Embed Size (px)

Citation preview

BUSINESS AND MANAGEMENT

ACCOUNTING AND FINANCE

Unit 3.4 Budgeting (Higher Level)

Content and Learning Outcomes Content

! Types and purpose of budgets ! Cash Flow Forecasts ! Variance Analysis

Learning Outcomes

! Explain the importance of budgeting for organisations. ! Prepare and analyse a Cash Flow forecast from given

information. ! Calculate and interpret variances

Reading Focus

• Stimpson. AS and A Level Business Studies, Chapter 30 • Hall, Jones and Raffo. Business Studies, 3rd Edition, Units

46,47&54 • Barratt and Mottershead. AS and A Level Business Studies,

Units • Jewell. An Integrated Approach to Business Studies, 4th

Edition, Units 28 & 34

Types and Purpose of Budgets Context

As businesses expand the need for control grows and becomes more difficult. A small business can be run informally. The owner is the manager, who will know everyone, be aware of what is going on and will make all decisions. In larger firms work and responsibility are delegated which makes informal control impractical. To improve control budgeting has been developed. This forces managers to be more accountable for their decisions.

A budget is a quantitative expression of a plan of action prepared in

advance of the period to which it relates. It must be a plan and not a forecast – a forecast is a prediction of what might happen in the future, where as a budget is a planned outcome which the firm hopes to achieve. A budget will show the money needed for spending and how this might be financed. (Barratt and Mottershead)

Budgets are based on the objectives of the business.

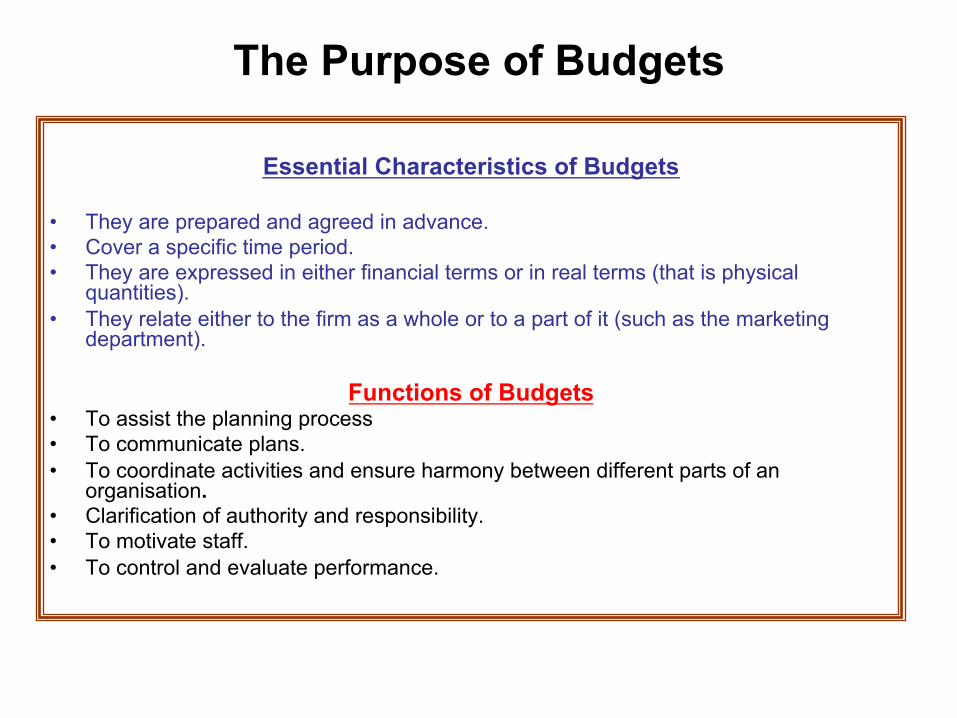

The Purpose of Budgets

Essential Characteristics of Budgets

• They are prepared and agreed in advance. • Cover a specific time period. • They are expressed in either financial terms or in real terms (that is physical

quantities). • They relate either to the firm as a whole or to a part of it (such as the marketing

department).

Functions of Budgets • To assist the planning process • To communicate plans. • To coordinate activities and ensure harmony between different parts of an

organisation. • Clarification of authority and responsibility. • To motivate staff. • To control and evaluate performance.

The Information Contained in a Budget

Information contained in a budget may include any or a combination of the following:

q Revenue q Sales q Expenses q Profit q Personnel q Cash q Capital

These are referred to as Budget Factors. A budget can include any

business variable which can be given a value

Types of Budgets

Objective Budgets These are based on the best way of achieving particular objectives. They contain information on how a business will achieve these objectives. For example, a sales budget might show how a sales target will be met.

Flexible Budgets These are designed to change a business changes. Changes in business conditions may result in very different outcomes than those budgeted for. A flexible budget takes these into account. For example, the sales budget could be altered if there is a sudden increase in demand resulting in much higher sales level.

Capital Budgets Plan the capital structure and the liquidity of the business over a long period of time. They are concerned with equity, liabilities, fixed and current assets and year-end cash balances.

Operating Budgets Plan the day to day use of resources. They are concerned with materials, labour, overheads, sales and cash

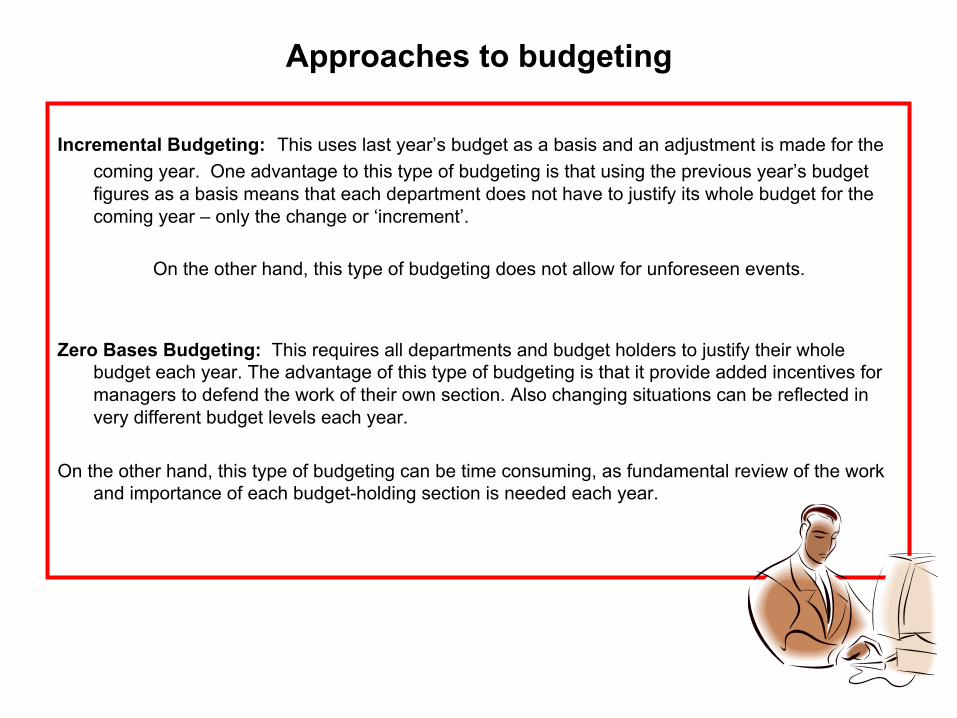

Approaches to budgeting

Incremental Budgeting: This uses last year’s budget as a basis and an adjustment is made for the coming year. One advantage to this type of budgeting is that using the previous year’s budget figures as a basis means that each department does not have to justify its whole budget for the coming year – only the change or ‘increment’.

On the other hand, this type of budgeting does not allow for unforeseen events.

Zero Bases Budgeting: This requires all departments and budget holders to justify their whole

budget each year. The advantage of this type of budgeting is that it provide added incentives for managers to defend the work of their own section. Also changing situations can be reflected in very different budget levels each year.

On the other hand, this type of budgeting can be time consuming, as fundamental review of the work

and importance of each budget-holding section is needed each year.

Organizational Objectives

External Factors

Forecasts of the future What happened last year

Key factor – likely to be sales

Sales budget: Production; Region; Departments

Cash Budget Administration Budget Materials Budget Selling& Distribution Budget

Coordination: This is essential

Master Budget: Balance Sheet & Trading and Profit and Loss Account

The Budget Process

The Budget Process

Stage 1: The most important organizational objectives for the coming year are established. These will be based on: the previous year’s performance; external changes likely to affect the organisation; forecasts based on research.

Stage 2: Identify the key and limiting factor which is most likely to affect the organisation. In most

businesses this is likely to be sales. Hence, the sales budget is the first to be prepared. Stage 3: The sales budget is prepared. Stage 4: The subsidiary budgets are prepared. These will include cash budgets; administration

budgets; materials budget; selling and distribution budgets. Stage 5: The budgets are coordinated to ensure consistency. Stage 6: A master budget is prepared. This will contain the details of all the other budgets and

conclude with a budgeted profit and loss account and balance sheet. Stage 7: The master budget is then presented to the board of directors for approval.

Preparation of plans

Analysis of variances Comparison of plans with

actual results

The Stages in Budgetary Control Process

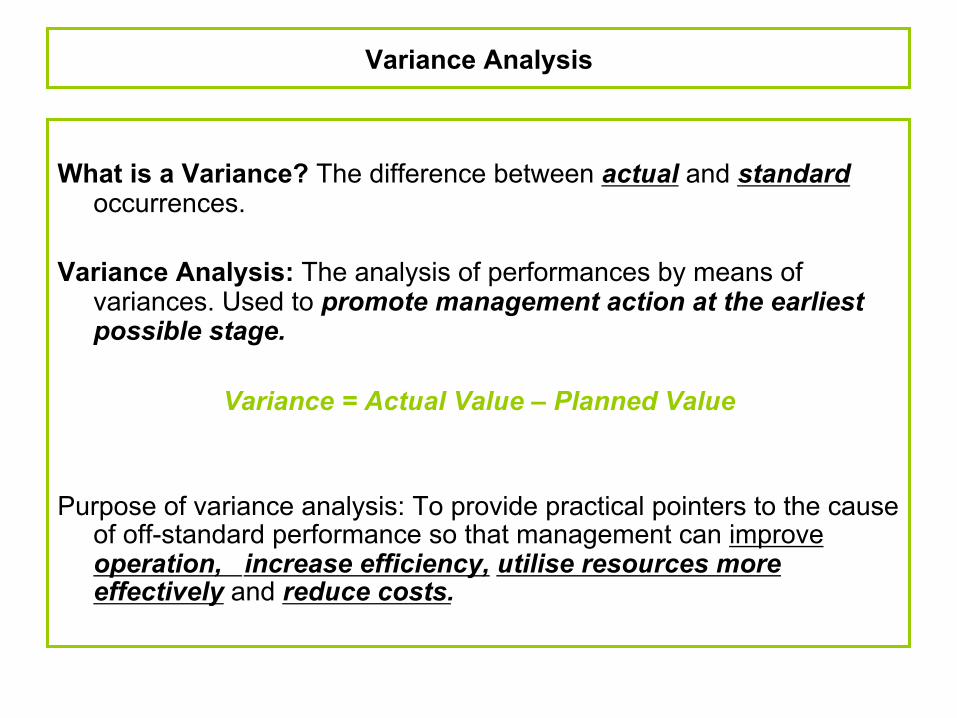

Variance Analysis

What is a Variance? The difference between actual and standard occurrences.

Variance Analysis: The analysis of performances by means of

variances. Used to promote management action at the earliest possible stage.

Variance = Actual Value – Planned Value

Purpose of variance analysis: To provide practical pointers to the cause of off-standard performance so that management can improve operation, increase efficiency, utilise resources more effectively and reduce costs.

Budgetary Control – Variance Analysis

A Variance in budgeting is the difference between the figure the business had budgeted for and the actual figure.

Variances are calculated at the end of the budget period as this is when the actual figures will be

known. These figures can be favourable (F) or adverse (A). Favorable variances occur when the actual figures are better than the budgeted figures.

Budgeted Sales Revenue and Costs for the month of August, 2006

Budgeted ($)

Actual ($)

Favourable Variance (F)

Adverse Variance (A)

25,000 (Revenue)

29,000 4,000

20,000 (Costs)

18,000

2,000

Adverse variances are when the actual figures are worse than the budgeted figures.

Activity: Question # 4

Source: Unit 47, page 334, Hall, Jones& Raffo, Business Studies 3rd Edition

Why is Variance Analysis an essential part of budgeting?

! It measure the difference from the planned performance of each department. ! It assist in analysing the cause of deviation from the budget. ! The deviations from the original planned levels can be used to change future budgets in order to

make them more accurate. For example, if sales revenue is lower than planned as a result of market resistance to higher prices, then this knowledge could be used to help prepare future budgets.

Case Study: Maison JP et Chateau JP

Source: Unit 47, page 334, Jones, Hall, Raffo, Business Studies 3rd Edition

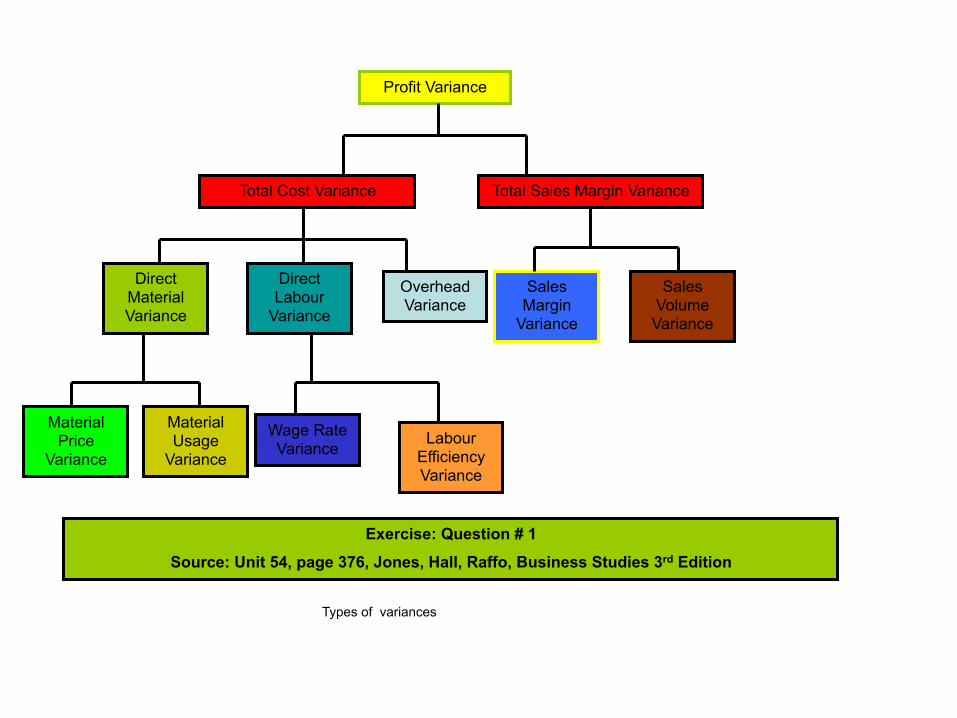

Profit Variance

Total Cost Variance Total Sales Margin Variance

Sales Volume Variance

Sales Margin

Variance

Direct Material Variance

Overhead Variance

Direct Labour

Variance

Material Price

Variance

Material Usage

Variance

Wage Rate Variance

Labour Efficiency Variance

Types of variances

Exercise: Question # 1

Source: Unit 54, page 376, Jones, Hall, Raffo, Business Studies 3rd Edition

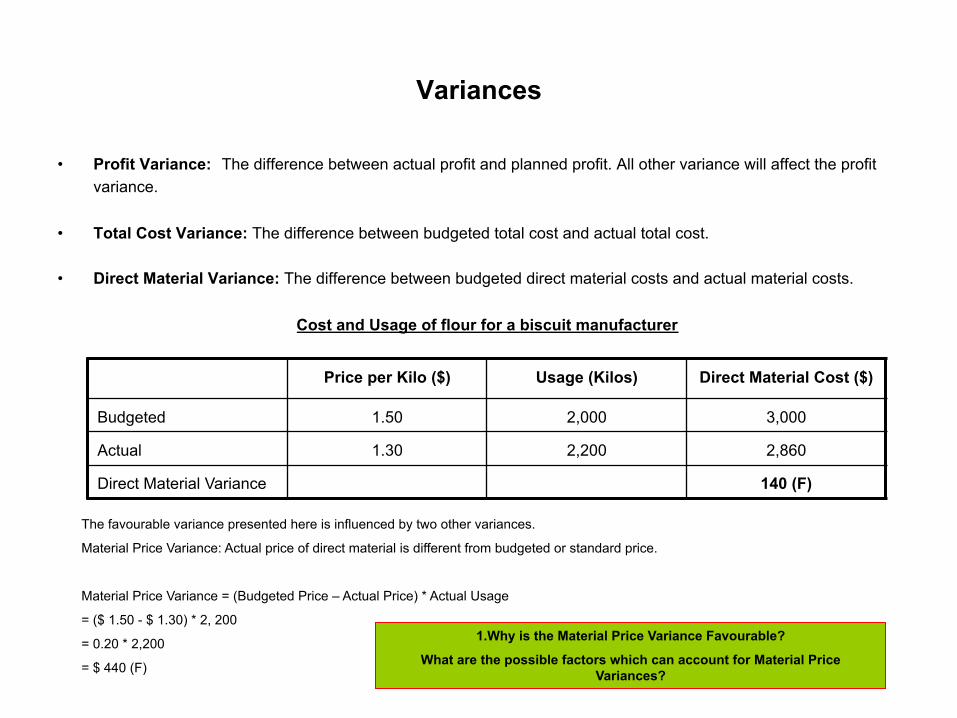

Variances

• Profit Variance: The difference between actual profit and planned profit. All other variance will affect the profit variance.

• Total Cost Variance: The difference between budgeted total cost and actual total cost. • Direct Material Variance: The difference between budgeted direct material costs and actual material costs.

Cost and Usage of flour for a biscuit manufacturer

Price per Kilo ($)

Usage (Kilos)

Direct Material Cost ($)

Budgeted

1.50

2,000

3,000

Actual

1.30

2,200

2,860

Direct Material Variance

140 (F)

The favourable variance presented here is influenced by two other variances.

Material Price Variance: Actual price of direct material is different from budgeted or standard price.

Material Price Variance = (Budgeted Price – Actual Price) * Actual Usage

= ($ 1.50 - $ 1.30) * 2, 200

= 0.20 * 2,200

= $ 440 (F)

1.Why is the Material Price Variance Favourable?

What are the possible factors which can account for Material Price Variances?

Variances

• Material Usage Variance: This is found by comparing the actual usage of material and the budgeted usage.

Material Usage Variance = (Budgeted Usage – Actual Usage) * Budgeted Price = ( 2,000 – 2,200) * $1.50 = - 200 * $ 1.50 = $ 300 (A)

The material usage is adverse because the actual usage is greater than the budgeted usage.

Material Usage Variance might arise because materials are:

• Wasted in production due to sloppy or careless work. • Wasted because they are inferior. • Wasted due to a machine malfunction. • Used more efficiently because staff take more care in their work.

Activity: Question #1& 2

Source: Unit 54, page 377, Hall, Raffo, Business Studies 3rd Edition

Variances

Direct Labour Variance: This will occur when the budgeted direct wage bill is different from the actual direct wage bill. Wage Rate Variances: This will result when there is a difference between the budgeted wage rate paid to workers and the actual wage rate paid.

Wage Rate ($)

No. of Labour Hours

Direct Wage Bill($) Budgeted

5.00

1,500

7,500

Actual

5.20

1,600

8,320

Direct Material Variance

820 (A)

Budgeted and actual wage rates and labour hours for the biscuit manufacturer

Wage Rate Variance = (Budgeted Wage Rate – Actual Wage Rate) * Actual Hours

= ( $5.00 - $ 5.20) * 1,600

= - 0.20 * 1,600

= $ 320 (A)

The wage rate variance is adverse because the actual wage rate is higher than the budgeted wage rate. The factors which might influence wage rates include:

1. Trade union pressure.

2. Shortage of skilled labour.

3. Government legislations such as raising the minimum wage.

Variances

Labour Efficiency Variances: There will be a labour efficiency variance if there is a difference between the budgeted number of labour hours required in a budget period and the actual number of labour hours used.

Labour Efficiency Variance = (Budgeted Labour Hours – Actual Labour Hours) * Budgeted Wage Rate = ( 1,500 – 1,600) * $5.00 = - 100 * $5.00 = $500 (A) The Labour Efficiency Variance is adverse because the actual number of hours worked is greater than the

budgeted number. The production manger may be responsible for this variance. The factors that might influence the number of labour hours used might include:

1. The productivity of workers. 2. The reliability of machinery used by workers. 3. How well trained workers are.

Activity: Question 3

Source: Unit 54, page 378, Hall, Jones, Raffo, Business Studies 3rd Edition.

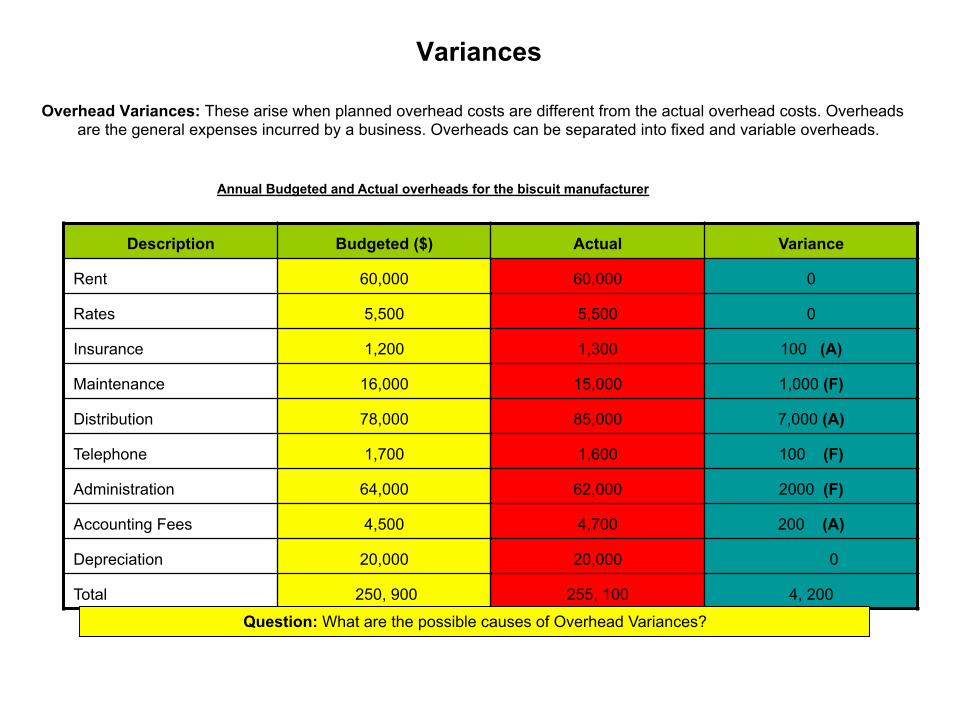

Variances

Overhead Variances: These arise when planned overhead costs are different from the actual overhead costs. Overheads are the general expenses incurred by a business. Overheads can be separated into fixed and variable overheads.

Description

Budgeted ($)

Actual

Variance

Rent

60,000

60,000

0

Rates

5,500

5,500

0

Insurance

1,200

1,300

100 (A)

Maintenance

16,000

15,000

1,000 (F)

Distribution

78,000

85,000

7,000 (A)

Telephone

1,700

1,600

100 (F)

Administration

64,000

62,000

2000 (F)

Accounting Fees

4,500

4,700

200 (A)

Depreciation

20,000

20,000

0

Total

250, 900

255, 100

4, 200

Annual Budgeted and Actual overheads for the biscuit manufacturer

Question: What are the possible causes of Overhead Variances?

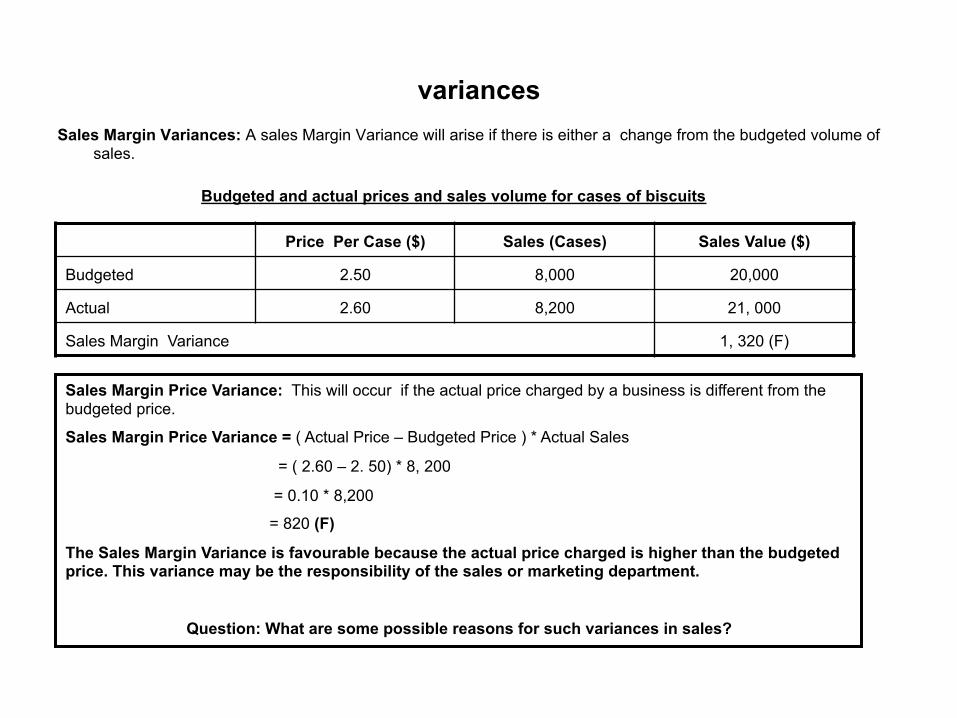

variances Sales Margin Variances: A sales Margin Variance will arise if there is either a change from the budgeted volume of

sales.

Price Per Case ($)

Sales (Cases)

Sales Value ($)

Budgeted

2.50

8,000

20,000

Actual

2.60

8,200

21, 000

Sales Margin Variance

1, 320 (F)

Budgeted and actual prices and sales volume for cases of biscuits

Sales Margin Price Variance: This will occur if the actual price charged by a business is different from the budgeted price.

Sales Margin Price Variance = ( Actual Price – Budgeted Price ) * Actual Sales

= ( 2.60 – 2. 50) * 8, 200

= 0.10 * 8,200

= 820 (F)

The Sales Margin Variance is favourable because the actual price charged is higher than the budgeted price. This variance may be the responsibility of the sales or marketing department.

Question: What are some possible reasons for such variances in sales?

Variances

Sales Volume Variance: This will occur if actual level of sales is different from the budgeted sales. For the biscuit manufacturer this is:

Sales Volume Variance = (Actual Sales – Budgeted Sales) * Budgeted Price ( 8,200 – 8000) * $2.50 = 200 * $ 2.50 = 500 (F) The Sales Volume Variance is favourable because the actual number of sales is greater than the budgeted number.

Sales Volume Variance is likely to arise due to: • Changes in the state of the economy. • Competitors’ actions. • Changes in consumer tastes. • Government action, such as a cut in income tax. • Changes in the quality of the product. • Changes in marketing techniques. The Sales Margin Variance for the biscuit manufacturer is $ 1, 320 (F). It is influenced by both the Sales Price

Margin Variance $ 820 (F), and Sales Volume Variance, $ 500 (F)

Activity: Question # 4 Source: Unit 54, page 380, Hall, Jones Raffo, Business Studies 3rd Edition.

Cash Variances

Reminder: Cash and Profit are not the same thing. A cash budget is concerned with liquidity, not profitability.

A cash Variance shows the difference between budgeted cash flow a and actual cash flow

Benefits of Variance Analysis

• It allows senior managers to monitor the performance of the organisation as a whole, as well as different sections of the organisation.

• Prompt variance analysis allows managers to assess whether variances re caused by internal or external factors.

• By identifying variances and their causes managers may b able to produce more accurate budgets in the future. This will aid planning and perhaps improve the performance of the business.

• Budgetary control in general helps improve accountability in the business.

Cases: West Indian Carpets Ltd and Oasis Cookers Ltd

Source: Unit 5, pages 466, Stimpson,AS and A Level Business Studies

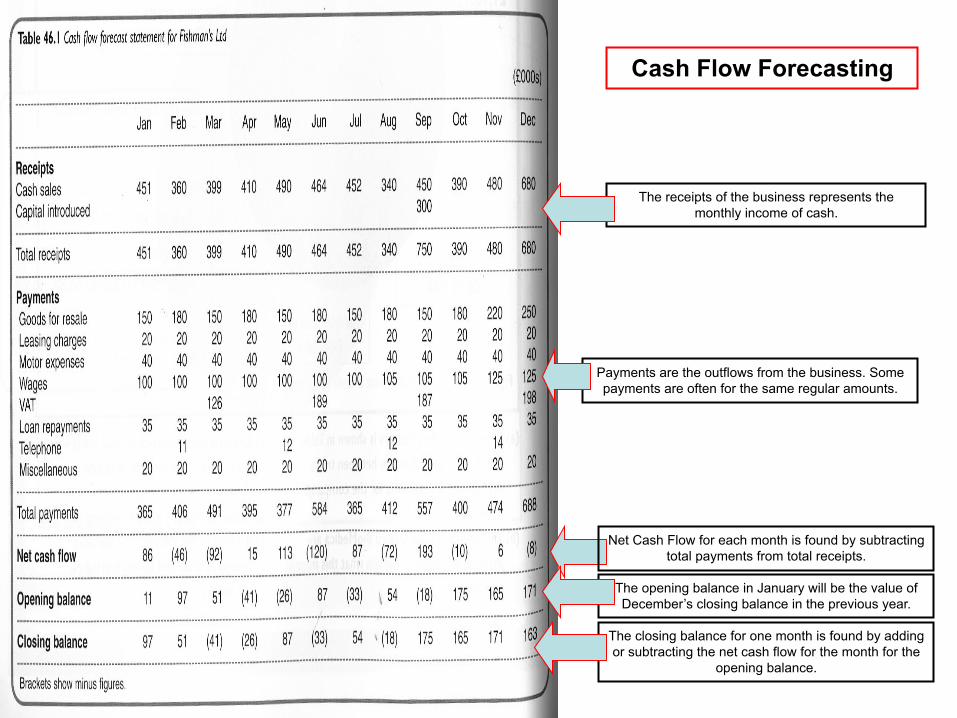

Cash Flow Forecasting

Why do businesses prepare cash flow forecasts

Cash flow forecasts are drawn up to help control and monitor cash flow in the business. The following are some advantages of using statements to control cash flows.

1. Identifying the timing of cash shortages and surpluses. 2. Supporting applications for funding. 3. Enhancing the planning process. 4. Monitoring cash flow.

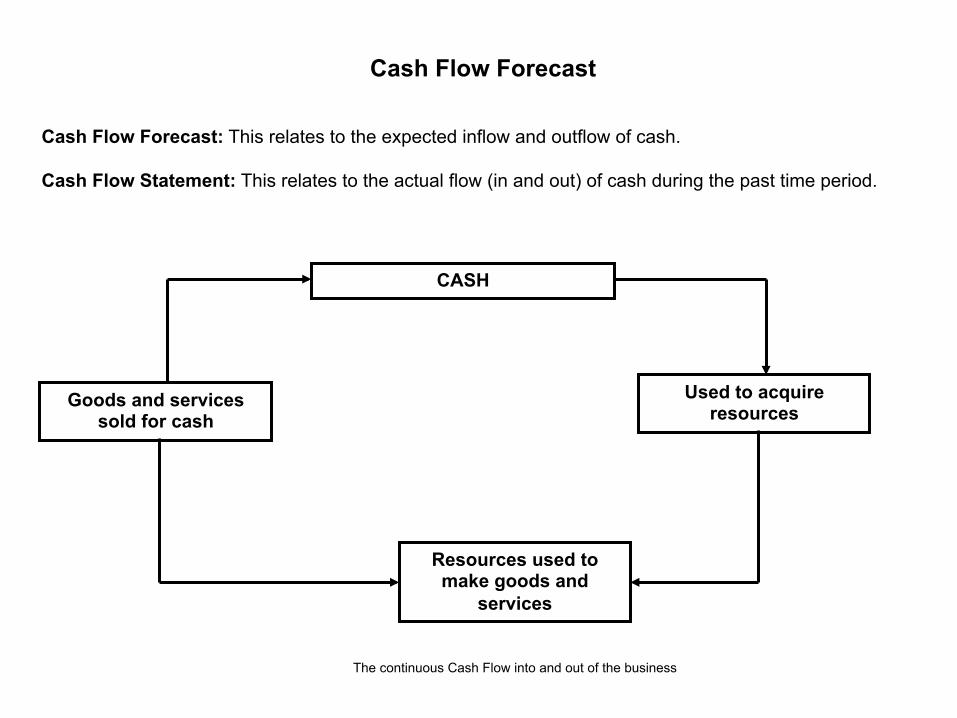

Cash Flow Forecast: This relates to the expected inflow and outflow of cash. Cash Flow Statement: This relates to the actual flow (in and out) of cash during the past time period.

Cash Flow Forecast

CASH

Used to acquire resources

Resources used to make goods and

services

Goods and services sold for cash

The continuous Cash Flow into and out of the business

Why Cash flow is important to business

ü Without sufficient cash flow businesses would not be able to pay its many creditors on time. The possible implications are: creditors may stop supplying goods or impose strict conditions such as ‘cash on delivery’; discounts will be lost for prompt payments of bills; other traders will be less prepared to deal with the firm except on a cash basis.

ü Wages and salary may not be paid on time and this will cause poor motivation; absenteeism; high labour turnover; and industrial unrest.

ü New capital assets cannot be afforded and this can reduce business efficiency.

ü Tax bills may not be paid

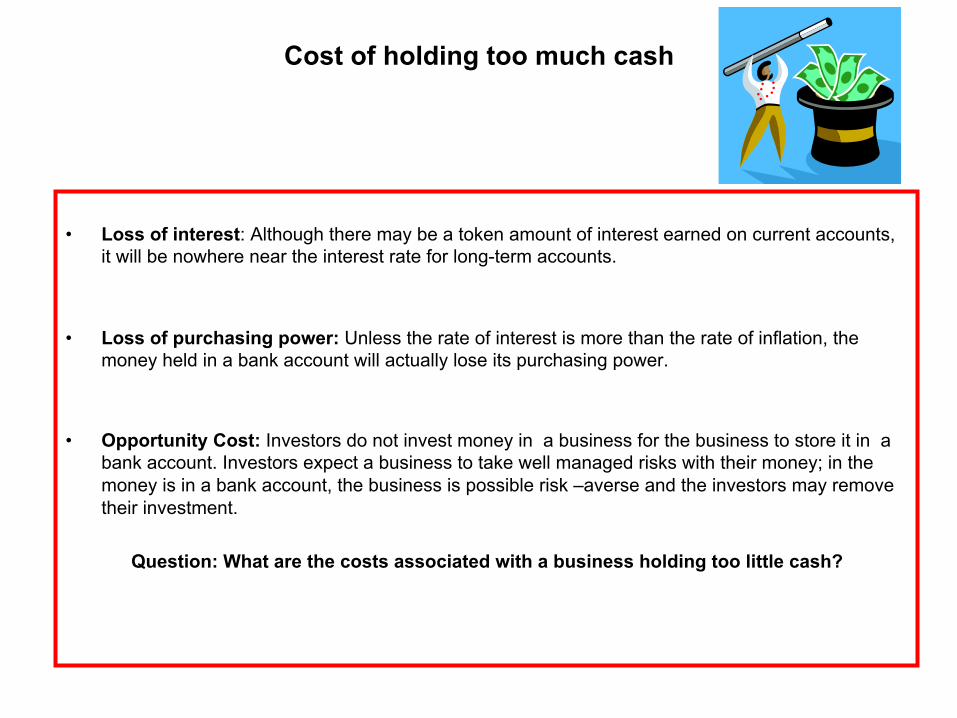

Cost of holding too much cash

• Loss of interest: Although there may be a token amount of interest earned on current accounts, it will be nowhere near the interest rate for long-term accounts.

• Loss of purchasing power: Unless the rate of interest is more than the rate of inflation, the

money held in a bank account will actually lose its purchasing power. • Opportunity Cost: Investors do not invest money in a business for the business to store it in a

bank account. Investors expect a business to take well managed risks with their money; in the money is in a bank account, the business is possible risk –averse and the investors may remove their investment.

Question: What are the costs associated with a business holding too little cash?

Causes of cash flow problems

p Overtrading p Holding too much stock

p High borrowing – therefore high interest payments.

p Allowing too many goods to be bought on credit.

p Businesses that rely on seasonal trade – during the time that sales are very low, cash still needs to be spent on running the businesses.

p High unemployment.

The Relationship between profit and cash

Note: A profitable business may run out of cash, whilst the business recording a loss may have a cash surplus. How is this possible?

• The business may be selling more of its output on credit. Therefore a profit is being made as the goods are

being recorded and sold, but the cash payment form customers will be received sometime in the future. This period of credit may leave the firm dangerously short of cash.

• The business may receive cash at the beginning of the trading year from sales made in the previous year. This would increase the cash balance but not affect profit.

• A business may buy resources from its suppliers and not pay for them until the next trading year. As a result

the trading cost will not be the same as the cash paid out.

• When additional capital is introduced into the business this will increase the cash balance, but have no effect on profit. This is because capital is not treated as revenue in the Profit and Loss Account.

• The purchase of fixed assets will reduce cash balance but have no effect on the profit a company makes. This is because the purchase of an asset is not treated as an expense in the Profit and Loss Account.

• Sale of fixed assets will increase cash balances but have no effect on profit unless a profit or loss is made on

the disposal of the asset. This is because profit from the sale of an asset is not included in the business turnover.

Activity: Question # 4, Unit 46, page 327 Hall Jones and Raffo, Business Studies, 3rd Edition.

The receipts of the business represents the monthly income of cash.

Payments are the outflows from the business. Some payments are often for the same regular amounts.

Net Cash Flow for each month is found by subtracting total payments from total receipts.

The opening balance in January will be the value of December’s closing balance in the previous year.

The closing balance for one month is found by adding or subtracting the net cash flow for the month for the

opening balance.

Cash Flow Forecasting

July August September October November Receipts

Capital injection 10,000 Sales revenue

2,000 4,000 8,000 12,000 16,000 Total cash in 12,000 4,000 8,000 12,000 16,000

Payments Capital Expenditure 15,000 2,000 2,000

2,000 4,000

Labour 2,000 3,000 4,000 6,000 6,000

Materials 3,000 4,000 4,000 4,000 4,000 Total Payments 2,000 9,000 10,000 12,000 14,000 Net Cash Flow ( 8,000) (5,000) (20,000) 0 X Opening Balance 0 (8,000) (13,000) (15,000) (15,000) Closing Balance (8,000) (13,000) (15,000) (15,000) Y

1. Calculate the missing values X and Y.

2. State two ways in which the business might be able to improve its forecasted cash flow.

3. Complete the table for December based on the following forecasts

Sales revenue raises by 10% from November.

Capital expenditure is double the November level.

Labour and material costs increase by 25%

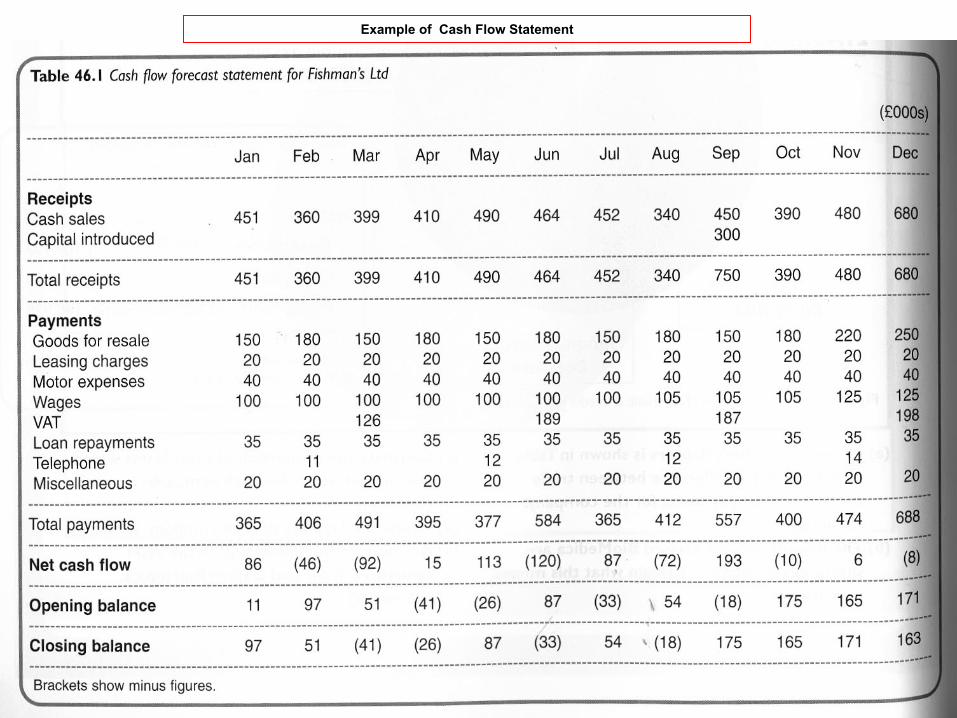

The following cash-flow forecast is for ‘Plants4U’ flower shop which is about to begin trading (all figures in $000s)

Example of Cash Flow Statement

Managing Cash Flow

Managing the floe of cash in and out of the business is one of the most important tasks of management. In order to do this effectively managers will need to assess:

• The likely timing of cash flow in d out of the business. This will largely depend on how

long debtors take to pay their bills. • The size and likely timing of payments out of the business; this will largely depend

on the costs of the business and period of credit offered by the suppliers. • Whether there are sources of finance to cover periods when cash shortage could rise.

Time is of great significance to cash flow management

Dealing with Cash-Flow Problems

q Reduce or delay expenditure

q Obtain cheaper supplies

q Rent or lease equipment rather than buying it outright

q Delay the payment of bills – extending the credit period

q Get cash in more quickly from the sale of goods q Use debt factor to release cash from debts q Obtain overdrafts or short term loans

Question: What are the advantages and disadvantages associated with these methods of dealing with cash flow problems?

Handout: Methods of improving Cash Flow, Advantages and Drawbacks

Case Studies

Westview Caravans Source: Unit 46, page 329, Jones, Hall, Raffo, Business Studies 3rd Edition

Tourist Trinkets Limited

Source: Unit 5, pages 461-467, Stimpson,AS and A Level Business Studies

Setting up in Business Source: Unit 5, pages 461, Stimpson,AS and A Level Business Studies

Windrush Training Services

Source: Unit 54, page 380, Jones, Hall, Raffo, Business Studies 3rd Edition

BIBLIOGRAPHY

1.Barratt Michael and Mottershead Andy. AS and A Level Business

Studies, Pearson Education Ltd,2000. 2.Jewell Bruce. An Integrated Approach to Business Studies, 4th Edition,

Pearson Education Ltd 2000. 3. Hall Dave, Jones Rob, Raffo Carlo. Business Studies, 3rd Edition,

Causeway Press Ltd, 2004.

4. Stimpson Peter. AS and A Level Business Studies, Cambridge University Press, 2000.

www.bized.ac.uk

WWW.NetMBA.com