, and hunting

Information

Transportation and warehousing

Wholesale

Construction

Other services, except government

Finance, insurance, real estate, etc.

Manufacturing

Arts, entertainment, food services, etc.

Retail

Professional and business services

Education, health care, and social assistance

Government

Employment by Industry in 2012 (Millions of People)

Total employment in 2012 for full and part-time work was 139,741,000 people, lower than the 139,770,000 people employed in 2005.

16 | BUSINESS IN AMERICA ILLUSTRATED

Pass-through businesses are now the dominant business structure in America, with over 30 million tax returns in 2011. Many people typically think of pass-through businesses as small businesses, and in many cases, they are. There is a good chance that your local laundromat, neighborhood restaurant, your employer, or even your own business organizes as a pass-through.

This doesn’t mean that all pass-throughs are small businesses, though. In some cases, pass-through businesses are very large, with tens of thousands, or even hundreds of thousands, of employees and billions of dollars in revenue.

So what makes a business a pass-through entity? This is determined by how owners of the business elect to structure their ownership stake and pay the business’s taxes. When a pass-through business earns a profit, the business does not send the check for the tax to the IRS. Instead, the profit is passed through the business and onto the tax returns of the owners of the business. The owners then write the check and pay the tax to the IRS.

This means that these businesses pay taxes through the individual tax code, so changes to the individual tax code directly impact them. In fact, recent changes pushed the top tax rate on pass-through businesses above 50 percent in some states.

Any tax reform proposal needs to consider how changes to the individual tax code impact pass-through businesses, which earn a majority of today’s business income.

Pass-through Businesses in the United StatesCHAPTER 3

CHAPTER 3 | 17

Q: How are pass-through businesses taxed?A: Pass-through entities get their name from the way they are taxed. When a pass-through business

earns a profit, the business does not pay the tax. Instead, the profit is passed through the business

to the business owner’s tax return. The owner then writes the check and pays the tax to the IRS. This

means that for tax purposes, pass-through businesses and all their income face the same marginal tax

rates as individuals.

Q: How many times do pass-throughs pay taxes?A: Unlike C corporations, which pay two layers of taxes—once at the corporate level and once at the shareholder level—pass-through businesses only face one layer of taxation, which is paid by the business owner.

Q: Are there different types of pass-through businesses? A: There are multiple types of pass-through entities. The types of pass-through entities include S corporations, sole proprietorships, and partnerships (such as LLCs).

Q: What taxes do pass-through businesses pay? A: Pass-through entities pay their income taxes at individual income tax rates through their owners’ tax returns. The top federal income tax rate faced by pass-through entities is 39.6 percent. Pass-

through businesses also pay self-employment taxes and state and local income taxes.

Q: Are pass-throughs and small businesses the same?A: While many small businesses tend to organize as pass-through businesses, not all pass-through businesses are small. In some cases, pass-through businesses are very large, with tens of thousands, or even hundreds of thousands of employees, and billions of dollars in revenue.

The Basics of the Taxes on Pass-through Businesses

18 | BUSINESS IN AMERICA ILLUSTRATED

Sole Proprietorships Are Three-Quarters of All Pass-through Businesses Share of Tax Returns and Share of Income by Type of Pass-through, 2011

Over three-quarters of all pass-through businesses are sole proprietorships. But these 23 million businesses only earn about a quarter of all pass-through business income and have a tendency to be smaller or newer businesses. In fact, sole proprietorships had an average income of just over $12,000 per return in 2011. S corporations, with over 4 million tax returns, are the second most popular type of pass-through business, with 13.5 percent of pass-through returns, and earn 30.3 percent of income. Partnerships earn the largest share of pass-through income at 46.9 percent, with $581 billion in income in 2011.

Source: IRS.

In total, pass-through businesses earned over $1.3 trillion in net income in 2011.

13.5% 10.6%

75.9%

30.3%

46.9%

22.8%

0

10

20

30

40

50

60

70

80%

S Corporation Partnership Sole Proprietorship

Share of Returns Share of Income

CHAPTER 3 | 19

Pass-through Businesses Employ Most of the Private Sector WorkforceShare of Private Sector Employment for Pass-through Businesses by State, 2012

Not only do pass-through businesses account for more than 50 percent of net business income in the United States, they also account for more than 50 percent of private sector employment. According to 2012 census data, 54.8 percent of all business employment (excluding nonprofits and governments) is pass-through business employment. This represents approximately 66.6 million workers and sole proprietors. C corporations comprise the remaining 45 percent, or 54.9 million workers.

Source: U.S. Census Bureau.

Pass-through employment as a share of total business employment is greater than 60 percent in Idaho, Maine, Montana, South Dakota, Vermont, and Wyoming.

VA52.0%

NC53.9%

SC 54.0%

GA53.5%

FL 55.4%

AL55.3%MS

55.4%

TN 51.1%

KY54.3%

OH53.3%IN

57.6%IL

53.6%

MO53.4%

AR54.3%

LA58.3%

IA53.0%

MN55.4%

WI55.6% MI

56.2%PA

54.7%

NY57.7%

ME61.7%

TX52.7%

OK56.9%

KS53.1%

NE56.2%

SD64.1%

ND59.4%

MT67.0%

WY60.1%

CO56.2%

NM58.2%

AZ52.8%

UT56.6%

NV52.4%

ID62.9%

OR57.2%

WA55.3%

CA55.5%

AK58.2%

HI47.4%

WV50.9%

51.7% MA

59.8% RI

53.0% CT

55.0% NJ

48.5% DE

56.1% MD

52.8%DC

64.1% VT

55.3% NH

Share of Private Sector Employment: Pass-through Businesses in 2012

Smaller Share

Larger Share

20 | BUSINESS IN AMERICA ILLUSTRATED

High-Income Earners Make Three-Quarters of Pass-through Business Income Share of Pass-through Business Income by Adjusted Gross Income, 2011

Individuals with incomes over $100,000 a year earn 74 percent of pass-through business income. Individuals with income over $1 million earn 29 percent of business income, the single largest group by share of income. This means that high tax rates on high-income earners unintentionally result in high taxes on businesses.

Source: IRS.

Businesses that operate under the individual tax code are hit with a heavy tax burden due to high marginal income tax rates on individuals.

$1 million and over

29%

Under $100K

26%

$500k to $1 million

15%$200k to$500k

19%

$100k to$200k

11%

CHAPTER 3 | 21

Pass-through Businesses Face Marginal Tax Rates over 50 Percent in Some StatesCombined Federal and State Top Marginal Tax Rates by State for Pass-through Businesses, 2014

Pass-through businesses don’t only pay federal income taxes, they also pay self-employment taxes and state and local income taxes. These taxes add up to a high top marginal tax rate. Sole proprietorships and partnerships in three states—California, Hawaii, and New York—face combined top marginal tax rates of over 50 percent. Nine states have no state personal income tax and tie for the lowest combined rate of 42.6 percent on pass-through businesses.

Source: Tax Foundation.

S corporations face slightly lower combined top marginal tax rates than other pass-through businesses due to different rules regarding self-employment taxes. This lowers combined top marginal tax rates for S corporations by about 3 percentage points in each state.

VA47.2%#25

NC47.3% #24

SC 48.0% #13GA

47.4%#22

FL 42.6% #41

AL45.7%#39

MS46.8%#29

TN 42.6% #41

KY48.3% #11

OH48.0%#13

IN46.6%#33

IL46.8%#29

MO47.5%#21

AR48.0%#13

LA46.0% #38

IA47.2%#25

MN49.7%

#5 WI48.4%#10 MI

46.5%#35 PA

46.5%#35

NY50.2%

#3

ME48.6%

#9

TX42.6%#41

OK46.9%#27

KS42.6%#41

NE47.9%#16

SD42.6%#41

ND45.7%#39

MT47.9%#16

WY42.6%#41

CO46.6%#33

NM46.7%#32

AZ46.5%#35

UT46.8%#29

NV42.6%#41

ID48.2%#12

OR49.8%

#4

WA42.6%#41

CA51.9%

#1

AK42.6%#41

HI50.4%

#2

WV47.7% #20

46.9% #27MA

47.4% #22RI

47.8% #18CT

49.2% #6NJ

47.8% #18DE

49.1% #8MD

49.2% (Not ranked)DC

49.2% #6VT

42.6% #41NH

Combined Top Marginal Federal and State Tax Rates on Pass-through Businesses

Lower Rate

Higher Rate

22 | BUSINESS IN AMERICA ILLUSTRATED

CHAPTER 4

While most businesses are pass-throughs, corporations are also crucial to the U.S. economy. Corporations tend to be significantly larger than pass-throughs and often compete with businesses in overseas markets.

In our globalized world, countries must make a greater effort to attract businesses with a competitive tax code. Unfortunately for the United States and its corporations, the U.S. has one of the least competitive corporate tax codes among the 34 members of the Organization for Economic Cooperation and Development (OECD).

The United States is home to the highest corporate tax rate in the developed world at 39.1 percent and third highest in the entire world, behind only Chad and the United Arab Emirates. To pile on, the U.S. has some of the highest taxes on capital gains and dividend income, the second highest integrated corporate tax rate in the OECD at 57.1 percent—behind only France—and the OECD’s highest effective tax rate on corporate investment.

It has been nearly 30 years since the last major corporate tax reform in the U.S. Over the years, the rest of the countries in the OECD left the U.S. far behind as they took action to lower corporate tax rates and limit the taxation of corporate investment.

For the United States to become more competitive, it will need to lower its corporate tax rate to near the average tax rate in the developed world of 25 percent.

The U.S. Corporate Tax System Is Uncompetitive

CHAPTER 4 | 23

The U.S. Corporate Tax Rate Is Out of Line with Our Trading Partners U.S. Corporate Tax Rate vs. OECD Average, 1981–2014

The U.S. corporate tax rate has remained nearly unchanged for more than 25 years. Meanwhile, lawmakers in other OECD countries have repeatedly cut their corporate income tax rates to make their economies more competitive and more attractive to investment. Today, the U.S. combined state and federal top marginal corporate tax rate is 39.1 percent, while the average rate among other OECD countries is 25 percent.

Note: Averages exclude the United States. Source: OECD Tax Database, Table II.1.

0

10

20

30

40

50

60%

1981 1986 1991 1996 2001 2006 2011

Average U.S. Rate

OECD Average (Weighted)

OECD Average (Simple)

24 | BUSINESS IN AMERICA ILLUSTRATED

The U.S. Has the Least Competitive Corporate Tax Rate in the OECD Top Marginal Corporate Tax Rates by OECD Country, 2014

After years of corporate tax cuts by our trading partners, U.S. corporations now face the highest statutory corporate income tax rate in the industrialized world at 39.1 percent. This overall rate is a combination of our 35 percent federal rate and the average rate levied by U.S. states. Corporations headquartered in any of the other 33 OECD countries face a lower corporate tax rate. Even corporations in high-tax European countries such as Belgium (34 percent), France (34.4 percent), and Sweden (22 percent) have rates lower than the United States.

Note: Averages exclude the United States. Source: OECD Tax Database, Table II.1.

39.1%United States 37.0%

12.5% 17.0%

19.0% 19.0% 19.0%

20.0% 20.0% 20.0% 20.0%

21.0% 21.0% 21.1%

22.0% 22.0%

24.2% 24.5% 24.8% 25.0% 25.0%

26.0% 26.3% 26.5% 27.0% 27.5% 28.0%

29.0% 29.2%

30.0% 30.0% 30.0% 30.2%

31.5% 34.0% 34.4%

Ireland Slovenia

Czech Republic Hungary

Poland Chile

Finland Iceland Turkey Estonia

United Kingdom Switzerland

Slovak Republic Sweden

Korea Denmark

Simple Average Austria

Netherlands Greece Canada

Israel Norway

Italy New Zealand

Weighted Average Luxembourg

Australia Mexico

Spain Germany Portugal Belgium

France Japan

CHAPTER 4 | 25

0

5

10

15

20

25

30

35

40%

Africa Asia North America

South America

Oceania Europe

20042014

Corporate Tax Rates Throughout the World Have Declined Over the Past Decade Average Corporate Tax Rates by Global Region, 2004 & 2014

The United States is not only falling behind other OECD countries with regard to tax competitiveness; it is also falling behind the entire world. While the United States’ corporate income tax rate has remained the same, countries throughout the world, in every global region, have been reducing theirs. African countries have reduced their rates from an average of 35 percent to under 30 percent, while Asian countries have reduced their corporate rates from an average of 31 percent to just above 20 percent. All regions of the world have an average corporate tax rate lower than the United States’ rate of 39.1 percent.

Source: Tax Foundation.

Of 163 countries, only Chad and the United Arab Emirates have a higher corporate tax rate than the United States.

26 | BUSINESS IN AMERICA ILLUSTRATED

0.0%0.0%

6.9%10.0%10.0%10.0%

15.0%16.0%

17.5%19.0%

20.0%20.0%20.0%20.0%

22.4%23.2%23.6%

25.0%25.0%25.0%25.0%25.0%25.5%

26.4%27.0%

28.0%28.0%28.6%

30.0%30.0%30.6%

33.8%35.4%

42.0%44.0%

48.0%

EstoniaSlovak Republic

New ZealandGreece

JapanMexico

Czech RepublicHungary

TurkeyPoland

SwitzerlandIceland

ItalyLuxembourg

FinlandOECD Simple Average

AustraliaAustria

BelgiumChile

NetherlandsSlovenia

OECD Weighted AverageGermany

SpainNorway

PortugalUnited States

IsraelSweden

United KingdomCanada

KoreaDenmark

FranceIreland

The U.S. Places a High Tax Burden on Personal Dividend Income Top Marginal Tax Rate on Personal Dividend Income by OECD Country, 2014

The corporate income tax is only the first layer of taxation on corporate investment. After a corporation pays tax on its profits, those profits are either distributed to shareholders as dividends, or retained by the corporation. When the after-tax profits are distributed to shareholders, these shareholders must pay income tax on their dividend income. The United States’ top marginal tax rate on personal dividend income of 28.6 percent is approximately 5 percentage points higher than the OECD average of 23.2 percent and ranks as the 9th highest of these 34 countries.

Source: OECD; Ernst & Young.

CHAPTER 4 | 27

The U.S. Capital Gains Tax Rate Is Higher Than the OECD Average Top Marginal Tax Rate on Capital Gains Income by OECD Country, 2014

If a corporation retains its earnings, it can boost the value of its stock. As a result, shareholders can realize a capital gain. The United States also places a high tax burden on capital gains income. The U.S. average top marginal tax rate on capital gains of 28.7 percent is the 6th highest rate in the OECD and is more than 10 percentage points higher than the simple average of 18 percent across the 34 countries. Nine countries don’t tax capital gains.

Source: Ernst & Young; Tax Foundation.0.0%0.0%0.0%0.0%0.0%0.0%0.0%0.0%0.0%

10.0%15.0%

16.0%18.2%

19.0%20.0%20.0%20.0%20.0%

21.0%22.5%22.5%22.9%

25.0%25.0%25.0%25.0%

27.0%27.0%

28.0%28.0%28.7%

30.0%32.0%

33.0%38.0%

42.0%

BelgiumCzech Republic

KoreaLuxembourgNetherlands

New ZealandSlovenia

SwitzerlandTurkeyMexicoGreece

HungaryOECD Simple Average

PolandChile

IcelandItaly

JapanEstonia

AustraliaCanada

OECD Weighted AverageAustria

GermanyIsrael

Slovak RepublicNorway

SpainPortugal

United KingdomUnited States

SwedenFinlandIrelandFrance

Denmark

28 | BUSINESS IN AMERICA ILLUSTRATED

The Combined Tax on Corporate Profits Is High in the U.S.Top Marginal Integrated Corporate Tax Rates on Dividend Income by OECD Country, 2014

When combined, the U.S. corporate income tax, dividend taxes, and capital gains taxes place a large tax burden on corporate income. This combined tax on corporate income is called an integrated corporate tax rate and reflects the total taxation of corporate income. The U.S. has an integrated corporate tax rate on distributed dividends of 57.6 percent, which is the second highest in the OECD.

Source: OECD Tax Database, Table II.4.21.022.0

31.232.0

33.033.434.034.4

36.036.937.8

40.041.842.042.0

43.443.843.8

45.145.4

46.546.7

48.648.648.949.850.550.751.051.2

54.556.2

57.664.4

EstoniaSlovak RepublicCzech Republic

HungaryNew Zealand

GreeceTurkeyPolandIceland

SwitzerlandSlovenia

ChileFinlandMexico

ItalyLuxembourg

AustriaNetherlands

United KingdomSweden

AustraliaNorway

IsraelGermany

SpainJapan

BelgiumPortugal

KoreaCanadaIreland

DenmarkUnited States

France

CHAPTER 4 | 29

The Total Tax Burden on Corporate Investment Is High in the U.S. Marginal Effective Corporate Tax Rate by OECD Country, 2014

When a corporation considers an investment, the cost of taxes plays an important part in its decision—and not just corporate taxes. Property taxes, sales taxes, and complex depreciation systems all combine to decrease the after-tax profit from an investment. In the U.S., all these taxes combine for the highest marginal effective tax rate on investment in the developed world of 35.3 percent.

Source: Jack Mintz & Duanjie Chen, The Effective Corporate Tax Rate: Myth and the Fact, Tax Foundation Special Report No. 214.

The marginal effective tax rate represents the tax cost for each additional dollar of investment made by a business. A high rate deters businesses from building new plants or buying more equipment.

5.7%7.7%

9.8%10.1%

12.7%14.2%14.6%15.0%

15.7%16.1%16.1%

17.1%17.3%17.4%17.5%17.5%17.5%

18.1%18.5%18.6%19.1%

21.6%22.9%

24.4%24.4%24.5%

25.9%25.9%26.0%26.2%

29.3%30.1%

35.2%35.3%

TurkeyChile

SloveniaIreland

Czech RepIcelandPoland

IsraelSlovak Republic

HungarySwedenEstonia

LuxembourgMexicoFinland

SwitzerlandNetherlands

GreeceBelgiumCanada

DenmarkNew Zealand

PortugalGermany

NorwayItaly

AustraliaUK

SpainAustria

JapanKorea

FranceUnited States

30 | BUSINESS IN AMERICA ILLUSTRATED

The U.S.’s uncompetitive corporate tax code has a cost. Between 1994 and 2011, U.S. corporations paid a total of $13 trillion in all types of taxes to governments around the world. Even after exemptions and deductions, U.S. corporations in almost every industry faced effective income tax rates above 30 percent on all their income.

This is bad for the economy. Corporate taxes increase the cost of investment, and investment is a key driver of economic growth. In fact, studies show that corporate taxes are the most harmful taxes to economic growth and lead to fewer jobs, lower wages, and lower living standards.

However, corporate taxes aren’t just bad for the economy; they’re bad for people. As we know, corporations are simply groups of people—organizations of workers, shareholders, and consumers. This means that when we tax corporations at high rates, it’s really these people that pay the tax. Workers pay for it through lower wages, shareholders pay for it through lower returns, and consumers pay for it through higher prices.

It’s likely that you fall into one of these three groups. Even if you don’t work for a corporation, you’re probably a shareholder through your retirement account, a customer, or both. As taxpayers, it’s important to realize that a tax on a corporation could end up as a hidden tax on yourself.

U.S. Corporations Pay a Lot in TaxesCHAPTER 5

CHAPTER 5 | 31

Corporations Pay Over $700 Billion in Total Taxes Per YearTotal Foreign and Domestic Taxes Paid by Corporations to All Levels of Government, 1994–2011 (Billions of 2011 Dollars)

While many claim that corporations pay little to nothing in taxes, the reality is a bit more expensive. Corporations pay a substantial amount in income, sales, property, and various other types of taxes to federal, state, and local governments in the United States and across the globe, according to IRS data. In 2011, U.S. corporations paid about $220 billion in income taxes to the U.S. government, over $100 billion in income taxes to foreign governments, and just under $385 billion in other types of taxes. In total, U.S. corporations paid over $711 billion in taxes.

Note: Foreign tax credit claimed is used to represent foreign income taxes. Only returns with net income included. Source: IRS.

0

200

400

600

800

1,000

1,200

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Foreign Income Taxes

U.S. Income Taxes

Other Taxes

U.S. corporations paid over $13 trillion in taxes to governments around the world between 1994 and 2011.

32 | BUSINESS IN AMERICA ILLUSTRATED

Large Companies Pay Nearly 90 Percent of Corporate Income TaxesShare of Taxable Income and Share of Income Taxes by Asset Size, 2011

In 2011, corporations earned slightly less than $1 trillion in taxable income and paid about $221 billion in income taxes. However, businesses with over $2.5 billion in assets paid the vast majority of corporate income taxes. These corporations earned 77 percent of corporate taxable income and paid 68 percent of all corporate income taxes. Corporations with under $10 million in assets earned 4 percent of corporate taxable income and paid 5 percent of corporate income taxes. Note: Data includes both C corporations and S

corporations. Source: IRS.

2% 2% 3%

16%

77%

3% 2% 5%

21%

68%

0

10

20

30

40

50

60

70

80

90%

Under $1 million

$1 million under $10 million

$10 million under $100 million

$100 million under $2.5 billion

$2.5 billion and more

Share of Corporate Taxable Income

Share of Corporate Income Tax Paid

The U.S. Treasury relies on fewer than 25,000 companies for around 10 percent of all federal revenue.

CHAPTER 5 | 33

Corporations Face High Effective Tax Rates Across All IndustriesEffective Tax Rate on All Income by Industry, 2011

The U.S. taxes corporate income on a worldwide basis, which means no matter where in the world a U.S corporation earns income, that income is subject to the U.S. federal corporate tax rate of 35 percent. We see this is close to what corporations actually pay when we look at corporate effective tax rates by industry on worldwide income taxes and worldwide income. Still, the effective tax rate varies by industry due to the profitability of an industry in a given year, how much business they do overseas, and different benefits in the tax code.

Note: Manufacturing does not include Petroleum and coal products. Foreign tax credit claimed is used to represented foreign income taxes. Source: IRS.

27.8% 29.3%

30.0% 31.1% 31.3% 31.4% 31.8% 31.8%

32.7% 32.9% 33.0%

33.4% 33.6% 34.0% 34.3% 34.4%

36.1%

Agriculture, forestry, fishing, and hunting Other services

Professional and business services Construction

Real estate, rental and leasing Arts, entertainment, food services, etc.

Utilities Administrative, waste management, etc.

Manufacturing Transportation and warehousing Health care and social assistance

Wholesale and retail Information

Petroleum and coal products Finance and insurance

Educational services Mining

34 | BUSINESS IN AMERICA ILLUSTRATED

Note: This exercise evaluates the present discounted value of the average allowable deduction over the life of an asset. Source: CBT Tax Database; Tax Foundation calculations.

Depreciation Requires Businesses to Pay Tax on Income That Doesn’t Exist Average Depreciation Allowance, Disallowed Cost Recovery, and Tax on $100 of Capital Investment in the U.S.

Economists define profit as all the money you make (revenue) minus all your costs. Unfortunately, this is not how the tax code defines profits. When it comes to capital investment—a business’s purchase of machines, equipment, buildings—the tax code requires businesses to spread costs over years, and sometimes decades. Due to inflation and the time value of money, this results in businesses not being able to claim the full cost of their investments. In fact, U.S. businesses are only able to deduct an average of 62.4 percent of costs across all types of capital investments.

Full expensing would bring neutral treatment to the tax code by allowing businesses to fully deduct the cost of capital investment.

$100.00

$62.40

$37.60

$13.16

0

10

20

30

40

50

60

70

80

90

$100

$100 Capital Investment Allowable Deduction Disallowed Cost Recovery Tax on Disallowed CostRecovery

On a $100 investment, a business can deduct an average of $62.40 from their revenue over the life of the asset, not the full $100 cost.

This means that a full $37.60 of that $100 investment does not count as a business cost. This understates costs and overstates business profits.

Due to this mistreatment of capital investment, businesses pay taxes on income that doesn't exist.

x 35% =

CHAPTER 6 | 35

$148 13%

$1,036 87%

Individual Tax Expenditures

Corporate Tax Expenditures

Corporations Receive Only 13 Percent of All Tax ExpendituresCorporate vs. Individual Tax Expenditures in Billions of Dollars, Fiscal Year 2014

Despite the notion that corporations receive a large amount of special tax breaks, the majority of tax expenditures benefit individual taxpayers. For the 2014 fiscal year, the Office of Management and Budget projects that corporations will receive only 13 percent of all tax expenditures, or $148 billion. Individuals, on the other hand, will receive $1.036 trillion in tax expenditures. In total, tax expenditures have an estimated value of $1.2 trillion in 2014.

Source: Office of Management and Budget.

36 | BUSINESS IN AMERICA ILLUSTRATED

17 U.S. States Have a Combined Corporate Tax Rate Over 40 PercentCombined Corporate Tax Rates Across the States, 2014

Corporations operating in the U.S. are liable for income taxes at both the federal and state level. It is widely known that the U.S. combined corporate tax rate (the federal rate of 35 percent plus the average state rate) is the highest in the developed world at 39.1 percent. But the combined tax rate in 29 U.S. states surpasses even this. The state with the highest combined corporate tax rate is Pennsylvania. Six states have no state-level corporate tax rate and are tied with a rate of 35 percent.

Source: Tax Foundation calculations.

44 states (including the District of Columbia) have higher corporate tax rates than any other place in the developed world.

VA38.9%#30NC

38.9% #30SC

38.3% #38GA

38.9%#30

FL 38.6% #37

AL37.0%#44

MS38.3%#38

TN 39.2% #24

KY38.9% #30

OH35.0%#45

IN39.9%#18

IL41.2%

#3MO

39.1%#29

AR39.2%#24

LA37.4% #43

IA38.6%#36

MN41.4%

#2 WI40.1%#15 MI

38.9%#30 PA

41.5%#1

NY39.6%#21

ME 40.8%

#8

TX35.0%#45

OK38.9%#30

KS39.6%#22

NE40.1%#16

SD35.0%#45

ND37.9%#42

MT39.4%#23

WY35.0%#45

CO38.0%#41

NM39.7%#20

AZ39.2%#24

UT38.3%#38

NV35.0%#45

ID39.8%#19

OR39.9%#17

WA35.0%#45

CA40.7%

#9

AK41.1%

#4

HI39.2%#28

WV39.2% #24

40.2% #14MA

40.9% #5RI

40.9% #5CT

40.9% #5NJ

40.7% #10DE

40.4% #13MD

41.5% (Not ranked)DC

40.5% #11VT

40.5% #11NH

Combined Federal and Top State Corporate Tax Rates

Lower Rate

Higher Rate

CHAPTER 1 | 37

U.S. businesses, like those in other countries, have greatly increased the amount of business they conduct internationally. This has required countries to rethink how they structure their corporate tax systems. While many countries have reformed their tax codes to remain welcoming to business, the United States has stood firm with its unfriendly tax system.

The U.S. is one of the remaining six OECD countries with an outdated worldwide system of taxation. This means that U.S. corporations are liable to pay the U.S. federal corporate tax rate of 35 percent on every dollar of income, no matter where in the world a corporation earns that income, when that money is brought back to the U.S.

As a result of the worldwide tax system, U.S. companies are disadvantaged when competing in foreign countries. For example, when a U.S. business competes with a French business anywhere in the world, the U.S. business is hit

with an additional tax that the French business doesn’t have to pay. This is because France—along with almost all of the OECD—only taxes businesses on income they earn within France.

In 2010, U.S. corporations paid $128 billion in corporate income taxes to foreign countries on income of $470 billion, an effective tax rate of 27.2 percent. This is all before they paid additional taxes to the U.S. government on that same income.

The International Corporate Tax System Is OutdatedCHAPTER 6

38 | BUSINESS IN AMERICA ILLUSTRATED

95 Percent of the World’s Population Is Outside the U.S. BordersThe U.S. Share of the World’s Population

In the last couple decades, the global economy has rapidly developed. This has increased the incomes of people throughout the world. As a result, demand for American goods and services abroad has also increased. In order for U.S. businesses to stay competitive in today’s global market, they must meet that demand. Today, 95 percent of potential consumers live outside of the United States.

Source: World Bank.

5%U.S. Population

World Population

95%

CHAPTER 6 | 39

U.S. Corporations Are Earning More Money and Paying More Taxes Overseas Foreign Taxable Earnings and Taxes Paid by U.S. Companies, 1992–2010

As U.S. multinationals expand operations overseas, their income earned abroad increases. Over the past 18 years, the amount of income that U.S. multinationals have reported earning overseas has grown substantially. According to IRS data, foreign taxable income grew in real terms by 248 percent, from a little less than $150 billion to more than $450 billion between 1992 and 2010. As a result, the foreign tax liability of U.S. corporations has grown. Over the same timeframe, foreign taxes paid grew by 265 percent from $35 billion to a little under $130 billion. Source: IRS Form 1118.

Foreign Taxable Income

Foreign Taxes Paid

0

50

100

150

200

250

300

350

400

450

$500

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

40 | BUSINESS IN AMERICA ILLUSTRATED

The U.S. Tax Code Puts U.S. Multinationals at a Disadvantage Comparing the Tax Bill of a U.S. and a French Corporation in the UK

To understand how a worldwide tax system like that of the U.S. harms the competitiveness of a company, one can look at how it affects a single U.S. company operating overseas. The two multinationals in this example are operating in the UK. One is based in France, which has a territorial tax system. The other is based in the U.S., which has a worldwide tax system. Both of these companies earn $100 in profits. As a result, they both pay the UK’s corporate tax rate of 21 percent. The French company then brings those profits back to France untouched by the French government. For the U.S. company, the United States will place an additional tax on those profits if the company brings them back. At the end of the day, the French company comes out on top, with higher after-tax returns simply due to the U.S.’s additional tax on foreign profits.

Source: Tax Foundation.

$65 $79

-$21 -$21

-$14

-40

-20

0

20

40

60

80

$100

U.S. Company French Company

After-Tax Profit

UK Corporate Income Tax

Additional U.S. Tax on Foreign

Income

CHAPTER 6 | 41

The Number of Worldwide Tax Systems Has Declined Over the Last Century Number of OECD Countries with Worldwide Tax Systems

As the global market has expanded, countries have recognized the competitive disadvantage worldwide tax systems place on their businesses and have adjusted their tax system to fit this new reality. At the beginning of the 20th century, 33 countries had a worldwide tax system. That number slowly dropped to 24 countries by the 1980s. By the 2000s, the number of countries switching to territorial systems accelerated, with more than 10 countries switching in 10 short years. Nearly all developed countries have moved to the superior territorial tax system that exempts the foreign earnings of domestic corporations. This system of taxation allows their multinational corporations to compete both overseas and domestically on an equal footing. Today, the United States is one of the remaining 6 OECD countries that continues to tax its multinationals’ worldwide income.

Source: Tax Foundation.

0

5

10

15

20

25

30

35

1891 1901 1911 1921 1931 1941 1951 1961 1971 1981 1991 2001 2011

42 | BUSINESS IN AMERICA ILLUSTRATED

The Effective Tax Rate on U.S. Foreign Corporate Earnings Has Averaged Above 25 Percent Since 1992 Effective Tax Rate on Foreign Taxable Earnings, 1992–2010

While U.S. multinationals’ foreign taxable income and taxes paid have grown, the effective tax rate on this income has remained steady. The average effective tax rate on foreign earned income between 1992 and 2010 was 26.4 percent. The lowest effective tax rate paid on this income was 24.9 percent in 1999. The highest effective tax rate on foreign-earned income was 29.3 percent in 2008. The most recent data indicates an effective tax rate of 27.2 percent, an effective rate higher than the nineteen-year average.

Source: Tax Foundation; IRS Form 1118 (1992–2010).

10

15

20

25

30

35%

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Effective Tax Rate

Average (1992–2010)

CHAPTER 6 | 43

Most Foreign Corporate Income Is Earned in Europe and AsiaShare of Foreign Earned Income and Foreign Corporate Income Taxes Paid by Region

U.S. corporations do business in every part of the world. However, most foreign income was concentrated in two regions. In 2010, U.S. multinationals reported the most activity in European countries. They reported $206.8 billion in income originating in Europe and paid $63.6 billion in corporate income taxes to European governments. This represents about half of all foreign taxable income and foreign taxes paid for 2010. Asia had the second-largest concentration of reported foreign taxable income, with U.S. corporations reporting $83.4 billion in taxable income and $21.6 billion in taxes paid. Source: IRS Form 1118 (2010).

0

10

20

30

40

50

60%

Europe Asia All Other Countries

Latin America Canada Oceania Africa

Taxable Income Taxes Paid

Canada was the 3rd largest county in terms of foreign income and taxes paid by U.S. corporations

Combined, Europe and Asia accounted for 62 percent of all foreign taxable income and 67 percent of all corporate income taxes paid reported by U.S. multinationals in 2010.

44 | BUSINESS IN AMERICA ILLUSTRATED

The Effective Tax Rate on Foreign Earnings Varies by RegionEffective Corporate Tax Rate on Foreign Earnings by Region

Although all U.S. multinationals will end up paying at least a 35 percent effective tax rate on their foreign active earnings once they are repatriated, the effective rate these earnings face in foreign countries and regions can vary substantially. U.S. corporations faced the highest effective tax rate on their foreign earnings (49.2 percent) in Africa in 2010. Latin America followed with an effective rate of 33.5 percent. The third highest effective rate was paid in Europe (30.7 percent), where a majority of foreign-earned income was reported in 2010. Only two regions (Oceania and Other Countries) had effective tax rates on foreign earnings below 25 percent.

Source: Tax Foundation; IRS Form 1118.

10%

22%

26%

30% 31%

34%

49%

0

10

20

30

40

50%

All Other Countries

Oceania Asia Canada Europe Latin America

Africa

CHAPTER 6 | 45

Effective Tax Rates on Foreign Income Vary Substantially by Industry Effective Foreign Tax Rates by Industry

The effective corporate income tax rate faced by corporations overseas varies by industry. According to the most recent IRS data, Petroleum and coal products companies faced an effective corporate tax rate of 36 percent, higher than any other industry. This was followed by Mining (35 percent) and Services (32 percent). Manufacturers, which accounted for a large portion of foreign-earned income, faced an average effective corporate tax rate of 22 percent on their foreign earnings.

Note: Manufacturing does not include Petroleum and coal products. Source: IRS Form 1118; Tax Foundation calculations.

6%

14%

19%

22%

22%

24%

27%

31%

32%

35%

36%

Agriculture, forestry, fishing and hunting

Transportation and warehousing

Finance, insurance, real estate, rental and leasing

Information

Manufacturing

Wholesale and retail

Construction

Utilities

Services

Mining

Petroleum and coal products

Although the foreign effective tax rate across industries differ, these companies will end up paying at least a 35 percent corporate tax rate on all their foreign earnings due to the U.S.’s worldwide corporate tax system.

46 | BUSINESS IN AMERICA ILLUSTRATED

Our current tax code isn’t good for business. It’s uncompetitive and imposes high tax rates on all types of business and investment. This is bad for the economy.

Incomes are stagnant, and 2 percent economic growth appears to be the new normal. Meanwhile, U.S. saving is in long-term decline and investment is barely keeping pace with the wearing out of the buildings and equipment businesses require to work.

We’ve tried nearly everything, but what would happen if we tried tax reform?

Lower taxes on businesses and investment would boost employment and incomes. A move to full expensing would allow businesses to fully account for the economic cost of investment in the tools they use to produce. A shift to a territorial tax system would place businesses operating in a foreign country on an equal footing with foreign competition.

These three changes would be a boon for economic growth and U.S. competitiveness. Cutting the corporate tax rate to 25 percent and moving to full expensing would increase the size of the economy by $1 trillion and add over 1 million new jobs. Cutting the tax rate for pass-through businesses would produce even more jobs and higher incomes.

At the end of the day, the goal of public policy should be to improve lives. Tax reform can help do that through higher wages, more jobs, and greater economic opportunity.

What Would Happen If We Fixed the Tax Code?CHAPTER 7

CHAPTER 7 | 47

Lowering the Corporate Tax Rate Would Increase GDP Without Reducing Revenue Effect of Federal Corporate Tax Rate Changes on GDP and Total Federal Revenue

Corporate tax rate changes have large effects on GDP and minimal effects on total federal revenue. The large effects on GDP come from a lower cost of capital. The competitive nature of corporate taxes makes for strong responses to tax changes. If the corporate income tax were eliminated, the size of the economy would grow by 6.1 percent in the long run. This would lead to more jobs and higher wages. In turn, this would leave total federal revenue virtually unchanged.

Source: Tax Foundation Taxes and Growth Model.

The loss of corporate tax revenue due to cutting the corporate tax rate is recouped through the combination of increased economic growth and the distribution of the untaxed money to taxpaying individuals.

6.1% 5.3%

4.5%

3.7%

2.9%

2.0%

1.0%

-1.1%

-2.3%

-3.5%

0.0% 0.1% 0.2% 0.3% 0.3% 0.3% 0.2% -0.3% -0.7% -1.2%

-4

-2

0

2

4

6

8%

0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50%

Percent Change in GDP Percent Change in Revenue

The current federal corporate tax rate is 35 percent.

48 | BUSINESS IN AMERICA ILLUSTRATED

Eliminating the Corporate Income Tax Is Self-Financing Sources that Offset Revenue Loss from Eliminating the Corporate Income Tax (Billions of 2013 Dollars)

In the long run, eliminating the corporate income tax would actually increase total federal revenue. This is due to economic growth and the distribution of corporate income to other taxpayers. The loss of corporate taxes as a revenue stream would lead to a loss of about $274 billion per year. However, this lost corporate revenue would be replaced entirely by an increase in total federal revenue of $274 billion due to more economic activity. In fact, more jobs and higher wages would result in $175.2 billion in new income tax revenue and over $80 billion dollars in new payroll tax revenue. Customs, excise taxes, and the estate tax would combine with a few other taxes for the remaining $17.9 billion.

Source: Tax Foundation Taxes and Growth Model.

-300

-200

-100

0

100

200

$300

Corporate Tax Revenue Lost

Total Federal Revenue Gained

Corporate Taxes

Income Taxes

Payroll Taxes

Excise Taxes Estate Taxes Other Taxes

-$273.5 Billion

$273.9 Billion

CHAPTER 7 | 49

Individual Tax Rate Cuts Would Grow the Economy, but Don’t Pay for ThemselvesPercent Change in GDP and Federal Revenues Due to Individual Tax Rate Changes

Cutting the individual tax rate would have positive effects for economic growth by leaving more money available for investment and increasing the incentive to work. The often-discussed tax rate cut to 25 percent would grow the economy by nearly 2 percent and create 1.1 million jobs. However, it’s important to note that individual tax cuts would also result in lost revenue for the federal government. Conversely, raising individual tax rates would raise federal revenue, but at the cost of slower growth and lower incomes for everyone.

Source: Tax Foundation Taxes and Growth Model.

Changes to individual tax rates affect pass-through businesses, because they pay taxes on individual tax returns.

Percent Change in Revenue

The current individual tax rate is 39.6 percent.

5.2%

3.5%

1.9% 1.1%

0.4%

-0.5% -1.0%

-1.5% -2.1%

-7.9%

-5.1%

-2.6%

-1.4% -0.5%

0.6% 1.1%

1.6% 2.0%

-10.0

-8.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0%

15% 20% 25% 30% 35% 40% 45% 50% 55% 60%

Percent Change in GDP

50 | BUSINESS IN AMERICA ILLUSTRATED

Lowering Investment Taxes Would Grow the Economy and Increase Revenues Percent Change in GDP and Revenue Due to Changes in Capital Gains and Dividend Tax Rates

Capital gains and dividend taxes are a second layer of taxes on corporate profits and have adverse economic effects. When we limit this double taxation, the economy responds positively. In fact, if we were to lower capital gains and dividend tax rates from 20 percent to 10 percent, we would see additional growth of 2.7 percent. That equates to over $445 billion in additional economic activity and over 500,000 new jobs. Because tax cuts on investment are so effective, the resulting increased economic activity would actually lead to higher federal revenues. Source: Tax Foundation Taxes and Growth Model.

5.92%

4.37%

2.73%

1.04% 0.79%

-0.24% -1.31%

-2.38%

-3.37%

2.94% 2.24%

1.42%

0.51% 0.38%

-0.11% -0.69%

-1.30% -1.87%

-4

-2

0

2

4

6

8%

0% 5% 10% 15% 20% 25% 30% 35% 40%

Percent Change in GDP Percent Change in Revenue

The current top capital gains and dividend tax rate is 23.8 percent.

CHAPTER 7 | 51

Full Expensing Would Grow the Economy by $870 Billion Economic Effect of Implementing Full Expensing of Physical Capital

The current tax code requires businesses to write off the cost of capital investment over multiple years. Full expensing would allow businesses to deduct the entire cost of investment in equipment, factories, and other tools of production in the year the cost is incurred. This would correctly define business income and lower the cost of investment, which would then increase investment in property and equipment. This in turn would increase GDP by more than 5 percent, wages by roughly 4.5 percent, and federal revenues by 4.6 percent.

Source: Tax Foundation Taxes and Growth Model.

5.33%

4.47% 4.64%

0

1

2

3

4

5

6%

GDP Wage Rate Federal Revenue

52 | BUSINESS IN AMERICA ILLUSTRATED

Tax Reform Could Grow the Economy by $2.5 Trillion Economic Effects of Corporate and Individual Rate Cut to 25 Percent, Capital Gains and Dividends to 10 Percent, and Full Expensing

Tax reform that lowered taxes on businesses and investment would provide a huge boost to the economy. If we were to cut tax rates to 25 percent on corporate and pass-through businesses, move to full expensing, and lower capital gains and dividend rates to 10 percent, the economy would be over 11 percent larger in the long run. As a result, the economy would be $2.5 trillion larger by 2024. This kind of tax reform would increase investment by 33 percent, boost wages by 8.4 percent, and create nearly 3 million jobs.

Source: Tax Foundation Taxes and Growth Model.

Due the increased economic activity from the pro-growth tax reform, total federal revenue would actually increase in the long run.

Increase of $2.5 trillion

15

17

19

21

23

25

27

$29

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029

Real GDP after Tax Reform

Projected Real GDP (2014 to 2029)

Attributions Scott Hodge President

Andrew Lundeen Manager of Federal Projects

Kyle Pomerleau Economist Alan Cole Economist

Publications Donnie Johnson Publications Manager Dan Carvajal Publications Associate, Designer

About the Tax FoundationThe Tax Foundation is the nation’s leading independent tax policy research organization. Since 1937, our principled research, insightful analysis, and engaged experts have informed smarter tax policy at the federal, state, and local levels.

54 | BUSINESS IN AMERICA ILLUSTRATED

NOTES

NOTES

56 | BUSINESS IN AMERICA ILLUSTRATED

NOTES

Americans often look at businesses impersonally. We think of them as lifeless entities that earn profits and don’t do much else. When we think of businesses this way, it becomes very easy to think that business taxes are somehow different than other taxes.

But the reality is that businesses are simply groups of people; they are workers, consumers, and shareholders. This means that when we tax businesses, we actually tax people.