Embed Size (px)

Citation preview

BUS312A/612A Financial Reporting I

Homework 9.10.2014 & 9.15.2014 The Accounting Cycle – Review

Chapter 3

E3-1 (Transaction Analysis-Service Company) During the first month of operations of her business (a sole proprietorship), the following events and transactions occurred.

Instructions Journalize the transactions in the general journal.

April 2 Invested $32,000 cash and equipment valued at $14,000 in the business.

2 Hired a secretary-receptionist at a salary of $290 per week payable monthly.

3 Purchased supplies on account $700. (Debit an asset account.)

7 Paid office rent of $600 for the month.

11 Completed a tax assignment and billed client $1,100 for services rendered. (Use Service Rev)

E3-1 (Transaction Analysis-Service Company) During the first month of operations of her business (a sole proprietorship), the following events and transactions occurred.

April 12 Received $3,200 advance on a management consulting engagement.

17 Received cash of $2,300 for services completed for Ferengi Co.

21 Paid insurance expense $110.

30 Paid secretary-receptionist $1,160 for the month.

30 A count of supplies indicated that $120 of supplies had been used.

30 Purchased a new computer for $6,100 with personal funds. (The computer will be used exclusively for business purposes.)

E3-17 March transactions:

March 1 Invested $50,000 cash for common stock

3 Purchased real estate for $38,000 cash (land $10,000, building 22,000, equipment 6,000)

5 Paid $1,600 to advertise the driving range & golf course

6 Paid $1,480 for a one-year insurance policy

10 Purchased golf equipment for $2,500 from Singh Company, payable in 30 days

E3-17 March transactions:

March18 Received golf fees of $1,200 in cash

25 Declared and paid a $500 cash dividend

30 Paid wages of $900

30 Paid Singh Company in full

31 Received $750 in cash for golf fees.

Adjusting & Reversing Entries: 4 Kinds

Adjusting & Reversing Entries: 4 Kinds

E3-6 (Adjusting Entries) Karen Weller, D.D.S., opened a dental practice on January 1, 2014.

During the first month of operations the following transactions occurred.

1. Performed services for patients who had dental plan insurance. At January 31, $750 of such services was earned but not yet billed to the insurance companies.

2. Utility expenses incurred but not paid prior to January 31 totaled $520.

3. Purchased dental equipment on January 1 for $80,000, paying $20,000 in cash and signing a $60,000, 3-year note payable. The equipment depreciates $400 per month. Interest is $500 per month.

Instructions Prepare the adjusting entries on January 31. Account titles are: Accumulated Depreciation-Dental Equipment; Depreciation Expense; Service Revenue; Accounts Receivable; Insurance Expense; Interest Expense; Interest Payable; Prepaid Insurance; Supplies; Supplies Expense; Utilities Expense; and Utilities Payable.

E3-6 (Adjusting Entries) Karen Weller, D.D.S., opened a dental practice on January 1, 2014.

During the first month of operations the following transactions occurred.

4. Purchased a one-year malpractice insurance policy on January 1 for $12,000. 5. Purchased $1,600 of dental supplies. On January 31, determined that $500 of supplies were on hand.

Instructions Prepare the adjusting entries on January 31. Account titles are: Accumulated Depreciation-Dental Equipment; Depreciation Expense; Service Revenue; Accounts Receivable; Insurance Expense; Interest Expense; Interest Payable; Prepaid Insurance; Supplies; Supplies Expense; Utilities Expense; and Utilities Payable.

Adjusting entries:

1. The balance in prepaid insurance is a one-year premium paid on June 1, 2014.

2. An inventory count on August 31 shows $450 of supplies on hand.

3. Annual depreciation rates are cottages (4%) and furniture (10%). Salvage value is estimated to be 10% of cost.

4. Unearned Rent Revenue of $3,800 was earned prior to August 31.

5. Salaries of $375 were unpaid at August 31.

6. Rentals of $800 were due from tenants at August 31.

7. The mortgage interest rate is 8% per year.

E3-10 (Adjusting Entries) Greco Resort opened for business on June 1 with eight air-conditioned units. Its trial balance on August 31 is as follows.

Cash $ 19,600

Prepaid Insurance 4,500

Supplies 2,600

Land 20,000

Buildings 120,000

Equipment 16,000

Accounts Payable $ 4,500

Unearned Rent Revenue 4,600

Mortgage Payable 60,000

Common Stock 91,000

Retained Earnings 9,000

Dividends 5,000

Rent Revenue 76,200

Salaries and Wages Expense 44,800

Utilities Expenses 9,200

Maintenance and Repairs Expense 3,600

$245,300 $245,300

Adjusted Trial Balance-Greco Resorts--WORKSHEET

Cash $ 19,600

Prepaid Insurance 4,500

Supplies 2,600

Land 20,000

Buildings 120,000

Equipment 16,000

Accounts Payable $ 4,500

Unearned Rent Revenue 4,600

Mortgage Payable 60,000

Common Stock 91,000

Retained Earnings 9,000

Dividends 5,000

Rent Revenue 76,200

Salaries and Wages Expense 44,800

Utilities Expenses 9,200

Maintenance and Repairs Expense 3,600

Insurance Expense

Supplies Expense

Depreciation Expense-Building

Depreciation Expense-Equipment

Interest Expense

$245,300

$245,300

4 Closing Entries: Income Statement and Dividend Accounts

2 Closing Entries: Income Statement and Dividend Accounts

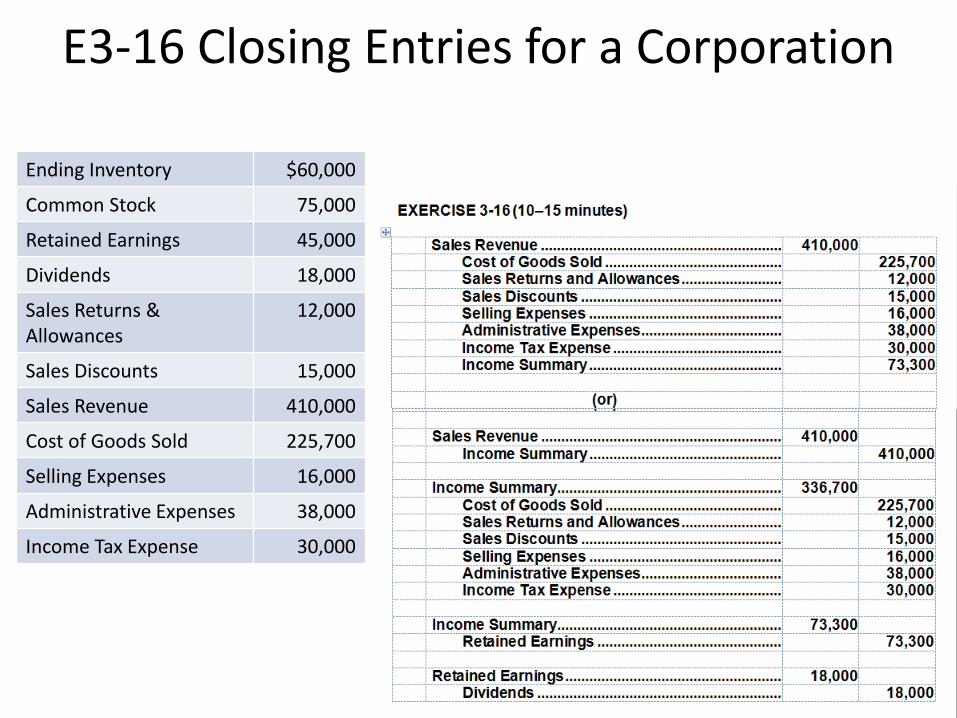

E3-16 Closing Entries for a Corporation

Ending Inventory $60,000

Common Stock 75,000

Retained Earnings 45,000

Dividends 18,000

Sales Returns & Allowances

12,000

Sales Discounts 15,000

Sales Revenue 410,000

Cost of Goods Sold 225,700

Selling Expenses 16,000

Administrative Expenses 38,000

Income Tax Expense 30,000

Income Statement: Multi-step

E3-15 Alatorre Company Eduaro Company Sales $90,000 (d) Sales returns (a) $ 5,000 Net sales 81,000 95,000 Cost of goods sold 56,000 (e) Gross profit (b) 38,000 Operating Expenses 15,000 23,000 Net income (c) 15,000

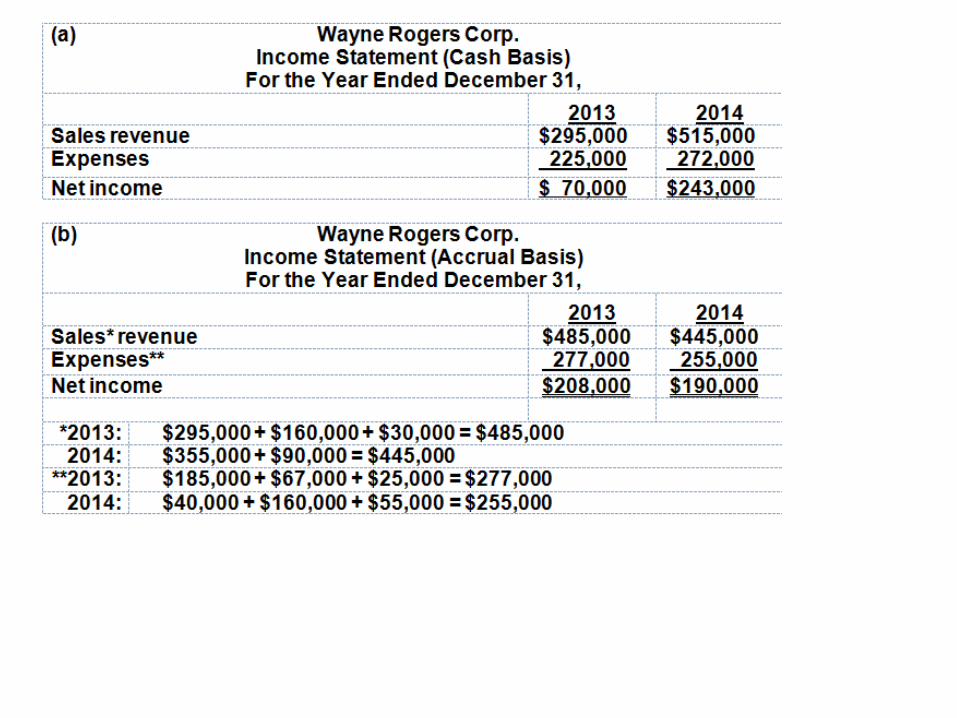

The difference between cash and accrual accounting

Washington Forest Products began operations on January 1, 2011. On December 31, 2011, the company accountant ascertains that the following amounts should be reported as expenses on the income statement: Insurance Expense $20,000; Supplies Expense $11,000; Rent Expense $14,000. A Review of the company’s cash disbursements indicates the company made related cash payments during 2011 as follows: Insurance $29,000; Supplies $27,000; Rent $8,000 Explain why the amounts shown as expenses do not equal the cash paid. For each expense account, compute the amount that should be shown in the related balance sheet account as of December 31, 2011 (remember the company begin operations this year).

E3-18 (Cash to Accrual) Jill Accardo, M.D., uses cash basis. During 2014, Accardo collected $142,600 from her patients and paid $55,470 in expenses. At 1/1/14 and 12/31/14, other accounts were:

1/1/14 12/31/14

Accounts receivable $9,250 $15,927

Unearned service revenue 2,840 4,111

Accrued expenses (L) 3,435 2,108

Prepaid expenses 1,917 3,232

Instructions: Convert to accrual basis.

Alt. E3-18 (Cash to Accrual) Corinne Dunbar, DDS, uses cash basis. During 2014, Dunbar collected $142,600 from her patients and paid $60,470 in expenses. At 1/1/14 and 12/31/14, other accounts were:

1/1/14 12/31/14

Accounts receivable $11,250 $15,927

Unearned service revenue 2,840 4,111

Accrued expenses 3,435 2,108

Prepaid expenses 1,917 3,232

Convert to accrual basis.

E3-20 Adjusting & Reversing entries