Embed Size (px)

Citation preview

EURAM 2014 June 4-7 Valencia Spain

Business Case Control:

The Key to Project Portfolio Success or Merely a Matter of Form?

Julian Kopmann,* Alexander Kock**, Catherine P Killen ***, and Hans Georg

Gemuenden****

* Technical University of Berlin (TU-Berlin), Institut für Technologie und Management

(ITM)

** Technical University of Darmstadt, Department of Law and Economics, [email protected]

darmstadt.de

*** University of Technology Sydney, School of Systems, Management and Leadership,

Faculty of Engineering and IT

**** Technical University of Berlin (TU-Berlin), Institut für Technologie und Management

(ITM)

Citation: Kopmann J, Kock A, Killen C P and Gemuenden H G, (2014) “Business case

control: The key to project portfolio success or merely a matter of form?”, European

Academy of Management, EURAM, 4-7 June, Valencia.

Winner IPMA-PMI Best Paper Award.

Abstract

Practitioner and professional organization literature places strong emphasis on business cases

with the expectation that the use of business cases to inform and drive investment decisions

will produce better results. In particular, from a project portfolio perspective the business case

of a project may provide the underlying rationale for value-oriented management. However,

academic research regarding the use of business cases at a project portfolio level is scarce. By

exploring the facets of business case control – encompassing the initial review of project

business cases, the ongoing monitoring during project execution, and the post-project tracking

until the business case is realized – this study investigates the relationship between business

2

control and project portfolio success. Furthermore, we analyze critical enablers and relevant

contingencies for the application of business case control. The results are based on a cross-

industry sample of 183 medium-sized and large companies and rely on two informants from

each firm. We found significant evidence for the positive relationship between business case

control and project portfolio success. In addition, accountability for business case realization

and corresponding incentive systems increase this positive effect. Finally, we found that

contingencies (portfolio size and external turbulence) also have a moderating effect. This

study contributes to research and practice by developing and validating a multi-dimensional

construct for business case control, providing evidence for its effectiveness and enabling

conditions.

Keywords: Project Portfolio Management, Business Case

3

Business Case Control:

The Key to Project Portfolio Success or Merely a Matter of Form?

Introduction

Practitioner and professional organization literature places strong emphasis on business cases

with the expectation that the use of business cases to inform and drive investment decisions

will produce better results. However, little academic research explores the relationship

between the use of business cases and project or portfolio success. In particular there are no

studies at the project portfolio level that investigate the application of business cases for

projects and the corresponding control mechanisms. Some studies suggest that the

mechanisms of a portfolio management process can become a routine „form-filling‟ exercise

if the purpose and benefits of the activities are not clear. If the right level of engagement is not

brought to the form-filling process, such as when business case templates must be completed,

the resulting information will not be suitable for decision making (Christiansen and Varnes,

2008). This paper takes a project portfolio perspective to investigate whether business case

control does indeed contribute to project portfolio success, or whether business cases can be

seen as merely „a matter of form‟ (or just another form to complete) in the project portfolio

management process.

The interest in portfolio-level management approaches has escalated as more and more

activities in organizations are executed by projects (Bredin and Söderlund, 2006; Midler,

1995). Projects are the preferred modus operandi when specific goals, which differ from the

day-to-day routine of organizations, need to be achieved in a purposeful and efficient manner.

However, a common criticism is that project management too often focuses on technical

aspects or cost and time restrictions rather than on the achievement of purposeful goals

(Atkinson, 1999; Cooke-Davies, 2007). Paradoxically, research has shown that organizations

continue to increase their investments in projects, even while most projects fail to deliver the

intended goals (Zwikael and Smyrk, 2012).

4

Cooke-Davies (2007) suggests that, in the project management discipline, the focus for

success measurement has been influenced by its origins in the engineering and construction

discipline. Success measures in project management tend to rely on the fulfillment of

technical requirements rather than the creation of value. This may be because construction

and engineering projects are typically based on contracts, which draw a strong distinction

between the contractor‟s and the client‟s responsibility. The project contractor is in charge of

delivering certain artifacts that are technically specified in the contract, while it is the client‟s

responsibility to exploit these artifacts and thus create additional value. Hence, the contractor

(project manager) is more concerned about the fulfillment of these requirements than about its

actual exploitation and the generation of benefits.

Despite the traditional focus on narrow technical measures for project success, in recent

decades project management research has advanced the understanding of project success and

has had continuous influence on the corresponding purposeful management of projects (Ika,

2009). The explicit distinction between project output (artifacts produced by a project),

project outcome (desired, measurable end-effect created by the exploitation of project outputs

by certain stakeholders) and benefits (flow of value triggered by the realization of target

outcomes) provides a framework to analyze established project management practices

(Zwikael and Smyrk, 2011; Zwikael and Smyrk, 2012). This research on project success and

benefits management calls for a paradigm shift in the understanding of project success from

output to outcome orientation with an emphasis on value creation rather than product creation

(Cohen and Graham, 2001; Winter and Szczepanek, 2009). These initiatives are not purely an

academic concern; practitioners and professional organizations also emphasize the importance

of methods that focus on the management of benefits and the creation of value (OGC, 2010,

2011a, 2011b; PMI, 2013c).

5

This context highlights the vital relevance of the business case for the project (referred to in

this paper as the „project business case‟ or simply the „business case‟). The business case

describes why and how the execution of a project can be beneficial for an organization. The

Association of Project Management (APM) defines a business case as the justification for a

project that evaluates the benefits and costs and considers alternative options as well as

opportunity costs (APM, 2006). The business case forms the underlying rationale for an

organization to invest in a project and sets the general conditions for the project scope.

Accordingly, the goal of a project is the realization of the benefits described in the business

case. The creation of value requires that the project management process focuses on the

project‟s business case and not solely on technical requirements.

The business case not only provides directions for project management but is also the basis

for decision making on a project portfolio level. Such decisions often involve the allocation of

limited resources through holistic analysis of project proposals, with the aim of maximizing

the value of the selected project portfolio. Furthermore, ongoing projects require regular re-

evaluation of benefits because they compete for the same resources as new project proposals

(Archer and Ghasemzadeh, 1999; Cooper et al., 2001). There is a substantial body of research

on project portfolio selection processes (i.e. Archer and Ghasemzadeh, 1999; Archer and

Ghasemzadeh, 2004; Ghapanchi et al., 2012; Müller et al., 2008) and evidence of wide

adoption of project portfolio processes in practice (OGC, 2011a; PMI, 2013c). However, the

quality of the project portfolio selection is constrained by the quality of the information

available from the business cases provided for each project. It follows that a sound business

case may be an antecedent to both project and project portfolio success.

While the importance of benefits management and the management of value is well

acknowledged (Morris et al., 2011) and the relevance of the business case is recognized

(Cooke-Davies, 2007), research on project business cases is scarce. In particular, from a

6

project portfolio perspective, where the main decisions in terms of project prioritization,

selection, control and termination are made, the project business case has not been subject to

academic research. Since there is no quantitative empirical analysis regarding application of

project business cases on a portfolio level, no measurement procedures are available. In

addition, although practitioners describe benefits management practices as key success factors

for project and project portfolio success, to the best of our knowledge there is no quantitative

empirical evidence for this claim.

This paper therefore analyzes the application of project business cases and the corresponding

control mechanisms at the project portfolio level, which we call business case control. The

following research questions guide this study in addressing the existence, effectiveness, and

contingencies of business case control:

1. What is business case control in project portfolio management and how can its application

be measured?

2. Does the application of project business case control contribute to project portfolio

success?

3. Which enablers and contingencies affect the performance contribution of business case

control?

This study empirically addresses these questions using an analysis of a cross-industry sample

of 183 firms. We use a double-informant design to address the issue of common method bias

(Podsakoff et al., 2003). This research offers several contributions to the literature on project

and project portfolio management: First, by combining literature streams from several aspects

of business case control we conceptually develop and empirically validate a multidimensional

construct called business case control. We demonstrate its relevance by empirically showing

the positive impact of business case control on project portfolio success. Next, we consider

the influence of the actors in the process and identify and empirically validate critical

7

enabling conditions for business case control. We find that accountability for business cases

and portfolio-based incentives both increase the positive effect of business case control.

Finally, we identify critical internal and external contingencies for the benefits of business

case control. The performance effects of business case control differ depending on the size of

the portfolio and the turbulence of the environment.

The paper is structured as follows. In the next section, research from project management,

project portfolio management, and benefits realization literature is reviewed to define the

construct business case control and to develop a framework for its relationship to project

portfolio success. After describing the sample and methods in the subsequent section, we

present the empirical results and discuss their implications for theory and practice.

Conceptual Framework and Hypotheses

Business case

The business case forms the raison d`être for any project (Cooke-Davies, 2007). It

demonstrates the advantages of organizational investment in a project and illustrates how the

project aims to create value (Jenner, 2010). Although the term „business case‟ is in common

use commercially, there is no accepted definition of the term for research purposes. Similarly,

in the rich entrepreneurship literature the analogous concept of business models also lacks a

common understanding (Zott et al., 2011).

In reflection of the established application of business cases in commercial environments,

professional organizations and practitioner-oriented literature provide a wide range of

business case definitions. Table 1 summarizes the definitions offered by the main project

management institutions.

-----------------------

Insert Table 1 here

-----------------------

8

These definitions reflect perspectives from the project, program, and portfolio level and differ

in terms of explicitness and their level of detail. However, the definitions are consistent

regarding the business case scope and also in their inclusion of recommendations for the use

of the business case throughout the project‟s life-cycle. Drawing upon these definitions, for

the purposes of this study we characterize a project business case as follows:

A project business case provides the necessary information to enable management to

prioritize projects and decide whether or not a project is worth funding and contains

estimates regarding the benefits, timescales, costs, and risks of a project.

Furthermore, several definitions refer also to the application of a business case and state that a

business case needs to be reviewed periodically and may require independent reviews (in the

case of complex business cases).

The business case definition and the recommendations for its application refer to a superior

level where funding decisions are made and the project portfolio is administered. Project

portfolio management prioritizes projects, makes funding and resource allocation decisions,

and constantly monitors the project portfolio (Blichfeldt and Eskerod, 2008). To facilitate

comparison of project information, the portfolio management process often dictates that

business case information is input on a standard form or template. The business case is

expected to provide essential information for the decisions on the portfolio level.

Furthermore, the use of business cases from a project portfolio perspective is not supposed to

maximize the benefits of a single project, but rather maximize the value of the entirety of the

investment in projects, namely project portfolio success. Hence, we consider the project

portfolio management literature to establish an understanding of the relevant management

system.

9

Project portfolio management and project portfolio success

A portfolio is a group of projects that are carried out and managed within an organization

(Archer and Ghasemzadeh, 1999) and compete for a shared pool of resources (Turner and

Müller, 2003). Cooper et al. (2001) summarized the purpose of project portfolio management

as “doing the right things” and contrasted it with project management that is about “doing

things right”. According to Cooper (2001), the right projects are the ones that provide

maximum value, achieve a balance and align with strategy. More recently researchers have

sought to develop a more comprehensive definition of project portfolio success (Cooper et al.,

2004a, 2004b; Killen et al., 2008; Martinsuo and Lehtonen, 2007; Meskendahl, 2010; Müller

et al., 2008; Teller and Kock, 2013). The present study defines project portfolio success

through five dimensions following prior research (Jonas et al., 2013; Teller and Kock, 2013;

Voss and Kock, 2013).

Projects are the main vehicles for the implementation of corporate strategies in many

organizations (Artto et al., 2008; Dietrich and Lehtonen, 2005; Killen et al., 2008; Morris and

Jamieson, 2005; Yelin, 2005). Hence, the strategy implementation success of a project

portfolio (Meskendahl, 2010) reflects successful project portfolio management and constitutes

the first success dimension. Future preparedness reflects the long-term perspective on

portfolio success and describes the organizations preparedness for the future in terms of

technological assets and competences (Shenhar et al., 2001). It evaluates the long-term

benefits offered by a project portfolio (i.e. creation of new markets and development of new

technologies and capabilities) (Voss and Kock, 2013). Portfolio balance concerns the

equilibrium of risks, long- and short-term opportunities and the steady utilization of resources

within the project portfolio‟s execution (Killen et al., 2008; Teller et al., 2012). Synergy

exploitation represents the added value that emerges from dedicated portfolio management in

addition to the single projects‟ contribution through the capitalization of interdependencies

10

and the avoidance of redundancies (Jonas, 2010; Meskendahl, 2010). The dimension average

project success corresponds to the assertion that project portfolio management is an

antecedent to project success (Killen et al., 2008; Martinsuo and Lehtonen, 2007). Following

the research on project success, the respective indicators for average project success should

not refer to the adherence to cost, time and scope (which reflects project management

success), but rather to quality of the project‟s outcome and the satisfaction of the project

customer (Atkinson, 1999). Hence, it focuses on project effectiveness instead of efficiency

(Lechler and Dvir, 2010).

In accordance with the definition of success, the interpretation of project portfolio

management extends beyond the initial evaluation, prioritization, and selection of projects and

also incorporates the allocation of resources, concurrent re-evaluation of projects, and

exploitation of the project portfolio (Blichfeldt and Eskerod, 2008; Engwall and Jerbrant,

2003; Hendriks et al., 1999). Jonas (2010) analyzed the project portfolio manager‟s tasks and

defined four phases of project portfolio management:

The first phase (portfolio structuring) refers to the definition of a target portfolio in alignment

with the corporate strategy (Morris and Jamieson, 2005; Platje et al., 1994) and comprises the

evaluation, prioritization, and selection of projects. Previous studies have identified

information quality and transparency over the project portfolio as the basis for successful

decision making and prioritization of projects (Jonas et al., 2013; Teller et al., 2012). Cooper

et al. (2001) described the lack of information quality as a major barrier to project portfolio

success.

The second phase (resource allocation) concerns the cross-project planning and allocation of

resources that reflect the projects priorities and aim for optimal utilization of available

resources (in particular human resources). In theory, this phase is very closely linked to the

portfolio structuring phase. However, in practice resource allocation is often not aligned with

11

the strategic priorities of the portfolio. Research identified the resource allocation as a main

challenge for multi-project organizations (Hendriks et al., 1999). Due to the competition for

scarce common resources, conflicts may arise between projects and between projects and the

line organization (Engwall and Jerbrant, 2003). Two reasons for the failure of resource

allocation have been identified by Engwall and Jerbrandt: 1) the dysfunction of classical

management accounting systems for multi-project environments which leads to contradicting

goals of projects as resource users and line management as resource providers and 2) the

opportunistic behavior of project management which overstates project priority and urgency

in order to get required resources assigned.

The third phase (portfolio steering) comprises continuous project portfolio management tasks

for the coordination and control of the project portfolio (Müller et al., 2008). Research has

shown that the organization‟s ability to proactively decide about a project‟s continued

existence or termination is an antecedent to portfolio success in terms of strategic fit (Unger et

al., 2012). These capabilities, as well as the overall project portfolio management

performance, depend heavily on the information available to management. Empirical studies

have shown that information quality is a linchpin of project portfolio management success

(Dietrich and Lehtonen, 2005; Jonas et al., 2013; Teller et al., 2012).

The fourth phase (organizational learning and portfolio exploitation) has rarely been

discussed in project portfolio management literature and addresses activities which are located

at the end of the project‟s life-cycle (Jonas, 2010). The importance of post-project evaluation

and reviews is highlighted from a learning perspective. There is a common agreement in this

research stream that post-project evaluation and the development of lessons learned helps to

advance the project management practice of an organization and contributes to the success of

subsequent projects (Anbari et al., 2008; Collier et al., 1996; Huemann and Anbari, 2007;

Koners and Goffin, 2007; von Zedtwitz, 2002, 2003). Portfolio exploitation refers to the

12

transition of project outputs to the customer and the transformation of these outputs to

outcomes and benefits. In particular, at the interface between the temporary organization of a

project and the line organization of the customer, essential knowledge and competence may

be lost (Winter and Szczepanek, 2009). Thus, benefits realization management literature

highlights the importance of clearly defined roles acting at this interface (Cooke-Davies,

2007).

These four phases of project portfolio management contribute to portfolio success in different

ways and brings certain challenges. In the structuring phase, portfolio management seeks to

define a target project portfolio that contributes the highest value to the organization. The

main challenge is to establish a sound information basis in terms of accuracy, validity, and

comparability to evaluate and prioritize project proposals for funding. Transparency about the

project portfolio and the relative importance of each project also is a major challenge in the

resource allocation phase. Often the required information for decision making is flawed:

benefits are overstated, costs underestimated (optimism bias), and exaggerated urgency is

proclaimed to undermine the selection process and falsely achieve high priority when it comes

to resource allocation (Engwall and Jerbrant, 2003; Gardiner and Stewart, 2000; Jenner,

2009).

In the steering phase, portfolio management aims to assure that the project portfolio will

contribute to the organizational goals as planned in terms of benefits, costs, progress, and

strategic contribution (OGC, 2011a). For a purposeful steering of the portfolio, information

about the projects and the external environment needs to be considered. Deviations from

project plans and changing external conditions both have the potential to result in the loss of

expected project benefits; these conditions may require re-evaluation and re-prioritization of

these projects through the portfolio management process. However, in practice ongoing

13

control mechanisms to ensure the validity of a project‟s business case are rarely implemented

(Gardiner and Stewart, 2000).

In the learning and portfolio exploitation phase, portfolio management tries to improve its

practice by reviewing the results of former decisions. Here, the main problem is that most

companies simply have not implemented respective processes successfully (Anbari et al.,

2008; Newell et al., 2006). After project closure, the motivation to invest further effort is

relatively low for several reasons (Busby, 1999). From a project-level perspective this is

understandable - the project team has already gained learning from the project and does not

benefit from a further formal process. Nevertheless, from an organizational or portfolio level

valuable assets are lost if learning and exploitation processes are not in place.

With the project portfolio management phases and the respective goals and challenges in

mind, we describe the role of the project business case and its application from a project

portfolio perspective (business case control) in the following section.

Business Case Control

In the present study, business case control describes the application of business cases from a

project portfolio-level control perspective. The scope of control comprises more than merely

monitoring; it encompasses planning, monitoring, reporting, taking necessary corrective

action, and re-planning (Morris, 2013).

We propose that business case control comprises three elements: 1) the use of business cases

for the evaluation and prioritization of project proposals (business case existence), 2) the

continuous monitoring of the validity of ongoing projects (business case monitoring) and 3)

the tracking of the business case in terms of benefits realized after project completion

(business case tracking). These three elements are consecutive in their application, in that

each dimension requires a certain proficiency of the previous one, and can be assigned to the

14

four project portfolio phases. Hereafter, each of the three dimensions of business case control

is described in more detail and its contribution to project portfolio success is analyzed.

Business case existence refers to application of business cases within the portfolio structuring

and resource allocation phases. Addressing the main issues of these phases, business case

existence not only encompasses the presence of a business case, but rather its quality in terms

of accuracy, validity, and comparability. To ensure high quality business cases, project

portfolio management have to establish common rules and guidelines for the business case

design (often through standard templates for forms) and perform rigor and independent

business case reviews (Cooke-Davies, 2007; GAPPS, 2011).

Business case monitoring is an activity that accompanies the project from initiation until

closure and is processed in the portfolio steering phase. It refers to the revalidation of a

project‟s business case considering changing project scope and timing as well as changing

environmental conditions. Gardiner and Steward (2000) emphasized the importance of the

continuous monitoring and stated that most companies discover deviations and changing

conditions too late to react. In the same vein, Dvir and Lechler (2004) suggests that the effect

of initial planning quality cannot compensate the effect on project success that changes during

a project life-cycle have. Hence, the ongoing monitoring of the business case enables

management to make proactive decisions about the portfolio of projects; early access to

information will widen options and may involve the adjustment of project scope or urgency –

or the cancelation of projects to make way for alternate opportunities.

Business case tracking refers to the evaluation of project results regarding the realization of

the business case. As the added value described in the business case usually does not refer to

the direct project output, but rather to the outcomes and benefits which result from the output,

business case tracking takes place after project completion. While the contribution of post-

project reviews to organizational learning is widely acknowledged in literature (Anbari et al.,

15

2008; Collier et al., 1996; Huemann and Anbari, 2007; Koners and Goffin, 2007; von

Zedtwitz, 2002, 2003), we propose an additional benefit of business case tracking. The very

existence of post-project reviews affects the behavior of those responsible for the business

case and prevents them from overstating benefits and understating efforts in the business case.

These definitions show how each of three dimensions of business case control supports

project portfolio management and has the potential to address some of the main challenges in

project portfolio management. In this way, business case control corresponds to prior

research, which claims that project portfolio controlling should not only applied for project

evaluation and selection (Archer and Ghasemzadeh, 1999; Archer and Ghasemzadeh, 2004;

Müller et al., 2008).

-----------------------

Insert Table 2 here

-----------------------

Business case control contributes to project portfolio success by increasing the transparency

over benefits of project proposals, reducing the optimism bias and flawed information, by

enabling the portfolio management to answer to changing conditions in a timely manner and

by fostering organizational learning. Hence, we argue that the application of business case

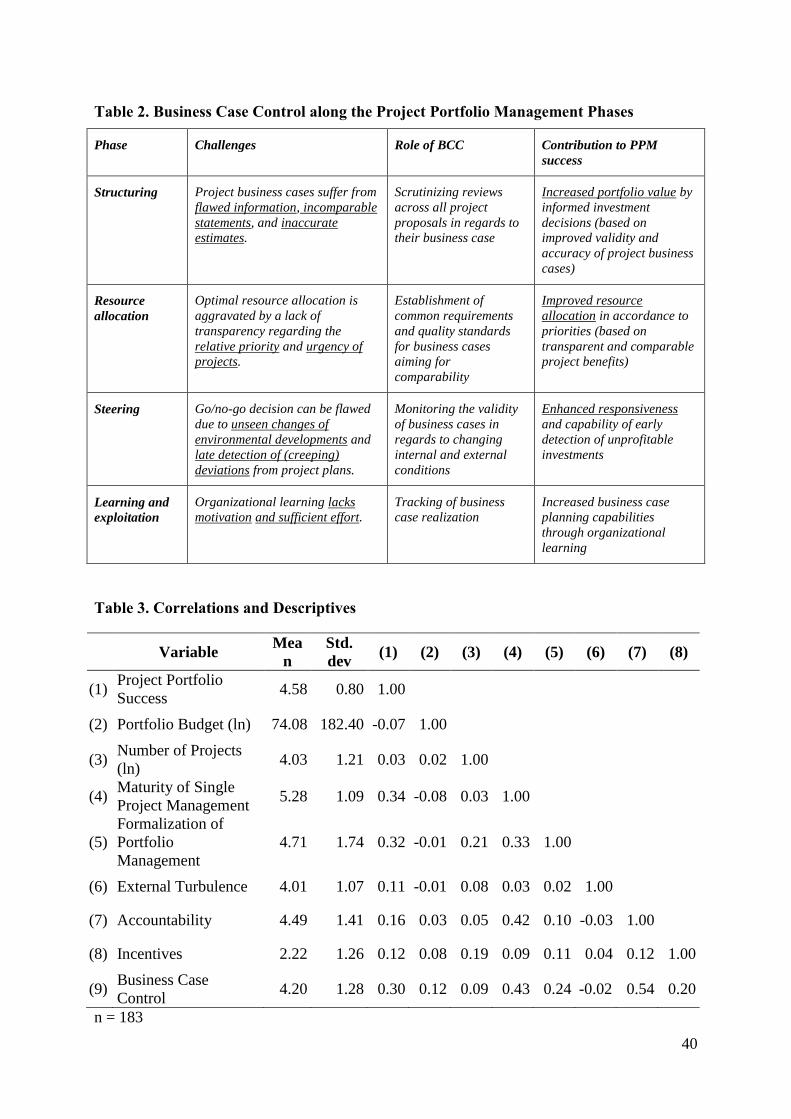

control is beneficial for project portfolio success. Table 2 summarizes how business case

control supports the project portfolio management process and by that contributes to project

portfolio success.

H1: The application of business case control is positively related to project portfolio success.

Enablers of Business Case Control

Business case control emphasizes the relevance of the value created by a project portfolio. We

have hypothesized that the process of business case control contributes to project portfolio

success. But drawing only on the existence of a process would show an incomplete picture.

16

The process forms the basis for a purposeful management, but the actors are of pivotal

importance when it comes to successful implementation (Beringer et al., 2013; Jonas, 2010).

In the same vein, Elonen and Artto (2003) stated that a lack of commitment, and unclear roles

and responsibilities are some of the major problem areas in multi-project management.

The benefits management literature often highlights the importance of „benefits owners‟ who

are in charge of benefits realization (Cooke-Davies, 2007; Morris, 2013; OGC, 2010, 2011a,

2011b; Zwikael and Smyrk, 2012). However, there is no agreement in literature where this

role is located in an organization. The OGC stated that a separate tier of management is not

required, but roles and responsibilities of the actors related to project, program, and portfolio

management should be extended (OGC, 2010). However, role assignment is a „toothless tiger‟

if it lacks corresponding stimuli to assure that respective actors perform as intended. Hence,

this study not so much examines the location or organizational level of the roles for benefits

realization, but rather the drivers that facilitate responsibility and motivation in terms of

accountability and incentive systems.

Accountability for the business case

Morris (Morris, 2013) stated that it is very important to identify benefits owners who are in

charge of „harvesting‟ project outcomes. Since benefits are mostly realized after project

completion (Zwikael and Smyrk, 2012), an overarching responsibility is required that outlives

the project (Cooke-Davies, 2007). In addition, a quantitative study conducted by Dvir (2005)

provides evidence that the project management support for the turn-over of project outputs to

the customer is positively related to project success. Furthermore, over-optimistic estimates

are associated with a lack of accountability that can cause the business case to be flawed

(Jenner, 2009). Nevertheless, in practice the assignment of such responsibilities is often a

difficult issue. (OGC, 2011a).

17

Zwikael and Smyrk (2011) described the key players within the outcome (business case)

realization phase. They underpinned the importance of the benefits owner and the line

manager in the utilization of project outputs, whereas the responsibility of the project manager

ends with delivery these outputs. Hence, the benefits owner and the line management are

responsible for the realization of the business case. However, they acknowledge that the

project manager may be the best candidate to support the realization phase, due to their

“intimate familiarity with the outputs that have been implemented”(Zwikael and Smyrk, 2011,

p. 264) is required.

It is quite common to evaluate the project managers‟ success based on the project

management performance (adherence to cost, time and scope/quality) (IPMA, 2006).

Information regarding adherence to cost and time are usually maintained quite well in the

course of a project, while the scope and quality are specified in the project scope statement

and verified at project close-out (PMI, 2013a). The success of the benefits ownership, on the

other hand, is measured against the business case realization (Zwikael and Smyrk, 2011).

Hence, those responsible and accountable for the business case realization will be highly

interested in information regarding business case realization.

Altogether, based on previous research it can be assumed that the assignment of

accountabilities plays an important role in the context of business case realization. We argue

that these accountabilities facilitate the effect of business case control on project portfolio

success by reducing optimism bias and increasing the relevance and utilization of the

information provided by business case control. By that, business case accountability fosters

the relationship between business case control and project portfolio success.

H2: The relationship between business case control and project portfolio success is stronger

when business case accountability is high (positive interaction).

Incentives for the business case

18

Monetary incentive systems have become increasingly popular in recent years (Gneezy et al.,

2011). Eisenhardt (1989) draws upon principal-agent theory to describe how incentive

systems are designed to align the interest of the agents with goals of the principal. However,

the impact incentive systems have on motivation is controversially discussed in research (Frey

and Jegen, 2001). Critics argue that intrinsic motivation, which is important to produce a

desired behavior, is undermined by extrinsic incentives, an issue also known as crowding-out

effect. (Deci et al., 1999; Frey and Jegen, 2001; Gneezy et al., 2011; Ryan and Deci, 2000).

In project management research the use of incentives or disincentives within project

contracting is generally supported and has been subject to several studies (Bubshait, 2003;

Jaafari, 1996; Meng and Gallagher, 2012; Shr and Chen, 2004). However, in the context of

business case control the drafting of contracts is rather a pre-condition and may be an input

factor to the evaluation of a business case. Hence, the present study does not focus on contract

design but rather on individual incentives for the actors involved in the realization of a

business case.

Tosi et al. (1997) provided evidence that incentive alignment has a stronger effect than

monitoring in order to ensure that agents are acting in the interest of the owner. Although,

their study could not provide evidence for the interaction effect between monitoring and

incentives, Tosi et al. highlighted the relevance of this effect as described Milgrom and

Roberts (1992). Accordingly, accurate monitoring is a required prerequisite to align the

actors‟ behavior with the owner‟s interest by setting respective incentives.

In the context of this study the owner is the organization that invests in the project proposals.

The interest of the organization is not necessarily the success of single projects in terms of its

outputs, but rather the value added by the whole portfolio (Zwikael and Smyrk, 2012). In this

context, the information provided by business case control constitutes the basis for an

incentive system that aligns the behavior of the actors to the owner‟s interest. Hence, only if

19

an organization is transparent about the value added by the project portfolio, do incentives

result in purposeful management behavior and contribute to project portfolio success.

Therefore, we suggest that incentive systems that are based on project portfolio success and

business case control are complementary in their effect on success.

H3: The relationship between business case control and project portfolio success is stronger

when incentives for the project portfolio success are high (positive interaction).

Contingencies of business case control

Not all portfolios are alike (Teller et al., 2012; Voss and Kock, 2013). Therefore, with

reference to the contingency theory (Donaldson, 2001), we hypothesize that there are further

moderating effects that affect the relationship between business case control and project

portfolio success. While the previously discussed enablers of business case control are part of

the management system itself, contingencies represents circumstances that are outside the

management‟s area of influence. Project portfolio management research often refers to

complexity as a main contingency (Heising, 2012; Teller et al., 2012; Voss and Kock, 2013).

However, there are numerous interpretations of complexity (Kim and Wilemon, 2009). The

present study differentiates internal complexity, in terms of portfolio size, and external

complexity, measured by external turbulence (Sethi and Iqbal, 2008).

Portfolio size matters. Researchers argue that the relevance of project portfolio management

and the formalization of portfolio processes increases with the size of an organization

(Martinsuo and Lehtonen, 2007) and its project portfolio (Teller et al., 2012). One of the main

outcomes of business case control is the provision of transparency. The larger a project

portfolio is, the more difficult it is to maintain transparency without dedicated control

functions. Conversely, in small project portfolios the effort to implement and maintain

business case control may not justify the value it contributes. Hence, we argue that the

20

contribution of business case control to project portfolio success increases with the number of

projects that the portfolio comprises.

H4: The relationship between business case controlling and project portfolio success is

stronger with increasing number of projects (positive moderation)

External turbulence affects business cases in two ways. First, a business cases is required to

make assumption regarding future environmental conditions (i.e., exchange rates, behavior of

competitors, market and technological developments). With increasing turbulence, there is

elevated uncertainty about future developments which is generally reflected in the business

case in terms of risk. From a business case control perspective this increases complexity of

the business case, which results in the need for even more rigorous reviews. Second,

unforeseeable and rapidly changing environmental conditions may affect the validity and

longevity of a business case. Hence, close monitoring is required to detect and respond to

these affects in a timely manner. Altogether, we propose that the relevance of business case

control is higher when external turbulence is high.

H5: The relationship between business case controlling and project portfolio success is

stronger in more turbulent environments (positive moderation).

-----------------------

Insert Figure 1 here

-----------------------

Figure 1 summarizes the conceptual model and all hypotheses.

Method

Sample

We use a cross-industry sample of medium-sized to large firms in Germany to test the

hypotheses. The object of analysis is the project portfolio of the firm or a business unit in case

21

of large firms. For each project portfolio we contacted two key informants – a decision maker

and a coordinator. Decision maker informants had to have decision authority over the

portfolio in deciding on initiation, termination, or reprioritization of projects. Typical

positions were CEO, CIO, head of business unit or head of R&D. Coordinator informants had

to have a good overview of the project landscape and were in charge of actively managing the

portfolio. They had typical titles such as portfolio manager, department manager, or head of

PMO. This two-informant approach allowed integrating information from different

perspectives and hierarchies within each firm. More importantly, this study design avoids

common method bias (Podsakoff et al., 2003), because decision maker informants assessed

the dependent variable project portfolio success and coordinator informants assessed the

independent variables.

We contacted firms with mail solicitation explaining the study in general and we sent a call

for registration to potential coordinator informants or their superiors. Afterwards we contacted

them by phone to encourage their participation and to register for the study. All registered

informants received e-mail with a personal letter explaining the multi-informant design and

the questionnaires with an introduction describing the terms and definitions. To increase the

response rate, follow-up phone calls were conducted and reminder e-mails were sent. We

received 189 decision maker questionnaires and 195 coordinator questionnaires from 200

firms, resulting in 184 matched dyads with data from both types of informants. One

observation had to be removed from analysis due to missing data. After study evaluation each

firm received an individual report of the findings and the overall study results were presented,

discussed, and validated on a conference with about 90 participants. The 183 firms

representing the final sample come from diverse industries (26% automotive, 18 %

electronics/IT, 16% finance, 11 % construction and utility, 8 % health care, 7 % logistics, 5%

pharmaceuticals/chemicals, 9 % others). The sample shows a reasonable spread according to

22

firm size with 32 % having less than 500, 29 % between 500 and 2000, and 39 % more than

2.000 employees. Portfolio budget was less than 20 million € in 37 %, between 20 and 100

million € in 39 %, and higher than 100 million € in 24 % of the portfolios. The median

number of projects in a portfolio is 50.

Measurement

We use multi-item scales for the constructs, which are anchored from 1, “strongly disagree”,

to 7, “strongly agree”. Since for most of the variables, there were no existing scales available

in the literature, we operationalized these scales following previous conceptual work: all

scales were pretested with 12 representatives from academia and industry to assure face

validity of constructs, improve item wording, and remove ambiguity. We validated the scales

using principal components factor analysis (PCFA) and confirmatory factor analysis (CFA)

(Ahire and Devaraj, 2001). PCFA tests for unidimensionality of each scale by checking

whether all items load onto a single factor. Cronbach‟s Alpha is used to assess scale reliability

with acceptable values larger than 0.7. The CFA confirmed the measurement model and the

second-order structure of business case control and project portfolio success. We follow the

guidelines of Hu and Bentler (1998) to evaluate structural equation models. They suggest a

Comparative Fit Index (CFI) of 0.95 for good and of 0.90 for acceptable fit, and a

Standardized Root Mean Squared Residual (SRMSR) below 0.08 and a Root Mean Squared

Error of Approximation (RMSEA) below 0.06 for good fit.

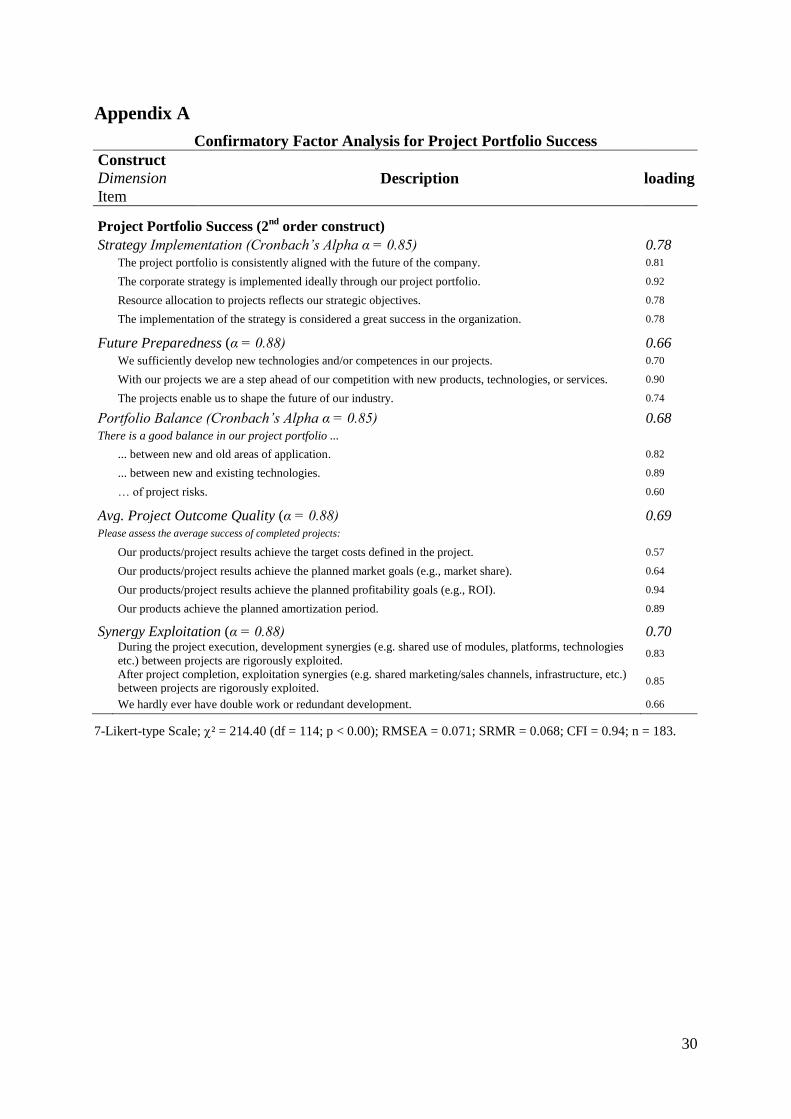

Dependent variable. Project portfolio success is measured as a five-dimensional second-order

construct using dimensions and their items from existing literature (Jonas et al., 2013; Teller

and Kock, 2013; Voss and Kock, 2013): strategy implementation (4 items), future

preparedness (3 items), portfolio balance (3 items), average project outcome (4 items), and

synergy exploitation (3). PCFA showed that all items load highly on their respective

dimensions with no cross-loadings above 0.30. The CFA confirms the second-order structure

23

in that all dimensions load highly on the overall construct project portfolio success and the

model fit is acceptable. The results and item wordings are shown in Appendix A. The

coordinator informant also assessed all items for project portfolio success. Although we do

not use it for hypothesis testing, we can use the information for further validation of the scale.

The coordinator assessment results in the same factor structure with similar loadings and is

highly correlated with the decision maker assessment (r=0.57, p<0.000), which gives strong

confidence in the validity of our measure.

Independent and moderator variable. We developed measures for business case control based

on conceptual literature (Cooke-Davies, 2007; OGC, 2010, 2011a; PMI, 2013c, 2013b) along

three dimensions: business case existence (5 items), business case monitoring (4 items), and

business case tracking (5 items). PCFA showed high cross-loadings in one item, which was

consequently eliminated. Accountability was measured using 5 items (Cooke-Davies, 2007;

Winter and Szczepanek, 2009). One item was eliminated. Incentives for portfolio success was

measured using 4 items (based on Milgrom and Roberts, 1992; Tosi et al., 1997).

Environmental turbulence included 3 technology and 3 market turbulence items taken from

(Sethi and Iqbal, 2008). Finally, number of projects is the natural logarithm of the number of

projects that comprise the portfolio. The CFA on all latent independent variables as shown in

Appendix B has an acceptable fit and confirms the second-order structure of business case

control. The three dimensions of business case control are highly correlated as the high

loadings show, yet they are empirically distinct dimensions.

Control variables. We further introduce three variables in our model that might affect project

portfolio success and should be controlled for. The maturity of single project management has

been shown to affect project portfolio management, as it might be a necessary condition for

its effectiveness (Martinsuo and Lehtonen, 2007; Teller et al., 2012). Single project

management maturity (Cronbach‟s Alpha = 0.82) is measured with 6 items based on (Teller et

24

al., 2012). On the level of the portfolio we control for the formalization of the PPM process

(Alpha = 0.93) that we measure with four items (Teller et al., 2012). In addition to the number

of projects in the portfolio, which is a moderator in this study, we finally control for the

budget of the portfolio measured as the natural logarithm of the budget in millions of Euro.

Correlations and descriptives for all variables are shown in table 3.

-----------------------

Insert Table 3 here

-----------------------

Results

We use ordinary least squares regression in order to test the hypotheses. The results are

displayed in table 4. The first model only contains the direct effects of all control and

moderator variables. Only the maturity of single project management and the formalization of

portfolio management are significantly related to project portfolio success (unstandardized

regression coefficient b = 0.17, p<0.01, and b = 0.11, p<0.01, respectively). Model 2

introduces business case control to the model, which has a positive and significant coefficient

(b=0.12, p<0.05). The model explains 21 % of variance in portfolio success, which can be

considered as very satisfactory if we consider that it is not inflated by common method bias.

The basic hypothesis that business case control is positively associated with project portfolio

success is therefore supported by the data. Model 3 to 6 test the moderation hypotheses using

the procedures proposed by (Aiken et al., 1991). In each model we introduce the product-term

between the centered independent variable and the centered moderator variable. If the

coefficient is significant and the explained variance of the model is significantly increased in

comparison to model 2, the moderation hypothesis is supported.

-----------------------

Insert Table 4 here

-----------------------

25

In model 3 the interaction effect with accountability for benefits realization is positive and

significant (b=0.06, p<0.05), which supports hypothesis 2. Incentives for project portfolio

success also show a positive interaction effect (b=0.11, p<0.01) in model 4, which is in

support of hypothesis 3. Also external contingencies significantly influence the benefits of

business case control. With increasing number of projects (b=0.11, p<0.01) and under higher

external turbulence (b=0.12, p<0.01) the relationship between business case control and

project portfolio success becomes stronger, supporting hypotheses 4 and 5, respectively.

For the visualization of the moderation effects we use marginal plots instead of simple slopes

as they show the strength and significance of the effect of business case control on project

portfolio success for each value of the moderator (Brambor et al., 2006). The solid lines in

figures 2 to 5 represent the overall effect over the whole range of moderator values. The

dashed lines represent 95%-confidence intervals. Figure 2 shows that business case control

only has a positive and significant effect on project portfolio success if accountability for

benefits realization is above 4, which is still lower than the mean in this sample (4.5). Lower

values in accountability diminish the effect of business case control on success. A similar

effect can be observed in figure 3. When incentives are higher than approximately 2, the

effect of business case control becomes significantly positive. Since the mean in our sample is

2.22, the results indicate that an above average degree of incentives for portfolio success leads

to a positive effect of business case control and below average incentives lead to a non-

significant effect. Figure 4 shows the effect for the number of projects (ln). Above a value of

4 (i.e. roughly 50 projects) the benefits of business case control become significantly positive,

otherwise the effect is non-significant. Concerning external turbulence, Figure 5 informs that

above the average turbulence of roughly 4 the effects are positive and significant and below

they are insignificant. Notably, none of the moderators leads to significantly negative effects

of business case control.

26

----------------------------

Insert Figures 2-5 here

----------------------------

Discussion

Implications for Research

The present study examined the role of business case control within project portfolio

management by employing literature from project, project portfolio and benefits realization

management and validated our hypotheses by empirical research. By doing so, this paper

provides the following main contributions to future research.

First, this study introduces the construct of business case control and shows its predictive

relevance for project portfolio success. Based on conceptual literature we have developed a

multi-dimensional conceptualization of business case control consisting of the dimensions

existence, monitoring, and tracking. We empirically validated the measurement of this

second-order construct by confirmatory factor analysis and find that the three dimensions are

highly correlated yet distinct. Furthermore, we find considerable variance of the overall

construct in our sample and can differentiate it from other related constructs in project

portfolio management research such as single project management maturity and the

formalization of project portfolio management. The three dimensions of business case control

suggest that project portfolio management concerns more than the initial structuring of a

project portfolio and highlight the importance of the steering and exploitation phases of

portfolio management. The study reveals that some firms currently incorporate business case

control more intensively than others. More importantly, for the very first time the application

of business case control as a method of benefits management on project portfolio level has

been subject to a large-scale quantitative study. Until now, research on benefits management

has mainly been anecdotal and primarily based on case studies. This study provides the

statistical evidence for the effectiveness of business case control with respect to project

27

portfolio success. By demonstrating the relevance of business case control, this study

contributes to research on project and project portfolio management. Future research can

utilize and further test the construct in different contexts.

Second, we have identified core enablers of business case control by showing that the control

process is positively moderated by dedicated roles, which provide accountability and

motivation for business case realization. In particular, the interaction effect between

monitoring and incentives has been subject to discussion while prior studies failed to confirm

this effect (Mahaney and Lederer, 2010; Tosi et al., 1997). These findings are valuable

because they show the conditions under which business case control works. We find that

without accountability and incentives for portfolio success business case control is ineffective.

Third, this research contributes to contingency research in project management by identifying

appropriate management practices depending on the context (Howell et al., 2010; Shenhar,

2001; Teller et al., 2012). We analyzed under which contextual conditions business case

control contributes to project portfolio success and found the control to be more effective in

larger project portfolios and more turbulent environments. These findings may open avenues

for further research that builds upon organizational control theory (Eisenhardt, 1985; Ouchi,

1977, 1979). The theory distinguishes between clan, process and, outcome control; the

effectiveness of each type of control is proposed to vary with the environment in which is it

applied (Ouchi, 1977, 1979). Accordingly, outcome control is the means of choice in complex

environments and when environmental changes are difficult to predict (Turner and Makhija,

2006). While the traditional project management control measures of time, cost, and quality

are types of process control, business case control represents an outcome control method

(Schultz et al., 2013). Hence, the findings in this study correspond with the insights from

organizational control theory and could lead the way for further research facilitating both

streams of literature organizational control and project portfolio management.

28

Implications for Management

This study provides a comprehensive description of business case control that can be used by

project portfolio managers to benchmark their current practice. In particular, the relevance of

business case monitoring and tracking and the respective relevance of the later phases of

project portfolio management indicate avenues for improving and extending project portfolio

management practices.

Furthermore, this study provides directions for the implementation of a business case control

process. Both the assignment of accountability for the business case, and the setting of

incentives for project portfolio success, facilitate the effect of business case control and hence

should be considered jointly. However, it has been also shown that business case control is

not always an appropriate approach for a project portfolio. Managers can build on this study

in order to evaluate the usefulness of business case control by taking internal and external

contingencies into account.

Altogether, it has been shown that the business case control is not a bureaucratic constraint or

a matter of form, but that it contributes to project portfolio success.

Limitations and Avenues for Future Research

There are some limitations of this research that need to be considered when interpreting the

results. First, although we use a two-informant research design to avoid common method bias,

a methodical limitation is that the analysis relies on cross-sectional data. We assume that

applying business case control in project portfolio management will increase portfolio success

and we could show a positive association even when controlling for the maturity of single

project management and the formality of project portfolio management. However, we cannot

rule out the possibility that the causation is reverse, i.e. that firms invest more in business case

control because they have been successful in the past (e.g. due to more resources at their

disposal). Only a longitudinal study could corroborate the suggested causality.

29

Second, although we could show a significant association between business case control and

success, we do not know the exact mechanisms through which these performance gains come

to pass. Applying business case control may have positive and negative effects that work

simultaneously. For example, too many formal controls may limit creativity and might strain

innovation, which could outweigh the positive effects in some portfolio environments such as

R&D project portfolios. The current study is therefore a good vantage point to further

investigate possible mediation effects and open the black box between business case control

and portfolio success. This type of study could also be done through in-depth qualitative

studies or large-scale quantitative studies.

In this context, an adaption of the success construct might also be adequate. While we used an

established multi-dimensional construct for project portfolio success, there might be other

dependent variables that could be affected by business case control, such as innovativeness of

the portfolio or the motivation of the affected stakeholders. Our results suggest that higher

incentives for portfolio success and more accountability for benefits realization increase the

performance effects of business case control. However, there might by negative effects, such

as the hidden cost of control by undermining motivation (Falk and Kosfeld, 2006). Future

research could therefore also explore other dependent variables that help to uncover the

overall effects of applying business case control in project portfolio management.

Finally, this study concentrated on two enabling conditions and two contingency factors that

facilitate the benefits of business case control. Future research could investigate other

conditions and moderating factors that might be relevant in this context (e.g. type of project,

project customer, industry, strategic orientation and aspects of corporate culture).

30

Appendix A

Confirmatory Factor Analysis for Project Portfolio Success

Construct

Dimension

Item

Description loading

Project Portfolio Success (2nd

order construct)

Strategy Implementation (Cronbach‟s Alpha α = 0.85) 0.78

The project portfolio is consistently aligned with the future of the company. 0.81

The corporate strategy is implemented ideally through our project portfolio. 0.92

Resource allocation to projects reflects our strategic objectives. 0.78

The implementation of the strategy is considered a great success in the organization. 0.78

Future Preparedness (α = 0.88) 0.66 We sufficiently develop new technologies and/or competences in our projects. 0.70

With our projects we are a step ahead of our competition with new products, technologies, or services. 0.90

The projects enable us to shape the future of our industry. 0.74

Portfolio Balance (Cronbach‟s Alpha α = 0.85) 0.68 There is a good balance in our project portfolio ... ... between new and old areas of application. 0.82

... between new and existing technologies. 0.89

… of project risks. 0.60

Avg. Project Outcome Quality (α = 0.88) 0.69 Please assess the average success of completed projects:

Our products/project results achieve the target costs defined in the project. 0.57

Our products/project results achieve the planned market goals (e.g., market share). 0.64

Our products/project results achieve the planned profitability goals (e.g., ROI). 0.94

Our products achieve the planned amortization period. 0.89

Synergy Exploitation (α = 0.88) 0.70

During the project execution, development synergies (e.g. shared use of modules, platforms, technologies

etc.) between projects are rigorously exploited. 0.83

After project completion, exploitation synergies (e.g. shared marketing/sales channels, infrastructure, etc.)

between projects are rigorously exploited. 0.85

We hardly ever have double work or redundant development. 0.66

7-Likert-type Scale; ² = 214.40 (df = 114; p < 0.00); RMSEA = 0.071; SRMR = 0.068; CFI = 0.94; n = 183.

31

Appendix B

Confirmatory Factor Analysis for Independent Variables

Construct

Dimension

Item

Description loading

Business Case Control (2nd

order construct)

Existence (Cronbach‟s Alpha α = 0.85) 0.81

All projects must have a business case in order to enter the selection process. 0.67

“Must-Projects“ also have to prove a business case. 0.66

We closely examine the business case within portfolio structuring. 0.84

The business case is examined by experts from different departments. 0.78

Overall, business cases are elaborated very well and conscientiously. (discarded in PCFA) -

Monitoring (α = 0.88) 0.94

We check the business case for validity at specified points in time or events in the course of the project and adjust if

necessary. 0.93

Once a project is approved a review of the objectives is rare. (reversed) 0.65

We check on a regular basis for each business case whether the necessary conditions are still valid. 0.86

When the project scope or course has changed the implications on the business case is always checked. 0.75

Tracking (α = 0.88) 0.79

Once a project is completed, no further consideration takes place. (reverse) 0.60

At project completion, we not only check the adherence to costs, time and specifications of the project, but also the

fulfillment of the business case. 0.72

Even within a certain period after project completion it is regularly checked if the originally targeted business case could

be realized. 0.92

We systematically analyze the results of the review of the business case. 0.86

The subsequent analysis of business cases provides us with valuable insights. 0.79

Incentives for portfolio success (α = 0.75)

Project managers receive a special bonus, which is based on the success of the project portfolio. 0.65

Portfolio coordinators receive a special bonus, which is based on the success of the project portfolio. 0.86

Line managers receive a special bonus, which is based on the success of the project portfolio. 0.65

Accountability (α = 0.88) For the take-over and exploitation of project results clear responsibilities and roles are defined. (discarded) -

Even after project completion responsibilities for the realization of the business case are clearly defined. 0.66

The role of the project user including certain duties is clearly defined. 0.71

Project users have clearly defined targets regarding the exploitation of the project results. 0.98

The line management on the project user's side have clearly defined targets regarding the exploitation of the project

results. 0.84

Environmental Turbulence (α = 0.84)

The technology in our industry is changing rapidly. 0.87

There are frequent technological breakthroughs in our industry. 0.92

Technological changes provide big opportunities in our industry. 0.71

In our industry, it is difficult to predict how customers‟ needs and requirements will evolve. 0.45

In our kind of business, customers' product preferences change quite a bit over time. 0.54

In our industry, it is difficult to forecast competitive actions. 0.60

7-Likert-type Scale; ² = 445.83 (df = 287; p < 0.00); RMSEA = 0.056; SRMR = 0.064; CFI = 0.94; n = 183.

32

References

Ahire, S. L. and Devaraj, S., 2001, "An empirical comparison of statistical construct validation approaches". IEEE Transactions on Engineering Management, 48(3): 319-329.

Aiken, L. S., West, S. G., and Reno, R. R., 1991, Multiple regression: testing and interpreting interactions. Newbury Park, Calif.: Sage Publications.

Anbari, F. T., Carayannis, E. G., and Voetsch, R. J., 2008, "Post-project reviews as a key project management competence". Technovation, 28(10): 633-643.

APM, 2006, APM Body of Knowledge. (5 ed.). Buckinghamshire, UK: Association for Project Management.

Archer, N. P. and Ghasemzadeh, F., 1999, "An integrated framework for project portfolio selection". International Journal of Project Management, 17(4): 207-216.

Archer, N. P. and Ghasemzadeh, F., 2004, "Project portfolio selection and management". In P. W. G. Morris & J. K. Pinto (Eds.), The Wiley guide to managing projects: 237-255: Wiley Online Library.

Artto, K., Kujala, J., Dietrich, P., and Martinsuo, M., 2008, "What is project strategy?". International Journal of Project Management, 26(1): 4-12.

Atkinson, R., 1999, "Project management: cost, time and quality, two best guesses and a phenomenon, its time to accept other success criteria". International Journal of Project Management, 17(6): 337-342.

Beringer, C., Jonas, D., and Kock, A., 2013, "Behavior of internal stakeholders in project portfolio management and its impact on success". International Journal of Project Management, 31(6): 830-846.

Blichfeldt, B. S. and Eskerod, P., 2008, "Project portfolio management – There’s more to it than what management enacts". International Journal of Project Management, 26(4): 357-365.

Brambor, T., Clark, W. R., and Golder, M., 2006, "Understanding interaction models: Improving empirical analyses". Political Analysis, 14(1).

Bredin, K. and Söderlund, J., 2006, "HRM and project intensification in R&D-based companies: a study of Volvo Car Corporation and AstraZeneca". R&D Management, 36(5): 467-485.

Bubshait, A. A., 2003, "Incentive/disincentive contracts and its effects on industrial projects". International Journal of Project Management, 21(1): 63-70.

Busby, J. S., 1999, "An assessment of post-project reviews". Project Management Journal, 30(3): 23-29.

Christiansen, J. K. and Varnes, C., 2008, "From models to practice: decision making at portfolio meetings". International Journal of Quality & Reliability Management, 25(1): 87-101.

Cohen, D. J. and Graham, R. J., 2001, The project manager's MBA : how to translate project decisions into business success. (1st ed.). San Francisco: Jossey-Bass.

Collier, B., DeMarco, T., and Fearey, P., 1996, "A defined process for project post mortem review". Software, IEEE, 13(4): 65-72.

Cooke-Davies, T., 2007, "Managing Benefits". In R. Turner (Ed.), Gower Handbook of Project Management, 4 ed. Burlington: Gower Publishing Limited.

Cooper, R. G., Edgett, S. J., and Kleinschmidt, E. J., 2001, "Portfolio management for new product development: Results of an industry practices study". R&D Management, 31(4): 361-380.

Cooper, R. G., Edgett, S. J., and Kleinschmidt, E. J., 2004a, "Benchmarking best NPD practices-I". Research-Technology Management, 47(1): 31-43.

33

Cooper, R. G., Edgett, S. J., and Kleinschmidt, E. J., 2004b, "Benchmarking best NPD practices-II". Research-Technology Management, 47(6): 43-55.

Deci, E. L., Koestner, R., and Ryan, R. M., 1999, "A meta-analytic review of experiments examining the effects of extrinsic rewards on intrinsic motivation". Psychological Bulletin, 125(6): 627-668.

Dietrich, P. and Lehtonen, P., 2005, "Successful management of strategic intentions through multiple projects–Reflections from empirical study". International Journal of Project Management, 23(5): 386-391.

Donaldson, L., 2001, The Contingency Theory of Organizations. SAGE Publications.

Dvir, D. and Lechler, T., 2004, "Plans are nothing, changing plans is everything: the impact of changes on project success". Research Policy, 33(1): 1-15.

Dvir, D., 2005, "Transferring projects to their final users: The effect of planning and preparations for commissioning on project success". International Journal of Project Management, 23(4): 257-265.

Eisenhardt, K. M., 1985, "Control: Organizational and economic approaches". Management Science, 31(2): 134-149.

Eisenhardt, K. M., 1989, "Agency theory: An assessment and review". Academy of Management Review, 14(1): 57-74.

Elonen, S. and Artto, K. A., 2003, "Problems in managing internal development projects in multi-project environments". International Journal of Project Management, 21(6): 395-402.

Engwall, M. and Jerbrant, A., 2003, "The resource allocation syndrome: the prime challenge of multi-project management?". International Journal of Project Management, 21(6): 403-409.

Falk, A. and Kosfeld, M., 2006, "The Hidden Costs of Control". American Economic Review, 96(5): 1611-1630.

Frey, B. S. and Jegen, R., 2001, "Motivation Crowding Theory". Journal of Economic Surveys, 15(5): 589-611.

Gambles, I., 2009, Making the Business Case: Proposals that Succeed for Projects that Work. Gower Publishing, Ltd.

GAPPS, 2011, A Framework for Performance Based Competency Standards for Program Managers. Sydney: Global Alliance for Project Performance Standards.

Gardiner, P. D. and Stewart, K., 2000, "Revisiting the golden triangle of cost, time and quality: the role of NPV in project control, success and failure". International Journal of Project Management, 18(4): 251-256.

Ghapanchi, A. H., Tavana, M., Khakbaz, M. H., and Low, G., 2012, "A methodology for selecting portfolios of projects with interactions and under uncertainty". International Journal of Project Management, 30(7): 791-803.

Gneezy, U., Meier, S., and Rey-Biel, P., 2011, "When and why Incentives (don't) work to modify behavior". The Journal of Economic Perspectives, 25(4): 191-209.

Heising, W., 2012, "The integration of ideation and project portfolio management — A key factor for sustainable success". International Journal of Project Management, 30(5): 582-595.

Hendriks, M. H. A., Voeten, B., and Kroep, L., 1999, "Human resource allocation in a multi-project R&D environment: Resource capacity allocation and project portfolio planning in practice". International Journal of Project Management, 17(3): 181-188.

34

Howell, D., Windahl, C., and Seidel, R., 2010, "A project contingency framework based on uncertainty and its consequences". International Journal of Project Management, 28(3): 256-264.

Hu, L. T. and Bentler, P. M., 1998, "Fit indices in covariance structure modeling: Sensitivity to underparameterized model misspecification". Psychological Methods, 3(4): 424-453.

Huemann, M. and Anbari, F. T., 2007, "Project auditing: a tool for compliance, governance, empowerment, and improvement". Journal of the Academy of Business & Economics, 7(2).

Ika, L. A., 2009, "Project success as a topic in project management journals". Project Management Journal, 40(4): 6-19.

IPMA, 2006, IPMA Competence Baseline (ICB) Version 3.0. Nijkerk: International Project Management Association.

Jaafari, A., 1996, "Twinning time and cost in incentive-based contracts". Journal of Management in Engineering, 12(4): 62-72.

Jenner, S., 2009, Realising Benefits from Government ICT Investment - A fool’s errand? . (1 ed.). Reading, UK: Academic Publishing International Ltd.

Jenner, S., 2010, Transforming government and public services: Realising benefits through project portfolio management. Gower Publishing Company.

Jonas, D., 2010, "Empowering project portfolio managers: How management involvement impacts project portfolio management performance". International Journal of Project Management, 28(8): 818-831.

Jonas, D., Kock, A., and Gemunden, H. G., 2013, "Predicting Project Portfolio Success by Measuring Management Quality—A Longitudinal Study". IEEE Transactions on Engineering Management, 60(2): 215-226.

Killen, C. P., Hunt, R. A., and Kleinschmidt, E. J., 2008, "Project portfolio management for product innovation". International Journal of Quality & Reliability Management, 25(1): 24-38.

Kim, J. and Wilemon, D., 2009, "An empirical investigation of complexity and its management in new product development". Technology Analysis & Strategic Management, 21(4): 547-564.

Koners, U. and Goffin, K., 2007, "Learning from Postproject Reviews: A Cross‐Case Analysis*". Journal of Product Innovation Management, 24(3): 242-258.

Lechler, T. G. and Dvir, D., 2010, "An alternative taxonomy of project management structures: Linking project management structures and project success". IEEE Transactions on Engineering Management, 57(2): 198-210.

Mahaney, R. C. and Lederer, A. L., 2010, "The role of monitoring and shirking in information systems project management". International Journal of Project Management, 28(1): 14-25.

Martinsuo, M. and Lehtonen, P., 2007, "Role of single-project management in achieving portfolio management efficiency". International Journal of Project Management, 25(1): 56-65.

Meng, X. and Gallagher, B., 2012, "The impact of incentive mechanisms on project performance". International Journal of Project Management, 30(3): 352-362.

Meskendahl, S., 2010, "The influence of business strategy on project portfolio management and its success - A conceptual framework". International Journal of Project Management, 28(8): 807-817.

Midler, C., 1995, "“Projectification” of the firm: The Renault case". Scandinavian Journal of Management, 11(4): 363-375.

Milgrom, P. R. and Roberts, J., 1992, Economics, organization and management. Prentice-Hall Englewood Cliffs, NJ.

35

Morris, P. W. G. and Jamieson, A., 2005, "Moving from corporate strategy to project strategy". Project Management Journal, 36(4): 5-18.

Morris, P. W. G., Pinto, J. K., and Söderlund, J., 2011, "Introduction - Towords the third wave of project management". In P. W. G. Morris & J. K. Pinto & J. Söderlund (Eds.), The Oxford handbook of project management: OUP Oxford.

Morris, P. W. G., 2013, Reconstructing project management. Somerset, NJ, USA: Wiley.

Müller, R., Martinsuo, M., and Blomquist, T., 2008, "Project portfolio control and portfolio management performance in different contexts". Project Management Journal, 39(3): 28-42.

Newell, S., Bresnen, M., Edelman, L., Scarbrough, H., and Swan, J., 2006, "Sharing Knowledge Across Projects Limits to ICT-led Project Review Practices". Management Learning, 37(2): 167-185.

OGC, 2010, Management of Value. (1 ed.). Norwich: The Stationery Office.

OGC, 2011a, Management of Portfolios. Norwich, UK: The Stationery Office.

OGC, 2011b, Managing successful programmes. Norwich, UK: The Stationery Office.

Ouchi, W. G., 1977, "The relationship between organizational structure and organizational control". Administrative Science Quarterly: 95-113.

Ouchi, W. G., 1979, "A conceptual framework for the design of organizational control mechanisms". Management science, 25(9): 833-848.

Platje, A., Seidel, H., and Wadman, S., 1994, "Project and portfolio planning cycle: Project-based management for the multiproject challenge". International Journal of Project Management, 12(2): 100-106.

PMI, 2013a, A Guide to the Project Management Body of Knowledge: PMBOK Guide. Project Management Institute, Incorporated.

PMI, 2013b, The Standard for Program Management. (3 ed.). Pensylvania: Project Management Institute, Inc.