Embed Size (px)

Citation preview

BUS424 (Ch 1& 2) 1

Bond Market Overview and Bond Pricing

1. Overview of Bond Market

2. Basics of Bond Pricing

3. Complications

4. Pricing Floater and Inverse Floater

5. Pricing Quotes and Accrued Interest

BUS424 (Ch 1& 2) 2

What is A Bond?

Bond: a debt instrument requiring the issuer (debtor) to repay to lender/investor the amount borrowed plus interest over a specified period of time

• Plain vanilla bonds

• Advanced debt contract – mortgage pass-through securities

BUS424 (Ch 1& 2) 3

Most Generic Classification

Government bonds – low/no risk, low yield, low expected returns

-- return is high when yield goes down

Risky bonds – non-government bonds, including corporate bonds, municipal bonds, mortgage securities (subprime market securities)

BUS424 (Ch 1& 2) 4

Sectors of US Bond MarketTreasury Sector

have you heard of saving bonds?

Agency Sector

Municipal Sector

Corporate Sector

Asset-Backed Security Sector

Mortgage Sector

See: www.investinginbonds.com

BUS424 (Ch 1& 2) 5

More Info of BondsFederal Reserve Flow of Funds report:

http://www.federalreserve.gov/releases/z1/

TRACE: http://www.finra.org/Industry/Compliance/MarketTransparency/TRACE/

Mergent FISD:

http://www.kellogg.northwestern.edu/rc/fisd.htm

BUS424 (Ch 1& 2) 6

BUS424 (Ch 1& 2) 7

Stocks vs. Bonds

1. Different Characteristics

2. Different Markets Stocks: traded on exchanges and OTC markets: NYSE, AMEX, NASDAQ Bonds: traded on OTC markets 3. Similarity: Buy stocks and bonds through online traders.

BUS424 (Ch 1& 2) 8

Returns of Aggregate Stocks, Gov Bonds, Corporate Bonds

-0.3

-0.2

-0.1

0

0.1

0.2

0.3

0.4

1985 1990 1995 2000 2005

Year

Re

turn

s

ret_stock ret_gov ret_credit

BUS424 (Ch 1& 2) 9

Overview of Bond Features• Term to maturity• Coupon rate

– Fixed rate bonds– Floating rate bonds

—Reference rate + quoted margin• Principal/Face Value• Interest rate/yield to maturity• Price

BUS424 (Ch 1& 2) 10

Example of a fixed payment bond

10 years, face value $1000, coupon rate 8%, semi-annually paid, interest rate 9%. What is the bond price?

There are many variations in bond designs: (1) deferred-coupon (2) amortizing securities: securities with a schedule of

periodical principle repayments. (3) options could be embedded (page 6)

BUS424 (Ch 1& 2) 11

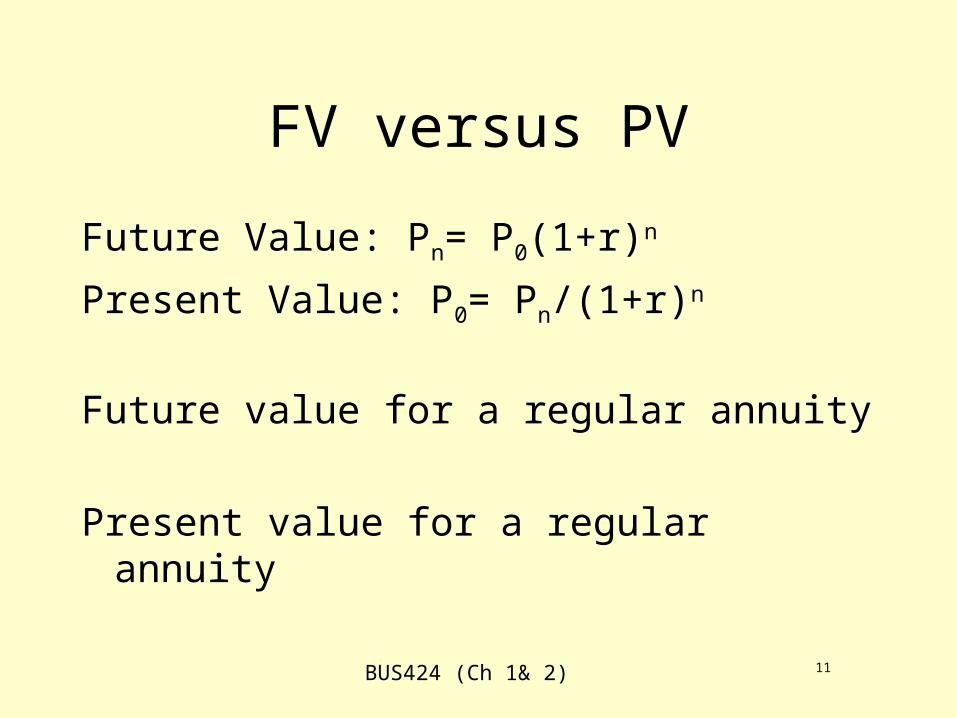

FV versus PV

Future Value: Pn= P0(1+r)n

Present Value: P0= Pn/(1+r)n

Future value for a regular annuity

Present value for a regular annuity

BUS424 (Ch 1& 2) 12

Examples

1. Cash flow (1): you receive $100 in year 1, $200 in year 2, $300 in year 3. Interest rate is 9%. What is the value of the cash flow?

2. Cash flow: you need to pay $100 in year 1, $200 in year 2, and $300 in year 3. Interest rate is 9%. How much you need invest today to pay for this loan?

3. Coupon Bond: 2 years, face value $1000, coupon rate $8, semi-annually paid, interest rate 9%. What is the bond price?

Using your financial calculator

BUS424 (Ch 1& 2) 13

Zero-coupon bonds

Price of zero-coupon bond: P0= M/(1+r)n

Example

BUS424 (Ch 1& 2) 14

Complications

• If the next payment is due in fewer than 6 months

• Cash flows may not be known

• What is the appropriate required yield and whether one discount rate can be applied to all cash flows

BUS424 (Ch 1& 2) 15

Next Due Payment < 6 months

n

tnt rr

M

rr

CP

111 )1()1()1()1(

periodmonth -sixin days

couponnext and settlementbetween days

In fact, this is a 3-step approach to calculate bond price. (1) In the first step, we compute bond price if I buy the bond in the next payment date (i.e., I won’t get any payment for it):

1

11)1()1(

n

tnt r

M

r

CP

(2) Add in the payment I receive in the next payment date, then

n

tnt

n

tnt r

M

r

C

r

M

r

CCP

111

1

11 )1()1()1()1(

(3) Discount the above price back to the date I purchase the bond. The idea is to suppose I buy the bond right before the next payment day, thus I can have the next payment, then discount the value back to time 0.

BUS424 (Ch 1& 2) 16

Price Quoted and Accrued Interest

Price quoted: 100: meaning 100% of its par value/face value

Accrued interest: when an investor purchases a bond between coupon payments, the investor must compensate the seller of the bond for the coupon interest earned from the time of the last coupon payment to the settlement date of the bond.

for a treasury bond, accrued interest is based on the actual number of days the bond is held by the seller.

Full price/dirty price = price + accrued interest

Clean price

BUS424 (Ch 1& 2) 17

Example

A bond face value $1000, YTM=5%, coupon rate=6% semiannually paid, maturity=5 years. The bond was issued on 7/1/2003, and bought on 11/1/2005. What is price of the bond.

v=?

n=?

BUS424 (Ch 1& 2) 18

Procedures of computing price

Step 1

Step 2

Step 3

BUS424 (Ch 1& 2) 19

Example (cont’d)

What is the accrued interest of the bond?

What is the dirty price of the bond?

BUS424 (Ch 1& 2) 20

Floater and Inverse Floater

See Exhibit 2-4.Inverse’s price = collateral’s price – floater’ price

Collateral is the fixed-rate security from which the inverse floater is created

Floor: the minimum interest rate on the inverse floaterCap: the maximum interest rate on the floaterThe sum of interests paid on floater and inverse floater

must always equal interests on the collateral.

BUS424 (Ch 1& 2) 21

Risk Associated with Bonds

1. Interest-rate risk2. Reinvestment risk3. Call risk4. Credit risk5. Inflation risk6. Exchange-rate risk7. Liquidity risk – institutional investor must trade

frequently in some extent8. Risk risk