Embed Size (px)

Citation preview

BUS 250

Seminar 7

Key Terms• Interest period: the amount of time which interest is

calculated and added to the principal.

• Compound interest: the total interest that accumulated after more than one interest period.

• Future value, maturity value, compound amount: the accumulated principal and interest after one or more interest periods.

• Period interest rate: the rate for calculating interest for one interest period-the annual interest rate is divided by the number of periods per year.

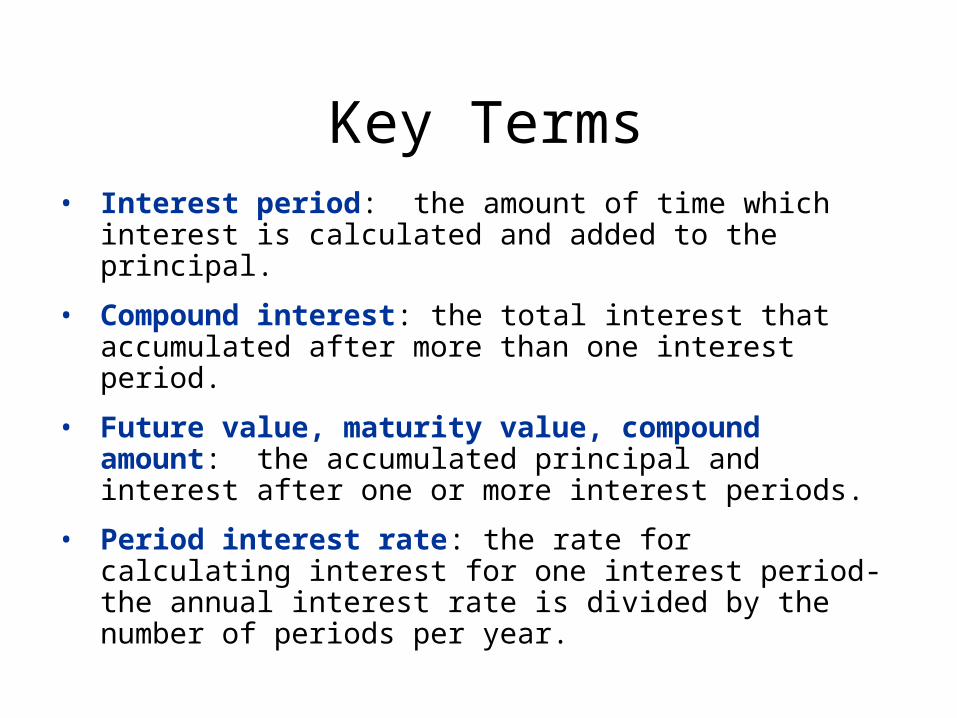

Find the period interest rate for:

• A 12% annual interest rate with 4 interest periods per year.

• 3%

• An 18% annual rate with 12 interest periods per year.

• 1 ½ %

• An 8% annual rate with 4 interest periods per year.

• 2%

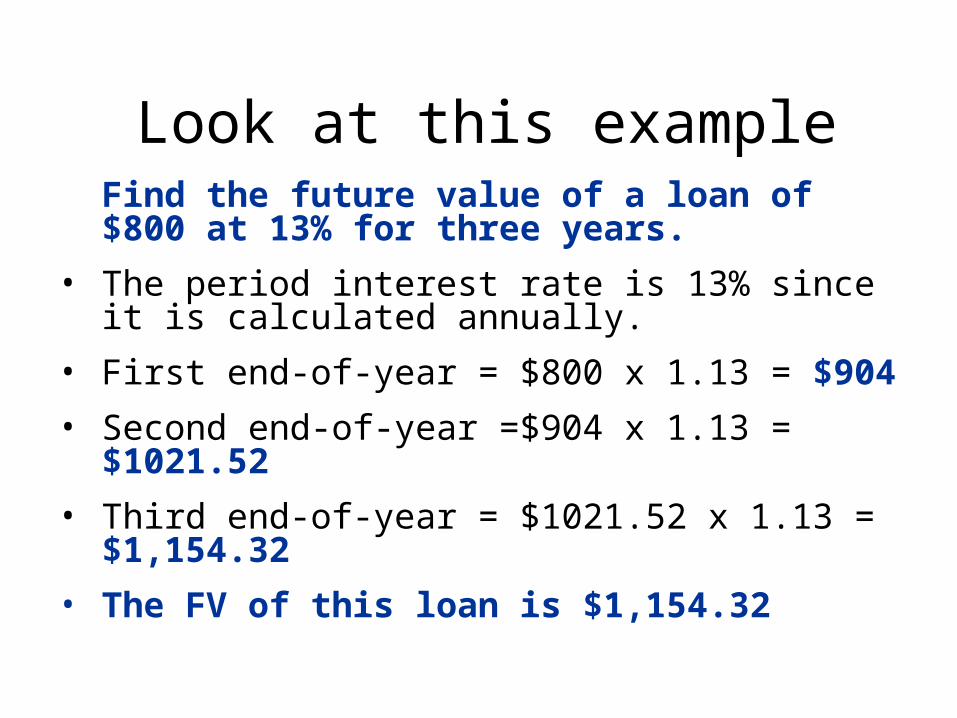

Look at this exampleFind the future value of a loan of $800 at 13% for three years.

• The period interest rate is 13% since it is calculated annually.

• First end-of-year = $800 x 1.13 = $904

• Second end-of-year =$904 x 1.13 = $1021.52

• Third end-of-year = $1021.52 x 1.13 = $1,154.32

• The FV of this loan is $1,154.32

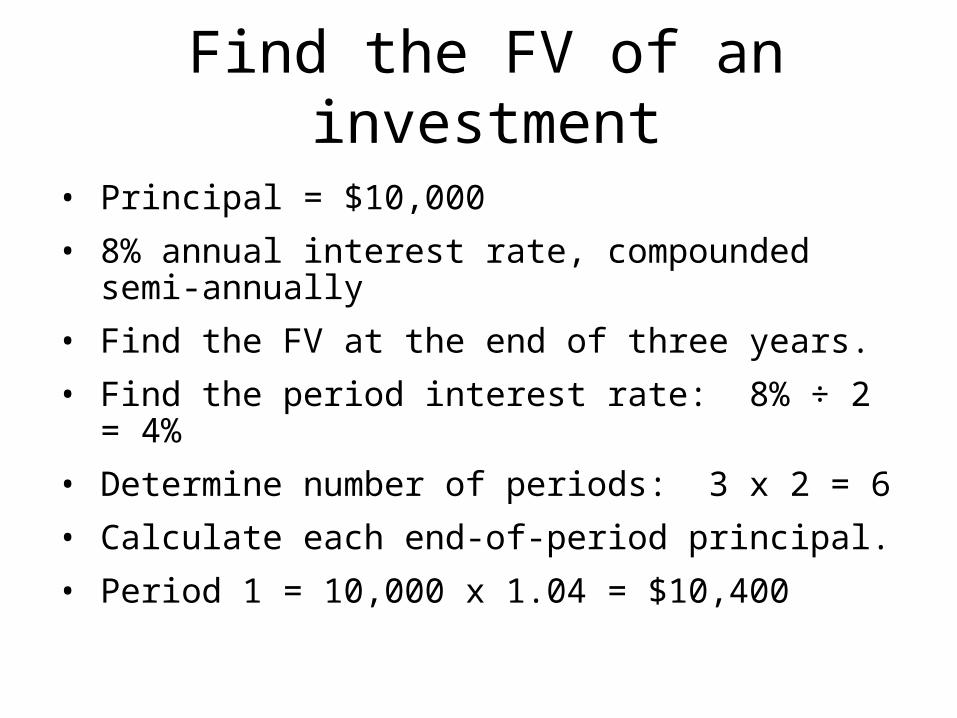

Find the FV of an investment

• Principal = $10,000

• 8% annual interest rate, compounded semi-annually

• Find the FV at the end of three years.

• Find the period interest rate: 8% ÷ 2 = 4%

• Determine number of periods: 3 x 2 = 6

• Calculate each end-of-period principal.

• Period 1 = 10,000 x 1.04 = $10,400

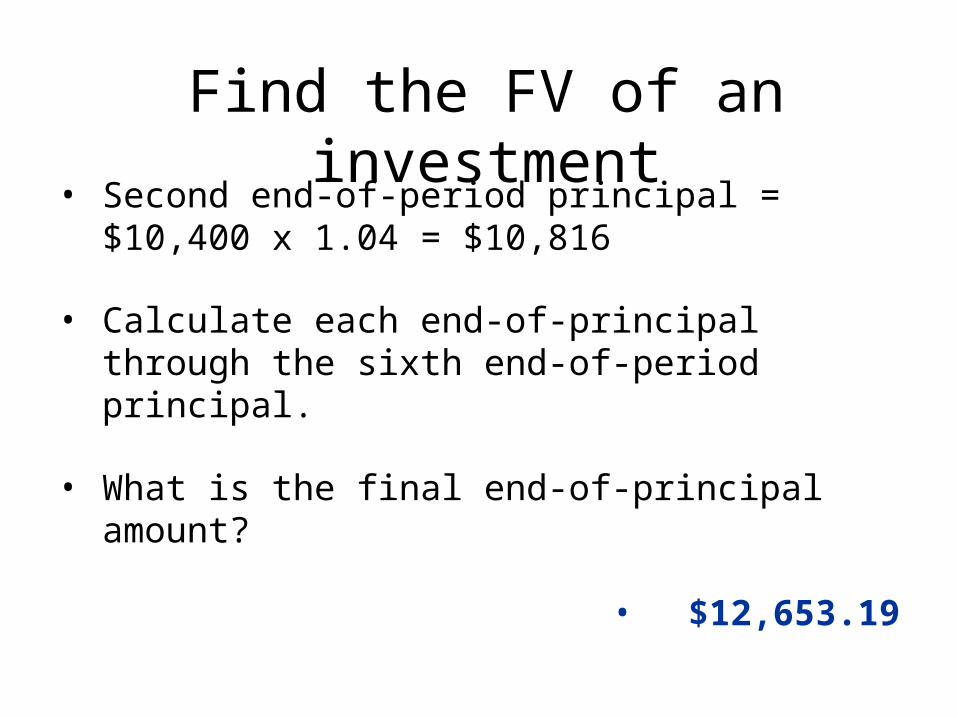

• Second end-of-period principal = $10,400 x 1.04 = $10,816

• Calculate each end-of-principal through the sixth end-of-period principal.

• What is the final end-of-principal amount?

• $12,653.19

Find the FV of an investment

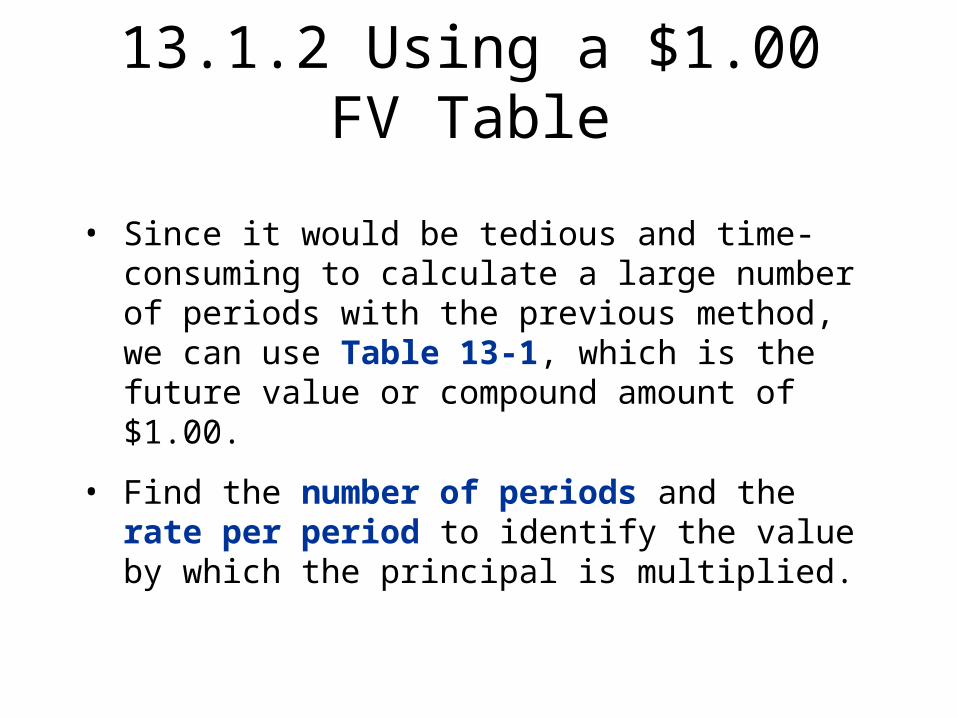

13.1.2 Using a $1.00 FV Table

• Since it would be tedious and time-consuming to calculate a large number of periods with the previous method, we can use Table 13-1, which is the future value or compound amount of $1.00.

• Find the number of periods and the rate per period to identify the value by which the principal is multiplied.

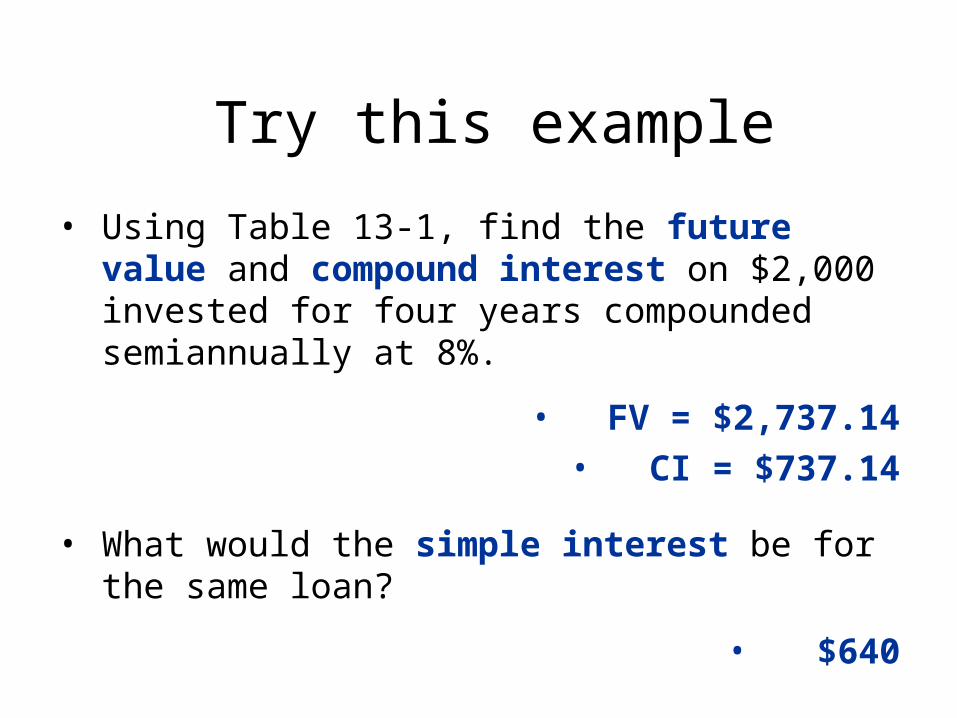

Try this example

• Using Table 13-1, find the future value and compound interest on $2,000 invested for four years compounded semiannually at 8%.

• FV = $2,737.14• CI = $737.14

• What would the simple interest be for the same loan?

• $640

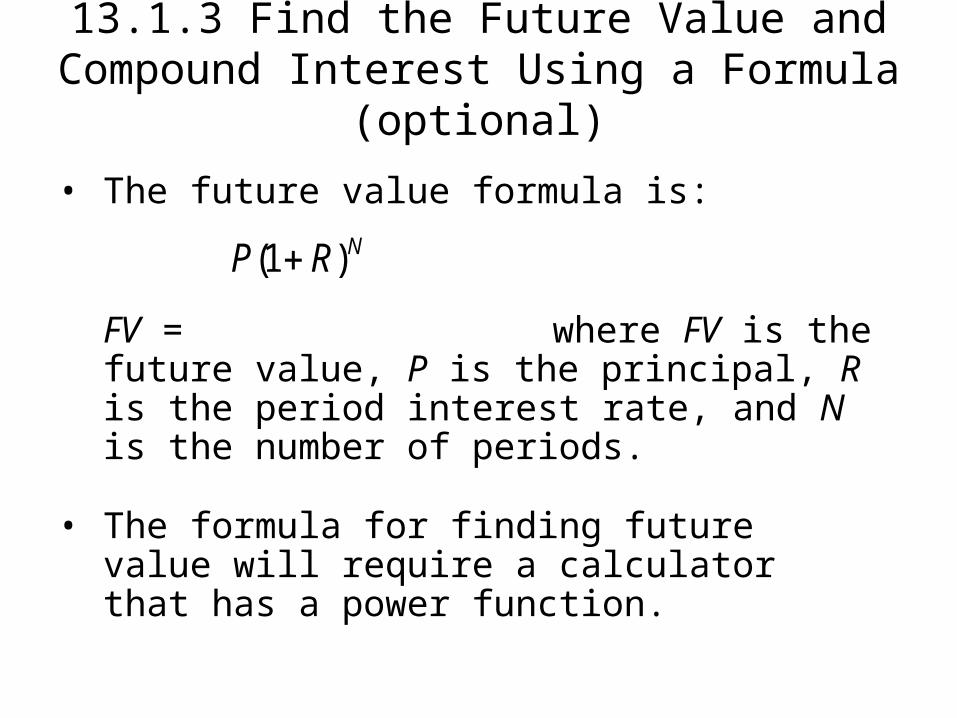

13.1.3 Find the Future Value and Compound Interest Using a Formula (optional)

• The future value formula is:

FV = where FV is the future value, P is the principal, R is the period interest rate, and N is the number of periods.

• The formula for finding future value will require a calculator that has a power function.

(1 )NP R

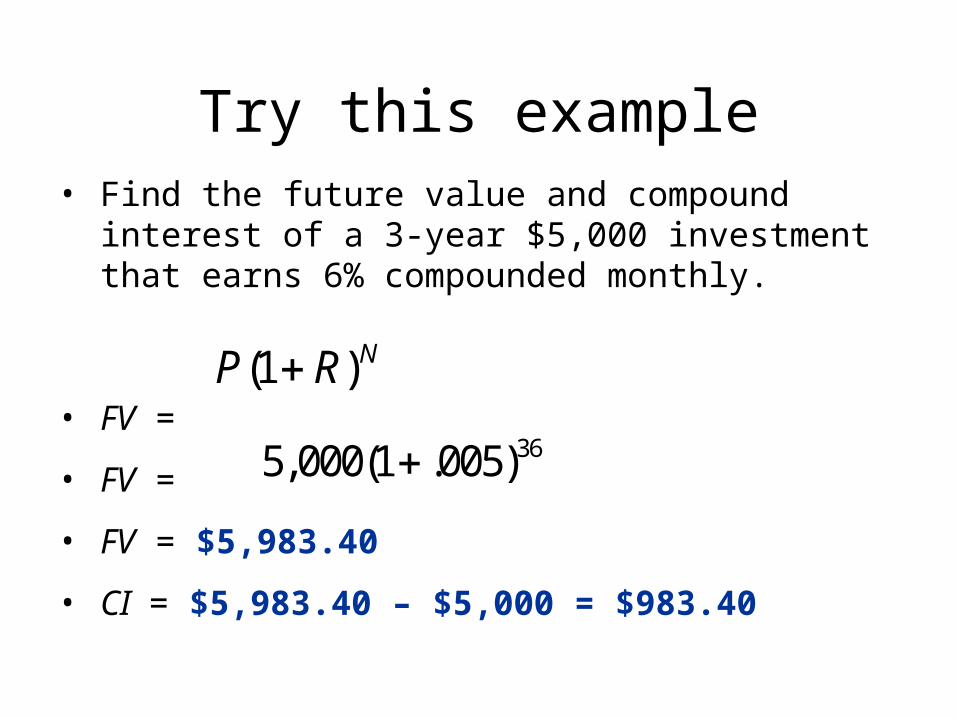

Try this example• Find the future value and compound interest

of a 3-year $5,000 investment that earns 6% compounded monthly.

• FV =

• FV =

• FV = $5,983.40

• CI = $5,983.40 – $5,000 = $983.40

(1 )NP R

365,000(1 .005)

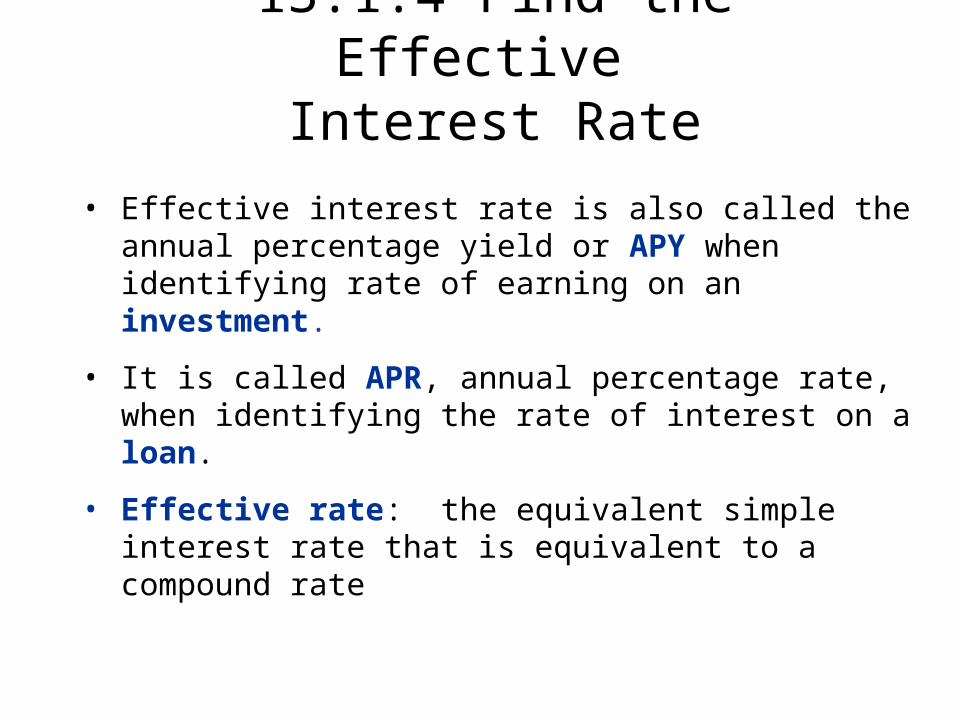

13.1.4 Find the Effective Interest Rate

• Effective interest rate is also called the annual percentage yield or APY when identifying rate of earning on an investment.

• It is called APR, annual percentage rate, when identifying the rate of interest on a loan.

• Effective rate: the equivalent simple interest rate that is equivalent to a compound rate

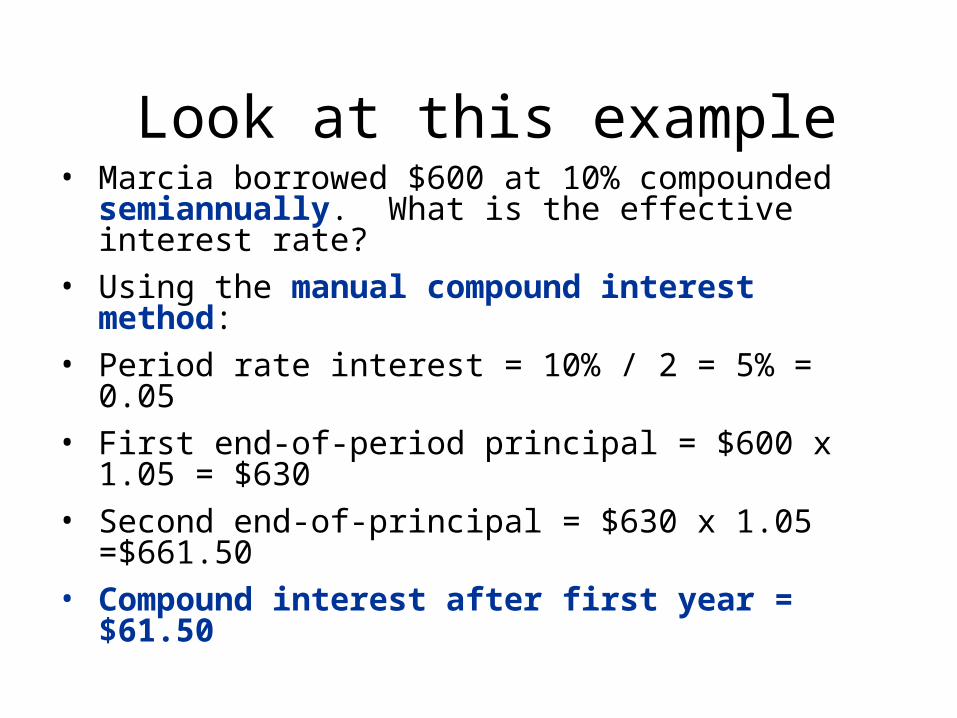

Look at this example• Marcia borrowed $600 at 10% compounded

semiannually. What is the effective interest rate?

• Using the manual compound interest method:

• Period rate interest = 10% / 2 = 5% = 0.05

• First end-of-period principal = $600 x 1.05 = $630

• Second end-of-principal = $630 x 1.05 =$661.50

• Compound interest after first year = $61.50

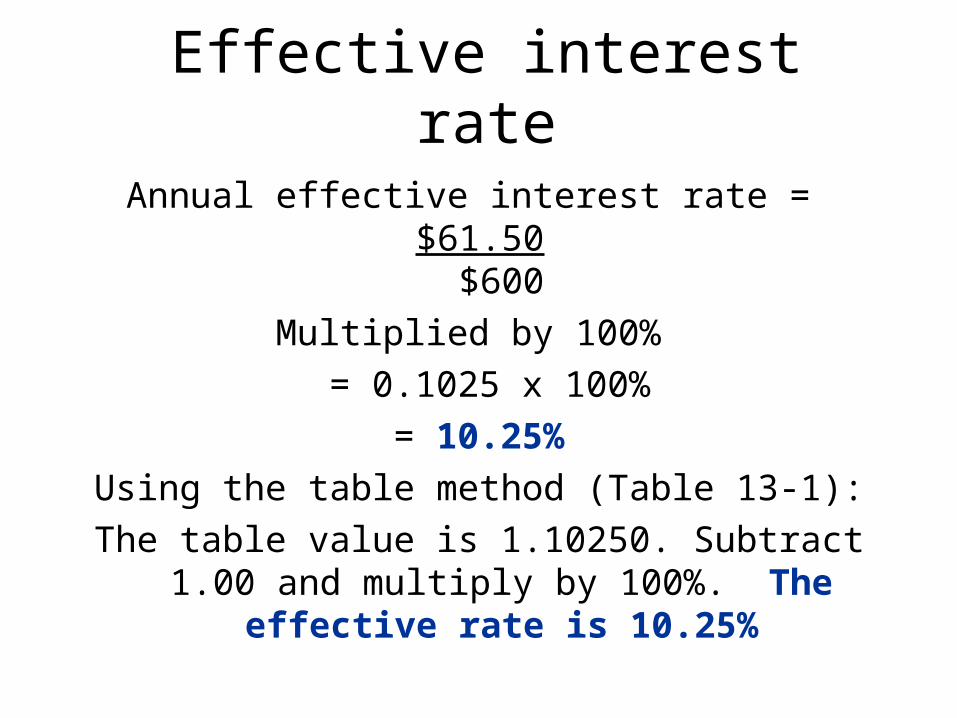

Effective interest rateAnnual effective interest rate =

$61.50 $600

Multiplied by 100%

= 0.1025 x 100%

= 10.25%

Using the table method (Table 13-1):

The table value is 1.10250. Subtract 1.00 and multiply by 100%. The effective rate is

10.25%

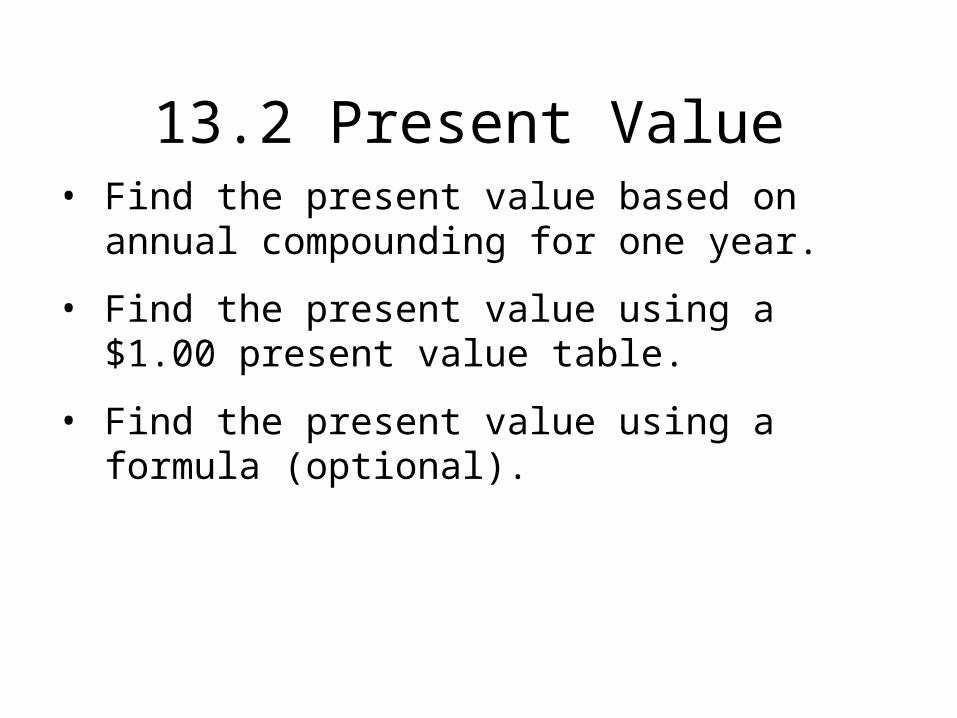

13.2 Present Value • Find the present value based on annual

compounding for one year.

• Find the present value using a $1.00 present value table.

• Find the present value using a formula (optional).

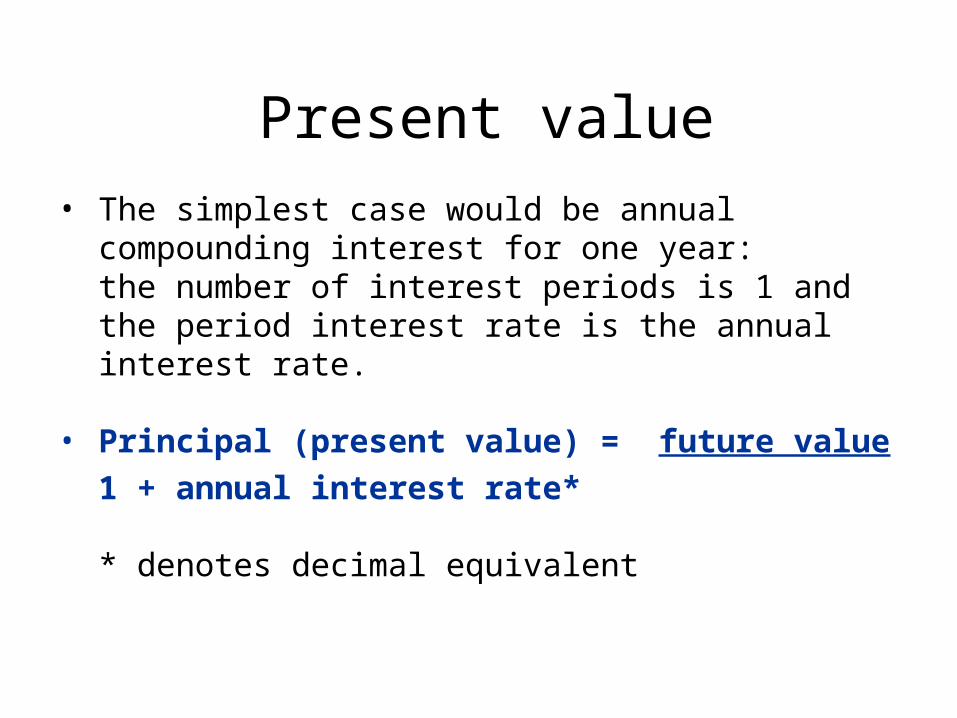

Present value

• The simplest case would be annual compounding interest for one year: the number of interest periods is 1 and the period interest rate is the annual interest rate.

• Principal (present value) = future value

1 + annual interest rate*

* denotes decimal equivalent

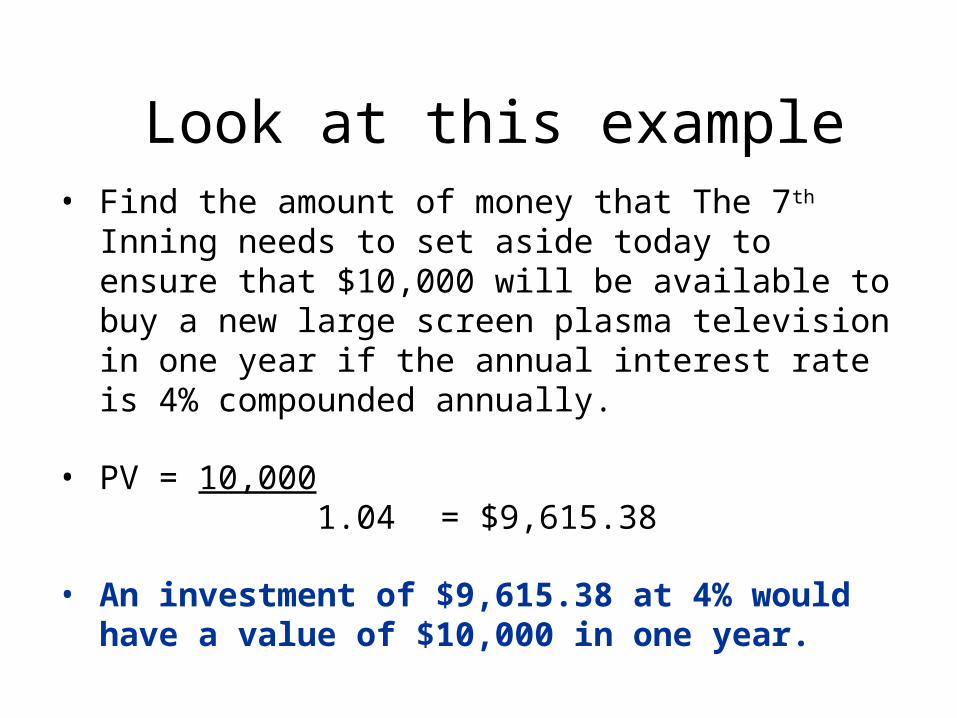

Look at this example• Find the amount of money that The 7th Inning

needs to set aside today to ensure that $10,000 will be available to buy a new large screen plasma television in one year if the annual interest rate is 4% compounded annually.

• PV = 10,000 1.04 = $9,615.38

• An investment of $9,615.38 at 4% would have a value of $10,000 in one year.

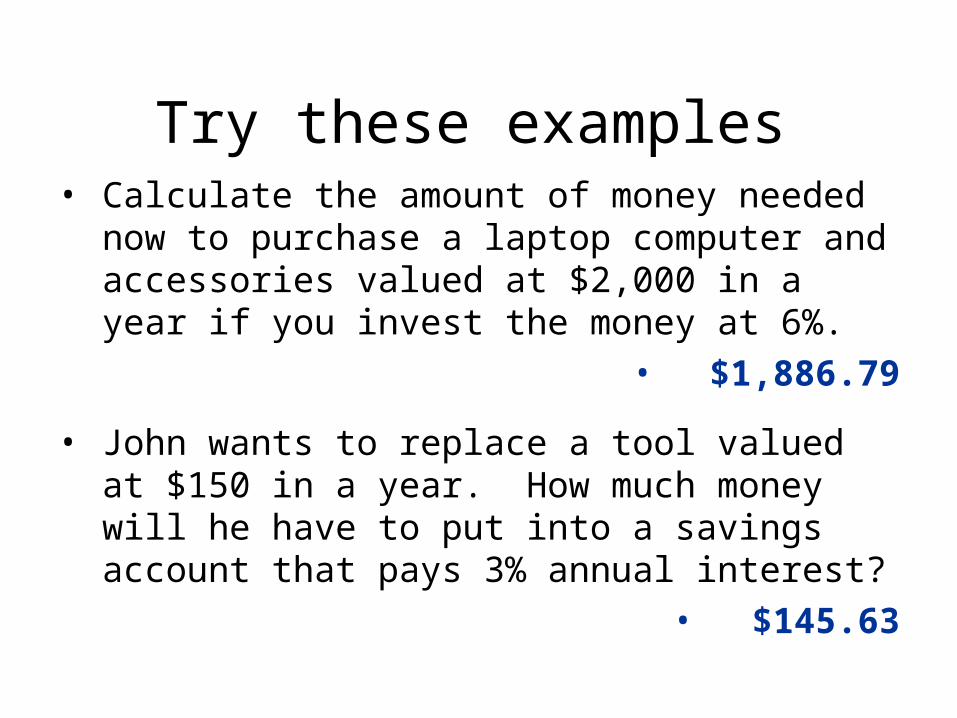

Try these examples• Calculate the amount of money needed now to

purchase a laptop computer and accessories valued at $2,000 in a year if you invest the money at 6%.

• $1,886.79

• John wants to replace a tool valued at $150 in a year. How much money will he have to put into a savings account that pays 3% annual interest?

• $145.63

13.2.2. Use a $1.00 Present Value Table

• Using a present value table is the most efficient way to calculate the money needed now for a future expense or investment.

• Table 13-3 shows the present value of $1.00 at different interest rates for different periods.

Look at this example

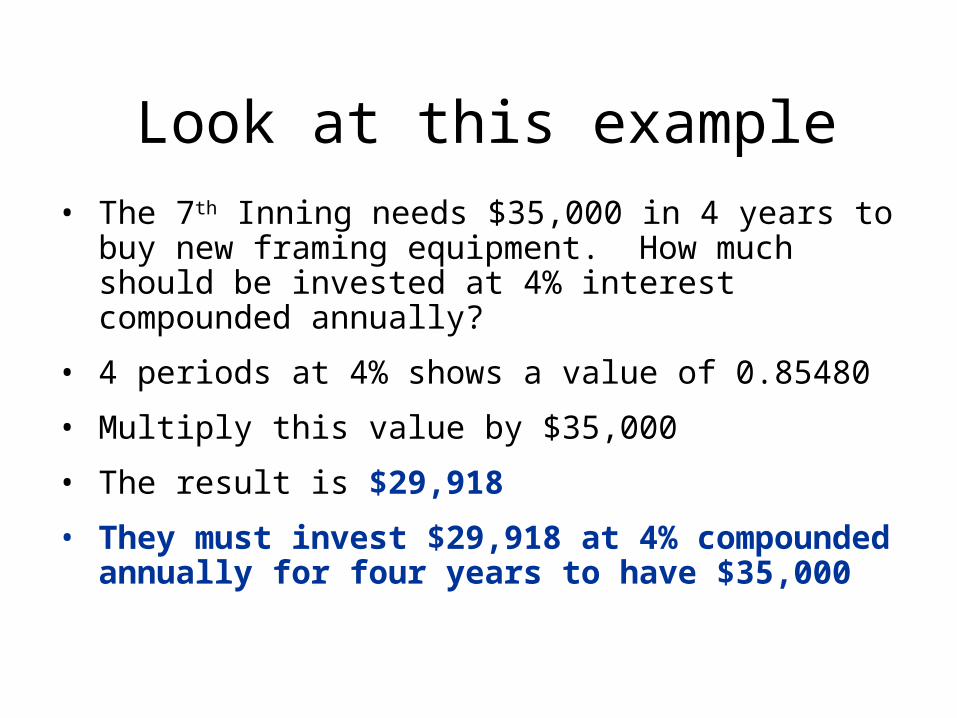

• The 7th Inning needs $35,000 in 4 years to buy new framing equipment. How much should be invested at 4% interest compounded annually?

• 4 periods at 4% shows a value of 0.85480

• Multiply this value by $35,000

• The result is $29,918

• They must invest $29,918 at 4% compounded annually for four years to have $35,000

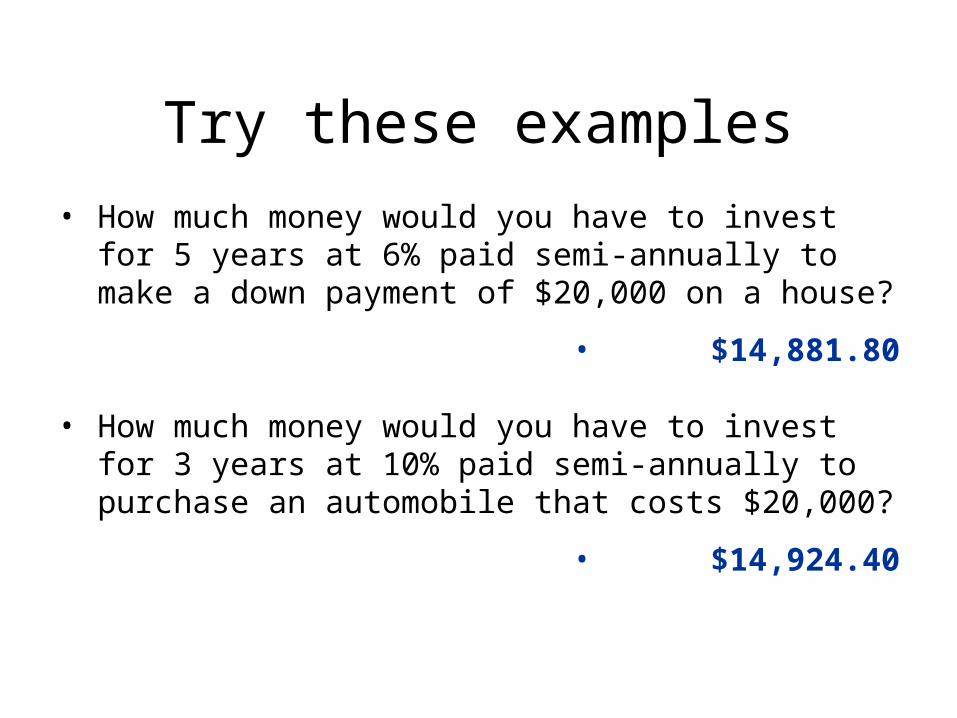

Try these examples

• How much money would you have to invest for 5 years at 6% paid semi-annually to make a down payment of $20,000 on a house?

• $14,881.80

• How much money would you have to invest for 3 years at 10% paid semi-annually to purchase an automobile that costs $20,000?

• $14,924.40

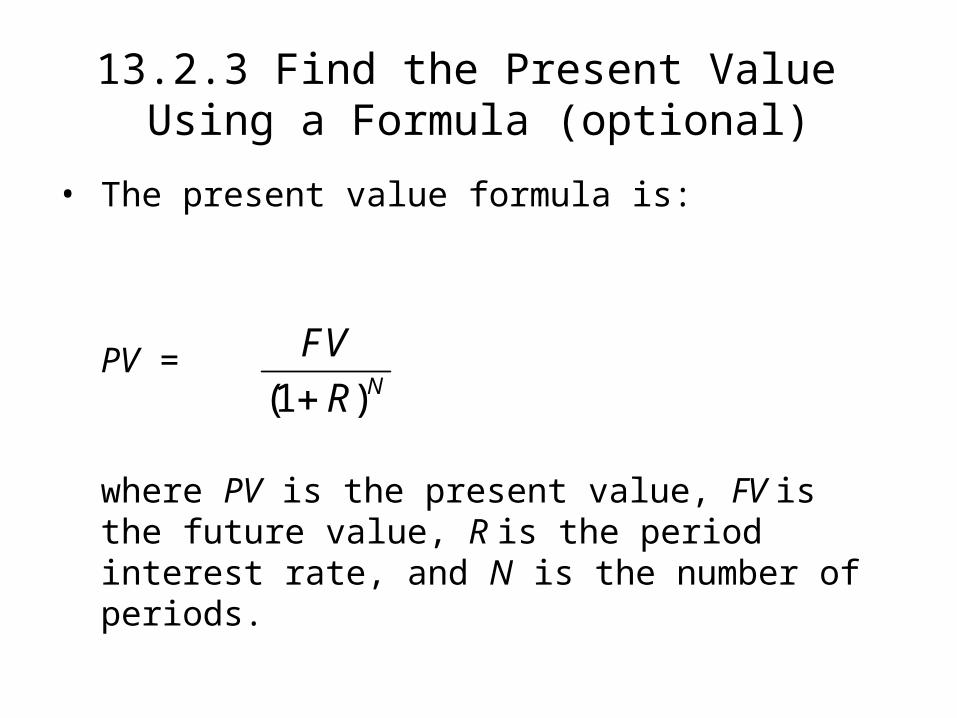

13.2.3 Find the Present Value Using a Formula (optional)

• The present value formula is:

PV =

where PV is the present value, FV is the future value, R is the period interest rate, and N is the number of periods.

(1 )NFV

R

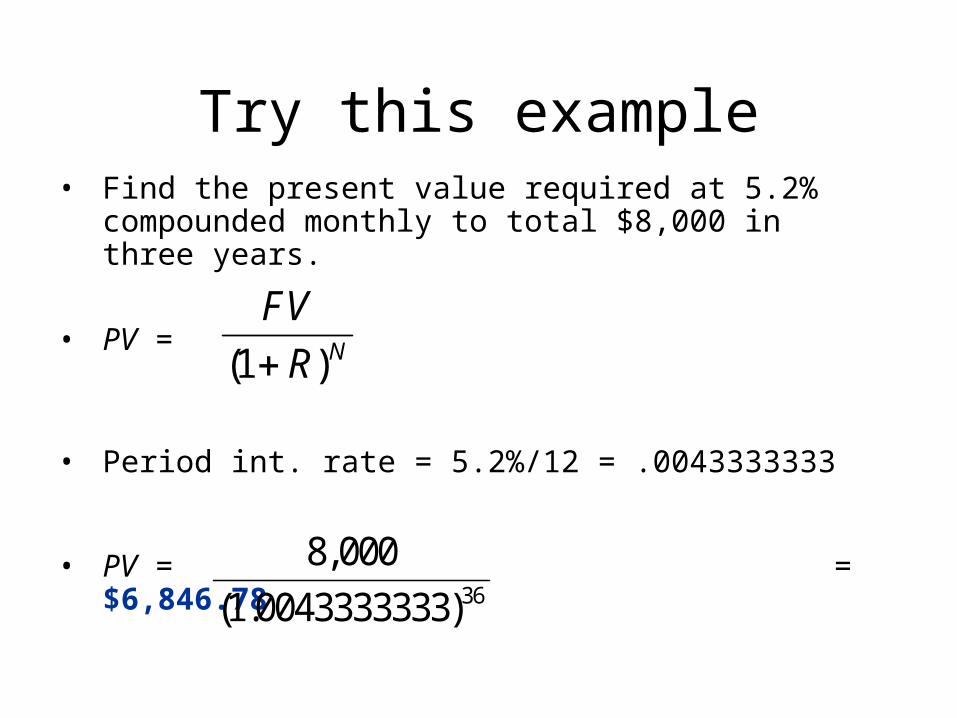

Try this example• Find the present value required at 5.2% compounded

monthly to total $8,000 in three years.

• PV =

• Period int. rate = 5.2%/12 = .0043333333

• PV = = $6,846.78

(1 )NFV

R

36

8,000

(1.0043333333)

![120+ Simple interest & Compound Interest Questions With … · 120+ Simple interest & Compound Interest Questions With Solution GovernmentAdda.com . Daily Visit : [GOVERNMENTADDA.COM]](https://img.pdfslide.us/doc/110x75/5e7b9ad23f4ca3416d59c1c7/120-simple-interest-compound-interest-questions-with-120-simple-interest.jpg)